Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

x | | ANNUAL REPORT UNDER SECTION 13 OR 15(D) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2008

o | | TRANSITION REPORT UNDER SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission file number 333-124924

155 East Tropicana, LLC

155 East Tropicana Finance Corp.

(Exact name of registrant as specified in its charter)

Nevada

Nevada | | 20-1363044

20-2546581 |

(State or other jurisdiction of incorporation or organization) | | (I.R.S. Employer Identification No.) |

115 East Tropicana Avenue, Las Vegas, NV 89109

(Address and telephone number of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (702) 597-6076

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | | Name of each exchange on which registered |

None. | | |

Securities registered pursuant to Section 12(g) of the Act:

None.

(Title of each class)

(Title of each class)

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), |

and (2) has been subject to such filing requirements for the past 90 days. | Yes x No o |

|

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements |

incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. | Yes x No o |

| | |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. :

Large accelerated filer o | | Accelerated filer o |

Non-Accelerated filer x | | Smaller reporting company o |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). | Yes o No x |

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day |

of the registrant’s most recently completed second fiscal quarter. | Not Applicable. |

DOCUMENTS INCORPORATED BY REFERENCE

Not applicable.

PART I

ITEM 1. BUSINESS.

Unless the context indicates otherwise, all references to the “Company”, “155”, “we”, “our”, “ours” and “us” refer to 155 East Tropicana, LLC.

Liquidity and Financial Position

For discussion of our liquidity and financial position, please see “Management’s Discussion and Analysis of Financial Condition and Results of Operations-Executive Overview-Liquidity and Financial Position” and Note 2 to the accompanying consolidated financial statements.

Forward-looking Statements

Certain information included herein contains statements that may be considered forward-looking, such as statements relating to projections of future results of operations or financial condition, expectations for our casino, and expectations of the continued availability of capital resources. Any forward-looking statement made by us necessarily is based upon a number of estimates and assumptions that, while considered reasonable by us, is inherently subject to significant business, economic and competitive uncertainties and contingencies, many of which are beyond our control, and are subject to change. Actual results of our operations may vary materially from any forward-looking statement made by us or on our behalf. Forward-looking statements should not be regarded as representation by us or any other person that the forward-looking statements will be achieved. Readers are cautioned not to place undue reliance on any forward-looking statements, which speak only as of the date thereof. We undertake no obligation to publicly release any revisions to such forward-looking statements to reflect events or circumstances after the date hereof. Some of the contingencies and uncertainties to which any forward-looking statement contained herein are subject to include, but are not limited to, those set forth below in the heading “ITEM 1A. Risk Factors.”

Corporate Organization

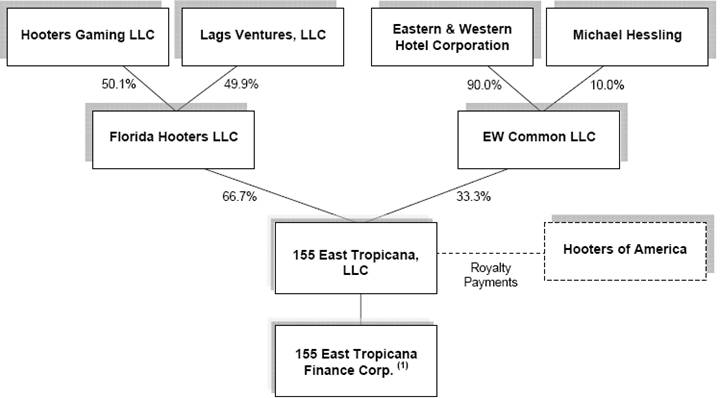

We were formed in June 2004 to acquire the Hôtel San Rémo Casino and Resort (the “Hôtel San Rémo”), a casino hotel located in Las Vegas, Nevada, from Eastern & Western Hotel Corporation (“Eastern & Western”). The Hôtel San Rémo was renovated and re-branded and is now known as Hooters Casino Hotel. Our common membership interests are held two-thirds through Florida Hooters LLC and one-third through EW Common LLC.

Florida Hooters LLC is a joint venture between Hooters Gaming LLC and Lags Ventures, LLC. Hooters Gaming LLC is owned by the holders of licenses to operate Hooters restaurants in the Tampa Bay, Chicago and Manhattan areas as well as for wholesale foods, calendars and Nevada hotel/gaming and includes most of the original founders of the Hooters brand. Lags Ventures, LLC is owned by a holder of the license rights to Hooters restaurants in south Florida. Pursuant to these license rights, the owners of Florida Hooters LLC operate 39 Hooters restaurants, publish Hooters calendars, and operate a Hooters food business. The owner of Lags Ventures, LLC is also the founder of the Dan Marino concept restaurants and owns and operates 2 Dan Marino concept restaurants.

EW Common LLC was formed to hold Eastern & Western’s membership interest in us. Eastern & Western owns 90% of EW Common LLC while our President owns the balance. Eastern & Western is beneficially owned by Sukeaki and Toyoroku Izumi. Eastern & Western and its affiliates owned the Hôtel San Rémo from November 1988 until our acquisition of the hotel casino in August 2004.

2

Table of Contents

Our affiliates have granted us assignments of certain licenses pertaining to the use of the Hooters brand as well as the Dan Marino, “13” Martini Bar and Pete & Shorty’s concept restaurants, solely for the purposes of allowing us to operate a Hooters Casino Hotel located at our property. Pursuant to the Hooters license assignment, we are required to pay the owner of the Hooters trademark, HI Limited Partnership, a royalty fee. For more information, see “Item 1. Business—Intellectual Property” and “Item 13. Certain Relationships and Related Transactions.” Hooters of America, Inc. is the general partner of HI Limited Partnership and we refer to HI Limited Partnership and Hooters of America, Inc. collectively as “Hooters of America.” The original founders of the Hooters brand sold the trademark rights (excluding certain rights they retained for themselves) to Hooters of America in 2001. As a result, Hooters of America is the trademark owner of the Hooters brand and the operator and franchisor of Hooters restaurants. We are not affiliated with Hooters of America.

Before we received our necessary gaming licenses and prior to November 1, 2005, the Hôtel San Rémo was operated by Eastern & Western pursuant to two separate leases with us. These leases were terminated when we received our gaming license. The following chart illustrates our corporate structure:

(1) 155 East Tropicana Finance Corp., which has no assets or operations, was formed for the sole purpose of facilitating the issuance of our 8 ¾ % Senior Secured Notes due 2012.

Asset Purchase Agreement

During 2007, the Company entered into a definitive Asset Purchase Agreement with Hedwigs Las Vegas Top Tier, LLC (“Hedwigs”), an affiliate of the investment group led by NTH Advisory Group,

3

Table of Contents

LLC, and subsequently entered into a first, second and third amendment to the Asset Purchase Agreement (collectively, the “Purchase Agreement”). In connection with the third amendment to the Purchase Agreement, Hedwigs was required to make a $0.5 million payment to the Company on or before June 6, 2008 or the Purchase Agreement automatically terminated. Hedwigs did not make the payment. Accordingly, the Purchase Agreement terminated on June 6, 2008.

