UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21750

Kayne Anderson Energy Total Return Fund, Inc.

(Exact name of registrant as specified in charter)

| | |

| 717 Texas Avenue, Suite 3100, Houston, Texas | | 77002 |

| (Address of principal executive offices) | | (Zip code) |

David Shladovsky, Esq.

KA Fund Advisors, LLC, 717 Texas Avenue, Suite 3100, Houston, Texas 77002

(Name and address of agent for service)

Registrant’s telephone number, including area code: (713) 493-2020

Date of fiscal year end: November 30, 2012

Date of reporting period: November 30, 2012

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The report of Kayne Anderson Energy Total Return Fund, Inc. (the “Registrant”) to stockholders for the fiscal year ended November 30, 2012 is attached below.

Energy Total Return Fund

KYE Annual Report

November 30, 2012

CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This report of Kayne Anderson Energy Total Return Fund, Inc. (the “Fund”) contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Fund’s historical experience and its present expectations or projections indicated in any forward-looking statement. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; energy industry risk; commodity pricing risk; leverage risk; valuation risk; non-diversification risk; interest rate risk; tax risk; and other risks discussed in the Fund’s filings with the Securities and Exchange Commission (“SEC”). You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Fund undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Fund’s investment objectives will be attained.

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

LETTER TO STOCKHOLDERS

January 24, 2013

Dear Fellow Stockholders:

In a year marked by renewed uncertainty about the health of the global economy, we are pleased to report that the Fund generated solid returns during fiscal 2012. While our overall performance was positive during the year, market conditions impacted each of the Fund’s investment sub-sectors differently. MLPs and Midstream Companies performed very well, while Income Trusts and Marine Transportation underperformed. We continue to believe in the merits of the Fund’s diversified portfolio and are optimistic about the outlook for the Fund’s portfolio in 2013.

As we highlighted in last year’s annual letter, unconventional reserves, which are commonly referred to as “shale plays,” continue to be the biggest story in the energy sector. Development of these reserves has fundamentally changed the domestic energy market and is having an increasing impact on the global energy market. This “Shale Revolution,” as we like to call it, continues to accelerate and is expected to have a major impact on the domestic economy. We agree with industry sources that expect the energy sector to create over 2.5 million net new jobs by 2020. This economic boon results not only from jobs directly attributable to the energy sector, but also from the re-industrialization of the U.S., as plentiful domestic energy supplies and low natural gas prices are facilitating a resurgence in manufacturing activity. Over the last two years alone, over $90 billion worth of domestic growth projects have been announced by manufacturing companies that are seeking to take advantage of low-cost domestic energy.

The growth in the production of oil, natural gas and natural gas liquids (“NGLs”) from the development of these reserves presents both significant opportunities and challenges for energy companies. For instance, a significant amount of new midstream assets must be built to facilitate transportation of this new production to end-users, which is very positive for MLPs and Midstream Companies. On the other hand, increased production of natural gas and NGLs has exceeded growth in demand and has had a negative impact on market prices for these commodities. These price declines have impacted cash flows for Income Trusts and other energy companies focused on exploration and production activities.

One of the measures we employ to evaluate our performance is Net Asset Value Return, which is equal to the change in net asset value per share plus the cash distributions paid during the period, assuming reinvestment through our dividend reinvestment program. Our Net Asset Value Return was 8.4% for fiscal 2012. During the same period, the MLP market, as measured by the Alerian MLP index, had a total return of 14.4% and the S&P 500 index had a total return of 16.1%. The strong performance of the Fund’s investments in MLPs, Midstream Companies and Energy Debt was offset by the underperformance of our Income Trusts and Marine Transportation holdings.

Another measure of the Fund’s performance is Market Return, which is equal to the change in share price plus the cash distributions paid during the period, assuming reinvestment through our dividend reinvestment program. Our Market Return was 13.0% for fiscal 2012. This measure exceeded our Net Asset Value Return, as the discount of our share price to NAV decreased during fiscal 2012. Our share price traded at a discount to NAV of 5.7% on November 30, 2011 and 1.6% on November 30, 2012.

Energy Market Overview

Development of unconventional reserves or shale plays continues to transform the domestic energy industry. It is the biggest story in the energy business and, arguably, a driving factor in the recovery of the domestic economy. Examples of unconventional shale plays include the Bakken Shale, Eagle Ford Shale, Marcellus Shale and Utica Shale.

1

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

LETTER TO STOCKHOLDERS

In our opinion, 2012 was the year in which it became clear that development of unconventional reserves could reap huge benefits for the domestic economy. Abundant new supplies of low-cost natural gas and NGLs are spurring a resurgence in domestic manufacturing activity. For instance, petrochemical companies have announced new projects to utilize low-cost ethane and propane as feedstocks in facilities that make higher value chemicals and plastics. In total, industry sources estimate that over $90 billion of new industrial projects are being considered domestically. Energy is truly the bright spot in an otherwise sluggish domestic economy, and we continue to be very excited about the potential job creation and other positive ripple effects of the Shale Revolution.

Driven by the development of the shale plays, domestic production of crude oil, NGLs and natural gas grew in 2012 – the fourth consecutive year the U.S. has increased production levels for each of these commodities. Domestic crude oil production is expected to increase by 780,000 barrels per day in 2012 (a 13.8% increase), which is the largest annual production increase in our country’s history! The U.S. is currently the largest producer of natural gas in the world, and many experts are predicting that it will become the largest producer of crude oil in the next 10 to 15 years. As a result, the U.S. has substantially decreased its dependence on crude oil from foreign sources and has become a large exporter of refined petroleum products. These statistics are pretty amazing when you consider the fact that just 10 years ago most experts believed domestic production was in a secular decline.

This rapid increase in production from unconventional reserves continues to create both opportunities and challenges. Growing supplies require new infrastructure to move the commodities to market, as well as refine, process and fractionate oil, natural gas and NGLs. In addition, there is increasing interest in exporting commodities to access higher value markets abroad. The backlog of infrastructure projects continues to grow and will likely take decades to fully develop.

Growing production also creates challenges for energy companies, especially those companies that have direct exposure to lower commodity prices such as Income Trusts. It is common for demand growth to lag production growth, which can put downward pressure on prices in the interim. We have seen this with natural gas, which bottomed in April 2012 at $1.82/MMbtu (its lowest price in over 10 years). Prices have since strengthened as production growth has moderated and lower prices stimulated growth in demand from power plants switching from coal to natural gas, which has led to declines in coal prices and very challenging market conditions for coal companies. Nevertheless, even with this rebound in the price of natural gas, domestic natural gas trades at a steep discount to international natural gas, a phenomenon which we believe will continue to spur additional sources of demand such as the development of liquefied natural gas (“LNG”) export facilities and new domestic manufacturing projects.

The shift in focus by upstream companies from drilling “dry” gas prospects to drilling “wet” gas prospects (gas wells that produce associated NGLs) over the last couple of years has caused a near-term oversupply of NGLs, particularly the ethane and propane components. As a result, we saw inventories of ethane and propane build throughout 2012 and a corresponding decrease in NGL prices. For propane, this dynamic was exacerbated by an abnormally warm 2011-2012 winter. During calendar 2012, the price of ethane fell 71%, and the price of propane fell 35%. This can impact Income Trusts and Gathering & Processing MLPs with commodity price exposure. We believe that this low NGL price environment is a temporary market dislocation and will resolve itself over the next 12 to 24 months.

Crude oil infrastructure has been one of the most active areas for MLPs and Midstream Companies over the past year. The rapid increase in domestic production has created numerous bottlenecks and dislocations between producing areas and the refiners that consume the crude oil. The most apparent bottleneck is at Cushing, Oklahoma, the pricing point for the domestic benchmark West Texas Intermediate (“WTI”) crude. Increasing supplies in the mid-continent and constraints in capacity to move crude to Gulf Coast refiners have resulted in a

2

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

LETTER TO STOCKHOLDERS

steep discount in the price of WTI relative to Brent, the international benchmark. This “differential” in prices is expected to persist for the near-term and gradually narrow over time as new pipelines relieve the logistical constraints at Cushing.

We believe, however, that regional crude oil prices will continue to price at wider differentials to benchmarks, which creates tremendous opportunities for many MLPs and Midstream Companies. We have already seen an increased focus on regional crude infrastructure opportunities, including projects to move crude oil via railroads, in areas such as North Dakota (Bakken Shale) and West Texas (Permian Basin), where differentials are much higher than historical averages. This dynamic enables MLPs and Midstream Companies with the capability to move the regionally oversupplied crude to higher value markets to be very profitable.

Income Trusts and other upstream companies, which are often price takers in regional markets, have seen pressure on their profits in areas where they must accept a discount to WTI. We expect these dynamics to continue to change rapidly as pipeline and rail facilities are built to alleviate existing supply bottlenecks, while production growth in new basins creates new supply bottlenecks.

