Management's Discussion and Analysis of

Results of Operations and Financial Condition

For the three and nine months ended

September 30, 2024

November 12, 2024

INTRODUCTION

This Management's Discussion and Analysis ("MD&A") dated November 12, 2024 is intended to supplement Hudbay Minerals Inc.'s unaudited condensed consolidated interim financial statements and related notes for the three and nine months ended September 30, 2024 and 2023 (the "consolidated interim financial statements"). The consolidated interim financial statements have been prepared in accordance with International Financial Reporting Standards ("IFRS"), including International Accounting Standard 34, Interim Financial Reporting, as issued by the International Accounting Standards Board ("IASB").

References to "Hudbay", the "Company", "we", "us", "our" or similar terms refer to Hudbay Minerals Inc. and its direct and indirect subsidiaries as at September 30, 2024.

Readers should be aware that:

- This MD&A contains certain "forward-looking statements" and "forward-looking information" (collectively, "forward-looking information") that are subject to risk factors set out in a cautionary note contained in our MD&A.

- This MD&A includes information with respect to Hudbay's acquisition of Copper Mountain, which was completed on June 20, 2023, including the results of the Copper Mountain mine's operations from the date of acquisition, June 20, 2023.

- This MD&A has been prepared in accordance with the requirements of the securities laws in effect in Canada, which may differ materially from the requirements of United States securities laws applicable to US issuers.

- We use a number of non-IFRS financial performance measures in our MD&A, which do not have standardized meaning under IFRS. For further information and detailed reconciliations of such measures, please see the discussion under the "Non-IFRS Financial Performance Measures" section herein.

- The technical and scientific information in this MD&A has been approved by qualified persons based on a variety of assumptions and estimates. Please see the discussion under the "Qualified Person and NI 43-101" section herein.

Readers are also urged to review the "Notes to Reader" section beginning on page 63 of this MD&A.

Additional information regarding Hudbay, including the risks related to our business and those that are reasonably likely to affect our consolidated interim financial statements in the future, is contained in our continuous disclosure materials, including our most recent AIF, consolidated interim financial statements and Management Information Circular available on SEDAR+ at www.sedarplus.ca and on EDGAR at www.sec.gov.

All amounts are in US dollars unless otherwise noted.

OUR BUSINESS

We are a diversified mining company with long-life assets in North and South America. Our Constancia operations in Cusco (Peru) produce copper with gold, silver and molybdenum by-products. Our Snow Lake operations in Manitoba (Canada) produce gold with copper, zinc and silver by-products. Our Copper Mountain operations in British Columbia (Canada) produce copper with gold and silver by-products. We have a copper-focused project development pipeline that includes the Copper World project in Arizona (United States) and the Mason project in Nevada (United States), and our growth strategy is focused on the exploration, development, operation, and optimization of properties we already control, as well as other mineral assets we may acquire that fit our strategic criteria. We are governed by the Canada Business Corporations Act and our shares are listed under the symbol "HBM" on the Toronto Stock Exchange, New York Stock Exchange and Bolsa de Valores de Lima.

OUR PURPOSE

We care about our people, our communities and our planet. Hudbay provides the metals the world needs. We work sustainably, transform lives and create better futures for communities.

We transform lives: We invest in our employees, their families and local communities through long-term employment, local procurement and economic development to improve their quality of life and ensure the communities benefit from our presence.

We operate responsibly: From exploration to closure, we operate safely and responsibly, we welcome innovation and we strive to minimize our environmental footprint while following leading operating practices in all facets of mining.

We provide critical metals: We produce copper and other metals needed for everyday products and essential for applications to support the energy transition toward a more sustainable future.

SUMMARY

Delivered Strong Third Quarter Operating and Financial Results, Led by Record Gold Production from Manitoba Operations; 2024 Production Guidance Reaffirmed and Cost Guidance Further Improved

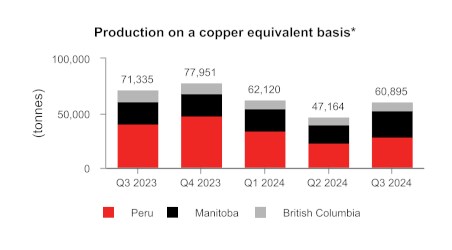

- Achieved consolidated copper production of 31,354 tonnes, in line with quarterly production cadence, and gold production of 89,073 ounces, far exceeding expectations, in the third quarter of 2024, representing an increase of 10% and 52%, respectively, from the second quarter of 2024.

- Enhanced operating platform delivered strong quarterly performance with record gold production at our Manitoba operations, the completion of planned stripping activities at Pampacancha in Peru and the benefits from stabilization and optimization initiatives at the Copper Mountain mine in British Columbia.

- Reaffirmed full year 2024 consolidated production guidance for all metals. Full-year consolidated copper production expected to trend towards the lower end of the guidance range and consolidated gold production expected to trend towards the higher end of the guidance range.

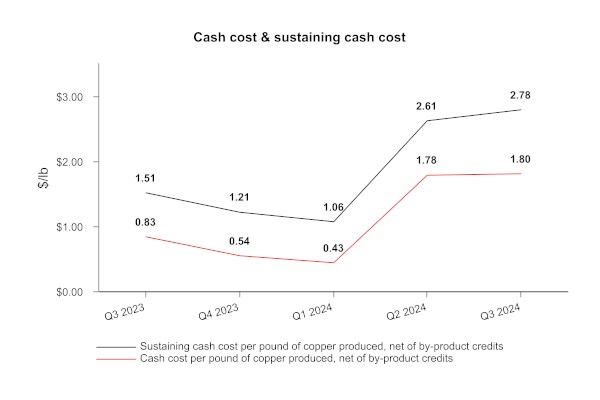

- Strong operating cost performance with consolidated cash cost1 and sustaining cash cost1 per pound of copper produced, net of by-product credits1, in the third quarter of 2024 of $0.18 and $1.71, respectively, an improvement of 84% and 35%, respectively, from the second quarter of 2024.

- Further improved 2024 annual operating cost guidance with decreased consolidated cash cost1 guidance range of $0.65 to $0.85 per pound, an additional improvement from the previously updated guidance range of $0.90 to $1.10 per pound, and decreased consolidated sustaining cash cost guidance range of $1.75 to $2.20 per pound from original guidance of $2.00 to $2.45 per pound, as a result of increased exposure to gold by-product credits and continued strong cost control across all operations.

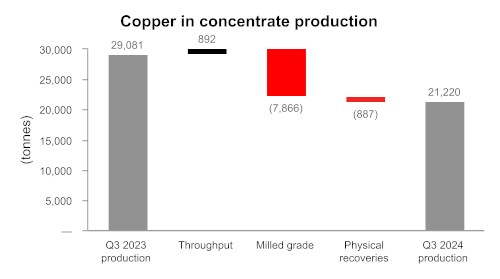

- Peru operations continued to benefit from strong mill throughput, achieving a quarterly average of approximately 88,000 tonnes per day in the third quarter. The Pampacancha stripping program to advance to higher grades was completed in late September and is on track to achieve higher copper and gold grade ore in the fourth quarter. Peru operations produced 21,220 tonnes of copper and 20,331 ounces of gold in the third quarter of 2024, in line with quarterly cadence expectations. Peru cash cost per pound of copper produced, net of by-product credits1, $1.80 in the third quarter and is expected to improve in the fourth quarter of 2024 with continued strong cost control and higher copper and gold production.

- Manitoba operations produced 62,468 ounces of gold in the third quarter of 2024, far exceeding management's quarterly cadence expectations and achieving record quarterly production levels as New Britannia continues to operate well above nameplate and budgeted throughput levels and the Lalor mine continues to achieve better-than-expected gold grades. Manitoba cash cost per ounce of gold produced, net of by-product credits1, was $372 during the third quarter of 2024, a decrease of 52% compared to the second quarter of 2024. Full year Manitoba gold production is expected to exceed the top end of the 2024 guidance range.

- British Columbia operations produced 6,736 tonnes of copper at a cash cost per pound of copper produced, net of by-product credits1, of $1.81 in the third quarter of 2024. Achieved record quarterly copper recoveries of 84% and strong unit cost performance as a result of the successful operational stabilization efforts as mine stripping activities accelerate and mill optimization initiatives are underway. Full-year British Columbia copper production is expected to be slightly below the lower end of the 2024 guidance range.

- Achieved revenue of $485.8 million and operating cash flow before change in non-cash working capital of $186.3 million in the third quarter of 2024. Strong financial results were driven by higher realized gold prices as well as robust gold production in Manitoba, while delivering on higher recovery, throughput and cost control initiatives across all business units.

- Third quarter net earnings attributable to owners and earnings per share attributable to owners were $49.8 million and $0.13, respectively. After adjusting for items on a pre-tax basis such as a non-cash gain of $2.0 million related to a quarterly revaluation of our closed site environmental reclamation provision, a $5.2 million mark-to-market revaluation loss on various instruments such as the gold prepayment liability, unrealized strategic gold and copper hedges, investments and share-based compensation and a $2.2 million write-down of PP&E, among other items, third quarter adjusted earnings1 per share attributable to owners was $0.13.

