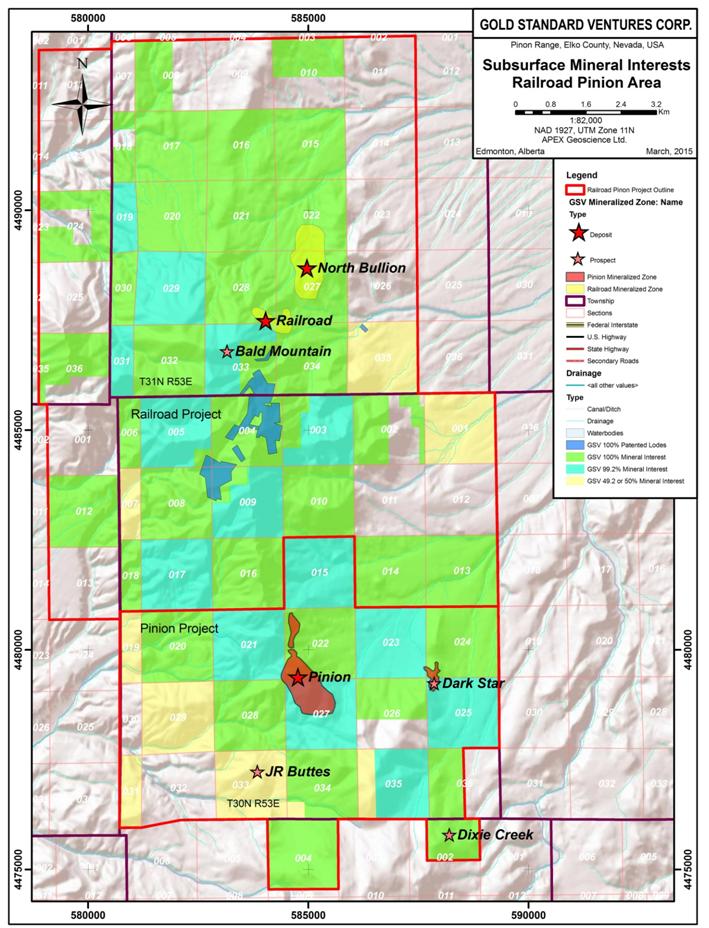

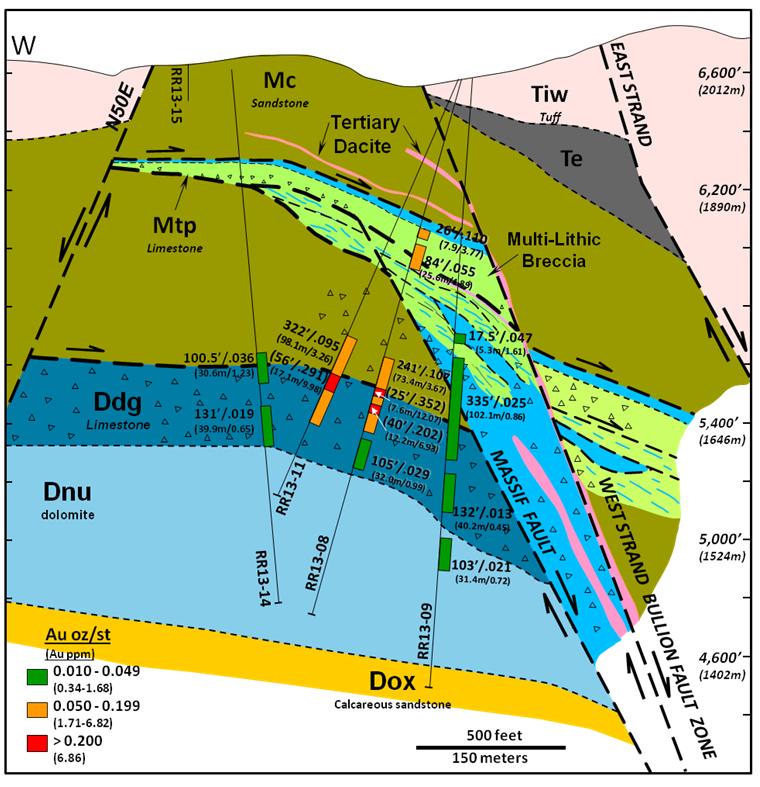

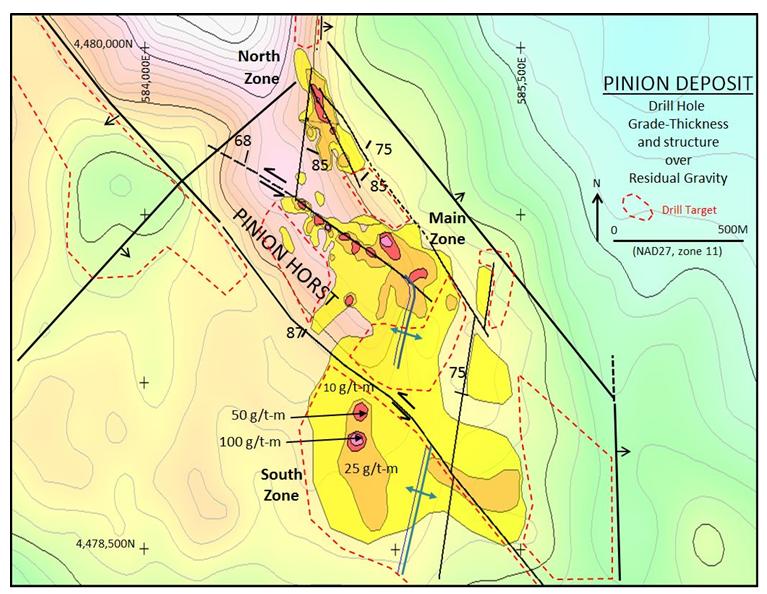

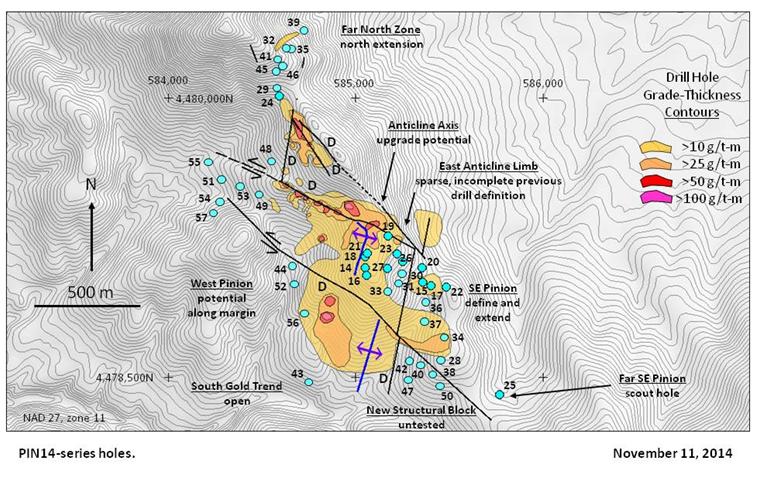

The main target areas tested included to the southeast, south, west, northwest and north of the existing resource at the Pinion Deposit (Figure 10.7). Some infill drilling was completed in the south-central portion of the Main Zone in order to extend the gold zone in gaps where prior historic drilling was not completed to the currently modelled depth of the gold zone or where mineralization was complicated by faults. See Figure 10.8 below extracted from the 2015 Railroad-Pinion Report.

The Phase 2 drilling targeted multilithic, dissolution collapse breccia within the highly permeable, silicified, and oxidized breccia which is favorably sandwiched between relatively impermeable silty micrite of the overlying Mississippian Tripon Pass Formation and thick-bedded calcarenite of the underlying Devils Gate Formation. All 44 holes drilled in late 2014, intersected multilithic dissolution collapse breccia with 38 of the 44 holes returning significant gold intercepts of at least 0.3 ppm or 0.009 oz/st over at least 6.1 m (20 ft). The highlights of the drill holes are provided in Table 10.7 below extracted from the 2015 Railroad-Pinion Report.

Only two holes (PIN14-48 and PIN14-55) drilled in the Phase 2 Program failed to intersect significant gold mineralization. These two holes were drilled to extend gold mineralization to the northwest of the Pinion Deposit. A further four holes intersected only weak gold mineralization over a variety of widths (<0.2 ppm over thicknesses ranging from 6.1 m up to 70 m). Three of these holes (PIN14-49, PIN14-51 and PIN14-53) were drilled to extend the Pinion gold zone to the northwest. One of the holes, PIN14-46, was drilled to extend gold mineralization of the North Zone to the north.

Table 10.7: 2014 Phase 2 Pinion Deposit Drilling Intersection Highlights.

| Hole Number | From (m) | To (m) | Length (m) | From (ft) | To (ft) | Length (ft) | Au (oz/st) | Au (ppm) |

