SILVER WHEATON CORP.

ANNUAL INFORMATION FORM

FOR THE YEAR ENDED DECEMBER 31, 2015

TABLE OF CONTENTS

| DESCRIPTION | PAGE NO. |

| | |

| INTRODUCTORY NOTES | 1 |

| CORPORATE STRUCTURE | 5 |

| GENERAL DEVELOPMENT OF THE BUSINESS | 6 |

| DESCRIPTION OF THE BUSINESS | 14 |

| Principal Product | 14 |

| Competitive Conditions | 24 |

| Operations | 24 |

| Risk Factors | 25 |

| TECHNICAL INFORMATION | 36 |

| SAN DIMAS MINES, MEXICO | 45 |

| PEÑASQUITO MINE, MEXICO | 53 |

| SALOBO MINE, BRAZIL | 64 |

| DIVIDENDS | 80 |

| DESCRIPTION OF CAPITAL STRUCTURE | 80 |

| TRADING PRICE AND VOLUME | 81 |

| DIRECTORS AND OFFICERS | 82 |

| LEGAL PROCEEDINGS AND REGULATORY ACTIONS | 86 |

| INTEREST OF MANAGEMENT AND OTHERS IN MATERIAL TRANSACTIONS | 87 |

| TRANSFER AGENT AND REGISTRAR | 87 |

| MATERIAL CONTRACTS | 87 |

| INTERESTS OF EXPERTS | 87 |

| AUDIT COMMITTEE | 88 |

| ADDITIONAL INFORMATION | 89 |

| SCHEDULE A - AUDIT COMMITTEE CHARTER | A-1 |

Silver Wheaton is a registered trademark of Silver Wheaton Corp. in Canada, the United States and certain other jurisdictions.

SILVER WHEATON2015 ANNUAL INFORMATION FORM

INTRODUCTORY NOTES

Cautionary Note Regarding Forward-Looking Statements

This annual information form contains “forward-looking statements” within the meaning of the United States Private Securities Litigation Reform Act of 1995 and “forward-looking information” within the meaning of applicable Canadian securities legislation. Forward-looking statements, which are all statements other than statements of historical fact, include, but are not limited to, statements with respect to:

| | payments by Silver Wheaton’s wholly owned subsidiary, Silver Wheaton (Caymans) Ltd. to Panoro Minerals Ltd. and its wholly owned subsidiary Cordillera Copper Ltd. in accordance with an early deposit precious metal purchase agreement for the Cotabambas project located in Peru, including any acceleration of payments, estimated throughput of the Cotabambas project and exploration potential associated with the Cotabambas project; |

| | | the normal course issuer bid (“NCIB”) and the number of shares that may be purchased under the NCIB; |

| | projected increases to Silver Wheaton Corp.’s (“Silver Wheaton” or the “Company”) production and cash flow profile; |

| | | the expansion and exploration potential at the Salobo mine located in Brazil; |

| | | projected changes to Silver Wheaton’s production mix; |

| | | anticipated increases in total throughput at the Salobo mine; |

| | the effect of the Servicio de Administración Tributaria (“SAT”) legal claim on Primero’s business, financial condition, results of operations and cash flows for 2010-2014 and 2015-2019; |

| | | the estimated future production; |

| | | the future price of commodities; |

| | | the estimation of mineral reserves and mineral resources; |

| | | the realization of mineral reserve estimates; |

| | the timing and amount of estimated future production (including 2016 and average attributable annual production over the next five years); |

| | | the costs of future production; |

| | | reserve determination; |

| | | estimated reserve conversion rates; |

| | any statements as to future dividends, the ability to fund outstanding commitments and the ability to continue to acquire accretive precious metal stream interests; |

| | | confidence in the Company’s business structure; |

| | the Company’s position relating to any dispute with the Canada Revenue Agency (the “CRA”) and the Company’s intention to defend reassessments issued by the CRA; the impact of potential taxes, penalties and interest payable to the CRA; possible audits for taxation years subsequent to 2013; estimates as to amounts that may be reassessed by the CRA in respect of taxation years subsequent to 2010; amounts that may be payable in respect of penalties and interest; the Company’s intention to file future tax returns in a manner consistent with previous filings; that the CRA will continue to accept the Company posting security for amounts sought by the CRA under notices of reassessment for the 2005-2010 taxation years or will accept posting security for any other amounts that may be sought by the CRA under other notices of reassessment; the length of time it would take to resolve any dispute with the CRA or an objection to a reassessment; and assessments of the impact and resolution of various tax matters, including outstanding audits, proceedings with the CRA and proceedings before the courts; and |

| | | assessments of the impact and resolution of various legal and tax matters. |

Generally, these forward-looking statements can be identified by the use of forward-looking terminology such as “plans”, “expects” or “does not expect”, “is expected”, “budget”, “scheduled”, “estimates”, “forecasts”, “projects”, “intends”, “anticipates” or “does not anticipate”, or “believes”, “potential”, or variations of such words and phrases or statements that certain actions, events or results “may”, “could”, “would”, “might” or “will be taken”, “occur” or “be achieved”.

Forward-looking statements are subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of Silver Wheaton to be materially different from those expressed or implied by such forward-looking statements, including but not limited to:

SILVER WHEATON2015 ANNUAL INFORMATION FORM [1]

| | | fluctuations in the price of commodities; |

| | risks related to the Mining Operations (as defined herein) including risks related to fluctuations in the price of the primary commodities mined at such operations, actual results of mining and exploration activities, environmental, economic and political risks of the jurisdictions in which the Mining Operations are located, and changes in project parameters as plans continue to be refined; |

| | absence of control over Mining Operations and having to rely on the accuracy of the public disclosure and other information Silver Wheaton receives from the owners and operators of the Mining Operations as the basis for its analyses, forecasts and assessments relating to its own business; |

| | differences in the interpretation or application of tax laws and regulations or accounting policies and rules; and Silver Wheaton’s interpretation of, or compliance with, tax laws and regulations or accounting policies and rules, is found to be incorrect or the tax impact to the Company’s business operations is materially different than currently contemplated; |

| | any challenge by the CRA of the Company’s tax filings is successful and the potential negative impact to the Company’s previous and future tax filings; the Company’s business or ability to enter into precious metal purchase agreements (as defined herein) is materially impacted as a result of any CRA reassessment; any reassessment of the Company’s tax filings and the continuation or timing of any such process is outside the Company’s control; any requirement to pay reassessed tax; the Company is not assessed taxes on its foreign subsidiary’s income on the same basis that the Company pays taxes on its Canadian income, if taxable in Canada; interest and penalties associated with a CRA reassessment having an adverse impact on the Company’s financial position; litigation risk associated with a challenge to the Company’s tax filings; |

| | | credit and liquidity risks; |

| | | hedging risk; |

| | | competition in the mining industry; |

| | | risks related to Silver Wheaton’s acquisition strategy; |

| | risks related to the market price of the common shares of Silver Wheaton (the “Common Shares”), including with respect to the market price of the Common Shares being too high to ensure that purchases under the NCIB benefit Silver Wheaton or its shareholders; |

| | equity price risks related to Silver Wheaton’s holding of long-term investments in other exploration and mining companies; |

| | | risks related to the declaration, timing and payment of dividends; |

| | the ability of Silver Wheaton and the Mining Operations to retain key management employees or procure the services of skilled and experienced personnel; |

| | | litigation risk associated with outstanding legal matters; |

| | | risks related to claims and legal proceedings against Silver Wheaton or the Mining Operations; |

| | | risks relating to unknown defects and impairments; |

| | | risks relating to security over underlying assets; |

| | | risks related to ensuring the security and safety of information systems, including cyber security risks; |

| | | risks related to the adequacy of internal control over financial reporting; |

| | | risks related to governmental regulations; |

| | | risks related to international operations of Silver Wheaton and the Mining Operations; |

| | | risks relating to exploration, development and operations at the Mining Operations; |

| | risks related to the ability of the companies with which the Company has precious metal purchase agreements to perform their obligations under those precious metal purchase agreements in the event of a material adverse effect on the results of operations, financial condition, cash flows or business of such companies; |

| | | risks related to environmental regulation and climate change; |

| | the ability of Silver Wheaton and the Mining Operations to obtain and maintain necessary licenses, permits, approvals and rulings; |

| | the ability of Silver Wheaton and the Mining Operations to comply with applicable laws, regulations and permitting requirements; |

| | | lack of suitable infrastructure and employees to support the Mining Operations; |

| | | uncertainty in the accuracy of mineral reserve and mineral resource estimates; |

| | | inability to replace and expand mineral reserves; |

| | risks relating to production estimates from Mining Operations, including anticipated timing of the commencement of production by certain Mining Operations; |

| | uncertainties related to title and indigenous rights with respect to the mineral properties of the Mining Operations; |

