Filed Pursuant to Rule 424(b)(3)

Registration No. 333-147998

PROSPECTUS

5,705,138 Shares

SINO GAS INTERNATIONAL HOLDINGS, INC.

Common Stock

This prospectus relates to shares of common stock of Sino Gas International Holdings, Inc. that may be offered for sale for the account of the Selling Stockholders identified in this prospectus (the “Selling Stockholders”). The Selling Stockholders may offer and sell from time to time up to 5,705,138 shares of our common stock.

The Selling Stockholders may sell all or any portion of their shares of common stock in one or more transactions on the over the counter stock market or in private, negotiated transactions. Each Selling Stockholder will determine the prices at which it sells its shares. Although we will incur expenses in connection with the registration of the common stock, we will not receive any of the proceeds from the sale of the shares of common stock by the Selling Stockholders.

Our common stock is quoted on the Over the Counter Bulletin Board (“OTCBB”) under the symbol “SGAS.OB.” On February 22, 2011, the closing price of our common stock quoted on the OTCBB was $0.43 per share.

We may amend or supplement this prospectus from time to time by filing amendments or supplements as required. You should read this entire prospectus and any amendments or supplements carefully before you make your investment decision.

The shares of common stock offered under this prospectus involve a high degree of risk. See “Risk Factors” beginning at page 4.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is March 11, 2011

TABLE OF CONTENTS

| Page | |||

| Prospectus Summary | 3 | ||

| Cautionary Statement Concerning Forward-Looking Information | 3 | ||

| Risk Factors | 4 | ||

| Use of Proceeds | 12 | ||

| Management’s Discussion and Analysis or Plan of Operation | 13 | ||

| Business of the Company | 23 | ||

| Management | 40 | ||

| Executive Compensation | 42 | ||

| Principal Stockholders | 45 | ||

| Selling Stockholders | 46 | ||

| Plan of Distribution | 49 | ||

| Description of Securities | 52 | ||

| Legal Matters | 54 | ||

| Experts | 54 | ||

| Available Information | 55 | ||

| Index to Consolidated Financial Statements | F-1 | ||

We have not authorized any person to give you any supplemental information or to make any representations for us. You should not rely upon any information about our company that is not contained in this prospectus or in one of our public reports filed with the Securities and Exchange Commission (“SEC”) and incorporated into this prospectus. Information contained in this prospectus or in our public reports may become stale. You should not assume that the information contained in this prospectus, any prospectus supplement or the documents incorporated by reference are accurate as of any date other than their respective dates, regardless of the time of delivery of this prospectus or of any sale of the shares. Our business, financial condition, results of operations and prospects may have changed since those dates. The Selling Stockholders are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted.

Unless otherwise indicated, or unless the context otherwise requires, all references in this prospectus to the terms “Company,” “Sino Gas,” “Registrant,” “we,” “our,” or “us” shall mean Sino Gas International Holdings, Inc., a Utah corporation.

2

Prospectus Summary

You should read this summary in conjunction with the more detailed information and financial statements appearing elsewhere in this prospectus.

Our Company

We are engaged in the development of natural gas distribution systems and the distribution of natural gas to residential, commercial and industrial customers in small- and medium-sized cities in the People’s Republic of China (the “PRC” or “China”), through our indirectly-owned subsidiaries in the PRC, Beijing Zhong Ran Wei Ye Gas Co., Ltd. (“Beijing Gas”) and its subsidiaries.

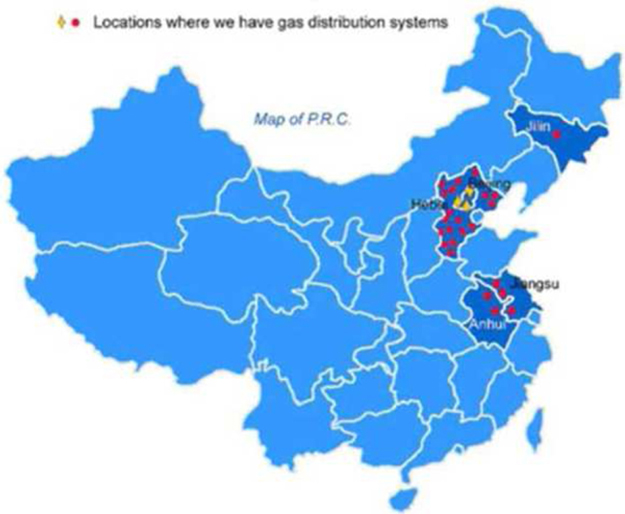

Through its subsidiaries, Beijing Gas is a natural gas services operator, principally engaging in the investment, operation and management of city gas pipeline infrastructure, and in the distribution of natural gas to residential an industrial users. Beijing Gas and its subsidiaries own and operate natural gas distribution systems in 35 small and medium size cities serving approximately 167,750 residential and 7 industrial customers. Our facilities include approximately 1,040 kilometers (“km”) of pipeline and delivery networks with a daily distribution of approximately 110,000 cubic meters of natural gas. We own and operate natural gas distribution systems primarily in small and medium sized cities in Hebei, Jiangsu, Jilin, Anhui provinces in addition to natural gas distribution systems in the suburbs of Beijing. Beijing is not a province but a municipality directly under the jurisdiction of China’s State Council and has many urban districts in the suburbs.

Our offices are located at No.18 Zhong Guan Cun Dong St., Haidian District, Beijing, P. R. China 100083. Our telephone number at this address is 86-10-8260-0527.

The Offering

This offering relates to the offer and sale of our common stock by the Selling Stockholders identified in this prospectus. The Selling Stockholders will determine when they will sell their shares, and in all cases will sell their shares at the current market price or at negotiated prices at the time of the sale. Although we have agreed to pay the expenses related to the registration of the shares being offered, we will not receive any proceeds from the sale of the shares by the Selling Stockholders.

Summary Consolidated Financial Information

The following summary financial data are derived from our consolidated financial statements. This information is only a summary and does not provide all of the information contained in our financial statements and related notes. You should read the “Management’s Discussion and Analysis or Plan of Operation” beginning on page 13 of this prospectus and our financial statements and related notes included elsewhere in this prospectus.

Statement of Operations Data:

| Year ended | ||||||||||||||||||||

| December 31, | December 31, | December 31, | December 31, | |||||||||||||||||

| 2005 | 2006 | 2007 | 2008 | 2009 | ||||||||||||||||

| Net revenue | $ | 10,907,289 | 10,870,718 | 20,267,756 | 21,448,488 | 27,591,501 | ||||||||||||||

| Net Income (Loss) | 5,702,433 | 5,165,757 | 7,707,370 | 1,600,493 | 4,047,584 | |||||||||||||||

Balance Sheet Data:

| December 31, | December 31, | December 31, | December 31, | |||||||||||||

| 2006 | 2007 | 2008 | 2009 | |||||||||||||

| Total assets | 33,882,796 | 65,356,250 | 73,696,538 | 93,077,664 | ||||||||||||

| Total liabilities | 8,476,015 | 14,509,644 | 15,841,188 | 29,809,802 | ||||||||||||

| Shareholders’ equity | 25,406,781 | 50,846,606 | 57,855,350 | 63,267,862 | ||||||||||||

Our historical results do not necessarily indicate results expected for any future periods.

