UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-21749

CRM Mutual Fund Trust

(Exact name of registrant as specified in charter)

c/o Cramer Rosenthal McGlynn, LLC.

28 Havemeyer Place

Greenwich, CT 06830

(Address of principal executive offices) (Zip code)

Corporation Service Company

2711 Centerville Road Suite 400

Wilmington, DE 19808

(Name and address of agent for service)

Copy to:

Lea Anne Copenhefer

Morgan, Lewis & Bockius LLP

One Federal Street

Boston, MA 02110

Registrant’s telephone number, including area code: 212-326-5300

Date of fiscal year end: June 30

Date of reporting period: December 31, 2022

Item 1. Reports to Stockholders.

The Report to Shareholders is attached herewith.

SEMI-ANNUAL REPORT

December 31, 2022 (Unaudited)

CRM Small Cap Value Fund

CRM Small/Mid Cap Value Fund

CRM Mid Cap Value Fund

CRM All Cap Value Fund

CRM Long/Short Opportunities Fund |

SEMI-ANNUAL REPORT (Unaudited) | December 31, 2022 |

President’s Message |

Dear Fellow Shareholders:

2022 was one of the worst years for the market over the last few decades. The market also ended on a weak note, selling-off in December after staging a rally earlier in the period. Last year was a normalization period for the market as fiscal and monetary accommodation was being removed from the system. Interestingly, the market correction was mainly driven by P/E multiple compression as the discount rate normalized due to the dramatic rise in interest rates. We still expect earnings to be reset lower for the market as demand normalizes and margins are pressured. This is the unpleasant part of a normal market cycle. But, as history has shown us, these market inflections tend to lead to regime changes and new leadership in the market. We see multiple reasons to be bullish on small to mid-cap stocks over the next few years which, by the way, is a part of the market that’s woefully underinvested versus history. This is an exciting time to be an active manager down cap.

Small caps trading at extreme discount vs large caps

only ever seen once before during the Tech Bubble

(Relative Forward P/E Russell 2000® vs. Russell 1000®, 1985-10/31/22)

We see multiple vectors of demand drivers for domestic small to mid-cap stocks. After enduring tariff wars between the U.S. and China, a global pandemic, and Russia’s war against Ukraine, CEOs are being forced to rethink their global

1 |

supply chains. Just-in-time manufacturing is being replaced with safety stock and re-shoring or near-shoring efforts. More focus is being placed on certainty of production and delivery than the lowest cost available. We believe this is a long-term positive for domestic oriented businesses. In addition, the U.S. government has also woken up to the fact they need to work in partnership with businesses to ensure the availability of strategically important products. Over the past 18 months, Congress has passed several important pieces of legislation to support this effort including the $1 trillion Infrastructure Investment and Jobs Act, the CHIPS and Science Act ($52 billion for domestic semiconductor manufacturing), and $740 billion Inflation Reduction Act ($369 billion allocated to clean energy funding). These bills should spur capital expenditures (“cap ex”) in the U.S., which is expected to provide a multi-year growth tail wind for domestic oriented businesses, which we believe will disproportionately benefit small and mid-cap stocks.

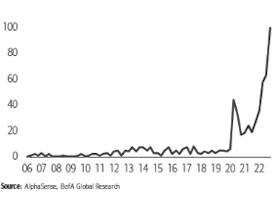

Small caps are particularly | Mentions of re-shoring on earnings calls have skyrocketed |

|  |

Inflation, although moderating from near term peak levels, remained higher than expected in 2022, which is highly constructive for small and mid-cap stocks. Goods inflation has led the recent declines in overall inflation as supply chains have been normalizing and consumer demand has shifted from goods to services. We still expect services inflation, the largest component of overall inflation, to remain sticky on the way down due to the robust labor market. Although recent indicators have pointed to a modest reduction in the labor costs (i.e., slower growth in December’s Average Hourly Earnings), the pandemic has likely resulted in a change in the percentage of profits shared with employees. The lack of labor availability due to health issues or immigration changes will likely slow the rebalancing necessary to return labor cost growth to a level more consistent with 2% inflation. We can debate the length of time required to achieve labor market equilibrium, but history tells us when inflation is above 3% but falling, this is a highly attractive market for small and mid-cap stocks.

2 |

The negative earnings revision cycle has begun. There are several pressures that will drive 2023 results downward including lower demand, higher interest rates, and less of a benefit from pricing. Since the second of half of 2022, small and mid-cap stocks have witnessed a sharper negative estimate revision cycle compared to large caps. Excluding the outsized energy sector contribution, the market now expects small and mid-caps’ estimates for 2023 to be flat to down while consensus still believe large cap stocks will generate positive earnings growth. As has been the case in the past, the market moves more quickly to revise small and mid-cap companies’ estimates compared to their larger cap brethren. As we have experienced in past cycles, stocks tend to rally before the trough in earnings, so the investor seeking to capture these returns needs to be invested prior to the turn. In addition, small and mid-cap stocks have historically tended to lead the market coming out of an economic slowdown.

At the same time, we continue to caution against relying on passive strategies to gain exposure to small and mid-cap stocks. As we have discussed in the past, the quality of market indices has declined dramatically over the past few years as newly formed SPACs, meme stocks, and non-profitable/non-revenue companies have become a greater percentage of the market. This creates an increasingly attractive market opportunity for nimble, active managers.

Return on Assets (“ROA”) levels are hitting new lows across the Russell indexes performance

Source: Factset; FTSE Russell; Jefferies

Nonearners weight has risen and will impact benchmark

Source: Factset; FTSE Russell; Jefferies

3 |

This was the third worst year for the Russell 2000® Value Index and the fourth worst year for the Russell Mid Cap® Value Index since 1979. Historically, small and mid-cap stocks tend to rally in the subsequent year after large downturns. The market sell-off has uncovered tremendous value for patient long-term investors. We believe investors should favor relative value, actively managed strategies with portfolios constructed with companies that have healthy balance sheets and growing market shares. We believe the small and mid-cap stocks have been more severely impacted during this sell-off and are extremely neglected today. This group, which tends to be more domestically oriented, should benefit from the re-shoring and near-shoring of supply chains that have failed many companies over the past few years. We also note that historically the best backdrop for small and mid-cap stocks tends to be when inflation is above 3% and declining, which appears to be the environment we are headed into. In sum, this appears to be a very attractive market for nimble, active managers in the small and mid cap value space.

The following is a discussion of factors that influenced the performance of each of the CRM Funds during the six-month period ended December 31, 2022.

CRM Small Cap Value Fund returned 10.08% and 9.94% for the Institutional and Investor Share classes, respectively, in the period, as compared to 3.42% and 3.91% for the Russell 2000® Value Index and the Russell 2000® Index, respectively2. Stock selection was the primary driver of outperformance during the period, most notably in the Industrials and Information Technology sectors. The portfolio also modestly benefitted from our underweight to the Communication Services and Industrials sectors relative to the benchmark. Leading contributors to performance for this period included (i) ChampionX Corporation; (ii) Valmont Industries, Inc.; and (iii) Agilysys, Inc. Oilfield services provider ChampionX Corporation (CHX) delivered strong third quarter 2022 results and raised its fourth quarter 2022 guidance. Over the near to medium term, we believe ChampionX will benefit from price increases enacted earlier in 2022, while raw materials costs begin to abate. Valmont Industries, Inc. (VMI), a utility and agricultural equipment provider, appreciated during the period as higher earnings were driven by strong customer demand and a favorable price/cost mix. The outlook for the company’s sales remains favorable, with elevated global farmer income along with tailwinds for utility spending based on resiliency upgrades and investments in renewable energy. Agilysys, Inc. (AGYS), a software provider to the hospitality and gaming industries, reported strong earnings during the period, supported by a combination of improving travel trends and continued market share gains.

Individual holdings that negatively impacted performance included (i) Kaman Corporation; (ii) Ollie’s Bargain Outlet Holdings, Inc.; and (iii) James River Group Holdings, Ltd. Kaman Corporation (KAMN), a diversified aviation and defense company, reported weaker-than-expected results during the period due to revenue recognition delays in its fuse and structures business that came about from supply

4 |

chain challenges. In addition, the company recently completed the acquisition of Parker-Hannifin’s aircraft wheel and brake business, a higher-value engineered products business, and funded the acquisition with debt. This increased balance sheet leverage, coupled with reduced earnings expectations in Kaman’s other business segments, reduced overall cash flows. Given the company’s reduced financial flexibility, we elected to exit the position during the period. Ollie’s Bargain Outlet Holdings, Inc. (OLLI), a retail chain operator that offers brand name products at deeply discounted prices, reported third quarter 2022 results that were below expectations due to a slowdown in retail spending towards the end of their fiscal quarter. James River Group Holdings (JRVR), a specialty Property & Casualty (P&C) insurer, declined following a third quarter 2022 earnings report in which the company reported in-line earnings but slower-than-expected premium growth. The lower premium growth relates to a conscious decision by management to reduce riskier exposures and focus on more stable lines of business, which we believe will benefit the company over the long-term.

