U.S. SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-Q

(Mark One)

x QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended September 30, 2012

o TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from _______________ to _______________

Commission File Number

Keyuan Petrochemicals, Inc.

(Exact name of registrant as specified in its charter)

| Nevada | 45-0538522 | |

| (State or other jurisdiction of incorporation or organization) | (IRS Employer Identification No.) |

Qingshi Industrial Park

Ningbo Economic & Technological Development Zone

Ningbo, Zhejiang Province

P.R. China 315803

(86) 574-8623-2955

(Issuer's telephone number)

(Former address)

Check whether the issuer (1) filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act of 1934 during the past 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (Sec. 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one)

| Large Accelerated Filer | o | Accelerated Filer | o | |

| Non-accelerated filer | o | Smaller reporting company | x |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Securities Exchange Act of 1934) Yes o No x

As of November 16, 2012, the Registrant has 57,646,160 shares of common stock outstanding and 5,333,340 shares of Series B Preferred Stock outstanding.

TABLE OF CONTENTS

| PART I - FINANCIAL INFORMATION | |

| Item 1. Financial Statements | 4 |

| Condensed Consolidated Balance Sheets | 4 |

Condensed Consolidated Statements of Comprehensive Income (Loss) | 5 |

| Condensed Consolidated Statements of Cash Flows | 6 |

| Notes to Condensed Consolidated Financial Statements | 7 – 22 |

| Item 2. Management’s Discussion and Analysis or Plan of Operation | 23 |

| Item 3. Quantitative and Qualitative Disclosures About Market Risk | 32 |

| Item 4. Controls and Procedures | 32 |

| PART II – OTHER INFORMATION | 35 |

| Item 1. Legal Proceedings | 35 |

| Item 1A. Risk Factors | 35 |

| Item 2. Unregistered Sales of Equity Securities And Use Of Proceeds | 35 |

| Item 3. Defaults Upon Senior Securities | 35 |

| Item 4. Mine Safety Disclosures | 35 |

| Item 5. Other Information | 35 |

| Item 6. Exhibits | 36 |

2

INTRODUCTORY NOTE

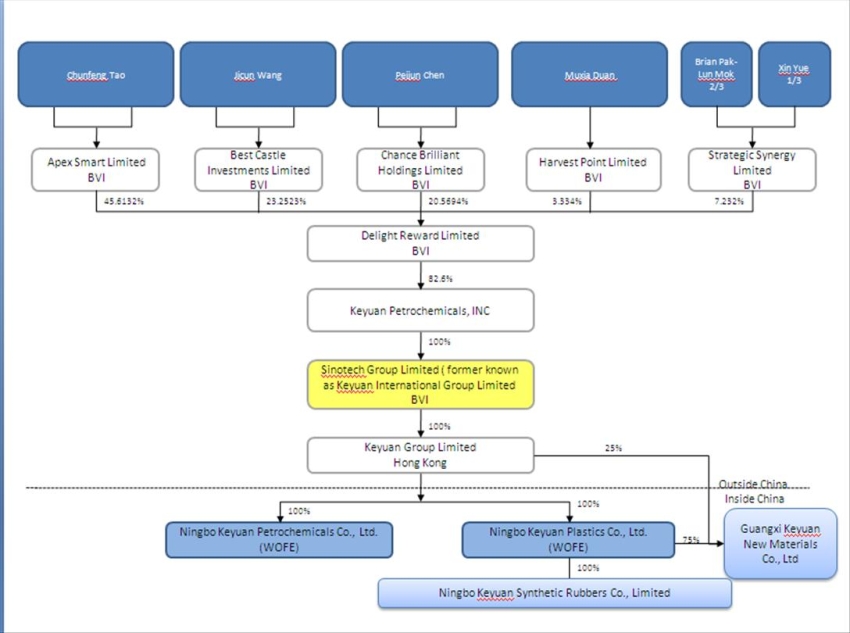

Except as otherwise indicated by the context, references in this interim report on Form 10-Q (this “Form 10-Q”) to the “Company,” “Keyuan” “we”, “us” or “our” are references to the combined business of Keyuan Petrochemicals, Inc. and its consolidated subsidiaries. References to “Sinotech” are references to our wholly-owned subsidiary, Sinotech Group Limited (formerly known as Keyuan International Group Limited)”; references to “Keyuan HK” are references to our wholly-owned subsidiary, Keyuan Group Limited; references to “Ningbo Keyuan” are references to our wholly-owned subsidiary, Ningbo Keyuan Plastics Co.,Ltd.; references to “Ningbo Keyuan Petrochemicals” are to our wholly-owned subsidiary, Ningbo Keyuan Petrochemicals Co., Ltd; references to “Keyuan Synthetic Rubbers” are references to our wholly-owned subsidiary, Ningbo Keyuan Synthetic Rubbers Co., Ltd.; references to ”Guangxi Keyuan” are references to our wholly-owned subsidiary, Guangxi Keyuan New Materials Co.,Ltd.References to “China” or “PRC” are references to the People’s Republic of China. References to “RMB” are to Renminbi, the legal currency of China, and all references to “$” and dollar are to the U.S. dollar, the legal currency of the United States.

Special Note Regarding Forward-Looking Statements

This report contains forward-looking statements and information that are based on the beliefs of our management as well as assumptions made by and information currently available to us. Such statements should not be unduly relied upon. When used in this report, forward-looking statements include, but are not limited to, the words “anticipate,” “believe,” “estimate,” “expect,” “intend,” “plan” and similar expressions, as well as statements regarding new and existing products, technologies and opportunities, statements regarding market and industry segment growth and demand and acceptance of new and existing products, any projections of sales, earnings, revenue, margins or other financial items, any statements of the plans, strategies and objectives of management for future operations, any statements regarding future economic conditions or performance, uncertainties related to conducting business in China, any statements of belief or intention, and any statements or assumptions underlying any of the foregoing. These statements reflect our current view concerning future events and are subject to risks, uncertainties and assumptions. There are important factors that could cause actual results to vary materially from those described in this report as anticipated, estimated or expected, including, but not limited to: competition in the industry in which we operate and the impact of such competition on pricing, revenues and margins, volatility in the securities market due to the general economic downturn; Securities and Exchange Commission (the “SEC”) regulations which affect trading in the securities of “penny stocks,” and other risks and uncertainties. Except as required by law, we assume no obligation to update any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward- looking statements, even if new information becomes available in the future. Depending on the market for our stock and other conditional tests, a specific safe harbor under the Private Securities Litigation Reform Act of 1995 may be available. Notwithstanding the above, Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”) expressly state that the safe harbor for forward-looking statements does not apply to companies that issue penny stock. Because we may from time to time be considered to be an issuer of penny stock, the safe harbor for forward-looking statements may not apply to us at certain times.

3

KEYUAN PETROCHEMICALS, INC. AND SUBSIDIAIRES

CONDENSED CONSOLIDATED BALANCE SHEETS

| Note | September 30, 2012 | December 31, 2011 | ||||||||||

| (Unaudited) | ||||||||||||

| ASSETS | ||||||||||||

| Current assets: | ||||||||||||

| Cash | 3 | $ | 7,255,600 | $ | 7,325,017 | |||||||

| Pledged bank deposits | 200,972,578 | 156,318,066 | ||||||||||

| Bills receivable | 633,200 | 1,574,000 | ||||||||||

| Accounts receivable | 4 | 2,419,301 | 2,226,288 | |||||||||

| Inventories | 5 | 69,292,607 | 38,945,968 | |||||||||

| Prepayments to suppliers | 6 | 29,063,792 | 15,781,294 | |||||||||

| Consumption tax refund receivable | 7 | 37,273,246 | 55,809,560 | |||||||||

| Amounts due from related parties | 22 | 39,575 | 39,350 | |||||||||

| Other current assets | 8 | 54,979,033 | 45,978,428 | |||||||||

| Deferred income tax assets | 17 | 37,561 | 37,348 | |||||||||

| Total current assets | 401,966,493 | 324,035,319 | ||||||||||

| Property, plant and equipment, net | 9 | 210,836,395 | 190,867,621 | |||||||||

| Intangible assets, net | 10 | 903,959 | 978,503 | |||||||||

| Land use rights | 11 | 10,794,017 | 11,068,762 | |||||||||

| VAT recoverable | 8 | 1,390,582 | 2,893,635 | |||||||||

| Total assets | $ | 625,891,446 | $ | 529,843,840 | ||||||||

| LIABILITIES AND STOCKHOLDERS’ EQUITY | ||||||||||||

| Current liabilities: | ||||||||||||

| Short-term bank borrowings | 12 | $ | 325,320,242 | $ | 225,969,421 | |||||||

| Bills payable | 107,327,400 | 63,550,250 | ||||||||||

| Current portion of long-term bank borrowings | 13 | 6,173,700 | 15,740,000 | |||||||||

