Mining Opportunities April 7, 2008 Howard Weil Energy Conference Bennett K. Hatfield President and CEO Exhibit 99.1 |

2 Mining Opportunities Statements that are not historical fact are forward-looking statements and may involve a number of risks and uncertainties. We have used the words “anticipate” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project” and similar terms and phrases, including references to assumptions, in this presentation to identify forward-looking statements. These forward-looking statements are made based on expectations and beliefs concerning future events affecting us and are subject to uncertainties and factors relating to our operations and business environment, all of which are difficult to predict and many of which are beyond our control, that could cause our actual results to differ materially from those matters expressed in or implied by these forward-looking statements. The following factors are among those that may cause actual results to differ materially from our forward-looking statements: market demand for coal, electricity and steel; availability of qualified workers; future economic or capital market conditions; weather conditions or catastrophic weather-related damage; our production capabilities; the consummation of financing, acquisition or disposition transactions and the effect thereof on our business; our plans and objectives for future operations and expansion or consolidation; our ability to obtain permits; our relationships with, and other conditions affecting, our customers; the availability and costs of key supplies or commodities such as diesel fuel, steel, explosives and tires; prices of fuels which compete with or impact coal usage, such as oil and natural gas; timing of reductions or increases in customer coal inventories; long- term coal supply arrangements; risks in coal mining; unexpected maintenance and equipment failure; environmental, safety and other laws and regulations, including those directly affecting our coal mining and production, and those affecting our customers’ coal usage; competition; railroad, barge, trucking and other transportation availability, performance and costs; employee benefits costs and labor relations issues; replacement of our reserves; our assumptions concerning economically recoverable coal reserve estimates; availability and costs of credit, surety bonds and letters of credit; title defects or loss of leasehold interests in our properties which could result in unanticipated costs or inability to mine these properties; future legislation and changes in regulations or governmental policies or changes in interpretations thereof, including with respect to safety enhancements; the impairment of the value of our goodwill; the ongoing effect of the Sago mine explosion; and our liquidity, results of operations and financial condition; the adequacy and sufficiency of our internal controls and legal and administrative proceedings, settlements, investigations and claims. You should keep in mind that any forward-looking statement made by us in this presentation speaks only as of the date on which we make it. See also the “Risk Factors” of our 2007 Annual Report on Form 10-K, which is currently available on our website at www.intlcoal.com. New risks and uncertainties arise from time to time, and it is impossible for us to predict these events or how they may affect us. We have no duty to, and do not intend to, update or revise the forward-looking statements in this presentation except as may be required by law. In light of these risks and uncertainties, you should keep in mind that any forward-looking statement made in this presentation might not occur. All data presented herein is as of December 31, 2007, unless otherwise noted. Forward-Looking Statements |

3 Mining Opportunities International demand has reshaped the US coal market – Strong export growth appears sustainable through 2009 & beyond – Imports expected to decline Domestic supply-demand “rebalancing” is underway – Lower Eastern production due to regulatory constraints and depletion – Improved electricity demand for coal driven by lower nuclear output and high natural gas prices – International dynamics add momentum and support Outlook indicates pricing strength has substantial duration Although US economic challenges pose some risk, coal demand is expected to be fairly resilient Overview of Current Coal Markets |

4 Mining Opportunities Broad supply constraints Australia’s export infrastructure continues to constrain output, with situation exacerbated by recent flooding South African utility Eskom facing chronic coal shortages that are expected to temper exports for at least 2 years Russia’s and Ukraine’s production issues continue Political instability discourages reliance on Venezuela Strong demand growth Remarkable demand growth in China will likely make them a net importer going forward India’s critical coal shortages are forcing sharp increase in imports; forward demand expected to outstrip domestic production growth International Market Issues |

