UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-QSB

(MARK ONE)

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE

ACT OF 1934

FOR THE QUARTERLY PERIOD ENDED September 30, 2006

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934 FOR THE

TRANSITION PERIOD FROM _________ TO __________

COMMISSION FILE NUMBER: 000-51364

Dolce Ventures, Inc.

(EXACT NAME OF SMALL BUSINESS ISSUER AS SPECIFIED IN ITS CHARTER)

Utah | 32-0028823 |

| (STATE OR OTHER JURISDICTION OF | (I.R.S. EMPLOYER IDENFIFICATION |

| INCORPORATION OR ORGANIZATION | NO.) |

The Farmhouse

558 Lime Rock Road

Lime Rock, Connecticut 06039

(ADDRESS OF PRINCIPAL EXECUTIVE OFFICES) (ZIP CODE)

ISSUER 'S TELEPHONE NUMBER, INCLUDING AREA CODE: (860) 435-7000

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o.

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x.

The number of shares of Common Stock of the Registrant, par value $0.001 per share, outstanding at November 13, 2006 was 100,770,140.

Transitional Small business Disclosure Format (Check one): Yes o; No x.

PART I. FINANCIAL INFORMATION

Item 1. FINANCIAL STATEMENTS

Dolce Ventures, Inc.

Consolidated Financial Statements

Unaudited

September 30, 2006

(Stated in US dollars)

Dolce Ventures, Inc. |

Consolidated Balance Sheet |

Unaudited |

At September 30, 2006 |

(Stated in US Dollars) |

| Sep 30, 2006 | Dec 31, 2005 | ||||||

Assets | |||||||

Current Assets | |||||||

| Cash and Cash Equivalents | $ | 5,328,306 | $ | 571,194 | |||

| Accounts Receivable | 6,887,070 | 7,770,168 | |||||

| Notes Receivables | 225,213 | - | |||||

| Advances to Suppliers | 250,406 | 372,442 | |||||

| Prepaid Expenses | 93,433 | 12,097 | |||||

| Other Receivables | 905,327 | 437,922 | |||||

| Total Current Assets | $ | 13,689,755 | $ | 9,163,823 | |||

Long Term Assets | |||||||

| Investments in Equity Securities | $ | 2,697,852 | $ | 2,443,378 | |||

| Plant and Equipment, Net | 3,443,273 | 3,200,682 | |||||

| Construction in Progress | 5,798,781 | 3,071,497 | |||||

| Intangible Assets | 448,406 | 437,265 | |||||

| Total Long Term Assets | $ | 12,388,312 | $ | 9,152,822 | |||

Total Assets | $ | 26,078,067 | $ | 18,316,645 | |||

Liabilities | |||||||

Current Liabilities | |||||||

| Accounts Payable | $ | 457,120 | $ | 3,090,870 | |||

| Other Payables | 5,509,741 | 2,264,965 | |||||

| Unearned Revenue | 103,616 | 133,035 | |||||

| Accrued Liabilities | 146,184 | 201,384 | |||||

| Total Current Liabilities | $ | 6,216,661 | $ | 5,690,254 | |||

Total Liabilities | $ | 6,216,661 | $ | 5,690,254 | |||

See Accompanying Notes to the Consolidated Financial Statements

2

Dolce Ventures, Inc. |

Consolidated Balance Sheet |

Unaudited |

At September 30, 2006 |

(Stated in US Dollars) |

Members’ Equity | - | $ | 12,626,391 | ||||

Stockholders’ Equity | |||||||

Series A Convertible Preferred Stock, Par value $0.001, Issued 14,361,647 shares at Sep 7, 2006; Series B Convertible Preferred Stock, Par value $0.001, Issued 2,509,782 shares at Sep 7, 2006. [SERIES A AND B PREFERRED WERE ISSUED AND OUTSTANDING AT 9/30] | - | - | |||||

| Common Stock, Par value $0.001, Authorized 250,000,000 shares, Issued 100,770,140 at September 30, 2006 | $ | 100,700 | - | ||||

| Additional Paid-In Capital | 11,262,749 | - | |||||

| Retained Earnings | 8,497,957 | - | |||||

| $ | 19,861,406 | - | |||||

Total Liabilities & Stockholders’ Equity | $ | 26,078,067 | $ | 18,316,645 |

See Accompanying Notes to the Consolidated Financial Statements

3

Dolce Ventures, Inc. |

Consolidated Statement of Income |

Unaudited |

September 30, 2006 |

(Stated in US Dollars) |

| Nine months ended | Three months ended | ||||||||||||

September 30, 2006 | September 30, 2006 | ||||||||||||

| 2006 | 2005 | 2006 | 2005 | ||||||||||

| Net Sales | $ | 4,971,156 | $ | 3,319,668 | $ | 3,471,616 | $ | 851,442 | |||||

| Cost of Sales | (1,849,128 | ) | (1,485,603 | ) | (865,641 | ) | (308,709 | ) | |||||

| Gross Profit | $ | 3,122,028 | $ | 1,834,065 | $ | 2,605,975 | $ | 542,733 | |||||

| Selling and Distributing Costs | (66,497 | ) | (66,668 | ) | (39,673 | ) | (24,805 | ) | |||||

| Administrative and Other | |||||||||||||

| Operating Expenses | (693,973 | ) | (386,973 | ) | (440,154 | ) | (158,568 | ) | |||||

| Income from Operations | $ | 2,361,558 | $ | 1,380,424 | $ | 2,126,148 | $ | 359,360 | |||||

| Interest (Expenses)/Income, net | (2,169 | ) | 1,182 | 973 | 37 | ||||||||

| Other Expenses, net | (159 | ) | (41,835 | ) | (30,417 | ) | (40,384 | ) | |||||

| Other Income | 13,205 | 11,838 | - | 51,928 | |||||||||

| Income before Taxes | $ | 2,372,435 | $ | 1,351,609 | $ | 2,096,704 | $ | 370,941 | |||||

| Income Tax | (183,755 | ) | (106,943 | ) | (166,168 | ) | (32,242 | ) | |||||

Net Income | $ | 2,188,680 | $ | 1,244,666 | $ | 1,930,536 | $ | 338,699 | |||||

| Net Income per Share, Basic & Diluted | 0.02 | 0.01 | 0.02 | 0.00 | |||||||||

| Weighted Average Shares Outstanding | 100,770,140 | 100,770,140* | 100,770,140* | 100,770,140* | |||||||||

* Number of shares outstanding the day of the merger for comparison only

See Accompanying Notes to the Consolidated Financial Statements

4

Dolce Ventures, Inc. |

Consolidated Statement of Cash Flows |

For the Nine Months Ended September 30, 2006 |

(Stated in US Dollars) |

| Nine months ended | |||||||

| September 30, 2006 | September 30, 2005 | ||||||

Cash Flows from Operating Activities | |||||||

| Net Income | $ | 2,188,680 | $ | 1,244,666 | |||

| Decrease/ (Increase) in Accounts Receivable | 617,274 | (3,047,138 | ) | ||||

| Increase in Notes Receivable | (225,213 | ) | - | ||||

| (Increase)/ Decrease in Prepayments and | |||||||

| Other Receivables | (426,705 | ) | 838,013 | ||||

| (Decrease)/ Increase in Accounts Payable | (2,633,750 | ) | 1,294,941 | ||||

| Increase in Other payables and Accruals | 3,160,157 | 329,185 | |||||

| Equity in an Investment | (254,474 | ) | (43,279 | ) | |||

| Depreciation and Amortization | 799,780 | 702,641 | |||||

| Net Cash Provided by Operating Activities | $ | 3,225,749 | $ | 1,319,029 | |||