Under the terms of the Purchase Agreement, Hedwigs offered to purchase essentially all of the assets of the Company for a purchase price of $98 million in cash, the payment of certain accrued royalties, and the assumption of certain outstanding liabilities of the Company. The Purchase Agreement also provided that Hedwigs would be responsible for the Company’s $130 million in principal amount of 8 ¾% Senior Secured Notes due 2012. In connection with the Purchase Agreement, Hedwigs paid a total of $5.5 million in deposits and extension fees to the Company, which were non-refundable and were fully earned on the dates of payment. The deposits and extension fees were taken to income in June 2008.

Hooters Casino Hotel

We purchased the former Hôtel San Rémo in August 2004 and commenced renovations in March 2005. On February 3, 2006, we opened the Hooters Casino Hotel to the public. Our property is located one-half block east of the intersection of Tropicana Avenue and Las Vegas Boulevard, a major intersection on the Las Vegas strip (“The Strip”) that is within walking distance to approximately 25,000 hotel rooms.

The Hooters Casino Hotel features the famous Hooters décor, and the Hooters brand is a prominent component of the facility. Our renovations have refreshed and upgraded the property, and provided several new restaurant offerings. The Hooters Casino Hotel features:

· an approximately 29,000 square foot “Hooters” themed casino floor with approximately 633 state-of-the-art slot and video poker machines and 28 table games;

· 696 hotel rooms, including 17 suites;

· a tropical pool area featuring beach sand, palm trees, lagoon style waterfall, and Nippers Pool Bar;

· distinctive dining and entertainment options, including:

· a world famous Hooters restaurant containing two hundred seats;

· Dan Marino’s, a restaurant featuring American cuisine which has offered 24 hour dining since October 24, 2007;

· Night Owl Showroom featuring nightly entertainment.

· Porch Dogs, a Caribbean themed casual indoor-outdoor club offering music and cocktails;

· Pete & Shorty’s Tavern, a casual and comfortable bar featuring a sports book and a poker room;

· The Lobby Bar, a 24-hour bar located at the entrance to the casino, featuring service by the world famous Hooters girls.

· Dixie’s Dam Country Bar

· Splurge and Bait Shoppe retail stores selling Hooters branded merchandise.

4

Table of Contents

· SASS, a day spa, salon and workout facility.

The Renovation

The renovation of the Hooters Casino Hotel commenced in March 2005, and the Hooters Casino Hotel opened to the public on February 3, 2006. Our strategy is to build on Hooters’ reputation as a casual, relaxed, fun, and welcoming environment. We believe that Hooters’ strong brand name recognition and our favorable location will generate visitor traffic. The key elements of our renovation of the property are:

Main Entrance. We renovated the main entrance to adopt the Hooters décor of natural wood, tin, and orange. The Hooters brand is a prominent component of the main entrance and we replaced the existing doors with new 12-foot high clear glass doors to make the casino area clearly visible from the outside and the immediate entrance area. We also made improvements to the traffic flow around the entrance areas that we expect will improve pedestrian traffic into the casino. In addition, we added significant new signage to the property, including a large marquee in front of the property. We anticipate that these improvements will result in more walk-in visitors to the casino and our other attractions and amenities.

Casino. We expanded and renovated our casino from approximately 24,000 square feet to approximately 29,000 square feet and designed the casino to be more inviting and to better use the available space, allowing us to add new gaming equipment. We now feature 679 state-of-the-art slot and video poker machines, 30 table games, sports book, and a poker room. To make the casino more inviting, we raised the elevation of the ceiling in some areas for a more open feeling, updated the ceiling with décor of natural wood, tin, and orange, re-carpeted the gaming area with new Hooters-themed carpet and installed wood floor in the surrounding area. In addition, adjacent to the entrance, we added a Hooters bar, serving beer and cocktails to casino guests, and a retail store, selling Hooters branded merchandise.

Dining and Entertainment Options. We offer distinctive dining and entertainment options, including the 200-seat Hooters Restaurant, the 287-seat Dan Marino’s 24-Hour Restaurant, the 100-seat Pete & Shorty’s Tavern, the 200-seat Porch Dogs, and a 350 person occupancy Nippers Pool Bar. The “13” Martini Bar and Dam Restaurant were both closed in 2007 and the Night Owl Showroom and Dixie’s Dam Country Bar opened. To house our new Dan Marino’s restaurant, we built a new building adjacent to the main entrance. The restaurant is visible from both outside and inside the property. In addition, Dan Marino’s restaurant features a bar that serves customers from both the casino floor and the restaurant.

Hotel. We significantly remodeled our hotel rooms. The 696 newly renovated rooms feature a Caribbean/Florida theme and new furniture, carpets, painted textured walls, lighting, art-work and bedspreads. We also renovated the bathrooms with new paint, fixtures, and upgraded amenities. The common hotel areas were updated with new carpet, paint, doors and signage.

Pool Area. We expanded and upgraded the existing pool area to include tropical heated pools with beach sand, palm trees, three in-ground Jacuzzis, lagoon style waterfalls and Nippers Pool Bar.

We spent approximately $53.0 million in cash expenditures for renovations and operating equipment and $10.1 million in pre-opening expenditures in 2005 and 2006. During the renovation, we continued to keep the existing Hôtel San Rémo operations open, although only on a limited basis from late October 2005 until the grand opening of the Hooters Casino Hotel on February 3, 2006.

5

Table of Contents

Competition

We face competition in the market in which we are located as well as in or near any geographic area from which we attract or expect to attract a significant number of our customers. As a result, our casino property faces direct competition from all other casinos and hotels in Las Vegas, NV and to a lesser extent, in the Mesquite, Laughlin, Reno and Lake Tahoe areas of Nevada and in Atlantic City, New Jersey, and in the California gaming market, as well as from other forms of gaming.

Las Vegas, Nevada. The hotel casino industry in Las Vegas is highly competitive. In response to recent economic downturn, many competing properties have significantly reduced their room rates, which has increased competition. The Hooters Casino Hotel competes on the basis of overall atmosphere, range of amenities, level of service, price, location, entertainment offered, theme and size. The Hooters Casino Hotel competes with numerous resorts and hotel casinos on The Strip and in downtown Las Vegas, as well as a large number of hotels and motels in and near Las Vegas. Many competing properties have themes and attractions which draw a significant number of visitors and compete with our property for hotel and gaming customers. Some of these facilities are operated by companies that have more than one operating facility, and many have greater name recognition and financial and marketing resources than us and market to the same target demographic group as we do. Additional major hotel casinos and significant expansion of existing properties, containing a significant number of hotel rooms and attractions, are expected to open in Las Vegas within the coming years. We seek to differentiate the Hooters Casino Hotel from other major Las Vegas hotel casino resorts by concentrating on the design, atmosphere, personal service and amenities that we provide and the added value of the Hooters brand.

California Gaming Market. Voters in California approved an amendment to the California constitution in 2000 that gave Native American tribes in California the right to offer a limited number of slots machines and a range of house-banked card games. A number of Native American tribes have already signed, and others have begun signing, gaming compacts with the State of California. According to the National Indian Gaming Commission, as of February 2009, there are approximately 62 operating tribal casinos in California. In addition, several Native American tribes in California have reached agreements with the State of California that allow for an increased number of gaming machines within the facilities operated by such tribes in exchange for a revenue-based payment to the state. The competitive impact on our gaming establishments from the continued growth of gaming in California cannot be definitively determined but, depending on the nature, extent and location of the growth, the impact could be material.