CRM Small/Mid Cap Value Fund returned 5.19% and 5.11% for the Institutional and Investor Share classes, respectively, in the period, as compared to 4.29% and 4.40% for the Russell 2500TM Value Index and the Russell 2500TM Index, respectively3. The Consumer Discretionary and Energy sectors were the top contributors to performance during the period, primarily due to stock selection within each sector. Conversely, stock selection in the Industrials and Health Care sectors detracted slightly from overall Fund performance during the period. Individual holdings that were leading contributors to performance included (i) ChampionX Corporation; (ii) Clean Harbors, Inc.; and (iii) Burlington Stores, Inc. Oilfield services provider ChampionX Corporation (CHX) delivered strong third quarter 2022 results and raised its fourth quarter 2022 guidance. Over the near to medium term, we believe ChampionX will benefit from price increases enacted earlier in 2022, while raw materials costs begin to abate. Clean Harbors, Inc. (CLH) provides environmental remediation and industrial waste management services to domestic customers. The company was a top contributor during the period as operating results in both segments materially outperformed expectations. Strong demand and pricing for its environmental services drove the highest margin outperformance in the peer waste management sector from an achieved pricing versus cost perspective. The company also reiterated guidance in its used motor oil collection segment. Lastly, Clean Harbors is seeing longer-term demand in its customer base to utilize the company’s services to assist in customers’ Environmental, Social and Governance (“ESG”) efforts. Burlington Stores, Inc. (BURL), an off-price retailer, reported third quarter 2022 results that showed improved execution as the company continues to benefit from an increasingly favorable inventory backdrop and an inflection in customer trends.

Individual holdings that negatively affected performance included (i) Clarivate PLC; (ii) Kaman Corporation; and (iii) Tenable Holdings, Inc. Clarivate PLC

5 |

(CLVT), a data and analytics company focused on life sciences and intellectual property end markets, underperformed during the period because of weaker than anticipated growth in the fourth quarter 2022 due mainly to transactional revenues. We believe the new management team has recalibrated expectations conservatively and are uniquely well suited for executing on improving organic growth strategy as well as margin and free cash flow opportunities over the next few years. The equity price incorporates substantial neglect around improving fundamentals and we believe it currently trades at a substantial discount to intrinsic value. Kaman Corporation (KAMN), a diversified aviation and defense company, reported weaker-than-expected results during the period due to revenue recognition delays in its fuse and structures business that came about from supply chain challenges. In addition, the company recently completed the acquisition of Parker-Hannifin’s aircraft wheel and brake business, a higher-value engineered products business, and funded the acquisition with debt. This increased balance sheet leverage, coupled with reduced earnings expectations in Kaman’s other business segments, reduced overall cash flows. Given the company’s reduced financial flexibility, we elected to exit the position during the period. Tenable Holdings, Inc. (TENB), a cybersecurity software provider, beat expectations and raised their guidance during the period, but like other software companies highlighted weakness in Europe, which led to growing concerns about the strength of their forward outlook. We believe demand trends remain very robust, and the next few quarters’ organic performance should resolve any demand-related concerns.

CRM Mid Cap Value Fund returned 5.17% and 5.05% for the Institutional and Investor Share classes, respectively, in the six-month period, as compared to 5.01% and 5.43% for the Russell Midcap® Value Index and the Russell Midcap® Index, respectively4. Stock selection in the Consumer Discretionary and Energy sectors, as well as our underweight to the Real Estate sector were the largest contributors to Fund performance during the period. Conversely, stock selection in the Health Care and Industrials sectors was a headwind to performance. Individual holdings that contributed positively to performance during the period included (i) Burlington Stores, Inc.; (ii) ChampionX Corporation; and (iii) Valmont Industries, Inc. Burlington Stores, Inc. (BURL), an off-price retailer, reported third quarter 2022 results that showed improved execution as the company continues to benefit from an increasingly favorable inventory backdrop and an inflection in customer trends. Oilfield services provider ChampionX Corporation (CHX) delivered strong third quarter 2022 results and raised its fourth quarter 2022 guidance. Over the near to medium term, we believe ChampionX will benefit from price increases enacted earlier in 2022, while raw materials costs begin to abate. Valmont Industries, Inc. (VMI), a utility and agricultural equipment provider, appreciated during the period as higher earnings were driven by strong customer demand and a favorable price/cost mix. The outlook for the company’s sales remains favorable, with elevated

6 |

global farmer income along with tailwinds for utility spending based on resiliency upgrades and investments in renewable energy.

Holdings that detracted from Fund performance during the period included (i) Clarivate PLC; (ii) Avantor, Inc.; and (iii) Nomad Foods, Ltd. Clarivate PLC (CLVT), a data and analytics company focused on life sciences and intellectual property end markets, underperformed during the period because of weaker than anticipated growth in the fourth quarter 2022 due mainly to transactional revenues. We believe the new management team has recalibrated expectations conservatively and are uniquely well suited for executing on improving organic growth strategy as well as margin and free cash flow opportunities over the next few years. The equity price incorporates substantial neglect around improving fundamentals and we believe it currently trades at a substantial discount to intrinsic value. Avantor, Inc. (AVTR) is a global manufacturer and distributor of laboratory equipment, consumables, and services in the pharmaceuticals, government, academic, healthcare, clinical, and industrial end markets. The company was a detractor during the period as they lowered forward outlook on revenue and profit expectations due to softer performance in their two recent acquisitions, lower COVID-19 testing and vaccine contributions, as well as foreign exchange impacts. Recently at an investor conference, the company further revised expectations for its acquisition performance, yet importantly maintained that the core business is achieving its organic growth expectations. The combination of softer current expectations, poor communication on setting appropriate expectations, elevated leverage, as well as macroeconomic concerns have driven Avantor’s valuation to recession levels and a substantial discount to life science peers. Nomad Food (NOMD) is a producer of branded frozen food in Western Europe, including: vegetables, fish, pizza, ice cream, and other products. The company was a detractor to performance during the period, as it continued to experience volume pressure based on increased product pricing, while private label competition has maintained lower pricing on a similar product offering. We believe the company is getting closer to improving its margin profile given the moderating of commodity costs, but increased promotional activity and a plateau in its plant-based protein products may not allow for profit improvement in the medium term. Free cash flow has also underperformed, as inventory management has been challenging during this uncertain environment for its fish supply. We sold our position and will revisit the investment case when a clearer picture of volume and profit performance exists.

CRM All Cap Value Fund returned 5.34% and 5.27% for the Institutional and Investor Share classes, respectively, during the period, as compared to 5.95% and 2.40% for the Russell 3000® Value Index and the Russell 3000® Index, respectively5. Stock selection within the Financials sector, as well as our underweight to both the Communication Services and Real Estate sectors were the primary drivers of relative performance during the period. Conversely, stock selection within the Industrials and Health Care sectors detracted from performance during the period.

7 |

Leading contributors to Fund performance were (i) Valmont Industries, Inc.; (ii) ChampionX Corporation; and (iii) Burlington Stores, Inc. Valmont Industries, Inc. (VMI), a utility and agricultural equipment provider, appreciated during the period as higher earnings were driven by strong customer demand and a favorable price/cost mix. The outlook for the company’s sales remains favorable, with elevated global farmer income along with tailwinds for utility spending based on resiliency upgrades and investments in renewable energy. Oilfield services provider ChampionX Corporation (CHX) delivered strong third quarter 2022 results and raised its fourth quarter 2022 guidance. Over the near to medium term, we believe ChampionX will benefit from price increases enacted earlier in 2022, while raw materials costs begin to abate. Burlington Stores, Inc. (BURL), an off-price retailer, reported third quarter 2022 results that showed improved execution as the company continues to benefit from an increasingly favorable inventory backdrop and an inflection in customer trends.

Individual holdings that negatively impacted performance included (i) Clarivate PLC; (ii) Kaman Corporation; and (iii) Avantor, Inc. Clarivate PLC (CLVT), a data and analytics company focused on life sciences and intellectual property end markets, underperformed during the period because of weaker than anticipated growth in the fourth quarter 2022 due mainly to transactional revenues. We believe the new management team has recalibrated expectations conservatively and are uniquely well suited for executing on improving organic growth strategy as well as margin and free cash flow opportunities over the next few years. The equity price incorporates substantial neglect around improving fundamentals and we believe it currently trades at a substantial discount to intrinsic value. Kaman Corporation (KAMN), a diversified aviation and defense company, reported weaker-than-expected results during the period due to revenue recognition delays in its fuse and structures business that came about from supply chain challenges. In addition, the company recently completed the acquisition of Parker-Hannifin’s aircraft wheel and brake business, a higher-value engineered products business, and funded the acquisition with debt. This increased balance sheet leverage, coupled with reduced earnings expectations in Kaman’s other business segments, reduced overall cash flows. Given the company’s reduced financial flexibility, we elected to exit the position during the period. Avantor, Inc. (AVTR) is a global manufacturer and distributor of laboratory equipment, consumables, and services in the pharmaceuticals, government, academic, healthcare, clinical, and industrial end markets. The company was a detractor during the period as they lowered their forward outlook on revenue and profit expectations due to softer performance in their two recent acquisitions, lower COVID-19 testing and vaccine contributions, as well as foreign exchange impacts. Recently at an investor conference, the company further revised expectations for its acquisition performance, yet importantly maintained that the core business is achieving its organic growth expectations. The combination of softer current expectations, poor communication on setting

8 |

appropriate expectations, elevated leverage, as well as macroeconomic concerns have driven Avantor’s valuation to recession levels and a substantial discount to life science peers.

