QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on May 7, 2004

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

Form S-1

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

BORDEN CHEMICAL, INC.

(Exact name of registrant as specified in its charter)

| New Jersey | 2821 | 13-0511250 | ||

| (Jurisdiction of incorporation | (Primary Standard Industrial | (I.R.S. Employer | ||

| or organization) | Classification Code Number) | Identification Number) | ||

180 East Broad Street Columbus, Ohio 43215 (614) 225-4000 | ||||

| (Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices) | ||||

Nancy G. Brown, Esq.

180 East Broad Street

Columbus, Ohio 43215

(614) 225-4000

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

| John B. Tehan, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 (212) 455-2000 | Kris F. Heinzelman, Esq. Cravath, Swaine & Moore LLP Worldwide Plaza 825 Eighth Avenue New York, New York 10019 (212) 474-1000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and the list Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be registered | Amount To Be Registered | Proposed Maximum Offering Price Per Unit | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee | ||||

|---|---|---|---|---|---|---|---|---|

| Common Stock, par value $0.01 per share | — | — | $200,000,000 | $25,340 | ||||

- (1)

- Estimated solely for the purpose of calculating the amount of the registration fee pursuant to Rule 457(o) under the Securities Act.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until this registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and we are not soliciting offers to buy these securities, in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED MAY 7, 2004

Shares

Borden Chemical, Inc.

Common Stock

The shares of common stock are being sold by the selling shareholder described in this prospectus. We will not receive any of the proceeds from the shares of common stock sold in this offering.

Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be between $ and $ per share. We will apply to list our common stock on The New York Stock Exchange under the symbol "BCI."

The underwriters have an option to purchase a maximum of additional shares from the selling shareholder to cover over-allotments of shares.

Investing in our common stock involves risks. See "Risk Factors" beginning on page 10.

| | Price to Public | Underwriting Discounts and Commissions | Proceeds to Selling Shareholder | ||||||

|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | ||||||

| Total | $ | $ | $ | ||||||

Delivery of the shares of common stock will be made on or about , 2004.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse First Boston | Morgan Stanley | |

| Lehman Brothers | UBS Investment Bank | |

The date of this prospectus is , 2004.

| Prospectus Summary | 1 | |

| Risk Factors | 10 | |

| Cautionary Statement Concerning Forward-Looking Statements | 25 | |

| Use of Proceeds | 26 | |

| Dividend Policy | 26 | |

| Capitalization | 27 | |

| Dilution | 28 | |

| Selected Historical Financial Data | 29 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 32 | |

| Business | 53 | |

| Management | 69 | |

| Principal and Selling Shareholder | 78 | |

| Certain Relationships and Related Party Transactions | 79 | |

| Description of Capital Stock | 82 | |

| Common Stock Eligible for Future Sale | 83 | |

| Description of Indebtedness | 84 | |

| Certain U.S. Federal Tax Consequences for Non-U.S. Holders | 88 | |

| Underwriting | 90 | |

| Notice to Canadian Residents | 93 | |

| Legal Matters | 94 | |

| Experts | 94 | |

| Where You Can Find More Information | 94 | |

| Glossary | G-1 | |

| Index to Consolidated Financial Statements | F-1 |

You should rely only on the information contained in this document or to which we have referred you. We have not authorized anyone to provide you with information that is different. This document may only be used where it is legal to sell these securities. The information in this document may only be accurate on the date of this document.

This prospectus includes industry data and forecasts that we obtained from industry publications and surveys and internal company surveys. Industry publications and surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable, but we cannot assure you as to the accuracy or completeness of included information. We have not independently verified any of the data from third-party sources nor have we ascertained the underlying economic assumptions relied upon therein. Similarly, internal company surveys, industry forecasts and market research, which we believe to be reliable, based upon management's knowledge of the industry, have not been verified by any independent sources.

Dealer Prospectus Delivery Obligation

Until , 2004 (25 days after commencement of the offering), all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers' obligation to deliver a prospectus when acting as underwriters and with respect to unsold allotments or subscriptions.

i

This summary highlights information about Borden Chemical, Inc. and the offering contained elsewhere in this prospectus. It is not complete and may not contain all the information that may be important to you. You should carefully read the entire prospectus before making an investment decision, especially the information presented under the heading "Risk Factors." In this prospectus, all references to "Borden Chemical," "the Company," "we," "us" and "our" refer to Borden Chemical, Inc., its subsidiaries and HA International, LLC, unless the context otherwise requires or where otherwise indicated. You should also see the "Glossary" for definitions of some of the terms used to describe our business and industry.

Overview

We are one of the world's leading integrated producers of thermoset resins, adhesives and binders for the global forest products and industrial markets. In addition, we are the world's largest producer by volume of formaldehyde, an important and versatile building block chemical used in a wide variety of applications. We are the largest North American producer by volume of thermoset resins used in the production of engineered wood products, including structural wood panels, beams and non-structural panels, furniture, door and window assemblies and wallboards. We are also the largest North American producer by volume of resin-coated proppant systems, which are used in oilfield and natural gas production, and of foundry resins, which are used in the production of cores and molds for metal castings. We have a strong presence in the production of both specialty resins used in industrial markets and UV coatings for the production of fiber-optic cables, DVDs and CDs. Our materials are designed to deliver superior binding and bonding performance to manufacturers of thousands of common, everyday products that enhance modern living. Our strong position in North America is complemented by our significant operations in Latin America and Europe and expansion opportunities in Asia Pacific and Latin America.

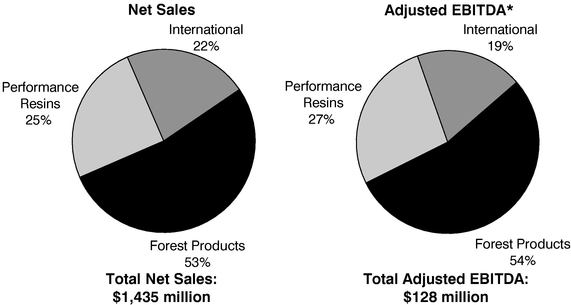

Through our worldwide network of 48 strategically located production facilities, we serve more than 3,000 customers, with our largest customer representing 5% of net sales in 2003. Our customers operate in many diverse end-markets, such as construction, furniture, automotive, oil and gas, chemicals, electronics, communications and agriculture. In 2003, we generated net sales of $1,435 million, Adjusted EBITDA (as defined) of $127.7 million, operating income of $66.5 million and net income of $23.0 million. In 2003, 63% of our net sales were derived from sales in the United States, 15% from Canada and 22% from Latin America, Europe and Asia Pacific.

Our Business

Our three reporting segments are (i) Forest Products, which includes the forest products resins and formaldehyde product lines produced in North America, (ii) Performance Resins, which includes the specialty resins, foundry resins, oilfield products and UV coatings product lines produced in North

1

America, and (iii) International, which includes all products produced outside of North America. The following is an illustration of our net sales and Adjusted EBITDA by reporting segment in 2003:

Net Sales and Adjusted EBITDA by Reporting Segment

* Percentages are calculated prior to allocation of corporate expenses.

