UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K

CURRENT REPORT

Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): April 1, 2013

| Eagle Bulk Shipping Inc. |

(Exact name of registrant as specified in its charter) |

| Republic of the Marshall Islands | 001-33831 | 98-0453513 |

(State or other jurisdiction of incorporation or organization) | (Commission File Number) | (IRS employer identification no.) |

| | | |

477 Madison Avenue New York, New York | | 10022 |

| (Address of principal executive offices) | | (Zip Code) |

(Registrant's telephone number, including area code): (212) 785-2500

(Former Name or Former Address, if Changed Since Last Report): None

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

[_] Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425)

[_] Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12)

| [_] | Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

| [_] | Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 2.02. Results of Operations and Financial Condition

On April 1, 2013, Eagle Bulk Shipping Inc. (the "Company") issued a press release (the "Press Release") relating to its financial results for the fourth quarter and fiscal year ended December 31, 2012.

In accordance with General Instruction B.2 to the Form 8-K, the information under this Item 2.02 and the Press Release, attached hereto as Exhibit 99.1, shall be deemed to be "furnished" to the Securities and Exchange Commission (the "SEC") and not be deemed to be "filed" with the SEC for purposes of Section 18 of the Securities Exchange Act of 1934, as amended, or otherwise subject to the liabilities of that section.

Item 8.01. Other Events

On April 2, 2013, the Company posted on its website, www.eagleships.com, under the section entitled "Investors - Webcasts & Presentations" a presentation dated April 2, 2013 of its financial results for the fourth quarter and fiscal year ended December 31, 2012. A copy of the presentation is hereby furnished to the SEC and is attached as Exhibit 99.2.

Item 9.01. Financial Statements and Exhibits

(d) Exhibits

| |

| Press Release dated April 1, 2013. |

| Financial Presentation dated April 2, 2013 |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned hereunto duly authorized.

| | EAGLE BULK SHIPPING INC. |

| | (registrant) |

| | |

| Dated: April 2, 2013 | By: | /s/ Adir Katzav |

| | Name: | Adir Katzav |

| | Title: | Chief Financial Officer |

EXHIBIT INDEX

| Exhibit No. | Description |

| 99.1 | Press Release dated April 1, 2013. |

| 99.2 | Financial Presentation dated April 2, 2013 |

Exhibit 99.1

Eagle Bulk Shipping Inc. Reports Fourth Quarter and Fiscal Year 2012 Results

NEW YORK, NY, April 1, 2013-- Eagle Bulk Shipping Inc. (Nasdaq: EGLE) today announced its results for the fourth quarter and fiscal year ended December 31, 2012.

For the Fourth Quarter:

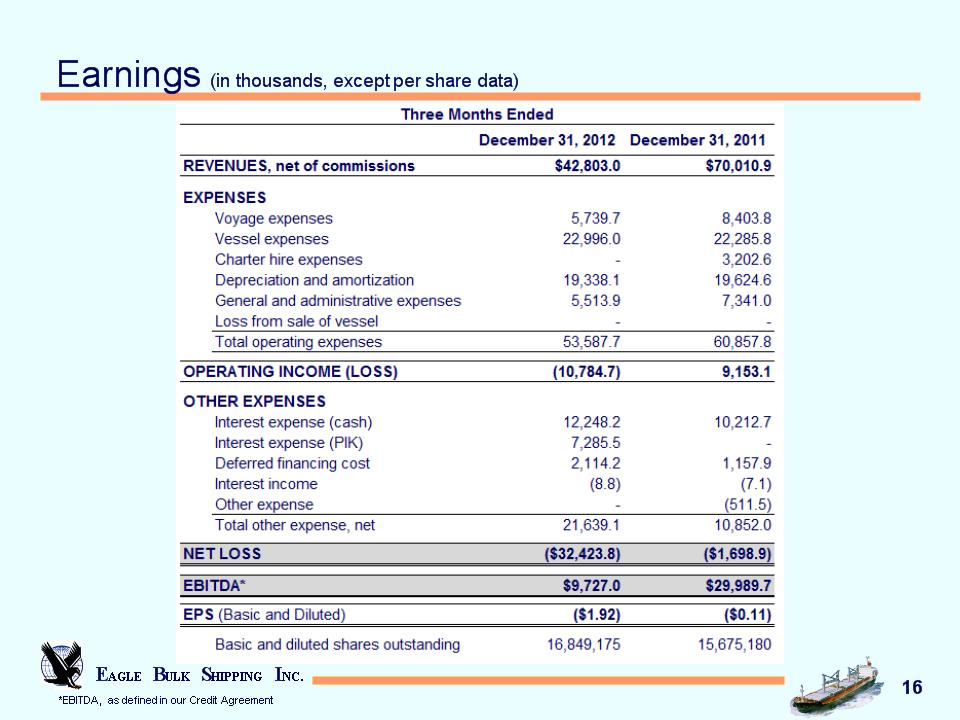

| | ● | Net reported loss of $32.4 million or $1.92 per share (based on a weighted average of 16,849,175 diluted shares outstanding for the quarter), compared to net loss of $1.7 million, or $0.11 per share, for the comparable quarter of 2011. |

| | ● | Net revenues of $42.8 million, compared to $70.0 million for the comparable quarter in 2011. Gross time charter and freight revenues of $44.6 million, compared to $71.7 million for the comparable quarter of 2011. |

| | ● | EBITDA, as adjusted for exceptional items under the terms of the Company's credit agreement, was $9.7 million for the fourth quarter of 2012, compared to $30.0 million for the fourth quarter of 2011. |

| | ● | Fleet utilization rate of 99.4%. |

For the Fiscal Year 2012:

| | ● | Net reported loss of $102.8 million or $6.30 per share (based on a weighted average of 16,328,132 diluted shares outstanding for the year), compared to net loss of $14.8 million, or $0.95 per share, for the comparable year of 2011. |

| | ● | Net revenues of $190.8 million, compared to $313.4 million for the comparable year of 2011. Gross time charter and freight revenues of $198.8 million, compared to $327.2 million for the comparable year of 2011. |

| | ● | EBITDA, as adjusted for exceptional items under the terms of the Company's credit agreement, was $46.0 million for the year of 2012, compared to $108.9 million for the year of 2011. |

| | ● | Fleet utilization rate of 99.3%. |

Sophocles N. Zoullas, Chairman and CEO, commented, "Amid ongoing challenges in the dry bulk market, Eagle Bulk continues to execute an opportunistic, short-term chartering strategy. This approach maximizes revenue upside while ensuring Eagle Bulk is well-positioned when the market improves. At the same time, management has successfully reduced costs while maintaining operational excellence across the board."

Subsequent Event

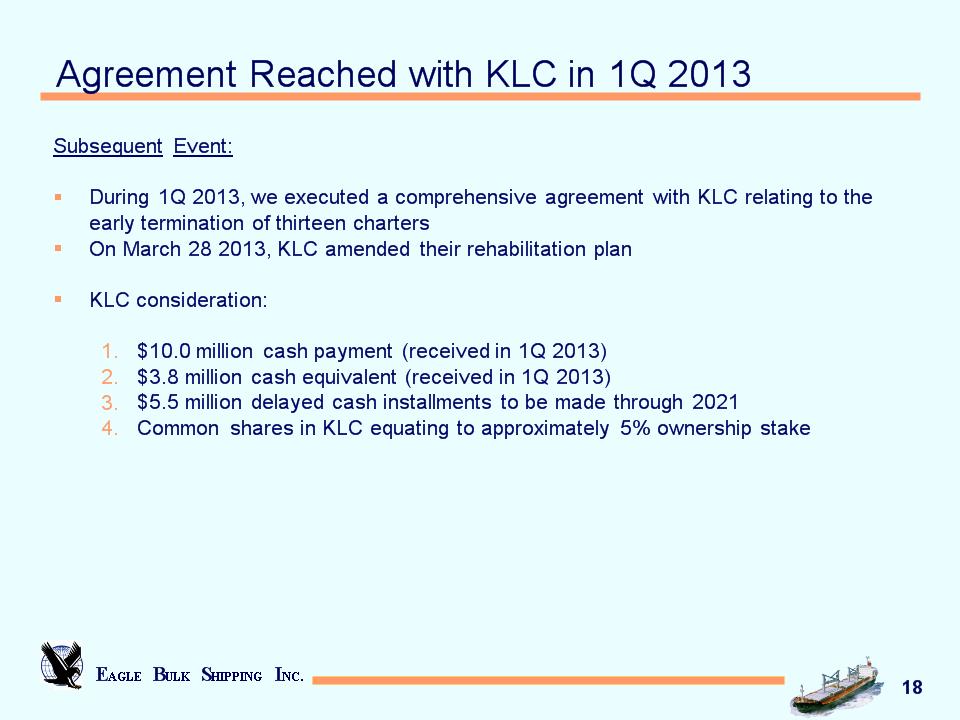

On January 3, 2013, a comprehensive termination agreement between the Company and KLC became effective, pursuant to which we agreed to accept $63.7million on an installment note and 1,224,094 common shares of KLC stock as compensation for the early termination of the 13 charters with KLC. Under the termination agreement, a payment of approximately $10.0 million of the cash settlement was paid in the first quarter of 2013, and the balance of $53.7million is to be paid in cash installments through 2021, with the majority of the payments to be paid in the last five years. The KLC stock certificates were issued on February 7, 2013 and are now being secured at the Korean Securities Depository until August 7, 2013, the date on which we would have been able to take possession of the share certificates. On March 28, 2013, the Korean court approved an amendment to KLC rehabilitation plan after receiving a favorable vote from the concerned parties. The amendment reduced our long term receivable from KLC to $5.5million to be paid in cash installments through 2021; discounted our existing shares by a 1 to 15 ratio; and converted the remainder of the long term receivable to shares that bring our holding of KLC shares after the amendment to approximately 5%.