Cautionary Statement Concerning Forward-Looking Information

This prospectus and the documents to which we refer you and incorporate into this prospectus by reference contain forward-looking statements. In addition, from time to time, we or our representatives may make forward-looking statements orally or in writing. We base these forward-looking statements on our expectations and projections about future events, which we derive from the information currently available to us. Such forward-looking statements relate to future events or our future performance. You can identify forward-looking statements by those that are not historical in nature, particularly those that use terminology such as “may,” “will,” “should,” “expects,” “anticipates,” “contemplates,” “estimates,” “believes,” “plans,” “projected,” “predicts,” “potential” or “continue” or the negative of these or similar terms. In evaluating these forward-looking statements, you should consider various factors, including those described in this prospectus under the heading “Risk Factors” beginning on page 4. These and other factors may cause our actual results to differ materially from any forward-looking statement. Forward-looking statements are only predictions. The forward-looking events discussed in this prospectus, the documents to which we refer you and other statements made from time to time by us or our representatives, may not occur, and actual events and results may differ materially and are subject to risks, uncertainties and assumptions about us.

3

Risk Factors

An investment in our common stock is speculative and involves a high degree of risk. You should carefully consider the risks described below and the other information in this prospectus before purchasing any shares of our common stock. The risks and uncertainties described below are not the only ones facing us. Additional risks and uncertainties may also adversely impair our business operations. If any of the events described in the risk factors below actually occur, our business, financial condition or results of operations could suffer significantly. In such case, the value of your investment could decline and you may lose all or part of the money you paid to buy the shares of common stock.

Risks Related to Our Business

Disruptions in the capital and credit markets related to the current national and worldwide financial crisis, which may continue indefinitely or intensify, could adversely affect our results of operations, cash flows and financial condition, or those of our customers and suppliers.

The current disruptions in the capital and credit markets may continue indefinitely or intensify, and adversely impact our results of operations, cash flows and financial condition, or those of our customers and suppliers. Disruptions in the capital and credit markets as a result of uncertainty, changing or increased regulation, reduced alternatives or failures of significant financial institutions could adversely affect our access to liquidity needed to conduct or expand our businesses or conduct acquisitions or make other discretionary investments, as well as our ability to effectively hedge our currency or interest rate. Such disruptions may also adversely impact the capital needs of our customers and suppliers, which, in turn, could adversely affect our results of operations, cash flows and financial condition.

We are dependent on supplies of natural gas to deliver to our customers.

The basic business model of our business is to purchase natural gas from our suppliers, and sell such natural gas to our industrial and residential customers for a profit.

As we do not own natural gas reserves, we depend on natural gas supply from a small number of suppliers. While we typically enter into multiple-year gas supply contracts with our suppliers, the supply contracts are subject to review every twelve months. If key terms of these supply contracts are changed after the annual review, or if our suppliers breach any of the key terms of the supply contracts, we will not be able to deliver the natural gas to our customers. While we have not experienced any shortage of supply in the past, we cannot assure you that natural gas will continue to be available to us. In the event that our current suppliers are unable to provide us with the natural gas we require, we may be unable to find alternative sources, or find alternative sources at reasonable prices. In such an event, our business and financial results would be materially and adversely affected.

If it were determined that our spin-off of Pegasus Tel, Inc. in August 2008 violated federal or state securities laws, we could incur monetary damages, fines or other damages which could have a material, adverse effect on our cash flow, financial condition and prospects.

We may have inadvertently violated the federal and state securities laws in connection with our spin-off of Pegasus Tel., Inc. (“Pegasus”) to our stockholders in August 2008. As we previously reported, on August 18, 2008, we consummated a spin-off of Pegasus, a Delaware corporation and a wholly-owned subsidiary of Sino Gas, to Sino Gas’ stockholders of record as of August 15, 2008 (“Spin-off”). In connection with the Spin-off, on May 7, 2007, Sino Gas caused Pegasus to file a Registration Statement on Form 10-SB (File No.: 0-52628) with the SEC to register the Pegasus common stock under Section 12(g) of the Securities Exchange Act of 1934 and, on November 28, 2007, Sino Gas filed with the SEC an Information Statement on Schedule 14C to inform shareholders of record that it was effecting the Spin-off. The ratio of distribution of the Spin-off was one (1) share of common stock of Pegasus for every twelve (12) shares of common stock of Sino Gas (1:12). Fractional shares were rounded up to the nearest whole-number. An aggregate of 2,215,136 shares of Pegasus common stock were issued pursuant to the Spin-off to an aggregate of 167 Sino Gas stockholders.

In the course of its review of our Registration Statement on Form S-1, the staff of the SEC provided comments requesting further information about the Spin-off and indicated its concern that the Pegasus Shares may have been issued without proper registration or an available exemption from registration. Under Staff Legal Bulletin No. 4 (“SLB 4”) promulgated by the Division of Corporation Finance (the “Division”) of the Securities and Exchange Commission (the “SEC”), the Division expressed its view that the shares of a subsidiary spun off from a reporting company are not required to be registered under the Securities Act of 1933, as amended (the “Securities Act”) when the following five (5) conditions are met: (i) the parent shareholders do not provide consideration for the spun-off shares; (ii) the spin-off is pro-rata to the parent shareholders; (iii) the parent provides adequate information about the spin-off and the subsidiary to its shareholders and to the trading markets; (iv) the parent has a valid business purpose for the spin-off; and (iv) if the parent spins-off “restricted securities,” it has held those securities for at least two (2) years.

If it were determined that the Spin-off did not satisfy the conditions for an exemption from registration, it would mean that the issuance of the Pegasus Shares violated Section 5 of the Securities Act and potentially the state securities laws of the U.S. states in which the holders of record for the Spin-off resided. The consequences of such a finding could be the imposition by the SEC and relevant state regulators of monetary fines or other sanctions as provided under relevant federal and state securities laws. Such regulators could also require us to make a rescission offer, which is an offer to repurchase the securities, to the holders of Pegasus Shares.

4

A finding that the issuance of the Pegasus Shares was in violation of federal or state securities law could also give certain current and former holders of the Pegasus Shares a private right of action to seek a rescission remedy under Section 12(a)(2) of the Securities Act. In general , this remedy allows a successful claimant to sell its shares back to the parent company in return for their original investment.

We are unable to quantify the extent of any monetary damages that we might incur if, monetary fines were imposed, rescission were required or one or more other claims were successful. However, we can give no assurance that the damages resulting from any such action or claims will not have a material, adverse effect on our cash flow, financial condition and prospects. As of the date of this prospectus, we are not aware of any pending or threatened claims that the Spin-Off violated any federal or state securities laws.

Based upon facts known to us at this time, we do not believe that assertion of such claims by any of our current or former holders of the Pegasus Shares is probable. However, there can be no assurance that any such claim will not be asserted in the future or that the claimant in any such action will not prevail. The possibility that such claims may be asserted in the future will continue until the expiration of the applicable federal and state statutes of limitations, which generally vary from one (1) to three (3) years from the date of sale. Claims under the anti-fraud provisions of the federal securities laws, if relevant, would generally have to be brought within two (2) years of discovery, but not more than five (5) years after occurrence.

The price of natural gas is subject to uncertain government regulations and market conditions.

The price of natural gas is subject to uncertain government regulations and market conditions in the PRC which are subject to change or fluctuations. While our costs for natural gas are subject to control by the PRC government and we have not experienced any significant price fluctuations over the past few years, we can not assure you that the price of natural gas will not vary significantly in the future. Numerous factors, most of which are beyond our control, drive the price and supply of natural gas. Some of these factors are: general international and domestic political and economic conditions, wars, OPEC actions, industry capacity utilization and government regulations. The war in Iraq and uncertain international political conditions could drive the price of natural gas upwards, thus reducing our profit margins in selling the natural gas to our customers. Any production restrictions imposed by OPEC on crude oil and natural gas could also reduce the inventory of the natural gas and drive the price upwards, reducing our profits. The price at which we sell to customers will be subject to approval by the Chinese government and is thus heavily regulated. Although in the past three (3) years there were no significant changes in regulations, we cannot assure you this will be the case in the future. Any change in PRC governmental regulations such as labor law regarding the minimum wage could materially and adversely affect our profits.