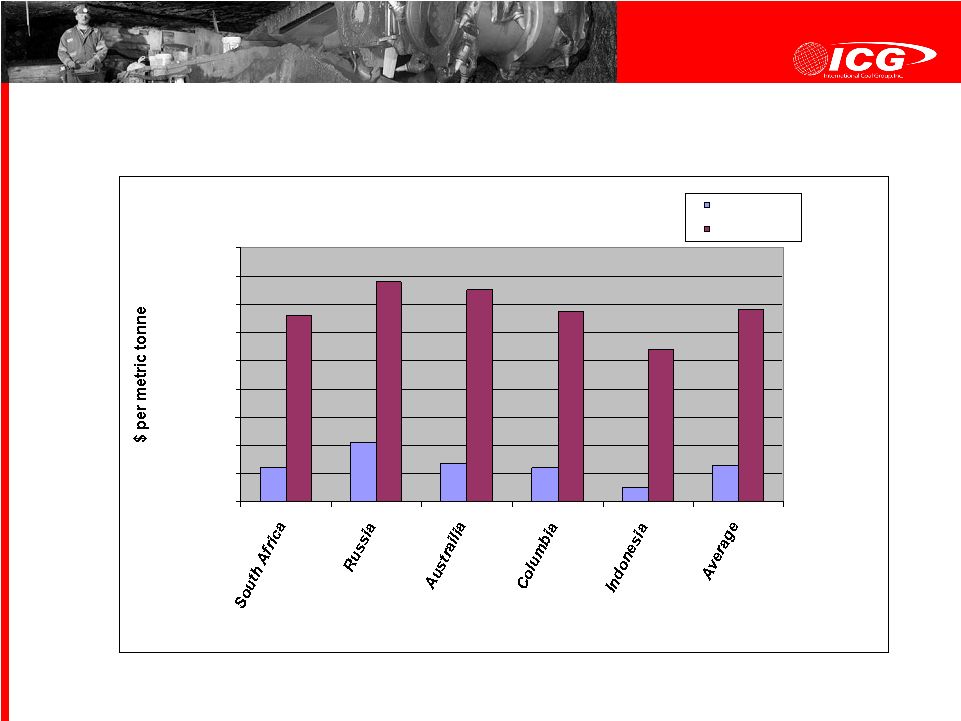

5 Mining Opportunities International FOB Vessel Prices $'s per Metric Ton $40.00 $50.00 $60.00 $70.00 $80.00 $90.00 $100.00 $110.00 $120.00 $130.00 Origin Country March, 2007 February, 2008 Selected World Price Trends |

6 Mining Opportunities Supply response to rising demand will likely face significant impediments to increasing Eastern production - Environmental activists will continue to challenge and litigate most new mining permit approvals, regardless of regulatory concessions, which will significantly extend Army Corps permitting timeframes; - Increased MSHA scrutiny of mine plans and heightened enforcement will continue to hinder productivity – particularly at underground mines - Labor shortages are significant, particularly in Southern WV coal fields - Appalachian production is down 3% YTD 2008 (per EIA) US coal demand will likely continue to grow Electricity output up 0.6% YTD (EEI) High natural gas prices and lower nuclear generation are expected to increase pressure on coal fired electrical generating plants Domestic Market Issues |

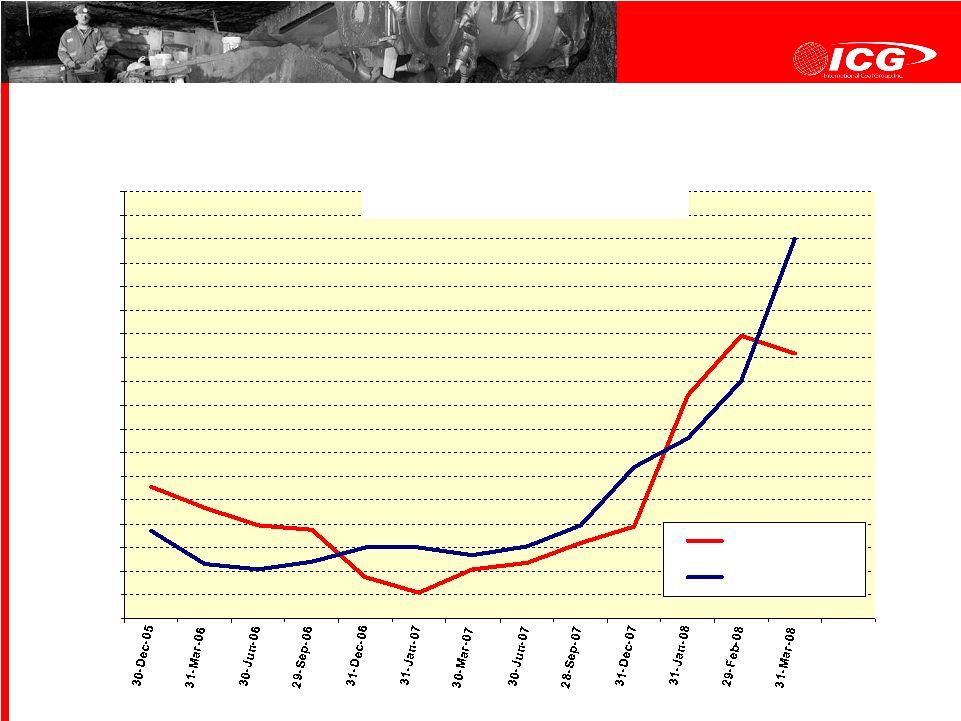

7 Mining Opportunities Prompt Month Spot Prices End of Month Values per ICAP United, Inc. $30.00 $35.00 $40.00 $45.00 $50.00 $55.00 $60.00 $65.00 $70.00 $75.00 $80.00 $85.00 $90.00 $95.00 $100.00 $105.00 $110.00 $115.00 $120.00 CSX 12500 1.6# Pitt 8 13000 3.4# US Spot Prices Are Up Sharply |