| PIN14-14 | 173.74 | 195.07 | 21.34 | 570 | 640 | 70 | 0.015 | 0.51 |

| PIN14-14 | 173.74 | 195.07 | 21.34 | 570 | 640 | 70 | 0.015 | 0.51 |

| including | 173.74 | 190.50 | 16.76 | 570 | 625 | 55 | 0.018 | 0.62 |

| and | 242.32 | 256.03 | 13.72 | 795 | 840 | 45 | 0.006 | 0.19 |

| PIN14-15 | 0.00 | 4.57 | 4.57 | 0 | 15 | 15 | 0.006 | 0.21 |

| | 74.68 | 161.54 | 86.87 | 245 | 530 | 285 | 0.007 | 0.23 |

| including | 74.68 | 115.82 | 41.15 | 245 | 380 | 135 | 0.009 | 0.32 |

| PIN14-16 | 216.41 | 272.80 | 56.39 | 710 | 895 | 185 | 0.015 | 0.52 |

| including | 217.93 | 251.46 | 33.53 | 715 | 825 | 110 | 0.023 | 0.80 |

| PIN14-17 | 99.06 | 115.82 | 16.76 | 325 | 380 | 55 | 0.006 | 0.22 |

| and | 134.11 | 156.97 | 22.86 | 440 | 515 | 75 | 0.011 | 0.37 |

| PIN14-18 | 153.92 | 185.93 | 32.00 | 505 | 610 | 105 | 0.066 | 2.25 |

| including | 178.31 | 184.40 | 6.10 | 585 | 605 | 20 | 0.114 | 3.90 |

| PIN14-19 | 176.78 | 291.08 | 114.30 | 580 | 955 | 375 | 0.016 | 0.55 |

| including | 176.78 | 202.69 | 25.91 | 580 | 665 | 85 | 0.020 | 0.69 |

| including | 184.40 | 198.12 | 13.72 | 605 | 650 | 45 | 0.033 | 1.14 |

| and | 231.65 | 291.08 | 59.44 | 760 | 955 | 195 | 0.017 | 0.60 |

| including | 260.60 | 271.27 | 10.67 | 855 | 890 | 35 | 0.036 | 1.23 |

| PIN14-20 | 126.49 | 190.50 | 64.01 | 415 | 625 | 210 | 0.007 | 0.24 |

| including | 126.49 | 152.40 | 25.91 | 415 | 500 | 85 | 0.011 | 0.39 |

| PIN14-21 | 161.54 | 196.60 | 35.05 | 530 | 645 | 115 | 0.040 | 1.36 |

| PIN14-22 | 3.05 | 10.67 | 7.62 | 10 | 35 | 25 | 0.008 | 0.27 |

| | 179.83 | 182.88 | 3.05 | 590 | 600 | 10 | 0.023 | 0.78 |

| PIN14-23 | 188.98 | 225.55 | 36.58 | 620 | 740 | 120 | 0.007 | 0.25 |

| including | 188.98 | 193.55 | 4.57 | 620 | 635 | 15 | 0.019 | 0.65 |

| and | 205.74 | 220.98 | 15.24 | 675 | 725 | 50 | 0.010 | 0.33 |

| PIN14-24 | 0.00 | 134.11 | 134.11 | 0 | 440 | 440 | 0.006 | 0.20 |

| including | 0.00 | 97.54 | 97.54 | 0 | 320 | 320 | 0.007 | 0.23 |

| including | 1.52 | 18.29 | 16.76 | 5 | 60 | 55 | 0.015 | 0.50 |

| PIN14-25 | 259.08 | 309.37 | 50.29 | 850 | 1015 | 165 | 0.012 | 0.42 |

| including | 278.89 | 298.70 | 19.81 | 915 | 980 | 65 | 0.023 | 0.81 |

| and | 377.95 | 408.43 | 30.48 | 1240 | 1340 | 100 | 0.007 | 0.25 |

| PIN14-26 | 193.55 | 275.84 | 82.30 | 635 | 905 | 270 | 0.008 | 0.28 |

| including | 193.55 | 225.55 | 32.00 | 635 | 740 | 105 | 0.017 | 0.58 |

| including | 193.55 | 202.69 | 9.14 | 635 | 665 | 30 | 0.044 | 1.49 |

| PIN14-27 | 175.26 | 213.36 | 38.10 | 575 | 700 | 125 | 0.022 | 0.74 |

| including | 176.78 | 184.40 | 7.62 | 580 | 605 | 25 | 0.065 | 2.22 |

| PIN14-28 | 160.02 | 188.98 | 28.96 | 525 | 620 | 95 | 0.013 | 0.44 |

| PIN14-29 | 65.53 | 85.34 | 19.81 | 215 | 280 | 65 | 0.006 | 0.21 |

| PIN14-30 | 176.78 | 262.13 | 85.34 | 580 | 860 | 280 | 0.004 | 0.15 |

| including | 176.78 | 199.64 | 22.86 | 580 | 655 | 75 | 0.008 | 0.28 |

| including | 176.78 | 181.36 | 4.57 | 580 | 595 | 15 | 0.017 | 0.60 |

| and | 192.02 | 199.64 | 7.62 | 630 | 655 | 25 | 0.014 | 0.46 |

| PIN14-31 | 160.02 | 193.55 | 33.53 | 525 | 635 | 110 | 0.032 | 1.08 |

| including | 166.12 | 176.78 | 10.67 | 545 | 580 | 35 | 0.066 | 2.26 |

| PIN14-32 | 65.53 | 88.39 | 22.86 | 215 | 290 | 75 | 0.011 | 0.36 |

| including | 70.10 | 80.77 | 10.67 | 230 | 265 | 35 | 0.018 | 0.61 |

| and | 115.82 | 120.40 | 4.57 | 380 | 395 | 15 | 0.007 | 0.23 |

| PIN14-33 | 182.88 | 230.12 | 47.24 | 600 | 755 | 155 | 0.008 | 0.26 |

| including | 182.88 | 199.64 | 16.76 | 600 | 655 | 55 | 0.018 | 0.61 |

| PIN14-34 | 124.97 | 172.21 | 47.24 | 410 | 565 | 155 | 0.009 | 0.30 |

| including | 152.40 | 172.21 | 19.81 | 500 | 565 | 65 | 0.013 | 0.46 |

| PIN14-35 | 86.87 | 118.87 | 32.00 | 285 | 390 | 105 | 0.014 | 0.49 |

| including | 86.87 | 91.44 | 4.57 | 285 | 300 | 15 | 0.081 | 2.79 |

| PIN14-36 | 36.58 | 53.34 | 16.76 | 120 | 175 | 55 | 0.022 | 0.75 |

| including | 38.10 | 45.72 | 7.62 | 125 | 150 | 25 | 0.035 | 1.22 |

| and | 77.72 | 134.11 | 56.39 | 255 | 440 | 185 | 0.005 | 0.17 |

| including | 86.87 | 111.25 | 24.38 | 285 | 365 | 80 | 0.008 | 0.26 |

| PIN14-37 | 53.34 | 65.53 | 12.19 | 175 | 215 | 40 | 0.021 | 0.71 |

| including | 53.34 | 56.39 | 3.05 | 175 | 185 | 10 | 0.058 | 1.99 |

| and | 123.44 | 224.03 | 100.58 | 405 | 735 | 330 | 0.007 | 0.23 |

| including | 126.49 | 135.64 | 9.14 | 415 | 445 | 30 | 0.016 | 0.56 |

| including | 164.59 | 170.69 | 6.10 | 540 | 560 | 20 | 0.019 | 0.65 |

| PIN14-38 | 202.69 | 268.22 | 65.53 | 665 | 880 | 215 | 0.026 | 0.90 |

| including | 222.50 | 257.56 | 35.05 | 730 | 845 | 115 | 0.044 | 1.52 |

| including | 243.84 | 249.94 | 6.10 | 800 | 820 | 20 | 0.198 | 6.78 |

| PIN14-39 | 108.20 | 170.69 | 62.48 | 355 | 560 | 205 | 0.004 | 0.15 |

| including | 134.11 | 156.97 | 22.86 | 440 | 515 | 75 | 0.007 | 0.24 |

| PIN14-40 | 76.20 | 82.30 | 6.10 | 250 | 270 | 20 | 0.010 | 0.34 |

| and | 160.02 | 210.31 | 50.29 | 525 | 690 | 165 | 0.009 | 0.30 |

| including | 196.60 | 208.79 | 12.19 | 645 | 685 | 40 | 0.015 | 0.52 |

| PIN14-41 | 15.24 | 71.63 | 56.39 | 50 | 235 | 185 | 0.006 | 0.21 |

| including | 96.01 | 105.16 | 9.14 | 315 | 345 | 30 | 0.008 | 0.27 |

| PIN14-42 | 80.77 | 91.44 | 10.67 | 265 | 300 | 35 | 0.011 | 0.39 |

| and | 152.40 | 239.27 | 86.87 | 500 | 785 | 285 | 0.014 | 0.47 |

| including | 170.69 | 198.12 | 27.43 | 560 | 650 | 90 | 0.021 | 0.72 |

| PIN14-43 | 551.69 | 612.65 | 60.96 | 1810 | 2010 | 200 | 0.010 | 0.35 |

| including | 551.69 | 560.83 | 9.14 | 1810 | 1840 | 30 | 0.024 | 0.82 |

| PIN14-44 | 108.20 | 137.16 | 28.96 | 355 | 450 | 95 | 0.019 | 0.64 |

| including | 108.20 | 111.25 | 3.05 | 355 | 365 | 10 | 0.070 | 2.40 |

| PIN14-45 | 21.34 | 88.39 | 67.06 | 70 | 290 | 220 | 0.006 | 0.19 |

| including | 35.05 | 48.77 | 13.72 | 115 | 160 | 45 | 0.009 | 0.30 |

| and | 65.53 | 86.87 | 21.34 | 215 | 285 | 70 | 0.007 | 0.24 |

| PIN14-46 | 76.20 | 105.16 | 28.96 | 250 | 345 | 95 | 0.004 | 0.14 |

| PIN14-47 | 56.39 | 64.01 | 7.62 | 185 | 210 | 25 | 0.008 | 0.28 |

| and | 115.82 | 199.64 | 83.82 | 380 | 655 | 275 | 0.004 | 0.13 |

| including | 187.45 | 199.64 | 12.19 | 615 | 655 | 40 | 0.007 | 0.25 |

| and | 243.84 | 275.84 | 32.00 | 800 | 905 | 105 | 0.011 | 0.39 |

| and | 291.08 | 298.70 | 7.62 | 955 | 980 | 25 | 0.021 | 0.70 |

| PIN14-48 | no significant intersection |

| PIN14-49 | 51.82 | 57.91 | 6.10 | 170 | 190 | 20 | 0.005 | 0.19 |

| PIN14-50 | 144.78 | 210.31 | 65.53 | 475 | 690 | 215 | 0.009 | 0.30 |

| including | 192.02 | 202.69 | 10.67 | 630 | 665 | 35 | 0.031 | 1.06 |

| PIN14-51 | 80.77 | 91.44 | 10.67 | 265 | 300 | 35 | 0.005 | 0.16 |

| PIN14-52 | 182.88 | 237.74 | 54.86 | 600 | 780 | 180 | 0.014 | 0.48 |

| including | 187.45 | 208.79 | 21.34 | 615 | 685 | 70 | 0.020 | 0.69 |

| PIN14-53 | 28.96 | 99.06 | 70.10 | 95 | 325 | 230 | 0.004 | 0.12 |

| PIN14-54 | 56.39 | 109.73 | 53.34 | 185 | 360 | 175 | 0.006 | 0.22 |

| including | 57.91 | 67.06 | 9.14 | 190 | 220 | 30 | 0.014 | 0.48 |

| PIN14-55 | no significant intersection |

| PIN14-56 | 278.89 | 359.66 | 80.77 | 915 | 1180 | 265 | 0.008 | 0.28 |

| including | 278.89 | 333.76 | 54.86 | 915 | 1095 | 180 | 0.011 | 0.38 |

| including | 315.47 | 329.18 | 13.72 | 1035 | 1080 | 45 | 0.017 | 0.57 |

| PIN14-57 | 138.68 | 147.83 | 9.14 | 455 | 485 | 30 | 0.020 | 0.67 |

| including | 138.68 | 143.26 | 4.57 | 455 | 470 | 15 | 0.030 | 1.02 |

Highlights of the 2014 Phase 2 Pinion drilling are summarized below:

East Pinion

Along the central east side of Pinion, a total of 15 RC holes intersected gold associated with oxidized multilithic, dissolution collapse breccia southeast, south and east of the near surface Main Zone mineralization (Figures 10.7 and 10.8). Some infill drilling was completed in order to extend the gold zone in gaps where prior historic drilling was not completed to the currently modelled depth of the gold zone or where mineralization was complicated by faults. Other drill holes were planned to expand mineralization in undrilled areas.

