Exhibit 99.1

HUDBAY MINERALS INC.

ANNUAL INFORMATION FORM

FOR THE

YEAR ENDED DECEMBER 31, 2010

March 29, 2011

TABLE OF CONTENTS

FORWARD-LOOKING INFORMATION | 1 | |||

NOTE TO UNITED STATES INVESTORS | 1 | |||

CURRENCY PRESENTATION AND EXCHANGE RATE DATA | 2 | |||

DOCUMENTS INCORPORATED BY REFERENCE | 2 | |||

CORPORATE STRUCTURE | 3 | |||

Incorporation and Registered Office | 3 | |||

Intercorporate Relationships | 3 | |||

Summary | 4 | |||

Three Year History | 4 | |||

DESCRIPTION OF OUR BUSINESS | 7 | |||

Principal Assets | 7 | |||

Our Strategy | 8 | |||

Products and Marketing | 38 | |||

Employees | 38 | |||

Corporate Social Responsibility | 38 | |||

RISK FACTORS | 40 | |||

DESCRIPTION OF CAPITAL STRUCTURE | 48 | |||

Common Shares | 48 | |||

Preference Shares | 49 | |||

Normal Course Issuer Bid | 49 | |||

DIVIDENDS | 49 | |||

MARKET FOR SECURITIES | 49 | |||

Price Range and Trading Volume | 49 | |||

DIRECTORS AND OFFICERS | 51 | |||

Board of Directors | 51 | |||

Executive Officers | 53 | |||

Corporate Cease Trade Orders, Bankruptcies, Penalties and Sanctions | 54 | |||

Conflict of Interest | 55 | |||

AUDIT COMMITTEE DISCLOSURE | 55 | |||

LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 57 | |||

INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 58 | |||

TRANSFER AGENT AND REGISTRAR | 58 | |||

MATERIAL CONTRACTS | 58 | |||

QUALIFIED PERSON | 58 | |||

INTEREST OF EXPERTS | 58 | |||

ADDITIONAL INFORMATION | 58 | |||

SCHEDULE A GLOSSARY OF MINING TERMS | A-1 | |||

SCHEDULE B AUDIT COMMITTEE CHARTER | B-1 |

FORWARD-LOOKING INFORMATION

This annual information form (“AIF”) contains “forward-looking information”, within the meaning of applicable Canadian and U.S. securities legislation. Forward-looking information includes, but is not limited to, information with respect to HudBay Minerals Inc.’s (“HudBay”) plans respecting the Constancia and Lalor projects and its other key mineral properties and the ability to secure and maintain required permits for such properties, exploration expenditures and activities and the possible success of such exploration activities, the estimation of mineral reserves and resources, the realization of mineral estimates, the timing and amount of estimated future production, costs of production, capital expenditures, costs and timing of the development of new deposits, mineral pricing, mine life projections, the availability of third party concentrate, business and acquisition strategies and the timing and possible outcome of pending litigation. Often, but not always, forward-looking information can be identified by the use of forward-looking words like “plans”, “expects”, or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “intends”, “understands”, “anticipates”, or “does not anticipate”, or “believes” or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might”, or “will be taken”, “occur”, or “be achieved”. Forward-looking information is based on the opinions and estimates of management as of the date such information is provided and is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of HudBay to be materially different from those expressed or implied by such forward-looking information, including risks associated with the mining industry such as economic factors (including future commodity prices, currency fluctuations and energy prices), failure of plant, equipment, processes and transportation services to operate as anticipated, dependence on key personnel and employee relations, environmental risks, government regulation, actual results of current exploration activities, possible variations in ore grade or recovery rates, permitting timelines, capital expenditures, reclamation activities, land titles, and social and political developments and other risks of the mining industry as well as those risk factors discussed or referred to in this AIF under the heading “Risk Factors”. Although HudBay has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that forward-looking information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. HudBay does not undertake to update any forward-looking information, except as required by applicable securities laws, or to comment on analyses, expectations or statements made by third parties in respect of HudBay, its financial or operating results or its securities.

NOTE TO UNITED STATES INVESTORS

Information concerning our mineral properties has been prepared in accordance with the requirements of Canadian securities laws, which differ in material respects from the requirements of the Securities and Exchange Commission (the “SEC”) Industry Guide 7. Under Industry Guide 7, mineralization may not be classified as a “reserve” unless the determination has been made that the mineralization could be economically and legally produced or extracted at the time of the reserve determination, and the SEC does not recognize the reporting of mineral deposits which do not meet the Industry Guide 7 definition of “Reserve”. In accordance with National Instrument 43-101 - Standards of Disclosure for Mineral Projects (“NI 43-101”) of the Canadian Securities Administrators, the terms “mineral reserve”, “proven mineral reserve”, “probable mineral reserve”, “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are defined in the Canadian Institute of Mining, Metallurgy and Petroleum (the “CIM”) Definition Standards for Mineral Resources and Mineral Reserves adopted by the CIM Council on December 11, 2005. While the terms “mineral resource”, “measured mineral resource”, “indicated mineral resource” and “inferred mineral resource” are recognized and required by NI 43-101, the SEC does not recognize them. You are cautioned that, except for that portion of mineral resources classified as mineral reserves, mineral resources do not have demonstrated economic value. Inferred mineral resources have a high degree of uncertainty as to their existence and as to whether they can be economically or legally mined. Under Canadian securities laws, estimates of inferred mineral resources may not form the basis of an economic analysis. It cannot be assumed that all or any part of an inferred mineral resource will ever be upgraded to a higher category. Therefore, you are cautioned not to assume that all or any part of an inferred mineral resource exists, that it can be economically or legally mined, or that it will ever be upgraded to a higher category. Likewise, you are cautioned not to assume that all or any part of measured or indicated mineral resources will ever be upgraded into mineral reserves. For more information on the technical terms as they are used under NI 43-101, please see Schedule A “Glossary of Mining Terms”.

CURRENCY PRESENTATION AND EXCHANGE RATE DATA

This AIF contains references to both United States dollars and Canadian dollars. All dollar amounts referenced, unless otherwise indicated, are expressed in Canadian dollars, and United States dollars are referred to as “United States dollars” or “US$”.

The closing, high, low and average exchange rates for the United States dollar in terms of the Canadian dollar for each of the three years ended December 31, 2010, 2009 and 2008, as reported by the Bank of Canada, are as follows:

| 2010 | 2009 | 2008 | ||||||||||

Closing | $ | 0.99 | $ | 1.05 | $ | 1.22 | ||||||

High | $ | 1.07 | $ | 1.30 | $ | 1.30 | ||||||

Low | $ | 0.99 | $ | 1.03 | $ | 0.97 | ||||||

Average(1) | $ | 1.03 | $ | 1.14 | $ | 1.07 | ||||||

Note:

| (1) | Calculated as an average of the daily noon rates for each period. |

On March 28, 2011 the Bank of Canada noon rate of exchange was US$1.00 = Cdn$0.98.

CONVERSION TABLE

To Convert | To | Multiply by | ||

| Tonnes | Tons | 1.102311 | ||

| Tonnes | Pounds | 2204.62 | ||

| Grams | Troy ounces | 0.032151 | ||

| Grams/tonne | Troy ounces/ton | 0.029167 | ||

| Hectares | Acres | 2.47105 | ||

| Kilometers | Miles | 0.62137 | ||

| Meters | Feet | 3.28084 |

DOCUMENTS INCORPORATED BY REFERENCE

Any statement contained in a document incorporated or deemed to be incorporated by reference herein shall be deemed to be modified or superseded for purposes of this AIF to the extent that a statement contained herein, or in any other subsequently filed document that also is incorporated or is deemed to be incorporated by reference herein, modifies or supersedes such statement. The modifying or superseding statement need not state that it has modified or superseded a prior statement or include any other information set forth in the document that it modifies or supersedes. The making of a modifying or superseding statement will not be deemed an admission for any purposes that the modified or superseded statement, when made, constituted a misrepresentation, an untrue statement of a material fact or an omission to state a material fact that is required to be stated or that is necessary to make a statement not misleading in light of the circumstances in which it was made. Any statement so modified or superseded shall not, except as so modified or superseded, constitute a part of this AIF after it has been modified or superseded.

Reference is made to the Glossary of Mining Terms attached as Schedule A to this AIF.

Unless the context suggests otherwise, references to “we”, “us”, “our” and similar terms, as well as references to “HudBay”, refer to HudBay Minerals Inc.