Other Forms of Gaming. We also compete, to some extent, with other forms of gaming on both a local and national level, including state-sponsored lotteries, Internet gaming, dockside casinos, riverboat casinos, on- and off-track wagering and card parlors. The recent and continued expansion of legalized casino gaming into new jurisdictions throughout the United States has increased competition faced by us and will continue to do so in the future. Additionally, if gaming were legalized or expanded in jurisdictions near any geographic area from which we attract or expect to attract a significant number of our customers, we could face additional competition which could have a significant adverse impact on our business, financial condition and results of operations. There can be no assurance that we will be able to continue to compete successfully in our existing markets or that we will be able to compete successfully against any such future competition.

Intellectual Property

We have entered into an assignment agreement with Florida Hooters, LLC which grants us the right to use certain intellectual property in connection with the operation of the Hooters Casino Hotel. The intellectual property covered by these agreements is described below. Additionally, we have been

6

Table of Contents

granted a royalty-free license to the Pete & Shorty’s mark. For more detailed information, see “Item 13. Certain Relationships and Related Transactions.”

Hooters Trademark. The Hooters trademark and logo insignia are the exclusive property of Hooters of America. We have an exclusive license to use the Hooters brand in connection with gaming, casino or combined hotel, gaming and casino operations solely at the Hooters Casino Hotel property. Florida Hooters, LLC originally obtained the license through an assignment from Hooters Gaming Corporation, an affiliated entity under common ownership with Hooters Gaming LLC. The underlying license agreement was executed between Hooters of America and Hooters Gaming Corporation, and granted to Hooters Gaming Corporation an exclusive license to use the licensed intellectual property in connection with gaming, casino or combined hotel, gaming and casino operations within the State of Nevada. Hooters Gaming Corporation retained any and all rights and obligations in the licensed intellectual property pursuant to the license agreement for all locations within Nevada other than the Hooters Casino Hotel. Under an Affirmation and Acknowledgement agreement between Hooters Gaming Corporation and 155 East Tropicana, LLC, Hooters Gaming Corporation has agreed not to operate (or license or assign its rights to operate) another Hooters Casino Hotel on The Strip, until such time as none of the Notes is outstanding. Additionally, under the agreement, Hooters Gaming Corporation agreed not to operate (or license or assign its rights to operate) another Hooters Casino Hotel in Clark County, Nevada for a period of four years from the issuance of the Notes or such earlier time as none of the Notes is outstanding.

Combined hotel, gaming and casino operations contemplated under the license agreement include, but are not limited to, the right to provide the following within the facility: (i) room service; (ii) restaurant operations; (iii) retail sales facilities in which third parties are permitted to conduct retail sales of all kinds; and (iv) entertainment facilities, subject to certain quality standards. In connection with such operations, we have the right to (i) sell approved merchandise bearing some or all of the licensed intellectual property, (ii) use the licensed intellectual property and Hooters Girls to promote, market, and advertise such facilities worldwide, and (iii) include Hooters Girls as part of any facility staff.

We are required to pay Hooters of America an annual fee equal to $500. In addition, we pay to Hooters of America a royalty in an amount equal to two percent (2%) of all net revenues generated in connection with licensed activities (which includes net revenues generated in connection with hotel, casino, and restaurant operations). We are also required by the license agreement to maintain certain quality standards for the use of the Hooters brand.

Hooters Restaurant Concept. Pursuant to a consent received in 2004 from Las Vegas Wings, Inc., we have the right to use the Hooters restaurant concept at the hotel casino. The consent permits worldwide promotion, marketing and advertising of the hotel casino and its services.

Dan Marino Concept Restaurants. We have an exclusive license to use certain intellectual property to operate and promote restaurants, taverns, lounges and bars using the marks “Dan Marino’s Fine Food & Spirits” and “‘13’ Martini Bar,” which was closed in 2007 and reopened as Night Owl Showroom. Florida Hooters LLC was granted the license from Lags Ventures, Inc., an affiliated entity under common ownership with Lags Ventures, LLC. The initial term of the agreement is 20 years but may be extended for an additional ten years. See “Item 13. Certain Relationships and Related Transactions.”

Pete & Shorty’s. Pete & Shorty’s, Inc. has granted us a nonexclusive, royalty-free license to use the Pete & Shorty’s mark in connection with a restaurant, bar and lounge at the Hooters Casino Hotel. Pursuant to the license agreement, we can also use the mark in connection with affiliated merchandise, entertainment and casino services. However, Pete & Shorty’s, Inc. maintains the right to obtain federal

7

Table of Contents

and/or state registrations for any and all additional services, other than restaurant, bar and cocktail lounge services, which we provide at the Hooters Casino Hotel.

Employees

As of December 31, 2008, we had 874 employees. None of our employees are covered by collective bargaining agreements.

Regulation and Licensing

The ownership and operation of casino gaming facilities in Nevada are subject to the Nevada Gaming Control Act and the regulations promulgated thereunder (“Nevada Act”), and various local regulations. In addition, our gaming operations are subject to the licensing and regulatory control of the Nevada Gaming Commission (“Nevada Commission”), the Nevada State Gaming Control Board (“Nevada Board”), and the Clark County Liquor and Gaming Licensing Board (“CCLGLB” together with the Nevada Commission and the Nevada Board, the “Nevada Gaming Authorities”). We received our license from the Nevada Gaming Authorities as a limited-liability company licensee in October 2005 and are registered with the Nevada Commission as a publicly traded corporation, referred to as a “Registered Corporation”. In addition, Florida Hooters LLC and EW Common LLC are registered with the Nevada Gaming Authorities as intermediary companies and licensed as the members of 155 East Tropicana, LLC. Hooters Gaming LLC, Lags Ventures, LLC, and Eastern & Western are registered with the Nevada Gaming Authorities as holding companies and were found suitable as members of Florida Hooters LLC and EW Common LLC, respectively. Also, Messrs. Lageschulte, DiGiannantonio, Ranieri, Droste, Johnson, Blakely, S. Izumi, T. Izumi and Hessling are individually licensed as our managers. Neil Kiefer, Deborah Pierce and Gary Gregg also hold individual licenses as our officers. Finally, because we pay a percentage of our net profits directly earned from our gaming activities to Hooters Gaming Corporation, it is licensed by the Nevada Gaming Authorities as well.

The laws, regulations and supervisory procedures of the Nevada Gaming Authorities are based upon declarations of public policy which are concerned with, among other things:

· the prevention of unsavory or unsuitable persons from having a direct or indirect involvement with gaming at any time or in any capacity;

· the establishment and maintenance of responsible accounting practices and procedures;

· the maintenance of effective controls over the financial practices of licensees, including the establishment of minimum procedures for internal fiscal affairs and the safeguarding of assets and revenues, providing reliable record keeping and requiring the filing of periodic reports with the Nevada Gaming Authorities;

· the prevention of cheating and fraudulent practices; and

· providing a source of state and local revenues through taxation and licensing fees.