| Accounts payable | 43,882,748 | 97,588,137 | ||||||||||

| Advances from customers | 31,359,642 | 7,821,623 | ||||||||||

| Accrued expenses and other payables | 14 | 27,129,341 | 30,287,946 | |||||||||

| Income taxes payable | 17 | 241,409 | 186,326 | |||||||||

| Dividends payable | 2,381,759 | 2,381,759 | ||||||||||

| Amounts due to related parties | 22 | - | 621,077 | |||||||||

| Total liabilities, all current | 543,816,241 | 444,146,539 | ||||||||||

| Series B convertible preferred stock: | ||||||||||||

| Par value: $0.001; Authorized: 8,000,000 shares | ||||||||||||

| 6% cumulative dividend with liquidation preference | ||||||||||||

| over common stock | ||||||||||||

| Issued and outstanding: 5,333,340shares, | ||||||||||||

| liquidation preference of $20,000,000 | 16,451,552 | 16,451,552 | ||||||||||

| Commitments and contingencies | 18 | - | - | |||||||||

| Stockholders’ equity: | ||||||||||||

| Common stock: | ||||||||||||

| Par value:$0.001; Authorized: 100,000,000 shares; | ||||||||||||

| Issued and outstanding: 57,646,160 shares as at September 30, 2012 and | ||||||||||||

| December 31, 2011 | 57,646 | 57,646 | ||||||||||

| Additional paid-in capital | 50,303,562 | 49,198,278 | ||||||||||

| Statutory reserve | 3,744,304 | 3,744,304 | ||||||||||

| Accumulated other comprehensive income | 5,848,820 | 6,545,811 | ||||||||||

| Retained earnings | 5,669,321 | 9,699,710 | ||||||||||

| Total stockholders’ equity | 65,623,653 | 69,245,749 | ||||||||||

| Total liabilities and stockholders' equity | $ | 625,891,446 | $ | 529,843,840 | ||||||||

See accompanying notes to the consolidated financial statements.

4

KEYUAN PETROCHEMICALS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF COMPREHENSIVE INCOME (LOSS) (UNAUDITED)

| Three Months Ended | Nine Months Ended | |||||||||||||||

| September 30, | September 30, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Sales | ||||||||||||||||

| External parties | $ | 164,347,259 | $ | 123,429,226 | $ | 532,097,663 | $ | 362,865,970 | ||||||||

| Related parties | - | 41,225,747 | - | 99,443,224 | ||||||||||||

| Total Sales | 164,347,259 | 164,654,973 | 532,097,663 | 462,309,194 | ||||||||||||

| Cost of sales | ||||||||||||||||

| External parties | 160,472,369 | 126,185,505 | 512,329,534 | 351,055,636 | ||||||||||||

| Related parties | - | 41,846,664 | - | 100,123,349 | ||||||||||||

| Total Cost of sales | 160,472,369 | 168,032,169 | 512,329,534 | 451,178,985 | ||||||||||||

| Gross profit (loss) | 3,874,890 | (3,377,196 | ) | 19,768,129 | 11,130,209 | |||||||||||

| Operating expenses | ||||||||||||||||

| Selling expenses | 251,399 | 91,607 | 892,522 | 846,287 | ||||||||||||

| General and administrative expenses | 2,127,023 | 5,220,525 | 7,393,838 | 12,985,350 | ||||||||||||

| Total operating expenses | 2,378,422 | 5,312,132 | 8,286,360 | 13,831,637 | ||||||||||||

| Income (loss) from operations | 1,496,468 | (8,689,328 | ) | 11,481,769 | (2,701,428 | ) | ||||||||||

Other income (expense) | ||||||||||||||||

| Interest income | 1,518,802 | 1,497,644 | 4,340,849 | 3,186,530 | ||||||||||||

| Interest expense | (5,863,569 | ) | (5,963,264 | ) | (13,172,551 | ) | (11,798,628 | ) | ||||||||

| Foreign exchange gain (loss), net | 331,405 | 1,466,275 | (33,113 | ) | 4,666,631 | |||||||||||

| Liquidated damages expense | - | (1,424,609 | ) | - | (2,725,339 | ) | ||||||||||

| Other | (5,439,250 | ) | (159,370 | ) | (5,656,289 | ) | 2,409,165 | |||||||||

Total other expenses | (9,452,612 | ) | (4,583,324 | ) | (14,521,104 | ) | (4,261,641 | ) | ||||||||

| Loss before income taxes | (7,956,144 | ) | (13,272,652 | ) | (3,039,335 | ) | (6,963,069 | ) | ||||||||

| Income tax (benefit) expense | (1,018,411 | ) | (2,613,449 | ) | 991,058 | 304,529 | ||||||||||

| Net loss attributable to Keyuan | ||||||||||||||||

| Petrochemicals Inc. stockholders | (6,937,733 | ) | (10,659,203 | ) | (4,030,393 | ) | (7,267,598 | ) | ||||||||

| Dividends to Series B convertible | ||||||||||||||||

| preferred stockholders | - | 306,247 | - | 908,753 | ||||||||||||

| Net loss attributable to Keyuan | ||||||||||||||||

| Petrochemicals Inc. common stockholders | $ | (6,937,733 | ) | $ | (10,965,450 | ) | $ | (4,030,393 | ) | $ | (8,176,351 | ) | ||||

| Net loss attributable to Keyuan | ||||||||||||||||

| Petrochemicals Inc. stockholders | $ | (6,937,733 | ) | $ | (10,659,203 | ) | $ | (4,030,393 | ) | $ | (7,267,598 | ) | ||||

| Other comprehensive (loss) income | ||||||||||||||||

| Foreign currency translation adjustment | (827,671 | ) | 942,212 | (696,991 | ) | 2,674,383 | ||||||||||

Comprehensive loss | $ | (7,765,404 | ) | $ | (9,716,991 | ) | $ | (4,727,384 | ) | $ | (4,593,215 | ) | ||||

Loss per share | ||||||||||||||||

Attributable to common stock | ||||||||||||||||

| - Basic | $ | (0.12 | ) | $ | (0.19 | ) | $ | (0.07 | ) | $ | (0.14 | ) | ||||

| - Diluted | $ | (0.12 | ) | $ | (0.19 | ) | $ | (0.07 | ) | $ | (0.14 | ) | ||||

| Weighted average number of shares of common stock used in calculation | ||||||||||||||||

| Basic | 57,646,160 | 57,579,490 | 57,646,160 | 57,579,096 | ||||||||||||

| Diluted | 57,646,160 | 57,579,490 | 57,646,160 | 57,579.096 | ||||||||||||

See accompanying notes to the consolidated financial statements.

5

KEYUAN PETROCHEMICALS, INC. AND SUBSIDIARIES

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS (UNAUDITED)

Nine Months Ended September 30, | ||||||||

| 2012 | 2011 | |||||||

| Cash flows from operating activities: | ||||||||

| Net loss | $ | (4,030,393 | ) | $ | (7,267,598 | ) | ||

| Adjustments to reconcile net loss to net cash provided by (used in) operating activities: | ||||||||

| Loss on disposal of property and equipment | - | 3,528 | ||||||

| Depreciation | 7,341,232 | 6,994,230 | ||||||

| Amortization | 80,251 | 78,033 | ||||||

| Land use rights amortization | 338,504 | 329,183 | ||||||

| Share-based compensation expense | 1,206,126 | 1,695,078 | ||||||

| Changes in operating assets and liabilities: | ||||||||

| Bills receivable | 951,117 | 6,972,884 | ||||||

| Account receivable | (180,533 | ) | - | |||||

| Inventories | (30,165,815 | ) | 41,427,530 | |||||

| Prepayments to suppliers | (13,210,595 | ) | (9,138,576 | ) | ||||

| Consumption tax refund receivable | 18,881,633 | (12,669,298 | ) | |||||

| Other assets | (6,491,085 | ) | (9,613,538 | ) | ||||

| Accounts payable | (54,641,410 | ) | 13,727,663 | |||||

| Accounts payable-related parties | (625,497 | ) | 505,542 | |||||

| Advances from customers | 23,525,946 | 7,750,302 | ||||||

| Income taxes payable | (409,611 | ) | (12,780,611 | ) | ||||

| Accrued expenses and other payables | (2,134,091 | ) | (7,281,521 | ) | ||||

| Net cash (used in) provided by operating activities | (59,564,221 | ) | 20,732,831 | |||||

| Cash flows from investing activities: | ||||||||

| Proceeds from property disposal of property and equipment | - | 10,582 | ||||||

| Purchase of property, plant and equipment, | (27,415,396 | ) | (23,631,456 | ) | ||||

| Net cash used in investing activities | (27,415,396 | ) | (23,620,874 | ) | ||||

| Cash flows from financing activities: | ||||||||

| Pledged bank deposits used for bank borrowings | (43,821,515 | ) | (56,821,639 | ) | ||||

| Proceeds from short-term bank borrowings | 663,720,065 | 189,192,525 | ||||||

| Repayment of short-term bank borrowings | (565,966,718 | ) | (130,501,038 | ) | ||||

| Proceeds from bills payable | 172,786,800 | 85,470,630 | ||||||

| Repayment of bills payable | (129,312,690 | ) | (94,796,100 | ) | ||||

| Repayments of long-term bank borrowings | (9,669,720 | ) | (13,101,900 | ) | ||||

| Short-term financing from related parties | - | 13,232,658 | ||||||

| Short-term financing to related parties | - | (13,118,390 | ) | |||||

| Proceeds from warrant exercise | - | 7,332 | ||||||

| Dividends paid | - | (2,585,647 | ) | |||||

| Net cash provided by (used in) financing activities | 87,736,222 | (23,021,569 | ) | |||||

| Effect of foreign currency exchange rate changes on cash | (826,022 | ) | 316,817 | |||||

| Net decrease in cash | (69,417 | ) | (25,592,795 | ) | ||||

| Cash at beginning of the period | 7,325,017 | 29,336,241 | ||||||

| Cash at end of the period | $ | 7,255,600 | $ | 3,743,446 | ||||

| Supplemental disclosure of cash flow information: | ||||||||

| Income taxes paid | $ | 1,820,668 | $ | 13,085,140 | ||||

| Interest paid, net of capitalized interest | $ | 9,264,849 | $ | 11,798,628 | ||||

| Dividends accrued | $ | - | $ | 4,436,753 | ||||

| Non-cash financing activities: | ||||||||

| Payable for purchase of property, plant and equipment | $ | 8,816,043 | $ | 14,668,112 | ||||

See accompanying notes to the consolidated financial statements.

