Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on July 9, 2014.

Registration No. 333-196875

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

IRADIMED CORPORATION

(Exact name of registrant as specified in its charter)

Delaware | 3841 | 73-1408526 | ||

(State or other jurisdiction of | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

1025 Willa Springs Dr.

Winter Springs, FL 32078

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Roger Susi

President

iRadimed Corporation

1025 Willa Springs Dr.

Winter Springs, FL 32078

(407) 677-8022

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to: | ||

Leib Orlanski, Esq. | Michael J. Kinkelaar, Esq. | |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ý

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer o (Do not check if a smaller reporting company) | Smaller reporting company ý |

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Proposed Maximum Aggregate Offering Price(1)(2) | Amount of Registration Fee(4) | ||

|---|---|---|---|---|

Common Stock, par value $0.0001 per share | $12,075,000 | $1,555.26 | ||

Underwriters' Warrant to Purchase Common Stock(3) | $— | $— | ||

Common Stock Underlying Underwriters' Warrants, $0.0001 par value per share(3) | $1,365,000 | $175.81 | ||

Total Registration Fee | $1,731.07 | |||

| ||||

- (1)

- Includes the aggregate offering price of additional shares the underwriters have the option to purchase in this offering to cover over-allotments, if any.

- (2)

- Estimated solely for purposes of calculating the registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended.

- (3)

- We have agreed to issue warrants exercisable within three years after the effective date of this registration statement representing 10% of the securities issued in the offering (the "Underwriter Warrant") to the underwriters. The initial issuance of the Underwriter Warrant and resales of shares of Common Stock issuable upon exercise of the Underwriter Warrant are registered hereby. See "Underwriting."

- (4)

- A total of $1,648.64 of the registration fee has been previously paid.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Commission acting pursuant to said section 8(a), may determine.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 9, 2014

![]()

1,750,000 Shares of Common Stock

This is the initial public offering of securities of iRadimed Corporation. We are offering to sell 1,750,000 shares of our common stock.

Prior to this offering, there has been no public market for our securities. The initial public offering price is expected to be between $5.00 and $6.00 per share. We intend to apply to list our shares of common stock on the NASDAQ Capital Market under the symbol "IRMD."

We are an "emerging growth company" and a "smaller reporting company" under federal securities laws and are subject to reduced public company reporting requirements. Investing in the common stock involves risks that are described in the "Risk Factors" section beginning on page 10 of this prospectus.

| | Per Share | Total | |||||

|---|---|---|---|---|---|---|---|

Public offering price | $ | $ | |||||

Underwriting discounts and commissions(1) | $ | $ | |||||

Proceeds, before expenses, to us | $ | $ | |||||

- (1)

- We have also granted warrants to the underwriters in connection with this offering. See "Underwriting" beginning on page 105 for a description of the compensation payable by us to the underwriters.

We have granted the underwriters a 45-day option to purchase a maximum of 262,500 additional shares from us at the public offering price, less the underwriting discounts and commissions, to cover over-allotments, if any.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Delivery of the shares will be made on or about , 2014.

Sole Book-Running Manager

Roth Capital Partners

Co-Manager

Monarch Capital Group

The date of this prospectus is , 2014

| | Page | |

|---|---|---|

Prospectus Summary | 1 | |

Offering Summary | 7 | |

Summary Financial and Other Data | 8 | |

Risk Factors | 10 | |

Special Note Regarding Forward-Looking Statements | 30 | |

Use of Proceeds | 32 | |

Dividend Policy | 33 | |

Capitalization | 34 | |

Dilution | 36 | |

Selected Financial and Other Data | 38 | |

Management's Discussion and Analysis of Financial Condition and Results of Operations | 41 | |

Business | 56 | |

Management | 81 | |

Executive and Director Compensation | 85 | |

Certain Relationships and Related Transactions | 91 | |

Beneficial Ownership of Common Stock | 92 | |

Description of Capital Stock | 94 | |

Shares Eligible for Future Sale | 99 | |

Material U.S. Federal Income Tax Considerations for Non-U.S. Holders | 101 | |

Underwriting | 105 | |

Legal Matters | 111 | |

Experts | 111 | |

Where You Can Find More Information | 111 | |

Index to Financial Statements | F-1 | |

Information Not Required in Prospectus | II-1 |

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. We take no responsibility for, and we provide no assurance as to the reliability of, any other information that others may give you. We are offering to sell, and seeking offers to buy, our securities only in jurisdictions where offers and sales are permitted. You should assume that the information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our securities. Our business, financial condition, results of operations, and prospects may have changed since that date.

Through and including , 2014 (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer's obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

For investors outside the U.S.: neither we nor the underwriters have done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the U.S. You are required to inform yourselves about and to observe any restrictions relating to this offering and the distribution of this prospectus.

Our name, our logo, and other trademarks or service marks of ours appearing in this prospectus are the property of iRadimed Corporation. Trade names, trademarks, and service marks of other companies appearing in this prospectus are the property of their respective holders.

i

We use industry and market data throughout this prospectus, which we have obtained from internal market research, independent industry publications, or other publicly available information. Some data is also based on our good faith estimates, which are derived from our internal research, industry publications, and our management's knowledge and experience in the markets in which we operate. Although we believe that each such source and our internal data are reliable as of their respective dates, the information contained in such sources has not been independently verified. While we are not aware of any misstatements regarding any industry and market data or our internal data presented herein, such data are subject to change based on various factors, including those discussed under the heading "Risk Factors" in this prospectus. We have not commissioned, nor are we affiliated with, any of the independent industry sources we cite.

ii

This summary highlights information contained in other parts of this prospectus. Because it is a summary, it does not contain all of the information that you should consider before investing in the shares of common stock. You should read the entire prospectus carefully, including "Risk Factors," "Selected Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations," Business," and our financial statements and related notes before deciding to invest in our common stock. References in this prospectus to "iRadimed," "our company," "we," "our," and "us" refer to iRadimed Corporation, unless the context indicates otherwise.

Our Company

We are the leading provider of non-magnetic intravenous ("IV") infusion pump systems that are safe for use during magnetic resonance imaging ("MRI") procedures. Electromechanical medical devices and pumps contain magnetic and electronic parts which generate radio frequency ("RF") noise, create interference and are dangerous to operate in the presence of the powerful magnet which drives an MRI. Our mRidium (3850/3860+) IV pump systems have been designed with non-ferrous parts, ceramic ultrasonic motors, non-magnetic mobile stand and other special features in order to safely and predictably deliver anesthesia and other IV fluids during various MRI procedures. Many critically-ill patients cannot be removed from their vital medications, and children and infants must generally be sedated in order to remain immobile during an MRI scan. Our pump solution provides a seamless approach to providing IV fluids before, during and after an MRI scan. Given the rate of new MRI installations, expanding use of MRI procedures, growing attention to patient safety, and limited direct competition, we believe the market opportunity for our mRidium MRI compatible IV infusion pumps will grow over the next five years to over $500 million, with additional revenue generated from the sale of disposable IV sets used during every patient infusion.