Cash Flows from Investing Activities | |||||||

| Purchases of Intangible Assets | $ | (11,141 | ) | $ | (374,588 | ) | |

| Payment of Construction in Progress | (2,727,284 | ) | (385,427 | ) | |||

| Purchase of Fixed Assets | (1,042,371 | ) | (1,072,002 | ) | |||

| Net Cash Used in Investing Activities | $ | (3,780,796 | ) | $ | (1,832,017 | ) | |

Cash Flows from Financing Activities | |||||||

| Issuance of Common Stock | $ | 5,246,891 | - | ||||

| Net Cash Provided by Financing Activities | $ | 5,246,891 | - | ||||

Net in Cash and Cash Equivalents(Used)/Sourced | $ | 4,691,844 | $ | (512,988 | ) | ||

Effect of Foreign Currency Translation on Cash and | |||||||

Cash Equivalents | 65,268 | 1,973 | |||||

Cash and Cash Equivalents - Beginning of Year | 571,194 | 668,346 | |||||

Cash and Cash Equivalents - End of Year | $ | 5,328,306 | $ | 157,331 | |||

See Accompanying Notes to the Consolidated Financial Statements

5

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

1. Basis of Presentation

The unaudited consolidated financial statements of Dolce Ventures, Inc. have been prepared in accordance with generally accepted accounting principles for interim financial information and pursuant to the requirements for reporting on Form 10-QSB and Item 310(b) of Regulation S-B. Accordingly, they do not include all the information and footnotes required by generally accepted accounting principles for complete financial statements. However, such information reflects all adjustments (consisting solely of normal recurring adjustments), which are, in the opinion of management, necessary for a fair statement of results for the interim periods. Results shown for interim periods are not necessarily indicative of the results to be obtained for a full fiscal year.

2. Organization and Principal Activities

The Company is a natural gas services operator, principally engaging in the investment, operation and management of city gas pipeline infrastructure, in the distribution of natural gas to residential and industrial users, in the construction and operation of natural gas stations, and in the development and application of natural gas related technologies.

6

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

3. Summary of Significant Accounting Policies

(A) Consolidation

The consolidated financial statements include the accounts of the Company and its subsidiaries (“the Group”). Significant intercompany transactions have been eliminated in consolidation. Investments in which the company has a 20 percent to 50 percent voting interest and where the company exercises significant influence over the investee are accounted for using the equity method.

As of September 30, 2006, the particulars of the subsidiaries are as follows:

| Name of Company | Place of Incorporation | Date of Incorporation | Attributable Equity Interest % | Registered Capital | ||||

| Pegasus Tel, Inc. | USA | 2/19/2002 | 100 | |||||

| GAS Investment China Co., Ltd. | BVI | 6/19/2003 | 100 | |||||

| Beijing Zhong Ran Wei Ye Gas Co., | ||||||||

| Ltd | PRC | 8/29/2001 | 100 | RMB 77,454,532 | ||||

| Ningjin Weiye Gas Co., Ltd | PRC | 12/3/2003 | 100 | RMB 3,000,000 | ||||

| Jinzhou Weiye Gas Co., Ltd | PRC | 7/19/2005 | 100 | RMB 3,000,000 | ||||

| Xingtang Weiye Gas Co., Ltd | PRC | 2/18/2005 | 100 | RMB 3,000,000 | ||||

| Linzhang Weiye Gas Co., Ltd | PRC | 7/6/2006 | 100 | RMB 1,000,000 | ||||

| Anping Weiye Gas Co., Ltd | PRC | 8/4/2006 | 100 | RMB 5,000,000 | ||||

| Wuqiao Gas Co., Ltd | PRC | 6/30/2005 | 100 | RMB 2,000,000 | ||||

Yutian Zhongran Weiye Gas Co., Ltd | PRC | 12/19/2003 | 100 | RMB 3,000,000 | ||||

| Langfang Development | ||||||||

| Region Weiye Dangerous | ||||||||

| Goods Transportation Co., Ltd | PRC | 3/22/2006 | 100 | RMB 1,000,000 | ||||

| Sihong Weiye Gas Co., Ltd | PRC | 12/3/2005 | 100 | RMB 10,000,000 | ||||

| Peixian Weiye Gas Co., Ltd | PRC | 8/22/2006 | 100 | RMB 5,000,000 | ||||

| Sishui Weiye Gas Co., Ltd | PRC | 12/22/2005 | 100 | RMB 3,000,000 | ||||

Longyao Zhongran Weiye Gas Co., Ltd | PRC | 10/13/2006 | 100 | RMB 3,000,000 | ||||

| Shenzhou Weiye Gas Co., Ltd | PRC | 12/23/2006 | 100 | RMB 3,000,000 |

7

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(B) Economic and Political Risks

The Company’s operations are conducted in the PRC. Accordingly, the Company’s business, financial condition and results of operations may be influenced by the political, economic and legal environment in the PRC, and by the general state of the PRC economy.

The Company’s operations in the PRC are subject to special considerations and significant risks not typically associated with companies in North America and Western Europe. These include risks associated with, among others, the political, economic and legal environment and foreign currency exchange. The Company’s results may be adversely affected by changes in the political and social conditions in the PRC, and by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion, remittances abroad, and rates and methods of taxation, among other things.

(C) Use of Estimates

In preparing of the consolidated financial statements in conformity with accounting principles generally accepted in the United States of America, management makes estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the dates of the consolidated financial statements, as well as the reported amounts of revenues and expenses during the reporting year. These accounts and estimates include, but are not limited to, the valuation of accounts receivable, inventories, deferred income taxes and the estimation on useful lives of plant and machinery. Actual results could differ from those estimates.

(D) Cash and Cash Equivalents

The Company considers all cash and other highly liquid investments with initial maturities of three months or less to be cash equivalents.

(E) Accounts and Other Receivable

Accounts and other receivable are recorded at net realizable value consisting of the carrying amount less an allowance for uncollectible accounts, as needed. The Company extends unsecured credit to customers in the normal course of business and does not accrue interest on trade accounts receivable. Allowance for uncollectible accounts as of September 30, 2006 is not significant.

8

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(F) Advances to Suppliers

Advances to suppliers represent the cash paid in advance for purchasing raw materials. The advances to suppliers are interest free and unsecured.

(G) Investments in Equity Securities

The consolidated statement of income includes the Group's share of the post-acquisition results of its associate for the year. In the consolidated balance sheet, investments in equity securities are stated at the Group's share of the net assets of the associates plus the premium paid less any discount on acquisition in so far as it has not already been amortized to the statement of income, less any identified impairment loss.

Portion of | ||||||||||

Nominal | ||||||||||

Name of | Place | Form of | Value of | |||||||

Associate | of | Business | Registered | Registered | Principal | |||||

Company | Registration | Structure | Capital | Capital | Activities | |||||

| Beijing Zhongran Xiangke Oil Gas Technology Co. Ltd | PRC | Sino-foreign equity joint venture | Registered RMB 20,000,000 | 40 | Trading of natural gas and gas pipeline construction |

Beijing Zhongran Xiangke Oil Gas Technology Co. Ltd is the Group's 40% owned joint venture company and is principally engaged in sale of compressed natural gas to domestic households and industrial around sub-urban areas of Beijing and part of sub-urban areas in Hebei Province and Tianjin.