The domestic energy market continues to evolve in response to the varied impacts of the Shale Revolution. While this can create price dislocations in the short-term, we firmly believe markets are efficient. Lower prices will spur demand growth, as well as cause upstream companies to re-allocate capital to higher return projects. Further, abnormally high differentials serve as an incentive for MLPs and Midstream Companies to build the needed infrastructure to reduce the differentials. We are excited to watch these events unfold over the next few years and believe our team of investment professionals is well positioned to identify and capitalize on these trends.

Market Overview

While MLPs performed very well for the year (14.4% total return), the broader markets performed even better, with the S&P 500 generating a total return of 16.1% for the year. Notably, calendar 2012 was the first year since 1999 that MLPs were outperformed by the S&P 500 index. Over that 13-year time period, MLPs generated a total return of over 830% versus a total return of approximately 24% for the S&P 500 index. That level of outperformance over a 13-year period is nothing short of stunning in our opinion! With an average yield of 6.1% for the group as of January 24, 2013 and attractive distribution growth prospects, we continue to view MLPs as a very compelling investment opportunity.

Distribution growth is the most important driver of MLP returns and, we believe, the leading reason for MLPs’ strong relative performance over the last 13 years. MLP distribution growth accelerated during the year, as MLPs benefited from acquisitions and completion of infrastructure development projects. Distributions grew 7.3% during 2012 compared to 6.3% in 2011 and 4.5% in 2010. We believe that prospects for distribution growth in 2013 are also very strong, and we are projecting distributions to grow by 6% to 7%. The development of unconventional reserves and the construction of related infrastructure assets will continue to fuel this distribution growth.

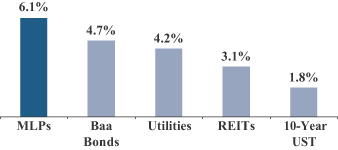

While the MLP market performed well during fiscal 2012, MLPs became even more attractively valued on a relative basis to other income alternatives. At the beginning of the fiscal year, the average MLP yield was 6.4%, which represented a 434 basis point premium (100 basis points equals one percent) to the yield on 10-year U.S. Treasury Bonds. This difference is often referred to as the “spread to Treasuries.” By November 30, 2012, the spread to Treasuries had increased to 473 basis points. As of January 24, 2012, the spread to Treasuries was 426 basis points, which is well above the 334 basis point average since 2000. As illustrated in Figure 1 below, MLP yields compare very favorably to other income-oriented investments. In addition to the spread to Treasuries, current yields for MLPs are much higher than yields for investment grade (BBB) bonds, utilities and REITs. This

3

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

LETTER TO STOCKHOLDERS

comparison is even more compelling when you take into account the prospect of strong distribution growth for MLPs.

Figure 1. MLP Yields versus Other Income Alternatives (January 24, 2013)

Capital expenditures by MLPs, including both acquisitions and new growth projects, continued at robust levels in 2012. We estimate that MLPs announced over $50 billion in acquisitions during calendar 2012. These acquisitions were a combination of third-party deals and “drop-down” transactions in which an MLP’s general partner sells assets to its affiliated MLP. These drop-down transactions are generally completed at attractive prices that are accretive to the MLP’s cash distributions. We estimate that MLPs also spent over $20 billion on capital projects during the year. We believe these projects are overwhelmingly driven by the need to provide midstream infrastructure to growing oil and natural gas production resulting from the development of unconventional resources. Furthermore, we view these types of projects to be the most reliable way for MLPs to generate returns in excess of their cost of capital when prudently executed by an experienced management team. While it is difficult to predict M&A activity, we expect MLPs to spend in excess of $25 billion on capital projects during 2013.

Capital markets activity for MLPs reached a record high in calendar 2012. During the year, MLPs raised $15 billion in follow-on equity and $28 billion in debt, surpassing activity levels in 2011. We also saw a continuation of the robust IPO market seen in 2011, with 13 IPOs raising approximately $3.3 billion. Like 2011, there was a wide disparity in the quality of the companies going public and in after-market trading performance. Consequently, we chose not to participate in many deals. On average, the IPOs in which we participated are up over 26% from their IPO price. While we expect the IPO market to remain active during 2013, we plan to be very selective in our participation.

During fiscal 2012, we substantially increased our exposure to Midstream Companies, which comprised 13% of our portfolio at year-end. Like MLPs, the Midstream Company sector had a very good year, generating a total return of 14.4%. Our portfolio of Midstream Companies performed even better than the sector as a whole with the Fund’s holdings in this sector delivering a total return in excess of 20%. Midstream Companies benefit from many of the same trends that are contributing to the positive long-term outlook for MLPs, and we believe that Midstream Companies should continue to provide attractive returns for many years to come. We also believe this sector has the highest dividend growth potential of any of the sectors in which the Fund invests.

Fiscal 2012 was a challenging year for the Income Trust sector. The Income Trust sector includes both Canadian companies that were formerly treated as royalty trusts (“Canadian trusts”) and royalty and grantor trusts with properties in the United States (“U.S. trusts”). These entities are engaged in the production of crude oil, NGLs and natural gas and, as a result, have direct exposure to changes in commodity prices.

4

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

LETTER TO STOCKHOLDERS

The Canadian trust sector generated a total return of negative 11.9% for the year, as low natural gas and NGL prices negatively impacted financial results. Further, many of the higher dividend names in which we invest had weaker than expected operating performance. As a result, several of these names chose to reduce dividends during the year, which caused these names to perform even worse than the sector as a whole. We have substantially reduced our Canadian trust holdings over the last two years (down by $90 million to $56 million) as we see better return prospects in other segments of the energy industry.

The Fund substantially increased its exposure to U.S. trusts during the year, in part by participating in three IPOs during fiscal 2012. While the sector had positive returns for most of our fiscal year, sector performance was terrible during November. This poor performance was attributable to operational issues at certain of the “drilling trusts,” as well as a negative reserve revision that was announced by SandRidge Energy, the sponsor of three drilling trusts. As a result, the U.S. trust sector ended the year with a total return of negative 22.8%. We believe that many of the drilling trusts were oversold at year-end and selectively added to certain positions. In fact, from the end of 2012 to the date of this letter, the drilling trusts have generated a total return of 7.5%.

The Marine Transportation sector generated a positive total return during fiscal 2012 (up 7.6%), but the sector continues to face headwinds. Specifically, global economic activity remains weak, which results in lower demand for shipping. At the same time, the sector continues to work through an oversupply situation as new ship deliveries are still outpacing the “scrapping” of older vessels. Consequently, charter rates for crude oil tankers and dry bulk vessels are well below historical averages. While we expect a recovery in the next 12 to 24 months, we remain very cautious on these two vessel types. We are much more optimistic about the near-term prospects for refined product and LNG vessels and have positioned our portfolio accordingly. Our investments in the Marine Transportation sector will be concentrated in companies with strong balance sheets, secure distributions and the potential for growth.

Energy Debt, as measured by the Merrill Lynch Energy High Yield Index, generated a total return of 12.0% for fiscal 2012. The Fund’s energy debt portfolio outperformed the index by investing in debt securities issued by Upstream companies with exposure to shale plays. These companies have benefited from improved credit quality as they execute on their strategy and “prove up” the value of their underlying reserves. Nevertheless, we remain cautious about the valuation levels for corporate bonds, and accordingly we have maintained a lower allocation to Energy Debt (13% of long-term investments).

2013 Outlook

Our outlook for 2013 is positive. We expect that distribution growth in the 6% to 7% range will lead to another year of low double-digit total returns for the MLP sector. Continued development of unconventional reserves will create plentiful growth opportunities for both MLPs and Midstream Companies, and we believe there is good visibility for distribution growth for an extended period of time in these sectors given the long-term investments required to develop the shale plays. This outlook, coupled with attractive yields for both MLPs and Midstream Companies, reinforces our belief that these companies remain desirable and sound long-term investments.

While we are cautious on the Marine Transportation sector, we believe the Fund’s portfolio is well positioned to benefit from a market recovery in the next 12 to 18 months. We are optimistic on the outlook for LNG tankers, as low domestic gas prices will increase the demand for these vessels to move LNG to higher priced markets. We are also optimistic on the outlook for refined products vessels, as fewer new vessel deliveries and increasing domestic exports of refined products should cause charter rates to increase.

In the Income Trust sector, we believe it will be critical to remain selective in 2013 as both Canadian and U.S. trusts continue to face challenges. We plan to continue to focus on Canadian trusts that offer attractive

5

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

LETTER TO STOCKHOLDERS

current yields, have strong operating track records and sustainable dividends. Our investments in U.S. trusts will be focused on companies with attractive total return prospects and predictable asset bases.

We look forward to executing on our business plan of achieving high after-tax total returns by investing in a diversified portfolio of MLPs, Midstream Companies, Income Trusts, Marine Transportation and other energy companies. We invite you to visit our website at kaynefunds.com for the latest updates.

