UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM SB-2

Registration Statement under the Securities Act of 1933

HEMIS CORPORATION

(Name of Small Business Issuer in its Charter)

| NEVADA | 1000 | 20-2749916 |

| (State or Jurisdiction of | (Primary Standard Industrial | (I.R.S. Employer |

| Incorporation or Organization) | Classification Code Number) | Identification No.) |

Bettlistrasse 35

8600 Dübendorf, Switzerland

(702) 387 2382

(Address and telephone number of principal executive offices)

EastBiz, Inc.

5348 Vegas Drive, #226

Las Vegas, Nevada 89108 USA

(702) 871 8678

(Name, address and telephone number of agent for service)

With a copy to:

Penny Green, Bacchus Law Group

1511 West 40th Avenue, Vancouver, BC V6M 1V7

Tel (604) 732 4804 Fax (604) 408 5177

Approximate Date of Proposed Sale to the Public:As soon as practicable after this Registration Statement is declared effective.

If any securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. [X]

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act Registration Statement number of the earlier effective Registration Statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act Registration Statement number of the earlier effective Registration Statement for the same offering. [ ]

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act Registration Statement number of the earlier effective Registration Statement for the same offering. [ ]

If delivery of the Registration Statement is expected to be made pursuant to Rule 434, check the following box. [ ]

1

| | | | Proposed | |

| | | Proposed | Maximum | |

| Title of Each Class of | Amount to be | Maximum | Aggregate Offering | Amount of |

| Securities to be | Registered | Offering Price | Price (2) | Registration Fee |

| Registered | | per Unit (1) ($) | ($) | ($) |

| | | | | |

| Shares of Common Stock, par value $0.001 | 28,435,885 | 1.39 | $39,525,880 | $1,213.44 |

| | | | | |

| 1 | Estimated solely for purposes of calculating the registration fee in accordance with Rule 457 of the Securities Act. |

2

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the SEC, acting pursuant to said Section 8(a), may determine.

PROSPECTUS

28,435,885 SHARES

COMMON STOCK

This Prospectus relates to the resale by selling shareholders of up to 28,435,885 shares of our common stock currently outstanding. Approximately 116 of our shareholders are offering shares of our common stock to the public by means of this Prospectus.

Our common stock became eligible for trading on the OTC Bulletin Board on February 8, 2007. Our common stock is quoted on the OTC Bulletin Board under the symbol “HMSO.OB”. The OTC Bulletin Board is a regulated quotation service that displays real-time quotes, last-sale prices and volume information for over-the-counter equity securities. Over-the-counter securities are traded by a community of market makers that enter quotes and trade through a sophisticated computer network. Information on the OTC Bulletin Board can be found atwww.otcbb.com. These quotations reflect inter-dealer prices, without retain mark-up, mark-down or commissions, and may not represent actual transactions. Our common stock is also quoted on the Frankfurt stock exchange under the symbol XZA.

On April 17, 2007, the last reported sales price of our common stock on the OTC Bulletin Board was $1.39 per share

An investment in our common stock is speculative. See "Risk Factors" starting at page 13 of this Prospectus.

Neither the U.S. Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this Prospectus. Any representation to the contrary is a criminal offense.

3

Table of Contents

Prospectus Summary

Our Business

Hemis Corporation (“Hemis”, “we”) is a start up mineral exploration company. We have had no revenues as of the end of our most recent fiscal year and we have only recently begun operations.

Our principal offices are located at Bettlistrasse 35, CH – 8600 Dübendorf, Switzerland, and we have an address for service and a telephone number in Las Vegas, Nevada. Our telephone number is (702) 387 2382. Our fiscal year end is December 31.

Our Interests

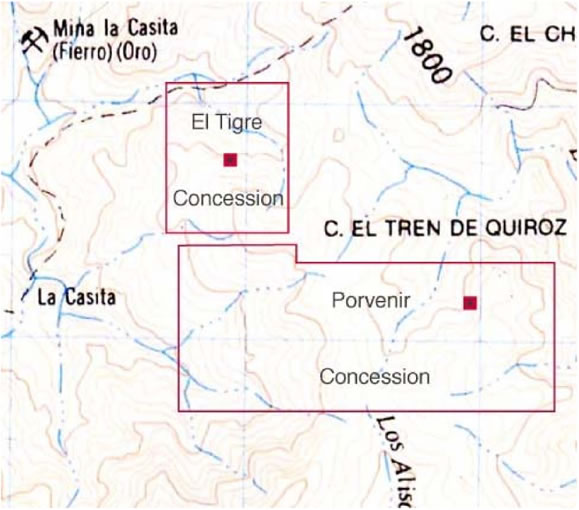

We are engaged in the acquisition and exploration of mineral properties in Zacatecas, Mexico, Sonora, Mexico, British Columbia, Canada and Alaska, U.S.A. We hold options to acquire interests in four mineral concessions on properties in Mexico and we hold the rights to acquire various offshore prospect permitting applications in Alaska. We also hold the rights to acquire interests in two mineral claims in Canada as described below:

| Name of Property | Location | Nature of Interest |

| Santa Rita Property | La Zacatecas, Mexico | Option to acquire a 49%

interest (of Corex Gold's

interest) in mining rights |

| El Tigre Property | Sonora, Mexico | Option to acquire a 67.5%

interest in mining rights |

| Porvenir Property | Sonora, Mexico | Option to acquire a 67.5%

interest in mining rights |

| La Centela Property | Sonora, Mexico | Options to acquire up to a 75%

interest in mining rights |

| Anchor Point Gold Project | Alaska, US | Rights to acquire various

offshore prospecting permit

applications and a non-

exclusive license of geologic

information |

Wolfe Creek and Covenant

nd Covenant Claims | British Columbia, Canada | Option to acquire 100%

interest in mining rights of two

properties |

5

The El Tigre, Porvenir and La Centela properties are all located adjacent to each other. We have recently finalized the initial exploration phase on the El Tigre concession. We intend to explore for gold and molybdenum (a mineral used in the production of steel) on the La Centela property. At this time our plan of operation is to explore for gold on the Santa Rita, Porvenir and Wolfe Creek and Covenant and Covenant properties. If we discover that any of our optioned properties hold potential for other minerals for which our management believes exploration is warranted, then we will include in our plan of operation exploration for those minerals.

In each of the Santa Rita, El Tigre, Porvenir, La Centela and Wolfe Creek and Covenant agreements, we have contracted with the owners of the mineral rights on the properties to acquire mining rights for the properties. The acquisition of these mineral rights will give us the right to exploit, mine and produce all minerals lying beneath the surface of each property.

The Anchor Point Gold Project relates to an area of the Cook Inlet, Alaska where we have been assigned various offshore prospecting permit applications from Aspen Exploration Corporation (“Aspen”), together with a non-exclusive license of all of Aspen’s right, title and interests to all maps, aeromagnetic surveys and geologic information developed by Aspen in the Cook Inlet, Alaska.

We have not acquired an interest in any physical property in the Cook Inlet, Alaska. Previously, Aspen have made two attempts to have the offshore prospecting permit applications granted, but both times, they were denied. We are in the process of applying to have the same applications granted. If we are successful in applying for them, we will have the right to exploit, mine and produce all minerals lying beneath the surface of the defined area. However, there is a risk that the State of Alaska will never accept these offshore prospecting permit applications in which case this asset will be of little value to us.

Payment

We expended no money or other consideration to acquire the options in the mining rights for the Santa Rita, El Tigre, Porvenir, La Centela and Wolfe Creek and Covenant and Covenant properties. In order for Hemis to be entitled to the rights pursuant to the Anchor Point Gold Project, we paid Aspen $50,000 on signing the Anchor Point Gold Project agreement on January 8, 2007.

Santa Rita

In order to exercise our option to the mineral rights of the Santa Rita Property we must pay $1,000,000 prior to January 31, 2009 and we must issue 200,000 shares of our common stock prior to January 31, 2009 as follows:

6

| Due Date | Payment | Common Shares |

| January 31, 2007 | $200,000 | 25,000 (Paid in October, 2006) |

| July 31, 2007 | $200,000 | 75,000 |

| January 31, 2008 | $200,000 | 50,000 |

| July 31, 2008 | $200,000 | 50,000 |

| January 31, 2009 | $200,000 | |

| Total | $1,000,000 | 200,000 |

El Tigre and Porvenir

To exercise our option to acquire a 67.5% interest in the mineral rights for the El Tigre and Porvenir properties, we were required to pay at least $15,000 by January 30, 2006, which we have paid, and we must spend at least another $200,000 prior to July 2, 2007.