9

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(H) Long-Lived Assets

The Group adopted Statement of Financial Accounting Standards No. 144, “Accounting for the Impairment or Disposal of Long-Live Assets” (“SFAS 144”), which addresses financial accounting and reporting for the impairment or disposal of long-lived assets. The Group periodically evaluates the carrying value of long-lived assets to be held and used in accordance with SFAS 144. SFAS 144 requires impairment losses to be recorded on long-lived assets used in operations when indicators of impairment are present and the undiscounted cash flows estimated to be generated by those assets are less than the assets’ carrying amounts. In that event, a loss is recognized based on the amount by which the carrying amount exceeds the fair market value of the long-lived assets. Loss on long-lived assets to be disposed of is determined in a similar manner, except that fair market values are reduced for the cost of disposal. Based on its review, the Company believes that, as of September, 2006, there were no significant impairments of its long-lived assets.

(I) Plant and Equipment

Plant and equipment, other than construction in progress, are stated at cost less depreciation and amortization and accumulated impairment loss.

Plant and equipment are carried at cost less accumulated depreciation. Depreciation is provided over their estimated useful lives, using the straight-line method. Estimated useful lives of the plant and equipment are as follows:

| Gas Pipelines | 25 years |

| Motor Vehicles | 10 years |

| Machinery & Equipment | 20 years |

| Buildings | 25 years |

| Leasehold Improvements | 25 years |

| Office Equipment | 8 years |

The cost and related accumulated depreciation of assets sold or otherwise retired are eliminated from the accounts and any gain or loss is included in the statement of income. The cost of maintenance and repairs is charged to income as incurred, whereas significant renewals and betterments are capitalized.

10

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(J) Intangible assets

Intangible assets, are stated at cost less amortization and accumulated impairment loss. Amortization is provided over their estimated useful lives, using the straight-line method. Estimated useful lives of the intangibles are as follows:

| Land use rights | 40 - 50 years |

| Franchises | 30 years |

| Other intangibles | 3 years |

(K) Construction in Progress

Construction in progress represents the cost of constructing pipelines and is stated at cost. Costs comprise direct and indirect incremental costs of acquisition or construction. Completed items are transferred from construction in progress to the gas pipelines of fixed assets when they are ready for their intended use. The major cost of construction relates to construction materials, direct labor wages and other overhead. Construction of pipeline, through which to distribute natural gas, is one of the Group’s principal businesses. The Group builds city main pipeline network and branch pipeline network to make gas connection to resident users, industrial, and commercial users, with the objective of generating revenue on gas connection and gas usage fees collected from these customers. As at September 30, 2006, the pipelines under construction include mainly the projects in several cities of Hebei and Jiangsu province, and in Beijing. These projects, once completed, will significantly increase the gas supply capacity.

(L) Unearned revenue

Unearned revenue represents prepayments by customers for gas purchases and advance payments on construction and installation of pipeline contracts. The Company records such prepayment as unearned revenue when the payments are received.

(M) Financial Instruments

The carrying amounts of all financial instruments approximate fair value. The carrying amounts of cash, accounts receivable, accounts payable and accrued liabilities approximate fair value due to the short-term nature of these items. The carrying amounts of borrowings approximate the fair value based on the Company’s expected borrowing rate for debt with similar remaining maturities and comparable risk.

11

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(N) Foreign Currency Translation

The Company maintains its consolidated financial statements in the functional currency. The functional currency of the Company is the Renminbi (RMB). Monetary assets and liabilities denominated in currencies other than the functional currency are translated into the functional currency at rates of exchange prevailing at the balance sheet dates. Transactions denominated in currencies other than the functional currency are translated into the functional currency at the exchanges rates prevailing at the dates of the transaction. Exchange gains or losses arising from foreign currency transactions are included in the determination of net income for the respective periods.

For financial reporting purposes, the consolidated financial statements of the Company which are prepared using the functional currency have been translated into United States dollars. Assets and liabilities are translated at the exchange rates at the balance sheet dates and revenue and expenses are translated at the average exchange rates and stockholders’ equity is translated at historical exchange rates. Any translation adjustments resulting are not included in determining net income but are included in foreign exchange adjustment to other comprehensive income, a component of stockholders’ equity.

September 30, 2006 | September 30, 2005 | ||||||

| Nine months end RMB : US$ exchange rate | 7.8989 | 8.0775 | |||||

| Average nine months end RMB : US$ exchange rate | 8.0013 | 8.2183 | |||||

| Average three months end RMB : US$ exchange rate | 7.9771 | 8.1520 | |||||

The RMB is not freely convertible into foreign currency and all foreign exchange transactions must take place through authorized institutions. No representation is made that the RMB amounts could have been, or could be, converted into US$ at the rates used in translation.

12

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(O) Revenue Recognition

Revenue is recognized when services are rendered to customers when a formal arrangement exists, the price is fixed or determinable, the delivery is completed, no other significant obligations of the Company exist and collectibility is reasonably assured. Payments received before all of the relevant criteria for revenue recognition are satisfied are recorded as unearned revenue.

Net sales, which consist of gas and connection fee revenue. And the cost of sales consists of gas cost and connection cost.

Gas connection revenue is recognized when the outcome of a contract can be estimated reliably and the stage of completion at the balance sheet date can be measured reliably.

Sales of natural gas are recognized when goods are delivered and title has passed.

(P) Other Income

Other income represents the Group’s share of post- acquisition results of its investment in equity securities for the year.

(Q) Income Taxes

Deferred income taxes are recognized for the tax consequences in future years of differences between the tax bases of assets and liabilities and their financial reporting amounts at each period end based on enacted tax laws and statutory tax rates applicable to the periods in which the differences are expected to affect taxable income. Valuation allowances are established when necessary to reduce deferred tax assets to the amount expected to be realized. At September 30, 2006, there was no significant book to tax differences.

Pursuant to the tax laws of PRC, general enterprises are subject to income tax at an effective rate of 33%. The Group is in the natural gas industry whose development is encouraged by the government. According to the income tax regulation, any company engaged in the natural gas industry enjoys a favorable tax rate. Also, the Company is exempt from corporate income tax for its first two years and is then entitled to a 50% tax reduction for the succeeding three years. The Company’s first profitable tax year was 2003. Accordingly, the Company’s income is subject to a reduced tax rate of 9%. Subsidiaries are subject to the effective rate of 33%.

13

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(R) Advertising

The Group expensed all advertising costs as incurred. Advertising costs for the years ended September 30, 2006 and 2005 were insignificant.

(S) Concentration of Credit Risk

Concentration of credit risk is limited to accounts receivable and is subject to the financial conditions of major customers. The Group does not require collateral or other security to support accounts receivable. The Group conducts periodic reviews of its clients’ financial condition and customers’ payment practices to minimize collection risk on accounts receivable.

(T) Statement of Cash Flows

In accordance with Statement of SFAS 95, “Statement of Cash Flows”, cash flows from the Company’s operations is calculated based upon the local currencies. As a result, amounts related to assets and liabilities reported on the statement of cash flows will not necessarily agree with changes in the corresponding balances on the balance sheet.

(U) Recent Accounting Pronouncements

In May 2006, the FASB issued a SFAS 154, “Accounting Changes and Error Corrections” to replace APB Opinion No. 20, “Accounting Changes” and SFAS 3, “Reporting Accounting Changes in Interim Financial Statements” requiring retrospective application to prior periods consolidated financial statements of changes in accounting principle, unless it is impracticable to determine either the period-specific effects or the cumulative effect of the change. When it is impracticable to determine the period-specific effects of an accounting change on one or more individual prior periods presented, SFAS 154 requires the new accounting principle be applied to the balances of assets and liabilities as of the beginning of the earliest period for which retrospective application is practicable and that a corresponding adjustment be made to the opening balance of retained earnings (or other appropriate components of equity or net assets in the statement of financial position) for that period rather than being reported in an income statement. When it is impracticable to determine the cumulative effect of applying a change in accounting principle to all prior periods, SFAS 154 requires that the new accounting principle be applied as if it were adopted prospectively from the earliest date practicable. The effective date for this statement is for accounting changes and corrections of errors made in fiscal year beginning after September 15, 2006.