Sincerely,

Kevin S. McCarthy

Chairman of the Board of Directors,

President and Chief Executive Officer

6

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

PORTFOLIO SUMMARY

(UNAUDITED)

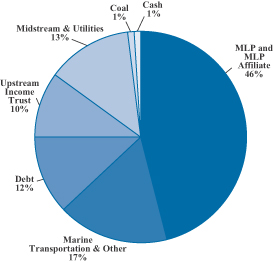

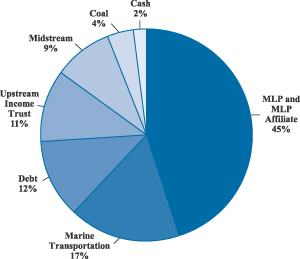

Portfolio Investments by Category

| | |

| November 30, 2012 | | November 30, 2011 |

| |  |

Top 10 Holdings by Issuer

| | | | | | | | | | | | |

| | | | | Percent of Total

Investments* as of

November 30, |

| Holding | | Sector | | 2012 | | 2011 |

1. Kinder Morgan Management, LLC | | MLP Affiliate | | | | 13.1 | % | | | | 13.1 | % |

2. Enbridge Energy Management, L.L.C. | | MLP Affiliate | | | | 9.3 | | | | | 10.4 | |

3. Plains All American Pipeline, L.P. | | Midstream MLP | | | | 7.6 | | | | | 5.4 | |

4. Golar LNG Partners LP | | Marine Transportation | | | | 4.2 | | | | | 2.7 | |

5. Teekay Offshore Partners L.P. | | Marine Transportation | | | | 4.1 | | | | | 4.3 | |

6. Capital Product Partners L.P. | | Marine Transportation | | | | 4.0 | | | | | 1.8 | |

7. The Williams Companies, Inc. | | Midstream | | | | 2.7 | | | | | 2.2 | |

8. Kinder Morgan, Inc. | | Midstream | | | | 2.6 | | | | | 2.7 | |

9. Navios Maritime Partners L.P. | | Marine Transportation | | | | 2.1 | | | | | 2.3 | |

10. Regency Energy Partners LP | | Midstream MLP | | | | 1.9 | | | | | 1.7 | |

| * | Includes cash and repurchase agreement (if any). |

7

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

Fund Overview

Kayne Anderson Energy Total Return Fund, Inc. is a non-diversified, closed-end fund. Our investment objective is to obtain a high total return with an emphasis on current income. We intend to achieve this objective by investing in a portfolio of companies in the energy sector, which focuses on securities of energy companies, with the majority of our investments in equity securities of master limited partnerships and limited liability companies taxed as partnerships (“MLPs”), MLP affiliates, marine transportation companies, midstream companies and upstream income trusts.

As of November 30, 2012, we had total assets of $1.3 billion, net assets applicable to our common stock of $901.8 million (net asset value per share of $25.43), and 35.5 million shares of common stock outstanding. As of November 30, 2012, we held $1.2 billion in equity investments and $166.5 million in debt investments.

Results of Operations — For the Three Months Ended November 30, 2012

Investment Income. Investment income totaled $9.3 million for the quarter and consisted primarily of net dividends and distributions and interest income on our investments. We received $13.9 million of cash dividends and distributions, of which $8.4 million was treated as a return of capital. Interest income was $3.7 million. Return of capital was increased by $0.8 million during the quarter due to 2011 tax reporting information that we received in fiscal 2012. We received $5.4 million of paid-in-kind dividends during the quarter, which are not included in investment income, but are reflected as an unrealized gain.

Operating Expenses. Operating expenses totaled $9.8 million, including $4.2 million of investment management fees, $3.5 million of interest expense, of which $0.2 million was the non-cash amortization of debt issuance costs, and $0.4 million of other operating expenses. Preferred stock distributions for the quarter were $1.7 million, of which $0.1 million was the non-cash amortization of offering costs.

Net Investment Loss. Our net investment loss totaled $0.5 million.

Net Realized Losses. We had net realized losses of $1.3 million. Net realized losses consisted of $3.0 million of losses from our investments and $1.7 million of gains from option activity.

Net Change in Unrealized Losses. We had a net change in unrealized losses of $8.4 million. The net change consisted of $8.1 million of unrealized losses from investments and $0.3 million of net unrealized losses from option activity.

Net Decrease in Net Assets Resulting from Operations. We had a decrease in net assets resulting from operations of $10.2 million. This decrease was comprised of a net investment loss of $0.5 million; net realized losses of $1.3 million; and net unrealized losses of $8.4 million, as noted above.

Results of Operations — For the Fiscal Year Ended November 30, 2012

Investment Income. Investment income totaled $39.2 million for the fiscal year and consisted primarily of net dividends and distributions and interest income on our investments. We received $56.6 million of cash dividends and distributions, of which $32.6 million was treated as a return of capital. Interest income was $14.5 million. Return of capital was increased by $0.8 million during the fiscal year due to 2011 tax reporting information that we received in fiscal 2012. Other income of $0.7 million includes a structuring fee associated with our Class B Unit investment in Capital Product Partners L.P and commitment fees earned from bridge loans during the fiscal year. We received $21.5 million of paid-in-kind dividends during the fiscal year, which are not included in investment income, but are reflected as an unrealized gain.

Operating Expenses. Operating expenses totaled $40.7 million, including $17.0 million of investment management fees, $15.2 million of interest expense, of which $0.9 million was the non-cash amortization of debt issuance costs, and $1.7 million of other operating expenses. Preferred stock distributions for the fiscal year were $6.8 million, of which $0.3 million was the non-cash amortization of offering costs.

8

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

Net Investment Loss. Our net investment loss totaled $1.5 million.

Net Realized Gains. We had net realized gains of $16.5 million. Net realized gains consisted of $8.8 million of gains from our investments, $7.8 million of gains from option activity and $0.1 million of realized losses from foreign currency related transactions.

Net Change in Unrealized Gains. We had a net change in unrealized gains of $58.3 million. The net change consisted of $58.1 million of unrealized gains from investments and $0.2 million of net unrealized gains from option activity.

Net Increase in Net Assets Resulting from Operations. We had an increase in net assets resulting from operations of $73.3 million for the fiscal year. This increase was comprised of a net investment loss of $1.5 million; net realized gains of $16.5 million; and net unrealized gains of $58.3 million, as noted above.

Distributions to Common Stockholders

We pay quarterly distributions to our common stockholders, generally funded by net distributable income (“NDI”) generated from our portfolio investments. NDI is the amount of income received by us from our portfolio investments less operating expenses, subject to certain adjustments as described below. NDI is not a financial measure under the accounting principles generally accepted in the United States of America (“GAAP”). Refer to the “Reconciliation of NDI to GAAP” section below for a reconciliation of this measure to our results reported under GAAP.

Income from portfolio investments includes (a) cash dividends and distributions, (b) paid-in-kind dividends received (i.e., stock dividends), (c) interest income from debt securities and commitment or structuring fees from private investments in public equity (“PIPE investments”) and (d) net premiums received from the sale of covered calls.

Operating expenses include (a) investment management fees paid to our investment adviser, (b) other expenses (mostly due to fees paid to other service providers) and (c) interest expense and preferred stock distributions.

Net Distributable Income (NDI)

(amounts in millions, except for per share amounts)

| | | | | | | | |

| | | Three Months

Ended

November 30,

2012 | | | Fiscal Year

Ended

November 30,

2012 | |

Distributions and Other Income from Investments | | | | | | | | |

Dividends and Distributions | | $ | 13.9 | | | $ | 56.6 | |

Paid-In-Kind Dividends and Distributions | | | 5.4 | | | | 21.5 | |

Interest and Other Income(1) | | | 3.7 | | | | 15.1 | |

Net Premiums Received from Call Options Written | | | 3.1 | | | | 14.2 | |

| | | | | | | | |

Total Distributions and Other Income from Investments | | | 26.1 | | | | 107.4 | |

Expenses | | | | | | | | |

Investment Management Fee | | | (4.2 | ) | | | (17.0 | ) |

Other Expenses | | | (0.4 | ) | | | (1.7 | ) |

Interest Expense | | | (3.3 | ) | | | (14.4 | ) |

Preferred Stock Distributions | | | (1.6 | ) | | | (6.5 | ) |

| | | | | | | | |

Net Distributable Income (NDI) | | $ | 16.6 | | | $ | 67.8 | |

| | | | | | | | |

Weighted Shares Outstanding | | | 35.4 | | | | 35.2 | |

NDI per Weighted Share Outstanding | | $ | 0.47 | | | $ | 1.93 | |

| | | | | | | | |

Adjusted NDI per Weighted Share Outstanding(2) | | $ | 0.48 | | | $ | 1.93 | |

| | | | | | | | |

Distributions paid per Common Share(3) | | $ | 0.48 | | | $ | 1.92 | |

9

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

| (1) | The fiscal year ended November 30, 2012 includes a $0.6 million structuring fee from Capital Product Partners L.P. related to our Class B Unit investment and $0.1 million of commitment fees from bridge loans. |

| (2) | In each of the last three years, The Williams Companies paid two dividends during our fiscal third quarter and no dividends during our fiscal fourth quarter. For the purposes of determining our dividend, we calculate “Adjusted NDI”, which treats the dividend received late in our fiscal third quarter as if it was received during our fiscal fourth quarter. |

| (3) | The distribution of $0.48 per share for the fourth quarter of fiscal 2012 was paid to common stockholders on January 11, 2013. Distributions for fiscal 2012 include the distributions paid in April 2012, July 2012, October 2012 and January 2013. |