CRM Long/Short Opportunities Fund returned 3.91% in the first half of the fiscal year as compared to 2.31% for the S&P 500® Index6. During the six-month period ended December 31, 2022, both sides of the book contributed to overall performance. From a sector perspective, Health Care, Financials, and Consumer Discretionary contributed most to performance during the period, while Information Technology was the largest detractor. In terms of exposure during the period, the Fund averaged approximately 89% gross long, 49% gross short, and 39% net long. The top contributors in the long portfolio were (i) Clean Harbors, Inc.; (ii) Burlington Stores, Inc.; and (iii) Valmont Industries, Inc. Clean Harbors, Inc. (CLH) provides environmental remediation and industrial waste management services to domestic customers. The company was a top contributor during the period as operating results in both segments materially outperformed expectations. Strong demand and pricing for its environmental services drove the highest margin outperformance in the peer waste management sector from an achieved pricing versus cost perspective. The company also reiterated guidance in its used motor oil collection segment. Lastly, Clean Harbors is seeing longer-term demand in its customer base to utilize the company’s services to assist in customers’ Environmental, Social and Governance (“ESG”) efforts. Burlington Stores, Inc. (BURL), an off-price retailer, reported third quarter 2022 results that showed improved execution as the company continues to benefit from an increasingly favorable inventory backdrop and an inflection in customers trends. Valmont Industries, Inc. (VMI), a utility and agricultural equipment provider, appreciated during the period as higher earnings were driven by strong customer demand and a favorable price/cost mix. The outlook for the company’s sales remains favorable, with elevated global farmer income along with tailwinds for utility spending based on resiliency upgrades and investments in renewable energy.

Top individual names that negatively impacted the long portfolio included (i) Tenable Holdings; (ii) G-III Apparel Group, Inc.; and (iii) Avantor, Inc. Tenable Holdings, Inc. (TENB), a cybersecurity software provider, beat expectations and raised their guidance during the period, but like other software companies highlighted weakness in Europe, which led to growing concerns about the strength of their forward outlook. We believe demand trends remain very robust, and the next few quarters’ organic performance should resolve any demand-related concerns. Shares of G-III Apparel Group, Inc. (GIII), a global apparel, accessory and footwear manufacturer, traded off as investors worried about higher inventories in the channel and potential promotions. We exited our position after the company announced weaker than expected earnings and notably the loss of two key licensed brands over a multi-year period. Given the future decline in earnings and the lack of visibility we sold the position for better risk/reward opportunities. Avantor, Inc. (AVTR) is a global

9 |

manufacturer and distributor of laboratory equipment, consumables, and services in the pharmaceuticals, government, academic, healthcare, clinical, and industrial end markets. The company was a detractor during the period as they lowered their forward outlook on revenue and profit expectations due to softer performance in their two recent acquisitions, lower COVID-19 testing and vaccine contributions, as well as foreign exchange impacts. Recently at an investor conference, the company further revised expectations for its acquisition performance, yet importantly maintained that the core business is achieving its organic growth expectations. The combination of softer current expectations, poor communication on setting appropriate expectations, elevated leverage, as well as macroeconomic concerns have driven Avantor’s valuation to recession levels and a substantial discount to life science peers.

Our top short contributors included (i) a contract manufacturer in the healthcare sector; (ii) a genetic testing company; and (iii) a provider of food and animal health products. A contract manufacturer in the healthcare sector missed recent and forward margin expectations and will likely be losing its largest customer in the middle of 2023. The company is experiencing manufacturing and supply chain problems and is seeing a slower macroeconomic environment putting pressure on its customers’ ability to spend on additional growth. A genetic testing company reported lower results in the most recent period and for the balance of the calendar year, when the peer group all experienced substantial testing volume upside in similar categories. The company also purchased a pharma company, which may not prove to be an appropriate fit with the testing business. A provider of food and animal health products came into the calendar year with much higher pro forma guidance for a large merger, which doubled the size of the company. Over the course of the calendar year before the merger was completed, both entities had lower sales and operating performance which lowered expectations by approximately 30% post deal closing.

The top detractors in the short portfolio were (i) a footwear company; (ii) a commodity components company; and (iii) a U.S. based advertising agency. During the period, a footwear company posted better than expected earnings in their international business despite increasing price pressure in their domestic business. A commodity components company appreciated during the period on still strong pricing increases and a more benign forecast on margin normalization. A U.S. based advertising agency appreciated as demand for their services remained robust

10 |

even as digital spending initiatives slowed and as companies begin to cut back on marketing outlays due to a more uncertain economic outlook.

Sincerely,

Ronald H. McGlynn

Trustee and President, CRM Mutual Fund Trust

1“Picks and Shovels” is an investment strategy that refers to investing in businesses that supply the tools, services, or underlying technology needed to produce a final product. It’s an indirect way of investing in an industry without the greater risk of investing directly in the company that produces the finished product.

2Russell 2000® Value Index is the Fund’s benchmark. The Russell 2000® Value Index measures the performance of those companies in the Russell 2000® Index with lower price-to-book ratios and lower forecasted growth values. The Russell 2000® Index is an unmanaged, capitalization weighted index of 2,000 small cap U.S. companies. The returns of the indexes include the reinvestment of dividends but do not account for transaction costs or other expenses which an investor might incur in attempting to obtain such returns. It is not possible to invest directly in an index.

3Russell 2500TM Value Index is the Fund’s benchmark. The Russell 2500TM Value Index is an unmanaged index that measures the performance of those companies in the Russell 2500TM Index with lower price-to-book ratios and lower forecasted growth values. The Russell 2500TM Index is an unmanaged index that measures the performance of the 2,500 smallest companies in the Russell 3000® Index. The returns of the indexes include the reinvestment of dividends but do not account for transaction costs or other expenses which an investor might incur in attempting to obtain such returns. It is not possible to invest directly in an index.

4Russell Midcap® Value Index is the Fund’s benchmark. The Russell Midcap® Value Index measures the performance of those companies in the Russell Midcap® Index with lower price-to-book ratios and lower forecasted growth values. The Russell Midcap® Index measures the performance of the 800 smallest companies in the Russell 1000® Index, which represents the performance of the 1,000 largest companies in the U.S. equity market. The returns of the indexes include the reinvestment of dividends but do not account for transaction costs or other expenses which an investor might incur in attempting to obtain such returns. It is not possible to invest directly in an index.

5Russell 3000® Value Index is the Fund’s benchmark. The Russell 3000® Value Index measures the performance of those companies in the Russell 3000® Index with lower price-to-book ratios and lower forecasted growth values. The Russell 3000® Index is an unmanaged, capitalization weighted index of the 3,000 largest U.S. companies, which represent approximately 98% of the investable U.S. equity market. The returns of the indexes include the reinvestment of dividends but do not account for transaction costs or other expenses which an investor might incur in attempting to obtain such returns. It is not possible to invest directly in an index.

6The S&P 500® Index is the Fund’s benchmark. The S&P 500® Index is an index of 500 companies chosen for market size, liquidity and industry grouping, among other factors. The S&P 500® is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe. The returns of the index include the reinvestment of dividends but do not account for transaction costs or other expenses which an investor might incur in attempting to obtain such returns. It is not possible to invest directly in an index.

11 |

Performance quoted represents past performance and does not guarantee future results. Investment return and principal value will fluctuate. Shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than that shown here. Performance data current to the most recent month-end is available by calling (800) CRM-2883. During the period, certain fees and expenses were waived by the Funds’ service providers. Without these waivers, total returns would have been lower.

Fund holdings and sector allocations are subject to change at any time and are not recommendations to buy or sell any security. Please refer to the Schedules of Investments for a complete list of Fund holdings. The information contained herein is not a complete analysis of every aspect of any market, industry, security, or Fund. Opinions expressed herein are as of December 31, 2022 and are subject to change at any time, are not guaranteed, and should not be considered investment advice.

Investments in small and mid capitalization companies generally are more volatile due to limited product lines, fewer capital resources and less depth of management than larger companies. Value-based investments are subject to the risk that the broad market may not recognize their intrinsic values or that the investment has not been undervalued by the market. Investments in foreign securities, including emerging markets, involve special risks such as greater social, economic, regulatory, and political uncertainties, and currency fluctuation.

The Long/Short Opportunities Fund will hold long equity securities that the Fund’s adviser has identified as undervalued and take short positions (through short sales) in equity securities that the Fund’s adviser has identified as overvalued or poised for underperformance. Short sales involve significant risks, including the risk that the Fund may have to cover its short position at a higher price than the short sale price, resulting in a loss. Short sales involve borrowing securities and then selling them, which may cause the value of the Fund’s shares to be more volatile than if the Fund did not borrow.

The information concerning the Funds included in the shareholder report contains certain forward-looking statements about the factors that may affect the performance of the Funds in the future. These statements are based on Fund management’s predictions and expectations concerning certain future events and their expected impact on the Funds, such as performance of the economy as a whole and of specific industry sectors, the impact of developing world events, and other factors that may influence the future performance of the Funds. Management believes these forward-looking statements to be reasonable, although they are inherently uncertain and difficult to predict. Actual events may cause adjustments in portfolio management strategies from those currently expected to be employed.

This report must be preceded or accompanied by the current prospectus for the Funds. Before investing, you should carefully read the prospectus and consider the investment objectives, risks, charges and expenses of the Funds. Additional copies of the prospectus may be obtained at www.crmfunds.com or at 800-CRM-2883.

