CORPORATE

PROFILE

SILVER WHEATON IS THE WORLD’S LARGEST PURE PRECIOUS METALS STREAMING COMPANY. IT OFFERS INVESTORS COST CERTAINTY, LEVERAGE TO INCREASING SILVER AND GOLD PRICES, AND GROWTH FROM A HIGH-QUALITY ASSET BASE. ITS BUSINESS MODEL IS BASED ON PAYING LOW, PREDICTABLE COSTS FOR PRECIOUS METALS FROM STREAMS ON A DIVERSE PORTFOLIO OF MINES, WITH ANY INCREASES IN PRECIOUS METAL PRICES FLOWING DIRECTLY TO THE BOTTOM LINE.

2

2015 REVIEW

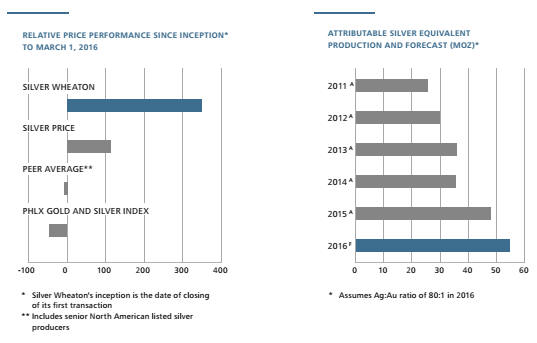

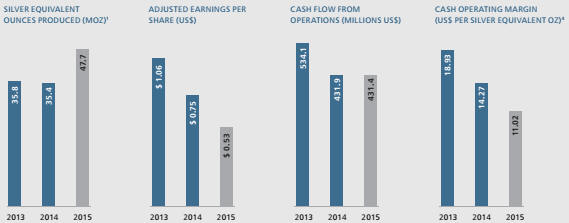

Silver Wheaton’s year over year production increased 35% and sales volume increased 26% in 2015. Attributable production was 47.7 million silver equivalent ounces, resulting in adjusted net earnings of $210.4 million ($0.53 per share) and operating cash flows of $431.4 million ($1.09 per share). With an average annual realized silver equivalent price of $15.60 per ounce, and cash operating costs1 of $4.58 per silver equivalent ounce, the cash operating margin1 in 2015 was $11.02 per silver equivalent ounce, or over 70%.

In 2016, based upon the company’s current portfolio of low-cost, long-life assets, attributable production is forecast to be approximately 54 million silver equivalent ounces, including 265,000 ounces of gold. Estimated average annual attributable production over the next five years is anticipated to be approximately 52 million silver equivalent ounces per year, including 260,000 ounces of gold.

Silver Wheaton’s future growth profile is expected to be driven by precious metal and gold streams on the Antamina, Salobo, Peñasquito and Constancia mines.

The company’s unique business model creates shareholder value by providing:

Leverage to increases in the price of silver and gold;

Organic growth through the acquisition of new streams;

A dividend yield tied to precious metal prices and our organic growth; and,

Participation in the expansion and exploration success of the mines underlying its current agreements.

Silver Wheaton offers these benefits, while seeking to reduce many of the downside risks faced by traditional mining companies. In particular, Silver Wheaton offers its investors both capital and operating cost certainty. Other than the initial upfront payment, the company typically has no ongoing capital or exploration costs. Furthermore, operating costs have been historically fixed at around $4 per ounce of silver produced and $400 per ounce of gold produced, subject to defined inflationary adjustments.

1 Refer to discussion on non-IFRS measures in the MD&A.

SILVER WHEATON 2015 ANNUAL REPORT 3

LETTER FROM

THE PRESIDENT & CEO

2015 WAS ANOTHER RECORD-BREAKING YEAR FOR SILVER WHEATON AS THE COMPANY’S ATTRIBUTABLE PRODUCTION INCREASED BY OVER 12 MILLION SILVER EQUIVALENT OUNCES AND WE CONTINUED TO GENERATE SOLID CASH FLOWS WITH CASH OPERATING MARGINS OF OVER 70%. THIS UNPRECEDENTED GROWTH WAS DRIVEN BOTH BY OUR EXISTING PORTFOLIO OF HIGH-QUALITY ASSETS AS WELL AS TACTICAL AND TIMELY ACQUISITIONS THAT DELIVERED IMMEDIATE RESULTS.

We achieved record production of 47.7 million silver equivalent ounces in 2015, significantly beating our 44.5 million forecast. This growth was driven organically by our fully-funded, high-quality portfolio of assets, along with our acquisitions of precious metals from two of the world’s best copper assets: the Salobo mine in Brazil and the Antamina mine in Peru.

While record sales volumes throughout the year were offset by significantly weaker commodity prices, Silver Wheaton was able to generate operating cash flows in line with 2014. Net earnings were below 2014 results due to non-cash charges being taken over the year on a few of our smaller streams.

While our assets performed well in 2015, the year was not without challenges. Along with downward pressure on precious metals prices through the year, in September we received Notices of Reassessment from the Canada Revenue Agency (CRA) for the years 2005 to 2010. We continue to vigorously defend our position and work towards the quickest avenue for resolution, and in January 2016 filed a Notice of Appeal with the Tax Court of Canada electing to pursue resolution of the matters through a judicial court process rather than to continue to pursue the CRA’s internal appeals process. We firmly believe in the strong underlying value of our shares, and, as such, initiated our first ever normal course issuer bid during the third quarter of 2015.

4

The strength of our portfolio should not be overshadowed by the dark clouds of the reassessment and weak commodity prices. Even in these times of depressed commodity prices, we continued to see growth and reinvestment in our cornerstone assets in 2015, underscoring the importance of investing in tier-one assets. We are proud of the strong performance of the San Dimas, Salobo and Peñasquito mines, and our new cornerstone addition, the Antamina mine. San Dimas, our first ever asset, had a record fourth quarter and an excellent year in 2015. It completed an expansion to 2,500 tonnes per day in the first quarter, ran well above this for most of the year, and expects to complete a further expansion to 3,000 tonnes per day in the second quarter of 2016. San Dimas has proven itself to be a great foundation asset.

Early in 2013, we acquired 25% of the gold production from the Salobo mine, the largest copper deposit ever found in Brazil. 2015 was a pivotal year for our Salobo stream, as Vale successfully ramped up the mine’s expansion, doubling its throughput. We also doubled our exposure by acquiring an additional 25% of the gold. In turn, Salobo was a key driver of our record production in 2015, and, with its significant expansion and exploration potential, we expect it to be a lead contributor going forward for many years.

In 2015, the Peñasquito mine had record production as higher grades were encountered in the core of the deposit. Goldcorp continues to construct the Northern Well Field, which should resolve water shortage issues caused by the unprecedented drought. In addition, we are excited about Goldcorp’s feasibility study on the Metallurgical Enhancement Project at Peñasquito, which has the potential to substantially increase the silver we receive over the life of the mine.

In November 2015, Silver Wheaton acquired a silver stream from Glencore tied to the Antamina mine in Peru. Antamina’s quality and scale make it the fourth cornerstone in our portfolio, as it is not only the eighth largest copper mine in the world but it is also one of the lowest cost copper mines in the world. This stream provided us with almost immediate production and operating cash flow from a proven and well-established asset, again with significant mine life ahead of it.

While our record year was driven in great part by the above-mentioned cornerstone mines, we also benefitted from the first contributions of gold and silver from Hudbay’s Constancia mine in Peru. Constancia achieved commercial production in April 2015, and Hudbay has done an excellent job of bringing the mine online and ramping up production. We have been very encouraged by Hudbay’s mine building ability, especially as they are also our partner on the Rosemont project.

Going forward, we forecast that Silver Wheaton will continue to grow from a fully-funded portfolio of streams, with most of the growth front-end loaded as a full-year of contributions from Antamina and a fully-ramped Salobo and Constancia are realized. We estimate average annual attributable production over the next five years to be approximately 52 million silver equivalent ounces per year. This does not include the optionality we have from streams such as Pascua-Lama or Rosemont, which total over an additional 19 million ounces of production per year.

On the corporate development front, we are happy to see that streaming is now a major consideration for miners seeking capital. We continue to see a number of high-quality, accretive opportunities, many from existing producers looking for funds to strengthen their balance sheets or to assist in acquisitions. While we are in a position to be able to grow, we will continue to acquire strategically and to search for well-managed, high-quality assets operating in the lowest-half of their respective cost-curves.

As we continue to grow, we also continue to give back to our communities. Since 2014, we have provided financial support for our partners’ social projects in mining communities near our partners’ mines. We are proud to be the leader in the streaming and royalty space by directly investing into the communities where we receive our precious metals. Our first projects supported Primero, to build new community facilities near San Dimas, and Barrick, to implement irrigation systems near Veladero and Pascua-Lama. We are now helping Barrick to expand their irrigation project, Goldcorp to improve education facilities near Peñasquito, and Vale to enhance medical services near Salobo. We believe these projects will have positive, long-term and sustainable benefits to these mining communities, and will also further reinforce the strength of our partnerships.

2015 was fundamentally a year of growth for Silver Wheaton, both organically and from an acquisition perspective. With record production and sector-leading cash flows, and with what we believe is the strongest asset base in the industry, we are optimistic for the future and will continue to focus on delivering growth while maintaining one of the lowest-cost profiles in the industry.

To our shareholders, partners, board of directors and employees: thank you once again for your continued commitment and support as we strive to make Silver Wheaton the premier investment vehicle for precious metals investors worldwide.

/s/ Randy Smallwood

RANDY SMALLWOOD, President & CEO

March 16, 2016

SILVER WHEATON 2015 ANNUAL REPORT 5

CORNERSTONE

ASSETS

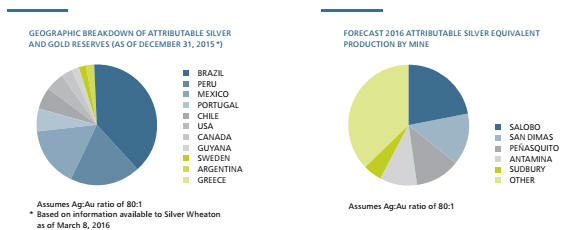

Silver Wheaton’s diversified portfolio of precious metal streams includes 22 operating mines and seven developmentprojects. With the acquisitions we made this year, we now have four cornerstone assets: the San Dimas, Peñasquito, Salobo and Antamina mines.