- 2 -

CORPORATE STRUCTURE

Incorporation and Registered Office

We were formed by the amalgamation of Pan American Resources Inc. and Marvas Developments Ltd. on January 16, 1996, pursuant to theBusiness Corporations Act (Ontario) and changed our name to Pan American Resources Inc. On March 12, 2002, we acquired ONTZINC Corporation, a private Ontario corporation, through a reverse takeover and changed our name to ONTZINC Corporation. On December 21, 2004, we acquired Hudson Bay Mining and Smelting Co., Limited (“HBMS”) and changed our name to HudBay Minerals Inc. In connection with the acquisition of HBMS, on December 21, 2004, we amended our articles to consolidate our common shares on a 30 to one basis. On October 25, 2005, we were continued under theCanada Business Corporations Act (“CBCA”).

Our registered office is located at 2200-201 Portage Avenue, Winnipeg, Manitoba R3B 3L3 and our principal executive office is located at 1 Adelaide Street East, Suite 2501, Toronto, Ontario M5C 2V9.

Our common shares are listed on the Toronto Stock Exchange (“TSX”) and the New York Stock Exchange (“NYSE”) under the symbol “HBM”.

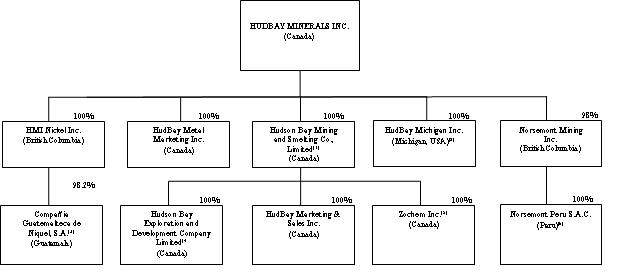

Intercorporate Relationships

The following chart shows our principal subsidiaries, their jurisdiction of incorporation and the percentage of voting securities we beneficially own or over which we have control or direction.

Notes:

| (1) | HBMS owns our 777, Trout Lake and Chisel North mines and our Lalor project. |

| (2) | HudBay Michigan Inc. owns a 51% interest in the Back Forty project, a joint venture with Aquila Resources Inc. |

| (3) | Compañia Guatemala de Niquel S.A. (“CGN”) owns our Fenix nickel project. |

| (4) | Hudson Bay Exploration and Development Company Limited (“HBED”) holds our key exploration properties and acts as agent for HBMS. |

| (5) | Our Zochem zinc oxide business was transferred from HBMS to Zochem Inc. effective January 1, 2010. |

| (6) | Norsemont Peru S.A.C. owns the Constancia copper project. |

- 3 -

GENERAL DEVELOPMENT OF OUR BUSINESS

Summary

We are a diversified Canadian mining company with assets in North, Central and South America. Through our subsidiaries, we own copper/zinc/gold mines, ore concentrators and zinc production facilities in northern Manitoba and Saskatchewan, a zinc oxide production facility in Ontario, a nickel project in Guatemala and a copper project in Peru. HudBay produces copper concentrate (containing copper, gold and silver), zinc metal and zinc oxide.

Three Year History

Acquisition of Norsemont Mining Inc.

We entered into a support agreement (the “Support Agreement”) with Norsemont Mining Inc. (“Norsemont”) on January 9, 2011. Norsemont is a publicly-listed company whose common shares trade on the TSX and the Lima Stock Exchange under the symbol “NOM”. It owns 100% of the Constancia copper project in southern Peru. The Constancia project has proven and probable mineral reserves containing 372 million tonnes grading 0.39% copper, 105 g/t molybdenum, 0.05 g/t gold and 3.6 g/t silver. Based on the optimization study released on February 21, 2011, the Constancia project is expected to produce an average of 85,000 tonnes of copper, 1,400 tonnes of molybdenum and 69 tonnes of silver each year over a 15.3 year mine life.

As contemplated by the Support Agreement, we mailed an offer and take-over bid circular (the “Norsemont Circular”) on January 24, 2011 to the holders of Norsemont’s common shares. As set forth in the Norsemont Circular, Norsemont shareholders were entitled to elect to receive as consideration for each deposited Norsemont common share, either: (a) 0.2617 of a HudBay common share and $0.001 in cash, or (b) cash in an amount that is greater than $0.001, not to exceed $4.50, and, if less than $4.50 in cash was elected, the number of HudBay common shares equal to the excess of $4.50 over such elected cash amount, divided by $17.19, subject, in each case, to pro-ration and rounding as set out in the Offer and take-over bid circular.

On March 1, 2011 we announced that we were successful in our bid to acquire Norsemont and that we had taken up a total of 104,635,351 Norsemont common shares which were deposited at the original expiry time of the Offer. We subsequently extended our offer until 5:00 p.m. (Toronto time) on March 15, 2011, and our offer expired on that date. Pursuant to the Offer, we issued 22,084,459 common shares and paid an aggregate of $127,680,990 in cash to former Norsemont shareholders. We now own approximately 98% of the issued and outstanding Norsemont common shares (on a fully-diluted basis). We intend to acquire the remaining Norsemont shares by way of a compulsory acquisition transaction under section 300 of theBusiness Corporations Act(British Columbia).

New Credit Facility

On November 3, 2010 we announced a new four-year $300 million revolving credit facility with a syndicate of lenders.

New York Stock Exchange Listing

Our common shares commenced trading on the NYSE on October 25, 2010 under the ticker symbol “HBM”, which is the same ticker symbol HBMS was listed under on the NYSE from 1938 until 1983. Our listing on the NYSE is intended to increase the trading liquidity of our common shares and provide greater visibility among U.S.-based investors.

Back Forty Joint Venture

On September 1, 2010 we exercised our option to earn a 51% interest in Aquila Resources Inc.’s (“Aquila”) Back Forty project in Michigan’s Upper Peninsula. We earned our joint venture interest pursuant to an option agreement entered into with Aquila on August 6, 2009 by incurring a minimum of US$10 million of

- 4 -

exploration expenditures on the project. We can increase our joint venture interest to 65% by completing a feasibility study and making the required permitting applications.

On October 15, 2010 we announced an updated NI 43-101 mineral resource estimate for the Back Forty project. The updated resource includes 18.1 million tonnes of measured and indicated mineral resources and 3.2 million tonnes of inferred mineral resources. See “Description of Our Business – Joint Ventures - Back Forty Joint Venture”.

Investment in Augusta Resource Corporation

On August 27, 2010 we acquired 10,905,590 units of Augusta Resource Corporation (“Augusta”) at a subscription price of $2.75 per unit and an aggregate acquisition cost of approximately $30 million. Each unit consists of one Augusta common share and one half of a common share purchase warrant which was exercisable for one common share at an exercise price of $3.90 until February 27, 2012. On March 18, 2011, we exercised all of our Augusta warrants after receiving notice from Augusta that, in accordance with Augusta’s rights under the warrants, the expiry time of the warrants had been accelerated to March 21, 2011. Following our exercise of the warrants, we now own approximately 14.3% of Augusta’s issued and outstanding common shares. Augusta’s primary asset is the Rosemont copper project in Arizona. The investment in Augusta was consistent with our strategy of investing in junior companies with promising near-development mining projects.

Lalor Production Decision

On August 4, 2010, our board of directors made a full commitment to the development of our 100% owned Lalor project near Snow Lake, Manitoba by authorizing the expenditures necessary to put the project into full production. Full production from the 985 meter production shaft is anticipated in late 2014. The project’s estimated capital cost of $560 million, which includes $59 million spent as at December 31, 2010, is expected to fund full project development. We intend to fully fund the project from our currently available liquidity and future cash flows.

Our board of directors had previously approved an $85 million expenditure to fund the development of an access ramp from our Chisel North mine to the deposit, which is expected to enable early production of zinc ore in early 2012 and provide access to the Lalor gold zone for additional underground exploration. Development of the ramp commenced in December 2009 and as of February 28, 2011 the ramp had advanced 1,750 meters. We are currently preparing a trade-off study to determine whether to refurbish our Snow Lake concentrator or construct a new concentrator at the Lalor mine site and we expect to be in a position to make a decision on whether to proceed with a new concentrator in mid-2011. For detail on the estimated mineral resources at Lalor and conceptual estimates of the tonnes and grade of the gold zone and copper-gold zone, see “Description of Our Business – Development Projects – Lalor Project”.

777 North Expansion

On August 4, 2010 we announced plans to expand our 777 mine. The 777 North expansion involves driving a ramp from surface to the 440 meter level to access mineral resources of 550,000 tonnes grading 1.5 g/t gold, 22.5 g/t silver, 1.0% copper and 3.6% zinc. These zones are connected to the underground workings of our 777 mine. Total capital costs for the expansion are estimated at $20 million. Production is expected to begin in 2012 at a rate of 330 tonnes per day, producing approximately 5,500 tonnes of copper metal and 20,000 tonnes of zinc metal over the six year life of the project.