Results of Operations for the three-month period ended December 31, 2012 and 2011

For the fourth quarter of 2012, the Company reported a net loss of $32,423,775 or $1.92 per share, based on a weighted average of 16,849,175 diluted shares outstanding. In the comparable fourth quarter of 2011, the Company reported net loss of $1,698,979 or $0.11 per share, based on a weighted average of 15,675,180 diluted shares outstanding.

The Company's revenues were earned from time and voyage charters. Gross time and voyage charter revenues in the quarter ended December 31, 2012 were $44,572,372 compared to $71,704,158 recorded in the comparable quarter in 2011. The decrease in gross revenues is attributable primarily to lower charter rates and a decrease in voyage charter revenues in the quarter ended December 31, 2012. Gross revenues recorded in the quarter ended December 31, 2012 and 2011, include an amount of $1,196,202 and $1,254,697, respectively, relating to the non-cash amortization of fair value below contract value of time charters acquired. Brokerage commissions incurred on revenues earned in the quarter ended December 31, 2012 and 2011 were $1,769,417 and $1,693,259, respectively. Net revenues during the quarter ended December 31, 2012 and 2011, were $42,802,955 and $70,010,899, respectively.

Total operating expenses for the quarter ended December 31, 2012 were $53,587,700 compared with $60,857,843 recorded in the fourth quarter of 2011. The Company operated 45 vessels in the fourth quarter of 2012 and 2011. The decrease in operating expenses was primarily due to a reduction in chartered-in days, and lower voyage expenses offset by the increase in vessels crew cost, insurances and vessel depreciation expense. The decrease in General and Administrative expenses is primarily attributable to a reduction in professional consultants' fees and a reduction in compensation expense compared to 2011.

EBITDA, adjusted for exceptional items under the terms of the Company's credit agreement, was $9,727,017 for the fourth quarter of 2012, compared with $29,989,681 for the fourth quarter of 2011. (Please see below for a reconciliation of EBITDA to net loss).

Results of Operations for the twelve-month period ended December 31, 2012 and 2011

For the twelve months ended December 31, 2012, the Company reported net loss of $102,800,903 or $6.30 per share, based on a weighted average of 16,328,132 diluted shares outstanding. In the comparable period of 2011, the Company reported net loss of $14,819,749 or $0.95 per share, based on a weighted average of 15,655,443 diluted shares outstanding.

The Company's revenues were earned from time and voyage charters. Gross revenues for the twelve-month period ended December 31, 2012 were $198,828,140 compared to $327,210,063 recorded in the comparable period of 2011. The decrease in gross revenues is attributable to lower time charter rates and a decrease in voyage revenues in the year, offset marginally by operating a larger fleet. Gross revenues recorded in the twelve-month period ended December 31, 2012 and 2011, include an amount of $4,770,214 and $5,088,268, respectively, relating to the non-cash amortization of fair value below contract value of time charters acquired. Brokerage commissions incurred on revenues earned in the twelve-month periods ended December 31, 2012 and 2011 were $8,016,881 and $13,777,632, respectively. Net revenues during the twelve-month period ended December 31, 2012, decreased to $190,811,259 from $313,432,431 in the comparable period of 2011.

Total operating expenses were $228,029,512 in the twelve-month period ended December 31, 2012 compared to $281,764,140 recorded in the same period of 2011. The decrease in operating expenses was primarily due to a reduction in chartered-in days and lower voyage expenses offset by the increase in operating a larger fleet size which includes increases in vessels crew cost, insurances and vessel depreciation expense. The decrease in General and Administrative expenses is primarily attributable to a reduction in professional consultants' fees and a reduction in compensation expense compared to 2011.

EBITDA, adjusted for exceptional items under the terms of the Company's credit agreement, was $46,034,385 for the twelve months ended December 31, 2012 compared with $108,853,142 for the same period of 2011. (Please see below for a reconciliation of EBITDA to net loss).

Liquidity and Capital Resources

Net cash provided by operating activities during the years ended December 31, 2012 and 2011was $4,777,961 and $58,296,117, respectively. The change in 2012 from 2011 was primarily due to lower charter rates on time charter renewals and from operating fleet for 16,389 days in 2012, and 17,514 days in 2011.

Net cash provided by investing activities during 2012 was $294,414, compared with net cash used in of $157,786,210 in 2011. Investing activities in 2011 reflected the purchase of the last eight newly constructed vessels, the Thrush, Nighthawk, Oriole, Owl, Petrel bulker, Puffin bulker, Roadrunner bulker and Sandpiper bulker, respectively. In July 2011, the Company sold, the Heron, for proceeds of $22,511,226, after brokerage commissions payable to a third party. In November 2011, Korea Line Corporation issued stock to Eagle Bulk at a fair value of $955,093, as part of our settlement with KLC.

Net cash used in financing activities in 2012 was $12,027,610, compared to net cash used of $4,556,384 in 2011. On June 20, 2012 the Company entered into a Fourth Amended and Restated Credit Agreement and incurred $11,788,295 of cash charges related to this amendment. In 2011, the Company repaid $21,875,735 toward our facility, and as part of our sixth amendatory and commercial framework agreement with our lenders we reduced our restricted cash by $19,000,000.

As of December 31, 2012, our cash balance was $18,119,968 compared to a cash balance of $25,075,203 at December 31, 2011. In addition, our Restricted cash balance includes $276,056, for collateralizing letters of credit relating to our office leases as of December 31, 2012. As of December 31, 2011, our Restricted cash balance included $276,056, for collateralizing letters of credit relating to our office leases and $394,362 which collateralized our derivatives positions.

At December 31, 2012, the Company's debt consisted of $1,129,478,741 in term loans and $15,387,468 paid-in-kind loans.

Disclosure of Non-GAAP Financial Measures

EBITDA represents operating earnings before extraordinary items, depreciation and amortization, interest expense, and income taxes, if any. EBITDA is included because it is used by certain investors to measure a company's financial performance. EBITDA is not an item recognized by U.S. GAAP and should not be considered a substitute for net income, cash flow from operating activities and other operations or cash flow statement data prepared in accordance with accounting principles generally accepted in the United States or as a measure of profitability or liquidity. EBITDA is presented to provide additional information with respect to the Company's ability to satisfy its obligations including debt service, capital expenditures, and working capital requirements. While EBITDA is frequently used as a measure of operating results and the ability to meet debt service requirements, the definition of EBITDA used herein may not be comparable to that used by other companies due to differences in methods of calculation.

Our term loan agreement require us to comply with financial covenants based on debt and interest ratio with extraordinary or exceptional items, interest, taxes, non-cash compensation, depreciation and amortization (Credit Agreement EBITDA). Therefore, we believe that this non-U.S. GAAP measure is important for our investors as it reflects our ability to meet our covenants. The following table is a reconciliation of net loss, as reflected in the consolidated statements of operations, to the Credit Agreement EBITDA:

| | | Three Months Ended | | | Twelve Months Ended | |

| | | December 31, 2012 | | | December 31, 2011 | | | December 31, 2012 | | | December 31, 2011 | |

| Net loss | | $ | (32,423,775 | ) | | $ | (1,698,979 | ) | | $ | (102,800,903 | ) | | $ | (14,819,749 | ) |

| Interest Expense | | | 21,647,858 | | | | 11,370,603 | | | | 66,643,296 | | | | 46,769,965 | |

| Depreciation and Amortization | | | 19,338,072 | | | | 19,624,596 | | | | 77,588,428 | | | | 73,084,105 | |

| Amortization of fair value below contract value of time charter acquired | | | (1,196,202 | ) | | | (1,254,697 | ) | | | (4,770,214 | ) | | | (5,088,268 | ) |

| EBITDA | | | 7,365,953 | | | | 28,041,523 | | | | 36,660,607 | | | | 99,946,053 | |

| Adjustments for Exceptional Items: | | | | | | | | | | | | | | | | |

| Non-cash Compensation Expense (1) | | | 2,361,064 | | | | 1,948,158 | | | | 9,373,778 | | | | 8,907,089 | |

| Credit Agreement EBITDA | | $ | 9,727,017 | | | $ | 29,989,681 | | | $ | 46,034,385 | | | $ | 108,853,142 | |

| (1) | Stock based compensation related to stock options, restricted stock units. |

Capital Expenditures and Drydocking

Our capital expenditures relate to the purchase of vessels and capital improvements to our vessels which are expected to enhance the revenue earning capabilities and safety of these vessels.

