UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

(Mark one) | | | | | |

| ☒ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2023

OR | | | | | |

| ☐ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 001-36127

COOPER-STANDARD HOLDINGS INC.

(Exact name of registrant as specified in its charter)

| | | | | | | | |

| Delaware | | 20-1945088 |

| (State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

40300 Traditions Drive

Northville, Michigan 48168

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (248) 596-5900

Securities registered pursuant to Section 12(b) of the Act: | | | | | | | | | | | | | | |

| Title of each class | | Trading Symbol(s) | | Name of each exchange on which registered |

| Common Stock, par value $0.001 per share | | CPS | | New York Stock Exchange |

| Preferred Stock Purchase Rights | | - | | New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

| | | | | | | | | | | |

| Large accelerated filer | ☐ | Accelerated filer | ☒ |

| Non-accelerated filer | ☐ | Smaller reporting company | ☒ |

| | Emerging growth company | ☐ |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management's assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

If securities are registered pursuant to Section 12(b) of the Act, indicate by check mark whether the financial statements of the registrant included in the filing reflect the correction of an error to previously issued financial statements. ☐

Indicate by check mark whether any of those error corrections are restatements that required a recovery analysis of incentive-based compensation received by any of the registrant’s executive officers during the relevant recovery period pursuant to §240.10D-1(b). ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

The aggregate market value of voting and non-voting common stock held by non-affiliates as of June 30, 2023 was $192,207,617.

The number of the registrant’s shares of common stock, $0.001 par value per share, outstanding as of February 9, 2024 was 17,197,479 shares.

Documents Incorporated by Reference

Certain portions, as expressly described in this report, of the Registrant’s Proxy Statement for the 2024 Annual Meeting of Stockholders are incorporated by reference into Part III of this Annual Report on Form 10-K.

TABLE OF CONTENTS | | | | | | | | |

| | | Page |

| PART I |

| | |

| Item 1. | Business | |

| Item 1A. | Risk Factors | |

| Item 1B. | Unresolved Staff Comments | |

| Item 1C. | Cybersecurity | |

| Item 2. | Properties | |

| Item 3. | Legal Proceedings | |

| Item 4. | Mine Safety Disclosures | |

|

| PART II |

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | |

| Item 6. | [Reserved] | |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | |

| Item 8. | Financial Statements and Supplementary Data | |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | |

| Item 9A. | Controls and Procedures | |

| Item 9B. | Other Information | |

| Item 9C. | Disclosure Regarding Foreign Jurisdictions that Prevent Inspections | |

|

| PART III |

| Item 10. | Directors, Executive Officers and Corporate Governance | |

| Item 11. | Executive Compensation | |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | |

| Item 13. | Certain Relationships and Related Transactions, and Director Independence | |

| Item 14. | Principal Accounting Fees and Services | |

|

| PART IV |

| Item 15. | Exhibits and Financial Statement Schedules | |

| Signatures | |

PART I

Item 1. Business

Cooper-Standard Holdings Inc. (together with its consolidated subsidiaries, the “Company,” “Cooper Standard,” “we,” “our” or “us”) is a leading manufacturer of sealing and fluid handling systems (consisting of fuel and brake delivery and fluid transfer systems). Our products are primarily for use in passenger vehicles and light trucks that are manufactured by global automotive original equipment manufacturers (“OEMs”) and replacement markets. We conduct substantially all of our activities through our subsidiaries.

Cooper Standard is listed on the New York Stock Exchange (“NYSE”) under the ticker symbol “CPS.” The Company has approximately 23,000 employees, including 3,000 contingent workers, with 128 facilities in 21 countries. We believe that we are the largest global producer of sealing systems, the second largest global producer of the types of fuel and brake delivery products that we manufacture and the third largest global producer of the types of fluid transfer systems that we manufacture. We design and manufacture our products in each major region of the world through a disciplined and sustained approach to engineering and operational excellence. We operate in 78 manufacturing locations and 50 design, engineering, administrative and logistics locations.

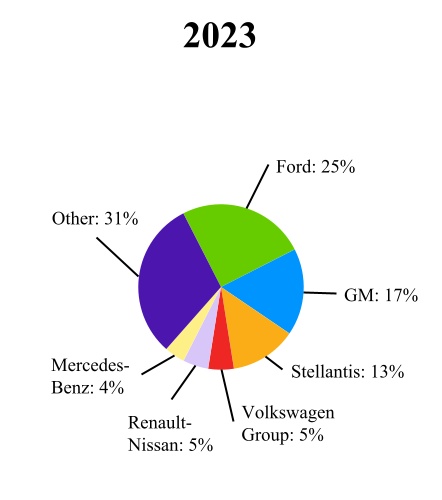

Approximately 84% of our sales in 2023 were to OEMs, including Ford Motor Company (“Ford”), General Motors Company (“GM”), Stellantis, Volkswagen Group, Daimler, Renault-Nissan, BMW, Toyota, Volvo, Jaguar/Land Rover, Honda and various other OEMs based in China. The remaining 16% of our 2023 sales were primarily to Tier I and Tier II automotive suppliers, non-automotive customers, and replacement market distributors. The Company’s products can be found on over 440 nameplates globally.

Our organizational structure primarily consists of a global automotive business (“Automotive”) and the Industrial and Specialty Group (“ISG”). For the periods presented herein, our business was organized in the following reportable segments: North America, Europe, Asia Pacific and South America. ISG and all other business activities were reported in Corporate, eliminations and other. This operating structure allowed us to offer our full portfolio of products and support our global and regional customers with complete engineering and manufacturing expertise in all major regions of the world. On an ongoing basis, we undertake restructuring, expansion and cost reduction initiatives to improve competitiveness.

Consistent with our strategy to drive future profitable growth, the Company has increased and intensified management focus on its two global automotive product line businesses. Effective January 1, 2024, the Company appointed a senior executive to lead each of our sealing and fluid handling systems businesses, and the chief operating decision maker will prospectively begin to assess operating performance by product line rather than geography. As a result, beginning with the first quarter of 2024, the Company expects to report its financial results in two reportable segments based on product line: Sealing Systems and Fluid Handling Systems.

Corporate History and Business Developments

Cooper-Standard Holdings Inc. was established in 2004 as a Delaware corporation and began operating on December 23, 2004 when it acquired the automotive segment of Cooper Tire & Rubber Company. Cooper-Standard Holdings Inc. operates the business primarily through its principal operating subsidiary, Cooper-Standard Automotive Inc. (“CSA U.S.”). Since the 2004 acquisition, the Company has expanded and diversified its customer base through a combination of organic growth and strategic acquisitions.

Our ISG business accelerates and maximizes the value stream of Cooper Standard’s materials science and manufacturing expertise in industrial and specialty markets. We furthered the expansion of our ISG business through the acquisition of Lauren Manufacturing and Lauren Plastics in 2018.

Cooper Standard signed multiple joint development agreements for our Fortrex™ chemistry platform throughout 2018 to 2021. In 2021, the Company reached a long-term commercial agreement to license its Fortrex™ technology to NIKE, Inc., with the footwear manufacturer launching the first related mass production programs in 2023.

In 2023, we finalized the divestiture of our European technical rubber products business and sold the Company’s entire controlling equity interest in a joint venture in the Asia Pacific region.

