QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on August 2, 2005

Registration No. 333-124396

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Post-Effective

Amendment No. 1

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Advanced Life Sciences Holdings, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or other jurisdiction of incorporation or organization) | 2854 (Primary Standard Industrial Classification Code Number) | 30-0296543 (I.R.S. Employer Identification Number) |

1440 Davey Road

Woodridge, Illinois 60517

(630) 739-6744

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Michael T. Flavin, Ph.D.

Chairman and Chief Executive Officer

Advanced Life Sciences Holdings, Inc.

1440 Davey Road

Woodridge, Illinois 60517

(630) 739-6744

(Name, address, including zip code, and telephone number, including area code, of agent for service)

| Copies to: | ||

| R. Cabell Morris, Jr. Winston & Strawn LLP 35 West Wacker Drive Chicago, Illinois 60601 (312) 558-5600 | Paul M. Kinsella Ropes & Gray LLP One International Place Boston, Massachusetts 02110 (617) 951-7000 | |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If the only securities being registered on this Form are being offered pursuant to dividend or interest reinvestment plans, please check the following box. o

If any of the securities being registered on this Form are being offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

Subject to Completion or Amendment

Preliminary Prospectus dated August 2, 2005

PRELIMINARY PROSPECTUS

6,000,000

Shares of Common Stock

We are offering 5,571,429 shares of our common stock through the underwriters. We are also offering 428,571 shares of our common stock in a concurrent offering directly to a current stockholder in exchange for a $3 million reduction of a milestone payment obligation under our license agreement with the stockholder. The consummation of the initial public offering and the concurrent offering are conditioned upon each other.

We expect the initial public offering price to be between $6.00 and $8.00 per share. The number of shares we are offering in the concurrent offering assumes an initial public offering price of $7.00 per share. The total public offering price, underwriting discount and the net proceeds to us shown in the table below reflect only shares of common stock we are offering through the underwriters.

No public market currently exists for our common stock. Our common stock has been approved for listing on the Nasdaq National Market under the symbol "ADLS."

Investment in our common stock involves risks.

See "Risk Factors" beginning on page 6 of this prospectus.

| | Per Share | Total | ||||

|---|---|---|---|---|---|---|

| Public offering price | $ | $ | ||||

| Underwriting discount | $ | $ | ||||

| Proceeds, before expenses, to us | $ | $ | ||||

The underwriters may also purchase up to an additional 835,714 shares from us at the public offering price less the underwriting discount within 30 days from the date of this prospectus to cover over-allotments of shares.

The underwriters expect to deliver the shares in New York, New York on or about , 2005.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| C.E. UNTERBERG, TOWBIN | THINKEQUITY PARTNERS LLC | |

MERRIMAN CURHAN FORD & CO. | ||

The date of this prospectus is , 2005.

| | Page | |

|---|---|---|

| Prospectus Summary | 1 | |

| Risk Factors | 6 | |

| Special Note Regarding Forward-Looking Statements | 22 | |

| Concurrent Offering | 23 | |

| Use of Proceeds | 24 | |

| Dividend Policy | 25 | |

| Capitalization | 26 | |

| Dilution | 27 | |

| Selected Financial Data | 29 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 30 | |

| Business | 40 | |

| Management | 69 | |

| Related Party Transactions | 81 | |

| Corporate Reorganization | 82 | |

| Principal Stockholders | 83 | |

| Description of Capital Stock | 85 | |

| Shares Eligible for Future Sale | 88 | |

| Underwriting | 90 | |

| Material U.S. Federal Income Tax Consequences to Non-U.S. Holders | 94 | |

| Legal Matters | 97 | |

| Experts | 97 | |

| Where You Can Find More Information | 97 | |

| Index to Consolidated Financial Statements | F-1 |

If it is against the law in any state to make an offer to sell these shares, or to solicit an offer from someone to buy these shares, then this prospectus does not apply to any person in that state, and no offer or solicitation is made by this prospectus to any such person.

You should rely only on the information contained in this prospectus. We have not authorized any person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not making an offering to distribute or sell these securities in any jurisdiction where the distribution or sale is not permitted. You should assume that the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

i

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read this entire prospectus carefully, including the section entitled "Risk Factors," and our financial statements and related notes included elsewhere in this prospectus, before making an investment decision. References in this prospectus to our amended and restated certificate of incorporation and bylaws refer to the certificate of incorporation and bylaws as the same shall be in effect upon completion of the offerings. Unless otherwise specified or the context otherwise requires, references in this prospectus to "we," "our" and "us" refer to Advanced Life Sciences Holdings, Inc. and its wholly-owned operating subsidiary, Advanced Life Sciences, Inc.

Our Business

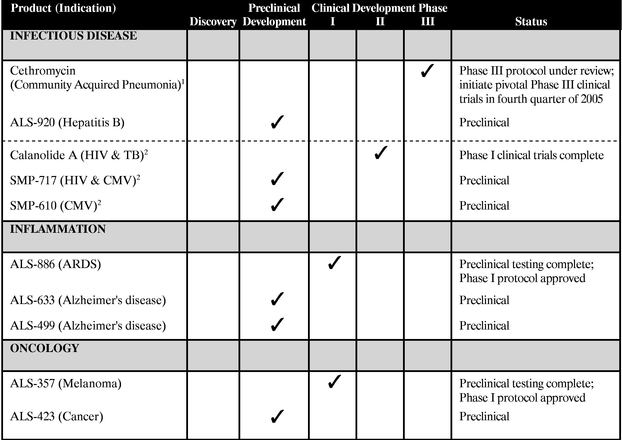

We are a biopharmaceutical company focused on the discovery, development and commercialization of novel drugs in the areas of infectious disease, inflammation and oncology. Using our internal discovery capabilities and our network of pharmaceutical and academic partners, we have assembled a promising pipeline of clinical and preclinical product candidates for the treatment of respiratory tract infections, human immunodeficiency virus (HIV), acute respiratory distress syndrome (ARDS) and cancer. We currently have four product candidates that are either in clinical development or approved to begin clinical development, and six additional product candidates that are in preclinical development.

We have an exclusive worldwide license (excluding Japan) from Abbott Laboratories to develop and commercialize cethromycin, a novel ketolide antibiotic in Phase III clinical development for the treatment of respiratory tract infections. Ketolides, a new class of antibiotic to treat respiratory tract infections, have demonstrated strong activity against bacteria that are resistant to many currently marketed antibiotics. Following the offerings, we intend to conduct two pivotal Phase III clinical trials of cethromycin for the treatment of mild-to-moderate community acquired pneumonia.

Through our 50/50 joint venture, Sarawak MediChem Pharmaceuticals, Inc., we have managed the development of Calanolide A, a potential treatment for HIV. We completed a series of Phase I clinical trials for Calanolide A and, subject to reaching a satisfactory agreement with our joint venture partner regarding our current business arrangement and our respective funding obligations for the next phase of development, we plan to enroll HIV-infected patients for a Phase IIa clinical trial of Calanolide A.

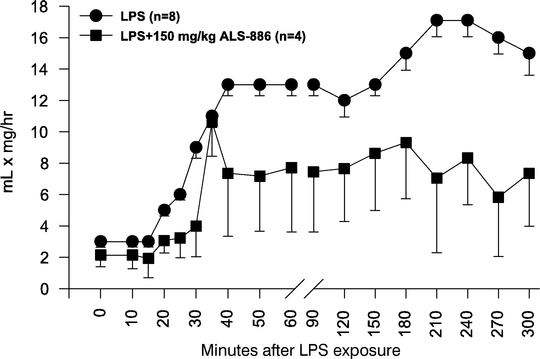

ALS-886 is a novel therapeutic entering clinical development for the treatment of inflammation-related tissue damage, including tissue damage associated with ARDS. We have established an open investigational new drug, or IND, application for ALS-886 with the FDA. We expect that the first Phase I clinical trial will involve approximately 40 patients to determine the safety profile of the compound in human subjects.

