Lazard World Dividend & Income Fund, Inc.

Investment Overview

Dear Shareholder,

We are pleased to present this semi-annual report for Lazard World Dividend & Income Fund, Inc. (“LOR” or the “Fund”), for the period ended June 30, 2006. LOR is a diversified, closed-end management investment company that began trading on the New York Stock Exchange (“NYSE”) on June 28, 2005. Its ticker symbol is “LOR.”

The Fund has been in operation for a year, and we are pleased with LOR’s overall performance since inception. We believe that the Fund has provided investors with an attractive yield and diversification, backed by the extensive experience, commitment, and professional management of Lazard Asset Management LLC (the “Investment Manager” or “Lazard”).

Portfolio Update (as of June 30, 2006)

For the second quarter of 2006, the Fund’s Net Asset Value per share (“NAV”) gained 0.6%, beating the benchmark, the Morgan Stanley Capital International (MSCI®) All Country World Index (ACWI®), which fell 0.8% during this period. Similarly, for the year-to-date, the Fund’s NAV return of 9.9% has comfortably outpaced the benchmark return of 6.1% . And since inception, the Fund’s annualized NAV return of 19.3%, compared to the Index return of 18.1% . Shares of LOR ended the second quarter of 2006 with a market price of $19.62, representing a 7.7% discount to the Fund’s NAV of $21.26. The Fund’s net assets were $143.4 million as of June 30, 2006, with total leveraged assets of $211.0 million, representing 32.0% leverage.

We believe that LOR’s investment thesis remains sound. NAV returns, over all the measured time periods since inception, have outperformed the MSCI ACWI Index. Returns on the smaller, short-duration currency and debt portion of the Fund have been relatively modest in 2006, but have been a positive contributor to performance this year and since inception.

As of June 30, 2006, 67.2% of the Fund’s total leveraged assets consisted of world equities and 32.4% consisted of emerging markets currency and debt instruments, while the remaining 0.4% consisted of cash and other assets.

Declaration of Dividends

The Fund’s Board of Directors has declared a monthly dividend distribution of $0.1167 per share on the Fund’s outstanding stock each month since inception. The first dividend was paid on September 23, 2005. This distribution level represents an annualized market yield of 7.1% based on the share price of $19.62 at the close of NYSE trading on June 30, 2006. As per LOR’s policy, all distribution obligations have been met without returning any capital to the Fund’s stockholders.

Additional Information

Please note that available on www.LazardNet.com are frequent updates on the Fund’s performance, press releases, and a monthly fact sheet that provides information about the Fund’s major holdings, sector weightings, regional exposures, and other characteristics. You may also reach Lazard by phone at 1-800-828-5548.

On behalf of Lazard, we thank you for your investment in Lazard World Dividend & Income Fund, Inc. and look forward to continuing to serve your investment needs in the future.

Message from the Portfolio Managers

World Equity Portfolio

(67.2% of total leveraged assets)

The Fund’s equity portfolio is invested primarily in 60 to 90 world equity securities, consisting primarily of the highest dividend-yielding stocks selected from the current holdings of other accounts managed by the Investment Manager. The equity portfolio is broadly diversified in both developed and emerging market countries and across the capitalization spectrum. Examples include Barclays PLC, which provides commercial and investment banking, insurance, financial and asset management services, and operates branches in more than 60 countries worldwide; National Grid PLC, which owns, operates, and develops electricity and gas networks throughout the U.K. and in the northeastern United States; Taiwan Semiconductor Manufacturing Company, which engages in the design, manufacturing, sale, packaging, and testing of integrated circuits and other semiconductor devices; and Statoil, Norway’s largest oil and gas company,

2

Lazard World Dividend & Income Fund, Inc.

Investment Overview (continued)

which is one of the largest net sellers of crude oil in the world and a major supplier of natural gas to the European continent.As of June 30, 2006, the world equity portfolio consisted 34.5% of stocks based in North America, 18.3% were from Continental Europe (not including the U.K.), 20.9% were from the U.K., 6.7% were from Asia, 12.2% were from Australia and New Zealand, 4.1% were Latin America, and 3.3% were from Africa and the Middle East. The world equity portfolio is similarly well diversified across a number of industry sectors. The top two sectors, by weight, at June 30, were financials (23.6%), which includes banks, insurance companies, and financial services companies, and telecommunications services (18.3%), a sector that encompasses those industries that provide voice, data, and video communications services. Other sectors include consumer discretionary, consumer staples, energy, health care, information technology, and industrials. The average dividend yield on the world equity portfolio was 5.4% at June 30.

World Equity Market Review

The rally in world equities continued through the first half of the second quarter of 2006, before stocks fell sharply amid concerns over a potential acceleration in inflation and its implications for future monetary policy. Comments from the newly installed Federal Reserve (“Fed”) Chairman, Benjamin Bernanke, regarding the “unwelcome” increase in prices, called into question the prevailing belief that the cycle of monetary tightening in the U.S. was nearing an end. Concerns that the Fed would continue to aggressively raise rates fueled fears of a material global economic slowdown and a sharp contraction in liquidity, as central banks around the world tightened monetary policy. Not surprisingly, the sectors of the market that had performed best in recent years, such as economically sensitive groups and companies in the fragile economies of Japan and Germany, were hardest hit in the sell-off. Smaller, less-liquid markets, such as Greece and Austria, also lagged in the decline. In contrast, the U.S. and U.K. markets proved resilient.

From a sector perspective, defensive groups, such as utilities and consumer staples, outperformed. Commodity producers were also volatile during the quarter and were particularly hard hit in the sell-off. However, they performed in line with the broad index for the overall quarter, thanks to their strength early in the period. Energy stocks outperformed, as the price of oil proved resilient and ended the quarter near an all-time high. Performing strongly through April, emerging-markets and small-cap stocks were the most severely impacted. Smaller-cap stocks underperformed for the quarter, after significantly outperforming their larger peers in recent years. Emerging-markets equities led markets sharply lower, culminating in close to a 25% decline over a period of approximately one month. Much of the selling appears to have been indiscriminate, with activity focused in relatively liquid shares. Markets then began to recover around the middle of June. Clearly, the markets are concerned about higher interest rates, tighter labor supplies around the world, and high commodity prices, particularly energy-related commodities. Any changes in these macro factors could have strong impacts on the market.

What Helped and What Hurt LOR

Delta Electronics (Taiwan), a technology holding, benefited performance of the Fund’s world equity portfolio, as its shares rose sharply after the company announced solid results. The position was opportunistically sold after its sharp rise and before markets corrected in mid May. BlueScope Steel (Australia), a materials holding, also performed well; a recovery in Asian steel prices was a primary driver of share appreciation, although continued industry consolidation has also helped. The portfolio’s utilities holdings, such as National Grid, Scottish and Southern Energy, and Enel, also benefited performance, as this normally defensive group performed well as the markets began to decline mid quarter.

Conversely, the world equity portfolio’s telecommunications holdings detracted from performance, as Telecom New Zealand declined after the New Zealand government decided that the company may need to provide greater access to its networks, possibly allowing rivals to gain market share. However, the actual regulatory outcome may be more benign than the current valuation would imply. If this is the case, Telecom New Zealand should be able to maintain profitability in the changing regulatory environment. At current levels, the stock is supported by a 9.5% dividend yield. Also hurting performance, Telemar Norte (Brazil) stock fell, after an unsuccessful attempt to simplify its capital structure.

3

Lazard World Dividend & Income Fund, Inc.

Investment Overview (continued)

Emerging Market Currency and Debt Portfolio

(32.4% of total leveraged assets)The Fund also seeks enhanced income through investing in high-yielding, short-duration1 (typically, under one-year) emerging market forward currency contracts and local currency debt instruments. At June 30, this portfolio consisted primarily of forward currency contracts (85.5%), and a smaller allocation to sovereign debt obligations (10.5%) and structured notes (4.0%) and had an average duration of approximately 4.7 months, with an average yield of 8.8% .2

At June 30, the Fund’s emerging market currency and debt holdings were highly diversified across 30 countries within Eastern Europe (17.2%), Asia (26.7%), Latin America (20.5%), the Middle East (7.7%), Africa (17.2%), and the Commonwealth of Independent States and Baltic countries (9.6%) .

Emerging Market Currency and Debt Market Review After a solid first quarter characterized by strong performance and buoyant risk appetite, emerging markets witnessed a tumultuous second quarter. As liquidity continued to be drained slowly by many central banks across the globe, market technicals, risk reduction, and consequent volatility were the important second-quarter themes. Emerging markets currencies experienced directional pressure on the massive outflow of foreign equity capital, and FX volatility rose in the second quarter. Losses were most significant across countries perceived to be overvalued, high-beta to global risk appetite, or simply crowded.

During the past few years, a large number of emerging markets countries have experienced record dollar inflows from current account and/or capital account surpluses, which should have pressured their currencies stronger. Yet, in the growth versus inflation policy trade-off, most central banks chose growth, as central banks absorbed most inflows by increasing FX reserves and expanding money supply, preventing currency appreciation and preserving external competitiveness. Inflation has been rising (albeit from very low levels), and central bank officials are now being forced to take note of the immense size of their reserves (mostly in U.S. dollars) and the currency exposure this implies. Many of these countries are now curtailing these increasingly expensive intervention policies, and are hiking rates to address currency volatility and restore market confidence. Furthermore, rising rates in the developed markets have also pressured emerging market central bankers to tighten monetary policy.

What Helped and Hurt LOR

The portfolio’s large exposure to Russia was the top contributor to performance, driven primarily by the 3.2% appreciation of the currency. Russia continues to see massive dollar inflows, primarily due to oil exports. The Central Bank intervened by accumulating dollars to prevent these inflows from pressuring the ruble stronger. This led to increasing money supply and, consequently, rising inflation. However, with inflation already close to 11% in Russia, there has been a refocus on inflation control, allowing the ruble to appreciate.