Distributed by ALPS Distributors, Inc.

12 |

CRM FUNDS EXPENSE DISCLOSURE (Unaudited) |

DISCLOSURE OF FUND EXPENSES

The following Expense Tables are shown so that you can understand the impact of fees on your investment. All mutual funds have operating expenses. As a shareholder of a Fund, you incur ongoing costs, including management fees, shareholder servicing fees and other Fund expenses. A Fund’s expenses are expressed as a percentage of its average net assets. This figure is known as the expense ratio. The following examples are intended to help you understand the ongoing costs (in dollars) of investing in a Fund and to compare these costs with the ongoing costs of investing in other mutual funds. The examples are based on an investment of $1,000 made at the beginning of the period shown and held for the entire period (July 1, 2022 through December 31, 2022). The “Annualized Expense Ratio” reflects the actual expenses, net of fee waivers, where applicable, for the six-month period July 1, 2022 to December 31, 2022.

The Expense Tables below illustrate your Fund’s expenses in two ways.

● | Actual fund return. The first line of the table below provides information about actual account values and actual expenses. You may use the information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During Period” to estimate the expenses you paid on your account during the period. |

● | Hypothetical 5% return. The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid for the period. You may use this information to compare the ongoing cost of investing in the Fund and other funds. To do so, compare this 5% hypothetical example with the 5% hypothetical examples that appear in the shareholder reports of the other funds. |

Please note that the expenses shown in the tables are meant to highlight your ongoing costs only and do not reflect any transactional costs that may be levied by

CRM Funds | ||

13 |

CRM FUNDS EXPENSE DISCLOSURE (Unaudited) (Continued) |

other funds, such as sales charges (loads), redemption fees, or exchange fees, if any. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total cost of owning different funds. In addition, if these transactional costs were included, your costs would have been higher. The “Annualized Expense Ratio” reflects the actual expenses for the period indicated.

For the Six Months Ended December 31, 2022

Expense Table

Fund/Class | Beginning | Ending | Annualized | Expenses | ||||||||||||

CRM Small Cap Value Fund - Investor Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,099.40 | 1.22 | % | $ | 6.46 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.06 | 1.22 | % | $ | 6.21 | ||||||||

CRM Small Cap Value Fund - Institutional Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,100.80 | 1.05 | % | $ | 5.56 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.91 | 1.05 | % | $ | 5.35 | ||||||||

CRM Small/Mid Cap Value Fund - Investor Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,051.10 | 1.19 | % | $ | 6.15 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.21 | 1.19 | % | $ | 6.06 | ||||||||

CRM Small/Mid Cap Value Fund - Institutional Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,051.90 | 1.03 | % | $ | 5.33 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.01 | 1.03 | % | $ | 5.24 | ||||||||

CRM Mid Cap Value Fund - Investor Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,050.50 | 1.15 | % | $ | 5.94 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.41 | 1.15 | % | $ | 5.85 | ||||||||

CRM Funds | ||

14 |

CRM FUNDS EXPENSE DISCLOSURE (Unaudited) (Concluded) |

Fund/Class | Beginning | Ending | Annualized | Expenses | ||||||||||||

CRM Mid Cap Value Fund - Institutional Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,051.70 | 0.99 | % | $ | 5.12 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,020.21 | 0.99 | % | $ | 5.04 | ||||||||

CRM All Cap Value Fund - Investor Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,052.70 | 1.37 | % | $ | 7.09 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,018.30 | 1.37 | % | $ | 6.97 | ||||||||

CRM All Cap Value Fund - Institutional Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,053.40 | 1.14 | % | $ | 5.90 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,019.46 | 1.14 | % | $ | 5.80 | ||||||||

CRM Long/Short Opportunities Fund - Institutional Shares | ||||||||||||||||

Actual Fund Return | $ | 1,000.00 | $ | 1,039.10 | 2.27 | % | $ | 11.67 | ||||||||

Hypothetical (5% Return Before Expenses) | $ | 1,000.00 | $ | 1,013.76 | 2.27 | % | $ | 11.52 | ||||||||

(1) | The expense ratio for CRM Long/Short Opportunities Fund includes the impact of dividend expense and net interest expense (when applicable), on securities sold short. Excluding such expenses, the ratio of expenses to average net assets would have been 1.60%. |

(2) | Expenses are equal to the Fund’s annualized expense ratio multiplied by the average account value over the period, multiplied by 184/ 365 (to reflect the most recent one-half year period). |

CRM Funds | ||

15 |

CRM FUNDS DISCLOSURE OF PORTFOLIO HOLDINGS (Unaudited) |

PORTFOLIO HOLDINGS

December 31, 2022

The following tables present a summary of the portfolio holdings of each of the CRM Funds as a percentage of their total investments, before short-term investments held as collateral for loaned securities.

CRM Small Cap Value Fund- | |

Common Stock | |

Financials | 21.5% |

Industrials | 18.5 |

Real Estate | 9.0 |

Consumer Staples | 8.3 |

Technology | 7.6 |

Health Care | 7.4 |

Utilities | 7.1 |

Energy | 6.8 |

Consumer Discretionary | 6.0 |

Materials | 2.5 |

Short-Term Investments | 5.3 |

100.0% | |

CRM Small/Mid Cap Value Fund- | |

Common Stock | |

Financials | 20.2% |

Industrials | 15.7 |

Technology | 12.6 |

Consumer Discretionary | 10.3 |

Materials | 9.9 |

Health Care | 9.4 |

Energy | 6.8 |

Utilities | 6.3 |

Real Estate | 5.7 |

Consumer Staples | 3.1 |

100.0% | |

CRM Mid Cap Value Fund- | |

Common Stock | |

Industrials | 16.8% |

Financials | 14.9 |

Technology | 12.6 |

Materials | 10.2 |

Utilities | 9.9 |

Consumer Discretionary | 9.8 |

Health Care | 8.1 |

Energy | 6.6 |

Real Estate | 3.9 |

Consumer Staples | 3.3 |

Short-Term Investments | 3.9 |

100.0% | |

CRM All Cap Value Fund- | |

Common Stock | |

Technology | 18.6% |

Financials | 17.2 |

Health Care | 17.2 |

Industrials | 12.8 |

Consumer Discretionary | 9.3 |

Energy | 6.5 |

Materials | 6.2 |

Consumer Staples | 3.0 |

Utilities | 2.5 |

Real Estate | 2.3 |

Short-Term Investments | 4.4 |

100.0% | |

CRM Funds | ||

16 |

CRM FUNDS DISCLOSURE OF PORTFOLIO HOLDINGS (Unaudited) (Concluded) |

The following tables present a summary of the portfolio holdings of the CRM Long/Short Opportunities Fund as a percentage of its total net assets.

CRM Long/Short Opportunities Fund- | |

Common Stock | |

Industrials | 16.7% |

Technology | 15.8 |

Consumer Discretionary | 15.3 |

Financials | 9.7 |

Health Care | 9.2 |

Consumer Staples | 5.2 |

Utilities | 5.0 |

Energy | 3.6 |

Communications | 3.4 |

Short-Term Investments | 13.4 |

Common Stock Sold Short | |

Industrials | (13.0) |

Consumer Discretionary | (10.2) |

Technology | (5.9) |

Financials | (4.3) |

Communications | (3.4) |

Health Care | (2.8) |

Consumer Staples | (2.5) |

Real Estate | (2.5) |

Materials | (1.6) |

Utilities | (1.3) |

Energy | (0.5) |

49.3% | |

Portfolio holdings are subject to change at any time.

CRM Funds | ||

17 |

CRM FUNDS CRM SMALL CAP VALUE FUND SCHEDULE OF INVESTMENTS December 31, 2022 (Unaudited) |