Our success depends on our ability to identify and develop operational locations and negotiate and enter into favorable franchise agreements with local governments at the operation locations.

Our success depends on our ability to identify new operational locations in small-and -medium-sized cities in China and negotiate and enter into favorable franchise agreements with local governments that grant us long-term exclusive right to develop the natural gas distribution network and supply natural gas in the operational location. Our failure to identify and develop new operational locations and obtain the exclusive rights to be the developer of natural gas distribution networks and distribute natural gas in such operational locations would curb our revenue growth and may adversely impact our financial condition and operating results.

Our success depends on our ability to obtain large industrial supply contracts and master residential supply contracts with large quantity of end users.

Our success depends on our ability to obtain large industrial supply contracts and master residential supply contracts with a large quantity of end users. Our failure to obtain large industrial supply contracts and master residential supply contracts with a large quantity of end users will adversely affect our ability to generate revenue and our growth potential and may adversely impact our financial condition and operating results.

Our inability to fund our capital expenditure requirements may adversely affect our growth and profitability.

Our business is capital intensive. Our continued growth is dependent upon our ability to generate more revenue from our existing distribution systems and raise capital from outside sources. We believe that in order to continue to capture additional market share, we will have to raise more capital to fund the construction and installation of the natural gas distribution network for our customers under existing contracts and for new customers. In order to expand our operation, we expect that we will need additional financing for acquisition and expansion in terms of debt financing or equity financing. Our ability to obtain needed financing at any time may depend on a number of factors, including our financial condition and results of operations, the condition of the PRC economy and the natural gas industry in the PRC, and conditions in relevant financial markets in the United States, the PRC and elsewhere in the world. In the future we may be unable to obtain the necessary financing on a timely basis and on acceptable terms, and our failure to do so may adversely affect our financial position, competitive position, growth and profitability.

We may not be able to effectively control and manage our growth.

From August 2003 to December 2010, we have entered into twenty-nine (29) franchise agreements to provide natural gas to certain newly developed residential communities, and we expect that we will secure more of such franchise agreements in the years to come.

5

If our business and markets grow and develop, it will be necessary for us to finance and manage expansion in an orderly fashion. In addition, we may face challenges in managing expanding natural gas distribution network and service offerings and in integrating acquired businesses with our own. Our business expansion has resulted, and will continue to result, in substantial demands on our management, operational, technological and other resources. To manage and support our growth, we must improve our existing operational, administrative and technological systems and our financial and management controls, and recruit, train and retain additional qualified technical and management personnel as well as other administrative and sales and marketing personnel, particularly as we expand into new markets. We cannot assure you that we will be able to effectively and efficiently manage the growth of our operations, recruit and retain qualified technical and management personnel and integrate new communities into our operations. Any failure to effectively and efficiently manage our expansion may materially and adversely affect our ability to capitalize on new business opportunities, which in turn may have a material adverse impact on our financial condition and results of operations.

The nature of our natural gas operations is highly risky and we may be subject to civil liabilities as a result of our business of gas operations.

Our natural gas operations are subject to potential hazardous accidents to the gathering, processing, separation, storage and delivery of natural gas, such as pipeline ruptures, explosions, product spills, leaks, emissions and fires. These potential hazardous accidents can cause personal injury and loss of life, severe damage to and destruction of property and equipment, and pollution or other environmental damage, and may result in suspension or shutting down of operations at the affected facilities of residential areas. Consequently, we may face civil liabilities in the ordinary course of our business. These liabilities may result in us being required to make indemnification payments in accordance with the applicable contracts and regulations. At present, we do not carry any insurance to cover such liabilities in the ordinary course of our business. Although we have not faced any civil liabilities in the past since we started the current line of business in the ordinary course of our natural gas operations, there is no assurance that we will not face such liabilities in the future. If such liabilities occur in the future, they may adversely and materially affect our operations and financial condition.

Changes in the regulatory environment could adversely affect our business.

The distribution of natural gas to industrial and residential customers and operation of filling stations are highly regulated in the PRC requiring registrations with the government for the issuance of licenses required by various governing authorities in the PRC. For example, to operate in our line of business, we are required to obtain and maintain licenses such as the Natural Gas Business License and the franchise Business License. In addition, there are various standards that must be met for filling stations including handling and storage of natural gas, tanker handling, and compressor operation which are regulated by the government. The costs of complying with regulations may increase which may in turn harm our business. Furthermore, future changes in environmental laws and regulations in the PRC could occur that could result in stricter standards and enforcement, larger fines and liability, and increased capital expenditure requirement and operating costs, any of which could have a material adverse effect on our financial condition or results of operations.

We may not be able to effectively protect our proprietary technology, which could harm our business and competitive position.

Our success depends, in part, on our ability to protect our proprietary technologies. At present, we use an unpatented proprietary natural gas compression process that allows us to effectively and economically compress natural gas and distribute it. This process was developed by us based on a patented technology co-owned by our Chairman and Chief Executive Officer, Mr. Yu-Chuan Liu, and another individual who is not associated with our company. We cannot assure you that we are, and will be able to effectively protect our technology, and our current or potential competitors do not have, and will not obtain or develop similar compression process, the occurrence of either of which could harm our business and competitive position.

Implementation of PRC intellectual property-related laws has historically been lacking, primarily because of ambiguities in the PRC laws and difficulties in enforcement. Accordingly, intellectual property rights and confidentiality protections in the PRC may not be as effective as in the United States or other developed countries. Policing unauthorized use of proprietary technology is difficult and expensive, and we might need to resort to litigation to enforce our rights or defend us, or to determine the enforceability, scope and validity of our proprietary rights or those of others. Such litigation may require significant expenditure of cash and management efforts and could harm our business, financial condition and results of operations. An adverse determination in any such litigation will impair our intellectual property rights and may harm our business, competitive position, and business prospects.

We may be exposed to intellectual property infringement and other claims by third parties, which, if successful, could cause us to pay significant damage awards and incur other costs.

At present, we use an unpatented, proprietary natural gas compression process that allows us to effectively and economically compress natural gas and distribute it. This process was developed by us based on a patented technology co-owned by our Chairman and Chief Executive Officer, Mr. Yu-Chuan Liu, and another individual who is not associated with our company. In developing the process, we did not obtain and have not obtained authorization from such individual to use the patented technology. We believe that the technology we use is significantly improved and distinguished from the original patented technology, and any infringement claim related to the original patented technology would be unlikely to succeed. However, we cannot assure you that our assessment is and will be correct. In addition, as litigation becomes more common in the PRC in resolving commercial disputes, we face a higher risk of being the subject of intellectual property infringement claims. The validity and scope of claims relating to natural gas compression technology and related devices and machines patents involve complex technical, legal and factual questions and analysis and, therefore, may be highly uncertain. The defense and prosecution of intellectual property suits, patent opposition proceedings and related legal and administrative proceedings can be both costly and time consuming and may significantly divert the efforts and resources of our technical and management personnel. An adverse determination in any such litigation or proceedings to which we may become a party could subject us to significant liability, including damage awards to third parties, court orders requiring us to seek licenses from third parties, to pay ongoing royalties, or to redesign our products or subject us to injunctions preventing us from providing gas services to our customers as required by various contracts we entered. Protracted litigation could also result in our customers or potential customers deferring or limiting their purchase or use of our products until resolution of such litigation.