SILVER WHEATON2015 ANNUAL INFORMATION FORM [2]

| | | fluctuation in the commodity prices other than silver or gold; |

| | | the ability of Silver Wheaton and the Mining Operations to obtain adequate financing; |

| | | the ability of Mining Operations to complete permitting, construction, development and expansion; |

| | | challenges related to global financial conditions; |

| | | risks relating to future sales or the issuance of equity securities; and |

| | | other risks disclosed under the heading “Risk Factors” in this annual information form. |

Forward-looking statements are based on assumptions management currently believes to be reasonable including, but not limited to:

| | | the Common Shares trading below their value from time to time; |

| | | no material adverse change in the market price of commodities; |

| | that the Mining Operations will continue to operate and the mining projects will be completed in accordance with public statements and achieve their stated production estimates; |

| | | the continuing ability to fund or obtain funding for outstanding commitments; |

| | | Silver Wheaton’s ability to source and obtain accretive precious metal stream interests; |

| | expectations regarding the resolution of legal and tax matters, including the ongoing class action litigation and CRA audit involving the Company; |

| | | Silver Wheaton will be successful in challenging any reassessment by the CRA; |

| | | Silver Wheaton has properly considered the application of Canadian tax law to its structure and operations; |

| | Silver Wheaton will continue to be permitted to post security for amounts sought by the CRA under notices of reassessment; |

| | | Silver Wheaton has filed its tax returns and paid applicable taxes in compliance with Canadian tax law; |

| | | Silver Wheaton will not change its business as a result of any CRA reassessment; |

| | Silver Wheaton’s ability to enter into new precious metal purchase agreements will not be impacted by any CRA reassessment; |

| | expectations and assumptions concerning prevailing tax laws and the potential amount that could be reassessed as additional tax, penalties and interest by the CRA; |

| | any foreign subsidiary income, if taxable in Canada, would be subject to the same or similar tax calculations as Silver Wheaton’s Canadian income, including the Company’s position, in respect of precious metal purchase agreements with upfront payments paid in the form of a deposit, that the estimates of income subject to tax is based on the cost of precious metal acquired under such precious metal purchase agreements being equal to the market value of such precious metal; |

| | the estimate of the recoverable amount for any precious metal purchase agreement with an indicator of impairment; and |

| | | other assumptions and factors as set out herein. |

Although Silver Wheaton has attempted to identify important factors that could cause actual results, level of activity, performance or achievements to differ materially from those contained in forward-looking statements, there may be other factors that cause results, level of activity, performance or achievements not to be as anticipated, estimated or intended. There can be no assurance that forward- looking statements will prove to be accurate and even if events or results described in the forward-looking statements are realized or substantially realized, there can be no assurance that they will have the expected consequences to, or effects on, Silver Wheaton. Accordingly, readers should not place undue reliance on forward-looking statements and are cautioned that actual outcomes may vary. The forward-looking statements included herein are for the purpose of providing investors with information to assist them in understanding Silver Wheaton’s expected financial and operational performance and may not be appropriate for other purposes. Any forward-looking statement speaks only as of the date on which it is made. Silver Wheaton does not undertake to update any forward-looking statements that are included or incorporated by reference herein, except in accordance with applicable securities laws.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [3]

Currency Presentation and Exchange Rate Information

This annual information form contains references to United States dollars and Canadian dollars. All dollar amounts referenced, unless otherwise indicated, are expressed in United States dollars. Canadian dollars are referred to herein as “Canadian dollars” or “C$”.

The high, low and closing noon spot rates for Canadian dollars in terms of the United States dollar for each of the three years in the period ended December 31, 2015, as quoted by the Bank of Canada, were as follows:

| | | Year ended December 31 | |

| | | 2015 | | | 2014 | | | 2013 | |

| | | | | | | | | | |

| High | | C$1.3959 | | | C$1.1643 | | | C$1.0706 | |

| Low | | 1.1763 | | | 1.0614 | | | 0.9832 | |

| Closing | | 1.3839 | | | 1.1601 | | | 1.0623 | |

On March 29, 2016, the noon spot rate for Canadian dollars in terms of the United States dollar, as quoted by the Bank of Canada, was US$1.00 = C$1.3154.

Silver Prices

The high, low, average and closing fixing silver prices in United States dollars per troy ounce for each of the three years in the period ended December 31, 2015, as quoted by the London Bullion Market Association (“LBMA”), were as follows:

| | | Year ended December 31 | |

| | | 2015 | | | 2014* | | | 2013 | |

| | | | | | | | | | |

| High | $ | 18.23 | | $ | 22.05 | | $ | 32.23 | |

| Low | | 13.71 | | | 15.28 | | | 18.61 | |

| Average | | 15.68 | | | 19.09 | | | 23.79 | |

| Closing | | 13.82 | | | 15.79 | | | 19.50 | |

* During 2014, the calculation of silver prices was transitioned to an electronic, auction-based benchmark.

On March 29, 2016, the LBMA Silver Price in United States dollars per troy ounce, as published by the LBMA, was $15.06.

Gold Prices

The high, low, average and closing afternoon fixing gold prices in United States dollars per troy ounce for each of the three years in the period ended December 31, 2015, as quoted by the LBMA, were as follows:

| | | Year ended December 31 | |

| | | 2015* | | | 2014 | | | 2013 | |

| | | | | | | | | | |

| High | $ | 1295.75 | | $ | 1,385.00 | | $ | 1,693.75 | |

| Low | | 1049.40 | | | 1,142.00 | | | 1,192.00 | |

| Average | | 1160.06 | | | 1,266.40 | | | 1,411.23 | |

| Closing | | 1160.00 | | | 1,206.00 | | | 1,204.50 | |

* During March 2015, the calculation of gold prices was transitioned to an electronic, auction-based benchmark.

On March 29, 2016, the LBMA Gold Price PM in United States dollars per troy ounce, as published by the LBMA, was $1,226.00.

SILVER WHEATON2015 ANNUAL INFORMATION FORM[4]

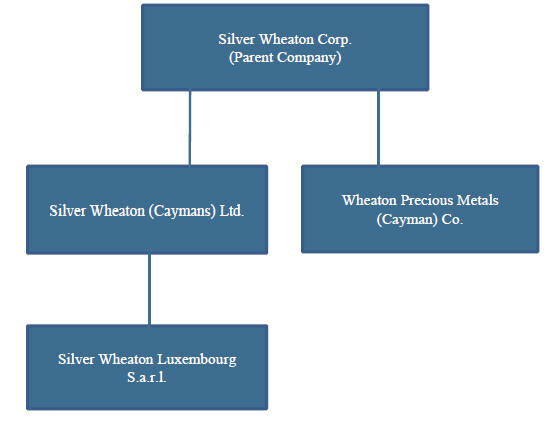

CORPORATE STRUCTURE

Pursuant to Articles of Continuance dated December 17, 2004, Silver Wheaton was continued under theBusiness Corporations Act (Ontario) (the “Act”).

The Company’s head office is located at 3500 – 1021 West Hastings Street, Vancouver, British Columbia, V6E 0C3 and its registered office is located at Suite 2100, 40 King Street West, Toronto, Ontario, M5H 3C2.

The Company’s active subsidiaries are Silver Wheaton (Caymans) Ltd. (“Silver Wheaton Caymans”) and Wheaton Precious Metals (Cayman) Co. (“Wheaton Precious Metals”), each of which is wholly-owned by the Company and is governed by the laws of the Cayman Islands and Silver Wheaton Luxembourg S.a.r.l. (“Silver Wheaton Luxembourg”) which is wholly-owned by Silver Wheaton Caymans and is governed by the laws of Luxembourg. As used in this annual information form, except as otherwise required by the context, reference to “Silver Wheaton” or the “Company” means Silver Wheaton Corp., Silver Wheaton Caymans, Silver Wheaton Luxembourg and Wheaton Precious Metals.