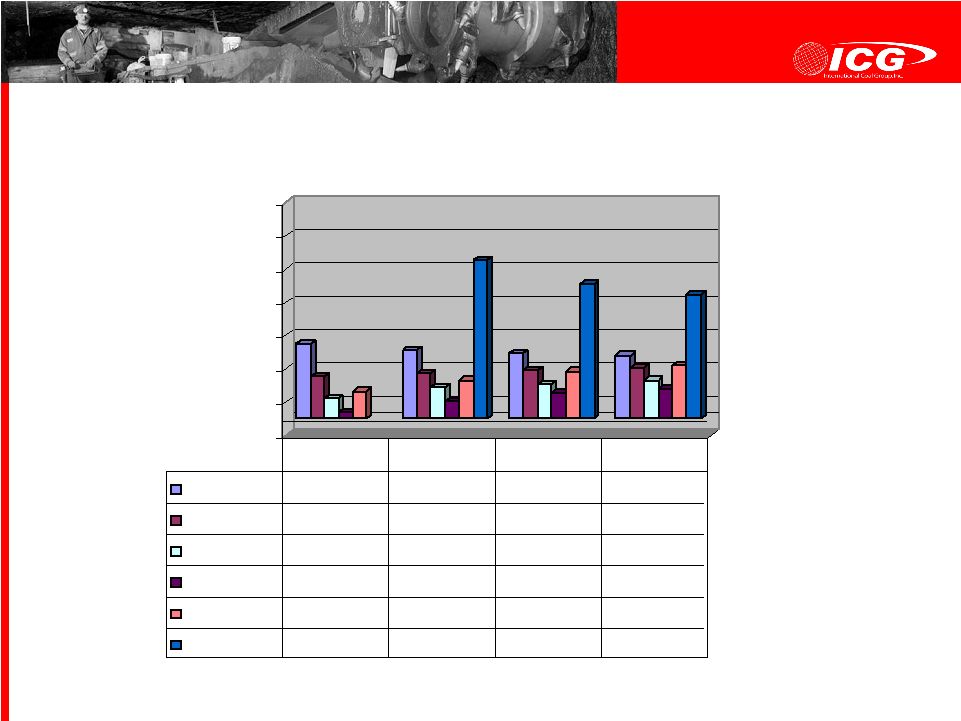

8 Mining Opportunities $30.00 $40.00 $50.00 $60.00 $70.00 $80.00 $90.00 $100.00 CAPP 12500 <1% Forward Prices 31-Jan-06 $57.50 $55.50 $54.75 $54.00 30-Sep-06 $47.85 $48.75 $49.50 $50.25 31-Dec-06 $41.25 $44.50 $45.50 $46.50 31-Jan-07 $37.00 $40.25 $42.75 $44.00 31-Jul-07 $43.25 $46.50 $49.35 $51.10 31-Mar-08 $82.75 $75.50 $72.25 2007 2008 2009 2010 Term Prices Are Also Strong |

9 Mining Opportunities Continued growth in coal demand to supply US and international energy needs Increased supply discipline as producers should have learned hard lessons from demand swings of 2005-07 Significant impediments to production expansion Build-out of scrubbers by Eastern utilities should generally favor Appalachian region coals over PRB – Higher BTU and lower transportation cost will be key advantages – Eastern supply expected to remain tight & pricing firm Overall strengthening of industry through consolidation General Outlook for Coal Industry |

10 Mining Opportunities Overview of International Coal Group |

11 Mining Opportunities Well-positioned with operations in 3 of 4 largest US coal producing regions Extensive reserve base (69% owned) supports internal growth opportunities Substantial holdings of metallurgical quality coal Growth strategy targeted toward higher margin metallurgical and premium steam coal markets 100% union free workforce Solid balance sheet with minimal long-term legacy liabilities Large investment grade customer base Key ICG Highlights Summary Statistics Market capitalization : $970.9 million Coal reserves: 964 million tons Reserve life: Approximately 55 years Employees: 2,330 2007 tons sold: 18.3 million 2007 tons produced: 16.4 million Notes: 1 Market capitalization is based on 152.9 million shares outstanding and a stock price of $6.35 as of March 31, 2008. 1 |