6

1 ORGANIZATION AND DESCRIPTION OF BUSINESS

(a) Organization

Keyuan Petrochemicals, Inc. (the “Company”) was incorporated in the State of Texas on May 4, 2004 in the former name of “Silver Pearl Enterprises, Inc”. The Company, through its wholly-owned subsidiary, Sinotech Group Limited (Formerly known as “Keyuan International Group Limited”) and its indirect subsidiaries, Keyuan Group Limited (“Keyuan HK”), Ningbo Keyuan Plastics Co., Ltd. (“Ningbo Keyuan”), Ningbo Keyuan Petrochemicals Co., Ltd. (Ningbo Keyuan Petrochemicals), Ningbo Keyuan Synthetic Rubbers Co., Ltd. (“Ningbo Keyuan Synthetic Rubbers”), and Guangxi Keyuan New Materials Co., Ltd. (“Guanxi Keyuan”), are collectively referred herein below as “the Group” and are engaged in the manufacture and sale of petrochemical products in the People’s Republic of China (“PRC”).

(b) Other Events

In 2011, Company’s former auditor, KPMG , LLP (“KPMG”), brought certain issues to the Company’s Audit Committee’s attention through a March 28, 2011 memorandum and an April 18, 2011 letter (collectively, the “KPMG Memoranda”). KPMG requested that the Company’s Audit Committee conduct an independent investigation (the “Independent Investigation”) into those issues. On March 31, 2011, the Audit Committee elected to commence such Independent Investigation and engaged the services of independent counsel, Pillsbury Winthrop Shaw Pittman LLP (“Pillsbury”), which in turn engaged the services of Deloitte Financial Advisory Services LLP (“Deloitte”), as independent forensic accountants, and King & Wood, as Audit Committee counsel in the PRC. Pillsbury, Deloitte and King & Wood are collectively referred to herein as the “Investigation Team”. On September 28, 2011, the Independent Investigation was completed. The Independent Investigation identified possible violations of PRC laws and U.S. Securities laws, including the maintenance of an off-balance sheet cash account that was used primarily to pay service providers and other Company-related expenses. Total activity in the off-balance sheet cash account amounted to approximately $800,000 through December 31, 2010, with a net income statement effect of approximately $12,000, and $400,000 for the period from January 1, 2011 to March 31, 2011, with a net income statement effect of approximately $192,000, at which time the Company ceased its use. The Independent Investigation identified certain other issues that could result in potential violations of PRC or U.S. laws. The Company continues to work with its legal counsel to evaluate the matters identified in the investigation and to determine the extent to which the Company may be exposed to fines and penalties. The Company has preliminarily concluded that the extent to which it may be exposed to fines and penalties in the PRC is limited, and to date, has not received any PRC governmental or regulatory communication or inquiry related to these matters. However, management is currently unable to determine the final outcome of these matters and their possible effects on the consolidated financial statements.

On October 7, 2011, trading of the Company’s common stock was delisted by NASDAQ, and is currently quoted on the Over-the-Counter Bulletin Board (symbol: KEYP).

On September 11, 2012, the Company received a “Wells Notice” from the Staff of the U.S. Securities and Exchange Commission ( the “Commission”) stating that the Staff intends to recommend that the Commission bring a civil injunctive action against the Company, alleging that the Company violated Section 17(a) of the Securities Act of 1933 as well as Section 10(b), 13(a), and 13b(2) of the Securities Exchange Act of 1934 and Rules 10b-5 and 13a-13 thereunder. On the same day, the Commission also issued a Wells Notice to Mr. Chunfeng Tao, the Company’s Chief Executive Officer, advising him that the Staff intends to recommend that the Commission bring a civil injunctive action against him alleging that he violated Section 304 of the Sarbanes-Oxley Act.

A Wells Notice by the Staff is neither a formal allegation of wrongdoing nor a determination of wrongdoing. A Wells Notice indicates that the Commission has determined it may bring a civil action and provides the Company and Mr. Tao with an opportunity to provide the Commission with information as to why such action should not be brought.

The Company cannot predict the outcome of the matter with the Commission, including whether a lawsuit will be filled or the term of any settlement that may be reached. The Company will determine how to proceed based on further consultation with its legal counsel. At this time, the company does not expect the notice to materially interfere with its day to day operating business.

7

The Company’s management believes that the Company’s cash, working capital, and access to cash through its bank loans provide adequate capital resources to fund its operations and working capital needs for at least the next twelve months.

2 BASIS OF PRESENTATION

The accompanying unaudited condensed consolidated financial statements have been prepared in accordance with U.S. general accepted accounting principles (U.S. GAAP) and include the financial statements of the Company and its subsidiaries. All intercompany balances and transactions are eliminated in consolidation. The financial statements have been prepared in accordance with U.S. GAAP applicable to interim financial information and the requirements of Form 10-Q and Article 10 of Regulation S-X of the Securities and Exchange Commission. Accordingly, they do not include all of the information and disclosures required by accounting principles generally accepted in the United States of America for complete financial statements. These interim financial statements should be read in conjunction with the audited financial statements for the years ended December 31, 2011 and 2010, as not all disclosures required by generally accepted accounting principles for annual financial statements are presented. The interim financial statements follow the same accounting policies and methods of computation as the audited financial statements for the years ended December 31, 2011 and 2010. Interim results are not necessarily indicative of results for a full year. In the opinion of management, all adjustments, consisting of normal recurring adjustments, considered necessary for a fair presentation of the financial position and the results of operations and cash flows for the interim periods have been included.

3 CASH

Cash consists of cash on hand and cash at banks. As of September 30, 2012 and December 31, 2011, cash of $6,859,231 and $7,101,505, respectively, was held in major financial institutions located in the PRC; and cash of $344,054 and $124,355, respectively was held in the Hong Kong Special Administrative Region. Management performs periodic evaluations of the relative credit standings of those financial institutions, and believes that these major financial institutions have high credit ratings.

4 ACCOUNTS RECEIVABLE

The Group generally requires a prepayment of 100% of the sales contract price from its customers shortly before products are delivered. Such prepayment is recorded as “advances from customers” in the Group’s consolidated balance sheet, until the products are delivered and the customer takes ownership and assumes the risk of loss. With the approval of the Company’s general manager, the Company occasionally extends credit to its long-term customers with a good credit rating. As of September 30, 2012 and December 31, 2011, the balance of accounts receivable was $2,419,301 and $2,226,288 respectively.

5 INVENTORIES

Inventories consist of the following:

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| Raw materials | $ | 55,506,637 | $ | 26,226,388 | ||||

| Finished goods | 8,677,501 | 10,891,825 | ||||||

| Work-in-process | 5,108,469 | 1,827,755 | ||||||

| Total | $ | 69,292,607 | $ | 38,945,968 | ||||

8

6 PREPAYMENTS TO SUPPLIERS

As of September 30, 2012 and December 31, 2011, prepayments to suppliers are made in connection with the purchase of raw materials and the construction of the Group’s facilities. Prepayments to suppliers are reclassified to inventories or construction-in-progress, when the Group applies the prepayments to related purchases of materials after the related invoices are received.

7 CONSUMPTION TAX REFUND RECEIVABLE

The PRC government enacted a regulation that provides that domestically purchased heavy oil to be used for producing ethylene and aromatics products would be exempted from a consumption tax. In addition, the consumption tax paid for imported heavy oil would be refunded if it was used for producing ethylene and aromatics products. Given all the Group’s purchased heavy oils are, or are to be used for the production of ethylene and aromatics products, the Group recognizes a consumption tax refund receivable when the consumption tax has been paid and the relevant heavy oils have been used for production. As of September 30, 2012 and December 31, 2011, the Group recorded an estimated consumption tax refund amounting to $37,273,246, and $55,809,560 respectively.

On August 15,2012, the Group received a consumption tax refund of $95,124,967 and consumption tax claims of $37,273,246 are in process and are expected to be approved and refunded by the end of this year.