6

Our limited operating history may not serve as an adequate basis to judge our future prospects and results of operations.

We have a limited operating history. We commenced our current line of business of offering natural gas to customers in certain cities in China in 2003. Our limited operating history may not provide a meaningful basis on which to evaluate our business. Although our revenues and profits have grown since we started our current business, we cannot assure you that we will maintain our profitability or that we will not incur net losses in the future. We will continue to encounter risks and difficulties frequently experienced by companies at a similar stage of development, including our potential failure to:

| | raise adequate capital for expansion and operations; |

| | implement our business model and strategy and adapt and modify them as needed; |

| | increase awareness of our brands, protect our reputation and develop customer loyalty; |

| | manage our expanding operations and service offerings, including the integration of any future acquisitions; |

| | maintain adequate control of our expenses; and |

| | anticipate and adapt to changing conditions in the natural gas utility market in which we operate as well as the impact of any changes in government regulations, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics. |

If we are not successful in addressing any or all of these risks, our business may be materially and adversely affected.

We do not have key man insurance on our Chairman and CEO, Mr. Liu, on whom we rely for the management of our business.

We depend, to a large extent, on the abilities and participation of our current management team, but have a particular reliance upon Mr. Yu Chuan Liu. The loss of the services of Mr. Liu, for any reason, may have a material adverse effect on our business and prospects. We cannot assure you that the services of Mr. Liu will continue to be available to us, or that we will be able to find a suitable replacement for Mr. Liu. We do not carry key man life insurance for any key personnel.

In addition, our future success also depends upon the continuing services of the other members of our senior management team, including our Marketing Director, Zhi Min Zhong; our Vice President and Chief Engineer, Shu Kui Bian; and our Chief Financial Officer, Yugang Zhang. If one or more of our senior executives or other key personnel are unable or unwilling to continue in their present positions, we may not be able to replace them easily or at all, and our business may be disrupted and our financial condition and results of operations may be materially and adversely affected. Competition for senior management and senior technology personnel in our line of business is intense in China, the pool of qualified candidates is very limited, and we may not be able to retain the services of our senior executives or senior technology personnel, or attract and retain high-quality senior executives or senior technology personnel in the future. Such failure could materially and adversely affect our future growth and financial condition.

We do not presently maintain product liability insurance, and our property equipment insurance does not cover their full value, which leaves us with exposure in the event of loss or damage to our properties or claims filed against us.

We currently do not carry any product liability or other similar insurance. While product liability lawsuits in the PRC are not common and we have never experienced significant failures of our products, we cannot assure you that we would not face such liability in the event of the failure of any of our products. We only carry basic property insurance to cover our real property, natural gas pipelines, storage facilities and equipment. However, we do not have other insurance such as business liability or disruption insurance coverage for our operations in the PRC.

7

We do not maintain a reserve fund for warranty or defective equipment claims. Our costs could substantially increase if we experience a significant number of warranty claims.

Currently, we provide one (1) year service warranty for the end user equipment, such as gas indoor pipes and gas meters to our customers after we have installed the gas distribution systems and commenced gas supply for them. The warranties require us to repair and replace defective components. Since we started our current line of business, we have received a very limited number of warranty claims for our products that only involved minor repairs and whose costs were negligible (around $250 in total). Consequently, the costs associated with our warranty claims have historically been very low. Therefore, we have not established any reserve funds for potential warranty claims. However, if we experience any increase in warranty claims or if our repair and replacement costs associated with warranty claims increase significantly, it would have a material adverse effect on our financial condition and results of operations.

Risks Related to Doing Business in the PRC.

We face the risk that changes in the policies of the PRC government could have a significant impact upon the business we may be able to conduct in the PRC and the profitability of such business.

All of our business operations are conducted in China. Accordingly, our business, financial condition, results of operations and prospects are affected significantly by economic, political and legal developments in China. The Chinese economy differs from the economies of most developed countries in many respects, including level of government involvement in economic activities, stage of national development, and control of foreign exchange.

While the Chinese economy has grown significantly in the past 20 years, the growth has been uneven, both geographically and among various sectors of the economy.

The PRC’s economy is in a transition from a planned economy to a market oriented economy subject to five-year and annual plans adopted by the government that set national economic development goals. Policies of the PRC government can have significant effects on the economic conditions of the PRC. The PRC government has confirmed that economic development will follow the model of a market economy. Under this direction, we believe that the PRC will continue to strengthen its economic and trading relationships with foreign countries and business development in the PRC will follow market forces. While we believe that this trend will continue, we cannot assure you that this will be the case. A change in policies by the PRC government could adversely affect our interests by, among other factors: changes in laws, regulations or the interpretation of laws and regulations, confiscatory taxation, restrictions on currency conversion, imports or sources of supplies, or the expropriation or nationalization of private enterprises. Although the PRC government has been pursuing economic reform policies for more than two decades, we cannot assure you that the government will continue to pursue such policies or that such policies may not be significantly changed, especially in the event of a change in leadership, social or political disruption, or other circumstances affecting the PRC’s political, economic and social life.

The PRC laws and regulations governing our current business operations are sometimes vague and uncertain. Any changes in such PRC laws and regulations may have a material and adverse effect on our business.

We conduct substantially all of our business through our subsidiary, Beijing Gas, established in China. Beijing Gas is generally subject to laws and regulations applicable to foreign investment in China and, in particular, laws applicable to wholly foreign-owned enterprises. The PRC legal system is based on written statutes. Prior court decisions may be cited for reference but have limited precedential value. There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including but not limited to the laws and regulations governing our business, or the enforcement and performance of our arrangements with customers in the event of the imposition of new laws or regulations, or new interpretation of existing laws and regulations. Beijing Gas and any future PRC subsidiaries are considered foreign invested enterprises under PRC laws, and as a result, we are required to comply with PRC laws and regulations governing foreign invested enterprises. These laws and regulations are sometimes vague and may be subject to future changes, and their official interpretation and enforcement may involve substantial uncertainty. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our businesses.

A slowdown or other adverse developments in the PRC economy may materially and adversely affect our customers, demand for our services and our business.

We are a holding company. All of our operations are conducted in the PRC and all of our revenues are generated from sales in the PRC. Although the PRC economy has grown significantly in recent years, we cannot assure you that such growth will continue. The use of natural gas for commercial and residential consumption in the PRC is relatively new and growing, but we do not know how sensitive we are to a slowdown in economic growth or other adverse changes in the PRC economy which may affect demand for natural gas. A slowdown in overall economic growth, an economic downturn or recession or other adverse economic developments in the PRC may materially reduce the demand for natural gas and materially and adversely affect our business.

Inflation in the PRC could negatively affect our profitability and growth.

While the PRC economy has experienced rapid growth in recent years, such growth has been uneven among various sectors of the economy and in different geographical areas of the country. Rapid economic growth can lead to growth in the money supply and rising inflation. If prices for our products and services rise at a rate that is insufficient to compensate for the rise in the costs of supplies, it may have an adverse effect on profitability. In order to control inflation in the past, the PRC government has imposed controls on bank credits, limits on loans for fixed assets and restrictions on state bank lending. Such an austerity policy can lead to a slowing of economic growth. In October 2004, the People’s Bank of China, the PRC’s central bank, raised interest rates for the first time in nearly a decade and indicated in a statement that the measure was prompted by inflationary concerns in the Chinese economy. In 2007, the People’s Bank of China raised the interest rates again. Repeated rises in interest rates by the central bank would likely slow economic activity in China which could, in turn, materially increase our costs and also reduce demand for our products and services.

8

Beijing Gas is subject to restrictions on paying dividends and making other payments to us.