- Adjusted EBITDA1 was $206.2 million during the third quarter of 2024, a 42% increase compared to the second quarter of 2024.

- Cash and cash equivalents and short-term investments increased by $233.5 million to $483.3 million during the first nine months of 2024 due to a successful equity offering and strong operating cash flows bolstered by higher copper and gold prices, which enabled a $412.1 million reduction in net debt1 during the first nine months of 2024.

Accelerated Deleveraging and Improved Balance Sheet Flexibility

- Hudbay's unique copper and gold diversification in Peru and North America provides exposure to higher copper and gold prices and attractive free cash flow generation.

- While a majority of revenues continue to be from copper, gold is representing an increasing portion of total revenues at 36% in the third quarter of 2024 and 33% year-to-date, compared to 27% and 26%, respectively, for the same periods in 2023, driven by higher gold production and strong leverage to higher gold prices.

- During the third quarter of 2024, deleveraging efforts continued with additional open market purchases of approximately $48.5 million of our senior unsecured notes in July and August 2024 at a discount. Long-term debt reduced to $1,108.9 million at September 30, 2024 from $1,287.5 million at December 31, 2023.

- On August 30, 2024, Hudbay completed the final monthly payment to settle the gold prepayment liability that was used to fund the refurbishment of the New Britannia gold mill. The elimination of the gold prepayment liability will further increase the Company's exposure to higher gold production in Snow Lake.

- Impressive operating cash flow before change in non-cash working capital generation of $186.3 million despite lower realized copper prices compared to the second quarter of 2024, capitalizing on higher gold production from Manitoba following the full repayment of our gold prepayment liability in August.

- Achieved trailing 12 month adjusted EBITDA1 of $839.8 million, a substantial increase from $498.5 million for the 12 months ending September 30, 2023.

- Reduced net debt1 to $625.6 million in the third quarter of 2024. The third quarter represents the fifth consecutive quarter of lower net debt as a result of deleveraging efforts and capitalizing on strong operating cash flow generation.

- The increase in cash and reduction in long-term debt significantly reduced our net debt to adjusted EBITDA ratio1 to 0.7x at September 30, 2024 compared to 1.6x at the end of 2023, well within the targeted 1.2x net debt to adjusted EBITDA ratio outlined in our three prerequisites plan (the "3-P plan") for advancing Copper World, including receipts of permits, a robust definitive feasibility study plan and a prudent financing strategy.

- Total liquidity substantially increased by 58% to $907.7 million at September 30, 2024 from $573.7 million at the end of 2023.

- Subsequent to the quarter end, further improved long-term balance sheet resilience with a proactive three-year extension of our senior secured revolving credit facilities from October 2025 to November 2028. The extended credit facilities provide increased financial flexibility to accretively maintain our 4.50% coupon 2026 senior unsecured notes outstanding to maturity and advance Copper World towards a sanctioning decision in accordance with the 3-P plan. The $450 million revolving credit facility includes an improved pricing grid reflecting the enhanced financial position of Hudbay and features an opportunity to increase the facility by an additional $150 million at our discretion during the four-year tenor, providing additional financial flexibility.

Advancing Growth Initiatives to Further Enhance Copper and Gold Exposure

- The successful completion of the planned stripping program at Pampacancha in September is expected to lead to significantly higher copper and gold grades in the fourth quarter of 2024, which together with maintaining strong operating performance at Constancia is expected to continue to generate meaningful free cash flow in Peru.

- The New Britannia mill continued to exceed expectations, driving continued strong gold production and free cash flow generation in Manitoba. The New Britannia mill achieved record throughput levels of approximately 2,080 tonnes per day in the third quarter, exceeding its original design capacity of 1,500 tonnes per day and its 2024 budgeted capacity of 1,800 tonnes per day due to the successful implementation of process improvement initiatives and effective preventative maintenance measures.

- We have successfully implemented post-acquisition plans to stabilize the Copper Mountain operations through mining fleet ramp-up activities and increased mill reliability and performance. Achieved record mill availability of 95% and record copper recoveries of 84% in the third quarter of 2024. Efforts are now focused on optimizing the operations through execution of the planned accelerated stripping program and mill throughput improvement projects.

- Received the Aquifer Protection Permit for Copper World in August, a key milestone and de-risking event in the advancement of the project. Continued to progress the 3-P plan for sanctioning Copper World, with transformed balance sheet near targeted levels and the remaining key state permit progressing on track. As disclosed in August, we commenced activities related to the preparation of feasibility studies for Copper World, resulting in an expected increase of $25 million in growth capital spending in Arizona.

- Drill permitting for highly prospective Maria Reyna and Caballito properties near Constancia continues to advance through the multi-step regulatory process with the environmental impact assessment applications approved for Maria Reyna in June and Caballito in September.

- The development of an access drift to the 1901 deposit in Snow Lake remains on track to reach mineralization in early 2025 and is intended to enable confirmation of the optimal mining method for the deposit and underground drilling to further evaluate the orebody and upgrade inferred gold resources to reserves. Initiated the development of an adjacent haulage drift to de-risk planned full production in 2027.

- Large 2024 exploration program continues in Snow Lake with eight drill rigs testing targets near Lalor and regional satellite properties. Includes follow-up drilling at Lalor Northwest located 400 metres from Lalor's underground infrastructure and the testing of a deep geophysical target at the Cook Lake North property.

- Continuing to advance Flin Flon tailings reprocessing opportunities through metallurgical test work and early economic evaluation to assess the possibility of producing critical minerals and precious metals while reducing the environmental footprint.

Summary of Third Quarter Results

Cash generated from operating activities of $146.2 million increased in the third quarter of 2024 compared to the second quarter of 2024, and was lower by $5.8 million compared to the same period in 2023. The decrease compared to the same period in 2023 is reflective of the timing of sales which occurred late in the current quarter, where payment was subsequently made by customers in October. Operating cash flow before change in non-cash working capital was $186.3 million during the third quarter of 2024, reflecting an increase of $4.3 million compared to the third quarter of 2023. The increase was primarily the result of higher gold production and sales volumes in Manitoba, strong operational cost performance across the business and higher realized metal prices. This was partially offset by lower copper sales volumes in Peru due to mining of the high-grade zones of the Pampacancha deposit in the third quarter of 2023 as well as a significant increase in cash taxes paid of $17.3 million at our Peru operations, compared to the same period in 2023.

Consolidated copper, gold, silver and zinc production in the third quarter of 2024 decreased by 25%, 12%, 7% and 22%, respectively, compared to the same period in 2023 primarily due to lower production and lower recoveries in Peru partially offset by higher gold production in Manitoba and British Columbia. With the completion of the planned stripping program in Peru at the end of the third quarter, October production results have already delivered higher grades as mining of the higher grade zones at Pampacancha is underway, in line with the mine plan.

Net earnings attributable to owners in the third quarter of 2024 was $49.8 million, or $0.13 per share, compared to $45.5 million, or $0.13 per share, in the third quarter of 2023. The third quarter of 2024 was impacted by various non-cash charges for unrealized losses on strategic copper and gold hedges and revaluation of share-based compensation due to a higher share price.

Adjusted net earnings attributable to owners1 and adjusted net earnings per share attributable to owners1 in the third quarter of 2024 were $50.3 million and $0.13 per share, respectively, after adjusting for items on a pre-tax basis such as a non-cash gain of $2.0 million related to a quarterly revaluation of our closed site environmental reclamation provision, a $5.2 million mark-to-market revaluation loss on various instruments such as the gold prepayment liability, unrealized strategic gold and copper hedges, investments and stock based compensation and a $2.2 million write-down of PP&E, among other items. This compares to adjusted net earnings attributable to owners1 and net earnings per share attributable to owners1 of $24.2 million and $0.07 per share in the same period of 2023.

Third quarter adjusted EBITDA1 was $206.2 million, an 8.1% increase compared to $190.7 million in the same period in 2023. The increase is the result of higher realized metal prices and successful operating cost control across the business despite lower sales volumes.

In the third quarter of 2024, consolidated cash cost per pound of copper produced, net of by-product credits1, was $0.18, compared to $1.10 in the same period in 2023. This decrease was mainly the result of significantly higher by-product credits and strong cost control leading to lower mining, milling, treatment and refining costs, partially offset by higher G&A costs from incorporating Copper Mountain and lower copper production. Consolidated sustaining cash cost per pound of copper produced, net of by-product credits1, was $1.71 in the third quarter of 2024 compared to $1.89 in the same period in 2023. This decrease was primarily due to the same reasons outlined above partially offset by higher cash sustaining capital expenditures.

Consolidated all-in sustaining cash cost per pound of copper produced, net of by-product credits1, was $1.95 in the third quarter of 2024, lower than $2.04 in the same period in 2023 due to significant gold by-product credits and continued strong cost control across all operations.

As at September 30, 2024, total liquidity was $907.7 million, including $443.3 million in cash and cash equivalents, $40.0 million in short-term investments as well as undrawn availability of $424.4 million under our revolving credit facilities. Net debt1 declined to $625.6 million at the end of the third quarter of 2024 compared to $1,037.7 million at the end of 2023. We expect that our current liquidity together with cash flows from operations will be sufficient to meet our liquidity needs for the next year.