Shares | Value | |||||||

COMMON STOCK — 95.8% | ||||||||

Consumer Discretionary — 6.1% | ||||||||

Apparel & Textile Products — 2.4% | ||||||||

| 86,139 | Steven Madden Ltd.1 | $ | 2,753,002 | |||||

Home Construction — 1.5% | ||||||||

| 32,586 | Skyline Champion Corporation1 | 1,678,505 | ||||||

Leisure Facilities & Services — 2.2% | ||||||||

| 94,286 | BJ’s Restaurants, Inc.1 | 2,487,265 | ||||||

Total Consumer Discretionary | 6,918,772 | |||||||

Consumer Staples — 8.4% | ||||||||

Beverages — 1.1% | ||||||||

| 81,607 | Primo Water Corporation | 1,268,173 | ||||||

Food — 4.9% | ||||||||

| 145,919 | Hostess Brands, Inc.1 | 3,274,422 | ||||||

| 60,865 | The Simply Good Foods Company1 | 2,314,696 | ||||||

| 5,589,118 | ||||||||

Retail - Consumer Staples — 2.4% | ||||||||

| 56,636 | Ollie’s Bargain Outlet Holdings, Inc.1 | 2,652,830 | ||||||

Total Consumer Staples | 9,510,121 | |||||||

Energy — 6.9% | ||||||||

Oil & Gas Producers — 3.1% | ||||||||

| 62,070 | Matador Resources Company | 3,552,887 | ||||||

Oil & Gas Services & Equipment — 3.8% | ||||||||

| 147,019 | ChampionX Corporation | 4,262,081 | ||||||

Total Energy | 7,814,968 | |||||||

Financials — 21.7% | ||||||||

Banking — 16.8% | ||||||||

| 26,827 | Amalgamated Financial Corporation | 618,094 | ||||||

| 127,484 | Cadence Bank | 3,143,755 | ||||||

| 139,415 | Central Pacific Financial Corporation1 | 2,827,336 | ||||||

| 131,555 | CVB Financial Corporation | 3,387,542 | ||||||

Shares | Value | |||||||

Financials — (continued) | ||||||||

Banking — (continued) | ||||||||

| 97,433 | First Interstate Bancsystem, Inc., Class A | $ | 3,765,786 | |||||

| 67,282 | Hancock Whitney Corporation | 3,255,776 | ||||||

| 159,059 | Heritage Commerce Corporation | 2,067,767 | ||||||

| 19,066,056 | ||||||||

Insurance — 4.9% | ||||||||

| 100,211 | Horace Mann Educators Corporation | 3,744,885 | ||||||

| 88,670 | James River Group Holdings, Ltd. | 1,854,090 | ||||||

| 5,598,975 | ||||||||

Total Financials | 24,665,031 | |||||||

Health Care — 7.5% | ||||||||

Biotechnology & Pharmaceuticals — 2.0% | ||||||||

| 147,712 | ABCAM PLC – ADR1,2,3 | 2,298,399 | ||||||

Medical Equipment & Devices — 5.5% | ||||||||

| 94,852 | Envista Holdings Corporation1 | 3,193,666 | ||||||

| 65,189 | LeMaitre Vascular, Inc. | 2,999,998 | ||||||

| 6,193,664 | ||||||||

Total Health Care | 8,492,063 | |||||||

Industrials — 18.7% | ||||||||

Aerospace & Defense — 3.1% | ||||||||

| 87,537 | Barnes Group, Inc. | 3,575,886 | ||||||

Commercial Support Services — 2.4% | ||||||||

| 24,061 | Clean Harbors, Inc.1 | 2,745,841 | ||||||

Electrical Equipment — 2.5% | ||||||||

| 43,263 | SPX Technologies, Inc.1 | 2,840,216 | ||||||

Engineering & Construction — 2.6% | ||||||||

| 54,995 | Arcosa, Inc. | 2,988,428 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

18 | ||

CRM FUNDS CRM SMALL CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Shares | Value | |||||||

Industrials — (continued) | ||||||||

Industrial Intermediate Products — 3.2% | ||||||||

| 78,285 | Janus International Group, Inc.1 | $ | 745,273 | |||||

| 8,569 | Valmont Industries, Inc. | 2,833,512 | ||||||

| 3,578,785 | ||||||||

Industrial Support Services — 1.9% | ||||||||

| 16,812 | Applied Industrial Technologies, Inc. | 2,118,816 | ||||||

Transportation & Logistics — 3.0% | ||||||||

| 52,410 | Kirby Corporation1 | 3,372,584 | ||||||

Total Industrials | 21,220,556 | |||||||

Materials — 2.5% | ||||||||

Chemicals — 2.5% | ||||||||

| 40,323 | HB Fuller Company | 2,887,933 | ||||||

Real Estate — 9.2% | ||||||||

REIT — 9.2% | ||||||||

| 70,962 | American Assets Trust, Inc. | 1,880,493 | ||||||

| 135,335 | Equity Commonwealth1 | 3,379,314 | ||||||

| 30,707 | Terreno Realty Corporation | 1,746,307 | ||||||

| 145,431 | Urban Edge Properties | 2,049,123 | ||||||

| 101,553 | Xenia Hotels & Resorts, Inc. | 1,338,469 | ||||||

Total Real Estate | 10,393,706 | |||||||

Technology — 7.7% | ||||||||

Software — 6.0% | ||||||||

| 38,794 | Agilysys, Inc.1 | 3,070,157 | ||||||

| 61,262 | Envestnet, Inc.1 | 3,779,866 | ||||||

| 6,850,023 | ||||||||

Technology Services — 1.7% | ||||||||

| 243,360 | Paya Holdings, Inc.1 | 1,915,243 | ||||||

Total Technology | 8,765,266 | |||||||

Shares | Value | |||||||

Utilities — 7.1% | ||||||||

Electric Utilities — 2.4% | ||||||||

| 38,674 | Black Hills Corporation | $ | 2,720,329 | |||||

Gas & Water Utilities — 4.7% | ||||||||

| 47,235 | Northwest Natural Holdings Company | 2,247,914 | ||||||

| 38,842 | SJW Group1 | 3,153,582 | ||||||

| 5,401,496 | ||||||||

Total Utilities | 8,121,825 | |||||||

TOTAL COMMON STOCK (Cost $97,327,443) | 108,790,241 | |||||||

SHORT-TERM INVESTMENTS — 5.4% | ||||||||

| 3,057,207 | Blackrock Liquidity Funds T-Fund, Institutional Shares, 4.03%4 | 3,057,207 | ||||||

| 3,057,209 | Federated Hermes Treasury Obligations Fund, Institutional Shares, 4.14%4 | 3,057,209 | ||||||

TOTAL SHORT-TERM INVESTMENTS (Cost $6,114,416) | 6,114,416 | |||||||

TOTAL INVESTMENTS — 101.2% (Cost $103,441,859) | $ | 114,904,657 | ||||||

LIABILITIES IN EXCESS OF OTHER ASSETS — (1.2)% | (1,404,245 | ) | ||||||

NET ASSETS — 100.0% | $ | 113,500,412 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

19 | ||

CRM FUNDS CRM SMALL CAP VALUE FUND SCHEDULE OF INVESTMENTS (Concluded) December 31, 2022 (Unaudited) |

A summary of inputs used to value the Fund’s investments as of December 31, 2022 is as follows (see Note 2 in Notes to Financial Statements):

Assets | Level 1 | Level 2 | Level 3 | Investments | ||||||||||||

Common Stock | $ | 108,790,241 | — | — | $ | 108,790,241 | ||||||||||

Short-Term Investments | 6,114,416 | — | — | 6,114,416 | ||||||||||||

Total | $ | 114,904,657 | — | — | $ | 114,904,657 | ||||||||||

There were no transfers into or out of Level 3 related to securities held at December 31, 2022.

1 | Non-income producing security. |

2 | PLC – Public Limited Company |

3 | ADR – American Depositary Receipt |

4 | Rate disclosed is the seven day effective yield as of December 31, 2022. |

See accompanying notes to financial statements. | CRM Funds | |

20 | ||

CRM FUNDS CRM SMALL/MID CAP VALUE FUND SCHEDULE OF INVESTMENTS December 31, 2022 (Unaudited) |

Shares | Value | |||||||

COMMON STOCK — 95.4% | ||||||||

Consumer Discretionary — 9.8% | ||||||||

Home Construction — 1.2% | ||||||||

| 37,289 | Skyline Champion Corporation1 | $ | 1,920,756 | |||||

Leisure Facilities & Services — 1.3% | ||||||||

| 15,271 | Marriott Vacations Worldwide Corporation1 | 2,055,324 | ||||||

Retail - Discretionary — 4.4% | ||||||||

| 25,878 | Burlington Stores, Inc.1 | 5,247,023 | ||||||

| 6,325 | RH1 | 1,689,977 | ||||||

| 6,937,000 | ||||||||

Wholesale - Discretionary — 2.9% | ||||||||

| 83,415 | LKQ Corporation | 4,455,195 | ||||||

Total Consumer Discretionary | 15,368,275 | |||||||

Consumer Staples — 3.0% | ||||||||

Food — 3.0% | ||||||||

| 52,899 | Lamb Weston Holdings, Inc. | 4,727,055 | ||||||

Energy — 6.5% | ||||||||

Oil & Gas Producers — 2.3% | ||||||||

| 15,851 | Pioneer Natural Resources Company | 3,620,210 | ||||||

Oil & Gas Services & Equipment — 3.7% | ||||||||

| 198,140 | ChampionX Corporation | 5,744,079 | ||||||

Renewable Energy — 0.5% | ||||||||

| 35,652 | Sunrun, Inc.1 | 856,361 | ||||||

Total Energy | 10,220,650 | |||||||

Financials — 19.3% | ||||||||

Asset Management — 2.4% | ||||||||

| 17,403 | LPL Financial Holdings, Inc. | 3,762,007 | ||||||

Banking — 9.6% | ||||||||

| 120,390 | Cadence Bank | 2,968,817 | ||||||

| 105,639 | CVB Financial Corporation | 2,720,204 | ||||||

Shares | Value | |||||||

Financials — (continued) | ||||||||

Banking — (Continued) | ||||||||

| 134,670 | First Interstate Bancsystem, Inc., Class A | $ | 5,204,995 | |||||

| 88,188 | Webster Financial Corporation | 4,174,820 | ||||||

| 15,068,836 | ||||||||

Insurance — 7.3% | ||||||||

| 37,488 | American Financial Group, Inc. | 5,146,352 | ||||||

| 105,488 | James River Group Holdings, Ltd. | 2,205,754 | ||||||

| 55,924 | W.R. Berkley Corporation | 4,058,405 | ||||||

| 11,410,511 | ||||||||

Total Financials | 30,241,354 | |||||||

Health Care — 8.9% | ||||||||

Biotechnology & Pharmaceuticals — 2.0% | ||||||||

| 203,612 | ABCAM PLC - ADR1,2,3 | 3,168,203 | ||||||

Medical Equipment & Devices — 6.9% | ||||||||

| 9,997 | Bio-Rad Laboratories, Inc., Class A1 | 4,203,639 | ||||||

| 126,685 | Envista Holdings Corporation1 | 4,265,484 | ||||||

| 27,923 | QuidelOrtho Corporation1 | 2,392,163 | ||||||

| 10,861,286 | ||||||||

Total Health Care | 14,029,489 | |||||||

Industrials — 15.0% | ||||||||

Aerospace & Defense — 1.5% | ||||||||

| 6,071 | Teledyne Technologies, Inc.1 | 2,427,854 | ||||||

Commercial Support Services — 3.0% | ||||||||

| 40,974 | Clean Harbors, Inc.1 | 4,675,953 | ||||||

Electrical Equipment — 4.1% | ||||||||

| 60,823 | nVent Electric PLC3 | 2,339,861 | ||||||

| 209,659 | Vontier Corporation1 | 4,052,708 | ||||||

| 6,392,569 | ||||||||

See accompanying notes to financial statements. | CRM Funds | |

21 | ||

CRM FUNDS CRM SMALL/MID CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Shares | Value | |||||||