Romania was also a leading contributor to performance. The National Bank of Romania has pursued its inflation-targeting policy with added fervor this year, after last year’s policy of easing rates to deter yield-seeking inflows (even in the face of persistent inflation) led to some loss of credibility. The Central Bank hiked rates in the second quarter and significantly raised reserve requirements.

Detracting from performance was the portfolio’s exposure to Turkey. While previously successful in controlling inflation, Turkey’s Central Bank came under scrutiny earlier in 2006. Turkey’s stock market has more than a 60% foreign-investor presence, led by hedge funds and private investors, and many of these investors rushed to the exits, when the stock market began to fall, and risk budgets were slashed. The Central Bank’s downplaying of the sell-off disappointed the already nervous market, and a subsequent release of the inflation numbers confirmed the market’s fears and fueled further panic selling. The Central Bank finally raised rates and announced it would intervene to support the currency. Turkish assets then recovered some of their losses, but still ended the quarter weaker.

Exposure to Colombia also hurt portfolio performance, as capital flight from the fixed income and equity markets led to a sell off in Colombia’s peso.

4

Lazard World Dividend & Income Fund, Inc.

Investment Overview (continued)

Notes to Investment Overview:

| 1 | A measure of the average cash weighted term-to-maturity of the investment holdings. Duration is a measure of the price sensitivity of a bond to interest rate movements. Duration for a forward currency contract is equal to its term-to-maturity. |

| |

| 2 | The quoted yield excludes the implicit cost of borrowing for the forward currency contracts. |

| |

All returns reflect reinvestment of all dividends and distributions. Past performance is not indicative, nor a guarantee, of future results.

The performance data of the index and other market data have been prepared from sources and data that the Investment Manager believes to be reliable, but no representation is made as to their accuracy. The index is unmanaged, has no fees or costs and is not available for investment.

The views of the Fund’s management and the portfolio holdings described in this report are as of June 30, 2006; these views and portfolio holdings may have changed subsequent to this date. Nothing herein should be construed as a recommendation to buy, sell, or hold a particular investment. There is no assurance that the portfolio holdings discussed herein will remain in the Fund at the time you receive this report, or that portfolio holdings sold will have not been repurchased. The specific portfolio holdings discussed may in aggregate represent only a small percentage of the Fund’s holdings. It should not be assumed that investments identified and discussed were, or will be, profitable, or that the investment decisions we make in the future will be profitable, or equal the performance of the investments discussed herein.

The views and opinions expressed are provided for general information only, and do not constitute specific tax, legal, or investment advice to, or recommendations for, any person. There can be no guarantee as to the accuracy of the outlooks for markets, sectors and securities as discussed herein. You should read the Fund’s prospectus for a more detailed discussion of the Fund’s investment objective, strategies, risks and fees.

5

Lazard World Dividend & Income Fund, Inc.

Investment Overview (continued)

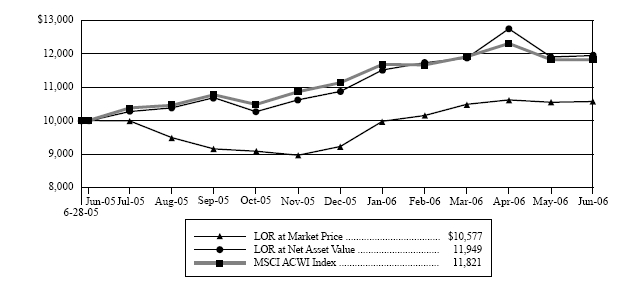

Comparison of Changes in Value of $10,000 Investment in

LOR and MSCI ACWI Index* (unaudited)

Average Annual Total Returns*

Periods Ended June 30, 2006

(unaudited)

| | | One | | Since | |

| | | Year | | Inception** | |

| |

|

| |

|

| |

| Market Price | | 5.66 | % | | 5.72 | % | |

| Net Asset Value | | 19.49 | | | 19.31 | | |

| MSCI ACWI Index | | 18.03 | | | 18.05 | | |

| * | All returns reflect reinvestment of all dividends and distributions. The performance quoted represents past performance. Current performance may be lower or higher than the performance quoted. Past performance is not indicative, nor a guarantee, of future results; the investment return, market price and net asset value of the Fund will fluctuate, so that an investor’s shares in the Fund, when sold, may be worth more or less than their original cost. The returns do not reflect the deduction of taxes that a stockholder would pay on the Fund’s distributions or on the sale of Fund shares. |

| |

| | The performance data of the index has been prepared from sources and data that the Investment Manager believes to be reliable, but no representation is made as to its accuracy. The MSCI ACWI Index is a free float-adjusted market capitalization index that is designed to measure equity market performance in the global developed and emerging markets. The index is unmanaged, has no fees or costs and is not available for investment. |

| |

| ** | The Fund’s inception date was June 28, 2005. |

| |

6

Lazard World Dividend & Income Fund, Inc.

Investment Overview (concluded)

Ten Largest Equity Holdings

June 30, 2006 (unaudited)

| | | | | Percentage |

| Security | Value | | Net Assets |

|

| |

|

| Bank of America Corp. | $ | 5,911,490 | | 4.12 | % |

| Eni SpA | | 5,045,177 | | 3.52 | |

| Bristol-Myers Squibb Co. | | 4,595,322 | | 3.20 | |

| Enel SpA | | 4,475,379 | | 3.12 | |

| Citizens Communications Co. | | 4,363,920 | | 3.04 | |

| Statoil ASA | | 4,044,756 | | 2.82 | |

| Altria Group, Inc. | | 4,016,621 | | 2.80 | |

| Lloyds TSB Group PLC | | 3,933,677 | | 2.74 | |

| Citigroup, Inc. | | 3,704,832 | | 2.58 | |

| OPAP SA | | 3,692,832 | | 2.58 | |

Portfolio Holdings Presented by Sector

June 30, 2006 (unaudited)

| | Percentage of |

| Sector | Total Investments |

|

|

|

| Commercial Services | 0.8 | % |

| Consumer Discretionary | 5.2 | |

| Consumer Durables | 0.5 | |

| Consumer Staples | 7.1 | |

| Emerging Markets Debt Obligations | 6.5 | |

| Energy | 8.3 | |

| Financials | 22.0 | |

| Health Care | 5.3 | |

| Process Industry | 9.9 | |

| Producer Manufacturing | 2.5 | |

| Technology | 1.5 | |

| Telecommunications | 17.0 | |

| Transportation | 1.6 | |

| Utilities | 11.6 | |

| Short-Term Investment | 0.2 | |

|

|

|

| Total Investments | 100.0 | % |

|

|

|

7

Lazard World Dividend & Income Fund, Inc.

Portfolio of Investments

June 30, 2006 (unaudited)

