Date: January 22, 2008

To: Mr. H. Christopher Owings

Assistant Director

United States Securities and Exchange Commission

100 F Street, North East

Washington, D.C. 20549

| Re: | Sino Gas International Holdings, Inc. |

File No. 333-147998

Form SB-2 filed on December 11, 2007

Dear Mr. Owings:

On behalf of Sino Gas International Holdings, Inc. (“Company”), we hereby submit this response to the comments of the staff (the “Staff”) of the Securities and Exchange Commission (the “Commission”) set forth in the Staff's letter, dated January 9, 2008, with respect to our registration statement on Form SB-2 (the “Form SB-2”). In addition to the clean and marked versions filed with the Commission through EDGAR, we will provide a hard copy of the marked version of our amended Form SB-2 through courier.

We understand and agree that:

| l | Sino Gas is responsible for the adequacy and accuracy of the disclosure in the filings |

| l | Staff comments or changes to disclosure in response to Staff comments in the filings reviewed by the Staff do not foreclose the Commission from taking any action with respect to the filing; and |

| l | Sino Gas may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States |

General

1. | We are in receipt of the responses you provided on December 11, 2007 relating to comments previously issued on your Form 10-K for the period ended December 31, 2006. Please ensure that these comments are resolved prior to seeking effectiveness. |

Response:

We are waiting for your further comments regarding our responses to your comments on our Form 10K. Please let us know if you have any additional comments so that we can resolve them as soon as possible.

2. | We note that 1,500,000 shares you seek to register have not yet been issued and are contingent upon certain events. Please revise to omit the 1,500,000 shares from your resale registration statement since these shares have not yet been issued and may not be issued to the selling stockholders unless you trigger a contingency or tell us why you believe it is appropriate for you to register these shares at this time. Refer to Telephone Interpretation B.77 under Compliance and Disclosure Interpretations at our web-site at <www.sec.gov>. |

Response:

Per your comment, we omitted the 1,500,000 “Make Good” shares not yet issued and made other appropriate revisions where applicable. Please see the changes to the prospectus cover page of our amended Form SB-2.

Prospectus Cover Page

3. | We note that your registration statement covers the resale of 271,074 shares of your common stock that underlie warrants. Please revise your cover page and your Prospectus Summary to separately state this amount so that it is clear what portion of the total amount you are registering is subject to the exercise of warrants. In an appropriate place in this prospectus, please also describe the terms of these warrants. |

Response:

Per your comment, we revised the cover page and Prospectus Summary to separately state the 271,074 shares of placement agent warrants. We also described the terms of placement agent warrants under the heading “warrants” at the bottom of page 15 of our amended Form SB-2.

Risk Factors, Page 4

4. | On page 4, you use the subheading “The price of natural gas is subject to government regulations and market conditions.” This subheading is not descriptive and appears to merely state a fact about your company. In addition, the accompanying discussion also does not provide enough information for investors to assess the risk. Please revise your subheading and accompanying text to ensure that they reflect the material risk to which investors should be made aware. |

Response:

Per your comment, we revised this risk factor and please see page 4 of our amended Form SB-2.

5. | Tell us why you believe that potential environmental liability is a material risk of which investors should be made aware when your disclosure on page 7 would seem to indicate that your business is not subject to any environmental regulations or liability. Alternatively, please delete this risk factor. |

Response:

Per your comment, we deleted this risk factor. Please see pages 7 of our amended Form SB-2 between risk factors 10 and 11 where this risk factor was.

6. | On page 8, where you refer to the warranty claims that have been made to date, please quantify this amount, so that investors can appreciate what you mean when you refer to a “very limited number” of claims. |

Response:

Per your comment, we made additional disclosure. Please see page 8 of our amended Form SB-2.

7. | On page 9, where you refer to the restrictions on paying dividends, please provide additional disclosure that explains what “accumulated profits” means, for purposes of PRC accounting standards, and compare it to U.S. GAAP, under which it would appear that you prepare your financial statements. Disclose whether historically you have been restricted in the amount you have been able to receive from your subsidiary and quantify the amounts that have been remitted to date. Also, the portion that you are required to set aside is in brackets; please remove these brackets or explain why it is necessary for you to keep them. |

Response:

The equivalent of “accumulated profits” in US GAAP is “ Retained Earnings”. The Chinese government requires a company to put aside at least 10% of retained earnings for the year into a reserve fund which is subject to a cap at 50% of the registered capital of that company. The purpose of this reserve fund is to make provision for operational losses in the following years for that company. The total reserve fund we have set aside is US$1.7 million as of Sept. 30th, 2007. So far we have not distributed or remitted any dividends from the subsidiaries in China. We do not anticipate doing so in the near future. Per your comment, we revised the risk factor. Please see the bottom of page 9 of our amended Form SB-2.