In addition to acquisitions that we may undertake in future periods, the Company's other major capital expenditures include funding the Company's program of regularly scheduled drydocking necessary to comply with international shipping standards and environmental laws and regulations. Although the Company has some flexibility regarding the timing of its dry docking, the costs are relatively predictable. Management anticipates that vessels are to be drydocked every two and a half years. Funding of these requirements is anticipated to be met with cash from operations. We anticipate that this process of recertification will require us to reposition these vessels from a discharge port to shipyard facilities, which will reduce our available days and operating days during that period.

Drydocking costs incurred are deferred and amortized to expense on a straight-line basis over the period through the date of the next scheduled drydocking for those vessels. In 2012 three of our vessels were drydocked and we incurred $1,094,325 in drydocking related costs. In 2011, four of our vessels were drydocked and we incurred $2,809,406 in drydocking related costs. In 2010, five of our vessels were drydocked and we incurred $2,827,534 in drydocking related costs. The following table represents certain information about the estimated costs for anticipated vessel drydockings in the next four quarters, along with the anticipated off-hire days:

| Quarter Ending | Off-hire Days(1) | Projected Costs(2) |

| March 31, 2013 | 22 | $0.60 million |

| June 30, 2013 | 44 | $1.20 million |

| September 30, 2013 | 22 | $0.60 million |

December 31, 2013 | 44 | $1.20 million |

| (1) | Actual duration of drydocking will vary based on the condition of the vessel, yard schedules and other factors. |

| (2) | Actual costs will vary based on various factors, including where the drydockings are actually performed. |

Summary Consolidated Financial and Other Data:

The following table summarizes the Company's selected consolidated financial and other data for the periods indicated below.

CONSOLIDATED STATEMENTS OF OPERATIONS

| | | Three Months Ended, December 31, (Unaudited) | | | Twelve Months Ended, December 31, | |

| | | 2012 | | | 2011 | | | 2012 | | | 2011 | |

| | | | | | | | | | | | | |

| Revenues, net of commissions | | $ | 42,802,955 | | | $ | 70,010,899 | | | $ | 190,811,259 | | | $ | 313,432,431 | |

| | | | | | | | | | | | | | | | | |

| Voyage expenses | | | 5,739,734 | | | | 8,403,814 | | | | 26,110,591 | | | | 44,345,774 | |

| Vessel expenses | | | 22,995,951 | | | | 22,285,822 | | | | 90,551,655 | | | | 85,049,671 | |

| Charter hire expenses | | | - | | | | 3,202,586 | | | | 1,713,417 | | | | 41,215,875 | |

| Depreciation and amortization | | | 19,338,072 | | | | 19,624,596 | | | | 77,588,428 | | | | 73,084,105 | |

| General and administrative expenses | | | 5,513,943 | | | | 7,341,025 | | | | 32,065,421 | | | | 37,559,639 | |

| Loss from sale of vessel | | | - | | | | - | | | | - | | | | 509,076 | |

Total operating expenses | | | 53,587,700 | | | | 60,857,843 | | | | 228,029,512 | | | | 281,764,140 | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Operating (loss) income | | | (10,784,745 | ) | | | 9,153,056 | | | | (37,218,253 | ) | | | 31,668,291 | |

| | | | | | | | | | | | | | | | | |

| Interest expense | | | 21,647,858 | | | | 11,370,603 | | | | 66,643,296 | | | | 46,769,965 | |

| Interest income | | | (8,828 | ) | | | (7,077 | ) | | | (32,271 | ) | | | (130,007 | ) |

| | | | | | | | | | | | | | | | | |

| Other Income | | | - | | | | (511,491 | ) | | | (1,028,375 | ) | | | (151,918 | ) |

Total other expense, net | | | 21,639,030 | | | | 10,852,035 | | | | 65,582,650 | | | | 46,488,040 | |

| | | | | | | | | | | | | | | | | |

| Net loss | | $ | (32,423,775 | ) | | $ | (1,698,979 | ) | | $ | (102,800,903 | ) | | $ | (14,819,749 | ) |

| | | | | | | | | | | | | | | | | |

Weighted average shares outstanding*: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Basic | | | 16,849,175 | | | | 15,675,180 | | | | 16,328,132 | | | | 15,655,443 | |

| Diluted | | | 16,849,175 | | | | 15,675,180 | | | | 16,328,132 | | | | 15,655,443 | |

Per share amounts: | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| Basic net loss | | $ | (1.92 | ) | | $ | (0.11 | ) | | $ | (6.30 | ) | | $ | (0.95 | ) |

| Diluted net loss | | $ | (1.92 | ) | | $ | (0.11 | ) | | $ | (6.30 | ) | | $ | (0.95 | ) |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | |

* Adjusted to give effect to the 1 for 4 reverse stock split that became effective on May 22, 2012.

Fleet Operating Data

| | Three Months Ended | | Twelve Months Ended |

| | December 31, 2012 | December 31, 2011 | | December 31, 2012 | December 31, 2011 |

| Ownership Days | 4,140 | 4,122 | | 16,470 | 15,290 |

| Chartered-in under operating lease Days | - | 182 | | 90 | 2,421 |

| Total | 4,140 | 4,304 | | 16,560 | 17,711 |

| Available Days | 4,140 | 4,283 | | 16,512 | 17,619 |

| Operating Days | 4,114 | 4,272 | | 16,389 | 17,514 |

| Fleet Utilization | 99.4% | 99.7% | | 99.3% | 99.4% |

CONSOLIDATED BALANCE SHEETS

| | | December 31, 2012 | | | December 31, 2011 | |

| ASSETS: | | | | | | |

| Current assets: | | | | | | |

Cash and cash equivalents | | $ | 18,119,968 | | | $ | 25,075,203 | |

Accounts receivable, net | | | 9,303,958 | | | | 13,960,777 | |

Prepaid expenses | | | 3,544,810 | | | | 3,969,905 | |

Inventories | | | 12,083,125 | | | | 11,083,331 | |

Investment | | | 197,509 | | | | 988,196 | |

Fair value above contract value of time charters acquired | | | 549,965 | | | | 567,315 | |

Fair value of derivative instruments | | | - | | | | 246,110 | |

Total current assets | | | 43,799,335 | | | | 55,890,837 | |

| Noncurrent assets: | | | | | | | | |

Vessels and vessel improvements, at cost, net of accumulated depreciation of $314,700,681 and $239,568,767, respectively | | | 1,714,307,653 | | | | 1,789,381,046 | |

| Other fixed assets, net of accumulated amortization of $515,896 and $324,691, respectively | | | 447,716 | | | | 605,519 | |

Restricted cash | | | 276,056 | | | | 670,418 | |

Deferred drydock costs | | | 2,132,379 | | | | 3,303,363 | |

Deferred financing costs | | | 25,095,469 | | | | 11,766,779 | |

Fair value above contract value of time charters acquired | | | 2,491,530 | | | | 3,041,496 | |

Other assets | | | 594,012 | | | | 2,597,270 | |

Total noncurrent assets | | | 1,745,344,815 | | | | 1,811,365,891 | |

| | | | | | | | | |

Total assets | | $ | 1,789,144,150 | | | $ | 1,867,256,728 | |

| | | | | | | | | |

| LIABILITIES & STOCKHOLDERS' EQUITY | | | | | | | | |

| Current liabilities: | | | | | | | | |

Accounts payable | | $ | 10,235,007 | | | $ | 10,642,831 | |

Accrued interest | | | 2,430,751 | | | | 2,815,665 | |

Other accrued liabilities | | | 14,330,141 | | | | 11,822,582 | |

Current portion of long-term debt | | | - | | | | 32,094,006 | |

| Deferred revenue and fair value below contract value of time charters acquired | | | 3,237,694 | | | | 5,966,698 | |

Unearned charter hire revenue | | | 3,755,166 | | | | 5,779,928 | |

| | | | | | | | | |

Total current liabilities | | | 33,988,759 | | | | 69,121,710 | |

| Noncurrent liabilities: | | | | | | | | |

Long-term debt | | | 1,129,478,741 | | | | 1,097,384,735 | |

Payment-in-kind loans | | | 15,387,468 | | | | - | |

| Deferred revenue and fair value below contract value of time charters acquired | | | 13,850,772 | | | | 17,088,464 | |

Fair value of derivative instruments | | | 2,243,833 | | | | 9,486,116 | |

| | | | | | | | | |

Total noncurrent liabilities | | | 1,160,960,814 | | | | 1,123,959,315 | |

Total liabilities | | | 1,194,949,573 | | | | 1,193,081,025 | |

| Commitment and contingencies | | | | | | | | |

| Stockholders' equity: | | | | | | | | |

Preferred stock, $.01 par value, 25,000,000 shares authorized, none issued | | | - | | | | - | |

Common stock, $.01 par value, 100,000,000 shares authorized, 16,638,092 and 15,750,796* shares issued and outstanding, respectively | | | 166,378 | | | | 157,508 | |

Additional paid-in capital | | | 762,313,030 | | | | 745,945,694 | |

Retained earnings (net of dividends declared of $262,118,388 as of December 31, 2012 and December 31, 2011, respectively) | | | (165,275,389 | ) | | | (62,474,486 | ) |

Accumulated other comprehensive loss | | | (3,009,442 | ) | | | (9,453,013 | ) |

Total stockholders' equity | | | 594,194,577 | | | | 674,175,703 | |

Total liabilities and stockholders' equity | | $ | 1,789,144,150 | | | $ | 1,867,256,728 | |

* Adjusted to give effect to the 1 for 4 reverse stock split that became effective on May 22, 2012.