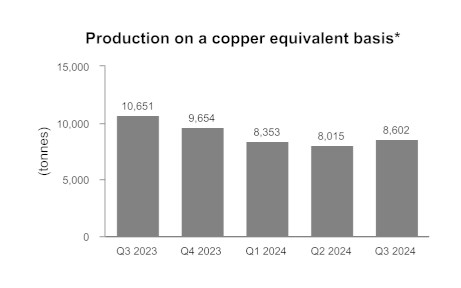

*Copper equivalent production is calculated using the quarter average LME prices for each metal.

1 Adjusted net earnings (loss) - attributable to owners and adjusted net earnings (loss) per share - attributable to owners, adjusted EBITDA, cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, cash cost, sustaining cash cost per ounce of gold produced, net of by-product credits, combined unit cost, net debt and net debt to adjusted EBITDA ratio are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

KEY FINANCIAL RESULTS

| Financial Condition | | | | | | |

| (in $ thousands, except net debt to adjusted EBITDA ratio) | | Sep. 30, 2024 | | | Dec. 31, 2023 | |

| Cash and cash equivalents and short-term investments | $ | 483,273 | | $ | 249,794 | |

| Total long-term debt | | 1,108,900 | | | 1,287,536 | |

| Net debt1 | | 625,627 | | | 1,037,742 | |

| Working capital2 | | 434,346 | | | 135,913 | |

| Total assets | | 5,508,075 | | | 5,312,634 | |

| Equity attributable to owners of the Company | | 2,537,845 | | | 2,096,811 | |

| Net debt to adjusted EBITDA 1 | | 0.7 | | | 1.6 | |

1 Net debt and net debt to adjusted trailing 12 month EBITDA are a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

2 Working capital is determined as total current assets less total current liabilities as defined under IFRS and disclosed on the consolidated interim financial statements.

| Financial Performance | | Three months ended | | | Nine months ended | |

| (in $ thousands, except per share amounts or as noted below) | | Sep. 30, 2024 | | | Sep. 30, 2023 | | | Sep. 30, 2024 | | | Sep. 30, 2023 | |

| Revenue | $ | 485,773 | | $ | 480,456 | | $ | 1,436,282 | | $ | 1,087,841 | |

| Cost of sales | | 345,987 | | | 374,057 | | | 1,066,915 | | | 892,036 | |

| Earnings before tax | | 79,701 | | | 84,149 | | | 147,892 | | | 70,848 | |

| Net earnings for the period | | 50,354 | | | 45,490 | | | 48,512 | | | 36,015 | |

| Net earnings attributable to owners | | 49,762 | | | 45,125 | | | 55,537 | | | 35,650 | |

| Basic and diluted earnings per share - attributable | | 0.13 | | | 0.13 | | | 0.15 | | | 0.12 | |

| Adjusted earnings per share - attributable1 | | 0.13 | | | 0.07 | | | 0.30 | | | 0.02 | |

| Operating cash flow before change in non-cash working capital2 | | 186.3 | | | 182.0 | | | 455.9 | | | 323.5 | |

| Adjusted EBITDA1,2 | | 206.2 | | | 190.7 | | | 565.2 | | | 373.4 | |

1 Adjusted earnings (loss) per share - attributable to owners and adjusted EBITDA are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

2 In $ millions.

KEY PRODUCTION RESULTS

| | Three months ended | Three months ended |

| Sep. 30, 2024 | Sep. 30, 2023 |

| Peru | Manitoba | British

Columbia3 | Total | Peru | Manitoba | British

Columbia3 | Total |

| Contained metal in concentrate and doré produced1 | | | | | |

| Copper | tonnes | 21,220 | 3,398 | 6,736 | 31,354 | 29,081 | 3,580 | 9,303 | 41,964 |

| Gold | oz | 20,331 | 62,468 | 6,274 | 89,073 | 40,596 | 56,213 | 4,608 | 101,417 |

| Silver | oz | 648,209 | 281,397 | 55,963 | 985,569 | 697,211 | 264,752 | 101,069 | 1,063,032 |

| Zinc | tonnes | - | 8,069 | - | 8,069 | - | 10,291 | - | 10,291 |

| Molybdenum | tonnes | 362 | - | - | 362 | 466 | - | - | 466 |

| | | | | | | | | | |

| Payable metal sold | | | | | | | | |

| Copper | tonnes | 18,803 | 2,931 | 6,026 | 27,760 | 27,490 | 2,925 | 8,956 | 39,371 |

| Gold2 | oz | 9,795 | 57,238 | 6,199 | 73,232 | 32,757 | 36,713 | 5,329 | 74,799 |

| Silver2 | oz | 365,198 | 244,974 | 53,241 | 663,413 | 460,001 | 197,952 | 91,002 | 748,955 |

| Zinc | tonnes | - | 8,607 | - | 8,607 | - | 7,125 | - | 7,125 |

| Molybdenum | tonnes | 343 | - | - | 343 | 426 | - | - | 426 |

| | Nine months ended | Nine months ended |

| Sep. 30, 2024 | Sep. 30, 2023 |

| Peru | Manitoba | British

Columbia3 | Total | Peru | Manitoba | British

Columbia 3 | Total |

| Contained metal in concentrate and doré produced1 | | | | | |

| Copper | tonnes | 65,013 | 9,189 | 20,479 | 94,681 | 67,280 | 8,419 | 10,542 | 86,241 |

| Gold | oz | 60,147 | 162,787 | 15,145 | 238,079 | 64,800 | 127,500 | 5,353 | 197,653 |

| Silver | oz | 1,738,760 | 711,867 | 221,566 | 2,672,193 | 1,669,021 | 596,144 | 112,987 | 2,378,152 |

| Zinc | tonnes | - | 24,954 | - | 24,954 | - | 28,895 | - | 28,895 |

| Molybdenum | tonnes | 1,128 | - | - | 1,128 | 1,169 | - | - | 1,169 |

| Payable metal sold | | | | | | | | |

| Copper | tonnes | 59,363 | 8,281 | 19,523 | 87,167 | 65,013 | 7,021 | 8,956 | 80,990 |

| Gold2 | oz | 65,905 | 162,004 | 14,699 | 242,608 | 59,062 | 107,662 | 5,329 | 172,053 |

| Silver2 | oz | 1,519,207 | 674,301 | 205,789 | 2,399,297 | 1,523,740 | 481,547 | 91,002 | 2,096,289 |

| Zinc | tonnes | - | 19,859 | - | 19,859 | - | 21,394 | - | 21,394 |

| Molybdenum | tonnes | 1,105 | - | - | 1,105 | 994 | - | - | 994 |

1 Metal reported in concentrate is prior to deductions associated with smelter contract terms.

2 Includes total payable gold and silver in concentrate and in doré sold.

3 Includes 100% of Copper Mountain mine production. Hudbay owns 75% of Copper Mountain mine. As Copper Mountain was acquired on June 20, 2023, the production for the nine months ended September 30, 2023 represents the period from acquisition date, June 20, 2023, through to the end of the third quarter of 2023.

KEY COST RESULTS

| | | Three months ended | | Nine months ended | Guidance |

| | | Sep. 30,

2024 | Sep. 30,

2023 | | Sep. 30,

2024 | Sep. 30,

2023 | Annual

20242 |

| Peru cash cost per pound of copper produced | | | | |

| Cash cost1 | $/lb | 1.80 | 0.83 | | 1.28 | 1.34 | 1.25 - 1.60 |

| Sustaining cash cost1 | $/lb | 2.78 | 1.51 | | 2.08 | 2.10 | |

| Manitoba cash cost per ounce of gold produced | | | | |

| Cash cost1 | $/oz | 372 | 670 | | 606 | 864 | 700 - 900 |

| Sustaining cash cost1 | $/oz | 553 | 939 | | 855 | 1,212 | |

| British Columbia cash cost per pound of copper produced3 | | | | |

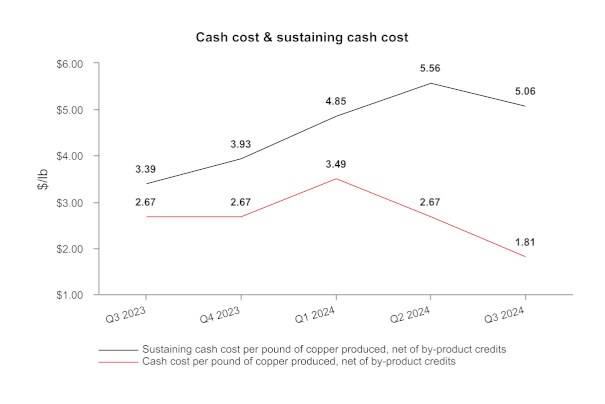

| Cash cost1 | $/lb | 1.81 | 2.67 | | 2.67 | 2.36 | 2.00 - 2.50 |

| Sustaining cash cost1 | $/lb | 5.06 | 3.39 | | 5.15 | 2.99 | |

| Consolidated cash cost per pound of copper produced | | | | |

| Cash cost1 | $/lb | 0.18 | 1.10 | | 0.46 | 1.14 | 0.65 - 0.85 |

| Sustaining cash cost1 | $/lb | 1.71 | 1.89 | | 1.74 | 2.04 | 1.75 - 2.20 |

| All-in sustaining cash cost1 | $/lb | 1.95 | 2.04 | | 2.06 | 2.24 | |

1 Cash cost, sustaining cash cost, all-in sustaining cash cost per pound of copper produced, net of by-product credits, gold cash cost, sustaining cash cost per ounce of gold produced, net of by-product credits, and unit operating cost are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

2 We have improved our 2024 annual consolidated cash cost guidance range to $0.65 to $0.85 per pound from the original guidance range of $1.05 to $1.25 per pound. We have also improved our 2024 annual consolidated sustaining cash cost guidance range to $1.75 to $2.20 per pound from the original guidance range of $2.00 to $2.45 per pound.