Management’s Discussion and Analysis or Plan of Operation, Page 16

8. | As currently disclosed, your disclosure under this section appears relatively brief. Accordingly, please expand your disclosure, as applicable, to fully address Items 303(b)(1) and (2) of Regulation S-B. In this regard, your discussion should address your past and future financial condition and results of operation, with particular emphasis on the prospects for the future. Your discussion should also address those key variable and other qualitative and quantitative factors which are necessary for an understanding and evaluation of your operations. For example, we note your statement that your net revenues increased 63% for the three months ended September 30, 2007 compared to the same period in 2006. Discuss whether you expect that trend to continue. Please provide additional analysis concerning the variability of your earnings and cash flows so that investors can ascertain the likelihood or the extent past performance is indicative of future performance. In another example, we note connection fees accounted for approximately 70% of your total revenues for three months ended September 30, 2007. Please discuss whether you expect levels to remain at this level or to increase or decrease. Please see Release No. 33-8350 for additional guidance. |

Response:

Per your comment, we have expanded our disclosure regarding future forecasts and analysis of past trends and events in our Management’s Analysis and Discussion section. Please see revisions on pages 19, 20, 21, 22, 23, 24, 26 and 27 of our amended Form SB-2.

9. | Here or in your Business discussion please explain how you determine the rates at which you charge your connection fees. In this regard, we note that the connection fee per new residential household appears to vary; $333 per connection in Peixian, Jiangsu Providence as compared $180 per connection in Baishan City, Jilin Providence. We note your disclosure on page 24 regarding this aspect of your business, however, you do not go into any detail regarding how you determine the rates you charge. |

Response:

Per your comment, we made additional disclosure in our amended Form SB-2. Please see our changes at pages 19 and 47 (in the Business section) of our amended Form SB-2 for the determination of rates and disclosure regarding Peixian and Baishan.

Gas Sales, page 23

10. | It appears that 35% of your total gas sales are sold through other gas distributors. In an appropriate place in your disclosure please explain this aspect of your business. |

Response:

Per your comment, we made additional disclosure on page 23 of our amended Form SB-2 regarding other gas distributors.

Liquidity and Capital Resources, page 26

11. | Please include a discussion of how long you can satisfy your cash requirements and whether you will have to raise additional funds in the next twelve months. In this regard, we note your risk factor disclosure on page 5; please provide similar disclosure here and explain how you intend to fund these capital expenditures. |

Response:

Per your comment, we made additional disclosure on page 26 of our amended Form SB-2.

Fiscal Years ended December 31, 2006 and 2005, page 27

12. | We refer you to the disclosure near the bottom of page 27 indicating that you are considering several potential acquisition targets, which would substantially contribute to our sales and net income if successfully acquired. Please expand your disclosure to more fully discuss your acquisition strategy, including the factors that you will consider in deciding whether or not to acquire complementary businesses. Please also revise to indicate any acquisitions that are currently under consideration and describe them or, if none are currently under consideration, please state this. |

Response:

Per your comment, we made additional disclosure. Please see bottom of page 27 of our amended Form SB-2.

13. | Please also update the disclosure at the top of page 28 to reflect your plans for the upcoming fiscal year. |

Response:

Per your comment, we changed the year 2006 to 2008 at the top of page 28 of our amended Form SB-2.

Business of the Company, page 36

Organizational History, page 40

14. | Please clarify your activities between May 2002 and September 7, 2006. If you were an inactive shell, please disclose this fact. |

Response:

Per your comment, we made additional disclosure. Please see page 40 of our amended form SB-2.

15. | We note your disclosure that Pegasus Tel, Inc. was spun of in the form of a dividend. We further note that you have filed an amended Schedule 14C on November 28, 2007 with respect to this spin-off and the Form 10 relating to the spin-off has not yet been cleared of comments. As a result, please tell us why you believe that the spin-off took place on August 30, 2007. |

Response:

Our former counsel handled the spin-off. It turned out the spin off has not been completed yet. Per your comment, we deleted the sentence “ We spun off Pegasus Tel in the form of a dividend to our shareholders of record as of August 30, 2007.” on page 41 of our amended Form SB-2.