| | · | At the new Anticline Target (Figures 10.7 and 10.8), gold bearing intercepts in PIN14-14, -16, -18 and -21 confirmed and expanded oxidized gold mineralization along the axis of a north-northeast-striking anticline. The four holes drilled into this target successfully intersected mineralization over a strike length of 170 m, representing a separate zone of thicker, higher grade gold extending south-southwest from Main Zone mineralization. Higher grade intervals, exceeding 2.0 ppm in PIN14-18 and -21, remain open along strike to the south. |

| | · | The gold-bearing intercept in PIN14-19 (0.55 ppm over 114.3 m hole length including two separate zones of 1.14 ppm over 13.72 m and 1.12 ppm over 10.67 m hole length; Table 10.7) successfully expanded the southeast strike extent of thicker breccia hosted mineralization along the Main Zone fault, an important gold-controlling structure at Pinion. This hole demonstrates that thick gold intercepts, developed well down into brecciated Devil’s Gate calcarenite, could be present southeast beneath the bottoms of shorter historic drill holes in that area. |

| | · | Along the eastern limb of the new Anticline Target, holes PIN14-23, -26, -27, -30, -31 and -33 successfully intersected oxide gold mineralization along a previously undrilled 200 meter by 100 meter north-northeast trend (Figures 10.7 and 10.8). |

| | · | At East Pinion, holes PIN14-20 and PIN14-22 expanded the lateral extent of the breccia hosted gold zone 75m to the north and 75m to the east, respectively, from historic drill intercepts. Mineralization in PIN14-20 is open to the north for additional exploration. |

| | · | Gold bearing intercepts in PIN14-15 and PIN14-17 successfully in-filled an area on the east side of Pinion where historic drill holes were spaced 30 to 60 meters apart. |

Southeast Pinion

Three target areas were tested by a series of eight holes: New Structural Block, Southeast Pinion and Far Southeast Pinion. The key multilithic, dissolution collapse breccia host was intersected in all holes and the areal extent of the host breccia was expanded to the south and east. Prior to the Gold Standard drilling, these target areas were characterized by no historic drill holes or historic holes spaced 60 to 400m apart. Similar to the targets explored in Phase 1 drilling, gold mineralization is continuous and widespread within this highly permeable, silicified breccia which is favorably sandwiched between relatively impermeable silty micrite of the overlying Mississippian Tripon Pass Formation and thick-bedded calcarenite of the underlying Devil’s Gate Formation.

| | · | At the Southeast Pinion target, where the gold-bearing horizon has tended to be deeper, drill holes PIN14-36 and PIN14-37 intersected shallow oxidized gold mineralization (including 16.8 m of 0.75 ppm Au and 12.2 m of 0.71 ppm Au, respectively) starting at approximately 40 m below surface. In this target area, a gold-bearing layer has unexpectedly intersected higher in the stratigraphic section within the Tripon Pass Formation silty micrite, resulting in a gold horizon present at a shallow depth. |

| | · | At the New Structural Block target, five holes successfully intersected gold-bearing multilithic, dissolution collapse breccia in this previously untested structural block between the South fault and the Uplifter fault (see Figures 10.7 and 10.8). PIN14-38 intersected an entirely oxidized interval of 48.8 m of 1.16 ppm Au from 202.7 to 251.5 m, including a higher grade internal interval of 6.1 m of 6.78 ppm Au. PIN14-38 is on the edge of the drill pattern and this oxide mineralization is open to the south. The gold zone intersected in holes PIN14-40, -42 and -47 is dominantly oxidized, but select intervals are mixed oxide-carbon-sulfide. |

| | · | At the Far Southeast Pinion target, gold-bearing intercepts in PIN14-25 successfully expanded the lateral extent of the breccia hosted mineralization 400 m to the southeast of the Pinion Deposit. This gold intercept is open in multiple directions and further drilling is warranted in 2015 to follow-up on these promising results. |

The three target areas noted above exhibit similar geological patterns including: (1) an increase in the volume and thickness of intrusive rock; (2) the presence of lamprophyre, an igneous rock commonly associated with gold deposits on the Carlin Trend; (3) gold-bearing multilithic, dissolution collapse breccia in the hanging wall of a shallow, west-dipping thrust fault that is a laterally-continuous feature as tracked through the drilling. Due to the potential for repetition of the favourable breccia stratigraphy, deeper untested targets similar to those at North Bullion are envisioned at this portion of the Pinion Project.

Southwest-West Pinion

A total of four holes were designed to test for and extend gold mineralization along the west-southwest margin of the known Pinion gold mineralization. All four holes intersected significant gold mineralization associated with oxidized multilithic, dissolution collapse breccia. Highlights of the drilling include the following:

| | · | At the west Pinion target, three holes successfully intersected oxidized gold bearing multilithic, dissolution collapse breccia along the west margin of the maiden resource block model. PIN14-44, PIN14-52 and PIN14-56 intersected entirely oxidized intervals of 29.0 m of 0.64 ppm Au, 51.8 m of 0.50 ppm Au, and 54.9 m of 0.38 ppm Au, respectively (Table 10.7). These holes demonstrate the Pinion mineralization is open to the northwest along the west margin of the deposit. |

| | · | At the Southwest Pinion target, a gold-bearing intercept of 48.8 m of 0.42 ppm Au in PIN14-43 successfully expanded the lateral extent of the breccia hosted mineralization 245 m to the southwest. PIN14-43 is on the southwest edge of the drill pattern and although 400 m in true vertical depth, this mineralization is oxidized and remains open in all directions. |

Northwest Pinion

A total of seven RC holes were drilled at the Northwest Pinion target. See Figure 10.8. All seven holes successfully intersected gold-bearing multilithic, dissolution collapse breccia along the Main Zone fault and the South fault. Two holes intersected thicker zones of gold mineralization including a shallow intercept of 13.7 m of 0.41 ppm Au in PIN14-54, and 9.1 m of 0.67 ppm Au in PIN14-57 (Table 10.7). These intercepts, along with those in PIN14-52, -54 and -56, suggest the South fault is a feeder structure at Northwest Pinion. The most northwest intercepts in PIN14-54 and -57 indicate that gold mineralization associated with multilithic, dissolution collapse breccia is open to the northwest along strike.

In addition to the seven drill holes, Gold Standard geologists collected 49 rock chip samples from oxidized and altered multilithic, dissolution collapse breccia in surface outcrop. At Northwest Pinion, altered and mineralized outcrops of multilithic, dissolution collapse breccia are exposed along a west-northwest strike for over 760 m, in the foot wall of the South Fault Zone. Individual samples consisted of 1.2 to 4.6 m continuous rock chip channels on larger outcrops or, panel samples from smaller outcrops. Gold assays for the samples ranged from 0.01 to 1.24 ppm Au. Seven composite channel sample intervals returned gold values above the 0.14 g Au/t lower cut-off grade utilized in the maiden Pinion NI 43-101 compliant mineral resource estimate. See "Mineral Resource Estimates" below. Individual intervals include: 9.1 m of 0.94 ppm Au, 12.2 m of 0.61 ppm Au, 12.2 m of 0.33 ppm Au, 15.2 m of 0.31 ppm Au, 10.7 m of 0.23 ppm Au, 22.6m of 0.19 ppm Au and 3.1 m of 0.59 ppm Au. Drilling and surface rock sampling results confirm that gold mineralization remains open to the northwest. Further drilling in 2015 is warranted to follow-up on these results.

North Pinion

Drilling at the north end of the Pinion Deposit, north along strike from the North Zone comprised inclined RC drilling and targeted two separate breccia hosts, a relatively stratiform dissolution collapse breccia at the top of the Devils Gate limestone and a fault breccia along the Bullion Fault Corridor. These breccia targets were tested down-dip from continuous surface rock chip channel samples of 130.8 m of 0.35 ppm Au; 14.0 m of 0.38 ppm Au; 9.5 m of 0.331 ppm Au; 6.1 m of 0.16 ppm Au; 6.1 m of 0.21 ppm Au; 3.1 m of 0.35 ppm Au and 2.4 m of 0.56 ppm Au. The target area is characterized by historic holes spaced 30 to 150 m apart. The host breccias and anomalous gold mineralization were intersected in all eight Gold Standard holes along a 430 m north-south strike length, demonstrating that surface sampling can be successfully pursued by drilling. Mineralization remains open to the north along strike, down-dip to the east, and to the west. Highlights include:

| | · | PIN14-24 returned five at- or near-surface, oxidized gold zones including 19.8 m of 0.44 ppm Au and 12.2 m of 0.34 ppm Au. Oxidized mineralization is hosted within quartz veined and brecciated Chainman Formation sandstone and mudstone, and fills a gap in the 3D block model. Intercepts in this hole extended the known gold mineralization at the north margin of the North Pinion gold zone. |

| | · | PIN14-32 intersected 21.3 m of 0.38 ppm Au at the fault contact between Webb Formation mudstone and Nevada Formation dolomite. Oxidized mineralization is associated with quartz veins, silicification, hematite and fault breccia. |

| | · | PIN14-35 intersected four zones of gold mineralization including a higher-grade gold zone of 4.6 m of 2.79 ppm Au within oxidized and silicified fault breccia. This gold zone is immediately below a clay-altered quartz-feldspar porphyry dike, within the Bullion Fault Corridor. |