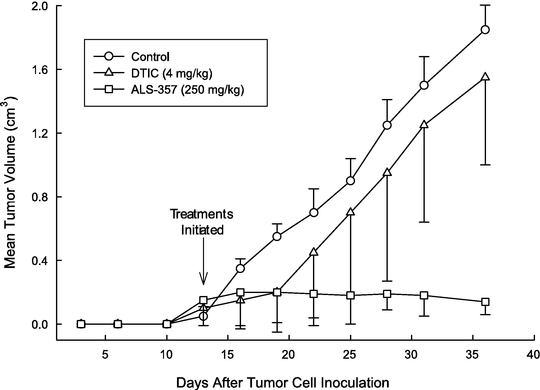

ALS-357 is a compound that has shown anti-tumor activity against malignant melanoma in preclinical trials. We have established an open IND application for ALS-357 with the FDA. The expected Phase I protocol contemplates using a topical cream to treat 16 patients with melanoma that has spread beyond the primary growth site.

In addition to the compounds summarized above, we have additional product candidates in preclinical development. These include compounds derived from natural products to treat infectious diseases, a novel class of synthetic chemotherapeutics to treat various cancers and small molecule inhibitors that may lead to a treatment for Alzheimer's disease.

1

Our Opportunity

We believe that there are attractive opportunities in the discovery, development and commercialization of product candidates in the areas of infectious disease, inflammation and oncology. Although these areas are highly competitive, we believe that the markets for the indications we intend to pursue are either too small or too fragmented for many large pharmaceutical companies. Many large pharmaceutical companies are exiting certain therapeutic areas and looking to out-license developmental products that fail to meet revenue thresholds. Our goal is to take advantage of in-licensing opportunities as they arise while also building on our foundation of internal drug discovery and development. We expect to compete effectively because of the proficiency of our experienced management team and the utility of our integrated chemistry and biology drug discovery platform.

Our Strategy

Our objective is to become a fully integrated pharmaceutical company that discovers and develops small molecule therapeutics to treat life-threatening diseases in the areas of infectious disease, inflammation and cancer, and then markets these products directly to physicians and hospitals. We plan to sustain our drug development pipeline through our internal drug discovery capabilities and by in-licensing promising compounds that fit into our areas of focus. Specific key aspects of our strategy include the following:

- •

- maximize the commercial potential of cethromycin;

- •

- advance the development of our other infectious disease, inflammation and oncology product candidates;

- •

- leverage our drug discovery and development capabilities;

- •

- continue to develop strategic collaborations; and

- •

- build commercial infrastructure to market our products.

None of our product candidates has received FDA marketing approval, and our revenues received to date consist of very limited amounts earned through management fees, grant programs and royalties. Our ability to generate any significant revenues in the near-term will depend solely on the successful development and commercialization of cethromycin, our most advanced product candidate, and our ability to market cethromycin to consumers effectively.

Our Collaborations

An integral part of our strategy is to establish strategic collaborations with leading pharmaceutical and biotechnology companies, governmental institutions and academic laboratories. We have entered into a collaboration with Abbott Laboratories to in-license cethromycin. We have established a 50/50 joint venture with the State Government of Sarawak, Malaysia for the development of Calanolide A. We have also licensed drug compounds from the National Institutes of Health, the University of Illinois at Chicago, Argonne National Laboratory and Baxter International in exchange for royalty and/or milestone obligations. In each of our collaborations, we have assumed complete responsibility to manage the development of the related product candidate.

Drug Discovery and Development Capabilities

We intend to expand our product portfolio by exploiting and enhancing our internal drug discovery and development capabilities. Our drug discovery efforts are focused on natural products, structural biology, medicinal chemistry and targeted biological screening. The integration of chemistry and biology gives us the capability to design, optimize and evaluate high potential drug candidates quickly and cost-effectively. Our chemistry capabilities include a strong emphasis on medicinal chemistry, the

2

discipline that seeks to identify optimal drug candidates through consideration of the biological effects of newly synthesized compounds. We then use our biological screening capabilities to obtain feedback regarding the therapeutic potential of the compounds synthesized by our chemists.

Risks Affecting Us

We are subject to a number of risks that you should be aware of before you decide to buy our common stock. These risks are discussed more fully in "Risk Factors." Our cumulative net loss and working capital deficit as of June 30, 2005 were $41.9 million and $16.4 million, respectively. We anticipate that our cumulative net losses will increase after the offerings. The opinion that we received from our independent registered public accounting firm regarding our 2004 financial statements contains an explanatory paragraph as to our ability to continue as a going concern. We have not received regulatory approval for any of our product candidates, and we do not anticipate generating any significant revenues for at least the next several years, if ever. It is possible that we may never successfully commercialize any of our product candidates.

Recent Development

On August 1, 2005, we agreed with Abbott Laboratories to reduce our royalty payment obligation to Abbott on the net sales of cethromycin if it is approved for commercialization. Under the new terms, we will owe Abbott royalty payments of 19.0% on the first $100 million of aggregate net sales of cethromycin, 18.0% on net sales once aggregate net sales exceed $100 million but are less than $200 million, and 17.0% on all net sales once aggregate net sales exceed $200 million. In addition, we agreed to amend our license agreement with Abbott in order to terminate our in-license of ABT-210, a second-generation ketolide antibiotic product candidate in preclinical development.

We were incorporated as a holding company in Delaware in 2004. Our wholly-owned operating subsidiary, Advanced Life Sciences, Inc., was incorporated in Illinois in 1999. Our principal executive offices are located at 1440 Davey Road, Woodridge, Illinois 60517. Our telephone number is (630) 739-6744. Our web site is http://www.advancedlifesciences.com. We do not intend the information found on our web site to be part of this prospectus and our web site may not contain all of the information that is important to you.

"Advancing Discoveries For Health" and the Advanced Life Sciences logo are trademarks of Advanced Life Sciences, Inc.

References in this prospectus to the offerings are to both the 5,571,429 shares of common stock we are offering through the underwriters in the initial public offering and the 428,571 shares of common stock we are offering in a concurrent offering directly to one of our stockholders.

References to data compiled by IMS Health are reprinted with permission, IMS Health, IMS National Prescription Audit, Copyright 2005, all rights reserved.

3

The Offerings

| Common stock we are offering in our initial public offering | 5,571,429 shares | |

| Common stock we are offering in the concurrent offering | 428,571 shares | |

Common stock to be outstanding after the offerings | 16,826,801 shares | |

Nasdaq National Market symbol | ADLS | |

Use of proceeds | Of the net proceeds from the initial public offering, we intend to use approximately $28.5 million to continue the clinical development of cethromycin and to make milestone and license payments to Abbott Laboratories and the remainder for general corporate purposes, including potential further development of our other product candidates and working capital. See "Use of Proceeds" section of this prospectus. |

The number of shares to be outstanding immediately after this offering is based on the number of shares outstanding as of June 30, 2005, excluding:

- •

- 686,837 shares of common stock issuable upon the exercise of options outstanding under our 1999 Stock Incentive Plan at a weighted average exercise price of $0.93 per share;

- •

- 2,072,455 additional shares of common stock reserved for future issuances under our 2005 Stock Incentive Plan; and

- •

- 14,887 shares of common stock issuable upon the exercise of warrants outstanding at an exercise price of $8.02 per share.