16. | Please expand your disclosure to include a description of each material acquisition, including the material terms of each acquisition including the business or assets acquired, the consideration paid (please include the dollar value) and whether any of the transactions were with related parties. |

Response:

Per your comment, we made additional disclosure regarding acquisitions. Please see the bottom of page 41 of our amended Form SB-2.

Organizational History of GAS (BVI) and Beijing Gas, page 41

17. | Here or in your Business discussion, please provide greater detail concerning the cities and the provinces in which you operate. |

Response:

Per your comment, please see our additional disclosure on page 41 of our amended Form SB-2.

18. | Please describe the “self-produced products” sold by Beijing Zhong Ran Xiang Ke. Also, explain whether you derive any material amount of revenues from this joint venture. |

Response:

Per your comment, we made additional disclosure on page 41 of our amended Form SB-2 regarding Beijing Zhong Ran Xiang Ke.

Our Industry, page 42

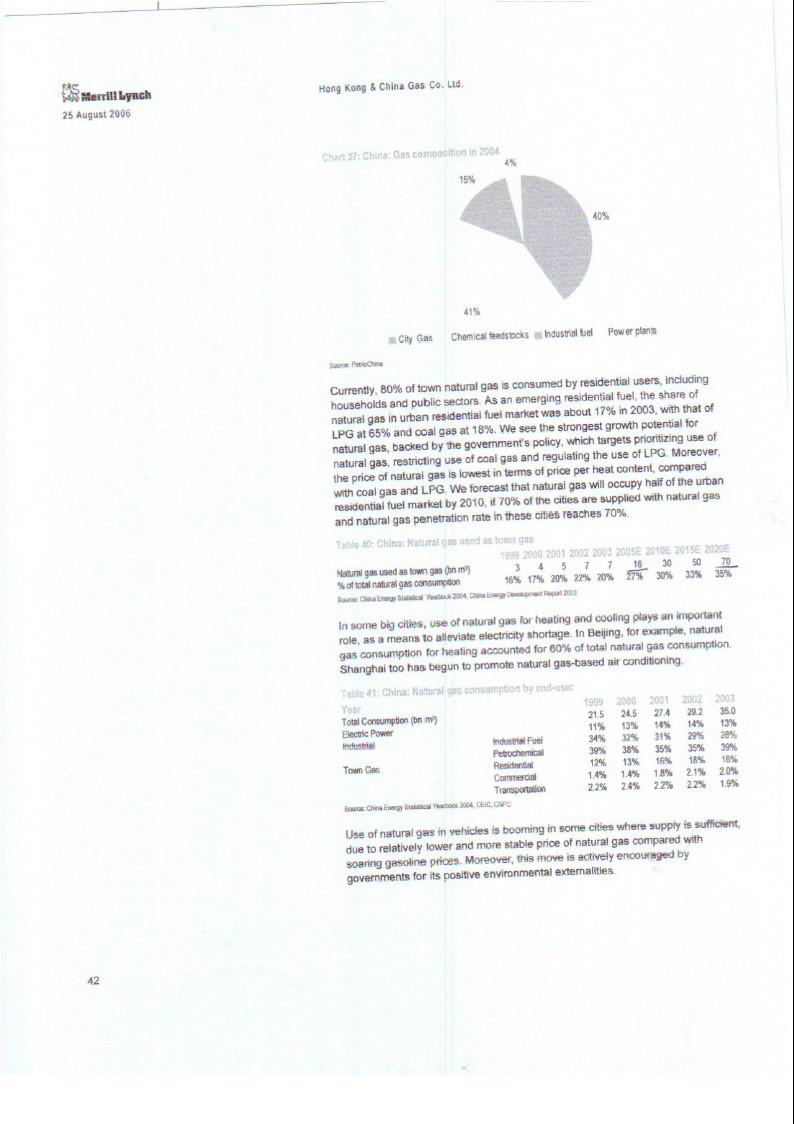

19. | We note your references to studies published by China Statistical Yearbook, Energy Information Administration, China National Development and Reform Commission, The Institute of Energy Economics of Japan and Merrill Lynch. Please provide copies of these studies to us, appropriately marked and dated. Also, if you commissioned any of the studies, please identify in your disclosure that you commissioned the study. You must also file as an exhibit, the author’s consent to be named in the registration statement. |