Industrials — (continued) | ||||||||

Industrial Intermediate Products — 2.9% | ||||||||

| 116,718 | Janus International Group, Inc.1 | $ | 1,111,155 | |||||

| 10,571 | Valmont Industries, Inc. | 3,495,513 | ||||||

| 4,606,668 | ||||||||

Machinery — 1.0% | ||||||||

| 13,289 | Regal Rexnord Corporation | 1,594,414 | ||||||

Transportation & Logistics — 2.5% | ||||||||

| 60,394 | Kirby Corporation1 | 3,886,354 | ||||||

Total Industrials | 23,583,812 | |||||||

Materials — 9.4% | ||||||||

Chemicals — 6.6% | ||||||||

| 54,305 | Ashland, Inc. | 5,839,416 | ||||||

| 46,320 | RPM International, Inc. | 4,513,884 | ||||||

| 10,353,300 | ||||||||

Construction Materials — 2.8% | ||||||||

| 33,689 | Eagle Materials, Inc. | 4,475,584 | ||||||

Total Materials | 14,828,884 | |||||||

Real Estate — 5.5% | ||||||||

REIT — 5.5% | ||||||||

| 153,916 | Equity Commonwealth1 | 3,843,282 | ||||||

| 27,932 | Terreno Realty Corporation | 1,588,493 | ||||||

| 222,006 | Urban Edge Properties | 3,128,065 | ||||||

Total Real Estate | 8,559,840 | |||||||

Technology — 12.0% | ||||||||

Software — 9.7% | ||||||||

| 497,407 | Clarivate PLC1,3 | 4,148,374 | ||||||

| 81,072 | Envestnet, Inc.1 | 5,002,143 | ||||||

| 22,338 | PTC, Inc.1 | 2,681,454 | ||||||

| 88,320 | Tenable Holdings, Inc.1 | 3,369,408 | ||||||

| 15,201,379 | ||||||||

Technology Hardware — 2.3% | ||||||||

| 71,382 | Ciena Corporation1 | 3,639,054 | ||||||

Total Technology | 18,840,433 | |||||||

Shares | Value | |||||||

Utilities — 6.0% | ||||||||

Electric Utilities — 3.7% | ||||||||

| 30,554 | Black Hills Corporation | $ | 2,149,168 | |||||

| 51,225 | NextEra Energy Partners LP4,5 | 3,590,360 | ||||||

| 5,739,528 | ||||||||

Gas & Water Utilities — 2.3% | ||||||||

| 133,764 | Nisource, Inc. | 3,667,809 | ||||||

Total Utilities | 9,407,337 | |||||||

TOTAL COMMON STOCK (Cost $118,346,416) | 149,807,129 | |||||||

TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENTS HELD AS COLLATERAL FOR LOANED SECURITIES – 95.4% (Cost $118,346,416) | 149,807,129 | |||||||

Principal | ||||||||

SHORT-TERM INVESTMENTS HELD AS COLLATERAL FOR LOANED SECURITIES — 2.5% | ||||||||

REPURCHASE AGREEMENTS — 2.5% | ||||||||

| 1,000,000 | With Citigroup Global Markets, Inc.: at 4.25%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $1,000,472 (collateralized by US Treasury Securities, par values ranging from $0 - $213,551, coupon rates ranging from 0.00% to 4.50%, 4/11/23 – 10/31/29; total market value $1,020,000) | 1,000,000 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

22 | ||

CRM FUNDS CRM SMALL/MID CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Principal | Value | |||||||

REPURCHASE AGREEMENTS — (continued) | ||||||||

| 922,949 | With HSBC Securities USA, Inc.: at 4.25%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $923,385 (collateralized by US Treasury Securities, par values ranging from $291 - $479,166, coupon rates ranging from 0.00% to 4.50%, 4/30/23 - 2/15/51; total market value $941,408) | $ | 922,949 | |||||

| 1,000,000 | With JP Morgan Securities LLC: at 4.26%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $1,000,473 (collateralized by US Treasury Securities, par values ranging from $7,219 - $1,017,711, coupon rates ranging from 0.00% to 0.13%, 5/15/23 – 12/28/23; total market value $1,020,000) | 1,000,000 | ||||||

Principal | Value | |||||||

REPURCHASE AGREEMENTS — (continued) | ||||||||

| 1,000,000 | With Mizuho Securities USA, LLC.: at 4.25%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $1,000,472 (collateralized by US Treasury Securities, par values ranging from $6,007 - $449,997, coupon rates ranging from 0.75% to 2.88%, 1/31/23 – 5/15/28; total market value $1,020,001) | $ | 1,000,000 | |||||

TOTAL SHORT-TERM INVESTMENTS HELD AS COLLATERAL FOR LOANED SECURITIES (Cost $3,922,949) | 3,922,949 | |||||||

TOTAL INVESTMENTS — 97.9% (Cost $122,269,365) | $ | 153,730,078 | 6 | |||||

OTHER ASSETS IN EXCESS OF LIABILITIES — 2.1% | 3,283,000 | |||||||

NET ASSETS — 100.0% | $ | 157,013,078 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

23 | ||

CRM FUNDS CRM SMALL/MID CAP VALUE FUND SCHEDULE OF INVESTMENTS (Concluded) December 31, 2022 (Unaudited) |

A summary of inputs used to value the Fund’s investments as of December 31, 2022 is as follows (see Note 2 in Notes to Financial Statements):

Assets | Level 1 | Level 2 | Level 3 | Investments | ||||||||||||

Common Stock | $ | 149,807,129 | — | — | $ | 149,807,129 | ||||||||||

Short-Term Investments Held As Collateral For Loaned Securities | — | $ | 3,922,949 | — | 3,922,949 | |||||||||||

Total | $ | 149,807,129 | $ | 3,922,949 | — | $ | 153,730,078 | |||||||||

There were no transfers into or out of Level 3 related to securities held at December 31, 2022.

1 | Non-income producing security. |

2 | ADR – American Depositary Receipt |

3 | PLC – Public Limited Company |

4 | LP – Limited Partnership |

5 | Security partially or fully on loan. |

6 | At December 31, 2022, the market value of securities on loan for CRM Small/Mid Cap Value Fund was $3,804,874. In the event that the collateral received is insufficient to cover the value of the loaned securities and provided such collateral shortfall is not the result of investment losses, the Fund’s securities lending agent, The Bank of New York Mellon, has agreed to pay the amount of the shortfall to the Fund, or at its discretion, replace the loaned securities. |

See accompanying notes to financial statements. | CRM Funds | |

24 | ||

CRM FUNDS CRM MID CAP VALUE FUND SCHEDULE OF INVESTMENTS December 31, 2022 (Unaudited) |