Changes in these laws, regulations and procedures could have an adverse effect on our business, financial condition and results of operations.

Corporations and other entities that operate casinos in Nevada are required to be licensed by the Nevada Gaming Authorities. A gaming license for such activities requires the periodic payment of fees and taxes and is not transferable. As a Registered Corporation, we are required to periodically submit detailed financial and operating reports to the Nevada Commission and to furnish any other information that the Nevada Commission may require.

8

Table of Contents

The Nevada Gaming Authorities may investigate any individual who has a material relationship to or material involvement with us in order to determine whether such individual is suitable or should be licensed as a business associate of a gaming licensee. Our owners, officers, managers and certain key employees are required to be licensed by the Nevada Gaming Authorities. The Nevada Gaming Authorities may deny an application for licensing for any cause that they deem reasonable. A finding of suitability is comparable to licensing, and both require submission of detailed personal and financial information followed by a thorough investigation. Changes in licensed positions must be reported to the Nevada Gaming Authorities and, in addition to their authority to deny an application for a finding of suitability or licensure, the Nevada Gaming Authorities have jurisdiction to disapprove a change in a corporate position.

If the Nevada Gaming Authorities were to find an owner, officer, manager or key employee unsuitable for licensing or unsuitable to continue having a relationship with us, we would have to sever all relationships with that person. In addition, the Nevada Commission may require us to terminate the employment of any person who refuses to file appropriate applications. Determinations of suitability or of questions pertaining to licensing are not subject to judicial review in Nevada.

As licensees, we are required to submit detailed financial and operating reports to the Nevada Commission. Substantially all material loans, leases, sales of securities and similar financing transactions by us must be reported to the Nevada Commission.

If it were determined that we violated the Nevada gaming laws, our gaming licenses and registrations with the Nevada Commission could be limited, conditioned, suspended or revoked, subject to compliance with certain statutory and regulatory procedures. In addition, we and the persons involved could be subject to substantial fines for each separate violation of the Nevada laws at the discretion of the Nevada Commission. Further, the Nevada Commission could appoint a supervisor to operate our gaming properties and, under certain circumstances, earnings generated during the supervisor’s appointment (except for the reasonable rental value of our gaming properties) could be forfeited to the State of Nevada. Limitation, conditioning or suspension of any gaming license or the appointment of a supervisor could (and revocation of any gaming license would) materially adversely affect our operations.

Since we do not intend to register or sell any of our equity securities, every holder of our equity securities is required to be licensed by the Nevada Gaming Authorities. In addition, as 155 East Tropicana, LLC has been licensed by the Nevada Gaming Authorities and has become a Registered Corporation, none of its membership interests can be issued, sold, assigned, transferred, pledged, or otherwise disposed of without the prior approval of the Nevada Board and the Nevada Commission. In addition, the pledge of our equity interests as security for the Notes was approved by the Nevada Board and the Nevada Commission at the time 155 East Tropicana, LLC was licensed by and registered with the Nevada Commission, which was necessary in order for such pledge to remain effective.

If certain exemptions are granted under the Nevada Act to a Registered Corporation, then any person who acquires more than 5% of a Registered Corporation’s voting securities is required to report the acquisition to the Nevada Commission. The Nevada Act requires that beneficial owners of more than 10% of a registered corporation’s voting securities apply to the Nevada Commission for a finding of suitability within 30 days after the Chairman of the Nevada Board mails the written notice requiring the filing for a finding of suitability. Under certain circumstances, an “institutional investor,” as defined in the regulations of the Nevada Commission, which acquires more than 10%, but not more than 15%, of our voting securities may apply to the Nevada Commission for a waiver of such finding of suitability if that institutional investor holds the voting securities for investment purposes only. An institutional investor will not be deemed to hold voting securities for investment purposes unless the voting securities were acquired and are held in the ordinary course of business as an institutional investor and not for the

9

Table of Contents

purpose of causing, directly or indirectly, the election of a majority of the members of our board of managers, any change in our corporate charter, bylaws, management, policies or operations, or any of our gaming affiliates, or any other action which the Nevada Commission finds to be inconsistent with holding our voting securities for investment purposes only. Activities which are not deemed to be inconsistent with holding voting securities for investment purposes only include:

· voting on all matters voted on by stockholders;

· making financial and other inquiries of management of the type normally made by securities analysts for informational purposes and not to cause a change in its management, policies or operations; and

· other activities as the Nevada Commission may determine to be consistent with such investment intent.

If the beneficial holder of voting securities who must be found suitable is a corporation, partnership or trust, it must submit detailed business and financial information including a list of beneficial owners. The applicant is required to pay all costs of investigation.

Under the Nevada Act, under certain circumstances, an institutional investor as defined in the Nevada Act, which intends to acquire not more than 15% of any class of securities of a privately-held corporation, limited partnership or limited-liability company that is also a registered holder or intermediary company of the holder of a gaming license, may apply to the Nevada Commission for a waiver of the usual prior licensing or finding of suitability requirements if such institutional investor holds such securities only for investment purposes. An institutional investor shall not be deemed to hold securities only for investment purposes unless the securities were acquired and are held in the ordinary course of business as an institutional investor, do not give the institutional investor management authority, and do not, directly or indirectly, allow the institutional investor to vote for the election or appointment of members of the board of directors, a general partner or manager, cause any change in the articles of organization, operating agreement, other organic document, management, policies or operations, or cause any other action that the Nevada Commission finds to be inconsistent with holding securities only for investment purposes. Activities that are not deemed to be inconsistent with holding securities only for investment purposes include:

· nominating any candidate for election or appointment to the entity board of directors or equivalent in connection with a debt restructuring;

· making financial and other inquiries of management of the type normally made by securities analysts for informational purposes and not to cause a change in the entity management, policies or operations; and

· such other activities as the Nevada Commission may determine to be consistent with such investment intent.

Any person who fails or refuses to apply for a finding of suitability or a license within 30 days after being ordered to do so by the Nevada Commission or the Chairman of the Nevada Board, may be found unsuitable. The same restrictions apply to a record owner if the record owner, after request, fails to identify the beneficial owner. Any stockholder found unsuitable and who holds, directly or indirectly, any beneficial ownership of the common stock of a registered corporation beyond the period of time as may be prescribed by the Nevada Commission may be guilty of a criminal offense. We may become subject to disciplinary action if, after receipt of notice that a person is unsuitable to be a stockholder or to have any other relationship with us, we:

10

Table of Contents

· pay that person any dividend or interest upon voting securities;

· allow that person to exercise, directly or indirectly, any voting right conferred through securities held by that person;

· pay remuneration in any form to that person for services rendered or otherwise; or

· fail to pursue all lawful efforts to require the unsuitable person to relinquish his voting securities for cash at fair market value.

Additionally, the CCLGLB has taken the position that it has the authority to approve all persons owning or controlling the stock of any corporation controlling a gaming license.