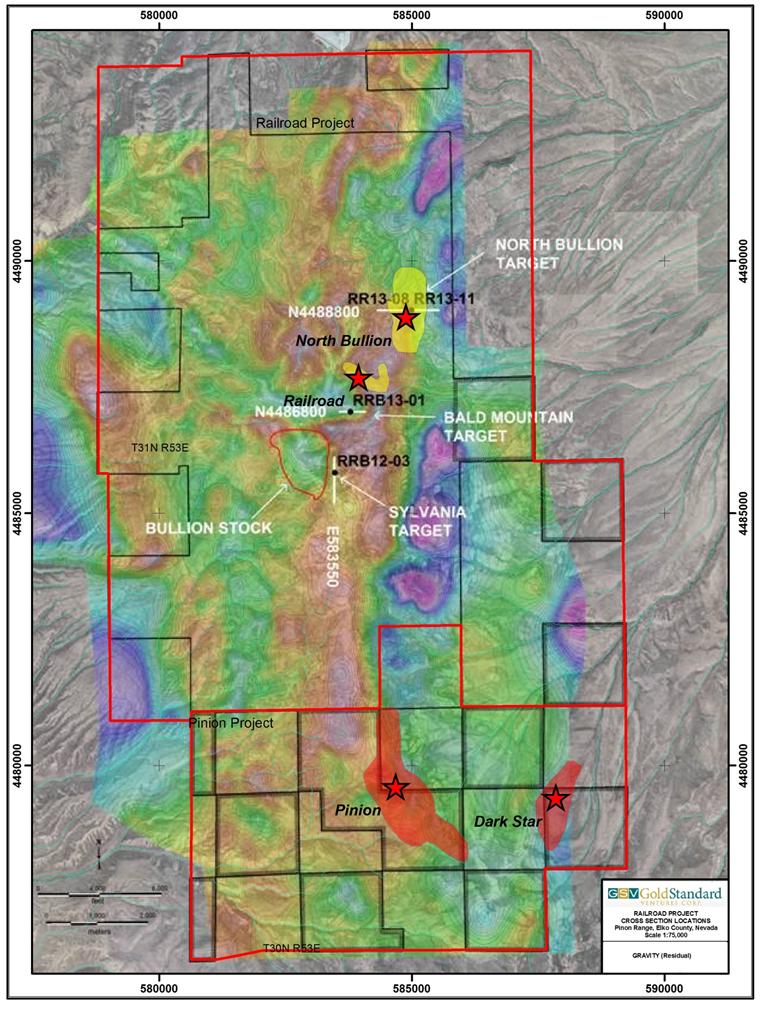

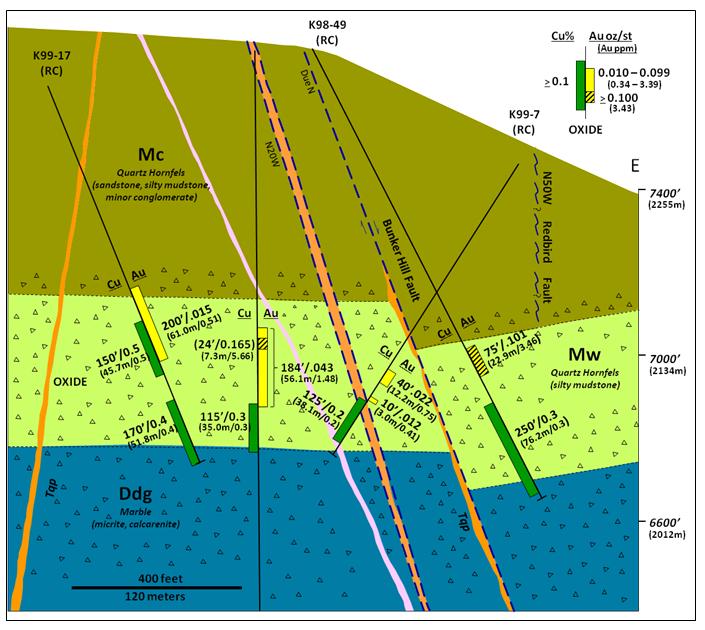

Bald Mountain

During late 2014, the Company completed vertical RC designed to expand the limits of known oxide copper-gold-silver-zinc mineralization at Bald Mountain intersected in prior drilling and RRB13-01, a vertical core hole completed in 2013. Mineralization is hosted in multi-lithic collapse breccia at the top of the Devils Gate Limestone, the same breccia host horizon as the Pinion and North Bullion deposits. Intercepts in RRB13-01 included 56.1 m of 1.47 ppm Au immediately above 23.3 m of 0.4% Cu. The Bald Mountain drilling totaled 1,896.2 m in 5 vertical RC holes and tested an area approximately 400 m by 250 m. Highlights of the 2014 drilling are provided in Table 10.8 below extracted from the 2015 Railroad-Pinion Report.

[remainder of page left blank intentionally]

Table 10.8: 2014 Bald Mountain Target Drilling Intersection Highlights.

Hole Number | From (m) | To (m) | Length (m) | From (ft) | To (ft) | Length (ft) | Au (ppm) | Ag (ppm) | Cu (%) | Zn (%) |

| RRB14-01 | 134.11 | 140.21 | 6.10 | 440 | 460 | 20 | 0.02 | 11.8 | 0.007 | 0.004 |

| and | 170.69 | 335.28 | 164.59 | 560 | 1100 | 540 | 0.03 | 7.2 | 0.159 | 0.116 |

| including | 249.94 | 262.13 | 12.19 | 820 | 860 | 40 | 0.07 | 18.9 | 0.038 | 0.006 |

| and | 274.32 | 329.19 | 54.86 | 900 | 1080 | 180 | 0.02 | 11.8 | 0.445 | 0.325 |

| including | 292.61 | 329.19 | 36.58 | 960 | 1080 | 120 | 0.02 | 9.3 | 0.620 | 0.414 |

| including | 317.00 | 329.19 | 12.19 | 1040 | 1080 | 40 | 0.02 | 9.5 | 1.235 | 0.565 |

| RRB14-02 | 73.15 | 109.73 | 36.58 | 240 | 360 | 120 | 0.03 | 1.8 | 0.093 | 0.011 |

| including | 73.15 | 79.25 | 6.10 | 240 | 260 | 20 | 0.03 | 2.1 | 0.172 | 0.014 |

| and | 103.63 | 109.73 | 6.10 | 340 | 360 | 20 | 0.01 | 1.5 | 0.178 | 0.016 |

| RRB14-03 | 12.19 | 18.29 | 6.10 | 40 | 60 | 20 | 0.38 | 12.9 | 0.120 | 0.043 |

| and | 237.75 | 426.73 | 188.98 | 780 | 1400 | 620 | 0.07 | 5.7 | 0.122 | 0.032 |

| including | 262.13 | 377.96 | 115.83 | 860 | 1240 | 380 | 0.08 | 8.5 | 0.182 | 0.035 |

| including | 274.32 | 298.71 | 24.38 | 900 | 980 | 80 | 0.11 | 18.0 | 0.334 | 0.005 |

| and | 323.09 | 359.67 | 36.58 | 1060 | 1180 | 120 | 0.08 | 7.4 | 0.267 | 0.007 |

| RRB14-04 | 310.90 | 391.67 | 80.77 | 1020 | 1285 | 265 | 0.05 | 2.5 | 0.086 | 0.145 |

| including | 312.42 | 320.04 | 7.62 | 1025 | 1050 | 25 | 0.11 | 2.5 | 0.121 | 0.030 |

| and | 371.86 | 374.91 | 3.05 | 1220 | 1230 | 10 | 0.03 | 12.3 | 0.430 | 0.410 |

| RRB14-05 | 149.35 | 301.76 | 152.40 | 490 | 990 | 500 | 0.08 | 4.0 | 0.145 | 0.031 |

| including | 158.50 | 184.41 | 25.91 | 520 | 605 | 85 | 0.26 | 8.3 | 0.391 | 0.038 |

| and | 211.84 | 239.27 | 27.43 | 695 | 785 | 90 | 0.08 | 3.7 | 0.288 | 0.044 |

| and | 265.18 | 295.66 | 30.48 | 870 | 970 | 100 | 0.01 | 3.5 | 0.020 | 0.033 |

The Bald Mountain drilling intersected multi-lithic, dissolution collapse breccia host in all five holes and the plan extent of the breccia was expanded in all directions. Gold, silver and base metal mineralization is widespread within the highly permeable, flat-tabular, multi-lithic collapse breccia which is sandwiched between relatively impermeable hornfels of the overlying Mississippian Webb Formation and thick-bedded marble of the underlying Devils Gate Formation. The stratigraphic position, thickness (35-120 m) and the lateral continuity of the Bald Mountain breccia unit is considered significant as this pattern is consistent with the gold-bearing breccia host at the Pinion and North Bullion deposits. Highlights of the 2014 drilling are as follows:

| | · | RRB14-05, a drill hole 205 m west of RRB13-01, intersected two separate zones of mineralization. The upper zone contained 12.2 m of 0.39 ppm Au along with 25.9 m of 0.39% Cu and 8.3 ppm Ag in oxidized multi-lithic collapse breccia and quartz-feldspar porphyry sills. The lower zone included 27.4 m of 0.29% Cu and 3.8 ppm Ag hosted in oxidized skarn and quartz-sericite-pyrite altered quartz-feldspar porphyry sills. Mineralization remains open to the west, north and south. |

| | · | Drill hole RRB14-01 targeted the main breccia zone proximal to the north-striking Bunker Hill fault, 210 m east-northeast of RRB13-01. The hole successfully intersected the fault, oxidized-silicified-clay altered breccia, and a 39.6 m interval of 0.58% Cu, 8.8 ppm Ag and 0.40% Zn. Mineralization is open to the north, east and south. |

| | · | Drill holes RRB14-02, -03 and -04 were drilled 110 m south-southwest, 150 m northeast, and 175 m northwest, respectively from RRB13-01. All three holes intersected altered and oxidized breccia with the most significant intercept being 36.6 m of 0.27% Cu and 7.4 ppm Ag in RRB14-03. |

In addition to the drilling and ground magnetics, McComb Petrographics completed a petrographic examination and interpretation of 16 core samples from the gold and copper zones in hole RRB13-01 and came up with the following conclusions:

| | · | Most of the core samples from RRB13-01 are altered skarn that is very similar in appearance to the copper-gold skarn at Fortitude in the Battle Mountain District of Nevada. Similarities include a skarn assemblage of garnet, pyroxene, and actinolite occurring with massive pyrrhotite (oxidized). |

| | · | Skarn alteration appears to be overprinted by a Carlin-style silicification event and is also similar to that present at Fortitude. |

| | · | The multilithic breccia host unit includes fragments of calc-silicate hornfels, skarn and porphyritic igneous material. |

Sample Preparation, Analysis and Security

The following summarizes the procedures employed by Gold Standard for, among other things, the handling of core and reverse-circulation cuttings samples.

Surface Soil and Rock Sampling

All sampling was conducted under the supervision of the Company’s project geologists and the chain of custody from the field to the sample preparation facility was continuously monitored. A blank or certified reference material was inserted approximately every forty samples for soil and rock samples. The samples are delivered to ALS Chemex Minerals' ("ALS" or "ALS Minerals") preparation facility in Elko, NV where the samples are crushed, screened and pulverized. Sample pulps are shipped to ALS' certified laboratory in Vancouver, B.C. for geochemical analysis. Pulps are digested and analyzed for gold using fire assay fusion and an ICP-AES finish on a 30 gram aliquot split. All other elements are determined by a wet chemical 2 acid ICP analysis at ALS in Vancouver. Data verification of the analytical results includes a statistical analysis of the duplicates, standards and blanks that must pass certain parameters for acceptance to insure accurate and verifiable results.

Drill core is collected from the drill rig by Gold Standard personnel and transported to Gold Standard’s Elko, Nevada office on a daily basis. At the secure Elko facility, Gold Standard personnel complete the following:

| | · | A geological log is completed on the whole core. Logs illustrate core recovery, sample intervals, lithologic data, hydrothermal alteration and structural features with respect to the core axis. |

| | · | The whole core is marked/tagged for sampling, and digitally photographed. High resolution digital jpeg photographs are archived for future reference. |

| | · | Whole core is sawed in half by contractors, working at Gold Standard’s Elko office. Sawed core sample intervals are recorded on daily cut core sheets for review each day. |

| | · | Half core is retained in the original core boxes, and the other half is bagged for geochemical analysis. |

| | · | Standard reference materials (standards and blanks) are inserted into the sample sequence at a rate of approximately 1 in every 10 to 15 samples. |

All original geochemical analyses were completed by ALS, an internationally accredited independent analytical company with ISO9001:2008 certification. ALS picks up the core samples from Gold Standard’s Elko office and delivers them to their Elko, Nevada sample preparation facility. At the ALS preparation facility the samples are logged into a computer-based tracking system, weighed and dried. The entire sample is crushed so that +70% passes a 6 mm screen, then it is finely crushed so that +70% passes a 2mm screen. A 250 g (~0.5 pound) spilt (original pulp) is then selected and pulverized to better than 85% passing a 75 micron screen. From Elko the pulp samples are shipped to Reno, Nevada or Vancouver, British Columbia for geochemical analysis.

At Reno or Vancouver, a 30 g aliquot is extracted from the pulp and is analyzed for gold using a fire assay fusion and an atomic absorption spectroscopy (AAS) finish. Samples were also analyzed for a suite of 30 other “trace elements” by ICP-AES (Inductively Coupled Plasma – Atomic Emission Spectroscopy) following aqua regia digestion.

Reverse-circulation drill hole cuttings

Reverse-circulation drill samples were collected by the drilling contractor using a wet sample splitter on the drill rig. Samples typically range from 5 to 20 pounds. Geochemical standards and/or blanks are inserted by Gold Standard geologists every 15 to 20 samples. The samples were picked up at the drill sites by ALS Minerals and delivered to its preparation lab in Elko, Nevada.