SAN DIMAS

Primero’s San Dimas mine had a great year, contributing 7.4 million silver ounces to Silver Wheaton in 2015, well above the forecast of 6.6 million ounces. The mine completed its expansion to 2,500 tonnes per day (tpd) in the first quarter of 2015, and was running well above nameplate capacity for most of the year. Primero is on track to complete its further expansion to 3,000 tpd in the first half of 2016.

PEÑASQUITO

Goldcorp’s Peñasquito mine produced 7.2 million ounces of silver for Silver Wheaton in 2015. Goldcorp continues to pursue the completion of the Northern Well Field, which will resolve water shortage issues caused by an unprecedented drought. The Metallurgical Enhancement Project feasibility study shows the potential to increase silver recoveries and is likely to result in a new life of mine plan.

SALOBO

Vale’s Salobo mine, the largest copper deposit in Brazil, produced a record 125,600 ounces of gold in 2015 for Silver Wheaton. With the acquisition of an additional 25% in March 2015, Silver Wheaton now receives 50% of the life of mine gold production from Salobo. Vale, furthermore, successfully ramped up Salobo II in 2015, which doubled mill throughput capacity, and is currently considering Salobo III, an additional 12Mtpa expansion. Silver Wheaton’s average attributable production forecast for the first 10 years is 140,000 ounces of gold per year.

ANTAMINA

In November 2015, Silver Wheaton acquired from Glencore Plc a silver stream tied to the Antamina mine. Antamina is one of the lowest cost copper mines globally, and it is also the eighth largest copper mine in the world. The mine is jointly owned by Glencore, BHP, Teck and Mitsubishi. The acquisition from Glencore immediately increased Silver Wheaton’s production and cash flow profile by adding expected average silver production of 5.1 million ounces per year in 2016 and 2017 and 4.7 million ounces per year over the first 20 years.

GROWTH

In 2016, based upon Silver Wheaton’s current portfolio of low-cost, long-life assets, attributable production is forecast to be approximately 54 million silver equivalent ounces, including 265,000 ounces of gold. Estimated average annual attributable production over the next five years is anticipated to be approximately 52 million silver equivalent ounces per year, including 260,000 ounces of gold.

SILVER WHEATON 2015 ANNUAL REPORT 7

PERFORMANCE

HIGHLIGHTS

| 2015 | 2014 | 2013 | |||||||

| (As of December 31 for each year) | |||||||||

| Financials | |||||||||

| Revenue ($000’s) | $ | 648,687 | $ | 620,176 | $ | 706,472 | |||

| Net (loss) earnings ($000’s) | $ | (162,042) | $ | 199,826 | $ | 375,495 | |||

| Adjusted net earnings1($000’s) | $ | 210,357 | $ | 267,977 | $ | 375,495 | |||

| Operating cash flow ($000’s) | $ | 431,359 | $ | 431,873 | $ | 534,133 | |||

| Net (loss) earnings per share | |||||||||

| Basic | $ | (0.41) | $ | 0.56 | $ | 1.06 | |||

| Diluted | $ | (0.41) | $ | 0.56 | $ | 1.05 | |||

| Adjusted earnings1per share | |||||||||

| Basic | $ | 0.53 | $ | 0.75 | $ | 1.06 | |||

| Diluted | $ | 0.53 | $ | 0.74 | $ | 1.05 | |||

| Operating cash flow per share2 | $ | 1.09 | $ | 1.20 | $ | 1.50 | |||

| Dividends paid ($000’s) | $ | 80,809 | $ | 93,400 | $ | 160,013 | |||

| Dividends paid per share | $ | 0.20 | $ | 0.26 | $ | 0.45 | |||

| Cash and cash equivalents ($000’s) | $ | 103,297 | $ | 308,098 | $ | 95,823 | |||

| Weighted average basic number of shares outstanding (000’s) | 395,755 | 359,401 | 355,588 | ||||||

| Share price (NYSE) | $ | 12.42 | $ | 20.33 | $ | 20.19 | |||

| Operating | |||||||||

| Attributable silver ounces produced (000’s) | 30,717 | 25,674 | 26,754 | ||||||

| Attributable gold ounces produced | 228,764 | 144,395 | 151,204 | ||||||

| Attributable silver equivalent ounces produced (000’s)3 | 47,697 | 35,400 | 35,832 | ||||||

| Silver ounces sold (000’s) | 26,566 | 23,484 | 22,823 | ||||||

| Gold ounces sold | 202,349 | 139,522 | 117,319 | ||||||

| Silver equivalent ounces sold (000’s)3 | 41,574 | 32,891 | 29,963 | ||||||

| Average realized silver price per ounce sold | $ | 15.64 | $ | 18.92 | $ | 23.86 | |||

| Average realized gold price per ounce sold | $ | 1,152 | $ | 1,261 | $ | 1,380 | |||

| Average silver cash cost per ounce sold4 | $ | 4.17 | $ | 4.14 | $ | 4.12 | |||

| Average gold cash cost per ounce sold4 | $ | 393 | $ | 386 | $ | 386 |

| 1 | Refer to discussion on non-IFRS measure (i) on page 42 of the MD&A. |

| 2 | Refer to discussion on non-IFRS measure (ii) on page 43 of the MD&A. |

| 3 | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during theperiod from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. |

| 4 | Refer to discussion on non-IFRS measure (iii) on page 44 of the MD&A. |

8

PRECIOUS METALS

STREAMING

SILVER WHEATON CREATED PRECIOUS METALS STREAMING IN ORDER TO UNLOCK HIDDEN VALUE BY ACQUIRING BY-PRODUCT PRECIOUS METAL FROM HIGH-QUALITY, LOW-COST MINES, WITH A GOAL OF PROVIDING INVESTORS SUPERIOR RETURNS AND SOME OF THE HIGHEST MARGINS IN THE INDUSTRY.

PRECIOUS METAL STREAMING – UNLOCKING VALUE

Silver Wheaton introduced the streaming model in 2004 after recognizing that silver produced as a by-product was not being fully valued by the financial markets. Streaming was created to unlock this value, both for Silver Wheaton’s shareholders and for Silver Wheaton’s partner mine owners. Since its introduction, the streaming model has also been applied to gold and other precious metals.

Streaming allows Silver Wheaton to purchase, in exchange for an upfront payment, a fixed percentage of the precious metals produced from a mine. Once an agreement is entered into, Silver Wheaton has the right to purchase the precious metal at a predetermined price as it is delivered. The production payment is set at a level intended to offset Silver Wheaton’s partners’ typical cost to produce an ounce of silver or gold.

Silver Wheaton does not own or operate mines and is therefore not exposed to rising capital and operating costs. However, the company’s agreements are typically for the life of the operation, giving Silver Wheaton exposure to the mine’s future expansions and exploration success.

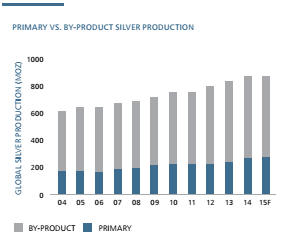

Silver remains a core focus of streaming, as 70% of worldwide silver is produced as a by-product and is therefore generally considered to be a non-core asset at the mine where it is produced. In many large base metal operations, gold production represents only a small fraction of the overall economics of the mine and it is therefore also considered non-core. While Silver Wheaton believes streaming creates the most value when targeting byproduct precious metals, given its value-enhancement and flexibility, the streaming model has also proven successful with primary metal production.

Benefits to Silver Wheaton’s Shareholders:

The key benefit of streaming to Silver Wheaton’s shareholders is cost certainty, which translates into direct leverage to increases in precious metal prices. Inflationary cost pressures have historically plagued the mining industry, driving capital and operating costs higher for traditional miners and cutting into their profit margins. Once Silver Wheaton makes the upfront payment, the company typically has no ongoing capital or exploration costs. Furthermore, Silver Wheaton’s operating costs are set at the time a stream is entered into at a predetermined production payment, allowing us to consistently deliver amongst the highest cash operating margins in the mining industry.

Benefits to Partner Mining Company’s Shareholders:

At Silver Wheaton, our goal is first and foremost to generate superior returns for our shareholders; however, we recognize that the sustainability of our model is dependent on uncovering value for all of the parties involved in a streaming agreement. Silver Wheaton is able to do this by unlocking the value of silver and gold produced as a by-product. By entering into a streaming agreement, mining companies can receive greater value for their precious metals than what is reflected in the market. These companies can use the upfront payment to continue growing their core business, either through exploration, production expansions or acquisitions, or, alternatively, the proceeds can be used to strengthen their balance sheet.

| ||

| Source: Thomson Reuters GFMS | ||

| Thomson Reuters GFMS estimates that 68% of 2015 global silver production was produced as a by-product of copper, lead, zinc or gold mines. This equates to almost 600Moz of silver, which represents a very large potential target market for Silver Wheaton to continue adding to its portfolio of silver stream assets. |

SILVER WHEATON 2015 ANNUAL REPORT 9

CORPORATE SOCIAL

RESPONSIBILITY

SILVER WHEATON HAS PRECIOUS METALS STREAMS WITH MINES LOCATED IN CANADA AND AROUND THE WORLD. AS THE COMPANY HAS GROWN, OUR FOCUS ON HELPING OTHERS HAS ALSO GROWN. LAST YEAR WE HAD THE GOOD FORTUNE TO ONCE AGAIN SUPPORT A NUMBER OF WORTHY PROJECTS IN CANADA AND BEYOND.

Since 2014, we have been investing directly into the communities from where we receive our precious metals. In 2015, we once again provided financial support for our partners’ social projects in mining communities located near our partners’ mines. We are proud to be the leader in the streaming and royalty space with this initiative, and hope that we inspire others to follow suit.

We began this program by supporting projects led by Primero, to build new community facilities near the San Dimas mine in Mexico, and by Barrick, to implement irrigation systems near the Veladero mine and Pascua-Lama project in Argentina. These projects were successfully completed in 2015 as planned.