3As Copper Mountain was acquired on June 20, 2023, the results for the nine months ended September 30, 2023 represents the period from the acquisition date, June 20, 2023, through to the end of the third quarter of 2023.

RECENT DEVELOPMENTS

2024 Production Guidance Reaffirmed and Cash Cost Guidance Further Improved

We reaffirm our full year 2024 consolidated production guidance for all metals as we continue to deliver strong operating performance and we expect the fourth quarter to be the highest copper production quarter in 2024, in line with our quarterly cadence expectations. We expect 2024 consolidated copper production to trend towards the lower end of the guidance range and 2024 consolidated gold production to trend towards the higher end of the guidance range.

In Peru, the fourth quarter is expected to be the strongest quarter this year, and full year copper production is expected to trend towards the lower end of the guidance range, while gold production is expected to trend towards the higher end of the guidance range. In British Columbia, we expect to continue improving operating efficiencies in the fourth quarter, and full year copper production is expected to be slightly below the lower end of the guidance range, while full year gold production is expected to be within the guidance ranges.

In Manitoba, we expect the strong operating performance to continue into the fourth quarter, and full year gold production is now expected to exceed the top end of the guidance range and full year copper production is expected to trend towards the higher end of the guidance range.

We are again improving our full-year 2024 consolidated cash cost guidance range to $0.65 to $0.85 per pound copper from the previously announced range of $0.90 to $1.10 per pound and the original guidance range of $1.05 to $1.25 per pound. We are also improving our 2024 annual consolidated sustaining cash cost guidance range to $1.75 to $2.20 per pound copper from the original guidance range of $2.00 to $2.45 per pound. This is a result of increased exposure to gold by-product credits and continued strong cost control at all operations. We have reaffirmed all other 2024 guidance metrics.

Continued Debt Reduction and Improved Balance Sheet Flexibility

We took several prudent measures in the third quarter of 2024 to further improve our balance sheet strength and flexibility:

• Repurchased and retired an additional $48.5 million of senior unsecured notes - We made open market purchases of $13.4 million of the 2026 senior unsecured notes and $35.1 million of the 2029 senior unsecured notes during the quarter. As a result, a total of $82.6 million of senior unsecured notes have been repurchased and retired since the beginning of the year.

• Delivered the final $16.9 million under gold forward sale and prepay agreement - We completed the last monthly gold delivery in August 2024, resulting in the full repayment of the gold prepay facility which was used to fund the refurbishment of the New Britannia gold mill.

• Three-year extension of revolving credit facilities to 2028 - Subsequent to the quarter end, we proactively extended our senior secured revolving credit facilities by three years from October 2025 to November 2028 and negotiated the flexibility to leave our 4.50% 2026 senior unsecured notes outstanding to maturity as we advance Copper World towards a sanctioning decision in accordance with the 3-P plan. The newly extended $450 million revolving credit facility, with the existing banking syndicate, includes an improved pricing grid reflecting the enhanced financial position of Hudbay, and features an opportunity to increase the facility by an additional $150 million at our discretion during the four-year tenor, providing additional financial flexibility. The revolving credit facilities are currently undrawn (excluding letters of credit), having repaid $100 million of prior drawings associated with the Copper Mountain acquisition in the first half of 2024.

We have delivered five consecutive quarters of meaningful free cash flow generation as a result of recent brownfield investments in our operations, continuous improvement efforts and steady cost control across the business. During the last twelve months, we have repaid a total of $296 million of debt and gold prepayment liabilities.

As a result of continued deleveraging efforts and cash flow generation, we have substantially reduced net debt1 to $625.6 million at September 30, 2024, from $1,037.7 million at the end of 2023. The net debt reduction, together with higher levels of adjusted EBITDA1 over the last twelve months, has significantly improved our net debt to adjusted EBITDA ratio1 to 0.7x compared to 1.6x at the end of 2023. The improved balance sheet flexibility and accelerated debt reduction significantly advances the Company's progress as part of its 3-P plan for sanctioning Copper World, and results in the successful achievement of the targeted 1.2x net debt to 12 month trailing adjusted EBITDA1 ratio well ahead of schedule.

Advancing Permitting at Copper World

In August 2024, Hudbay received the Aquifer Protection Permit for the Copper World project from the Arizona Department of Environmental Quality ("ADEQ"). The Company proactively engaged with the ADEQ, ensuring a transparent and thorough permitting process by providing comprehensive and detailed information. The issuance of this permit is a key milestone in the advancement of Copper World, which is a standalone operation requiring state and local permits and is expected to produce 85,000 tonnes of copper per year over a 20-year mine life.

There are three key state permits required for Copper World sanctioning:

• Mined Land Reclamation Plan - Completed - the Mined Land Reclamation Plan was initially approved by the Arizona State Mine Inspector in October 2021 and was subsequently amended and approved to reflect a larger private land project footprint. This approval was challenged in state court, but the challenge was dismissed in May 2023.

• Aquifer Protection Permit - Completed - the Aquifer Protection Permit was received on August 29, 2024 from the ADEQ following a robust process that included detailed analysis by the agency and Hudbay, along with a public comment period that was completed in the second quarter of 2024.

• Air Quality Permit - On Track - the Air Quality Permit application was submitted to the ADEQ in late 2022 and follows a similar robust process, including a public comment period that concluded in September 2024.

With the receipt of the Aquifer Protection Permit on August 29, 2024, we announced that we commenced activities related to the preparation of feasibility studies for Copper World, resulting in an expected $25 million increase in growth capital spending in Arizona, compared to the original annual guidance of $20 million.

We intend to commence a minority joint venture partner process after receiving the Air Quality Permit. The potential joint venture partner is anticipated to participate in the funding of definitive feasibility study activities in 2025 as well as in the final project design and construction for Copper World.

The opportunity to sanction Copper World is not expected until 2026 based on current estimated timelines. Once in production, Copper World is expected to be a meaningful copper producer in the U.S. domestic copper supply chain, which will be required to help secure growing U.S. metal demand related to increased manufacturing capacity, infrastructure development, increased energy independence and domestic battery supply chain and production needs. The "Made-in-America" copper cathode anticipated to be produced at Copper World is expected to be sold entirely to domestic U.S. customers and would make Copper World the third largest cathode producer in the U.S. Hudbay is pleased with the level of local support received at the public comment meetings and looks forward to providing significant social and environmental benefits for the community and local economy in Arizona. Over the proposed initial 20-year mine life, the company expects to contribute more than $850 million in U.S. taxes, including approximately $170 million in taxes to the state of Arizona. Hudbay also expects Copper World to create more than 400 direct jobs and up to 3,000 indirect jobs in Arizona.

_________________________________________

1 Adjusted EBITDA and net debt to adjusted EBITDA ratio are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

Copper Mountain Stabilization Complete and Optimization Initiatives Underway

Stabilization Phase Completed

Since acquiring Copper Mountain in June 2023, our stabilization efforts have been focused on ramping up the mining fleet to execute a planned accelerated stripping campaign to gain access to higher grades, as well as plant improvement initiatives to improve mill reliability and recoveries.

• Mine Ramp-up Activities Completed - Successfully remobilized all 28 haul trucks and added five additional haul trucks this year to execute the planned three-year accelerated stripping campaign at a lower cost and avoid contractor mining costs.

• Mill Stabilization Activities Completed - Implemented several mill initiatives, including reprogramming the mill expert system, installing advanced grinding control instrumentation, flotation operational strategy improvements and improved maintenance practices. This has resulted in record mill availability of 95% and record copper recovery of 84% being achieved in the third quarter of 2024.

• Operating Costs Stabilized - Achieved sequential quarterly improvements in unit operating costs and cash costs this year with the third quarter of 2024 being the lowest cost quarter at Copper Mountain since Hudbay's acquisition in June 2023.

• Corporate Synergies Target Achieved - Exceeded the targeted $10 million in annualized corporate synergies.

Optimization Phase Underway

Efforts are now focused on several optimization initiatives at Copper Mountain to access higher grades, further improve mill throughput and increase copper production and operating cash flows.

• Accelerated Stripping - Commenced a three-year accelerated stripping program to mitigate the substantially reduced stripping that occurred over the four years prior to Hudbay's acquisition. The stripping program is intended to unlock access to higher grade ore and further benefit operating costs.