12 Mining Opportunities 12 active mining complexes - 7 in Central Appalachia, 4 in Northern Appalachia, and 1 in Illinois Basin 3 mine complexes (Raven, Sentinel and Beckley) opened within last 18 months; Tygart #1 expected to open by late 2009 Current and Future Operations ICG Illinois Illinois Kentucky Ohio Beckley West Virginia Virginia MD East Kentucky Flint Ridge Hazard Knott County Raven Eastern Buckhannon Sentinel Tygart Valley #1 Vindex Patriot Jennie Creek Current Operations Future Operations ADDCAR ICG Corporate |

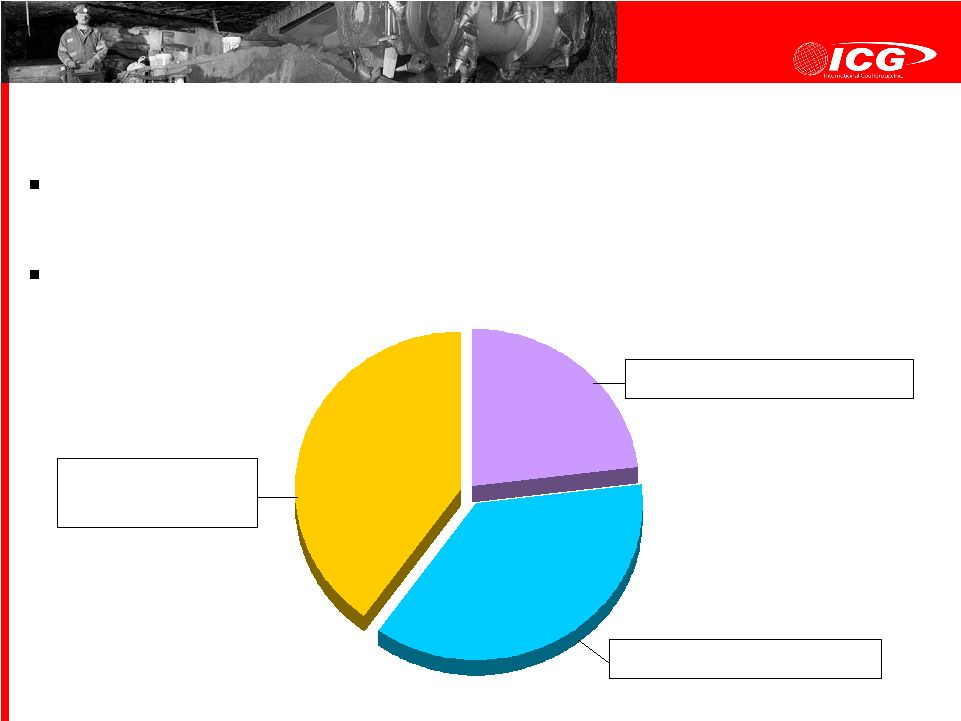

13 Mining Opportunities ICG controls 964 million tons of high-quality reserves that are primarily high BTU, low sulfur steam and metallurgical coal CAPP/NAPP reserves of 578 million tons are 55% met quality High-Caliber Reserve Base CAPP, 221 million tons NAPP, 357 million tons Illinois Basin, 386 million tons 40% 23% 37% |