We are a holding company incorporated in the State of Utah and do not have any assets or conduct any business operations other than our investments in our subsidiaries. As a result of our holding company structure, we rely primarily on dividends payments from our subsidiary in China. However, PRC regulations currently permit payment of dividends only out of retained earnings, as determined in accordance with PRC accounting standards and regulations. The “retained earning” has the same meaning under both US GAAP and PRC accounting standards in general, except that under PRC regulations, minimum ten percent (10%) of net profit after tax has to be set aside as the reserve fund. The upper limit of the reserve fund is fifty percent (50%) of the total registered capital of the Company. Only after such set-aside reserve fund is satisfied, can dividends be paid out of retained earnings. Thus, the impact of such set-aside reserve fund on the Company is the restriction upon the Company’s ability to pay dividends to shareholders. For the most recently completed fiscal year, we have satisfied the set-aside reserve fund requirement and dividends could have been paid out of retained earnings. However, this year, we do not have plans to distribute dividends. Our subsidiary and affiliated entity in China are also required to set aside a ten percent (10%) of their after-tax profits according to PRC accounting standards and regulations to fund certain reserve funds. The PRC government also imposes controls on the conversion of Renminbi (the Chinese currency) into foreign currencies and the remittance of currencies out of China. We may experience difficulties in completing the administrative procedures necessary to obtain and remit foreign currency. See “Government control of currency conversion may affect the value of your investment” herein. Furthermore, if our subsidiary or affiliated entity in China incurs debt on their own in the future, the instruments governing the debt may restrict their ability to pay dividends or make other payments. If we or our subsidiary is unable to receive the revenues due from our operations, we may be unable to pay dividends on our common stock. As of now, we have not attempted to distribute and remit any dividends from our subsidiaries in China and therefore, we have not experienced restrictions.

Governmental control of currency conversion may affect the value of your investment.

The PRC government imposes controls on the convertibility of Renminbi (“RMB”), the Chinese currency, into foreign currencies and, in certain cases, the remittance of currency out of the PRC. We receive substantially all of our revenues in RMB, which is currently not a freely convertible currency. Shortages in the availability of foreign currency may restrict our ability to remit sufficient foreign currency to pay dividends, or otherwise satisfy foreign currency dominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, and interest payments, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate governmental authorities is required where RMB is to be converted into foreign currency and remitted out of the PRC to pay capital expenses such as the repayment of bank loans denominated in foreign currencies.

The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay certain of our expenses as they come due.

The fluctuation of the Renminbi may materially and adversely affect your investment.

The value of the RMB against the U.S. dollar and other currencies may fluctuate and is affected by, among other things, changes in the PRC’s political and economic conditions. As we rely entirely on revenues earned in the PRC’s, any significant revaluation of the RMB may materially and adversely affect our cash flows, revenues and financial condition. For example, to the extent that we need to convert U.S. dollars we receive from an offering of our securities into RMB for our operations, appreciation of the RMB against the U.S. dollar could have a material adverse effect on our business, financial condition and results of operations. Conversely, if we decide to convert our RMB into U.S. dollars for the purpose of making payments for dividends on our common stock or for other business purposes and the U.S. dollar appreciates against the RMB, the U.S. dollar equivalent of the RMB we convert would be reduced. In addition, the depreciation of significant U.S. dollar denominated assets could result in a charge to our income statement and a reduction in the value of these assets.

On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the RMB to the U.S. dollar. Under the new policy, the RMB is permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. This change in policy has resulted in an approximately twenty-one percent (25%) appreciation of the RMB against the U.S. dollar between July 21, 2005 and January 28, 2011. While the international reaction to the RMB revaluation has generally been positive, there remains significant international pressure on the PRC government to adopt an even more flexible currency policy, which could result in a further and more significant appreciation of the RMB against the U.S. dollar.

9

The discontinuation of any preferential tax treatment currently available to us and the increase in the enterprise income tax in the PRC could in each case result in a decrease of our net income and materially and adversely affect our results of operations.

The PRC government has provided various incentives to foreign-invested enterprises and domestic companies operating in a national level economic and technological development zone, including reduced tax rates and other measures. For example, Beijing Gas, which is registered and operating in a high-tech zone in Beijing, has been qualified as a “high or new technology enterprise.” As a result, it is entitled to a preferential enterprise income tax rate of fifteen percent (15.0%) so long as it continues to operate in the high-tech zone and maintains its “high or new technology enterprise” status. Beijing Gas received a two (2) year exemption from the enterprise income tax for its first two (2) profitable years of operation, which were 2003 and 2004. Beijing Gas was thereafter entitled to a preferential enterprise income tax rate of seven and a half percent (7.5%) for the succeeding three (3) years (with an exceptional tax rate of nine percent (9.0%) for 2005), which expired on December 31, 2007. However, we cannot assure you that the current preferential tax treatments and the current level of the enterprise income tax enjoyed by our PRC operating subsidiary will continue, and any legislative changes to the tax regime could discontinue any preferential tax treatment and increase the enterprise income tax rate applicable to our principal subsidiaries in the PRC. Specifically, the PRC Enterprise Income Tax Law (the “EIT Law”), was enacted on March 16, 2007. Under the EIT Law, effective on January 1, 2008, China adopted a uniform tax rate of twenty-five percent (25.0%) for all enterprises (including foreign-invested enterprises) and revoke the current tax exemption, reduction and preferential treatments applicable to foreign-invested enterprises. However, the current preferential tax rate of fifteen percent (15.0%) applicable to high and new technology enterprises and the current preferential tax treatments for all enterprises (including foreign-invested enterprises) will be grandfathered for a period of five (5) years following the effective date of the EIT Law until January 1, 2013. The EIT Law applies to all of our PRC operating subsidiaries, including Beijing Gas, which is currently both a high and new technology enterprise and a foreign-invested enterprise. Any future increase in the enterprise income tax rate applicable to our PRC operating subsidiaries or other adverse tax treatments, such as the discontinuation of preferential tax treatments, would have a material adverse effect on our results of operations and financial condition.

Dividends payable by us to our foreign investors may become subject to withholding taxes under PRC tax laws.

Under the EIT Law, dividends payable to foreign investors which are “derived from sources within the PRC” may be subject to income tax at the rate of twenty percent (20%) by way of withholding. Since we are a holding company and substantially all of our income will come from dividends that we receive from our PRC subsidiaries, dividends that we declare from such income may be deemed “derived from sources within the PRC” for purposes of the EIT Law and therefore subject to a twenty percent (20%) withholding tax. While the EIT Law stipulates that such taxes may be exempted or reduced, since no rules or guidance concerning the new tax law have been issued yet, it is unclear under what circumstances, and to what extent, such tax would be exempted or reduced. One example of a limitation on the twenty percent (20%) withholding tax is the way in which, pursuant to a treaty for the avoidance of double taxation, income tax levied by the PRC authorities on U.S. investors may not exceed ten percent (10%) of the gross amount of the dividends, provided that we are deemed to be a PRC resident enterprise under the new tax law. If we are required under the EIT Law to withhold PRC income tax on our dividends payable to our foreign shareholders, the value of your investment in our common stock may be materially and adversely affected.

Gains on the sales of our shares may become subject to PRC income taxes.

Under the EIT Law, our foreign corporate shareholders may be subject to a twenty percent (20%) income tax upon any gains they realize from the transfer of their shares, if such income is regarded as income from “sources within the PRC.” What will constitute “sources within the PRC” and whether or not there will be any exemption or reduction in taxation for our foreign corporate investors, however, are unclear since no rules or guidance concerning the new tax law has been issued yet. If our foreign shareholders are required to pay PRC income tax on the transfers of their shares, the value of your investment in our common stock may be materially and adversely affected.