Upon completion, the 777 North expansion will provide an additional egress from the mine and supply additional ore feed to the Flin Flon concentrator and zinc plant. It will also help to sustain employment in Flin Flon as the Trout Lake mine reaches the end of mine life and facilitate the development of an underground exploration platform to evaluate additional exploration opportunities near the 777 mine.

- 5 -

CEO Appointment

David Garofalo joined us as our President and Chief Executive Officer (“CEO”) on July 12, 2010, succeeding W. Warren Holmes, who had served as our Interim CEO since January 1, 2010 and our Executive Vice Chairman since November 12, 2009.

Mr. Garofalo was previously Senior Vice President, Finance and Chief Financial Officer at Agnico-Eagle Mines Limited, where he had been employed since 1998. Before that, Mr. Garofalo served as Treasurer and in various finance roles with another international mining company between 1990 and 1998.

Reed Lake Joint Venture

On July 5, 2010 we entered into a joint venture agreement and four option agreements with VMS Ventures Inc. (“VMS Ventures”) respecting our copper-rich Reed Lake property and a series of adjacent mineral properties held by VMS Ventures in the Flin Flon Greenstone Belt.

Pursuant to the joint venture agreement, we have a 70% interest and VMS Ventures has a 30% interest in a joint venture respecting the Reed Lake property and the two claims immediately to the south. See “Description of Our Business – Joint Ventures – Reed Lake Joint Venture”.

Closure of Copper Smelter and Refinery

On June 11, 2010 we completed the closure of our copper smelter in Flin Flon, which had been in operation for over 80 years. Our White Pine copper refinery closed soon thereafter once the final anodes produced at the smelter were processed.

Re-Start of Chisel North Mine and Snow Lake Concentrator

On October 30, 2009 we announced the re-start of operations at our Chisel North mine and Snow Lake concentrator, which were placed on care and maintenance in the first quarter of 2009 due to depressed metals prices. In connection with the re-start of Chisel North, we entered into a hedge of approximately 50% of our anticipated zinc production from Chisel North at an average price of approximately US$1.01 per pound of zinc. This forward sale is intended to ensure that Chisel North remains economic at lower zinc prices while providing unfettered upside for the remaining 50% of production. Full production from the Chisel North mine was achieved in the second quarter of 2010 and, along with early zinc production from the ramp to the Lalor deposit, Chisel North is expected to provide a source of zinc feed to our Flin Flon zinc plant pending full production at Lalor.

Board and Executive Transition

Our previous board of directors resigned on March 23, 2009 following the resolution of a proxy contest initiated by a shareholder and on that date the current board of directors (as constituted at the time) was appointed. In connection with the board transition, Colin K. Benner resigned as Interim CEO and Peter R. Jones was appointed CEO. Mr. Benner had replaced Allen J. Palmiere, who resigned as CEO on March 9, 2009.

On November 12, 2009 we announced that Mr. Jones would be retiring, effective December 31, 2009, and our President and Chief Operating Officer, Michael D. Winship, was resigning from the Company. We also announced on that date that W. Warren Holmes had been appointed Executive Vice Chairman and, from January 1, 2010 to July 12, 2010, Mr. Holmes also served as Interim CEO.

Arrangement Agreement with Lundin Mining Corporation and Share Subscription

On November 21, 2008 we entered into an arrangement agreement (the “Arrangement Agreement”) with Lundin Mining Corporation (“Lundin”) pursuant to which we would have acquired all of the issued and outstanding common shares of Lundin. Also on November 21, 2008 we entered into a subscription agreement with Lundin whereby we agreed to acquire 96,997,492 common shares of Lundin at a price of $1.40 per share (the “Share

- 6 -

Subscription”), with aggregate gross proceeds to Lundin of $135.8 million. The Share Subscription was completed on December 11, 2008, and on its completion we held 19.9% of the issued and outstanding Lundin common shares.

On January 23, 2009 the Ontario Securities Commission (“OSC”) set aside a decision of the TSX granting conditional approval for the listing of the HudBay common shares to be issued as consideration pursuant to the Arrangement Agreement. The OSC determined in its decision that HudBay shareholder approval of the acquisition of Lundin was required as a condition to the listing of the additional common shares.

After the previous board concluded that we were not likely to receive the requisite shareholder approval, we entered into a termination agreement with Lundin (the “Termination Agreement”) on February 23, 2009, which provided for the termination of the Arrangement Agreement.

On May 26, 2009 we sold all of the Lundin shares we acquired in the Share Subscription for gross proceeds of approximately $236 million, representing a gain of approximately $100 million.

Acquisition of Skye Resources Inc.

On August 26, 2008, we acquired all of the issued and outstanding common shares of Skye Resources Inc. (“Skye”) on the basis of 0.61 of a HudBay common share plus $0.001 in cash for each Skye common share. In total, we issued approximately 31 million common shares at the completion of the transaction. We also exchanged Skye’s outstanding stock options and warrants for similar securities of HudBay at a corresponding exchange ratio. Skye, now our wholly-owned subsidiary, has since been renamed HMI Nickel Inc.

Skye’s primary asset is the Fenix project, a substantial nickel laterite deposit in eastern Guatemala. See “Description of Our Business – Development Properties – Fenix Project”.

Suspension of Balmat Operations

On August 22, 2008 we announced the suspension of operations at our Balmat zinc mine and concentrator until economic conditions warrant re-evaluation.

DESCRIPTION OF OUR BUSINESS

Principal Assets

We have the following principal assets:

| 1. | Operating Mines: three underground mines, including our 777 mine in Flin Flon, Manitoba, the Trout Lake mine near Flin Flon, and the Chisel North mine near Snow Lake, Manitoba; |

| 2. | Processing Facilities: ore concentrators in Flin Flon and Snow Lake and a zinc pressure leach and electro-winning plant in Flin Flon; |

| 3. | Development Projects: the Lalor project, a zinc, gold and copper deposit near our facilities in Snow Lake, Manitoba that is currently under construction, with full production expected by late 2014, the Constancia copper project in Peru, which we recently acquired through our acquisition of Norsemont, and the Fenix project, a substantial nickel laterite project in eastern Guatemala; |

| 4. | Joint Ventures: a joint venture with Aquila, pursuant to which we hold a 51% interest in the Back Forty project, an advanced stage exploration project evaluating a zinc and gold-rich VMS deposit in Michigan’s Upper Peninsula, and a joint venture with VMS Ventures, pursuant to which we hold a 70% interest in the copper-rich Reed Lake deposit, near Snow Lake; and |

| 5. | Exploration Properties: a land position of approximately 400,000 hectares in Manitoba and Saskatchewan, and other land holdings in Guatemala, Yukon, Chile and New York, all of which offer us the opportunity to develop and grow our business through our exploration program. |

- 7 -

In addition to our principal assets, we have: a zinc oxide plant in Brampton, Ontario with an annual production capacity of approximately 45,000 tonnes of zinc oxide, which purchases approximately 25% of our annual zinc metal production, and the Balmat mine and concentrator in Balmat, New York, which were placed on care and maintenance in August 2008. We closed our copper smelter in Flin Flon and White Pine copper refinery in Michigan in 2010.

Our cash and cash equivalents as of December 31, 2010 were $901.6 million, and are held in low risk liquid investments and deposit accounts pursuant to our investment policy.

Our Strategy

The key elements of our strategic plan are as follows: (i) optimize operations and grow our principal operating platform in northern Manitoba, including aggressively pursuing development of our Lalor project and continuing exploration in the Flin Flon Greenstone Belt; and (ii) grow beyond our Manitoba base, including through the development of the Constancia and Back Forty projects, and seeking acquisitions of VMS and porphyry deposits with exploration upside in mining friendly jurisdictions in the Americas.

The following map shows where our key assets and properties are located.

- 8 -

| 1. | Operating Mines |

777 Mine, Trout Lake Mine and Chisel North Mine

The technical and scientific information included in the following description of the northern Manitoba mines, including the estimated measured and indicated mineral resource and the estimated inferred mineral resource and the estimated mineral reserve for our producing properties have been prepared under the supervision of Robert Carter, P.Eng., who is employed by HBMS as Superintendent, Mines Technical Services and who is a Qualified Person under NI 43-101.

Location

Other than the Chisel North mine, our northern Manitoba mines are within six kilometers of Flin Flon. The Chisel North mine is approximately 215 kilometers east of Flin Flon, near Snow Lake. Flin Flon has a population of approximately 6,000 people, with an additional 3,000 people living in the surrounding community, and has well developed access to road, rail and air transportation.