| Description | Shares | | | Value |

|

|

|

|

|

| Common Stocks—97.8% | | | | |

| Australia—9.6% | | | | |

| Amcor, Ltd. (c) | 575,000 | | $ | 2,853,670 |

| Australia and New Zealand Banking Group, Ltd. (c) | 70,660 | | | 1,395,891 |

| BlueScope Steel, Ltd. (c) | 409,775 | | | 2,420,316 |

| Coca-Cola Amatil, Ltd. | 270,608 | | | 1,425,431 |

| National Australia Bank, Ltd. | 51,563 | | | 1,346,935 |

| Telstra Corp., Ltd. (c) | 983,700 | | | 2,689,490 |

| Wesfarmers, Ltd. | 64,779 | | | 1,700,346 |

| | |

|

|

| Total Australia | | | | 13,832,079 |

| | |

|

|

| Brazil—2.9% | | | | |

| Brasil Telecom Participacoes SA ADR | 37,100 | | | 1,208,347 |

| Souza Cruz SA (c) | 203,200 | | | 3,024,176 |

| | |

|

|

| Total Brazil | | | | 4,232,523 |

| | |

|

|

| Greece—3.3% | | | | |

| Motor Oil (Hellas) Corinth Refineries SA | 37,100 | | | 988,606 |

| OPAP SA | 102,052 | | | 3,692,832 |

| | |

|

|

| Total Greece | | | | 4,681,438 |

| | |

|

|

| Hong Kong—1.2% | | | | |

| Pacific Basin Shipping, Ltd. | 3,882,000 | | | 1,761,819 |

| | |

|

|

| Israel—0.9% | | | | |

| Bank Hapoalim BM | 298,400 | | | 1,269,802 |

| | |

|

|

| Italy—9.6% | | | | |

| Enel SpA | 519,300 | | | 4,475,379 |

| Eni SpA | 171,329 | | | 5,045,177 |

| Mediaset SpA | 235,912 | | | 2,781,202 |

| Telecom Italia SpA | 546,376 | | | 1,411,220 |

| | |

|

|

| Total Italy | | | | 13,712,978 |

| | |

|

|

| Japan—1.0% | | | | |

| Ichiyoshi Securities Co., Ltd. | 46,100 | | | 698,063 |

| Nissan Motor Co., Ltd. | 63,900 | | | 698,727 |

| | |

|

|

| Total Japan | | | | 1,396,790 |

| | |

|

|

| Mexico—2.2% | | | | |

| Grupo Mexico SAB de CV, Series B | 530,400 | | | 1,522,457 |

| Kimberly-Clark de Mexico SA de CV | 503,200 | | | 1,601,302 |

| | |

|

|

| Total Mexico | | | | 3,123,759 |

| | |

|

|

| Morocco—1.5% | | | | |

| Maroc Telecom | 167,200 | | | 2,197,764 |

| | |

|

|

| Netherlands—1.8% | | | | |

| Royal Dutch Shell PLC, A Shares | 77,579 | | | 2,608,864 |

| | |

|

|

| New Zealand—2.5% | | | | |

| Telecom Corp. of New Zealand, Ltd. | 1,426,400 | | $ | 3,516,085 |

| | |

|

|

| Norway—3.5% | | | | |

| ABG Sundal Collier ASA | 686,000 | | | 1,045,107 |

| Statoil ASA | 142,600 | | | 4,044,756 |

| | |

|

|

| Total Norway | | | | 5,089,863 |

| | |

|

|

| South Africa—0.8% | | | | |

| Kumba Resources, Ltd. | 64,700 | | | 1,161,230 |

| | |

|

|

| South Korea—1.4% | | | | |

| KT Corp. Sponsored ADR (c) | 91,900 | | | 1,971,255 |

| | |

|

|

| Spain—1.0% | | | | |

| Gestevision Telecinco SA | 57,651 | | | 1,382,164 |

| | |

|

|

| Taiwan—3.0% | | | | |

| Chunghwa Telecom Co., Ltd. Sponsored ADR (c) | 39,300 | | | 725,871 |

| Fubon Financial Holding Co., Ltd. . | 1,625,000 | | | 1,405,318 |

| Taiwan Semiconductor Manufacturing Co., Ltd. | 1,228,778 | | | 2,216,408 |

| | |

|

|

| Total Taiwan | | | | 4,347,597 |

| | |

|

|

| Turkey—0.7% | | | | |

| Turkcell Iletisim Hizmetleri AS ADR | 88,954 | | | 1,054,996 |

| | |

|

|

| United Kingdom—18.9% | | | | |

| Barclays PLC | 196,800 | | | 2,236,728 |

| Dignity PLC | 268,834 | | | 2,371,749 |

| Drax Group PLC (a) | 102,670 | | | 1,560,923 |

| Gallaher Group PLC | 154,500 | | | 2,414,634 |

| HSBC Holdings PLC | 125,300 | | | 2,205,088 |

| Lloyds TSB Group PLC | 400,156 | | | 3,933,677 |

| National Grid PLC | 204,112 | | | 2,208,465 |

| Provident Financial PLC | 95,500 | | | 1,086,287 |

| Royal & Sun Alliance Insurance Group PLC | 628,065 | | | 1,562,403 |

| Royal Bank of Scotland Group PLC | 54,984 | | | 1,808,149 |

| Scottish and Southern Energy PLC | 88,600 | | | 1,886,145 |

| Scottish Power PLC | 118,895 | | | 1,282,030 |

| Tomkins PLC | 196,161 | | | 1,043,985 |

| Vodafone Group PLC | 675,342 | | | 1,439,564 |

| | |

|

|

| Total United Kingdom | | | | 27,039,827 |

| | |

|

|

| United States—32.0% | | | | |

| Altria Group, Inc. (c) | 54,700 | | | 4,016,621 |

| Bank of America Corp. (c) | 122,900 | | | 5,911,490 |

| Brandywine Realty Trust (c) | 35,100 | | | 1,129,167 |

| Bristol-Myers Squibb Co. (c) | 177,700 | | | 4,595,322 |

| Centerplate, Inc. (c) | 90,800 | | | 1,216,720 |

| CenterPoint Energy, Inc. (c) | 59,300 | | | 741,250 |

| Citigroup, Inc. (c) | 76,800 | | | 3,704,832 |

The accompanying notes are an integral part of these financial statements.

8

Lazard World Dividend & Income Fund, Inc.

Portfolio of Investments (continued)

June 30, 2006 (unaudited)

| Description | Shares | | | Value | |

|

|

|

|

|

|

| Citizens Communications Co. (c) | 334,400 | | $ | 4,363,920 | |

| Du Pont (E.I.) de Nemours & Co. (c) | 46,000 | | | 1,913,600 | |

| Embarq Corp. (a) | 17,600 | | | 721,424 | |

| Ferrellgas Partners LP (c) | 30,200 | | | 672,252 | |

| Health Care Property Investors, Inc. (c) | 76,000 | | | 2,032,240 | |

| Healthcare Realty Trust, Inc. | 22,700 | | | 722,995 | |

| Pfizer, Inc. (c) | 49,100 | | | 1,152,377 | |

| Pitney Bowes, Inc. | 24,600 | | | 1,015,980 | |

| The Dow Chemical Co. (c) | 61,800 | | | 2,412,054 | |

| The Southern Co. (c) | 109,300 | | | 3,503,065 | |

| US Shipping Partners LP | 30,700 | | | 648,384 | |

| Verizon Communications, Inc. (c) . | 89,000 | | | 2,980,610 | |

| Weyerhaeuser Co. | 18,300 | | | 1,139,175 | |

| Xcel Energy, Inc. (c) | 64,900 | | | 1,244,782 | |

| | |

|

| |

| Total United States | | | | 45,838,260 | |

| | |

|

| |

| Total Common Stocks | | | | | |

| (Identified cost $137,407,303) | | | | 140,219,093 | |

| | |

|

|

| Preferred Stock—1.1% | | | | | |

| Brazil—1.1% | | | | | |

| Telemar Norte Leste SA | | | | | |

| (Identified cost $1,964,346) (c) | 81,400 | | | 1,632,325 | |

| | |

|

| |

| |

| | Principal | | | | |

| | Amount | | | | |

| Description | (000) (d) | | | Value | |

|

|

|

|

|

|

| | | | | | |

| Foreign Government Obligations—5.2% | | | | | |

| Costa Rica—0.5% | | | | | |

| Costa Rican Treasury Bill, | | | | | |

| 0.00%, 10/11/06 | 386,550 | | | 725,018 | |

| | |

|

| |

| Egypt—3.2% | | | | | |

| Egypt Treasury Bills: | | | | | |

| 0.00%, 09/05/06 | 6,950 | | | 1,188,021 | |

| 0.00%, 09/12/06 | 1,450 | | | 247,440 | |

| 0.00%, 09/26/06 | 7,900 | | | 1,343,563 | |

| 0.00%, 10/17/06 | 10,925 | | | 1,848,669 | |

| | |

|

| |

| Total Egypt | | | | 4,627,693 | |

| | |

|

| |

| Mexico—0.2% | | | | | |

| Mexico Government Bond, | | | | | |

| 9.00%, 12/20/12 | 4,080 | | | 365,180 | |

| | |

|

| |

| Turkey—1.3% | | | | | |

| Turkey Government Bonds: | | | | | |

| 0.00%, 03/07/07 | 1,301 | | $ | 715,169 | |

| 0.00%, 05/09/07 | 552 | | | 292,239 | |

| 15.00%, 02/10/10 | 1,361 | | | 818,228 | |

| | |

|

|

|

| Total Turkey | | | | 1,825,636 | |

| | |

|

|

|

| Total Foreign Government | | | | | |

| Obligations | | | | | |

| (Identified cost $7,893,572) | | | | 7,543,527 | |

| | |

|

|

|

| Structured Notes—1.7% | | | | | |

| Brazil—1.2% | | | | | |

| Citibank Brazil Inflation-Linked | | | | | |

| Bond NTN-B: | | | | | |

| 10.52%, 05/18/09 (e) | 557 | | | 540,714 | |

| 10.54%, 08/17/10 (e) | 698 | | | 672,041 | |

| 9.90%, 05/18/15 (e) | 659 | | | 581,807 | |

| | |

|

|

|

| Total Brazil | | | | 1,794,562 | |

| | |

|

|

|

| Colombia—0.2% | | | | | |

| Citibank Colombia TES Linked Deposit, | | | | | |

| 10.83%, 04/26/12 (e) | 251 | | | 235,047 | |

| | |

|

|

|

| Zambia—0.3% | | | | | |

| Smith Barney ZMK Linked Deposit, | | | | | |

| 13.00%, 09/29/06 | 1,304,500 | | | 372,183 | |

| | |

|

|

|

| Total Structured Notes | | | | | |

| (Identified cost $2,544,784) | | | | 2,401,792 | |

| | |

|

|

|

| Repurchase Agreement—0.2% | | | | | |

| State Street Bank and Trust Co., | | | | | |

| 3.98%, 07/03/06 | | | | | |

| (Dated 06/30/06, collateralized by | | | | | |

| $245,000 United States Treasury | | | | | |

| Note, 4.625%, 03/31/08, with a | | | | | |

| value of $245,520) | | | | | |

| Proceeds of $237,079 | | | | | |

| (Identified cost $237,000) (c) | $237 | | | 237,000 | |

| | |

|

|

|

| Total Investments—106.0% | | | | | |

| (Identified cost $150,047,005) (b) | | | $ | 152,033,737 | |

| Liabilities in Excess of Cash | | | | | |

| and Other Assets—(6.0)% | | | | (8,630,126 | ) |

| | |

|

|

|

| Net Assets—100.0% | | | $ | 143,403,611 | |

| | |

|

|

|

The accompanying notes are an integral part of these financial statements.

9

Lazard World Dividend & Income Fund, Inc.