In fiscal year 2012, we undertook a direct sales strategy in the United States. Today, our direct sales force consists of eight sales representatives, supplemented by two clinical support representatives, and our goal is to expand our U.S. sales force to 10 sales representatives and three clinical support representatives by the end of 2014. We have distribution agreements with 35 independent distributors selling our products internationally.

As of March 31, 2014 we estimate that we had approximately 1,917 IV infusion pump systems installed globally. Each system consists of an mRidium MRI compatible IV infusion pump, non-magnetic mobile stand, and proprietary disposable IV tubing sets and many systems contain additional optional upgrade accessories. We generate revenue from the one-time sale of pumps and accessories, ongoing service contracts and the sale of our proprietary disposable IV tubing sets, which are required to be used by our pump systems during each patient infusion. Our revenue growth has accelerated since initiating our direct sales effort. In fiscal year 2013, our revenue reached $11.3 million and our operating profit was $2.8 million representing an operating margin of 24.6%. This operating margin reflects the blended results of our IV infusion pumps, pump upgrades and disposable IV tubing sets.

Today, we believe we face limited direct competition for our MRI compatible IV infusion pump system. During 2013, our largest competitor announced its decision to commence removal of its pump systems from the U.S. market, and to discontinue support throughout the world by June 30, 2015 due to ongoing regulatory issues. Since our inception, we have initiated two voluntary recalls on some of our pump systems when we became aware of operating issues in field use. However, we are currently selling all of our pump systems, and we intend to aggressively market our mRidium 3860+ IV pump

1

system to the current users of our competitor's discontinued pump system as well as to new acute care facilities and trauma hospitals globally.

Our Products

The mRidium MRI compatible IV infusion pump system is based upon a patented non-magnetic ultrasonic motor and fluid control system and other uniquely-designed non-magnetic parts in order to provide accurate and dependable fluid delivery to patients undergoing a magnetic resonance ("MR") procedure. Our mRidium MRI compatible IV infusion pump system has been designed to offer numerous advantages to hospitals, clinicians and patients. mRidium's strengths include the following:

- •

- The only truly non-magnetic MRI compatible IV infusion pump system specifically designed and built for the MRI environment.

- •

- A mobile, rugged, easy-to-operate, and reliable system with a strong safety track record.

- •

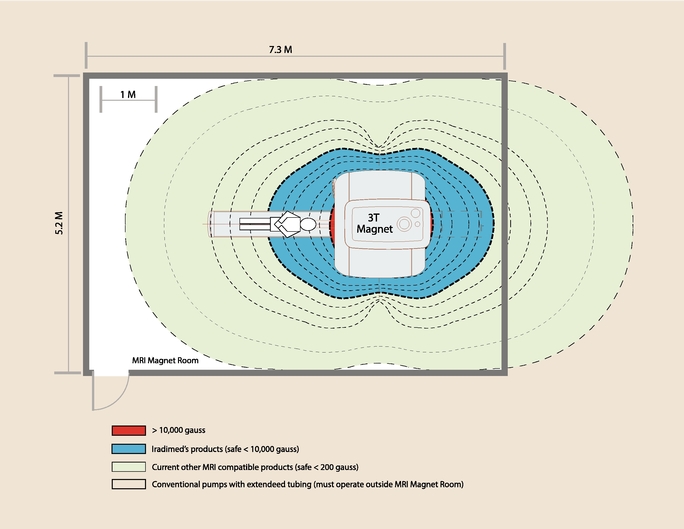

- Able to operate virtually anywhere in the MRI scanner room; approved for use in the presence of 0.2T to 3T magnets and fully operational in up to a 10,000 gauss magnetic field.

- •

- The only non-magnetic MRI compatible IV infusion pump available with a Dose Error Reduction System ("DERS") to reduce the risk of medication errors and simplify clinician monitoring.

- •

- Available with a wireless remote display/control providing clinicians and technicians control and visibility from outside of the MRI scanner room.

- •

- Available with an add-on channel allowing for the easy addition of a second IV line for patients requiring multiple IV medications at a low incremental cost to the hospital.

- •

- Available with a built-in SpO2 monitor using Masimo SET® technology and a specially designed fiber optic SpO2 sensor allowing one device to monitor oxygen saturation levels while safely providing IV infusion during an MRI procedure.

Our MRI compatible IV infusion pump systems include the 3850, 3850R and 3860+ MRI compatible IV infusion pump, proprietary single-use IV tubing sets, a non-magnetic pole and a lithium battery. The newest model, 3860+, is currently being given the greatest marketing effort as we move to obsolete the 3850 type. In addition, we offer optional system upgrades including the 3865 Remote Display/Control, 3861 Side Car, DERS software feature, and an SpO2 sensor.

Market Opportunity

MRI provides physicians a noninvasive method to visualize vital organs and to identify blockages, growths and other difficult to detect diseases, conditions and other valuable diagnostic information. Hospitals and other medical facilities have been increasingly developing and using MRI for new procedures. These procedures include cardiac stress testing, intraoperative MRI and neurology MRI techniques. We believe that our mRidium products offer a unique and effective way to offer delivery of critical IV fluids safely and accurately in the expanding MRI field. While the benefits and utility of MRI systems and interventional MR are manifest and increasing, there are hazards intrinsic to the MR environment which must be respected. The MRI suite is a harsh place for medical devices, and safe and proper patient care requires specialty equipment that is specifically designed and built for the MR environment.

Intravenous fluids are needed during MRI procedures for many different reasons other than as contrast enhancement agents. Infusion pumps are often required in the MR scan room for patients who are not able to lie still without sedation or who require critical medications. For those medical facilities

2

that do not currently own an MRI compatible IV infusion pump, one of the most common methods is to attempt to use a conventional (magnetic) pump with long IV lines at a great distance from the patient and MR machine or from outside the MRI scanner room. However, overextended tubing can cause inaccurate drug delivery and false alarms or, more seriously, delayed alarms for equipment issues such as occlusion, especially when low-delivery rates are being used. Such makeshift extension sets can also affect the effectiveness of fluid delivery. A user's adjustment of dosage and other settings may take longer to reach the patient due to the over-extended tubing, with an attendant waste of oftentimes expensive drugs.

More seriously, there are risks in using a conventional IV pump that is mistakenly believed to be positioned at a safe distance from the MR scanner. The invisible powerful magnetic fields present during the MR procedure may result in metal objects in the MR environment being drawn with great force into the bore of the MR system, resulting in potentially deadly projectiles. Moreover, an MR scanner's radio frequency and time variant electro-magnetic field can induce currents in cables and other conductive materials near the MR system and cause the cables to heat. Hot cables may result in burns if they come into contact with a patient. Other problems in working in a MR environment include devices malfunctioning and low-quality images due to artifacts caused by RF interference.

During 2012, our only direct competitor in the MRI compatible IV infusion pump business, Bayer Radiology (formerly MEDRAD, Inc.), became the subject of an FDA recall with respect to its market-leading Continuum device. In late 2013, Bayer Radiology announced to its customers its decision to remove all Continuum pumps from the market. Bayer Radiology currently intends to complete its removal of its Continuum pumps no later than June 30, 2015, at which time Bayer Radiology will end its limited supply of its proprietary consumable IV sets that some current customers are receiving. As a result of Bayer Radiology's announced exit from the market, we anticipate that many Continuum customers will replace their MRI compatible pumps with our mRidium 3860+. Based on this exit from the market, plus the estimated size of the untapped portion of the market for MRI compatible IV infusion pumps, we believe our current market opportunity represents approximately 19,800 pump systems.

