UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

_____________________________________________

FORM 10-K

_____________________________________________

|

| |

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2019

OR

|

| |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File Number 1-71

_____________________________________________

HEXION INC.

(Exact name of registrant as specified in its charter)

_____________________________________________

|

| | |

| New Jersey | | 13-0511250 |

| (State of incorporation) | | (I.R.S. Employer Identification No.) |

| | |

| 180 East Broad St., Columbus, OH 43215 | | 614-225-4000 |

| (Address of principal executive offices) | | (Registrant’s telephone number) |

_____________________________________________

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT: |

| | |

| Title of each class | Trading Symbol(s) | Name of each exchange on which registered |

| None | | None |

_____________________________________________

|

|

| (Former name, former address and fiscal year, if changed since last report) |

_____________________________________________

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: NONE

_____________________________________________

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x.

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes o No x.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes o No x.

Explanatory Note: While the registrant is not subject to the filing requirements of Section 13 or 15(d) of the Securities Exchange Act of 1934, it has filed all reports required to be filed by such filing requirements during the preceding 12 months.

Indicate by check mark whether the registrant has submitted electronically, if any, every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes x No o.

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer, a smaller reporting company or an emerging growth company. See definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

| | | | | | |

| Large accelerated filer | | o | | Accelerated filer | | o |

| Non-accelerated filer | | x | | | | |

| | | | | Smaller reporting company | | o |

| | | | | Emerging growth company | | o |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x.

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

At December 31, 2019, the aggregate market value of voting and non-voting common equity of the Registrant held by non-affiliates was zero.

Number of shares of common stock, par value $0.01 per share, outstanding as of the close of business on March 1, 2020: 100

Documents incorporated by reference. None

HEXION INC.

INDEX

|

| | |

| | | Page |

| PART I | |

| | |

| | |

| | |

| | |

| | |

| | |

| | | |

| PART II | |

| | |

| | |

| | |

| | |

| | |

| Consolidated Financial Statements of Hexion Inc. | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| Financial Statement Schedules: | | |

| | |

| | |

| | |

| | |

| | | |

| PART III | | |

| | |

| | |

| | |

| | |

| | |

| | | |

| PART IV | | |

| | |

| | |

| | |

PART I

(dollars in millions)

Forward Looking and Cautionary Statements

Certain statements in this report, including without limitation, certain statements made under Item 1, “Business,” and Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” are forward-looking statements within the meaning of and made pursuant to the safe harbor provisions of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. In addition, our management may from time to time make oral forward-looking statements. All statements, other than statements of historical facts, are forward-looking statements. Forward-looking statements may be identified by the words “believe,” “expect,” “anticipate,” “project,” “might,” “plan,” “estimate,” “may,” “will,” “could,” “should,” “seek” or “intend” and similar expressions. Forward-looking statements reflect our current expectations and assumptions regarding our business, the economy and other future events and conditions and are based on currently available financial, economic and competitive data and our current business plans. Actual results could vary materially depending on risks and uncertainties that may affect our operations, markets, services, prices and other factors as discussed in the Risk Factors section of this report and our other filings with the Securities and Exchange Commission (the “SEC”). While we believe our assumptions are reasonable, we caution you against relying on any forward-looking statements as it is very difficult to predict the impact of known factors, and it is impossible for us to anticipate all factors that could affect our actual results. Important factors that could cause actual results to differ materially from those in the forward-looking statements include, but are not limited to, a weakening of global economic and financial conditions, interruptions in the supply of or increased cost of raw materials, the loss of, or difficulties with the further realization of, cost savings in connection with our strategic initiatives, the impact of our indebtedness, our failure to comply with financial covenants under our credit facilities or other debt, pricing actions by our competitors that could affect our operating margins, changes in governmental regulations and related compliance and litigation costs and the other factors listed in the Risk Factors section of this report and in our other SEC filings. For a more detailed discussion of these and other risk factors, see the Risk Factors section of this report and our most recent filings made with the SEC. All forward-looking statements are expressly qualified in their entirety by this cautionary notice. The forward-looking statements made by us speak only as of the date on which they are made. Factors or events that could cause our actual results to differ may emerge from time to time. We undertake no obligation to publicly update or revise any forward-looking statement as a result of new information, future events or otherwise, except as otherwise required by law.

ITEM 1 - BUSINESS

Overview

Hexion Inc. (“Hexion” or the “Company”), a New Jersey corporation with predecessors dating from 1899, is one of the world’s largest producers of thermosetting resins, or thermosets, and a leading producer of adhesive and structural resins and coatings. Thermosetting resins include materials such as phenolic resins, epoxy resins and urethane resins. Our products include a broad range of critical components and formulations used to impart valuable performance characteristics such as durability, gloss, heat resistance, adhesion, and strength to our customers and their customers’ final products. We serve highly diversified growing end-markets such as residential and non-residential construction, wind energy, industrial, automotive, consumer goods, and electronics.

Our business is organized based on the products we offer and the markets we serve. At December 31, 2019, we had three reportable segments: Forest Products Resins; Epoxy, Phenolic and Coating Resins; and Corporate and Other. Effective January 1, 2020, we have changed our segment reporting structure and aligned the reporting structure around two growth platforms: Adhesives; and Coatings and Composites. Corporate and Other will continue to be a reportable segment. See Note 18 in Item 8 of Part II of this Annual Report on Form 10-K for more information.

Emergence from Chapter 11 Bankruptcy

On April 1, 2019, the Company, Hexion Holdings LLC, Hexion LLC and certain of the Company’s subsidiaries (collectively, the “Debtors”) filed voluntary petitions (the “Bankruptcy Petitions”) for reorganization under Chapter 11 (“Chapter 11”) of the U.S. Bankruptcy Code (the “Bankruptcy Code”) in the United States Bankruptcy Court for the District of Delaware, (the “Bankruptcy Court”). The Chapter 11 proceedings were jointly administered under the caption In re Hexion TopCo, LLC, No. 19-10684 (the “Chapter 11 Cases”). The Debtors continued to operate their businesses as “debtors-in-possession” under the jurisdiction of the Bankruptcy Court and in accordance with the applicable provisions of the Bankruptcy Code and orders of the Bankruptcy Court.

On June 25, 2019, the Court entered an order (the “Confirmation Order”) confirming the Second Amended Joint Chapter 11 Plan of Reorganization of Hexion Holdings LLC and its Debtor Affiliates under Chapter 11 (the “Plan”). On the morning of July 1, 2019, in accordance with the terms of the Plan and the Confirmation Order, the Plan became effective and the Debtors emerged from bankruptcy (the “Emergence”).

As a result of our reorganization and emergence from Chapter 11 on the morning of July 1, 2019 (the “Effective Date”), our direct parent is Hexion Intermediate Holding 2, Inc. (“Hexion Intermediate”), a holding company and wholly owned subsidiary of Hexion Intermediate Holding 1, Inc., a holding company and wholly owned subsidiary of Hexion Holdings Corporation, the ultimate parent of Hexion (“Hexion Holdings”). Prior to its reorganization, the Company’s parent was Hexion LLC, a holding company and wholly owned subsidiary of Hexion Holdings LLC (now known as Hexion TopCo, LLC or “TopCo”), the previous ultimate parent entity of Hexion, which was controlled by investment funds managed by affiliates of Apollo Management Holdings, L.P. (together with Apollo Global Management, Inc. and its subsidiaries, “Apollo”).