CONSOLIDATED STATEMENTS OF CASH FLOWS

| | | Year Ended December 31, | |

| | | 2012 | | | 2011 | | | 2010 | |

| Cash flows from operating activities: | | | | | | | | | |

| Net income (loss) | | $ | (102,800,903 | ) | | $ | (14,819,749 | ) | | $ | 26,844,650 | |

| Adjustments to reconcile net income (loss) to net cash provided by operating activities: | | | | | | | | | | | | |

| Items included in net income not affecting cash flows: | | | | | | | | | | | | |

| Depreciation and amortization | | | 75,323,119 | | | | 69,887,121 | | | | 59,503,895 | |

| Amortization of deferred drydocking costs | | | 2,265,309 | | | | 3,196,984 | | | | 3,441,583 | |

| Amortization of deferred financing costs | | | 6,542,727 | | | | 4,172,604 | | | | 3,202,455 | |

| Amortization of fair value (below) above contract value of time charter acquired | | | (4,770,214 | ) | | | (5,088,268 | ) | | | (4,754,407 | ) |

| Loss (gain) on sale of vessel | | | - | | | | 509,076 | | | | (291,011 | ) |

| Payment-in-kind interest on loans | | | 15,387,468 | | | | - | | | | - | |

| Unrealized (gain) loss on derivatives, net | | | 246,110 | | | | (373,868 | ) | | | 127,758 | |

| Allowance for accounts receivable | | | 5,351,609 | | | | 1,811,320 | | | | - | |

| Non-cash compensation expense | | | 9,373,778 | | | | 8,907,089 | | | | 14,741,813 | |

| Drydocking expenditures | | | (1,094,325 | ) | | | (2,809,406 | ) | | | (2,827,534 | ) |

| Changes in operating assets and liabilities: | | | | | | | | | | | | |

| Accounts receivable | | | (694,790 | ) | | | (1,405,602 | ) | | | (6,923,045 | ) |

| Other assets | | | 2,003,258 | | | | (2,527,269 | ) | | | (70,001 | ) |

| Prepaid expenses | | | 425,095 | | | | (510,184 | ) | | | 1,529,725 | |

| Inventories | | | (999,794 | ) | | | (7,893,279 | ) | | | (3,190,052 | ) |

| Accounts payable | | | (407,824 | ) | | | 4,553,558 | | | | 3,799,940 | ) |

| Accrued interest | | | (384,914 | ) | | | (4,526,690 | ) | | | (4,211,361 | ) |

| Accrued expenses | | | 1,666,181 | | | | 5,972,108 | | | | 2,022,756 | |

| Deferred revenue | | | (629,167 | ) | | | (448,024 | ) | | | 159,467 | |

| Unearned charter hire revenue | | | (2,024,762 | ) | | | (311,404 | ) | | | 1,233,199 | |

| | | | | | | | | | | | | |

| Net cash provided by operating activities | | | 4,777,961 | | | | 58,296,117 | | | | 94,339,830 | |

| Cash flows from investing activities: | | | | | | | | | | | | |

| Vessels and vessel improvements and Advances for vessel construction | | | (58,521 | ) | | | (179,105,635 | ) | | | (301,795,862 | ) |

| Purchase of other fixed assets | | | (33,402 | ) | | | (356,631 | ) | | | (255,713 | ) |

| Proceeds from sale of vessel | | | - | | | | 22,511,226 | | | | 21,055,784 | |

| Investment | | | (8,025 | ) | | | (955,093 | ) | | | - | |

| Changes in restricted cash | | | 394,362 | | | | 119,923 | | | | - | |

| | | | | | | | | | | | | |

| Net cash provided by (used in) investing activities | | | 294,414 | | | | (157,786,210 | ) | | | (280,995,791 | ) |

| Cash flows from financing activities: | | | | | | | | | | | | |

| Bank borrowings | | | - | | | | - | | | | 251,183,596 | |

| Repayment of debt | | | - | | | | (21,875,735 | ) | | | - | |

| Changes in restricted cash | | | - | | | | 19,000,000 | | | | (6,014,285 | ) |

| Deferred financing costs | | | (11,788,295 | ) | | | - | | | | - | |

| Cash used to settle net share equity awards | | | (239,315 | ) | | | (1,680,649 | ) | | | (736,443 | ) |

| | | | | | | | | | | | | |

| Net cash provided by (used in) financing activities | | | (12,027,610 | ) | | | (4,556,384 | ) | | | 244,432,868 | |

| Net increase/(decrease) in Cash | | | (6,955,235 | ) | | | (104,046,477 | ) | | | 57,776,907 | |

| Cash at beginning of period | | | 25,075,203 | | | | 129,121,680 | | | | 71,344,773 | |

| | | | | | | | | | | | | |

| Cash at end of period | | $ | 18,119,968 | | | $ | 25,075,203 | | | $ | 129,121,680 | |

| | | | | | | | | | | | | |

| Supplemental cash flow information: | | | | | | | | | | | | |

Cash paid during the period for Interest (including capitalized interest and commitment fees of $209,883, $3,200,486 and $13,725,858 in 2012, 2011 and 2010, respectively) | | $ | 45,098,012 | | | $ | 48,498,289 | | | $ | 57,480,100 | |

The following table represents certain information about our revenue earning charters on our operating fleet as of December 31, 2012:

Vessel | Year Built | Dwt | Charter Expiration (1) | Daily Charter Hire Rate |

| | | | | |

| Avocet | 2010 | 53,462 | Jan 2013 | Voyage(2) |

| | | | | |

| Bittern | 2009 | 57,809 | Jan 2013 | $10,000(2) |

| | | | | |

| Canary | 2009 | 57,809 | Jan 2013 | $13,000(2) |

| | | | | |

| Cardinal | 2004 | 55,362 | Jan 2013 | $9,750 (2) |

| | | | | |

| Condor | 2001 | 50,296 | Jan 2013 | Voyage |

| | | | | |

| Crane | 2010 | 57,809 | Jan 2013 | $8,000 |

| | | | | |

| Crested Eagle | 2009 | 55,989 | Feb 2013 to May 2013 | $11,000 |

| | | | | |

| Crowned Eagle | 2008 | 55,940 | — | Spot(2) |

| | | | | |

| Egret Bulker | 2010 | 57,809 | Jan 2013 | $13,000(2) |

| | | | | |

| Falcon | 2001 | 50,296 | Jan 2013 | $8,000(2) |

| | | | | |

| Gannet Bulker | 2010 | 57,809 | Jan 2013 | $17,650 (with 50% profit share over $20,000) |

| | | | | |

| Golden Eagle | 2010 | 55,989 | Jan 2013 to Feb 2013 | $7,250 |

| | | | | |

| Goldeneye | 2002 | 52,421 | Feb 2013 to May 2013 | Index(3) |

| | | | | |

| Grebe Bulker | 2010 | 57,809 | Feb 2013 to Jun 2013 | $17,650 (with 50% profit share over $20,000) |

| | | | | |

| Harrier | 2001 | 50,296 | Jan 2013 | $7,250(2) |

| | | | | |

| Hawk I | 2001 | 50,296 | Jan 2013 | $6,500(2) |

| | | | | |

| Ibis Bulker | 2010 | 57,775 | Mar 2013 to Jul 2013 | $17,650 (with 50% profit share over $20,000) |

| | | | | |

| Imperial Eagle | 2010 | 55,989 | Jan 2013 to Feb 2013 | $8,250 |

| | | | | |

| Jaeger | 2004 | 52,248 | — | Spot |

| | | | | |

| Jay(2) | 2010 | 57,802 | Jan 2013 | Voyage |

| | | | | |

| Kestrel I | 2004 | 50,326 | Mar 2013 to May 2013 | $9,500 |

| | | | | |

| Kingfisher | 2010 | 57,776 | Jan 2013 to Mar 2013 | $8,900 |

| | | | | |

| Kite | 1997 | 47,195 | — | Spot(2) |

| | | | | |

| Kittiwake | 2002 | 53,146 | Jan 2013 | $10,500(2) |

| | | | | |

| Martin | 2010 | 57,809 | Jan 2013 | $8,000 |

| | | | | |

| Merlin | 2001 | 50,296 | Jan 2013 | $8,500(2) |

| | | | | |

| Nighthawk | 2011 | 57,809 | Feb 2013 | Voyage(2) |

| | | | | |

| Oriole | 2011 | 57,809 | Jan 2013 | $10,250(2) |

| | | | | |

| Osprey I | 2002 | 50,206 | Apr 2013 to Aug 2013 | $8,000(2) |

| | | | | |

| Owl | 2011 | 57,809 | — | Spot(2) |

| Peregrine | 2001 | 50,913 | Jun 2013 to Sep 2013 | $8,250(2) |

| | | | | |

| Petrel Bulker | 2011 | 57,809 | Jul 2014-Nov 2014 | $17,650(4) (with 50% profit share over $20,000) |

| | | | | |

| Puffin Bulker | 2011 | 57,809 | May 2014-Sep 2014 | $17,650(4) (with 50% profit share over $20,000) |