We are now helping Barrick to expand their highly successful irrigation project in Argentina. We are also providing financial support to Goldcorp to improve educational facilities and increase student learning opportunities at a vocational college near the Peñasquito mine in Mexico. Furthermore, we are assisting Vale in their efforts to promote healthy practices and to improve the type and quality of medical services provided in the community near the Salobo mine in Brazil.

We believe these projects will have positive, long-term and sustainable benefits to the mining communities in Argentina, Brazil and Mexico. We are proud of our mining partnerships, and are committed to supporting new projects with existing and future mining partners.

10

| FINANCIALS | ||

| MANAGEMENT'S DISCUSSION AND ANALYSIS | 13 | |

| FINANCIAL STATEMENTS | 76 |

| · | Record attributable silver equivalent production for the three months and year ended December 31, 2015 of 15.5 million ounces (10.3 million ounces of silver and 69,200 ounces of gold) and 47.7 million ounces (30.7 million ounces of silver and 228,800 ounces of gold), respectively, representing an increase of 70% and 35% over the comparable periods in 2014. |

| · | Record silver equivalent sales volume for the three months and year ended December 31, 2015 of 13.6 million ounces (8.8 million ounces of silver and 64,900 ounces of gold) and 41.6 million ounces (26.6 million ounces of silver and 202,300 ounces of gold), respectively, representing an increase of 59% and 26% over the comparable periods in 2014. |

| · | As at December 31, 2015, approximately 6.9 million payable silver equivalent ounces attributable to the Company have been produced at the various mines and will be recognized in future sales as they are delivered to the Company under the terms of their contracts. This represents an increase of 0.5 million payable silver equivalent ounces during the three month period ended December 31, 2015. Payable ounces produced but not yet delivered to Silver Wheaton are expected to average approximately 2 to 3 months of annualized production but may vary from quarter to quarter due to a number of factors including mine ramp-up, delays in shipments, etc.1 |

| · | Average realized sale price per silver equivalent ounce sold for the three months and year ended December 31, 2015 of $14.73 ($14.75 per ounce of silver and $1,100 per ounce of gold) and $15.60 ($15.64 per ounce of silver and $1,152 per ounce of gold), compared with $16.43 and $18.86 for the comparable periods in 2014, representing a decrease of 10% and 17%, respectively. |

| · | Revenue for the three months and year ended December 31, 2015 of $200.5 million and $648.7 million, respectively, compared with $140.4 million and $620.2 million for the comparable periods in 2014, representing an increase of 43% and 5%, respectively. |

| · | Net loss for the three months and year ended December 31, 2015 was $169.3 million ($0.42 per share) and $162.0 million ($0.41 per share), respectively, compared with net earnings of $52.0 million ($0.14 per share) and $199.8 million ($0.56 per share) for the comparable periods in 2014. |

| · | During the three months and year ended December 31, 2015, the Company recognized impairment charges of $230.9 million and $384.9 million, respectively. |

| · | After removing the after tax impact of the impairment charge, adjusted net earnings² for the three months and year ended December 31, 2015 of $57.4 million ($0.14 per share) and $210.4 million ($0.53 per share), respectively, compared with adjusted net earnings² of $52.0 million ($0.14 per share) and $268.0 million ($0.75 per share) for the comparable periods in 2014, representing an increase of 10% during the three month period and a decrease of 22% during the twelve month period as compared to the comparable periods in 2014. |

| · | Operating cash flows for the three months and year ended December 31, 2015 of $133.4 million ($0.33 per share¹) and $431.4 million ($1.09 per share¹), respectively, compared with $94.1 million ($0.26 per share¹) and $431.9 million ($1.20 per share¹) for the comparable periods in 2014, representing an increase of 42% during the quarter while the annual cashflow was virtually unchanged as compared to the prior year.1 |

| · | On March 16, 2016, the Board of Directors declared a dividend in the amount of $0.05 per common share as per the Company's stated dividend policy whereby the quarterly dividend will be equal to 20% of the average of the operating cash flow of the previous four quarters. This dividend is payable to shareholders of record on March 31, 2016 and is expected to be distributed on or about April 14, 2016. The Company has implemented a dividend reinvestment plan ("DRIP") whereby shareholders can elect to have dividends reinvested directly into additional Silver Wheaton common shares at a discount of 3% of the Average Market Price, as defined in the DRIP. |

| · | Average cash costs² for the three months and year ended December 31, 2015 of $4.50 and $4.58 per silver equivalent ounce, respectively.2 |

| · | Cash operating margin³ for the three months and year ended December 31, 2015 of $10.23 and $11.02 per silver equivalent ounce, respectively, representing a decrease of 14% and 23% relative to the comparable periods in 2014. |

| · | On March 2, 2015, the Company announced that it had agreed to amend its agreement with Vale S.A ("Vale") to acquire an additional amount of gold equal to 25% of the life of mine gold production from any minerals from the Salobo mine that enter the Salobo mineral processing facility from and after January 1, 2015. This acquisition is in addition to the 25% of the Salobo mine gold production that the Company acquired pursuant to its agreement in 2013. |

| · | On April 22, 2015, the Company amended its early deposit precious metal purchase agreement with Sandspring Resources Ltd. ("Sandspring") to include the acquisition of an amount equal to 50% of the silver production from its Toroparu project located in the Republic of Guyana, South America. |

| · | On November 3, 2015, the Company announced that it had agreed to acquire from a subsidiary of Glencore plc ("Glencore") an amount of silver equal to 33.75% of the Antamina silver production until the delivery of 140 million ounces of silver and 22.5% of silver production thereafter for the life of mine at a fixed 100% payable rate for a total upfront cash payment of $900 million. In addition, Silver Wheaton will make ongoing payments of 20% of spot price per silver ounce delivered under the agreement. |

| · | On January 27, 2016, the Company announced that it had signed a nonbinding term sheet with Panoro Minerals Ltd. ("Panoro") to enter into an Early Deposit Precious Metal Purchase Agreement for the Cotabambas project located in Peru. |

| · | On July 6, 2015, the Company announced that it had received a proposal letter (the "Proposal") from the Canada Revenue Agency ("CRA") in which the CRA was proposing to reassess Silver Wheaton under the transfer pricing provisions contained in the Income Tax Act (Canada) (the "Act"). Subsequent to the issuance of the Proposal, on September 24, 2015, the Company announced that it had received Notices of Reassessment (the "Reassessments") from the CRA for the 2005-2010 taxation years. The Reassessments are consistent with the Proposal and seek to increase the Company's income subject to tax in Canada for the 2005-2010 taxation years by approximately Cdn$715.3 million which would result in federal and provincial taxes of approximately Cdn$201.3 million. In addition, the CRA is seeking to impose transfer pricing penalties of approximately Cdn$71.5 million and interest and other penalties of Cdn$80.6 million (calculated to September 24, 2015) for the 2005-2010 taxation years. Total tax, interest and penalties sought by the CRA for the 2005-2010 taxation years is Cdn$353.4 million. Management believes that the Company has filed its tax returns and paid applicable taxes in compliance with Canadian tax law, and as a result, no amounts have been recorded for any potential liability arising from this matter. Silver Wheaton intends to vigorously defend its tax filing positions. |

| · | On October 8, 2015, Silver Wheaton filed a notice of objection for each of the 2005-2010 taxation years. Silver Wheaton is required to make a deposit of 50% of the reassessed amounts of tax, interest and penalties. On March 1, 2016, Silver Wheaton received approval from the CRA to post security in the form of a letter of guarantee as opposed to a cash deposit. The letter of guarantee is to be in the amount of Cdn$191.7 million which includes interest accrued to-date plus estimated interest for the following year. |

| · | On January 8, 2016, Silver Wheaton filed a Notice of Appeal with the Tax Court of Canada, electing to pursue resolution of the matters relating to the Reassessments for the 2005-2010 taxation years through a judicial court process rather than continue to pursue the CRA's internal appeals process. On January 19, 2016, Silver Wheaton received correspondence advising that the CRA would be commencing an audit of the Company's international transactions covering the 2011-2013 taxation years. This correspondence is not a proposal or notice of reassessment and the Company is not in a position to determine what, if any, position the CRA will take in respect of the 2011-2013 taxation years. Taxation years subsequent to 2013 also remain open to audit by the CRA. |

| · | On January 5, 2015, the Company announced that it had amended its silver purchase agreement related to Barrick Gold Corporation's ("Barrick") Pascua-Lama project ("Pascua-Lama"). The amendment entails Silver Wheaton being entitled to 100% of the silver production from Barrick's Lagunas Norte, Pierina and Veladero mines until March 31, 2018 - an extension of 1 ¼ years, and extending the completion test deadline an additional 2 ½ years to June 30, 2020. As a reminder, if the requirements of the completion test have not been satisfied by the amended completion date, the agreement may be terminated by Silver Wheaton. In such an event, Silver Wheaton will be entitled to the return of the upfront cash consideration of $625 million less a credit for any silver delivered up to that date. |

| · | On February 27, 2015, the Company announced that it had amended its $1 billion revolving credit facility (the "Revolving Facility") by increasing the available credit from $1 billion to $2 billion and extending the term by 2 years. The Company used proceeds drawn from this amended Revolving Facility together with cash on hand to repay the non-revolving term loan. |

| · | On March 2, 2015, the Company announced that, in connection with the amended Salobo precious metal purchase agreement, it had entered into an agreement with a syndicate of underwriters led by Scotiabank, pursuant to which they agreed to purchase, on a bought deal basis, 38,930,000 common shares of Silver Wheaton at a price of $20.55 per share (the "Offering"), for aggregate gross proceeds to Silver Wheaton of approximately $800 million. |

| · | On March 17, 2015, the Company announced that it had closed the Offering and received $800 million in gross proceeds (net proceeds of approximately $769 million after payment of underwriters' fees and expenses). |

| · | On September 18, 2015, the Company announced that it had received approval from the Toronto Stock Exchange ("TSX") to purchase up to 20,229,671 common shares (representing 5% of the Company's 404,593,425 total issued and outstanding common shares as of September 11, 2015) over a period of twelve months commencing on September 23, 2015. The normal course issuer bid ("NCIB") will expire no later than September 22, 2016. To date, the Company has repurchased 2,887,854 common shares under the NCIB at an average price of $13.58 per share, including 2,123,065 purchased subsequent to December 31, 2015. On January 27, 2016, Silver Wheaton announced that it had entered into an automatic securities purchase plan (the "Plan") with a broker in order to facilitate repurchases of its Common Shares under the NCIB. Purchases under the Plan will be made by Silver Wheaton's broker based on the parameters prescribed by the TSX and the NYSE, applicable Canadian securities laws and the terms of the parties' written agreement. Under the Plan, the broker may purchase Common Shares under the NCIB when Silver Wheaton would ordinarily not be permitted. The Plan commences on January 27, 2016 and expires on September 22, 2016, and has been approved by the TSX. |

| · | On March 15, 2016, the Company was notified that its lenders had agreed to extend the term of the Revolving Facility by an additional year, with the facility now maturing on February 27, 2021. |