Response:

We did not commission any of the studies. Per your comment, we attached the following copies of statistics as exhibits:

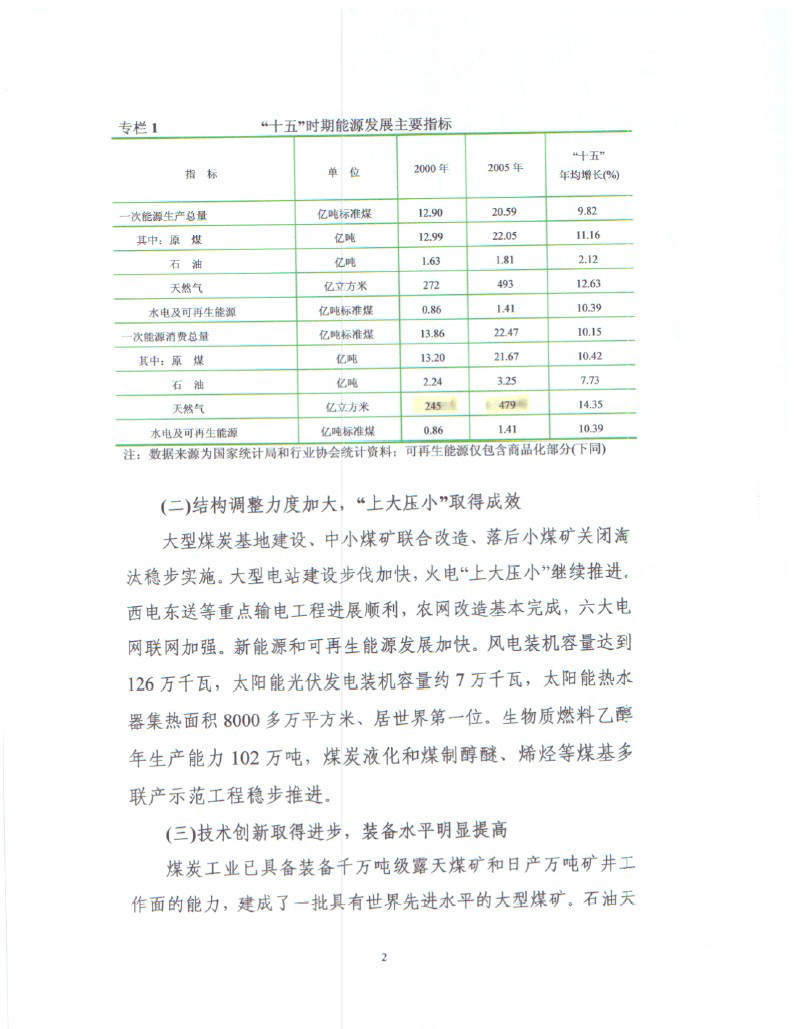

Exhibit 1: Total Consumption of Energy and Its Composition; http://www.stats.gov.cn/tjsj/ndsj/2006/html/G0702e.htm