8 OTHER CURRRENT ASSETS

Other current assets consist of the following:

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| VAT recoverable | $ | 31,544,594 | $ | 9,991,877 | ||||

Receivable from Ningbo Litong (Note 22) | 690,584 | 2,740,970 | ||||||

| Customs deposits for imported inventories | 16,656,326 | 29,102,193 | ||||||

| Others | 5,624,467 | 4,143,388 | ||||||

| Income tax receivable | 463,062 | - | ||||||

| $ | 54,979,033 | $ | 45,978,428 | |||||

The estimate of deductible input VAT on the purchase of property, plant and equipment is determined using vendor contracts, engineering and other estimates, as well as historical experience, and is included in VAT recoverable. Approximately $1.4 million and $2.9 million is included in non-current assets as of September 30, 2012 and December 31, 2011 respectively.

Customs deposits for imported inventories represent amounts paid to the local customs office in connection with the importing of raw materials inventories. Upon approval by the customs authorities, these amounts become refundable by the local tax authority and are reclassified as consumption tax refund receivable (Note 7).

9 PROPERTY, PLANT AND EQUIPMENT

Property, plant and equipment consist of the following:

| Sptember 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| Buildings | $ | 3,910,467 | $ | 3,888,234 | ||||

| Machinery and equipment | 230,024,640 | 175,736,470 | ||||||

| Vehicles | 785,091 | 663,985 | ||||||

| Office equipment and furniture | 247,592 | 134,929 | ||||||

| Construction-in-progress | 302,729 | 27,449,846 | ||||||

| 235,270,519 | 207,873,464 | |||||||

| Less: Accumulated depreciation | (24,434,124 | ) | (17,005,843 | ) | ||||

| $ | 210,836,395 | $ | 190,867,621 | |||||

9

Depreciation expense on property, plant and equipment is allocated to the following items:

| Three months ended | Nine months ended | |||||||||||||||

| September 30 | September 30 | |||||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | |||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Cost of sales | $ | 1,846,619 | $ | 2,280,341 | $ | 7,206,265 | $ | 6,870,200 | ||||||||

| Selling, general and administrative expenses | 47,300 | 42,323 | 134,967 | 124,030 | ||||||||||||

| $ | 1,893,919 | $ | 2,322,664 | $ | 7,341,232 | $ | 6,994,230 | |||||||||

For the nine months ended September 30, 2012 and the year ended December 31,2011, interest capitalized amounted to $794,400 and $1,246,179, respectively.

10 INTANGIBLE ASSETS

Intangible assets consist of the following:

| Amortization | September 30, | December 31, | |||||||||||

| Period | 2012 | 2011 | |||||||||||

| Years | (Unaudited) | ||||||||||||

| Licensing agreements | 10-20 | $ | 1,503,850 | $ | 1,495,300 | ||||||||

| Less: Accumulated amortization | (599,891 | ) | (516,797 | ) | |||||||||

| $ | 903,959 | $ | 978,503 | ||||||||||

For the nine months ended September 30, 2012 and 2011, amortization expense for intangible assets amounted to $80,251 and $78,033, respectively. For the three months ended September 30, 2012 and 2011, amortization expense for intangible assets amounted to $26,750 and $26,358, respectively. Estimated amortization expense for each of the next five years is estimated to be approximately $100,000.

11 LAND USE RIGHTS

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| Land use rights | $ | 12,251,756 | $ | 12,182,100 | ||||

| Less: Accumulated amortization | (1,457,739 | ) | (1,113,338 | ) | ||||

| $ | 10,794,017 | $ | 11,068,762 | |||||

For the nine months ended September 30, 2012 and 2011, amortization expense related to land use rights was $338,504 and $329,183, respectively. For the three months ended September 30, 2012 and 2011, amortization expense related to land use rights was $112,835 and $111,184, respectively.

12 SHORT-TERM BANK BORROWINGS

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| Bank borrowings-secured/guaranteed | $ | 325,320,242 | $ | 225,969,421 | ||||

10

Short−term bank borrowings outstanding as of September 30, 2012 carry a weighted average interest rate of 6.14% (2011: 5.23%) for bank loans in RMB; a weighted average interest rate of 4.28% (2011: 3.47%) for bank loans in USD; a weighted average interest rate of 2.46% for bank loans in EUR, and have maturity terms ranging from one to twelve months and interest rates ranging from 1.27% to 7.93% (2011: 2.97% to 4.92%).

At September 30, 2012, approximately $48,835,000 and $28,966,374 included in short-term bank borrowings are payable to Shanghai Pudong Development Bank, which is secured by a one-year fixed term deposit with a carrying amount of $48,835,000 and is guaranteed by Kewei (Note 22). In addition, $142,371,739 payable to Bank of China is secured by one year fixed term deposits and pledged deposits with a carrying amount of $101,454,957 and by certain of the Group’s land use rights and properties; $35,630,975 payable to China Construction bank is secured by pledged deposits with a carrying amount of $8,147,382 and is guaranteed by Ningbo Pacific Ocean Shipping Co., Ltd (Note 22); and $22,144,350 payable to China Merchants bank is secured by pledged deposits with a carrying amount of $5,000,000 and is guaranteed by Ningbo Litong (Note 22). Among the rest of the Group's short-term borrowings, $47,371,804 is guaranteed by related party and third-party entities and individuals, including $9,923,700 which is guaranteed by the Company’s Chief Executive Officer as of September 30, 2012.

13 LONG-TERM BANK BORROWINGS

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| Loan from China Construction Bank | $ | 6,173,700 | $ | 15,740,000 | ||||

| Less: current portion | (6,173,700 | ) | (15,740,000 | ) | ||||

| $ | - | $ | - | |||||

As of September 30, 2012 and December 31, 2011, the Group's long-term bank loans are secured/ guaranteed by related-party entities and Mr. Tao (Note 22), bear interest from 7.29 % to 7.74% (2011:7.29% to 7.74%) and were repaid in October 2012.There were no additional long term bank borrowings in the nine months ended September 30, 2012.

14 ACCRUED EXPENSES AND OTHER PAYABLES

Accrued expenses and other payables as of September 30, 2011 and December 31, 2010 consist of:

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

(Unaudited) | ||||||||

| Payable for purchase of property, plant and equipment | $ | 21,477,138 | $ | 24,590,217 | ||||

| Accrued payroll and welfare | 370,791 | 1,061,508 | ||||||

| Liquidated damages | 2,493,326 | 2,493,326 | ||||||

| Other accruals and payables | 2,788,086 | 2,142,895 | ||||||

| $ | 27,129,341 | $ | 30,287,946 | |||||

15 STOCKHOLDERS’ EQUITY AND RELATED FINANCING AGREEMENTS

Dividends

Fixed dividends are accrued and cumulative one year from the date of the initial issuance of the Series B convertible preferred stock, are payable on a quarterly basis, and are determined as 6% of $3.75 for each share of the Series B convertible preferred stock.

On January 17, 2011, the Company’s Board of Directors approved the distribution of annual cash dividend of $0.36 per share for 2010 to be paid quarterly to its common stock stockholders at the assigned dates of record. In January 2011, certain stockholders of the Company announced the waiver of their rights to receive such cash dividends. In addition, Dragon State International Limited, the primary Series B convertible stockholder agreed to waive their rights to receive cash dividend for 2010 should they choose to convert their preferred stock before the record date. The estimated dividends to be distributed and the dividends waived are approximately $3.5 million and $17.2 million, respectively. In October 2011, the Company’s Board of Directors suspended the payment of quarterly cash dividends on the Company’s common stock while it pursues strategic alternatives including, but not limited to, taking the Company private, a merger or other transaction.

During the year ended December 31, 2011, 66,670 shares of the Series B convertible preferred stock were converted into 66,670 shares of the Company’s common stock. In addition,1,150 Series A warrants and 500 Series B warrants were exercised, and the Company issued 1,150 shares and 500 shares of the Company’s common stock, receiving proceeds of $4,863 and $2,468, respectively. There were no dividends to be paid and accrued for the three months ended September 30, 2012.

11

Registration rights agreement

In connection with the Series A Private Placement, the Company entered into a registration rights agreement with the Series A Investors, in which the Company agreed to file a registration statement with the Securities and Exchange Commission (“SEC”) to register for resale of the issued common stock, the common stock issuable upon conversion of the Series A convertible preferred stock, and the common stock underlying the Series A and Series B Warrants and the Placement agent warrants, within 30 calendar days of April 22, 2010 and to have this registration statement declared effective within 150 calendar days of April 22, 2010 or within 180 calendar days of April 22, 2010 in the event of a full review of the registration statement by the SEC. If the Company doesn’t comply with the foregoing obligations under the registration rights agreement, the Company will be required to pay liquidated damages in cash to each investor, at the rate of 1% of the applicable subscription amount for each 30 day period in which the Company is not in compliance; provided, that such liquidated damages will be capped at 10% of the subscription amount of each investor and will not apply to any registrable securities that may be sold pursuant to Rule 144 under the Securities Act if all of the conditions in Rule 144(i)(2) are satisfied at the time of the proposed sale, or are subject to an SEC comment with respect to Rule 415 promulgated under the Securities Act.