Fresh Start Accounting

On the Effective Date, in accordance with ASC 852, the Company applied fresh start accounting to its financial statements as (i) the holders of existing voting shares of the Company prior to its emergence received less than 50% of the voting shares of the Company outstanding following its emergence from bankruptcy and (ii) the reorganization value of the Company’s assets immediately prior to confirmation of the plan of reorganization was less than the post-petition liabilities and allowed claims. Fresh start accounting was applied to the Company’s consolidated financial statements as of July 1, 2019, the date it emerged from bankruptcy, which resulted in a new basis of accounting and the Company became a new entity for financial reporting purposes. As a result, the Company allocated the reorganization value of the Company to its individual assets based on their estimated fair values. Reorganization value represents the fair value of the Company’s assets before considering liabilities. The excess reorganization value over the fair value of identified tangible and intangible assets was reported as goodwill. Refer to Note 4 in Item 8 of Part II of this Annual Report on Form 10-K for more information.

Financial Results Summary

Our financial results for the period from January 1, 2019 through July 1, 2019 and for fiscal years ended 2018 and 2017 are referred to as those of the “Predecessor” period. Our financial results for the period from July 2, 2019 through December 31, 2019 are referred to as those of the “Successor” period. Our results of operations as reported in our Consolidated Financial Statements for these periods are prepared in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”), which requires that we report on our results for the period from January 1, 2019 through July 1, 2019 and the period from July 2, 2019 through December 31, 2019 separately.

We do not believe that reviewing the results of these periods in isolation would be useful in identifying trends in or reaching conclusions regarding our overall operating performance. We believe that the key performance metrics such as Net sales, Operating income and Segment EBITDA for the Successor period when combined with the 2019 Predecessor period provides more meaningful comparisons to other periods and are useful in identifying current business trends. Accordingly, in addition to presenting our results of operations as reported in our Consolidated Financial Statements in accordance with U.S. GAAP, the tables and discussions below also present the combined results for the year ended December 31, 2019.

The combined results (referenced as “Non-GAAP Combined” or “Combined”) for the year ended December 31, 2019, which we refer to herein as results for the “Year Ended December 31, 2019” represent the sum of the reported amounts for the Predecessor period January 1, 2019 through July 1, 2019 combined with the Successor period from July 2, 2019 through December 31, 2019. These Combined results are not considered to be prepared in accordance with U.S. GAAP and have not been prepared as pro forma results under applicable regulations. The Non-GAAP Combined operating results are presented for supplemental purposes only, may not reflect the actual results we would have achieved absent our emergence from bankruptcy, may not be indicative of future results and should not be viewed as a substitute for the financial results of the Predecessor period and Successor period presented in accordance with U.S. GAAP.

Products and Markets

We have a broad range of thermoset resin technologies, with high quality research, applications development and technical service capabilities. We provide a broad array of thermosets and associated technologies, and have significant market positions in each of the key markets that we serve.

Our products are used in thousands of applications and are sold into diverse markets, such as forest products, architectural and industrial paints, packaging, consumer products, composites and automotive coatings. Major industry sectors that we serve include industrial/marine, construction, consumer/durable goods, automotive, wind energy, aviation, electronics, architectural, civil engineering, repair/remodeling and oil and gas field support. The diversity of our products limits our dependence on any one market or end-use. We have a history of product innovation and success in introducing new products to new markets, as evidenced by more than 750 granted patents, the majority of which relate to the development of new products and manufacturing processes, and we are constantly looking at ways to introduce new products in our currently established markets.

As of December 31, 2019, we had 45 active production sites around the world. Through our worldwide network of strategically located production facilities, we serve more than 3,100 customers in approximately 85 countries. Our position in certain additives, complementary materials and services further enables us to leverage our core thermoset technologies and provide our customers with a broad range of product solutions. As a result of our focus on innovation and a high level of technical service, we have cultivated long-standing customer relationships. Our global customers include leading companies in their respective industries, such as Akzo Nobel, BASF, Norbord, Louisiana Pacific, Monsanto, Owens Corning, PPG Industries, Sherwin Williams and Weyerhaeuser.

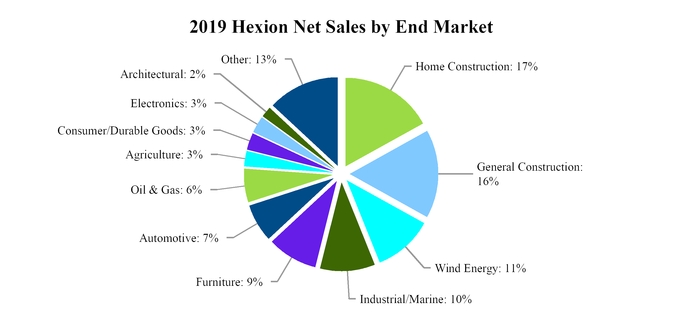

In 2019, our revenue base included sales in the following end markets:

Industry & Competitors

We are a large participant in the specialty chemicals industry. Thermosetting resins are generally considered specialty chemical products because they are sold primarily on the basis of performance, technical support, product innovation and customer service. However, as a result of the impact of the ongoing global economic uncertainty and overcapacity in certain markets, certain of our competitors have focused more on price to retain business and market share, which we have selectively followed in certain markets to maintain market share and remain a market leader.

We compete with many companies in most of our product lines, including large global chemical companies and small specialty chemical companies. No single company competes with us across all of our segments and existing product lines. The principal competitive factors in our industry include technical service, breadth of product offerings, product innovation, product quality and price. Some of our competitors are larger, have greater financial resources and may be able to better withstand adverse changes in industry conditions, including pricing, and the economy as a whole. Further, our competitors may have more resources to support continued expansion than we do. Some of our competitors also have a greater range of products and may be more vertically integrated than we are within specific product lines or geographies.

We believe that the principal factors that contribute to success in the specialty chemicals market, and our ability to maintain our position in the markets we serve, are (i) consistent delivery of high-quality products; (ii) favorable process economics; (iii) the ability to provide value to customers through both product attributes and strong technical service and (iv) an international footprint and presence in growing and developing markets.

Our Businesses

The following is a discussion of our reportable segments, their corresponding major product lines and the primary end-use applications of our key products as of December 31, 2019.

Forest Products Resins Segment

2019 Net Sales: $1,485

Formaldehyde Based Resins and Intermediates

We are the leading producer of formaldehyde-based resins for the North American forest products industry, and also hold significant positions in Latin America, Australia, New Zealand, and Europe. Formaldehyde-based resins, also known as forest products resins, are a key adhesive and binding ingredient used in the production of a wide variety of engineered lumber products, including medium-density fiberboard (“MDF”), particleboard, oriented strand board (“OSB”) and various types of plywood and laminated veneer lumber (“LVL”). These products are used in a wide range of applications in the construction, remodeling and furniture industries. Nearly all of our formaldehyde requirements for the production of forest products resins are provided by internal production, giving us a competitive advantage versus our non-integrated competitors.

In addition, we are a significant producer of formaldehyde, a key raw material used to manufacture thousands of other chemicals and products, including the manufacture of methylene diphenyl diisocyanate (“MDI”) and butanediol (“BDO”). Formaldehyde consuming products are used in multiple applications including agricultural, construction, energy and automotive industries.