Business Strategy

Cooper Standard’s Purpose statement - Creating Sustainable Solutions Together - represents the Company’s focus on creating solutions for the long-term health of the business as a whole and the sustained value that we work each day to deliver to our stakeholders (customers, investors, employees, suppliers and communities). Our key strategic imperatives are defined as:

| | | | | |

| Financial Strength: | Execute our business plans achieving and sustaining double-digit EBITDA margins, ROIC and strong free cash flow generation. |

| |

| World-Class Execution: | Attain world-class results across all our business allowing the Company to Be the First Choice of the Stakeholders We Serve. |

| |

| Profitable Growth Driven by Innovation: | Leverage our materials science and product knowledge, innovation and manufacturing expertise across our product groups in the pursuit of organic and inorganic growth. |

| |

| Corporate Responsibility: | Deliver value to all our stakeholders through our environmental, social and governance initiatives to ensure the long-term sustainability of the Company. |

Cooper Standard’s global alignment around these imperatives continues to drive further value in many areas of the business.

Operational and Strategic Initiatives

As part of Cooper Standard’s world-class operations, the Company relies upon its CSOS (Cooper Standard Operating System) to fully position the Company for growth and ensure global consistency in engineering design, program management, manufacturing process, purchasing and IT systems. Standardization across all regions is especially critical in support of customers’ global platforms that require the same design, quality and delivery standards everywhere across the world. As a result of these initiatives, the Company has leveraged CSOS to drive an average savings from improved operating efficiency of approximately $60 million each of the past five years.

In addition, as part of our continued focus on sustainability and corporate responsibility, the Company’s Global Sustainability Council provides executive level oversight for the Company’s sustainability strategy to help ensure alignment and integration with business goals and stakeholder priorities. The council maintains a holistic look at the Company’s ESG (environmental, social and governance) initiatives, tracks rapidly-evolving best practices and further develops long-term goals as the Company strives for ESG excellence.

Cooper Standard continues to progress its diversification strategy through its ISG business, which is charged with accelerating and maximizing expertise in the Company’s core product types for applications in the industrial and specialty markets. Cooper Standard also drives growth and diversification through the Company’s applied materials science offerings, which include the Fortrex™ chemistry platform that provides performance advantages over many other materials, as well as a significantly reduced carbon footprint.

Leveraging Technology and Materials Science for Innovative Solutions

We use our technical and materials science expertise to provide customers with innovative and sustainable product solutions. Our engineers use the results of advanced computational simulations and incorporate a broad understanding of materials science to design products which meet or exceed our customers’ stringent requirements. We believe our reputation for successful innovation in product design and materials is the reason our customers consult us early in the development and design process of their next-generation vehicles or products.

The Company’s CS Open Innovation is an initiative that aims to position Cooper Standard as the partner of choice for start-ups, universities and other suppliers through a proactive outreach program. The initiative is focused in the areas of materials science, manufacturing and process technology, digital/artificial intelligence and advanced product technology.

Cooper Standard uses its i3 Innovation Process (Imagine, Initiate and Innovate) and CS Open Innovation as mechanisms to capture novel ideas while promoting a culture of innovation. Ideas are carefully evaluated by our global product line teams and Global Technology Council, and those that are selected are put on an accelerated development cycle. We are developing innovative technologies based on materials expertise, process know-how, and application vision, which may drive future product direction. An example is Fortrex™, the Company’s synthetic elastomer chemistry platform, offering reduced weight while delivering superior material performance and aesthetics. We have also developed several other significant technologies,

especially related to advanced materials, processing and weight reduction. These include: FlushSeal™, an advanced integrated solution for frame under glass static sealing systems offering better appearance, improved aerodynamics, quieter ride and reduced weight; TPV body seal, a next generation body seal that replaces traditionally less sustainable EPDM and metal with recyclable thermoplastic materials which save significant component weight; MagAlloy™, a processing technology for brake lines that increases long term durability through superior corrosion resistance; and Easy-Lock™, a small package coolant and fuel vapor quick connect. Given the trajectory and anticipated future growth of electric vehicles, Cooper Standard has developed innovations to provide lightweight plastic tubing with our PlastiCool® 2000 multilayer tubing, smooth and clear vinyl tubing (“CVT”) mid-temperature multilayer tubing, and our next-generation Ergo-Lock™ and Ergo-Lock™ + VDA quick connectors for glycol thermal management needs.

Cooper Standard is strategically integrating digital tools and advanced analysis to help deliver the best solutions. We offer advanced computer-aided engineering and digital simulations for engineered solutions. In addition, our team of experts has developed digital tools that enable them to conduct prototype testing without the need for physical samples, resulting in sustainability benefits. We can provide up to 100% virtual testing for certain products.

Among our newer technologies is Cooper Standard’s artificial intelligence (A.I.)-enhanced development cycle for polymer compounds that has shortened material development times while realizing rapid discovery of new compounds that offer superior performance properties, which yield superior products. We have also developed proprietary technology for A.I. automated processes control improvements, called Liveline Technologies, a wholly owned subsidiary of Cooper Standard. This technology enables full automation of polymer extrusion and other complex continuous processes, reducing process variation (a top driver of scrap), increasing product quality, improving operational metrics and reducing our carbon footprint. In addition, the Company is piloting multiple A.I. applications to help drive efficiencies in various functions.

Our innovations are receiving industry recognition. Cooper Standard earned an Environment + Energy Leader Award in 2022 for our Fortrex™ chemistry platform, in addition to being named a General Motors Overdrive Award winner in the category of ‘Sustainability’ in 2021, a 2018 Automotive News PACE Award winner, and a 2018, 2019, and 2023 Society of Plastics Engineers Innovation Award finalist. Also, Cooper Standard’s artificial intelligence-enhanced development cycle for polymer compound development was named a finalist for the 2019 Automotive News PACE Awards.

Cooper Standard’s fluid handling products were selected as the Society of Plastics Engineers 2022 Automotive Innovation Award winner for the Material category for our innovative battery electric vehicle thermoplastic thermal management solution utilizing PlastiCool® 2000 multilayer tube and Ergo-Lock® connectors.

Industry

The automotive industry is one of the world’s largest and most competitive markets. Consumer demand for new vehicles largely determines sales and production volumes of global OEMs. The business and commercial environment in each region also plays a role in vehicle demand as it relates to fleet vehicle sales and industrial-use vehicles such as light and heavy trucks.

OEMs compete for market share in a variety of ways including pricing and incentives, the development of new, more attractive models, branding and advertising, and the ability to customize vehicle features and options to meet specific consumer needs or demands. They rely heavily on thousands of specialized suppliers to provide the many distinct components and systems that comprise the modern vehicle. They also rely on these automotive suppliers to develop technological innovations that will help them meet internal and consumer demands as well as regulatory requirements.

The supplier industry is a highly competitive industry and is generally characterized by high barriers to entry, significant start-up costs and long-standing customer relationships. The criteria by which OEMs judge automotive suppliers include quality, price, service, launch performance, design and engineering capabilities, innovation, timely delivery, financial stability and global footprint. Over the last decade, suppliers that have been able to achieve manufacturing scale globally, reduce structural costs, diversify their customer base and provide innovative, value-added technologies have been the most successful.