Portfolio of Investments (continued)

June 30, 2006 (unaudited)

Forward Currency Contracts open at June 30, 2006:

| | | | | | | | U.S. $ Cost | | | U.S. $ | | | | | | |

| Forward Currency | | Expiration | | Foreign | | | on Origination | | | Current | | | Unrealized | | | Unrealized |

| Purchase Contracts | | Date | | Currency | | | Date | | | Value | | | Appreciation | | | Depreciation |

| |

| |

| |

|

| |

|

| |

|

| |

|

|

| ARS | | 07/11/06 | | 2,895,799 | | $ | 937,000 | | $ | 937,024 | | $ | 24 | | $ | — |

| ARS | | 07/12/06 | | 1,168,700 | | | 377,000 | | | 378,094 | | | 1,094 | | | — |

| ARS | | 07/14/06 | | 993,495 | | | 321,000 | | | 321,286 | | | 286 | | | — |

| ARS | | 07/17/06 | | 1,091,935 | | | 353,000 | | | 352,913 | | | — | | | 87 |

| ARS | | 07/28/06 | | 1,165,278 | | | 383,000 | | | 375,807 | | | — | | | 7,193 |

| BRL | | 09/01/06 | | 5,505,701 | | | 2,459,000 | | | 2,520,598 | | | 61,598 | | | — |

| BRL | | 12/20/06 | | 1,114,775 | | | 430,000 | | | 497,710 | | | 67,710 | | | — |

| BRL | | 12/28/06 | | 1,570,000 | | | 641,733 | | | 699,716 | | | 57,983 | | | — |

| BWP | | 07/05/06 | | 2,342,812 | | | 430,000 | | | 388,533 | | | — | | | 41,467 |

| BWP | | 07/10/06 | | 2,295,082 | | | 392,000 | | | 380,245 | | | — | | | 11,755 |

| BWP | | 07/19/06 | | 1,526,138 | | | 257,000 | | | 252,409 | | | — | | | 4,591 |

| BWP | | 07/20/06 | | 2,144,629 | | | 363,000 | | | 354,631 | | | — | | | 8,369 |

| BWP | | 08/22/06 | | 1,828,371 | | | 326,000 | | | 300,437 | | | — | | | 25,563 |

| BWP | | 09/05/06 | | 2,927,752 | | | 479,000 | | | 479,818 | | | 818 | | | — |

| CLP | | 07/17/06 | | 203,962,500 | | | 375,000 | | | 377,889 | | | 2,889 | | | — |

| CLP | | 07/20/06 | | 166,358,500 | | | 319,000 | | | 308,215 | | | — | | | 10,785 |

| COP | | 07/10/06 | | 1,041,006,500 | | | 449,000 | | | 402,942 | | | — | | | 46,058 |

| COP | | 07/21/06 | | 501,540,000 | | | 195,000 | | | 193,998 | | | — | | | 1,002 |

| COP | | 07/27/06 | | 1,193,567,500 | | | 505,000 | | | 461,504 | | | — | | | 43,496 |

| COP | | 08/08/06 | | 1,575,921,750 | | | 611,000 | | | 608,950 | | | — | | | 2,050 |

| COP | | 08/11/06 | | 705,472,000 | | | 302,000 | | | 272,560 | | | — | | | 29,440 |

| COP | | 08/24/06 | | 3,266,520,000 | | | 1,304,000 | | | 1,261,206 | | | — | | | 42,794 |

| COP | | 09/08/06 | | 894,558,000 | | | 361,000 | | | 345,092 | | | — | | | 15,908 |

| COP | | 10/10/06 | | 937,886,000 | | | 404,000 | | | 361,068 | | | — | | | 42,932 |

| COP | | 11/17/06 | | 350,640,000 | | | 144,000 | | | 134,669 | | | — | | | 9,331 |

| CSD | | 08/11/06 | | 25,293,000 | | | 361,277 | | | 375,413 | | | 14,136 | | | — |

| EUR | | 07/27/06 | | 420,000 | | | 526,617 | | | 538,075 | | | 11,458 | | | — |

| EUR | | 08/08/06 | | 968,000 | | | 1,220,677 | | | 1,241,113 | | | 20,436 | | | — |

| GHC | | 08/31/06 | | 1,355,756,000 | | | 146,000 | | | 146,899 | | | 899 | | | — |

| GHC | | 09/07/06 | | 4,953,273,000 | | | 527,000 | | | 536,249 | | | 9,249 | | | — |

| GHC | | 09/18/06 | | 1,047,358,000 | | | 111,599 | | | 113,240 | | | 1,641 | | | — |

| GHC | | 10/13/06 | | 1,283,279,000 | | | 137,000 | | | 138,284 | | | 1,284 | | | — |

| IDR | | 07/27/06 | | 3,083,960,000 | | | 326,000 | | | 332,933 | | | 6,933 | | | — |

| IDR | | 09/19/06 | | 16,572,200,000 | | | 1,720,000 | | | 1,789,075 | | | 69,075 | | | — |

| IDR | | 11/13/06 | | 3,357,185,000 | | | 377,000 | | | 362,430 | | | — | | | 14,570 |

| ILS | | 09/19/06 | | 6,155,410 | | | 1,370,000 | | | 1,386,841 | | | 16,841 | | | — |

| ILS | | 09/29/06 | | 1,630,658 | | | 356,000 | | | 367,371 | | | 11,371 | | | — |

| INR | | 07/05/06 | | 72,353,520 | | | 1,558,000 | | | 1,571,343 | | | 13,343 | | | — |

| INR | | 07/07/06 | | 16,766,420 | | | 374,000 | | | 364,108 | | | — | | | 9,892 |

| INR | | 08/17/06 | | 9,931,650 | | | 219,000 | | | 215,477 | | | — | | | 3,523 |

| INR | | 09/05/06 | | 55,592,500 | | | 1,202,000 | | | 1,205,606 | | | 3,606 | | | — |

| ISK | | 07/10/06 | | 25,814,295 | | | 351,000 | | | 339,013 | | | — | | | 11,987 |

| KRW | | 07/05/06 | | 1,760,673,000 | | | 1,817,000 | | | 1,856,187 | | | 39,187 | | | — |

| KRW | | 08/07/06 | | 1,716,911,000 | | | 1,813,000 | | | 1,811,980 | | | — | | | 1,020 |

| KRW | | 08/08/06 | | 278,772,800 | | | 296,000 | | | 294,218 | | | — | | | 1,782 |

| KZT | | 09/15/06 | | 23,911,630 | | | 200,500 | | | 202,552 | | | 2,052 | | | — |

| KZT | | 12/15/06 | | 23,835,440 | | | 200,500 | | | 202,351 | | | 1,851 | | | — |

| MXN | | 08/17/06 | | 8,569,000 | | | 760,809 | | | 757,215 | | | — | | | 3,594 |

| MXN | | 11/24/06 | | 7,791,679 | | | 687,000 | | | 684,576 | | | — | | | 2,424 |

The accompanying notes are an integral part of these financial statements.

10

Lazard World Dividend & Income Fund, Inc.

Portfolio of Investments (continued)

June 30, 2006 (unaudited)

Forward Currency Contracts open at June 30, 2006 (continued):

| | | | | | | | U.S. $ Cost | | | U.S. $ | | | | | | |

| Forward Currency | | Expiration | | Foreign | | | on Origination | | | Current | | | Unrealized | | | Unrealized |

| Purchase Contracts | | Date | | Currency | | | Date | | | Value | | | Appreciation | | | Depreciation |