Our Business Strategy

Our goal is to provide access to MRI diagnostics to the patients who need assistance from IV pumps in the harsh magnetic MRI environment. We seek to grow our business by, among other things:

- •

- Driving market awareness of MRI compatible IV infusion pumps and the safety risks associated with using conventional IV pumps with long IV lines. We believe that the largest potential market for our MRI compatible IV infusion pumps is the segment of the market that is currently using workaround solutions. Such solutions include using conventional pumps outside the MRI scanner room and attaching multiple extension IV tubing sets through the wall or under the door into the magnet room to reach the patient. This practice of makeshift setups is fraught with risks to the patient and unnecessary costs and inefficiencies. We believe that increased market awareness and education will be required for these customers to appreciate the value for patients and the hospital of an efficient and patient-safe MRI environment which includes MRI compatible IV infusion pumps.

- •

- Expanding our MRI-focused sales force and customer service teams. We feel the single greatest impact of our commercialization strategy is the continued development and expansion of our direct sales force. Since there is currently no direct competitor for our MRI compatible IV infusion pump in the U.S., our focus is on expansion of the market through better education on advantages to patients, clinicians and hospitals of our pump systems and the shortcomings of current workaround solutions. Our challenge in the past

3

- •

- Continuing to innovate with MRI compatible patient care products. Our management team collectively has more than 100 years of experience with MRI compatible products. We have entrenched relationships with many of the industry's top thought leaders, and we have, and will continue to, closely collaborate with them to build upon mRidium's innovative MRI compatible technologies to create next generation pump systems and other MRI compatible products. We currently have under development a new MRI compatible resuscitation device which includes multi-parameter vital signs, and are researching the market for a patient thermal management unit.

- •

- Acquiring synergistic MRI patient care companies or products where we can leverage our experience and organization. We have an experienced team of engineering and operations managers committed to improving on existing MRI patient care designs through our internal development efforts and the acquisition of technologies and intellectual property of others. We have an effective and growing direct sales organization in the U.S. and a team of experienced international distributors that can effectively go to market with additional MRI patient care products. We intend to actively analyze opportunities to improve our product mix and profitability.

has been an understaffed sales team and our limited ability to educate new potential customers. We intend to devote a significant amount of time and resources to ensure that we provide our customers with a first-class clinical education to facilitate the adoption of our products. We believe that educated customers and potential customers, coupled with a positive user experience, will be critical to driving increased rates of utilization of our pump systems and their associated consumable IV sets.

Selected Risk Factors Associated with Our Business

An investment in our common stock involves substantial risks and uncertainties that may adversely affect our business, financial condition, results of operations, and cash flows. You should fully read and consider the information set forth under the "Risk Factors" section beginning on page 10 and all other information included in this prospectus before investing in our common stock. Some of the more significant risks relating to an investment in our company include the following:

- •

- Our financial performance is currently dependent on a single product which could be rendered obsolete or economically impractical by numerous factors, many of which are beyond our control;

- •

- We have single-source suppliers for multiple components of our products, and the disruption of any part of our supply chain could negatively impact our business;

- •

- If we or our suppliers fail to obtain, or experience delays in obtaining regulatory approval, our business could suffer;

- •

- We manufacture and store our products at a single facility;

- •

- We are highly dependent on our founder, Chief Executive Officer, President and controlling shareholder, Roger Susi, who will be able to exert significant control over matters subject to stockholder approval;

- •

- If we fail to maintain relationships with group purchasing organizations, sales of our products could decline;

- •

- Sales of our products generally require a lengthy sales cycle, which entails the passage of three to six months between initial discussions and the sale;

4

- •

- We rely on distributors to sell our products outside the U.S., and if they do not continue to purchase products from us our revenues could decline;

- •

- We may be unable to scale our operations successfully;

- •

- We may incur substantial product liability losses or become subject to other lawsuits relating to our products or business;

- •

- Our success depends on our ability to protect our intellectual property, and we cannot guarantee that the steps we have taken or will take in the future will be adequate;

- •

- The market for our stock is likely to be illiquid meaning that it may be difficult for you to sell your stock in the future;

- •

- If you purchase shares of common stock in this offering, you will incur immediate and substantial dilution; and

- •

- We may need to raise additional capital.

Corporate Information

Our company is incorporated under the name iRadimed Corporation in Delaware. We were originally incorporated in Oklahoma under the name IRI Development, Inc. in 1992, and we merged our Oklahoma corporation into the newly formed Delaware corporation in April 2014. Our principal executive offices are located at 1025 Willa Springs Dr., Winter Springs, FL 32078, and our telephone number is (407) 677-8022. Our internet address is www.iradimed.com. Information contained in, or accessed through, our website is not a part of this prospectus.

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act ("JOBS Act"), enacted in April 2012. An "emerging growth company" may take advantage of reduced reporting requirements that are otherwise applicable to public companies. These reduced reporting requirements include:

- •

- not being required to comply with the audit or attestation requirements of Section 404(b) of the Sarbanes-Oxley Act of 2002, as amended ("Sarbanes-Oxley Act");

- •

- reduced disclosure obligations regarding executive compensation in this prospectus and in our future periodic reports, proxy statements and registration statements; and

- •

- not being required to hold a nonbinding advisory vote on executive compensation or to seek stockholder approval of any golden parachute payments not previously approved.

We may take advantage of these reduced reporting obligations until the last day of our fiscal year following the fifth anniversary of the date of the first sale of our common stock pursuant to an effective registration statement under the Securities Act of 1933, as amended ("Securities Act"). This fifth anniversary will occur in 2019. However, if certain events occur prior to the end of such five-year period, including if we become a "large accelerated filer," our annual gross revenue exceeds $1.0 billion or we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company.

5

The JOBS Act provides that an emerging growth company can utilize an extended transition period for complying with new or revised accounting standards. We are choosing to "opt out" of this transition period and, as a result, we will comply with new or revised accounting standards when they are required to be adopted by issuers. This decision to opt out of the extended transition period under the JOBS Act is irrevocable.

We are also currently considered a "smaller reporting company," which generally means that we have a public float of less than $75 million and annual revenues of less than $50 million during the most recently completed fiscal year. If we are still considered a "smaller reporting company" at such time as we cease to be an "emerging growth company," we will be subject to increased disclosure requirements. However, the disclosure requirements will still be less than they would be if we were not considered either an "emerging growth company" or a "smaller reporting company." Specifically, similar to "emerging growth companies", "smaller reporting companies" are able to provide simplified executive compensation disclosures in their filings; are exempt from the provisions of Section 404(b) of the Sarbanes-Oxley Act requiring that independent registered public accounting firms provide an attestation report on the effectiveness of internal control over financial reporting; and have certain other decreased disclosure obligations in their SEC filings, including, among other things, only being required to provide two years of audited financial statements in annual reports.