14

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

(U) Recent Accounting Pronouncements (Cont’d)

In February 2006, the FASB issued a SFAS 155, “Accounting for Certain Hybrid Financial Instruments” to amend FASB Statements No. 133, Accounting for Derivative Instruments and Hedging Activities, and No. 140, Accounting for Transfers and Servicing of Financial Assets and Extinguishments of Liabilities. This statement permits fair value remeasurement for any hybrid financial instrument that contains an embedded derivative that otherwise would require bifurcation and eliminate the prohibition on a qualifying special-purpose entity from holding a derivative financial instrument that pertains to a beneficial interest other than another derivative financial instrument. This statement is effective for all financial instruments acquired or issued after the beginning of an entity’s first fiscal year that begins after September 15, 2006.

The Group does not anticipate that the adoption of these two standards will have a material impact on these consolidated financial statements.

15

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

4. Plant and Equipment

Plant and Equipment consist of the following as of September 30:

| 2006 | ||||

At Cost | ||||

| Gas Pipelines | $ | 2,936,293 | ||

| Motor Vehicles | 299,945 | |||

| Machinery & Equipment | 258,650 | |||

| Buildings | 88,873 | |||

| Leasehold Improvements | 47,053 | |||

| Office Equipment | 46,463 | |||

| $ | 3,677,277 | |||

Less: Accumulated depreciation | ||||

| Gas Pipelines | $ | 138,746 | ||

| Motor Vehicles | 38,076 | |||

| Machinery & Equipment | 23,082 | |||

| Buildings | 5,910 | |||

| Leasehold Improvements | 17,075 | |||

| Office Equipment | 11,115 | |||

| $ | 234,004 | |||

| $ | 3,443,273 | |||

16

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

5. Intangible Assets

Intangible assets consist of the following as of September 30:

| 2006 | ||||

| Land use rights | $ | 112,652 | ||

| Franchises | 335,754 | |||

$ | 448,406 | |||

The Group operates as a local natural gas distributor in a city or county, known as an operational location, under an exclusive franchise agreement between the Group and the local government or entities in charge of gas utility. Franchises are the rights to develop sites in Anping and Jinzhou in China. They are stated at cost less accumulated depreciation.

6. Income Taxes

In accordance with the relevant tax laws and regulations of PRC, the corporation income tax rate is 33%. However, in accordance with the relevant taxation laws in the PRC, the Group is eligible for tax concessions and was exempted from part of the PRC income taxes for the year.

The following table accounts for the differences between the actual tax provision and the amounts obtained by applying the applicable PRC corporation income tax rate of 33% to income before taxes for the years ended September 30,.

| 2006 | 2005 | ||||||

| Income before Taxes | $ | 2,372,435 | $ | 1,351,609 | |||

| Provision for income taxes at PRC income tax rate | 782,904 | 446,031 | |||||

| Effect of tax exemption granted to the Group | (599,149 | ) | (339,088 | ) | |||

| Income Tax | $ | 183,755 | $ | 106,943 | |||

17

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

7. Business and Geographical Segments

The Company has contracted with customers usually in two business segments: one is for the construction and installation of gas facilities and another one is the subsequent sales of gas to those customers through the gas facilities the Company constructs. However, the respective gas facilities contracts and gas supply contracts have separate bases for revenue recognition.

For management purposes, the Group is currently organized into two major operating divisions - gas pipeline construction (installation of gas facilities) and sales of piped gas. These principal operating activities are the basis on which the Group reports its primary segment information.

Nine months ended | Gas pipeline | Sales of | ||||||||

September 30, 2006 | construction | piped gas | Consolidated | |||||||

| Net Sales | $ | 3,104,605 | $ | 1,866,551 | $ | 4,971,156 | ||||

| Cost of sales | (469,824 | ) | (1,379,304 | ) | (1,849,128 | ) | ||||

| Segment result | $ | 2,634,781 | $ | 487,247 | $ | 3,122,028 | ||||

Nine months ended | Gas pipeline | Sales of | ||||||||

September 30, 2005 | construction | piped gas | Consolidated | |||||||

| Net Sales | $ | 1,959,227 | $ | 1,360,441 | $ | 3,319,668 | ||||

| Cost of sales | (260,322 | ) | (1,225,281 | ) | (1,485,603 | ) | ||||

| Segment result | $ | 1,698,905 | $ | 135,160 | $ | 1,834,065 | ||||

18

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

Three months ended | Gas pipeline | Sales of | ||||||||

September 30, 2006 | construction | piped gas | Consolidated | |||||||

| Turnover | $ | 2,745,948 | $ | 725,668 | $ | 3,471,616 | ||||

| Cost of sales | (405,609 | ) | (460,032 | ) | (865,641 | ) | ||||

| Segment result | $ | 2,340,339 | $ | 265,636 | $ | 2,605,975 | ||||

Three months ended | Gas pipeline | Sales of | ||||||||

September 30, 2005 | construction | piped gas | Consolidated | |||||||

| Turnover | $ | 653,076 | $ | 198,366 | $ | 851,442 | ||||

| Cost of sales | (130,050 | ) | (178,659 | ) | (308,709 | ) | ||||

| Segment result | $ | 523,026 | $ | 19,707 | $ | 542,733 | ||||

The Group's operations are located in the PRC. All revenue is from customers in the PRC. All of the Group’s assets are located in the PRC. Sales of piped gas and gas pipeline construction are carried out in the PRC. Accordingly, no analysis of the Group's sales and assets by geographical market is presented.

19

Dolce Ventures, Inc. |

Notes to the Consolidated Financial Statements |

For the Nine Months Ended September 30, 2006 and, 2005 |

(Stated in US Dollars) |

8. Related Party Transactions

The following material transactions with related parties were carried out in the ordinary course of business and on normal commercial terms:

Sales to Beijing Zhongran Xiangke Oil Gas Technology Co. Ltd (Zhongran Xiangke), an investee for which the equity method is used, for the nine month ended 2006 and 2005 were $107,551 and $869,809 respectively. The amounts receivable from Zhongran Xiangke for September 2006 and 2005 were $57,561 and $162,823 respectively.

Sales to Beijing Zhongyou Xiangke Oil Gas Technology Co. Ltd (Zhongyou Xiangke), an investee of Zhongran Xiangke, for the nine month ended 2006 and 2005 were nil and $ 52,495 respectively. The amounts receivable from Zhongyou Xiangke for the September 2006 and 2005 were $13,688 and $19,620 respectively.

20

DISCLAIMER REGARDING FORWARD-LOOKING STATEMENTS

Our disclosure and analysis in this Quarterly Report contains some forward-looking statements. Certain of the matters discussed concerning our operations, cash flows, financial position, economic performance and financial condition, including, in particular, future sales, product demand, the market for our products in the People’s Republic of China, competition, exchange rate fluctuations and the effect of economic conditions include forward-looking statements within the meaning of section 27A of the Securities Act and Section 21E of the Exchange Act.

Statements that are predictive in nature, that depend upon or refer to future events or conditions or that include words such as "expects," "anticipates," "intends," "plans," "believes," "estimates" and similar expressions are forward-looking statements. Although we believe that these statements are based upon reasonable assumptions, including projections of orders, sales, operating margins, earnings, cash flow, research and development costs, working capital, capital expenditures and other projections, they are subject to several risks and uncertainties, and therefore, we can give no assurance that these statements will be achieved.

