Exhibit 99.1

1 1 2017 Third Quarter Financial Results November 1, 2017 NYSE: CF 2020 First Quarter Financial Results May 6, 2020 NYSE: CF

2 Safe harbor s tatement All statements in this communication by CF Industries Holdings, Inc. (together with its subsidiaries, the “Company”), other t han those relating to historical facts, are forward - looking statements. Forward - looking statements can generally be identified by their use of terms s uch as “anticipate,” “believe,” “could,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will” or “would” and similar terms and phrases, including references to assumptions. Forward - looking statements are not guarantees of future performance and are subject to a number of as sumptions, risks and uncertainties, many of which are beyond the Company’s control, which could cause actual results to differ materiall y f rom such statements. These statements may include, but are not limited to, statements about strategic plans and statements about futur e f inancial and operating results. Important factors that could cause actual results to differ materially from those in the forward - looking statements include, among others, the impact of the novel coronavirus disease 2019 (COVID - 19) pandemic, including measures taken by governmental authoriti es to slow the spread of the virus, on our business and operations; the cyclical nature of the Company’s business and the impact of global supply and demand on the Company’s selling prices; the global commodity nature of the Company’s fertilizer products, the conditions in the international market for nitrogen products, and the intense global competition from other fertilizer producers; conditions in the United States, Europe and other agricultural areas; the volatility of natural gas prices in North America and Europe; difficulties in securing the supply and delivery of raw mat eri als, increases in their costs or delays or interruptions in their delivery; reliance on third party providers of transportation services and eq uip ment; the significant risks and hazards involved in producing and handling the Company’s products against which the Company may not be fully insured; the Co mpany’s ability to manage its indebtedness and any additional indebtedness that may be incurred; the Company's ability to maintain compliance with covenants under its revolving credit agreement and the agreements governing its indebtedness; downgrades of the Company’s credit ratings; risks associated with cyber security; weather conditions; risks associated with changes in tax laws and disagreements with taxing authorities; the Company’s reliance on a limited number of key facilities; potential liabilities and expenditures related to environmental, he alt h and safety laws and regulations and permitting requirements; future regulatory restrictions and requirements related to greenhouse gas emissions; ri sks associated with expansions of the Company’s business, including unanticipated adverse consequences and the significant resources that could b e r equired; the seasonality of the fertilizer business; the impact of changing market conditions on the Company’s forward sales programs; ris ks involving derivatives and the effectiveness of the Company’s risk measurement and hedging activities; risks associated with the operation or management of the strategic venture with CHS Inc. (the "CHS Strategic Venture "), risks and uncertainties relating to the market prices of the fertilizer products that are the subject of the supply agreement with CHS Inc. over the life of the supply agreement and the risk that any challenges rel ated to the CHS Strategic Venture will harm the Company's other business relationships; risks associated with the Company’s Point Lisas Nitro gen Limited joint venture; acts of terrorism and regulations to combat terrorism; risks associated with international operations; and deteriora tio n of global market and economic conditions. More detailed information about factors that may affect the Company’s performance and could cause actual results to differ materially from those in any forward - looking statements may be found in CF Industries Holdings, Inc.’s filings with the Securiti es and Exchange Commission, including CF Industries Holdings, Inc.’s most recent annual and quarterly reports on Form 10 - K and Form 10 - Q, which are available in the Investor Relations section of the Company’s website . Forward - looking statements are given only as of the date of this presentation and the Company disclaims any obligation to update or revise the forward - looking statements, whether as a result of new information, fut ure events or otherwise, except as required by law.

3 Note regarding n on - GAAP f inancial m easures The Company reports its financial results in accordance with U.S. generally accepted accounting principles (GAAP). Managemen t b elieves that EBITDA, adjusted EBITDA, free cash flow, free cash flow to adjusted EBITDA conversion, and free cash flow yield, which are non - GAAP financial measures, provide additional meaningful information regarding the Company's performance and financial strength. No n - G AAP financial measures should be viewed in addition to, and not as an alternative for, the Company's reported results prepared in ac cordance with GAAP. In addition, because not all companies use identical calculations, EBITDA, adjusted EBITDA, free cash flow, and free c ash flow yield included in this presentation may not be comparable to similarly titled measures of other companies. Reconciliations of EBIT DA, adjusted EBITDA, free cash flow, and free cash flow yield to the most directly comparable GAAP measures are provided in the tables acc omp anying this presentation. EBITDA is defined as net earnings attributable to common stockholders plus interest expense - net, income taxes, and depreciatio n and amortization. Other adjustments include the elimination of loan fee amortization that is included in both interest and amort iza tion, and the portion of depreciation that is included in noncontrolling interest. The Company has presented EBITDA because management uses the measure to track performance and believes that it is frequently used by securities analysts, investors and other interested parties i n t he evaluation of companies in the industry. Adjusted EBITDA is defined as EBITDA adjusted with the selected items included in EBITDA as summarized in the tables accompan yin g this presentation. The Company has presented adjusted EBITDA because management uses adjusted EBITDA, and believes it is useful to investors, as a supplemental financial measure in the comparison of year - over - year performance . Free cash flow is defined as net cash provided by operating activities, as stated in the consolidated statements of cash flow s, reduced by capital expenditures and distributions to noncontrolling interest. Free cash flow to adjusted EBITDA conversion is defined as free cash flow divided by a djusted EBITDA. Free cash flow yield is defined as free cash flow divided by market value of equity (market cap). The Company has pre sen ted free cash flow, free cash flow to adjusted EBITDA conversion, and free cash flow yield because management uses these measures and believes they are useful to investors, as indications of the strength of the Company and its ability to generate cash and to eva luate the Company’s cash generation ability relative to its industry competitors. It should not be inferred that the entire free cash flow amount is available for discretionary expenditures.