La Centela

On September 7, 2006 we signed an option agreement to acquire a 75% interest in the mineral rights to the La Centela property. The agreement was amended on October 4, 2006. The option consists of two parts; an option for the first 70% and an option for a further 5%. To acquire the first 70% of the mining rights we must pay $500,000 and issue 500,000 of our common shares to the mineral rights owner, spend at least $2,000,000 in exploration expenses, all prior to October 5, 2010, and make a final share payment of one share for every ounce of gold we identify, if we identify any gold, to a maximum of 10,000,000 shares. If we exercise our option to acquire the first 70% of the mineral rights, we may then acquire a further 5% of the total claim by making a cash payment of $1,000,000.

To exercise the first 70% of the mining rights on the La Centela property, we must deliver the following stock and payments to the mining concession owners, and make the following exploration expenditures:

- pay $25,000 and issue 25,000 common shares by October 14, 2006 (which has already been paid and delivered, and on October 10, 2006 we issued the 25,000 common shares valued at $0.95 per share, the fair market value of the shares on the date of issuance, for a total value of $23,750);

- by October 5, 2007, pay an additional $50,000, issue 50,000 more common shares and spend $200,000 on exploration expenses;

- by October 5, 2008, pay an additional $75,000, issue 75,000 more common shares and spend $200,000 on additional exploration expenses;

- by October 5, 2009, pay an additional $100,000, issue 100,000 more common shares and spend an additional $200,000 on exploration expenses;

- by October 5, 2010, pay an additional $250,000, issue 250,000 more common shares and spend an additional $1,400,000 on exploration expenses; and

- issue one common shares for every once of gold we estimate that we have identified, up to a maximum of 10,000,000 shares, if we can identify any gold at the time of making our final payments to exercise the option.

7

If we do not make the specified annual expenditures, we will forfeit our rights to exercise the options.

Anchor Point Gold Project

In order for us to continue to be entitled to the offshore prospecting permit applications and licenses relating to the Anchor Point Gold Project, we have agreed to pay Aspen $50,000 on signing the agreement, and an annual payment of $50,000 thereafter, beginning in September, 2007. We have also granted Aspen a 5% gross royalty in any ores, minerals, and mineral resources produced from the offshore prospecting permit applications, including all offshore prospecting permit applications acquired by us in the area of interest in the Cook Inlet, Alaska. In particular, the 5% royalty on all placer gold produced shall be paid in kind. Royalty for minerals other than placer gold shall be 5% of the gross revenue received by or on behalf of us from the sale or other dispositions of the ores, minerals, and mineral resources. If we fail to make these payments, we will forfeit our rights to the Anchor Point Gold Project.

Wolfe Creek and Covenant

In order for us to continue to be entitled to the 100% interest in the mining rights of the two Canadian properties, we must pay $1,000,000 in exploration expenses over the next three years in addition to paying royalties of 3% to Stacs GmbH, the owner of the mineral rights on the properties.

Our plan of operations is to carry out exploration of our mineral properties. Our specific exploration plan for each of our mineral properties, together with information regarding the location and access, history of operations, present condition and geology of each of our properties, is presented in this Prospectus under the heading “Description of Properties.” All of our exploration programs are preliminary in nature in that their completion will not result in a determination that any of our properties contains commercially exploitable quantities of mineralization.

We are an exploration stage company. All of our projects are at the exploration stage and there is no assurance that any of our mining claims contain a commercially viable ore body. We plan to undertake further exploration of our properties. We anticipate that we will require additional financing in order to pursue full exploration of these claims. We do not have sufficient financing to undertake full exploration of our mineral claims at present and there is no assurance that we will be able to obtain the necessary financing.

There is no assurance that a commercially viable mineral deposit exists on any of our mineral properties. Further exploration beyond the scope of our planned exploration activities will be required before a final evaluation as to the economic and legal feasibility of mining of any of our properties is determined. There is no assurance that further exploration will result in a final evaluation that a commercially viable mineral deposit exists on any of our mineral properties.

8

We have no revenues, we have achieved losses since inception, have been issued a going concern opinion by our auditors and rely upon the sale of our securities to fund operations. We will not generate revenues even if our exploration program indicates that a mineral deposit may exist on our mineral claims. Accordingly, we will be dependent on future additional financing in order to maintain our operations and continue our exploration activities.

The Offering

The 28,435,885 common shares represent approximately 40% of our issued and outstanding stock. Both before and after the offering, our current directors and officers will control Hemis. Before the offering, Bruno Weiss, our Chief Financial Officer, owns a total of 13,374,000 shares, which is approximately 19% of our issued and outstanding stock. After the offering, if he sells all 2,000,000 shares he is registering in this Prospectus, he will have 11,374,000 shares, which would be approximately 16% of our issued and outstanding stock. Before the offering, Norman Meier, our Chief Executive Officer, owns or controls a total of 25,950,000 shares, which is approximately 37% of our issued and outstanding stock. After the offering, if he sells all 8,000,000 shares he is registering in this Prospectus, he will have 17,950,000 shares, which would be approximately 26% of our issued and outstanding stock. Before and after the offering, Doug Oliver, our Vice President Operations, owns 100,000 shares which is less than 1% of our issued and outstanding stock. Dr. Oliver is not selling any of his shares.

| Securities Offered: | Up to 28,435,885 common shares offered by the selling shareholders. |

| | |

Market for Our Common

Stock | Our common stock is quoted on the OTC Bulletin Board, under the trading symbol “HMSO.OB”, and on the Frankfurt Stock Exchange under symbol XZA. The market for our stock is highly volatile. We cannot assure you that there will be a market in the future for our common stock. |

| | |

| | 70,272,786 |

| | |

| Use of Proceeds: | We will not receive any proceeds from the sale of the common stock by the selling shareholders. |

The above information regarding common stock to be outstanding after the offering is based on 70,272,786 shares of common stock outstanding as of April 16, 2007.

Financial Condition

Since inception, we have reported significant losses resulting in a total comprehensive loss of $8,067,139 since inception on February 9, 2005 until December 31, 2006. We have generated no revenues to date, have incurred operating expenses and have sustained losses. Our auditors stated that these factors raise substantial doubt about our ability to continue as a going concern.

9

We will need additional working capital to continue or to be successful in any future business activities. Therefore, our continuation as a going concern is dependent upon obtaining the additional working capital necessary to accomplish our objectives. We plan to seek equity financing to raise the necessary working capital. As of April 16, 2007, we had approximately $300,000 in our bank accounts. We expect to require approximately an additional $9,053,000 in financing to continue our planned operations for the next year, beginning April 1, 2007, to cover the following expenses:

| Description of Expense | Amount |

| Exploration of the joint El Tigre Gold Project (the joint El Tigre, Porvenir and La Centela Claims) | $ 620,000 |

| Payment towards acquisition of La Centela mining rights | $ 250,000 |

| Payment towards acquisition of rights in respect of the Cook Inlet Permit Applications | $ 50,000 |

| Exploration of the Anchor Point Gold Project, Alaska | $ 1,000,000 |

| Payment towards acquisition of Santa Rita mining rights | $ 400,000 |

| Payment towards acquisition of El Tigre and Porvenir mining rights | $ 200,000 |

| Payment towards acquisition of Wolfe Creek and Covenant mining rights | $ 333,000 |

| Exploration of the Wolfe Creek and Covenant mining rights | $ 500,000 |

| Obtaining interests in other mining rights | $ 2,000,000 |

| General and Administrative Expenses | $ 4,000,000 |

| Total | $9,353,000 |

The above amounts include the amounts we need to spend to maintain all of our rights and options to acquire interests in the properties. In order to maintain these rights and options we must spend the following amounts over the next three calendar years:

| Property | Year | Amount We Must Spend |

| Santa Rita | 2007 | $200,000 (1) |

| | 2008 | $400,000 |

| | 2009 | $200,000 |

| El Tigre and Porvenir | 2007 | $200,000 (2) |

10

| La Centela | 2007 | $250,000 |

| | 2008 | $275,000 |

| | 2009 | $300,000 |

| Anchor Point Gold Project (3) | 2007 | $50,000 |

| | 2008 | $50,000 |

| | 2009 | $50,000 |

| Wolfe Creek and Covenant Properties (4) | 2007 | $333,000 |

| | 2008 | $333,000 |

| | 2009 | $333,000 |

(1) We must pay $200,000 by July 31, 2007, to maintain our option to acquire an interest in the Santa Rita property.

(2) If we spend $200,000 by July 2, 2007, we will have exercised the option.