Payment of future distributions is subject to Board of Directors approval, as well as meeting the covenants of our debt agreements and terms of our preferred stock. In determining our quarterly distribution to common stockholders, our Board of Directors considers a number of factors that include, but are not limited to:

| | • | | NDI generated in the current quarter; |

| | • | | Expected NDI over the next twelve months, and |

| | • | | Realized and unrealized gains generated by the portfolio. |

Reconciliation of NDI to GAAP

The difference between distributions and other income from investments in the NDI calculation and total investment income as reported in our Statement of Operations is reconciled as follows:

| | • | | GAAP recognizes that a significant portion of the cash distributions received from MLPs is characterized as a return of capital and therefore excluded from investment income, whereas the NDI calculation includes the return of capital portion of such distributions. |

| | • | | NDI includes the value of paid-in-kind dividends, whereas such amounts are not included as investment income for GAAP purposes, but rather are recorded as unrealized gains upon receipt. |

| | • | | NDI includes commitment fees from PIPE investments, whereas such amounts are generally not included in investment income for GAAP purposes, but rather are recorded as a reduction to the cost of the investment. |

| | • | | Many of our investments in debt securities were purchased at a discount or premium to the par value of such security. When making such investments, we consider the security’s yield to maturity, which factors in the impact of such discount (or premium). Interest income reported under GAAP includes the non-cash accretion of the discount (or amortization of the premium) based on the effective interest method. When we calculate interest income for purposes of determining NDI, in order to better reflect the yield to maturity, the accretion of the discount (or amortization of the premium) is calculated on a straight-line basis to the earlier of the expected call date or the maturity date of the debt security. |

| | • | | We may sell covered call option contracts to generate income or to reduce our ownership of certain securities that we hold. In some cases, we are able to repurchase these call option contracts at a price less than the fee that we received, thereby generating a profit. The amount we received from selling call options, less the amount that we pay to repurchase such call option contracts, is included in NDI. For GAAP purposes, premiums received from call option contracts sold is not included in investment income. See Note 2 — Significant Accounting Policies for a full discussion of the GAAP treatment of option contracts. |

10

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

The treatment of expenses included in NDI also differs from what is reported in the Statement of Operations as follows:

| | • | | The non-cash amortization or write-offs of capitalized debt issuance costs and preferred stock offering costs related to our financings is included in interest expense and distributions on mandatory redeemable preferred stock for GAAP purposes, but is excluded from our calculation of NDI. |

Liquidity and Capital Resources

Total leverage outstanding at November 30, 2012 of $433.0 million was comprised of $273.0 million of senior unsecured notes (“Senior Notes”), $40.0 million of borrowings outstanding under our unsecured revolving credit facility (the “Credit Facility”) and $120.0 million of mandatory redeemable preferred stock. During fiscal 2012, we redeemed $28.0 million of our Senior Notes, funded by borrowings from our Credit Facility. Total leverage represented 32% of total assets at November 30, 2012. As of January 24, 2013, we had $8.0 million of borrowings outstanding under our Credit Facility, and we had $0.9 million of cash.

The Credit Facility matures on June 11, 2013 and has a commitment amount of $100.0 million. The interest rate may vary between LIBOR plus 1.75% and LIBOR plus 3.00%, depending on our asset coverage ratios. Outstanding loan balances accrue interest daily at a rate equal to one-month LIBOR plus 1.75% based on current asset coverage ratios. We pay a commitment fee of 0.40% per annum on any unused amounts of the Credit Facility. We expect to renew our Credit Facility prior to its maturity date. A full copy of our Credit Facility is available on our website, www.kaynefunds.com.

At November 30, 2012, our asset coverage ratios under the Investment Company Act of 1940, as amended (the “1940 Act”), were 426% and 308% for debt and total leverage (debt plus preferred stock), respectively. We currently target an asset coverage ratio with respect to our debt of 415%, but at times may be above or below our target depending upon market conditions.

We had $273.0 million of Senior Notes outstanding at November 30, 2012. During 2013, we have $128.0 million of Senior Notes that mature, which we expect to refinance with new notes. Our remaining Senior Notes mature between 2014 and 2018. As of November 30, 2012, we had $120.0 million of mandatory redeemable preferred stock outstanding, which is subject to mandatory redemption in 2017 and 2018.

As of November 30, 2012, our total leverage consisted of both fixed rate (78%) and floating rate (22%) obligations. As of such date, the weighted average interest rate on our total leverage was 4.60%.

11

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2012

(amounts in 000’s, except numbers of option contracts)

| | | | | | | | | | | | |

Description | | | | | | No. of

Shares/Units | | | Value | |

Long-Term Investments — 147.2% | | | | | | | | | | | | |

Equity Investments(1) — 128.7% | | | | | | | | | | | | |

United States — 119.2% | | | | | | | | | | | | |

MLP(2)(3) — 35.8% | | | | | | | | | | | | |

Access Midstream Partners, L.P.(4) | | | 48 | | | $ | 1,674 | |

Alliance Holdings GP, L.P. | | | 63 | | | | 2,892 | |

Alliance Resource Partners, L.P.(4) | | | 14 | | | | 813 | |

BreitBurn Energy Partners L.P. | | | 528 | | | | 9,757 | |

Buckeye Partners, L.P.(5) | | | 117 | | | | 5,900 | |

Buckeye Partners, L.P. — Class B Units(5)(6)(7) | | | 206 | | | | 9,789 | |

Crestwood Midstream Partners LP | | | 227 | | | | 5,292 | |

Crosstex Energy, L.P. | | | 377 | | | | 5,691 | |

DCP Midstream Partners, LP(4) | | | 502 | | | | 21,010 | |

Energy Transfer Equity, L.P.(4) | | | 250 | | | | 11,357 | |

Energy Transfer Partners, L.P.(4) | | | 77 | | | | 3,385 | |

Enterprise Products Partners L.P.(4) | | | 186 | | | | 9,661 | |

Exterran Partners, L.P. | | | 688 | | | | 14,984 | |

Global Partners LP | | | 409 | | | | 10,194 | |

Inergy, L.P. | | | 627 | | | | 11,827 | |

Inergy Midstream, L.P. | | | 348 | | | | 8,184 | |

Lehigh Gas Partners LP(8) | | | 18 | | | | 352 | |

MarkWest Energy Partners, L.P.(5) | | | 299 | | | | 15,471 | |

Mid-Con Energy Partners, LP | | | 520 | | | | 10,769 | |

MPLX LP(8) | | | 55 | | | | 1,584 | |

Niska Gas Storage Partners LLC | | | 212 | | | | 2,373 | |

NuStar Energy L.P. | | | 106 | | | | 4,845 | |

ONEOK Partners, L.P.(4) | | | 18 | | | | 1,019 | |

PetroLogistics LP | | | 493 | | | | 5,778 | |

Plains All American Pipeline, L.P.(5) | | | 2,178 | | | | 101,445 | |

PVR Partners, L.P.(5) | | | 428 | | | | 10,319 | |

Regency Energy Partners LP (4) | | | 1,106 | | | | 24,736 | |

Suburban Propane Partners, L.P.(4) | | | 25 | | | | 985 | |

Summit Midstream Partners, LP(8) | | | 126 | | | | 2,492 | |

Western Gas Partners, LP(4) | | | 29 | | | | 1,430 | |

Williams Partners L.P.(4) | | | 139 | | | | 7,072 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 323,080 | |

| | | | | | | | | | | | |

MLP Affiliates — 33.1% | | | | | | | | | | | | |

Enbridge Energy Management, L.L.C.(6) | | | 4,189 | | | | 123,585 | |

Kinder Morgan Management, LLC(4)(6) | | | 2,303 | | | | 174,779 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 298,364 | |

| | | | | | | | | | | | |

Marine Transportation & Other — 25.0% | | | | | | | | | | | | |

Capital Product Partners L.P. | | | 3,866 | | | | 26,175 | |

Capital Product Partners L.P. — Class B Units(7)(9) | | | 3,333 | | | | 27,800 | |

Golar LNG Limited(4) | | | 75 | | | | 2,931 | |

Golar LNG Partners LP | | | 1,869 | | | | 55,876 | |

Kirby Corporation(4)(10) | | | 208 | | | | 12,045 | |

Navios Maritime Partners L.P. | | | 2,096 | | | | 28,070 | |

See accompanying notes to financial statements.