The technology of today’s vehicles is evolving rapidly. This evolution is being driven by many factors including consumer preferences and social behaviors, a competitive drive for differentiation, regulatory requirements and environmental impact and safety. Cooper Standard supports these trends by providing innovations that reduce weight, increase life-cycle and durability, reduce interior noise, enhance exterior appearance, simplify the manufacturing and assembly process, and help reduce a vehicle’s environmental impact. These are innovations that can be applicable and valuable to virtually any vehicle (including internal combustion, hybrid or battery electric powertrains) or vehicle manufacturer and, in many cases, can also be transferred to non-automotive applications in adjacent markets. Cooper Standard remains closely aligned with our customers and is prepared to meet their evolving needs as they shift their fleets and offer more electric vehicle (“EV”) options. We are focused on growing

our business in the EV segment by leveraging our technology and innovation to provide value-add solutions for increasingly specialized technical requirements.

Markets Served

Our automotive business is focused on the passenger car and light truck market, up to and including Class 3 full-size, full-frame trucks, better known as the global light vehicle market. This is our largest market and accounts for approximately 94% of our global sales.

Customers

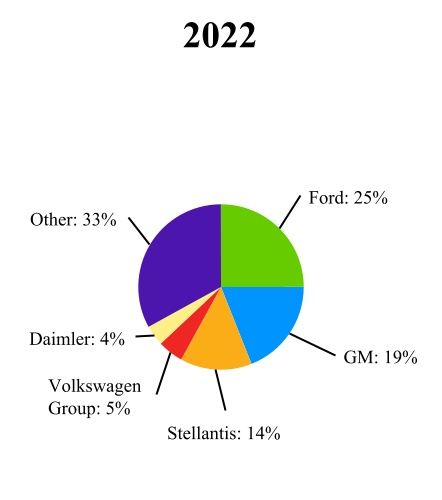

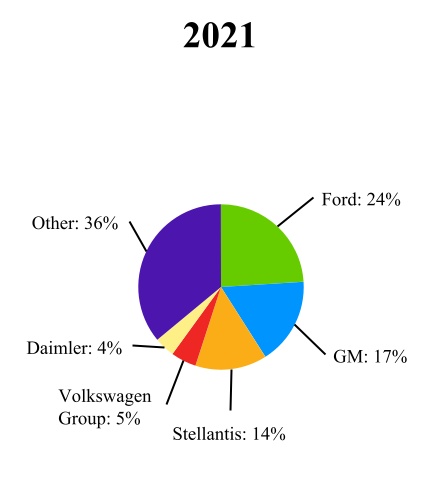

We are a leading supplier to the following OEMs and are increasing our presence with major OEMs throughout the world. The following charts show the percentage of sales to our top customers for the years ended December 31, 2023, 2022 and 2021:

Our other customers include OEMs such as BMW, Toyota, Volvo, Jaguar/Land Rover, Honda and various other OEMs based in China. Our business with any given customer is typically split among several contracts for different parts on a number of platforms.

Products

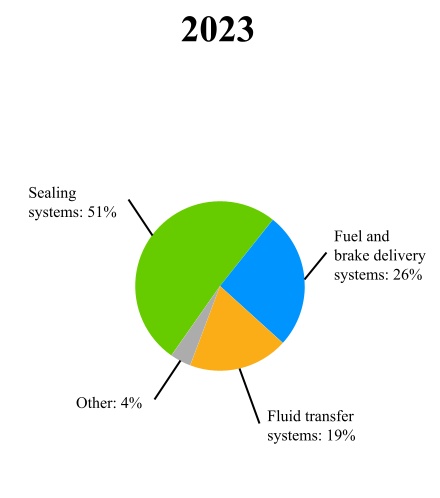

Our product lines include sealing systems and fluid handling systems (consisting of fuel and brake delivery and fluid transfer systems). These products are produced and supplied globally to a broad range of customers in multiple markets.

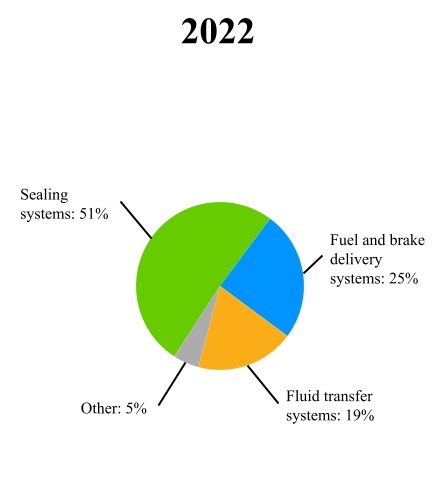

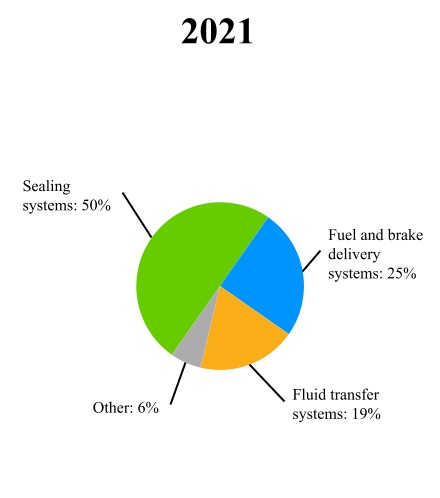

In addition to these product lines, we also sell our core products into other adjacent markets. The percentage of sales by product line and other markets for the years ended December 31, 2023, 2022 and 2021 are as follows:

| | | | | | | | | | | | | | | | | | | | | | | |

| Product Lines | | | | | | | Market Position |

| SEALING SYSTEMS | | Protect vehicle interiors from weather, dust and noise intrusion for improved driving experience; provide aesthetic and functional class-A exterior surface treatment | | Global leader |

| | Products: | | | | |

| | – | Fortrex® | – | FlushSeal™ systems | | |

| | – | Dynamic seals | – | Variable extrusion | | |

| | – | Static seals | – | Specialty sealing products | | |

| | – | Encapsulated glass | – | Stainless steel trim | | |

| | – | Tex-A-Fib (Textured Surface with Cloth Appearance) | – | Frameless Systems | | |

| | – | Obstacle detection sensor system | | | | |

| | | | | |

| FUEL & BRAKE DELIVERY SYSTEMS | | Sense, deliver and control fluid and fluid vapors for fuel and brake systems | | Top 2 globally |

| | Products: | | | | |

| | – | Chassis and tank fuel lines and bundles (fuel lines, vapor lines and bundles) | – | Direct injection & port fuel rails (fuel rails and fuel charging assemblies) | | |

| | – | Metallic brake lines and bundles | – | MagAlloy™ break tube coating | | |

| | – | Quick connects | – | ArmorTube™ brake tube coating | | |

| | – | Low oligomer multi-layer convoluted tube | – | Series 300 and S300LT (low temperature) quick connects | | |

| | – | Brake jounce lines | – | Gen III Posi-Lock® quick connects | | |

| | | | | |

| FLUID TRANSFER SYSTEMS | | Sense, deliver, connect and control fluid delivery for optimal thermal management, powertrain & HVAC operation | | Top 3 globally |

| | Products: | | | | |

| | – | Heater/coolant hoses | – | Turbo charger hoses | | |

| | – | Quick connects (SAE and VDA) | – | Charged air cooler ducts/assemblies | | |

| | – | Diesel particulate filter (DPF) lines | – | Secondary air hoses | | |

| | – | Degas tanks and deaerators | – | Brake and clutch hoses | | |

| | – | Charged air cooling (air intake and discharge) | – | Easy-Lock™ quick connect | | |

| | – | Transmission oil cooling hoses | – | Ergo-Lock™ VDA quick connect | | |

| | – | Multilayer tubing for glycol thermal management | – | Ergo-Lock™ + VDA quick connect | | |

| | – | PlastiCool® 5000 high temperature MLT | – | PlastiCool® 2000 multi-layer tubing for glycol thermal management | | |

| | | | | |

Competition

We believe that the principal competitive factors in our industry are quality, price, service, launch performance, design and engineering capabilities, innovation, timely delivery, financial stability and global footprint. We believe that our capabilities in these core competencies are integral to our position as a market leader in each of our product lines. Our sealing systems products compete with Toyoda Gosei, Henniges, Hutchinson Standard Profil, HSR&A, SaarGummi and JianXin, among others. Our fuel and brake delivery products compete with TI Automotive, Sanoh, Martinrea, Maruyasu and SeAH, among others. Our fluid transfer products compete with Conti-Tech, Hutchinson, Teklas, Tristone, Akwel and Fränkische, among others.