(3) In order to maintain the rights to the Anchor Point Gold Project we must make annual payments to Aspen for the next 30 years or until the agreement between us and Aspen is terminated.

(4) We must incur $1,000,000 in exploration costs over the next three years.

As at April 16, 2007 we have satisfied all our obligations to maintain our rights and options to date.

Financial Summary Information

All of the references to currency in this filing are to US Dollars, unless otherwise noted. The following table sets forth selected financial information, which should be read in conjunction with the information set forth under "Management’s Discussion and Analysis" at page 79 and our accompanying consolidated Financial Statements and related notes included elsewhere in this Prospectus.

11

Income Statement Data

| | | | For the period from |

| | | For the period from | February 9, 2005 |

| | For the 12 month | February 9, 2005 | (inception) |

| | period ended | (inception) through | through December |

| | December 31, 2006 | December 31, 2005 | 31, 2006 |

| | | | |

| | ($) | ($) | ($) |

| Revenue | 0 | 0 | 0 |

| Expenses | 6,658,400 | 1,237,203 | 7,895,603 |

| Total Comprehensive Loss | (6,829,936) | (1,237,203) | (8,067,139) |

| Loss per Common Share | (0.47) | (0.16) | |

Balance Sheet Data

| | December 31, 2006 | December 31, 2005 |

| | ($) | ($) |

| | | |

| Working Capital | 1,818,252 | 280,173 |

| Total Current Assets | 2,736,646 | 381,393 |

| Total Current Liabilities | 918,394 | 101,220 |

Recent Developments

From January 1, 2007 until April 16, 2007 we have raised capital through the following share issuances:

In January 2007 we raised a total of $1,510,571 through the following issuances: 21,052 shares at $0.95 per share; 1,233,810 shares at $1.20 per share; and the exercise of 10,000,000 options to purchase shares at $0.001.

In February 2007 we raised a total of $224,224 through the following issuances: 100,080 shares at $0.60 per share; and 124,164 shares at $1.20 per share. On February 12, 2007 we issued166,800 shares of common stock for cash to Pampero Limited at $0.60 per share. Pampero Limited submitted their subscription agreement and paid for 83,400 shares at a price of $1.20 per share on December 21, 2006 but due to an administrative delay we did not accept their until February 12, 2007, which is after the date that we issued a stock dividend to our shareholders (which occurred on January 12, 2007). In order to reflect the fact that Pampero Limited would have been included in the dividend declaration were it not for our late acceptance of the subscription agreement, we issued double the number of shares (166,800 shares) for the same proceeds of $60,048, resulting in a price per share of $0.60.

12

On February 13, 2007 we repurchased and returned to treasury for cancellation 2,411,346 shares from 33 shareholders at a cost to us of $1,503,382. This repurchase was carried out pursuant to agreements we had reached with certain shareholders in October 2006 whereby we had agreed that we would repurchase half of each shareholders’ shares pursuant to investments made prior to October 2006. Our management believed that the repurchase of these shares would make it easier for us to raise capital at a higher price because it would reduce the number of shares issued and outstanding.

In March 2007 we raised a total of $204,400 through the following issuances: 232,200 shares at $0.65 per share; and 40,000 shares at $1.34 per share. On March 22, 2007 we issued an aggregate of 232,000 common shares to four investors. These investors had submitted their subscription agreements and paid for their shares at a price of $0.65 per share previously when our stock price was lower, but due to an administrative delay, their subscription agreements were not processed for issuance until March 22, 2007 by which time the price of our shares as quoted on the OTC Bulletin Board was $1.45.

On April 10, 2007 we issued 12,500 shares to Charles Reed in exchange for geologist consulting services he provided us from January 1, 2007 to March 31, 2007, and in accordance with his employment contract dated May 15, 2005. On April 13, 2007 we issued an aggregate of 14,400 shares to non-US investors for cash at $1.00 per share. The closing price of the shares as quoted on the OTC Bulletin Board on April 13, 2007 was $1.40.

Risk Factors

Please consider the following risk factors before deciding to invest in our common stock. Throughout this Prospectus and Registration Statement, when we state "we", "us", "our”, the “Company” or "Hemis" we are referring to Hemis Corporation.

Any investment in our common stock is speculative. You should carefully consider the risks described below and all of the information contained in this Prospectus before deciding whether to purchase our common stock. If any of the following risks actually occur, our business, financial condition and results of operations could be harmed. The trading price of our common stock could decline, and you may lose all or part of your investment in our common stock.

Risks Related to Our Operating Results

1. If we do not obtain additional financing, our business plan will fail, which could prevent us from becoming profitable.

13

As of April 16, 2007, we had approximately $300,000 in our bank account. Our business plan calls for us to spend approximately $9,353,000 during the twelve months beginning April 1, 2007, which includes amounts we need to spend to maintain all of our options to acquire mining interests, as well as additional amounts we plan to spend in exploring the five properties in which we have rights and options, expenses to acquire interests in other mineral properties and all of our general and administrative expenses. Based on our approximate cash position as of April 16, 2006 of $300,000, we will require additional financing in the approximate amount of $9,053,000 in order to complete our plan of operations for the next twelve months beginning April 1, 2007. We are currently attempting to raise capital through the issuances of shares to non US residents. We may not be able to obtain all of the financing we require. Our ability to obtain additional financing is subject to a number of factors, including the market price of gold, market conditions, investor acceptance of our business plan, and investor sentiment. These factors may make the timing, amount, terms and conditions of additional financing unattractive or unavailable to us. If we are unable to raise additional financing, we will have to significantly reduce our spending, delay or cancel planned activities or substantially change our current corporate structure. In such an event, we intend to implement expense reduction plans in a timely manner. However, these actions would have material adverse effects on our business, revenues, operating results, and prospects, resulting in a possible failure of our business.

2. Because we have only recently commenced preliminary exploration of our mineral claims, we face a high risk of business failure and this could result in a total loss of your investment.

We have just recently begun the initial stages of exploration of our mineral claims, and thus have no way to evaluate the likelihood of whether we will be able to operate our business successfully. To date, we have been involved primarily in organizational activities, acquiring interests in mineral claims and in conducting preliminary exploration of mineral claims. We have not earned any revenues and have not achieved profitability as of the date of this Prospectus. Potential investors should be aware of the difficulties normally encountered by new mineral exploration companies and the high rate of failure of such enterprises. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that we plan to undertake. These potential problems include, but are not limited to, unanticipated problems relating to exploration and additional costs and expenses that may exceed current estimates. We have no history upon which to base any assumption as to the likelihood that our business will prove successful, and we can provide no assurance to investors that we will generate any operating revenues or ever achieve profitable operations. If we are unsuccessful in addressing these risks, our business will likely fail and you will lose your entire investment in this offering.

3. Because we do not have any revenues, we expect to incur operating losses for the foreseeable future.

We have never earned revenues and we have never been profitable. Prior to completing exploration on our mineral properties, we anticipate that we will incur increased operating expenses without realizing any revenues. We therefore expect to incur significant losses into the foreseeable future. If we are unable to generate financing to continue the exploration of our mineral claims, we will fail and you will lose your entire investment in this offering.

14

4. We have yet to attain profitable operations and because we will need additional financing to fund our exploration activities, we may have to cease operations.

We have incurred a total comprehensive loss of $8,067,139 for the period from February 9, 2005 (inception) to December 31, 2006, and have no revenues to date. Our ability to continue the exploration of our mineral claims is dependent upon our ability to obtain financing. These factors raise substantial doubt that we will be able to continue as a going concern.

Our financial statements included with this Prospectus have been prepared assuming that we will continue as a going concern. Our auditors have made reference to the substantial doubt as to our ability to continue as a going concern in their audit report on our audited financial statements for the year ended December 31, 2006. If we are not able to achieve revenues, then we may not be able to continue as a going concern and our financial condition and business prospects will be adversely affected.

5. If our costs of exploration are greater than anticipated, then we will not be able to complete our planned exploration programs for our mineral claims without additional financing, of which there is no assurance that we would be able to obtain. This could prevent us from achieving revenues.

We are proceeding with the initial stages of exploration on some of our mineral claims. We have prepared budgets for our exploration programs. However, there is no assurance that our actual costs will not exceed the budgeted costs. Factors that could cause actual costs to exceed budgeted costs include increased prices due to competition for personnel and supplies during the Mexico summer exploration season, unanticipated problems in completing the exploration programs and delays experienced in completing the exploration program. Increases in exploration costs could result in us not being able to carry out our exploration programs without additional financing. There is no assurance that we would be able to obtain additional financing in this event. This could prevent us from achieving revenues.