4 CF response to spread of COVID - 19 successful to date Leadership planning and policies Sales and supply chain Manufacturing and distribution • Implemented new company - wide corporate travel restrictions to both CDC and non - CDC recognized countries • Non - essential employee work from home program implemented March 2020; o nly essential employees have entered corporate and operational locations to complete critical job duties • Essential employees shift schedule changes to reduce exposure risk • Increased cleaning and sanitation schedules • Temperature screening of employees and contractors; limited visitor access • Procured and distributed face coverings to all site employees • Established strict social distancing practices through control room p lexiglass partitions, arranged seating/standing enforcing 6’ distance, reduced shared paperwork (e.g. truck drivers, vendors) and personnel in control rooms • Constant contact with transportation partners to understand their preparations and contingency plans for the pandemic and to share CF policy changes and site procedures • Engaged customers to offer flexible solutions to ensure their nitrogen requirements are met

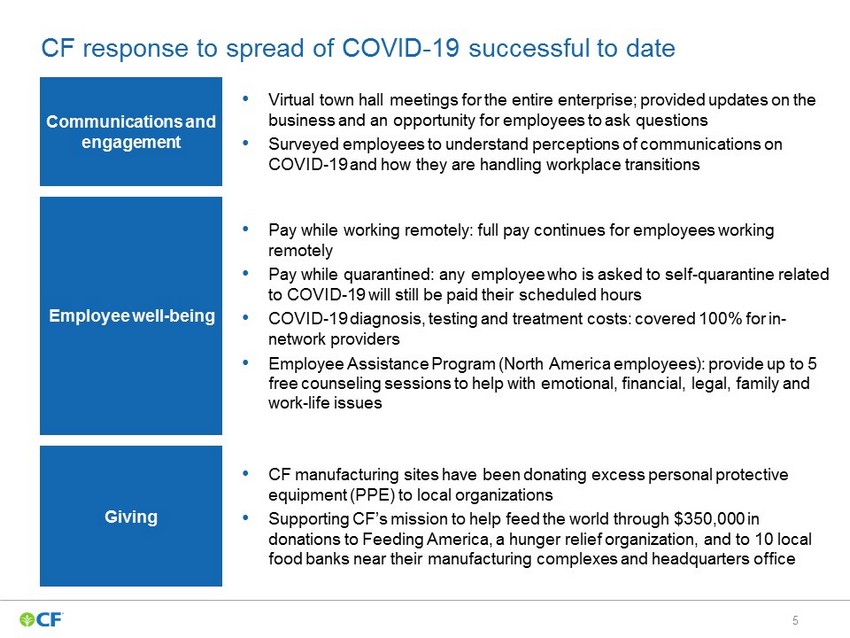

5 CF response to spread of COVID - 19 successful to date Communications and e ngagement Giving Employee well - being • V irtual town hall meetings for the entire enterprise; provided updates on the business and an opportunity for employees to ask questions • Surveyed employees to understand perceptions of communications on COVID - 19 and how they are handling workplace transitions • CF manufacturing sites have been donating excess personal protective equipment (PPE) to local organizations • Supporting CF’s mission to help feed the world through $350,000 in donations to Feeding America, a hunger relief organization , and to 10 local food banks near their manufacturing complexes and headquarters office • Pay while working remotely: full pay continues for employees working remotely • Pay while quarantined: any employee who is asked to self - quarantine related to COVID - 19 will still be paid their scheduled hours • COVID - 19 d iagnosis , testing and treatment costs: covered 100% for in - network providers • Employee Assistance Program (North America employees): provide up to 5 free counseling sessions to help with emotional, financial, legal, family and work - life issues