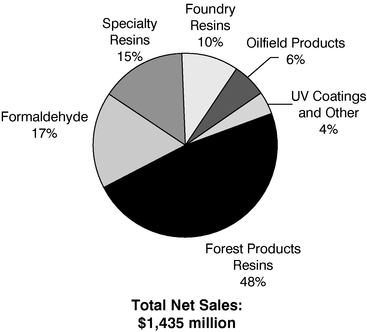

Our primary product lines include forest products resins, formaldehyde, specialty resins, foundry resins, oilfield products and UV coatings and other. Our net sales by product line for 2003 are illustrated below:

Forest Products Resins. We are the leading producer of forest products thermoset resins in North America with an approximate 46% market share by volume in urea formaldehyde resins, or UF resins, and an approximate 40% market share by volume in phenol formaldehyde resins, or PF resins. Our thermoset resin systems are used by our customers to bind wood particles and bond wood segments to provide strength and durability to oriented strand board, or OSB; particleboard; medium density fiberboard, or MDF; and plywood.

Formaldehyde. We are the world's largest producer of formaldehyde by volume and the largest provider of formaldehyde to end-users in North America with an approximate 59% share of the merchant market. We manufacture more than five billion pounds of formaldehyde solution each year, of which approximately half is consumed internally for resin production and the other half is sold to external customers. Formaldehyde is a versatile building block chemical used in thousands of diverse end-use applications such as resin systems for forest products and industrial bonding, household

2

products, including shampoo, cosmetics, disinfectants and fabric softeners, and specialty fabrics, paper products, fertilizers and animal feeds.

Specialty Resins. We are a major supplier of high performance specialty resins used in the binding and bonding of a diverse range of materials, primarily in the construction, automotive, electronics and steel industries. Typical end-use product applications include electronics for circuit boards, adhesives for brake linings and other friction products, flame-resistant composites for trains and planes, acoustical insulation for automobiles and glass matting for roofing shingles and thermal insulation.

Foundry Resins. Through our 75% economic interest in our joint venture HA International, LLC, which we refer to as HAI, we are the leading producer by volume of foundry resins in North America with an approximate 42% market share. We pioneered the development of thermoset resins as binders for sand cores and molds used in metal castings over 40 years ago and continue to serve the North American market with a broad distribution network and significant production capability. Our foundry resin manufacturing capabilities include the largest foundry resin plant in the United States, which is located in Louisville, Kentucky. Our foundry resin systems are used by major automotive and industrial companies in the production of engine blocks, transmissions, brake and drive train components and various other casting products.

Oilfield Products. We are the leading producer of oilfield resin systems and proppants in North America with an approximate 51% market share by volume. Our innovative flow back control technology allows oil and gas service providers to improve yields and extract oil and gas from deeper and more complex geological formations.

UV Coatings. We make coating and adhesive systems that utilize ultraviolet light-curing technology and have an approximate 21% global market share by volume. Our UV light-curable products are used in fiber optic cable, CDs, CD-ROMs, DVDs, electronics and other specialty applications. These materials play an important role in modern communications technology by enhancing durability and performance.

Industry

According to SRI Consulting, an independent industry consulting firm, the global chemicals industry is a $1.9 trillion market, divided into two primary markets: commodity chemicals and specialty chemicals. We are an important participant in both markets. We participate in the commodity chemicals market through our presence in the merchant formaldehyde market. We participate in the specialty chemicals market through our presence in thermoset resins, including our forest products resins, our resins serving the electronics and oil field services markets and our UV coatings products. The portion of the specialty chemicals market in which we participate is estimated at $6.4 billion globally. These products are principally sold on the basis of performance, technical support and service levels to customers and product innovation.

The principal factors contributing to success in the chemicals market vary between the specialty and commodity chemicals markets. Success in the specialty chemicals market is largely driven by (i) consistent delivery of high-quality products, (ii) advantageous production technologies, (iii) the ability to provide value to customers through both product attributes and strong technical support and service and (iv) a presence in large and growing markets. Success in the commodity chemicals market is largely driven by (i) large scale and high plant productivity, (ii) a low cost structure including cost-effective raw material procurement and (iii) strong customer relationships.

Competitive Strengths

- •

- Leading Market Positions. We are one of the world's leading producers of thermoset resins for the forest products and industrial markets. We believe that we have the number one or number

3

two market position in North America by volume in products accounting for virtually all our net sales. The following table illustrates our market position by volume in our key product areas:

| Product | Market | 2003 Market Position | Approximate Market Share | ||||

|---|---|---|---|---|---|---|---|

| Forest Products Resins | |||||||

| UF Resins | North America | 1 | 46% | ||||

| PF Resins | North America | 1 | 40% | ||||

| Merchant Formaldehyde | North America | 1 | 59% | ||||

| Industrial Resins | North America | 1 | 28% | ||||

| Foundry Resins | North America | 1 | 42% | ||||

| Oilfield Resins | North America | 1 | 51% | ||||

| UV Fiber-Optic Coatings | Global | 2 | 21% | ||||

- •

- Competitive Advantage in Thermoset Resins Business. We believe we enjoy a cost advantage in our thermoset resins business as a result of our manufacturing scale and vertical integration with our formaldehyde business. Formaldehyde accounts for an average of approximately 30% of the raw material costs of formaldehyde-based resins.

- •

- Strong Relationships with Our Customers. As a result of our focus on developing innovative, high-quality products with a high level of technical service, we have developed stable, long-term relationships with our customers on a global basis. Most of our resin customers require products that are tailored to their individual production needs and require a high degree of technical service and product reformulation. We have a total systems approach to meeting customer needs. This approach involves using our global technology and experience in order to deliver the appropriate resin for the customer's application and production process and subsequently providing ongoing in-plant technical support and service. We believe that this represents a competitive advantage and contributes to our reputation as the world's leading supplier of thermoset resins.

- •

- Low Cost Position Through Scale and Strategically Located Plants. We believe that we are North America's lowest cost producer of formaldehyde and formaldehyde-based resins. Our cost advantage in formaldehyde is a result of our manufacturing technology and leading global market position, which allow us to utilize our plants more efficiently and source raw materials at lower prices. Most of our manufacturing plants are strategically located close to, or linked with, our customers' manufacturing facilities. This allows us a significant logistical advantage since formaldehyde cannot be cost-effectively transported long distances.

- •

- Diversified Revenue Base. We have a diversified revenue and customer base in a variety of end-markets and geographies, which reduces our exposure to economic, industry and commodity chemical cycles. In 2003, our largest customer accounted for 5% of our net sales and our top ten customers accounted for 27% of our net sales. We sell our products into numerous end-markets including construction, furniture, automotive, oilfield services, chemicals, electronics, communications and steel production. Our largest end-market is construction, which accounted for approximately 35% of our net sales in 2003. Because demand for our products is driven by both new housing starts and the home remodeling and repair market, we have been able to maintain our net sales volumes of forest products resins during periods of declining housing starts.

- •

- Well Positioned for Improving Raw Material Pricing Environment. We have recently experienced dramatically higher raw material costs. For example, in 2003, the prices of methanol, phenol and urea increased by 42%, 22% and 50%, respectively. However, we are typically able to pass along raw material price increases, albeit with a "lag," which leads to lower margins during periods of rapidly increasing raw material prices and higher margins during periods of rapidly decreasing raw material prices. We believe that our recent operating performance in a

4

- •

- Favorable Trends in Forest Products Resin Demand. As a result of the scarcity of "mature growth" forests in North America and Europe, there is a continuing shift away from plywood to OSB, a plywood substitute that uses less wood. This trend has been driving demand for our products because manufacturing of OSB uses approximately 50% more of our resins than plywood.