6. Because of the speculative nature of exploration of mining properties, there is substantial risk that no commercially exploitable minerals will be found and our business will fail, and you could lose your entire investment.

With the exception of the El Tigre mineral claim where we have recently finalized the initial exploration phase, we are at best, in the initial stages of exploration of all our other mineral claims, and more specifically:

- Extensive mapping and sampling were carried out during the first quarter of 2006 on the Santa Rita property and some regional sampling has also been done to examine geophysical anomalies and major structures to see if they are related to mineralization;

- The only work done on the Porvenir Property to date is some geochemical sampling;

- On the La Centela property, we have conducted some preliminary sampling and mapping, and have constructed 2 drill pads. We are also in the process of constructing an exploration camp on the land;

15

- We are still in the early stages of developing our full exploration plan for the Wolfe Creek and Covenant properties, and don’t anticipate that we will begin exploration of these properties for another six months; and

- We still have yet to have the offshore prospecting permit applications approved which relate to the Anchor Point Gold Project.

Since we are only in the initial stages of exploration for most of our mineral claims, we have no way to evaluate the likelihood that we will be successful in establishing commercially exploitable reserves of gold or other valuable minerals on these mineral claims. Potential investors should be aware of the difficulties normally encountered by new mineral exploration companies and the high rate of failure of such enterprises. The search for valuable minerals as a business is extremely risky. We may not find commercially exploitable reserves of gold or molybdenum or other minerals in any of our mineral claims. Exploration for minerals is a speculative venture necessarily involving substantial risk. The expenditures to be made by us on our exploration programs may not result in the discovery of commercial quantities of ore. The likelihood of success must be considered in light of the problems, expenses, difficulties, complications and delays encountered in connection with the exploration of the mineral properties that we plan to undertake. Problems such as unusual or unexpected formations and other conditions are involved in mineral exploration and often result in unsuccessful exploration efforts. In such a case, we would be unable to complete our business plan, and you could lose your entire investment.

7. Because of the inherent dangers involved in mineral exploration, there is a risk that we may incur liability or damages as we conduct our business, which could cause us to liquidate our assets and go out of business.

The search for valuable minerals involves numerous hazards. In the course of carrying out exploration of our mineral claims, we may become subject to liability for such hazards, including pollution, cave-ins, lost circulations, stuck drill steel, adverse weather precluding drill site access and other hazards against which we cannot insure or against which we may elect not to insure. We currently have no such insurance nor do we expect to get such insurance for the foreseeable future. If a hazard were to occur, the costs of rectifying the hazard may exceed our asset value and cause us to liquidate all of our assets, resulting in the loss of your entire investment in this offering.

8. If we discover commercial reserves of precious metals on any of our mineral properties, we can provide no assurance that we will be able to successfully advance the mineral claims into commercial production. If we cannot commence commercial production, we may not be able to achieve revenues.

Our mineral properties do not contain any known bodies of ore. If our exploration programs are successful in establishing ore of commercial tonnage and grade on any of our mineral claims, we will require additional funds in order to advance the mineral claims into commercial production. In such an event, we may be unable to obtain any such funds, or to obtain such funds on terms that we consider economically feasible, we may not be able to achieve revenues.

16

9. Because access to our mineral claims is often restricted by inclement weather, we may be delayed in our exploration and any future mining efforts, which could increase our operating expenses and prevent us from being profitable.

Access to certain of our mineral claims may be restricted to the period between April and December of each year due to storms in the area. Inclement weather may result in significant delays in exploration efforts and may increase the costs of exploration, with the result that we may not be able to complete our exploration programs within the anticipated time frames or within our anticipated budgets, which could increase our operating expenses and prevent us from being profitable.

10. As we undertake exploration of our mineral claims, we will be subject to compliance with government regulation that may increase the anticipated time and cost of our exploration program, which could increase our expenses.

We will be subject to the mining laws and regulations as contained in Mexico and British Columbia, Canada as we carry out our exploration program, and if the offshore prospecting permit applications are approved for the Anchor Point Gold Project, we will be subject to the mining laws and regulations of Alaska. We will be required to prove our compliance with relevant Mexican, Canadian and perhaps Alaskan environmental and workplace safety laws, regulations and standards by submitting receipts showing the purchase of equipment used for workplace safety of the prevention of pollution or the undertaking of environmental remediation projects before we are able to obtain drilling permits. We will also be required to pay mining taxes to the Mexican and Canadian governments. If our exploration activities lead us to make a decision to go into mining production, before we initial a major drilling program, we will have to obtain an environmental impact statement authorization. This could potentially take more than 10 months to obtain and could potentially be refused. While our planned exploration program budgets for regulatory compliance, there is a risk that new regulations could increase our time and costs of doing business and prevent us from carrying out our exploration program. These factors could prevent us from becoming profitable.

11. We may lose our rights to exercise options to acquire mining rights to properties if we fail to meet certain expenditure requirements. If we lose our options to acquire property rights, we may never achieve revenues and our business could fail.

We currently have four option agreements to acquire mining rights. The first gives us, indirectly, an option to acquire a mining interest in the Santa Rita property in Mexico. The second is an option to acquire mining interests in the El Tigre and Porvenir properties in Mexico, the third is an option to acquire mineral interests in the La Centela property, which is adjacent to El Tigre and Porvenir, and the fourth is an option to acquire mining interests in the Wolfe Creek and Covenant properties in British Columbia, Canada.

In order to maintain and exercise our option in the Santa Rita property, we must pay $200,000 and issue 75,000 common shares by July 31, 2007, pay an additional $200,000 and issue 50,000 more shares by January 1, 2008 pay an additional $200,000 and issue 50,000 more shares by July 31, 2008, and pay a final amount of $200,000 by January 31, 2009.

17

In order to maintain and exercise our option on the El Tigre and Porvenir claims, we must spend $200,000 prior to July 2, 2007.

In order to exercise our option to acquire the first 70% of the La Centela mining claim, we must, within the next four years, spend $2,000,000 in exploration expenses, pay a further $475,000 and issue a further 500,000 common shares, plus issue additional shares if we identify any gold. We are not required to issue any additional shares if we identify any molybdenum. If we fail to make these expenditures within the required time periods, we will forfeit our rights to exercise the options.

We have also acquired the rights to certain offshore prospecting permit applications in respect of the Anchor Point Gold Project, which have yet to be approved. In order to maintain the rights to these permit applications, we have to make annual payments of $50,000.

In order to exercise our option to acquire the 100% interest in the Wolfe Creek and Covenant mining claims, we must within the next three years, spend $1,000,000 in exploration expenses and pay a royalty of 3% to the current owner of the mining rights.

There can be no assurance that we will always make the required payments and spend the required amount of exploration expenses by the requisite dates. If we lose our options to acquire mining rights and the rights to the offshore prospecting permit applications, we may never achieve revenues.

12. We face competition from other mining companies for access to mining equipment, crews and geologists. Our inability to obtain labor and equipment could prevent us from completing our exploration program, which could prevent us from achieving revenues.

We plan to complete exploration programs for which we will need drill rigs and other equipment, contract geologists, and crews to operate the equipment. We have not yet entered into any agreements with services companies to provide us access to a drilling rig or a drilling crew in Mexico or Canada. We face competition from other mining companies for access to mining equipment, crews and geologists. Currently, in Mexico and Canada, there are large numbers of companies competing to obtain the services of rigs and crews. There are inadequate rigs to meet the demand and the owners of the rigs often give preference to larger drilling programs that we plan to carry out. There is also a shortage of skilled workers which could mean that we are unable to operate efficiently. If we are unable to obtain mining equipment and labor on commercially reasonable terms, this could increase our operating costs. If we are unable to obtain mining equipment or labor we will not be able to complete our exploration program and we may not be able to achieve revenues.

18

13. We are exposed to currency exchange risks which could cause our reported earnings or losses to fluctuate.

Although we intend to report our financial results in US dollars, a portion of our operating costs may be denominated in Swiss Francs, Canadian Dollars, Mexican Pesos or other currencies. In addition, we are exposed to currency exchange risk on any of our assets that we denominate in other currencies. Since we present our financial statements in US dollars, any change in the value of the Swiss Franc or Mexican Peso or other currency we use relative to the US dollar during a given financial reporting period would result in a foreign currency loss or gain on the translation of some of our assets into US dollars. Consequently, our reported earnings or losses could fluctuate materially as a result of foreign exchange translation gains or losses.

Risks Associated with this Offering

14. Because the SEC imposes additional sales practice requirements on brokers who deal in our shares which are penny stocks, some brokers may be unwilling to trade them. This means that you may have difficulty reselling your shares and this may cause the price of the shares to decline.