12

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2012

(amounts in 000’s, except numbers of option contracts)

| | | | | | | | | | | | |

Description | | | | | | No. of

Shares/Units | | | Value | |

Marine Transportation & Other (continued) | | | | | | | | | | |

| | |

Seadrill Limited(4) | | | 307 | | | $ | 11,813 | |

Seadrill Partners LLC(8) | | | 223 | | | | 5,855 | |

Teekay Offshore Partners L.P.(4) | | | 2,040 | | | | 54,329 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 224,894 | |

| | | | | | | | | | | | |

Midstream & Utilities — 15.3% | | | | | | | | | | | | |

CenterPoint Energy, Inc. | | | 50 | | | | 986 | |

Kinder Morgan, Inc.(4) | | | 1,032 | | | | 34,884 | |

Marathon Petroleum Corporation(4) | | | 100 | | | | 5,954 | |

OGE Energy Corp. | | | 102 | | | | 5,816 | |

ONEOK, Inc.(4) | | | 542 | | | | 24,313 | |

Phillips 66(4) | | | 100 | | | | 5,237 | |

The Southern Company | | | 50 | | | | 2,178 | |

Spectra Energy Corp.(4) | | | 639 | | | | 17,857 | |

Targa Resources Corp.(4) | | | 107 | | | | 5,360 | |

The Williams Companies, Inc.(4) | | | 1,095 | | | | 35,947 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 138,532 | |

| | | | | | | | | | | | |

Upstream Income Trust — 8.1% | | | | | | | | | | | | |

Cross Timbers Royalty Trust | | | 73 | | | | 1,938 | |

Enduro Royalty Trust | | | 1,030 | | | | 17,617 | |

Pacific Coast Oil Trust | | | 1,263 | | | | 22,233 | |

SandRidge Mississippian Trust II(11) | | | 427 | | | | 7,146 | |

SandRidge Permian Trust(11) | | | 261 | | | | 4,521 | |

VOC Energy Trust | | | 908 | | | | 12,618 | |

Whiting USA Trust II | | | 422 | | | | 6,877 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 72,950 | |

| | | | | | | | | �� | | | |

Coal — 1.9% | | | | | | | | | | | | |

CONSOL Energy Inc.(4) | | | 239 | | | | 7,483 | |

Peabody Energy Corporation(4) | | | 373 | | | | 9,358 | |

SunCoke Energy, Inc.(4)(10) | | | 15 | | | | 244 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 17,085 | |

| | | | | | | | | | | | |

Total United States (Cost — $747,364) | | | | | | | 1,074,905 | |

| | | | | | | | | | | | |

Canada — 9.5% | | | | | | | | | | | | |

Upstream Income Trust — 6.2% | | | | | | | | | | | | |

Bonavista Corporation(6) | | | 101 | | | | 1,684 | |

Crescent Point Energy Corp. | | | 603 | | | | 23,694 | |

Enerplus Corporation(4)(6) | | | 830 | | | | 11,064 | |

Pengrowth Energy Corporation | | | 3,809 | | | | 19,616 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 56,058 | |

| | | | | | | | | | | | |

Midstream — 3.3% | | | | | | | | | | | | |

Enbridge Inc. | | | 125 | | | | 5,036 | |

Keyera Corp. | | | 53 | | | | 2,515 | |

Pembina Pipeline Corporation | | | 778 | | | | 22,033 | |

| | | | | | | | | | | | |

| | | | | | | | | | | 29,584 | |

| | | | | | | | | | | | |

Total Canada (Cost — $112,403) | | | | 85,642 | |

| | | | | | | | | | | | |

Total Equity Investments (Cost — $859,767) | | | | 1,160,547 | |

| | | | | | | | | | | | |

See accompanying notes to financial statements.

13

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2012

(amounts in 000’s, except numbers of option contracts)

| | | | | | | | | | | | | | | | |

Description | | Interest

Rate | | | Maturity

Date | | | Principal

Amount | | | Value | |

Debt Instruments — 18.5% | | | | | | | | | | | | | | | | |

United States — 16.1% | | | | | | | | | | | | | | | | |

Upstream — 9.9% | | | | | | | | | | | | | | | | |

Aurora Oil & Gas Limited | | | 9.875 | % | | | 2/15/17 | | | $ | 5,660 | | | $ | 6,000 | |

Carrizo Oil & Gas, Inc. | | | 7.500 | | | | 9/15/20 | | | | 7,750 | | | | 7,905 | |

Clayton Williams Energy Inc. | | | 7.750 | | | | 4/1/19 | | | | 9,625 | | | | 9,649 | |

Comstock Resources, Inc. | | | 7.750 | | | | 4/1/19 | | | | 7,750 | | | | 7,847 | |

Comstock Resources, Inc. | | | 9.500 | | | | 6/15/20 | | | | 3,750 | | | | 4,003 | |

EP Energy LLC | | | 9.375 | | | | 5/1/20 | | | | 9,000 | | | | 10,011 | |

Gulfport Energy Corporation | | | 7.750 | | | | 11/1/20 | | | | 5,000 | | | | 4,975 | |

Halcón Resources Corporation | | | 9.750 | | | | 7/15/20 | | | | 14,500 | | | | 15,443 | |

Halcón Resources Corporation | | | 8.875 | | | | 5/15/21 | | | | 3,250 | | | | 3,372 | |

Midstates Petroleum Company, Inc. | | | 10.750 | | | | 10/1/20 | | | | 3,700 | | | | 3,904 | |

PDC Energy, Inc. | | | 7.750 | | | | 10/15/22 | | | | 6,000 | | | | 6,090 | |

Resolute Energy Corporation | | | 8.500 | | | | 5/1/20 | | | | 9,775 | | | | 10,044 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 89,243 | |

| | | | | | | | | | | | | | | | |

Marine Transportation — 3.7% | | | | | | | | | | | | | | | | |

Genco Shipping & Trading Limited(12) | | | 5.000 | | | | 8/15/15 | | | | 5,000 | | | | 1,716 | |

Navios Maritime Holdings Inc. | | | 8.125 | | | | 2/15/19 | | | | 19,102 | | | | 16,905 | |

Teekay Corporation | | | 8.500 | | | | 1/15/20 | | | | 14,165 | | | | 14,979 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | 33,600 | |

| | | | | | | | | | | | | | | | |

Coal — 2.5% | | | | | | | | | | | | | | | | |

Foresight Energy LLC | | | 9.625 | | | | 8/15/17 | | | | 21,000 | | | | 21,945 | |

| | | | | | | | | | | | | | | | |

Total United States (Cost — $143,845) | | | | | | | | | | | | | | | 144,788 | |

| | | | | | | | | | | | | | | | |

Canada — 2.4% | | | | | | | | | | | | | | | | |

Upstream — 2.4% | | | | | | | | | | | | | | | | |

Athabasca Oil Corporation | | | 7.500 | | | | 11/19/17 | | | | (13) | | | | 7,567 | |

Southern Pacific Resource Corp. | | | (14) | | | | 1/7/16 | | | | 13,915 | | | | 14,123 | |

| | | | | | | | | | | | | | | | |

Total Canada (Cost — $21,496) | | | | 21,690 | |

| | | | | | | | | | | | | | | | |

Total Debt Investments (Cost — $165,341) | | | | 166,478 | |

| | | | | | | | | | | | | | | | |

Total Long-Term Investments (Cost — $1,025,108) | | | | 1,327,025 | |

| | | | | | | | | | | | | | | | |

| | | | | | | | |

| | |

| | | No. of

Contracts | | | | |

Liabilities | | | | | | | | |

Call Option Contracts Written(10) | | | | | | | | |

United States | | | | | | | | |

MLP | | | | | | | | |

Access Midstream Partners, L.P., call option expiring 12/21/12 @ $35.00 | | | 450 | | | | (36 | ) |

Alliance Resource Partners, L.P., call option expiring 12/21/12 @ $60.00 | | | 100 | | | | (3 | ) |

DCP Midstream Partners, LP, call option expiring 12/21/12 @ $45.00 | | | 500 | | | | (2 | ) |

Energy Transfer Equity, L.P., call option expiring 12/21/12 @ $45.00 | | | 1,800 | | | | (198 | ) |

Energy Transfer Partners, L.P., call option expiring 12/21/12 @ $42.50 | | | 600 | | | | (102 | ) |

Enterprise Products Partners L.P., call option expiring 1/18/2013 @ $52.50 | | | 500 | | | | (50 | ) |

ONEOK Partners, L.P., call option expiring 12/21/12 @ $60.00 | | | 100 | | | | (3 | ) |

Regency Energy Partners LP, call option expiring 12/21/12 @ $22.50 | | | 760 | | | | (27 | ) |

Suburban Propane Partners, L.P., call option expiring 12/21/12 @ $40.00 | | | 250 | | | | (8 | ) |

Western Gas Partners, LP, call option expiring 12/21/12 @ $50.00 | | | 250 | | | | (11 | ) |

Williams Partners L.P., call option expiring 12/21/12 @ $50.00 | | | 250 | | | | (36 | ) |

| | | | | | | | |

| | | | | | | (476 | ) |

| | | | | | | | |

See accompanying notes to financial statements.