- •

- Strong Management Team. We have a new management team led by Craig O. Morrison, who was appointed President and Chief Executive Officer on March 25, 2002. Subsequently, nine of the eleven members of our senior management team joined the Company. This has significantly expanded the capability and capacity of the management team. Initiatives introduced by this management team, such as Six Sigma, new product development, assessment processes and global product line management, are beginning to have a positive impact on our financial results.

difficult raw material environment positions us to capitalize on what we believe generally will be an improving raw material pricing environment.

Strategy

We are focused on increasing shareholder value, our return on investment, cash flows and profitability. We believe we can achieve these goals through the following strategies:

- •

- Expand Our Global Reach. We will continue to grow internationally by expanding our product sales to our multi-national customers outside of North America and by entering new markets. In particular, we believe that our leading formaldehyde and formaldehyde-based resin technology and our relationships with large multi-national customers as a "supplier of choice" of formaldehyde offers us a significant competitive advantage as we enter new markets. We are particularly focused on growing our business in the Asian-Pacific and Latin American markets, where the usage of our products is increasing. For example, having recently targeted Brazil as a growth market, our volumes in that country have grown by 35% from 2001 to 2003 and Adjusted EBITDA has grown to $15 million. In China, we have initiated three joint ventures and have two plants under construction in order to expand our operations for forest products, formaldehyde and UV coating.

- •

- Develop and Market New Products. We will continue to expand our product offerings through internal product innovation, joint research and development initiatives with our customers and research partnership formations. In 2003, approximately 15% of our net sales were derived from products developed or re-engineered within the last three years. We have implemented a new, systematic approach to new product development and have identified promising new technologies that have begun to yield significant results. In 2003, we introduced new materials in all of our product lines. For example, last year we developed and began marketing XRT™, a resin for the oilfield products end-market, which generated $10 million in net sales in 2003. We also have increased our investments in UV light-curable products for the display, CD and ink jet markets and electronics products for the photolithography market.

- •

- Focus on Operational Excellence. We will continue to focus on opportunities to optimize our resources, improve our cost position and drive new product innovation. In 2002, we implemented a major Six Sigma process initiative, which is adding discipline and focus to the way we approach productivity. Since the beginning of 2002, our average productivity per employee has increased by approximately 25%.

- •

- Pursue Targeted Add-On Acquisitions and Joint Ventures. We intend to continue pursuing add-on acquisitions and joint ventures in areas that allow us to build upon our core strengths, expand our product portfolio and better serve our customers. For example, during 2003 we spent a total of $14.7 million for the acquisition of an international manufacturer of specialty chemical products and for the acquisition of the assets of a domestic producer of specialty adhesives.

5

Recent Developments

On May 6, 2004, we reported net income of $4.9 million for the first quarter ended March 31, 2004, compared with a first quarter 2003 loss of $3.4 million. Operating income for the quarter rose to $20.8 million, up 189% from $7.2 million recorded in the prior year period. Results for the quarter were driven by strong sales volumes, reduced expenses due to productivity initiatives and favorable product mix.

Net sales for the period totaled $385.4 million, up 10% from first quarter 2003 sales of $349.3 million as a result of increased sales volumes, higher selling prices, favorable product mix and the positive impact of foreign currency translation.

Sales volumes for the quarter increased 4% as compared to the prior year period, with growth across most major segments. A recovering domestic economy, continued strength in construction markets and improved results from international operations all contributed to the sales volume increase.

Our efforts to reduce costs and improve productivity were reflected in a reduction in general and administrative expenses for the quarter of more than $6.0 million compared to last year's period. Gross margins improved to 19.7% from 18.8% in the previous year period as we were able to recover higher costs for the key raw materials of methanol, phenol and urea, and benefited from growth in higher margin business segments. Adjusted EBITDA was $34.8 million, a 71% improvement over the first quarter of 2003.

Forest Products net sales increased $15.9 million or 8.9% in the first quarter of 2004 compared to the first quarter of 2003, while Adjusted EBITDA was up $5.6 million, or 31%. The sales increase resulted from improved volumes driven by the strong construction market, improved pricing reflecting strong demand for PF resins and favorable foreign currency translation due to the stronger Canadian dollar as compared to the U.S. dollar. The Adjusted EBITDA increase reflects improved volumes and the positive impact of a realignment program announced in June 2003, which we refer to as the 2003 Realignment. Higher selling prices and improved margins also contributed to the Adjusted EBITDA increase.

Performance Resins net sales increased $6.4 million, or 6.7%, in the first quarter of 2004 compared to 2003. Increased drilling activity and improved conditions in the non-automotive castings sector drove improved volumes in the oilfield and foundry businesses, respectively. Adjusted EBITDA increased $0.2 million, or 2.1%, as increased processing costs and investments supporting geographic expansion and new product development substantially offset the positive earnings impact of the increased volume.

International net sales increased $13.7 million, or 18.4%, in the first quarter of 2004 compared to the first quarter of 2003. The positive impact of foreign currency translation, the 2003 acquisition of Fentak Pty. Ltd., or Fentak, and improved volumes in the Latin American forest products sector were the key drivers. Adjusted EBITDA increased $0.5 million, or 6.4%, reflecting improved volumes and favorable product mix.

Our History

We were incorporated in 1899. In 1995, when certain affiliates of Kohlberg Kravis Roberts & Co. L.P., or KKR, acquired control of the Company (then known as Borden, Inc.), our businesses consisted of the following business segments: Chemical, Foods, Other Consumer Products (including Consumer Adhesives), Decorative Products, Dairy and businesses held for sale. We sold all of these business segments, except for the Chemical segment, by the end of 2001.

Our principal executive offices are located at 180 East Broad Street, Columbus, Ohio 43215. Our telephone number is (614) 225-4000. We maintain a website at www.bordenchem.com where general information about our business is available. The information contained on our website is not a part of this prospectus.

6

| Common stock offered by the Selling Shareholder(1)(2) | shares | |

Common stock to be outstanding after this offering(3) | shares | |

Use of proceeds | We will not receive any of the proceeds from the sale of shares of our common stock sold in this offering. The Selling Shareholder will receive all net proceeds from the sale of shares of our common stock in this offering. | |

Dividend policy | We currently intend to pay quarterly dividends on our common stock. See "Dividend Policy." | |

Proposed New York Stock Exchange trading symbol | "BCI" | |

Risk factors | You should carefully read and consider the information set forth under the caption "Risk Factors" and all other information set forth in this prospectus before investing in our common stock. |

- (1)

- The Selling Shareholder is Borden Holdings, LLC, an affiliate of KKR. See "Principal and Selling Shareholder."

- (2)

- Except as otherwise indicated, all information in this prospectus assumes:

- •

- no exercise of the underwriters' over-allotment option and

- •

- a for share exchange, which will occur prior to the closing of this offering.

- (3)

- Assuming that the underwriters' over-allotment option is not exercised, the aggregate number of shares of common stock that will be outstanding after this offering is comprised of shares held by the Selling Shareholder, shares sold in this offering and shares held by our directors, officers and employees. This number excludes:

- •

- shares of our common stock with a weighted average exercise price of $ per share, issuable upon exercise of outstanding stock options; and

- •

- shares of our common stock reserved for future issuances under our existing employee and director compensation plans.