6

| Issuer | iRadimed Corporation | |

| Common stock offered by us | 1,750,000 shares (2,012,500 shares if the underwriters' over-allotment is exercised in full). | |

| Underwriters' over-allotment option | We have granted the underwriters a 45-day option to purchase up to a maximum of 262,500 additional shares from us at the public offering price, less the underwriting discounts and commissions, to cover over-allotments, if any. | |

| Common stock outstanding after this offering | 10,150,000 shares (10,412,500 shares if the over-allotment option is exercised in full). | |

| Participation by Insiders | The Chairman of our Board of Directors has agreed to purchase up to $500,000 of our common stock in this offering. | |

| Use of proceeds | We intend to use approximately $1.5 to $2.0 million of the net proceeds from this offering to invest in our sales and marketing efforts, approximately $1.0 to $1.5 million to fund research and development of our products and product candidates, and approximately $1.0 to $1.5 million for working capital and other general corporate purposes. We also plan to use the remainder of the net proceeds for potential acquisitions of products or businesses; however, we currently do not have any agreements or commitments relating to any potential acquisitions. See "Use of Proceeds." | |

| Risk factors | You should read the section entitled "Risk Factors" beginning on page 10 of this prospectus for a discussion of factors to consider carefully before deciding to invest in shares of our common stock. | |

| Proposed NASDAQ Capital Market Symbol | IRMD |

The number of shares of our common stock to be outstanding after this offering is based on a total of 7,000,000 shares of our common stock and 1,400,000 shares of our preferred stock, which will automatically convert into shares of common stock upon completion of this offering, outstanding as of March 31, 2014 and excludes:

- •

- 1,833,192 shares of common stock issuable upon exercise of options outstanding, with a weighted-average exercise price of $1.24 per share;

- •

- 175,000 shares of common stock issuable upon the exercise of the warrant to be issued to the underwriters as compensation in connection with this offering; and

- •

- 1,000,000 shares of common stock reserved for future grant under our 2014 Equity Incentive Plan.

Unless otherwise indicated, the information in this prospectus assumes:

- •

- the automatic conversion of all outstanding shares of preferred stock into 1,400,000 shares of common stock;

- •

- the 1.75 for 1 stock split ratio applied to all of our outstanding shares and stock options outstanding in connection with our reincorporation from Oklahoma to Delaware; and

- •

- no exercise of the underwriters' over-allotment option.

7

SUMMARY FINANCIAL AND OTHER DATA

The following tables summarize our financial and other data. You should read this summary financial and other data together with the section titled "Selected Financial and Other Data" included elsewhere in this prospectus and the section titled "Management's Discussion and Analysis of Financial Condition and Results of Operations" as well as our financial statements and related notes contained in this prospectus.

We have derived the statements of operations data for the years ended December 31, 2013 and 2012 from our audited financial statements and related notes contained in this prospectus. The summary financial data for the three months ended March 31, 2014 and 2013, and as of March 31, 2014, are derived from our unaudited financial statements and related notes contained in this prospectus and are not indicative of results to be expected for the full year. Moreover, our historical results are not necessarily indicative of the results that should be expected in the future.

| | Three Months Ended March 31, | Years Ended December 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2013 | 2012 | |||||||||

| | (unaudited) | | | ||||||||||

Statements of Operations Data: | |||||||||||||

Revenue | $ | 3,557,237 | $ | 2,628,269 | $ | 11,340,097 | $ | 7,685,061 | |||||

Cost of revenue(1) | 656,366 | 467,113 | 2,853,385 | 2,125,921 | |||||||||

| | | | | | | | | | | | | | |

Gross profit | 2,900,871 | 2,161,156 | 8,486,712 | 5,559,140 | |||||||||

| | | | | | | | | | | | | | |

Operating expenses: | |||||||||||||

General and administrative(1) | 1,092,695 | 503,189 | 2,392,305 | 1,550,034 | |||||||||

Sales and marketing(1) | 759,789 | 568,723 | 2,297,309 | 1,930,395 | |||||||||

Research and development(1) | 224,304 | 160,411 | 1,009,872 | 654,070 | |||||||||

| | | | | | | | | | | | | | |

Total operating expenses | 2,076,788 | 1,232,323 | 5,699,486 | 4,134,499 | |||||||||

| | | | | | | | | | | | | | |

Income from operations | 824,083 | 928,833 | 2,787,226 | 1,424,641 | |||||||||

Other income (expense), net | 3,452 | (3,340 | ) | (3,458 | ) | 7,424 | |||||||

| | | | | | | | | | | | | | |

Income before provision for income taxes | 827,535 | 925,493 | 2,783,768 | 1,432,065 | |||||||||

Provision for income taxes | 304,168 | 281,566 | 846,878 | 465,980 | |||||||||

| | | | | | | | | | | | | | |

Net income | $ | 523,367 | $ | 643,927 | $ | 1,936,890 | $ | 966,085 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Net income per share: | |||||||||||||

Basic | $ | 0.07 | $ | 0.09 | $ | 0.28 | $ | 0.14 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Diluted | $ | 0.06 | $ | 0.08 | $ | 0.22 | $ | 0.11 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Weighted average shares outstanding:(2) | |||||||||||||

Basic | 7,000,000 | 7,000,000 | 7,000,000 | 7,000,000 | |||||||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Diluted | 8,859,015 | 8,492,475 | 8,624,314 | 8,462,240 | |||||||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

Other Financial Data: | |||||||||||||

Non-GAAP income from operations(3) | $ | 986,892 | $ | 996,813 | $ | 3,059,145 | $ | 1,597,881 | |||||

Non-GAAP net income(4) | $ | 628,585 | $ | 685,011 | $ | 2,104,710 | $ | 1,062,606 | |||||

Free cash flow(5) | $ | 457,817 | $ | (72,319 | ) | $ | 1,311,222 | $ | 1,396,216 | ||||

- (1)

- Includes stock-based compensation expense as follows:

8

| | Three Months Ended March 31, | Years Ended December 31, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2014 | 2013 | 2013 | 2012 | |||||||||

| | (unaudited) | | | ||||||||||

Cost of revenue | $ | 959 | $ | 3 | $ | 13 | $ | 2,050 | |||||

General and administrative | 56,935 | 4,115 | 16,461 | 1,770 | |||||||||

Sales and marketing | 95,536 | 63,775 | 255,096 | 168,316 | |||||||||

Research and development | 9,379 | 87 | 349 | 1,104 | |||||||||

| | | | | | | | | | | | | | |

Total | $ | 162,809 | $ | 67,980 | $ | 271,919 | $ | 173,240 | |||||

| | | | | | | | | | | | | | |

| | | | | | | | | | | | | | |

- (2)

- The basic and diluted net income per common share data in the statement of operations data for the three months ended March 31, 2014 (unaudited) and 2013 (unaudited) and the years ended December 31, 2013 and 2012 take into account the 1.75:1 stock split effected in conjunction with our reincorporation from Oklahoma to Delaware. The number of diluted weighted average shares outstanding during each of the periods presented includes 1,400,000 shares of our outstanding convertible preferred stock, which will automatically convert into 1,400,000 shares of our common stock upon the closing of this offering.