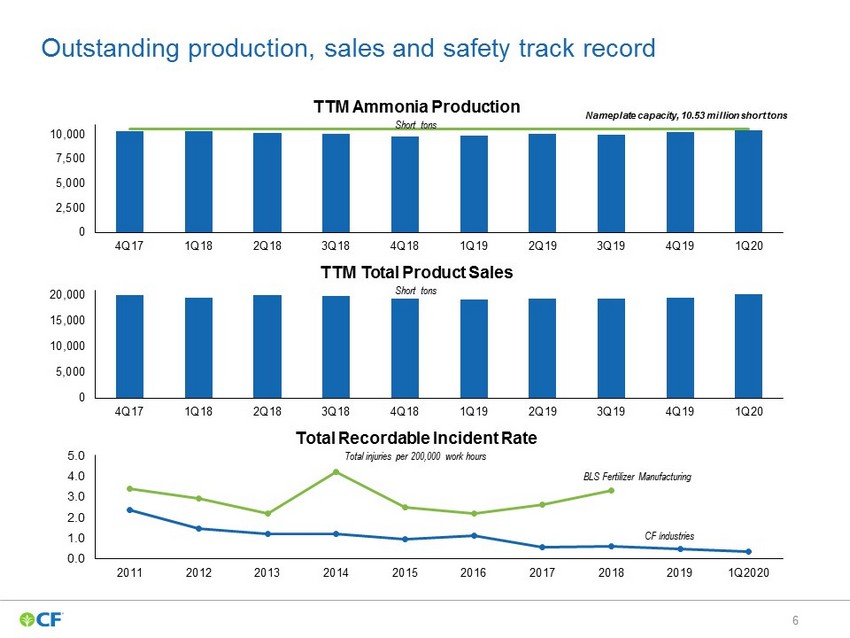

6 Outstanding production, sales and safety track record 0.0 1.0 2.0 3.0 4.0 5.0 2011 2012 2013 2014 2015 2016 2017 2018 2019 1Q2020 Total Recordable Incident Rate Total injuries per 200,000 work hours 0 5,000 10,000 15,000 20,000 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 TTM Total Product Sales Short tons 0 2,500 5,000 7,500 10,000 4Q17 1Q18 2Q18 3Q18 4Q18 1Q19 2Q19 3Q19 4Q19 1Q20 TTM Ammonia Production Short tons Nameplate capacity, 10.53 million short tons BLS Fertilizer Manufacturing CF Industries

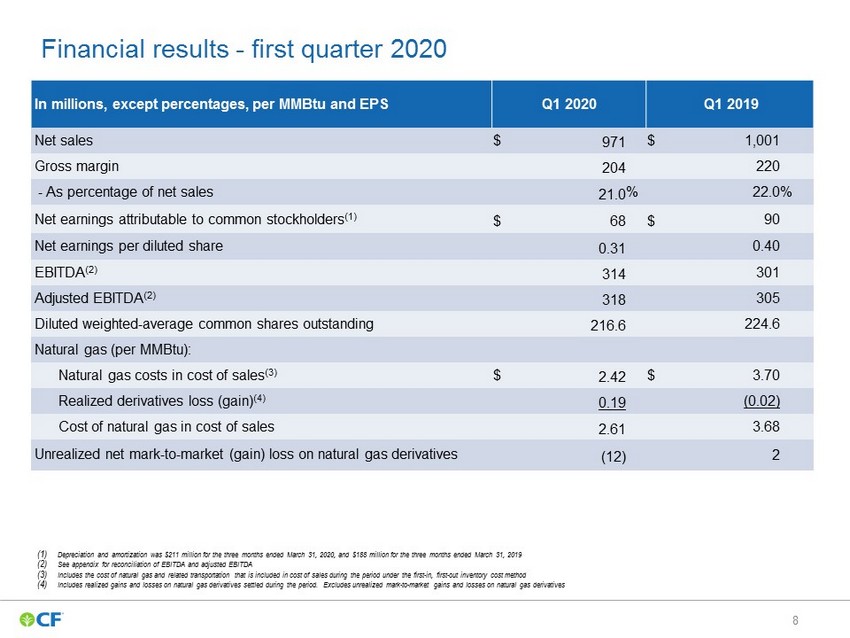

7 First quarter 2020 results (1) See appendix for reconciliation of EBITDA and adjusted EBITDA (2) Represents cash provided by operating activities (cash from operations) less capital expenditures less distributions to noncontrolling interest; see appendix for reconciliation of free cash flow • First quarter net earnings of $68 million, or $0.31 per diluted share; EBITDA (1 ) of $314 million and adjusted EBITDA (1) of $318 million • Trailing twelve month net cash from operating activities of $1,491 million, free cash flow (2) of $912 million • CF repurchased ~2.6 million shares for $100 million during Q1 2020; since share repurchase authorization in February 2019, CF has repurchased ~10.2 million shares for $437 million Financial Overview Safe and Efficient Operations • As of March 31, 2020, the 12 - month rolling average recordable incident rate was 0.34 incidents per 200,000 work hours, the lowest level recorded by CF • Gross ammonia production for Q1 2020 was approximately 2.7 million tons, which is the second highest quarterly volume in Company history Commercial Environment • Average selling prices for Q1 2020 were lower than Q1 2019 across all segments due to increased global supply availability as lower global energy costs drove higher global operating rates • Lower selling prices were mostly offset by higher sales volumes across all segments for Q1 2020 compared to Q1 2019 • Cost of sales for Q1 2020 was slightly lower than Q1 2019 due to lower realized natural gas costs and lower maintenance costs, offset by the impact of higher sales volumes • In Q1 2020 the average cost of natural gas reflected in CF’s cost of sales was $2.61 per MMBtu compared to $3.68 per MMBtu in Q1 2019