7

Summary Historical Financial Data

The following tables summarize certain of our historical financial data. The summary historical consolidated financial information as of December 31, 2003 and 2002 and for each of the three years in the period ended December 31, 2003 has been derived from, and should be read in conjunction with, our audited Consolidated Financial Statements and the related notes included elsewhere in this prospectus as well as "Management Discussion and Analysis of Financial Condition and Results of Operations." The consolidated financial information as of December 31, 2001 is not included in this prospectus.

| | Year ended December 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | |||||||||

| | (in thousands, except per share data) | |||||||||||

| Consolidated Statement of Operations:(1) | ||||||||||||

| Net sales | $ | 1,434,813 | $ | 1,247,885 | $ | 1,372,141 | ||||||

| Gross margin(2) | 286,294 | 279,228 | 311,499 | |||||||||

| Operating income (loss) | 66,542 | 33,708 | (75,495 | ) | ||||||||

| Net income (loss) | 22,976 | (36,583 | ) | (124,800 | ) | |||||||

| Preferred stock dividends | — | — | (61,846 | ) | ||||||||

| Net income (loss) applicable to common stock | 22,976 | (36,583 | ) | (186,646 | ) | |||||||

Common and Preferred Share Data: | ||||||||||||

| Earnings (loss) per share:(3) | ||||||||||||

| Basic and diluted from continuing operations | $ | 0.11 | $ | (0.03 | ) | $ | (0.69 | ) | ||||

| Basic and diluted | 0.11 | (0.18 | ) | (0.94 | ) | |||||||

| Dividends per: | ||||||||||||

| Common share | $ | — | $ | — | $ | 0.18 | ||||||

| Series A Preferred share | — | — | 2.52 | |||||||||

| Weighted average common shares outstanding: | ||||||||||||

| Basic | 200,898 | 200,458 | 198,997 | |||||||||

| Diluted | 200,924 | 200,458 | 198,997 | |||||||||

Other Data: | ||||||||||||

| Adjusted EBITDA(4) | $ | 127,746 | $ | 121,726 | $ | 139,215 | ||||||

| Cash flows from operating activities | 34,026 | 10,360 | 95,120 | |||||||||

| Capital expenditures | 41,820 | 38,773 | 47,408 | |||||||||

Consolidated Balance Sheet Data (at period end):(1) | ||||||||||||

| Total assets | $ | 993,866 | $ | 1,011,780 | $ | 1,123,278 | ||||||

| Total long-term debt | 529,966 | 523,287 | 532,497 | |||||||||

| Total liabilities | 1,090,059 | 1,172,673 | 1,220,583 | |||||||||

| Total shareholders' equity (deficit) | (96,193 | ) | (160,893 | ) | (97,305 | ) | ||||||

- (1)

- Operating results in 2003 include $4,748 in business realignment and impairment expense. Operating results in 2002 include $19,699 in business realignment and impairment expense consisting principally of $12,584 in plant closure costs, $3,265 in severance and $6,315 in non-cash impairment expense offset by a gain of $2,465 on the sale of a closed facility. Operating results in 2001 include $126,408 in business realignment and impairment expense consisting principally of $98,163 in impairment charges for our melamine crystal business that was shut down in early 2002, $23,285 in plant closure costs and $12,582 in severance offset by a gain of $10,507 on the sale of a closed facility. Also in 2001, we discontinued construction of a new plant and recorded a charge of $2,885. Our 2001 results also include $27,000 in impairment expense related to investments in and receivables from affiliates. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Adjustments to EBITDA."

- (2)

- Gross margin is calculated by deducting the cost of raw materials and processing from the amount of net sales. Costs of distributing the product to the final customer are separately reported as a distribution expense. Because not all companies use identical calculations, this presentation of gross margin may not be comparable to other similarly titled measures presented by other companies.

8

- (3)

- Basic and diluted net income (loss) attributable to common stock is computed by dividing net income by the weighted average number of common shares outstanding during the period including the effect of dilutive options, when applicable. See Note 2 to the Consolidated Financial Statements included elsewhere in this prospectus for additional information.

- (4)

- Adjusted EBITDA is defined as net income (loss) before depreciation and amortization, interest expense, other non-operating (expense) income, investment impairment, income taxes, income from discontinued operations, cumulative effect of change in accounting principle and other adjustments (including costs associated with business realignment activities, dispositions and pension settlement charges). See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Adjustments to EBITDA." We use Adjusted EBITDA as the primary measure of segment performance because we believe it gives us a more complete understanding of our financial condition and operating results. We use Adjusted EBITDA to calculate various financial ratios and to measure our performance, and we believe some debt and equity investors also utilize this metric for similar purposes. Adjusted EBITDA is intended to show unleveraged, pre-tax operating results. This is the profitability measure we use to set management and executive incentive compensation. Adjusted EBITDA is not intended to represent any measure of performance in accordance with generally accepted accounting principles, or GAAP. Because not all companies use identical calculations, this presentation of Adjusted EBITDA may not be comparable to other similarly titled measures presented by other companies. This non-GAAP measure should not be used in isolation or as a substitute for a measure of performance or liquidity prepared in accordance with GAAP or as indicative of whether cash flows will be sufficient to fund our future cash requirements. The table below reconciles Adjusted EBITDA to net income (loss), which we believe to be the most directly comparable GAAP financial measure.

Reconciliation of Adjusted EBITDA to Net Income (Loss)

| | Year ended December 31, | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | 2003 | 2002 | 2001 | |||||||

| | (in thousands) | |||||||||

| Adjusted EBITDA | $ | 127,746 | $ | 121,726 | $ | 139,215 | ||||

| Depreciation and amortization | (47,319 | ) | (47,947 | ) | (59,361 | ) | ||||

| Adjustments to EBITDA(a) | (13,885 | ) | (40,071 | ) | (155,349 | ) | ||||

| Interest expense | (46,138 | ) | (47,315 | ) | (51,613 | ) | ||||

| Affiliated interest expense | (558 | ) | (1,402 | ) | (11,488 | ) | ||||

| Other non-operating (expense) income(b) | (1,529 | ) | 5,989 | (1,841 | ) | |||||

| Investment impairment(c) | — | — | (27,000 | ) | ||||||

| Income tax benefit | 4,659 | 2,262 | 30,833 | |||||||

| Income from discontinued operations, net of tax(d) | — | — | 11,804 | |||||||

| Cumulative effect of change in accounting principle | — | (29,825 | ) | — | ||||||

| Net income (loss) | $ | 22,976 | $ | (36,583 | ) | $ | (124,800 | ) | ||

- (a)

- For the year ended December 31, 2003, Adjustments to EBITDA consisted of $6,988 related to plant closure costs, $6,837 related principally to administrative workforce reduction programs, $3,183 in impairment charges and $3,123 in other income. For the year ended December 31, 2002, Adjustments to EBITDA consisted of $12,584 related to plant closure costs, $3,265 related primarily to administrative workforce reduction programs, $6,315 in impairment charges, a pension settlement charge of $13,600 and $4,307 in other expenses. For the year ended December 31, 2001, Adjustments to EBITDA consisted of $23,285 related to plant closure costs, $12,582 in severance costs, $101,048 in impairment charges, a pension settlement charge of $15,813 and $2,621 in other expenses. For more information about Adjustments to EBITDA see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Adjustments to EBITDA".