SILVER WHEATON AND ITS PRINCIPAL SUBSIDIARIES

SILVER WHEATON2015 ANNUAL INFORMATION FORM [5]

GENERAL DEVELOPMENT OF THE BUSINESS

Three Year History

| 2013 | | 2014 | | 2015 |

| | | | | |

| February | | August | | February |

| Entered into New revolving and non- revolving credit facilities | | Acquisition of first royalty interest on Metates properties | | Increase of revolving credit facility to $2 billion and termination of non- revolving credit facility |

| | | | | |

| February | | December | | March |

| Acquisition of $1.9 billion total gold streams on Salobo mine & Sudbury mine | | Amendment to extend deliveries from Barrick Gold Corporation’s producing mines for 15 months | | Completed $800 million Common Share offering |

| | | | | |

| November | | December | | March |

| Acquisition of $135 million gold stream on Constancia mine | | Cancellation of silver stream on Campo Morado mine | | Acquisition of additional $900 million gold stream on Salobo mine |

| | | | | |

| November | | | | April |

| Acquisition of early deposit gold stream on Toroparu project | | | | Early deposit acquisition of $5 million silver stream on Toroparu project |

| | | | | |

| | | | | July/September |

| | | | Receipt of CRA proposal letter and reassessments |

| | | | | |

| | | | | November |

| | | | Acquisition of $900 million silver stream on Antamina mine |

SILVER WHEATON2015 ANNUAL INFORMATION FORM [6]

Streaming Transactions

Antamina Transaction (Peru)

On November 3, 2015, Silver Wheaton Caymans entered into an agreement (the “Antamina Purchase Agreement”) to acquire from Anani Investments Ltd. (“Anani”), a subsidiary of Glencore plc (“Glencore”), an amount of silver equal to 33.75% of the silver production from the Antamina mine in Peru until the delivery of 140 million ounces of silver and 22.5% of silver production thereafter for the life of mine at a fixed 100% payable rate. Silver Wheaton Caymans paid total upfront cash consideration of $900 million for the silver stream in December 2015 by using cash on hand together with amounts drawn from the Company’s $2 billion Amended Revolving Facility (as defined herein). In addition, Silver Wheaton Caymans will make ongoing payments of 20% of the spot price per silver ounce delivered under the Antamina Purchase Agreement. In connection with the Antamina Purchase Agreement, Glencore and Noranda Antamina SCRL (the holder of Glencore’s interest in the Antamina mine) also provided Silver Wheaton Caymans with corporate guarantees and certain other assurances, including encumbrance and debt restrictions by Noranda.

The Antamina transaction immediately increases Silver Wheaton's production and cash flow profile by adding expected average silver production of 4.7 million ounces per year over the first 20 years. |

Vale Transactions

SALOBOMINE(BRAZIL)

On February 28, 2013, Silver Wheaton Caymans entered into an agreement (the “Salobo Purchase Agreement”) to acquire from Vale Switzerland SA (“Vale Switzerland”), a subsidiary of Vale S.A. (“Vale”), an amount of gold equal to 25% of the life of mine gold production from its currently producing Salobo mine (the “Salobo mine”), located in Brazil. Silver Wheaton Caymans paid total upfront cash consideration of $1.33 billion in March 2013. Vale also provided Silver Wheaton Caymans with a corporate guarantee.

Silver Wheaton completed over $1.8 billion in stream acquisitions in 2015. |

On March 2, 2015, Silver Wheaton Caymans agreed to amend the Salobo Purchase Agreement with Vale Switzerland (the “Amended Salobo Purchase Agreement”) to acquire from Vale Switzerland an additional amount of gold equal to 25% of the life of mine gold production from any minerals from the Salobo mine that enter the Salobo mineral processing facility from and after January 1, 2015. With this amendment, Silver Wheaton Caymans increased the gold stream from 25% to 50% of the life of mine gold production from the Salobo mine.

Under the Amended Salobo Purchase Agreement, Silver Wheaton Caymans paid Vale cash consideration of $900 million on March 24, 2015 for the increased gold stream. In addition, Silver Wheaton Caymans is required to make ongoing payments of the lesser of $400 per ounce of gold plus an inflationary adjustment of 1% commencing as of January 1, 2017 for the full 50% of gold production or the prevailing market price per ounce of gold delivered.

As reported by Vale, Vale is in the process of ramping up mill throughput at the Salobo mine from 12 million tonnes per annum (“Mtpa”) to 24 Mtpa, with the potential to further increase throughput beyond 24 Mtpa. Under the terms of the Amended Salobo Purchase Agreement, if the expansion to 24 Mtpa is not completed by December 31, 2016, Silver Wheaton Caymans continues to be entitled to a gross up (a temporary increased percentage of gold production) based on the pro-rata achievement of the target production. Extensive mineral reserves and exploration potential suggest that an even greater throughput expansion potential exists. If throughput capacity is expanded within a predetermined period, Silver Wheaton Caymans will be required to make an additional payment to Vale, relative to the 50% stream, based on a set fee schedule ranging from $88 million if throughput is expanded beyond 28 Mtpa by January 1, 2036, to up to $720 million if throughput is expanded beyond 40 Mtpa by January 1, 2018. There will be no additional deposit due if the expansion does not occur until after January 1, 2036.

See “Further Disclosure Regarding Mineral Projects on Material Properties – Salobo Mine, Brazil” for details regarding the Salobo mine.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [7]

SUDBURYMINE(CANADA)

On February 28, 2013, the Company entered into an agreement to acquire from Vale an amount of gold equal to 70% of the payable gold production from certain of its currently producing Sudbury mines located in Canada, including the Coleman mine, Copper Cliff mine, Garson mine, Stobie mine, Creighton mine, Totten mine and the Victor project (the “Sudbury mines”) for a period of 20 years. Silver Wheaton made a total upfront cash payment in March, 2013 of $570 million plus warrants to purchase 10 million Common Shares of Silver Wheaton common stock at a strike price of $65, with a term of 10 years. In addition, Silver Wheaton will make ongoing payments of the lesser of $400 per ounce of gold or the prevailing market price per ounce of gold delivered. In connection with the Sudbury agreement, Vale also provided Silver Wheaton Caymans with a corporate guarantee.

Hudbay Transaction

CONSTANCIAMINE(INCLUDINGPAMPACANCHADEPOSIT)(PERU)

On August 8, 2012, Silver Wheaton Caymans entered into an agreement with Hudbay Minerals Inc. (“Hudbay”) and its subsidiary Hudbay (BVI) Inc. to acquire 100% of the life of mine payable silver production from the Constancia mine in Peru (the “Constancia mine”). On November 4, 2013, Silver Wheaton Caymans amended its agreement with Hudbay to include the acquisition of an amount equal to 50% of the life of mine payable gold production from the Constancia mine.

As at the end of the first quarter of 2014, as a result of capital expenditures at the Constancia mine reaching $1 billion, a $125 million cash payment was made by Silver Wheaton Caymans to Hudbay. On September 10, 2014, Silver Wheaton Caymans further amended its agreement with Hudbay and as a result of capital expenditures meeting the $1.35 billion requirement, on September 26, 2014 Silver Wheaton Caymans paid further cash consideration of $135 million to Hudbay by delivery of 6,112,282 Common Shares, at an average issuance price of $22.09 per share. As at December 31, 2014, Silver Wheaton Caymans had paid Hudbay total upfront cash consideration of $429.9 million.

Silver Wheaton Caymans will make ongoing payments of the lesser of $5.90 per ounce of silver and $400 per ounce of gold (both subject to an inflationary adjustment of 1% beginning in the fourth year) or the prevailing market price per ounce of silver and gold delivered.

The silver and gold production at the Constancia mine are subject to the same completion test. The completion test requires Hudbay to complete the Constancia mine processing plant to at least 90% of expected throughput and silver recovery by December 31, 2016. If Hudbay fails to satisfy the requirements of the completion test, Silver Wheaton Caymans would be entitled to continued delivery of 100% of the gold production from Hudbay’s 777 mine. If the completion test has not been satisfied by December 31, 2020, Silver Wheaton Caymans would be entitled to a proportionate return of the upfront cash consideration relating to the Constancia mine. In addition, Silver Wheaton Caymans would be entitled to additional compensation in respect of the gold stream should there be a delay in achieving completion or mining the Pampacancha deposit (the “Pampacancha deposit”) beyond the end of 2018. Hudbay has granted Silver Wheaton Caymans a right of first refusal on any future streaming agreement, royalty agreement, or similar transaction related to the production of silver or gold from the Constancia mine. In connection with the Hudbay agreement, Hudbay and Hudbay Peru S.A.C. each provided Silver Wheaton Caymans with corporate guarantees and certain other security over their assets and the Constancia mine. Silver Wheaton Caymans has also entered into intercreditor arrangements with lenders to Hudbay.

Recovery rates for gold under the amended agreement have been fixed given the early nature of the metallurgical test work on gold recoveries from the Pampacancha deposit. Recoveries will be set at 55% for the Constancia mine deposit and 70% for the Pampacancha deposit until Silver Wheaton Caymans receives 265,000 payable ounces, after which actual recoveries will be applied.

The Constancia mine commenced commercial production on May 1, 2015 (Hudbay’s 2015 annual MD&A). |

According to Hudbay’s annual management’s discussion and analysis (“MD&A”) for the year ended December 31, 2015, during the fourth quarter of 2015, mining operations continued as planned and cost optimization is underway. Equipment availabilities are within design parameters and both loading and hauling efficiencies remain consistent with expectations. Hudbay reported that during the fourth quarter of 2015, shipments of copper concentrate from the Constancia mine to the port in Matarani increased with improved trucking capacity, resulting in significant inventory drawdown.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [8]

Hudbay also reported that expansion at the port of Matarani is nearing completion, and initial shipments from the new “Pier F” facility began in mid-February 2016. Completion of the new facility is expected to alleviate port congestion as other mines ramp up production.