8 Financial results - first quarter 2020 I n millions, except percentages, per MMBtu and EPS Q1 20 20 Q1 201 9 Net sales $ 971 $ 1,001 Gross margin 204 220 - As percent age of net sales 21.0 % 22.0 % Net earnings attributable to common stockholders (1) $ 68 $ 90 Net earnings per diluted share 0.31 0.40 EBITDA ( 2 ) 314 301 Adjusted EBITDA ( 2 ) 318 305 Diluted weighted - average common shares outstanding 216.6 224.6 Natural g as (per MMBtu): Natural gas costs in cost of sales ( 3 ) $ 2.42 $ 3.70 Realized derivatives loss (gain) ( 4 ) 0.19 (0.02) Cost of natural gas in cost of sales 2.61 3.68 Unrealized net mark - to - market (gain) loss on natural gas derivatives (12) 2 (1) Depreciation and amortization wa s $211 million for the three months ended March 31, 2020, and $188 million for the three months ended March 31, 2019 (2) See appendix for reconciliation of EBITDA and adjusted EBITDA (3) Includes the cost of natural gas and related transportation that is included in cost of sales during the period under the first - in, first - out inventory cost method (4) Includes realized gains and losses on natural gas derivatives settled during the period. Excludes unrealized mark - to - market gains and lo sses on natural gas derivatives

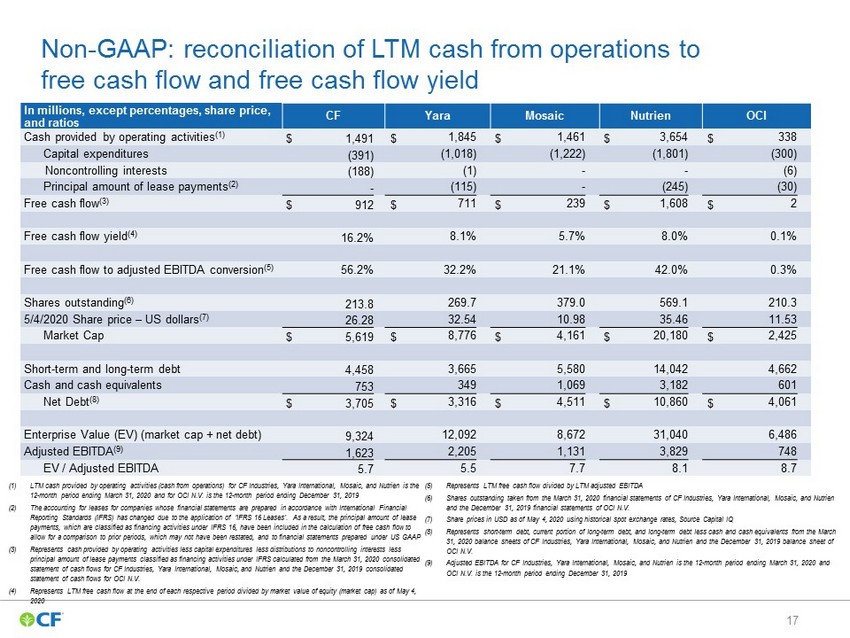

9 (1) Market capitalization is calculated as shares outstanding as of the end of each respective period multiplied by the closing s har e price of each company on May 4, 2020; see appendix for the calculation of market capitalization (2) Represents c ash p rovided by operating a ctivities (cash from operations) less capital expenditures less distributions to noncontrolling interests less principal amount of lease payments classified as financing activities under IFRS; see appendix for reconciliation of free cash flow (3) Represents LTM free cash flow divided by LTM adjusted EBITDA (or EBITDA excluding special items); see appendix for the calcul ati on of free cash flow and for reconciliation of CF LTM (1Q20) adjusted EBITDA 912 711 239 1,608 2 (400) - 400 800 1,200 1,600 2,000 CF Yara Mosaic Nutrien OCI CF continues to generate significant free cash flow Free cash flow compared to peers (2) USD in millions LTM 4Q19 Cash from operations (USD in millions) Market Cap (1) (USD in millions) CF $1,491 OCI $338 Nutrien $3,654 Mosaic $1,461 Yara $1,845 $5,619 $8,776 $4,161 $20,180 $2,425 42.0% 0. 3 % 21.1% 32.2% 56.2% FCF to Adjusted EBITDA Conversion (3) LTM 1Q20