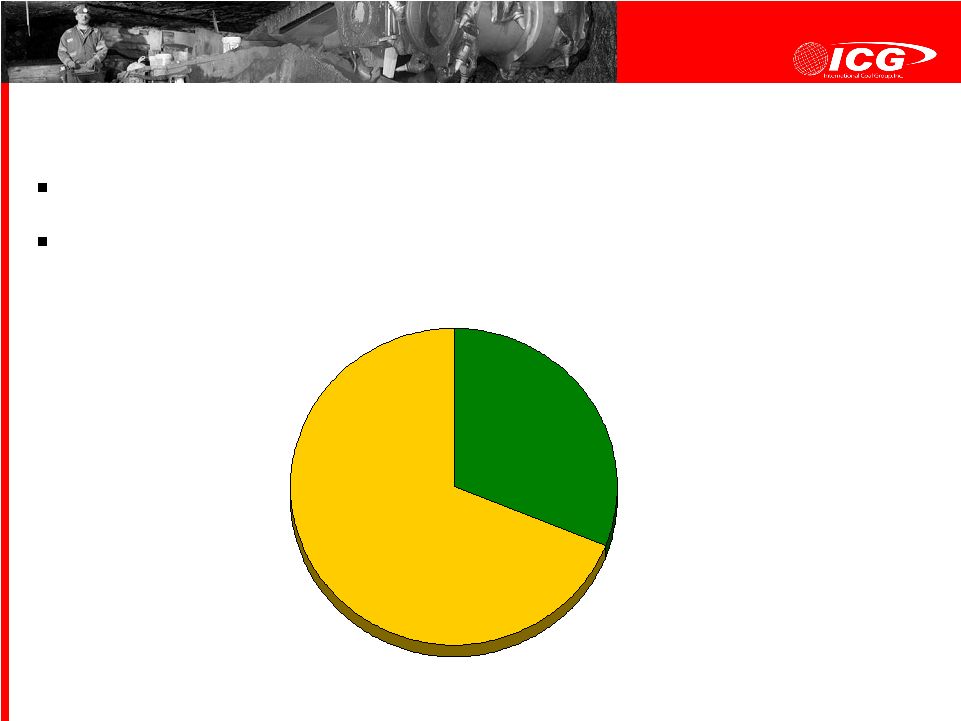

14 Mining Opportunities Total Reserve Profile: Owned vs. Leased 69% 31% Leased 298 million tons ICG ownership % is among largest of publicly traded peers Peer group median ownership is less than 30% Owned 666 million tons |