Except as otherwise indicated, information in this prospectus:

- •

- gives effect to a 3.97-for-one stock split effective on June 29, 2005; and

- •

- assumes the underwriters have not exercised their option to purchase 835,714 shares to cover over-allotments.

4

The following table summarizes our consolidated financial data. The summary financial data as of December 31, 2003 and 2004 and for the years ended December 31, 2002, 2003 and 2004 are derived from our audited financial statements included elsewhere in this prospectus. The balance sheet data as of December 31, 2000, 2001 and 2002, and the statement of operations data for the years ended December 31, 2000 and 2001, have been derived from our audited financial statements not included in this prospectus. The balance sheet data as of June 30, 2005 and the statement of operations data for each of the six months ended June 30, 2004 and 2005 have been derived from our unaudited financial statements, which include, in the opinion of management, all adjustments necessary to present fairly the data for such periods. You should read this data together with our financial statements and related notes included elsewhere in this prospectus and the information under "Selected Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations."

| | Years ended December 31, | Six months ended June 30, | Period from Inception (January 1, 1999) to June 30, 2005 | |||||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2000 | 2001 | 2002 | 2003 | 2004 | 2004 | 2005 | |||||||||||||||||||

| Statement of Operations Data: | ||||||||||||||||||||||||||

| Revenue | $ | 447,525 | $ | 225,218 | $ | 496,207 | $ | 180,427 | $ | 319,780 | $ | 182,973 | $ | 44,379 | $ | 2,125,129 | ||||||||||

| Operating expenses: | ||||||||||||||||||||||||||

| Research and development(1) | 3,159,383 | 2,771,517 | 924,799 | 1,362,255 | 25,661,868 | 570,986 | 724,347 | 37,516,266 | ||||||||||||||||||

| Selling, general and administrative | 344,607 | 461,001 | 668,622 | 1,198,722 | 1,649,953 | 639,085 | 780,161 | 5,177,282 | ||||||||||||||||||

| Loss from operations | (3,056,465 | ) | (3,007,300 | ) | (1,097,214 | ) | (2,380,550 | ) | (26,992,041 | ) | (1,027,098 | ) | (1,460,129 | ) | (40,568,419 | ) | ||||||||||

Interest expense, net | 231,930 | 377,029 | 164,337 | 170,938 | 194,877 | 96,389 | 204,249 | 1,370,252 | ||||||||||||||||||

| Net loss | (3,288,395 | ) | (3,384,329 | ) | (1,261,551 | ) | (2,551,488 | ) | (27,186,918 | ) | (1,123,487 | ) | (1,664,378 | ) | (41,938,671 | ) | ||||||||||

| Less accumulating preferred dividends for the period | 175,000 | 175,000 | 175,000 | 175,000 | 175,000 | 87,500 | 87,500 | 1,057,292 | ||||||||||||||||||

| Net loss available to common shareholders | $ | (3,463,395 | ) | $ | (3,559,329 | ) | $ | (1,436,551 | ) | $ | (2,726,488 | ) | $ | (27,361,918 | ) | $ | (1,210,987 | ) | $ | (1,751,878 | ) | $ | (42,995,963 | ) | ||

Basic and diluted loss per common share | $(2.18 | ) | $(2.24 | ) | $(0.90 | ) | $(1.72 | ) | $(13.27 | ) | $(0.76 | ) | $(0.16 | ) | ||||||||||||

Weighted average shares outstanding—basic | 1,588,000 | 1,588,000 | 1,588,000 | 1,588,000 | 2,062,351 | 1,588,134 | 10,780,148 | |||||||||||||||||||

| | As of December 31, | | |||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

As of June 30, 2005 | |||||||||||||||||||

| | 2000 | 2001 | 2002 | 2003 | 2004 | ||||||||||||||

| Balance Sheet Data: | |||||||||||||||||||

| Cash | $ | 94,757 | $ | 7,846 | $ | 18,739 | $ | 61,203 | $ | 194,555 | $ | 39,951 | |||||||

| Total assets | 251,687 | 160,467 | 146,917 | 255,127 | 1,015,932 | 1,769,858 | |||||||||||||

| Long-term debt and lease payable, less current portion | 5,002,992 | 2,000,000 | 2,000,000 | 2,000,000 | 2,027,279 | 2,020,498 | |||||||||||||

| Total liabilities(2) | 5,876,597 | 2,252,835 | 2,339,836 | 2,661,806 | 19,289,733 | 21,102,004 | |||||||||||||

| Deficit accumulated during the development stage | (5,874,910 | ) | (9,274,336 | ) | (10,535,887 | ) | (13,087,375 | ) | (40,274,293 | ) | (41,938,671 | ) | |||||||

| Total stockholders' deficit | (5,624,910 | ) | (2,092,368 | ) | (2,192,919 | ) | (2,406,679 | ) | (18,273,801 | ) | (19,332,146 | ) | |||||||

- (1)

- Amount for 2004 includes approximately $24.5 million of in-process research and development expense related to compounds licensed from Abbott Laboratories in December 2004.

- (2)

- Amount for 2004 includes $14.0 million in payments due in 2005 under our license agreement with Abbott Laboratories executed in December 2004. See Note 11 to our consolidated financial statements. As a result of the concurrent offering, the amount of license payments due to Abbott will be reduced by $3.0 million. See "Concurrent Offering" and "Capitalization."

5

An investment in our common stock involves a high degree of risk. You should carefully consider the following risk factors and other information in this prospectus, including our consolidated financial statements and the notes thereto, before deciding whether to purchase our common stock. Additional risks and uncertainties not presently known to us or that we currently deem immaterial may also impair our business, results of operations and your investment. If any of the events or developments described below actually occurs, our business, financial condition and results of operations may suffer. In that case, the value of our common stock may decline, and you could lose all or part of your investment.

Risks Related to Our Industry and Business

We are at an early stage of development and may never attain product sales.

We have not received FDA approval for any of our product candidates. Any compounds that we discover or in-license will require extensive and costly development, preclinical testing and/or clinical trials prior to seeking regulatory approval for commercial sales. Our most advanced product candidate, cethromycin, and any other compounds we discover, develop or in-license, may never be approved for commercial sale. The time required to attain product sales and profitability is lengthy and highly uncertain, and we cannot assure you that we will be able to achieve or maintain product sales.

We expect our net operating losses to continue for at least several years, and we are unable to predict the extent of future losses or when we will become profitable, if ever.

We have incurred significant net losses since our formation in 1999. Our cumulative net loss was $41.9 million as of June 30, 2005, and we anticipate that our cumulative net losses will increase after the offerings. Our operating losses are due in large part to the significant research and development costs required to identify, validate and license potential product candidates, conduct preclinical studies and conduct clinical trials of our more advanced product candidates. To date, we have generated only limited revenues, consisting of management fees and one-time or limited payments associated with our collaborations or grants, and we do not anticipate generating any significant revenues for at least the next several years, if ever. We expect to increase our operating expenses over the next several years as we plan to:

- •

- expand the clinical trial program for cethromycin;

- •

- continue the preclinical development and commence the clinical development of our other product candidates, such as ALS-886 and ALS-357;

- •

- expand our research and development activities;

- •

- acquire or in-license new technologies and product candidates; and

- •

- increase our required corporate infrastructure and overhead.