Recent PRC State Administration of Foreign Exchange (“SAFE”) regulations regarding offshore financing activities by PRC residents, have undertaken continuous changes which may increase the administrative burden we face and create regulatory uncertainties that could adversely affect the implementation of our acquisition strategy, and a failure by our shareholders who are PRC residents to make any required applications and filings pursuant to such regulations may prevent us from being able to distribute profits and could expose us and our PRC resident shareholders to liability under PRC law.

Recent regulations promulgated by the PRC State Administration of Foreign Exchange, or SAFE, regarding offshore financing activities by PRC residents have undergone a number of changes which may increase the administrative burden we face.

In October 2005, SAFE promulgated regulations in the form of public notices, which require registrations with, and approval from, SAFE on direct or indirect offshore investment activities by PRC resident individuals. The SAFE regulations require that if an offshore company directly or indirectly formed by or controlled by PRC resident individuals, known as “SPC”, intends to acquire a PRC company, such acquisition will be subject to strict examination by the SAFE. Without registration, the PRC entity cannot remit any of its profits out of the PRC as dividends or otherwise. Gas (BVI) is deemed a SPC under these SAFE regulations. As such, our shareholders who are PRC residents, must comply with the registration and disclosure requirements provided under the SAFE regulations. Mr. Yu Chuan Liu, our Chairman and Chief Executive Officer, has completed the registration with the SAFE and has been issued a SAFE certificate was issued by SAFE to Beijing Gas in August 2006. We have determined that there are about a dozen of additional shareholders who are subject to the SAFE regulations and whose compliance status will have a material effect on our ability to remit any of our profits out of the PRC as dividends or otherwise. In addition, we have agreed with the Investors of this round of financing that within ninety (90) days of the closing such additional shareholders will file registration with SAFE, and obtain SAFE certificates. The failure by our shareholders who are PRC residents to make any required applications and filings pursuant to such regulations may prevent us from being able to distribute profits and could expose us and our PRC resident shareholders to liability under PRC law.

10

Any recurrence of severe acute respiratory syndrome, or SARS, or another widespread public health problem, could adversely affect our operations.

In 2002, a breakout of SARS in China and other parts of Asia resulted in major disruptions to the economy of China and Asia. A renewed outbreak of SARS or another widespread public health problem in the PRC, where all of the Company’s revenue is derived, could have an adverse effect on our operations. Our operations may be impacted by a number of health-related factors, including quarantines or closures of some of our offices that would adversely disrupt our operations.

Any of the foregoing events or other unforeseen consequences of public health problems could adversely affect our operations.

Because our principal assets are located outside of the United States and nearly all of our directors and all of our officers reside outside of the United States, it may be difficult for you to enforce your rights based on U.S. Federal Securities Laws against us, our officers, or our directors in the U.S. or to enforce a U.S. Court Judgment against us or our directors or officers in the PRC.

All of our five directors and all of our officers reside outside of the United States. In addition, our operating subsidiaries are located in the PRC and substantially all of our assets are located outside of the United States. It may therefore be difficult for investors in the United States to enforce their legal rights based on the civil liability provisions of the U.S. Federal securities laws against us in the courts of either the U.S. or the PRC and, even if civil judgments are obtained in U.S. courts, to enforce such judgments in PRC courts. Further, it is unclear if extradition treaties now in effect between the United States and the PRC would permit effective enforcement against us or our officers and directors of criminal penalties, under the U.S. Federal securities laws or otherwise.

We may face obstacles from the communist system in the PRC.

Foreign companies conducting operations in PRC face significant political, economic and legal risks. The Communist regime in the PRC, including a cumbersome bureaucracy, may hinder Western investment.

We may have difficulty establishing adequate management, legal and financial controls in the PRC.

The PRC historically has not adopted a western style of management and financial reporting concepts and practices, as well as in modern banking, computer and other control systems. We may have difficulty in hiring and retaining a sufficient number of qualified employees to work in the PRC. As a result of these factors, we may experience difficulty in establishing management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet Western standards.

Risks Related to Our Common Stock.

Our officers, directors and affiliates control us through their positions and stock ownership and their interests may differ from other stockholders.

Our officers, directors and affiliates beneficially own approximately 55.4% of our Common Stock. Yu chuan Liu, our Chairman, and Chief Executive Officer, beneficially owns approximately 24.0% and Mr. Quandong Sun, a director, beneficially owns 19.8% of our Common Stock. As a result, Mr. Liu and Mr. Sun are able to influence the outcome of stockholder votes on various matters, including the election of directors and extraordinary corporation transactions including business combinations. Yet Mr. Liu and Mr. Sun’s interests may differ from other stockholders. Furthermore, the current ratios of ownership of our common stock reduce the public float and liquidity of our common stock which can in turn affect the market price of our common stock. Please refer to “Security Ownership of Certain Beneficial Owners and Management” of this Registration Statement for more information regarding beneficial ownership of securities of our management.

We are not likely to pay cash dividends in the foreseeable future.

We currently intend to retain any future earnings for use in the operation and expansion of our business. We do not expect to pay any cash dividends in the foreseeable future but will review this policy as circumstances dictate. Should we decide in the future to do so, as a holding company, our ability to pay dividends and meet other obligations depends upon the receipt of dividends or other payments from our operating subsidiary in the PRC. In addition, our operating subsidiary, from time to time, may be subject to restrictions on its ability to make distributions to us, including as a result of restrictions on the conversion of local currency into U.S. dollars or other hard currency and other regulatory restrictions.

There is currently a limited trading market for our common stock.

Our common stock is quoted on the Over-the-Counter Bulletin Board (the “OTCBB”). However, our bid and asked quotations have not regularly appeared on the OTCBB for any consistent period of time. There is no established trading market for our common stock and our common stock may never be included for trading on any stock exchange or through any other quotation system (including, without limitation, the NASDAQ Stock Market). You may not be able to sell your shares due to the absence of a trading market.

11

Our Common Stock may be considered to be a “penny stock” and, as such, the market for our Common Stock may be further limited by certain SEC rules applicable to penny stocks.

To the extent the price of our common stock remains below $5.00 per share, we have net tangible assets of $2,000,000 or less, or if we fall below certain other thresholds, our common shares will be subject to certain “penny stock” rules promulgated by the SEC. Those rules impose certain sales practice requirements on brokers who sell penny stock to persons other than established customers and accredited investors (generally institutions with assets in excess of $5,000,000 or individuals with net worth in excess of $1,000,000). For transactions covered by the penny stock rules, the broker must make a special suitability determination for the purchaser and receive the purchaser’s written consent to the transaction prior to the sale. Furthermore, the penny stock rules generally require, among other things, that brokers engaged in secondary trading of penny stocks provide customers with written disclosure documents, monthly statements of the market value of penny stocks, disclosure of the bid and asked prices and disclosure of the compensation to the brokerage firm and disclosure of the sales person working for the brokerage firm. These rules and regulations adversely affect the ability of brokers to sell our common shares and limit the liquidity of our securities.

Our common stock is illiquid and subject to price volatility unrelated to our operations.

The market price of our common stock could fluctuate substantially due to a variety of factors, including market perception of our ability to achieve our planned growth, quarterly operating results of other companies in the same industry, trading volume in our common stock, changes in general conditions in the economy and the financial markets or other developments affecting our competitors or us. In addition, the stock market is subject to extreme price and volume fluctuations. This volatility has had a significant effect on the market price of securities issued by many companies for reasons unrelated to their operating performance and could have the same effect on our common stock.