Joint Ventures and Strategic Alliances

Joint ventures represent an important part of our business, both operationally and strategically. We have utilized joint ventures to enter and expand in geographic markets such as China, India and Thailand, to acquire new customers and to develop new technologies. When entering new geographic markets, teaming with a local partner can reduce capital investment by leveraging pre-existing infrastructure. In addition, local partners in these markets can provide knowledge and insight into local practices and access to local suppliers of raw materials and components.

The following table shows our significant unconsolidated joint ventures as of December 31, 2023:

| | | | | | | | | | | |

| Country | Name | Product Line | Ownership Percentage |

| Thailand | Nishikawa Tachaplalert Cooper Ltd. | Sealing systems | 20% |

| India | Polyrub Cooper Standard FTS Private Limited | Fluid transfer systems | 35% |

| United States | Nishikawa Cooper LLC | Sealing systems | 40% |

| China | Yantai Leading Solutions Auto Parts Co., Ltd. | Fuel and brake delivery systems | 50% |

| China | Shenya Sealing (Guangzhou) Company Limited | Sealing and fluid transfer systems | 51% |

Research and Development

We have a dedicated team of technical and engineering resources for each product line, some of which are located at our customers’ facilities. We utilize simulation, digital tools, best practices, standardization and track key process indicators to drive efficiency in execution with an emphasis on manufacturability and quality. Our development teams work closely with our customers to design and deliver innovative solutions, unique for their applications. Amounts spent on engineering, research and development, and program management were as follows:

| | | | | | | | | | | | | | |

| Year | | Amount | | Percentage of Sales |

| (Dollar amounts in millions) |

| 2023 | | $84.1 | | 3.0% |

| 2022 | | $80.5 | | 3.2% |

| 2021 | | $90.0 | | 3.9% |

Intellectual Property

We believe that one of our key competitive advantages is our ability to translate customer needs and our ideas into innovation through the development of intellectual property. We hold a significant number of patents and trademarks worldwide.

Our patents are grouped into two major categories: (1) specific product invention claims and (2) specific manufacturing processes that are used for producing products. The vast majority of our patents fall within the product invention category. We consider these patents to be of value and seek to protect our rights throughout the world against infringement. While in the aggregate these patents are important to our business, we do not believe that the loss or expiration of any one patent would materially affect our Company. We continue to seek patent protection for our new products and we develop significant technologies that we treat as trade secrets and choose not to disclose to the public through the patent process. These technologies nonetheless provide significant competitive advantages and contribute to our global leadership position in various markets. We believe that our trademarks, including FlushSeal™, Gen III Posi-Lock®, Easy-Lock®, MagAlloy®, Ergo-Lock® +, PlastiCool® and Fortrex™, help differentiate us and lead customers to seek our partnership.

We also have technology sharing and licensing agreements with various third parties, including Nishikawa Rubber Company, one of our joint venture partners in sealing products. We have mutual agreements with Nishikawa Rubber Company for sales, marketing and engineering services on certain sealing products. Under those agreements, each party pays for services provided by the other and royalties on certain products for which the other party provides design or development services. We also have licensing and joint development agreements for commercial applications of our Fortrex™ chemistry platform in non-automotive industries. A joint development agreement has also been put in place for the collaborative creation of novel dynamic fluid control products and systems.

Innovation, Materials, and Product Lifecycle

The international response to risks and opportunities of climate change is transforming our global economy. Our most significant opportunity to contribute to this low-carbon and circular economy is through reducing the environmental impact of our products and manufacturing processes. We purposefully apply sustainable principles in the design and production of our

products, reducing the environmental impact from sourcing through end-of-life. These efforts also enable our customers to reduce their environmental impacts.

When obtaining or innovating materials for our products, we seek to sustainably source raw materials, increase the use of recycled content or recyclable material where feasible, decrease our use of hazardous chemicals where possible, and properly disclose restricted materials to customers and regulators. We believe our culture of innovation is a key differentiator, allowing us to compete and succeed within our dynamic global markets.

Supplies and Raw Materials

Cooper Standard is committed to building strong relationships with our supply partners. We recognize the importance of engaging with suppliers to create value for our customers.

The principal raw materials for our business include synthetic and natural rubber, carbon black, process oils, and plastic resins. Principal procured components are primarily made from plastic, carbon steel, aluminum and stainless steel. We manage the procurement of our direct and indirect materials to assure supply continuity and to obtain the most favorable total cost. Procurement arrangements include short-term and long-term supply agreements that may contain formula-based pricing based on commodity indices. These arrangements provide quantities needed to satisfy normal manufacturing demands. We believe we have adequate sources for the supply of raw materials and components for our products with suppliers located around the world.

Raw material prices are susceptible to fluctuations which may place operational and profitability burdens on the entire supply chain. Following the pandemic, market prices for key raw materials, such as steel, aluminum, and oil-derived

commodities, experienced a period of extreme volatility, which led to significant cost increases for our business in 2021 and

2022. In response, we worked with our customers throughout 2022 and 2023 to implement or expand index-based commercial

agreements that have enabled us to partially recover incremental material costs incurred and significantly reduced our exposure

and risk related to commodity price fluctuations going forward. Global commodity markets and pricing have stabilized to a

large degree in 2023 and into the beginning of 2024.

Seasonality

Within the automotive industry, sales to OEMs are lowest during the months prior to model changeovers or during assembly plant shutdowns. Automotive production is traditionally reduced during July, August and year-end holidays, and our quarterly results may reflect these trends. However, economic conditions and consumer demand may change the traditional seasonality of the industry. In recent years, for example, global light vehicle production, inventory and consumer demand all experienced extreme dislocations from historic norms due to the global COVID-19 pandemic and related restrictions on production and consumer activity. Post-pandemic, global light vehicle production continued to be negatively impacted by widespread supply chain disruptions, limiting the global automotive OEM’s ability to rebuild inventory and meet pent-up consumer demand.

Backlog

Our OEM sales are generally based upon purchase orders issued by the OEMs, with updated releases for volume adjustments. As such, we typically do not have a firm and definitive backlog of orders at any point in time. Once selected to supply products for a particular platform, we typically supply those products for the platform life, which is normally five to eight years, although there is no guarantee that this will occur. In addition, when we are the incumbent supplier to a given platform, we believe we have a competitive advantage in winning the redesign or replacement platform, although there is no guarantee that this will occur.

Human Capital and Safety

As of December 31, 2023, we had approximately 23,000 employees, including 3,000 contingent workers. We maintain good relations with both our union and non-union employees and, in the past ten years, have not experienced any major work stoppages.