Investors are cautioned that our forward-looking statements are not guarantees of future performance and the actual results or developments may differ materially from the expectations expressed in the forward-looking statements.

As for the forward-looking statements that relate to future financial results and other projections, actual results will be different due to the inherent uncertainty of estimates, forecasts and projections may be better or worse than projected. Given these uncertainties, you should not place any reliance on these forward-looking statements. These forward-looking statements also represent our estimates and assumptions only as of the date that they were made. We expressly disclaim a duty to provide updates to these forward-looking statements, and the estimates and assumptions associated with them, after the date of this filing to reflect events or changes in circumstances or changes in expectations or the occurrence of anticipated events.

We undertake no obligation to publicly update any forward-looking statement, whether as a result of new information, future events or otherwise. You are advised, however, to consult any additional disclosures we make in our reports on Form 10-KSB, Form 10-QSB, Form 8-K, or their successors. We also note that we have provided a cautionary discussion of risks and uncertainties under the caption "Risk Factors" in this Current Report. These are factors that we think could cause our actual results to differ materially from expected results. Other factors besides those listed here could also adversely affect us.

21

The following discussion and analysis of our financial condition and results of operations should be read in conjunction with the financial statements and accompanying notes and the other financial information appearing in Part I, Item 1 and elsewhere in this Quarterly Report.

Overview

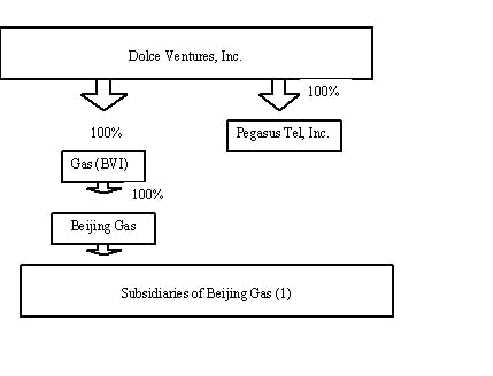

Dolce Ventures, Inc. (“we”, “us” or the “Company”) is engaged in the development of natural gas distribution systems in small- and medium-sized cities in the People’s Republic of China (“PRC”), as well as the distribution of natural gas to residential, commercial and industrial customers in the PRC, through our indirectly-owned subsidiaries in the PRC, Beijing ZhongRan Weiye Gas Company and its subsidiaries (“Beijing Gas”). We also have a subsidiary, Pegasus Tel, Inc., which owns and operates payphones. We plan to spin off our payphone operation by making a dividend of the Pegasus Tel, Inc. shares to our shareholders of record as of August 30, 2006. The discussion and analysis in this Section is focused on our natural gas business operated by Beijing Gas and its subsidiaries in the PRC as the operations of Pegasus Tel., Inc. are negligible.

Beijing Gas is organized as a operating and holding company with 13 subsidiaries, known as project companies, in three provinces, and four branches offices in Beijing, as shown on the corporate structure chart provided below. The project companies are the operating subsidiaries of Beijing Gas. Each project company operates as a local natural gas distributor in a city or county, known as an operational location, under an exclusive franchise agreement between Beijing Gas and the local government or entities in charge of gas utility, pursuant to which Beijing Gas formed the project company to operate the natural gas distribution project in the operational location.

In addition, Beijing Gas holds a 40% equity interest in Beijing Zhong Ran Xiang Ke Oil and Gas Technology Co. Ltd. (“Beijing Zhong Ran Xiang Ke”), a PRC joint venture entity engaged in the business of development, licensing and sale of oil and gas technologies and equipment, and sale of self-produced products.

Beijing Gas owns and operates natural gas distribution systems primarily in Hebei, Jiangsu, and Shandong provinces in the PRC.

Recent Developments

On September 7, 2006, in connection with a reverse merger transaction in which the Company (i) consummated a share exchange transaction with the shareholders of GAS Investment China Co., Ltd. (“Gas (BVI)”), whereby the Company exchanged 14,361,647 shares of our Series A Convertible Preferred Stock, par value $0.001 per share (the “Series A Stock”) for all of the issued and outstanding stock of Gas (BVI) held by the shareholders of Gas (BVI) (the “Share Exchange Transaction”), and (ii) consummated the initial closing of a private placement offering, whereby the Company, issued to the investors of the initial funding 2,509,782 shares of the Series B Stock, and Series A, B, J, C and D warrants in exchange for $6,876,800 (the “Private Financing”, together with “Share Exchange Transaction”, and, collectively, the “Reverse Merger Transaction”).

22

As a result of the Share Exchange Transaction, Gas (BVI) became a wholly-owned subsidiary of the Company, and Beijing Gas became an indirectly wholly owned subsidiary of the Company.

On October 20, 2006, we entered into and closed a stock purchase transaction (the “October Financing”) pursuant to which we issued for an aggregate of $2,404,800 in gross cash proceeds, 877,664 shares of our Series B Convertible Preferred Stock, par value $0.001 per share (the “Series B Stock”), at $2.74 per share and Series A, B, J, C and D warrants. As a result of the consummation of the Private Financing and October Financing, we raised an aggregate of $9,281,600 gross cash proceeds.

Corporate Structure

23

RESULTS OF OPERATIONS

Nine month ended Sep 30, 2006 and nine months ended Sep 30, 2005

For the nine months ended September 30, 2006, we believe that the Company made notable progress as shown in the table below. We have been able to increase net sales, gross profits, operating income and net income by at least 50% compared with the same period last year.

Net Sales reached $4,971,156, an increase of 50% from $3,319,668 last year, driven by our successful expansion in both the residential markets and industrial markets. While we believe that our business is growing at a significant rate, our gross profit margin has also improved, reaching 63%, an increase over last year’s 55%, due primarily to our strengthened efforts to expand our connection business which has significantly higher margins than natural gas sales. As a result, gross profit increased 70% to $3,122,028, a significantly higher rate than the 50% increase in net sales. Net income reached $2,188,680 for the nine months ended September 30, 2006 compared to $1,244,666 for the same period last year, an increase of 76%.

| Nine months ended September 30, 2006 | ||||||||||

| 2006 | 2005 | Change | ||||||||

| US$ | US$ | % | ||||||||

| Net sales | 4,971,156 | 3,319,668 | 50 | % | ||||||

| Gross profit | 3,122,028 | 1,834,065 | 70 | % | ||||||

| Income from operations | 2,361,558 | 1,380,424 | 71 | % | ||||||

| Net income | 2,188,680 | 1,244,666 | 76 | % | ||||||

| Gross profit margin (%) | 63 | % | 55 | % | 6 | % | ||||

Net Sales

Net sales for the nine months ended September 30, 2006 was $4,971,156, an increase of $1,651,488, or 50%, compared with net sales of $3,319,668 for the nine months ended September 30, 2005. Revenue from new connections grew at a faster pace than revenue from supplying gas and accounted for a larger percentage of our total revenue. We believe this change is a positive development for the Company, as connections bring a higher profit margin than supplying gas.

24

For the first nine months this year we have signed with 27,247 residential households for connections of natural gas in the cities we had entered by the end of last year. Among them are approximately 10,000 households from a single project, Da Tun Mei Dian project in Peixian County, JiangSu province. Those connection contracts have resulted in $3,104,605 in revenues.