Hudbay also reported that Constancia's production in the first quarter of 2016 is expected to be affected by the planned replacement of the trunnions on both the SAG and ball mills on one of the two grinding circuits. The trunnions were damaged due to a lubrication failure during the commissioning period, and the affected line is expected to be shut down at the end of February to begin an estimated six to eight-week outage to replace the trunnions, during which the second grinding circuit should continue to operate normally.

Early Deposit Gold and Silver Interest – Sandspring Transaction (Guyana)

On November 11, 2013, Silver Wheaton Caymans entered into a life of mine early deposit precious metal purchase agreement (the “Toroparu Early Deposit Agreement”) to acquire from Sandspring Resources Ltd. (“Sandspring”) an amount of gold equal to 10% of the gold production from its Toroparu project (the “Toroparu project”) located in the Republic of Guyana, South America. Under the Toroparu Early Deposit Agreement, the Company agreed to pay Sandspring total upfront cash consideration of $148.5 million, of which $13.5 million has been paid to date, with the additional $135 million payable on an installment basis to partially fund construction of the mine. In addition, the Company will make ongoing payments of the lesser $400 per ounce of gold (subject to an inflationary adjustment of 1% beginning in the fourth year of satisfaction of the completion test) or the prevailing market price per ounce of gold delivered.

On April 22, 2015, the Company amended the Toroparu Early Deposit Agreement to include the acquisition of an amount equal to 50% of the payable silver production from the Toroparu project. Silver Wheaton Caymans will make a total upfront cash payment of $5 million in connection with this amendment, of which $2 million has been paid to date, and $3 million will be payable on an installment basis to partially fund construction of the mine. In addition, Silver Wheaton will make ongoing payments of the lesser of $3.90 per ounce of silver (subject to an inflationary adjustment of 1% beginning in the fourth year of satisfaction of the completion test) or the prevailing market price per ounce of silver delivered. As a result of the addition of the silver stream to the Toroparu Early Deposit Agreement, Silver Wheaton will now pay Sandspring a total upfront cash consideration of $153.5 million. In connection with the amendment to the Toroparu Early Deposit Agreement, Sandspring and ETK Inc., the owner of the Toroparu project, provided Silver Wheaton with corporate guarantees and certain other security over their assets.

Under the amended Toroparu Early Deposit Agreement, the due date for the feasibility study, environmental study and impact assessment and other related documents (collectively the “Toroparu Feasibility Documentation”) was extended to December 31, 2016. There will be a 60 day period following the delivery of Toroparu Feasibility Documentation, or after December 31, 2016 if the Toroparu Feasibility Documentation has not been delivered to Silver Wheaton by such date, where Silver Wheaton may elect not to proceed with the Toroparu Early Deposit Agreement. If Silver Wheaton elects to terminate, Silver Wheaton will be entitled to a return of the amounts advanced less $2 million which is non-refundable or, at Sandspring’s option, the gold stream percentage will be reduced from 10% to 0.909% and the silver stream percentage will be reduced from 50% to nil.

For relatively little upfront capital, the early deposit model allows Silver Wheaton access to high-quality, earlier stage projects. |

Early Deposit Gold and Silver Interest – Panoro Minerals Transaction (Peru)

On January 27, 2016, Silver Wheaton Caymans signed a nonbinding term sheet with Panoro Minerals Ltd. and its wholly owned subsidiary Cordillera Copper Ltd. (“Panoro”) to enter into an early deposit precious metal purchase agreement (the “Cotabambas Early Deposit Agreement”) for the Cotabambas project located in Peru (the “Cotabambas project”). On March 21, 2016, Silver Wheaton Caymans entered into the definitive Cotabambas Early Deposit Agreement.

Under the terms of the Cotabambas Early Deposit Agreement, Silver Wheaton Caymans is entitled to purchase 100% of the payable silver production and 25% of the payable gold production from the Cotabambas project until 90 million silver equivalent ounces attributable to Silver Wheaton Caymans have been delivered, at which point the stream would decrease to 66.67% of payable silver production and 16.67% of payable gold production for the life of mine. Under the Cotabambas Early Deposit Agreement, Silver Wheaton Caymans will pay a total cash consideration of US$140 million plus an ongoing production payment of the lesser of: (i) US$5.90 for each silver ounce and US$450 for each gold ounce (both subject to a 1% annual inflation adjustment starting in the fourth year after the completion test is satisfied) and (ii) the

SILVER WHEATON2015 ANNUAL INFORMATION FORM [9]

prevailing market price. Once certain conditions have been met, Silver Wheaton Caymans will advance US$14 million to Panoro, spread over up to nine years. Following the delivery of certain feasibility documentation Silver Wheaton Caymans may elect to terminate the Cotabambas Early Deposit Agreement. If Silver Wheaton Caymans elects to terminate, Silver Wheaton Caymans will be entitled to a return of the portion of the US$14 million paid less US$2 million payable upon certain triggering events occurring. Until January 1, 2020, Panoro has a one-time option to repurchase 50% of the precious metals stream on a change in control for an amount based on a calculated rate of return for Silver Wheaton Caymans.

Royalty Transactions

Chesapeake Gold Transaction (Mexico)

On August 7, 2014, the Company, through its wholly owned subsidiary Wheaton Precious Metals purchased a 1.5% net smelter return royalty interest (the “Royalty”) in the Metates properties from Chesapeake Gold Corp. (“Chesapeake”) for $9 million. Under the terms of the agreement, at any time prior to August 7, 2019, Chesapeake may reacquire two-thirds of the Royalty, or 1%, for the sum of $9 million. The Company also has a right of first refusal on any silver streaming, royalty or any other transaction on the Metates properties. In connection with the Royalty, American Gold Metates, S. de R.L. de C.V., the owner of the Metates properties, granted Silver Wheaton a mortgage on the Metates properties.

Canada Revenue Agency Dispute and Audit of International Transactions

On July 6, 2015, the Company received a proposal letter (the “Proposal”) from the Canada Revenue Agency (the “CRA”) in which the CRA was proposing to reassess the Company under the transfer pricing provisions contained in the Income Tax Act (Canada) (the “Tax Act”). Subsequent to the issuance of the Proposal, on September 24, 2015, the Company received Notices of Reassessment (the “Reassessments”) from the CRA for the 2005-2010 taxation years. The Reassessments are consistent with the Proposal and seek to increase Silver Wheaton’s income subject to tax in Canada for the 2005-2010 taxation years by approximately C$715.3 million, which would result in federal and provincial taxes of approximately C$201.3 million. In addition, the CRA is seeking to impose transfer pricing penalties of approximately C$71.5 million and interest and other penalties of C$80.6 million (calculated to September 24, 2015) for the 2005-2010 taxation years. Total tax, interest and penalties sought by the CRA for the 2005-2010 taxation years is C$353.4 million. The CRA’s position in the Reassessments is that the transfer pricing provisions of the Tax Act relating to income earned by Silver Wheaton’s foreign subsidiaries outside of Canada should apply such that Silver Wheaton’s income subject to tax in Canada should be increased by an amount equal to substantially all of the income earned outside of Canada by Silver Wheaton’s foreign subsidiaries for the 2005 to 2010 taxation years.

Management believes that it has filed its tax returns and paid applicable taxes in compliance with Canadian tax law, and as a result no amounts have been recorded for any potential liability arising from this matter. Silver Wheaton intends to vigorously defend its tax filing positions.

Silver Wheaton believes that it has filed its tax returns and paid applicable taxes in compliance with Canadian tax law. |

On October 8, 2015, Silver Wheaton filed a notice of objection for each of the 2005-2010 taxation years. Silver Wheaton is required to make a deposit of 50% of the reassessed amounts of tax, interest and penalties. On March 1, 2016, the Company received approval from the CRA to post security in the form of a letter of guarantee for this amount as opposed to a cash deposit. The letter of guarantee in the amount of Cdn$191.7 million which includes interest accrued to-date plus estimated interest for the following year was delivered to the CRA on March 15, 2016(1).

On January 8, 2016, Silver Wheaton filed a Notice of Appeal with the Tax Court of Canada, electing to pursue resolution of the matters relating to the Reassessments issued by the CRA for the 2005-2010 taxation years through a judicial court process rather than continue to pursue the CRA’s internal appeals process. The timing for the court process is uncertain.

On January 19, 2016, Silver Wheaton received correspondence advising that the CRA would be commencing an audit of the Company's international transactions covering the 2011-2013 taxation years. This correspondence is not a proposal or notice of reassessment and the Company is not in a position to determine what, if any, position the CRA will

| (1) | See Note (1) to Status of CRA Matters table below. |

SILVER WHEATON2015 ANNUAL INFORMATION FORM [10]

take in respect of the 2011-2013 taxation years. However, if the CRA were to take a position similar to that underlying the Reassessments for the 2005-2010 taxation years, the Company estimates that the CRA could assert that taxes payable in Canada would increase for the 2011-2013 taxation years by approximately US$310 million(2)(3). Taxation years subsequent to 2013 also remain open to audit by the CRA.