10 5.7 5.5 7.7 8.7 8.1 0 2 4 6 8 10 16.2% 8.1% 5.7% 8.0% 0.1% 0% 2% 4% 6% 8% 10% 12% 14% 16% CF YAR MOS NTR OCI CF offers investors industry best free cash flow yield CF YAR MOS NTR OCI EV / Adj. EBITDA (2)(3) FCF Yield (1) LTM 4Q19 LTM 4Q19 (1) Represents LTM free cash flow divided by market value of equity (market cap) as of May 4, 2020, LTM free cash flow for CF Ind ust ries, Yara International, Mosaic, and Nutrien is the 12 - month period ending March 31, 2020 and OCI N.V. is the 12 - month period ending December 31, 2019; see appendix for reconciliation of free cash flow and calculation of market capitaliza tion (2) Enterprise value (EV) is calculated as the sum of market cap and net debt; see appendix for calculation of EV (3) Represents LTM adjusted EBITDA (or EBITDA excluding special items) as reported by CF Industries, Yara International, Mosaic, Nut rien and OCI N.V.; see appendix for reconciliation of CF LTM (1Q20) adjusted EBITDA Source : Capital IQ May 4, 2020 LTM 1Q20 LTM 1Q20

11 Capital Management • The Company repurchased approximately 2.6 million shares for $100 million during the first quarter of 2020 • Since the share repurchase authorization was announced in February 2019, the Company has repurchased approximately 10.2 million shares for $437 million Capital allocation h ighlights Capital structure & f ixed charges • Lowered fixed charges to provide greater long - term flexibility • C ash interest exp ense ~$190 million annually • Target liquidity: > $1 billion • Dividend of $1.20 per share annually • 2020 capex expected to be approximately $350 - 400 million; this is lower than the previous estimate of $400 - 450 million due to certain activities likely to b e deferred as a result of the COVID - 19 pandemic Philosophy remains unchanged • Return to investment grade and consistently return excess cash to shareholders in a timely fashion through dividends and share repurchases • Pursue growth within our strategic fairway, where returns exceed the risk - adjusted cost of capital

12 2.6 6.0 (1) 6.0 6.1 6.6 (2) 6.6 7.0 (3) 8.1 (4) 8.1 8.2 (5) 8.2 8.2 All N production numbers based on year - end figures per 10 - K filings (1) Beginning in 2010 includes capacity from Terra Industries acquisition (2) Beginning in 2013 includes incremental 34% of Medicine Hat production to reflect CF acquisition of Viterra's interests (3) Beginning in 2015 includes incremental 50% interest in CF Fertilisers UK acquired from Yara International (4) Beginning in 2016 excludes nitrogen equivalent of 1.1 million tons of urea and 0.58 million tons of UAN under CHS supply agreement and includes expansion project capacity at Donaldsonville and Port Neal (5) Beginning in 2018 includes incremental 15% of Verdigris production to reflect CF’s acquisition of publicly traded TNH units (6) Share count based on end of year or quarter common shares outstanding. Share count prior to 2015 based on 5 - for - 1 split - adjusted shares Production Capacity (M nutrient tons) Annual Nitrogen Equivalent Tons per 1,000 Shares Outstanding CF Industries’ Nitrogen Volumes and Shares Outstanding as of Quarter - end Million Shares Outstanding (6) 2009 – Q1 2020 Nitrogen per share CAGR: 13.3% Capacity growth coupled with share repurchases continue to drive nitrogen participation per share 11 17 18 19 24 27 30 35 35 37 38 39 0 50 100 150 200 250 300 350 400 0 5 10 15 20 25 30 35 40 45 2009 2010 2011 2012 2013 2014 2015 2016 2017 2018 2019 Q1 2020