Our shares are classified as penny stocks and are covered by Section 15(g) of the Securities Exchange Act of 1934 (the “Exchange Act”) which impose additional sales practice requirements on brokers-dealers who sell our securities in this offering or in the aftermarket. For sales of our securities, the broker-dealer must make a special suitability determination and receive from you a written agreement prior to making a sale for you. Because of the imposition of the foregoing additional sales practices, it is possible that brokers will not want to make a market in our shares. This could prevent you from reselling your shares and may cause the price of the shares to decline.

Our stock is traded on the Frankfurt Stock Exchange (symbol: XZA), and on the OTC Bulletin Board (symbol: HMSO.OB). Trading of securities on both the Frankfurt Stock Exchange and the OTC Bulletin Board is often sporadic and investors may have difficulty buying and selling or obtaining market quotations, which may have a depressive effect on the market price for our common stock. Accordingly, you may have difficulty reselling any shares your purchase from us.

15. Because our officers and directors, will own close to 50% of the outstanding shares after this offering, they will be able to exercise significant control of us and be able to decide who will be directors and you may not be able to remove them as directors which could prevent us from becoming profitable.

19

Before the offering, Bruno Weiss, our Chief Financial Officer, owns a total of 13,374,000 shares, which is 19% of our issued and outstanding stock. After the offering, if he sells all 2,000,000 shares he is registering in this Prospectus, he will have 11,374,000 shares, which would be approximately 16% of our issued and outstanding stock. Before the offering, Norman Meier, our Chief Executive Officer, owns or controls a total of 25,950,000 shares, which is approximately 37% of our issued and outstanding stock. After the offering, if he sells all 8,000,000 shares he is registering in this Prospectus, he will have 17,950,000 shares, which would be approximately 26% of our issued and outstanding stock. Before and after the offering, Doug Oliver, our Vice President Operations, owns 100,000 shares which is less than 1% of our issued and outstanding stock. Dr. Oliver is not selling any of his shares.

After the offering, assuming all of the shares being registered are sold, Norman Meier, Bruno Weiss and Doug Oliver will together own more than 42% of our issued common stock, and therefore they will have a significant voting capability in terms of electing all of our directors and controlling our operations. They may have an interest in pursuing acquisitions, divestitures and other transactions that involve risks. For example, they could greatly influence decisions that cause us to make acquisitions that increase our indebtedness or to sell revenue generating assets. They may from time to time acquire and hold interests in businesses that compete directly or indirectly with us. If the directors fail to act in our best interests or fail to perform adequately to manage us, you may have difficulty in removing them as directors, which could prevent us from becoming profitable.

Use of Proceeds

We will not receive any proceeds from the sale of the common stock offered through this Prospectus by the Selling Shareholders.

Dilution

All 28,435,885 shares of the common stock to be sold by the Selling Shareholders is common stock that is currently issued and outstanding. Accordingly, it will not cause dilution to our existing shareholders.

Plan of Distribution

The Selling Shareholders may sell some or all of their common stock in one or more transactions, including block transactions:

on such public markets as the common stock may be trading;

in privately negotiated transactions;

through the writing of options of the common stock; or

in any combination of these methods of distribution.

The sales price to the public may be:

20

- the market price prevailing at the time of sale;

- a price related to such prevailing market price; or

- such other price as the selling shareholders determine.

We are bearing all costs relating to the registration of the common stock. The Selling Shareholders, however, will pay any commissions or other fees payable to brokers or dealers in connection with any sale of the common stock.

The Selling Shareholders and other persons participating in the sale or distribution of the common stock will be subject to applicable provisions of the Securities Act and the Exchange Act, and the rules and regulations under the Exchange Act, including Regulation in the offer and sale of the common stock. In particular, during such times as the Selling Shareholders may be deemed to be engaged in a distribution of the common stock, and therefore be considered to be an underwriter, they must comply with applicable laws and may, among other things:

not engage in any stabilization activities in connection with our common stock;

furnish each broker or dealer through which common stock may be offered, such copies of this Prospectus, as amended from time to time, as may be required by such broker or dealer; and

not bid for or purchase any of our securities or attempt to induce any person to purchase any of our securities other than as permitted under the Exchange Act.

Regulation M may restrict the ability of any person engaged in the distribution of the common stock to engage in market-making activities with respect to the particular common stock being distributed for a period of up to five business days before the distribution. These restrictions may affect the marketability of the common stock and the ability of any person or entity to engage in market-making activities with respect to the common stock.

Selling Shareholders who are deemed underwriters within the meaning of the Securities Act will be subject to the Prospectus delivery requirements of the Securities Act. The SEC staff is of a view that selling stockholders who are registered broker-dealers are deemed to be underwriters under the Securities Act while affiliates of registered broker-dealers may be underwriters under the Securities Act. We will not pay any compensation or give any discounts or commissions to any underwriter in connection with the securities being offered by this Prospectus.

None of the Selling Shareholders will engage in any electronic offer, sale or distribution of the shares. Further, neither Hemis nor any of the selling shareholders have any arrangements with a third party to host or access our Prospectus on the Internet.

The Selling Shareholders and any underwriters, dealers or agents that participate in the distribution of our common stock may be deemed to be underwriters, and any commissions or concessions received by any such underwriters, dealers or agents may be deemed to be underwriting discounts and commissions under the Securities Act. Shares may be sold from time to time by the selling shareholders in one or more transactions at a fixed offering price, which may be changed, or at any varying prices determined at the time of sale or at negotiated prices. We may indemnify any underwriter against specific civil liabilities, including liabilities under the Securities Act.

21

Selling Security Holders

The 116 Selling Shareholders are offering shares of common stock already issued. Since inception, we have made the following unregistered share issuances:

On May 1, 2005, we issued an aggregate of 10,000,000 shares of common stock to our directors, Norman Meier and Bruno Weiss. The common shares issued were valued at par value of our common stock.

In May 2005, we issued an aggregate of 30,000 shares of common stock in exchange for cash at $0.55 per share.

In July 2005, we issued an aggregate of 500 shares of common stock in exchange for cash at $0.55 per share. We also issued an aggregate of 100,000 shares of common stock at $0.55 per share to Charles Reed, our Chief Geologist in exchange for $55,000 worth of mining related consulting services. Compensation costs of $55,000 were charged to operations during the year ended December 31, 2005.

In August 2005, we issued an aggregate of 458,183 shares of common stock in exchange for cash at $0.55 per share. We incurred commission costs of $25,200 in connection with the issuance of these common shares.

In September 2005, we issued 50,000 shares of common stock at $0.55 per share to Craig Schneider for consulting services valued at $27,500 provided by Mr. Schneider as a member of our Advisory Board. In September we also issued 50,000 common shares at $0.55 per share to Chris Bogart for consulting services valued at $27,500 provided by Mr. Bogart as a member of our Advisory Board.

In January 2006, we issued an aggregate of 593,638 shares of common stock at $0.55 per share for common stock subscribed in December 2005.

In February 2006, we issued an aggregate of 274,795 shares of common stock at $0.55 per share in exchange for $93,125 of common stock subscribed in December 2005 and $48,012 of proceeds, net of commission and costs.

In March 2006, we issued an aggregate of 164,337 shares of common stock at $0.55 per share in exchange for $11,000 of common stock subscribed in December, 2005 and $68,549 of proceeds, net of commission and costs.

In May 2006, we issued an aggregate of 480,000 shares of common stock in exchange for cash at $0.55 per share, and an aggregate of 25,000 shares of common stock in exchange for cash of $0.75 per share. We also issued 1,070,880 shares of common stock to Michael Friedrich for $588,984 of services in exchange for the following services provided by Mr. Friedrich: introduction to potential investors, preparing presentations to potential investors in Zurich, introducing us to investment professional and financial institutions, introducing us to high net worth individuals and assisting us in developing our business plans. The shares issued in exchange for services were valued at approximated the fair value of shares issued during the period services were rendered.

In June 2006, we issued an aggregate of 308,772 shares of common stock in exchange for cash at $0.55 per share and 150,000 shares of common stock on exchange for cash at $0.75 per share. We also issued an aggregate of 175,000 shares of common stock in exchange for consulting services to the following individuals: 50,000 shares to Karl-Heinz

22

Heiland for $37,500 of financial consulting, 50,000 shares to Doris Neuweiler for $37,500 of business development consulting, 50,000 shares to Doug Oliver, a Director of Hemis, for $27,500 of services as a geologist, 25,000 shares to Charles Reed for $18,750 of geological consulting services.