14

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2012

(amounts in 000’s, except numbers of option contracts)

| | | | | | | | |

Description | | No. of

Contracts | | | Value | |

MLP Affiliate | | | | | | | | |

Kinder Morgan Management, LLC, call option expiring 12/21/12 @ $75.00 | | | 700 | | | $ | (101) | |

| | |

Marine Transportation & Other | | | | | | | | |

Golar LNG Limited, call option expiring 12/21/12 @ $40.00 | | | 500 | | | | (27) | |

Golar LNG Limited, call option expiring 12/21/12 @ $45.00 | | | 250 | | | | (2) | |

Kirby Corporation, call option expiring 12/21/12 @ $55.00 | | | 525 | | | | (169) | |

Kirby Corporation, call option expiring 12/21/12 @ $60.00 | | | 250 | | | | (12) | |

Kirby Corporation, call option expiring 1/18/13 @ $60.00 | | | 700 | | | | (81) | |

Seadrill Limited, call option expiring 12/21/12 @ $40.00 | | | 300 | | | | (1) | |

Teekay Offshore Partners L.P., call option expiring 12/21/12 @ $27.00 | | | 12 | | | | (0) | |

| | | | | | | | |

| | | | | | | (292) | |

| | | | | | | | |

Midstream & Utilities | | | | | | | | |

Kinder Morgan, Inc., call option expiring 12/21/12 @ $35.00 | | | 500 | | | | (14) | |

Kinder Morgan, Inc., call option expiring 1/18/13 @ $35.00 | | | 1,000 | | | | (65) | |

Marathon Petroleum Corporation, call option expiring 12/21/12 @ $55.00 | | | 250 | | | | (113) | |

Marathon Petroleum Corporation, call option expiring 12/21/12 @ $57.50 | | | 500 | | | | (146) | |

Marathon Petroleum Corporation, call option expiring 12/21/12 @ $60.00 | | | 250 | | | | (33) | |

ONEOK, Inc., call option expiring 12/21/12 @ $45.00 | | | 500 | | | | (35) | |

ONEOK, Inc., call option expiring 1/18/13 @ $47.50 | | | 500 | | | | (9) | |

Phillips 66, call option expiring 12/21/12 @ $49.00 | | | 375 | | | | (143) | |

Phillips 66, call option expiring 12/21/12 @ $50.00 | | | 625 | | | | (188) | |

Spectra Energy Corp., call option expiring 12/21/12 @ $27.00 | | | 1,000 | | | | (100) | |

Targa Resources Corp., call option expiring 12/21/12 @ $48.00 | | | 250 | | | | (58) | |

Targa Resources Corp., call option expiring 12/21/12 @ $50.00 | | | 225 | | | | (21) | |

Targa Resources Corp., call option expiring 1/18/13 @ $50.00 | | | 400 | | | | (64) | |

The Williams Companies, Inc., call option expiring 1/18/13 @ $33.00 | | | 350 | | | | (37) | |

The Williams Companies, Inc., call option expiring 1/18/13 @ $34.00 | | | 350 | | | | (25) | |

The Williams Companies, Inc., call option expiring 1/18/13 @ $35.00 | | | 1,000 | | | | (49) | |

| | | | | | | | |

| | | | | | | (1,100) | |

| | | | | | | | |

Coal | | | | | | | | |

CONSOL Energy Inc., call option expiring 12/21/12 @ $36.00 | | | 1,000 | | | | (6) | |

CONSOL Energy Inc., call option expiring 12/21/12 @ $39.00 | | | 1,000 | | | | (1) | |

Peabody Energy Corporation, call option expiring 12/21/12 @ $28.00 | | | 500 | | | | (7) | |

Peabody Energy Corporation, call option expiring 1/18/13 @ $26.00 | | | 1,500 | | | | (173) | |

SunCoke Energy, Inc., call option expiring 12/21/12 @ $17.50 | | | 150 | | | | (2) | |

| | | | | | | | |

| | | | | | | (189) | |

| | | | | | | | |

Total United States (Premium Received — $2,060) | | | | | | | (2,158) | |

| | | | | | | | |

Canada | | | | | | | | |

Upstream Income Trust | | | | | | | | |

Enerplus Corporation, call option expiring 12/21/12 @ $13.00 | | | 1,000 | | | | (50) | |

| | | | | | | | |

Total Canada (Premium Received — $49) | | | | (50) | |

| | | | | | | | |

Total Call Option Contracts Written (Premium Received — $2,109) | | | | (2,208) | |

| | | | | | | | |

See accompanying notes to financial statements.

15

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2012

(amounts in 000’s, except number of option contracts)

| | | | | | |

Description | | | | Value | |

Credit Facility | | $ | (40,000 | ) |

Senior Unsecured Notes | | | (273,000 | ) |

Mandatory Redeemable Preferred Stock at Liquidation Value | | | (120,000 | ) |

Other Liabilities | | | (10,406 | ) |

| | | | | | |

Total Liabilities | | | (445,614 | ) |

Other Assets | | | 20,376 | |

| | | | | | |

Total Liabilities in Excess of Other Assets | | | (425,238 | ) |

| | | | | | |

Net Assets Applicable To Common Stockholders | | $ | 901,787 | |

| | | | | | |

| (1) | Unless otherwise noted, equity investments are common units/common shares. |

| (2) | Securities are treated as a publicly-traded partnership for regulated investment company (“RIC”) qualification purposes. To qualify as a RIC for tax purposes, the Fund may directly invest up to 25% of its total assets in equity and debt securities of entities treated as publicly-traded partnerships. The Fund had less than 25% of its total assets invested in publicly-traded partnerships at November 30, 2012. It is the Fund’s intention to be treated as a RIC for tax purposes. |

| (3) | Includes limited liability companies. |

| (4) | Security or a portion thereof is segregated as collateral on option contracts written. |

| (5) | The Fund believes that it is an affiliate of Buckeye Partners, L.P., MarkWest Energy Partners, L.P., Plains All American Pipeline, L.P. and PVR Partners, L.P. See Note 6 — Agreements and Affiliations. |

| (6) | Distributions are paid-in-kind. |

| (7) | Fair valued security, restricted from public sale. See Notes 2, 3 and 7 in Notes to Financial Statements. |

| (8) | Security is not currently paying cash distributions, but is expected to pay cash distributions within the next 12 months. |

| (9) | Security is convertible on a one-for-one basis into common units of Capital Product Partners L.P. and is senior to the common units in terms of liquidation preference and priority of distributions. The Class B units pay quarterly cash distributions of $0.21375 per unit and are convertible at any time at the option of the holder. If Capital Product Partners L.P. does not redeem the Class B units by May 2022, then the distribution increases by 25% per quarter to a maximum of $0.33345 per unit. Capital Product Partners L.P. may force the Class B units to convert into common units after three years (May 2015) if the common unit price exceeds $11.70 per unit, and the Class B units are callable after five years (May 2017) at a price of $9.27 per unit and after seven years (May 2019) at $9.00 per unit. |

| (10) | Security is non-income producing. |

| (11) | Security is treated as a publicly-traded partnership for RIC qualification purposes. |

| (12) | Security is convertible into common shares of the issuer. |

| (13) | Principal amount is 7,500 Canadian dollars. |

| (14) | Floating rate second lien secured term loan. Security pays interest at base rate + 750 basis points (10.75% as of November 30, 2012). |

See accompanying notes to financial statements.