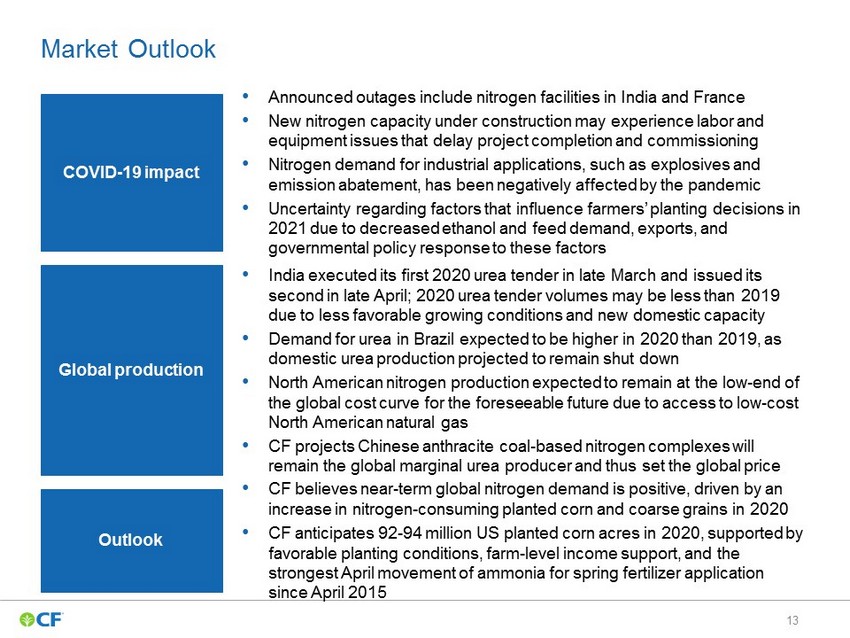

13 Global production Outlook COVID - 19 impact Market Outlook • A nnounced outages include nitrogen facilities in India and France • New nitrogen capacity under construction may experience labor and equipment issues that delay project completion and commissioning • Nitrogen demand for industrial applications, such as explosives and emission abatement, has been negatively affected by the pandemic • Uncertainty regarding factors that influence farmers’ planting decisions in 2021 due to decreased ethanol and feed demand, exports, and governmental policy response to these factors • India executed its first 2020 urea tender in late March and issued its second in late April; 2020 urea tender volumes may be less than 2019 due to less favorable growing conditions and new domestic capacity • Demand for urea in Brazil expected to be higher in 2020 than 2019, as domestic urea production projected to remain shut down • North American nitrogen production expected to remain at the low - end of the global cost curve for the foreseeable future due to access to low - cost North American natural gas • CF projects Chinese anthracite coal - based nitrogen complexes will remain the global marginal urea producer and thus set the global price • CF believes near - term global nitrogen demand is positive, driven by an increase in nitrogen - consuming planted corn and coarse grains in 2020 • CF anticipates 92 - 94 million US planted corn acres in 2020, supported by favorable planting conditions, farm - level income support, and the strongest April movement of ammonia for spring fertilizer application since April 2015

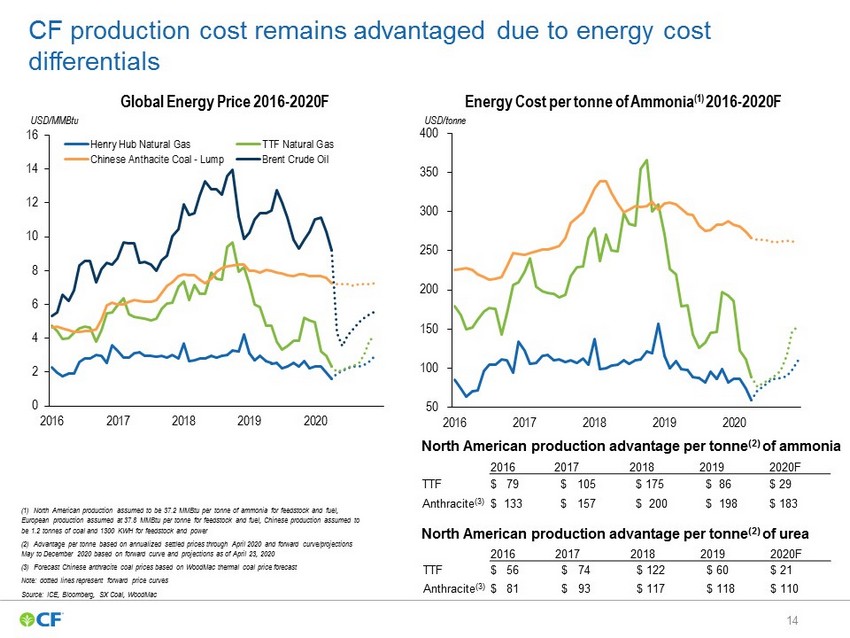

14 CF production cost remains advantaged due to energy cost differentials (1) North American production assumed to be 37.2 MMBtu per tonne of ammonia for feedstock and fuel, European production assumed at 37.8 MMBtu per tonne for feedstock and fuel, Chinese production assumed to be 1.2 tonnes of coal and 1300 KWH for feedstock and power (2) Advantage per tonne based on annualized settled prices through April 2020 and forward curve/projections May to December 2020 based on forward curve and projections as of April 23, 2020 (3) Forecast Chinese anthracite coal prices based on WoodMac thermal coal price forecast Note: dotted lines represent forward price curves Source: ICE, Bloomberg, SX Coal, WoodMac Global Energy Price 2016 - 2020F USD/MMBtu Energy Cost per tonne of Ammonia (1) 2016 - 2020F USD/ tonne North American production advantage per tonne (2) of ammonia 2016 2017 2018 2019 2020F TTF $ 79 $ 105 $ 175 $ 86 $ 29 Anthracite (3) $ 133 $ 157 $ 200 $ 198 $ 183 50 100 150 200 250 300 350 400 2016 2017 2018 2019 2020 0 2 4 6 8 10 12 14 16 2016 2017 2018 2019 2020 Henry Hub Natural Gas TTF Natural Gas Chinese Anthacite Coal - Lump Brent Crude Oil North American production advantage per tonne (2) of urea 2016 2017 2018 2019 2020F TTF $ 56 $ 74 $ 122 $ 60 $ 21 Anthracite (3) $ 81 $ 93 $ 117 $ 118 $ 110