Both forest products resins and formaldehyde have relatively short shelf lives, and as such, our manufacturing facilities are strategically located in close proximity to our customers.

|

| | |

| Products | | Key Applications |

| Forest Products Resins: | | |

| Engineered Wood Resins | | Softwood and hardwood plywood, OSB, LVL, particleboard, MDF and decorative laminates |

| | |

| Specialty Wood Adhesives | | Laminated beams, cross-laminated timber, structural and nonstructural fingerjoints, wood composite I-beams, truck-decking, cabinets, doors, windows, furniture, molding and millwork and paper laminations |

| | |

| Wax Emulsions | | Moisture resistance for panel boards and other specialty applications |

Principal Competitors: Arclin, Georgia-Pacific, Huntsman and BASF

|

| | |

| Products | | Key Applications |

| Formaldehyde Applications: | | |

| Formaldehyde | | MDI, BDO, herbicides and fungicides, scavengers for oil and gas production, fabric softeners, urea formaldehyde resins, phenol formaldehyde resins, melamine formaldehyde resins, hexamine and other catalysts |

Principal Competitors: Foremark Performance Chemicals, Georgia-Pacific and Arclin

Epoxy, Phenolic and Coating Resins Segment

2019 Net Sales: $1,889

Epoxy Specialty Resins

We are a leading producer of epoxy specialty resins, modifiers and curing agents in Europe and the United States with a global reach to our end markets, which include other regions such as China and Latin America. Epoxy resins are the fundamental component of many types of materials and are often used in the automotive, construction, wind energy, aerospace and electronics industries due to their superior adhesion, strength and durability. We internally consume approximately 30% of our liquid epoxy resin (“LER”) production in specialty composite, coating and adhesive applications, which ensures a consistent supply of our required intermediate materials. Our position in basic epoxy resins, along with our technology and service expertise, has enabled us to offer formulated specialty products in certain markets. In composites, our specialty epoxy products are used either as replacements for traditional materials such as metal, wood and ceramics, or in applications where traditional materials do not meet demanding engineering specifications.

We are a leading producer of resins that are used in fiber reinforced composites. Composites are a fast growing class of materials that are used in a wide variety of applications ranging from aircraft components and wind turbine blades to sports equipment, and increasingly in automotive and transportation. We supply epoxy resin systems to composite fabricators in the wind energy, automotive and pipe markets.

Epoxy specialty resins are also used for a variety of high-end coating applications that require the superior adhesion, corrosion resistance and durability of epoxy, such as protective coatings for industrial flooring, pipe, marine and construction applications and automotive coatings. Epoxy-based surface coatings are among the most widely used industrial coatings due to their long service life and broad application functionality combined with overall economic efficiency. We also leverage our resin and additives position to supply custom resins to specialty coatings formulators.

|

| | |

| Products | | Key Applications |

| Adhesive Applications: | | |

| Civil Engineering | | Building and bridge construction, concrete enhancement and corrosion protection |

| | |

| Adhesives | | Automotive: hem flange adhesives and panel reinforcements |

| | |

| | | Construction: ceramic tiles, chemical dowels and marble |

| | |

| | | Aerospace: metal and composite laminates |

| | |

| | | Electronics: chip adhesives and solder masks |

| Electrical Applications: | | |

| Electronic Resins | | Unclad sheets, paper impregnation and electrical laminates for printed circuit boards |

| | | |

| Electrical Castings | | Generators and bushings, transformers, medium and high-voltage switch gear components, post insulators, capacitors and automotive ignition coils |

Principal Competitors: Olin, Nan Ya, Huntsman, Spolchemie, Leuna Harze and Aditya Birla (Thai Epoxy)

|

| | |

| Products | | Key Applications |

| Composites: | | |

| Composite Epoxy Resins | | Pipes and tanks, automotive, sports (ski, snowboard, golf), boats, construction, aerospace, wind energy and industrial applications |

Principal Competitors: Olin, Aditya Birla (Thai Epoxy), Huntsman, Swancor, Bohui, Techstorm and Kangda

|

| | |

| Products | | Key Applications |

| Coating Applications: | | |

| Floor Coatings (LER, Solutions, Performance Products) | | Chemically resistant, antistatic and heavy duty flooring used in hospitals, the chemical industry, electronics workshops, retail areas and warehouses |

| | |

| Ambient Cured Coatings (LER, Solid Epoxy Resin (“SER”) Solutions, Performance Products) | | Marine (manufacturing and maintenance), shipping containers and large steel structures (such as bridges, pipes, plants and offshore equipment) |

| | |

Waterborne Coatings (EPI-REZTM Epoxy Waterborne Resins) | | Substitutes of solvent-borne products in both heat cured and ambient cured applications |

Principal Competitors: Olin, Huntsman, Nan Ya, Evonik and Allnex

Basic Epoxy Resins and Intermediates

We are one of the world’s largest suppliers of basic epoxy resins, such as SER and LER. These base epoxies are used in a wide variety of industrial coatings applications. In addition, we are a major producer of bisphenol-A (“BPA”) and epichlorohydrin (“ECH”), key precursors in the downstream manufacture of basic epoxy resins and epoxy specialty resins. We internally consume the majority of our BPA, and all of our ECH, which ensures a consistent supply of our required intermediate materials.

|

| | |

| Products | | Key Applications |

| Electrocoat (LER, SER, BPA) | | Automotive, general industry and white goods (such as appliances) |

| | |

| Powder Coatings (SER, Performance Products) | | White goods, pipes for oil and gas transportation, general industry (such as heating radiators) and automotive (interior parts and small components) |

| | |

| Heat Cured Coatings (LER, SER) | | Metal packaging and coil-coated steel for construction and general industry |

Principal Competitors: Olin, Kukdo, Nan Ya and the Formosa Plastics Group and CCP

Versatic Acids and Derivatives

We are the world’s largest producer of Versatic acids and derivatives. Versatic acids and derivatives are specialty monomers that provide significant performance advantages for finished coatings, including superior adhesion, hydrolytic stability, water resistance, appearance and ease of application. Our products include basic Versatic acids and derivatives sold under the Versatic™, VEOVA™ vinyl ester and CARDURA™ glycidyl ester names. Applications for these specialty monomers include decorative, automotive and protective coatings, as well as other uses, such as adhesives and intermediates.

|

| | |

| Products | | Key Applications |

| CARDURA™ glycidyl ester | | Automotive repair/refinishing, automotive original equipment manufacturing (“OEM”) and industrial coatings |

| | |

| Versatic™ Acids | | Chemical intermediates (e.g., for peroxides, pharmaceuticals and agrochemicals) and adhesion promoters (e.g., for tires) |

| | |

VEOVA™ vinyl ester | | Architectural coatings, construction and adhesives |

Principal Competitors: ExxonMobil and Hebei Shield Excellence Technology

Phenolic Specialty Resins and Molding Compounds

We are one of the leading producers of phenolic specialty resins, which are used in applications that require extreme heat resistance and strength, such as after-market automotive and OEM truck brake pads, filtration, aircraft components and foundry resins. These products are sold under globally recognized brand names such as BORDEN, BAKELITE, DURITE and CELLOBOND. Our phenolic specialty resins are known for their binding qualities and are used widely in the production of mineral wool and glass wool used for commercial and domestic insulation applications. We are also a leading producer of phenolic resin encapsulated sand and ceramic substrates that are used in oil field applications. Our highly specialized compounds and resins are designed to perform well under extreme conditions, such as intense heat, high-closure stress and corrosive environments, that characterize oil and gas drilling, and are also used to enhance oil and gas recovery rates and extend well life.