The timing of the court process for the 2005-2010 taxation years and the audit of the 2011-2013 taxation years is uncertain; however, management intends to vigorously defend any challenge to the Company's tax filing positions. For ease of reference, the following provides an overview of the current status of CRA matters:

Status of CRA Matters

| CRA Position/Status | Potential IncomeInclusion | Potential Income TaxPayable | PaymentsMade/Pending | Timing |

| 2005-2010taxationyears | Transfer pricing provisions of the Tax Act should apply such that Silver Wheaton’s income subject to tax in Canada should be increased by an amount equal to substantially all of the income earned outside of Canada by Silver Wheaton’s foreign subsidiaries. | CRA has reassessed Silver Wheaton and is seeking to increase Silver Wheaton’s income subject to tax in Canada by C$715.3 million. | CRA has reassessed Silver Wheaton and is seeking to impose income tax of C$201.3 million, transfer pricing penalties of C$71.5 million and interest (calculated to September 24, 2015) and other penalties of C$80.6 million for total of C$353.4 million.(1) | Silver Wheaton received approval from the CRA to post security in the form of a letter of guarantee. Letter of guarantee in the amount of C$191.7 million which includes interest accrued to date plus estimated interest for the following year delivered March 15, 2016.(1) | Notice of Appeal filed January 8, 2016. Timing of resolution of the matter in court is uncertain. |

| | | | | | |

| 2011-2013taxationyears | CRA Audit commenced January 19, 2016. CRA hasnotissued a proposal or reassessment. | If CRA were to reassess on similar basis as 2005-2010 taxation years, CRA would seek to increase Silver Wheaton’s income subject to tax in Canada by approximately US$1.2 billion.(2) | If CRA were to audit and reassess on similar basis as 2005-2010 taxation years, CRA would seek to impose income tax of approximately US$310 million. (2) (3) | N/A | Time to complete CRA audit unknown. |

| | | | | | |

| 2014-2015taxationyears | Remain open to audit by CRA. | If CRA were to audit and reassess on similar basis as 2005-2010 taxation years, CRA would seek to increase Silver Wheaton’s income subject to tax in Canada by approximately US$410 million.(2) | If CRA were to audit and then reassess on similar basis as 2005- 2010 taxation years, CRA would seek to impose income tax of approximately US$106 million.(2)(3) | N/A | N/A |

| See Cautionary Note Regarding Forward-Looking Statements and Risk Factors in this Annual Information Form for material risks, assumptions and important disclosure. |

| (1) | Estimates of interest given as of the date stated. Interest accrues until payment date. |

| (2) | For precious metal purchase agreements with upfront payments paid in the form of a deposit, the estimates of income inclusion and tax payable are based on the cost of precious metal acquired under such precious metal purchase agreements being equal to the market value of such precious metal. |

| (3) | This amount does not include potential interest and penalties to the extent may be applicable. |

SILVER WHEATON2015 ANNUAL INFORMATION FORM [11]

U.S. Shareholder Class Action

During July 2015, after the receipt of the Proposal, two putative securities class action lawsuits were filed against the Company in the U.S. District Court for the Central District of California in connection with the Proposal (the “Complaints”).

On October 19, 2015, the Complaints were consolidated into one action,In re Silver Wheaton Securities Litigation, as against the Company, Randy Smallwood, President & Chief Executive Officer, Gary Brown, Senior Vice President & Chief Financial Officer and Peter Barnes, former Chief Executive Officer (together the “Defendants”) and a lead plaintiff (the “Plaintiff”) was selected. On December 18, 2015, the Plaintiff filed a consolidated amended complaint (the “Amended Complaint”). The Amended Complaint alleges, among other things, that the Defendants made false and/or misleading statements, as well as failed to disclose material adverse facts about the Company’s business, operations, prospects and performance in violation of Sections 10(b) and 20(a) of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). Specifically, the Amended Complaint focuses on the Reassessments. The Amended Complaint does not specify a quantum of damages. The Amended Complaint purports to be brought on behalf of persons who purchased or otherwise acquired the Company’s securities during an alleged class period of March 30, 2011 to July 6, 2015.

On January 29, 2016, the Defendants filed a motion to dismiss and on March 4, 2016 the plaintiff filed an opposition to the motion to dismiss. A hearing date has been set for May 2016.

The Company believes the allegations are without merit and intends to vigorously defend against this matter.

Normal Course Issuer Bid

On September 18, 2015, Silver Wheaton announced that it had received approval from the Toronto Stock Exchange (“TSX”) to purchase up to 20,229,671 Common Shares (representing 5% of the Company’s 404,593,425 total issued and outstanding Common Shares as of September 11, 2015) over a period of twelve months commencing on September 23, 2015. The NCIB will expire no later than September 22, 2016. On January 27, 2016, Silver Wheaton announced that it had entered into an automatic securities purchase plan (the “Plan”) with a broker in order to facilitate repurchases of its Common Shares under the NCIB. Purchases under the Plan will be made by Silver Wheaton’s broker based on the parameters prescribed by the TSX and the New York Stock Exchange (“NYSE”), applicable Canadian securities laws and the terms of the parties' written agreement. Under the Plan, the broker may purchase Common Shares under the NCIB when Silver Wheaton would ordinarily not be permitted. The Plan commenced on January 27, 2016 and expires on September 22, 2016, and has been approved by the TSX. To March 17, 2016, Silver Wheaton has repurchased 3,060,454 common shares under the NCIB at an average price of $13.81 per share, including 2,295,665 purchased subsequent to December 31, 2015.

Amended Revolving Credit Facilities

The Amended Revolving Facility increased Silver Wheaton’s available credit to $2.0 billion. |

On February 28, 2013, the Company entered into two new credit facilities, comprised of (i) a $1.0 billion revolving credit facility having a five year term (the “Revolving Facility”); and (ii) a $1.5 billion bridge financing facility having a one year term (the “Bridge Facility”). The Revolving Facility and Bridge Facility replaced the pre-existing $400 million revolving loan and the $200 million non-revolving term loan, with the latter being repaid in full on February 22, 2013. On May 28, 2013, the Company entered into a $1 billion non-revolving term loan (“NRT Loan”) with a three-year term, extendable by one year with the unanimous consent of lenders. On March 31, 2014, the term of the NRT Loan was extended by one year to May 28, 2017. The $1 billion proceeds from the NRT Loan were used to repay the remaining balance of $560 million under the Company’s $1.5 billion Bridge Facility and $440 million outstanding under the Company’s Revolving Facility. The Bridge Facility was terminated following the repayment of the outstanding balance.

On February 27, 2015, each of The Bank of Nova Scotia and Bank of Montreal, as co-lead arrangers, joint book-runners and lenders, Canadian Imperial Bank of Commerce, Royal Bank of Canada and The Toronto-Dominion Bank, as co-documentation agents and lenders, HSBC Bank Canada, Bank of Tokyo-Mitsubishi (UFJ) (Canada) and Export Development Canada, as Senior Managers and lenders, and Bank of America, N.A., Canada Branch, Mizuho Bank, Ltd. and National Bank of Canada, as lenders agreed with the Company to amend and restate the Revolving Facility (the “Amended Revolving Facility”). The Amended Revolving Facility increased the available credit from $1 billion to $2 billion and extended the term by two years, with the Amended Revolving Facility now maturing on February 27, 2020.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [12]

As part of the Amended Revolving Facility, the financial covenants were amended to require the Company to maintain: (i) a net debt to tangible net worth ratio of less than or equal to 0.75:1; and (ii) an interest coverage ratio of greater than or equal to 3.00:1. These covenants replaced the previously applicable leverage ratio and tangible net worth covenants. Effective November 20, 2015, the Amended Revolving Facility was amended to only include cash interest expenses for the purposes of calculating the interest coverage ratio. At the Company’s option, amounts drawn under the Revolving Facility incur interest based on the Company’s leverage ratio at either (i) LIBOR plus 1.20% to 2.20%; or (ii) the Bank of Nova Scotia’s Base Rate plus 0.20% to 1.20% . Undrawn amounts under the Revolving Facility are subject to a stand-by fee of 0.24% to 0.44% per annum, dependent on the Company’s leverage ratio. Effective March 18, 2016, the maturity date for the Amended Revolving Facility was extended by one year to February 27, 2021.

The Company used proceeds drawn from the Amended Revolving Facility, together with cash on hand, to repay $1 billion of debt previously outstanding under the NRT Loan and terminated the NRT Loan. Effective December 31, 2015, the Company had $1.466 billion drawn under the Amended Revolving Facility.