You may face difficulties in protecting your interests, and your ability to protect your rights through the U.S. federal courts may be limited, we are incorporated in non-U.S. jurisdictions, we conduct substantially all of our operations in China, and all of our officers reside outside the United States.

We conduct substantially all of our operations in China through our wholly owned subsidiaries in China. All of our officers reside outside the United States and some or all of the assets of those persons are located outside of the United States. As a result, it may be difficult or impossible for you to bring an action against us or against these individuals in China in the event that you believe that your rights have been infringed under the securities laws or otherwise. Even if you are successful in bringing an action of this kind, the laws of the PRC may render you unable to enforce a judgment against our assets or the assets of our directors and officers. As a result of all of the above, our public stockholders may have more difficulty in protecting their interests through actions against our management, directors or major stockholders than would stockholders of a corporation doing business entirely within the United States.

A large number of shares will be eligible for future sale and may depress our stock price.

We are required under the Registration Rights Agreement to register for sale by the investors and certain other parties a total number of 12,681,255 shares of Common Stock, including 1,771,074 shares of common stock which are issuable upon (i) exercise of warrants issued to the Placement Agent in the Private Financing, and (ii) shares of Common Stock issued based on the “Make Good” provisions of the Stock Purchase Agreement. As these shares are placed on the market for sale, it will increase the supply of stocks for sale, and therefore depress the selling price of our stock. On February 11, 2010, our registration statement on Form S-1, registration no. 333-147998 was declared effective by the SEC, pursuant to which 5,705,138 shares of our common stock are eligible for sale through the registration statement.

Sales of substantial amounts of common stock, or a perception that such sales could occur, and the existence of options or warrants to purchase shares of common stock at prices that may be below the then current market price of the common stock, could adversely affect the market price of our common stock and could impair our ability to raise capital through the sale of our equity securities.

The exercise of certain warrants will dilute the investment by current investors.

Currently our outstanding warrants include: (i) series A warrants to purchase an aggregate of 241,708 shares of common stock at $3.84 per share, (ii) series C warrants to purchase an aggregate of 3,083,588 shares of common stock at $3.375 per share, (iii) series G warrants to purchase an aggregate of 109,489 shares of common stock at $3.84 per share, and (iv) warrants to purchase 3,898,687 shares of common stock accompanying 8% senior secured convertible notes at $0.744 per share. Under the existing warrants, a total of 7,333,473 common shares will need to be issued by us if the warrant holders decide to exercise the warrants. If this happens, the investment of our current shareholders would be significantly diluted.

Use of Proceeds

We will not receive any proceeds from the sale by the Selling Stockholders of the shares of common stock covered by this prospectus.

Market for Common Equity and Related Stockholder Matters

Our common stock is quoted on the OTCBB under the symbol SGAS.OB. Since our September 7, 2006 reverse merger with GAS Investment China Co., Ltd. (“Gas (BVI)”), there has been minimal trading activity in our shares. The following table provides the high and low sales prices for our common stock as reported for the past three (3) years.

12

Such prices are based on inter-dealer bid and asked prices, without markup, markdown, commissions, or adjustments and may not represent actual transactions.

| HIGH | LOW | |||||||

| CALENDAR QUARTER ENDED | BID(S) | BID(S) | ||||||

| First Quarter of, 2008 | $ | 4.0 | $ | 2.10 | ||||

| Second Quarter of, 2008 | $ | 2.45 | $ | 1.35 | ||||

| Third Quarter of, 2008 | $ | 1.45 | $ | 0.77 | ||||

| Fourth Quarter of 2008 | $ | 0.80 | $ | 0.30 | ||||

| First Quarter of 2009 | $ | 0.40 | $ | 0.06 | ||||

| Second Quarter of 2009 | $ | 0.50 | $ | 0.13 | ||||

| Third Quarter of 2009 | $ | 0.50 | $ | 0.31 | ||||

| Fourth Quarter of 2009 | $ | 1.21 | $ | 0.46 | ||||

| First Quarter of 2010 | $ | 1.05 | $ | 0.72 | ||||

| Second Quarter of 2010 | $ | 0.95 | $ | 0.53 | ||||

| Third Quarter of 2010 | $ | 0.58 | $ | 0.29 | ||||

| Fourth Quarter of 2010 | $ | 0.50 | $ | 0.38 | ||||

As of December 31, 2010, there were 657 holders of record of our common stock.

Dividends

To date, we have neither declared nor paid any cash dividends on shares of our common stock. We presently intend to retain earnings to finance the operation and expansion of our business and do not anticipate declaring cash dividends in the foreseeable future.

Warrants

There are series A warrants to purchase an aggregate of 241,708 shares of common stock at $3.84 per share, series C warrants to purchase an aggregate of 3,083,588 shares of common stock at $3.375 per share, and series G warrants to purchase an aggregate of 109,489 shares of common stock at $3.84 per share. The warrants were issued to investors on September 7, 2007. The warrants expire in 2012. There are also outstanding warrants to purchase 3,898,687 shares of the Company’s common stock accompanying the 8% senior secured convertible notes. The warrants are exercisable until November 30, 2012 at an exercise price of $0.744 per share.

Securities authorized for issuance under equity compensation plans

The Board of Directors of the Company adopted a Stock Option Plan (the “Plan”) on November 19, 2007. Under the Plan, the Company is authorized to issue options to purchase up to 1,460,000 shares of the common stock and the options may be issued as incentive stock options, non-qualified options, restricted stock options, or stock appreciation rights. The Company revoked the Plan in December 2008. As of December 31, 2009, no options have been issued under the Plan since the inception of the Plan.

Management’s Discussion and Analysis or Plan of Operation

The following discussion and analysis of our consolidated financial condition and results of operations should be read in conjunction with the consolidated financial statements and related notes of Beijing Gas appearing elsewhere in this prospectus. This discussion and analysis contains forward-looking statements that involve risks, uncertainties and assumptions. Actual results may differ materially from those anticipated in these forward-looking statements as a result of certain factors, including, but not limited to, those set forth under “Risk Factors” in this prospectus.

Overview

We are engaged in the development of natural gas distribution systems and the distribution of natural gas to residential, and industrial customers in small and medium-sized cities in China, through our indirectly-owned subsidiaries in the PRC, Beijing Gas and its subsidiaries .

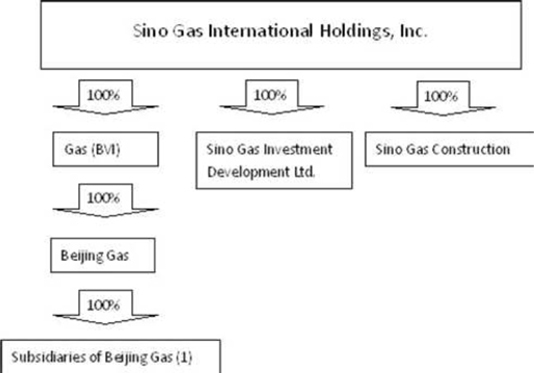

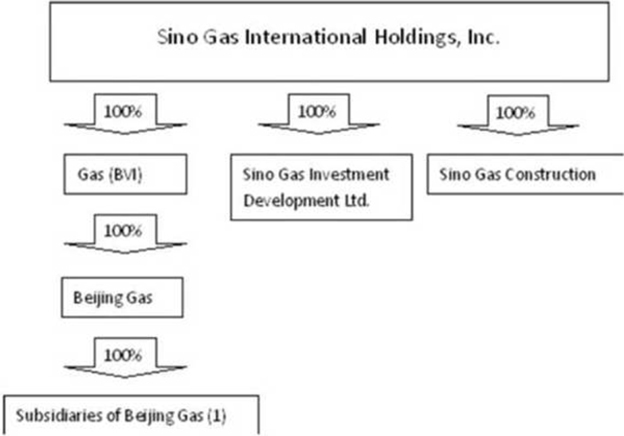

Beijing Gas is organized as a holding company with twenty-seven (27) subsidiaries, known as project companies, in four (4) provinces, and four (4) branches offices in Beijing, as shown on the corporate structure chart provided below. The project companies are the operating subsidiaries of Beijing Gas. Each project company operates as a local natural gas distributor in a city or county, known as an operational location, under an exclusive franchise agreement between Beijing Gas and the local government or entities in charge of gas utility, pursuant to which Beijing Gas formed the project company to operate the natural gas distribution project in the operational location. These exclusive franchise agreements last between 20-30 years.