The water supply for Flin Flon is taken from Trout Lake. Electrical power is supplied from the Manitoba Hydro and Saskatchewan Power Corporation power grids, which are fed by three hydroelectric generating stations. Our arrangement with Manitoba Hydro represents the single largest supply contract for our operations.

The geographical area has cool summers and very cold winters with a mean annual temperature of 0.6° C. The predominant vegetation is closed stands of black spruce and jack pine with a shrub layer of ericaceous shrubs and ground cover of mosses and lichens.

Geology

Our northern Manitoba mines are located within the Flin Flon Greenstone Belt in the Canadian Shield, one of the world’s largest exposed areas of Precambrian rocks. Within the Canadian Shield are large, deformed remnants of ancient volcanic-sedimentary terrain known as greenstone belts, which historically have been proven locations of base and precious metals.

The ore bodies of the Flin Flon Greenstone Belt occur in a highly prospective early Proterozoic island-arc assemblage that stretches for an exposed length of 250 kilometers east-west and 75 kilometers north-south. The deposits are copper-zinc VMS type, rich in gold and silver, hosted in both felsic and mafic volcanic rocks with the felsic type hosting the largest deposits. VMS ore bodies in the area have ranged in size from less than 100,000 tonnes to more than 60 million tonnes.

Exploration

Diamond drilling is the only drilling type carried out for the purposes of exploration, ore zone definition and sampling of our material properties. Drilling is done by drilling contractors under the supervision of our geologists.

Core recovered is placed in wooden core boxes covered with lids and transported to surface where it is logged by our geologists. Core from exploration holes outside the operating parts of the mine are generally reboxed and saved after logging. Core from holes for the purposes of orebody definition that is not sampled is discarded after logging.

Diamond drilling for the purpose of exploration within all operating mines during 2010 totalled 25,500 meters to test for extensions to orebodies. A further 31,000 meters of diamond drilling was conducted in our operating mines to define parts of the orebodies to provide adequate definition for the purpose of ore extraction. This diamond drilling was separate from exploration diamond drilling that was done for the testing and discovery of new mineral deposits on the surface of our exploration lands.

- 9 -

Drilling/Sampling and Analysis

Core recovery from diamond drilling is generally excellent and the drill cores are considered a reliable sampling media. Core size is generally NQ or BQ.

Core recovered from diamond drilling within our operating mines was logged and mineralized sections were marked for sampling and assaying by our geologists. The marked sections are either whole core sampled, placed in plastic bags and tagged with unique sample numbers, or sawn in half by a diamond saw and one half of the core placed in plastic bags and tagged with unique sample numbers, while the second half is returned to the core box and stored.

Each bagged core sample is placed in a plastic pail with a sample listing and sealed prior to being transported to our assay laboratory in Flin Flon, Manitoba where it is dried, crushed and pulverized and a 250 gram sample is prepared for assaying.

From each 250 gram sample 0.25 grams is removed and leached in aqua regia and analyzed by ICP-AES for Ag, Cu, Zn, As, Pb, Ni and Fe. Also from the 250-gram sample, 15 to 30 grams is removed for gold determination by fire assaying with Atomic Absorption finish.

Assaying integrity is monitored internally with a quality control program, which includes the use of assay sample standards, blanks, duplicates and repeats and externally through national and international programs. In addition, within each group of 50 core samples, one core sample has a second 250 gram split collected for external independent lab check assaying at Acme Analytical Laboratories Ltd. in Vancouver, B.C.

Core samples obtained from exploration diamond drilling on the surface of our exploration lands are processed in a similar way but differs in that all core samples are sawn in half and one check assay sample is collected from within each group of 20 core samples.

History

Through HBMS, we have operated in the Flin Flon Greenstone Belt for more than 80 years. During this period, we have mined approximately 145 million tonnes of ore.

Under the ownership of Minorco, S.A. in the mid-1990s, a strategic review of the northern Manitoba and Saskatchewan operations depicted a company with declining reserves, lower ore grades, rising costs and a poor safety record. At that time, it was concluded that a less than a 10-year mine life was possible and closure of operations before 2005 was planned.

In connection with the closure plan, it was decided to continue exploration efforts until 1998, the latest time an ore body could be developed for production prior to the planned closure. In 1993, based on the drilling program, the 777 deposit was first indicated by an underground exploration hole that intersected the mineralization at a depth of 1,000 meters. In 1995, a drilling program delineated the ore body and by 1997, this ore body was defined. In 1999, development of the 777 mine was commenced as part of the “777 Project” and commercial production from the mine commenced in January 2004. It was determined that the 777 ore body had the potential to extend operations to 2014 if a number of critical factors were first addressed. As a result, our northern Manitoba and Saskatchewan operations lowered their overall unit operating cost, improved safety performance and created a performance-oriented culture.

777 Mine

The 777 mine is an underground copper and zinc mine located immediately adjacent to our principal concentrator and zinc pressure leach plant in Flin Flon and straddles the Manitoba/Saskatchewan border. Development of the mine commenced in 1999 and commercial production began in 2004. It is part of a cluster of interlinked ore bodies including the prior Callinan mine and the prior Flin Flon mine.

- 10 -

The 777 mine property is located on Saskatchewan Mineral Leases and Manitoba Order in Council (“OIC”) leases totalling approximately 4,400 hectares, including approximately 1,100 hectares in Manitoba and approximately 3,300 hectares in Saskatchewan. HBMS owns a 100% interest in these mineral leases. Annual lease rentals payable to the Manitoba government are $16,730 and $1,600 to the Saskatchewan government. There is an annual work expenditure requirement for the Saskatchewan property of $257,025. Individual leases have different expiry dates that range from 2011 to 2031. All mineral production from the 777 mine property is subject to a 6 2/3% net proceeds of production and $0.25 per ton royalty agreement payable to Consolidated Callinan Flin Flon Mines Limited. Surface rights are held under several leases and permits that also host the concentrator and metallurgical plants.

The Flin Flon cluster of ore bodies, which encompasses the Flin Flon, Callinan and 777 ore bodies, is hosted by a sequence of volcanic flow and volcaniclastic rocks that are predominantly basaltic in nature. In the mine area, the mine horizon stratigraphic sequence lies on the west side of the Hidden Lake Syncline and strikes about 350 degrees and dips 50 to 60 degrees to the east.

The mine has an internal ramp system to allow movement between working levels and to the Callinan mine. The 777 shaft is a 6.7 meter diameter vertical shaft to a depth of 1,530 meters. Ore and waste hoisting is with a double-drum hoist with a capacity in excess of 1.35 million tonnes per year using 16-tonne skips. A separate double drum hoist operates a man and material cage and counterweight and a single drum hoist operates a small man cage.

Mining is primarily by long-hole open stoping. Paste backfill is used to fill mined stopes and is delivered from the Flin Flon concentrator by pumping through a network of lined boreholes and pipes. Pillars are left as regional support in addition to the backfill. The host country rock, particularly in the hanging wall, is competent.

Ventilation control is adequate, and the main shaft is the primary fresh air intake. Compressors supply compressed air. Pipes are installed to distribute the compressed air and water through the mine. The mine also has adequate electrical power for mining purposes.

The anticipated mine life is until 2020.

The following table sets forth the production of the 777 mine for the years ended December 31, 2010, 2009 and 2008.

777 Mine Historical Statistics

December 31 | ||||||||||||||

Units | 2010 | 2009 | 2008 | |||||||||||

Ore mined | 000s tonnes | 1,488.01 | 1,540.35 | 1,470.29 | ||||||||||

Zinc grade in ore | % | 4.01 | 4.35 | 4.36 | ||||||||||

Copper grade in ore | % | 2.89 | 2.49 | 2.61 | ||||||||||

Gold grade in ore | grams/tonne | 2.09 | 2.12 | 2.13 | ||||||||||

Silver grade in ore | grams/tonne | 25.89 | 26.39 | 24.82 | ||||||||||

777 North Expansion

The 777 North mine expansion was approved by our board of directors on August 4, 2010 and its development involves driving a ramp from surface to a depth of 440 meter to access mineral resources located in the north and east zones of the Callinan ore body. These zones are situated directly up plunge of the 777 ore body and are connected to underground workings of the 777 mine. Upon its completion, the 777 North mine expansion will provide an additional egress from the 777 mine and supply additional copper and zinc ore feed to the Flin Flon concentrator. It will also provide an underground exploration platform to enable the evaluation of additional exploration opportunities near the 777 mine.