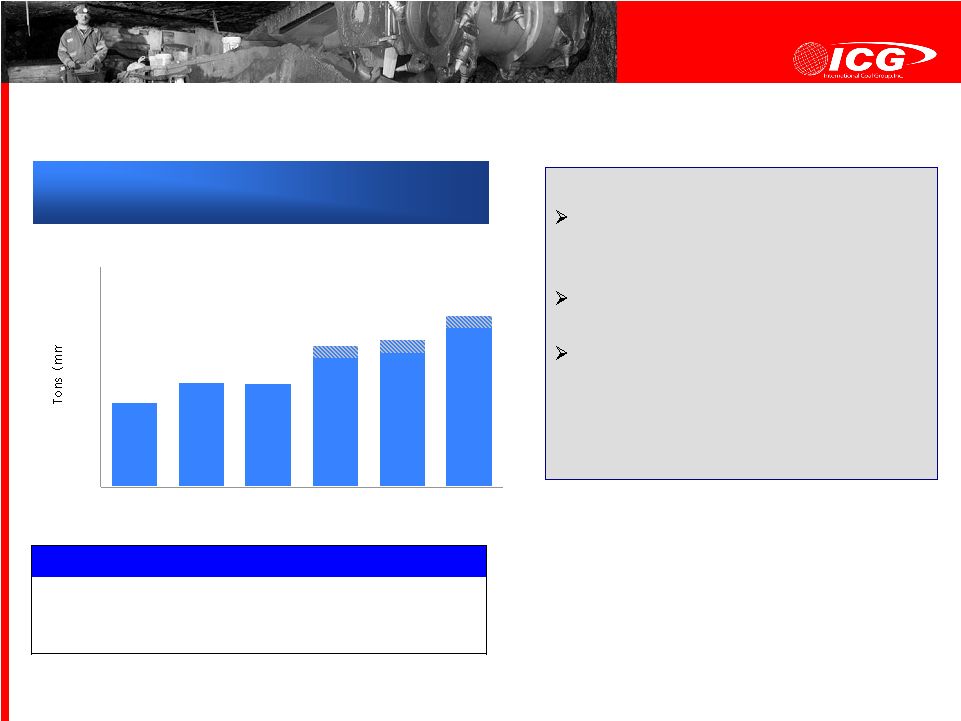

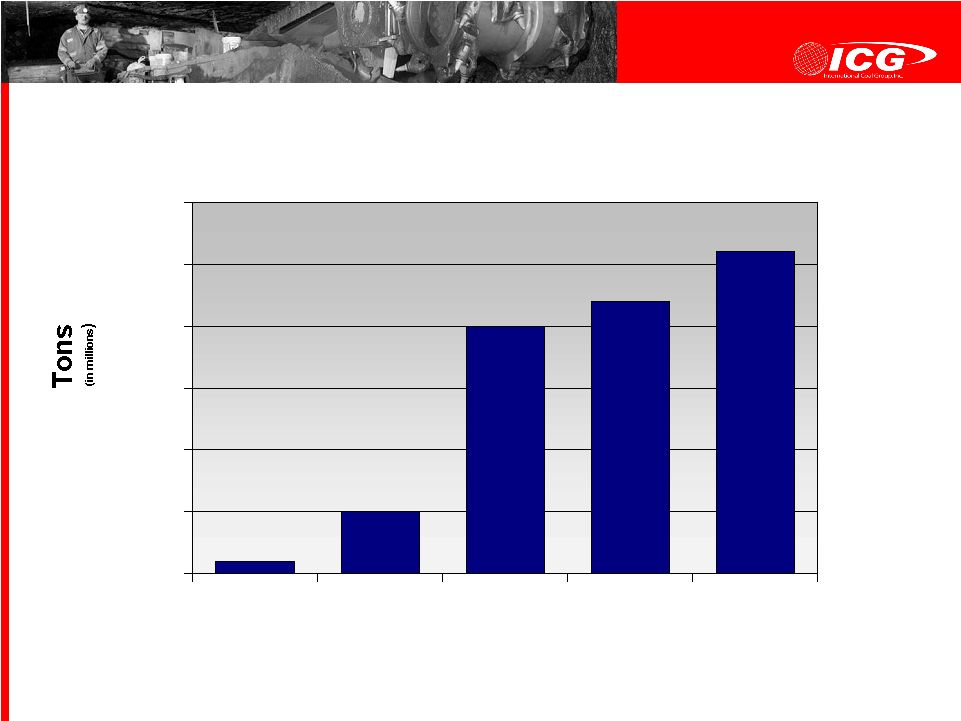

15 Mining Opportunities Projected Production 2008-2010 16.40 16.50 14.90 8 10 12 14 16 18 20 22 24 26 2005 2006 2007 2008 2009 2010 Note: 1 2005 pro forma for acquisition of Anker / CoalQuest 2 Per management guidance as of 3/31/08 CAPP 66% 68% 68% 66% 66% 64% NAPP 19% 19% 19% 22% 21% 24% ILB 15% 13% 13% 12% 13% 12% Production by Region 1 Target projects that create high margin production Key focus: increase met tons Three mine complexes developed in past 18 months added 3.9 million annual tons production capacity 18.5-19.5 19-20 21-22 2 Production Plans Call For Selective Growth |