In addition, Beijing Gas holds a forty percent (40%) equity interest in Beijing Zhong Ran Xiang Ke Oil and Gas Technology Co. Ltd. (“Beijing Zhong Ran Xiang Ke”), a PRC joint venture entity engaged in the business of development, licensing and sale of oil and gas technologies and equipment, and sale of self-produced products.

13

Through its subsidiaries, Beijing Gas is a natural gas distributor, principally engaging in the investment, operation and management of city gas pipeline infrastructure, in the distribution of natural gas to residential and industrial users, in the construction and operation of natural gas distribution networks, and in the development and application of natural gas related technologies. Beijing Gas and it subsidiaries own and operate natural gas distribution systems in 35 small and medium size cities serving approximately 167,750 residential and seven (7) industrial customers. Our facilities include approximately 1,040 km of pipeline and delivery networks with a daily capacity of approximately 110,000 cubic meters of gas. We own and operate natural gas distribution systems primarily in Hebei, Jiangsu, Jilin, Anhui and Beijing.

Below is our corporate structure as of December 1, 2010:

(1) See “Organizational History of Gas (BVI) and Beijing Gas” under “Description of Business” of this prospectus regarding the subsidiaries of Beijing Gas.

Executive Summary

Economic & Industrial Trend

We generate revenue from two sources: (i) connection fees for constructing connections to our natural gas distribution network and (ii) sales of natural gas. Our connection activities are closely related to the development of the real estate industry in our targeted cities in China, given the fact that almost all of our connection fees are from new residential apartments. Natural gas facilities in new apartments are often required by local governments, who aim to promote the use of natural gas to improve local residents’ quality of life.

We have experienced high growth of our connection activities since inception of our business due to the Chinese real estate boom in the past years. However, in 2007, the Chinese government implemented a series of policies and regulations to curb inflation and the property market. These policies, together with the worldwide financial crisis in 2008, has resulted a slowdown of the real estate market in China and our business, in turn, has been affected in 2008. Starting in 2008, the Chinese government had changed its policy and prioritized boosting of the economy. The Chinese government had adopted new policies to address the slowdown of the real estate market, such as reducing stamp duties and transactions fees, lowering interest rates, and loosening bank lending policies. The Chinese government had also decided to inject a stimulus package to boost the overall economy, including allocation of funds for mass housing projects. We saw signs of recovery of the real estate market in China at the beginning of 2009, and experienced the increased activities in the third and fourth quarters of 2009. Starting in April 2010, the Chinese government issued new policies to curb the rise of housing prices in certain cities. The new initiatives from the government resulted in lower transaction volumes during the second and third quarters of 2010. However, the transaction volumes started to pick up again in the fourth quarter of 2010.

14

Even with the up and down of the Chinese real estate market in the past two years, we believe that the future growth trend of the real estate market will not change because of the continuous urbanization in China. Moreover, the Chinese government, at both the national and the local level, continues to strongly support the use of clean energy, particularly natural gas.

There are three (3) pillars in the Chinese economy: (i) domestic consumption (both private and public), (ii) net exports, and (iii) domestic investment. The Chinese Government’s RMB 4 trillion stimulus package has had great impacts on China’s domestic production and investments in the past two years. In 2009, GDP growth rebounded to 7.9% in the second quarter from 6.1% in the first quarter, which represented a 10-year low. In the third quarter and fourth quarter of 2009, China’s economic growth accelerated to 9.1% and 10.7% respectively. China’s GDP grew by 8.7 percent in 2009, exceeding the target 8%. The GDP growth rate remained strong through the first two quarters of 2010. China’s GDP grew 11.9%, and 10.3% in the first and second quarters of 2010, respectively, from the same periods in 2009. Furthermore, China’s GDP increased by 9.6% during the third quarter of 2010 as compared to the third quarter of 2009.

Our gas users are composed of industrial and residential users. Gas sales from residential users are much less affected by economic and industrial factors and would maintain stable growth in the future, due to the increasing pool of our residential customers. Gas sales from industrial users is subject to the operating performance of the end industrial user. As we develop into more cities, we expect to add more industrial users in the coming year if capital requirements are available.

Material Opportunities

The gas distribution market is quite fragmented in the small (population less than 300,000) to medium (population between 300,000 to 1,000,000) sized cities. We are exploring potential project targets. The size of the projects varies from small cities to medium-sized cities. For small city markets, many of them are still untapped or undeveloped. The development of these markets is generally considered major growth components of the Company.

Regarding medium-sized or large cities, most of them have already been developed by large distributors or are still operated by state-owned companies. Acquisition opportunities exist for those still run by state-owned companies, as the central government encourages suppliers to turn them into privately-owned companies. The acquisition of these markets would have material impact on the Company, increasing the Company’s assets and revenues significantly. The Company intends to raise money for accretive acquisitions when they become available.

Material Challenges

There are vast number of small-to-medium sized cities left undeveloped, but the competition is growing, as there are many small new players in the market attracted by the profitability and growth potential of the business. Meanwhile, from time to time, we are also facing competitions from stronger competitors, as large city markets are getting saturated and our competitors are beginning to expand into smaller cities.

We are facing limited opportunities in developing into first-tier cities in China, as most of them have already been taken by other large gas distributors, such as Xin’ao Gas Co. Ltd (largest in China) in the past decade.

Still, potential users in small and medium-sized cities need to be educated by the benefits of natural gas. It takes some time for them to get to know how natural gas can improve the quality of life. This is especially true for new markets, where there is no use of natural gas. Small cities tend to be more reluctant for use of new energies than large cities where residents depend more on coal, rather than natural gas.

China’s energy market is highly regulated by the government, with regard to purchase price and sale price of natural gas. Whenever there is an adjustment to purchase price by the government, gas distributors would increase the sale price correspondingly, subject to a public hearing and government approval. The increase of natural gas prices in China is lagging behind that in the international markets. The Chinese government has seldom adjusted the price of natural gas and we cannot rule out the possibility of an increase in natural gas prices by the government in the future. Even though we could adjust the sale price accordingly after the increase in purchase price, thereby passing the increase onto the end users, the fact remains that such price increases would make natural gas more expensive, as compared to other alternative energies, and in turn hinder our business development.

Risks in Short-Term and Long-Term

In each of the cities we are developing and aiming to develop, the real estate market is the major factor that impacts us. Most of our residential customers are new home buyers. If the real estate market turns downward, the demand for new homes would decrease, resulting in fewer natural gas connections, which would negatively impact our business.

To reduce the Company’s dependence on connection fees, the Company is looking at opportunities to diversify its business by expanding into related industries, such as pipelines and gas stations. However, we do not expect to develop into those areas in full in the near future..

15

RESULTS OF OPERATIONS

Nine Months Ended September 30, 2010 Compared to Nine Months Ended September 30, 2009