| | | | | |

| Redwing | 2007 | 53,411 | Jan 2013 | $7,500(2) |

| | | | | |

| Roadrunner Bulker | 2011 | 57,809 | Aug 2014-Dec 2014 | $17,650(4) (with 50% profit share over $20,000) |

| | | | | |

| Sandpiper Bulker | 2011 | 57,809 | Jul 2014-Nov 2014 | $17,650(4) (with 50% profit share over $20,000) |

| | | | | |

| Shrike | 2003 | 53,343 | Jan 2013 | $11,300(2) |

| | | | | |

| Skua | 2003 | 53,350 | Jan 2013 | $10,000(2) |

| | | | | |

| Sparrow | 2000 | 48,225 | Mar 2013 to May 2013 | $7,500(2) |

| | | | | |

| Stellar Eagle | 2009 | 55,989 | Mar 2013 to Jun 2013 | Index(3) |

| | | | | |

| Tern | 2003 | 50,200 | Jan 2013 | $8,000(2) |

| | | | | |

| Thrasher | 2010 | 53,360 | — | Spot(2) |

| | | | | |

| Thrush | 2011 | 53,297 | Jan 2013 | $12,300(2) |

| | | | | |

| Woodstar | 2008 | 53,390 | Jan 2013 | Voyage |

| | | | | |

| Wren | 2008 | 53,349 | Jan 2013 | $6,250(2) |

| (1) | The date range provided represents the earliest and latest date on which the charterer may redeliver the vessel to the Company upon the termination of the charter. The time charter hire rates presented are gross daily charter rates before brokerage commissions, ranging from 0.625% to 5.00%, to third party ship brokers. |

| (2) | Upon conclusion of the previous charter the vessel will commence a short term charter for up to six months. |

| (3) | Index, an average of the trailing Baltic Supramax Index. |

| (4) | The charterer has an option to extend the charter by 2 periods of 11 to 13 months each. |

Glossary of Terms:

Ownership days: The Company defines ownership days as the aggregate number of days in a period during which each vessel in its fleet has been owned. Ownership days are an indicator of the size of the fleet over a period and affect both the amount of revenues and the amount of expenses that is recorded during a period.

Chartered-in under operating lease days: The Company defines chartered-in under operating lease days as the aggregate number of days in a period during which the Company chartered-in vessels.

Available days: The Company defines available days as the number of ownership days less the aggregate number of days that its vessels are off-hire due to vessel familiarization upon acquisition, scheduled repairs or repairs under guarantee, vessel upgrades or special surveys and the aggregate amount of time that we spend positioning our vessels. The shipping industry uses available days to measure the number of days in a period during which vessels should be capable of generating revenues.

Operating days: The Company defines operating days as the number of its available days in a period less the aggregate number of days that the vessels are off-hire due to any reason, including unforeseen circumstances. The shipping industry uses operating days to measure the aggregate number of days in a period during which vessels actually generate revenues.

Fleet utilization: The Company calculates fleet utilization by dividing the number of our operating days during a period by the number of our available days during the period. The shipping industry uses fleet utilization to measure a company's efficiency in finding suitable employment for its vessels and minimizing the amount of days that its vessels are off-hire for reasons other than scheduled repairs or repairs under guarantee, vessel upgrades, special surveys or vessel positioning. Our fleet continues to perform at very high utilization rates.

Conference Call Information

Members of Eagle Bulk's senior management team will host a teleconference and webcast at 8:30 a.m. ET on Tuesday, April 2nd to discuss the results.

To participate in the teleconference, investors and analysts are invited to call 877-703-6102 in the U.S., or 857-244-7301 outside of the U.S., and reference participant code 91106673. A simultaneous webcast of the call, including a slide presentation for interested investors and others, may be accessed by visiting http://www.eagleships.com.

A replay will be available following the call until 11:59 PM ET on April 9th, 2013. To access the replay, call 888-286-8010 in the U.S., or 617-801-6888 outside of the U.S., and reference passcode 36113886.

About Eagle Bulk Shipping Inc.

Eagle Bulk Shipping Inc. is a Marshall Islands corporation headquartered in New York. The Company is a leading global owner of Supramax dry bulk vessels that range in size from 50,000 to 60,000 deadweight tons and transport a broad range of major and minor bulk cargoes, including iron ore, coal, grain, cement and fertilizer, along worldwide shipping routes.

Forward-Looking Statements

Matters discussed in this release may constitute forward-looking statements. Forward-looking statements reflect our current views with respect to future events and financial performance and may include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and other statements, which are other than statements of historical facts.

The forward-looking statements in this release are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, management's examination of historical operating trends, data contained in our records and other data available from third parties. Although Eagle Bulk Shipping Inc. believes that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies which are difficult or impossible to predict and are beyond our control, Eagle Bulk Shipping Inc. cannot assure you that it will achieve or accomplish these expectations, beliefs or projections.

Important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements include the strength of world economies and currencies, general market conditions, including changes in charter hire rates and vessel values, changes in demand that may affect attitudes of time charterers to scheduled and unscheduled drydocking, changes in our vessel operating expenses, including dry-docking and insurance costs, or actions taken by regulatory authorities, potential liability from future litigation, domestic and international political conditions, potential disruption of shipping routes due to accidents and political events or acts by terrorists.

Risks and uncertainties are further described in reports filed by Eagle Bulk Shipping Inc. with the US Securities and Exchange Commission.

Visit our website at www.eagleships.com

Contact:

Company Contact:

Adir Katzav

Chief Financial Officer

Eagle Bulk Shipping Inc.

Tel. +1 212-785-2500

Investor Relations / Media:

Jonathan Morgan

Perry Street Communications, New York

Tel. +1 212-741-0014

--------------------------------------------------------------------------------

Source: Eagle Bulk Shipping Inc.

Exhibit 99.2

EAGLE BULK SHIPPING INC. 4Q 2012 Results Presentation 2 April 2013

EAGLE BULK SHIPPING INC. * Forward Looking Statements This presentation contains certain statements that may be deemed to be “forward-looking statements” within the meaning of the Securities Acts. Forward-looking statements reflect management’s current views with respect to future events and financial performance and may include statements concerning plans, objectives, goals, strategies, future events or performance, and underlying assumptions and other statements, which are other than statements of historical facts. The forward-looking statements in this presentation are based upon various assumptions, many of which are based, in turn, upon further assumptions, including without limitation, management's examination of historical operating trends, data contained in our records and other data available from third parties. Although Eagle Bulk Shipping Inc. believes that these assumptions were reasonable when made, because these assumptions are inherently subject to significant uncertainties and contingencies which are difficult or impossible to predict and are beyond our control, Eagle Bulk Shipping Inc. cannot assure you that it will achieve or accomplish these expectations, beliefs or projections. Important factors that, in our view, could cause actual results to differ materially from those discussed in the forward-looking statements include the strength of world economies and currencies, general market conditions, including changes in charter hire rates and vessel values, changes in demand that may affect attitudes of time charterers to scheduled and unscheduled drydocking, changes in our vessel operating expenses, including dry-docking and insurance costs, or actions taken by regulatory authorities, ability of our counterparties to perform their obligations under sales agreements, charter contracts, and other agreements on a timely basis, potential liability from future litigation, domestic and international political conditions, potential disruption of shipping routes due to accidents and political events or acts by terrorists. Risks and uncertainties are further described in reports filed by Eagle Bulk Shipping Inc. with the US Securities and Exchange Commission.

EAGLE BULK SHIPPING INC. * Results and Highlights Commercial Industry Financials Q&A Appendix Agenda

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. Results and Highlights

EAGLE BULK SHIPPING INC. 4Q and FY 2012 Results and Highlights * * 4Q 2012 Net reported loss of $32.4 million or $1.92 per share (based on a weighted average of 16,849,175 diluted shares outstanding for the quarter), compared to net loss of $1.7 million, or $0.11 per share, for the comparable quarter of 2011. Net revenues of $42.8 million, compared to $70.0 million for the comparable quarter in 2011. Gross time charter and freight revenues of $44.6 million, compared to $71.7 million for the comparable quarter of 2011. EBITDA, as adjusted for exceptional items under the terms of the Company's credit agreement, was $9.7 million for the fourth quarter of 2012, compared to $30.0 million for the fourth quarter of 2011. Fleet utilization rate of 99.4%. FY 2012 Net reported loss of $102.8 million or $6.30 per share (based on a weighted average of 16,328,132 diluted shares outstanding for the year), compared to net loss of $14.8 million, or $0.95 per share, for the comparable year of 2011. Net revenues of $190.8 million, compared to $313.4 million for the comparable year of 2011. Gross time charter and freight revenues of $198.8 million, compared to $327.2 million for the comparable year of 2011. EBITDA, as adjusted for exceptional items under the terms of the Company's credit agreement, was $46.0 million for the year of 2012, compared to $108.9 million for the year of 2011. Fleet utilization rate of 99.3%. *EBITDA, as defined in our Credit Agreement