| |

| |

| |

|

| |

|

| |

|

| |

|

|

| MXN | | 01/08/07 | | 3,997,965 | | $ | 358,000 | | $ | 350,274 | | $ | — | | $ | 7,726 |

| MXN | | 03/30/07 | | 4,133,238 | | | 366,000 | | | 360,085 | | | — | | | 5,915 |

| MYR | | 07/12/06 | | 1,932,480 | | | 528,000 | | | 526,296 | | | — | | | 1,704 |

| MYR | | 07/31/06 | | 1,530,165 | | | 413,000 | | | 417,206 | | | 4,206 | | | — |

| MYR | | 08/07/06 | | 1,360,836 | | | 367,000 | | | 371,168 | | | 4,168 | | | — |

| MYR | | 08/14/06 | | 633,822 | | | 178,000 | | | 172,936 | | | — | | | 5,064 |

| MYR | | 08/14/06 | | 3,000,051 | | | 813,000 | | | 818,551 | | | 5,551 | | | — |

| MYR | | 11/10/06 | | 1,253,120 | | | 356,000 | | | 343,592 | | | — | | | 12,408 |

| MYR | | 11/13/06 | | 1,921,000 | | | 522,153 | | | 526,803 | | | 4,650 | | | — |

| NGN | | 08/10/06 | | 88,536,640 | | | 674,000 | | | 684,904 | | | 10,904 | | | — |

| NGN | | 10/05/06 | | 98,557,700 | | | 755,000 | | | 755,862 | | | 862 | | | — |

| PEN | | 08/23/06 | | 1,171,238 | | | 359,000 | | | 359,349 | | | 349 | | | — |

| PHP | | 07/17/06 | | 108,606,660 | | | 2,027,000 | | | 2,042,135 | | | 15,135 | | | — |

| PHP | | 07/31/06 | | 5,375,000 | | | 100,000 | | | 100,980 | | | 980 | | | — |

| PHP | | 08/11/06 | | 34,686,420 | | | 673,000 | | | 651,154 | | | — | | | 21,846 |

| PHP | | 09/18/06 | | 33,402,720 | | | 624,000 | | | 625,547 | | | 1,547 | | | — |

| PHP | | 06/26/07 | | 20,815,180 | | | 382,000 | | | 382,990 | | | 990 | | | — |

| PLN | | 07/19/06 | | 1,641,613 | | | 511,000 | | | 515,417 | | | 4,417 | | | — |

| PLN | | 07/24/06 | | 1,452,000 | | | 470,344 | | | 455,970 | | | — | | | 14,374 |

| PLN | | 07/31/06 | | 1,525,194 | | | 499,000 | | | 479,081 | | | — | | | 19,919 |

| PLN | | 08/14/06 | | 8,386,907 | | | 2,677,000 | | | 2,635,769 | | | — | | | 41,231 |

| RON | | 07/10/06 | | 1,663,000 | | | 606,072 | | | 594,277 | | | — | | | 11,795 |

| RON | | 07/19/06 | | 1,001,164 | | | 358,250 | | | 357,491 | | | — | | | 759 |

| RON | | 07/19/06 | | 720,000 | | | 257,594 | | | 257,094 | | | — | | | 500 |

| RON | | 07/24/06 | | 5,886,000 | | | 2,094,289 | | | 2,100,842 | | | 6,553 | | | — |

| RON | | 07/26/06 | | 2,190,000 | | | 771,127 | | | 781,525 | | | 10,398 | | | — |

| RON | | 07/31/06 | | 987,000 | | | 344,467 | | | 352,070 | | | 7,603 | | | — |

| RUB | | 02/01/07 | | 120,623,940 | | | 4,282,000 | | | 4,499,520 | | | 217,520 | | | — |

| RUB | | 02/26/07 | | 10,641,940 | | | 394,000 | | | 396,946 | | | 2,946 | | | — |

| RUB | | 02/26/07 | | 1,958,400 | | | 68,000 | | | 73,049 | | | 5,049 | | | — |

| RUB | | 09/19/08 | | 16,102,170 | | | 549,000 | | | 592,072 | | | 43,072 | | | — |

| SGD | | 07/13/06 | | 784,247 | | | 483,000 | | | 496,240 | | | 13,240 | | | — |

| SGD | | 08/07/06 | | 812,749 | | | 519,000 | | | 514,875 | | | — | | | 4,125 |

| SGD | | 08/07/06 | | 2,739,764 | | | 1,732,000 | | | 1,735,637 | | | 3,637 | | | — |

| SGD | | 08/23/06 | | 344,000 | | | 212,692 | | | 218,080 | | | 5,388 | | | — |

| SGD | | 08/28/06 | | 92,308 | | | 57,000 | | | 58,532 | | | 1,532 | | | — |

| SGD | | 10/13/06 | | 1,375,975 | | | 858,000 | | | 874,483 | | | 16,483 | | | — |

| SIT | | 07/17/06 | | 286,697,000 | | | 1,529,867 | | | 1,531,159 | | | 1,292 | | | — |

| SKK | | 07/27/06 | | 16,915,149 | | | 568,500 | | | 563,182 | | | — | | | 5,318 |

| SKK | | 08/10/06 | | 18,270,780 | | | 627,000 | | | 608,525 | | | — | | | 18,475 |

| SKK | | 08/28/06 | | 11,889,007 | | | 389,000 | | | 396,127 | | | 7,127 | | | — |

| THB | | 07/10/06 | | 2,449,920 | | | 64,000 | | | 64,191 | | | 191 | | | — |

| THB | | 07/21/06 | | 39,062,275 | | | 1,015,000 | | | 1,023,143 | | | 8,143 | | | — |

| TRY | | 07/05/06 | | 5,177,286 | | | 3,870,000 | | | 3,252,008 | | | — | | | 617,992 |

| TRY | | 07/05/06 | | 603,602 | | | 409,000 | | | 379,141 | | | — | | | 29,859 |

| TRY | | 07/05/06 | | 695,074 | | | 454,000 | | | 436,597 | | | — | | | 17,403 |

| TRY | | 08/03/06 | | 2,636,847 | | | 1,647,000 | | | 1,635,134 | | | — | | | 11,866 |

| TRY | | 02/09/07 | | 1,049,000 | | | 638,661 | | | 602,430 | | | — | | | 36,231 |

The accompanying notes are an integral part of these financial statements.

11

Lazard World Dividend & Income Fund, Inc.

Portfolio of Investments (concluded)

June 30, 2006 (unaudited)

Forward Currency Contracts open at June 30, 2006 (concluded):

| | | | | | | | U.S. $ Cost | | | U.S. $ | | | | | | |

| Forward Currency | | Expiration | | Foreign | | | on Origination | | | Current | | | Unrealized | | | Unrealized |

| Purchase Contracts | | Date | | Currency | | | Date | | | Value | | | Appreciation | | | Depreciation |

| |

| |

| |

|

| |

|

| |

|

| |

|

|

| TZS | | 07/05/06 | | 121,188,000 | | $ | 100,654 | | $ | 96,500 | | $ | — | | $ | 4,154 |

| TZS | | 07/20/06 | | 943,228,000 | | | 748,000 | | | 749,585 | | | 1,585 | | | — |

| TZS | | 08/09/06 | | 192,030,000 | | | 155,421 | | | 152,123 | | | — | | | 3,298 |

| TZS | | 08/16/06 | | 227,695,000 | | | 186,082 | | | 180,143 | | | — | | | 5,939 |

| TZS | | 10/13/06 | | 507,482,000 | | | 412,973 | | | 397,376 | | | — | | | 15,597 |

| TZS | | 10/26/06 | | 314,160,000 | | | 255,000 | | | 245,401 | | | — | | | 9,599 |

| TZS | | 10/26/06 | | 264,557,500 | | | 215,000 | | | 206,655 | | | — | | | 8,345 |

| TZS | | 12/05/06 | | 77,481,000 | | | 60,994 | | | 60,075 | | | — | | | 919 |

| TZS | | 12/15/06 | | 269,059,000 | | | 210,805 | | | 208,229 | | | — | | | 2,576 |

| TZS | | 12/20/06 | | 442,308,000 | | | 348,000 | | | 341,992 | | | — | | | 6,008 |

| TZS | | 05/08/07 | | 1,030,179,000 | | | 785,796 | | | 773,601 | | | — | | | 12,195 |

| UAH | | 08/01/06 | | 1,301,000 | | | 258,002 | | | 259,163 | | | 1,161 | | | — |

| UAH | | 08/07/06 | | 7,822,080 | | | 1,552,000 | | | 1,556,960 | | | 4,960 | | | — |

| UAH | | 08/10/06 | | 824,580 | | | 162,000 | | | 164,066 | | | 2,066 | | | — |

| UAH | | 09/11/06 | | 1,246,560 | | | 245,000 | | | 246,993 | | | 1,993 | | | — |

| | | | | |

|

| |

|

| |

|

| |

|

|

| Total Forward Currency Purchase Contracts | $ | 73,922,455 | | $ | 73,409,164 | | $ | 831,462 | | $ | 1,344,753 |

| |

|

| |

|

| |

|

| |

|

|

| | | | | | | | U.S. $ Cost | | | U.S. $ | | | | | | |

| Forward Currency | | Expiration | | Foreign | | | on Origination | | | Current | | | Unrealized | | | Unrealized |

| Sale Contracts | | Date | | Currency | | | Date | | | Value | | | Appreciation | | | Depreciation |

| |

| |

| |

|

| |

|

| |

|

| |

|

|

| ARS | | 07/17/06 | | 1,091,935 | | $ | 351,760 | | $ | 352,913 | | $ | — | | $ | 1,153 |

| BRL | | 12/28/06 | | 1,100,274 | | | 476,000 | | | 490,369 | | | — | | | 14,369 |

| BWP | | 07/05/06 | | 2,342,812 | | | 386,564 | | | 388,532 | | | — | | | 1,968 |

| COP | | 07/10/06 | | 1,041,006,500 | | | 403,961 | | | 402,942 | | | 1,019 | | | — |

| COP | | 10/10/06 | | 937,886,000 | | | 362,678 | | | 361,068 | | | 1,610 | | | — |

| EUR | | 08/08/06 | | 968,000 | | | 1,234,703 | | | 1,241,113 | | | — | | | 6,410 |

| INR | | 07/05/06 | | 55,850,290 | | | 1,212,029 | | | 1,212,933 | | | — | | | 904 |

| INR | | 07/05/06 | | 16,503,230 | | | 359,000 | | | 358,410 | | | 590 | | | — |

| INR | | 07/07/06 | | 16,766,420 | | | 363,855 | | | 364,108 | | | — | | | 253 |

| KRW | | 07/05/06 | | 1,760,673,000 | | | 1,857,250 | | | 1,856,187 | | | 1,063 | | | — |

| MXN | | 08/17/06 | | 4,196,800 | | | 366,149 | | | 370,858 | | | — | | | 4,709 |

| PEN | | 08/23/06 | | 1,171,238 | | | 356,324 | | | 359,349 | | | — | | | 3,025 |

| RUB | | 07/21/06 | | 27,021,960 | | | 1,008,000 | | | 1,007,210 | | | 790 | | | — |

| SKK | | 07/27/06 | | 16,114,560 | | | 526,617 | | | 536,527 | | | — | | | 9,910 |

| TRY | | 07/05/06 | | 504,000 | | | 321,203 | | | 316,577 | | | 4,626 | | | — |

| TRY | | 07/05/06 | | 351,874 | | | 229,788 | | | 221,023 | | | 8,765 | | | — |

| TRY | | 07/05/06 | | 2,791,154 | | | 1,766,553 | | | 1,753,207 | | | 13,346 | | | — |

| TRY | | 07/05/06 | | 1,173,000 | | | 750,720 | | | 736,796 | | | 13,924 | | | — |

| TRY | | 07/05/06 | | 484,515 | | | 356,287 | | | 304,338 | | | 51,949 | | | — |

| TRY | | 07/05/06 | | 524,308 | | | 387,000 | | | 329,333 | | | 57,667 | | | — |

| TRY | | 07/05/06 | | 647,112 | | | 472,000 | | | 406,470 | | | 65,530 | | | — |

| TRY | | 02/09/07 | | 295,000 | | | 209,413 | | | 169,415 | | | 39,998 | | | — |

| TRY | | 02/09/07 | | 754,000 | | | 525,179 | | | 433,014 | | | 92,165 | | | — |

| TZS | | 05/08/07 | | 1,030,179,000 | | | 776,907 | | | 773,601 | | | 3,306 | | | — |

| UAH | | 07/11/06 | | 3,007,000 | | | 595,033 | | | 600,378 | | | — | | | 5,345 |

| | | | | |

|

| |

|

| |

|

| |

|

|

| Total Forward Currency Sale Contracts | $ | 15,654,973 | | $ | 15,346,671 | | | 356,348 | | | 48,046 |

| | | |

|

| |

|

| |

|

| |

|

|

| Gross unrealized appreciation/depreciation on Forward Currency Contracts | $ | 1,187,810 | | $ | 1,392,799 |

| | | | |

|

| |

|

|

The accompanying notes are an integral part of these financial statements.12

Lazard World Dividend & Income Fund, Inc.