Samples submitted to ALS utilized the exact same preparation and analytical procedures as described above for the core samples.

Samples submitted to ALS Minerals were logged into a computer-based tracking system, sorted, weighed and dried. The entire sample is crushed so that +75% passes a 2 mm screen. A 250 g (~0.5 pound) spilt is then selected and pulverized to better than 85% passing a 75 micron screen. From Elko the samples were shipped to Vancouver, B.C. for geochemical analysis. Pulp samples were analyzed for gold using a fire assay fusion and an atomic absorption spectroscopy (AAS) finish on a 30 gram split. Samples were also analyzed for a suite of 30 other “trace elements” by ICP-AES (Inductively Coupled Plasma – Atomic Emission Spectroscopy) following aqua regia digestion.

The sample collection, security, transportation, preparation, insertion of geochemical standards and blanks, and analytical procedures are within industry norms and best practices. The procedures utilized by Gold Standard are considered adequate to insure that the results disclosed are accurate within scientific limitations and are not misleading.

Data Verification

One of the co-authors of the 2015 Railroad-Pinion Report, Steven R. Koehler, the Company's Manager of Projects, has verified the location of numerous drill sites throughout the project area and compared them with coordinates in the Gold Standard drill database and has not found any issues. Mr. Koehler has also conducted visits to the ALS sample preparation facility in Elko, NV and no issues with respect to sample security or integrity were identified. In addition, the authors of the 2015 Railroad-Pinion Report have conducted a review of geological and geochemical data within the Gold Standard drill database by comparing database values to original drill logs (paper copies) and original assay certificates provided by ALS, and Inspectorate America Corporation and no issues were identified.

For non-analytical field data Gold Standard has instituted a number of protocols and procedures to insure data integrity. For example, with respect to surface geochemical sampling (rock grab and soil sampling), samplers are required to enter sample locations and descriptive information into computers daily and locations are checked to eliminate data input errors. With respect to non-analytical drill hole information, Gold Standard employs a similar protocol of continuous data checking to insure the accurate recording within the project’s drilling database of collar and down hole survey information along with all geological and geotechnical information from core and RC chip logging. The procedures employed are considered reasonable and adequate with respect to insuring data integrity.

Quality Assurance and Quality Control (QA/QC) Program

The primary goal of the QA/QC program employed by Gold Standard at the Railroad-Pinion Project is to monitor the assaying of drill core and RC chip samples by providing a basis for measuring the accuracy and precision of assay results. To this end, Gold Standard personnel insert standard reference material (standard and blank) samples into the sample sequence. The analytical quality control measures employed are consistent with industry standards and sufficient to properly monitor analytical accuracy and precision.

The following sections discuss the details of the QA/QC program employed by Gold Standard at the Railroad-Pinion Project during the Phase 2 Pinion drill program completed during 2014. The QA/QC procedures and data for the 2012 and 2013 Railroad Project drill programs are discussed in detail within a previous technical report (Koehler et al., 2014). Similarly, the QA/QC program employed during the Phase 1 Pinion drill program completed in early 2014 is discussed in the Pinion Resource Report (Dufresne et al. 2014). As with previous drill programs conducted by Gold Standard at the Railroad-Pinion Project, certified blank and standard samples used during the Phase 2 Pinion drill program in 2014 were obtained from Shae Clark Smith MEG Inc. in Reno, NV ("SCS"). A review of the sample preparation and certification procedures employed by SCS indicates that reference materials are produced according to industry standards to insure reasonable homogeneity and they appear to be reasonably well tested to establish expected values and acceptable ranges.

2014 Phase 2 Pinion RC Drill Program QAQC

The Phase 2 Pinion drill program comprised a total of 35,730 ft (10,891 m) of drilling in 44 RC holes that were completed in late 2014. The drill program comprised the analysis of some 7,817 samples, which included 7,142 actual drill samples and 675 QAQC samples representing a rate of 1 QAQC sample for every 10.6 drilling samples. This is a reasonable frequency to allow for a thorough evaluation of laboratory assay procedures and analysis. The QAQC samples comprised 329 blank pulp samples and 346 standard samples that were inserted into the sample sequence.

1. Blanks

A total of 329 blank samples were inserted in the sample stream by Gold Standard personnel during the Phase 2 2014 Pinion drill program. The blank pulp materials are certified by SCS to comprise material that should assay <0.003 ppm Au (<3 ppb Au). All of the blanks were analyzed by 30 g fire assay with a wet chemical finish with a lower detection limit 0.005 ppm Au (5 ppb Au). In total, all but 5 blank samples assayed below detectable limits for gold (<0.005 ppm Au) or 1.5% of the blank samples, which relative to a 95% confidence level is considered acceptable. There were no significant issues with respect to the analysis of the blank samples inserted into the Phase 2 Pinion drill program in 2014.

2. Standard Reference Materials

Throughout the 2014 Phase 2 Pinion drill program some 346 standard samples were inserted in the sample stream by Gold Standard personnel. The results for the standard samples fell within acceptable limits and therefore no significant issues with respect to laboratory precision were identified and it is the view of the authors of the 2015 Railroad-Pinion Report that no re-assaying is required.

3. Umpire Check Assays, Duplicate Core Sample Assays and Lab-inserted Standard Reference Materials

There has been no umpire assaying conducted on any of the 2014 Bald Mountain drill samples and no duplicate samples were collected during the 2014 Phase 2 Pinion drilling program. In addition, there were no lab-inserted standard sample results or repeat analysis results reported within the digital assay files provided by the laboratories for the 2014 Phase 2 Pinion drill program.

2014 Bald Mountain RC Drill Program QAQC

The 2014 Bald Mountain drill program comprised a total of 6,220 feet (1895.9 m) of drilling in 5 holes. The drill program comprised the analysis of some 1,365 samples, which included 1,242 actual drill samples and 123 QAQC samples representing a rate of 1 QAQC sample for every 10.1 drilling samples. The QAQC samples comprised 61 blank pulp samples and 62 standard samples that were inserted into the sample sequence by Gold Standard personnel. The QC sample insertion frequency is acceptable, however, the use of 6 different standard reference materials by Gold Standard during the relatively short 2014 Bald Mountain drill program resulted in the analysis of only 9 to 14 (average 10.3) samples of each standard, which is an insufficient number of each to allow for a proper statistical analysis of their results. That being said, the 2014 Bald Mountain drilling together with the Phase 2 Pinion drill program comprised the analysis of some 798 QC samples including 390 blanks and 408 standards, which comprises a statistically valid average of 68 analyses for each standard.

1. Blanks

A total of 61 blank pulp samples were inserted in the sample stream during the 2014 Bald Mountain drill program. The blank pulp materials are certified by SCS to comprise material that should assay <0.003 ppm Au (<3 ppb Au). All of the blanks were analyzed by 30 g fire assay with a wet chemical finish with a lower detection limit 0.005 ppm Au (5 ppb Au). All but 1 blank sample assayed below detectable limits for gold (<0.005 ppm Au) or 1.6% of the blank samples, which relative to a 95% confidence level, is considered acceptable. There were no significant issues with respect to the analysis of the blank samples inserted into the 2014 Bald Mountain drill program.

2. Standard Reference Materials

Throughout the 2014 Bald Mountain drill program 62 standard samples were inserted in the sample stream by Gold Standard personnel. The certified values and acceptable analytical ranges for each of the six (6) standard reference materials used during the drill program are the same as those used during the 2014 Phase 2 Pinion drill program. The results for the standard samples fell within acceptable limits and therefore no significant issues with respect to laboratory precision were identified and it is the view of the authors of the 2015 Railroad-Pinion Report that no re-assaying is required.

3. Umpire Check Assays, Duplicate Core Sample Assays and Lab-inserted Standard Reference Materials

There has been no umpire assaying conducted on any of the 2014 Bald Mountain drill samples and no duplicate samples were collected during the 2014 Bald Mountain drilling program. In addition, there were no lab-inserted standard sample results or repeat analysis results reported within the digital assay files provided by the laboratories for the 2014 Bald Mountain drill program.

Mineral Processing and Metallurgical Testing

A variety of historic and modern metallurgical tests have been conducted on material for three Railroad Project prospects including Railroad, North Bullion and Bald Mountain. Two separate and unique first-pass metallurgical tests were completed on drill samples from the North Bullion Deposit and the Bald Mountain Target. A number of historic metallurgical tests have been conducted on material from the Pinion Deposit. The samples, test work and results of metallurgical work conducted to date are summarized below. Both projects are in need of modern and more extensive metallurgical work.

In 2006, a total of 63 bottle roll tests and 3 column leach tests were completed by Kappes, Cassiday & Associates on behalf of Royal Standard Minerals on material from core from the Railroad (POD) prospect located on the Railroad Project. A total of 475 lbs of sample material was submitted for the column leach tests and the individual bottle roll tests comprised samples from individual 5 and 10 foot drill hole intervals (Kappes, Cassiday & Associates, 2006). The individual samples were collected from drill holes POD05-01, POD05-02, POD05-04 and POD05-07.

Prior to the initiation of the column leach tests, assays were conducted to establish the head grade of the original 475 lbs of sample material as 0.069 oz/st (2.37 g/t) Au. The sample was also submitted for an initial simple bottle roll test that yielded gold recovery of 85%. The column leach tests were conducted on 3 crush sizes (1.5”, 0.5” and 0.25”) and the results approximated the initial bottle roll test averaging 85% for the 3 sizes. After 82 days of leaching, the three crush size columns returned gold recoveries of 83%, 86% and 88%, respectively.

The metallurgical work also included running a series of bottle roll tests from the individual core samples. The results of the 63 individual bottle roll tests were highly variable yielding from 0% to 83% gold recoveries. The Kappes, Cassiday & Associates (2006) report identified carbonaceous materials and pointed out that black siltstone and black jasperoid samples yielded the poorest recoveries.

Three samples were selected from composited, quarter-cut North Bullion drill core from the Railroad Project and provided to Newmont USA Limited, a subsidiary of Newmont. Each sample was taken from drill core and was expected to be refractory. A scope of work was generated to conduct gold head assays (duplicate fire assays, cyanide leachable gold assays, and preg-rob assays), carbon and sulfur assays (with a LECO furnace) and a multi-element ICP-MS analysis. The tests were designed to determine if North Bullion deposit mineralization is amenable to the established recovery technologies commonly used for Carlin-type ores.

Newmont provided the Company with two reports summarizing the results of metallurgical and mineralogical tests from the North Bullion deposit. All 3 samples were characterized as carbonaceous and sulfidic refractory material with very different gold grades, arsenic grades and sulfide sulfur contents (Arthur, 2013; McComb, 2013). The three samples assayed 0.067 oz Au/st (2.30 g/t), 0.340 oz Au/st (11.66 g/t) and 0.235 oz Au/st (8.06 g/t), respectively. Roaster recoveries were 83.1%, 90.0% and 78.8%, respectively, indicating that North Bullion mineralization is likely to be conducive to roaster processing (Arthur, 2013). The cause of the recovery variances was not determined. Sulfide sulfur burns were between 94% and 96% and organic carbon burns were between 78% and 93%. The results suggest that the roast was complete (Arthur, 2013). The calcines had calculated preg-rob values between 0 and 0.007 opt with AA/FA ratios between 77% and 84% further supporting the conclusion that all of the organic carbon was burned (Arthur, 2013).