|

| | |

| Products | | Key Applications |

| Phenolic Specialty Resins: | | |

| Composites and Electronic Resins | | Aircraft & rail components, ballistic applications, industrial grating, pipe, jet engine components, computer chip encasement and photolithography |

| | |

| Automotive Phenol Formaldehyde Resins | | Acoustical insulation, engine filters, brakes, friction materials, interior components, molded electrical parts and assemblies |

| | |

| Construction Phenol Formaldehyde Resins and Urea Formaldehyde Resins | | Fiberglass insulation, floral foam, insulating foam, lamp cement for light bulbs, molded appliance and electrical parts, molding compounds, sandpaper, fiberglass mat and coatings |

| | |

| Molding Compounds: | | |

| Phenolic, Epoxy, Unsaturated Polyesters | | High performance automotive transmissions and under-hood components, heat resistant knobs and bases, switches and breaker components, pot handles and ashtrays |

| | | |

| Glass | | High load, dimensionally stable automotive underhood parts and commutators |

| | | |

| Phenolic Encapsulated Substrates: | | |

| Resin Encapsulated Proppants | | Oil and gas fracturing |

Principal Competitors: Sumitomo (Durez), SI Group, Plenco, Dynea International, Arclin, Georgia-Pacific, Shenquan, Covia Holdings Corporation, Preferred Sands, Badger Mining Corporation, and Carbo Ceramics

Corporate and Other Segment

Our Corporate and Other segment primarily includes corporate general and administrative expenses that are not allocated to the other segments, such as shared service and administrative functions, foreign exchange gains and losses and legacy company costs.

For additional information about our segments, see Note 18 to our Consolidated Financial Statements in Item 8 of Part II of this Annual Report on Form 10-K.

Marketing, Customers and Seasonality

Our products are sold to industrial users worldwide through a combination of a direct sales force that services our larger customers and third-party distributors that more cost-effectively serve our smaller customers. Our customer service and support network is made up of key regional customer service centers. We have global account teams that serve the major needs of our global customers for technical service and supply and commercial term requirements. Where operating and regulatory factors vary from country to country, these functions are managed locally.

In 2019, our largest customer accounted for approximately 3% of our net sales, and our top ten customers accounted for approximately 20% of our net sales. Neither our overall business nor any of our reporting segments depends on any single customer or a particular group of customers; therefore, the loss of any single customer would not have a material adverse effect on either of our two reporting segments or the Company as a whole. Our primary customers are manufacturers, and the demand for our products is seasonal in certain of our businesses, with the highest demand in the summer months and lowest in the winter months. Therefore, the dollar amount of our backlog orders as of December 31, 2019 is not significant. Demand for our products can also be cyclical, as general economic health and industrial and commercial production levels are key drivers for our business.

International Operations

Our non-U.S. operations accounted for 56%, 56% and 58% of our sales in 2019, 2018 and 2017, respectively. While our international operations may be subject to a number of additional risks, such as exposure to foreign currency exchange risk, we do not believe that our foreign operations, on the whole, carry significantly greater risk than our operations in the United States. Information about sales by geographic region for the past three years and long-lived assets by geographic region for the past two years can be found in Note 18 in Item 8 of Part II of this Annual Report on Form 10-K. More information about our methods and actions to manage exchange risk and interest rate risk can be found in Item 7A of Part II of this Annual Report on Form 10-K.

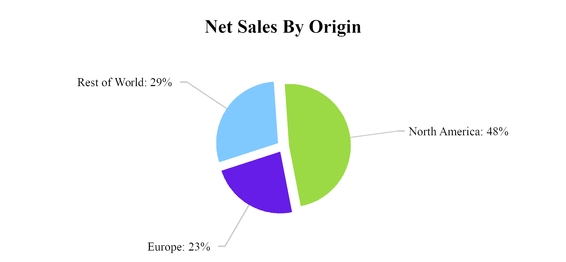

In 2019, our revenue base included sales in the following regions:

Raw Materials

In 2019, we purchased approximately $2.0 billion of raw materials, representing approximately 75% of our cost of sales (excluding depreciation expense). The three largest raw materials that we use are phenol, methanol and urea, which collectively represented approximately 50% of our total raw material expenditures in 2019. The majority of raw materials that we use to manufacture our products are available from more than one source, and are readily available in the open market. We have long-term purchase agreements for certain raw materials that ensure the availability of adequate supply. These agreements generally have periodic price adjustment mechanisms and do not have minimum annual purchase requirements. Smaller quantity materials that are single sourced generally have long-term supply contracts to maximize supply reliability. Prices for our main feedstocks are generally driven by underlying petrochemical benchmark prices and energy costs, which are subject to price fluctuations. Although we seek to offset increases in raw material prices with increases in our product prices, we may not always be able to do so, and there are periods when price increases lag behind raw material price increases.

Research and Development

Our research and development activities are geared towards developing and enhancing products, processes and application technologies so that we can maintain our position as the world’s largest producer of thermosetting resins. We focus on:

| |

| • | developing new or improved applications based on our existing product lines and identified market trends; |

| |

| • | developing new resin products and applications for customers to improve their competitive advantage and profitability; |

| |

| • | providing premier technical service for customers of specialty products; |

| |

| • | providing technical support for manufacturing locations and assisting in optimizing our manufacturing processes; |

| |

| • | ensuring that our products are manufactured consistent with our global environmental, health and safety policies and objectives; |

| |

| • | developing lower cost manufacturing processes globally; and |

| |

| • | expanding our production capacity. |

We have over 360 scientists and technicians worldwide. Our research and development facilities include a broad range of synthesis, testing and formulating equipment and small-scale versions of customer manufacturing processes for applications development and demonstration.

More recently, we have focused research and development resources on the incorporation of green chemistry principles into technology innovations to remain competitive and to address our customers’ demands for more environmentally preferred solutions. Our efforts have focused on developing resin technologies that reduce emissions, maximize efficiency and increase the use of bio-based raw materials. Some examples of meaningful results of our investment in the development of green products include:

| |

| • | EPIKOTE™ / EPIKURE™ epoxy systems for wind energy applications, which provide superior mechanical and process properties, reducing air emissions when hours of energy are created; |

| |

| • | EPIKOTE™ and Bakelite® resin systems for automotive applications, which produce lightweight automotive composite components and other automotive parts that allow customers to build cars with better mileage, reducing air emissions without sacrificing performance; |

| |

| • | EcoBind™ Resin Technology, an ultra low-emitting binder resin used to produce engineered wood products, |

| |

| • | Epi-Rez™ Epoxy Waterborne Resins, which provide for lower volatile organic compounds, reducing air emissions; and |

| |

| • | VeoVa™ vinyl ester, a Versatics acid and derivatives product, which is an isocyanate-free resin. |

In 2019, 2018 and 2017, our research and development and technical services expense was $50, $53 and $58, respectively. We take a customer-driven approach to discovering new applications and processes and providing customer service through our technical staff. Through regular direct contact with our key customers, our research and development associates can become aware of evolving customer needs in advance, and can anticipate their requirements to more effectively plan customer programs. We also focus on continuous improvement of plant yields and production capacity and reduction of fixed costs.