Our people have always been the driving force of value at Cooper Standard. We continue to embrace new ways of working, a growing international movement for civil rights, and our unwavering dedication to keeping our employees healthy and safe has only made them more critical to our success. We accomplish this by developing the capabilities of our employees through continuous learning and performance management processes. Additionally, building an internal talent pipeline supports the achievement of this priority. In 2023, our internal fill rate was approximately 36%. This metric, which is based on salaried, director-level positions and above, helps us to understand where employees are advancing in their careers and the effectiveness of our internal development programs. For 2023, our voluntary employee turnover rate was approximately 15%. We believe that our culture and continued effort to provide our employees with growth opportunities contributes to retaining our strong talent.

In addition, we aim to diversify our workforce because we recognize the value of engaging different opinions and backgrounds in a global company. We are committed to recruiting, developing and retaining a high-performing and diverse workforce. A global measurement for our diversity is women in the company and women in leadership. In 2023, women made up approximately 40% of our workforce. Of our leadership positions, defined as vice president positions and above, women held approximately 24% of such roles.

Safety continues to be a top priority and primary focus of management. An emphasis on reducing workplace incidents helps Cooper Standard to maintain a safe workforce and continue to deliver world class results for product quality. In 2023, our total incident rate (“TIR”) was 0.32, which represents an Occupational Safety and Health Administration measurement of on-the-job injuries in relation to total hours worked. Based on our review of industry peer sustainability reports, we have a lower TIR relative to our peer group. Additionally, throughout the COVID-19 pandemic, we have remained focused on protecting the health and safety of our employees while meeting the needs of our customers.

Community Involvement

Supported by the Cooper Standard Foundation, our employees are highly engaged in their local communities. The Foundation’s mission is to strengthen the communities where Cooper Standard employees work and live through the passionate support of children’s charities, education, health and wellness, and community revitalization. The Cooper Standard Foundation is a 501(c)(3) organization with oversight by its Board of Directors, Board of Trustees and Philanthropic Committee. For more information on the Company’s community involvement, please visit our Corporate Responsibility Report located on the Cooper Standard website.

Environmental, Social and Governance (ESG)

In 2023, the Company was named to Newsweek’s list of America’s Most Responsible Companies for the fifth consecutive year and achieved Ecovadis Silver Status for sustainability efforts that also earned the Company recognition from Nissan for sustainability and social responsible practices. These awards are a further testament to Cooper Standard’s commitment to ESG topics, including our core value of integrity.

Cooper Standard considers itself a steward of the environment, and we monitor the environmental impact of our business and products. We prioritize our environmental management as a means of driving and sustaining excellence. We are subject to a broad range of federal, state, and local environmental and occupational safety and health laws and regulations in the United States and other countries, including regulations governing: emissions to air, discharges to water, noise and odor emissions; the generation, handling, storage, transportation, treatment, reclamation and disposal of chemicals and waste materials; the cleanup of contaminated properties; and human health and safety. We have made, and will continue to make, expenditures to comply with environmental requirements. While our costs to defend and settle known claims arising under environmental laws have not been material in the past and are not currently estimated to have a material adverse effect on our financial condition, such costs could be material to our financial statements in the future. Further details regarding our commitments and contingencies are provided in Note 20. “Contingent Liabilities” to the consolidated financial statements included in Item 8. “Financial Statements and Supplementary Data” of this Annual Report on Form 10-K (the “Report”).

Market Data

Certain market data and other statistical information used throughout this Annual Report on Form 10-K is based on data from independent firms such as S&P Global. Other data is based on good faith estimates, which are derived from our review of internal analyses, as well as third-party sources. Although we believe these third-party sources are reliable, we have not independently verified the information and cannot guarantee its accuracy and completeness. To the extent that we have been unable to obtain information from third-party sources, we have expressed our belief on the basis of our own internal analyses of our products and capabilities in comparison to our competitors.

Available Information

We make available free of charge on our website (www.cooperstandard.com) our Annual Report on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to those reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934, as amended, (the “Exchange Act”), as soon as reasonably practicable after we electronically file such material with, or furnish it to, the U.S. Securities and Exchange Commission (“SEC”). Our reports filed with the SEC also may be found on the SEC’s website at www.sec.gov. We may also use our website as a distribution channel of material company information. Neither the information on our website nor the information on the SEC’s website is incorporated by reference into this Report unless expressly noted.

Forward-Looking Statements

This Annual Report on Form 10-K includes “forward-looking statements” within the meaning of U.S. federal securities laws, and we intend that such forward-looking statements be subject to the safe harbor created thereby. Our use of words “estimate,” “expect,” “anticipate,” “project,” “plan,” “intend,” “believe,” “outlook,” “guidance,” “forecast,” or future or conditional verbs, such as “will,” “should,” “could,” “would,” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. All forward-looking statements are based upon our current expectations and various assumptions. Our expectations, beliefs, and projections are expressed in good faith and we believe there is a reasonable basis for them. However, we cannot assure you that these expectations, beliefs and projections will be achieved. Forward-looking statements are not guarantees of future performance and are subject to significant risks and uncertainties that may cause actual results or achievements to be materially different from the future results or achievements expressed or implied by the forward-looking statements. Among other items, such factors may include: volatility or decline of the Company’s stock price, or absence of stock price appreciation; impacts and disruptions related to the wars in Ukraine and the Middle East; our ability to achieve commercial recoveries and to offset the adverse impact of higher commodity and other costs through pricing and other negotiations with our customers; work stoppages or other labor disruptions with our employees or our customers’ employees; prolonged or material contractions in automotive sales and production volumes; our inability to realize sales represented by awarded business; escalating pricing pressures; loss of large customers or significant platforms; our ability to successfully compete in the automotive parts industry; availability and increasing volatility in costs of manufactured components and raw materials; disruption in our supply base; competitive threats and commercial risks associated with our diversification strategy; possible variability of our working capital requirements; risks associated with our international operations, including changes in laws, regulations, and policies governing the terms of foreign trade such as increased trade restrictions and tariffs; foreign currency exchange rate fluctuations; our ability to control the operations of our joint ventures for our sole benefit; our substantial amount of indebtedness and variable rates of interest; our ability to obtain adequate financing sources in the future; operating and financial restrictions imposed on us under our debt instruments; the underfunding of our pension plans; significant changes in discount rates and the actual return on pension assets; effectiveness of continuous improvement programs and other cost savings plans; significant costs related to manufacturing facility closings or consolidation; our ability to execute new program launches; our ability to meet customers’ needs for new and improved products; the possibility that our acquisitions and divestitures may not be successful; product liability, warranty and recall claims brought against us; laws and regulations, including environmental, health and safety laws and regulations; legal and regulatory proceedings, claims or investigations against us; the potential impact of any future public health events on our financial condition and results of operations; the ability of our intellectual property to withstand legal challenges; cyber-attacks, data privacy concerns, other disruptions in, or the inability to implement upgrades to, our information technology systems; the possible volatility of our annual effective tax rate; the possibility of a failure to maintain effective controls and procedures; the possibility of future impairment charges to our goodwill and long-lived assets; our ability to identify, attract, develop and retain a skilled, engaged and diverse workforce; our ability to procure insurance at reasonable rates; and our dependence on our subsidiaries for cash to satisfy our obligations.