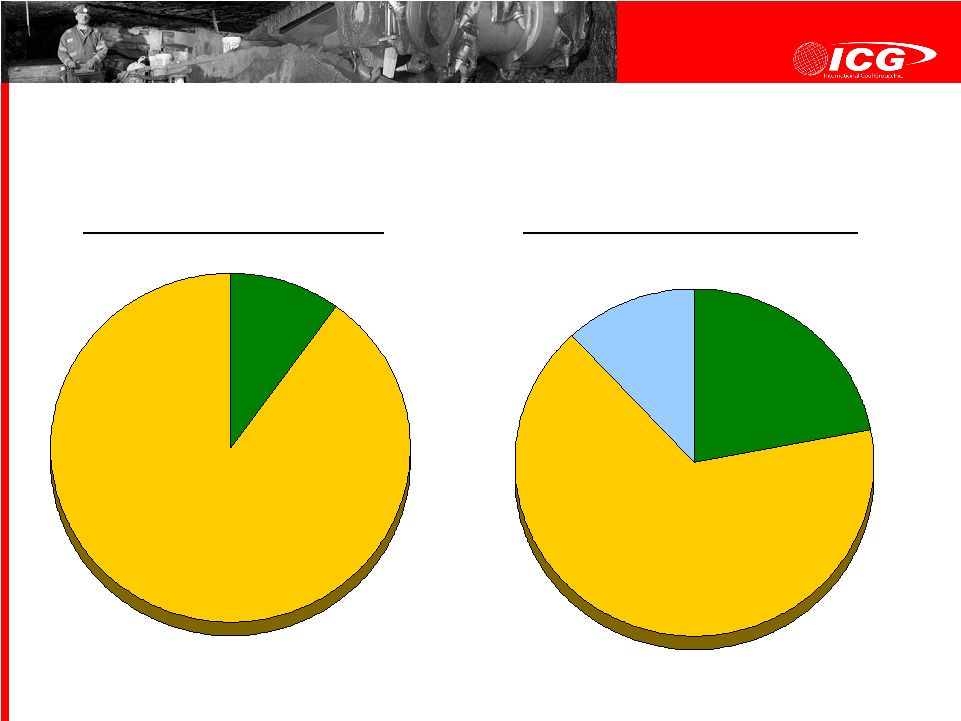

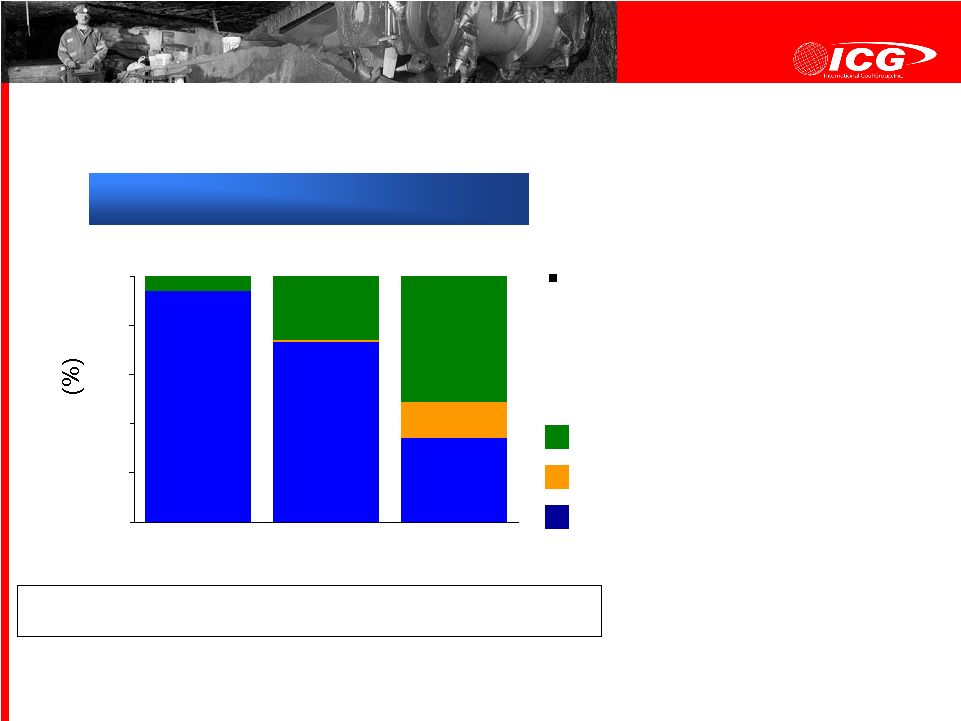

16 Mining Opportunities Production By Type Production By Region 2008 Production Profile 22% NAPP 66% CAPP 12% ILB 10% Met 90% Steam |

17 Mining Opportunities 2.6 2.2 2.0 0.5 0.1 0.0 0.5 1.0 1.5 2.0 2.5 3.0 2006 2007 2008 2009 2010 Increasing Metallurgical Coal Production |

18 Mining Opportunities 0 500 1,000 1,500 2,000 2,500 3,000 3,500 2006 Actual 2007 Projected 2008 Projected Year Thermal Met Total Exports Increasing Export Sales |

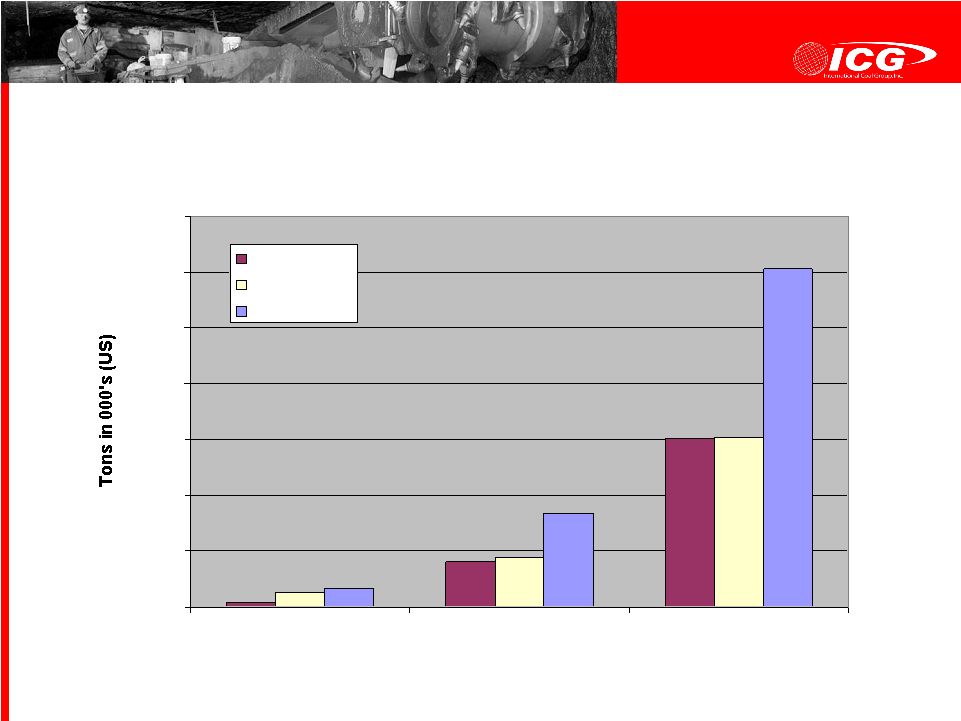

19 Mining Opportunities Projected Sales 19.5-20.5 20.0-21.0 21.0-22.0 (mm tons) Committed Tonnage Strong committed sales level for 2008-2009, yet substantial room for upside from market improvement 2 Note: 1 Committed tonnages for 2008-2010 are estimated as of 03/31/08 2 Per management guidance as of 03/31/08 94 73 34 1 15 6 26 51 0 20 40 60 80 100 2008 2009 2010 Favorable Sales Position Uncommitted Committed (subject to re-pricing) Committed and priced 1 |