- (b)

- For the year ended December 31, 2003, other non-operating (expense) income consisted primarily of a loss on the settlement of an intercompany loan resulting from foreign currency translation. For the year ended December 31, 2002, other non-operating (expense) income consisted of $2,741 of gain on the repurchase of debt in the open market and $1,722 of gain on an interest swap. For the year ended December 31, 2001, other non-operating (expense) income consisted principally of a loss on an interest rate swap.

- (c)

- For the year ended December 31, 2001, investment impairment consisted of $17,000 related to the write-down of a receivable from, and preferred stock investments in, WKI Holding Company, Inc. ("WKI"), one of our former affiliates, and $10,000 related to our write-off of our remaining investment in BCPM.

- (d)

- For the year ended December 31, 2001, income from discontinued operations, net of tax, consisted of earnings from our consumer adhesives business prior to its sale. See Note 7 to the Consolidated Financial Statements included elsewhere in this prospectus.

9

An investment in our common stock involves a high degree of risk. You should carefully consider the following information, together with other information in this prospectus, before buying shares of our common stock. If any of the following risks or uncertainties occurs, our business, financial condition and results of operations could be materially and adversely affected. The trading price of our common stock could decline and you may lose all or a part of the money you paid to buy our common stock. The risks described below are not the only ones facing our company. Additional risks not currently known to us or that we currently deem immaterial also may impair our business, financial condition and results of operations.

Risks Relating to Our Business

Demand for our products is cyclical and we may experience prolonged depressed market conditions for our products, which may adversely affect our results of operations.

Our products are used in industries that are cyclical in nature, such as the construction, furniture, automotive, oilfield services, chemicals, electronics, communications and steel production industries. We sell our products to manufacturers in those industries who incorporate them into their own products. Our largest end-market is the construction industry, which accounted for approximately 35% of our net sales in 2003. Sales to the construction industry are driven by trends in commercial and residential construction, housing starts and trends in residential repair and remodeling. Consumer confidence, mortgage rates and income levels play a significant role in driving demand in the residential construction, repair and remodeling sector. A drop in consumer confidence or an increase in mortgage rates or unemployment could cause a slowdown in the construction industry, and in particular the residential construction, repair and remodeling industry. We cannot assure you that such adverse developments will not occur and, if they do occur, that they will not have a material adverse effect on our results of operations.

Downturns in one or more of the other businesses that use our products can adversely affect our net sales and operating profit. Many of our customers are in businesses that are cyclical in nature and sensitive to changes in general economic conditions. In 2003, our North American forest products thermoset resins business was adversely affected by a decline in the furniture sector in the United States. In 2002, sales of our oilfield services products declined 29% as a result of reduced drilling activity. We also experienced a decline in the demand for our UV coating products as a result of significantly lower demand for fiber-optic cable in 2002. Demand for our products depends, in part, on general economic conditions, and a decline in economic conditions in the industries served by our customers has, and may continue to have, a material adverse effect on our business. We cannot assure you that an economic downturn in one or more of the businesses or geographic regions in which we sell our products would not have a material adverse effect on our results of operations.

We rely significantly on raw materials in the production of our products and fluctuations in costs could adversely effect our financial condition and profitability.

The three primary feedstock raw materials that we use in our manufacturing processes are methanol, phenol and urea. Our manufacturing operations depend upon obtaining adequate supplies of these raw materials on a timely basis. These raw materials are generally available from numerous independent suppliers. During the past three years, the price of these materials has been volatile. In 2003, for example, the average prices of methanol, phenol and urea increased by 42%, 22% and 50%, respectively. We are exposed to price risks associated with these raw material purchases. The availability and prices of raw materials may be subject to curtailment or change due to, among other things, new laws or regulations, suppliers' allocations to other purchasers, interruptions in production

10

by suppliers, changes in exchange rates, cost components of raw materials and worldwide price levels. Our results of operations could be adversely affected if we were unable to obtain adequate supplies of raw materials in a timely manner or if the costs of raw materials increased significantly. From time to time, suppliers may extend lead times, limit supplies or increase prices due to capacity constraints or other factors. Although certain of our contracts include competitive price clauses that allow us to buy outside the contract if market pricing falls below contract pricing and other contracts have minimum-maximum monthly volume commitments that allow us to take advantage of spot pricing, we cannot assure you that we will be able to purchase raw materials at market price. In addition, some of our customer contracts include selling price provisions that are indexed to publicly available indices for these commodity raw materials; however, we may not be able to immediately pass on raw material price increases to our customers, if at all. Due to differences in timing of the pricing mechanism trigger points between our sales and purchase contracts there is often a "lead-lag" impact during which margins are negatively impacted for the short term in periods of rising raw material prices and positively impacted in periods of falling raw material prices. We cannot assure you that raw material prices will decrease from currently high levels or that we will be able to capitalize on any such reductions in a timely manner, if at all. In addition, we cannot assure you that the fluctuation in price of our primary raw materials will not have an adverse effect on our financial condition and profitability.

Rising energy costs may result in increased operating expenses and reduced net income.

Natural gas is essential in our manufacturing processes, and its cost can vary widely and unpredictably. Energy costs have risen significantly over the past several years due to the increase in the cost of oil and natural gas and the recent shortages of energy in various states. Our operating expenses increased in 2003 and will continue to increase if these costs continue to rise or do not return to historical levels. Rising energy costs may also increase our raw material costs. If we cannot pass these costs through to our customers, our business, financial condition or results of operations may be adversely affected. In addition, rising energy costs also negatively impact our customers and the demand for our products. These risks will be exacerbated if our customers or production facilities are in locations experiencing severe energy shortages.

Environmental matters could have a substantial negative impact on our results of operations.

Our operations involve the use, handling, processing, storage, transportation and disposal of hazardous materials and are subject to extensive environmental laws and regulations at the national, state, local and international level. Such environmental laws and regulations include those governing the discharge of pollutants into the air and water, the management and disposal of hazardous materials and wastes, the cleanup of contaminated sites and occupational health and safety. We have incurred, and will continue to incur, significant costs and capital expenditures in complying with these laws and regulations. In 2003, we incurred $5.2 million in capital expenditures to comply with environmental laws and regulations. In addition, violations of environmental laws or permits may result in restrictions being imposed on our operating activities or in our being subjected to substantial fines, penalties, criminal proceedings, third party property damage or personal injury claims or other costs. In addition, future developments or increasingly stringent regulation could require us to make additional unforeseen environmental expenditures.

Even if we fully comply with environmental laws, we are subject to liability associated with hazardous substances in soil, groundwater and elsewhere at a number of sites. These include sites that we formerly owned or operated, and sites where hazardous wastes and other substances from our current and former facilities and operations have been treated, stored or disposed of, as well as sites that we currently own or operate. Depending upon the circumstances, our liability may be joint and several, meaning that we may be held responsible for more than our proportionate share, or even all, of the liability involved. Environmental conditions at such sites can lead to claims against us for

11

personal injury or wrongful death, property damages, and natural resource damages, as well as to claims and obligations for the investigation and cleanup of environmental conditions. The extent of any such liabilities can be difficult to predict.