• Mill Throughput Optimization - Advancing various engineering studies to increase mill throughput to its permitted levels of 50,000 tonnes per day earlier than was originally contemplated in the technical report, including the potential conversion of the third ball mill to a SAG mill to alleviate capacity limitations.

• On Track to Achieve Three-Year Operating Efficiencies Target - Stabilization initiatives have resulted in improved operating efficiencies, as demonstrated by improved mill throughput, record copper recoveries and lower unit operating costs since Hudbay's acquisition. On track to realize our three-year annual operating efficiencies target of $20 million.

New Britannia Mill Performance Exceeding Expectations and Driving Higher Gold Production

The New Britannia mill has been consistently exceeding performance expectations, achieving throughput levels of 1,650 tonnes per day in 2023, more than 1,850 tonnes per day in the first half of 2024, and reaching a quarterly record of 2,080 tonnes per day in the third quarter of 2024. We completed the brownfield investment in New Britannia in 2021 and refurbished the mill with a nominal capacity of 1,500 tonnes per day to provide additional processing capacity at our Snow Lake operations and allow us to achieve higher gold recoveries of approximately 90% as Lalor transitioned to the higher gold and copper areas of the mine plan. The Snow Lake operations achieved record quarterly gold production in the third quarter of 2024, and we now expect gold production in Manitoba to exceed the top end of the 2024 gold production guidance range of 200,000 ounces.

In August 2024, we completed the final payment under the New Britannia gold prepay facility, which further enhances our exposure to higher gold production in Snow Lake. With approximately two million ounces of contained gold in current mineral reserve estimates and another 1.4 million ounces of contained gold in inferred mineral resources, the New Britannia investment has unlocked significant value in Snow Lake. This could be further enhanced by regional exploration upside and the current strong gold price environment.

In the first quarter of 2024, we received a permit approval to increase the production rate at New Britannia to 2,500 tonnes per day, which will provide the opportunity to process more Lalor ore at the New Britannia mill and create additional processing capacity at Stall for potential new regional discoveries in Snow Lake.

Exploration Update

Large Exploration Drill Program Continues in Snow Lake

Hudbay continues to execute its 2024 exploration program with the goal of extending known mineralization near the Lalor deposit to further extend mine life as well as to find a new anchor deposit within trucking distance of the Snow Lake processing infrastructure. The 2024 program included the largest geophysical program in Hudbay's history in Snow Lake, with surface electromagnetic surveys detecting targets at more than 1,000 metres below surface and covering a 25 square-kilometre area including the Cook Lake claims that had been previously untested by modern deep geophysics.

We had eight drill rigs turning in Snow Lake during the third quarter, including two drills completing follow-up drilling at Lalor Northwest, located within 400 metres of the existing Lalor underground infrastructure. Six drill rigs were testing new geophysical targets and completing follow-up drilling at potential regional satellite deposits at the Cook Lake, Reed, Rail and Bur properties. One of the geophysical targets is a very strong deep anomaly located at Cook Lake North, approximately six kilometres from Lalor. Drilling activities are expected to continue throughout the winter season and assay results are pending.

We continue to advance the development of the exploration drift from the existing Lalor ramp towards the 1901 deposit, and the drift is expected to reach mineralization in early 2025. We plan to conduct definition drilling in 2025 to confirm the optimal mining method, evaluate the orebody geometry and continuity, and convert inferred mineral resources in the gold lenses to mineral reserves. In October, we initiated the development of an adjacent haulage drift to further de-risk future full production from the 1901 deposit in 2027.

Advancing Engineering Work for Flin Flon Tailings Reprocessing

Zinc Plant Tailings - Metallurgical test work continues following positive results from the initial confirmatory drill program completed earlier this year in the section of the tailings facility that was utilized by the zinc plant for 25 years. The results confirmed the grades of precious metals and critical minerals previously estimated from historical zinc plant records. An early economic study to evaluate the opportunity to reprocess the zinc plant tailings has confirmed the potential for a technically viable reprocessing alternative, and further engineering work is underway.

Mill Tailings - We continue to advance metallurgical test work on the opportunity to reprocess Flin Flon mill tailings where 100 million tonnes of tailings were deposited over 90 years. An early economic study on the mill tailings is planned.

Maria Reyna and Caballito Drill Permits Expected in 2025

Hudbay controls a large, contiguous block of mineral rights with the potential to host mineral deposits in close proximity to the Constancia processing facility, including the past producing Caballito property and the highly prospective Maria Reyna property. The company commenced early exploration activities at Maria Reyna and Caballito after completing a surface rights exploration agreement with the community of Uchucarcco in August 2022. As part of the drill permitting process, environmental impact assessment applications were submitted for the Maria Reyna property in November 2023 and for the Caballito property in April 2024. The environmental impact assessment (EIA) for Maria Reyna was approved by the government in June 2024 and the Caballito EIA was approved in September 2024. This represents one of several steps in the drill permitting process, which is expected to be completed in 2025.

PERU OPERATIONS REVIEW

| | Three months ended | Nine months ended |

Sep. 30,

2024 | Sep. 30,

2023 | Sep. 30,

2024 | Sep. 30,

2023 |

| Constancia ore mined1 | tonnes | 3,022,931 | 1,242,198 | 10,860,132 | 8,292,778 |

| Copper | % | 0.36 | 0.30 | 0.31 | 0.32 |

| Gold | g/tonne | 0.04 | 0.04 | 0.03 | 0.04 |

| Silver | g/tonne | 3.20 | 2.91 | 2.76 | 2.56 |

| Molybdenum | % | 0.02 | 0.01 | 0.01 | 0.01 |

| Pampacancha ore mined1 | tonnes | 1,777,092 | 5,894,013 | 5,280,235 | 9,199,803 |

| Copper | % | 0.48 | 0.53 | 0.50 | 0.48 |

| Gold | g/tonne | 0.27 | 0.30 | 0.28 | 0.33 |

| Silver | g/tonne | 6.23 | 4.22 | 4.98 | 3.94 |

| Molybdenum | % | 0.01 | 0.02 | 0.01 | 0.02 |

| Total ore mined | tonnes | 4,800,023 | 7,136,211 | 16,140,367 | 17,492,581 |

| Strip ratio2 | | 2.62 | 1.36 | 2.07 | 1.61 |

| Ore milled | tonnes | 8,137,248 | 7,895,109 | 23,934,171 | 22,781,885 |

| Copper | % | 0.32 | 0.43 | 0.32 | 0.36 |

| Gold | g/tonne | 0.11 | 0.21 | 0.11 | 0.13 |

| Silver | g/tonne | 3.70 | 3.75 | 3.35 | 3.42 |

| Molybdenum | % | 0.01 | 0.02 | 0.01 | 0.01 |

| Copper concentrate | tonnes | 100,462 | 132,828 | 304,190 | 311,072 |

| Concentrate grade | % Cu | 21.12 | 21.89 | 21.37 | 21.63 |

| Copper recovery | % | 82.6 | 85.2 | 83.6 | 82.7 |

| Gold recovery | % | 68.1 | 74.8 | 69.2 | 68.0 |

| Silver recovery | % | 67.0 | 73.2 | 67.4 | 66.6 |

| Molybdenum recovery | % | 39.0 | 37.2 | 42.7 | 39.1 |

| Combined unit operating costs3,4 | $/tonne | 12.78 | 12.20 | 12.12 | 12.55 |

1 Reported tonnes and grade for ore mined are estimates based on mine plan assumptions and may not reconcile fully to ore milled.

2 Strip ratio is calculated as waste mined divided by ore mined.

3 Reflects combined mine, mill and general and administrative ("G&A") costs per tonne of ore milled. Reflects the deduction of expected capitalized stripping costs.

4 Combined unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

| | | Three months ended | Nine months ended |

| | | Sep. 30, 2024 | Sep. 30, 2023 | Sep. 30, 2024 | Sep. 30, 2023 |

| Contained metal in concentrate produced | | | | | |

| Copper | tonnes | 21,220 | 29,081 | 65,013 | 67,280 |

| Gold | oz | 20,331 | 40,596 | 60,147 | 64,800 |

| Silver | oz | 648,209 | 697,211 | 1,738,760 | 1,669,021 |

| Molybdenum | tonnes | 362 | 466 | 1,128 | 1,169 |

| Payable metal sold | | | | | |

| Copper | tonnes | 18,803 | 27,490 | 59,363 | 65,013 |

| Gold | oz | 9,795 | 32,757 | 65,905 | 59,062 |

| Silver | oz | 365,198 | 460,001 | 1,519,207 | 1,523,740 |

| Molybdenum | tonnes | 343 | 426 | 1,105 | 994 |

| Cost per pound of copper produced | | | | | |

| Cash cost1 | $/lb | 1.80 | 0.83 | 1.28 | 1.34 |

| Sustaining cash cost1 | $/lb | 2.78 | 1.51 | 2.08 | 2.10 |

1 Cash cost and sustaining cash costs per pound of copper produced, net of by-product credits, are not recognized under IFRS. For more detail on these non-IFRS financial performance measures, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

Overview

Peru operations continued to benefit from strong mill throughput, averaging approximately 87,000 tonnes processed per day year-to-date and achieving an average of 88,000 tonnes per day in the third quarter. Cost performance for the nine months ended September 30, 2024 was also strong, despite lower grades milled, achieving lower unit operating costs, cash cost and sustaining cash cost compared to the comparative 2023 period. Cash cost also benefited from higher gold by-product sales revenues throughout 2024.