Intellectual Property

As of December 31, 2019, we own, license or have rights to over 750 patents and over 1,100 registered trademarks, as well as various patent and trademark applications and technology licenses around the world, which we currently use or hold for use in our operations. A majority of our patents relate to developing new products and processes for manufacturing and will expire between 2020 and 2037. We renew our trademarks on a regular basis. While we view our patents and trademarks to be valuable, because of the broad scope of our products and services, we do not believe that the loss or expiration of any single patent or trademark would have a material adverse effect on our results of operations, financial position or the continuation of our business.

Industry Regulatory Matters

Domestic and international laws regulate the production and marketing of chemical substances. Almost every country has its own legal procedures for registration and import. Of these, the laws and regulations in the European Union, the United States (Toxic Substances Control Act) and China are the most significant to our business. Additionally, other laws and regulations may also limit our expansion into other countries. Chemicals that are not included on one or more of these, or any other country’s chemical inventory lists, can usually be registered and imported, but may first require additional testing or submission of additional administrative information.

The European Commission enacted a regulatory system in 2006, known as Registration, Evaluation, Authorization and Restriction of Chemical substances (“REACH”), which requires manufacturers, importers and consumers of certain chemicals to register these chemicals and evaluate their potential impact on human health and the environment. As REACH matures, significant market restrictions could be imposed on the current and future uses of chemical products that we use as raw materials or that we sell as finished products in the European Union. Other countries may also enact similar regulations.

Environmental Regulations

Our policy is to operate our plants in a manner that protects the environment, health and safety of our employees, customers and communities. We have implemented company-wide environmental, health and safety policies managed by our Environmental, Health and Safety (“EH&S”) department and overseen by the EH&S Committee of Hexion Holdings’ Board of Directors. Our EH&S department provides support and oversight to our operations worldwide to ensure compliance with environmental, health and safety laws and regulations. This responsibility is executed via training, communication of EH&S policies, formulation of relevant policies and standards, EH&S audits and incident response planning and implementation. Our EH&S policies include systems and procedures that govern environmental emissions, waste generation, process safety management, handling, storage and disposal of hazardous substances, worker health and safety requirements, site security, emergency planning and response and product stewardship.

Our operations involve the use, handling, processing, storage, transportation and disposal of hazardous materials, and we are subject to extensive environmental regulation at the federal, state and international levels. We are also exposed to the risk of claims for environmental remediation or restoration. Our production facilities require operating permits that are subject to renewal or modification. Violations of environmental laws or permits may result in restrictions being imposed on operating activities, substantial fines, penalties, damages or other costs. In addition, statutes such as the federal Comprehensive Environmental Response, Compensation and Liability Act and comparable state and foreign laws impose strict, joint and several liability for investigating and remediating the consequences of spills and other releases of hazardous materials, substances and wastes at current and former facilities, as well as third-party disposal sites. Other laws permit individuals to seek recovery of damages for alleged personal injury or property damage due to exposure to hazardous substances and conditions at our facilities or to hazardous substances otherwise owned, sold or controlled by us. Therefore, notwithstanding our commitment to environmental management and environmental health and safety, we may incur liabilities in the future, and these liabilities may result in a material adverse effect on our business, financial condition, results of operations or cash flows.

Although our environmental policies and practices are designed to ensure compliance with international, federal and state laws and environmental regulations, future developments and increasingly stringent regulation could require us to make additional unforeseen environmental expenditures. In addition, our former operations, including our ink, wallcoverings, film, phosphate mining and processing, thermoplastics and food and dairy operations, may give rise to claims relating to our period of ownership.

We expect to incur future costs for capital improvements and general compliance under environmental, health and safety laws, including costs to acquire, maintain and repair pollution control equipment. In 2019, we incurred related capital expenditures of $20. We estimate that capital expenditures in 2020 for environmental controls at our facilities will be between $25 and $30. This estimate is based on current regulations and other requirements, but it is possible that a material amount of capital expenditures, in addition to those we currently anticipate, could be necessary if these regulations or other requirements or other facts change.

Employees

At December 31, 2019, we had approximately 4,000 employees. Approximately 40% of our employees are members of a labor union or are represented by workers’ councils that have collective bargaining agreements, including most of our European employees. We believe that we have good relations with our union and non-union employees.

Our Board of Directors expects honest and ethical conduct from every employee. We strive to adhere to the highest ethical standards in the conduct of our business and to comply with all laws and regulations that are applicable to the business. Each employee has a responsibility to maintain and advance the ethical values of the Company. In support of this, our employees receive training to emphasize the importance of compliance with our Code of Conduct.

Where You Can Find More Information

The public may read and copy any materials that we file with the Securities and Exchange Commission (the “SEC”) on the SEC’s website at www.sec.gov. In addition, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and amendments to these reports are available free of charge to the public through our internet website at www.hexion.com under “Investor Relations - SEC Filings”. The content on any website referenced in this filing is not incorporated by reference into this filing unless expressly noted otherwise.

ITEM 1A - RISK FACTORS

(In millions, except share data)

Following are our principal risks. These factors may or may not occur, and we cannot express a view on the likelihood that any of these may occur. Other factors may exist that we do not consider significant based on information that is currently available or that we are not currently able to anticipate. Any of the following risks could materially adversely affect our business, financial condition or results of operations and prospects.

Risks Related to Our Business

If global economic conditions are weak or deteriorate, it will negatively impact our business operations, results of operations and financial condition.

Changes in global economic and financial market conditions could impact our business operations in a number of ways including, but not limited to, the following:

| |

| • | reduced demand in key customer segments, such as building, construction, wind energy, oil and gas, automotive and electronics, compared to prior years; |

| |

| • | weak economic conditions in our primary regions of operations: U.S., Europe, and Asia; |

| |

| • | payment delays by customers and reduced demand for our products caused by customer insolvencies and/or the inability of customers to obtain adequate financing to maintain operations |

| |

| • | insolvency of suppliers or the failure of suppliers to meet their commitments resulting in product delays; |

| |

| • | more onerous credit and commercial terms from our suppliers such as shortening the required payment period for outstanding accounts receivable or reducing or eliminating the amount of trade credit available to us; and |

| |

| • | potential delays in accessing our ABL Facility and the potential inability of one or more of the financial institutions included in our syndicated ABL Facility to fulfill their funding obligations. |

Many of our key customer segments are sensitive to macroeconomic conditions, which are currently uncertain. Accordingly, the short and long-term outlook for our business is difficult to predict and our results of operations could, as a result of this uncertainty, fall below our expectations.

Fluctuations in direct or indirect raw material costs could have an adverse impact on our business.

Raw materials costs made up approximately 75% of our cost of sales (excluding depreciation expense) in 2019. The prices of our direct and indirect raw materials have been, and we expect them to continue to be, volatile. If the cost of direct or indirect raw materials increases significantly and we are unable to offset the increased costs with higher selling prices, our profitability will decline. Increases in prices for our products could also hurt our ability to remain both competitive and profitable in the markets in which we compete.