Silver and Gold Interests | Mine Owner | Location of Mine | Upfront Consideration 1 | Attributable Production to be Purchased | Term of Agreement | Date of Original Contract | |

| Silver | Gold | ||||||

| San Dimas | Primero | Mexico | $ 189,799 | 100% 2 | 0% | Life of Mine | 15-Oct-04 |

| Yauliyacu | Glencore | Peru | $ 285,000 | variable 3 | 0% | Life of Mine 3 | 23-Mar-06 |

| Peñasquito | Goldcorp | Mexico | $ 485,000 | 25% | 0% | Life of Mine | 24-Jul-07 |

| Salobo | Vale | Brazil | $ 2,230,000 4 | 0% | 50% | Life of Mine | 28-Feb-13 |

| Sudbury | $ 623,572 5 | ||||||

| Coleman | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Copper Cliff | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Garson | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Stobie | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Creighton | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Totten | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Victor | Vale | Canada | 0% | 70% | 20 years | 28-Feb-13 | |

| Barrick | $ 625,000 | ||||||

| Pascua-Lama | Barrick | Chile/Argentina | 25% | 0% | Life of Mine | 8-Sep-09 | |

| Lagunas Norte | Barrick | Peru | 100% | 0% | 8.5 years | 8-Sep-09 | |

| Pierina | Barrick | Peru | 100% | 0% | 8.5 years 6 | 8-Sep-09 | |

| Veladero | Barrick | Argentina | 100% 7 | 0% | 8.5 years | 8-Sep-09 | |

| Antamina | Glencore | Peru | $ 900,000 | 33.75% 8 | 0% | Life of Mine | 3-Nov-15 |

| Other | $ 1,482,683 | ||||||

| Los Filos | Goldcorp | Mexico | $ 4,463 | 100% | 0% | 25 years | 15-Oct-04 |

| Zinkgruvan | Lundin | Sweden | $ 77,866 | 100% | 0% | Life of Mine | 8-Dec-04 |

| Stratoni | Eldorado Gold 9 | Greece | $ 57,500 | 100% | 0% | Life of Mine | 23-Apr-07 |

| Minto | Capstone | Canada | $ 54,805 | 100% | 100% 10 | Life of Mine | 20-Nov-08 |

| Cozamin | Capstone | Mexico | $ 41,959 | 100% | 0% | 10 years | 4-Apr-07 |

| Neves-Corvo | Lundin | Portugal | $ 35,350 | 100% | 0% | 50 years | 5-Jun-07 |

| Aljustrel | I'M SGPS | Portugal | $ 2,451 | 100% 11 | 0% | 50 years | 5-Jun-07 |

| Keno Hill | Alexco | Canada | $ 50,000 | 25% | 0% | Life of Mine | 2-Oct-08 |

| Rosemont | Hudbay | United States | $ 230,000 12 | 100% | 100% | Life of Mine | 10-Feb-10 |

| Loma de La Plata | Pan American | Argentina | $ 43,289 13 | 12.5% | 0% | Life of Mine | n/a 14 |

| 777 | Hudbay | Canada | $ 455,100 | 100% | 100%/50% 15 | Life of Mine | 8-Aug-12 |

| Constancia | Hudbay | Peru | $ 429,900 | 100% | 50% 16 | Life of Mine | 8-Aug-12 |

| Early Deposit | |||||||

| Toroparu | Sandspring | Guyana | $ 153,500 17 | 50% 17 | 10% 17 | Life of Mine | 11-Nov-13 |

| Cotabambas | Panoro | Peru | $ 140,000 18 | 100% 19 | 25% 19 | Life of Mine | n/a 20 |

| 1) | Expressed in United States dollars, rounded to the nearest thousand; excludes closing costs and capitalized interest, where applicable. |

| 2) | Until August 6, 2014, Primero delivered to Silver Wheaton a per annum amount equal to the first 3.5 million ounces of payable silver produced at San Dimas and 50% of any excess, plus Silver Wheaton received an additional 1.5 million ounces of silver per annum which was delivered by Goldcorp. Beginning August 6, 2014, Primero will deliver a per annum amount to Silver Wheaton equal to the first 6 million ounces of payable silver produced at San Dimas and 50% of any excess. |

| 3) | On November 30, 2015, the Company amended its silver purchase agreement with Glencore. The term of the agreement, which was set to expire in 2026, was extended to the life of mine. Glencore will deliver a per annum amount to Silver Wheaton equal to the first 1.5 million ounces of payable silver produced at Yauliyacu and 50% of any excess. |

| 4) | Does not include the contingent payment related to the Salobo mine expansion. Vale has completed the expansion of the mill throughput capacity at the Salobo mine to 24 million tonnes per annum ("Mtpa") from its previous 12 Mtpa. If actual throughput is expanded above 28 Mtpa within a predetermined period, Silver Wheaton will be required to make an additional payment to Vale based on a set fee schedule ranging from $88 million if throughput is expanded beyond 28 Mtpa by January 1, 2036, up to $720 million if throughput is expanded beyond 40 Mtpa by January 1, 2018. |

| 5) | Comprised of a $570 million upfront cash payment plus warrants to purchase 10 million common shares of Silver Wheaton at a strike price of $65, with a term of 10 years. |

| 6) | As per Barrick's disclosure, closure activities were initiated at Pierina in August 2013. |

| 7) | Silver Wheaton's attributable silver production is subject to a maximum of 8% of the silver contained in the ore processed at Veladero during the period. |

| 8) | Once the Company has received 140 million ounces of silver under the Antamina agreement, the Company's attributable silver production to be purchased will be reduced to 22.5%. |

| 9) | 95% owned by Eldorado Gold Corporation. |

| 10) | The Company is entitled to acquire 100% of the first 30,000 ounces of gold produced per annum and 50% thereafter. |

| 11) | Silver Wheaton only has the rights to silver contained in concentrate containing less than 15% copper at the Aljustrel mine. |

| 12) | The upfront consideration is currently reflected as a contingent obligation, payable on an installment basis to partially fund construction of the Rosemont mine once certain milestones are achieved, including the receipt of key permits and securing the necessary financing to complete construction of the mine. |

| 13) | Comprised of $10.9 million allocated to the silver interest upon the Company's acquisition of Silverstone Resources Corp. in addition to a contingent liability of $32.4 million, payable upon the satisfaction of certain conditions, including Pan American receiving all necessary permits to proceed with the mine construction. |

| 14) | Definitive terms of the agreement to be finalized. |

| 15) | Silver Wheaton is entitled to acquire 100% of the life of mine gold production from Hudbay's 777 mine until Hudbay's Constancia mine satisfies a completion test, or the end of 2016, whichever is later. At that point, Silver Wheaton's share of gold production from 777 will be reduced to 50% for the life of the mine. |

| 16) | Gold recoveries will be set at 55% for the Constancia deposit and 70% for the Pampacancha deposit until 265,000 ounces of gold have been delivered to the Company. |

| 17) | Comprised of $15.5 million paid to date and $138.0 million to be payable on an installment basis to partially fund construction of the mine. During the 60 day period following the delivery of a feasibility study, environmental study and impact assessment, and other related documents (collectively, the "Toroparu Feasibility Documentation"), or after December 31, 2016 if the Toroparu Feasibility Documentation has not been delivered to Silver Wheaton by such date, Silver Wheaton may elect not to proceed with the precious metal purchase agreement, at which time Silver Wheaton will be entitled to a return of the amounts advanced less $2 million which is non-refundable or, at Sandspring's option, the gold stream percentage will be reduced from 10% to 0.909% and the silver stream percentage will be reduced from 50% to nil. Silver Wheaton may also elect to terminate the Toroparu Early Deposit Agreement upon the occurrence of certain events prior to the payment of any initial construction payment and elect to reduce the stream percentages or obtain a return of the amounts advanced less $2 million. |

| 18) | The upfront consideration is currently reflected as a contingent obligation. Once certain conditions have been met, Silver Wheaton will advance $14 million to Panoro, spread over up to nine years. Following the delivery of certain feasibility documentation, Silver Wheaton may elect to terminate the Cotabambas Early Deposit Agreement. If Silver Wheaton elects to terminate, Silver Wheaton will be entitled to a return of the portion of the $14 million paid less $2 million payable upon certain triggering events occurring. Until January 1, 2020, Panoro has a one-time option to repurchase 50% of the precious metals stream on a change of control for an amount based on a calculated rate of return for Silver Wheaton. |

| 19) | Once 90 million silver equivalent ounces attributable to Silver Wheaton have been produced, the attributable production to be purchased will decrease to 66.67% of silver production and 16.67% of gold production for the life of mine. |

| 20) | The entering into of the Cotabambas Early Deposit Agreement is subject to the negotiation and completion of definitive documentation. There can be no assurance that the Cotabambas Early Deposit Agreement will be completed on the terms set out in the non-binding term sheet, or at all. |