16

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

NOVEMBER 30, 2012

(amounts in 000’s, except share and per share amounts)

| | | | |

ASSETS | | | | |

Investments, at fair value: | | | | |

Non-affiliated (Cost — $973,064) | | $ | 1,184,101 | |

Affiliated (Cost — $52,044) | | | 142,924 | |

| | | | |

Total investments (Cost — $1,025,108) | | | 1,327,025 | |

Cash and cash denominated in foreign currency (Cost — $7,284) | | | 7,288 | |

Deposits with brokers | | | 255 | |

Receivable for securities sold (Cost — $5,106) | | | 5,106 | |

Interest, dividends and distributions receivable (Cost — $4,867) | | | 4,867 | |

Deferred debt issuance and preferred stock offering costs and other assets | | | 2,860 | |

| | | | |

Total Assets | | | 1,347,401 | |

| | | | |

|

LIABILITIES | |

Payable for securities purchased (Cost — $3,349) | | | 3,349 | |

Investment management fee payable | | | 1,375 | |

Call option contracts written (Premiums received — $2,109) | | | 2,208 | |

Accrued directors’ fees and expenses | | | 40 | |

Accrued expenses and other liabilities | | | 5,642 | |

Credit facility | | | 40,000 | |

Senior unsecured notes | | | 273,000 | |

Mandatory redeemable preferred stock, $25.00 liquidation value per share (4,800,000 shares issued and outstanding) | | | 120,000 | |

| | | | |

Total Liabilities | | | 445,614 | |

| | | | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS | | $ | 901,787 | |

| | | | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS CONSIST OF | | | | |

Common stock, $0.001 par value (35,467,035 shares issued and outstanding and 195,200,000 shares authorized) | | $ | 35 | |

Paid-in capital in excess of taxable income | | | 643,919 | |

Accumulated net investment income less distributions not treated as tax return of capital | | | (30,780 | ) |

Accumulated net realized gains less distributions not treated as tax return of capital | | | (13,208 | ) |

Net unrealized gains | | | 301,821 | |

| | | | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS | | $ | 901,787 | |

| | | | |

NET ASSET VALUE PER COMMON SHARE | | $ | 25.43 | |

| | | | |

See accompanying notes to financial statements.

17

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

STATEMENT OF OPERATIONS

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2012

(amounts in 000’s)

| | | | |

INVESTMENT INCOME | | | | |

Income | | | | |

Dividends and distributions: | | | | |

Non-affiliated investments | | $ | 49,550 | |

Affiliated investments | | | 7,068 | |

| | | | |

Total dividends and distributions (after foreign taxes withheld of $1,078) | | | 56,618 | |

Return of capital | | | (32,629 | ) |

| | | | |

Net dividends and distributions | | | 23,989 | |

Interest | | | 14,457 | |

Other income | | | 712 | |

| | | | |

Total investment income | | | 39,158 | |

| | | | |

Expenses | | | | |

Investment management fees | | | 16,991 | |

Administration fees | | | 336 | |

Professional fees | | | 463 | |

Reports to stockholders | | | 214 | |

Custodian fees | | | 165 | |

Directors’ fees and expenses | | | 162 | |

Insurance | | | 84 | |

Other expenses | | | 294 | |

| | | | |

Total expenses — before interest expense and preferred distributions | | | 18,709 | |

Interest expense and amortization of debt issuance costs | | | 15,221 | |

Distributions on mandatory redeemable preferred stock and amortization of offering costs | | | 6,768 | |

| | | | |

Total expenses | | | 40,698 | |

| | | | |

Net Investment Loss | | | (1,540 | ) |

| | | | |

REALIZED AND UNREALIZED GAINS (LOSSES) | | | | |

Net Realized Gains (Losses) | | | | |

Investments — non-affiliated | | | 3,702 | |

Investments — affiliated | | | 5,103 | |

Foreign currency transactions | | | (93 | ) |

Options | | | 7,785 | |

| | | | |

Net Realized Gains | | | 16,497 | |

| | | | |

Net Change in Unrealized Gains (Losses) | | | | |

Investments — non-affiliated | | | 30,830 | |

Investments — affiliated | | | 27,330 | |

Foreign currency translations | | | (10 | ) |

Options | | | 181 | |

| | | | |

Net Change in Unrealized Gains | | | 58,331 | |

| | | | |

Net Realized and Unrealized Gains | | | 74,828 | |

| | | | |

NET INCREASE IN NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS RESULTING FROM OPERATIONS | | $ | 73,288 | |

| | | | |

See accompanying notes to financial statements.

18

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

STATEMENT OF CHANGES IN NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS

(amounts in 000’s, except share amounts)

| | | | | | | | |

| | | For the Fiscal Year Ended

November 30, | |

| | | 2012 | | | 2011 | |

OPERATIONS | | | | | | | | |

Net investment loss(1) | | $ | (1,540 | ) | | $ | (2,702 | ) |

Net realized gains | | | 16,497 | | | | 100,067 | |

Net change in unrealized gains (losses) | | | 58,331 | | | | (75,438 | ) |

| | | | | | | | |

Net Increase in Net Assets Resulting from Operations | | | 73,288 | | | | 21,927 | |

| | | | | | | | |

DIVIDENDS AND DISTRIBUTIONS TO COMMON STOCKHOLDERS(2) | | | | | |

Dividends | | | (24,799 | ) | | | — | |

Distributions — net long-term capital gains | | | — | | | | (66,578 | ) |

Distributions — return of capital | | | (42,717 | ) | | | — | |

| | | | | | | | |

Dividends and Distributions to Common Stockholders | | | (67,516 | ) | | | (66,578 | ) |

| | | | | | | | |

CAPITAL STOCK TRANSACTIONS | | | | | | | | |

Issuance of 74,201 shares of common stock | | | 1,932 | | | | — | |

Underwriting discounts and offering expenses associated with the issuance of common stock | | | (38 | ) | | | — | |

Issuance of 390,359 and 510,293 newly issued shares of common stock from reinvestment of dividends and distributions | | | 10,154 | | | | 13,554 | |

| | | | | | | | |

Net Increase in Net Assets Applicable to Common Stockholders from Capital Stock Transactions | | | 12,048 | | | | 13,554 | |

| | | | | | | | |

Total Increase (Decrease) in Net Assets Applicable to Common Stockholders | | | 17,820 | | | | (31,097 | ) |

| | | | | | | | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS | | | | | | | | |

Beginning of year | | | 883,967 | | | | 915,064 | |

| | | | | | | | |

End of year | | $ | 901,787 | | | $ | 883,967 | |

| | | | | | | | |

| (1) | Distributions on the Fund’s mandatory redeemable preferred stock are treated as an operating expense under GAAP and are included in the calculation of net investment loss. See Note 2 — Significant Accounting Policies. Distributions in the amount of $6,497 paid to mandatory redeemable preferred stockholders for the fiscal year ended November 30, 2012 were characterized as dividend income. Distributions in the amount of $5,796 paid to mandatory redeemable preferred stockholders for the fiscal year ended November 30, 2011 were characterized as long-term capital gains. This characterization is based on the Fund’s earnings and profits. |

| (2) | The information presented in each of these items is a characterization of a portion of the total dividends and distributions paid to common stockholders for the fiscal years ended November 30, 2012 and 2011 as either a dividend (a portion of which may be eligible to be treated as qualified dividend income) or distributions (long-term capital gains or return of capital). This characterization is based on the Fund’s earnings and profits. |

See accompanying notes to financial statements.

19

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

STATEMENT OF CASH FLOWS

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2012

(amounts in 000’s)

| | | | |

CASH FLOWS FROM OPERATING ACTIVITIES | | | | |

Net increase in net assets resulting from operations | | $ | 73,288 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by operating activities: | | | | |

Return of capital distributions | | | 32,629 | |

Net realized gains (excluding foreign currency transactions) | | | (16,590 | ) |

Unrealized gains (excluding impact on cash of foreign currency translations) | | | (58,341 | ) |

Accretion of bond discounts, net | | | (37 | ) |

Purchase of long-term investments | | | (776,908 | ) |

Proceeds from sale of long-term investments | | | 770,104 | |

Increase in deposits with brokers | | | (5 | ) |

Increase in receivable for securities sold | | | (295 | ) |

Increase in interest, dividends and distributions receivable | | | (253 | ) |

Amortization of deferred debt issuance costs | | | 870 | |

Amortization of mandatory redeemable preferred stock offering costs | | | 271 | |

Increase in other assets, net | | | (85 | ) |

Decrease in payable for securities purchased | | | (5,092 | ) |

Increase in investment management fee payable | | | 32 | |

Increase in call option contracts written, net | | | 1,676 | |

Decrease in accrued directors’ fees and expenses | | | (2 | ) |

Decrease in accrued expenses and other liabilities | | | (658 | ) |

| | | | |

Net Cash Provided by Operating Activities | | | 20,604 | |

| | | | |

CASH FLOWS FROM FINANCING ACTIVITIES | | | | |

Issuance of shares of common stock, net of offering costs | | | 1,894 | |

Proceeds from credit facility | | | 40,000 | |

Redemption of senior unsecured notes | | | (28,000 | ) |

Cash distributions paid to common stockholders, net | | | (57,362 | ) |

| | | | |

Net Cash Used in Financing Activities | | | (43,468 | ) |

| | | | |

NET DECREASE IN CASH | | | (22,864 | ) |

CASH — BEGINNING OF YEAR | | | 30,152 | |

| | | | |

CASH — END OF YEAR | | $ | 7,288 | |

| | | | |

Supplemental disclosure of cash flow information:

Non-cash financing activities not included herein consist of reinvestment of distributions of $10,154 pursuant to the Fund’s dividend reinvestment plan. During the fiscal year ended November 30, 2012, interest paid was $14,828, and there were no income taxes paid.