Although some of our material contracts include competitive price clauses that allow us to buy outside the contract if market pricing falls below contract pricing, and certain contracts have minimum-maximum monthly volume commitments that allow us to take advantage of spot pricing, we may be unable to purchase raw materials at market prices. In addition, some of our customer contracts have fixed prices for a certain term, and as a result, we may not be able to pass on raw material price increases to our customers immediately, if at all. Due to differences in timing of the pricing trigger points between our sales and purchase contracts, there is often a “lead-lag” impact. In many cases this “lead-lag” impact can negatively impact our margins in the short term in periods of rising raw material prices and positively impact them in the short term in periods of falling raw material prices. Future raw material prices may be impacted by new laws or regulations, suppliers’ allocations to other purchasers, changes in our supplier manufacturing processes as some of our products are byproducts of these processes, interruptions in production by suppliers, natural disasters, volatility in the price of crude oil and related petrochemical products and changes in exchange rates.

An inadequate supply of direct or indirect raw materials and intermediate products could have a material adverse effect on our business.

Our manufacturing operations require adequate supplies of raw materials and intermediate products on a timely basis. The loss of a key source or a delay in shipments could have a material adverse effect on our business. Raw material availability may be subject to curtailment or change due to, among other things:

| |

| • | new or existing laws or regulations; |

| |

| • | suppliers’ allocations to other purchasers; |

| |

| • | interruptions in production by suppliers; and |

Many of our raw materials and intermediate products are available in the quantities we require from a limited number of suppliers. Should any of our key suppliers fail to deliver these raw materials or intermediate products to us or no longer supply us, we may be unable to purchase these materials in necessary quantities, which could adversely affect our volumes, or may not be able to purchase them at prices that would allow us to remain competitive. During the past several years, certain of our suppliers have experienced force majeure events rendering them unable to deliver all, or a portion of, the contracted-for raw materials. On these occasions, we have been forced to limit production or were forced to purchase replacement raw materials in the open market at significantly higher costs or place our customers on an allocation of our products. In the past, some of our customers have chosen to discontinue or decrease the use of our products as a result of these measures. We have experienced force majeure events by certain of our suppliers which have had significant negative impacts on our business. For example, over the past several years there have been various supply interruption events due to hurricanes, supplier production fires and other supply issues which have impacted our ability to obtain key raw materials. Additionally, we cannot predict whether new regulations or restrictions may be imposed in the future which may result in reduced supply or further increases in prices. We cannot assure investors that we will be able to renew our current materials contracts or enter into replacement contracts on commercially acceptable terms, or at all. Fluctuations in the price of these or other raw materials or intermediate products, the loss of a key source of supply or any delay in the supply could result in a material adverse effect on our business.

Our production facilities are subject to significant operating hazards which could cause environmental contamination, personal injury and loss of life, and severe damage to, or destruction of, property and equipment.

Our production facilities are subject to hazards associated with the manufacturing, handling, storage and transportation of chemical materials and products, including human exposure to hazardous substances, pipeline and equipment leaks and ruptures, explosions, fires, inclement weather and natural disasters, mechanical failures, unscheduled downtime, transportation interruptions, remedial complications, chemical spills, discharges or releases of toxic or hazardous substances or gases, storage tank leaks and other environmental risks. Additionally, a number of our operations are adjacent to operations of independent entities that engage in hazardous and potentially dangerous activities. Our operations or adjacent operations could result in personal injury or loss of life, severe damage to or destruction of property or equipment, environmental damage, or a loss of the use of all or a portion of one of our key manufacturing facilities. Such events at our facilities, or adjacent third-party facilities, could have a material adverse effect on us.

We may incur losses beyond the limits or coverage of our insurance policies for liabilities that are associated with these hazards. In addition, various kinds of insurance for companies in the chemical industry have not been available on commercially acceptable terms, or, in some cases, have been unavailable altogether. In the future, we may not be able to obtain coverage at current levels, and our premiums may increase significantly on coverage that we maintain.

Environmental obligations and liabilities could have a substantial negative impact on our financial condition, cash flows and profitability.

Our operations involve the use, handling, processing, storage, transportation and disposal of hazardous materials and are subject to extensive and complex U.S. federal, state, local and non-U.S. supranational, national, provincial, and local environmental, health and safety laws and regulations. These environmental laws and regulations include those that govern the discharge of pollutants into the air and water, the generation, use, storage, transportation, treatment and disposal of hazardous materials and wastes, the cleanup of contaminated sites, occupational health and safety and those requiring permits, licenses, or other government approvals for specified operations or activities. Our products are also subject to a variety of international, national, regional, state, and provincial requirements and restrictions applicable to the manufacture, import, export or subsequent use of such products. In addition, we are required to maintain, and may be required to obtain in the future, environmental, health and safety permits, licenses, or government approvals to continue current operations at most of our manufacturing and research facilities throughout the world.

Compliance with environmental, health and safety laws and regulations, and maintenance of permits, can be costly and complex, and we have incurred and will continue to incur costs, including capital expenditures and costs associated with the issuance and maintenance of letters of credit, to comply with these requirements. In 2019, we incurred capital expenditures of $20 to comply with environmental, health and safety laws and regulations and to make other environmental improvements. If we are unable to comply with environmental, health and safety laws and regulations, or maintain our permits, we could incur substantial costs, including fines and civil or criminal sanctions, third party property damage or personal injury claims or costs associated with upgrades to our facilities or changes in our manufacturing processes in order to achieve and maintain compliance, and may also be required to halt permitted activities or operations until any necessary permits can be obtained or complied with, or decide to close the impacted facility. In addition, future developments or increasingly stringent regulations could require us to make additional unforeseen environmental expenditures, which could have a material adverse effect on our business.

Environmental, health and safety requirements change frequently and have tended to become more stringent over time. We cannot predict what environmental, health and safety laws and regulations or permit requirements will be enacted or amended in the future, how existing or future laws or regulations will be interpreted or enforced or the impact of such laws, regulations or permits on future production expenditures, supply chain or sales. Our costs of compliance with current and future environmental, health and safety requirements could be material. Such future requirements include legislation designed to reduce emissions of carbon dioxide and other substances associated with climate change (“greenhouse gases”). The European Union has enacted greenhouse gas emissions legislation and continues to expand the scope of such legislation. The U.S. Environmental Protection Agency (the “USEPA”) has promulgated regulations applicable to projects involving greenhouse gas emissions above a certain threshold, and the United States and certain states within the United States have enacted, or are considering, limitations on greenhouse gas emissions. These requirements to limit greenhouse gas emissions could significantly increase our energy costs, and may also require us to incur material capital costs to modify our manufacturing facilities.

In addition, we are subject to liability associated with hazardous substances in soil, groundwater and elsewhere at a number of sites. These include sites that we formerly owned or operated and sites where hazardous wastes and other substances from our current and former facilities and operations have been sent, treated, stored, or recycled or disposed of, as well as sites that we currently own or operate. Depending upon the circumstances, our liability may be strict, joint and several, meaning that we may be held responsible for more than our proportionate share, or even all, of the liability involved regardless of our fault or whether we are aware of the conditions giving rise to the liability. Even where liability has been allocated among parties, we may be subject to material changes in such allocation in the future for a number of reasons, including the discovery of new contamination, the insolvency of a responsible party, or a heightened nexus to the remediation site. Environmental conditions at these sites can lead to environmental cleanup liability and claims against us for personal injury or wrongful death, property damages and natural resource damages, as well as to claims and obligations for the investigation and cleanup of environmental conditions. The extent of any of these liabilities is difficult to predict, but in the aggregate such liabilities could be material.