As a result, we expect to continue to incur significant and increasing operating losses for the foreseeable future. Because of the numerous risks and uncertainties associated with our research and product development efforts, we are unable to predict the extent of any future losses or when we will become profitable, if ever. Even if we do achieve profitability, we may not be able to sustain or increase profitability on an ongoing basis.

We will require additional funding to satisfy our future capital needs, and future financing strategies may adversely affect holders of our common stock.

Our operations will require significant additional funding in large part due to our research and development expenses, future preclinical and clinical testing costs, the possibility of expanding our

6

facilities, and the absence of any meaningful revenues during the foreseeable future. We do not know whether additional financing will be available to us on favorable terms or at all. If we cannot raise additional funds, we may be required to reduce our capital expenditures, scale back product development or programs, reduce our workforce and license to others products or technologies that we may otherwise be able to commercialize. We believe that the net proceeds from the initial public offering will be sufficient to meet our anticipated operating requirements through 2006; however, we have based this estimate on assumptions that may prove to be incorrect.

To the extent we raise additional capital by issuing equity securities, our stockholders could experience substantial dilution. Any additional equity securities we issue may have rights, preferences or privileges senior to those of existing holders of stock, including purchasers of our common stock in the offerings. To the extent that we raise additional funds through collaboration and licensing arrangements, we may be required to relinquish some rights to our technologies or product candidates, or grant licenses on terms that are not favorable to us.

Our financial statements include a "going concern" limitation, and there is no guarantee that we will be able to operate our business or generate revenues.

Our ability to continue as a going concern is dependent on our ability to raise additional capital, including from the offerings. We do not currently have sufficient capital to fund our operations through 2005. The opinion that we received from our independent registered public accounting firm regarding our 2004 financial statements contains an explanatory paragraph as to our ability to continue as a going concern. If the proceeds from the initial public offering are inadequate to fund our operations through 2006, we may also receive a going concern modification on our 2005 financial statements. If doubts are raised about our ability to continue as a going concern following the offerings, our stock price could drop and our ability to raise additional funds may be adversely affected. Any of these outcomes would be detrimental to our operations.

Following the offerings, we intend to conduct two pivotal Phase III clinical trials of cethromycin for the treatment of mild-to-moderate community acquired pneumonia, and our business would be materially harmed if these trials are unsuccessful.

We anticipate that our ability to generate any significant product revenues in the near future will depend solely on the successful development and commercialization of cethromycin, our most advanced product candidate. Following the offerings, we intend to conduct two pivotal Phase III clinical trials of cethromycin for the treatment of mild-to-moderate community acquired pneumonia. Prior to licensing the compound to us, Abbott Laboratories conducted an initial Phase III clinical trial of cethromycin for the treatment of community acquired pneumonia. Although the results of this study met the primary endpoints for efficacy, this is no assurance that our pivotal Phase III clinical trials will be successful.

The Abbott study used cethromycin dosing levels of 150 mg once-daily and 150 mg twice-daily. Our proposed pivotal Phase III protocol uses a dosing level of 300 mg once-daily, even though Abbott was able to demonstrate efficacy at 150 mg once-daily. We do not expect that the different dosing regimen will reduce the effectiveness of cethromycin in our pivotal Phase III clinical trials, but we could be incorrect. Clinical trials at the higher dosage level are also likely to increase the frequency of adverse side effects. The Abbott study did not include a standard of care comparator arm. Antibiotic products currently in the marketplace are generally effective and, for this reason, the required threshold to demonstrate non-inferiority for new antibiotic compounds is often very high. There can be no assurance that our pivotal Phase III clinical trials of cethromycin will establish non-inferiority when a comparator arm is applied.

The success of our pivotal Phase III clinical trials in treating mild-to-moderate community acquired pneumonia may depend on many factors that are beyond our control and unrelated to the safety or

7

efficacy of cethromycin. For instance, clinical studies may demonstrate lower than expected cure rates because of the lack of patient compliance with prescribed dosing regimens. Cethromycin is our most advanced product candidate, and, as a company, we do not have any prior experience in conducting Phase III clinical trials. If we are unable to complete these trials successfully or ultimately receive FDA marketing approval for cethromycin, our ability to generate revenues and our business will be materially harmed.

Prior clinical trials of cethromycin have shown evidence of side effects that may diminish its prospects for commercialization and wide market acceptance.

The gastrointestinal adverse events reported in prior clinical trials of cethromycin were generally at frequencies consistent with Ketek and other antibiotic treatments. These gastrointestinal side effects included nausea, diarrhea, vomiting, headache and abdominal pain. Taste perversion was the adverse event most frequently observed in prior clinical trials of cethromycin, occurring in 17% of subjects across once-daily dosing regimens of 150 mg, 300 mg and 600 mg. According to available data, taste perversion has not occurred at any significant level for other antibiotic treatments. We do not believe that, by itself, taste perversion presents a safety risk for patients. However, taste perversion may lead to higher levels of patient non-compliance, which could have the effect of reducing overall cure rates in our planned pivotal Phase III clinical trials of cethromycin. If overall cure rates in our pivotal Phase III clinical trials are not sufficient to establish non-inferiority, we may not receive FDA approval for cethromycin and our business will be materially harmed.

Prior pivotal Phase III comparator trials of cethromycin in the treatment of bronchitis and pharyngitis failed to establish non-inferiority, and our inability to expand cethromycin into these indications would harm our ability to generate additional revenues in the future.

Abbott Laboratories conducted four pivotal Phase III comparator trials for cethromycin in treating bronchitis and pharyngitis at a dosing level of 150 mg once-daily. Each of these trials failed to establish non-inferiority against comparator antibiotics. While we believe that the negative outcomes of the Abbott comparator trials were related to dosing levels, we may be incorrect. The failure to meet primary endpoints in the Abbott trials may not have been dose related, as we believe, but rather a result of the compound's lack of sufficient clinical efficacy. Clinical trials using a 300 mg once-daily regimen are also likely to increase the occurrence of adverse side effects. Even if we receive FDA approval to market cethromycin for the treatment of community acquired pneumonia, our failure to expand cethromycin into other indications would harm our ability to generate additional revenues in the future.

Because we are heavily dependent on our license agreement with Abbott Laboratories and our collaborations with other third parties, our product development programs may be delayed or terminated by factors beyond our control.

In December 2004, we entered into a license agreement with Abbott Laboratories for certain patent applications, patents and proprietary technology relating to cethromycin. We have also entered into a number of license agreements for intellectual property and other rights needed to develop our product candidates that are in earlier stages of development. Our primary collaborators other than Abbott include the National Institutes of Health, the University of Illinois at Chicago, Argonne National Laboratory and Baxter International. A description of our agreements with collaborators can be found under the headings "Business—Abbott Laboratories Collaboration" and "Business—Other Collaborations and License Agreements." Our collaborations generally present additional risks to our business, such as the risk that our collaborators encounter conflicts of interest to their arrangements with us, inadequately defend our intellectual property rights or develop other products that compete with us. Our ability to generate any significant product revenues in the near future will depend solely

8

on the successful commercialization of cethromycin. If for any reason we are unable to realize the expected benefits of our license agreement with Abbott, or under any of our other collaborations, then our business and financial condition may be materially harmed.

If we are unable to restructure the debt and joint venture relationship with the State Government of Sarawak, Malaysia, then our development program for Calanolide A may be delayed or abandoned.