- (3)

- Non-GAAP income from operations is a non-GAAP financial measure that we calculate as income from operations excluding stock-based compensation expense. For more information about non-GAAP income from operations and a reconciliation of non-GAAP income from operations to income from operations, the most directly comparable financial measure calculated and presented in accordance with U.S. Generally Accepted Accounting Principles ("GAAP"), see the section titled "Selected Financial and Other Data – Non-GAAP Financial Results."

- (4)

- Non-GAAP net income is a non-GAAP financial measure that we calculated as net income excluding stock-based compensation expense, net of tax. For more information about non-GAAP net income and a reconciliation of non-GAAP net income to net income, the most directly comparable financial measure calculated and presented in accordance with GAAP, see the section titled "Selected Financial and Other Data – Non-GAAP Financial Results."

- (5)

- Free cash flow is a non-GAAP financial measure that we calculate as net cash provided by operating activities less net cash used in investing activities for purchases of property and equipment. For more information about free cash flow and a reconciliation of free cash flow to net cash provided by operating activities, the most directly comparable financial measure calculated and presented in accordance with GAAP, see the section titled "Selected Financial and Other Data – Non-GAAP Financial Results."

| | | As of December 31, | ||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | As of March 31, 2014 | |||||||||

| | 2013 | 2012 | ||||||||

| | (unaudited) | | | |||||||

Balance Sheets Data: | ||||||||||

Cash and cash equivalents | $ | 2,908,641 | $ | 2,461,559 | $ | 1,697,306 | ||||

Working capital | $ | 5,338,852 | $ | 4,931,949 | $ | 2,665,444 | ||||

Total assets | $ | 7,758,562 | $ | 6,986,871 | $ | 5,554,212 | ||||

Total stockholders' equity | $ | 6,111,136 | $ | 5,422,784 | $ | 3,220,200 | ||||

9

Investing in our common stock involves a high degree of risk. You should carefully consider the risks and uncertainties described below, together with all of the other information contained in this prospectus, including our financial statements and the related notes thereto, before making a decision to invest in our common stock. Our future operating results may vary substantially from anticipated results due to a number of risks and uncertainties, many of which are beyond our control. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties that we are unaware of, or that we currently believe are not material, may also become important factors that affect us. The following discussion highlights some of these risks and uncertainties and the possible impact of these risks on future results of operations. If any of the following risks occur, our business, financial condition or results of operations could be materially and adversely affected. In that case, the market value of our stock could decline substantially and you could lose part or all of your investment.

Risks Relating to Our Business and Financial Condition

Our financial performance is currently dependent on a single product.

Our current revenue and profitability is dependent on the sale of the mRidium 3860+ and 3850/R MRI compatible IV infusion pump system and the ongoing sale of disposable tubing sets related to them. Sales of the mRidium 3860+ and 3850/R MRI compatible IV infusion pump systems comprised approximately 85% or $3.0 million of our net revenue for the three months ended March 31, 2014 and approximately 80%, or $8.9 million, of our net revenue for the year ended December 31, 2013. Our near-term revenue and profitability will, accordingly, be dependent upon our ability to successfully market and sell this Class II medical device. Should our mRidium pump encounter technical problems in the field, unexpected competition, or regulatory issues with the FDA, our revenue could be materially adversely impacted.

The mRidium 3860+ or 3850/R MRI compatible IV infusion pumps could be rendered obsolete or economically impractical by numerous factors, many of which are beyond our control, including:

- •

- entrance of new competitors into our markets;

- •

- loss of key relationships with suppliers, group purchasing organizations, or end-user customers;

- •

- manufacturing or supply interruptions;

- •

- product liability claims;

- •

- our reputation and product market acceptance; and

- •

- product recalls or safety alerts.

Any major factor adversely affecting the sale of our mRidium 3860+ MRI compatible IV infusion pump would cause our revenues to decline and have a material adverse impact on our business, financial condition and our common stock.

Our continued success depends on the integrity of our supply chain, including multiple single-source suppliers, the disruption of which could negatively impact our business.

Many of the component parts of our mRidium MRI compatible IV infusion pumps are obtained through supply agreements with third parties. Some of these parts require our partners to engage in complex manufacturing processes. In light of our dependence on third-party suppliers, several of which are single-source suppliers, we are subject to inherent uncertainties and risks related to their ability to

10

produce parts on a timely basis, to comply with product safety and other regulatory requirements and to provide quality parts to us at a reasonable price.

For example, we are dependent upon a single vendor for the ultrasonic motor at the core of our mRidium MRI compatible IV infusion pump. If this vendor fails to meet our volume requirements, which we anticipate will increase over time, or if the vendor becomes unable or unwilling to continue supplying motors to us, this would impact our ability to supply our pumps to customers until a replacement source is secured. Our executed agreement with this vendor provides that the price at which we purchase products from the vendor is determined by mutual agreement from time to time or should material costs change. Although we have had a long history of stable pricing with this supplier, this provision may make it difficult for us to continue to receive motors from this vendor on favorable terms or at all if we do not agree on pricing in the future. In such event, it could materially and adversely affect our commercial activities, operating results and financial condition.

In the near term, we do not anticipate finding alternative sources for our primary suppliers, including single source suppliers. Therefore, if our primary suppliers become unable or unwilling to manufacture or deliver materials, we could experience protracted delays or interruptions in the supply of materials which would ultimately delay our manufacture of products for commercial sale, which could materially and adversely affect our development programs, commercial activities, operating results and financial condition.

Additionally, any failure by us to forecast demand for, or to maintain an adequate supply of, raw materials or finished products could result in an interruption in the supply of certain products and a decline in our sales.

The manufacture of our products requires strict adherence to regulatory requirements governing medical devices and if we or our suppliers encounter problems our business could suffer.

The manufacture of our pumps and products must comply with strict regulatory requirements governing Class II medical devices in the U.S. and other regulatory requirements in foreign locations. Problems may arise during manufacturing, quality control, storage or distribution of our products for a variety of reasons, including equipment malfunction, failure to follow specific protocols and procedures, manufacturing quality concerns, or problems with raw materials, electromechanical, software and other components, supplier issues, and natural disasters. If problems arise during production of our pump, the batch may have to be discarded. Manufacturing problems or delays could also lead to increased costs, lost sales, damage to customer relations, failure to supply penalties, time and expense spent investigating the cause and, depending on the cause, similar losses with respect to other batches of products. If problems are not discovered before the product is released to the market, voluntary recalls, corrective actions or product liability related costs may also be incurred. Should we encounter difficulties in the manufacture of our products or be subject to a product recall, our business could suffer materially.

We manufacture and store our products at a single facility in Florida.

Until recently, we manufactured and stored our products at a single facility in Winter Park, Florida. We are in the process of moving into a new larger facility being built in nearby Winter Springs by Susi, LLC, an entity controlled by our founder, Roger Susi, in order to expand our production and storage capabilities to accommodate our expected growth. If by reason of fire, hurricane or other natural disaster, or for any other reason, the facility is destroyed or seriously damaged, our ability to provide products to our customers would be seriously interrupted or impaired and our operating results and financial condition would be negatively affected.

11

More than 10% of our accounts receivables were held by one customer during the past two fiscal years, and our inability to collect on our accounts receivables held by significant customers may have an adverse effect on our business operations and financial condition.