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. Commercial

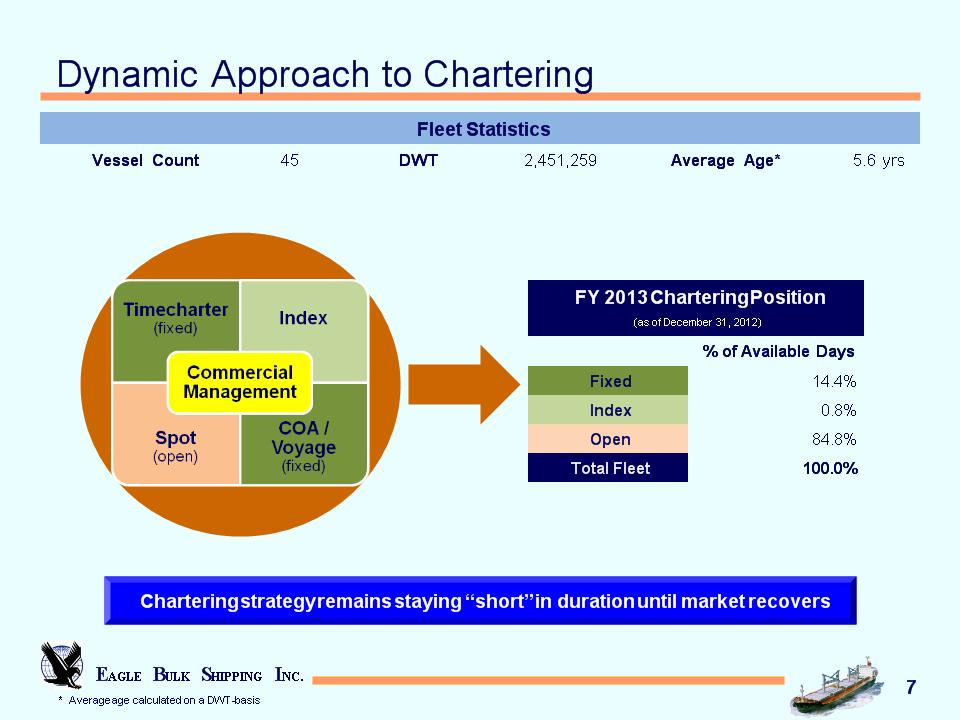

EAGLE BULK SHIPPING INC. * Dynamic Approach to Chartering Chartering strategy remains staying “short” in duration until market recovers Fleet Statistics Fleet Statistics Fleet Statistics Fleet Statistics Fleet Statistics Fleet Statistics Vessel Count 45 DWT 2,451,259 Average Age* 5.6 yrs * Average age calculated on a DWT-basis FY 2013 Chartering Position (as of December 31, 2012) FY 2013 Chartering Position (as of December 31, 2012) % of Available Days Fixed 14.4% Index 0.8% Open 84.8% Total Fleet 100.0%

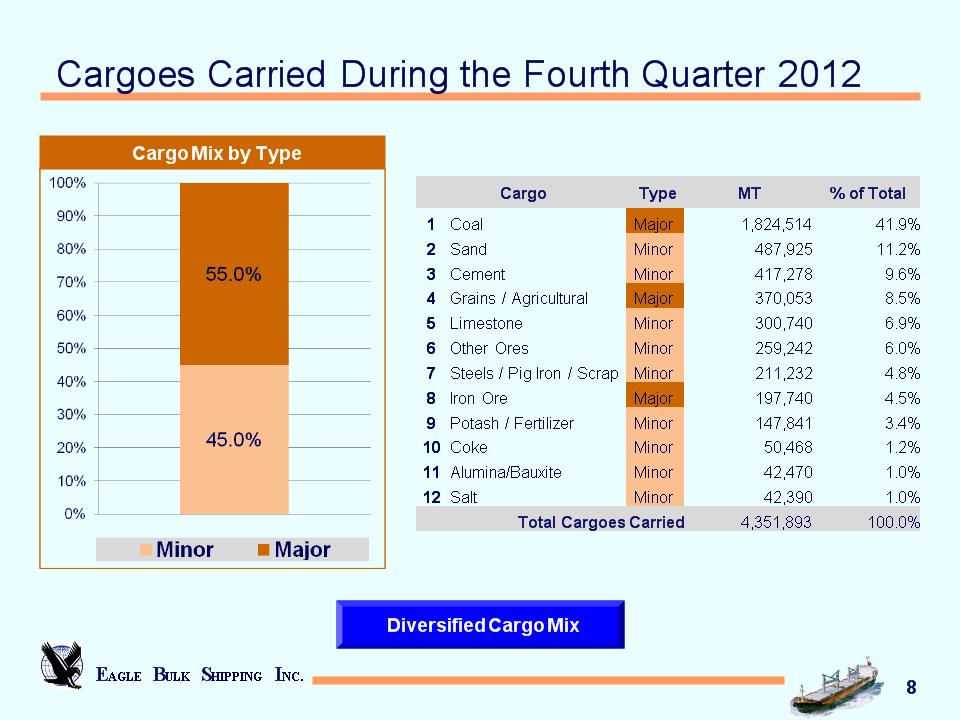

EAGLE BULK SHIPPING INC. * Cargoes Carried During the Fourth Quarter 2012 Diversified Cargo Mix Cargo Cargo Type MT % of Total 1 Coal Major 1,824,514 41.9% 2 Sand Minor 487,925 11.2% 3 Cement Minor 417,278 9.6% 4 Grains / Agricultural Major 370,053 8.5% 5 Limestone Minor 300,740 6.9% 6 Other Ores Minor 259,242 6.0% 7 Steels / Pig Iron / Scrap Minor 211,232 4.8% 8 Iron Ore Major 197,740 4.5% 9 Potash / Fertilizer Minor 147,841 3.4% 10 Coke Minor 50,468 1.2% 11 Alumina/Bauxite Minor 42,470 1.0% 12 Salt Minor 42,390 1.0% Total Cargoes Carried Total Cargoes Carried Total Cargoes Carried 4,351,893 100.0% Cargo Mix by Type

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. Industry

EAGLE BULK SHIPPING INC. * Source(s): Clarksons 2012: Another Year Dominated by Oversupply Supramax outperforms in weak market FY 2012 Drybulk Supply-Demand Growth (% annual growth measured in MT) FY 2012 Drybulk Fleet Utilization (\ Average Daily Spot Rates Average Daily Spot Rates Average Daily Spot Rates Average Daily Spot Rates Supramax Panamax Capesize 2011 $14,405 $14,000 $15,639 2012 $9,471 $7,684 $7,680 Year-on-Year % Change -34.3% -45.1% -50.9%

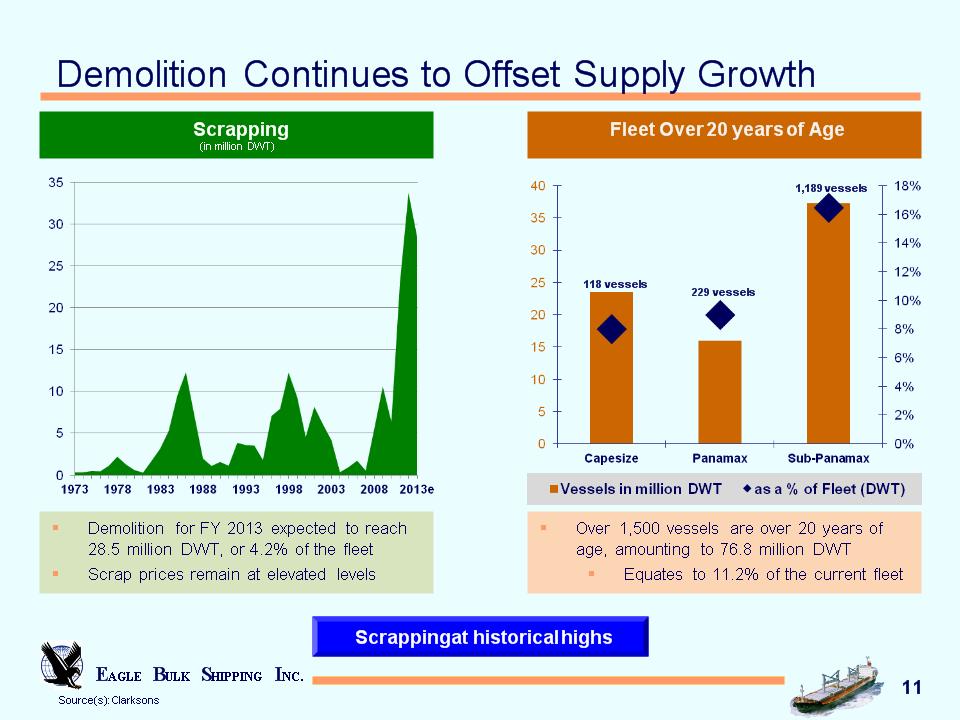

EAGLE BULK SHIPPING INC. * Source(s): Clarksons Scrapping at historical highs Demolition Continues to Offset Supply Growth Scrapping (in million DWT) Fleet Over 20 years of Age ( 118 vessels 229 vessels 1,189 vessels Demolition for FY 2013 expected to reach 28.5 million DWT, or 4.2% of the fleet Scrap prices remain at elevated levels Over 1,500 vessels are over 20 years of age, amounting to 76.8 million DWT Equates to 11.2% of the current fleet