You should not place undue reliance on these forward-looking statements. Our forward-looking statements speak only as of the date of this Annual Report on Form 10-K and we undertake no obligation to publicly update or otherwise revise any forward-looking statement, whether as a result of new information, future events or otherwise, except where we are expressly required to do so by law.

This Annual Report on Form 10-K also contains estimates and other information that is based on industry publications, surveys and forecasts. This information involves a number of assumptions and limitations, and we have not independently verified the accuracy or completeness of the information.

Item 1A. Risk Factors

We have listed below (not necessarily in order of importance or probability of occurrence) the most significant risk factors that could cause our actual results to vary materially from recent or anticipated results and could materially and adversely affect our business, results of operations, financial condition and cash flows.

Operational Risks

Our business, financial condition and results of operations may be adversely impacted by the effects of inflation.

Inflation has the potential to adversely affect our business, financial condition and results of operations by increasing our overall cost structure. Other inflationary pressures could affect wages, the cost and availability of components and raw materials and other inputs and our ability to meet customer demand. Inflation may further exacerbate other risk factors, including supply chain disruptions, risks related to international operations and the recruitment and retention of qualified employees. If we are

unsuccessful in negotiating pricing adjustments with our customers to raise the prices of our products sufficiently to keep up with the rate of inflation, our profit margins and cash flows may be adversely affected.

Increases in the costs, or reduced availability, of raw materials and manufactured components may adversely affect our profitability.

Raw material costs can be volatile. The principal raw materials to produce our products include synthetic and natural rubber, carbon black, process oils, and plastic resins. Principal procured components are primarily made from plastic, carbon steel, aluminum and stainless steel. Material costs represented approximately 51% of our total cost of products sold in 2023. The costs and availability of raw materials and manufactured components can fluctuate due to factors beyond our control, including as a result of existing and potential changes to U.S. policies related to global trade and tariffs. Further, climate change may have an adverse impact on global temperatures, weather patterns, and the frequency and severity of extreme weather and natural disasters, which may adversely affect the availability or pricing for certain raw materials including natural rubber. A significant increase in the price of raw materials, or a restriction in their availability, could materially increase our operating costs and adversely affect our profitability because it is generally difficult to pass through these increased costs to our customers. While we entered into index pricing agreements with some of our customers which provide for a price adjustment based on quoted market prices to attempt to address some of these risks (notably with respect to steel and rubber), there can be no assurance that commodity price fluctuations will not adversely affect our results of operations and cash flows. In addition, while the use of index pricing adjustments may provide us with some protection from adverse fluctuations in commodity prices, by utilizing these instruments, we potentially forego the benefits that might result from favorable fluctuations in price.

Disruptions in the supply chain could have an adverse effect on our business, financial condition, results of operations and cash flows.

We obtain components and other products and services from numerous suppliers and other vendors throughout the world. We are responsible for managing our supply chain, including suppliers that may be the sole sources of products that we require, that our customers direct us to use or that have unique capabilities that would make it difficult and/or expensive to re-source. In certain instances, entire industries may experience short-term capacity constraints. Any significant disruptions in the automotive industry due to industry-wide parts shortages and global supply chain constraints could adversely affect our operations and financial performance. Uncertain economic or industry conditions resulting from such supply chain constraints could result in financial distress within our supply base, thereby further increasing the risk of supply disruption. Furthermore, any economic downturn or other unfavorable conditions in one or more of the regions in which we operate could cause supply disruptions and thereby adversely affect our financial condition, operating results and cash flows.

Work stoppages or other disruptions to our operations could negatively affect our operations and financial performance.

We may experience work stoppages caused by labor disputes under existing collective bargaining agreements or in connection with the negotiation of new agreements given that we have a number of agreements that expire in any given year. Further, there is no certainty that we will be successful in negotiating new collective bargaining agreements that extend beyond the current expiration dates or that new agreements will be on terms as favorable to us as past labor agreements. In addition, it is possible that our workforce will become more unionized in the future. Unionization activities could increase our costs, which could negatively affect our results of operations.

Our operations may also be disrupted by other labor issues, including absenteeism, public health events and government restrictions; major equipment failure with prolonged downtime or a complete loss of critical equipment where either no other comparable equipment exists or the remaining equipment does not have enough capacity to pick up the demand; or natural disaster-related plant closures or disruptions. In particular, natural disasters and adverse weather conditions can be caused or exacerbated by climate change.

Regardless of the cause, any significant disruption to our production could negatively affect our operations, customer relationships and financial performance. Similar disruptions at one or more of our suppliers or our customers’ suppliers could adversely affect our operations if an alternative source of supply were not readily available. Additionally, similar disruptions at our customers’ facilities could result in reduced demand for our products causing us to delay or cancel production and could have an adverse effect on our business.

A disruption in, or the inability to successfully implement upgrades to, our information technology systems, including disruptions relating to cybersecurity as well as data privacy concerns, could adversely affect our business and financial performance.

We rely upon information technology networks, systems and processes, including the information technology networks of third parties such as suppliers and joint venture partners, to manage and support our business. We have implemented a number

of procedures and practices designed to protect against breaches or failures of our systems. Despite the security measures that we have implemented, including those measures to prevent cyber-attacks, our systems could be breached or damaged by computer viruses or unauthorized physical or electronic access. Like other public companies, our computer systems and those of our third-party vendors, partners and service providers are regularly subject to, and will continue to be the target of, computer viruses, malware or other malicious codes (including ransomware), unauthorized access, cyber-attacks or other computer-related penetrations which may cause disruptions to our operations. While we have experienced threats to our data and systems, to date, we are not aware that we have experienced a cybersecurity incident that has materially affected our business strategy, results of operations, or financial condition. Over time, however, the sophistication of these threats continues to increase. The preventative actions we take to reduce the risk of cyber incidents and protect our information may be insufficient. A breach of our information technology systems, or those of the third parties on whom we rely, could result in theft of our intellectual property, disruption to business or unauthorized access to customer or personal information. Such a breach could adversely impact our operations and/or our reputation and may cause us to incur significant time and expense to cure or remediate the breach.

Further, we continually update and expand our information technology systems to enable us to run our business more efficiently, including the potential incorporation of traditional and generative A.I. solutions into our information systems and processes. The increasing use and evolution of this technology creates potential risks for loss or misuse of sensitive Company data that forms part of any data set that was collected, used, stored, or transferred to run our business, and unintentional dissemination or intentional destruction of confidential information stored in our or our third party providers' systems, portable media or storage devices, which may result in significantly increased business and security costs, a damaged reputation, administrative penalties, or costs related to defending legal claims. In addition, if the content, analyses, or recommendations that A.I. programs assist in producing are or are alleged to be deficient, inaccurate, or biased, our business, financial condition, and results of operations and our reputation may be adversely affected. If these systems are not implemented successfully and in a timely, cost-effective, compliant and responsible manner, our operations and business could be disrupted and our ability to report accurate and timely financial results could be adversely affected.

An inability to effectively manage the timing, quality and costs of new program launches could adversely affect our financial performance.

In connection with the award of new business, we may obligate ourselves to deliver new products that are subject to our customers’ timing, performance and quality standards. Given the number and complexity of new program launches, we may experience difficulties managing product quality, timeliness and associated costs. In addition, new program launches require a significant ramp up of costs. Our sales related to these new programs generally are dependent upon the timing and success of our customers’ introduction of new vehicles. An inability to effectively manage the timing, quality and costs of these new program launches could adversely affect our financial condition, operating results and cash flows.