| i. | Pascua-Lama SMA Regulatory Sanctions |

| ii. | Pascua-Lama Constitutional Protection Action |

| iii. | Pascua-Lama Chilean Environmental Court Ruling |

| iv. | Argentine Glacier Legislation |

| i. | As part of the agreement with Goldcorp to acquire silver from the Luismin mining operations, on October 15, 2004, the Company entered into an agreement with Goldcorp to acquire 100% of the silver production from its Los Filos mine in Mexico for a period of 25 years, commencing October 15, 2004. In addition, pursuant to Goldcorp's sale of the San Dimas mine, Goldcorp delivered to Silver Wheaton 1.5 million ounces of silver per year until August 6, 2014, which is reflected in this MD&A and financial statements as part of the silver production and sales relating to San Dimas; |

| ii. | On December 8, 2004, the Company entered into an agreement with Lundin Mining Corporation ("Lundin") to acquire 100% of the silver produced by Lundin's Zinkgruvan mining operations in Sweden for the life of mine; |

| iii. | On April 23, 2007, the Company entered into an agreement with European Goldfields Limited (which was acquired by Eldorado Gold Corporation ("Eldorado Gold") on February 24, 2012), to acquire 100% of the life of mine silver production from its 95% owned Stratoni mine in Greece (see additional discussion below); |

| iv. | On October 2, 2008, the Company entered into an agreement with Alexco Resource Corp. ("Alexco") to acquire an amount equal to 25% of the life of mine silver production from its Keno Hill silver district in Canada, including the Bellekeno mine (see additional discussion below); |

| v. | On May 21, 2009, the Company completed the acquisition of Silverstone Resources Corp. (the "Silverstone Acquisition"). As part of the Silverstone Acquisition, the Company acquired a precious metal purchase agreement with Capstone Mining Corp. ("Capstone") to acquire 100% of the silver and gold produced (subject to certain thresholds) from Capstone's Minto mine in Canada for the life of mine. The Company is entitled to acquire 100% of all the silver produced and 100% of the first 30,000 ounces of gold produced per annum and 50% thereafter; |

| vi. | As part of the Silverstone Acquisition, the Company acquired a silver purchase agreement with Capstone to acquire 100% of the silver produced from Capstone's Cozamin mine in Mexico for a period of 10 years, commencing on April 4, 2007; |

| vii. | As part of the Silverstone Acquisition, the Company acquired an agreement with Lundin to acquire 100% of the silver production from its Neves-Corvo mine in Portugal for a period of 50 years, commencing June 5, 2007; |

| viii. | As part of the Silverstone Acquisition, the Company acquired an agreement with I'M SGPS to acquire 100% of the silver production from its Aljustrel mine in Portugal for a period of 50 years, commencing June 5, 2007. As part of an agreement with I'M SGPS dated July 16, 2014, Silver Wheaton agreed to limit its rights to only silver contained in concentrates containing less than 15% copper; |

| ix. | As part of the Silverstone Acquisition, the Company acquired an agreement with Aquiline Resources Inc., which was acquired by Pan American Silver Corp. ("Pan American") on December 22, 2009, to acquire an amount equal to 12.5% of the life of mine silver production from the Loma de La Plata zone of the Navidad project in Argentina, the definitive terms of which are to be finalized. The Company is committed to pay Pan American total upfront cash payments of $32.4 million following the satisfaction of certain conditions, including Pan American receiving all necessary permits to proceed with the mine construction; |

| x. | On February 10, 2010, the Company entered into an agreement with Augusta Resource Corporation, which was acquired by Hudbay on July 16, 2014, to acquire an amount equal to 100% of the life of mine silver and gold production from the Rosemont Copper project ("Rosemont") in the United States. The Company is committed to pay Hudbay total upfront cash payments of $230 million, payable on an installment basis to partially fund construction of the Rosemont mine once certain milestones are achieved, including the receipt of key permits and securing the necessary financing to complete construction of the mine; and |

| xi. | On August 8, 2012, the Company entered into an agreement with Hudbay to acquire an amount equal to 100% of the life of mine silver and gold production from its 777 mine, located in Canada. Silver Wheaton's share of gold production at 777 will remain at 100% until the later of the end of 2016 or the satisfaction of a completion test relating to Hudbay's Constancia mine (see Other silver and gold interest xii, below), after which it will be reduced to 50% for the remainder of the mine life. |

| xii. | On August 8, 2012, the Company entered into an agreement with Hudbay to acquire an amount equal to 100% of the life of mine silver production from the Constancia mine ("Constancia") in Peru. On November 4, 2013, the Company amended its agreement with Hudbay to include the acquisition of an amount equal to 50%1 of the life of mine gold production from Constancia. If the Constancia processing plant fails to achieve at least 90% of expected throughput and silver recovery by December 31, 2016, Silver Wheaton would be entitled to continued delivery of 100% of the gold production from Hudbay's 777 mine. If the completion test has not been satisfied by December 31, 2020, Silver Wheaton would be entitled to a proportionate return of the upfront cash consideration relating to Constancia. In addition, Silver Wheaton would be entitled to additional compensation in respect of the gold stream should there be a delay in achieving completion or mining the Pampacancha deposit beyond the end of 2018. Hudbay has granted Silver Wheaton a right of first refusal on any future streaming agreement, royalty agreement, or similar transaction related to the production of silver or gold from Constancia. |

| Dec 31, 2015 | Three Months Ended Dec 31, 2015 | Year Ended Dec 31, 2015 | Year Ended Dec 31, 2015 | |

| (in thousands) | Fair Value | Fair Value Adjustment Gains (Losses) Included in OCI | Realized Loss on Disposal | |

Bear Creek | $ 5,558 | $ (1,572) | $ (10,678) | $ - |

| Revett | - | - | (1,401) | (11,870) |

| Other | 14,218 | 3,793 | (1,006) | (2,781) |

Total common shares held | $ 19,776 | $ 2,221 | $ (13,085) | $ (14,651) |

| Dec 31, 2014 | Three Months Ended Dec 31, 2014 | Year Ended Dec 31, 2014 | |

| (in thousands) | Fair Value | Fair Value Adjustment Gains (Losses) Included in OCI | |

Bear Creek | $ 16,236 | $ (5,658) | $ (1,972) |

| Revett | 3,873 | (2,022) | 47 |

| Other | 12,763 | (3,469) | (6,004) |

Total common shares held | $ 32,872 | $ (11,149) | $ (7,929) |

2015 | 2014 | 2013 | ||||

Silver equivalent production 1 | ||||||

| Attributable silver ounces produced (000's) | 30,717 | 25,674 | 26,754 | |||

| Attributable gold ounces produced | 228,764 | 144,395 | 151,204 | |||

Attributable silver equivalent ounces produced (000's) 1 | 47,697 | 35,400 | 35,832 | |||

Silver equivalent sales 1 | ||||||

| Silver ounces sold (000's) | 26,566 | 23,484 | 22,823 | |||

| Gold ounces sold | 202,349 | 139,522 | 117,319 | |||

Silver equivalent ounces sold (000's) 1 | 41,574 | 32,891 | 29,963 | |||

| Average realized price ($'s per ounce) | ||||||

| Average realized silver price | $ | 15.64 | $ | 18.92 | $ | 23.86 |

| Average realized gold price | $ | 1,152 | $ | 1,261 | $ | 1,380 |

Average realized silver equivalent price 1 | $ | 15.60 | $ | 18.86 | $ | 23.58 |

Average cash cost ($'s per ounce) 2 | ||||||

| Average silver cash cost | $ | 4.17 | $ | 4.14 | $ | 4.12 |

| Average gold cash cost | $ | 393 | $ | 386 | $ | 386 |

Average silver equivalent cash cost 1 | $ | 4.58 | $ | 4.59 | $ | 4.65 |

Total revenue ($000's) | $ | 648,687 | $ | 620,176 | $ | 706,472 |

Net (loss) earnings ($000's) | $ | (162,042) | $ | 199,826 | $ | 375,495 |

| Add back - impairment loss, net of tax | 372,399 | 68,151 | - | |||

Adjusted net earnings 3 ($000's) | $ | 210,357 | $ | 267,977 | $ | 375,495 |

| (Loss) earnings per share | ||||||

| Basic | $ | (0.41) | $ | 0.56 | $ | 1.06 |

| Diluted | $ | (0.41) | $ | 0.56 | $ | 1.05 |

Adjusted earnings per share 3 | ||||||

| Basic | $ | 0.53 | $ | 0.75 | $ | 1.06 |

| Diluted | $ | 0.53 | $ | 0.74 | $ | 1.05 |

Cash flow from operations ($000's) | $ | 431,359 | $ | 431,873 | $ | 534,133 |

| Dividends | ||||||

| Dividends paid ($000's) | $ | 80,809⁴ | $ | 93,400⁴ | $ | 160,013 |

| Dividends paid per share | $ | 0.20 | $ | 0.26 | $ | 0.45 |

Total assets ($000's) | $ | 5,632,211 | $ | 4,647,763 | $ | 4,389,844 |

Total non-current financial liabilities ($000's) | $ | 1,468,732 | $ | 1,001,914 | $ | 999,973 |

Total other liabilities ($000's) | $ | 12,744 | $ | 17,113 | $ | 23,325 |

Shareholders' equity ($000's) | $ | 4,150,735 | $ | 3,628,736 | $ | 3,366,546 |

Shares outstanding | 404,039,065 | 364,777,928 | 357,396,778 |

| 1) | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during the period from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. |

| 2) | Refer to discussion on non-IFRS measure (iii) on page 44 of this MD&A. |

| 3) | Refer to discussion on non-IFRS measure (i) on page 42 of this MD&A. |

| 4) | During the year ended December 31, 2015, the Company declared and paid dividends to its shareholders in the amount of $0.20 per common share for total dividends of $80.8 million, with the payment being comprised of $68.6 million in cash and $12.2 million in common shares issued, with the Company issuing 847,064 common shares under the Company's dividend reinvestment plan. For the comparable period in 2014, the Company declared and paid dividends to its shareholders in the amount of $0.26 per common share for total dividends of $93.4 million, with the payment being comprised of $79.8 million in cash and $13.6 million in common shares issued, with the Company issuing 646,618 common shares under the Company's dividend reinvestment plan. . |

| 2015 | 2014 | |||||||

Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | |

Silver ounces produced 2 | ||||||||

San Dimas 3 | 2,317 | 1,418 | 1,786 | 1,928 | 1,744 | 1,290 | 1,118 | 1,608 |

| Yauliyacu | 749 | 696 | 696 | 576 | 687 | 875 | 658 | 718 |

| Peñasquito | 1,766 | 2,092 | 1,932 | 1,447 | 1,582 | 1,630 | 2,054 | 2,052 |

| Antamina | 2,403 | - | - | - | - | - | - | - |

Barrick 4 | 627 | 506 | 610 | 640 | 690 | 397 | 299 | 301 |

Other 5 | 2,422 | 2,178 | 2,177 | 1,751 | 1,701 | 1,903 | 2,182 | 2,185 |

| Total silver ounces produced | 10,284 | 6,890 | 7,201 | 6,342 | 6,404 | 6,095 | 6,311 | 6,864 |