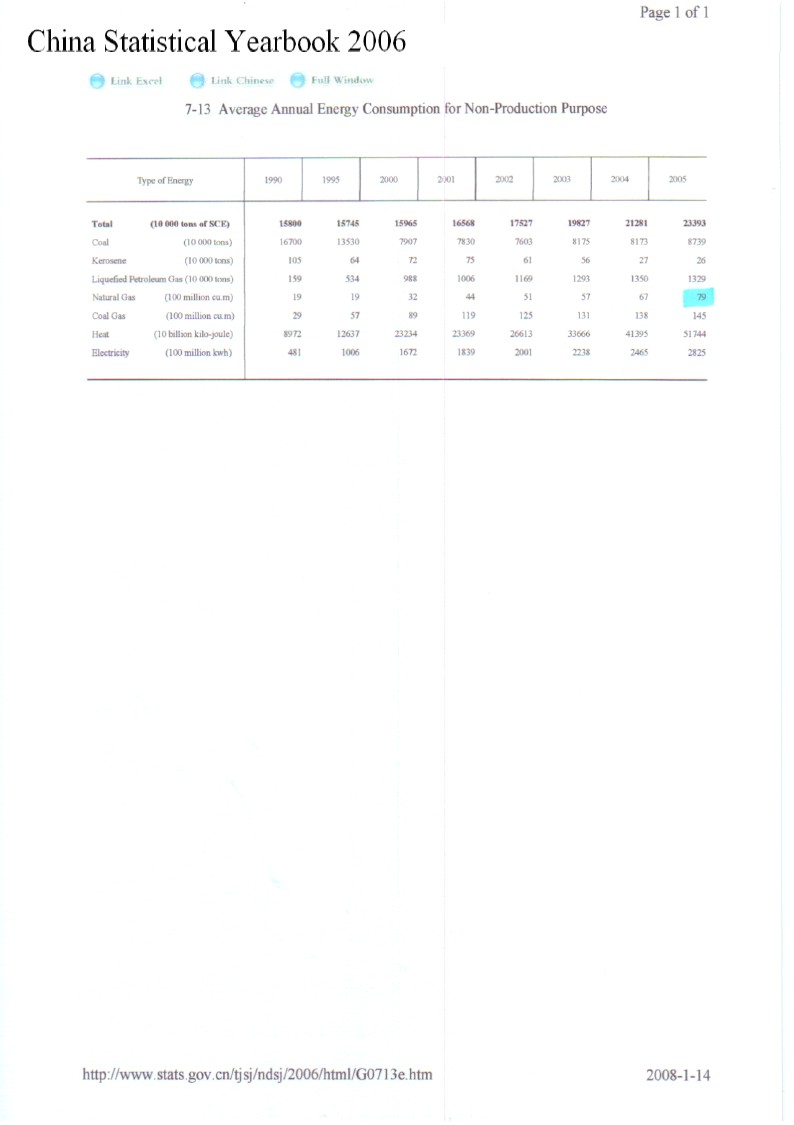

Exhibit 2: Average Annual Energy Consumption for Non-Production Purpose;