The intellectual property for Calanolide A is held by Sarawak MediChem Pharmaceuticals, Inc., our 50/50 joint venture with the State Government of Sarawak, Malaysia. The original intent of our business relationship was that we would contribute intellectual property and management to the joint venture and our partner would provide funding. To advance Calanolide A, the Sarawak Government funded $9 million by purchasing its 50% equity position and loaned an additional $12 million to the joint venture. According to the terms of the loan agreement with the Sarawak Government, $9 million of this debt is past due and $0.5 million and $2.5 million are due in the third and fourth quarters of 2005, respectively. As a result of this default in payment by the joint venture, the Sarawak Government has the option under the loan agreement to take over the control and management of the Calanolide A project or the affairs of the joint venture until such time as the loan is repaid in full. The Sarawak Government recently asserted its rights to assume control of the management of the joint venture. We have initiated discussions with the Sarawak Government to determine the form in which their representative would assume control of the affairs and management of the joint venture. The Sarawak Government also expressly reserved all contractual and legal remedies available in light of the default and indicated its intent to fully exercise its rights as a creditor of the joint venture. Ultimately, we believe that in order for the joint venture to continue, the terms of the debt must be amended to extend its maturity to a date after commercialization of Calanolide A.

Further development will require that we and the Sarawak Government agree to restructure and extend the debt and determine the source of financing for Phase IIa clinical trials of Calanolide A. We have proposed to the Sarawak Government that, for the first time, we would jointly fund the next development phase of Calanolide A through future advances of debt or purchases of equity. We currently estimate that it would cost approximately $2 million to conduct a Phase IIa clinical trial of Calanolide A. No agreement has yet been reached, and we do not intend to expend any meaningful funds advancing the development of Calanolide A unless and until we restructure the joint venture's debt and reach a satisfactory agreement with the Sarawak Government to amend our joint venture relationship and establish our respective obligations regarding the future funding of the next phase of developing Calanolide A. As a result, we are unable to predict when, or if at all, we will proceed with our plans to commence Phase IIa clinical trials for Calanolide A.

Further, our joint venture agreement with the Sarawak Government provides that, upon termination of the joint venture, any liabilities of the joint venture will be settled by the parties equally and all patents or licenses of the joint venture shall be reassigned back to us, including rights to clinical trials. If we and the Sarawak Government are unable to restructure the debt of the joint venture or if any dispute arises with the Sarawak Government, then our ability to continue the development of Calanolide A may be adversely affected, and we may cease future participation in the program. See "Business—Other Collaborations and License Agreements—Sarawak MediChem Pharmaceuticals, Inc."

Because the results of preclinical studies for our preclinical product candidates are not necessarily predictive of future results, our product candidates may not have favorable results in later clinical trials or ultimately receive regulatory approval.

Only two product candidates in our development pipeline, cethromycin and Calanolide A, have been tested in clinical trials. Our other product candidates have only been through preclinical studies. Positive results from preclinical studies, particularlyin vitro studies, are no assurance that later clinical trials will succeed. Preclinical trials are not designed to establish the efficacy of our preclinical product

9

candidates. We will be required to demonstrate through clinical trials that these product candidates are safe and effective for use before we can seek regulatory approvals for their commercial sale. There is typically an extremely high rate of failure as product candidates proceed through clinical trials. If our product candidates fail to demonstrate sufficient safety and efficacy in any clinical trial, we would experience potentially significant delays in, or be required to abandon, development of that product candidate. This would adversely affect our ability to generate revenues and may damage our reputation in the industry and in the investment community.

The future clinical testing of our product candidates could be delayed, resulting in increased costs to us and a delay in our ability to generate revenues.

Our product candidates will require preclinical testing and extensive clinical trials prior to submitting a regulatory application for commercial sales. We do not know whether planned clinical trials will begin on time, if at all. Delays in the commencement of clinical testing could significantly increase our product development costs and delay product commercialization. In addition, many of the factors that may cause, or lead to, a delay in the commencement of clinical trials may also ultimately lead to denial of regulatory approval of a product candidate. Each of these results would adversely affect our ability to generate revenues.

The commencement of clinical trials can be delayed for a variety of reasons, including delays in:

- •

- demonstrating sufficient safety to obtain regulatory approval to commence a clinical trial;

- •

- reaching agreement on acceptable terms with prospective contract research organizations and trial sites;

- •

- manufacturing sufficient quantities of a product candidate; and

- •

- obtaining institutional review board approvals to conduct clinical trials at prospective sites.

In addition, the commencement of clinical trials may be delayed due to insufficient patient enrollment, which is a function of many factors, including the size of the patient population, the nature of the protocol, the proximity of patients to clinical sites, the availability of effective treatments for the relevant disease, and the eligibility criteria for the clinical trial. Because community acquired pneumonia is generally seasonal in nature, achieving sufficient patient enrollment for our pivotal Phase III clinical trials of cethromycin may be particularly difficult. We have not yet received approval from the FDA for our proposed pivotal Phase III protocol in treating mild-to-moderate community acquired pneumonia, and we are not able to begin our pivotal Phase III clinical trials of cethromycin until after we receive this approval.

The FDA required one of our competitors, Aventis Pharmaceuticals, to undertake a 24,000 patient safety study prior to approving Ketek® for commercialization. We do not expect the FDA to require a similarly sized trial for cethromycin because Ketek was the first ketolide introduced and no previous safety testing had been conducted for this class of antibiotics. Since that time, Ketek has been administered to over ten million patients and, to our knowledge, has not demonstrated any severe safety risks. If the FDA does require a large safety trial for cethromycin, however, it would significantly increase our costs and extend the time required to receive regulatory approval.

We will depend on outside parties to conduct our clinical trials, and any failure of those parties to fulfill their obligations could result in costs and delays beyond our control that prevent us from obtaining regulatory approval or successfully commercializing product candidates.

Although we do not currently have any agreements with contract research organizations, we intend to engage contract research organizations to perform data collection and analysis and other aspects of our clinical trials of cethromycin and our other product candidates. We do not have the physical and

10

human resources to conduct our clinical trials independently. The contract research organizations we engage will interact with clinical investigators and medical institutions to enroll patients in our clinical trials. As a result, we will depend on these clinical investigators, medical institutions and contract research organizations to perform the studies and trials properly. If these parties do not successfully carry out their contractual duties or obligations or meet expected deadlines, or if the quality, completeness or accuracy of the clinical data they obtain is compromised due to the failure to adhere to our clinical protocols or for other reasons, our clinical trials may be extended, delayed or terminated. Many of these factors will be outside of our oversight and beyond our control. We may not be able to enter into replacement arrangements without undue delays or considerable expenditures. If there are delays in testing or regulatory approvals as a result of the failure to perform by third parties, our drug discovery and development costs will increase, and we may not be able to obtain regulatory approval for our product candidates. In addition, we may not be able to establish or maintain relationships with these parties on favorable terms, if at all.

Even if we successfully complete clinical trials of cethromycin or any other product candidate, we may fail to obtain FDA approval of a new drug application.

The FDA may not approve in a timely manner, or at all, any NDA we submit. If we are unable to submit an NDA for cethromycin or any other product candidate, or if any NDA we submit is not approved by the FDA, we will be unable to commercialize that product in the United States. The FDA can and does reject NDAs, and often requires additional clinical trials, even when product candidates performed well or achieved favorable results in large-scale Phase III clinical trials. The FDA imposes substantial requirements on the introduction of pharmaceutical products through lengthy and detailed laboratory and clinical testing procedures, sampling activities and other costly and time-consuming procedures. Satisfaction of these requirements typically takes several years and may vary substantially based upon the type and complexity of the pharmaceutical product. A number of our product candidates are novel compounds, which may further increase the period of time required for satisfactory testing procedures.