Gold ounces produced 2 | ||||||||

Sudbury 6 | 12,203 | 7,300 | 8,195 | 8,666 | 9,924 | 12,196 | 7,473 | 6,426 |

| Salobo | 37,680 | 32,954 | 27,805 | 27,185 | 12,253 | 10,415 | 8,486 | 8,903 |

Other 7 | 19,293 | 15,592 | 14,082 | 17,809 | 13,925 | 19,064 | 16,796 | 18,534 |

| Total gold ounces produced | 69,176 | 55,846 | 50,082 | 53,660 | 36,102 | 41,675 | 32,755 | 33,863 |

Silver equivalent ounces of gold produced 8 | 5,179 | 4,203 | 3,672 | 3,926 | 2,675 | 2,786 | 2,144 | 2,121 |

Silver equivalent ounces produced 8 | 15,463 | 11,093 | 10,873 | 10,268 | 9,079 | 8,881 | 8,455 | 8,985 |

Silver equivalent ounces produced - as originally reported 2, 8 | n.a. | 10,993 | 10,904 | 10,371 | 8,964 | 8,447 | 8,365 | 8,977 |

Increase (Decrease) 2 | n.a. | 100 | (31) | (103) | 115 | 434 | 90 | 8 |

| Silver ounces sold | ||||||||

San Dimas 3 | 2,097 | 2,014 | 1,265 | 1,901 | 1,555 | 1,295 | 1,194 | 1,529 |

| Yauliyacu | 987 | 428 | 809 | 320 | 761 | 1,373 | 111 | 1,097 |

| Peñasquito | 2,086 | 2,053 | 1,420 | 1,573 | 1,640 | 1,662 | 1,958 | 1,840 |

| Antamina | 1,340 | - | - | - | - | - | - | - |

Barrick 4 | 569 | 514 | 633 | 648 | 671 | 377 | 291 | 361 |

Other 5 | 1,672 | 1,566 | 1,448 | 1,223 | 1,106 | 1,592 | 1,673 | 1,398 |

| Total silver ounces sold | 8,751 | 6,575 | 5,575 | 5,665 | 5,733 | 6,299 | 5,227 | 6,225 |

| Gold ounces sold | ||||||||

Sudbury 6 | 6,256 | 6,674 | 12,518 | 8,033 | 11,251 | 5,566 | 6,718 | 6,878 |

| Salobo | 44,491 | 21,957 | 32,156 | 9,794 | 14,270 | 7,180 | 11,902 | 10,560 |

Other 7 | 14,152 | 19,446 | 16,300 | 10,572 | 12,383 | 23,972 | 16,158 | 12,684 |

| Total gold ounces sold | 64,899 | 48,077 | 60,974 | 28,399 | 37,904 | 36,718 | 34,778 | 30,122 |

Silver equivalent ounces of gold sold 8 | 4,863 | 3,619 | 4,468 | 2,058 | 2,808 | 2,441 | 2,267 | 1,891 |

Silver equivalent ounces sold8 | 13,614 | 10,194 | 10,043 | 7,723 | 8,541 | 8,740 | 7,494 | 8,116 |

Gold / silver ratio 8 | 74.9 | 75.3 | 73.3 | 72.5 | 74.1 | 66.5 | 65.2 | 62.8 |

Cumulative payable silver equivalent ounces produced but not yet delivered 9 | 6,891 | 6,380 | 6,398 | 6,445 | 4,952 | 5,147 | 5,996 | 6,042 |

| 1) | All figures in thousands except gold ounces produced and sold. |

| 2) | Ounces produced represent the quantity of silver and gold contained in concentrate or doré prior to smelting or refining deductions. Production figures are based on information provided by the operators of the mining operations to which the silver or gold interests relate or management estimates in those situations where other information is not available. Certain production figures may be updated in future periods as additional information is received. |

| 3) | The ounces produced and sold include ounces received from Goldcorp in connection with Goldcorp's four year commitment, commencing August 6, 2010, to deliver to Silver Wheaton 1.5 million ounces of silver per annum resulting from their sale of San Dimas to Primero. |

| 4) | Comprised of the Lagunas Norte, Pierina and Veladero silver interests. |

| 5) | Comprised of the Los Filos, Zinkgruvan, Keno Hill, Cozamin, Neves-Corvo, Stratoni, Minto, 777, Aljustrel and Constancia silver interests in addition to the previously owned Campo Morado and Mineral Park silver interests. |

| 6) | Comprised of the Coleman, Copper Cliff, Garson, Stobie, Creighton and Totten gold interests. |

| 7) | Comprised of the Minto, 777 and Constancia gold interests. |

| 8) | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during the period from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. |

| 9) | Payable silver equivalent ounces produced but not yet delivered are based on management estimates. These figures may be updated in future periods as additional information is received. |

| 2015 | 2014 | |||||||||||||||||||||||

Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | Q2 | Q1 | |||||||||||||||||

| Total silver ounces sold (000's) | 8,751 | 6,575 | 5,575 | 5,665 | 5,733 | 6,299 | 5,227 | 6,225 | ||||||||||||||||

Average realized silver price¹ | $ | 14.75 | $ | 15.05 | $ | 16.42 | $ | 16.95 | $ | 16.46 | $ | 18.98 | $ | 19.81 | $ | 20.36 | ||||||||

| Silver sales (000's) | $ | 129,087 | $ | 98,926 | $ | 91,552 | $ | 96,012 | $ | 94,395 | $ | 119,535 | $ | 103,540 | $ | 126,744 | ||||||||

| Total gold ounces sold | 64,899 | 48,077 | 60,974 | 28,399 | 37,904 | 36,718 | 34,778 | 30,122 | ||||||||||||||||

Average realized gold price¹ | $ | 1,100 | $ | 1,130 | $ | 1,195 | $ | 1,214 | $ | 1,213 | $ | 1,261 | $ | 1,295 | $ | 1,283 | ||||||||

| Gold sales (000's) | $ | 71,409 | $ | 54,325 | $ | 72,883 | $ | 34,492 | $ | 45,980 | $ | 46,317 | $ | 45,030 | $ | 38,635 | ||||||||

Total silver equivalent ounces sold (000's) 2 | 13,614 | 10,194 | 10,043 | 7,723 | 8,541 | 8,740 | 7,494 | 8,116 | ||||||||||||||||

Average realized silver equivalent price 1, 2 | $ | 14.73 | $ | 15.03 | $ | 16.38 | $ | 16.90 | $ | 16.43 | $ | 18.98 | $ | 19.83 | $ | 20.38 | ||||||||

| Total sales (000's) | $ | 200,496 | $ | 153,251 | $ | 164,435 | $ | 130,504 | $ | 140,375 | $ | 165,852 | $ | 148,570 | $ | 165,379 | ||||||||

Average cash cost, silver 1, 3 | $ | 4.06 | $ | 4.26 | $ | 4.26 | $ | 4.14 | $ | 4.13 | $ | 4.16 | $ | 4.15 | $ | 4.12 | ||||||||

Average cash cost, gold 1, 3 | $ | 396 | $ | 389 | $ | 395 | $ | 388 | $ | 391 | $ | 378 | $ | 393 | $ | 381 | ||||||||

Average cash cost, silver equivalent 1, 2, 3 | $ | 4.50 | $ | 4.58 | $ | 4.76 | $ | 4.46 | $ | 4.51 | $ | 4.59 | $ | 4.72 | $ | 4.57 | ||||||||

| Net (loss) earnings (000's) | $ | (169,263) | $ | (95,925) | $ | 53,726 | $ | 49,419 | $ | 52,030 | $ | 4,496 | $ | 63,492 | $ | 79,809 | ||||||||

| Add back - impairment loss (net of tax) | 226,673 | 145,726 | - | - | - | 68,151 | - | - | ||||||||||||||||

Adjusted net earnings 4 (000's) | $ | 57,410 | $ | 49,801 | $ | 53,726 | $ | 49,419 | $ | 52,030 | $ | 72,647 | $ | 63,492 | $ | 79,809 | ||||||||

| (Loss) earnings per share | ||||||||||||||||||||||||

| Basic | $ | (0.42) | $ | (0.24) | $ | 0.13 | $ | 0.13 | $ | 0.14 | $ | 0.01 | $ | 0.18 | $ | 0.22 | ||||||||

| Diluted | $ | (0.42) | $ | (0.24) | $ | 0.13 | $ | 0.13 | $ | 0.14 | $ | 0.01 | $ | 0.18 | $ | 0.22 | ||||||||

Adjusted earnings per share 4 | ||||||||||||||||||||||||

| Basic | $ | 0.14 | $ | 0.12 | $ | 0.13 | $ | 0.13 | $ | 0.14 | $ | 0.20 | $ | 0.18 | $ | 0.22 | ||||||||

| Diluted | $ | 0.14 | $ | 0.12 | $ | 0.13 | $ | 0.13 | $ | 0.14 | $ | 0.20 | $ | 0.18 | $ | 0.22 | ||||||||

| Cash flow from operations (000's) | $ | 133,389 | $ | 99,547 | $ | 109,292 | $ | 89,131 | $ | 94,120 | $ | 120,379 | $ | 102,543 | $ | 114,832 | ||||||||