In connection with the Series B private placement, the Company entered into a registration rights agreement with the Series B Investors, in which the Company agreed to file a registration statement with the SEC to register for resale of the common stock issuable upon the conversion of the Series B convertible preferred stock, common stock underlying the Series C and Series D Warrants, and common stock underlying the placement agent warrants, within 30 calendar days following the later of (i) the closing date of the offering or (ii) the effective date of the prior registration statement for resale of the Issued Common Stock and common stock issuable upon the conversion of the Series A Preferred Stock, Series A and Series B Warrants, and placement agent warrants issued in the Series A Private Placement (the “Prior Registration Statement”), and to have the registration statement declared effective within 150 calendar days ( or 180 calendar days of the Closing Date in the event of a full review of the registration statement by the SEC) following the later to occur of (i) the closing date of the Series B Private Placement or (ii) the effective date of the Prior Registration Statement. If the Group does not comply with the foregoing obligations under the registration rights agreement, the Group will be required to pay cash liquidated damages to each Series B Investor, at the rate of 1% of the applicable subscription amount for each 30 day period in which the Group are not in compliance; provided, that such liquidated damages will be capped at 10% of the subscription amount of each investor and will not apply to any registrable securities that may be sold pursuant to Rule 144 under the Securities Act if all of the conditions in Rule 144(i)(2) are satisfied at the time of the proposed sale, or are subject to an SEC comment with respect to Rule 415 promulgated under the Securities Act.

12

Liquidated damages are also payable in the event that the Registration Statement is not maintained continuously effective for approximately 180 days, or if trading of the Company’s common stock is suspended or if the Company’s common stock is delisted from the principal exchange on which it is traded (NASDAQ) for more than three days.

On April 1, 2011, trading of the Company’s common stock was suspended and on October 7, 2011 was delisted by NASDAQ. Management determined that the registration statements were no longer effective commencing on April 7, 2011 and registerable securities in connection with the Series A and B private placements were not able to be sold pursuant to Rule 144 under the Securities Act until November 1, 2011. Accordingly, in the year ended December 31, 2011, an estimated contingent liability for $2,493,326 was accrued with a corresponding charge to earnings. Liquidated damages during the nine months ended September 30, 2012 and 2011 were nil and $2,725,339 respectively.

16 SHARE-BASED PAYMENTS

Effective June 30, 2010, the Board of Directors approved the Company’s 2010 Equity Incentive Plan ( the “Plan”). The maximum numbers of shares of common stock of the Company issuable pursuant to the Plan is 6,000,000 shares. The Plan shall be administered by the Board; provided however, that the Board may delegate such administration to a plan Committee.

On June 30, 2010, the Company granted a total of 3,000,000 stock options to certain senior management employees with a contractual term of 5 years. The exercise price of these stock options is $4.20 per share and the grant-date fair value of these stock options amounted to $3,347,298. A total of 2,810,000 stocks options vest over three years as follow: 30% shall vest and become exercisable one year after the grant date, 40% shall vest and become exercisable two years after the grant date, and 30% shall vest and become exercisable three years after the grant date. For the remaining 190,000 stock options: 40% shall vest and become exercisable one year after the grant date and 60% shall vest and become exercisable two years after the grant date.

On July 1, 2010, the Company granted a total of 80,000 stock options to two independent directors with contractual terms of 5 years. The exercise price of these stock options is $4.20 per share and the grant-date fair value of these stock options amounted to $91,349. A total of 40,000 of the options shall vest and become exercisable one year after the grant date and the remaining 40,000 of the stock options shall vest and become exercisable two years after the grant date, provided that the independent directors are re-elected for successive one year terms one year after the stock options issuance date.

On August 4, 2010, the Company granted 700,000 stock options to employees, with a contractual term of 5 years. The exercise price of these stock options was $4.50 per share and the grant-date fair value of these stock options amounted to $1,338,761. These stock options vest over three years as follows: 30% shall vest and become exercisable one year after the grant date, 40% shall vest and become exercisable two years after grant date and 30% shall vest and become exercisable three years after the grant date.

On December 29, 2010, 600,000 stock options granted to certain employees on August 4, 2010, were cancelled. As compensation for such cancellation, the Company committed to pay these employees incremental cash payments during the period through August 2013. The fair value of the committed cash payment on December 29, 2010 was approximately $400,000 and no incremental compensation costs resulted from the cancellation of these stock options. Included in accrued expenses and other payables is approximately $290,839 representing the liability related to the committed cash payment as of September 30, 2012.

No options were granted during the three and nine months ended September 30, 2012.

For the three months ended September 30, 2012 and 2011, share-based compensation expenses related to employee stock options charged to general and administrative expenses in the consolidated statements of operations were $386,630 and $406,098, respectively. For the nine months ended September 30, 2012 and 2011, share-based compensation expenses related to employee stock options charged to general and administrative expenses in the consolidated statements of operations were $1,206,126 and $1,695,078, respectively.

13

As of September 30, 2012, there were unrecognized compensation costs related to employee stock options of approximately $740,812. These costs are expected to be recognized on a straight-line basis, over the remaining weighted average service period of 0.69 years.

17 INCOME TAXES

The Company and its subsidiaries file separate income tax returns.

The United States of America

The Company is incorporated in the State of Nevada in the U.S., and is subject to the U.S. federal corporate income tax at progressive rates ranging from 15% to 35%. The state of Nevada does not impose any state corporate income tax.

British Virgin Islands

Keyuan International is incorporated in the British Virgin Islands (“BVI”). Under the current laws of British Virgin Islands, Keyuan International is not subject to tax on income or capital gains. In addition, upon payments of dividends by Keyuan International, no BVI withholding tax is imposed.

Hong Kong

Keyuan HK is incorporated in Hong Kong. Keyuan HK did not earn any income that was derived in Hong Kong for the nine months ended September 30, 2012 and 2011 and therefore was not subject to Hong Kong Profits Tax. The payments of dividends by Hong Kong companies are not subject to any Hong Kong withholding tax.

PRC

Ningbo Keyuan, Ningbo Keyuan Petrochemicals, Ningbo Keyuan Synthetic Rubbers and Guangxi Keyuan are incorporated in the PRC and the applicable PRC statutory income tax rate is 25%.

Components of loss before income tax expense (benefit) arose in the following jurisdictions:

Three months ended September 30, | Nine months ended September 30, | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | |||||||||||||

| PRC | $ | (7,152,274 | ) | $ | 9,087,464 | $ | 850,930 | $ | 2,852,121 | |||||||

| U.S. | (554,940 | ) | 3,610,942 | (1,980,970 | ) | (8,315,021 | ) | |||||||||

| Hong Kong and BVI | (248,928 | ) | 574,246 | (1,909,295 | ) | (1,500,169 | ) | |||||||||

| Loss before income taxes | $ | (7,956,142 | ) | $ | 13,272,652 | $ | (3,039,335 | ) | $ | (6,963,069 | ) | |||||

The Group’s income tax (benefit) expense in the consolidated statements of operations consists of the following:

| PRC: | Three months ended September 30, | Nine months ended September 30, | ||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | |||||||||||||

| Current income tax (benefit) expense | $ | (1,018,411 | ) | $ | - | $ | 991,058 | $ | 304,529 | |||||||

| Deferred income tax benefit | - | (2,613,449 | ) | - | - | |||||||||||

| Total income tax (benefit) expense | $ | (1,018,411 | ) | $ | (2,613,449 | ) | $ | 991,058 | $ | 304,529 | ||||||

14

Reconciliation between income tax (benefit) expense and the amounts computed by applying the PRC statutory income tax rate of 25% to (loss) income before income taxes is as follows:

| Three months ended September 30, | ||||||||||||||||

| 2012 | 2011 | |||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

Loss before income | $ | (7,956,142 | ) | $ | (13,272,652 | ) | ||||||||||

| Computed income tax (benefit) expense | (1,989,036 | ) | 25.0 | % | (3,318,163 | ) | 25.0 | % | ||||||||

| NOLs from overseas subsidiaries | 200,967 | (4.1 | %) | 1,356,212 | (10.2 | %) | ||||||||||

| Others/Timing differences | 769,658 | 9.7 | % | (651,498 | ) | 4.9 | % | |||||||||

| Actual income tax (benefit) expense | $ | (1,018,411 | ) | 21.0 | % | $ | 2,613,449 | 19.7 | % | |||||||

| Nine months ended September 30, | ||||||||||||||||

| 2012 | 2011 | |||||||||||||||

| (Unaudited) | (Unaudited) | |||||||||||||||

| Income (Loss) before income taxes | $ | (3,039,335 | ) | $ | (6,963,069 | ) | ||||||||||

| Computed expected income tax expense | (759,834 | ) | 25.0 | % | (1,740,767 | ) | 25.0 | % | ||||||||

| NOLs from overseas subsidiaries | 972,566 | 131 | % | 3,155,416 | (45.4 | %) | ||||||||||

| Others/Timing differences | 778,326 | 26 | % | (1,110,120 | ) | 16 | % | |||||||||

| Actual income tax expense | $ | 991,058 | 117 | % | $ | 304,529 | (4.4 | %) | ||||||||

The PRC income tax rate has been used because the majority of the Group’s consolidated income (loss) before income taxes arises in the PRC.

According to the prevailing PRC income tax law and its relevant regulations, non-PRC-resident enterprises are levied withholding tax at 10%, unless reduced by tax treaties or similar arrangements, on dividends from their PRC-resident investees for earnings accumulated beginning on January 1, 2008, and undistributed earnings generated prior to January 1, 2008 are exempt from such withholding tax. Further, the Company’s distributions from its PRC subsidiaries are subject to U.S. federal income tax at 35%, less any applicable qualified foreign tax credits. Due to the Company’s policy of permanently reinvesting substantially all of its earnings in its PRC business, the Company has not provided for deferred income tax liabilities for U.S. federal income tax purposes on its PRC subsidiaries’ undistributed earnings of $34.4 million and $31 million as of September 30, 2012 and December 31, 2011, respectively.