Recognizing the potential economic significance of the Bald Mountain gold discovery, Gold Standard commissioned metallurgical tests of the core from drill hole RRB13-01. Inspectorate of Sparks, Nevada used the following procedure: 30 gram pulp samples were agitation-leached for one hour at room temperature in 60 ml of 0.3% sodium cyanide solution. The solution also had a 0.3% concentration of sodium hydroxide in order to stabilize the pH at greater than 10. Pregnant solutions were analyzed by a matrix-matched-calibrated AAS. Internal blanks, standards and duplicates were also analyzed at a frequency of approximately one of each for every 35 samples.

Fourteen of fifteen samples provided an unweighted average recovery of 82.2%. The better recoveries were skewed toward the higher grade samples.

An initial program of metallurgical test work was conducted in 1992 by Crown Metals using RC drill cuttings samples that were composited and processed at McClelland Laboratories in Sparks, NV. A total of 158 – 5 foot RC samples were combined into 8 composite samples that were subjected to basic cyanidation (leach) tests without further preparation (i.e. no additional grinding or screening was conducted). The results of this work indicated that the samples (RC cuttings) were amenable to direct cyanidation with recoveries ranging from 75% to 91.3% and averaged 81.8%. The samples were subjected to 96 hours of leaching but results indicated that gold leaching was relatively rapid and was substantially completed between 6 and 24 hours. Cyanide consumption was low and lime requirements were moderate to high (Calloway, 1992b; DeMatties, 2003).

Additional metallurgical test work was completed in 1994, also at McClelland Laboratories (McPartland, 1995; DeMatties, 2003). Bottle roll and column percolation leach tests were performed on 35 RC drill hole cuttings composites, comprising material from 529 individual RC drill cuttings samples, as well as an 880 lb bulk sample collected from a surface exposure of the Pinion mineralization. Additional column percolation leach testing at various grind sizes, along with mineralogical testing, was recommended.

The results for column leach testing conducted on the Pinion (surface) bulk sample indicate that gold recoveries increase with finer grinding up to 80.6% by column leaching on material ground to 100 mesh. It was concluded from the simulated heap leach cyanidation testing completed that the Pinion (referred to as “South Bullion”) bulk sample material was amenable to leaching at 62% - 2” and 82% - ¾” feed sizes.

With respect to the bottle roll testing of the 35 composited cuttings samples, the data indicates that the samples are amenable to direct cyanidation at a nominal grind of 10 mesh with recoveries averaging 66.1%. Ten of the 35 composites were subjected to further grinding to 80% passing 65 mesh and resulted in an average increase in recovery of 13.7% from 60.6% to 68.0%, with 5 of the 10 samples averaging a 25% increase in recovery. Further grinding to 200 mesh had little effect on recoveries, which increased by an average of 3.8%. Leaching was fairly rapid, cyanide consumption was considered low and lime requirements were moderate. There was no strong correlation between composite depth and gold recovery, recovery rate or reagent requirements.

In 2004, personnel from Kappes, Cassiday & Associates (2004) supervised a trenching program on behalf of Royal Standard Minerals at the Pinion Deposit that resulted in the collection of 6 bulk (or composite) samples (a single 55 gal drum) from 6 trenches at the deposit with metallurgical testing completed on 5 of the samples and several grab samples from the trenches.

Metallurgical tests including bottle rolls and column leach tests, were completed on an equal weighted composite of the 5 bulk trench samples. A cyanide bottle roll leach test was completed on a composite sample that ran for a period of 72 hours. Gold extraction from the pulverized material was 78% after 72 hours of leaching based upon a calculated head grade of 0.048 oz/st (1.64 ppm) Au. Silver extraction was 54% based upon a calculated head grade of 0.67 oz/st (22.97 ppm) Ag. Sodium cyanide consumption for the test is was 0.63 lbs NaCN/ton. Hydrated lime consumption was 4.0 lbs Ca(OH)2/ton (Kappes, Cassiday & Associates, 2004).

Three (3) separate column leach tests were conducted on the composite sample comprising material from five of the trenches completed at the Pinion Project. These tests were conducted at crush sizes of 100% minus 1 ½”, minus ½” and minus ¼”. The gold extractions from the PC Composite sample were 57%, 59% and 69% for these crush sizes, respectively. The silver extractions from the PC Composite sample were 31%, 33% and 62% for the same crush sizes, respectively. Sodium cyanide consumption averaged 1.44 lbs NaCN/ton and hydrated lime consumption averaged 2.0 lbs Ca(OH)2/ton. The minus ¼” crush column leach test required 2.0 lbs cement/ton.

In addition, 76 hand samples were collected from the 6 Pinion trenches and measured for specific gravity using the wax coated water displacement technique. The average of the 76 analyses was 2.65 g/cm3. However, this value was skewed slightly by an unusually high average SG value of 3.20 g/cm3 returned from one trench. The average SG value for the remaining 5 trenches was 2.55 g/cm3, which is very close to (98.8% of) the value of 2.58 g/cm3 that was determined from the 171 SG measurements made on 2014 Pinion drill core samples (Dufresne at al., 2014). The average trench sample SG value excluding both the highest and the lowest individual trench averages (3.03g/cm3 and 2.41g/cm3), then the average of the remaining trench averages is 2.58 g/cm3, which is equal to the SG value determined for the Pinion Deposit determined from 2014 drill core samples (Dufresne at al., 2014).

Mineral Resource Estimates

On September 10, 2014 and March 3, 2015, Gold Standard announced the results of the two separate mineral resource estimation efforts at the Pinion and Dark Star prospects. APEX completed both the Pinion and Dark Star maiden resource estimation efforts. Details of the 2014 Pinion mineral resource estimate are contained in the Pinion Resource Report (Defresne et al., 2014) and summarized below. A technical report for the recent (2015) Dark Star resource estimation effort is currently being prepared and the information summarized below is derived from the Company's news release of March 3, 2015.

2014 Pinion Deposit Mineral Resource Estimate

Following its acquisition of the Scorpio Pinion Interests in March 2014, the Company initiated a Phase 1 drill program of 13 holes designed to test and confirm mineralization within the Pinion Deposit. Results from the 2014 Phase 1 Pinion drilling confirmed historical assays from several twinned holes and further confirmed that the collapse breccia-hosted oxide gold zone at the Pinion Deposit is widespread and continuous, and that breccia development and mineralization appeared to thicken and strengthen adjacent to high angle fault zones and fault intersections. A thorough review of historical drill data from the Pinion Deposit was completed by the Company in early 2014, which included a significant core and RC chip re-logging effort, and was conducted in conjunction with personnel from APEX. At the conclusion of the historical Pinion drill database review it was concluded that the data was of sufficient quantity and quality to warrant the completion of a maiden NI 43-101 mineral resource estimate for the Pinion Deposit. The Pinion resource was released on September 10, 2014 and the following information is taken from the subsequent Pinion Resource Report (Dufresne et al., 2014).

Mineral resource modelling and estimation was carried out using a 3-dimensional block model based on geostatistical applications using MICROMINE (v14.0.6), a commercially available resource estimation and mine planning software.

The Pinion resource estimate is reported in accordance with NI 43-101 and has been estimated using the CIM “Estimation of Mineral Resources and Mineral Reserves Best Practice Guidelines” dated November 23rd, 2003 and CIM “Definition Standards for Mineral Resources and Mineral Reserves” dated November 27th, 2010. Mineral resources are not mineral reserves and do not have demonstrated economic viability. There is no guarantee that any part of the mineral resource discussed in the Pinion Resource Report will be converted into a mineral reserve in the future.

Modeling was conducted in Universal Transverse Mercator (UTM) coordinate space relative to the North American Datum (NAD) 1927 and UTM Zone 11. The Pinion resource modeling utilized 392 drill holes that were completed from 1981 to 2014. Mr. Dufresne visited the Pinion Project in May, 2013, April, 2014 and October, 2014 in order to verify and validate the historic drill hole database and to verify the drilling of the recently completed 2014 core and RC holes completed by Gold Standard. Over the period of the last 8 months, APEX personnel were intimately involved in the verification, validation, drill hole collar surveying and QA/QC analysis of the entire Pinion drill hole database. It is the opinion of the authors of the Pinion Resource Report that the drill hole database is deemed of good enough quality to create an accurate geological interpretation and model, including the construction of mineralization wireframes, and complete a statistical analysis and resource estimate.

The predominantly oxide gold-silver mineralization has been estimated within three dimensional solids that were created from cross-sectional lode interpretation. The upper contact has been cut by the topographic surface. There is little to no significant overburden present at the Pinion Deposit. Grade was estimated into a block model with parent block size of 10 m (X) by 10 m (Y) by 3 m (Z) and sub-blocked down to 5 m (X) by 5 m (Y) by 1 m (Z). A total of 171 density measurements made during 2014 on diamond drill core samples. These measurements in combination with historic results yield an average nominal density of 2.58 kg/m3 for gold mineralization hosted in the multi-lithic collapse breccia. Grade estimation of gold and silver was performed using the Inverse Distance squared (ID2) methodology. The indicated and inferred resources are constrained within a drilled area that extends approximately 2.3 km along strike to the north-northwest, 1.1 km across strike to the east-northeast and 400 m below surface.

The 2014 Pinion mineral resource has been classified as comprising both Indicated and Inferred resources according to the CIM definition standards. The classification of the Pinion Indicated and Inferred Mineral Resource was based on geological confidence, data quality and grade continuity. The most relevant factors used in the classification process were:

| · | Drill hole spacing density. |

| · | Level of confidence in the geological interpretation, which is a result of the extensive re-logging of drill chips. The observed stratigraphic horizons are easily identifiable along strike and across the deposit which provides confidence in the geological and mineralization continuity. |

| · | Estimation parameters i.e. continuity of mineralization |

| · | Proximity to the recently completed 2014 drill holes. |

All mineral resources are reported within an optimized pit shell using US$1,250/ounce for gold and US$21.50/ounce for silver. The volume and tonnage for the reported resources within the US$1,250/ounce of gold optimized pit shell represents approximately 82% of the total tonnage of the unconstrained block model (utilizing a lower cutoff of 0.1 g/t Au).

The mineral resource estimates are reported at a range of gold cut-offs grades in Table 14.1 and Table 14.2 (extracted from the Pinion Resource Report) for both Indicated and Inferred categories, for gold and silver respectively. No portion of the current mineral resource has been assigned to the “Measured” category. The Pinion Indicated and Inferred Mineral Resource uses a lower cut-off grade of 0.14 g/t Au, which is constrained within an optimised pit shell and includes an Indicated Mineral Resource of 20.84 million tonnes at 0.63 g/t Au for a total of 423,000 ounces of gold and an additional Inferred Mineral resource of 55.93 million tonnes at 0.57 g/t Au for 1.022 million ounces of gold. The base case cut-off of 0.14 g/t Au is highlighted in each table. Other cut-off grades are presented for review ranging from 0.1 g/t Au to 1.0 g/t Au for sensitivity analysis. The current reported mineral resource reports only oxide mineral resources.