We have been notified that we are or may be responsible for environmental remediation at a number of sites in the United States, and we are also undertaking a number of voluntary cleanups. We believe the most significant of these and the site that makes up over half of our remediation accrual is the site formerly owned by us in Geismar, Louisiana. We cannot assure you that, as a result of former, current or future operations, there will not be additional environmental remediation or restoration liabilities or claims of personal injury by employees or members of the public due to exposure or alleged exposure to hazardous materials in connection with our operations, properties or products. We are aware of several sites, sold by us over 20 years ago, that may have significant site closure or remediation costs. It has been reported in the local press that closure or remediation costs associated with one of these sites will exceed $100 million. Actual costs at these sites, as well as our share, if any, are unknown to us at this time. In addition, we have been named in two tort actions relating to one of these sites.

We cannot assure you that these environmental liabilities or obligations, or any that may arise or become known to us in the future, will not have a material adverse effect on our business, financial condition, results of operations or cash flows.

We are subject to government regulation.

We are subject to regulation by many U.S. and non-U.S. supranational, national, federal, state and local governmental authorities. In some circumstances, before we may sell some of our products these authorities must approve these products, our manufacturing processes and facilities. As our facilities grow, we may become subject to additional regulation or higher compliance standards. We are also subject to ongoing reviews of our products and manufacturing processes. In order to obtain regulatory approval of certain new products, we must, among other things, demonstrate to the relevant authority that the product is safe for its intended uses and that we are capable of manufacturing the product in accordance with current regulations. The process of seeking approvals can be costly, time consuming and subject to unanticipated and significant delays. We cannot assure you that approvals will be granted to us on a timely basis, or at all. Any delay in obtaining, or any failure to obtain or maintain, these approvals would adversely affect our ability to introduce new products and to generate revenue from those products. New laws and regulations may be introduced in the future that could result in additional compliance costs, seizures, confiscation, recall or monetary fines, any of which could prevent or inhibit the development, distribution or sale of our products. If we fail to comply with applicable laws and regulations, we may be subject to civil remedies, including fines, injunctions, recalls or seizures, which could have an adverse effect on our business, financial condition or results of operations.

We produce hazardous chemicals that require appropriate procedures and care to be used in handling them or using them to manufacture other products. For example, formaldehyde is an extensively regulated chemical, which various government agencies continue to evaluate to determine whether to promulgate additional regulations. In the past year, several updates of epidemiology reports were published, two of which suggest a potential relationship between formaldehyde and leukemia for workers exposed to formaldehyde. Today scientists are analyzing these newest reports to determine their validity and significance before any health conclusions are drawn from the reports' findings. However, certain government-related health assessment reviews are proceeding very rapidly based, at least in part, on these new reports, without detailed scientific evaluations and analyses of these newest reports. As a result, the International Agency for Research on Cancer, or IARC, is expected to make a determination whether formaldehyde should be reclassified as a "known human carcinogen" from a "probable human carcinogen." Such a reclassification could lead to further federal and state

12

governmental review of existing regulations on formaldehyde, which could result in additional requirements and capital expenditures to achieve and maintain compliance. In addition, the European Commission recently published a proposal, known as Registration, Evaluation and Authorisation of Chemicals, or REACH, which would require manufacturers, importers and consumers of certain chemicals to register such chemicals and evaluate their potential impacts on human health and the environment. Based on the results of the evaluation, a newly created regulatory body would then determine if the chemical should be further regulated, restricted or banned from use. If REACH is enacted in its current form, it is possible that significant market restrictions could be imposed on the current and future uses of formaldehyde-based materials in the European Union. Because the timing and ultimate form of the potential REACH regulation is not yet known, we cannot accurately predict future compliance costs. Such costs could, however, be significant.

We also produce resin-coated sand, and because sand consists primarily of crystalline silica, the potential for silica exposure exists, which is a well known and recognized health hazard. The Occupational Safety and Health Administration, or OSHA, has indicated that a comprehensive standard for crystalline silica is likely needed to provide for exposure monitoring, medical surveillance and worker training. In order to achieve compliance with these possible future OSHA regulations, we may incur incremental costs over time, including increased capital expenditures in order to implement engineering controls to meet any new requirements. We cannot assure you that additional regulation of hazardous substances, including formaldehyde and silica, unfavorable publicity or increased litigation relating to such chemicals will not have a material adverse effect on our business, financial condition or results of operations.

We are subject to numerous legal actions that could have an impact on our profitability and our ability to operate certain businesses.

In 1998, pursuant to a merger and recapitalization transaction sponsored by The Blackstone Group, which we refer to as Blackstone, and financed by The Chase Manhattan Bank, which we refer to as Chase, Borden Decorative Products Holdings, Inc., or BDPH, one of our wholly owned subsidiaries, was acquired by Blackstone and subsequently merged with Imperial Wallcoverings to create Imperial Home Décor Group, or IHDG. Blackstone provided $84.5 million in equity, a syndicate of banks funded $198.0 million of senior secured financing and $125.0 million of senior subordinated notes were privately placed. We received approximately $314.4 million in cash and 11% of IHDG common stock for our interest in BDPH. On January 5, 2000, IHDG filed for reorganization under Chapter 11 of the U. S. Bankruptcy Code. The IHDG Litigation Trust, which we refer to as the Trust, was created pursuant to the plan of reorganization in the IHDG bankruptcy to pursue preference and other avoidance claims on behalf of the unsecured creditors of IHDG. In November 2001, the Trust filed a lawsuit against us and certain of our affiliates seeking to have the IHDG recapitalization transaction voided as a fraudulent conveyance and asking for a judgment to be entered against us for $314.4 million plus interest, costs and attorney fees. Discovery is proceeding in the case with a cut-off currently scheduled for November 2004. We have not recorded a liability for any potential losses because a loss is not considered probable based on current information. We believe that we have strong defenses to the Trust's allegations and we intend to defend the case vigorously. At this time, we are unable to estimate the amount of any reasonably possible losses and we cannot assure you that those losses will not be material.

In addition, we have historically faced a substantial number of lawsuits, including class action lawsuits, claiming liability for death, injury or property damage caused by products manufactured by us or with our components. These lawsuits, and any future lawsuits, could result in substantial damage awards against us, which in turn could encourage additional lawsuits. If formaldehyde is re-classified as a "known human carcinogen" by IARC, then it is possible that we will face product liability litigation, in addition to the cases we currently face, alleging injury from formaldehyde exposure. In addition,

13

there has been increased publicity about asbestos liabilities faced by manufacturing companies and, as a result of the bankruptcies of many producers of asbestos-containing products, plaintiff attorneys are increasing their focus on peripheral defendants, including us, and on other products, including silica and vinyl chloride monomer, or VCM. While we do not currently believe that we face any material liabilities as a result of product liability litigation and believe we have adequate insurance and reserves, we cannot assure you that these lawsuits will not result in material awards against us or other material costs to us.