We market our products to end users in the United States and to distributors internationally. Sales to end users in the United States are generally made on open credit terms. Management maintains an allowance for potential credit losses. Accounts receivables for one customer accounted for 10.8% of our gross accounts receivable as of December 31, 2013, while another single customer accounted for 15.4% of our gross accounts receivable as of December 31, 2012. As a result, we are exposed to a certain level of concentration of credit risk. If a major customer experiences financial difficulties, the effect on us could be material and have an adverse effect on our business, financial condition and results of operations.

If we fail to maintain relationships with GPOs, sales of our products could decline.

Our ability to sell our products to U.S. acute care facilities and outpatient imaging centers depends in part on our relationships with group purchasing organizations ("GPOs"). Many existing and potential customers for our products are members of GPOs. GPOs negotiate pricing arrangements and contracts, which are sometimes exclusive, with medical supply manufacturers and distributors, and these negotiated prices are made available to a GPO's affiliated hospitals and other members. We pay the GPOs an administrative fee in the form of a percentage of the volume of products sold to their affiliated hospitals and other members. If we are not an approved provider selected by a GPO, affiliated hospitals and other members may be less likely to purchase our products. Should a GPO negotiate a sole source or bundling contract covering a future competitor's products, we may be precluded from making sales to members of that GPO for the duration of the contractual arrangement. Our failure to renew contracts with GPOs may cause us to lose market share and could have a material adverse effect on our sales, financial condition and results of operations. We currently have GPO contracts with four major GPOs, and one of these contracts will expire in 2014 unless it is renewed. In the future, if another competitive supplier emerges, and we fail to keep our relationships and develop new relationships with GPOs, our competitive position would likely suffer.

Cost-containment efforts of our customers and purchasing groups could adversely affect our sales and profitability.

Our MRI compatible IV infusion pumps are considered capital equipment by many potential customers, and hence changes in the budgets of healthcare organizations and the timing of spending under these budgets and conflicting spending priorities can have a significant effect on the demand for our products and related services. Any decrease in expenditures by these healthcare facilities could decrease demand for our products and related services and reduce our revenue.

Any failure in our efforts to educate clinicians, anesthesiologists, radiologists, and hospital administrators regarding the advantages of our products could significantly limit our product sales.

Our future success will require us to educate a sufficient number of clinicians, anesthesiologists, radiologists, hospital administrators and other purchasing decision-makers about our products and the costs and benefits of MRI compatible IV infusion pump systems. If we fail to demonstrate the safety, reliability and economic benefits of our products to hospitals and acute medical facilities, our products may not be adopted and our sales will suffer.

The lengthy sales cycle for the mRidium 3860+ MRI compatible IV infusion pump could delay our sales.

The decision-making process of customers is often complex and time-consuming. Based on our experience, we believe the period between initial discussions concerning the mRidium 3860+ MRI compatible IV infusion pump and a purchase of a unit is three to six months. The process can be

12

delayed as a result of capital budgeting procedures. Moreover, even if one or two units are sold to a hospital, we believe that it will take additional time and experience with the mRidium 3860+ MRI compatible IV infusion pump before other medical professionals routinely use the mRidium 3860+ MRI compatible IV infusion pump for other procedures and in other departments of the hospital. Such time would delay potential sales of additional units and disposable tubing or additional optional accessories to that medical facility or hospital. These delays could have an adverse effect on our business, financial condition and results of operations.

Because we rely on distributors to sell our products outside of the U.S., our revenues could decline if our existing distributors do not continue to purchase products from us or if our relationship with any of these distributors is terminated.

We rely on distributors for all of our sales outside the U.S. and hence do not have direct control over foreign sales activities. These distributors also assist us with regulatory approvals and the education of physicians and government agencies. Our revenues outside the U.S. represented approximately 28.6% of our net revenues in fiscal year 2013, and we intend to continue our efforts to increase our sales in Europe, Japan and other countries. If our existing international distributors fail to sell our products or sell at lower levels than we anticipate, we could experience a decline in revenues or fail to meet our forecasts. We cannot be certain that we will be able to attract new international distributors that market our products effectively or provide timely and cost-effective customer support and service. None of our existing distributors are obligated to continue selling our products.

If we do not successfully develop and commercialize enhanced products or new products that remain competitive, we could lose revenue opportunities and customers, and our ability to achieve growth would be impaired.

The medical device industry is characterized by rapid product development and technological advances, which places our products at risk of obsolescence. Our long-term success depends upon the development and successful commercialization of new products, new or improved technologies and additional applications for non-magnetic infusion technology. The research and development process is time-consuming and costly and may not result in products or applications that we can successfully commercialize. If we do not successfully adapt our technology, products and applications, we could lose revenue opportunities and customers. In addition, we may not be able to improve our products or develop new products or technologies quickly enough to maintain a competitive position in our markets and continue to grow our business.

We are highly dependent on our founder, CEO, President, Director and controlling shareholder, Roger Susi.

Roger Susi developed our mRidium MRI compatible IV infusion pump system, and we believe that he will play a significant role in our continued success and in the development of new products including an MRI compatible device for patient resuscitation. Our current and future operations could be adversely impacted if we were to lose his services. We intend to carry key man life insurance on Roger Susi in the amount of $2,000,000. Accordingly, our success will be dependent on appropriately managing the risks related to executing a succession plan for Mr. Susi on a timely basis.

If we fail to attract and retain the talent required for our business, our business could be materially harmed.

Competition for highly skilled personnel is often intense in the medical device industry, and more specifically in the MRI compatible medical device industry. A number of our executives and employees are former employees of Invivo Corporation, where Mr. Susi developed the first MRI compatible patient monitoring system. If our current employees with experience in the MRI compatible device industry leave our company, we may have difficulty finding replacements with an equivalent amount of experience and skill, which could harm our operations. Our future success will also depend in part on our ability to identify, hire and retain additional personnel, including skilled engineers to develop new

13

products, and executives to oversee our marketing, sales, customer support and production staff. We may not be successful in attracting, integrating or retaining qualified personnel to meet our current growth plans or future needs. Our productivity may be adversely affected if we do not integrate and train our new employees quickly and effectively.

Also, to the extent we hire personnel from competitors, we may be subject to allegations that we have improperly solicited, or that they have divulged proprietary or other confidential information, or that their former employers own their inventions or work product.

We may be unable to scale our operations successfully.

Our plan is to grow rapidly. Our growth, if it occurs as planned, will place significant demands on our management and manufacturing capacity, as well as our financial, administrative and other resources. We cannot guarantee that any of the systems, procedures and controls we put in place will be adequate to support the manufacture and distribution of our products. Our operating results will depend substantially on the ability of our officers and key employees to manage changing business conditions and to implement and improve our financial, administrative and other resources. If we are unable to respond to and manage changing business conditions, or the scale of our products, services and operations, then the quality of our services, our ability to retain key personnel and our business could be harmed.

We engage in related party transactions, which result in a conflict of interest involving our management.