We have been notified that we are or may be responsible for environmental remediation at a number of sites in North America, Europe and South America. We are also performing a number of voluntary cleanups. The most significant sites at which we are performing or participating in environmental remediation are sites formerly owned by us in Geismar, Louisiana and Plant City, Florida. As the result of former, current or future operations, there may be additional environmental remediation or restoration liabilities or claims of personal injury by employees or members of the public due to exposure or alleged exposure to hazardous materials in connection with our operations, properties or products. Sites sold by us in past years may have significant site closure or remediation costs and our share, if any, may be unknown to us at this time. These environmental liabilities or obligations, or any that may arise or become known to us in the future, could have a material adverse effect on our financial condition, cash flows and profitability.

Future chemical regulatory actions may decrease our profitability.

Several governmental agencies have enacted, are considering or may consider in the future, regulations that may impact our ability to sell certain chemical products in certain geographic areas. The European Registration, Evaluation and Authorization of Chemicals (“REACH”) regulation requires manufacturers, importers and consumers of certain chemicals manufactured in, or imported into, the European Union to register such chemicals and evaluate their potential impacts on human health and the environment. REACH may result in certain chemicals being further regulated, restricted or banned from use in the European Union. In addition, the Frank R. Lautenberg Chemical Safety for the 21st Century Act (“LCSA”) was signed into law on June 22, 2016, and updates and revises the Toxic Substances Control Act. LCSA requires the implementing agency to conduct risk evaluations on high priority chemicals, which could include chemical products we manufacture. Other countries have implemented, or are considering implementation of, similar chemical regulatory programs. When fully implemented, REACH, LCSA and other similar regulatory programs may result in significant adverse market impacts on the affected chemical products. If we fail to comply with REACH, LCSA or other similar laws and regulations, we may be subject to penalties or other enforcement actions, including fines, injunctions, recalls or seizures, which would have a material adverse effect on our financial condition, cash flows and profitability. Additionally, studies conducted in association with these regulatory programs, or otherwise conducted through trade associations, may result in new information regarding the health effects and environmental impact of our products and raw materials. Such studies could result in future regulations restricting the manufacture or use of our products, liability for adverse environmental or health effects linked to our products, and/or de-selection of our products for specific applications. These restrictions, liability, and product de-selection could have a material adverse effect on our business, our financial condition and/or liquidity.

Because of certain government public health agencies’ concerns regarding the potential for adverse human health effects, formaldehyde is a regulated chemical and public health agencies continue to evaluate its safety. A division of the World Health Organization, the International Agency for Research on Cancer, or IARC, and the National Toxicology Program, or NTP, within the U.S. Department of Health and Human Services, have classified formaldehyde as being carcinogenic to humans. The USEPA, under its Integrated Risk Information System, or IRIS, released a draft of its toxicological review of formaldehyde in 2010, stating that formaldehyde meets the criteria to be described as “carcinogenic to humans.” The National Academy of Sciences peer reviewed the draft IRIS toxicological review and issued a report in April 2011 that criticized the draft IRIS toxicological review and stated that the methodologies and the underlying science used in the draft IRIS review did not clearly support a conclusion of a causal link between formaldehyde exposure and leukemia. USEPA may or may not issue a revised draft IRIS toxicological review to reflect the NAS findings, including the conclusions regarding a causal link between formaldehyde exposure and leukemia. On March 20, 2019, EPA announced the next set of candidate chemical substances that will undergo review by its LCSA/TSCA risk evaluation program. This announcement formally begins the prioritization process and starts a 9-to-12 month statutory time frame during which the Agency must designate 20 chemical substances as high priority. Formaldehyde was identified as a high-priority candidate chemical for TSCA risk evaluation. Designation of formaldehyde as a high-priority chemical “does not constitute a finding of risk.” A high-priority designation means the EPA has nominated formaldehyde for further risk evaluation. Effective January 1, 2016, ECHA classified formaldehyde as a Category 2 Mutagen, but rejected reclassification as a Category 1A Carcinogen. It is possible that new regulatory requirements could be promulgated to limit human exposure to formaldehyde, that we could incur substantial additional costs to meet any such regulatory requirements, and that there could be a reduction in demand for our formaldehyde-based products. These additional costs and reduced demand could have a material adverse effect on our operations and profitability.

BPA, which is manufactured and used as an intermediate at our Deer Park, Texas and Pernis, Netherlands manufacturing facilities, and is also sold directly to third parties, is currently considered under certain state and international regulatory programs as a reproductive toxicant and an “endocrine disrupter,” meaning BPA could disrupt normal biological processes. BPA continues to be subject to scientific, regulatory and legislative review and negative media attention. In Europe, the EU Committee for Risk Assessment adopted an opinion to change the existing harmonized classification and labeling of BPA from a category 2 reproductive Toxicant to a category 1B reproductive Toxicant. This classification change was effective beginning March 1, 2018. The EU Member State Committee agreed to add BPA to the Substance of Very High Concern (“SVHC”) candidate list based upon its classification as a reproductive toxicant, as well as for its endocrine disrupting properties to both human health and the environment. The REACH Risk Management Option Analysis (RMOA) was released July 6, 2017, in which BPA is identified as

an endocrine disruptor for the environment with no safe threshold, and REACH restrictions are identified as the preferred risk management measure. The California Environmental Protection Agency’s Office of Environmental Health Hazard Assessment (“OEHHA”) listed BPA under Proposition 65 as a developmental and reproductive toxicant, requiring warning labels unless BPA exposures are shown to be less than a risk-based level (the maximum allowable dose level (“MADL”)). As of May 11, 2016, products containing BPA sold into California must comply with Proposition 65’s requirements. Despite these hazard designations and listings, the US Food and Drug Administration (“FDA”) is also actively engaged in the scientific and regulatory review of BPA and, in a letter submitted to OEHHA dated April 6, 2015, reaffirmed that BPA is safe as currently permitted in FDA-regulated food contact uses and concluded that FDA’s National Center for Toxicological Research study did not support the listing of BPA as a reproductive toxicant. In 2018, NTP released the results of the CLARITY Core Study. Senior scientists at FDA’s National Center for Toxicological Research (NCTR) conducted the study with funding from NTP. The study involved exposure of laboratory animals to BPA beginning and during pregnancy and continuing in the offspring throughout their entire lifetime. A wide range of dose levels were examined, from low doses close to actual consumer exposure to doses about 250,000 times higher. As stated in the conclusion of the study report, “BPA produced minimal effects that were distinguishable from background.” NTP selected a panel of six independent expert scientists to conduct a formal peer review of the study. In general, the peer review panel supported the design and conduct of the study and agreed with the overall conclusion that the study found minimal effects for the range of doses studied. In December 2012, France enacted a law that bans direct contact of packaging containing BPA with food and consumer products. In January 2015, the European Food Safety Authority (“EFSA”) concluded that BPA poses no health risk to consumers of any age group (including unborn children, infants and adolescents) at currently permitted exposure levels. EFSA confirmed this conclusion in October 2016. Regulatory and legislative initiatives such as these, or product de-selection resulting from such regulatory actions, may result in a reduction in demand for BPA and our products containing BPA and could also result in additional liabilities as well as an increase in operating costs to meet more stringent regulations. Such increases in operating costs and/or reduction in demand could have a material adverse effect on our operations and profitability.