Shares | Value | |||||||

COMMON STOCK — 96.1% | ||||||||

Consumer Discretionary — 9.8% | ||||||||

Apparel & Textile Products — 1.9% | ||||||||

| 247,272 | Steven Madden Ltd.1 | $ | 7,902,813 | |||||

Leisure Facilities & Services — 1.2% | ||||||||

| 38,632 | Marriott Vacations Worldwide Corporation1 | 5,199,481 | ||||||

Retail - Discretionary — 3.7% | ||||||||

| 75,466 | Burlington Stores, Inc.1 | 15,301,486 | ||||||

Wholesale - Discretionary — 3.0% | ||||||||

| 233,933 | LKQ Corporation | 12,494,362 | ||||||

Total Consumer Discretionary | 40,898,142 | |||||||

Consumer Staples — 3.3% | ||||||||

Food — 3.3% | ||||||||

| 152,608 | Lamb Weston Holdings, Inc. | 13,637,051 | ||||||

Energy — 6.6% | ||||||||

Oil & Gas Producers — 2.8% | ||||||||

| 51,932 | Pioneer Natural Resources Company | 11,860,749 | ||||||

Oil & Gas Services & Equipment — 3.8% | ||||||||

| 544,720 | ChampionX Corporation | 15,791,433 | ||||||

Total Energy | 27,652,182 | |||||||

Financials — 14.9% | ||||||||

Asset Management — 2.4% | ||||||||

| 45,822 | LPL Financial Holdings, Inc. | 9,905,342 | ||||||

Banking — 5.6% | ||||||||

| 246,212 | Cadence Bank | 6,071,588 | ||||||

| 61,865 | First Republic Bank | 7,540,725 | ||||||

| 202,759 | Webster Financial Corporation | 9,598,611 | ||||||

| 23,210,924 | ||||||||

Institutional Financial Services — 1.0% | ||||||||

| 55,703 | State Street Corporation | 4,320,882 | ||||||

Shares | Value | |||||||

Financials — (continued) | ||||||||

Insurance — 5.9% | ||||||||

| 104,372 | American Financial Group, Inc. | $ | 14,328,187 | |||||

| 141,310 | W.R. Berkley Corporation | 10,254,867 | ||||||

| 24,583,054 | ||||||||

Total Financials | 62,020,202 | |||||||

Health Care — 8.1% | ||||||||

Medical Equipment & Devices — 8.1% | ||||||||

| 236,950 | Avantor, Inc.1 | 4,997,276 | ||||||

| 26,572 | Bio-Rad Laboratories, Inc., Class A1 | 11,173,260 | ||||||

| 333,977 | Envista Holdings Corporation1 | 11,245,005 | ||||||

| 74,453 | QuidelOrtho Corporation1 | 6,378,389 | ||||||

Total Health Care | 33,793,930 | |||||||

Industrials — 16.8% | ||||||||

Aerospace & Defense — 4.1% | ||||||||

| 21,165 | Teledyne Technologies, Inc.1 | 8,464,095 | ||||||

| 90,168 | Woodward, Inc. | 8,711,131 | ||||||

| 17,175,226 | ||||||||

Electrical Equipment — 6.6% | ||||||||

| 81,191 | AMETEK, Inc. | 11,344,006 | ||||||

| 161,569 | nVent Electric PLC2 | 6,215,559 | ||||||

| 503,594 | Vontier Corporation1 | 9,734,472 | ||||||

| 27,294,037 | ||||||||

Industrial Intermediate Products — 2.2% | ||||||||

| 28,161 | Valmont Industries, Inc. | 9,311,998 | ||||||

Industrial Support Services — 0.7% | ||||||||

| 21,394 | Applied Industrial Technologies, Inc. | 2,696,286 | ||||||

Machinery — 1.0% | ||||||||

| 35,456 | Regal Rexnord Corporation | 4,254,011 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

25 | ||

CRM FUNDS CRM MID CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Shares | Value | |||||||

Industrials — (continued) | ||||||||

Transportation & Logistics — 2.2% | ||||||||

| 123,740 | Canadian Pacific Railway Ltd.3 | $ | 9,229,767 | |||||

Total Industrials | 69,961,325 | |||||||

Materials — 10.2% | ||||||||

Chemicals — 10.2% | ||||||||

| 140,448 | Ashland, Inc. | 15,102,373 | ||||||

| 259,876 | Corteva, Inc. | 15,275,512 | ||||||

| 123,283 | RPM International, Inc. | 12,013,928 | ||||||

Total Materials | 42,391,813 | |||||||

Real Estate — 3.9% | ||||||||

REIT — 3.9% | ||||||||

| 77,380 | American Assets Trust, Inc. | 2,050,570 | ||||||

| 402,152 | Equity Commonwealth1 | 10,041,735 | ||||||

| 152,522 | Highwoods Properties, Inc. | 4,267,566 | ||||||

Total Real Estate | 16,359,871 | |||||||

Technology — 12.6% | ||||||||

Semiconductors — 2.2% | ||||||||

| 133,943 | Microchip Technology, Inc. | 9,409,496 | ||||||

Software — 6.2% | ||||||||

| 1,325,798 | Clarivate PLC1,2 | 11,057,155 | ||||||

| 58,872 | PTC, Inc.1 | 7,066,995 | ||||||

| 197,679 | Tenable Holdings, Inc.1 | 7,541,454 | ||||||

| 25,665,604 | ||||||||

Technology Hardware — 2.3% | ||||||||

| 190,509 | Ciena Corporation1 | 9,712,149 | ||||||

Technology Services — 1.9% | ||||||||

| 36,117 | Morningstar, Inc. | 7,822,581 | ||||||

Total Technology | 52,609,830 | |||||||

Shares | Value | |||||||

Utilities — 9.9% | ||||||||

Electric Utilities — 4.7% | ||||||||

| 134,224 | Black Hills Corporation | $ | 9,441,316 | |||||

| 145,873 | NextEra Energy Partners LP3 | 10,224,239 | ||||||

| 19,665,555 | ||||||||

Gas & Water Utilities — 5.2% | ||||||||

| 86,189 | Atmos Energy Corporation | 9,659,201 | ||||||

| 430,362 | Nisource, Inc. | 11,800,526 | ||||||

| 21,459,727 | ||||||||

Total Utilities | 41,125,282 | |||||||

TOTAL COMMON STOCK (Cost $309,961,522) | 400,449,628 | |||||||

SHORT-TERM INVESTMENTS — 3.9% | ||||||||

| 8,059,393 | Blackrock Liquidity Funds T-Fund, Institutional Shares, 4.03%4 | 8,059,393 | ||||||

| 8,059,395 | Federated Hermes Treasury Obligations Fund, Institutional Shares, 4.14%4 | 8,059,395 | ||||||

TOTAL SHORT-TERM INVESTMENTS (Cost $16,118,788) | 16,118,788 | |||||||

TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENTS HELD AS COLLATERAL FOR LOANED SECURITIES — 100.0% (Cost $326,080,310) | 416,568,416 | |||||||

See accompanying notes to financial statements. | CRM Funds | |

26 | ||

CRM FUNDS CRM MID CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Principal | ||||||||

SHORT-TERM INVESTMENTS HELD AS COLLATERAL FOR LOANED SECURITIES — 3.3% | ||||||||

REPURCHASE AGREEMENTS — 3.3% | ||||||||

| 683,504 | With Bank of America Securities, Inc.: at 4.25%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $683,827 (collateralized by US Treasury Securities, par values ranging from $344,655 - $386,857, coupon rates ranging from 0.75% to 4.50%, 11/15/25 – 3/31/26; total market value $697,174) | $ | 683,504 | |||||

| 3,248,983 | With Citigroup Global Markets, Inc.: at 4.25%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $3,250,517 (collateralized by US Treasury Securities, par values ranging from $0 - $693,822, coupon rates ranging from 0.00% to 4.50%, 4/11/23 – 10/31/29 total market value $3,313,963) | 3,248,983 | ||||||

| 3,248,983 | With Deutsche Bank Securities, Inc.: at 4.26%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $3,250,521 (collateralized by US Treasury Securities, par values ranging from $59,307 - $785,110, coupon rates ranging from 0.00% to 0.00%, 1/10/23 – 6/29/23; total market value $3,313,963) | 3,248,983 | ||||||

Principal | Value | |||||||

REPURCHASE AGREEMENTS — (continued) | ||||||||

| 3,248,983 | With JP Morgan Securities LLC: at 4.26%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $3,250,521 (collateralized by US Treasury Securities, par values ranging from $23,456 - $3,306,527, coupon rates ranging from 0.00% to 0.13%, 5/15/23 – 12/28/23; total market value $3,313,963) | $ | 3,248,983 | |||||

| 3,248,983 | With Mizuho Securities USA, LLC.: at 4.25%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $3,250,517 (collateralized by US Treasury Securities, par values ranging from $19,517 - $1,462,033, coupon rates ranging from 0.75% to 2.88%, 1/31/23 – 5/15/28; total market value $3,313,964) | 3,248,983 | ||||||

TOTAL SHORT-TERM INVESTMENTS HELD AS COLLATERAL FOR LOANED SECURITIES (Cost $13,679,436) | 13,679,436 | |||||||

TOTAL INVESTMENTS — 103.3% (Cost $339,759,746) | $ | 430,247,852 | 5 | |||||

LIABILITIES IN EXCESS OF OTHER ASSETS — (3.3)% | (13,555,020 | ) | ||||||

NET ASSETS — 100.0% | $ | 416,692,832 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

27 | ||

CRM FUNDS CRM MID CAP VALUE FUND SCHEDULE OF INVESTMENTS (Concluded) December 31, 2022 (Unaudited) |

A summary of inputs used to value the Fund’s investments as of December 31, 2022 is as follows (see Note 2 in Notes to Financial Statements):

Assets | Level 1 | Level 2 | Level 3 | Investments | ||||||||||||

Common Stock | $ | 400,449,628 | — | — | $ | 400,449,628 | ||||||||||

Short-Term Investments | 16,118,788 | — | — | 16,118,788 | ||||||||||||

Short-Term Investments Held As Collateral For Loaned Securities | — | $ | 13,679,436 | — | 13,679,436 | |||||||||||

Total | $ | 416,568,416 | $ | 13,679,436 | — | $ | 430,247,852 | |||||||||

There were no transfers into or out of Level 3 related to securities held at December 31, 2022.