During the fiscal year ended November 30, 2012, the Fund received $21,492 of paid-in-kind dividends. See Note 2 — Significant Accounting Policies.

See accompanying notes to financial statements.

20

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Fiscal Year Ended

November 30, | | | For the

Period

June 28,

2005(1)

through

November 30,

2005 | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Per Share of Common Stock(2) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 25.25 | | | $ | 26.53 | | | $ | 20.04 | | | $ | 13.43 | | | $ | 29.01 | | | $ | 25.44 | | | $ | 24.13 | | | $ | 23.84 | (3) |

Net investment income (loss)(4) | | | (0.04 | ) | | | (0.08 | ) | | | 0.16 | | | | 0.31 | | | | 0.88 | | | | 1.09 | | | | 1.17 | | | | 0.23 | |

Net realized and unrealized gains (losses) | | | 2.14 | | | | 0.71 | | | | 8.24 | | | | 8.26 | | | | (14.09 | ) | | | 4.82 | | | | 2.34 | | | | 0.33 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total income (loss) from operations | | | 2.10 | | | | 0.63 | | | | 8.40 | | | | 8.57 | | | | (13.21 | ) | | | 5.91 | | | | 3.51 | | | | 0.56 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Dividends and distributions — auction rate preferred(4)(5) | | | — | | | | — | | | | — | | | | — | | | | (0.34 | ) | | | (0.50 | ) | | | (0.44 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Common dividends(5) | | | (0.71 | ) | | | — | | | | (1.92 | ) | | | (0.62 | ) | | | (0.38 | ) | | | (0.83 | ) | | | (0.86 | ) | | | (0.23 | ) |

Common dividends — short-term capital gains(5) | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.53 | ) | | | (0.81 | ) | | | (0.04 | ) |

Common distributions — long-term capital gains(5) | | | — | | | | (1.92 | ) | | | — | | | | — | | | | — | | | | (0.48 | ) | | | — | | | | — | |

Common distributions — return of capital(5) | | | (1.21 | ) | | | — | | | | — | | | | (1.34 | ) | | | (1.68 | ) | | | — | | | | (0.03 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total dividends and distributions — common | | | (1.92 | ) | | | (1.92 | ) | | | (1.92 | ) | | | (1.96 | ) | | | (2.06 | ) | | | (1.84 | ) | | | (1.70 | ) | | | (0.27 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Effect of common stock repurchased | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | 0.05 | | | | — | |

Underwriting discounts and offering costs on the issuance of common and preferred stock | | | — | | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.11 | ) | | | — | |

Gain on 765 shares of Series B Preferred Stock redeemed at a discount to liquidation value | | | — | | | | — | | | | — | | | | — | | | | 0.03 | | | | — | | | | — | | | | — | |

Effect of shares issued in reinvestment of distributions | | | — | | | | 0.01 | | | | 0.01 | | | | — | | | | — | | | | — | | | | — | | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total capital stock transactions | | | — | | | | 0.01 | | | | 0.01 | | | | — | | | | 0.03 | | | | — | | | | (0.06 | ) | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net asset value, end of period | | $ | 25.43 | | | $ | 25.25 | | | $ | 26.53 | | | $ | 20.04 | | | $ | 13.43 | | | $ | 29.01 | | | $ | 25.44 | | | $ | 24.13 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Market value per share of common stock, end of period | | $ | 25.02 | | | $ | 23.82 | | | $ | 28.34 | | | $ | 22.28 | | | $ | 10.53 | | | $ | 25.79 | | | $ | 25.00 | | | $ | 21.10 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total investment return based on common stock market value(6) | | | 13.0 | % | | | (9.7 | )% | | | 37.9 | % | | | 139.9 | % | | | (55.2 | )% | | | 10.2 | % | | | 27.2 | % | | | (14.6 | )%(7) |

See accompanying notes to financial statements.

21

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the Fiscal Year Ended

November 30, | | | For the

Period

June 28,

2005(1)

through

November 30,

2005 | |

| | | 2012 | | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Supplemental Data and Ratios(8) | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net assets applicable to common stockholders, end of period | | $ | 901,787 | | | $ | 883,967 | | | $ | 915,064 | | | $ | 677,678 | | | $ | 437,946 | | | $ | 934,434 | | | $ | 806,063 | | | $ | 776,963 | |

Ratio of expenses to average net assets | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Management fees | | | 1.8 | % | | | 1.8 | % | | | 1.7 | % | | | 1.7 | % | | | 1.6 | % | | | 1.7 | % | | | 1.7 | % | | | 1.3 | % |

Other expenses | | | 0.2 | | | | 0.2 | | | | 0.3 | | | | 0.3 | | | | 0.3 | | | | 0.3 | | | | 0.3 | | | | 0.4 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Subtotal | | | 2.0 | | | | 2.0 | | | | 2.0 | | | | 2.0 | | | | 1.9 | | | | 2.0 | | | | 2.0 | | | | 1.7 | |

Interest expense and distributions on mandatory redeemable preferred stock(4) | | | 2.4 | | | | 2.3 | | | | 2.3 | | | | 2.6 | | | | 0.7 | | | | 0.2 | | | | 0.1 | | | | — | |

Management fee waivers | | | — | | | | — | | | | — | | | | — | | | | — | | | | (0.1 | ) | | | (0.3 | ) | | | (0.2 | ) |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total expenses | | | 4.4 | % | | | 4.3 | % | | | 4.3 | % | | | 4.6 | % | | | 2.6 | % | | | 2.1 | % | | | 1.8 | % | | | 1.5 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Ratio of net investment income (loss) to average net assets(4) | | | (0.2 | )% | | | (0.3 | )% | | | 0.7 | % | | | 2.0 | % | | | 3.1 | % | | | 3.8 | % | | | 4.6 | % | | | 2.3 | % |

Net increase (decrease) in net assets applicable to common stockholders resulting from operations to average net assets | | | 7.8 | % | | | 2.3 | % | | | 37.2 | % | | | 55.8 | % | | | (47.7 | )% | | | 19.1 | % | | | 12.3 | % | | | 2.4 | %(7) |

Portfolio turnover rate | | | 57.2 | % | | | 57.6 | % | | | 62.0 | % | | | 88.8 | % | | | 65.0 | % | | | 52.1 | % | | | 63.8 | % | | | 23.2 | %(7) |

Average net assets | | $ | 934,388 | | | $ | 940,587 | | | $ | 771,297 | | | $ | 512,647 | | | $ | 915,456 | | | $ | 906,692 | | | $ | 802,434 | | | $ | 759,550 | |

Senior unsecured notes outstanding, end of period | | | 273,000 | | | | 301,000 | | | | 250,000 | | | | 165,000 | | | | 225,000 | | | | — | | | | — | | | | — | |

Credit facility outstanding, end of period | | | 40,000 | | | | — | | | | 67,000 | | | | 47,000 | | | | — | | | | 41,000 | | | | — | | | | 40,000 | |

Auction rate preferred stock, end of period | | | — | | | | — | | | | — | | | | — | | | | — | | | | 300,000 | | | | 300,000 | | | | — | |

Mandatory redeemable preferred stock, end of period | | | 120,000 | | | | 120,000 | | | | 90,000 | | | | — | | | | — | | | | — | | | | — | | | | — | |

Average shares of common stock outstanding | | | 35,222,412 | | | | 34,742,802 | | | | 34,177,249 | | | | 33,272,958 | | | | 32,258,146 | | | | 32,036,996 | | | | 31,809,344 | | | | 32,204,000 | |

Asset coverage of total debt(9) | | | 426.4 | % | | | 433.5 | % | | | 417.1 | % | | | 419.7 | % | | | 294.6 | %(10) | | | — | | | | — | | | | — | |

Asset coverage of total leverage (debt and preferred stock)(11) | | | 308.3 | % | | | 310.0 | % | | | 324.8 | % | | | 419.7 | % | | | 294.6 | %(10) | | | 374.0 | % | | | 368.7 | % | | | — | |

Average amount of borrowings per share of common stock during the period | | $ | 8.70 | | | $ | 8.92 | | | $ | 7.71 | | | $ | 5.18 | | | $ | 3.53 | | | $ | 0.53 | | | $ | 0.08 | | | | — | |

See accompanying notes to financial statements.

22

KAYNE ANDERSON ENERGY TOTAL RETURN FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| (1) | Commencement of operations. |

| (2) | Based on average shares of common stock outstanding. |

| (3) | Initial public offering price of $25.00 per share less underwriting discounts of $1.125 per share and offering costs of $0.04 per share. |

| (4) | Distributions on the Fund’s mandatory redeemable preferred stock are treated as an operating expense under GAAP and are included in the calculation of net investment income (loss). See Note 2 — Significant Accounting Policies. |