- 11 -

The 777 North mine expansion is located entirely within the associated 777 mine property and is covered by 777’s Saskatchewan Mineral Leases and Manitoba OIC leases.

Development of the portal, which is located adjacent to the HBMS metallurgical plant area, began in August and the first underground blast occurred on October 12, 2010. The ramp had advanced a total of 265 meters as of December 31, 2010.

Production is expected to begin in 2012 at a rate of 330 tonnes per day.

Trout Lake Mine

The Trout Lake mine is an underground zinc and copper mine located approximately six kilometers northeast of Flin Flon.

The Trout Lake mine is located on Manitoba mineral leases that total approximately 2,240 hectares and expire April 1, 2013. Annual mineral lease payments total approximately $19,000. HBMS owns a 100% interest in these leases. There are no royalties payable other than those potentially payable to the Province. Surface rights are held under miscellaneous leases and general permits with total annual rental payments of $5,150.

The Trout Lake mine was discovered by Granges Exploration in the 1970s, as a result of testing by drilling an electromagnetic geophysical target located in an area beneath Trout Lake believed to be underlain by felsic volcanic rocks similar to those that host the Flin Flon ore bodies. Commercial production commenced at the Trout Lake mine in 1982.

The Trout Lake ore body sub-crops beneath Trout Lake and contains more than 30 lenses in several zones. The lenses dip approximately 60 degrees and the average lens width is eight meters. The ore body is a proximal volcanic massive sulphide deposit. Chalcopyrite and sphalerite are the main base metal sulphides and occur with pyrite in massive sulphide layers.

The main shaft has been sunk to a depth of 1,091 meters. The mine development includes a number of inclined ramps and steeply inclined ventilation shafts and ore passes. The shaft is a circular two-compartment 4.9 meter diameter vertical shaft operating to a depth of 1,091 meters. The ramp extends to approximately 1,460 meters below surface at an inclination of 15% from the horizontal. A 762 meter long inclined conveyor delivers the ore from the underground crusher to the ore bin adjacent to the shaft.

Mining is by longhole open stoping using trackless equipment. Crushed ore is trucked from the mine site to the Flin Flon concentrator for processing.

The anticipated mine life is until the fourth quarter of 2011.

The following table sets forth the production of the Trout Lake mine for the years ended December 31, 2010, 2009 and 2008.

Trout Lake Mine Historical Statistics

| December 31 | ||||||||||||||

| Units | 2010 | 2009 | 2008 | |||||||||||

Ore mined | 000s tonnes | 540.64 | 679.33 | 776.21 | ||||||||||

Zinc grade in ore | % | 2.67 | 3.10 | 3.70 | ||||||||||

Copper grade in ore | % | 2.35 | 1.96 | 1.93 | ||||||||||

Gold grade in ore | grams/tonne | 1.30 | 1.30 | 1.38 | ||||||||||

Silver grade in ore | grams/tonne | 12.03 | 15.72 | 19.21 | ||||||||||

- 12 -

Chisel North Mine

The Chisel North mine is an underground zinc mine located 15 kilometers west of the Snow Lake concentrator and about six kilometers south of the town of Snow Lake, Manitoba, which is approximately 215 kilometers from Flin Flon. The mine and concentrator were placed on care and maintenance in January 2009 due to depressed base metal prices related to the global economic downturn. The mine returned to full production in the second quarter of 2010.

The Chisel North mine is located on Manitoba OIC leases that total approximately 4,193 hectares with annual rental payments payable to the Manitoba government of $53,343. HBMS holds a 100% interest in these leases. Most of these mineral leases terminate in 2023. There are no royalties payable other than those potentially payable to the Province. Surface rights are held under miscellaneous leases, surface leases and general permits with total annual rentals of $15,271.

In 1986, an exploration program was initiated to systematically explore the Chisel basin. Additional drilling was carried out between 1993 and 1997 to suitably define the ore body for a feasibility study. A total of 77,632 meters in 130 holes and wedges were drilled by 1998. Commercial production commenced at the Chisel North mine in June, 2000.

The deposit consists of metamorphosed massive sulphides overlain by barren basalt volcanic flows. Sphalerite and minor amounts of chalcopyrite are the main base metal sulphides and occur with pyrite in massive sulphide layers conformable to stratigraphy. The Chisel North mine mineral reserves only consisted of zinc ore until this year when copper and gold mineralization, located downplunge to the north and northwest of Lens 1, were estimated separate to the zinc mining areas. The mineral reserves are between 400 meter and 650 meter depths in four stacked zinc rich sulphide lenses.

The mine depth is to the 687 meter level. Mining is by room and pillar, post pillar cut and fill and blast hole stoping using trackless equipment with unconsolidated rock fill as backfill. Ore is truck hauled to surface for crushing. The zinc ore is trucked to the Snow Lake concentrator while the copper ore is trucked to the Flin Flon concentrator by independent trucking contractors.

HBMS commissioned a 2,000 US gpm water treatment plant in the spring of 2008 at Chisel Lake, approximately four kilometers from Chisel North mine. The treatment plant operates at 1,000 US gpm (peak 1,600 US gpm) to treat Chisel North mine discharge water and water from the Chisel Lake open pit. Treated water is discharged to the environment south of the Chisel Lake open pit.

Manitoba Hydro services the Chisel Lake mine with a 110 kV overhead transmission line. Voltage is stepped down to 6,000 V using an HBMS-owned substation at the termination of the Manitoba Hydro line. Power from the main substation is stepped up to 21 kV using a modern substation and is fed to the Chisel North minesite via a four kilometer long overhead transmission line.

The following chart sets forth the production of the Chisel North mine for the years ended December 31, 2010, 2009 and 2008. A small amount of copper ore was mined in 2010 and 2009 and is not included in the table below. Production for 2010 is based on mining from March to the end of the year and production for 2009 was from January and February prior to the mine being placed on care and maintenance.

The anticipated mine life is until the second quarter of 2012.

Chisel North Mine Zinc Historical Statistics

| December 31 | ||||||||||||||

| Units | 2010 | 2009 | 2008 | |||||||||||

Ore mined | 000s tonnes | 213.64 | 48.69 | 325.16 | ||||||||||

Zinc grade in ore | % | 7.30 | 9.18 | 7.42 | ||||||||||

- 13 -

Mineral Reserves and Inferred Mineable Resources

In-Mine Mineral Reserves – January 1, 2011 (1)(2)(3)

| Tonnes | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | ||||||||||||||||

777 Mine | ||||||||||||||||||||

Proven | 4,516,000 | 2.27 | 29.38 | 2.87 | 4.44 | |||||||||||||||

Probable | 8,307,000 | 1.79 | 27.31 | 1.78 | 4.24 | |||||||||||||||

777 North | ||||||||||||||||||||

Proven | 81,000 | 1.61 | 26.52 | 0.68 | 4.89 | |||||||||||||||

Probable | 449,000 | 1.44 | 21.48 | 1.09 | 3.31 | |||||||||||||||

Trout Lake Mine | ||||||||||||||||||||

Proven | 409,000 | 2.06 | 9.66 | 2.10 | 3.53 | |||||||||||||||

Probable | 36,000 | 1.17 | 1.01 | 2.18 | 1.43 | |||||||||||||||

Chisel North Mine - Zinc | ||||||||||||||||||||

Proven | 164,000 | — | — | — | 8.77 | |||||||||||||||

Probable | 56,000 | — | — | — | 10.60 | |||||||||||||||

Chisel North Mine - Copper | ||||||||||||||||||||

Proven | — | — | — | — | — | |||||||||||||||

Probable | 92,000 | 2.41 | 31.56 | 1.72 | 3.67 | |||||||||||||||

Total Proven | 5,170,000 | |||||||||||||||||||

Total Probable | 8,940,000 | |||||||||||||||||||

Total Mineral Reserve | 14,110,000 | |||||||||||||||||||

Notes:

| (1) | This table shows the estimated reserves at our producing properties in Manitoba. To estimate mineral reserves, measured and indicated mineral resources were first estimated in a 12-step process, which includes determination of the integrity and validation of the data collected, including confirmation of specific gravity, assay results and methods of data recording. The process also includes determining the appropriate geological model, selection of data and the application of statistical models including probability plots and restrictive kriging to establish continuity and model validation. The resultant estimates of measured and indicated mineral resources are then converted to proven and probable mineral reserves by the application of mining dilution and recovery, as well as the determination of economic viability using full cost analysis. Other factors such as depletion from production are applied as appropriate. |

| (2) | The zinc price used for mineral reserve estimation was US$1.00 per pound, the copper price was US$2.50 per pound, the gold price was US$900 per ounce and the silver price was US$15 per ounce using an exchange of 1.10 C$/US$. |

| (3) | The estimate as at January 1, 2011 was prepared in accordance with NI 43-101 and the Canadian Institute on Mining, Metallurgy and Petroleum CIM Standards on Mineral Resources and Reserves: Definitions and Guidelines. |