The planned stripping program at Pampacancha was completed in late September, and mining activities at Pampacancha are now focused on the next mining phase to deliver higher copper and gold grades in the fourth quarter of 2024.

The Company is evaluating opportunities to further increase mill throughput in the medium-to-long-term after the Peruvian Ministry of Energy and Mines approved a regulatory change in June 2024 to allow mining companies in Peru to increase throughput by up to 10% above permitted levels.

Mining Activities

Total ore mined in the third quarter of 2024 decreased by 33% compared to the same period in 2023, in line with our mine plan as we completed the planned stripping program at Pampacancha in late September. Ore mined from Pampacancha during the third quarter decreased to 1.8 million tonnes compared with 5.9 million tonnes in the third quarter of 2023 when we were in an unusually high period of ore mined from Pampacancha as per the 2023 mine plan cadence.

Year-to-date ore mined was 8% lower than the same period in 2023 due to the same factors as the quarterly variance.

Milling Activities

Ore milled during the third quarter of 2024 was 3% higher than the comparative 2023 period mainly due to the treatment of softer ore from stockpiles. Ore milled included supplemental ore feed from stockpiles during the quarter as the team completed pit stripping activities. Milled copper and gold grades decreased by 26% and 48%, respectively, in the third quarter of 2024 compared to the same period in 2023 due to lower amounts of high grade copper and gold from Pampacancha as the stripping campaign was underway, in addition to lower grades from the processing of stockpiled ore.

Ore milled during the first nine months of 2024 was 5% higher than the comparative 2023 period due to the same factors as the quarterly variance. Milled copper and gold grades decreased by 11% and 15%, respectively, in the first nine months of 2024 compared to the same period in 2023 due to the same factors as the quarterly variance.

Recoveries of copper and gold during the third quarter of 2024 were 83% and 68%, respectively, representing a decrease of 3% and 9%, respectively, compared with the same period in 2023 and were in line with our metallurgical models for the ore types that were being processed. Copper and gold recoveries are expected to increase in the fourth quarter as more higher grade ore is processed and less stockpile ore is used to supplement mill feed.

Recoveries of copper, gold and silver during the first nine months of 2024 were 84%, 69% and 67%, representing an increase of 1%, 2%, and 1%, respectively, compared with the 2023 period. This is also in line with our metallurgical models.

Production and Sales Performance

Third quarter 2024 production of copper, gold, silver and molybdenum was 21,220 tonnes, 20,331 ounces, 648,209 ounces and 362 tonnes, respectively, representing a decrease of 27%, 50%, 7% and 22%, respectively, compared with the same period in 2023 due to lower planned grades and recoveries as we completed the planned Pampacancha stripping activities and supplemented mill feed from lower grade stockpiles.

Year-to-date production of copper, gold and molybdenum was 65,013 tonnes, 60,147 ounces, and 1,128 tonnes, respectively, representing a decrease of 3%, 7% and 4%, respectively, from the comparative 2023 period due to the same factors as the quarterly variance. Production of silver was 1,738,760 ounces, representing an increase of 4% from the comparative 2023 period due to higher silver grades from Pampacancha.

Quantities of payable copper, gold and silver sold during the third quarter of 2024 were lower by 32%, 70% and 21%, respectively, than the corresponding period in 2023 primarily due to the same reasons affecting production and the timing of precious metal sales at the end of the quarter.

Year-to-date copper metal sold was 9% lower than the comparable period due to lower copper production levels. Gold metal sold was 12% higher than the comparable period primarily due to timing of precious metal sales at the beginning of the year.

*Copper equivalent production is calculated using the quarter average LME prices for each metal excluding molybdenum.

Cost Performance

Combined mine, mill and G&A unit operating costs in the third quarter were $12.78 per tonne, 5% higher than the same period in 2023 primarily due to higher mining and milling costs following a one-time payment associated with a revised labour agreement. This was partially offset by higher ore milled. Combined mine, mill and G&A unit operating costs in the first nine months of 2024 were $12.12 per tonne, a 3% decrease compared to the same period in 2023 primarily due to lower milling costs and higher ore milled, partially offset by higher mining and G&A costs.

Cash cost per pound of copper produced, net of by-product credits, in the third quarter of 2024 was $1.80, an increase compared to $0.83 in the same period in 2023 due to lower by-product credits mostly as a result of lower gold sales volumes, fewer pounds of copper produced as a result of lower grades, as well as higher mining and milling costs. This was partially offset by lower treatment, refining and freight costs.

On a year-to-date basis, cash costs per pound of copper produced, net of by-product credits was $1.28, a decrease compared to $1.34 in the comparable 2023 period due to higher by-product credits, lower treatment and refining costs and lower milling costs. This was partially offset by higher profit sharing, higher mining cost, and lower pounds of copper produced.

Sustaining cash cost per pound of copper produced, net of by-product credits, was $2.78 in the third quarter, an increase compared to $1.51 in the same period in 2023 for the same factors as described for the cash cost variance above. On a year-to-date basis, sustaining cash cost per pound of copper produced, net of by-products, was consistent with the comparable period in 2023.

Peru Guidance Outlook

| | | Three months ended | Nine months ended | Guidance |

| | | Sep. 30,

2024 | Sep. 30,

2023 | Sep. 30,

2024 | Sep. 30,

2023 | Annual 2024 |

| Contained metal in concentrate produced | | | | | | |

| Copper | tonnes | 21,220 | 29,081 | 65,013 | 67,280 | 98,000 - 120,000 |

| Gold | oz | 20,331 | 40,596 | 60,147 | 64,800 | 76,000 - 93,000 |

| Silver | oz | 648,209 | 697,211 | 1,738,760 | 1,669,021 | 2,500,000 - 3,000,000 |

| Molybdenum | tonnes | 362 | 466 | 1,128 | 1,169 | 1,250 - 1,500 |

| Cost per pound of copper produced | | | | | | |

| Cash cost1 | $/lb | 1.80 | 0.83 | 1.28 | 1.34 | 1.25 - 1.60 |

1 Cash cost per pound of copper produced, net of by-product credits, are not recognized under IFRS. For more detail on these non-IFRS financial performance measures, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

We expect to achieve our 2024 production and cost guidance range for all metals in Peru as the fourth quarter is expected to be the strongest quarter in Peru in 2024. We expect Peru 2024 full year copper production to trend towards the lower end of the guidance range due to lower than expected grades, while gold production is expected to trend towards the higher end of the guidance range due to a larger portion of the feed coming from higher gold grade Pampacancha stockpiles. Cash cost is expected to be favourably positioned at the lower end of the cost guidance range primarily due to high gold by-product credits.