Our success depends in part on our development of improved products, and our efforts may fail to meet the needs of customers on a timely or cost-effective basis.

Our continued success depends on our ability to maintain advanced technological capabilities and knowledge necessary to adapt to changing market demands, as well as to develop and commercialize innovative products. We may be unable to develop new products successfully or to keep pace with technological developments by our competitors and the industry in general, which in recent years includes the rapid development and rising use of digital, A.I. and machine learning technologies. In addition, we may develop specific technologies and capabilities in anticipation of customers’ demands for new innovations and technologies. If such demand does not materialize, we may be unable to recover the costs incurred in the development of such technologies and capabilities. If we are unable to recover these costs or if any such programs do not progress as expected, our business, results of operations and financial condition could be adversely affected.

We may incur material losses and costs as a result of product liability and warranty and recall claims that may be brought against us.

We may be exposed to product liability and warranty claims in the event that our products actually or allegedly fail to perform as specified or expected or the use of our products results, or is alleged to result, in bodily injury and/or property damage. Accordingly, we could experience material warranty or product liability expenses in the future and incur significant costs to defend against these claims. In addition, if any of our products are, or are alleged to be, defective, we may be required to participate in a recall of that product if the defect or the alleged defect relates to automotive safety. Product recalls could cause us to incur material costs and could harm our reputation or cause us to lose customers, particularly if any such recall causes customers to question the safety or reliability of our products. Also, while we possess considerable historical warranty and recall data with respect to the products we currently produce, we do not have such data relating to new products, assembly programs or

technologies, including any new fuel and emissions technology and systems being brought into production, to allow us to accurately estimate future warranty or recall costs.

In addition, the increased focus on systems integration platforms utilizing fuel and emissions technology with more sophisticated components from multiple sources could result in an increased risk of component warranty costs over which we have little or no control and for which we may be subject to an increasing share of liability to the extent any of the other component suppliers are in financial distress or are otherwise incapable of fulfilling their warranty or product recall obligations. Our costs associated with providing product warranties and responding to product recall claims could be material. Product liability, warranty and recall costs may adversely affect our business, results of operations and financial condition.

Our commitment to drive value through culture, innovation and results is dependent on our ability to identify, attract, develop and retain a skilled, engaged and diverse workforce.

Our people are the driving force behind our success at Cooper Standard. Our ability to pursue breakthrough technology innovations, implement cutting-edge manufacturing and business processes, and achieve our operating and strategic goals is dependent on the engagement, skills, experience and knowledge of our employees. Any failure or delay in attracting, retaining and developing such a workforce, including the loss of key technological and leadership personnel, could adversely impact our business, financial condition and operating results.

Our financial condition and results of operations have been previously, and may in the future be, adversely affected by public health events.

We could face risks related to public health events, including epidemics and pandemics like the recent COVID-19 pandemic. Preventative measures taken to contain or mitigate public health events (including, but not limited to, vaccination, social distancing policies, restrictions on travel and reduced operations and extended closures of many businesses and institutions) may materially impact our financial condition and operations results due to shutdowns of our and our customers’ and suppliers’ facilities; increased operating and production costs; disruptions and financial distress in the supply chain; disruptions in our production cycle; lost or absent members of the workforce; a decline in demand due to an economic downturn; and inability to access capital due to disruptions in the global financial markets.

The full impact of another public health event on our financial condition and operations results will depend on various factors, such as the ultimate duration and scope of the crisis, its impact on our customers, suppliers and logistics partners, how quickly normal operations can resume and the duration and magnitude of the economic downturn caused by the health crisis in our key markets. A public health event may also exacerbate the other risks disclosed in this Item 1A. Risk Factors.

Strategic Risks

We are highly dependent on the automotive industry. A prolonged or material contraction in automotive sales and production volumes could adversely affect our business, results of operations and financial condition.

Automotive sales and production are cyclical and depend on, among other things, general economic conditions and consumer spending, vehicle demand and preferences (which can be affected by a number of factors, including fuel costs, employment levels and the availability of consumer financing). These factors could make it difficult for us, our suppliers and our customers to forecast accurately and plan future business activities. As the volume of automotive production and the mix of vehicles produced fluctuate, the demand for our products also fluctuates. Prolonged or material contraction in automotive sales and production volumes, or significant changes in the mix of vehicles produced, could cause our customers to reduce orders of our products, which could adversely affect our business, results of operations and financial condition and our ability to provide accurate forecasts and guidance.

We may not realize sales represented by awarded business, which could adversely affect our business, financial condition, results of operations and cash flows.

The realization of future sales from awarded business is subject to risks and uncertainties inherent in the cyclicality of vehicle production. In addition, our customers generally have the right to resource awarded business without penalty. Therefore, the ultimate amount of our sales is not guaranteed. If actual production orders from our customers are not consistent with the projections we use in calculating the amount of awarded business, we could realize substantially less sales and profit over the life of these awards than currently projected.

Pricing pressures may adversely affect our business.

Vehicle manufacturers often seek price reductions in both the initial bidding process and during the term of the contract. Price reductions historically have adversely impacted our sales and profit margins and may do so in the future. If we are not able

to offset price reductions through improved operating efficiencies and reduced expenditures, those price reductions may have a negative impact on our financial condition.

Our business could be adversely affected if we lose any of our largest customers or significant platforms.

While we provide parts to virtually every major global OEM for use on a wide range of different platforms, sales to our three largest customers, Ford, GM, and Stellantis, on a worldwide basis represented approximately 55% of our sales for the year ended December 31, 2023. Our ability to reduce the risks inherent in certain concentrations of business will depend, in part, on our ability to continue to diversify our sales on a customer, product, platform and geographic basis. Although business with each customer is typically split among numerous contracts, the loss of a major customer, significant reduction in purchases of our products by such customer, or any discontinuance or resourcing of a significant platform could adversely affect our business, results of operations and financial condition.

We operate in a highly competitive industry and efforts by our competitors to gain market share could adversely affect our financial performance.

The automotive parts industry is highly competitive. We face numerous competitors in each of our product lines. In general, there are three or more significant competitors and numerous smaller competitors for most of the products we offer. We also face competition for certain of our products from suppliers producing in lower-cost regions such as Asia and Eastern Europe. Our competitors’ efforts to grow market share could exert downward pressure on the pricing of our products and our margins.

The benefits of our continuous improvement programs and other cost savings plans may not be fully realized.

Our operations strategy includes continuous improvement programs and implementation of lean manufacturing tools across all facilities to achieve cost savings and increased performance. Further, we have and may continue to initiate restructuring actions designed to improve future profitability and competitiveness. The cost savings that we anticipate from these initiatives may not be achieved on schedule or at the level we anticipate. If we are unable to realize these anticipated savings, our operating results and financial condition may be adversely affected.

We may continue to incur significant costs related to manufacturing facility closings or consolidation which could have an adverse effect on our financial condition.

If we close or consolidate manufacturing locations, the exit costs associated with such closures or consolidation, including employee termination costs, may be significant. Such costs could negatively affect our cash flows, results of operations and financial condition.

We are subject to other risks associated with our international operations.