1 | Non-income producing security. |

2 | PLC – Public Limited Company |

3 | Security partially or fully on loan. |

4 | Rate disclosed is the seven day effective yield as of December 31, 2022. |

5 | At December 31, 2022, the market value of securities on loan for CRM Mid Cap Value Fund was $13,205,972. In the event that the collateral received is insufficient to cover the value of the loaned securities and provided such collateral shortfall is not the result of investment losses, the Fund’s securities lending agent, The Bank of New York Mellon, has agreed to pay the amount of the shortfall to the Fund, or at its discretion, replace the loaned securities. |

See accompanying notes to financial statements. | CRM Funds | |

28 | ||

CRM FUNDS CRM ALL CAP VALUE FUND SCHEDULE OF INVESTMENTS December 31, 2022 (Unaudited) |

Shares | Value | |||||||

COMMON STOCK — 95.7% | ||||||||

Consumer Discretionary — 9.3% | ||||||||

Apparel & Textile Products — 1.7% | ||||||||

| 13,114 | Steven Madden Ltd.1 | $ | 419,123 | |||||

Home Construction — 1.7% | ||||||||

| 7,953 | Skyline Champion Corporation1 | 409,659 | ||||||

Leisure Facilities & Services — 1.3% | ||||||||

| 2,359 | Marriott Vacations Worldwide Corporation1 | 317,498 | ||||||

Retail - Discretionary — 2.6% | ||||||||

| 3,155 | Burlington Stores, Inc.1 | 639,708 | ||||||

Wholesale - Discretionary — 2.0% | ||||||||

| 9,129 | LKQ Corporation | 487,580 | ||||||

Total Consumer Discretionary | 2,273,568 | |||||||

Consumer Staples — 3.0% | ||||||||

Food — 3.0% | ||||||||

| 8,271 | Lamb Weston Holdings, Inc. | 739,097 | ||||||

Energy — 6.5% | ||||||||

Oil & Gas Producers — 2.7% | ||||||||

| 24,593 | Marathon Oil Corporation | 665,733 | ||||||

Oil & Gas Services & Equipment — 3.8% | ||||||||

| 31,619 | ChampionX Corporation | 916,634 | ||||||

Total Energy | 1,582,367 | |||||||

Financials — 17.3% | ||||||||

Asset Management — 2.8% | ||||||||

| 8,183 | Charles Schwab Corporation (The) | 681,317 | ||||||

Banking — 9.6% | ||||||||

| 3,102 | First Republic Bank | 378,103 | ||||||

| 12,601 | Hancock Whitney Corporation | 609,762 | ||||||

| 14,475 | Truist Financial Corporation | 622,859 | ||||||

| 15,518 | Webster Financial Corporation | 734,622 | ||||||

| 2,345,346 | ||||||||

Shares | Value | |||||||

Financials — (continued) | ||||||||

Insurance — 4.9% | ||||||||

| 4,401 | American Financial Group, Inc. | $ | 604,169 | |||||

| 9,120 | American International Group, Inc. | 576,749 | ||||||

| 1,180,918 | ||||||||

Total Financials | 4,207,581 | |||||||

Health Care — 17.2% | ||||||||

Biotechnology & Pharmaceuticals — 3.2% | ||||||||

| 4,463 | Johnson & Johnson | 788,389 | ||||||

Health Care Facilities & Services — 3.5% | ||||||||

| 1,635 | Humana, Inc. | 837,431 | ||||||

Medical Equipment & Devices — 10.5% | ||||||||

| 13,494 | Avantor, Inc.1 | 284,588 | ||||||

| 2,757 | Danaher Corporation | 731,763 | ||||||

| 18,169 | Envista Holdings Corporation1 | 611,750 | ||||||

| 5,233 | LeMaitre Vascular, Inc. | 240,823 | ||||||

| 8,139 | QuidelOrtho Corporation1 | 697,268 | ||||||

| 2,566,192 | ||||||||

Total Health Care | 4,192,012 | |||||||

Industrials — 12.8% | ||||||||

Aerospace & Defense — 2.4% | ||||||||

| 6,159 | Woodward, Inc. | 595,021 | ||||||

Electrical Equipment — 1.0% | ||||||||

| 6,265 | nVent Electric PLC2 | 241,015 | ||||||

Industrial Intermediate Products — 2.5% | ||||||||

| 1,829 | Valmont Industries, Inc. | 604,795 | ||||||

Transportation & Logistics — 6.9% | ||||||||

| 7,450 | Canadian Pacific Railway Ltd.3 | 555,696 | ||||||

| 17,435 | Kirby Corporation1 | 1,121,942 | ||||||

| 1,677,638 | ||||||||

Total Industrials | 3,118,469 | |||||||

��

See accompanying notes to financial statements. | CRM Funds | |

29 | ||

CRM FUNDS CRM ALL CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Shares | Value | |||||||

Materials — 6.2% | ||||||||

Chemicals — 6.2% | ||||||||

| 6,539 | Ashland, Inc. | $ | 703,139 | |||||

| 13,865 | Corteva, Inc. | 814,984 | ||||||

Total Materials | 1,518,123 | |||||||

Real Estate — 2.3% | ||||||||

REIT — 2.3% | ||||||||

| 6,442 | Terreno Realty Corporation | 366,357 | ||||||

| 14,581 | Xenia Hotels & Resorts, Inc. | 192,178 | ||||||

Total Real Estate | 558,535 | |||||||

Technology — 18.6% | ||||||||

Semiconductors — 3.0% | ||||||||

| 5,178 | Microchip Technology, Inc. | 363,755 | ||||||

| 3,464 | QUALCOMM, Inc. | 380,832 | ||||||

| 744,587 | ||||||||

Software — 7.5% | ||||||||

| 98,589 | Clarivate PLC1,2 | 822,231 | ||||||

| 4,277 | PTC, Inc.1 | 513,411 | ||||||

| 12,672 | Tenable Holdings, Inc.1 | 483,437 | ||||||

| 1,819,079 | ||||||||

Technology Hardware — 4.5% | ||||||||

| 13,079 | Ciena Corporation1 | 666,767 | ||||||

| 33,757 | DZS, Inc.1 | 428,039 | ||||||

| 1,094,806 | ||||||||

Technology Services — 3.6% | ||||||||

| 1,237 | MasterCard, Inc., Class A | 430,142 | ||||||

| 57,993 | Paya Holdings, Inc.1 | 456,405 | ||||||

| 886,547 | ||||||||

Total Technology | 4,545,019 | |||||||

Utilities — 2.5% | ||||||||

Electric Utilities — 2.5% | ||||||||

| 7,388 | NextEra Energy, Inc. | 617,637 | ||||||

TOTAL COMMON STOCK (Cost $19,716,185) | 23,352,408 | |||||||

Shares | Value | |||||||

SHORT-TERM INVESTMENTS — 4.4% | ||||||||

| 537,094 | Blackrock Liquidity Funds T-Fund, Institutional Shares, 4.03%4 | $ | 537,094 | |||||

| 537,094 | Federated Hermes Treasury Obligations Fund, Institutional Shares, 4.14%4 | 537,094 | ||||||

TOTAL SHORT-TERM INVESTMENTS (Cost $1,074,188) | 1,074,188 | |||||||

TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT HELD AS COLLATERAL FOR LOANED SECURITIES — 100.1% (Cost $20,790,373) | 24,426,596 | |||||||

See accompanying notes to financial statements. | CRM Funds | |

30 | ||

CRM FUNDS CRM ALL CAP VALUE FUND SCHEDULE OF INVESTMENTS (Continued) December 31, 2022 (Unaudited) |

Principal | Value | |||||||

SHORT-TERM INVESTMENT HELD AS COLLATERAL FOR LOANED SECURITIES — 2.3% | ||||||||

REPURCHASE AGREEMENT — 2.3% | ||||||||

| 573,277 | With JP Morgan Securities LLC: at 4.26%, dated 12/30/22, to be repurchased on 1/3/23, repurchase price $573,548 (collateralized by US Treasury Securities, par values ranging from $4,139 - $583,430, coupon rates ranging from 0.00% to 0.13%, 5/15/23 - 12/28/23; total market value $584,743) | $ | 573,277 | |||||

TOTAL SHORT-TERM INVESTMENT HELD AS COLLATERAL FOR LOANED SECURITIES (Cost $573,277) | 573,277 | |||||||

TOTAL INVESTMENTS — 102.4% (Cost $21,363,650) | $ | 24,999,873 | 5 | |||||

LIABILITIES IN EXCESS OF OTHER ASSETS — (2.4)% | (591,478 | ) | ||||||

NET ASSETS — 100.0% | $ | 24,408,395 | ||||||

See accompanying notes to financial statements. | CRM Funds | |

31 | ||

CRM FUNDS CRM ALL CAP VALUE FUND SCHEDULE OF INVESTMENTS (Concluded) December 31, 2022 (Unaudited) |

A summary of inputs used to value the Fund’s investments as of December 31, 2022 is as follows (see Note 2 in Notes to Financial Statements):

Assets | Level 1 | Level 2 | Level 3 | Investments | ||||||||||||

Common Stock | $ | 23,352,408 | — | — | $ | 23,352,408 | ||||||||||

Short-Term Investments | 1,074,188 | — | — | 1,074,188 | ||||||||||||

Short-Term Investments Held As Collateral For Loaned Securities | — | $ | 573,277 | — | 573,277 | |||||||||||

Total | $ | 24,426,596 | $ | 573,277 | — | $ | 24,999,873 | |||||||||

There were no transfers into or out of Level 3 related to securities held at December 31, 2022.

1 | Non-income producing security. |

2 | PLC - Public Limited Company. |

3 | Security partially or fully on loan. |

4 | Rate disclosed is the seven day effective yield as of December 31, 2022. |