We may be required to disclose to the Nevada Board and the Nevada Commission the identities of all holders of our Notes. The Nevada Commission may, in its discretion, require the holder of any debt security of a Registered Corporation, including our Notes, to file applications, be investigated and be found suitable to own the debt security of a Registered Corporation. If the Nevada Commission determines that a person is unsuitable to own a debt security, then pursuant to the Nevada Act, the Registered Corporation can be sanctioned, including the loss of its approvals, if without the prior approval of the Nevada Commission, it:

· pays to the unsuitable person any dividend, interest, or any distribution whatsoever;

· recognizes any voting right by the unsuitable person in connection with debt securities;

· pays the unsuitable person remuneration in any form; or

· makes any payment to the unsuitable person by way of principal, redemption, conversion, exchange, liquidation or similar transaction.

We are required to maintain a current membership ledger in Nevada, which may be examined by the Nevada Gaming Authorities at any time. If any securities are held in trust by an agent or by a nominee, the record holder may be required to disclose the identity of the beneficial holder to the Nevada Gaming Authorities. A failure to make such disclosure may be grounds for finding the record holder unsuitable. We are also required to render maximum assistance in determining the identity of the beneficial owner. The Nevada Commission has the power to require our securities to bear a legend indicating that the securities are subject to the Nevada Act. However, to date, the Nevada Commission has not imposed such a requirement on us.

We may not make a public offering of securities without the prior approval of the Nevada Commission if the securities or proceeds from the securities are intended to be used to construct, acquire or finance gaming facilities in Nevada, or to retire or extend obligations incurred for the purposes of constructing, acquiring or financing gaming facilities. Furthermore, any approval, if granted, does not constitute a finding, recommendation or approval by the Nevada Commission or the Nevada Board as to the accuracy or adequacy of the prospectus or the investment merits of the securities offered. Any representation to the contrary is unlawful. Pursuant to the Nevada Act, any entity which is not an “affiliated company,” as such term is defined in the Nevada Act, or which is not otherwise subject to the provisions of the Nevada Act, including us, which plans to make a public offering of securities intending to use such securities or the proceeds from the sale thereof for the construction or operation of gaming facilities in Nevada, or to retire or extend obligations incurred for such purposes, may apply to the Nevada Commission for prior approval of such public offering. The Nevada Commission may find an applicant unsuitable based solely on the fact that it did not submit such an application, unless upon a written request for a ruling, the Chairman of the Nevada Board has ruled that it is not necessary to submit such an application.

11

Table of Contents

Changes in control of a Registered Corporation through merger, consolidation, stock or asset acquisitions, management or consulting agreements, or any act or conduct by a person whereby that person obtains control (including foreclosure on pledged shares), may not occur without the prior approval of the Nevada Commission. Entities seeking to acquire control or ownership of a Registered Corporation must satisfy the Nevada Board and Nevada Commission in a variety of stringent standards prior to assuming control of such Registered Corporation. The Nevada Commission may also require the stockholders, officers, managers and other persons having a material relationship or involvement with the entity proposing to acquire control, to be investigated and licensed as part of the approval process relating to the transaction.

The Nevada legislature has declared that some corporate acquisitions opposed by management, repurchases of voting securities and corporate defense tactics affecting Nevada gaming licensees, and Registered Corporations that are affiliated with those operations, may be injurious to stable and productive corporate gaming. The Nevada Commission has established a regulatory scheme to ameliorate the potentially adverse effects of these business practices upon Nevada’s gaming industry and to further Nevada’s policy to:

· assure the financial stability of corporate gaming operators and their affiliates;

· preserve the beneficial aspects of conducting business in the corporate form; and

· promote a neutral environment for the orderly governance of corporate affairs.

Approvals are, in certain circumstances, required from the Nevada Commission before we can make exceptional repurchases of voting securities above the current market price thereof and before a corporate acquisition opposed by management can be consummated. The Nevada Act also requires prior approval of a plan of recapitalization proposed by the board of directors in response to a tender offer made directly to the Registered Corporation’s owners for the purposes of acquiring control of the Registered Corporation.

License fees and taxes, computed in various ways depending on the type of gaming or activity involved, are payable to the State of Nevada and to the counties and cities in which the Nevada licensee’s respective operations are conducted. Depending upon the particular fee or tax involved, these fees and taxes are payable monthly, quarterly or annually and are based upon either:

· a percentage of the gross revenues received;

· the number of gaming devices operated; or

· the number of table games operated.

Any person who is licensed, required to be licensed, registered, required to be registered, or is under common control with such persons, or “licensees,” and who is or who proposes to become involved in a gaming venture outside of Nevada, is required to deposit with the Nevada Board, and thereafter maintain, a revolving fund in the amount of $10,000 to pay the expenses of investigation by the Nevada Board of the licensees’ participation in foreign gaming. The revolving fund is subject to increase or decrease in the discretion of the Nevada Commission. Thereafter, licensees are also required to comply with certain reporting requirements imposed by the Nevada Act. Licensees are also subject to disciplinary action by the Nevada Commission if they knowingly violate any laws of the foreign jurisdiction pertaining to a foreign gaming operation, fail to conduct the foreign gaming operation in accordance with the standards of honesty and integrity required of Nevada gaming operations, engage in activities or enter into associations that are harmful to the State of Nevada or its ability to collect gaming

12

Table of Contents

taxes and fees, or employ, contract with or associate with a person in the foreign operation who has been denied a license or a finding of suitability in Nevada on the ground of personal unsuitability.

Potential Changes in Tax and Regulatory Requirements

In the past, federal and state legislators and officials have proposed changes in tax law, or in the administration of the laws, affecting the gaming industry. Regulatory commissions and state legislatures sometimes consider limitations on the expansion of gaming in jurisdictions where we operate and other changes in gaming laws and regulations. Proposals at the national level have included a federal gaming tax and limitations on the federal income tax deductibility of the cost of furnishing complimentary promotional items to customers, as well as various measures which would require withholding on amounts won by customers or on negotiated discounts provided to customers on amounts owed to gaming companies. It is not possible to determine with certainty the likelihood of possible changes in tax or other laws or in the administration of the laws. The changes, if adopted, could have a material adverse effect on our financial results.

Compliance with Other Laws and Regulations

In addition to the regulations described above, our operations are also subject to extensive state and local laws, regulations and ordinances that apply to non-gaming businesses generally, and, on a periodic basis, we must obtain various other licenses and permits, including those required to sell alcoholic beverages. We have not incurred, and do not expect to incur, material expenditures with respect to these laws and regulations. There can be no assurances, however, that we will not incur material liability under these laws and regulations in the future. See also “Item 1A. Risk Factors—Risks Related to Our Business—Governmental Regulations” and “—Factors Beyond Our Control.”

ITEM 1A. RISK FACTORS.

The following risks, if any one or more occurs, could materially harm our business, financial condition or future results of operations.

Risks Related to Our Business

Going Concern—There is substantial doubt about our ability to continue as a going concern.

Uncertainties related to (1) our ability to meet our payment obligations under the Notes and our other indebtedness and (2) our reoccurring losses raise a substantial doubt about our ability to continue as a going concern. The accompanying consolidated financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets or the amounts and classifications of liabilities that may result should we be unable to continue as a going concern. As a result, the report of our independent registered public accounting firm on our consolidated financial statements for the year ended December 31, 2008 contains an explanatory paragraph with respect to our ability to continue as a going concern. We can provide no assurance that we will be able to secure a waiver or amendment related to potential noncompliance under the Notes or the Credit Facility in such a way as to be able to continue as a going concern.