MANITOBA OPERATIONS REVIEW

| | Three months ended | Nine months ended |

| Sep. 30, 2024 | Sep. 30, 2023 | Sep. 30, 2024 | Sep. 30, 2023 |

| Lalor ore mined | tonnes | 411,295 | 367,491 | 1,204,481 | 1,154,345 |

| Gold | g/tonne | 5.45 | 5.08 | 4.70 | 4.35 |

| Copper | % | 0.91 | 1.02 | 0.82 | 0.80 |

| Zinc | % | 2.73 | 3.31 | 2.80 | 3.25 |

| Silver | g/tonne | 30.45 | 27.80 | 25.46 | 23.08 |

| New Britannia ore milled | tonnes | 191,298 | 146,927 | 529,606 | 431,874 |

| Gold | g/tonne | 6.77 | 6.93 | 6.39 | 6.27 |

| Copper | % | 0.93 | 1.22 | 1.00 | 0.87 |

| Zinc | % | 1.12 | 0.90 | 0.96 | 0.84 |

| Silver | g/tonne | 30.24 | 23.88 | 25.62 | 24.01 |

| Copper concentrate | tonnes | 10,856 | 10,313 | 31,853 | 21,997 |

| Concentrate grade | % Cu | 15.18 | 16.93 | 15.70 | 16.06 |

| Gold recovery1 | % | 90.0 | 88.8 | 89.5 | 88.5 |

| Copper recovery | % | 92.8 | 97.4 | 94.5 | 94.3 |

| Silver recovery1 | % | 79.9 | 82.0 | 81.4 | 80.8 |

| Contained metal in concentrate produced | | | |

| Gold | oz | 24,355 | 21,189 | 68,000 | 53,038 |

| Copper | tonnes | 1,648 | 1,745 | 5,001 | 3,531 |

| Silver | oz | 114,157 | 71,290 | 277,132 | 202,193 |

| Metal in doré produced2 | | | |

| Gold | oz | 16,768 | 14,403 | 44,106 | 26,095 |

| Silver | oz | 42,244 | 39,926 | 118,977 | 62,735 |

| Stall ore milled | tonnes | 222,621 | 255,516 | 671,506 | 736,768 |

| Gold | g/tonne | 4.23 | 3.70 | 3.44 | 3.21 |

| Copper | % | 0.89 | 0.77 | 0.71 | 0.74 |

| Zinc | % | 4.12 | 4.88 | 4.23 | 4.72 |

| Silver | g/tonne | 30.20 | 28.82 | 25.43 | 22.81 |

| Copper concentrate | tonnes | 8,438 | 9,036 | 21,807 | 23,962 |

| Concentrate grade | % Cu | 20.74 | 20.32 | 19.20 | 20.41 |

| Zinc concentrate | tonnes | 15,338 | 19,431 | 48,456 | 55,046 |

| Concentrate grade | % Zn | 52.61 | 52.97 | 51.50 | 52.50 |

| Gold recovery | % | 70.5 | 67.8 | 68.3 | 63.7 |

| Copper recovery | % | 88.3 | 93.9 | 88.5 | 89.8 |

| Zinc recovery | % | 88.1 | 82.6 | 87.9 | 83.0 |

| Silver recovery | % | 57.8 | 64.9 | 57.4 | 61.3 |

| Contained metal in concentrate produced | | | |

| Gold | oz | 21,345 | 20,621 | 50,681 | 48,367 |

| Copper | tonnes | 1,750 | 1,835 | 4,188 | 4,888 |

| Zinc | tonnes | 8,069 | 10,291 | 24,954 | 28,895 |

| Silver | oz | 124,996 | 153,536 | 315,758 | 331,216 |

1 Gold and silver recovery includes total recovery from concentrate and doré.

2 Doré includes sludge, slag and carbon fines.

| | Three months ended | Nine months ended |

Sep. 30,

2024 | Sep. 30,

2023 | Sep. 30,

2024 | Sep. 30,

2023 |

| Total contained metal in concentrate and doré produced1 |

| Gold | oz | 62,468 | 56,213 | 162,787 | 127,500 |

| Copper | tonnes | 3,398 | 3,580 | 9,189 | 8,419 |

| Zinc | tonnes | 8,069 | 10,291 | 24,954 | 28,895 |

| Silver | oz | 281,397 | 264,752 | 711,867 | 596,144 |

| Payable metal sold in concentrate and doré | | | | |

| Gold | oz | 57,238 | 36,713 | 162,004 | 107,662 |

| Copper | tonnes | 2,931 | 2,925 | 8,281 | 7,021 |

| Zinc | tonnes | 8,607 | 7,125 | 19,859 | 21,394 |

| Silver | oz | 244,974 | 197,952 | 674,301 | 481,547 |

| Unit Operating Costs2 | | | | | |

| Lalor | C$/tonne | 132.97 | 151.14 | 143.10 | 140.81 |

| New Britannia | C$/tonne | 66.14 | 91.07 | 71.66 | 85.80 |

| Stall | C$/tonne | 46.72 | 36.56 | 41.92 | 35.46 |

| Combined mine/mill unit operating costs3,4 | C$/tonne | 211 | 217 | 224 | 218 |

| Cost per ounce of gold produced | | | | | |

| Cash cost4 | $/oz | 372 | 670 | 606 | 864 |

| Sustaining cash cost4 | $/oz | 553 | 939 | 855 | 1,212 |

1 Metal reported in concentrate is prior to deductions associated with smelter terms.

2 Reflects costs per tonne of ore mined/milled.

3 Reflects combined mine, mill and G&A costs per tonne of milled ore.

4 Combined unit costs, cash cost and sustaining cash cost per ounce of gold produced, net of by-product credits, are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

Overview

The Snow Lake operations in Manitoba delivered record production results during the third quarter of 2024, continuing to exceed expectations in performance and efficiency.

Performance from the Lalor mine was strong, benefiting from improved longhole muck fragmentation and a consistent higher-grade mining sequence that surpassed forecasted metal grades. In August, we successfully completed a five-day planned maintenance program aimed at enhancing the efficiency and reliability of our key infrastructure at the mine. Ongoing modifications to stope design further enhanced mucking efficiency throughout the lifecycle of stopes.

The New Britannia mill had another quarter of exceptional performance with the mill operating consistently above name plate capacity of 1,500 tonnes per day and achieving a new quarterly production record with an average throughput of 2,080 tonnes per day in the third quarter. Plant availability continues to improve, supported by low-capital projects aimed at further increasing throughput while continuing to achieve targeted gold recoveries of 90%. These efforts align with our long-term objectives of maximizing gold production by processing more high-grade ore from Lalor through the New Britannia mill, leading to higher gold recoveries. Notably, enhancements in the elution and stripping cycles contributed to increased gold doré production.

At the Stall mill, there was a slight reduction in throughput as more ore was diverted to New Britannia. Benefits from recent recovery improvement programs continue to be realized with gold recoveries of 71% and 68% achieved in the third quarter and year-to-date, respectively, compared to 64% in the first nine months of 2023. Efforts to continue to optimize recovery were advanced with the installation of new elongated cyclones in one of the two milling circuits late in third quarter. These cyclones are designed to improve grind size and, pending positive performance results, could be implemented across other circuits. Additionally, transitioning operational and maintenance responsibilities for the external crusher from contractors to the in-house team has resulted in more efficient cost management, supporting long-term savings at the Snow Lake operations.

Progress on the 1901 exploration drift is on track to intersect mineralization by early 2025, laying the groundwork for the 1901 haulage drift that will support full production from the 1901 deposit by 2027. Diamond drilling will soon follow to evaluate the orebody and optimize the mining approach for future conversion of inferred mineral resources into mineral reserves.

Environmental initiatives continue to progress well in Manitoba. At the Anderson tailings facility, enhanced deposition efficiency enabled deferral of dam construction capital to future years, while a new trial exploring alternative shore deposition techniques shows potential for further gains in efficiency. The operations remain on track to meet their environmental targets for 2024, with significant reductions in propane and diesel consumption achieved year-to-date compared to 2023. In addition, an initiative at Lalor to recycle natural groundwater for use as process water has successfully reduced the mine's reliance on fresh water.

Mining Activities

Total ore mined in Manitoba in the third quarter of 2024 was 12% higher than the comparable quarter in 2023. Gold and silver grades mined at Lalor during the third quarter were 7% and 10% higher, respectively, compared with the same period in 2023. Copper and zinc grades mined at Lalor during the third quarter were 11% and 18% lower, respectively, compared with the same period in 2023. The third quarter of 2024 saw significant improvements in ore production and precious metal grade quality. These changes align with improvements in mining techniques, most notably in longhole muck fragmentation, and anticipated higher grade precious metal sequences as part of the mine plan for the quarter.

Total ore mined at our Manitoba operations during the first nine months of 2024 was 4% higher than the same period in 2023. Gold, copper and silver grades mined at Lalor during the first nine months of 2024 were 8%, 3% and 10% higher, respectively, compared with the same period in 2023, consistent with the mine plan. Zinc grades mined at Lalor during the first nine months of 2024 were 14% lower than the same period in 2023.

Milling Activities

Consistent with our strategy of allocating more Lalor ore feed to New Britannia, the New Britannia mill throughput averaged approximately 2,080 tonnes per day in the third quarter of 2024, approximately 30% above average daily throughput levels in the same period in 2023. Recoveries of gold, copper and silver in the third quarter of 2024 were 90%, 93% and 80%, respectively, representing an increase of 1%, and a decrease of 5% and 3%, respectively, compared to the same period in 2023. Year-to-date total ore milled at New Britannia was 23% higher than the prior period for the same reason. With the higher ore grade processed, precious metals recoveries also increased by 1% year-to-date compared to the same period in 2023.

During the three and nine months ended September 30, 2024, the Stall mill processed 13% and 9% less ore, respectively, compared with the same period in 2023, which is aligned with our strategy of allocating more Lalor ore feed to New Britannia, as noted above. The Stall mill achieved gold recoveries of 71% in the third quarter, reflecting benefits from recent recovery improvement programs as higher gold grade ore is processed.

Production and Sales Performance

Manitoba operations achieved a new quarterly record for gold production at 62,468 ounces in the third quarter of 2024. The operations also produced 3,398 tonnes of copper, 8,069 tonnes of zinc and 281,397 ounces of silver during the third quarter of 2024. Compared to the third quarter of 2023, production of gold and silver in the third quarter of 2024 increased by 11% and 6%, respectively, while production of copper and zinc declined by 5% and 22%, respectively. The increased gold and silver production in the quarter is mainly due to our strategy of mining and allocating more Lalor gold ore feed to New Britannia to achieve higher recoveries, which resulted in planned lower production of copper and zinc.

Production of gold, copper and silver in the first nine months of 2024 was higher by 28%, 9% and 19%, respectively, than the comparative 2023 period mainly due to the same reasons as noted above, as well as higher production from copper-gold zones in the first quarter of 2024. Zinc production in the first nine months of 2024 decreased by 14%, aligned with forecasted production and strategy to mine more gold ore at Lalor.

Quantities of payable metal during the third quarter of 2024 were higher than the comparable periods in 2023 for all metals sold, primarily due to the same factors impacting contained metal production, as noted above. For the nine months ended September 30, 2024, payable metals sold for gold, copper and silver were higher than the comparable period, while zinc metal sold was lower than the comparable period.