Notes to Portfolio of Investments

June 30, 2006 (unaudited)

| (a) | Non-income producing security. |

| |

| (b) | For federal income tax purposes, the aggregate cost was $150,047,005, aggregate gross unrealized appreciation was $7,837,148, aggregate gross unrealized depreciation was $5,850,416 and the net unrealized appreciation was $1,986,732. |

| |

| (c) | Segregated security for forward currency contracts. |

| |

| (d) | Principal amount denominated in respective country’s currency unless otherwise specified. |

| |

| (e) | Pursuant to Rule 144A under the Securities Act of 1933, these securities may only be traded among “qualified institutional buyers.” Principal amount denominated in U.S. dollar. |

| |

| Security Abbreviations: | |

| ADR | — American Depositary Receipt | |

| NTN-B | — Brazil Sovereign “Nota do Tesouro Nacional” | |

| TES | — Titulos de Tesoreria | |

| | | | | |

| | | | | |

| Currency Abbreviations: | | |

| | | | | |

| ARS | — Argentine Peso | MYR | — Malaysian Ringgit | |

| BRL | — Brazilian Real | NGN | — Nigerian Naira | |

| BWP | — Botswanian Pula | PEN | — Peruvian New Sol | |

| CLP | — Chilean Peso | PHP | — Philippine Peso | |

| COP | — Colombian Peso | PLN | — Polish Zloty | |

| CSD | — Serbian Dinar | RON | — Romanian Leu | |

| EUR | — Euro | RUB | — Russian Ruble | |

| GHC | — Ghanaian Cedi | SGD | — Singapore Dollar | |

| IDR | — Indonesian Rupiah | SIT | — Slovenian Tolar | |

| ILS | — Israeli Shekel | SKK | — Slovenska Koruna | |

| INR | — Indian Rupee | THB | — Thai Baht | |

| ISK | — Iceland Krona | TRY | — New Turkish Lira | |

| KRW | — South Korean Won | TZS | — Tanzanian Shilling | |

| KZT | — Kazakhstanian Tenge | UAH | — Ukranian Hryvnia | |

| MXN | — Mexican Peso | ZMK | — Zambian Kwacha | |

| Portfolio holdings by industry (as percentage of net assets): |

| Industry | | | |

| Alcohol & Tobacco | 6.6 | % | |

| Automotive | 0.5 | | |

| Banking | 11.3 | | |

| Chemicals | 3.0 | | |

| Commercial Services | 0.8 | | |

| Drugs | 4.0 | | |

| Electric | 11.8 | | |

| Energy Integrated | 8.8 | | |

| Financial Services | 8.3 | | |

| Food & Beverages | 1.0 | | |

| Forest & Paper Products | 3.9 | | |

| Gas Utilities | 0.5 | | |

| Health Services | 1.7 | | |

| Insurance | 1.1 | | |

| Leisure & Entertainment | 5.5 | | |

| Manufacturing | 2.6 | | |

| Metals & Mining | 3.6 | | |

| Real Estate | 2.7 | | |

| Semiconductors & Components | 1.5 | | |

| Telecommunications | 18.0 | | |

| Transportation | 1.7 | | |

|

|

| |

| Subtotal | 98.9 | | |

| Foreign Government Obligations | 5.2 | | |

| Structured Notes | 1.7 | | |

| Repurchase Agreement | 0.2 | | |

|

|

| |

| Total Investments. | 106.0 | % | |

|

|

| |

The accompanying notes are an integral part of these financial statements.

13

Lazard World Dividend & Income Fund, Inc.

Statement of Assets and Liabilities

June 30, 2006 (unaudited)

| ASSETS | | | |

| Investments in securities, at value (cost $150,047,005) | $ | 152,033,737 | |

| Cash | | 501 | |

| Receivables for: | | | |

| Investments sold | | 1,750,532 | |

| Dividends and interest | | 618,115 | |

| Gross appreciation on forward currency contracts | | 1,187,810 | |

|

|

|

|

| Total assets | | 155,590,695 | |

|

|

|

|

| |

| LIABILITIES | | | |

| Payables for: | | | |

| Management fees | | 154,030 | |

| Accrued directors’ fees | | 486 | |

| Line of credit outstanding | | 9,050,000 | |

| Investments purchased | | 1,456,123 | |

| Gross depreciation on forward currency contracts | | 1,392,799 | |

| Other accrued expenses and payables | | 133,646 | |

|

|

|

|

| Total liabilities | | 12,187,084 | |

|

|

|

|

| Net assets | $ | 143,403,611 | |

|

|

|

|

| NET ASSETS | | | |

| Paid in capital | $ | 128,564,427 | |

| Distributions in excess of net investment income | | (413,085 | ) |

| Accumulated undistributed net realized gain | | 13,463,203 | |

| Net unrealized appreciation (depreciation) on: | | | |

| Investments | | 1,986,732 | |

| Foreign currency and forward currency contracts | | (197,666 | ) |

|

|

|

|

| Net assets | $ | 143,403,611 | |

|

|

|

|

| |

| Shares of common stock outstanding* | | 6,745,237 | |

| Net assets per share of common stock | $ | 21.26 | |

| Market value per share | $ | 19.62 | |

* $0.001 par value, 500,000,000 shares authorized for the Fund.The accompanying notes are an integral part of these financial statements.

14

Lazard World Dividend & Income Fund, Inc.

Statement of Operations

For the six months ended June 30, 2006 (unaudited)

INVESTMENT INCOME

| Income: | | | |

| Dividends (net of foreign withholding taxes of $338,593) | $ | 5,114,956 | |

| Interest | | 421,559 | |

|

|

|

|

| Total investment income | | 5,536,515 | |

|

|

|

|

| |

| Expenses: | | | |

| Management fees | | 929,629 | |

| Custodian fees | | 58,395 | |

| Professional services | | 50,964 | |

| Administration fees | | 32,769 | |

| Shareholders’ reports | | 24,537 | |

| Shareholders’ services | | 20,706 | |

| Shareholders’ meeting | | 7,144 | |

| Directors’ fees and expenses | | 4,669 | |

| Other | | 19,571 | |

|

|

|

|

| Total gross expenses before interest expense | | 1,148,384 | |

| Interest expense | | 206,988 | |

|

|

|

|

| Total gross expenses | | 1,355,372 | |

| Expense reductions | | (2,803 | ) |

|

|

|

|

| Total net expenses | | 1,352,569 | |

|

|

|

|

| Net investment income | | 4,183,946 | |

|

|

|

|

| NET REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS AND FOREIGN CURRENCY | | | |

| Net realized gain on: | | | |

| Investments (net of foreign capital gains taxes of $35,603) | | 11,277,168 | |

| Foreign currency and forward currency contracts | | 1,108,586 | |

| Net change in unrealized depreciation on: | | | |

| Investments | | (3,323,461 | ) |

| Foreign currency and forward currency contracts | | (5,966 | ) |

|

|

|

|

| Net realized and unrealized gain on investments and foreign currency | | 9,056,327 | |

|

|

|

|

| Net increase in net assets resulting from operations | $ | 13,240,273 | |

|

|

|

|

The accompanying notes are an integral part of these financial statements.

15

Lazard World Dividend & Income Fund, Inc.

Statements of Changes in Net Assets

| | | Six Months Ended | | | | | |

| | | June 30, 2006 | | | | Period Ended | |

| | | (unaudited) | | | | December 31, 2005** | |

|

|

|

| |

|

|

|

| INCREASE IN NET ASSETS | | | | | | | |

| Operations: | | | | | | | |

| Net investment income | $ | 4,183,946 | | | $ | 1,779,876 | |

| Net realized gain on investments and foreign currency | | 12,385,754 | | | | 4,258,543 | |

| Net change in unrealized appreciation (depreciation) on investments | | | | | | | |

| and foreign currency | | (3,329,427 | ) | | | 5,118,493 | |

|

|

|

| |

|

|

|

| Net increase in net assets resulting from operations | | 13,240,273 | | | | 11,156,912 | |

|

|

|

| |

|

|

|

| Distributions to Stockholders: | | | | | | | |

| From net investment income | | (4,723,015 | ) | | | (4,834,986 | ) |

|

|

|

| |

|

|

|

| Net decrease in net assets resulting from distributions | | (4,723,015 | ) | | | (4,834,986 | ) |

|

|

|

| |

|

|

|

| Capital Stock Transactions: | | | | | | | |

| Proceeds from common shares issued in offering | | — | | | | 128,734,000 | |

| Offering costs for common shares charged to paid in capital | | — | | | | (269,600 | ) |

|

|

|

| |

|

|

|

| Net increase in net assets from capital stock transactions | | — | | | | 128,464,400 | |

|

|

|

| |

|

|

|

| Total increase in net assets | | 8,517,258 | | | | 134,786,326 | |

| Net assets at beginning of period*** | | 134,886,353 | | | | 100,027 | |

|

|

|

| |

|

|

|

| Net assets at end of period* | $ | 143,403,611 | | | $ | 134,886,353 | |

|

|

|

| |

|

|

|

| *Includes undistributed (distributions in excess of) net investment income | $ | (413,085 | ) | | $ | 125,984 | |

|

|

|

| |

|

|

|

| |

| |

| Transactions in Capital Shares: | | | | | | | |

| Common shares outstanding at beginning of period*** | | 6,745,237 | | | | 5,237 | |

|

|

|

| |

|

|

|

| Common shares issued in offering | | — | | | | 6,740,000 | |

|

|

|

| |

|

|

|

| Net increase | | — | | | | 6,740,000 | |

|

|

|

| |

|

|

|

| Common shares outstanding at end of period | | 6,745,237 | | | | 6,745,237 | |

|

|

|

| |

|

|

|

| ** | Fund commenced operations on June 28, 2005. |

| |

| *** | Represents initial seed capital on June 20, 2005 for the period ended December 31, 2005. |

| |

The accompanying notes are an integral part of these financial statements.