We have engaged in the past, and continue to engage, in related party transactions, particularly between our company and Roger Susi and his affiliates. One significant related party transaction is the lease agreement between our company and Susi, LLC, an affiliate of Roger Susi, with respect to our planned facility in Winter Springs, Florida. Additional detail regarding this lease is included in the section entitled "Properties" on page 79 of this prospectus. In addition, related party transactions present difficult conflicts of interest, could result in disadvantages to our company and may impair investor confidence, which could materially and adversely affect us. Related party transactions could also cause us to become materially dependent on related parties in the ongoing conduct of our business, and related parties may be motivated by personal interests to pursue courses of action that are not necessarily in the best interests of our company and our stockholders. Please refer to the section entitled "Certain Relationships and Related Transactions" on page 91 for further detail regarding related party transactions and our company's policies and procedures with respect to such transactions.

Risks Related to Our Industry

We are subject to substantial government regulation that is subject to change and could force us to make modifications to how we develop, manufacture and price our products.

The medical device industry is regulated extensively by governmental authorities, principally the FDA in the U.S. and corresponding state and foreign regulatory agencies. The majority of our manufacturing processes are required to comply with quality systems regulations, including current good manufacturing practice requirements that cover the methods and documentation of the design, testing, production, control, quality assurance, labeling, packaging and shipping of our products. Failure to comply with applicable medical device regulatory requirements could result in, among other things, warning letters, fines, injunctions, civil penalties, repairs, replacements, refunds, recalls or seizures of products, total or partial suspensions of production, refusal of the FDA or other regulatory agencies to grant pre-market clearances or approvals for our products, withdrawals or suspensions of future current clearances or approvals and criminal prosecution.

14

In addition, our products are subject to pre-approval requirements by the FDA and similar international agencies that govern a wide variety of product activities from design and development to labeling, manufacturing, promotion, sales and distribution. Compliance with these regulations may be time consuming, burdensome and expensive for us. The failure to obtain, or the loss or suspension of any such pre-approval, would negatively affect our ability to sell our products, and harm our anticipated revenues.

Foreign governmental authorities that regulate the manufacture and sale of medical devices have become increasingly stringent and, to the extent we sell our products in foreign countries, we may be subject to rigorous regulation in the future. Regulatory changes could result in restrictions on our ability to carry on or expand our operations, higher than anticipated costs or lower than anticipated revenue.

If we fail to obtain, or experience significant delays in obtaining, FDA clearances or other necessary approvals to commercially distribute new products, our ability to grow will suffer.

Our current products are Class II medical devices and hence require regulatory pre-market approval by the FDA and other federal and state authorities prior to their sale in the U.S. Similar approvals are required by foreign governmental authorities for sale of our products outside of the U.S. We are responsible for obtaining the applicable regulatory approval for the commercial distribution of our products. As part of our growth strategy, we plan to seek approvals for new MRI compatible products. The process of obtaining approvals, particularly from the FDA, can be costly and time consuming, and there can be no assurance that we will obtain the required approvals on a timely basis, or at all. Failure to receive approvals for new products will hurt our ability to grow.

We are subject to risks associated with doing business outside of the U.S.

Sales to customers outside of the U.S. comprised approximately 28.6% of our revenue in fiscal 2013, and we expect that non-U.S. sales will contribute to future growth. A majority of our international sales originate from Europe and Japan, and we also make sales in Canada, Hong Kong, Australia, Mexico and certain parts of the Middle East. The risks associated with operations outside the United States include:

- •

- foreign regulatory and governmental requirements that could change and restrict our ability to manufacture and sell our products;

- •

- possible failure to comply with anti-bribery laws such as the U.S. Foreign Corrupt Practices Act and similar anti-bribery laws in other jurisdictions;

- •

- foreign currency fluctuations that can impact our financial statements when foreign figures are translated into U.S. dollars;

- •

- different local product preferences and product requirements;

- •

- trade protection and restriction measures and import or export licensing requirements;

- •

- difficulty in establishing, staffing and managing non-U.S. operations;

- •

- failure to maintain relationships with distributors, especially those who have assisted with foreign regulatory or government clearances;

- •

- changes in labor, environmental, health and safety laws;

- •

- potentially negative consequences from changes in or interpretations of tax laws;

- •

- political instability and actual or anticipated military or political conflicts;

15

- •

- economic instability and inflation, recession or interest rate fluctuations;

- •

- uncertainties regarding judicial systems and procedures; and

- •

- minimal or diminished protection of intellectual property.

These risks, individually or in the aggregate, could have an adverse effect on our results of operations and financial condition.

We may incur product liability losses, or become subject to other lawsuits related to our products, business, and insurance coverage could be inadequate or unavailable to cover these losses.

Our business is subject to potential product liability risks that are inherent in the design, development, manufacture and marketing of our medical devices and consumable products. We carry third party product liability insurance coverage to protect against such risks, but there can be no assurance that our policy is adequate. In the ordinary course of business, we may become the subject of product liability claims and lawsuits alleging that our products have resulted or could result in an unsafe condition or injury to patients. Any product liability claim brought against us, with or without merit, could be costly to defend and could result in settlement payments and adjustments not covered by or in excess of our product liability insurance. We currently have third-party product liability insurance with maximum coverage of $3,000,000; however, such coverage requires a substantial deductible that we must pay before becoming eligible to receive any insurance proceeds. The deductible amount is currently equal to $25,000 per occurrence and $125,000 in the aggregate. We will have to pay for defending product liability or other claims that are not covered by our insurance. These payments could have a material adverse effect on our profitability and financial condition. Product liability claims and lawsuits, safety alerts, recalls or corrective actions, regardless of their ultimate outcome, could have a material adverse effect on our business, financial condition, reputation and on our ability to attract and retain customers. In addition, we may not be able to obtain insurance in the future on terms acceptable to us or at all.

Defects or failures associated with our products and/or our quality control systems could lead to the filing of adverse event reports, recalls or safety alerts and negative publicity and could subject us to regulatory actions.

Safety problems associated with our products could lead to a product recall or the issuance of a safety alert relating to such products and result in significant costs and negative publicity. An adverse event involving one of our products could require us to file an adverse event report with the FDA. Such disclosure could result in reduced market acceptance and demand for all of our products, and could harm our reputation and our ability to market our products in the future. In some circumstances, adverse events arising from or associated with the design, manufacture or marketing of our products could result in the suspension or delay of regulatory reviews of our applications for new product approvals or clearances.

We may also voluntarily undertake a recall of our products or temporarily shut down production lines based on internal safety, quality monitoring and testing data. For example, in August 2012, we initiated a voluntary recall of a particular lot of mRidium Series 1000 MR Infusion Sets, Type 1058 MR IV, an extension set used with our mRidium MRI compatible IV infusion pumps, due to an out-of-specification dimension of one section of the IV set. We retrieved and destroyed all unused infusion sets subject to the recall. In July 2013, the FDA notified us that it had concluded its audit and confirmed that the recall was considered terminated. In July 2013, we issued a voluntary recall of our MRI compatible IV infusion pump systems equipped with mRidium 1145 DERS Drug Library due to their potential risk in providing an incorrect recommended value for the infusion rate during the pump's initial infusion setup. To avoid future product recalls we have made and continue to invest in our quality systems, processes and procedures. We will continue to make improvements to our products and systems to further reduce issues related to patient safety. However, there can be no assurance our

16

systems will be sufficient. Future quality concerns, whether real or perceived, could adversely affect our operating results. For a more detailed description of recalls, see the section captioned "Governmental Regulation and Other Matters" in the "Business" section on page 73.