20 Mining Opportunities Maintain a prudent capital structure and flexible balance sheet to support multiple internal growth initiatives Pursue measured growth initiatives through the development of owned and controlled reserves Maintain financial flexibility for the possible acquisition of reserves and/or operations Financial and Investment Strategy |

21 Mining Opportunities Cash and equivalents (in millions) $ 107.2 Debt (in millions): Credit facility $ 0 - matures June 2011 10.25% Senior Notes 175.0 - matures July 2014 9% Convertible Senior Notes 225.0 - matures August 2012 Other debt 12.3 - matures on various dates $412.3 Debt-to-capitalization ratio of 44.4% Debt-to-market capitalization ratio of 33.5% Credit Agreement statistics: – Borrowing capacity of $100 million (requirements reduced by Convertible Notes) – $70.0 million of letters-of-credit outstanding, no other draws – $30.0 million of borrowing capacity remains – In compliance with all debt covenants Capital Structure as of December 31, 2007 |

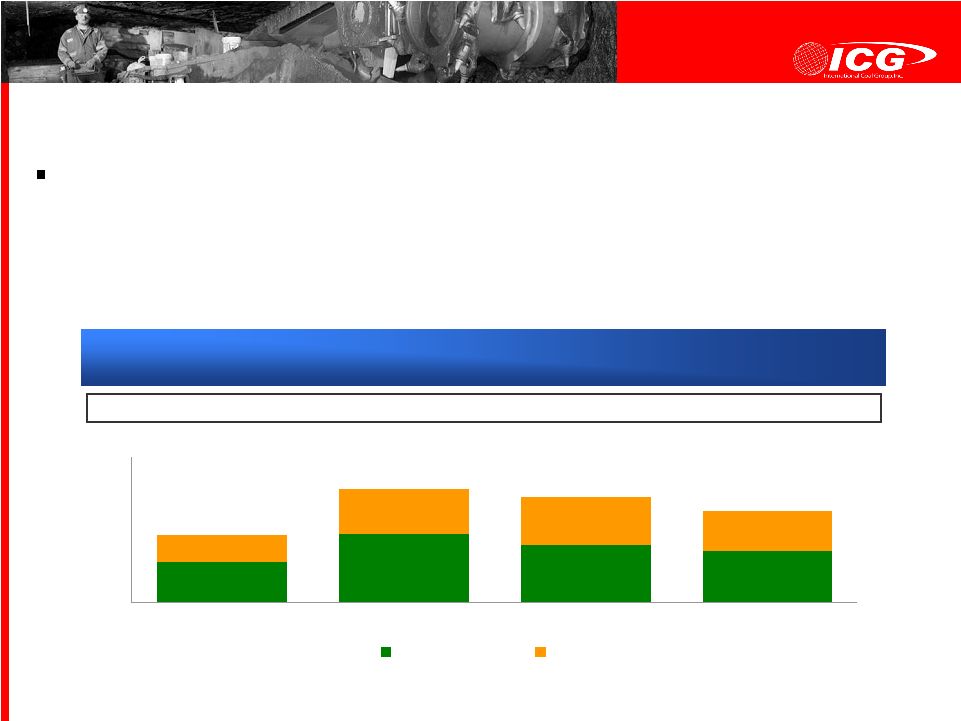

22 Mining Opportunities Projected 2008 capital spending of $157 million includes: – Completion of the Sentinel and Beckley projects – Initial site development & slope construction at Tygart #1 Complex – Continued upgrading of equipment & facilities at other ICG operations Capital Expenditures Capital Expenditures ($mm) 60% 60% 55% 57% 43% 45% 40% 40% 0 50 100 150 200 250 2005 2006 2007 2008 Maintenance Growth Total $116 $196 $181 $157 Frcst. Frcst. . |

23 Mining Opportunities We anticipate substantial performance upside due to favorable timing of new met operations ICG expects to benefit from entering the strong 2008 market period with high uncommitted steam tonnage We intend to continue layering in new contracts to balance risk and enhance revenue stability Capital spending prioritizes development of higher margin reserves, favoring met quality and owned properties Summary |

24 Mining Opportunities Thank You! |