Data obtained from preclinical and clinical activities are susceptible to varying interpretations, which could delay, limit or prevent regulatory approval. In addition, delays or rejections may be encountered based on changes in, or additions to, regulatory policies for drug approval during the period of product development and regulatory review. The effect of government regulation may be to delay or prevent the commencement of clinical trials or marketing of our product candidates for a considerable period of time, to impose costly procedures upon our activities and to provide an advantage to our competitors that have greater financial resources or are more experienced in regulatory affairs. The FDA may not approve our product candidates for clinical trials or marketing on a timely basis or at all. Delays in obtaining or failure to obtain such approvals would adversely affect the marketing of our product candidates and our liquidity and capital resources.

Drug products and their manufacturers are subject to continual regulatory review after the product receives FDA approval. Later discovery of previously unknown problems with a product or manufacturer may result in additional clinical testing requirements or restrictions on such product or manufacturer, including withdrawal of the product from the market. Failure to comply with applicable regulatory requirements can, among other things, result in fines, injunctions and civil penalties, suspensions or withdrawals of regulatory approvals, product recalls, operating restrictions or shutdown and criminal prosecution. We may lack sufficient resources and expertise to address these and other regulatory issues as they arise.

11

If we fail to obtain regulatory approvals in other countries for our product candidates under development, we will not be able to generate revenues in such countries.

In order to market our products outside of the United States, we must comply with numerous and varying regulatory requirements of other countries. Approval procedures vary among countries and can involve additional product testing and additional administrative review periods. The time required to obtain approval in other countries might differ from that required to obtain FDA approval in the United States. Regulatory approval in one country does not ensure regulatory approval in another, but a failure or delay in obtaining regulatory approval in one country may negatively impact the regulatory process in others. The risks involved in the non-U.S. regulatory approval process, as well as the consequences for failing to comply with applicable regulatory requirements, generally include the same considerations as in the United States. A description of U.S. regulatory considerations can be found under the section entitled "—Even if we successfully complete clinical trials of cethromycin or any other product candidate, we may fail to obtain FDA approval of a new drug application."

Even if we successfully develop and obtain approval for cethromycin or any of our other product candidates, our business will not be profitable if those products do not achieve and maintain market acceptance.

Even if any of our product candidates are approved for commercial sale by the FDA or other regulatory authorities, the degree of market acceptance of any approved product candidate by physicians, healthcare professionals, patients and third-party payors, and our resulting profitability and growth, will depend on a number of factors, including:

- •

- our ability to provide acceptable evidence of safety and efficacy;

- •

- relative convenience and ease of administration;

- •

- the prevalence and severity of any adverse side effects;

- •

- the availability of alternative treatments;

- •

- the details of FDA labeling requirements, including the scope of approved indications and any safety warnings;

- •

- pricing and cost effectiveness;

- •

- the effectiveness of our or our collaborators' sales and marketing strategy;

- •

- our ability to obtain sufficient third-party insurance coverage or reimbursement; and

- •

- our ability to have the product listed on insurance company formularies.

If any of our product candidates achieve market acceptance, we may not be able to maintain that market acceptance over time if new products or technologies are introduced that are received more favorably or are more cost effective. Complications may also arise, such as antibiotic or viral resistance, that render our products obsolete. We rely on the favorable resistance profile of cethromycin exhibited in clinical trials to be a potential competitive distinction from currently marketed compounds. Even if we receive FDA approval to market cethromycin, antibiotic resistance may emerge that will substantially harm our ability to generate revenues from its sale.

We are initially seeking FDA approval for cethromycin as a 7-10 day treatment regimen. There are currently a number of antibiotic products that are marketed as 5-day therapies. In the event that the marketplace considers this to be a significant competitive distinction, it is uncertain whether we will be able to make cethromycin available for a lower dosing period. In addition, we expect that cethromycin, if approved for sale, would be used primarily in the outpatient setting.

12

Our most advanced product candidate, cethromycin, will face significant competition in the marketplace if it receives marketing approval from the FDA.

Initially, we plan to conduct pivotal Phase III clinical trials of cethromycin for the treatment of mild-to-moderate community acquired pneumonia. We also intend to pursue opportunities for cethromycin in the treatment of other respiratory tract infections such as bronchitis, sinusitis and pharyngitis. There are several classes of antibiotics that are primary competitors for the treatment of one or more of these indications, including:

- •

- macrolides such as Biaxin® (clarithromycin), a product of Abbott Laboratories; and Zithromax® (azithromycin), a product of Pfizer Inc.;

- •

- one other ketolide antibiotic, Ketek® (telithromycin), recently launched in the United States and Europe by Aventis Pharmaceuticals;

- •

- semi-synthetic penicillins such as Augmentin® (amoxicillin and clavulanate potassium), a product of GlaxoSmithKline; and

- •

- fluoroquinolones such as Levaquin® (levofloxacin), a product of Ortho-McNeil Pharmaceutical, Inc.; Tequin® (gatifloxacin), a product of Bristol-Myers Squibb Company; FACTIVE® (gemifloxacin mesylate) tablets, a product of Oscient Pharmaceuticals; and Cipro® (ciprofloxacin) and Avelox® (moxifloxacin), both products of Bayer Corporation.

If cethromycin is approved by the FDA, it will not be the first ketolide antibiotic introduced to the marketplace. Ketek has been available for sale in Europe since 2002 and in the United States since August 2004. There are several additional ketolide product candidates in preclinical development or entering clinical development, including ABT-210, a second-generation ketolide antibiotic product candidate that we transferred back to Abbott Laboratories in July 2005. If ultimately approved by the FDA, these product candidates may have improved efficacy, ease of administration or side effect profiles when compared to cethromycin. The availability of additional ketolide antibiotics may have an adverse affect on our ability to generate product revenues and achieve profitability.

The availability of generic equivalents may adversely affect our ability to generate product revenues from cethromycin.

Many generic antibiotics are currently prescribed to treat respiratory tract infections. As competitive products lose patent protection, makers of generic drugs will likely begin to market additional competing products. Companies that produce generic equivalents are generally able to offer their products at lower prices. Ketek may lose patent protection as early as 2015, which would enable generic drug manufacturers to sell generic ketolide antibiotics at a lower cost than cethromycin. Generic equivalents of Biaxin and Zithromax, two macrolide antibiotic products, may be available as early as 2005. Cethromycin, if approved for commerical sale, may be at a competitive disadvantage because of its higher cost relative to generic products. This may have an adverse effect on our ability to generate product revenues from cethromycin.

We will face significant competition from other biotechnology and pharmaceutical companies, and our operating results will suffer if we fail to compete effectively.

We are a development stage company with 20 employees. Many of our competitors, such as Pfizer, GlaxoSmithKline and Bayer, are large pharmaceutical companies with substantially greater financial, technical and human resources than we have. The biotechnology and pharmaceutical industries are intensely competitive and subject to rapid and significant technological change. Many of the drugs that we are attempting to discover or develop will compete with existing therapies if we receive marketing approval. Because of their significant resources, our competitors may be able to use discovery technologies and techniques, or partnerships with collaborators, in order to develop competing products

13

that are more effective or less costly than the product candidates we develop. This may render our technology or product candidates obsolete and noncompetitive. Academic institutions, government agencies, and other public and private research organizations may seek patent protection with respect to potentially competitive products or technologies and may establish exclusive collaborative or licensing relationships with our competitors.