- In August 2006, we issued an aggregate of 1,033,730 shares of common stock at $0.75 per share in exchange for net cash proceeds of $700,853 after commission of $74,444.

- In August 2006, we issued an aggregate of 5,000 shares of common stock at $0.75 per share as compensation for a salary bonus of $3,750.

- In September 2006, we issued an aggregate of 961,428 shares of common stock in exchange for cash at $0.75 per share for net cash proceeds of $625,050 after commission of $96,021.

- In October 2006, we issued an aggregate 244,000 shares of common stock in exchange for cash at $0.75 per share and 357,420 shares of common stock in exchange for cash at $0.95. We also issued an aggregate 1,500,000 shares of common stock in exchange for consulting services to the following individuals: 1,000,000 shares to Michael Forster for $750,000 of business development consulting services; 500,000 shares to Sedona AG for $375,000 of capital raising consulting services. We also issued an aggregate of 50,000 shares of common stock pursuant to two of our mining options.

- In November 2006, we issued an aggregate of 295,528 shares of common stock for cash at $0.95 per share. We also issued 52,614 shares of common stock for cash at $0.75 in November 2006. The price was low because the subscription agreements had been submitted by the investors in August 2006 at which time we were offering shares to investors at $0.75 per share. However, due to an administrative delay in processing the subscription agreements, the shares were not issued until November by which time the price per share had risen to $0.95. We also issued an aggregate of 1,310,180 shares of common stock in exchange for consulting services to the following individuals: 2,130 shares to Rene Gahlinger for $1,597.50 of consulting services; 900,000 shares to Hudson Capital for $855,000 of business development consulting services; and 8,050 shares to Michael Forster for $7,647.50 of business development consulting services; and 400,000 shares of common stock in exchange for marketing consulting for $380,000 to an individual.

- In December 2006, we issued an aggregate of 549,150 shares of common stock for cash at $1.20 per share. We issued 15,789 shares of common stock for cash at $0.95 per share. We also issued an aggregate of 3,429 shares of common stock to Rene Gahlinger in exchange for $4,111 of consulting services.

23

In January 2007, we issued an aggregate of 1,233,810 shares of common stock for cash at $1.20 per share. Due to an unforeseen administrative delay in processing subscription agreements, we also issued 21,052 shares for cash at $0.95 per share. On January 13, 2007 two of our directors, Norman Meier and Bruno Weiss also chose to exercise their option agreements and each purchase for cash, five million shares of common stock of Hemis at a price of $0.001 per share. In January 2007 we also issued an aggregate of 63,461 shares of common stock in exchange for consulting and other services to the following individuals: 4,100 shares to Michael Forster for $4,920 of capital raising consulting services; 7,500 shares to Tobias Weber for $9,000 of consulting services; 7,500 shares to Joachim Schwarze for $9,000 of consulting services; 7,500 shares to Andreas Spaeth for $9,000 of consulting services; 6990 shares to Peter Stuessi for 8,388 of consulting services; 20,000 shares to Island Stock Transfer for $24,000 of services; 8,101 shares to Rene Gahlinger for $9,721 of consulting services; 1,770 shares to Brigitte Weiss for $2,124 of business development consulting services. Also, on January 17, 2006 we issued a stock dividend of one common share for each common share outstanding as of January 17, 2007, pursuant to which we issued an aggregate of 31,675,926 shares of common stock to our existing shareholders.

On February 12, 2007 we issued an aggregate of 103,470 shares of common stock for cash at $1.20 per share. We also issued 166,800 shares of common stock for cash to Pampero Limited at $0.60 per share. Pampero Limited submitted their subscription agreement and paid for 83,400 shares at a price of $1.20 per share on December 21, 2006 but due to an administrative delay this subscription agreement was not processed for issuance until February 12, 2007, which is after the date that the dividend declaration took place. In order to reflect the fact that Pampero Limited should have been included in the dividend declaration, we issued double the number of shares (166,800 shares) for the same compensation which reduced the price per share to $0.60. We also issued an aggregate of 647,500 shares of common stock in exchange for consulting and other services to the following individuals: 640,000 shares to Viktor Puentener for $768,000 of consulting services; 2,500 shares to Tobias Weber for $3,000 of consulting services; 2,500 shares to Joachim Schwarze for $3,000 of consulting services; and 2,500 shares to Andreas Spaeth for $3,000 of consulting services.

On February 13, 2007 we repurchased and returned to treasury for cancellation 2,411,346 shares from 33 shareholders, and returned these shares to treasury for cancellation.

On February 14, 2007 we issued an aggregate of 3,600 shares of common stock to Michael Forster in exchange for capital raising consulting services amounting to $4,320.

On February 20, 2007 we issued 10,000 shares to William Galine for providing business development and strategic planning consulting services amounting to $19,000.

On March 22, 2007 we issued an aggregate of 232,000 common shares to non-US investors for cash at $0.65 per share. The investors had completed their subscription agreements and paid for their shares previously, but due to an administrative error, they were not processed until March 22, 2007 by which time the shares were quoted on the OTC Bulletin Board at $1.45. We also issued an aggregate of 36,604 shares in exchange for consulting services to the following individuals: 7,604 shares to Costantino Pinelli for $11,026 of capital raising consulting services; and 29,000 shares to Orazio Domeniconi for $42,050 of consulting services.

24

On March 28, 2007 we issued an aggregate of 40,000 shares in exchange for consulting services to the following individuals: 20,000 shares to George Eliopulos in exchange for $26,800 of geologist consulting services; and 20,000 shares to Casey Danielson in exchange for $26,800 of geologist consulting services.

On April 10, 2007 we issued 12,500 shares to Charles Reed in exchange for geologist consulting services from January 1, 2007 to March 31, 2007, and in accordance with his employment contract dated May 15, 2005.

On April 13, 2007 we issued an aggregate of 14,400 shares to non-US investors for cash at $1.00 per share. The closing price of the shares as quoted on the OTC Bulletin Board on April 13, 2007 was $1.40.

Shares issued to U.S. residents Harvey Roseff, Doug Oliver, Charles Reed, Casey Danielson and George Eliopulos were exempt from registration pursuant to Rule 4(2) of the Securities Act. All of the other issuances described above were exempt from registration under Regulation S of the Securities Act. Where the purchasers of the shares in the issuances described above are not named, they are all non U.S. residents, unless otherwise noted.

Of the above described issuances, 28,435,885 shares are being registered by the Selling Shareholders.

The following table provides as of April 16, 2007 information regarding the beneficial ownership of our common stock held by each of the Selling Shareholders, including:

- the number of shares owned by each prior to this offering;

- the total number of shares that are to be offered for each;

- the total number of shares that will be owned by each upon completion of the offering; assuming all shares are sold that are being registered;

- the percentage owned by each; and

- the identity of the beneficial holder of any entity that owns the shares.

Name of Selling Shareholder

|

Shares

Owned Prior

to this

Offering (1)