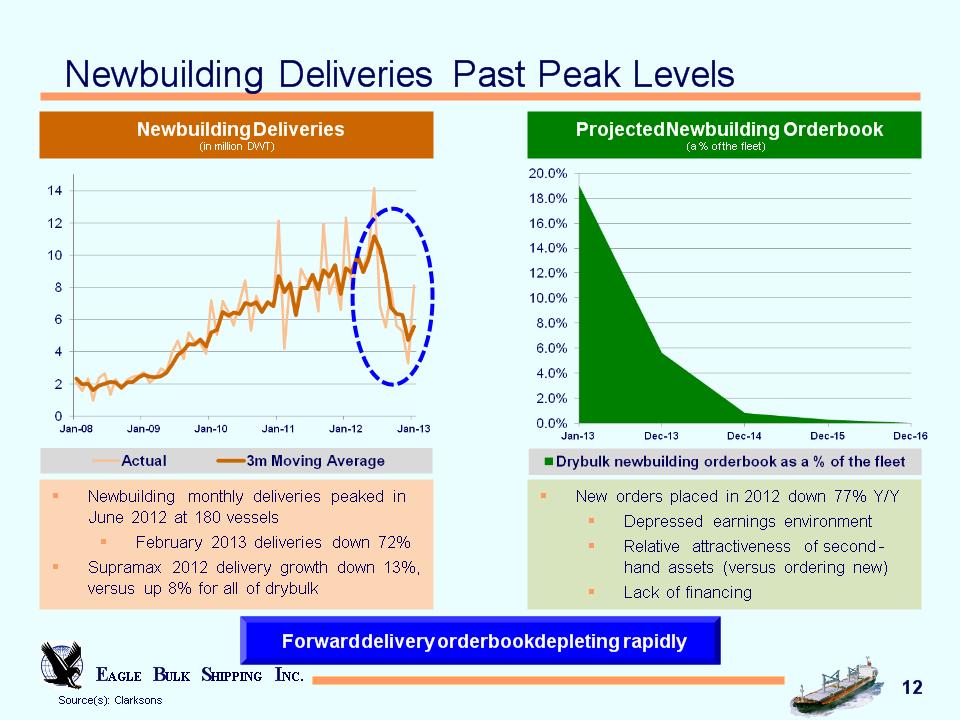

EAGLE BULK SHIPPING INC. * Source(s): Clarksons Newbuilding Deliveries Past Peak Levels Forward delivery orderbook depleting rapidly Projected Newbuilding Orderbook (a % of the fleet) Newbuilding Deliveries (in million DWT) New orders placed in 2012 down 77% Y/Y Depressed earnings environment Relative attractiveness of second-hand assets (versus ordering new) Lack of financing Newbuilding monthly deliveries peaked in June 2012 at 180 vessels February 2013 deliveries down 72% Supramax 2012 delivery growth down 13%, versus up 8% for all of drybulk

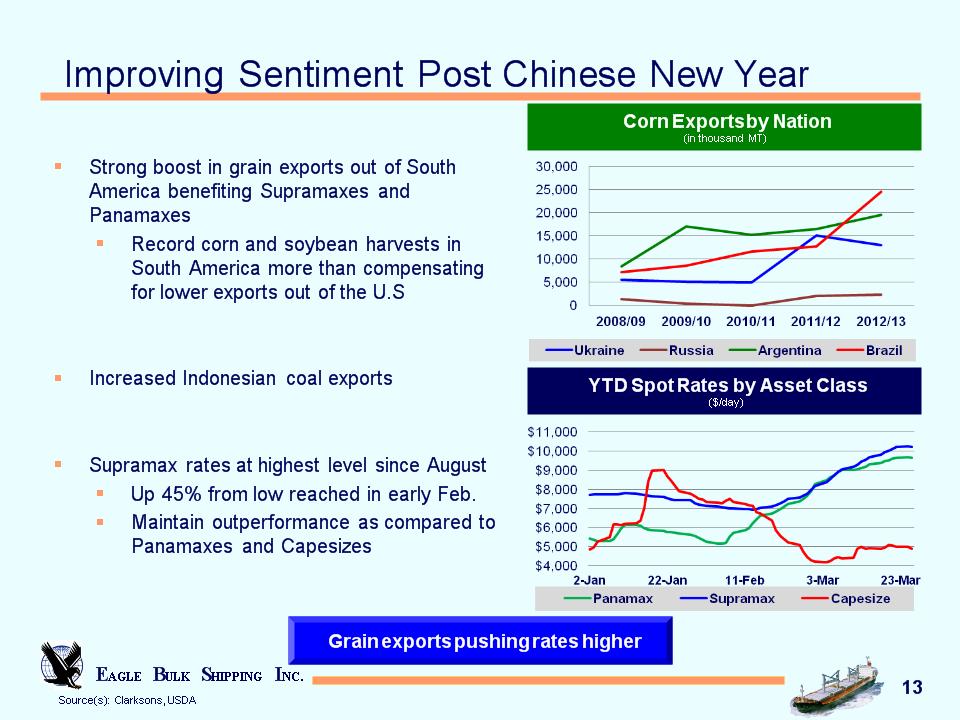

EAGLE BULK SHIPPING INC. * Source(s): Clarksons, USDA Strong boost in grain exports out of South America benefiting Supramaxes and Panamaxes Record corn and soybean harvests in South America more than compensating for lower exports out of the U.S Increased Indonesian coal exports Supramax rates at highest level since August Up 45% from low reached in early Feb. Maintain outperformance as compared to Panamaxes and Capesizes Improving Sentiment Post Chinese New Year Grain exports pushing rates higher Corn Exports by Nation (in thousand MT) YTD Spot Rates by Asset Class ($/day)

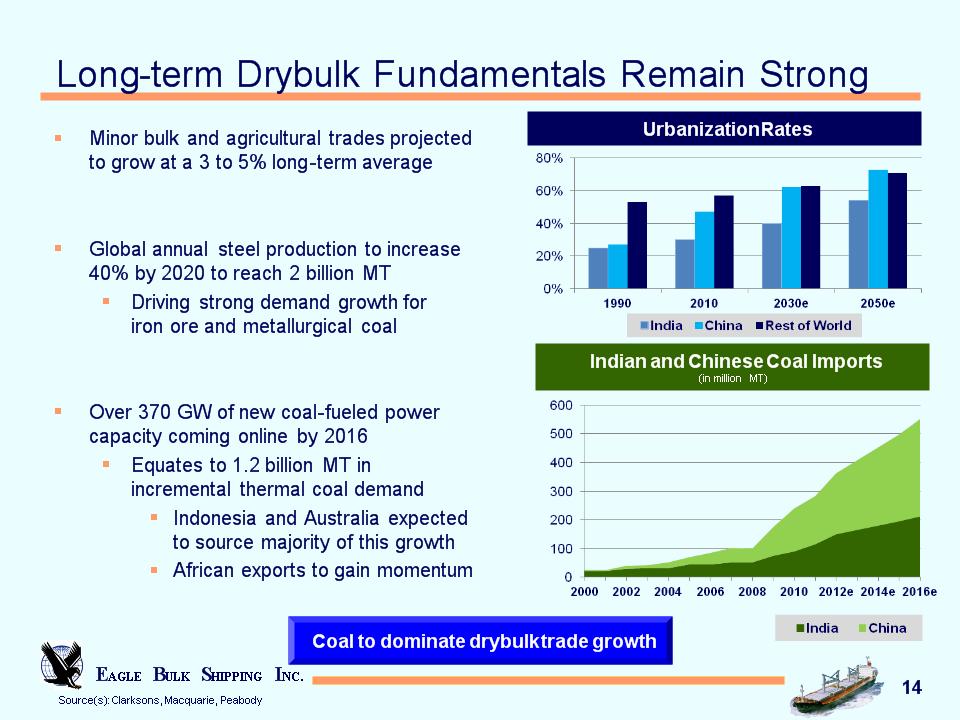

EAGLE BULK SHIPPING INC. * Source(s): Clarksons, Macquarie, Peabody Minor bulk and agricultural trades projected to grow at a 3 to 5% long-term average Global annual steel production to increase 40% by 2020 to reach 2 billion MT Driving strong demand growth for iron ore and metallurgical coal Over 370 GW of new coal-fueled power capacity coming online by 2016 Equates to 1.2 billion MT in incremental thermal coal demand Indonesia and Australia expected to source majority of this growth African exports to gain momentum Long-term Drybulk Fundamentals Remain Strong Coal to dominate drybulk trade growth Indian and Chinese Coal Imports (in million MT) Urbanization Rates

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. Financials

EAGLE BULK SHIPPING INC. * Earnings (in thousands, except per share data) *EBITDA, as defined in our Credit Agreement

EAGLE BULK SHIPPING INC. * Balance Sheet (in thousands)

EAGLE BULK SHIPPING INC. * Agreement Reached with KLC in 1Q 2013 Subsequent Event: During 1Q 2013, we executed a comprehensive agreement with KLC relating to the early termination of thirteen charters On March 28 2013, KLC amended their rehabilitation plan KLC consideration: $10.0 million cash payment (received in 1Q 2013) $3.8 million cash equivalent (received in 1Q 2013) $5.5 million delayed cash installments to be made through 2021 Common shares in KLC equating to approximately 5% ownership stake

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. Q&A

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC.