Table 14.1: The Pinion Initial NI 43-101 Mineral Resource Estimate for Gold at Various Lower Cut-offs.

Classification* | Au Cutoff (grams per tonne) | Tonnage (million metric tonnes) | Au Grade (grams per tonne) | Contained Au*** (troy ounces) |

| Indicated | 0.1 | 20.85 | 0.63 | 423,000 |

0.14** | 20.84 | 0.63 | 423,000 |

| 0.2 | 20.73 | 0.63 | 422,000 |

| 0.3 | 19.70 | 0.65 | 414,000 |

| 0.4 | 17.42 | 0.69 | 388,000 |

| 0.5 | 14.07 | 0.75 | 339,000 |

| 0.6 | 10.12 | 0.83 | 269,000 |

| 0.7 | 6.72 | 0.92 | 198,000 |

| 0.8 | 4.29 | 1.01 | 140,000 |

| 0.9 | 2.65 | 1.12 | 95,000 |

| 1.0 | 1.59 | 1.23 | 63,000 |

| | | | | |

| Inferred | 0.1 | 56.82 | 0.56 | 1,026,000 |

0.14** | 55.93 | 0.57 | 1,022,000 |

| 0.2 | 53.91 | 0.58 | 1,011,000 |

| 0.3 | 45.66 | 0.64 | 943,000 |

| 0.4 | 35.08 | 0.73 | 824,000 |

| 0.5 | 26.17 | 0.83 | 695,000 |

| 0.6 | 19.38 | 0.92 | 576,000 |

| 0.7 | 14.48 | 1.02 | 474,000 |

| 0.8 | 10.55 | 1.12 | 379,000 |

| 0.9 | 7.09 | 1.25 | 285,000 |

| 1.0 | 4.66 | 1.41 | 211,000 |

*Indicated and Inferred Mineral Resources are not Mineral Reserves. Mineral resources which are not mineral reserves do not have demonstrated economic viability. There has been insufficient exploration to define the inferred resources as an indicated or measured mineral resource, and it is uncertain if further exploration will result in upgrading them to an indicated or measured resource category. There is no guarantee that any part of the mineral resources discussed herein will be converted into a mineral reserve in the future.

**The recommended reported resources are highlighted in bold and have been constrained within a US$1,250/ounce of gold and US$21.50/ounce of silver optimized pit shell.

***Contained ounces may not add due to rounding.

The mineral resource estimate for silver was constrained to the gold block model. Based upon the extent of sample data and the statistics for silver the current mineral resource was classified as entirely an Inferred Mineral Resource using the lower cutoff grade of the gold block model and constrained within the optimized pit shell that utilizes a price of US$1,250 per ounce of gold and US$21.50 per ounce of silver. The Pinion Inferred Mineral Resource for silver consists of 76.77 million tonnes at 3.82 g/t Ag for 9.43 million ounces of silver (Table 14.2).

[remainder of page left blank intentionally]

Table 14.2: The Pinion Initial NI 43-101 Mineral Resource Estimate for Silver at Various Lower Gold Cut-offs.

Classification* | Au Cutoff (grams per tonne) | Tonnage (million metric tonnes) | Ag Grade (grams per tonne) | Contained Ag*** (troy ounces) |

| Inferred | 0.1 | 77.66 | 3.79 | 9,474,000 |

0.14** | 76.77 | 3.82 | 9,430,000 |

| 0.2 | 74.64 | 3.87 | 9,290,000 |

| 0.3 | 65.35 | 4.05 | 8,509,000 |

| 0.4 | 52.49 | 4.24 | 7,163,000 |

| 0.5 | 40.24 | 4.39 | 5,684,000 |

| 0.6 | 29.49 | 4.47 | 4,243,000 |

| 0.7 | 21.20 | 4.51 | 3,076,000 |

| 0.8 | 14.84 | 4.54 | 2,165,000 |

| 0.9 | 9.74 | 4.52 | 1,415,000 |

| 1.0 | 6.26 | 4.45 | 896,000 |

*Indicated and Inferred Mineral Resources are not Mineral Reserves. Mineral resources which are not mineral reserves do not have demonstrated economic viability. There has been insufficient exploration to define the inferred resources as an indicated or measured mineral resource, and it is uncertain if further exploration will result in upgrading them to an indicated or measured resource category. There is no guarantee that any part of the mineral resources discussed herein will be converted into a mineral reserve in the future.

**The recommended reported resources are highlighted in bold and have been constrained within a US$1,250/ounce of gold and US$21.50/ounce of silver optimized pit shell.

***Contained ounces may not add due to rounding.

2015 Dark Star Deposit Resource Estimate

In late 2014, Gold Standard secured additional mineral rights within the Pinion Project area, which were not part of the Scorpio Pinion Interests acquired in March 2014. This agreement secured the mineral rights to the Dark Star gold prospect located approximately 2 miles (3km) east of the Pinion Deposit. A review of the historical Dark Star drilling information was completed by Gold Standard personnel in conjunction with APEX, which confirmed that the existing Dark Star drilling data was of sufficient quantity and quality to warrant a formal resource estimation effort for the prospect. APEX was retained to complete geological modeling and resource estimation for the Dark Star prospect and a maiden resource estimate was recently completed (see Gold Standard's news release dated March 3, 2015). A NI 43-101 compliant technical report detailing the Dark Star deposit mineral resource estimation effort is currently being prepared by APEX and will be filed on the SEDAR website (www.sedar.com) within 45 days of the date of the news release.

The initial mineral resource estimate for the Dark Star gold deposit comprises an Inferred Mineral Resource of 23.11 million tonnes (Mt) grading 0.51 grams per tonne (g/t) gold (Au), totaling 375,000 ounces (oz) of gold, using a cut-off grade of 0.14 g/t Au. See Table 14.3 below extracted from the 2015 Railroad-Pinion Report. A sensitivity analysis of the grade and tonnage relationships at a variety of cutoff grades is also shown in Table 14.3.

[remainder of page left blank intentionally]

Table 14.3: The Dark Star NI 43-101 Mineral Resource Estimate at Various Lower Gold Cut-Offs (*).

| Classification* | Cutoff Grade - Au | Tonnage - Au | Grade - Au | Contained |

| | (grams per tonne) | (million metric tonnes) | (grams per tonne) | Ounces Au *** (troy ounces) |

| | 0.1 | 23.11 | 0.51 | 375,000 |

| | 0.14** | 23.11 | 0.51 | 375,000 |

| | 0.2 | 23.05 | 0.51 | 375,000 |

| Inferred | 0.3 | 21.43 | 0.52 | 361,000 |

| | 0.4 | 16.83 | 0.57 | 309,000 |

| | 0.5 | 9.95 | 0.65 | 209,000 |

| | 0.6 | 4.66 | 0.78 | 117,000 |

*Inferred Mineral Resources are not Mineral Reserves. Mineral resources which are not mineral reserves do not have demonstrated economic viability. There has been insufficient exploration to define the inferred resource as an indicated or measured mineral resource, and it is uncertain if further exploration will result in upgrading the resource to an indicated or measured resource category. There is no guarantee that any part of the mineral resources discussed herein will be converted into a mineral reserve in the future.

** Reported resources have been constrained within a $1250/ounce of gold pit shell.

*** “Contained Ounces” values have been rounded to the nearest 1000 ounces.

The maiden NI 43-101 mineral resource estimate for the Dark Star gold deposit was prepared by Michael Dufresne, M.Sc., P.Geol., and Steven Nicholls, BA.Sc., MAIG of APEX, both Qualified Persons as defined by NI 43-101. The current Inferred Mineral Resource estimate is based on the results of 105 RC drill holes from multiple historical drilling campaigns conducted by other companies 1991 to 1999. In recent months APEX personnel have been intimately involved along with Gold Standard personnel in a comprehensive data verification and validation program with respect to the Dark Star drill hole database. This effort includes a project-wide drill hole re-logging program by Gold Standard personnel designed to standardize geological information in order to facilitate geological modeling throughout the area. The data verification program has resulted in an increased level of confidence in the geologically controlled mineralization model for Dark Star. In the opinion of APEX, the Dark Star database is suitable for resource estimation.

The resource block model was generated using a total of 105 RC drill holes. Drilling has been completed on roughly east-west cross-sections that range in spacing from 15 to 50 m. The Dark Star assay file comprised 9,364 analyses of variable lengths, of which 9,103 samples have been assayed for gold. Silver assays are sporadic at best and so the silver content of the deposit was not estimated. Of the 9,364 samples in the Dark Star database, roughly one fifth (2,113 assays) are situated within the gold mineralized lodes. Statistical analysis indicates that the Dark Star gold assays represent a single population of data. Mineralized wireframes/solids were constructed to separate the different mineralized horizons. A capping value of 3.2 g/t Au was applied to the data used in the reported resource estimate, which only affected 10 samples. Subsequent analysis of capped and uncapped resource figures indicated that the capping had little effect on the reported resource estimate.

The mineral resource was estimated by the inverse distance squared method within a three dimensional mineralization envelope that was tailored to the geological model, which was assisted by the detailed data verification effort described above that included chip re-logging, geological re-interpretation and modelling. Grade was estimated into 15 m (X) x 15 m (Y) x 3 m (Z) parent blocks which were sub-blocked down to 5 m (X) x 5 m (Y) x 1 m (Z) to provide a better representation of the lode volume. Silver was not estimated. An incremental search ellipsoid ranging from 30 m x 30 m x 45 m to 180 m x 180 m x 270 m orientated along 12° was used for the gold grade interpolation. A nominal density of 2.58 tonnes per cubic meter was applied to all mineralized blocks, which is based upon the density measurement utilized at the nearby Pinion mineral resource (see Dufresne et al, 2015) and was confirmed with outcrop samples from Dark Star. The gold resource has been classified as entirely inferred.

Historic metallurgical test work has been completed to date, which included an analysis of the suitability of Dark Star gold mineralization to direct cyanide soluble leaching methods. Bottle roll leach test work was completed by Crown Resources Corp. in 1991. This test work obtained recoveries of gold ranging from 75.0 to 91.3%, in direct cyanidation of RC chips in 96 hours of leaching. Gold recovery rates were fairly rapid and extraction was substantially complete after 24 hours. Cyanide consumptions were low with lime consumptions moderate to high. Further metallurgical test work is planned but these initial results are encouraging and warrant further investigation.

In order to demonstrate that the Dark Star deposit has potential for economic extraction, the unconstrained resource block model was subjected to various preliminary pit optimization scenarios. The criteria used in the whittle pit optimizer were standard for Nevada heap leach deposits and were run at gold prices of US$1,250/ounce, US$1,400/ounce and US$1,550/ounce. All mineral resources have been reported within the optimized pit shell using the US$1,250/ounce and are shown in Table 14.3. The volume and tonnage for the reported resources within the US$1,250/ounce optimized pit shell represents approximately 90% of the total tonnage in the unconstrained block model.