|

Percent

| Maximum

Number of

Shares

Being

Offered

|

Beneficial

Ownership

After

Offering

| Percentage

Owned upon

Completion

of

the Offering

|

| Adrian Maritz | 4,000 | (2) | 2,000 | 2,000 | (2) |

| Adrian Morger | 10,000 | (2) | 10,000 | 0 | 0 |

| Alessandra Domeniconi | 20,000 | (2) | 20,000 | 0 | 0 |

| Andreas Baumann | 10,000 | (2) | 10,000 | 0 | 0 |

25

| Andreas Huber | 127,274 | (2) | 127,274 | 0 | 0 |

| Andreas Roethlisberger | 40,000 | (2) | 40,000 | 0 | 0 |

| Andreas Spaeth | 17,500 | (2) | 17,500 | 0 | 0 |

| Anton G. Stiffler | 40,000 | (2) | 40,000 | 0 | 0 |

| Anton Willy Stockli | 24,290 | (2) | 24,290 | 0 | 0 |

| Asset Management Switzerland AG (3) | 32,000 | (2) | 32,000 | 0 | 0 |

| Aurelio Perret | 242,000 | (2) | 242,000 | 0 | 0 |

| Brigitte Thrier | 81,212 | (2) | 26,666 | 54,546 | (2) |

| Brigitte Weiss (4) | 71,770 | (2) | 1,770 | 24,000 | (2) |

| Bruno Bieri | 40,000 | (2) | 40,000 | 0 | 0 |

| Bruno Bigger | 80,000 | (2) | 80,000 | 0 | 0 |

| Bruno Weiss (5) | 13,374,000 | 19% | 2,000,000 | 11,374,000 | 16% |

| Casey Danielson | 20,000 | (2) | 20,000 | 0 | 0 |

| Celeste Mueller | 10,000 | (2) | 10,000 | 0 | 0 |

| Cesarino Angelo Baumann | 82,000 | (2) | 32,000 | 50,000 | (2) |

| Christina Berta Domeniconi- Surber | 68,000 | (2) | 48,000 | 20,000 | (2) |

26

| Christoph Vogelsanger | 80,000 | (2) | 80,000 | 0 | 0 |

| Corex Gold Corp.(6) | 50,000 | (2) | 50,000 | 0 | 0 |

| Cornelia Bruggmann | 10,000 | (2) | 10,000 | 0 | 0 |

| Costantino Pinelli (7) | 1,067,604 | 1.5% | 57,604 | 40,000 | (2) |

| Daniel Erb | 86,000 | (2) | 86,000 | 0 | 0 |

| Daniel Linder | 10,000 | (2) | 10,000 | 0 | 0 |

| Daniel Marin | 20,000 | (2) | 20,000 | 0 | 0 |

| Daniel Nussberger | 20,000 | (2) | 20,000 | 0 | 0 |

| Daniel Thung | 100,000 | (2) | 100,000 | 0 | 0 |

| Danielle Della Morte | 60,000 | (2) | 10,000 | 50,000 | (2) |

| Dennis Guggenheim | 25,200 | (2) | 25,200 | 0 | 0 |

| Dieter Hohler | 21,052 | (2) | 21,052 | 0 | 0 |

| Doris Neuweiler | 108,268 | (2) | 8,268 | 100,000 | 0 |

| Doris Renidear | 10,000 | (2) | 10,000 | 0 | 0 |

| Electrum Capital, Inc (8) | 50,000 | (2) | 50,000 | 0 | 0 |

| Emil Summermatter | 40,300 | (2) | 40,300 | 0 | 0 |

27

| Ernst Peter Roduner | 80,000 | (2) | 80,000 | 0 | 0 |

| Franz Burri | 140,000 | (2) | 110,000 | 30,000 | (2) |

| Frederic Farkas | 20,000 | (2) | 20,000 | 0 | 0 |

| Friedrich Activ Asset Management (9) | 1,144,315 | 1.6% | 1,144,315 | 0 | 0 |

| Friedrich Ort | 72,000 | (2) | 72,000 | 0 | 0 |

| Fritz Kohler | 16,800 | (2) | 16,800 | 0 | 0 |

| Georg Hafner | 30,000 | (2) | 30,000 | 0 | 0 |

| Georg Seitz | 110,000 | (2) | 110,000 | 0 | 0 |

| George Eliopulos | 20,000 | (2) | 20,000 | 0 | 0 |

| Gerald Wong (10) | 100,000 | (2) | 100,000 | 0 | 0 |

| Gerold Eberhard | 20,000 | (2) | 20,000 | 0 | 0 |

| Guido N Bassing | 50,000 | (2) | 20,000 | 30,000 | (2) |

| Hanspeter Steiner | 120,000 | (2) | 120,000 | 0 | 0 |

| Hemis Switzerland GmbH (4) | 46,000 | (2) | 46,000 | 0 | 0 |

| Hudson Capital Corporation (11) | 1,800,000 | 2.6% | 1,800,000 | 0 | 0 |

| Irene Naef | 10,410 | (2) | 10,410 | 0 | 0 |

28

| Island Stock Transfer (12) | 40,000 | (2) | 40,000 | 0 | 0 |

| Ivan Bergamin | 296,000 | (2) | 296,000 | 0 | 0 |

| Joachim Schwarze | 17,500 | (2) | 17,500 | 0 | 0 |

| Johannes Solenthaler | 20,000 | (2) | 20,000 | 0 | 0 |

| Jorg Bodenmann | 20,000 | (2) | 20,000 | 0 | 0 |

| Jusaj-Stiftung | 100,000 | (2) | 100,000 | 0 | 0 |

| Karl Bruck | 165,788 | (2) | 165,788 | 0 | 0 |

| Karl Kellenberger | 20,000 | (2) | 20,000 | 0 | 0 |

| Karl Mitterlechner | 129,936 | (2) | 129,936 | 0 | 0 |

| Karl-Heinz Heiland | 108,268 | (2) | 8,268 | 100,000 | (2) |

| Karl-Heinz Weger | 80,000 | (2) | 80,000 | 0 | 0 |

| Laura Andreoli | 10,000 | (2) | 10,000 | 0 | 0 |

| Marc Lutziger | 32,000 | (2) | 32,000 | 0 | 0 |

| Marcus Stutz (13) | 60,000 | (2) | 60,000 | 0 | 0 |

| Marc Stutz (13) | 20,000 | (2) | 20,000 | 0 | 0 |

| Markus Brunner | 14,000 | (2) | 14,000 | 0 | 0 |

29

| Markus Tschudin | 10,600 | (2) | 10,600 | 0 | 0 |

| Martin Stadler | 31,578 | (2) | 31,578 | 0 | 0 |

| Mary L. Little | 21,052 | (2) | 21,052 | 0 | 0 |

| Mathias Voigt | 154,000 | (2) | 154,000 | 0 | 0 |

| Michael Abay | 30,000 | (2) | 30,000 | 0 | 0 |

| Michael Forster (3) | 2,475,620 | 3.5% | 2,443,620 | 0 | 0 |

| Michael Friedrich (9) | 2,986,075 | 4.2% | 1,541,760 | 300,000 | (2) |

| NOEME Investment Corporation (14) | 2,000,000 | 2.8% | 2,000,000 | 0 | 0 |

| Norman Meier (14) | 25,950,000 | 37% | 6,000,000 | 17,950,000 | 26% |

| Orazio Domeniconi | 29,000 | (2) | 29,000 | 0 | 0 |

| Pampero Limited (15) | 166,800 | (2) | 166,800 | 0 | 0 |

| Patrick Kaczynski | 20,000 | (2) | 20,000 | 0 | 0 |

| Patrik Martin Seitz | 20,000 | (2) | 20,000 | 0 | 0 |

| Paul Caviezel | 100,000 | (2) | 100,000 | 0 | 0 |

| Paul-Henri Francey | 10,000 | (2) | 10,000 | 0 | 0 |

| Paxar AG (16) | 190,000 | (2) | 190,000 | 0 | 0 |

30

| Peter di Gallo | 110,000 | (2) | 110,000 | 0 | 0 |

| Peter Stüssi | 391,980 | (2) | 391,980 | 0 | 0 |

| Philip Jungen | 84,210 | (2) | 84,210 | 0 | 0 |

| Philip Roth | 21,052 | (2) | 21,052 | 0 | 0 |

| Ralf Naef | 840,000 | 1.2% | 840,000 | 0 | 0 |

| Rene Gahlinger (17) | 749,692 | 1.1% | 249,692 | 0 | 0 |

| Robert Nuesch | 20,000 | (2) | 20,000 | 0 | 0 |

| Roland Hurter | 20,000 | (2) | 20,000 | 0 | 0 |

| Roland Illi | 84,000 | (2) | 84,000 | 0 | 0 |

| Rosmarie Duebi | 10,000 | (2) | 10,000 | 0 | 0 |

| Rowena M. Midel | 1,000 | (2) | 1,000 | 0 | 0 |

| Rudolph Hohenester | 20,000 | (2) | 20,000 | 0 | 0 |

| Sedona AG (7) | 970,000 | 1.4% | 970,000 | 0 | 0 |

| Sonja Rast | 20,000 | (2) | 20,000 | 0 | 0 |

| Stefan Kuny | 47,368 | (2) | 47,368 | 0 | 0 |

| STWE Zentrumsplatz 7+9 (18) | 20,000 | (2) | 20,000 | 0 | 0 |

31

| Swissfirst Bank (Liechtenstein) AG (20) | 3,000,000 | 4.3% | 3,000,000 | 0 | 0 |