Cash flow from operations per share 5 | ||||||||||||||||||||||||

| Basic | $ | 0.33 | $ | 0.25 | $ | 0.27 | $ | 0.24 | $ | 0.26 | $ | 0.34 | $ | 0.29 | $ | 0.32 | ||||||||

| Diluted | $ | 0.33 | $ | 0.25 | $ | 0.27 | $ | 0.24 | $ | 0.26 | $ | 0.34 | $ | 0.29 | $ | 0.32 | ||||||||

| Dividends | ||||||||||||||||||||||||

| Dividends declared (000's) | $ | 20,192 | $ | 20,214 | $ | 20,205 | $ | 20,198 6 | $ | 21,861 | $ | 21,484 | $ | 25,035 | $ | 25,020 7 | ||||||||

| Dividends declared per share | $ | 0.05 | $ | 0.05 | $ | 0.05 | $ | 0.05 | $ | 0.06 | $ | 0.06 | $ | 0.07 | $ | 0.07 | ||||||||

Total assets (000's) | $ | 5,632,211 | $ | 5,009,177 | $ | 5,203,371 | $ | 5,268,074 | $ | 4,647,763 | $ | 4,618,131 | $ | 4,521,595 | $ | 4,476,865 | ||||||||

Total liabilities (000's) | $ | 1,481,476 | $ | 666,356 | $ | 735,672 | $ | 840,578 | $ | 1,019,027 | $ | 1,017,815 | $ | 1,021,391 | $ | 1,045,190 | ||||||||

Total shareholders' equity (000's) | $ | 4,150,735 | $ | 4,342,821 | $ | 4,467,699 | $ | 4,427,496 | $ | 3,628,736 | $ | 3,600,316 | $ | 3,500,204 | $ | 3,431,675 | ||||||||

| 1) | Expressed as United States dollars per ounce. |

| 2) | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during the period from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. |

| 3) | Refer to discussion on non-IFRS measure (iii) on page 44 of this MD&A. |

| 4) | Refer to discussion on non-IFRS measure (i) on page 42 of this MD&A |

| 5) | Refer to discussion on non-IFRS measure (ii) on page 43 of this MD&A. |

| 6) | On March 18, 2015, the Company declared dividends of $0.05 per common share for total dividends of $20.2 million, which was paid on April 14, 2015. |

| 7) | On March 20, 2014, the Company declared dividends of $0.07 per common share for total dividends of $25.0 million, which was paid on April 15, 2014. |

| Three Months Ended December 31, 2015 | ||||||||||||||||||||||

Ounces Produced² | Ounces Sold | Sales | Average Realized Price ($'s Per Ounce) | Average Cash Cost ($'s Per Ounce)3 | Average Depletion ($'s Per Ounce) | Gross Margin | Impairment Charges 4 | Other | Net Earnings | Cash Flow From Operations | Total Assets | |||||||||||

| Silver | ||||||||||||||||||||||

| San Dimas | 2,317 | 2,097 | $ | 29,954 | $ | 14.28 | $ | 4.24 | $ | 0.88 | $ | 19,218 | $ | - | $ | - | $ | 19,218 | $ | 21,061 | $ | 146,555 |

| Yauliyacu | 749 | 987 | 15,189 | 15.39 | 4.20 | 6.43 | 4,693 | - | - | 4,693 | 11,044 | 165,282 | ||||||||||

| Peñasquito | 1,766 | 2,086 | 32,125 | 15.40 | 4.07 | 2.85 | 17,700 | - | - | 17,700 | 23,636 | 430,847 | ||||||||||

| Antamina | 2,403 | 1,340 | 18,858 | 14.07 | 2.80 | 9.93 | 1,802 | - | - | 1,802 | 15,110 | 886,981 | ||||||||||

Barrick 5 | 627 | 569 | 8,231 | 14.47 | 3.90 | 3.24 | 4,171 | (109,723) | - | (105,552) | 5,595 | 498,090 | ||||||||||

Other 6 | 2,422 | 1,672 | 24,730 | 14.79 | 4.82 | 4.32 | 9,449 | (20,569) | - | (11,120) | 17,208 | 458,911 | ||||||||||

| 10,284 | 8,751 | $ | 129,087 | $ | 14.75 | $ | 4.06 | $ | 4.17 | $ | 57,033 | $ | (130,292) | $ | - | $ | (73,259) | $ | 93,654 | $ | 2,586,666 | |

| Gold | ||||||||||||||||||||||

Sudbury 7 | 12,203 | 6,256 | $ | 6,965 | $ | 1,113 | $ | 400 | $ | 841 | $ | (801) | $ | (49,439) | $ | - | $ | (50,240) | $ | 4,463 | $ | 506,250 |

| Salobo | 37,680 | 44,491 | 49,051 | 1,103 | 400 | 420 | 12,579 | - | - | 12,579 | 31,255 | 2,156,757 | ||||||||||

Other 8 | 19,293 | 14,152 | 15,393 | 1,088 | 381 | 531 | 2,476 | (51,170) | - | (48,694) | 10,090 | 219,739 | ||||||||||

| 69,176 | 64,899 | $ | 71,409 | $ | 1,100 | $ | 396 | $ | 485 | $ | 14,254 | $ | (100,609) | $ | - | $ | (86,355) | $ | 45,808 | $ | 2,882,746 | |

Silver equivalent 9 | 15,463 | 13,614 | $ | 200,496 | $ | 14.73 | $ | 4.50 | $ | 4.99 | $ | 71,287 | $ | (230,901) | $ | - | $ | (159,614) | $ | 139,462 | $ | 5,469,412 |

| Corporate | ||||||||||||||||||||||

| General and administrative | $ | (9,011) | $ | (9,011) | ||||||||||||||||||

| Other | (638) | (638) | ||||||||||||||||||||

| Total corporate | $ | (9,649) | $ | (9,649) | $ | (6,073) | $ | 162,799 | ||||||||||||||

| 15,463 | 13,614 | $ | 200,496 | $ | 14.73 | $ | 4.50 | $ | 4.99 | $ | 71,287 | $ | (230,901) | $ | (9,649) | $ | (169,263) | $ | 133,389 | $ | 5,632,211 | |

| 1) | All figures in thousands except gold ounces produced and sold and per ounce amounts. |

| 2) | Ounces produced represent the quantity of silver and gold contained in concentrate or doré prior to smelting or refining deductions. Production figures are based on information provided by the operators of the mining operations to which the silver or gold interests relate or management estimates in those situations where other information is not available. Certain production figures may be updated in future periods as additional information is received. |

| 3) | Refer to discussion on non-IFRS measure (iii) on page 44 of this MD&A. |

| 4) | Please see Impairment of Silver and Gold Interests section in this MD&A for further information. |

| 5) | Comprised of the operating Lagunas Norte, Pierina and Veladero silver interests in addition to the non-operating Pascua-Lama silver interest. |

| 6) | Comprised of the operating Los Filos, Zinkgruvan, Cozamin, Neves-Corvo, Stratoni, Minto, 777 and Constancia silver interests in addition to the non-operating Keno Hill, Rosemont, Aljustrel and Loma de La Plata silver interests. |

| 7) | Comprised of the operating Coleman, Copper Cliff, Garson, Stobie, Creighton and Totten gold interests in addition to the non-operating Victor gold interest. |

| 8) | Comprised of the operating Minto, 777 and Constancia gold interests in addition to the non-operating Rosemont gold interest. |

| 9) | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during the period from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. The gold / silver ratio during the three months ended December 31, 2015 was 74.9. |

| Three Months Ended December 31, 2014 | ||||||||||||||||||||

Ounces Produced² | Ounces Sold | Sales | Average Realized Price ($'s Per Ounce) | Average Cash Cost ($'s Per Ounce)3 | Average Depletion ($'s Per Ounce) | Gross Margin | Other | Net Earnings | Cash Flow From Operations | Total Assets | ||||||||||

| Silver | ||||||||||||||||||||

| San Dimas | 1,744 | 1,555 | $ | 25,571 | $ | 16.44 | $ | 4.20 | $ | 0.81 | $ | 17,773 | $ | - | $ | 17,773 | $ | 19,040 | $ | 152,951 |

| Yauliyacu | 687 | 761 | 11,896 | 15.63 | 4.16 | 5.92 | 4,221 | - | 4,221 | 8,730 | 187,478 | |||||||||

| Peñasquito | 1,582 | 1,640 | 27,493 | 16.76 | 4.05 | 2.98 | 15,966 | - | 15,966 | 20,851 | 451,145 | |||||||||

Barrick 4 | 690 | 671 | 11,216 | 16.72 | 3.90 | 3.26 | 6,411 | - | 6,411 | 8,600 | 605,328 | |||||||||

Other 5 | 1,701 | 1,106 | 18,219 | 16.47 | 4.29 | 3.95 | 9,101 | - | 9,101 | 12,929 | 559,747 | |||||||||

| 6,404 | 5,733 | $ | 94,395 | $ | 16.46 | $ | 4.13 | $ | 3.00 | $ | 53,472 | $ | - | $ | 53,472 | $ | 70,150 | $ | 1,956,649 | |

| Gold | ||||||||||||||||||||

Sudbury 6 | 9,924 | 11,251 | $ | 14,231 | $ | 1,265 | $ | 400 | $ | 841 | $ | 263 | $ | - | $ | 263 | $ | 10,168 | $ | 583,862 |

| Salobo | 12,253 | 14,270 | 16,924 | 1,186 | 400 | 462 | 4,625 | - | 4,625 | 11,216 | 1,302,202 | |||||||||

Other 7 | 13,925 | 12,383 | 14,825 | 1,197 | 373 | 616 | 2,573 | - | 2,573 | 10,316 | 405,552 | |||||||||

| 36,102 | 37,904 | $ | 45,980 | $ | 1,213 | $ | 391 | $ | 625 | $ | 7,461 | $ | - | $ | 7,461 | $ | 31,700 | $ | 2,291,616 | |