The Group files income tax returns in the United States and the PRC. The Company is subject to U.S. federal income tax examination by tax authorities for tax years beginning in 2004. According to the PRC Tax Administration and Collection Law, the statute of limitations is three years if the underpayment of taxes is due to computational errors made by the taxpayer or the withholding agent. The statute of limitations is extended to five years under special circumstances where the underpayment of taxes is more than RMB100,000 ($15,000). In the case of transfer pricing issues, the statute of limitation is ten years. There is no statute of limitation in the case of tax evasion. The PRC tax returns for the Company’s PRC subsidiary are open to examination by the PRC state and local tax authorities for the tax years beginning in 2008.

18 CONTINGENCY

In the normal course of business, the Group is subject to loss contingencies, such as legal proceedings and claims arising out of its business. An accrual for a loss contingency is recognized when it is probable that a liability has been incurred and the amount of loss can be reasonably estimated.

15

In connection with the shipping of finished products, inaccurate product information has been provided to the PRC Port authority. In addition, through June 30, 2011, Ningbo Keyuan failed to withhold income tax of approximately $50,000 from payments to certain external service providers and employees. In consultation with PRC legal counsel, management has evaluated the contingencies associated with the provision of inaccurate information and expects that the penalty, if any, will not be significant and will not have a material impact on the consolidated financial statement.

In addition, the Group had outstanding Letter’s of Credit as of September 30, 2012 of $20,721,987.

19 EARNINGS (LOSS) PER SHARE

The following table sets forth the computation of basic net income (loss) per share:

| Three months ended | Nine months ended | |||||||||||||||

| September 30, | September 30, | September 30, | September 30, | |||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | |||||||||||||

| Net loss income attribute to Keyuan Petrochemicals, Inc. stockholders | $ | (6,937,733 | ) | $ | (10,659,203 | ) | $ | (4,030,393 | ) | $ | (7,267,598 | ) | ||||

| Less: Dividend attributable to preferred stockholders | - | 306,247 | - | 908,753 | ||||||||||||

| Net loss attributable to Keyuan Petrochemical Inc. common stockholders | $ | (6,937,733 | ) | $ | (10,965,450 | ) | $ | (4,030,392 | ) | $ | (8,176,351 | ) | ||||

| Weighted average common shares basic and diluted | 57,646,160 | 57,579,490 | 57,646,160 | 57,579,096 | ||||||||||||

| Net loss per share-basic and diluted | $ | (0.12 | ) | $ | (0.19 | ) | $ | ( 0.07 | ) | $ | (0.14 | ) | ||||

20 FAIR VALUE MEASUREMENTS

The Company did not have any assets and liabilities that are measured at fair value on a recurring basis as of September 30, 2012 and 2011.

The fair values of cash, pledged bank deposits, bills receivable, accounts receivable, consumption tax refund receivable, short-term bank borrowings, bills payable, current portion of long-term borrowings, and accounts payable approximate their respective carrying amounts due to their short-term nature. Amounts due to related parties are not practicable to estimate due to the related party nature of the underlying transactions. The Group’s long-term debt, secured by various assets, bears interest at rates commensurate with market rates and therefore management believes carrying values approximate fair values.

21 SIGNIFICANT CONCENTRATIONS AND RISKS

As of September 30, 2012 and December 31, 2011, the Group held cash and pledged bank deposits in financial institutions of approximately $208,175,863 and $163,591,879, respectively. They were primarily held in major financial institutions located in mainland China and the Hong Kong Special Administrative Region. Management believes that these financial institutions have high credit ratings.

16

Sales to major customers, which individually exceeded 4% of the Group’s total net revenues, are as follows:

| Three months ended September 30, 2012 | Three months ended September 30, 2011 | ||||||||||||||||

| (Unaudited) | (Unaudited) | ||||||||||||||||

| Largest | Amount of | % Total | Largest | Amount of | % Total | ||||||||||||

Customers | Sales | Sales | Customers | Sales | Sales | ||||||||||||

| Customer A | $ | 25,073,797 | 15 | % | Customer A | $ | 41,225,299 | 25 | % | ||||||||

| Customer B | 19,205,656 | 12 | % | Customer I | 13,170,091 | 8 | % | ||||||||||

| Customer C | 9,186,080 | 6 | % | Customer F | 11,137,634 | 7 | % | ||||||||||

| Customer D | 8,164,027 | 5 | % | Customer J | 12,173,190 | 7 | % | ||||||||||

| Customer E | 7,836,830 | 5 | % | Customer K | 6,372,752 | 4 | % | ||||||||||

| Total | $ | 69,466,390 | 43 | % | Total | $ | 84,078,966 | 51 | % | ||||||||

| Nine months ended September 30, 2012 | Nine months ended September 30, 2011 | ||||||||||||||||

| (Unaudited) | (Unaudited) | ||||||||||||||||

| Largest | Amount of | % Total | Largest | Amount of | % Total | ||||||||||||

Customers | Sales | Sales | Customers | Sales | Sales | ||||||||||||

| Customer A | $ | 77,871,098 | 15 | % | Customer A | $ | 99,376,211 | 21 | % | ||||||||

| Customer B | 33,060,210 | 6 | % | Customer L | 42,569,008 | 9 | % | ||||||||||

| Customer F | 26,439,522 | 5 | % | Customer F | 41,406,576 | 9 | % | ||||||||||

| Customer G | 24,755,435 | 5 | % | Customer M | 19,465,251 | 4 | % | ||||||||||

| Customer H | 20,021,342 | 4 | % | Customer N | 18,257,022 | 4 | % | ||||||||||

| Total | $ | 182,147,607 | 35 | % | Total | $ | 221,074,068 | 47 | % | ||||||||

The Group currently buys a majority of its heavy oil, an important component of its products, from three suppliers. Although there are a limited number of suppliers of the particular heavy oil, management believes that other suppliers could provide similar heavy oil on comparable terms. A change in suppliers, however, could cause a delay in manufacturing and a possible loss of sales, which would affect operating results adversely. Purchases (net of VAT) from the largest three suppliers for three months ended September 30, 2012 and 2011 were $117,369,604 and $85,220,085, respectively. These purchases represented 77% and 77% respectively of all of the Company’s purchases for three months end September 30, 2012 and 2011. Purchases (net of VAT) from the largest three suppliers for nine months ended September 30, 2012 and 2011 were $372,708,756 and $317,299,110, respectively. These purchases represented 76% and 79% respectively of all of the Group’s purchases for the nine months ended September 30, 2012 and 2011.

The Group’s operations are carried out in the PRC. Accordingly, the Group’s business, financial condition and results of operations may be influenced by the political, economic and legal environments in the PRC as well as by the general state of the PRC’s economy. The business may be influenced by changes in governmental policies with respect to laws and regulations, anti-inflationary measures, currency conversion and remittance abroad, and rates and methods of taxation, among other things.

17

22 RELATED PARTY TRANSACTIONS AND RELATIONSHIPS AND TRANSACTIONS WITH CERTAIN OTHER PARTIES

(1) Related Party Transactions

The Company considers all transactions with the following parties to be the related party transactions.

| Name of parties | Relationship | |

| Mr. Chunfeng Tao | Majority stockholder | |

| Mr. Jicun Wang | Principal stockholder | |

| Mr. Peijun Chen | Principal stockholder | |

| Ms. Sumei Chen | Member of the Company’s Board of Supervisors and spouse of Mr. Wang | |

| Ms. Yushui Huang | Vice President of Administration, Ningbo Keyuan | |

| Mr. Weifeng Xue | Vice President of Accounting, Ningbo Keyuan through August 2011 | |

| Mr. Hengfeng Shou | Vice President of Sales, Ningbo Keyuan Petrochemical | |

| Ningbo Kewei Investment Co., Ltd | A company controlled by Mr. Tao through September 2011 | |

| (Ningbo Kewei) | ||

| Ningbo Pacific Ocean Shipping Co., Ltd | 100% ownership by Mr. Wang | |

| (Ningbo Pacific) | ||

| Ningbo Hengfa Metal Product Co., Ltd | 100% ownership by Mr. Chen | |

| (Ningbo Hengfa, former name "Ningbo Tenglong") | ||

| Shandong Tengda Stainless Steel Co., Ltd | 100% ownership by Mr. Chen | |

| (Shandong Tengda) | ||

| Ningbo Xinhe Logistic Co., Ltd | ||

| (Ningbo Xinhe) | 10% ownership by Ms. Huang | |

| Ningbo Kunde Petrochemical Co, Ltd. | Mr. Tao’s mother was a 65% nominee shareholder for Mr. Hu, a third party through September 2011 and included in transactions with certain other beginning October 1, 2011 | |

| (Ningbo Kunde) | ||

| Ningbo Jiangdong Jihe Construction Materials | Controlled by Mr. Xue’s Brother-in-law | |