Cost Performance

Lalor mining costs during the third quarter of 2024 decreased by 12% compared to the same period in 2023, achieving the lowest cost in the past 2 years, despite inflationary factors over that period, as a result of efficiency improvements and higher tonnage mined. Compared to the same period in 2023, milling costs at the Stall mill were 28% higher during the third quarter of 2024, primarily due to lower throughput as described earlier. New Britannia milling costs decreased by 27% during the third quarter of 2024 versus the same period in 2023, primarily a result of higher throughput as described earlier. Combined mine, mill and G&A unit operating costs in the third quarter of 2024 were C$211 per tonne, representing a 3% decrease compared to the same period in 2023. Combined mine, mill and G&A unit operating costs in the first nine months of 2024 increased by 3% to C$224 per tonne. The marginal increase in combined operating costs year-over-year was the result of higher administrative costs and longer haulage distances, which were partially offset by the effect of higher total throughput.

Cash cost per ounce of gold produced, net of by-product credits, in the third quarter of 2024 was $372, a decrease of 44% compared to the same period in 2023 due to significantly higher gold production and higher by-product credits, partially offset by higher G&A costs.

Sustaining cash cost per ounce of gold produced, net of by-product credits, in the third quarter of 2024 was $553, a decrease of 41% compared to the same period in 2023, primarily due to the same factors affecting cash cost and lower sustaining capital costs during the quarter.

Cash cost per ounce of gold produced, net of by-product credits, in the first nine months of 2024 was $606 per ounce. These costs were 30% lower compared to the same period in 2023 primarily due to higher gold production and by-product credits, partially offset by higher mining, milling and G&A costs resulting from higher employee profit sharing costs. Sustaining cash cost per ounce of gold produced, net of by-product credits, for the first nine months of 2024 was $855 per ounce, a decrease of 29% from the comparative 2023 period primarily due to the same factors affecting cash cost noted above, with lower sustaining capital expenditures compared to the prior year.

Manitoba Guidance Outlook

| | Three months ended | Nine months ended | Guidance |

Sep. 30,

2024 | Sep. 30,

2023 | Sep. 30,

2024 | Sep. 30,

2023 | Annual 2024 |

| Total contained metal in concentrate and doré produced1 | |

| Gold2 | oz | 62,468 | 56,213 | 162,787 | 127,500 | 170,000 - 200,000 |

| Copper | tonnes | 3,398 | 3,580 | 9,189 | 8,419 | 9,000 - 12,000 |

| Zinc | tonnes | 8,069 | 10,291 | 24,954 | 28,895 | 27,000 - 35,000 |

| Silver3 | oz | 281,397 | 264,752 | 711,867 | 596,144 | 750,000 - 1,000,000 |

| Cost per ounce of gold produced | |

| Cash cost4 | $/oz | 372 | 670 | 606 | 864 | 700 - 900 |

1 Metal reported in concentrate is prior to deductions associated with smelter terms.

2 Gold production guidance includes gold contained in concentrate produced and gold in doré.

3 Silver production guidance includes silver contained in concentrate produced and silver in doré.

4 Combined unit costs, cash cost per ounce of gold produced, net of by-product credits, are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

We now expect to exceed the top end of the 2024 gold production guidance range in Manitoba driven by outperformance at New Britannia with throughput achieving new record levels and the Lalor mine delivering better-than-expected gold grades by focusing on ore quality improvements. We also expect copper production to trend towards the higher end of the 2024 guidance range, and we are well on track to achieve zinc and silver 2024 production guidance. Similarly, we expect 2024 gold cash cost to be favourably positioned at the lower end of the cost guidance range, reflecting the strong cost control and gold production achieved to date.

BRITISH COLUMBIA OPERATIONS REVIEW

| | | Three months ended | Nine months

ended5 | Since

acquisition to5 |

| | | Sep. 30, 2024 | Sep. 30, 2023 | Sep. 30, 2024 | Sep. 30, 2023 |

| Ore mined1 | tonnes | 3,098,863 | 3,792,568 | 8,986,081 | 4,347,991 |

| Strip ratio2 | | 6.05 | 2.96 | 5.62 | 2.90 |

| Ore milled | tonnes | 3,363,176 | 3,158,006 | 9,775,752 | 3,600,261 |

| Copper | % | 0.24 | 0.36 | 0.25 | 0.36 |

| Gold | g/tonne | 0.09 | 0.08 | 0.08 | 0.08 |

| Silver | g/tonne | 0.73 | 1.40 | 0.97 | 1.36 |

| Copper concentrate | tonnes | 28,049 | 39,068 | 87,974 | 44,629 |

| Concentrate grade | % Cu | 24.0 | 23.8 | 23.3 | 23.8 |

| Copper recovery | % | 84.1 | 80.9 | 83.2 | 80.5 |

| Gold recovery | % | 67.3 | 56.1 | 62.2 | 57.5 |

| Silver recovery | % | 71.2 | 71.3 | 72.6 | 72.2 |

| Combined unit operating costs3,4 | C$/tonne | 15.58 | 24.88 | 19.56 | 21.82 |

1 Reported tonnes and grade for ore mined are estimates based on mine plan assumptions and may not reconcile fully to ore milled.

2 Strip ratio is calculated as waste mined divided by ore mined.

3 Reflects combined mine, mill and general and administrative ("G&A") costs per tonne of ore milled. Reflects the deduction of expected capitalized stripping costs.

4 Combined unit costs is a non-IFRS financial performance measure with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

5 Copper Mountain mine results are stated at 100%. Hudbay owns 75% of Copper Mountain mine. As Copper Mountain was acquired on June 20, 2023, the results for the nine months ended September 30, 2023 represents the period from the acquisition date, June 20, 2023, through to the end of the third quarter of 2023.

| | | Three months ended | Nine months

ended2 | Since

acquisition to2 |

| | | Sep. 30, 2024 | Sep. 30, 2023 | Sep. 30, 2024 | Sep. 30, 2023 |

| Contained metal in concentrate produced | | | | |

| Copper | tonnes | 6,736 | 9,303 | 20,479 | 10,542 |

| Gold | oz | 6,274 | 4,608 | 15,145 | 5,353 |

| Silver | oz | 55,963 | 101,069 | 221,566 | 112,987 |

| Payable metal sold | | | | | |

| Copper | tonnes | 6,026 | 8,956 | 19,523 | 8,956 |

| Gold | oz | 6,199 | 5,329 | 14,699 | 5,329 |

| Silver | oz | 53,241 | 91,002 | 205,789 | 91,002 |

| Cost per pound of copper produced | | | | |

| Cash cost1 | $/lb | 1.81 | 2.67 | 2.67 | 2.36 |

| Sustaining cash cost1 | $/lb | 5.06 | 3.39 | 5.15 | 2.99 |

1 Cash cost and sustaining cash cost, net of by-product credits, are non-IFRS financial performance measures with no standardized definition under IFRS. For further information and a detailed reconciliation, please see the discussion under the "Non-IFRS Financial Performance Measures" section of this MD&A.

2 Copper Mountain mine results are stated at 100%. Hudbay owns 75% of Copper Mountain mine. As Copper Mountain was acquired on June 20, 2023, the results for the nine months ended September 30, 2023 represents the period from the acquisition date, June 20, 2023, through to the end of the third quarter of 2023.

Overview

Since acquiring Copper Mountain in June 2023, Hudbay has been focused on advancing operational stabilization plans, including opening up the mine by re-activating the full mining fleet, adding additional mining faces, optimizing the ore feed to the plant and implementing plant improvement initiatives that mirror Hudbay's successful processes at Constancia. These stabilization plans have successfully increased the total tonnes moved and resulted in stronger mill performance as demonstrated by record high mill availability of 95% and above-target copper recoveries of 84% in the third quarter of 2024. As a result, year-to-date mill performance has resulted in the highest mill availability and highest copper recoveries achieved at Copper Mountain mine in the last decade. Similarly, the stabilization efforts have successfully reduced combined unit operating costs to C$19.56 per tonne year-to-date, compared to C$21.38 per tonne milled in second half of 2023 (or first six months since acquisition).

Efforts are now focused on optimizing the operations throughout the balance of 2024 and into 2025. Mining activities will continue to execute the three-year accelerated stripping program intended to bring higher grade ore into the mine plan. Feasibility engineering has commenced to debottleneck and increase the nominal plant capacity to its permitted capacity of 50,000 tonnes per day earlier than contemplated in the most recent technical report.

Mining Activities

Total ore mined at Copper Mountain in the third quarter of 2024 was 3.1 million tonnes, a decrease of 18% compared to the third quarter of 2023. As planned, ore stockpiles were utilized as ore feed to the mill while the mine operation team increased waste stripping activities. Total material moved continued to ramp up in the quarter to 23.0 million tonnes, compared to 16.5 million tonnes in the same period last year, as a result of effective usage of the mining fleet to execute the accelerated stripping program to access higher head grades. The focus in the third quarter of 2024 was on mining efficiencies and operator recruitment to effectively utilize the available haul trucks fleet. As a result, total material moved is expected to continue to increase quarter-over-quarter as per the mine plan.

Milling Activities