Recent Economic Developments — Recent instability in the financial markets may continue to impact our business.

Recently, the residential real estate market in Las Vegas and the U.S. has experienced a significant downturn due to declining real estate values, substantially reducing mortgage loan originations and

13

Table of Contents

securitizations, and precipitating more generalized credit market dislocations and a significant contraction in available liquidity globally. These factors, combined with fluctuating oil prices, declining business and consumer confidence and increased unemployment, have precipitated an economic recession. Individual consumers are experiencing higher delinquency rates on various consumer loans and defaults on indebtedness of all kinds have increased. Further declines in real estate values in Las Vegas and the U.S. or elsewhere and continuing credit and liquidity concerns could have an adverse affect on our results of operations and are likely to continue until such time as these aforementioned conditions improve.

Dependence Upon Cash Flow of Property—With our Credit Facility fully drawn, our cash flow to meet our payment obligations under the Notes and our other indebtedness and to fund our operations is dependent solely on the hotel casino.

Currently our Credit Facility is fully extended and we have no additional availability to borrow against the Credit Facility. As a result, we now rely exclusively on cash flow generated by the hotel casino to meet our payment obligations under the Notes and our other indebtedness and to fund our operations and planned or committed capital expenditures, including any renovation of our existing property. If adverse regional and national economic conditions persist, worsen, or fail to improve significantly, we could experience decreased revenues from our operations attributable to decreases in consumer spending levels and could fail to generate sufficient cash to fund our liquidity needs or fail to meet our payment obligations under the Notes for future interest payments and our other indebtedness. We cannot provide assurance that our business will generate sufficient cash flow from operations to enable us to pay our indebtedness or to fund our other liquidity needs. See “Item 1A. Risk Factors—Risks Related to the Notes and Other Company Debt—Ability to Service Debt.”

Sensitivity to Consumer Spending—Our business is particularly sensitive to reductions in discretionary consumer spending as a result of downturns in the economy.

Consumer demand for casino hotel properties, such as ours, are particularly sensitive to downturns in the economy and the corresponding impact on discretionary spending on leisure activities. Changes in discretionary consumer spending or consumer preferences brought about by factors such as perceived or actual general economic conditions, the current housing crisis and the credit crisis, the impact of high energy and food costs, the increased cost of travel, the potential for continued bank failures, perceived or actual disposable consumer income and wealth, effects of the current recession and changes in consumer confidence in the economy, or fears of war and future acts of terrorism could further reduce customer demand for the amenities that we offer, thus imposing practical limits on pricing and harming our operations.

Domestic and International Events — Our business may be adversely impacted by domestic and international events.

The terrorist attacks that took place in the United States on September 11, 2001, were unprecedented events that created economic and business uncertainties, especially for the travel and tourism industry. The potential for future terrorist attacks, the national and international responses, and other acts of war or hostility, including the ongoing conflicts in Iraq and Afghanistan, have created economic and political uncertainties that could materially adversely affect our business, results of operations and financial condition in ways we cannot predict.

Gaming Taxes and Fees — If the State of Nevada or Clark County increases gaming taxes and fees, our results of operations could be adversely affected.

14

Table of Contents

State and local authorities raise a significant amount of revenue through taxes and fees on gaming activities. From time to time, legislators and officials have proposed changes in tax laws, or in the administration of such laws, affecting the gaming industry. In addition, worsening economic conditions could intensify the efforts of state and local governments to raise revenues through increases in gaming taxes. If the State of Nevada or Clark County, Nevada were to increase gaming taxes and fees, our results of operations could be adversely affected. There are several gaming tax increase proposals currently circulating in Nevada. One such proposal, a 3% increase in the room tax, was recently approved by Nevada legislature. These proposals would take the form of voter referendum. If successfully implemented, such an increase would have a material adverse effect on our financial condition, results of operations or cash flows.

License Agreement—We are required to pay numerous royalty and other fees to the licensors, some of whom are our affiliates, for the right to use certain intellectual property.

The Hooters trademark and logo insignia are the exclusive property of Hooters of America. Pursuant to certain licenses and an assignment of those license rights to us, we have a royalty-bearing license to use certain intellectual property related to the Hooters brand solely for purposes of the operation of a Hooters Casino Hotel located at our property. Our operation of the Hooters Casino Hotel is conditioned on payment of certain royalty fees to Hooters of America and some of our affiliates based on percentages of revenues and sales generated by our gaming and restaurant activities, as described under “Item 1. Business—Intellectual Property” and “Item 13. Certain Relationships and Related Transactions,” and satisfaction of other conditions under the license. Failure to satisfy the conditions could result in termination of the license. Furthermore, in a bankruptcy of a licensor, the bankruptcy court could conclude that the trademark license agreements are executory contracts and, subject to certain legal requirements, may approve rejection of the license agreements. Although we would take the position that our license agreement with Hooters of America is perpetual and not an executory contract, there can be no assurance that a bankruptcy court would so conclude in a bankruptcy of Hooters of America. Rejection would give rise to a claim for damages for breach of the license and might prevent us from continuing to use the trademark or on the same terms. The loss of our license rights could prevent us from operating as the Hooters Casino Hotel, which would have a material adverse effect on our business, financial condition and results of operations.

Use of Hooters Brand—Use of the Hooters brand by entities other than us, including in Las Vegas and other areas of Nevada, could adversely affect our business, financial condition and results of operations.

We believe we benefit from the name recognition and reputation generated by the Hooters restaurants that are operated worldwide. We have the right to use the Hooters brand and certain related intellectual property solely for purposes of the Hooters Casino Hotel. Hooters Gaming Corporation, an affiliate under common ownership with Hooters Gaming LLC, is the sole owner of the right to use the Hooters brand in connection with the conduct of gaming and the operation of hotels elsewhere in the state of Nevada. Hooters Gaming Corporation has agreed not to operate (or license or assign its rights to operate) another Hooters Casino Hotel on The Strip until our Notes are no longer outstanding. Additionally, Hooters Gaming Corporation has agreed not to operate (or license or assign its rights to operate) another Hooters Casino Hotel in Clark County, Nevada for a period of four years from the issuance of our Notes or such earlier time as none of our Notes are outstanding. However, Hooters Gaming Corporation or its assignee can exploit the Hooters brand and logo in connection with hotel casinos and casinos in other areas of Nevada and elsewhere, including marketing worldwide, and once the Notes are no longer outstanding, on The Strip. For example, other Hooters Casino Hotels could be opened in areas (other than The Strip) in Las Vegas and Nevada and throughout the world where gaming

15

Table of Contents

operations are permitted. We cannot assure that the development of other hotel casinos, casinos or restaurants using the Hooters brand in Nevada or elsewhere will not adversely affect our business, financial condition and results of operations. Nor can we assure that our business, financial condition and results of operations will not be adversely affected by the management of the Hooters brand or any negative public image or other adverse event that becomes associated with the Hooters brand.