In January, 2006, Hebei Zhong Steel, our largest industrial customer, started to use our natural gas supply. With a designed gas supply capacity of 30,000 cubic meters per day, the actual usage of natural gas by Hebei Zhong Steel is in excess of 10,000 cubic meters per day, on average. Gas usage by Hebei Zhong Steel has enabled us to increase gas revenues despite our strategic reduction of gas suppkies to certain lower-margin customers such as Zhong Ran Xiang Ke and Zhong You Xiang Ke.

| Nine months ended September 30, 2006 | ||||||||||||||||

| 2006 | 2005 | Change | ||||||||||||||

| US$ | % | US$ | % | % | ||||||||||||

| Net sales | 4,971,156 | 100 | % | 3,319,668 | 100 | % | 50 | % | ||||||||

| Gas | 1,866,551 | 38 | % | 1,360,441 | 41 | % | 37 | % | ||||||||

| Connection Fees | 3,104,605 | 62 | % | 1,959,227 | 59 | % | 58 | % | ||||||||

Gross profit

Gross profit for the nine months ended September 30, 2006 was $3,122,028, an increase of 70% from $1,834,065 for the nine months ended September 30, 2005. 80% of our gross profits resulted from connection fees.

Our gross profit margin reached 63% for the nine months ended September 30, 2006. A significant increase over the 55% gross profit margin for the nine months ended September 30, 2005. The increase reflects the improvements in our profit margins for the supply of natural gas due to our focus on natural gas supply to higher margin customers.

With the beginning of gas supply to Hebei Zhong Steel and new residential users, we have substantially reduced gas supply to Zhong Ran Xiang Ke and Zhong You Xiang Ke, two affiliates of the company with low profit margins. The total gas supplied to these two customers have decreased to around 574,000 cubic meters for the first nine months this year, compared with 5,277,000 cubic meters the same period last year.

25

| Nine months ended September 30 | |||||||||||||||||||

| 2006 | 2005 | ||||||||||||||||||

| US$ | % | Gross margin | US$ | % | Gross margin | ||||||||||||||

| Gross profit | 3,122,028 | 100 | % | 63 | % | 1,834,065 | 100 | % | 55 | % | |||||||||

| Gas | 487,247 | 16 | % | 26 | % | 135,160 | 7 | % | 10 | % | |||||||||

| Connection | 2,634,781 | 84 | % | 85 | % | 1,698,905 | 93 | % | 87 | % | |||||||||

Income from operations

For the reasons set forth above, income from operations was $2,361,558 for the nine months ended September 30, 2006, a 71% increase from $1,380,424 for the same period last year.

Cost of sales

As shown in the table below, cost of sales for the nine months ended September 30, 2006 was $1,849,128, an increase of 24% from $1,485,603 in 2005. The cost of gas still constituted the majority of cost of sales, but the percentage fell to 75% from 82% one year ago. The connection cost increased 80% to $469,824 from $260,322 last year, but still account for only approximately 25% of total costs.

The changes of our cost structure reflect our strong growth in the connection business during the first nine months of this year, which is critical to sustainable growth in the future. As set forth above, we have signed with 27,247 new residential households to connect to our natural gas network which resulted in an 80% increase in connection costs. With respect to gas usage, we have substantially reduced gas supply to customers that lower our overall profit margin, a move offset by increased gas supply to industrial and residential users. The net result is that the cost of gas increased by approximately 13% for the nine months ended September 30, 2006 when compared to the same period last year.

| Nine months ended September 30 | ||||||||||||||||

| 2006 | 2005 | Change | ||||||||||||||

| US$ | % | US$ | % | % | ||||||||||||

| Cost of sales | 1,849,128 | 100 | % | 1,485,603 | 100 | % | 24 | % | ||||||||

| Gas | 1,379,304 | 75 | % | 1,225,281 | 82 | % | 13 | % | ||||||||

| Connection | 469,824 | 25 | % | 260,322 | 18 | % | 80 | % | ||||||||

26

Operating expenses

| Nine months ended Sep 30 | ||||||||||

| 2006 | 2005 | |||||||||

| US$ | US$ | % | ||||||||

| Selling Expenses | 66,497 | 66,668 | - | |||||||

| General & Administrative Expenses | 693,973 | 386,973 | 79 | % | ||||||

| Total Operating Expenses | 760,470 | 453,641 | 68 | % | ||||||

Total operating expenses were $760,470 for the nine months ended September 30, 2006, an increase of 68% from $453,641 for the same period last year. The increase was principally the result of an increase in general and administrative expenses relating to our equity financing and reverse merger in September, 2006, including auditing fees, placement agent fees and legal fees. In addition, the amortization of intangible assets and leasing expense increased to approximately $35,000 due to business expansion.

Selling expenses remained flat for the nine months ended September 30, 2006, compared with the same period last year.

Net Income

Net income was $2,188,680 for the nine months ended September 30, 2006, an increase of 76% from $1,244,666 for the same period in 2005.

For the first half of this year, we principally focused on completion of construction commenced in 2005, maintenance of existing gas stations and recovery of accounts receivable. As a result, we reported a decrease of net income for that period compared with one year ago.

27

The September 30 quarter is typically strong for the natural gas distribution industry as the weather is starting to become cold leading to demand for natural gas for heating and many connections are completed during this time at the end of construction projects which are finishing before the winter. In addition, most natural gas distribution networks are constructed during the second and third calendar quarters. The construction time of each period is ranging from four months to six months, depending on the size of the projects. Therefore, network construction projects are usually completed and revenue recognized during the third quarter.

| Nine months ended Sep 30 | ||||||||||

| 2006 | 2005 | Change | ||||||||

| US$ | US$ | % | ||||||||

| Net Income | 2,188,680 | 1,244,666 | 76 | % | ||||||

Liquidity and capital resources

We have typically financed our operations and expansion from our cash flow generated from operations and capital contributed by our shareholders. We consummated the Reverse Merger Transaction and raised approximately $6,876,800 in gross proceeds in the Private Financing on September 7, 2006. After the deduction of financing fees, the net proceeds from the Private Financing was $ 5,246,891.

Cash and cash equivalents

Cash and cash equivalents was $5,328,306 for the nine months ended September 30, 2006, an increase of $4,757,112 from $571,194 for the same period last year. The large increase was primarily due to the cash inflow from the Private Financing. In addition, we collected approximately $3,282,575 in accounts receivable.

Cash flows from operating activities

Cash flows from operating activities were $3,225,749 for the nine months ended September 30, 2006, an increase of $1,906,720, or 145%, from $1,319,029 for same period last year. This significant increase was principally due to our collection of $3,282,575 in accounts receivable.

28

Cash flows from investing activities

We had a net cash outflow from investing activities for the nine months ended September 30, 2006. Net cash used in investing activities was $3,780,796, an increase of $1,948,779, or 106%, from $1,832,017 for the same period last year. The increase was principally due to increased payments for our projects under development, such as Da Tun Mei Dian or old projects, such as those in Mi Yun, Jin Zhou, Si Hong and Pei Xian. Each of the projects required a large amount of investment for building the network connections.

Cash flows from financing activities

We raised approximately $6,876,800 in gross proceeds in the Private Financing. After the deduction of financing fees, the net proceeds from the initial closing of the Private Financing is $5,246,891.

Accounts Receivable

Accounts receivable were $6,887,070 as of September 2006, a decrease of $883,098, or 11%, from December 31, 2005. The decrease is primarily due to the collection of $3,282,575 in accounts receivable, partially offset by approximately $2,390,000 in accounts receivable from the Da Tun Mei Dian project in Pei Xian County, Jiangsu Province.

Construction In Progress

Construction in progress was $5,798,781 for the nine months ended September 2006, an increase of $2,727,284, or 89%, from $3,071,497 for the same period last year. Construction in progress principally comprises this year’s new project, Da Tun Mei Dian, as well the already existing projects, such as project in Beijing’s Mi Yun and Jiangsu’s Si Hong and Pei Xian.