We have significant manufacturing operations outside the United States, including joint ventures and other alliances. Our operations are located in 21 countries, and we export to several other countries. In 2023, approximately 78% of our sales were attributable to products manufactured outside the United States. Risks inherent in our international operations include:

•currency exchange rate fluctuations, currency controls and restrictions, and the ability to hedge currencies;

•changes in local economic conditions;

•repatriation restrictions or requirements, including tax increases on remittances and other payments by our foreign subsidiaries;

•global sovereign fiscal uncertainty and hyperinflation in certain foreign countries;

•changes in laws and regulations, including laws or policies governing the terms of foreign trade, and in particular increased trade restrictions, tariffs, or taxes or the imposition of embargoes on imports from countries where we manufacture products;

•operating in foreign jurisdictions where the ability to protect and enforce our intellectual property rights is limited as a statutory or practical matter;

•exposure to possible expropriation or other government actions;

•disease, pandemics or other severe public health events; and

•exposure to local political or social unrest including resultant acts of war, terrorism, or similar events, including the wars in Ukraine and the Middle East and the related sanctions imposed on Russia.

The occurrence of any of these risks may adversely affect the results of operations and financial condition of our international operations and our business as a whole.

In addition, we are subject to the Foreign Corrupt Practices Act (the “FCPA”) and other laws which prohibit improper payments to foreign governments and their officials by U.S. and other business entities. Certain of the countries in which we operate present heightened corruption risks, which therefore increases the risks of our exposure under the FCPA and other applicable anti-bribery and corruption laws and regulations.

A portion of our operations are conducted by joint ventures which have unique risks.

Certain of our operations are carried out by joint ventures. In joint ventures, we share the management of the company with one or more partners who may not have the same goals, resources or priorities as we do. The operations of our joint ventures are subject to agreements with our partners, which typically include additional organizational formalities as well as requirements to share information and decision making and may also limit our ability to sell our interest. Additional risks include one or more partners failing to satisfy contractual obligations, a change in ownership of any of our partners and our limited ability to control our partners’ compliance with applicable laws, including the FCPA. Any such occurrences could adversely affect our financial condition, operating results, cash flow or reputation.

Any acquisitions or divestitures we make may be unsuccessful, may take longer than anticipated or may negatively impact our business, financial condition, results of operations and cash flows.

We may pursue acquisitions or divestitures in the future as part of our strategy. Acquisitions and divestitures involve numerous risks, including identifying attractive target acquisitions, undisclosed risks affecting the target, difficulties integrating acquired businesses, the assumption of unknown liabilities, potential adverse effects on existing customer or supplier relationships, and the diversion of management’s attention from day-to-day business. We may not have, or be able to raise on acceptable terms, sufficient financial resources to make acquisitions. Our ability to make investments may also be limited by the terms of our existing or future financing arrangements. Any acquisitions or divestitures we pursue may not be successful or prove to be beneficial to our operations and cash flow.

Financial Risks

Global, market and economic conditions could impact our ability to access liquidity sources.

Our continued access to sources of liquidity depends on multiple factors, including global economic conditions, public health events and any global supply chain disruptions on our customers and their production rates, the costs of raw materials, the state of the overall automotive industry, the condition of global financial markets, the availability of sufficient amounts of financing, our operating performance and cash flows and our credit ratings. In particular, the global automotive industry is susceptible to uncertain economic conditions that could adversely impact new vehicle demand and production, and business conditions may vary significantly from period to period or region to region. In recent years, global automotive production was negatively impacted by lingering impacts of the COVID-19 pandemic and broad supply chain challenges stemming, in part, from a sharp rebound in overall industrial demand. Further, rising inflation, interest rates and supply chain challenges contributed to global economic uncertainty. In addition, continuing military actions in Eastern Europe and the Middle East are having broad negative impacts on key sectors of the global economy. Our business is also directly affected by the automotive vehicle production rates in North America, Europe, Asia Pacific and South America which have been adversely impacted by a series of events in recent years.

Our ability to borrow against our senior asset-based revolving credit facility (the “ABL Facility”) is limited to our borrowing base, which consists primarily of our U.S. and Canadian accounts receivable and inventory. Production shutdowns or disruptions in both the United States and Canada could lead to significant reductions in these working capital balances and significantly decrease our ability to borrow under our ABL Facility.

In addition, if the Company has borrowing availability under its ABL Facility less than the greater of (i) $15.0 million and (ii) 10% of the Borrowing Base (as defined in the ABL Facility), it must be in compliance with a springing Fixed Charge Coverage Ratio maintenance covenant of 1.00:1.00. Any adverse effects on the Company’s business due to global, market and economic conditions may adversely impact the Company’s ability to satisfy such covenant. As of December 31, 2023, there were no obligations outstanding under the ABL Facility, the Company’s borrowing base was $169.5 million and the monthly fixed charge coverage ratio was at a level that provided the Company full access to the borrowing base. Net of $7.1 million of outstanding letters of credit, the Company effectively had $162.4 million available for borrowing under its ABL Facility.

Furthermore, production shutdowns or disruptions will result in working capital swings which could result in increased outflows. As a result of current ecomonic conditions and global supply chain disruptions, we may be required to raise additional capital, and our access to and cost of financing will depend on, among other things, our performance, changing global economic conditions, conditions in the global financing markets, the availability of sufficient amounts of financing, our prospects and our credit ratings. Such capital may not be available on favorable terms or at all.

The ongoing situations in Ukraine and Russia and the Middle East and related disruptions could adversely affect our liquidity, business, and results of operations.

The ongoing military conflict between Russia and Ukraine and the resulting sanctions have caused, and are currently expected to continue to cause, significant disruptions to the global financial system, international trade, and the transportation and energy sectors, among others. The impacts of the conflict on the supply chain and commodity prices are expected to be profound and have resulted and may continue to result in substantial inflation in one or more countries (or globally). In addition, the recent Israel-Hamas war and escalating tensions in the Middle East could affect oil prices and have other, potentially recessionary, effects on the global economy. Prolonged inflationary conditions and periods of high interest rates could further negatively affect U.S. and international commerce and exacerbate or further extend the period of high energy prices and supply chain constraints. These and other issues resulting from the global economic slowdown and financial market turmoil have adversely affected and may continue to adversely affect the automotive industry, which may lead to a decline in the general demand for our products and erosion of their procurement or sale prices. We do not have operations in Ukraine, Russia or the Middle East, nor do we sell into these markets. Nonetheless, if the global economic slowdown and the Russia-Ukraine and Israel-Hamas wars continue, our liquidity, business, and results of operations may continue to be adversely affected.

We have a substantial amount of indebtedness, which could have a material adverse effect on our financial condition and our ability to obtain financing in the future and to react to changes in our business.

We have a significant amount of indebtedness. As of December 31, 2023, we had total indebtedness of $1,095 million. Our substantial amount of debt and our debt service obligations could limit our ability to satisfy our obligations, limit our ability to operate our business and impair our competitive position. For example, it could:

•make it more difficult for us to satisfy our obligations;

•increase our vulnerability to general adverse economic and industry conditions, including interest rate fluctuations, because a portion of our borrowings accrues interest at variable rates;

•require us to dedicate a substantial portion of our cash flows from operations to payments on our debt and debt service obligations, which would reduce the availability of cash to fund working capital, capital expenditures, research and development efforts, acquisitions or other general corporate purposes;

•limit our flexibility in planning for, or reacting to, changes in our business and the markets in which we compete;

•place us at a disadvantage compared to competitors that may have less debt; and

•limit our ability to obtain additional debt or equity financing for working capital, capital expenditures, research and development efforts, debt service requirements, acquisitions and general corporate purposes.