http://www.stats.gov.cn/tjsj/ndsj/2006/html/G0713e.htm

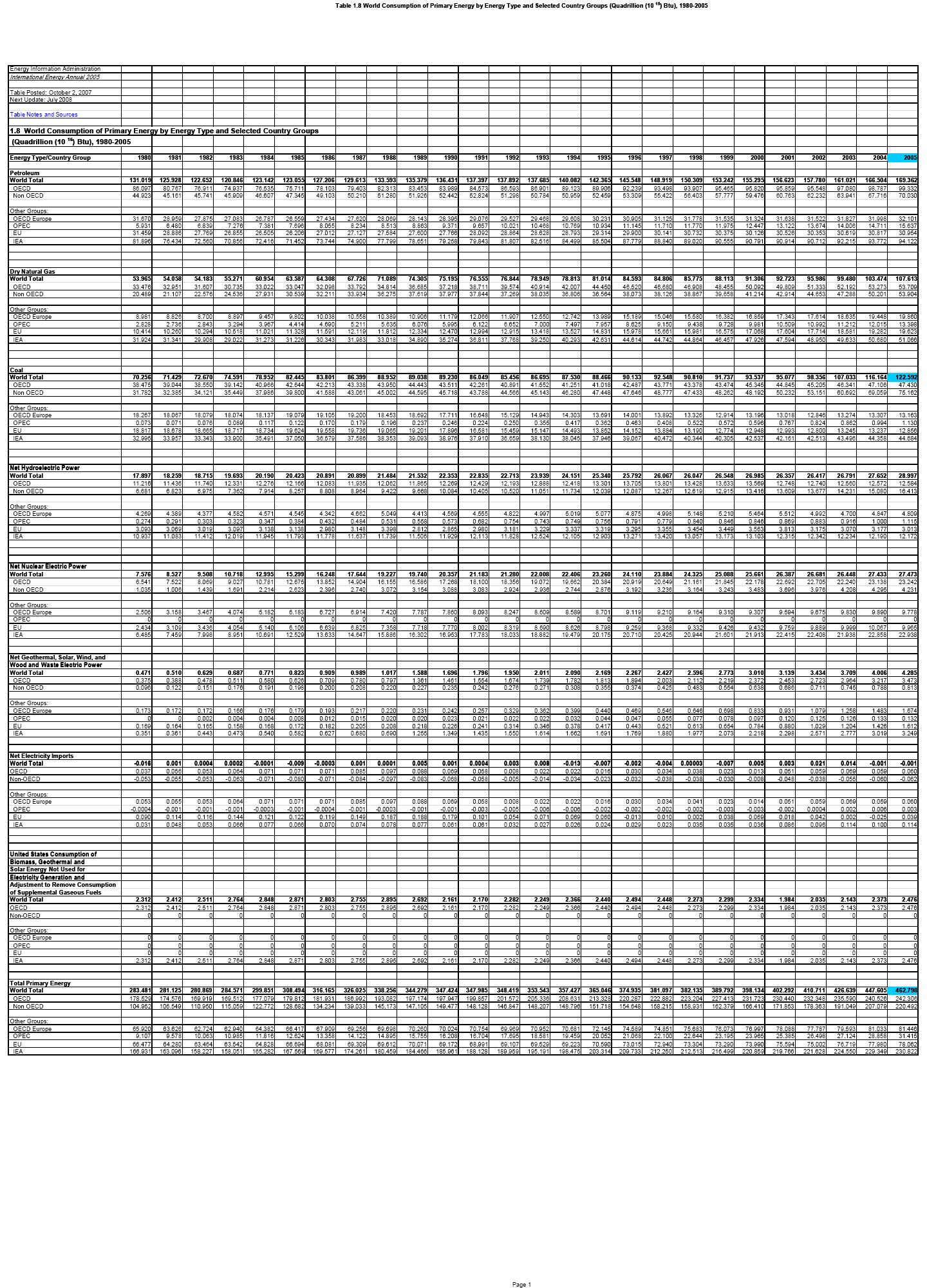

Exhibit 3A: World Consumption of Primary Energy by Energy Type and Selected Country Groups;

http://www.eia.doe.gov/iea/wecbtu.html

Exhibit 3B: Table 18 from Energy Information Administration Website;

http://www.eia.doe.gov/iea/wecbtu.html

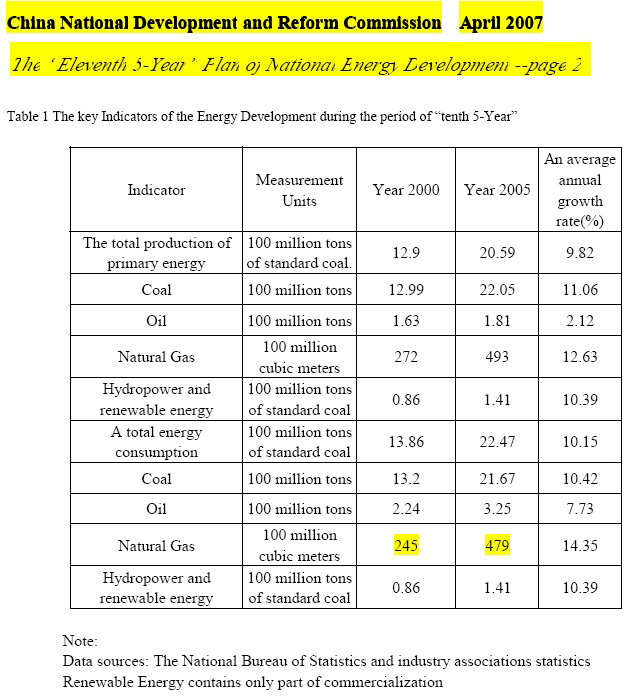

Exhibit 4: The Eleventh 5-Year Plan of National Energy Development (translated from attached original Chinese version);

http://www.sdpc.gov.cn/nyjt/nyzywx/P020070410417020191418.pdf

Exhibit 5: Merrill Lynch report; (no hyperlink to website)