Licensing—We are required to maintain gaming, liquor and other licenses to operate the Hooters Casino Hotel. The gaming industry is highly regulated.

Our operation of the Hooters Casino Hotel is contingent upon the maintenance of various regulatory licenses, permits, approvals, registrations, findings of suitability, orders and authorizations. The laws, regulations, and ordinances requiring these licenses, permits and other approvals generally relate to the responsibility, financial suitability and character of the owners and managers of our gaming operations, as well as persons financially interested or involved in our gaming operations, almost all of whom had never been licensed previously. The scope of the approvals required to operate a facility were extensive. Failure to maintain the necessary approvals could adversely affect our ability to operate the Hooters Casino Hotel. See “Item 1. Business—Regulation and Licensing.”

Risk of a New Venture—We have a limited operating history or history of earnings as the Hooters Casino Hotel.

We were formed to acquire, operate, renovate and re-brand the Hôtel San Rémo. While the Hôtel San Rémo has a history of operations and a history of earnings, our operating history is limited. Moreover, our hotel/casino is identified by the Hooters brand which has not been associated with other hotels or casinos. Consequently, we cannot be certain that we will ultimately attract the number and type of hotel and casino customers and other visitors we desire to achieve our objective of improving the profitability of the hotel casino.

We are subject to significant business, economic, regulatory and competitive uncertainties frequently encountered by new businesses in competitive environments, many of which are beyond our control. Because we have a limited operating history, it may be more difficult for us to prepare for and respond to these types of risks, and the other types of risks described herein, as compared with an established business. Our business prospects should be evaluated in light of the difficulties frequently encountered by companies in the early stages of gaming projects and the risks inherent in the establishment of a new business enterprise. There can be no assurance that we will be able to successfully operate the hotel casino or manage these risks successfully, that the hotel casino will be profitable or that we will generate sufficient cash flow to meet our payment obligations under the Notes and our other indebtedness, which would in turn negatively affect our business, financial condition and results of operations.

Competition—We are subject to intense local competition as well as competition in the gaming industry that could hinder our ability to operate profitably.

Competition in Las Vegas has increased over the last several years as a result of significant increases in hotel rooms, casino sizes and convention, trade show and meeting facilities. In response to the recent economic downturn, many competing properties have significantly reduced their room rates, which has increased competition. Our success is dependent upon the success of the hotel casino and its continuing ability to attract visitors and operate profitably. The hotel casino, located one-half block east of The Strip, competes with high-quality Las Vegas resorts and other Las Vegas hotel casinos, including those located on The Strip and in downtown Las Vegas, on the basis of overall atmosphere, range of amenities, level of service, price, location, entertainment offered, theme and size. Currently, there are

16

Table of Contents

approximately 37 major gaming properties located on or near The Strip, 13 additional major gaming properties in the downtown area and additional gaming properties located in other areas of Las Vegas. Some of these facilities are operated by companies that have more than one operating facility, and many have greater name recognition and financial and marketing resources than us and market to the same target demographic group as we do. Furthermore, additional major hotel casinos and significant expansion of existing properties, containing a significant number of hotel rooms and attractions, are expected to open in Las Vegas within the coming years. There can be no assurance that the Las Vegas market will continue to grow or that hotel casino resorts will continue to be popular. A decline or leveling off of the growth or popularity of such facilities would adversely affect our business, financial condition and results of operations. See “Item 1. Business—Competition.”

There also is substantial competition among gaming companies in the gaming industry generally, which includes land-based casinos, dockside casinos, riverboat casinos, casinos located on Native American land, including in California, and other forms of legalized gambling. If other casinos operate more successfully, if existing properties are enhanced or expanded, or if additional hotels and casinos are established in and around the locations where we conduct business, we may lose market share. We also compete, to some extent, with other forms of gaming on both a local and national level, including state-sponsored lotteries, Internet gaming, on- and off-track wagering and card parlors. In particular, the legalization of gaming or the expansion of legalized gaming in or near any geographic area from which we attract or expect to attract a significant number of our customers could have a significant adverse effect on our business, financial condition and results of operations.

Increased competition may also require us to make substantial capital expenditures to maintain and enhance the competitive position of our hotel casino. Because we are highly leveraged, after satisfying our obligations under our outstanding indebtedness, there can be no assurance that we will have sufficient financing to make such expenditures. If we are unable to make such expenditures, our competitive position and our results of operations could be materially adversely affected.

Governmental Regulations—We face extensive regulation from gaming and other government authorities.

As owners and operators of gaming facilities, we are subject to extensive Nevada state and local regulation. Nevada state and local government authorities require us and our subsidiaries to maintain gaming licenses and require our officers and key employees to demonstrate suitability to hold gaming licenses. The Nevada state and local government may limit, condition, suspend or revoke a license for any cause deemed reasonable by the respective licensing agency. They may also levy substantial fines against us or the individuals involved in violating gaming laws or regulations. The occurrence of any of these events could have a material adverse effect on our business, financial condition and results of operations.

No assurances can be given that any new licenses, registrations, findings of suitability, permits and approvals, including for any proposed expansion of our hotel casino, will be renewed when they expire. Any failure to renew or maintain our licenses or receive new licenses when necessary would have a material adverse effect on us.

We are subject to a variety of other rules and regulations, including zoning, environmental, construction and land-use laws and regulations governing the serving of alcoholic beverages. We also pay substantial taxes and fees in connection with our operations as a gaming company, which taxes and fees are subject to increase or other change at any time. Any changes to these laws could have a material adverse effect on our business, financial condition and results of operations.

17

Table of Contents

The compliance costs associated with these laws, regulations and licenses are significant. A change in the laws, regulations and licenses applicable to our business or a violation of any current or future laws or regulations or our gaming licenses could require us to make material expenditures or could otherwise materially adversely affect our business, financial condition or results of operations. For more detailed information, see “Item 1. Business—Regulation and Licensing.”

Union Efforts to Organize Employees—Our business, financial condition, and results of operations may be harmed by union efforts to organize our employees.

Our employees were not covered by collective bargaining agreements as of December 31, 2008. All 22 employees in our engineering department voted on March 9, 2007 to be represented by Operating Engineers Local #501 and Teamsters #995 jointly in collective bargaining. However, they voted to terminate that election in April of 2008.

Unionization of our employees could result in disruption in our business and could incur significant costs, both of which could have a material adverse effect on our results of operation and financial condition. We could experience significant increases in our labor costs which could also have a material adverse effect on our business, financial condition, and results of operations.

Possible Conflicts of Interest—The relationship of our chief executive officer to Hooters Inc. and related entities creates potential for conflicts of interest.

Neil Kiefer, our chief executive officer is the President, Chief Executive Officer and director of Hooters Inc. and related entities, which are based in Florida, and some of which may have interests adverse to us. Due to Mr. Kiefer’s responsibilities to serve both companies, there is potential for conflicts of interest. At any particular time, the needs of Hooters Inc. could cause Mr. Kiefer to devote attention to Hooters Inc. at the expense of devoting attention to us. In addition, matters may arise that place Mr. Kiefer in conflicting positions. No assurance can be given that material conflicts will not arise which could be detrimental to our business, financial condition and results of operations.