In-Mine Inferred Mineral Resources – January 1, 2011(1)

| Tonnes | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | ||||||||||||||||

777 Mine | 1,326,000 | 1.91 | 34.40 | 1.25 | 5.21 | |||||||||||||||

777 North Mine | 67,000 | 1.49 | 20.32 | 1.02 | 3.47 | |||||||||||||||

Trout Lake Mine | — | — | — | — | — | |||||||||||||||

Chisel North Mine – Zinc | 28,000 | — | — | — | 6.44 | |||||||||||||||

Chisel North Mine – Copper | — | — | — | — | — | |||||||||||||||

Total Resources | 1,421,000 | |||||||||||||||||||

Notes:

| (1) | This table shows our estimated inferred mineral resources at our material mining properties in Manitoba. Estimated inferred mineral resources within our mines were estimated by a similar 12-step process, used to estimate measured and indicated resources. The inferred mineral resources contained in our mines have had dilution and recovery applied and were economically tested using the same full cost analysis and long term metal prices as those used for the estimation of the mineral reserves. |

- 14 -

| 2. | Processing Facilities |

Concentrators

Our primary ore concentrator is located in Flin Flon, Manitoba. The concentrator, which is directly adjacent to our metallurgical zinc plant, produces zinc and copper concentrates from ore mined at our 777 and Trout Lake mines. Its capacity is approximately 2.18 million tonnes of ore per year and in 2010, 2.25 million tonnes of ore were milled. The concentrator can handle ore from each mine separately, and blending is done at the grinding stage. The Flin Flon concentrator facility includes a paste backfill plant and associated infrastructure such as maintenance shops and laboratories. In 2010 we completed a copper concentrate filtration plant and other facilities to allow for the shipping of the copper concentrate we produce. Tailings from the concentrator are pumped to the Flin Flon tailings impoundment immediately adjacent to the concentrator.

Our concentrator in Snow Lake, Manitoba was re-started in the first half of 2010 after being placed on care and maintenance in January 2009. The concentrator processes zinc ore from the Chisel North mine and produces zinc concentrate, which is shipped by truck for processing at the zinc plant in Flin Flon. The concentrator, which has crushing, grinding, flotation, thickening, filtering and drying capabilities, has a capacity of approximately 1.2 million tonnes of ore per year and could be refurbished to allow ore produced from Lalor to be milled at the concentrator. Tailings generated by the Snow Lake concentrator are deposited in our Anderson Lake tailings facility, which we believe mitigates environmental concerns, as the tailings are deposited in a subaqueous manner, minimizing the potential for generation of acid rock drainage.

We also have a concentrator in Balmat, New York, which processed zinc ore produced from our Balmat mine. The Balmat mine and concentrator were placed on care and maintenance on August 22, 2008.

Zinc Plant

Our zinc plant located in Flin Flon, Manitoba produces special high-grade zinc metal in three cast shapes from zinc concentrate. Our plant is one of three primary zinc producers in North America. We produced 110,283 tonnes of cast zinc in 2010. The capacity of the zinc plant is approximately 115,000 tonnes of cast zinc per year, and an additional approximate 15% expansion is possible at comparatively low capital investment. Included in the zinc plant are an oxygen plant, a concentrate handling, storage and regrinding facility, a zinc pressure leach plant, a solution purification plant, a modern electro-winning cell house, a casting plant and a zinc storage area with the ability to load trucks or rail cars. The zinc plant has a dedicated leach residue disposal facility. The bulk of the waste material is gypsum, iron and elemental sulphur. Wastewater is treated and recycled through the zinc plant.

Both domestic concentrate produced from our mines and concentrate purchased from third parties are processed at the zinc plant. Purchased concentrate accounted for 26% of zinc metal produced at our zinc plant in 2010. The zinc plant currently has excess capacity beyond our domestic concentrate production and we intend to utilize this capacity by purchasing concentrate and advancing our development projects, including Lalor, to production.

Zochem

Zochem is our zinc oxide production facility, and is located in Brampton, Ontario. Zochem has the capacity to off-take approximately 37,000 tonnes (or approximately 25% of our production) of our zinc metal per year, having the potential to buffer our production schedules and inventories against the impact of zinc market cyclicality. Zochem is the third largest producer of zinc oxide in North America, accounting for approximately 20% of the North American market.

The Zochem facility has a total capacity of approximately 45,000 tonnes per year of zinc oxide. In 2010, Zochem produced approximately 41,000 tonnes of zinc oxide.

- 15 -

Copper Smelter

Due in part to the anticipated costs of compliance with pending emissions reduction targets and increasingly competitive market conditions for copper smelting operations, we closed our copper smelter in Flin Flon in June, 2010.

White Pine Copper Refinery

White Pine, which is located in the western Upper Peninsula of Michigan, processed our copper anode from the copper smelter into refined copper cathode with the recovery of precious metals in a saleable slimes product. In connection with the closure of our copper smelter, we closed the White Pine refinery in the third quarter of 2010.

| 3. | Development Properties |

Lalor Project

The technical and scientific information included in the following description of the Lalor project, including the estimated mineral reserves and mineral resources, and the estimated tonnes and grade of the gold zone and copper-gold zone, have been prepared under the supervision of Robert Carter, P.Eng., who is employed by HBMS as Superintendant, Mines Technical Services and who is a Qualified Person under NI 43-101. On November 20, 2009, we filed a NI 43-101 compliant technical report entitled “Technical Report, Lalor Deposit, Snow Lake, Manitoba, Canada”, dated October 8, 2009, which is available at www.sedar.com.

Project Description and Location

Lalor is a zinc, copper and gold project currently under construction near the town of Snow Lake in the province of Manitoba. Lalor is located approximately 210 km by road east of Flin Flon, Manitoba of which 197 km is paved highway. The project is three kilometers to the northwest of our Chisel North mine.

We own a 100% interest in the property through five claims and eight mineral leases that total approximately 916 hectares with annual rental payments payable to the Manitoba government of $1,742. Application has been submitted to convert the claims to a mineral lease which has an initial term of 21 years. The mineral leases terminate in April and September 2023. There is no royalties payable other than those potentially payable to the province. Surface rights are held under miscellaneous leases, surface leases and general permits with total annual rentals of $145.

An underground production ramp from HudBay’s Chisel North mine to the Lalor deposit began in December 2009. The ramp is expected to provide early production of zinc rich ore and access to the gold zones for additional underground exploration. A ventilation raise bore driven from surface provides fresh air for the ramp development. As of February 20, 2011 a total of 1,709 meters of ramp was excavated from a planned length of approximately 2,750 meters. On August 4, 2010, HudBay’s board of directors made a full commitment to the development of the Lalor project by authorizing the expenditures necessary to put the project into full production.

We undertook fast-track prefeasibility work on early 2010 and completed an updated prefeasibility study in February 2011.

Accessibility, Climate, Local Resources, and Infrastructure

The project infrastructure includes a four kilometer main access road that was constructed in 2010 from provincial road 395 and provides access from the Chisel North mine site and Lalor site. This road will also serve as the route for the electrical power lines, the fresh water supply line, and the mine discharge water line between Lalor and the Chisel North sites. Access to the site is off of paved provincial highway 392 which runs to Snow Lake and provides access to Flin Flon.

- 16 -

The Snow Lake area has a typical mid-continental climate, with short summers and long, cold winters. Climate generally has only a minor effect on local exploration and mining activities. The project areas is approximately 300 meters above sea level, consisting of ridged to hummocky sloping rocks with depressional lowlands, and has gentle relief that rarely exceeds 10 meters. The area of Lalor and surrounding water bodies (Snow, File, Woosey, Anderson and Wekusko lakes) are located in the Churchill River Upland Ecoregion in the Wekusko Ecodistrict. The dominant soils are well to excessively drained dystic brunisols that have developed on shallow, sandy and stony veneers of water-worked glacial till overlying bedrock. Significant areas consist of peat-filled depressions with very poorly drained Typic and Terric Fibrisolic and Mesisolic Organic soils overlying loamy to clayey glaciolacustrine sediments.

The Chisel North concentrator and Anderson Lake tailings facilities are 18 kilometers from Lalor. See “Processing Facilities – Concentrators”.

HBMS operates a mine water pump station for the Chisel North mine at the north end of Chisel Lake approximately three kilometers from Lalor. In addition, HBMS commissioned a 2,000 US gpm water treatment plant in the spring of 2008 at Chisel Lake, approximately seven kilometers by road from Lalor.