Bought Deal Offering

On March 2, 2015, the Company announced that, in connection with the Amended Salobo Purchase Agreement, it had entered into an agreement with a syndicate of underwriters led by Scotiabank, pursuant to which the underwriters agreed to purchase, on a bought deal basis, 38,930,000 Common Shares at a price of $20.55 per share (the “2015 Offering”), for aggregate gross proceeds to Silver Wheaton of approximately $800 million. Silver Wheaton also agreed to grant to the underwriters an option to purchase up to an additional 5,839,500 Common Shares at a price of $20.55 per share, on the same terms and conditions as the 2015 Offering, exercisable at any time, in whole or in part, until 30 days following the closing of the 2015 Offering (the “Over Allotment Option”). On March 17, 2015, the Company announced that it had closed the 2015 Offering and received $800 million in gross proceeds (net proceeds of approximately $769 million after payment of underwriters’ fees and expenses).

Long-Term Investments

At December 31, 2015, the Company held long-term investments with a market value of approximately $19.8 million.

Bear Creek Mining Corporation

At December 31, 2015, Silver Wheaton owned approximately 13.3 million common shares of Bear Creek Mining Corporation (TSXV: BCM) (“Bear Creek”), representing approximately 14% of the outstanding shares of Bear Creek. At December 31, 2015, the fair value of the Company’s investment in Bear Creek was approximately $5.6 million.

Revett Mining Company, Inc./Hecla Mining Company

During 2015, Revett Mining Company, Inc. (formerly Revett Minerals Inc.) was acquired by Hecla Mining Company (NYSE: HL) (“Hecla”) and all former shareholders of Revett Mining Company, Inc. were issued shares of Hecla. Silver Wheaton disposed of its investment of 5.3 million common shares of Revett in the transaction. At December 31, 2015, Silver Wheaton owned approximately 0.9 million common shares of Hecla, which are included under “Other” below.

Other

At December 31, 2015, Silver Wheaton owned common shares and common share purchase warrants of several other publicly-traded mineral exploration, development and mining companies. At December 31, 2015, the fair value of such other long-term investments was approximately $14.2 million. As Silver Wheaton’s investment represents less than 10% of the outstanding shares of each of the respective companies and is not considered material to Silver Wheaton’s overall financial position, these investments are not separately identified in this annual information form.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [13]

DESCRIPTION OF THE BUSINESS

Silver Wheaton is a mining company which generates its revenue primarily from the sale of silver and gold. The Company is listed on the NYSE (symbol: SLW) and the TSX (symbol: SLW).

As of December 31, 2015, the Company has entered into 19 long-term purchase agreements and two (2) early deposit long-term purchase agreements (including the Cotabambas Early Deposit Agreement entered into subsequent to December 31, 2015) associated with silver and/or gold (“precious metal purchase agreements”), relating to 30 different mining assets, whereby Silver Wheaton acquires silver and gold production from the counterparties for a per ounce cash payment at or below the prevailing market price. The primary drivers of the Company’s financial results are the volume of silver and gold production at the various mines to which the precious metal purchase agreements relate and the price of silver and gold realized by Silver Wheaton upon sale. Attributable silver and gold as referred to in this annual information form is the silver and gold production to which Silver Wheaton is entitled pursuant to the various precious metal purchase agreements.

The Company is actively pursuing future growth opportunities, primarily by way of entering into additional long-term precious metal purchase agreements. There is no assurance, however, that any potential transaction will be successfully completed. The following map illustrates the geographic location of the Company’s diversified portfolio of interests in the 22 operating mines and eight development projects (including the Cotabambas project) comprising its high-quality asset base.

Principal Product

The Company’s principal product is silver that it has agreed to purchase pursuant to precious metal purchase agreements. The Company also acquires gold that it has agreed to purchase pursuant to precious metal purchase agreements. The following table summarizes the silver and gold interests currently owned by the Company (collectively, the “Mining Operations”). Note that statements made in this section contain forward-looking information. Please see “Cautionary Note Regarding Forward-Looking Statements” for material risks, assumptions and important disclosure associated with this information.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [14]

Silver and Gold

Interests

|

Mine

Owner

|

Location of

Mine

|

|

Upfront

Consideration1

|

|

| Attributable

Production to be

Purchased |

|

Term of

Agreement

|

Date of

Original

Contract

|

Silver

|

|

|

Gold

| |

San Dimas | Primero | Mexico | $ | 189,799 | | | 100% | 2 | | 0% | | Life of Mine | 15-Oct-04 |

Yauliyacu | Glencore | Peru | $ | 285,000 | | | variable | 3 | | 0% | | Life of Mine3 | 23-Mar-06 |

Peñasquito | Goldcorp | Mexico | $ | 485,000 | | | 25% | | | 0% | | Life of Mine | 24-Jul-07 |

Salobo | Vale | Brazil | $ | 2,230,000 | 4 | | 0% | | | 50% | | Life of Mine | 28-Feb-13 |

Sudbury | | | $ | 623,572 | 5 | | | | | | | | |

Coleman | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Copper Cliff | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Garson | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Stobie | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Creighton | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Totten | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Victor | Vale | Canada | | | | | 0% | | | 70% | | 20 years | 28-Feb-13 |

Barrick | | | $ | 625,000 | | | | | | | | | |

Pascua-Lama | Barrick | Chile/Argentina | | | | | 25% | | | 0% | | Life of Mine | 8-Sep-09 |

Lagunas Norte | Barrick | Peru | | | | | 100% | | | 0% | | 8.5 years | 8-Sep-09 |

Pierina | Barrick | Peru | | | | | 100% | | | 0% | | 8.5 years6 | 8-Sep-09 |

Veladero | Barrick | Argentina | | | | | 100% | 7 | | 0% | | 8.5 years | 8-Sep-09 |

Antamina | Glencore | Peru | $ | 900,000 | | | 33.75% | 8 | | 0% | | Life of Mine | 3-Nov-15 |

Other | | | $ | 1,482,683 | | | | | | | | | |

Los Filos | Goldcorp | Mexico | $ | 4,463 | | | 100% | | | 0% | | 25 years | 15-Oct-04 |

Zinkgruvan | Lundin | Sweden | $ | 77,866 | | | 100% | | | 0% | | Life of Mine | 8-Dec-04 |

Stratoni | Eldorado Gold 9 | Greece | $ | 57,500 | | | 100% | | | 0% | | Life of Mine | 23-Apr-07 |

Minto | Capstone | Canada | $ | 54,805 | | | 100% | | | 100% | 10 | Life of Mine | 20-Nov-08 |

Cozamin | Capstone | Mexico | $ | 41,959 | | | 100% | | | 0% | | 10 years | 4-Apr-07 |

Neves-Corvo | Lundin | Portugal | $ | 35,350 | | | 100% | | | 0% | | 50 years | 5-Jun-07 |

Aljustrel | I'M SGPS | Portugal | $ | 2,451 | | | 100% | 11 | | 0% | | 50 years | 5-Jun-07 |

Keno Hill | Alexco | Canada | $ | 50,000 | | | 25% | | | 0% | | Life of Mine | 2-Oct-08 |

Rosemont | Hudbay | United States | $ | 230,000 | 12 | | 100% | | | 100% | | Life of Mine | 10-Feb-10 |

Loma de La Plata | Pan American | Argentina | $ | 43,289 | 13 | | 12.5% | | | 0% | | Life of Mine | n/a14 |

777 | Hudbay | Canada | $ | 455,100 | | | 100% | | | 100%/50% | 15 | Life of Mine | 8-Aug-12 |

Constancia | Hudbay | Peru | $ | 429,900 | | | 100% | | | 50% | 16 | Life of Mine | 8-Aug-12 |

Early Deposit | | | | | | | | | | | | | |

Toroparu | Sandspring | Guyana | $ | 153,500 | 17 | | 50% | 17 | | 10% | 17 | Life of Mine | 11-Nov-13 |