Silver equivalent 8 | 9,079 | 8,541 | $ | 140,375 | $ | 16.43 | $ | 4.51 | $ | 4.79 | $ | 60,933 | $ | - | $ | 60,933 | $ | 101,850 | $ | 4,248,265 |

| Corporate | ||||||||||||||||||||

| General and administrative | $ | (8,992) | $ | (8,992) | ||||||||||||||||

| Other | 89 | 89 | ||||||||||||||||||

| Total corporate | $ | (8,903) | $ | (8,903) | $ | (7,730) | $ | 399,498 | ||||||||||||

| 9,079 | 8,541 | $ | 140,375 | $ | 16.43 | $ | 4.51 | $ | 4.79 | $ | 60,933 | $ | (8,903) | $ | 52,030 | $ | 94,120 | $ | 4,647,763 | |

| 1) | All figures in thousands except gold ounces produced and sold and per ounce amounts. |

| 2) | Ounces produced represent the quantity of silver and gold contained in concentrate or doré prior to smelting or refining deductions. Production figures are based on information provided by the operators of the mining operations to which the silver or gold interests relate or management estimates in those situations where other information is not available. Certain production figures may be updated in future periods as additional information is received. |

| 3) | Refer to discussion on non-IFRS measure (iii) on page 44 of this MD&A. |

| 4) | Comprised of the operating Lagunas Norte, Pierina and Veladero silver interests in addition to the non-operating Pascua-Lama silver interest. |

| 5) | Comprised of the operating Los Filos, Zinkgruvan, Cozamin, Neves-Corvo, Stratoni, Minto, Constancia, 777 and Aljustrel silver interests, the non-operating Rosemont, Keno Hill and Loma de La Plata silver interests; and the previously owned Campo Morado and Mineral Park silver interests. |

| 6) | Comprised of the operating Coleman, Copper Cliff, Garson, Stobie, Totten and Creighton gold interests in addition to the non-operating Victor gold interest. |

| 7) | Comprised of the operating Minto, Constancia and 777 gold interests in addition to the non-operating Rosemont gold interest. |

| 8) | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during the period from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. The gold / silver ratio during the three months ended December 31, 2014 was 74.1. |

| 9) | Certain comparative figures have been reclassified to conform with the financial statement presentation adopted for the current year. |

| · | 2.4 million ounce increase related to the recently acquired silver stream at the Antamina mine; |

| · | 1.9 million silver equivalent ounce (210%) increase related to gold production at the Salobo mine (25,400 gold ounces), with the increase in gold production being primarily due to higher throughput as a result of the continuing ramp up of the first 12 Mtpa line, the commissioning of the second 12 Mtpa line which commenced late in the second quarter of 2014, and the acquisition of an additional 25% gold interest in the Salobo mine as explained in the Silver and Gold interests section of this MD&A; |

| · | 722,000 ounce (42%) increase related to silver production at the Other mines, due primarily to the ramping up of production at the Constancia mine; |

| · | 573,000 ounce (33%) increase related to the San Dimas mine, due primarily to the mining of higher grade material; and |

| · | 391,000 silver equivalent ounce (38%) increase related to gold production at the Other mines (5,400 gold ounces), due primarily to ramping up of production at the Constancia mine. |

| · | $36.0 million increase related to a 68% increase in payable silver ounces produced; and |

| · | $6.2 million increase related to a 92% increase in payable gold ounces produced; and |

| · | $0.5 million increase related to the composition of mines from which silver is produced; and |

| · | $3.4 million increase related to the composition of mines from which gold is produced; and |

| · | $6.7 million decrease as a result of the timing of shipments of stockpiled concentrate and doré, primarily attributable to the following factors: |

| i. | $9.9 million decrease relating to the Antamina mine; partially offset by |

| ii. | $2.3 million increase relating to the Peñasquito mine; and |

| iii. | $1.9 million increase relating to the Salobo mine. |

| · | $29.1 million decrease due to a reduction in the operating margin per ounce, due primarily to a 10% decrease in the average realized selling price per silver equivalent ounce sold; and |

| · | $230.9 million decrease as a result of an impairment charge taken during the period, as more fully explained in the Impairment of Silver and Gold Interests section of this MD&A; and |

| · | $0.7 million decrease as a result of an increase in corporate costs as explained in the Corporate Costs section of the MD&A ($1.7 million increase from a cash flow perspective). |

| Year Ended December 31, 2015 | ||||||||||||||||||||||

Ounces Produced² | Ounces Sold | Sales | Average Realized Price ($'s Per Ounce) | Average Cash Cost ($'s Per Ounce)3 | Average Depletion ($'s Per Ounce) | Gross Margin | Impairment Charges 4 | Other | Net Earnings | Cash Flow From Operations | Total Assets | |||||||||||

| Silver | ||||||||||||||||||||||

| San Dimas | 7,449 | 7,277 | $ | 113,198 | $ | 15.56 | $ | 4.22 | $ | 0.88 | $ | 76,122 | $ | - | $ | - | $ | 76,122 | $ | 82,518 | $ | 146,555 |

| Yauliyacu | 2,717 | 2,544 | 40,079 | 15.75 | 4.19 | 6.43 | 13,040 | - | - | 13,040 | 29,407 | 165,282 | ||||||||||

| Peñasquito | 7,237 | 7,132 | 114,083 | 16.00 | 4.07 | 2.85 | 64,759 | - | - | 64,759 | 85,057 | 430,847 | ||||||||||

| Antamina | 2,403 | 1,340 | 18,858 | 14.07 | 2.80 | 9.93 | 1,802 | - | - | 1,802 | 15,110 | 886,981 | ||||||||||

Barrick 5 | 2,383 | 2,364 | 37,103 | 15.70 | 3.90 | 3.24 | 20,237 | (109,723) | - | (89,486) | 27,887 | 498,090 | ||||||||||

Other 6 | 8,528 | 5,909 | 92,257 | 15.61 | 4.63 | 4.49 | 38,328 | (74,291) | - | (35,963) | 65,899 | 458,911 | ||||||||||

| 30,717 | 26,566 | $ | 415,578 | $ | 15.64 | $ | 4.17 | $ | 3.41 | $ | 214,288 | $ | (184,014) | $ | - | $ | 30,274 | $ | 305,878 | $ | 2,586,666 | |

| Gold | ||||||||||||||||||||||

Sudbury 7 | 36,364 | 33,481 | $ | 39,201 | $ | 1,171 | $ | 400 | $ | 841 | $ | (2,364) | $ | (49,439) | $ | - | $ | (51,803) | $ | 25,371 | $ | 506,250 |

| Salobo | 125,624 | 108,398 | 124,250 | 1,146 | 400 | 420 | 35,389 | - | - | 35,389 | 80,890 | 2,156,757 | ||||||||||

Other 8 | 66,776 | 60,470 | 69,658 | 1,152 | 376 | 568 | 12,579 | (151,469) | - | (138,890) | 46,595 | 219,739 | ||||||||||

| 228,764 | 202,349 | $ | 233,109 | $ | 1,152 | $ | 393 | $ | 534 | $ | 45,604 | $ | (200,908) | $ | - | $ | (155,304) | $ | 152,856 | $ | 2,882,746 | |

Silver equivalent 9 | 47,697 | 41,574 | $ | 648,687 | $ | 15.60 | $ | 4.58 | $ | 4.78 | $ | 259,892 | $ | (384,922) | $ | - | $ | (125,030) | $ | 458,734 | $ | 5,469,412 |

| Corporate | ||||||||||||||||||||||

| General and administrative | $ | (32,237) | $ | (32,237) | ||||||||||||||||||

| Other | (4,775) | (4,775) | ||||||||||||||||||||

| Total corporate | $ | (37,012) | $ | (37,012) | $ | (27,375) | $ | 162,799 | ||||||||||||||

| 47,697 | 41,574 | $ | 648,687 | $ | 15.60 | $ | 4.58 | $ | 4.78 | $ | 259,892 | $ | (384,922) | $ | (37,012) | $ | (162,042) | $ | 431,359 | $ | 5,632,211 | |

| 1) | All figures in thousands except gold ounces produced and sold and per ounce amounts. |

| 2) | Ounces produced represent the quantity of silver and gold contained in concentrate or doré prior to smelting or refining deductions. Production figures are based on information provided by the operators of the mining operations to which the silver or gold interests relate or management estimates in those situations where other information is not available. Certain production figures may be updated in future periods as additional information is received. |

| 3) | Refer to discussion on non-IFRS measure (iii) on page 44 of this MD&A. |

| 4) | Please see Impairment of Silver and Gold Interests section in this MD&A for further information. |

| 5) | Comprised of the operating Lagunas Norte, Pierina and Veladero silver interests in addition to the non-operating Pascua-Lama silver interest. |

| 6) | Comprised of the operating Los Filos, Zinkgruvan, Cozamin, Neves-Corvo, Stratoni, Minto, 777 and Constancia silver interests in addition to the non-operating Keno Hill, Rosemont, Aljustrel and Loma de La Plata silver interests. |

| 7) | Comprised of the operating Coleman, Copper Cliff, Garson, Stobie, Creighton and Totten gold interests in addition to the non-operating Victor gold interest. |

| 8) | Comprised of the operating Minto, 777 and Constancia gold interests in addition to the non-operating Rosemont gold interest. |

| 9) | Gold ounces produced and sold are converted to a silver equivalent basis based on either (i) the ratio of the average silver price received to the average gold price received during the period from the assets that produce both gold and silver; or (ii) the ratio of the price of silver to the price of gold on the date of sale as per the London Bullion Metal Exchange for the assets which produce only gold. The gold / silver ratio during the year ended December 31, 2015 was 74.2. |

| Year Ended December 31, 2014 | ||||||||||||||||||||||

Ounces Produced² | Ounces Sold | Sales | Average Realized Price ($'s Per Ounce) | Average Cash Cost ($'s Per Ounce)3 | Average Depletion ($'s Per Ounce) | Gross Margin | Impairment Charges 4 | Other | Net Earnings | Cash Flow From Operations | Total Assets | |||||||||||

| Silver | ||||||||||||||||||||||

San Dimas 5 | 5,760 | 5,573 | $ | 104,095 | $ | 18.68 | $ | 4.19 | $ | 0.81 | $ | 76,228 | $ | - | $ | - | $ | 76,228 | $ | 80,769 | $ | 152,951 |

| Yauliyacu | 2,938 | 3,342 | 64,011 | 19.15 | 4.15 | 5.92 | 30,353 | - | - | 30,353 | 50,152 | 187,478 | ||||||||||