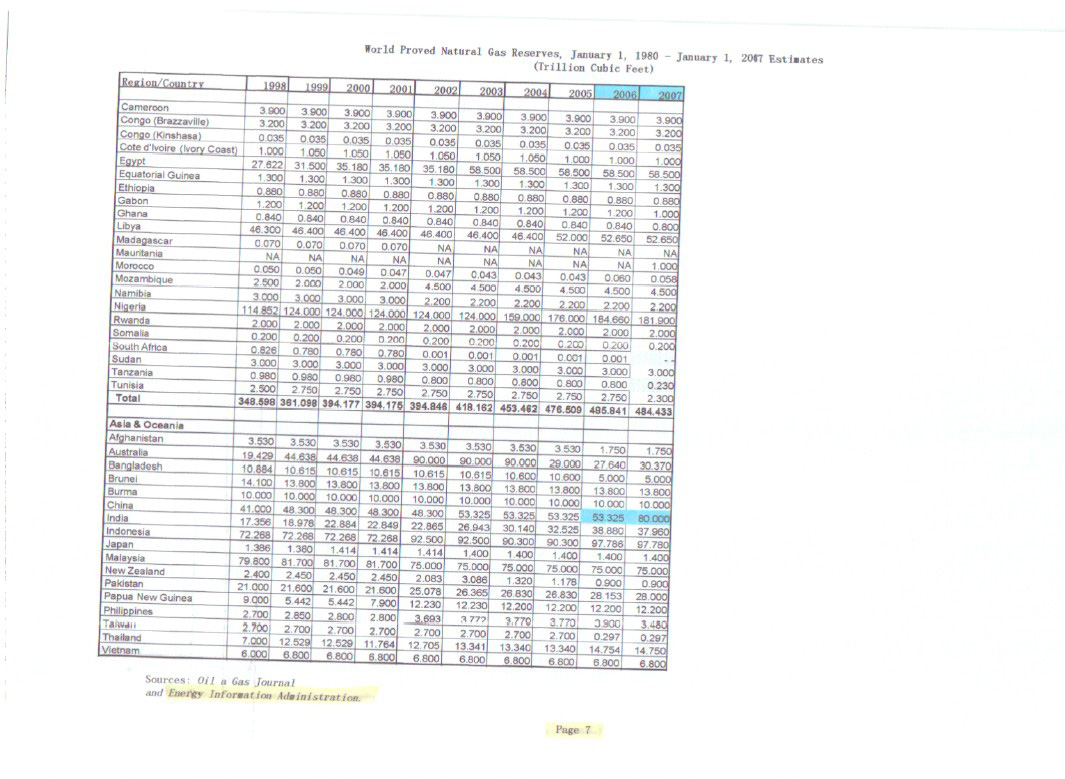

Exhibit 6A: Energy Information Administration Webpage and Exhibit 6B: Natural Gas Reserves by Energy Information Administration;

http://www.eia.doe.gov/emeu/international/gasreserves.html

Exhibit 7: China’s Natural Gas Industry and Gas to Power Generation by Institute of Energy Economics of Japan. http://eneken.ieej.or.jp/en/data/pdf/397.pdf

Directors and Executive Officers, page 60

20. | Please disclose the name of your promoters. In additional, in an appropriate section, please disclose the names of the promoters and controls persons of the company prior to the reverse merger as well as any information required by Item 404 of Regulation S-B. See Item 404(c) of Regulation S-B. |

Response:

Per your comment, please see our additional disclosure on page 62 of our amended Form SB-2.

Executive Compensation, page 62

21. | Please ensure that you have updated your disclosure, here and elsewhere in your disclosure document as applicable, to reflect information for your recently completed fiscal year ending December 31, 2007. Specifically, please update this section to provide compensation information for the recently completed fiscal year. In this regard, refer to “Interpretive Responses Regarding Particular Situations” Item 4.01 under Item 402 of Regulation S-K of our Compliance and Disclosure Interpretations. |

Response:

Per your comment, please see our revised executive compensation on page 62 of our amended Form SB-2, updated for 2007.

Selling Stockholders, page 68

22. | Under an appropriate subheading, please briefly describe the transactions pursuant to which the selling shareholders acquired their share. |

Response:

Per your comment, please see our additional disclosure on page 71 of our amended Form SB-2.

Certain Relationships and Related Transactions, page 74

Kuhns Bothers Consulting Agreement, page 74

23. | Please revise to provide more details concerning your consulting agreement with Kuhns Brothers. |

Response:

Per your comment, please see our additional disclosure on page 75 of our amended Form SB-2.

If you have any further questions or comments, please do not hesitate to contact me or our attorney, Jiannan Zhang, Ph.D., Cadwalader, Wickersham & Taft LLP 2301 China Central Place, Tower 2 No. 79 Jianguo Road, Beijing 100025, China. +86 (10) 6599-7270 (Direct Phone)

+86 (10) 6599-7300 (Main Fax), Jiannan.zhang@cwt.com.

Very truly yours, /s/ Yuchuan Liu Yuchuan Liu Chairman & CEO |

Enclosure:

Amended Form SB-2 and exhibits

Exhibit 1

Exhibit 2

Exhibit 3

Exhibit 4

Exhibit 5

Exhibit 6

Exhibit 7