Cotabambas | Panoro | Peru | $ | 140,000 | 18 | | 100% | 19 | | 25% | 19 | Life of Mine | 21-Mar-16 |

| 1) | Expressed in United States dollars, rounded to the nearest thousand; excludes closing costs and capitalized interest, where applicable. |

| 2) | Until August 6, 2014, Primero delivered to Silver Wheaton a per annum amount equal to the first 3.5 million ounces of payable silver produced at San Dimas and 50% of any excess, plus Silver Wheaton received an additional 1.5 million ounces of silver per annum which was delivered by Goldcorp. Beginning August 6, 2014, Primero will deliver a per annum amount to Silver Wheaton equal to the first 6 million ounces of payable silver produced at San Dimas and 50% of any excess. |

| 3) | On November 30, 2015, the Company amended its silver purchase agreement with Glencore. The term of the agreement, which was set to expire in 2026, was extended to the life of mine. Glencore will deliver a per annum amount to Silver Wheaton equal to the first 1.5 million ounces of payable silver produced at Yauliyacu and 50% of any excess. |

| 4) | Does not include the contingent payment related to the Salobo mine expansion. Vale has completed the expansion of the mill throughput capacity at the Salobo mine to 24 million tonnes per annum (“Mtpa”) from its previous 12 Mtpa. If actual throughput is expanded above 28 Mtpa within a predetermined period, Silver Wheaton will be required to make an additional payment to Vale based on a set fee schedule ranging from $88 million if throughput is expanded beyond 28 Mtpa by January 1, 2036, up to $720 million if throughput is expanded beyond 40 Mtpa by January 1, 2018. |

| 5) | Comprised of a $570 million upfront cash payment plus warrants to purchase 10 million common shares of Silver Wheaton at a strike price of $65, with a term of 10 years. |

| 6) | As per Barrick’s disclosure, closure activities were initiated at Pierina in August 2013. |

| 7) | Silver Wheaton's attributable silver production is subject to a maximum of 8% of the silver contained in the ore processed at Veladero during the period. |

| 8) | Once the Company has received 140 million ounces of silver under the Antamina Purchase Agreement, the Company’s attributable silver production to be purchased will be reduced to 22.5%. |

| 9) | 95% owned by Eldorado Gold Corporation. |

| 10) | The Company is entitled to acquire 100% of the first 30,000 ounces of gold produced per annum and 50% thereafter. |

| 11) | Silver Wheaton only has the rights to silver contained in concentrate containing less than 15% copper at the Aljustrel mine. |

| 12) | The upfront consideration is currently reflected as a contingent obligation, payable on an installment basis to partially fund construction of the Rosemont mine once certain milestones are achieved, including the receipt of key permits and securing the necessary financing to complete construction of the mine. |

| 13) | Comprised of $10.9 million allocated to the silver interest upon the Company’s acquisition of Silverstone Resources Corp. in addition to a contingent liability of $32.4 million, payable upon the satisfaction of certain conditions, including Pan American receiving all necessary permits to proceed with the mine construction. |

| 14) | Definitive terms of the agreement to be finalized. |

| 15) | Silver Wheaton is entitled to acquire 100% of the life of mine gold production from Hudbay’s 777 mine until Hudbay’s Constancia mine satisfies a completion test, or the end of 2016, whichever is later. At that point, Silver Wheaton’s share of gold production from 777 will be reduced to 50% for the life of mine. |

| 16) | Gold recoveries will be set at 55% for the Constancia deposit and 70% for the Pampacancha deposit until 265,000 ounces of gold have been delivered to the Company. |

| 17) | Comprised of $15.5 million paid to date and $138.0 million to be payable on an installment basis to partially fund construction of the mine. During the 60 day period following the delivery of the Toroparu Feasibility Documentation, or after December 31, 2016 if the Toroparu Feasibility Documentation has not been delivered to Silver Wheaton by such date, Silver Wheaton may elect not to proceed with the Toroparu Early Deposit Agreement, at which time Silver Wheaton will be entitled to a return of the amounts advanced less $2 million which is non-refundable or, at Sandspring’s option, the gold stream percentage will be reduced from 10% to 0.909% and the silver stream percentage will be reduced from 50% to nil. Silver Wheaton may also elect to terminate the Toroparu Early Deposit Agreement upon the occurrence of certain events prior to the payment of any initial construction payment and elect to reduce the stream percentages or obtain a return of the amounts advanced less $2 million. |

| 18) | The upfront consideration is currently reflected as a contingent obligation. Once certain conditions have been met, Silver Wheaton will advance $14 million to Panoro, spread over up to nine years. Following the delivery of certain feasibility documentation, Silver Wheaton may elect to terminate the Cotabambas Early Deposit Agreement. If Silver Wheaton elects to terminate, Silver Wheaton will be entitled to a return of the portion of the $14 million paid less $2 million payable upon certain triggering events occurring. Until January 1, 2020, Panoro has a one-time option to repurchase 50% of the precious metals stream on a change of control for an amount based on a calculated rate of return for Silver Wheaton. |

| 19) | Once 90 million silver equivalent ounces attributable to Silver Wheaton have been produced, the attributable production to be purchased will drop to 66.67% of silver production and 16.67% of gold production for the life of mine. |

Further details regarding the precious metal purchase agreements entered into by the Company in respect of these silver and gold interests can be found under the heading “General Development of the Business – Three Year History” above, except for the following interests which were entered into prior to the past three years:

SILVER WHEATON2015 ANNUAL INFORMATION FORM[15]

San Dimas Transaction (Mexico)

On October 15, 2004, the Company entered into a silver purchase agreement (the “San Dimas Silver Purchase Agreement”) with Goldcorp Inc. (“Goldcorp”) to acquire an amount equal to 100% of the silver produced by Goldcorp’s Luismin mining operations in Mexico (owned at the date of the transaction) for a period of 25 years. The Luismin operations consisted primarily of the San Dimas mine (the “San Dimas mine”) and Los Filos mine (the “Los Filos mine”).

On August 6, 2010, Goldcorp completed the sale of the San Dimas mine to Primero Mining Corp. (“Primero”). In conjunction with the sale, Silver Wheaton amended its silver purchase agreement relating to the mine. The term of the silver purchase agreement, as it relates to San Dimas, has been extended to the life of mine. During the first four years following the closing of the transaction, Primero delivered to Silver Wheaton a per annum amount equal to the first 3.5 million ounces of payable silver produced at the San Dimas mine and 50% of any excess, plus Silver Wheaton will receive an additional 1.5 million ounces of silver per annum to be delivered by Goldcorp. Beginning in the fifth year after closing, Primero will deliver a per annum amount to Silver Wheaton equal to the first 6 million ounces of payable silver produced at San Dimas and 50% of any excess. In addition, a per ounce cash payment of the lesser of $4.04 per ounce of silver (subject to an annual inflationary adjustment) or the prevailing market price is due, for silver delivered under the agreement. Goldcorp will continue to guarantee the delivery by Primero of all silver produced and owing to the Company until 2029. Primero has provided Silver Wheaton with a right of first refusal on any metal stream or similar transaction it enters into. In connection with the San Dimas Silver Purchase Agreement, each of Goldcorp, Primero, Primero Empresa Minera SA de CV (“PEM”) and Primero Mining Luxembourg have also provided Silver Wheaton with corporate guarantees and certain other security over their assets and the San Dimas mine. Silver Wheaton Caymans has also entered into intercreditor arrangements with lenders to Primero.

As per Primero’s MD&A for the year ended December 31, 2015, in connection with the project to expand the San Dimas mine production from 2,500 tonnes per day to 3,000 tonnes per day in 2016, Primero successfully connected the tunnel between the Sinaloa-Graben and Central mining blocks, enabling one-way traffic flow within the San Dimas mine and reducing average haulage distances by approximately 3 kilometres. This provides a critical de-bottlenecking in the flow of machinery through the San Dimas mine. At the San Dimas mill, Primero reports that they have received delivery of the new secondary crusher and the deaerator tower and has completed the foundations of the new tailings filter installations. Primero states that the new deaerator tower will start-up by the end of February 2016 and the completion of the modifications to the secondary crushing plant is expected by the end of May 2016. They further state that fabrication of the tailings filter and thickener has been affected by the severe flooding in southern India which has shifted the delivery of this equipment from India to early Q2 2016 with start-up expected in Q3 2016.

Primero has noted that three of the properties included in the Primero mine for which Primero has legal title are subject to legal proceedings commenced by Ejidos seeking title to the property. None of the proceedings name Primero as a party and Primero therefore has no standing to participate in them. In all cases, the defendants are previous owners of the properties, either deceased individuals who, according to certain public deeds, owned the properties more than 80 years ago, corporate entities that are no longer in existence, or Goldcorp companies. The proceedings also name the Tayolita Property Public Registry as co-defendant. Two of the legal proceedings were decided in favour of the Ejidos in 2015, resulting in Primero gaining standing rights as an affected third party. Primero has disclosed that it has sought to annul these decisions through an Amparo claim on the basis that it is the legitimate owner and is in possession of these properties. Primero has indicated that the San Dimas mine could face higher costs associated with agreed or mandated payments that would be payable to the Ejidos for use of the properties.