| Store (Jiangdong Jihe) | ||

| Ningbo Wanze Chemical Co., Ltd | Mr. Tao’s sister-in-law is the legal representative | |

| (Ningbo Wanze) | ||

Ningbo Zhenhai Jinchi Petroleum Chemical Co., Ltd | Controlled by Mr. Shou | |

| (Zhenhai Jinchi) |

Related party transactions and amounts outstanding with the related parties as of and for the three months and nine months ended September 30, 2012 and 2011 are summarized as follows:

| Three Months ended September 30, | ||||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Sales of products (a) | $ | - | $ | 41,225,747 | ||||

| Purchase of raw material (b) | $ | - | $ | - | ||||

| Purchase of transportation services (c) | $ | 1,011,084 | $ | 1,230,893 | ||||

| Credit line of guarantee provision for bank borrowings (d) | $ | 34,398,840 | $ | - | ||||

| Loan guarantee fees (d) | $ | 102,889 | $ | 402,447 | ||||

| Short-term financing from related parties (e) | $ | - | $ | - | ||||

| Short-term financing to related parties (e) | $ | - | $ | - | ||||

| Nine Months ended September 30, | ||||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Sales of products (a) | $ | - | $ | 99,443,224 | ||||

| Purchase of raw material (b) | $ | - | $ | 7,113,589 | ||||

| Purchase of transportation services (c) | $ | 2,675,446 | $ | 2,158,772 | ||||

| Credit line of guarantee provision for bank borrowings (d) | $ | 34,398,840 | $ | - | ||||

| Loan guarantee fees (d) | $ | 306,873 | $ | 1,159,365 | ||||

| Short-term financing from related parties (e) | $ | - | $ | 13,232,658 | ||||

| Short-term financing to related parties (e) | $ | - | $ | 13,118,390 | ||||

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Amounts due from related parties (f) | $ | 39,575 | $ | 39,350 | ||||

| Amounts due to related parties (g) | $ | - | $ | 621,077 | ||||

18

(a) During the three months ended September 30, 2011, the Group sold finished products of $41,225,747 to Ningbo Kunde. During the nine months ended September 30, 2011, the Group sold finished products of $99,376,211 to Ningbo Kunde, and $67,013 to Zhenhai Jinchi, respectively.

(b) The Group purchased raw materials of $7,113,589 from Ningbo Kunde during the nine months ended September 30, 2011.

(c) The Group purchased transportation services of $1,011,084 and $1,230,893 from Ningbo Xinhe during the three months ended September 30, 2012 and 2011, respectively. The Group purchased transportation services of $2,675,446 and $2,158,772 from Ningbo Xinhe during the nine months ended September 30, 2012 and 2011, respectively.

(d) Guarantees for Bank Loans

Guarantees for bank loans provided by related parties during the three and nine months ended September 30, 2012 and 2011, are as follows:

Guarantee provided during the three months ended September 30 | Guarantee provided during the nine months ended September 30 | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| (Unaudited) | (Unaudited) | (Unaudited) | (Unaudited) | |||||||||||||

| Mr. Tao | $ | 16,644,600 | $ | - | $ | 16,644,600 | $ | - | ||||||||

| Jicun Wang and Chen | 17,754,240 | - | 17,754,240 | - | ||||||||||||

| Bank Loans guaranteed | ||||||||

| as of | ||||||||

| September 30 | December 31 | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | (Unaudited) | |||||||

| Mr. Tao | $ | 9,923,700 | $ | 34,628,000 | ||||

| Jicun Wang and Chen | 6,399,600 | 1,983,523 | ||||||

| Ningbo Pacific | 29,290,544 | 27,918,200 | ||||||

| Ningbo Hengfa | - | 14,795,600 | ||||||

| Shandong Tengda | - | 944,400 | ||||||

| Total | $ | 45,613,844 | $ | 80,269,723 | ||||

Beginning in 2011 loan guarantee fees of 0.3% the loan principal guaranteed are to be paid quarterly. During the three months ended September 30, 2012, loan guarantee fees were $32,767 and $70,122 for Ningbo Hengfa and Ningbo Pacific, respectively. In the three months ended September 30,2011, loan guarantee fees were $75,616,$241,921 and $84,910 for Ningbo Hengfa, Ningbo Pacific and Ningbo Kewei, respectively. During the nine months ended September 30, 2012, loan guarantee fees were $97,789 and $209,084 for Ningbo Hengfa and Ningbo Pacific , respectively. In the nine months ended September 30, 2011, loan guarantee fees were $225,732, $543,167 and $390,466 for Ningbo Hengfa ,Ningbo Pacific and Ningbo Kewei, respectively.

(e) Short-term financing transactions with related parties

There were no short-term financing activities with related parties during the three months ended September 30,2012 and 2011.

Short-term financing activities with related parties during the nine months ended September 30, 2012 and 2011 are as follows:

| Nine Months Ended September 30 | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| From(i) | To(i) | Balance(ii) | From(i) | To(i) | Balance(ii) | |||||||||||||||||||

| Ningbo Kewei | $ | - | $ | - | $ | - | $ | 5,394,900 | $ | (5,394,900 | ) | $ | - | |||||||||||

| Ningbo Kunde | - | - | - | 5,394,900 | (5,394,900 | ) | - | |||||||||||||||||

| Jiangdong Jihe | - | - | - | 2,442,858 | (2,328,590 | ) | ||||||||||||||||||

| $ | - | $ | - | $ | - | $ | 13,232,658 | $ | (13,118,390 | ) | $ | - | ||||||||||||

(i) Transactions during the year are translated at average exchange rates.

(ii) Balances at year end are translated at the balance sheet exchange rate.

19

(f) Amounts due from related parties consist of the following:

| September 30, | December 31, | |||||||

| 2012 | 2011 | |||||||

| Related Party | (Unaudited) | (Unaudited) | ||||||

| Mr. Tao | $ | 39,575 | $ | 39,350 | ||||

| $ | 39,575 | $ | 39,350 | |||||

Amounts due from Mr. Tao represent advances made for business expenses which are unsecured, interest free and due on demand.

(g) Amount due to related parties consists of the following:

| September 30, | December 31, | |||||||

| Related Party | 2012 | 2011 | ||||||

| (Unaudited) | (Unaudited) | |||||||

| Ninbo Xinhe | $ | - | $ | 621,077 | ||||

Amount due to related parties represent balances due for raw materials purchase and freight.

(2) Relationships and transactions with certain other parties

The Group has the following relationships and transactions with certain other parties:

| Name of parties | Relationship | |

| Ningbo Litong Petrochemical Co., Ltd | Former 12.75% nominee shareholder of Ningbo | |

| (Ningbo Litong) | Keyuan | |

| Ningbo Jiangdong Haikai Construction | Controlled by cousin of Mr. Weifeng Xue, Vice | |

| Materials Store (Jiangdong Haikai) | President of Accounting through August 2011 | |

| Ningbo Jiangdong Deze Chemical Co., Ltd | Controlled by cousin of Mr. Weifeng Xue, Vice | |

| (Jiangdong Deze) | President of Accounting through August 2011 | |

| Ningbo Anqi Petrochemical Co., Ltd | Controlled by cousin of Mr. Weifeng Xue, Vice | |

| (Ningbo Anqi) | President of Accounting through August 2011 | |

| Ningbo Kewei Investment Co., Ltd | A related party through September 2011 when control | |

| (Ningbo Kewei) | transferred, and included in transactions with certain other parties beginning October 1, 2011 | |

| Ningbo Kunde Petrochemical Co., Ltd | A related party through September 2011 when control | |

| (Ningbo Kunde) | transferred, and included in transactions with certain other parties beginning October 1, 2011 |

20

Transactions and amounts outstanding with these parties for the three and nine months ended September 30, 2012 and 2011, are summarized as follows:

| Three Months Ended September 30, | ||||||||

(Unaudited) | ||||||||

| 2012 | 2011 | |||||||

| Sales of products (h) | $ | 25,073,797 | $ | - | ||||

| Purchase of raw material (i) | $ | 17,183,224 | $ | 5,302,905 | ||||

| Credit line of guarantee for bank borrowings (j) | $ | 51,043,440 | $ | - | ||||

| Loan guarantee fees(j) | $ | 374,184 | $ | 256,020 | ||||

| Short-term financing from theses parties (k) | $ | - | $ | 3,949,020 | ||||

| Short-term financing to these parties (k) | $ | - | $ | 3,949,020 | ||||

| Amounts due from these parties | $ | 1,731,172 | $ | - | ||||

| Nine Months Ended September 30, | ||||||||

(Unaudited) | ||||||||

| 2012 | 2011 | |||||||

| Sales of products (h) | $ | 95,033,299 | $ | 777,960 | ||||

| Purchase of raw material (i) | $ | 39,521,516 | $ | 14,839,187 | ||||

| Credit line of guarantee for bank borrowings (j) | $ | 192,105,440 | $ | - | ||||

| Loan guarantee fees(j) | $ | 1,116,489 | $ | 761,676 | ||||

| Short-term financing from theses parties (k) | $ | - | $ | 51,835,741 | ||||

| Short-term financing to these parties (k) | $ | - | $ | 49,582,214 | ||||

| Amounts due from these parties | $ | 1,731,172 | $ | - | ||||

| Amounts due to these parties | $ | - | $ | 64,201 | ||||

(h) During the three months ended September 30 , 2012 and 2011, the Group sold finished products of $25,073,797 and nil to Ningbo Kunde, respectively. During the nine months ended September 30, 2012 and 2011, the Group sold finished products of $17,162,201 and $777,960, respectively, to Ningbo Litong, and $77,871,098 and nil respectively to Ningbo Kunde,. Amounts received in advance from Ningbo Kunde were $1,731,172 as of September 30, 2012, and are included in advances from customers on the consolidated balance sheet.