Scientists periodically conduct studies on the potential human health and environmental impacts of chemicals, including products we manufacture and sell. Also, nongovernmental advocacy organizations and individuals periodically issue public statements alleging human health and environmental impacts of chemicals, including products we manufacture and sell. Based upon such studies or public statements, our customers may elect to discontinue the purchase and use of our products, even in the absence of any government regulation. Such actions could significantly decrease the demand for our products and, accordingly, have a material adverse effect on our business, financial condition, cash flows and profitability.

We are subject to certain risks related to litigation filed by or against us, and adverse results may harm our business.

We cannot predict with certainty the cost of defense, of prosecution or of the ultimate outcome of litigation and other proceedings filed by or against us, including penalties or other civil or criminal sanctions, or remedies or damage awards, and adverse results in any litigation and other proceedings may materially harm our business. Litigation and other proceedings may include, but are not limited to, actions relating to intellectual property, international trade, commercial arrangements, product liability, environmental, health and safety, joint venture agreements, labor and employment or other harms resulting from the actions of individuals or entities outside of our control. In the case of intellectual property litigation and proceedings, adverse outcomes could include the cancellation, invalidation or other loss of material intellectual property rights used in our business and injunctions prohibiting our use of business processes or technology that are subject to third-party patents or other third-party intellectual property rights. Litigation based on environmental matters or exposure to hazardous substances in the workplace or based upon the use of our products could result in significant liability for us, which could have a material adverse effect on our business, financial condition and/or profitability.

Because we manufacture and use materials that are known to be hazardous, we are subject to, or affected by, certain product and manufacturing regulations, for which compliance can be costly and time consuming. In addition, we may be subject to personal injury or product liability claims as a result of human exposure to such hazardous materials.

We produce hazardous chemicals that require care in handling and use that are subject to regulation by many U.S. and non-U.S. national, supra-national, state and local governmental authorities. In some circumstances, these authorities must review and, in some cases approve, our products and/or manufacturing processes and facilities before we may manufacture and sell some of these chemicals. To be able to manufacture and sell certain new chemical products, we may be required, among other things, to demonstrate to the relevant authority that the product does not pose an unreasonable risk during its intended uses and/or that we are capable of manufacturing the product in compliance with current regulations. The process of seeking any necessary approvals can be costly, time consuming and subject to unanticipated and significant delays. Approvals may not be granted to us on a timely basis, or at all. Any delay in obtaining, or any failure to obtain or maintain, these approvals would adversely affect our ability to introduce new products and to generate revenue from those products. New laws and regulations may be introduced in the future that could result in additional compliance costs, bans on product sales or use, seizures, confiscation, recall or monetary fines, any of which could prevent or inhibit the development, distribution or sale of our products and could increase our customers’ efforts to find less hazardous substitutes for our products. We are subject to ongoing reviews of our products and manufacturing processes.

As discussed above, we manufacture and sell products containing formaldehyde, and certain governmental bodies have stated that there is a causal link between formaldehyde exposure and certain types of cancer, including myeloid leukemia and NPC. These conclusions could adversely impact our business and also become the basis of product liability litigation.

Other products we have made or used have been and could be the focus of legal claims based upon allegations of harm to human health. While we cannot predict the outcome of pending suits and claims, we believe that we maintain adequate reserves, in accordance with our policy, to address currently pending litigation and are adequately insured to cover currently pending and foreseeable future claims. However, an unfavorable outcome in these litigation matters could have a material adverse effect on our business, financial condition and/or profitability and cause our reputation to decline.

We are subject to claims from our customers and their employees, environmental action groups and neighbors living near our production facilities.

We produce and use hazardous chemicals that require appropriate procedures and care to be used in handling them or in using them to manufacture other products. As a result of the hazardous nature of some of the products we produce and use, we may face claims relating to incidents that involve our customers’ improper handling, storage and use of our products. We have historically faced lawsuits, including class action lawsuits that claim liability for death, injury or property damage caused by products that we manufacture or that contain our components. Additionally, we may face lawsuits alleging personal injury or property damage by neighbors living near our production facilities. These lawsuits, and any future lawsuits, could result in substantial damage awards against us, which in turn could encourage additional lawsuits and could cause us to incur significant legal fees to defend such lawsuits, either of which could have a material adverse effect on our business, financial condition and/or profitability. In addition, the activities of environmental action groups could result in litigation or damage to our reputation.

Our manufacturing facilities are subject to disruption due to operating hazards

The storage, handling, manufacturing and transportation of chemicals at our facilities and adjacent facilities could result in leaks, spills, fires or explosions, which could result in production downtime, production delays, raw material supply delays, interruptions and environmental hazards. We have experienced incidents at our own facilities and a raw material supplier located adjacent to our facility that have resulted mostly in short term, but some long term, production delays. Production interruption may also result from severe weather, particularly with respect to our southern U.S. operations near the Gulf Coast. Production lapses caused by any such delays can often be absorbed by our other manufacturing facilities, and we maintain insurance to cover such potential events. However, such events could negatively affect our operations.

As a global business, we are subject to numerous risks associated with our international operations that could have a material adverse effect on our business.

We have significant manufacturing and other operations outside the United States. Some of these operations are in jurisdictions with unstable political or economic conditions. There are numerous inherent risks in international operations, including, but not limited to:

| |

| • | exchange controls and currency restrictions; |

| |

| • | currency fluctuations and devaluations; |

| |

| • | tariffs and trade barriers imposed by the current U.S. administration or foreign governments; |

| |

| • | renegotiation of trade agreements by the current U.S. administration; |

| |

| • | export duties and quotas; |

| |

| • | changes in local economic conditions; |

| |

| • | changes in laws and regulations; |

| |

| • | exposure to possible expropriation or other government actions; |

| |

| • | acts by national or regional banks, including the European Central Bank, to increase or restrict the availability of credit; |

| |

| • | hostility from local populations; |

| |

| • | diminished ability to legally enforce our contractual rights in non-U.S. countries; |

| |

| • | restrictions on our ability to repatriate dividends from our subsidiaries; and |

| |

| • | unsettled political conditions and possible terrorist attacks against U.S. interests. |

Our international operations expose us to different local political and business risks and challenges. For example, we may face potential difficulties in staffing and managing local operations, and we may have to design local solutions to manage credit risks of local customers and distributors. In addition, some of our operations are located in regions that may be politically unstable, having particular exposure to riots, civil commotion or civil unrests, acts of war (declared or undeclared) or armed hostilities or other national or international calamity. In some of these regions, our status as a U.S. company also exposes us to increased risk of sabotage, terrorist attacks, interference by civil or military authorities or to greater impact from the national and global military, diplomatic and financial response to any future attacks or other threats.

In addition, intellectual property rights may be more difficult to enforce in non-U.S. or non-Western European countries.

If global economic and market conditions, or economic conditions in Europe, China, Brazil, Australia, the United States or other key markets remain uncertain or deteriorate further, the value of associated foreign currencies and the global credit markets may weaken. Additionally, general financial instability in countries where we do not transact a significant amount of business could have a contagion effect and contribute to the general instability and uncertainty within a particular region or globally. If this were to occur, it could adversely affect our customers and suppliers and in turn have a materially adverse effect on our international business and results of operations.