On February 3, 2016, Primero announced that its Mexican subsidiary, PEM had received a legal claim from the Mexican tax authorities, Servicio de Administración Tributaria ("SAT"), seeking to nullify the Advance Pricing Agreement ("APA") issued by SAT in 2012. The APA confirmed Primero’s basis for paying taxes on realized silver prices for the years 2010 to 2014 and represented SAT's agreement to accept that basis for those years. The legal claim initiated does not identify any different basis for paying taxes. Primero has indicated in its MD&A for the year ended December 31, 2015 that if the SAT is successful in retroactively nullifying the APA, the SAT may seek to audit and reassess PEM in respect of its sales of silver in connection with the Primero silver purchase agreement for 2010 through 2014. Primero has also indicated that while PEM would have rights of appeal in connection with any reassessments, if the legal proceeding is finally concluded in favour of the SAT, the amount of additional taxes that the SAT could charge PEM for the tax years 2010 through 2014 on the silver sold in connection with the Primero silver purchase agreement would likely have a material adverse effect on Primero’s results of operations, financial condition and cash flows. Primero has stated that it intends to vigorously defend the validity of the APA and intends to explore opportunities to minimize the potential impact

SILVER WHEATON2015 ANNUAL INFORMATION FORM [16]

on Primero in the event that the SAT is successful in its legal claim to nullify the APA, but there is no assurance that Primero will find or be able to implement a reasonable solution. Primero also notes in its MD&A for the year ended December 31, 2015 that for the 2015 tax year, Primero continued to record its revenue from sales of silver for purposes of Mexican tax accounting in a manner consistent with the APA on the basis that the applicable facts and laws have not changed. Primero indicates that its legal and financial advisors continue to believe that Primero has filed its tax returns compliant with applicable Mexican law and that Primero has until the end of 2016 to file an application for a renewed APA in respect of 2015 and the four subsequent tax years. Given the legal challenge by the SAT against the APA for the 2010-2014 tax years, Primero has indicated that it currently believes it is unlikely the SAT will agree to an Advance Pricing Agreement for the 2015-2019 tax years on terms similar to the challenged APA. Primero stated that to the extent the SAT determines that the appropriate price of silver sales under the Primero silver purchase agreement is significantly different from the price actually paid by Silver Wheaton under the Primero silver purchase agreement and while PEM would have rights of appeal in connection with any reassessments, it is likely to have a material adverse effect on Primero’s business, financial condition and results of operations.

See “Further Disclosure Regarding Mineral Projects on Material Properties – San Dimas mine, Mexico” for details regarding the San Dimas mine.

Los Filos Transaction (Mexico)

Silver Wheaton has an agreement with Goldcorp to acquire 100% of the silver production from its Los Filos mine in Mexico for a period of 25 years, commencing October 15, 2004. In addition, pursuant to Goldcorp’s sale of the San Dimas mine, Goldcorp delivered to Silver Wheaton 1.5 million ounces of silver per year until August 6, 2014, and will continue to guarantee the delivery by Primero of all silver produced and owing to the Company until 2029.

Zinkgruvan Mine (Sweden)

On December 8, 2004, Silver Wheaton Caymans entered into an agreement with Lundin Mining Corporation (“Lundin”) and Zinkgruvan Mining AB (“Zinkgruvan AB”) to acquire 100% of the payable silver produced by Lundin’s Zinkgruvan mining operations (the “Zinkgruvan mine”) in Sweden for the life of mine for the lesser of $3.90 per ounce of silver (subject to an annual inflationary adjustment) and the then prevailing market price per ounce of silver. Upfront consideration payable to Zinkgruvan AB was approximately $77.9 million. According to Lundin’s news release dated January 21, 2016, Lundin is reportedly undertaking an expansion project aimed at increasing Zinkgruvan’s mill capacity by approximately 10% by the end of 2017. In connection with the Zinkgruvan agreement, Lundin provided Silver Wheaton with a corporate guarantee and a pledge of charge deed over mining operations.

Yauliyacu Mine (Peru)

On March 23, 2006, Silver Wheaton Caymans entered into a silver purchase agreement with Glencore International AG (“Glencore International”) and Anani to acquire an amount equal to 100% of the payable silver produced from the Yauliyacu mining operations (the “Yauliyacu mine”) in Peru, up to a maximum of 4.75 million ounces per year, for a period of 20 years commencing in March of 2006, for $3.90 per ounce of silver (subject to an annual inflationary adjustment).

On November 30, 2015, Silver Wheaton Caymans amended the Yauliyacu silver purchase agreement. The term of the agreement, which was set to expire in 2026, was extended to the life of mine. Additionally, effective January 1, 2016, Glencore will deliver to Silver Wheaton a per annum amount equal to the first 1.5 million ounces of payable silver produced at the Yauliyacu mine and 50% of any excess. The price paid for each ounce of silver delivered under the agreement has been increased by an additional $4.50 per ounce plus, if the market price of silver exceeds $20 per ounce, 50% of the excess, to a maximum of $40 per ounce.

During the term of the contract, Silver Wheaton Caymans has a right of first refusal on any future sales of silver streams from the Yauliyacu mine and a right of first offer on future sales of silver streams from any other mine owned by Glencore at the time of the initial transaction. In addition, Glencore International provided Silver Wheaton with a corporate guarantee.

SILVER WHEATON2015 ANNUAL INFORMATION FORM [17]

Stratoni Mine (Greece)

On April 23, 2007, Silver Wheaton Caymans entered into a silver purchase agreement (the “Stratoni Silver Purchase Agreement”) with European Goldfields Limited (“European Goldfields”) (which was acquired by Eldorado Gold Corporation (“Eldorado”) on February 24, 2012), and Hellas Gold S.A. (“Hellas Gold”), a 95%-owned subsidiary of European Goldfields, pursuant to which Silver Wheaton Caymans agreed to purchase 100% of the payable silver produced by Hellas Gold from the Stratoni mine (the “Stratoni mine”) located in Greece over its entire mine life, for total upfront cash consideration of $57.5 million, plus a payment equal to the lesser of $3.90 per ounce of delivered silver (subject to an annual inflationary adjustment after April 23, 2010) and the then prevailing market price per ounce of silver. During the term of the Stratoni Silver Purchase Agreement, Silver Wheaton Caymans has a right of first refusal on any future sales of silver streams from any other mine owned by Hellas Gold or European Goldfields. In connection with the Stratoni Silver Purchase Agreement, Hellas Gold and European Goldfields provided certain covenants in respect of their obligations.

In October 2015, in order to incentivize additional exploration and potentially extend the limited remaining mine life of the Stratoni mine, Silver Wheaton Caymans and Eldorado agreed to modify the Stratoni Silver Purchase Agreement. The primary modification was to increase the production price per ounce of silver delivered to Silver Wheaton Caymans over the current fixed price by one of the following amounts: (i) $2.50 per ounce of silver delivered if 10,000 metres of drilling is completed outside of the existing ore body and within Silver Wheaton Cayman’s defined area of interest (“Expansion Drilling”); (ii) $5.00 per ounce of silver delivered if 20,000 metres of Expansion Drilling is completed; and (iii) $7.00 per ounce of silver delivered if 30,000 metres of Expansion Drilling is completed. Drilling in all three cases must be completed by December 31, 2020 in order for the agreed upon increase in production price to be initiated.

On January 11, 2016, Eldorado indicated that it is evaluating the merits of implementing an estimated US$25 million development and drilling campaign over the next three years at the Stratoni mine in light of the current investment climate in Greece. Eldorado has indicated that the Stratoni mine currently has a life of mine of approximately three years based on the known proven and probable reserves.

Peñasquito Mine (Mexico)

On July 24, 2007, Silver Wheaton Luxembourg entered into a silver purchase agreement (the “Peñasquito Silver Purchase Agreement”) with Goldcorp and Minera Peñasquito, S.A. de C.V. (“Minera Peñasquito”), a wholly-owned subsidiary of Goldcorp, pursuant to which Silver Wheaton Luxembourg agreed to purchase 25% of the payable silver produced by Minera Peñasquito from the Peñasquito mine located in Mexico (the ��Peñasquito mine”) over its entire mine life, for upfront consideration of $485 million, plus a payment equal to the lesser of $3.90 per ounce of delivered silver (subject to an annual inflationary adjustment three years after commercial production commences) and the then prevailing market price per ounce of silver. Silver Wheaton Luxembourg and Silver Wheaton Caymans entered into a back to back silver purchase agreement in respect of the Peñasquito mine. In connection with the Peñasquito Silver Purchase Agreement, Goldcorp also provided Silver Wheaton with a corporate guarantee.

As disclosed in Goldcorp MD&A for the year ended December 31, 2015, construction of the Northern Well Field project ("NWF") resumed during the fourth quarter of 2015 following prior suspension of construction due to an illegal blockade by a local community. Completion of the NWF is now expected to be in late 2016. Contingency plans remain in place to ensure that fresh water supply to the mine continues unimpeded until the NWF is fully operational.

During the fourth quarter of 2015, Goldcorp completed the Metallurgical Enhancement Project ("MEP") Feasibility Study and determined that the Concentrate Enrichment Process component of the MEP no longer met Goldcorp’s required rates of return due to improved fundamentals in the concentrate smelting market. The other component of the MEP, the Pyrite Leach Plant ("PLP") envisages leaching a pyrite concentrate from the zinc flotation circuit tails to recover gold and silver that would otherwise report to the tailings facility at the Peñasquito mine. Goldcorp states that an investment decision on PLP is expected by mid-2016, which, if approved, is expected to be in production by the end of 2018.