Our products or product types could be subject to negative publicity, which could have a material adverse effect on our financial position and results of operations and could cause the market value of our common stock to decline.

The market's perception of our products could be harmed if any of our products or similar products offered by others in our industry become the subject of negative publicity due to a product safety issue, withdrawal, recall, or are proven or are claimed to be harmful to patients. The harm to market perception may have a material adverse effect on our business, financial position and results of operations and could cause the market value of our common stock to decline.

Any acquisitions of technologies, products and businesses, may be difficult to integrate, could adversely affect our relationships with key customers, and/or could result in significant charges to earnings.

We plan to periodically review potential acquisitions of technologies, products and businesses that are complementary to our products and that could accelerate our growth. However, our company has never completed an acquisition and there can be no assurance that we will be successful in finding any acquisitions in the future. The process of identifying, executing and realizing attractive returns on acquisitions involves a high degree of uncertainty. Acquisitions typically entail many risks and could result in difficulties in integrating operations, personnel, technologies and products. If we are not able to successfully integrate our acquisitions, we may not obtain the advantages and synergies that the acquisitions were intended to create, which may have a material adverse effect on our business, results of operations, financial condition and cash flows, our ability to develop and introduce new products and the market price of our stock.

Recent U.S. healthcare policy changes, including the Affordable Care Act and PPACA, may have a material adverse effect on our financial condition and results of operations.

The Patient Protection and Affordable Care Act, as amended by the Health Care and Education Affordability Reconciliation Act (collectively, the "PPACA"), enacted in March 2010, implemented changes that are expected to significantly impact the medical device industry. Beginning on January 1, 2013, the Affordable Care Act imposed a 2.3% excise tax on sales of products defined as "medical devices" by the regulations of the FDA. We believe that all of our medical products are "medical devices" within the meaning of the FDA regulations. For the three months ended March 31, 2014 and the year ended December 31, 2013, we recorded $51,333 and $161,246, respectively, in medical device taxes, which is included as a component of general and administrative expense. If this tax rate is increased in future years, it would negatively impact our operating results.

Other significant measures contained in the PPACA include research on the comparative clinical effectiveness of different technologies and procedures, initiatives to revise Medicare payment methodologies, such as bundling of payments across the continuum of care by providers and physicians, and initiatives to promote quality indicators in payment methodologies. The PPACA also includes significant new fraud and abuse measures, including required disclosures of financial arrangements with physician customers, lower thresholds for violations and increasing potential penalties for such violations. In addition, the PPACA established an Independent Payment Advisory Board ("IPAB"), to reduce the per capita rate of growth in Medicare spending. The IPAB has broad discretion to propose policies to reduce health care expenditures, which may have a negative impact on payment rates for services, including treatments and procedures which incorporate use of our products. The IPAB proposals may impact payments for treatments and procedures that use our technology beginning in 2016 and for hospital services beginning in 2020, and may indirectly reduce demand for our products.

17

The taxes imposed by the new federal legislation and the expansion in government's effect on the U.S. healthcare industry may result in decreased profits to us, lower reimbursements by payers for our products or reduced medical procedure volumes, all of which may adversely affect our business, financial condition and results of operations.

We are subject to healthcare fraud and abuse regulations that could result in significant liability, require us to change our business practices and restrict our operations in the future.

We and our customers are subject to various U.S. federal, state and local laws targeting fraud and abuse in the healthcare industry, including anti-kickback and false claims laws. Violations of these laws are punishable by criminal or civil sanctions, including substantial fines, imprisonment and exclusion from participation in healthcare programs such as Medicare and Medicaid, and Veterans' Administration health programs and health programs outside the U.S. These laws and regulations are broad in scope and are subject to evolving interpretations, which could require us to alter one or more of our sales or marketing practices. In addition, violations of these laws, or allegations of such violations, could disrupt our business and result in a material adverse effect on our sales, profitability and financial condition. Furthermore, since many of our customers rely on reimbursement from Medicare, Medicaid and other governmental programs to cover a substantial portion of their expenditures, if we or our customers are excluded from such programs as a result of a violation of these laws, it could have an adverse effect on our results of operations and financial condition. We have developed and implemented business practices and processes to train our personnel to perform their duties in compliance with healthcare fraud and abuse laws and conduct informal oversight to detect and prevent these types of fraud and abuse. However, we lack formal written policies and procedures at this time. If we are unable to formally document and implement the controls and procedures required in a timely manner or we are otherwise found to be in violation of such laws, we might suffer adverse regulatory consequences or face criminal sanctions, which could harm our operations, financial reporting or financial results.

The environment in which we operate makes it increasingly difficult to forecast our business performance.

Significant changes and volatility in the global financial markets, in the consumer and business environment, and our general competitive landscape may make it increasingly difficult for us to predict our revenues and earnings into the future. Our quarterly sales and profits depend substantially on the volume and timing of orders fulfilled during the quarter, and such orders are difficult to forecast. Product demand is dependent upon the capital spending budgets of our customers and prospects as well as government funding policies, and matters of public policy as well as product and economic cycles that can affect the spending decisions of these entities. As a result, any revenue or earnings guidance or outlook which we have given or might give may turn out to be inaccurate. Though we will endeavor to give reasonable estimates of future revenues and earnings at the time we give such guidance, based on then-current conditions, there is a significant risk that such guidance or outlook will turn out to be incorrect. Historically, companies that have overstated their operating guidance have suffered significant declines in their stock price when such results are announced to the public.

We could be adversely affected by violations of the U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery laws.

The U.S. Foreign Corrupt Practices Act and similar worldwide anti-bribery laws generally prohibit companies and their intermediaries from making improper payments to non-U.S. officials for the purpose of obtaining or retaining business. We intend to adopt policies for compliance with these anti-bribery laws, which often carry substantial penalties. We cannot assure you that our internal control policies and procedures always will protect us from reckless or other inappropriate acts committed by our affiliates, employees or agents. Violations of these laws, or allegations of such violations, could have a material adverse effect on our business, financial position and results of operations and could cause the market value of our common stock to decline.

18

There are inherent uncertainties involved in estimates, judgments and assumptions used in the preparation of financial statements in accordance with United States GAAP. Furthermore, portions of GAAP require the use of fair value mathematical models which are variable in application and methodology from appraiser to appraiser. Any changes in estimates, judgments and assumptions used could have a material adverse effect on our business, financial position and operating results.

The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the amounts reported in the financial statements and accompanying notes. Such assumptions and estimates include those related to revenue recognition, accruals for product returns, valuation of inventory, impairment of intangibles and long-lived assets, accounting for income taxes and stock-based compensation and reserves for potential litigation. We base our estimates on historical experience and on various other assumptions that we believe to be reasonable under the circumstances, as discussed in greater detail in the section titled "Management's Discussion and Analysis of Financial Condition and Results of Operations." Our actual operating results may differ and fall below our assumptions and the financial forecasts of securities analysts and investors, resulting in a significant decline in our stock price.