Prepaid Expenses and other current assets

Prepaid expenses and advances to suppliers totaled $343,839 for the nine months ended September 30, 2006, a slight decrease of 11% from $384,539 for the same period last year. Other receivables increased 107% to $905,327, compared with $437,922 last year.

29

Loans

The company had no bank or other loans for the nine months ended September 30, 2006.

Three months ended September 30, 2006 and three months ended September 30, 2005.

| Three months ended Sep 30 | ||||||||||

| 2006 | 2005 | Change | ||||||||

| US$ | US$ | % | ||||||||

| Net Sales | $ | 3,471,616 | $ | 851,442 | 308 | % | ||||

| Gross Profit | $ | 2,605,975 | $ | 542,733 | 380 | % | ||||

| Income from operations | $ | 2,126,148 | $ | 359,360 | 492 | % | ||||

| Net Income | $ | 1,930,536 | $ | 338,699 | 470 | % | ||||

| Gross profit margin | 75 | % | 64 | % | 11 | % | ||||

As shown in the table above, we achieved significant growth during the aurter ended September 30, 2006.

Net sales increased more than 300% to $3,471,616 during the three-month period, as compared with $851,442 for the same period last year. Gross profit reached $2,605,975, an increase of 380% from the third quarter last year. Both income from operations and net income grew at a rate of nearly 500%, with net income reaching $1,930,536 and income from operations reaching $2,126,148. Gross profit margins also improved by 11% from last year’s 64%.

The strong performance for the quarter was principally the result of the development of the Da Tun Mei Dian project which is located in Pei Xian County, Jiangsu Province. Da Tun Mei Dian is a medium-size state-owned enterprise in the PRC. In July, we signed an agreement with this company to supply 17,000 households within its residential area with natural gas, replacing coal. By September 30, 2006, we completed construction of the network 10,000 households.

30

Net Sales

| Three months ended Sep 30 | ||||||||||||||||

| 2006 | 2005 | Change | ||||||||||||||

| US$ | % | US$ | % | % | ||||||||||||

| Net Sales | $ | 3,471,616 | 100 | % | $ | 851,442 | 100 | % | 308 | % | ||||||

| Connection | $ | 2,745,948 | 79 | % | $ | 653,076 | 77 | % | 320 | % | ||||||

| Gas | $ | 725,668 | 21 | % | $ | 198,366 | 23 | % | 266 | % | ||||||

As shown from the table above, net sales were $3,471,616 for the three months ended September 30, 2006, an increase of 308% from $851,442 for the same period last year. This significant increase was principally due to the progress made with the Da Tun Mei Dian project. For this project we have signed connection agreements with a total of 17,000 households and completed the construction of networks to 10,000 households, bringing in nearly $2,400,000 revenues.

Gross Profit

| Three months ended Sep 30 | |||||||||||||||||||

| 2006 | 2005 | ||||||||||||||||||

| US$ | % | Gross margin | US$ | % | Gross Margin | ||||||||||||||

| Gross profit | $ | 2,605,975 | 100 | % | 75 | % | $ | 542,733 | 100 | % | 64 | % | |||||||

| Connection | $ | 2,340,339 | 90 | % | 85 | % | $ | 523,026 | 96 | % | 80 | % | |||||||

| Gas | $ | 265,636 | 10 | % | 37 | % | $ | 19,707 | 4 | % | 10 | % | |||||||

As shown from the table above, gross profit grew nearly 400% to $2,605,975 from $542,733. As we discussed previously, the Da Tun Mei Dian project resulted in our revenue growth and generated nearly $2,000,000 in gross profits.

Cost of sales

Cost of sales was $865,641 for the three months ended September 30, 2006, increasing 180% from $308,709 for the same period last year. The increasing rate of cost of sales is significantly lower than that of revenues, as the revenue was mostly driven by connection fees from Da Tun Mei Dian, which has the highest profit margin among any of our current projects.

31

| Three months ended Sep 30 | ||||||||||||||||

| 2006 | 2005 | Change | ||||||||||||||

| US$ | % | US$ | % | % | ||||||||||||

| Cost of sales | $ | 865,641 | 100 | % | $ | 308,709 | 100 | % | 180 | % | ||||||

| Connection | $ | 405,609 | 47 | % | $ | 130,050 | 42 | % | 212 | % | ||||||

| Gas | $ | 460,032 | 53 | % | $ | 178,659 | 58 | % | 157 | % | ||||||

Operating expense

| Three months ended Sep 30 | ||||||||||

| 2006 | 2005 | Change | ||||||||

| US$ | US$ | % | ||||||||

| Selling expense | $ | 39,673 | $ | 24,805 | 60 | % | ||||

| Administrative & Other | $ | 440,154 | $ | 158,568 | 178 | % | ||||

| Total operating expenses | $ | 479,827 | $ | 183,373 | 162 | % | ||||

With the first closing of Private Financing in early September, financing related fees accounted for most of the increase operating expenses, such as auditing fees, placement agent fees and legal fees.

Net Income

The September 30 quarter is typically strong for the natural gas distribution industry as the weather is starting to become cold leading to demand for natural gas for heating and many connections are completed during this time at the end of construction projects which are finishing before the winter. In addition, most natural gas distribution networks are constructed during the second and third calendar quarters. The construction time of each period is ranging from four months to six months, depending on the size of the projects. Therefore, network construction projects are usually completed and revenue recognized during the third quarter.

32

In addition, we made significant progress in market development, revenue structure adjustments and project management. All the factored combined together, the company’s net income rose to $1,930,536, a 470% increase from $338,699 last year.

Critical Accounting Policies

Management's discussion and analysis of its financial condition and results of operations is based upon Beijing Gas’ consolidated financial statements, which have been prepared in accordance with United States generally accepted accounting principles. Beijing Gas’ financial statements reflect the selection and application of accounting policies which require management to make significant estimates and judgments. Management bases its estimates on historical experience and on various other assumptions that are believed to be reasonable under the circumstances. Actual results may differ from these estimates under different assumptions or conditions. Beijing Gas believes that the following reflect the more critical accounting policies that currently affect Beijing Gas’ financial condition and results of operations.

(A) Method of Accounting

Beijing Gas maintains its general ledger and journals with the accrual method accounting for financial reporting purposes. The financial statements and note are representations of management. Accounting policies adopted by Beijing Gas conform to generally accepted accounting principles in the United States of America and have been consistently applied in the presentation of financial statements, which are compiled on the accrual basis of accounting.

(B) Consolidation

The consolidated financial statements include the accounts of the Company and its subsidiaries (“the Group”). Significant intercompany transactions have been eliminated in consolidation. Investments in which the company has a 20 percent to 50 percent voting interest and where the company exercises significant influence over the investee are accounted for using the equity method.