(i) During the three months ended September 30, 2012 and 2011, the Group purchased raw materials of $16,868,696 and $5,302,905, respectively, from Ningbo Litong, and $314,528 and nil, respectively from Ningbo Kunde. During the nine months ended September 30, 2012 and 2011, the Group purchased raw materials of $26,084,507 and $14,839,187, respectively from Ningbo Litong, and $13,437,009 and nil, respectively from Ningbo Kunde.

(j) Guarantees for Bank Loans

Guarantee provided during the three months endedSeptember 30 (Unaudited) | Guaranted provided during the nine months endedSeptember 30 (Unaudited) | |||||||||||||||

| 2012 | 2011 | 2012 | 2011 | |||||||||||||

| Ningbo Litong | $ | 16,644,600 | $ | - | $ | 67,252,200 | $ | 39,907,500 | ||||||||

| Ningbo Kewei | $ | 34,398,840 | $ | - | $ | 145,362,840 | $ | - | ||||||||

Bank loans guaranteed As of | ||||||||

| September 30 | December 31 | |||||||

| 2012 | 2011 | |||||||

| (Unaudited) | ||||||||

| Ningbo Litong | $ | 41,261,306 | $ | 61,632,077 | ||||

| Ningbo Keiwei | $ | 32,716,374 | $ | - | ||||

Beginning in 2011 loan guarantee fees of 0.3% the loan principal guaranteed after January 1, 2011 are to be paid quarterly. In the three months ended September 30, 2012, loan guarantee fees were $188,558 and $185,626 for Ningbo Litong and Ningbo Kewei, respectively. In the three months ended September 30,2011, loan guarantee fees were $256,020 and $84,910 for Ningbo Litong and Ningbo Kewei, respectively. In the nine months ended September 30,2012, loan guarantee fees were $562,821 and $553,666 for Ningbo Litong and Ningbo Kewei, respectively. In the nine months ended September 30,2011, loan guarantee fees were $761,646 and $390,466 for Ningbo Litong and Ningbo Kewei.

21

(k) Short-term financing transactions

Historically the Group and its theses parties have provided each other with short-term financing, typically, in the form of cash, bills receivable and bills payable.

Three Months Ended September 30 (Unaudited) | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| From(i) | To(i) | Balance(ii) | From(i) | To(i) | Balance(ii) | |||||||||||||||||||

| Ningbo Anqi | - | - | - | 3,949,020 | (3,949,020 | ) | - | |||||||||||||||||

| $ | - | $ | - | $ | - | $ | 3,949,020 | $ | (3,949,020 | ) | $ | - | ||||||||||||

Nine Months Ended September 30 (Unaudited) | ||||||||||||||||||||||||

| 2012 | 2011 | |||||||||||||||||||||||

| From(i) | To(i) | Balance(ii) | From(i) | To(i) | Balance(ii) | |||||||||||||||||||

| Ningbo Litong | $ | - | $ | - | $ | - | $ | 38,399,357 | $ | (36,145,830 | ) | $ | - | |||||||||||

| Jiangdong Deze | - | - | - | 2,620,380 | (2,620,380 | ) | - | |||||||||||||||||

| Ningbo Anqi | - | - | - | 10,816,004 | (10,816,004 | ) | - | |||||||||||||||||

| $ | - | $ | - | $ | - | $ | 51,835,741 | $ | (49,582,214 | ) | $ | - | ||||||||||||

(i) Transactions during the year are translated at average exchange rates.

(ii) Balances at year end are translated at the balance sheet exchange rate.

22

Item 2. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

The following discussion and analysis of our financial condition and result of operations contains forward-looking statements and involves numerous risks and uncertainties, including, but not limited to, those described in the "Risk Factors" section of the other reports we file with the Securities and Exchange Commission. Actual results may differ materially from those contained in any forward-looking statements.

The following discussion and analysis of financial condition and results of operations relates to the operations and financial condition reported in the financial statements of Keyuan for the nine months ended September 30, 2012 and 2011 and should be read in conjunction with such financial statements and related notes included in this report and the Company’s Annual Report on Form 10-K for the year ended December 31, 2011.

Overview

Operating through our wholly-owned subsidiaries, Ningbo Keyuan and Ningbo Keyuan Petrochemicals, our operations include (i) a production facility with an annual petrochemical production capacity of 720,000 metric tons (MT) of a variety of petrochemical products, (ii) facilities for the storage and loading of raw materials and finished goods and (iii) a manufacturing technology that can support our manufacturing process with relatively low raw material costs and high utilization and yields, all of which are led by a management team consisting of petrochemical experts with proven track records from some of China’s largest state-owned enterprises in the petrochemical industry.

In order to facilitate the Company’s future growth, Ningbo Keyuan Petrochemicals, Ltd. was incorporated in Ningbo, China with a registered capital of $3 million as a wholly-owned subsidiary of Keyuan Group Limitd (the Hong Kong entity) on August 27, 2010. Ningbo Keyuan Petrochemicals is responsible for the sales and marketing, raw materials sourcing and market analysis for the Company. Dr. Jingtao Ma was appointed as the General Manager of the new entity. Dr. Ma was the head of the former sales and marketing division at Keyuan. This new entity will also serve as the “market thermometer” that can better monitor market conditions and obtain first hand market data through buying and selling activities. Management believes that the consolidation of the sales and marketing and raw material procurement function under one business unit will help efficiently manage the future expansion of the Company. In addition, on December 2, 2011, Mr. Jingtao Ma was appointed as the new General Manager of Ningbo Keyuan, replacing Mr. Chunfeng Tao so that Mr. Tao can focus on the overall development and strategy of the Company.

In order to optimize the Company’s expansion projects, Guangxi Keyuan New Materials Co., Ltd was incorporated on April 4, 2012 in Guangxi province, China as the base for developing the Guangxi Project. Ningbo Keyuan Synthetic Rubbers Co., Limited was incorporated on June 15, 2012 as a foreign owned enterprise to engage in the sales and marketing of various petrochemical products, specifically synthetic rubbers.

On October 15, 2012, Keyuan International Group Limited changed its name to Sinotech Group Limited.

23

Our organization chart is as follows:

In April 2011, we expanded our annual production capacity from 550,000 MT to 720,000 MT. We completed the construction of a Styrene-Butadience-Styrene (the “SBS”) production facility with an annual production capacity of 70,000 MT in September 2011. One SBS production line began commercial production in December 2011 and the second line began commercial production in August, 2012. In addition, we had originally planned to add additional storage capacity and to complete a raw material pre-treatment facility and an asphalt production facility by the end of 2012. However, due to the recent developments in market conditions, management is currently re-evaluating the effectiveness and feasibility of the entire manufacturing capacity expansion strategy considering the long-term development and the industry environment and the completion timetable was temporarily adjusted to the end of June 3013 until evaluation results become available.

In January 2012, we signed a cooperation agreement with Fangchenggang City to build a new petrochemicals production facility in Guangxi Keyuan New Materials Industrial Park, in Guangxi Province. The total investment amount to construct this new production facility is RMB 12.8 billion (approximately USD $2.02 billion). We commenced pre-construction activities including but not limited to applying for the governmental approvals and licenses in February 2012 and expect to complete the pre-construction preparations by the end of 2012, and intend to finish the initial stage of construction and begin operations by the end of 2013. However, the timeline is subject to revision pending the status of project financing. This new production facility, as a part of our expansion plan, will improve our competitive position by extending and expanding our supply chain and manufacturing base. Once the facility is fully operational, it is expected to have annual production capacity of 400,000 metric tons of Acrylonitrile Butadiene Styrene (the “ABS”). We plan to fund the construction and operation of the new production facility through outside financing. If such financing is not available on terms acceptable to us, construction of this facility will be delayed until appropriate financing is available. According to the cooperation agreement, the government of Fangchenggang City will be responsible to provide land use rights for the facility.

In the first nine months of 2012, the extreme fluctuation in international oil prices has caused substantial negative impact on the petrochemical industry, including us. To address this issue, we engaged with research institutes in Shanghai and Zhejiang province to study the possibility and feasibility of diversifying our products, developing high value-added products and improving our production efficiency so that we can have a more stable long-term development plan, to optimize product structures, and to reduce the adverse effects of oil price fluctuations and the general economic environment. Currently, the institutes have commenced related research and we anticipate that their research can achieve a result that will improve our anti-risk capability and benefit us in following years.

24

Our Facility and Equipment

Facility

As of September 30, 2012, we have invested a total of approximately $235 million in the construction and improvement of our production facility. Our current production facility encompasses roughly 1.3 million square feet, including 594,000 square feet for production and 19,500 square feet for laboratories and offices. We also acquired an additional 1.2 million square feet of land in August 2010 for our future expansion.