16

Lazard World Dividend & Income Fund, Inc.

Financial Highlights

Selected data for a share of common stock outstanding throughout each period:

| | Six Months | | | For the Period | |

| | Ended | | | 6/28/05* to | |

| | 6/30/06† | | | 12/31/05 | |

|

|

|

| |

|

|

|

| Net asset value, beginning of period | $ | 20.00 | | | $ | 19.06 | (a) |

|

|

|

| |

|

|

|

| Income from investment operations: | | | | | | | |

| Net investment income | | 0.62 | | | | 0.26 | |

| Net realized and unrealized gain | | 1.34 | | | | 1.40 | |

|

|

|

| |

|

|

|

| Total from investment operations | | 1.96 | | | | 1.66 | |

|

|

|

| |

|

|

|

| Less distributions from: | | | | | | | |

| Net investment income | | (0.70 | ) | | | (0.72 | ) |

|

|

|

| |

|

|

|

| Total distributions | | (0.70 | ) | | | (0.72 | ) |

|

|

|

| |

|

|

|

| Net asset value, end of period | $ | 21.26 | | | $ | 20.00 | |

|

|

|

| |

|

|

|

| Market value, end of period | $ | 19.62 | | | $ | 17.76 | |

|

|

|

| |

|

|

|

| Total Return based upon: | | | | | | | |

| Net asset value (b) | | 9.85 | % | | | 8.77 | % |

| Market value (b) | | 14.52 | % | | | (7.64 | )% |

| Ratios and Supplemental Data: | | | | | | | |

| Net assets, end of period (in thousands) | $ | 143,404 | | | $ | 134,886 | |

| Ratios to average net assets: | | | | | | | |

| Net expenses (c) | | 1.89 | % | | | 2.00 | % |

| Gross expenses (c) | | 1.90 | % | | | 2.00 | % |

| Gross expenses excluding interest expense (c) | | 1.61 | % | | | 1.79 | % |

| Net investment income (c) | | 5.85 | % | | | 2.65 | % |

| Portfolio turnover rate | | 57 | % | | | 37 | % |

| † | Unaudited. |

| | |

| * | Commencement of operations. |

| | |

| (a) | Net of initial sales load, underwriting and offering costs of $0.94 per share. |

| |

| (b) | Total return based on per share market price assumes the purchase of common shares at the market price on the first day and sales of common shares at the market price on the last day of the period indicated; dividends and distributions are assumed to be reinvested in accordance with the Fund’s Dividend Reinvestment Plan. The total return based on net asset value, or NAV, assumes the purchase of common shares at NAV on the first day and sales of common shares at NAV on the last day of the period indicated; distributions are assumed to be reinvested at NAV. Past performance is not idicative, nor a guarantee, of future results; the investment return, market price and net asset value of the Fund will fluctuate, so that an investor’s shares in the Fund, when sold, may be worth more or less than their orginal cost. The returns do not reflect the deduction of taxes that a stockholder would pay on the Fund’s distributions or on the sale of Fund shares. Periods of less than one year are not annualized. |

| |

| (c) | Annualized for periods of less than one year. |

| |

The accompanying notes are an integral part of these financial statements.

17

Lazard World Dividend & Income Fund, Inc.

Notes to Financial Statements

June 30, 2006 (unaudited)

1. Organization

Lazard World Dividend & Income Fund, Inc. (the “Fund”) was incorporated in Maryland on April 6, 2005 and is registered under the Investment Company Act of 1940, as amended (the “Act”), as a diversified, closed-end management investment company. The Fund trades on the New York Stock Exchange (“NYSE”) under the ticker symbol LOR and commenced operations on June 28, 2005. The Fund’s investment objective is total return through a combination of dividends, income and capital appreciation.

2. Significant Accounting Policies

The following is a summary of significant accounting policies:

(a) Valuation of Investments—Market values for securities are generally based on the last reported sales price on the principal exchange or market on which the security is traded, generally as of the close of regular trading on the NYSE (normally 4:00 p.m. Eastern time) on each valuation date. Any securities not listed, for which current over-the-counter market quotations or bids are readily available, are valued at the last quoted bid price or, if available, the mean of two such prices. Forward currency contracts are valued at the current cost of offsetting the contract. Securities listed on foreign exchanges are valued at the last reported sales price except as described below; securities not traded on the valuation date are valued at the last quoted bid price.

Bonds and other fixed-income securities that are not exchange-traded are valued on the basis of prices provided by pricing services which are based primarily on institutional trading in similar groups of securities, or by using brokers’ quotations.

If a significant event affecting the value of securities occurs between the close of the exchange or market on which the security is principally traded and the time when the Fund’s net asset value is calculated, or when current market quotations otherwise are determined not to be readily available or reliable, such securities will be valued at their fair values as determined in good faith by or under the supervision of the Board of Directors. Fair valuing of foreign securities may be determined with the assistance of a pricing service, using correlations between the movement of prices of such securities and indices of domestic securities and other appropriate indicators, such as closing market prices of relevant ADRs or futures contracts. The Valuation Committee of the Investment Manager may evaluate a variety of factors to determine the fair value of securities for which current market quotations are determined not to be readily available or reliable. These factors include, but are not limited to, the type of security, the value of comparable securities, observations from financial institutions and relevant news events. Input from the Investment Manager’s analysts will also be considered. The effect of using fair value pricing is that the net asset value of the Fund will reflect the affected securities’ values as determined in the judgment of the Board of Directors, or its designee, instead of being determined by the market. Using a fair value pricing methodology to price securities may result in a value that is different from the most recent closing price of a security and from the prices used by other investment companies to calculate their portfolios’ net asset values.

(b) Portfolio Securities Transactions and Investment Income—Portfolio securities transactions are accounted for on trade date. Realized gain (loss) on sales of investments are recorded on a specific identification basis. Dividend income is recorded on the ex-dividend date and interest income is accrued daily. The Fund amortizes premiums and accretes discounts on fixed-income securities using the effective yield method.

(c) Repurchase Agreements—In connection with transactions in repurchase agreements, the Fund’s custodian takes possession of the underlying collateral securities, the fair value of which at all times is required to be at least equal to the principal amount, plus accrued interest, of the repurchase transaction. If the seller defaults, and the fair value of the collateral declines, realization of the collateral by the Fund may be delayed or limited.

(d) Securities Lending—The Fund may lend portfolio securities to qualified borrowers in order to earn additional income. The terms of the lending agreements require that loans are secured at all times by cash, U.S. Government securities or irrevocable letters of credit in an amount at least equal to 102% of the market value of domestic securities loaned (105% in the case of foreign securities), plus accrued interest and dividends, determined on a daily basis. Cash collateral received is invested in State Street Navigator Securities Lending Prime Portfolio, a regulated investment company offered by State Street Bank and Trust Company (“State Street”). If the borrower defaults on its obligation to return the securities loaned because of insolvency or other reasons, the Fund could experience delays and costs in recovering the securities loaned or in gaining access to the collateral.

In accordance with accounting principles generally accepted in the United States, cash received as collateral for securities lending transactions which is invested in income producing securities is included in the Portfolio of Investments. The related amount payable upon the return

18

Lazard World Dividend & Income Fund, Inc.

Notes to Financial Statements (continued)

June 30, 2006 (unaudited)

of the securities on loan, where cash is received as collateral, is shown on the Statement of Assets and Liabilities.At June 30, 2006, the Fund had no securities on loan.

(e) Leveraging—The Fund intends to use leverage to invest Fund assets in currency investments, primarily using forward currency contracts and by borrowing under a credit facility with State Street, up to a maximum of 33 1 / 3% of the Fund’s total leveraged assets. If the assets of the Fund decline due to market conditions such that this 33 1 / 3% threshold will be exceeded, leverage risk will increase.

If the Fund is able to realize a higher return on the leveraged portion of its investment portfolio than the cost of such leverage together with other related expenses, the effect of the leverage will be to cause the Fund to realize a higher net return than if the Fund were not so leveraged. There is no assurance that any leveraging strategy the Fund employs will be successful.

Using leverage is a speculative investment technique and involves certain risks. These include higher volatility of net asset value, the likelihood of more volatility in the market value of Common Stock and, with respect to borrowings, the possibility either that the Fund’s return will fall if the interest rate on any borrowings rises, or that income will fluctuate because the interest rate of borrowings varies.

If the market value of the Fund’s portfolio declines, the leverage will result in a greater decrease in net asset value than if the Fund were not leveraged. A greater net asset value decrease also will tend to cause a greater decline in the market price of the Fund’s Common Stock. To the extent that the Fund is required or elects to prepay any borrowings, the Fund may need to liquidate investments to fund such prepayments. Liquidation at times of adverse economic conditions may result in capital losses and may reduce returns.

(f) Foreign Currency Translation and Forward Currency Contracts—The accounting records of the Fund are maintained in U.S. dollars. Portfolio securities and other assets and liabilities denominated in a foreign currency are translated daily into U.S. dollars at the prevailing rates of exchange. Purchases and sales of securities, income receipts and expense payments are translated into U.S. dollars at the prevailing exchange rates on the respective transaction dates.