Adjacent Properties

The Railroad and Pinion Projects are situated along the southeastern portion of the Carlin Gold Trend. The Rain Mining District, which is largely controlled by Newmont, is located only 2 to 3 km (1.2 to 2 miles) north of the north boundary of the Railroad Project. The Rain District has been an active exploration and mining area for several decades and is the location for Newmont’s current mining activities at the Emigrant Mine. The Rain-Emigrant series of deposits has seen extensive exploration over the last three decades. To the south of the Railroad-Pinion Project, several exploration areas have received sporadic exploration over the past three to four decades. These areas include Pony Creek and the Dixie Creek Properties. Adjacent properties with bearing or influence on the Railroad-Pinion Project are described below. The authors of the 2015 Railroad-Pinion Report have not visited or worked at any of these projects and where references are made to past production and/or historic or current mineral resources the authors have not verified the information.

Rain is a Carlin-style, sedimentary rock-hosted gold deposit that is located approximately four miles (seven kilometers) north of the Company's North Bullion Target. Newmont operated the Rain open pit mine, the Rain Underground mine and the SMZ open pit mine from 1988 to 2000 and produced approximately 870,000 ounces of gold (Longo et al., 2002). Longo et al. (2002) summarized a number of mineral resources for the three deposits as follows: Rain open pit 15.5 million tons (14.1 million tonnes) at 0.066 oz Au/st (2.3 g/t) for a total of 1,017,300 ounces of gold; Rain Underground 1.154 million tons (1.04 million tonnes) at 0.23 oz Au/st (7.9 g/t) for a total of 265,000 ounces of gold and the SMZ open pit 1.5 million tons (1.4 million tonnes) at 0.019 oz Au/st (0.65 g/t) for a total of 30,000 ounces of gold. No mining has been conducted at these Rain deposits since the date of the Longo et al. (2002) report. The resources pre-date NI 43-101 and little or no detailed information such as potential resource category or number of drill holes etc. is presented for the estimates or how the resources were arrived at, therefore the estimates are considered historic in nature and should not be relied upon. None the less, the information provides an indication of the potential size of the gold mineralized system and deposits held by Newmont immediately north of the Company's Railroad-Pinion Project.

Along strike to the northwest of the Rain Project and likely on the same structure is the Saddle and Tess gold deposits. The mineralized zones are roughly 3.5 km (2 miles) north of the Railroad Project and 10 km (6 miles) northwest of the North Bullion Target. Longo et al. (2002) states that Newmont identified a primarily underground high sulphide resource of 1.37 million tons (1.23 million tonnes) at 0.572 oz Au/st (19.6 g/t) for a total of 782,000 ounces of gold at Saddle and 3.99 million tons (3.59 million tonnes) at 0.37 oz Au/st (12.7 g/t) for a total of 1,475,000 ounces of gold at Tess. The project is currently part of a joint venture between Premier Gold Mines and Newmont. No mining has been conducted at the two deposits. The resources pre-date NI 43-101 and little or no detailed information such as potential resource category or number of drill holes etc. is presented for the estimates or how the resources were arrived at, therefore the estimates are considered historic in nature and should not be relied upon.

The Rain trend of mineralization is characterized by disseminated gold mineralization hosted in dominantly oxidized, silicified, dolomitized and barite rich collapse breccia with rare sulfides, developed along the Webb Formation mudstone/Devils Gate Formation limestone contact and along the Rain Fault. Important ore-controlling features at Rain include the west-northwest striking Rain fault, the Webb/Devils Gate contact, collapse breccia and northeast striking faults. As at the Saddle and Tess deposits along the trend, shallow oxide zones give way to deeper sulfide and carbon rich zones of substantial size and grade.

West-northwest striking structures, possibly similar in nature to the Rain Fault, are present at the Railroad and Pinion targets within the Railroad-Pinion Project area. The west-northwest structure at the Railroad Project appears to control the spatial distribution of the breccia and gold mineralization. At the Pinion Project the west-northwest appears to separate and partially control gold mineralization of the North Pod and the northern portion of the Main Zone. The structure parallels or is possibly coincident with a series of west-northwest fold axial planes.

Emigrant Springs is a Carlin-style, sedimentary rock-hosted gold deposit that is located approximately four miles (seven kilometers) north-northeast of the Company's North Bullion Target. Newmont is currently mining the deposit through open pit methods and processing the ore at an onsite, run of mine heap leach operation. Disseminated gold mineralization is hosted in oxidized, silicified, dolomitized and barite rich collapse breccia developed within the Webb Formation mudstone. Important ore-controlling features at Emigrant include the north-south-striking Emigrant Fault, collapse breccia and the Northeast Fault.

Open pit, oxide resource and reserve calculations for Newmont’s Carlin Trend operations are typically commingled into a single heading of “Carlin open pits, Nevada” category. In 2003, reserves at Emigrant were published at 1,200,000 ounces (Newmont, 2003). No details were provided by Newmont as to the quality of the reserves. The mine is expected to produce roughly 80,000 ounces of gold over a plus ten year mine life and has recently commenced production (Harding, 2012).

Pony Creek is located approximately six miles (10 kilometers) south of Gold Standard’s Pinion Deposit. Gold mineralization is hosted in north to northeast-trending shears in rhyolite intrusive and Mississippian to Permian age sediments proximal to the intrusive (Russell, 2006). A total of 175 drill holes were completed on the project from 1981 through 2004, and in these holes, 151 contained gold intercepts of at least 5 ft (1.5 m) of 0.010 oz Au/st (0.34 g/t) (Russell, 2006). No NI 43-101 compliant resource has been disclosed at Pony Creek.

The presence of gold mineralization, resources and/or reserves at the above adjacent properties is not necessarily indicative of the gold mineralization, potential resources or potential reserves at the Railroad-Pinion Project.

Other Relevant Data and Information

There are no additional data for the Railroad-Pinion Project beyond that discussed in the preceding sections.

Interpretation and Conclusions

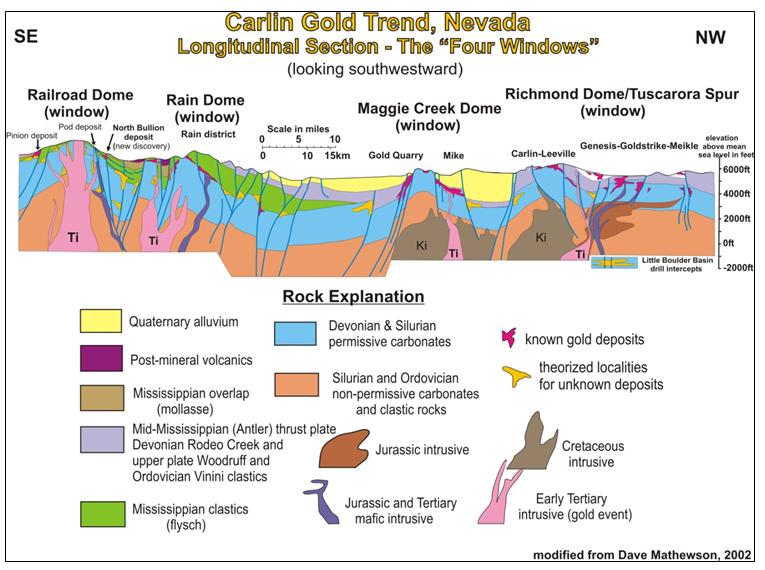

Gold Standard’s Railroad–Pinion Project is located at the southeast end of the Carlin (Gold) Trend, a northwest alignment of sedimentary rock-hosted gold deposits in northeastern Nevada. The Carlin Trend comprises more than 40 separate gold deposits that have produced in excess of 80 million ounces of gold to date (Muntean, 2014). The Project is located in the Piñon Range of mountains and is centered on the southernmost of four domed features along the Carlin Trend (Jackson and Koehler, 2014). The domes are cored by igneous intrusions that uplift and expose Paleozoic rocks that are favorable for hosting Carlin-style gold deposits.

Gold Standard has been conducting aggressive, geologic model-driven exploration programs at the Railroad portion of the Project area since its initial acquisition in 2010 and has confirmed and/or expanded previously identified zones of mineralization and has discovered several new zones (and styles) of mineralization. Currently, the Railroad Project area hosts a variety of mineralization types including; 1) classic Carlin-style disseminated gold in carbonate dissolution collapse breccia at the North Bullion prospect; 2) stacked, tabular oxide gold and copper zones in quartz hornfels breccia at the Bald Mountain target; and 3) skarn-hosted silver, copper, lead and zinc mineralization at the Central Bullion target (Jackson and Koehler, 2014; Koehler et al., 2014).

Drilling conducted in the Railroad Project area during 2012 and 2013 confirmed and expanded a significant Carlin-style, disseminated gold system at the North Bullion target, and identified new mineralized zones at the Bald Mountain and Central Bullion targets (Koehler et al., 2014). Drilling conducted by Gold Standard in 2014 focused on the Bald Mountain prospect and intersected significant thicknesses of altered and brecciated lithologies hosting Au-Ag-Cu mineralization. Drilling at North Bullion has been focused on expanding a zone of gold mineralization within the “lower collapse breccia” where sufficient data now exists to warrant an initial mineral resource estimate. Continued drilling on the Bald Mountain and Central Bullion targets is also warranted based on early-stage drill results. Early-stage results from 10 other target areas at the Railroad portion of the Project area indicate that additional geologic work and drilling is also warranted.

In early 2014, Gold Standard significantly increased its land position with the acquisition of the Pinion Project area which is contiguous to the south end of the Company’s original Railroad Project area (Koehler et al., 2014). The Pinion transaction primarily comprised the acquisition of mineral rights on lands where the Company previously held a minority interest, along with other lands where it previously held no interest, and was part of an on-going effort to consolidate the mineral rights for the greater Railroad District under a single operator. In April 2014, Gold Standard announced a further consolidation of mineral rights at Bald Mountain within the Railroad Project area and later announced the acquisition of lands and additional mineral rights within, and south of, the Pinion Project area covering the Dark Star and Dixie Creek gold prospects.

The acquisition, and further consolidation, of mineral rights at the Pinion Project area by Gold Standard in 2014 represents an important step in the advancement of the Railroad-Pinion Project. The Pinion portion of the Railroad-Pinion Project area now includes the Pinion, Dark Star and Dixie Creek gold prospects. Work by Gold Standard at the Pinion Project area in 2014 comprised the compilation and review of historic data at the Pinion and Dark Star Deposits and included a significant re-logging effort of archived Pinion core along with Pinion and Dark Star RC chip samples. An initial phase of drilling at the Pinion Deposit comprising 13 holes confirmed historic drilling assay results and the geological model for the deposit, which were utilized for a maiden NI 43-101 compliant mineral resource estimate that was constructed in September, 2014 (Dufresne et al., 2014). In late 2014, a second phase of drilling including 44 RC holes was completed at the Pinion Deposit area and was successful in expanding the extent of gold mineralization. Recent work has included the completion of a maiden NI 43-101 compliant mineral resource estimate for the Dark Star Deposit (Dufresne et al., 2015).

2014 Pinion Deposit Mineral Resource

The maiden NI 43-101 compliant Pinion mineral resource estimate was completed by APEX under the supervision and direction of Mr. Michael Dufresne, M.Sc., P.Geol., P.Geo. a co-author of the 2015 Railroad-Pinion Report. The Pinion Deposit mineral resource estimate is discussed in detail in the Pinion Resource Report by Dufresne et al. (2014).