15 Appendix

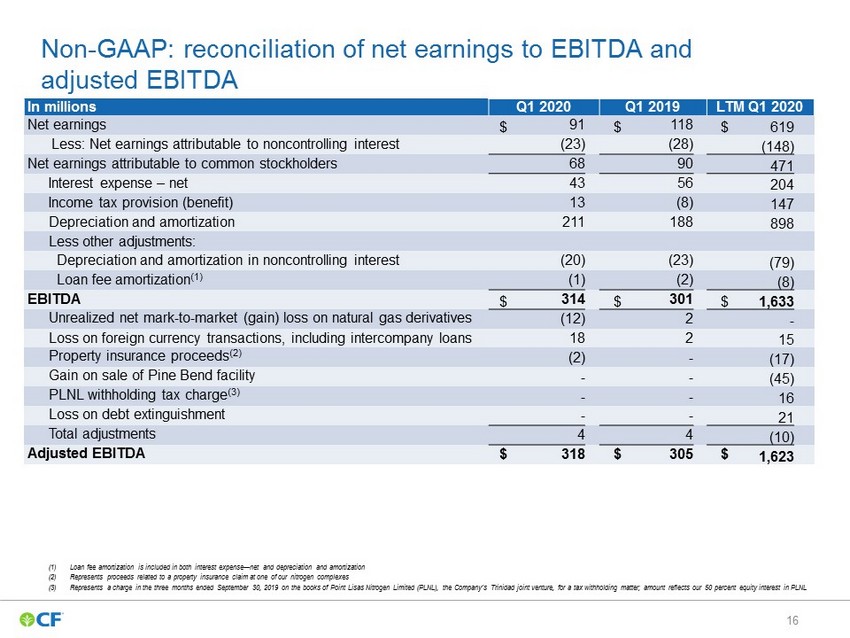

16 Non - GAAP: reconciliation of net earnings to EBITDA and adjusted EBITDA In millions Q1 20 20 Q1 2019 LTM Q1 2020 Net earnings $ 91 $ 118 $ 619 Less: Net earnings attributable to noncontrolling interest (23) (28) (148) Net earnings attributable to common stockholders 68 90 471 Interest expense – net 43 56 204 Income tax provision (benefit) 13 (8) 147 Depreciation and amortization 211 188 898 Less other adjustments: Depreciation and amortization in noncontrolling interest (20) (23) (79) Loan fee amortization (1) (1) (2) (8) EBITDA $ 314 $ 301 $ 1,633 Unrealized net mark - to - market (gain) loss on natural gas derivatives (12) 2 - Loss on foreign currency transactions, including intercompany loans 18 2 15 Property insurance proceeds (2) (2) - (17) Gain on sale of Pine Bend facility - - (45) PLNL withholding tax charge (3) - - 16 Loss on debt extinguishment - - 21 Total adjustments 4 4 (10) Adjusted EBITDA $ 318 $ 305 $ 1,623 (1) Loan fee amortization is included in both interest expense — net and depreciation and amortization (2) Represents proceeds related to a property insurance claim at one of our nitrogen complexes (3) Represents a charge in the three months ended September 30, 2019 on the books of Point Lisas Nitrogen Limited (PLNL), the Company’s Trinidad joint venture, for a tax withholding matter; amount reflects our 50 percent e qu ity interest in PLNL

17 Non - GAAP: reconciliation of LTM cash from operations to free cash flow and free cash flow yield In millions , except percentages , share price, and ratios CF Yara Mosaic Nutrien OCI Cash provided by operating activities (1) $ 1,491 $ 1,845 $ 1,461 $ 3,654 $ 338 C apital expenditures (391) (1,018) (1,222) (1,801) (300) Noncontrolling interests (188) (1) - - (6) Principal amount of lease payments (2) - (115) - (245) (30) Free cash flow (3) $ 912 $ 711 $ 239 $ 1,608 $ 2 Free cash flow yield (4) 16.2% 8.1% 5.7% 8.0% 0.1% Free cash flow to ad justed EBITDA conversion (5) 56.2% 32.2% 21.1% 42.0% 0.3% Shares outstanding (6) 213.8 269.7 379.0 569.1 210.3 5/4/2020 Share price – US dollars (7) 26.28 32.54 10.98 35.46 11.53 Market Cap $ 5,619 $ 8,776 $ 4,161 $ 20,180 $ 2,425 Short - term and long - term debt 4,458 3,665 5,580 14,042 4,662 Cash and cash equivalents 753 349 1,069 3,182 601 Net Debt (8) $ 3,705 $ 3,316 $ 4,511 $ 10,860 $ 4,061 Enterprise Value (EV) (market cap + net debt) 9,324 12,092 8,672 31,040 6,486 Adjusted EBITDA (9) 1,623 2,205 1,131 3,829 748 EV / Adjusted EBITDA 5.7 5.5 7.7 8.1 8.7 (1) LTM cash provided by operating activities (cash from operations) for CF Industries, Yara International, Mosaic, and Nutrien is the 12 - month period ending March 31, 2020 and for OCI N.V. is the 12 - month period ending December 31, 2019 (2) The accounting for leases for companies whose financial statements are prepared in accordance with International Financial Reporting Standards (IFRS) has changed due to the application of ‘IFRS 16 Leases’. As a result, the principal amount of lea se payments, which are classified as financing activities under IFRS 16, have been included in the calculation of free cash flow to allow for a comparison to prior periods, which may not have been restated, and to financial statements prepared under US GAAP (3) Represents c ash provided by operating activities less capital expenditures less distributions to noncontrolling interests less principal amount of lease payments classified as financing activities under IFRS calculated from the March 31, 2020 consolidated s tatement of cash f lows for CF Industries, Yara International, Mosaic, and Nutrien and the December 31, 2019 consolidated statement of cash flows for OCI N.V. (4) Represents LTM free cash flow at the end of each respective period divided by market value of equity (market cap) as of May 4, 2020 (5) Represents LTM free cash flow divided by LTM adjusted EBITDA (6) Shares outstanding taken from the March 31, 2020 financial statements of CF Industries, Yara International, Mosaic, and Nutrien and the December 31, 2019 financial statements of OCI N.V. (7) Share prices in USD as of May 4, 2020 using historical spot exchange rates, Source Capital IQ (8) Represents short - term debt, current portion of long - term debt, and long - term debt less cash and cash equivalents from the March 31, 2020 balance sheets of CF Industries, Yara International, Mosaic, and Nutrien and the December 31, 2019 balance sheet of OCI N.V. (9) Adjusted EBITDA for CF Industries, Yara International, Mosaic, and Nutrien is the 12 - month period ending March 31, 2020 and OCI N.V. is the 12 - month period ending December 31, 2019