As a company, we do not have any prior experience in conducting Phase III clinical trials. Our competitors may succeed in obtaining FDA or other regulatory approvals for product candidates more rapidly than us. Companies that complete clinical trials, obtain required regulatory agency approvals and commence commercial sale of their drugs before we do may achieve a significant competitive advantage, including certain FDA marketing exclusivity rights that would delay or prevent our ability to market certain products. Any approved drugs resulting from our research and development efforts, or from our joint efforts with our existing or future collaborative partners, might not be able to compete successfully with our competitors' existing or future products.

Our collaborators and third party manufacturers may not be able to manufacture our product candidates in larger quantities, which would prevent us from commercializing our product candidates.

To date, each of our product candidates has been manufactured in small quantities by our collaborators and third party manufacturers for preclinical and clinical trials. We do not currently have any agreements with third party manufacturers. If any of our product candidates is approved by the FDA or other regulatory agencies for commercial sale, we will need to enter into agreements with third parties to manufacture the product in larger quantities. Due to factors beyond our control, our collaborators and third party manufacturers may not be able to increase their manufacturing capacity for any of our product candidates in a timely or economic manner, or at all. Significant scale-up of manufacturing may require additional validation studies, which the FDA must review and approve. If we are unable to increase the manufacturing capacity for a product candidate successfully, the regulatory approval or commercial launch of that product candidate may be delayed or there may be a shortage in the supply of the product candidate. Our product candidates require precise, high-quality manufacturing. The failure of our collaborators and third party manufacturers to achieve and maintain these high manufacturing standards, including the incidence of manufacturing errors, could result in patient injury or death, product recalls or withdrawals, delays or failures in product testing or delivery, cost overruns or other problems that could seriously harm our business.

If we are unable to establish sales and marketing capabilities or enter into agreements with third parties to sell and market any products we may develop, we may be unable to generate revenues.

We do not currently have product sales and marketing capabilities. If we receive regulatory approval to commence commercial sales of any of our product candidates, we will have to establish a sales and marketing organization with appropriate technical expertise and distribution capabilities or make arrangements with third parties to perform these services. If we receive approval to commercialize cethromycin for the treatment of community acquired pneumonia, we intend to market the product directly in the United States. Our ability to generate any significant revenues in the near-term is dependent entirely on the successful commercialization and market acceptance of cethromycin. Factors that may inhibit our efforts to commercialize cethromycin or other product candidates without strategic partners or licensees include:

- •

- difficulty recruiting and retaining adequate numbers of effective sales and marketing personnel;

- •

- the inability of sales personnel to obtain access to, or persuade adequate numbers of, physicians to prescribe our products;

- •

- the lack of complementary products to be offered by sales personnel, which may put us at a competitive disadvantage against companies with broader product lines; and

14

- •

- unforeseen costs associated with creating an independent sales and marketing organization.

As an alternative to establishing our own sales and marketing organization, we may engage other pharmaceutical or health care companies with existing distribution systems and direct sales organizations to assist us in North America and abroad. We may not be able to negotiate favorable distribution partnering arrangements, if at all. To the extent we enter co-promotion or other licensing arrangements, any revenues we receive will depend on the efforts of third parties and will not be under our control. If we are unable to establish adequate sales, marketing and distribution capabilities, whether independently or with third parties, our ability to generate product revenues, and become profitable, would be severely limited.

Off-label promotion of our products could result in substantial penalties.

If any of our product candidates receives marketing approval, we will only be permitted to promote the product for the uses indicated on the label cleared by the FDA. Our pivotal Phase III clinical trials of cethromycin are for the treatment of mild-to-moderate community acquired pneumonia, although we believe that cethromycin may have other applications in bronchitis, pharyngitis and sinusitis. If we request additional label indications for cethromycin or our other product candidates, the FDA may deny those requests outright, require extensive clinical data to support any additional indications or impose limitations on the intended use of any approved products as a condition of approval. U.S. Attorneys' offices and other regulators, in addition to the FDA, have recently focused substantial attention on off-label promotional activities and have initiated civil and criminal investigations related to such practices. If it is determined by these or other regulators that we have promoted our products for off-label use, we could be subject to fines, legal proceedings, injunctions or other penalties.

If our efforts to obtain rights to new products or product candidates from third parties are not successful, we may not generate product revenues or achieve profitability.

Our long-term ability to earn product revenues depends on our ability to identify, through internal research programs, potential product candidates that may be developed into new pharmaceutical products and/or obtain new products or product candidates through licenses from third parties. If our internal research programs do not generate sufficient product candidates, we will need to obtain rights to new products or product candidates from third parties. We may be unable to obtain suitable products or product candidates from third parties for a number of reasons, including:

- •

- we may be unable to purchase or license products or product candidates on terms that would allow us to make an appropriate return from resulting products;

- •

- competitors may be unwilling to assign or license product or product candidate rights to us;

- •

- we may not have access to the capital necessary to purchase or license products or product candidates; or

- •

- we may be unable to locate suitable products or product candidates within, or complementary to, our areas of interest.

If we are unable to obtain rights to new products or product candidates from third parties, our ability to generate product revenues and achieve profitability may suffer.

Because our product candidates and development and collaboration efforts depend on our intellectual property rights, adverse events affecting our intellectual property rights will harm our ability to commercialize products.

Our success will depend to a large degree on our own, our licensees' and our licensors' ability to obtain and defend patents for each party's respective technologies and the compounds and other

15

products, if any, resulting from the application of such technologies. The patent positions of pharmaceutical and biotechnology companies can be highly uncertain and involve complex legal and factual questions. No consistent policy regarding the breadth of claims allowed in biotechnology patents has emerged to date. Accordingly, we cannot predict the breadth of claims that will be allowed or maintained, after challenge, in our or other companies' patents.

The degree of future protection for our proprietary rights is uncertain, and we cannot ensure that:

- •

- we were the first to make the inventions covered by each of our pending patent applications;

- •

- we were the first to file patent applications for these inventions;

- •

- others will not independently develop similar or alternative technologies or duplicate any of our technologies;

- •

- any of our pending patent applications will result in issued patents;

- •

- any patents issued to us or our collaborators will provide a basis for commercially viable products, will provide us with any competitive advantages or will not be challenged by third parties;

- •

- we will develop additional proprietary technologies that are patentable; or

- •

- the patents of others will not have a negative effect on our ability to do business.

We are a party to certain in-license agreements that are important to our business, and we generally do not control the prosecution of in-licensed technology. Accordingly, we are unable to exercise the same degree of control over this intellectual property as we exercise over our internally developed technology. Moreover, some of our academic institution licensors, research collaborators and scientific advisors have rights to publish data and information in which we have rights. If we cannot maintain the confidentiality of our technology and other confidential information in connection with our collaborations, then our ability to receive patent protection or protect our proprietary information will be impaired. In addition, some of the technology we have licensed relies on patented inventions developed using U.S. government resources. Under applicable law, the U.S. government has the right to require us to grant a nonexclusive, partially exclusive, or exclusive license for such technology to a responsible applicant or applicants, upon terms that are reasonable under the circumstances, if the government determines that such action is necessary.

Confidentiality agreements with employees and others may not adequately prevent disclosure of trade secrets and other proprietary information and may not adequately protect our intellectual property.

We rely on trade secrets to protect our technology, particularly when we do not believe patent protection is appropriate or obtainable. However, trade secrets are difficult to protect. In order to protect our proprietary technology and processes, we rely in part on confidentiality and intellectual property assignment agreements with our corporate partners, employees, consultants, outside scientific collaborators and sponsored researchers and other advisors. These agreements may not effectively prevent disclosure of confidential information nor result in the effective assignment to us of intellectual property, and may not provide an adequate remedy in the event of unauthorized disclosure of confidential information or other breaches of the agreements. In addition, others may independently discover our trade secrets and proprietary information, and in such case we could not assert any trade secret rights against such party. Enforcing a claim that a party illegally obtained and is using our trade secrets is difficult, expensive and time consuming, and the outcome is unpredictable. In addition, courts outside the United States may be less willing to protect trade secrets. Costly and time-consuming litigation could be necessary to seek to enforce and determine the scope of our proprietary rights, and failure to obtain or maintain trade secret protection could adversely affect our competitive business position.