In 1992, the State of Sao Paolo Tax Bureau issued an assessment against our primary Brazilian subsidiary claiming that excise taxes were owed on certain intercompany loans made for centralized cash management purposes, characterized by the Tax Bureau as intercompany sales. Since that time, the subsidiary and the Tax Bureau have held discussions, and our subsidiary has filed an administrative appeal seeking cancellation of the assessment. In December 2001, the Administrative Court upheld the assessment in the amount of 52.0 million Brazilian Real, an amount which includes tax, penalties, monetary correction and interest, or approximately $18.0 million. In September 2002, our subsidiary filed a second appeal with the highest level administrative court, again seeking cancellation of the assessment. We believe we have a strong defense against the assessment and we will pursue the appeal vigorously, including appealing to the judicial level. At this time we do not believe a loss is probable; therefore, only related legal fees have been accrued. Nonetheless, we cannot assure you that the assessment will not be upheld.

While it is not feasible to predict the outcome of pending suits and claims, the ultimate resolution of these matters could have an adverse effect upon our business, financial condition, results of operations or reputation. For more information about these and other legal proceedings see "Business—Legal Proceedings."

We are subject to liabilities arising out of the sale of several of our previously owned businesses.

We have sold various businesses and business lines and, in some instances, retained liability for those businesses pursuant to the sale contract or pursuant to applicable law. Although the majority of the contractual liabilities have expired, some remain in effect and could result in claims against us. For example, recently we reached tentative agreements with the successors in interest to two of our former subsidiaries that filed for protection under Chapter 11 of the United States Bankruptcy Code. The agreements provide for the settlement of all claims for an aggregate payment by us of approximately $7.1 million. We anticipate that the settlement agreements will be finalized and submitted to the bankruptcy court for approval in June 2004. However, we cannot assure you that these settlements will be approved or that additional claims will not be brought. See "Business—Legal Proceedings."

Our production facilities are subject to operating hazards.

We are dependent on the continued operation of our 48 production facilities, in particular our most significant plant in Louisville, Kentucky. These production facilities are subject to hazards associated with the manufacture, handling, storage and transportation of chemical materials and products, including pipeline leaks and ruptures, explosions, fires, inclement weather and natural disasters, mechanical failure, unscheduled downtime, labor difficulties, transportation interruptions, and environmental hazards, such as spills, discharges or releases of toxic or hazardous substances and gases, storage tank leaks and remediation complications. These hazards can cause personal injury and loss of life, severe damage to, or destruction of, property and equipment and environmental contamination and other environmental damage and could have a material adverse effect on our business, financial condition or results of operations. In addition, due to the nature of our business operations we have been and may continue to be subject to environmental movements. For example, currently there is an environmental movement at our Louisville facility led by residents of the "Rubbertown" area, in which there are many chemical facilities, including our plant. As is typical with these movements, residents

14

are claiming that the chemical facilities have caused health and property damage. We are also aware of two lawsuits involving one of our predecessor entities that allege residents living near one of our plants suffered health issues as a result of exposure to chemicals used at that plant. We cannot assure you that these movements will not result in litigation or damage to our reputation. See Note 22 to the Consolidated Financial Statements included elsewhere in this prospectus.

We are subject to adverse claims from our customers and their employees as a result of the hazardous nature of our products.

We produce hazardous chemicals that require appropriate procedures and care to be used in handling them or using them to manufacture other products. As a result of the nature of our products, we may face exposure relating to incidents involving our customers' handling, storage and use of our products. On February 20, 2003, an explosion occurred at the facility of one of our customers, CTA Acoustics, Inc., which we refer to as CTA. Seven plant workers were killed in the explosion and more than 40 workers were injured. There are six lawsuits in Laurel County, Kentucky, arising out of this incident, primarily seeking recovery for wrongful death personal injury, emotional distress, loss of consortium, property damage and indemnity. Because injured workers pursue claims against their employer in workers' compensation proceedings, they frequently pursue claims under various theories against product suppliers. We faced a similar lawsuit in the past. Although we believe that we have adequate insurance coverage to address any payments and/or legal fees in excess of $5 million involved in any single incident, we cannot assure you that we will not be subject to significant judgments given the nature of this litigation. We are also subject to suits involving asbestos, silica and VCM. Although (i) we typically obtain dismissals from asbestos product litigation because of plaintiffs' failure to identify a product containing asbestos that we manufactured; (ii) our only silica product is resin-coated sand, as contrasted with the sand used in sandblasting and other applications most commonly associated with silicosis; and (iii) many years ago we discontinued manufacturing VCM, which was manufactured primarily for our own use rather than for customer sale, we have been joined in such litigation as one of numerous defendants. We do not believe that we have a material asbestos, silica or VCM exposure and believe we have adequate reserves for such litigation. In addition, we have special arrangements providing limited insurance coverage for asbestos and VCM exposure. However, we cannot assure you that we will not be subject to significant judgments given the nature of the claims against us. We could have difficulty maintaining insurance coverage at reasonable rates if the number of claims involving products of a hazardous nature significantly increases. In addition, if formaldehyde is reclassified as a "known human carcinogen," we may face increased regulation and litigation.

Due to the nature of our business, we may not be able to provide complete insurance against all potential accidents.

Our operations are subject to the usual hazards associated with chemical manufacturing and the related storage and transportation of feedstocks, products and wastes, including explosions, fires, inclement weather and natural disasters, mechanical failure, unscheduled downtime, transportation interruptions, remediation, chemical spills, discharges or releases of toxic or hazardous substances or gases and other environmental risks. The hazards can cause personal injury and loss of life, severe damage to or destruction of property and equipment and environmental damage, and may result in suspension of operations and the imposition of civil or criminal penalties. Although we maintain property, business interruption and casualty insurance that we believe is in accordance with customary industry practices, we cannot assure you that we will not incur losses beyond the limits of, or outside the coverage of, our insurance policies. In addition, our insurance provides very limited, if any, coverage for liabilities associated with environmental matters or that may arise out of such accidents. From time to time, various types of insurance for companies in the chemical industry have not been available on commercially acceptable terms or, in some cases, have been unavailable, including

15

coverage for silica claims. We cannot assure you that in the future we will be able to maintain existing coverage or that premiums will not increase significantly.

We are exposed to political, economic and other risks that are inherent in operating an international business. Our substantial international operations subject us to risks not faced by domestic competitors, which include unfavorable political, regulatory, labor and tax conditions in other countries.

We have significant manufacturing operations outside the United States. In 2003, our net sales outside the United States represented 37% of our total sales. We have 21 production facilities located outside the United States, primarily concentrated in Canada, Brazil, the U.K., Australia and Malaysia. Accordingly, our business is subject to the differing legal, political, social and regulatory requirements and economic conditions of many jurisdictions. Risks are inherent in international operations, including, but not limited to, the following:

- •

- difficulty in enforcing agreements through foreign legal systems;

- •

- foreign customers may have longer payment cycles;

- •

- foreign countries may impose additional withholding taxes or otherwise tax our foreign income, impose tariffs or adopt other restrictions on foreign trade and investment, including currency exchange controls;

- •

- fluctuations in exchange rates may affect product demand and may adversely affect the profitability in U.S. dollars of products and services provided by us in foreign markets where payment for our products and services is made in the local currency;

- •

- increased costs of transportation or shipping;

- •

- risk of nationalization of private enterprises;

- •

- changes in general economic and political conditions in the countries in which we operate;

- •

- unexpected adverse changes in foreign laws or regulatory requirements, including with respect to environmental protection, export duties and quotas;

- •

- difficulty with staffing and managing widespread operations; and

- •

- required compliance with a variety of foreign laws and regulations.