Power for the site construction is currently being transmitted at 25 kV using a modern substation at the Chisel North Mine site via a four kilometer long overhead transmission line.

Process water required for the office, shop, hoist house and underground operation is estimated to be 45 to 50 m3/hr. The process water will be drawn through existing pump stations located at Chisel Lake and Ghost Lake which are currently supplying process water to Chisel North mine. Each pump station has a capacity of supplying 68 m3/hr.

Work on the project components of ventilation and shaft sinking and site construction is currently being done by specialized contractors with contracts in place. As of the end of 2010, 11 permanent employees were on staff and 88 construction contractors were on site. A 196 person temporary Lalor project construction camp was mobilized and installed in the Town of Snow Lake in the fall of 2010 to accommodate the project construction crew.

Personnel requirements for the mine will largely be drawn from the immediate area where there is a history of operating mines and commencement of operations at Lalor is expected to coincide with the shutdown of our Chisel North mine. We believe there are sufficient skilled operating, maintenance and technical personnel available to bring Lalor to its planned full production. Lalor mine in full operation will require approximately 300 employees and 72 employees for the Snow Lake concentrator.

History

Exploration in the Chisel Basin has been active since 1955. The Chisel Basin area has hosted three producing mines, namely, Chisel Lake, Chisel Open Pit and Chisel North. All three mines have very similar lithological and mineralogical features. This basin is also the host of the Lalor deposit.

A Crone Geophysics survey in 2003 indicated a highly conductive shallow-dipping anomaly at a vertical depth of 800 meters. In early 2007, drill hole DUB168 was drilled almost vertically to test the anomaly and intersected a band of conductive mineralization between 781.74 m and 826.87 m (45.13 m). Assay results include 0.30% Cu and 7.62% Zn over the 45.13 meters, including 0.19% Cu and 17.26% Zn over 16.45 meters. Drilling at Lalor has been continuous since the discovery of mineralization on the property.

Regional Geology

The Lalor property lies in the eastern (Snow Lake) portion of the Paleoproterozoic Flin Flon Greenstone Belt and is overlain by a thin veneer of Pleistocene glacial/fluvial sediments. Located within the Trans-Hudson Orogen, the Flin Flon Belt consists of a variety of distinct 1.92 to 1.87 Ga tectonostratigraphic assemblages including juvenile arc, back-arc, ocean-floor and ocean-island and evolved volcanic arc assemblages that were amalgamated to form an accretionary collage (named the Amisk Collage) prior to the emplacement of voluminous intermediate to granitoid plutons and generally subsequent deformation. The volcanic assemblages consist of mafic

- 17 -

to felsic volcanic rocks with intercalated volcanogenic sedimentary rocks. The younger plutons and coeval successor arc volcanics, volcaniclastic, and sedimentary successor basin rocks include the older, largely marine turbidites of the Burntwood Group and the terrestrial metasedimentary sequences of the Missi Group.

Local and Property Geology

The Snow Lake arc assemblage that hosts the producing and past-producing mines in the Snow Lake area is a 20 kilometers wide by 6 kilometers thick section that records a temporal evolution in geodynamic setting from ‘primitive arc’ (Anderson sequence to the south) to ‘mature arc’ (Chisel Basin sequence) to ‘arc-rift’ (Snow Creek sequence to the northeast). The ‘mature arc’ Chisel Basin sequence that hosts the zinc rich Chisel, Ghost, Chisel North, and Lalor deposits typically contains thin and discontinuous volcaniclastic deposits and intermediate to felsic flow-dome complexes.

The Lalor deposit is similar to other massive sulphide bodies in the Chisel Basin sequence (Chisel Lake, Ghost Lake and Chisel North), and lies along the same stratigraphic horizon as the Chisel Lake and Chisel North deposits. It is interpreted that the top of the zone is near a decollement contact with the overturned hanging wall rocks.

Mineralization

Lalor is interpreted as a VMS deposit that precipitated at or near the seafloor in association with contemporaneous volcanism, forming a stratabound accumulation of sulphide minerals. VMS deposits typically form during periods of rifting along volcanic arcs, fore arcs, and in extensional back arc basins. Rifting causes extension and thinning of the crust, providing the high heat source required to generate and sustain a high-temperature hydrothermal system.

The location of VMS deposits is often controlled by synvolcanic faults and fissures, which permit a focused discharge of hydrothermal fluids. A typical deposit will include the massive mineralization located proximal to the active hydrothermal vent, footwall stockwork mineralization, and distal products, which are typically thin but extensive. Footwall, and less commonly, hanging wall semiconformable alteration zones are produced by high temperature water-rock interactions.

The depositional environment for the mineralization at Lalor is similar to that of present and past producing base metal deposits in felsic to mafic volcanic and volcaniclastic rocks in the Snow Lake mining camp. The deposit appears to have an extensive associated hydrothermal alteration pipe.

The Lalor VMS deposit is flat lying, with zinc mineralization beginning at approximately 570 meters from surface and extending to a depth of approximately 1,160 meters. The mineralization trends about 310° to 320° azimuth and dips between 20° and 30° to the north. It has a lateral extent of about 920 meters in the north-south direction and 710 meters in the east-west direction.

Sulphide mineralization is pyrite and sphalerite. In the near solid (semi-massive) to solid (massive) sulphide sections, pyrite occurs as fine to coarse grained crystals ranging one to six millimeters and averaging two to three millimeters in size. Sphalerite occurs interstitial to the pyrite. A crude bedding or lamination is locally discernable between these two sulphide minerals. Near solid coarse grained sphalerite zones occur locally as bands or boudins that strongly suggest that remobilization took place during metamorphism.

Notable gold and silver rich zones have also been intersected outside the current zinc rich base metal mineral resources on the property. The precious metal mineralization begins at approximately 720 meters from surface and extends to a depth of approximately 1,390 meters. The mineralization trends about 310° to 330° azimuth and dips between 20° to 25° to the north. The precious metal zones have lateral extents of 1,060 meters in the north-south direction and 460 meters in the east-west direction.

Gold and silver enriched zones occur near the margins of the sulphide lenses and in local silicified footwall alteration. These silicified areas often correlate with disseminated to stringer chalcopyrite and galena, whether together or independent of each other. This association has been confirmed in thin section.

- 18 -

Six distinct stacked zinc rich mineralized zones and five stacked gold lenses or zones of low sulphide either in contact with or entirely separate to the zinc rich base metal resources were interpreted. The interpreted gold zones are generally co-paralleled and/or separate to the zinc rich base metal mineral resource zones. However, gold and potential gold zones locally merge, overlap and cut through zinc rich base metal resources.

The potential gold zones remain open down plunge to the north.

Exploration and Drilling

Exploration in the Lalor deposit area is conducted by HBED. A field office, including core logging and storage facilities, is situated at the HBMS Snow Lake concentrator site.

Time-domain borehole EM surveys with three dimensional probes are routinely conducted on drill holes. The survey results identify any off-hole conductors that have been missed and indicate direction to the target as well as the dimensions and the attitude of the conductor. The survey also may detect any possible conductors which lie past the end of the hole allowing the geologist to know whether or not the hole should be deepened.

Recent exploration drilling at Lalor has focused on exploration of the recently discovered copper-gold zone, in-fill drilling at the potential gold zone and testing targets peripheral to the Lalor deposit.

As of December 31, 2010, 121 parent and 96 wedge holes, amounting to 248,265 meters of drilling, has been conducted on the property.

All diamond drilling was completed from surface retrieving whole core sizes of BQ and NQ. Wedge offsets and associated directional drilling were completed on parent holes, resulting in time and cost savings over drilling a new hole from surface. Wedging and directional drilling were used at Lalor for acquiring metallurgical sample and delineation purposes. For delineation purposes, wedge offsets are oriented towards specific targets selected by the geologists along a path calculated by the directional drilling technicians. In metallurgical sampling wedge offsets are unoriented and the wedge is set just above the zone that is to be sampled such that the core sample collected is generally within 10 to 20 meters of the parent hole intersection.

Core recovery at Lalor is near 100% on all holes and all the diamond drilling at Lalor was conducted by Major Drilling Inc.

Sampling, Analysis and Security of Samples

Bagged samples are delivered to our Flin Flon assay laboratory and after preparation the samples are delivered to Acme Analytical Laboratories in Vancouver for analysis. Base metals and silver assaying is completed by aqua regia digestion and read by a simultaneous ICP unit. Gold analysis conducted at our Flin Flon laboratory is completed by atomic absorption spectrometry and gold analysis conducted by Acme is completed on ICP after fire assay lead collection. Samples greater than 10 g/t are re-assayed using a gravimetric finish. Assaying integrity is monitored internally with a quality control program which includes the use of assay sample standards, blanks, duplicates and repeats. In addition, within each group of 20 core samples, one sample is check assayed at a different laboratory.