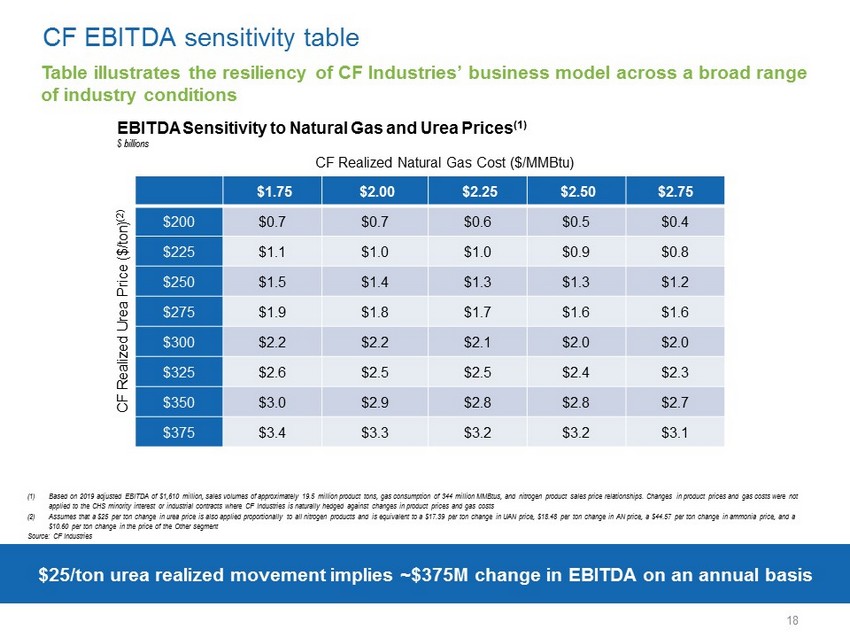

18 (1) Based on 2019 adjusted EBITDA of $ 1,610 million, sales volumes of approximately 19.5 million product tons, gas consumption of 344 million MMBtus, and nitrogen product sales price relationships. Changes in product prices and gas costs were not applied to the CHS minority interest or industrial contracts where CF Industries is naturally hedged against changes in product prices and gas costs (2) Assumes that a $25 per ton change in urea price is also applied proportionally to all nitrogen products and is equivalent to a $ 17.39 per ton change in UAN price, $ 18.48 per ton change in AN price, a $44.57 per ton change in ammonia price, and a $ 10.60 per ton change in the price of the Other segment Source: CF Industries CF EBITDA sensitivity table $25/ton urea realized movement implies ~$ 375M change in EBITDA on an annual basis Table illustrates the resiliency of CF Industries’ business model across a broad range of industry conditions CF Realized Natural Gas Cost ($/MMBtu ) CF Realized Urea Price ($/ ton ) (2) $ billions $1.75 $2.00 $2.25 $2.50 $2.75 $200 $0.7 $0.7 $0.6 $0.5 $0.4 $225 $1.1 $1.0 $1.0 $0.9 $0.8 $250 $1.5 $1.4 $1.3 $1.3 $1.2 $275 $1.9 $1.8 $1.7 $1.6 $1.6 $300 $2.2 $2.2 $2.1 $2.0 $2.0 $325 $2.6 $2.5 $2.5 $2.4 $2.3 $350 $3.0 $2.9 $2.8 $2.8 $2.7 $375 $3.4 $3.3 $3.2 $3.2 $3.1 EBITDA Sensitivity to Natural Gas and Urea Prices (1)