The Fund does not isolate the portion of operations resulting from changes in foreign exchange rates on investments from the fluctuations arising from changes in their market prices. Such fluctuations are included in net realized and unrealized gain (loss) on investments. Net realized gain (loss) on foreign currency transactions represents net foreign currency gain (loss) from forward currency contracts, disposition of foreign currencies, currency gain (loss) realized between the trade and settlement dates on securities transactions, and the difference between the amount of dividends, interest and foreign withholding taxes recorded on the Fund’s accounting records and the U.S. dollar equivalent amounts actually received or paid. Net unrealized foreign currency gain (loss) arises from changes in the value of assets and liabilities, other than investments in securities, as a result of changes in exchange rates.

A forward currency contract is an agreement between two parties to buy or sell currency at a set price on a future date. Upon entering into these contracts, risks may arise from the potential inability of counterparties to meet the terms of their contracts and from unanticipated movements in the value of the foreign currency relative to the U.S. dollar.

The U.S. dollar value of forward currency contracts is determined using forward exchange rates provided by quotation services. Daily fluctuations in the value of such contracts are recorded as unrealized gain (loss). When the contract is closed, the Fund records a realized gain (loss) equal to the difference between the value at the time it was opened and the value at the time it was closed. Such gain (loss) is disclosed in the realized and unrealized gain (loss) on foreign currency in the Fund’s accompanying Statement of Operations.

(g) Structured Investments—The Fund may invest in structured investments, whose values are linked either directly or inversely to changes in foreign currencies, interest rates, commodities, indices, or other underlying instruments. The Fund may use these investments to increase or decrease its exposure to different underlying instruments, to gain exposure to markets that might be difficult to invest in through conventional securities or for other purposes. Structured investments may be more volatile than their underlying instruments, but any loss is limited to the amount of the original investment.

(h) Federal Income Taxes—The Fund’s policy is to continue to qualify as a regulated investment company under Sub-chapter M of the Internal Revenue Code and to distribute all of its taxable income, including any net realized capital gains, to shareholders. Therefore, no federal income tax provision is required.

At December 31, 2005, the Fund had no unused capital loss carryforwards.

Under current tax law, certain capital and net foreign currency losses realized after October 31 within the taxable

19

Lazard World Dividend & Income Fund, Inc.

Notes to Financial Statements (continued)

June 30, 2006 (unaudited)

year may be deferred and treated as occurring on the first day of the following tax year. For the tax year ended December 31, 2005, the Fund did not elect to defer any net capital and currency losses arising between November 1, 2005 and December 31, 2005.(i) Dividends and Distributions—The Fund intends to declare and to pay dividends monthly from net investment income. Distributions to stockholders are recorded on the ex-dividend date. During any particular year, net realized gains from investment transactions in excess of available capital loss carryforwards would be taxable to the Fund if not distributed. The Fund intends to declare and distribute these amounts, at least annually, to stockholders; however, to avoid taxation, a second distribution may be required.

Income dividends and capital gains distributions are determined in accordance with federal income tax regulations which may differ from accounting principles generally accepted in the United States. These book/tax differences, which may result in distribution reclassifications, are primarily due to differing treatments of foreign currency transactions. Book/tax differences relating to stockholder distributions may result in reclassifications among certain capital accounts.

The Fund may at times in its discretion pay out less than the entire amount of net investment income earned in any particular period and may at times pay out such accumulated undistributed income in addition to net investment income earned in other periods in order to permit the Fund to maintain a more stable level of distributions. As a result, the dividends paid by the Fund to stockholders for any particular period may be more or less than the amount of net investment income earned by the Fund during such period. However, the Fund will adjust the level of distribution as appropriate to seek to avoid making distributions that constitute a return of capital. The Fund is not required to maintain a stable level of distributions, or distributions at any particular rate.

(j) Expense Reductions—When the Fund leaves excess cash in a demand deposit account, it may receive credits which are available to offset custody expenses. The Statement of Operations reports gross custody expenses, and reports the amount of such credits separately as an expense reduction.

(k) Estimates—The preparation of financial statements in conformity with accounting principles generally accepted in the United States requires the Fund to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of increases and decreases in net assets from operations during the reporting period. Actual results could differ from those estimates.

3. Investment Management Agreement

The Fund has entered into an investment management agreement (the “Management Agreement”) with the Investment Manager. Pursuant to the Management Agreement, the Investment Manager regularly provides the Fund with investment research, advice and supervision and furnishes continuously an investment program for the Fund consistent with its investment objective and policies, including the purchase, retention and disposition of securities.

The Fund has agreed to pay the Investment Manager an annual investment management fee of 0.90% of the Fund’s average daily “Total Leveraged Assets” (the Fund’s total assets including Financial Leverage (defined below)) for the services and facilities provided by the Investment Manager, payable on a monthly basis. The fee paid to the Investment Manager will be higher when the Investment Manager uses Currency Commitments and Borrowings (“Financial Leverage”) to make Currency Investments, rather than by reducing the percentage of “Net Assets” (the Fund’s assets without taking into account Financial Leverage) invested in World Equity Investments for the purposes of making Currency Investments. “World Equity Investments” refers to investments in the Fund’s world equity strategy consisting of equity securities of companies with market capitalizations of $3 billion or greater at the time of the Fund’s initial purchase. “Currency Investments” refers to investments in the Fund’s emerging income strategy, consisting of emerging market currencies (primarily by entering into forward currency contracts), or instruments whose value is derived from the performance of an underlying emerging market currency, but also may invest in debt obligations, including government, government agency and corporate obligations and structured notes denominated in emerging market currencies. “Currency Commitments” are the aggregate financial exposures created by forward currency contracts in excess of that represented in the Fund’s Net Assets, and “Borrowings” refers to the borrowings under the Fund’s credit facility. Assuming Financial Leverage in the amount of 33 1 / 3% of the Fund’s Total Leveraged Assets, the annual fee payable to the Investment Manager would be 1.35% of Net Assets (i.e., not including amounts attributable to Financial Leverage).

The following is an example of this calculation of the Investment Manager’s fee, using very simple illustrations. If the Fund had assets of $1,000, it could invest $1,000 in World Equity Investments and enter into $500 in forward currency contracts (because the Fund would not have to

20

Lazard World Dividend & Income Fund, Inc.

Notes to Financial Statements (continued)

June 30, 2006 (unaudited)

pay money at the time it enters into the currency contracts). Similarly, the Fund could invest $1,000 in World Equity Investments, borrow $500 and invest the $500 in foreign currency denominated bonds. In either case, the Investment Manager’s fee would be calculated based on $1,500 of assets, because the fee is calculated based on Total Leveraged Assets (Net Assets plus Financial Leverage). In our example, the Financial Leverage is in the form of either the forward currency contracts (Currency Commitments) or investments from Borrowings. The amount of the Financial Leverage outstanding, and therefore the amount of Total Leveraged Assets on which the Investment Manager’s fee is based, fluctuates daily based on changes in value of the Fund’s portfolio holdings, including changes in value of the currency involved in the forward currency contracts and foreign currency denominated bonds acquired with the proceeds of Borrowings. However, the Investment Manager’s fee will be the same regardless of whether Currency Investments are made with Currency Commitments or with Borrowings (without taking into account the cost of Borrowings).This method of calculating the Investment Manager’s fee is different than the way closed-end investment companies typically calculate management fees. Traditionally, closed-end investment companies calculate management fees based on Net Assets plus Borrowings (excluding Financial Leverage obtained through Currency Commitments). The Investment Manager’s fee is different because the Fund’s leverage strategy is different than the leverage strategy employed by many other closed-end investment companies. Although the Fund may employ Borrowings in making Currency Investments, the Fund’s leverage strategy relies primarily on Currency Commitments, rather than relying exclusively on borrowing money or/and issuing preferred stock, as is the strategy employed by most closed-end investment companies. The Investment Manager’s fee would be lower if its fee were calculated only on Net Assets plus Borrowings, because the Investment Manager would not earn fees on Currency Investments made with Currency Commitments (forward currency contracts). Using the example above, where the Fund has assets of $1,000 and invests $1,000 in World Equity Investments and $500 in forward currency contracts, the following table illustrates how the Investment Manager’s fee would be different if it did not earn management fees on these types of Currency Investments. A discussion of the most recent review and approval by the Fund’s Board of Directors of the Management Agreement (including the method of calculating the Investment Manager’s fee) is included in the Fund’s Semi-Annual Report dated June 30, 2005 under “Other Information—Board Consideration of Management Agreement.”

| | Fund’s | | Typical |

| | management | | management |

| | fee based on | | fee formula, |

| | Total Leveraged | | calculated |

| | Assets (includes | | excluding |

| | Currency | | Currency |

| Beginning assets of $1,000 | Commitments) | | Commitments |

| |

| World Equity Investments | | | | | | | |

| (Net Assets) | $ | 1,000 | | | $ | 1,000 | |

| Currency Commitments | $ | 500 | | | $ | 500 | |

| Assets used to calculate | | | | | | | |

| management fee | $ | 1,500 | | | $ | 1,000 | |

| Management fee (0.90%) | $ | 13.50 | | | $ | 9.00 | |

Investment Manager Fee Conflict Risk—The fee paid to the Investment Manager for investment management services will be higher when the Fund uses Financial Leverage, whether through forward currency contracts or Borrowings, because the fee paid will be calculated on the basis of the Fund’s assets including this Financial Leverage. Consequently, the Investment Manager may have a financial interest for the Fund to utilize such Financial Leverage, which may create a conflict of interest between the Investment Manager and the stockholders of the Fund.The Fund has implemented procedures to monitor this potential conflict.

4. Administrative Agreement