16

Market acceptance and sales of our product candidates will be severely limited if we cannot arrange for favorable reimbursement policies.

Our ability to commercialize any product candidates successfully will depend in part on the extent to which governmental authorities, private health insurers and other organizations establish reimbursement levels for the cost of our products and related treatments. Third-party payors are increasingly challenging the prices charged for medical products and services. Also, the trend toward managed health care in the United States, as well as legislative proposals to reform health care, control pharmaceutical prices or reduce government insurance programs, may also result in exclusion of our product candidates from reimbursement programs. Because many generic antibiotics are available for the treatment of respiratory tract infections, our ability to list cethromycin on insurance company formularies will depend on its effectiveness compared to lower-cost products. The cost containment measures that health care payors and providers are instituting, and the effect of any health care reform, could materially and adversely affect our ability to earn revenues from the sales of cethromycin and our other product candidates.

The recent Medicare prescription drug coverage legislation and future legislative or regulatory reform of the healthcare system could limit future revenues from our product candidates.

In the United States, there have been a number of legislative and regulatory proposals to change the healthcare system in ways that could affect our ability to market and sell our product candidates profitably. In particular, in December 2003, President Bush signed into law new Medicare prescription drug coverage legislation. Under this legislation, the Centers for Medicare and Medicaid Services, or CMS, the agency within the Department of Health and Human Services that administers Medicare and will be responsible for reimbursement of the cost of drugs, has asserted the authority of Medicare to elect not to cover particular drugs if CMS determines that the drugs are not "reasonable and necessary" for Medicare beneficiaries or to elect to cover a drug at a lower rate similar to that of drugs that CMS considers to be "therapeutically comparable." Changes in reimbursement policies or health care cost containment initiatives that limit or restrict reimbursement for our products may cause our revenues to decline.

Another development that may affect the pricing of drugs is regulatory action regarding drug reimportation into the United States. The Medicare Prescription Drug, Improvement and Modernization Act of 2003, which became law in December 2003, requires the Secretary of the U.S. Department of Health and Human Services to promulgate regulations allowing drug reimportation from Canada into the United States under certain circumstances. These provisions will become effective only if the Secretary certifies that such imports will pose no additional risk to the public's health and safety and result in significant cost savings to consumers. To date, the Secretary has made no such finding, but he could do so in the future. Proponents of drug reimportation may also attempt to pass legislation that would remove the requirement for the Secretary's certification or allow reimportation under circumstances beyond those anticipated under current law. If legislation is enacted, or regulations issued, allowing the reimportation of drugs, it could decrease the reimbursement we receive for any products that we may commercialize, negatively affecting our anticipated revenues and prospects for profitability.

We will need to increase the size of our organization, and we may encounter difficulties managing our growth, which could adversely affect our results of operations.

We are currently a development stage company with 20 employees. We will need to expand and effectively manage our managerial, operational, financial and other resources in order to successfully pursue our research, development and commercialization effort. To manage any growth, we will be required to continue to improve our operational, financial and management controls, reporting systems and procedures and to attract and retain sufficient numbers of talented employees. We may be unable

17

to successfully manage the expansion of our operations or operate on a larger scale and, accordingly, may not achieve our research, development and commercialization goals.

If we are unable to attract and retain qualified scientific, technical and key management personnel, or if any of our key executives, Michael T. Flavin, Ph.D., Ze-Qi Xu, Ph.D., or John L. Flavin, discontinues his employment with us, it may delay our research and development efforts.

We are highly dependent upon the efforts of our senior management team and scientific staff. The loss of the services of one or more members of the senior management team might impede the achievement of our development objectives. In particular, we are highly dependent upon and our business would be significantly harmed if we lost the services of Michael T. Flavin, Ph.D., our founder and Chairman and Chief Executive Officer, Ze-Qi Xu, Ph.D., our Executive Vice President and Chief Scientific Officer, or John L. Flavin, our President. We do not currently have any key man life insurance policies. We have entered into employment agreements with members of our senior management team, but this does not ensure that we will retain their services for any period of time in the future. Our research and drug discovery programs also depend on our ability to attract and retain highly skilled chemists, biologists and preclinical and clinical personnel. We may not be able to attract or retain qualified scientific personnel in the future due to intense competition among biotechnology and pharmaceutical businesses, particularly in the Chicago area. If we are not able to attract and retain the necessary personnel to accomplish our business objectives, we may experience constraints that will significantly impede the achievement of our research and development objectives and our ability to meet the demands of our collaborators in a timely fashion.

Our business will expose us to potential product liability risks and there can be no assurance that we will be able to acquire and maintain sufficient insurance to provide adequate coverage against potential liabilities.

Our business will expose us to potential product liability risks that are inherent in the testing, manufacturing and marketing of pharmaceutical products. The use of our product candidates in clinical trials also exposes us to the possibility of product liability claims and possible adverse publicity. These risks will increase to the extent our product candidates receive regulatory approval and are commercialized. We do not currently have any product liability insurance, although we plan to obtain product liability insurance in connection with future clinical trials of our product candidates. There can be no assurance that we will be able to obtain or maintain any such insurance on acceptable terms. Moreover, our product liability insurance may not provide adequate coverage against potential liabilities. On occasion, juries have awarded large judgments in class action lawsuits based on drugs that had unanticipated side effects. A successful product liability claim or series of claims brought against us would decrease our cash reserves and could cause our stock price to fall significantly.

We face regulation and risks related to hazardous materials and environmental laws, violations of which may subject us to claims for damages or fines that could materially affect our business, financial condition and results of operations.

Our research and development activities involve the controlled use of hazardous materials and chemicals. The risk of accidental contamination or injury from these materials cannot be completely eliminated. In the event of an accident, we could be held liable for any damages or fines that result, and the liability could have a material adverse effect on our business, financial condition and results of operations. We are also subject to federal, state and local laws and regulations governing the use, manufacture, storage, handling and disposal of hazardous materials and waste products. If we fail to comply with these laws and regulations or with the conditions attached to our operating licenses, the licenses could be revoked, and we could be subjected to criminal sanctions and substantial liability or be required to suspend or modify our operations. In addition, we may have to incur significant costs to

18

comply with future environmental laws and regulations. We do not currently have a pollution and remediation insurance policy.

Our business and operations would suffer in the event of system failures.

Despite the implementation of security measures, our internal computer systems are vulnerable to damage from computer viruses, unauthorized access, natural disasters, terrorism, war and telecommunication and electrical failures. Our drug discovery and preclinical testing systems are highly technical and proprietary. Any system failure, accident or security breach that causes interruptions in our operations could result in a material disruption of our drug discovery programs. To the extent that any disruption or security breach results in a loss or damage to our data or applications, or inappropriate disclosure of confidential or proprietary information, we may incur liability as a result, our drug discovery programs may be adversely affected and the further development of our product candidates may be delayed. In addition, we may incur additional costs to remedy the damages caused by these disruptions or security breaches.

Risks Related to the Offerings

An active trading market for our common stock may not develop, and we expect that our stock price will fluctuate significantly due to events and developments unique to our business or the life sciences industry generally.