EAGLE BULK SHIPPING INC. EAGLE BULK SHIPPING INC. Appendix

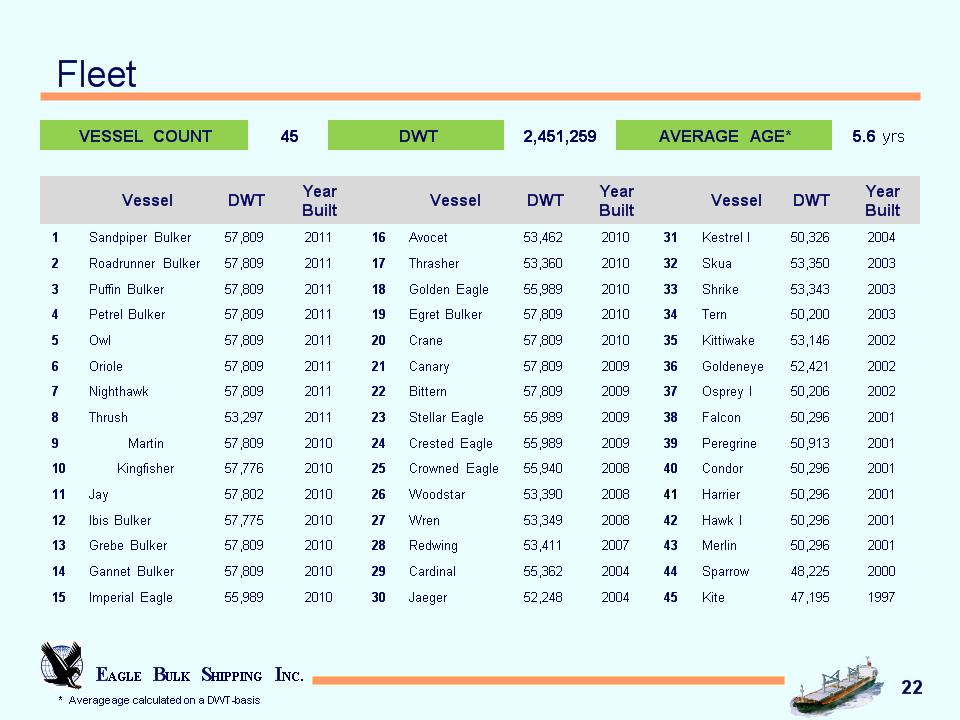

EAGLE BULK SHIPPING INC. * Fleet Vessel DWT Year Built Vessel DWT Year Built Vessel DWT Year Built 1 Sandpiper Bulker 57,809 2011 16 Avocet 53,462 2010 31 Kestrel I 50,326 2004 2 Roadrunner Bulker 57,809 2011 17 Thrasher 53,360 2010 32 Skua 53,350 2003 3 Puffin Bulker 57,809 2011 18 Golden Eagle 55,989 2010 33 Shrike 53,343 2003 4 Petrel Bulker 57,809 2011 19 Egret Bulker 57,809 2010 34 Tern 50,200 2003 5 Owl 57,809 2011 20 Crane 57,809 2010 35 Kittiwake 53,146 2002 6 Oriole 57,809 2011 21 Canary 57,809 2009 36 Goldeneye 52,421 2002 7 Nighthawk 57,809 2011 22 Bittern 57,809 2009 37 Osprey I 50,206 2002 8 Thrush 53,297 2011 23 Stellar Eagle 55,989 2009 38 Falcon 50,296 2001 9 Martin 57,809 2010 24 Crested Eagle 55,989 2009 39 Peregrine 50,913 2001 10 Kingfisher 57,776 2010 25 Crowned Eagle 55,940 2008 40 Condor 50,296 2001 11 Jay 57,802 2010 26 Woodstar 53,390 2008 41 Harrier 50,296 2001 12 Ibis Bulker 57,775 2010 27 Wren 53,349 2008 42 Hawk I 50,296 2001 13 Grebe Bulker 57,809 2010 28 Redwing 53,411 2007 43 Merlin 50,296 2001 14 Gannet Bulker 57,809 2010 29 Cardinal 55,362 2004 44 Sparrow 48,225 2000 15 Imperial Eagle 55,989 2010 30 Jaeger 52,248 2004 45 Kite 47,195 1997 * Average age calculated on a DWT-basis VESSEL COUNT 45 DWT 2,451,259 AVERAGE AGE* 5.6 yrs

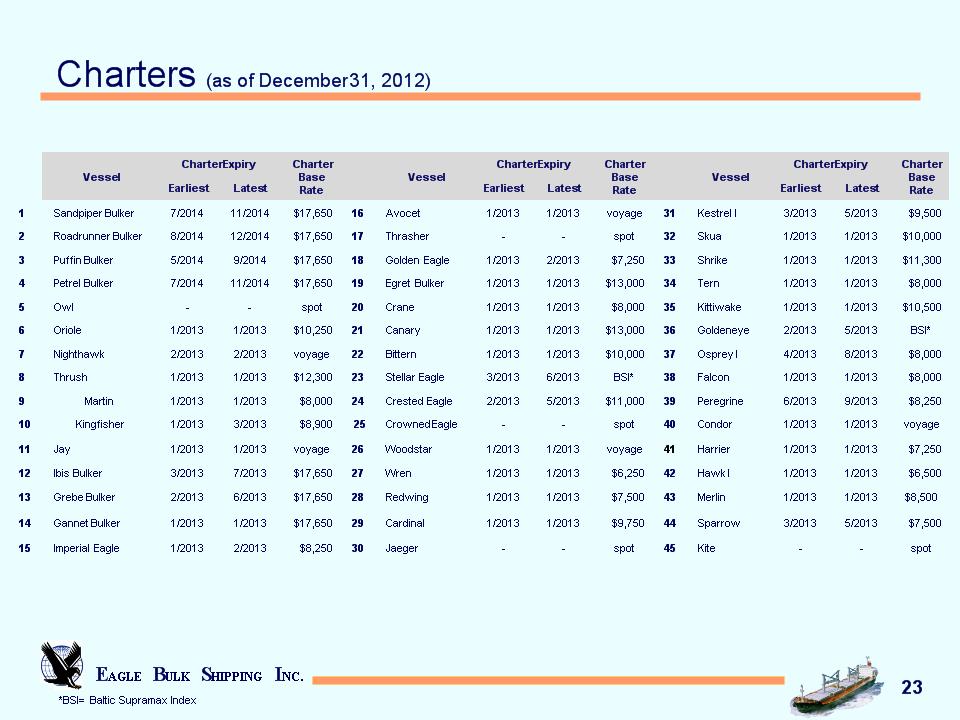

EAGLE BULK SHIPPING INC. * Charters (as of December 31, 2012) Vessel Charter Expiry Charter Expiry Charter Base Rate Vessel Charter Expiry Charter Expiry Charter Base Rate Vessel Charter Expiry Charter Expiry Charter Base Rate Vessel Earliest Latest Charter Base Rate Vessel Earliest Latest Charter Base Rate Vessel Earliest Latest Charter Base Rate 1 Sandpiper Bulker 7/2014 11/2014 $17,650 16 Avocet 1/2013 1/2013 voyage 31 Kestrel I 3/2013 5/2013 $9,500 2 Roadrunner Bulker 8/2014 12/2014 $17,650 17 Thrasher - - spot 32 Skua 1/2013 1/2013 $10,000 3 Puffin Bulker 5/2014 9/2014 $17,650 18 Golden Eagle 1/2013 2/2013 $7,250 33 Shrike 1/2013 1/2013 $11,300 4 Petrel Bulker 7/2014 11/2014 $17,650 19 Egret Bulker 1/2013 1/2013 $13,000 34 Tern 1/2013 1/2013 $8,000 5 Owl - - spot 20 Crane 1/2013 1/2013 $8,000 35 Kittiwake 1/2013 1/2013 $10,500 6 Oriole 1/2013 1/2013 $10,250 21 Canary 1/2013 1/2013 $13,000 36 Goldeneye 2/2013 5/2013 BSI* 7 Nighthawk 2/2013 2/2013 voyage 22 Bittern 1/2013 1/2013 $10,000 37 Osprey I 4/2013 8/2013 $8,000 8 Thrush 1/2013 1/2013 $12,300 23 Stellar Eagle 3/2013 6/2013 BSI* 38 Falcon 1/2013 1/2013 $8,000 9 Martin 1/2013 1/2013 $8,000 24 Crested Eagle 2/2013 5/2013 $11,000 39 Peregrine 6/2013 9/2013 $8,250 10 Kingfisher 1/2013 3/2013 $8,900 25 Crowned Eagle - - spot 40 Condor 1/2013 1/2013 voyage 11 Jay 1/2013 1/2013 voyage 26 Woodstar 1/2013 1/2013 voyage 41 Harrier 1/2013 1/2013 $7,250 12 Ibis Bulker 3/2013 7/2013 $17,650 27 Wren 1/2013 1/2013 $6,250 42 Hawk I 1/2013 1/2013 $6,500 13 Grebe Bulker 2/2013 6/2013 $17,650 28 Redwing 1/2013 1/2013 $7,500 43 Merlin 1/2013 1/2013 $8,500 14 Gannet Bulker 1/2013 1/2013 $17,650 29 Cardinal 1/2013 1/2013 $9,750 44 Sparrow 3/2013 5/2013 $7,500 15 Imperial Eagle 1/2013 2/2013 $8,250 30 Jaeger - - spot 45 Kite - - spot *BSI= Baltic Supramax Index