Security measures taken to ensure the validity and integrity of the samples collected are handled in a professional manner and consistent with industry standards for base metal deposits.

Mineral Resource and Conceptual Estimates

The mineral resource and conceptual estimates are effective as of a May 1, 2010 cut-off date for diamond drilling, which includes a total of 95 parent and 76 wedge offsets drilled from surface on the Lalor property. The zinc rich base metal estimate was completed using MineSight 5.00-03 block modeling software in UTM NAD83 coordinates (MineSight). The block model was constrained by interpreted 3D wireframes of the zinc rich base metal mineralized zones. Gold, silver, copper, zinc, lead, and iron grades and specific gravity were estimated into blocks using Ordinary Kriging (OK) interpolation. Zone intersections were selected based on a minimum 4% Zinc

- 19 -

Equivalency formula (ZNEQ) over a two meter core length. The ZNEQ was calculated from metal price and metal recovery assumptions, with economic contributions from gold, silver, copper and zinc. Each block was assigned a ZNEQ.

The gold estimate was completed using MineSight in UTM NAD83 coordinates. The block model was constrained by interpreted 3D wireframes of the gold mineralized zones. A 1.0 g/t gold cut-off over a two meter core length was used to determine the zone outlines for continuity purposes to build the 3D wireframes. Gold, silver, copper, zinc, lead, and iron grades and specific gravity were estimated into blocks using either Inverse Distance Squared Weighted or OK interpolation.

In order to avoid any disproportionate influence of random, anomalously high grade assays on the estimated average metal grade, histograms, cumulative frequency log probability charts, cutting curves, and decile analysis charts were created to examine the assay grade distribution and assess the need for grade capping.

The zinc rich mineral resources are classified on the basis of the model blocks to the nearest composite, minimum number of composites, and minimum number of drill holes that contribute to the interpolation at the 4% ZNEQ cut-off. The gold resources and conceptual estimates are classified on the basis of the model blocks to the nearest composite, continuity and variability of the gold mineralization at the 1.0 g/t cut-off. Potential gold and copper-gold estimates are conceptual in nature and to date there has been insufficient exploration to define a mineral resource compliant with NI 43-101. It is uncertain if further exploration will result in the target deposit being delineated as a mineral resource.

Summary of Zinc Rich Mineral Resource – May 1, 2010

Category | Tonnes (Millions) | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | |||||||||||||||

Indicated | 13.3 | 1.6 | 24.9 | 0.66 | 8.87 | |||||||||||||||

Inferred | 4.8 | 1.3 | 26.2 | 0.58 | 9.25 | |||||||||||||||

Summary of Gold Mineral Resource – May 1, 2010

Category | Tonnes (Millions) | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | |||||||||||||||

Inferred | 5.4 | 4.7 | 30.6 | 0.47 | 0.46 | |||||||||||||||

Notes:

| (1) | CIM definitions were followed for the mineral resources. |

| (2) | Zinc rich base metal mineral resources are estimated at ZNEQ cut-off of 4% (ZNEQ% equals Zn% + Cu% x 2.352 + Au g/t x 0.867 + Ag g/t x 0.014) and a minimum two meter true width. |

| (3) | Gold zone mineral resources are estimated at a 1.0 g/t gold cut-off and a minimum two meter true width. |

| (4) | Long term $US metal prices of $700/oz gold, $12.00/oz silver, $2.00/lb copper and $0.85/lb zinc were used for the estimation of ZNEQ. |

| (5) | Metal recovery assumptions of 65% gold, 60% silver, 90% copper and 90% zinc were used for the estimation of ZNEQ. |

| (6) | Specific gravity measurements were taken on a large portion of the samples. Where actual measurements were not available stoichiometric values were calculated. |

Summary of Potential Gold Conceptual Estimate – May 1, 2010

Tonnes (Millions) | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | ||||

5.1 – 6.1 | 4.3 – 5.1 | 23 – 27 | 0.2 – 0.4 | 0.2 – 0.4 |

- 20 -

Summary of Potential Copper-Gold Conceptual Estimate – May 1, 2010

Tonnes (Millions) | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | ||||

1.8 – 2.2 | 5.8 – 7.0 | 18 – 22 | 3.2 – 4.0 | 0.2 – 0.3 |

Mineral Reserves

The mineral reserves at Lalor are estimated from the indicated zinc-rich mineral resources as shown above and are inclusive of those mineral resources modified to produce the mineral reserves shown below. Mineral reserves are based on an updated prefeasibility study completed by HudBay in February 2011 that provides the basis for an economic project. The updated prefeasibility study includes: re-calculated mineral resource model incorporating the 2009/2010 winter diamond drilling program, detailed calculation of dilutions and recoveries per mining area, completion of trade off studies for mine backfill, mine ore haulage and milling options, paste backfill requirement, detailed capital and operating cost estimates for refurbishing the Snow Lake concentrator. The mineral reserve also accounts for relevant economic, marketing, legal, environment and socio-economic factors.

Lalor Probable Mineral Reserves – January 1, 2011(1)

Tonnes (Millions) | Au (g/t) | Ag (g/t) | Cu (%) | Zn (%) | ||||

10.5 | 1.6 | 21.0 | 0.64 | 8.31 |

Notes:

| (1) | The zinc price used for mineral reserve estimation was US$1.00 per pound, the copper price was US$2.50 per pound, the gold price was US$900 per ounce and the silver price was US$15 per ounce using an exchange of 1.10 C$/US$. |

Metallurgical Testing

Lalor mineralization is typical of the polymetallic base metal ores in the Chisel Basin, containing gold, silver, copper, zinc and lead. The previous fast track prefeasibility study was completed using preliminary metallurgical information. During 2010, grind optimization, reagents selection, locked cycle testwork and locked cycle variability testwork were completed to support the metallurgical process selection, recoveries and concentrate grades. The mineralization is mostly coarse grained and exhibits a high degree of liberation at a relatively coarse grind. The high degree of mineralization has led to good concentrates grades and copper and zinc recoveries for the Lalor deposit.

Mining

Current mine planning is based on underground mining of the probable reserves from the two principal base metal zones: the zinc rich Zone 10 and the zinc rich with elevated copper and gold Zone 20. The planned production rate is 3,500 tonnes per day. The total expected mine life is 11 years, which includes a three year ramp up to full production.

Lalor reserves will be accessed from footwall access drifts off the main ramp. Mining is by post pillar cut and fill with a combination of paste and unconsolidated waste backfill. The underground ore handling system will be done by truck to an ore pass with rock breaker and grizzly dump, hoisted to surface via a 6.7 meter diameter shaft and trucked hauled to the Snow Lake mill for crushing and concentrating. The Lalor shaft is based on the 777 shaft design and is designed to a planned vertical depth of 995 meters.

The refurbished Snow Lake concentrator is planned to have two circuits, producing copper and zinc concentrates. Concentrates will be shipped to Flin Flon where the zinc concentrates are processed at our zinc plant and copper concentrates will be loaded onto rail cars and sent to third party smelters.

Based on current planning, the Snow Lake concentrator will include a tailings plant producing a dewatered filter cake for the paste backfill system.

- 21 -

Permitting and Environmental

General permit GP59093 was originally granted to HBED in 2007 for the construction of an exploration road to service the exploration drill activities. HBMS held a Quarry Lease (QL-1928) and this quarry provided a source of roadbed material for the exploration road.

We received an Advanced Exploration Permit approval in April 2010 from the Manitoba government which allows us to upgrade the existing exploration road, construct an exploration shaft and related facilities, develop an underground exploration platform, and extract up to a 10,000 tonne sample from the gold and copper-gold zones for metallurgical testing.

In 2010, additional permits were granted to HBMS to enable road construction and other site construction. Before the Lalor project can move into full mine production an Environmental Act Licence must be received. Mine site planning, engineering components and baseline environmental field studies are now complete to a stage which will enable us to proceed with an Environment Act licence application.

Recent Activities and Development Plans

Since the advanced exploration permit approval, construction at the Lalor site has started and is accelerating in support of the project activities. The access road to the site is complete, the main surface exhaust raise site has been cleared and construction on the 6.1 meter ventilation raise has been started. All power poles for the site have been installed and the line wiring is ongoing. Water lines for process water and discharge water are being placed and civil work on the pump stations is underway.