| Tennishalle Dietlikon AG (20) | 20,000 | (2) | 20,000 | 0 | 0 |

| Theodor Obrist | 200,000 | (2) | 200,000 | 0 | 0 |

| Theophil Mueller (21) | 330,000 | (2) | 330,000 | 0 | 0 |

| Therese Naef | 13,880 | (2) | 13,880 | 0 | 0 |

| Thomas Fischer | 21,052 | (2) | 21,052 | 0 | 0 |

| TMR Welfare Foundation (21) | 20,000 | (2) | 20,000 | 0 | 0 |

| Tobias Weber | 17,500 | (2) | 17,500 | 0 | 0 |

| Triaxis Trust AG (21) | 40,000 | (2) | 40,000 | 0 | 0 |

| Ueli Voegelin | 10,000 | (2) | 10,000 | 0 | 0 |

| Urs P. Mueller | 200,000 | (2) | 200,000 | 0 | 0 |

| Viktor Puentener | 640,000 | (2) | 640,000 | 0 | 0 |

| Walter Duebi | 10,000 | (2) | 10,000 | 0 | 0 |

| Walter von Allmen | 10,800 | (2) | 10,800 | 0 | 0 |

| Wilhelm Widmer | 30,000 | (2) | 30,000 | 0 | 0 |

32

| William Galine | 20,000 | (2) | 20,000 | 0 | 0 |

| Total | | | 28,435,885 | | |

| (1) | The number and percentage of shares beneficially owned is determined in accordance with the Rules of the Commission, and the information is not necessarily indicative of beneficial ownership for any other purpose. Under such rules, beneficial ownership includes any shares as to which the selling stockholder has sole or shared voting power or investment power and also any shares which the selling stockholder has the right to acquire within 60 days of the date of this Prospectus |

| | |

| (2) | Less than 1%. |

| | |

| (3) | Michael Forster has voting and investment control over Asset Management Switzerland AG. Mr. Forster owns 2,443,620 shares in his own name, and controls 32,000 shares held by Asset Management Switzerland AG. All 2,475,620 of the shares owned and controlled by Mr. Forster are being registered in this Prospectus. |

| | |

| (4) | Brigitte Weiss has voting and investment control over shares held by Hemis Switzerland GmbH. Ms. Weiss owns 25,770 in her own name, and controls 46,000 shares held by Hemis Switzerland GmbH. In this Prospectus, Ms. Weiss is registering 1,770 shares in her own name and 46,000 shares held by Hemis Switzerland GmbH. |

| | |

| (5) | Bruno Weiss is a director and is Chief Financial Officer of Hemis. |

| | |

| (6) | Craig Schneider has voting and investment control over Corex Gold Corp. |

| | |

| (7) | Costantino Pinelli has voting and investment control over Sedona AG. Mr. Pinelli owns 97,604 shares in his own name, and controls 970,000 shares held by Sedona AG. Mr Pinelli is registering 57,604 shares in his own name and 970,000 shares held by Sedona AG. . |

| | |

| (8) | Alan Carter has voting and investment control over Electrum Capital, Inc. |

| | |

| (9) | Michael Friedrich has voting and investment control over Friedrich Activ Asset Management. Mr. Friedrich owns 1,841,760 shares in his own name and controls 1,144,315 shares held by Friedrich Activ Asset Management. Mr. Friedrich is registering 1,541,760 shares in his own name, and 1,144,315 shares held by Friedrich Activ Asset Management. |

| | |

| (10) | Gerald Wong is the accountant for Hemis. |

| | |

| (11) | Jordan Shapiro has investment and voting control over shares held by Hudson Capital Corporation. Mr. Shapiro has acted as our consultant. Mr. Shapiro owns no shares in his own name, but controls 1,800,000 shares held by Hudson Capital. |

| | |

| (12) | Micah Eldred has voting and investment control over Island Stock Transfer. Island Stock Transfer is our stock transfer agent. |

| | |

| (13) | Marc Stutz and Marcus Stutz are not related. |

| | |

| (14) | Norman Meier is a director and is President and Chief Executive Officer of Hemis, Dr. Meier has voting and investment control over Noeme Investment Corporation. Dr. Meier owns 233,950,000 |

33

| shares in his own name, and controls 2,000,000 shares held by Noeme Investment Corporation. Dr. Meier is registering 6,000,000 shares in his own name and 2,000,000 shares held by Noeme Investment Corporation. |

| | |

| (15) | Hilary May and Kenneth Simpson have voting and investment control over Pampero Limited. |

| | |

| (16) | Werner Gmuer has voting and investment control over Paxar AG. |

| | |

| (17) | Mr. Gahlinger owns 249,692 shares in his own name. Also, Swissalis AG has the right to receive 500,0000 shares from us within the next 60 days pursuant to an agreement that was entered into on April 10, 2007 between Hemis and Swissalis. Mr. Gahlinger has voting and investment control over Swissalis AG. |

| | |

| (18) | Theophil Mueller has voting and investment control over STWE Zentrumsplatz 7+9. |

| | |

| (19) | Swissfirst Bank (Liechstein) has purchased 1,500,000 Hemis shares on behalf of Safeport Gold & Silver Fund (located in Triesen, Liechtenstein) in their capacity as banker/broker. Dr. J. Schatz has voting and investment control over the Safeport Gold & Silver Fund. |

| | |

| (20) | Cyrill Keller has voting and investment control over Tennishalle Dietlikon AG. |

| | |

| (21) | Theophil Mueller has voting and investment control over TMR Welfare Foundation. |

| | |

| (22) | Heinz Brmettler, Urs W. Brander, Beate Mosimann, and Regine Schoch have voting and investment control over Triaxis Trust. |

The percentages are based on the 70,272,786 shares of common stock outstanding on April 16, 2007 and assume all shares being registered are sold by the Selling Shareholders.

Other than as described above, none of the Selling Shareholders or their beneficial owners has had a material relationship with us other than as a shareholder at any time within the past three years, or has ever been one of our officers or directors or an officer or director of our predecessors or affiliates.

Island Stock Transfer is an affiliate of Spartan Securities, an NASD registered broker/dealer. Other than Island Stock, no selling shareholders are NASD registered broker-dealers or affiliates of NASD registered broker-dealers.

Legal Proceedings

We are not aware of any pending or threatened legal proceedings which involve Hemis or any of its properties or subsidiaries.

Directors, Executive Officers, Promoters, and Control Persons

Directors and Officers

Our bylaws allow the number of directors to be fixed by the Board of Directors. Our Board of Directors has fixed the number of directors at four.

34

Our current directors and officers are as follows:

| Name | Age | Position |

| | | |

| Dr. Norman Meier, PhD, MBA | 32 | Director, President, Chief Executive Officer, |

| | | |

| Bruno Weiss | 53 | Director, Chief Financial Officer, Secretary |

| | | |

| Dr. Douglas Oliver, PhD | 56 | Director, Vice President of Operations |

| | | |

| Richard Hamelin | 52 | Director |

The directors will serve as directors until our next shareholder meeting or until a successor is elected who accepts the position. Officers hold their positions at the will of the Board of Directors. There are no arrangements, agreements or understandings between non-management shareholders and management under which non-management shareholders may directly or indirectly participate in or influence the management of our affairs.

Dr. Norman Meier, Director, President and Chief Executive Officer

Norman Meier is a founder of Hemis and has been a director since our inception in February 2005 and President and Chief Executive Officer since May 1, 2005. From May 2004 to May 2005 Dr. Meier was the founder and President of LEAP Institute LLC, a company in the business of providing financial services and investment advice to private investors and companies. From November 2002 to April 2004 he worked as Manager Global Sales Support for Man Investments, Switzerland, where he managed a global sales team in the hedge fund industry to raise money from financial institutions, bank and brokers around the world. From April 2002 to October 2002 Dr. Meier worked as an Investment Advisor at Canaccord Capital in Vancouver, British Columbia, Canada, where he established and managed portfolios, integrated risk management strategies, evaluated performance models for existing portfolios, provided investment advice and traded in securities. From 1995 to 2001 he worked at AWD Independent Financial Services, Switzerland, initially as a financial advisor, and later as a team manager. Norman Meier has a PhD in Human Behavior, an MBA and a BA, all from Newport University in Switzerland. He holds two designations from the Canadian Securities Institute: a Canadian Investment Manager Designation and a Derivatives Market Specialist Designation. He also holds a Financial Planning Designation from AWD Switzerland. Dr. Meier is also a director, President and Chief Executive Officer of Tecton Corporation, a public company that is required to file annual and quarterly reports with the SEC. Tecton has applied for a symbol on the OTC Bulletin Board.

Bruno Weiss, Director and Chief Financial Officer

Bruno Weiss has been a director of Hemis since our inception in February 2005. He was appointed as Chief Financial Officer in May 2005. Mr. Weiss has worked in the financial field for over 30 years. He has extensive experience in foreign exchange trading and management and in marketing hedge funds. From July 2002 to the present, Mr. Weiss has been the Managing Director and Hedge Fund Consultant for Glayva Investment GmbH, Switzerland, where he marketed different classes of hedge funds until February 2006. Glavya Investment GmbH changed its name in 2005 to Hemis Switzerland GmbH, and since the incorporation of Hemis Corp. in February 2005, it has been principally involved in providing consulting services to us or

35