As of September 30, 2006, the particulars of the subsidiaries are as follows:

| Name of Company | Place of Incorporation | Date of Incorporation | Attributable Equity Interest % | Registered Capital | ||||

| Pegasus Tel, Inc. | USA | 2/19/2002 | 100 | |||||

| GAS Investment China Co., Ltd. | BVI | 6/19/2003 | 100 | |||||

| Beijing Zhong Ran Wei Ye Gas Co., | ||||||||

| Ltd | PRC | 8/29/2001 | 100 | RMB 77,454,532 | ||||

| Ningjin Weiye Gas Co., Ltd | PRC | 12/3/2003 | 100 | RMB 3,000,000 | ||||

| Jinzhou Weiye Gas Co., Ltd | PRC | 7/19/2005 | 100 | RMB 3,000,000 | ||||

| Xingtang Weiye Gas Co., Ltd | PRC | 2/18/2005 | 100 | RMB 3,000,000 | ||||

| Linzhang Weiye Gas Co., Ltd | PRC | 7/6/2006 | 100 | RMB 1,000,000 | ||||

| Anping Weiye Gas Co., Ltd | PRC | 8/4/2006 | 100 | RMB 5,000,000 | ||||

| Wuqiao Gas Co., Ltd | PRC | 6/30/2005 | 100 | RMB 2,000,000 | ||||

Yutian Zhongran Weiye Gas Co., Ltd | PRC | 12/19/2003 | 100 | RMB 3,000,000 | ||||

| Langfang Development | ||||||||

| Region Weiye Dangerous | ||||||||

| Goods Transportation Co., Ltd | PRC | 3/22/2006 | 100 | RMB 1,000,000 | ||||

| Sihong Weiye Gas Co., Ltd | PRC | 12/3/2005 | 100 | RMB 10,000,000 | ||||

| Peixian Weiye Gas Co., Ltd | PRC | 8/22/2006 | 100 | RMB 5,000,000 | ||||

| Sishui Weiye Gas Co., Ltd | PRC | 12/22/2005 | 100 | RMB 3,000,000 | ||||

Longyao Zhongran Weiye Gas Co., Ltd | PRC | 10/13/2006 | 100 | RMB 3,000,000 | ||||

| Shenzhou Weiye Gas Co., Ltd | PRC | 12/23/2006 | 100 | RMB 3,000,000 |

33

(D) Use of Estimates

In preparing of the consolidated financial statements in conformity with accounting principles generally accepted in the United States of America, management makes estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the dates of the consolidated financial statements, as well as the reported amounts of revenues and expenses during the reporting year. These accounts and estimates include, but are not limited to, the valuation of accounts receivable, inventories, deferred income taxes and the estimation on useful lives of plant and machinery. Actual results could differ from those estimates.

(E) Cash and Cash Equivalents

The Company considers all cash and other highly liquid investments with initial maturities of three months or less to be cash equivalents.

(F) Accounts and Other Receivable

Accounts and other receivable are recorded at net realizable value consisting of the carrying amount less an allowance for uncollectible accounts, as needed. The Company extends unsecured credit to customers in the normal course of business and does not accrue interest on trade accounts receivable.

(G) Advances to Suppliers

Advances to suppliers represent the cash paid in advance for purchasing raw materials. The advances to suppliers are interest free and unsecured.

34

(H) Investments in Equity Securities

The consolidated statement of income includes the Group's share of the post-acquisition results of its associate for the six months ended September 30. In the consolidated balance sheet, investments in equity securities are stated at the Group's share of the net assets of the associates plus the premium paid less any discount on acquisition in so far as it has not already been amortized to the statement of income, less any identified impairment loss.

Portion of | ||||||||||

Nominal | ||||||||||

Name of | Place | Form of | Value of | |||||||

Associate | of | Business | Registered | Registered | Principal | |||||

Company | Registration | Structure | Capital | Capital | Activities | |||||

| Beijing Zhongran Xiangke Oil Gas Technology Co. Ltd | PRC | Sino-foreign equity joint venture | Registered RMB 20,000,000 | 40 | Trading of natural gas and gas pipeline construction |

Beijing Zhongran Xiangke Oil Gas Technology Co. Ltd is Beijing Gas’ 40% owned joint venture company and is principally engaged in sale of compressed natural gas to domestic households and industrial around sub-urban areas of Beijing and part of sub-urban areas in Hebei Province and Tianjin.

(J) Plant and Equipment

Plant and equipment, other than construction in progress, are stated at cost less depreciation and amortization and accumulated impairment loss.

Plant and equipment are carried at cost less accumulated depreciation. Depreciation is provided over their estimated useful lives, using the straight-line method. Estimated useful lives of the plant and equipment are as follows:

| Gas Pipelines | 25 years |

| Motor Vehicles | 10 years |

| Machinery & Equipment | 20 years |

| Buildings | 25 years |

| Leasehold Improvements | 25 years |

| Office Equipment | 8 years |

The cost and related accumulated depreciation of assets sold or otherwise retired are eliminated from the accounts and any gain or loss is included in the statement of income. The cost of maintenance and repairs is charged to income as incurred, whereas significant renewals and betterments are capitalized.

(K) Construction in Progress

Construction in progress represents the cost of constructing pipelines. The major cost of construction relates to material, labor and overhead. Construction of pipeline, through which to distribute natural gas, is one of the Group’s principal businesses. The Group builds city main pipeline network and branch pipeline network to make gas connection to resident users, industrial, and commercial users, with the objective of generating revenue on gas connection and gas usage fees collected from these customers.

35

(L) Revenue Recognition

Revenue is recognized when services are rendered to customers when a formal arrangement exists, the price is fixed or determinable, the delivery is completed, no other significant obligations of the Company exist and collectibility is reasonably assured. Payments received before all of the relevant criteria for revenue recognition are satisfied are recorded as unearned revenue.

Gas connection revenue is recognized when the outcome of a contract can be estimated reliably and the stage of completion at the balance sheet date can be measured reliably.

Sales of natural gas are recognized when goods are delivered and title has passed.

(Q) Income Taxes

Pursuant to the tax laws of PRC, general enterprises are subject to income tax at an effective rate of 33%. Beijing Gas is in the natural gas industry whose development is encouraged by the government. According to the income tax regulation, any company engaged in the natural gas industry enjoys a favorable tax rate. In addition, Beijing Gas has been approved as a hi-technology company and has been enjoying preferential income tax treatment under China’s income tax policies that provide certain preferential income tax treatment to entities qualified as hi-technology entities. Under such policies, Beijing Gas is exempt from corporate income taxes for the first two years commencing from its first profitable year and thereafter, will be entitled to a 50% tax reduction for the succeeding three years. The company’s first profitable tax year was 2003. Accordingly, the company’s income would be subject to a reduced tax rate of 9% from 2005 to 2007. From 2008, the income tax rate will be 18%. The subsidiaries of Beijing Gas are subject to the effective rate of 33%.

Item 3. Controls and Procedures.

(a) Evaluation of disclosure controls and procedures. Our Chief Executive Officer and our Chief Financial Officer, after evaluating the effectiveness of the Company's "disclosure controls and procedures" (as defined in the Securities Exchange Act of 1934, as amended (the "Exchange Act"), Rules 13a-15e and 15d-15e) as of the end of the period covered by this report (the "Evaluation Date"), have concluded that, as of the Evaluation Date, our disclosure controls and procedures were effective.

(b) Changes in internal controls. During the fiscal quarter covered by this quarterly report, there was no change in our internal control over financial reporting that has materially affected, or is reasonably likely to materially affect our internal control over financial reporting.

36

PART II

Item 6. Exhibits

(a) Exhibits

21.1 - List of Subsidiaries

31.1 - Certification of Chief Executive Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002.

31.2 - Certification of Chief Financial Officer pursuant to Section 302 of the Sarbanes-Oxley Act of 2002.

32.1 - Certification of Chief Executive Officer and Chief Financial Officer pursuant to Section 906 of the Sarbanes-Oxley Act of 2002.

37

SIGNATURES

Pursuant to the requirements of the Securities Act of 1934, the Registrant has duly caused this report to be signed on its behalf by the undersigned there unto duly authorized.

| DOLCE VENTURES, INC. | ||

| | | |

| Date: Novemebr 14, 2006 | BY: | /s/ Chen Fang |

Chen Fang Chief Financial Officer | ||

38