In addition, intellectual property rights may be more difficult to enforce in foreign countries. We currently have joint ventures in China, where we will be licensing technology to our joint venture partners. We cannot assure you that we will be able to adequately protect our intellectual property in China or elsewhere. Our business in emerging markets requires us to respond to rapid changes in market conditions in these countries. Our overall success as a global business depends, in part, upon our ability to succeed in differing legal, regulatory, economic, social and political conditions. We cannot assure you that we will continue to succeed in developing and implementing policies and strategies which will be effective in each location where we do business. Furthermore, we cannot assure you that any of the foregoing factors will not have a material adverse effect on our business, financial condition and results of operations.

Currency translation risk and currency transaction risk may adversely affect our results of operations.

We conduct our business and incur costs in the local currency of most countries in which we operate. Accordingly, our results of operations are reported in the relevant local currency and then translated to U.S. dollars at the applicable currency exchange rate for inclusion in our financial statements. Changes in exchange rates between those foreign currencies and the U.S. dollar will affect

16

our net sales, cost of goods sold and operating margins and could result in exchange losses. In addition to currency translation risks, we incur currency transaction risk whenever one of our operating subsidiaries enters in either a purchase or a sales transaction using a different currency from the currency in which it receives revenues. In an effort to mitigate the impact of exchange rate fluctuations we engage in exchange rate hedging activities. However, we cannot assure you that the hedging transactions we enter into will be effective or will not result in foreign exchange hedging loss. The impact of future exchange rate fluctuations on our results of operations cannot be accurately predicted. Given the volatility of exchange rates, we cannot assure you that we will be able to effectively manage our currency transaction and/or translation risks, and any volatility in currency exchange rates may have an adverse effect on our financial condition or results or operations.

Terrorist attacks may negatively affect our operations, financial condition and results of operations.

The attacks of September 11, 2001 and subsequent events, including the continuing military action in Iraq and Afghanistan, have caused instability throughout the world. Terrorist attacks, including even modest individual incidents, may adversely affect our operations, financial condition and results of operations and may impact any or all of our physical facilities and operations, which are located in North America, Latin America, Europe and Asia Pacific, or those of our customers. Chemical-related assets may be at greater risk of future terrorist attacks than other possible targets in the United States and throughout the world. The resulting damage from a direct attack on our assets or assets used by us would be difficult to assess, may be severe and could include loss of life and property damage. In addition, available insurance coverage may not be sufficient to cover all of the damage incurred or may be prohibitively expensive.

Our cost reduction programs may not achieve the cost savings and operations improvements and efficiencies we expect, and we may have to implement further cost reduction programs and incur additional related charges.

In 2002, we implemented a major Six Sigma process initiative and in June 2003, we initiated the 2003 Realignment, which was designed to reduce operating expenses and increase organizational efficiency. To achieve the goals of these cost reduction and efficiency programs, we are reducing our workforce, streamlining processes, consolidating manufacturing processes and reducing general and administrative expenses. We will continue to implement cost reduction and efficiency programs intended to achieve cost savings and improve our operational results. These programs are subject to significant risks and uncertainties and, in certain circumstances, may require third party or governmental approval. Our ability to achieve the goals relating to our cost reduction programs and business realignments, including any anticipated expense reductions or operations improvements, will depend on a number of factors, some of which are outside of our control. Even if we complete our Six Sigma process initiative and our 2003 Realignment, we cannot assure you that we will achieve any of the cost reductions we anticipate or on the timetable we contemplate.

We may not be able to develop the new products that we need to remain competitive.

Our results of operations depend to a significant extent on our ability to expand our product offerings, and to continue to develop our production processes to be a competitive producer. We are committed to remaining a competitive producer and believe that our portfolio of new or re-engineered products is strong. We believe that approximately 15% of our net sales in 2003 were derived from products developed or re-engineered within the last three years. However, we may not be able to continue to develop new products, re-engineer our existing products successfully or bring them to market in a timely manner. For example, our historical research and development efforts generally have focused on customer service, and we may be unsuccessful in shifting our focus to the type of research that will lead to significant new product development. In addition, our research and development

17

scientists are generally located at our individual plants rather than at a research facility, which may impede their ability to share ideas and create new products. While we believe that the products, pricing, and services we offer customers are competitive, we cannot assure you that we will be able to continue to attract and retain customers to which to sell our products.

We face competition from other chemical companies, which could force us to lower our prices thereby adversely affecting our operating margins, financial condition and results of operations.

The markets in which we operate are highly competitive, and this competition could harm our business, results of operations, cash flow and financial condition. Our competitors include major international producers as well as smaller regional competitors. We believe that the most significant competitive factor for our products is selling price. We could be subject to adverse results caused by our competitors' pricing decisions. In addition, current and anticipated future consolidation among our competitors and customers may cause us to lose market share as well as put downward pressure on pricing. In addition, some of our competitors are larger, have greater financial resources and have less debt than we do. As a result, those competitors may be better able to withstand a change in conditions within our industry and throughout the economy as a whole. If we do not compete successfully, our business, financial condition and results of operations could be adversely affected.

Competition from producers of materials that are substitutes for formaldehyde-based resins could lead to declines in our net sales attributable to these products.

We face competition from a number of products that are potential substitutes for formaldehyde-based resins. Currently, we estimate that formaldehyde-based resins make up most of the resins used as panelboard resins, wood and specialty adhesives and industrial resins. Decreases in the average selling price of formaldehyde may have a material adverse effect on our profitability. For example, competition among producers of foundry and specialty resins has led to erosion in certain product prices in the past. Our ability to maintain or increase our profitability will continue to be dependent, in large part, upon our ability to offset decreases in average selling prices by improving production efficiency or by shifting to higher margin chemical products. If we are unable to do so, our business, financial condition and results of operations could be materially and adversely affected. In addition, in some markets, non-formaldehyde based resins may be an alternative to our formaldehyde-based resins. Considerable growth in these substitutes for formaldehyde-based resins could adversely affect our market share, net sales and profit margins. Furthermore, the movement toward substitute products could be exacerbated if the IARC, which is reviewing the carcinogenic classification of formaldehyde in June 2004, reclassifies formaldehyde from a "probable human carcinogen" to a "known human carcinogen." For more information, see the risk described above under the heading "—We are subject to government regulation."

Our strategy of supplementing our products through selective acquisitions and joint ventures presents risks.

We have made acquisitions of related businesses and entered into joint ventures in the recent past and intend to selectively pursue acquisitions of, and joint ventures with, related businesses as one element of our growth strategy. Our ability to implement this growth strategy will be limited by our ability to identify appropriate acquisition and joint venture candidates and our financial resources, including available cash and borrowing capacity. The expense incurred in consummating acquisitions of related businesses, or our failure to integrate such businesses successfully into our existing businesses, could result in our incurring unanticipated expenses and losses. Furthermore, we may not be able to realize any anticipated benefits from acquisitions or joint ventures. The process of integrating acquired operations into our existing operations may result in unforeseen operating difficulties and may require significant financial resources that would otherwise be available for the ongoing development or

18

expansion of existing operations. Some of the risks associated with our acquisition and joint venture strategy include:

- •

- potential disruption of our ongoing business and distraction of management;

- •

- unexpected loss of key employees or customers of the acquired company;

- •