Factors Beyond Our Control—Our business, financial condition and results of operations are dependent in part on a number of factors that are beyond our control.

The economic health of our business is generally affected by a number of factors that are beyond our control, including:

· continued increases in healthcare costs;

· general economic conditions and economic conditions specific to our primary markets;

· inaccessibility to our property due to construction on adjoining or nearby properties, streets or walkways;

· levels of disposable income of casino customers;

· increased transportation costs;

· local conditions in key gaming markets, including seasonal and weather-related factors;

· increase in gaming taxes or fees;

· decline in tourism and travel due to occurrences or threats of terrorism or other destabilizing events;

· substantial increase in the cost of electricity, natural gas and other forms of energy;

18

Table of Contents

· competitive conditions in the gaming industry, including the effect of such conditions on the pricing of our games and products;

· the relative popularity of entertainment alternatives to casino gaming that compete for the leisure dollar;

· the adoption of anti-smoking regulations; and

· an outbreak or suspicion of an outbreak of an infectious communicable disease.

Any of these factors could negatively impact our property or geographic location in particular or the casino industry generally, and as a result, our business, financial condition and results of operations.

Environmental Matters—We are subject to environmental laws and potential exposure to environmental liabilities. This may cause us to incur costs or affect our ability to develop, sell or rent our property or to borrow money using such property as collateral.

We are subject to various federal, state and local environmental laws, ordinances and regulations, including those governing discharges to air and water, the generation, handling, management and disposal of petroleum products, asbestos containing materials and other hazardous substances, and the health and safety of our employees. Permits may be required for our operations and these permits are subject to renewal, modification and, in certain cases, revocation. In addition, as a property owner and operator, we may be liable for the costs of investigating and remediating these substances or products on, under or in our property, without regard to whether we knew of, or caused, the presence of the contaminants, and regardless of whether the practices that resulted in the contamination were legal at the time they occurred. The presence of, or failure to remediate properly, the substances may adversely affect our ability to sell or lease our property or to borrow funds using it as collateral. Additionally, we may be subject to claims by third parties based on damages and costs resulting from environmental contamination emanating from our property.

We have not identified any such issues associated with our property that could reasonably be expected to have an adverse effect on us or the results of our operations. However, it is possible that historical or neighboring activities have affected our property and, as a result, there can be no assurance that material obligations or liabilities under environmental laws will not arise in the future which may have a material adverse effect on us. Moreover, it is also possible that future developments could lead to material environmental compliance costs or other liabilities for us and that these costs could have a material adverse effect on our business and financial condition.

Uninsured Losses—We may incur losses that are not adequately covered by insurance which may harm our financial condition and results of operations.

Although we maintain insurance that we believe is customary and appropriate for our business, we cannot assure you that insurance will be available or adequate to cover all loss and damage to which our business and our assets might be subjected. In connection with insurance renewals subsequent to the terrorist events of September 11, 2001, the insurance coverage for certain types of damages or occurrences have been diminished substantially and is unavailable at commercial rates. The lack of adequate insurance for certain types or levels of risk could expose us to significant losses in the event that a catastrophe or lawsuit occurred for which we are underinsured. Any losses we incur that are not adequately covered by insurance may decrease our future operating income, require us to find a replacement for or repair destroyed property and reduce the funds available for payment of our obligations on the Notes and our other indebtedness.

19

Table of Contents

Risks Related to the Notes and Other Company Debt

Substantial debt- our substantial level of debt could adversely affect our finanacial condition and prevent us from fulfilling our obligations under the Notes and our other debt.

We have substantial debt. Our substantial level of debt could adversely affect our financial condition and prevent us from fulfilling our obligations under the Notes and our other debt. As of December 31, 2008, we have total debt of $141.4 million and $144.8 at March 3, 2009. Due to economic conditions and our results of operations, we will not be able to make our scheduled interest payment on our Notes on April 1, 2009. If we are unable to make the interest payment within the 30-day grace period, an event of default will exist. A default under the indenture governing our Notes permits the lenders under our Credit Facility to declare a default under the Credit Agreement. See “Risks Related to the Notes and Other Company Debt” regarding limitations on collateral and ability to exercise remedies. Our substantial debt could have important consequences and significant effects on our business. For example, it could:

· make it more difficult for us to satisfy our obligations under the Notes and our other debt;

· result in an event of default if we fail to satisfy our obligations under the Notes or our other debt or fail to comply with the financial and other restrictive covenants contained in the indenture governing the Notes or our Credit Facility, which event of default could result in all of our debt becoming immediately due and payable and could permit our lenders to foreclose on our assets securing such debt;

· require us to dedicate a substantial portion of our cash flow from our business operations to pay our debt, thereby reducing the availability of cash flow to fund working capital, capital expenditures, development projects, general operational requirements and other purposes;

· limit our ability to obtain additional financing for working capital, capital expenditures and other activities;

· limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate;

· increase our vulnerability to general adverse economic and industry conditions or a downturn in our business; and

· place us at a competitive disadvantage compared to competitors that are not as highly leveraged.

Any of the above-listed factors could have a material adverse effect on our business, financial condition and results of operations and our ability to meet our payment obligations under the Notes and our other debt.

Ability to Service Debt—To service our debt, we will require a significant amount of cash. Based on current operations we are currently unable to service our Notes.

With our Credit Agreement fully extended, we will rely exclusively on funds generated from our operations to pay our expenses and to pay the amounts due under the Notes, our Credit Facility and our other debt. Due to our current cash and anticipated cash flow from operations, we will not make the $5.7 million interest payment due on April 1, 2009. if we are unable to make this interest payment within the 30-day grace period, an event of default under our indenture will occur and a default under our indenture will also be a default under our Credit Agreement. Our ability to meet our expenses and pay additional amounts due under the Notes and other debt will depend on our future performance, which will be

20

Table of Contents

affected by financial, business, economic and other factors, many of which we cannot control. If adverse regional and national economic conditions persist, worsen, or fail to improve significantly, we could experience decreased revenues from our operations attributable to decreases in consumer spending levels and could fail to generate sufficient cash to pay additional amounts due under our debt, including the Notes, or to fund other liquidity needs, such as future capital expenditures. If recent economic conditions, including the availability of credit, persist, worsen, or fail to improve significantly, we also may be unable to refinance all or part of our debt, sell assets, reduce or delay capital expenditures or borrow more money. In addition, the terms of existing or future debt agreements, including our Credit Facility and the indenture governing the Notes, may restrict us from adopting any of these alternatives.

Limitations on Collateral—The collateral securing the Notes does not include any of our gaming assets or certain other excluded assets.

The Notes and any subsidiary guarantees thereof are secured by a security interest in substantially all of our and any subsidiary guarantors’ existing and future assets (other than certain excluded assets), a pledge of our equity interests and the equity interests in any subsidiary guarantors. As of December 31, 2008, there are no subsidiary guarantors. The collateral does not include gaming licenses or any gaming equipment or other assets securing furniture, fixtures and equipment financing, and there are no restrictions on the amount of gaming equipment financed in this manner. The collateral also does not include contracts, agreements, licenses (including gaming and liquor licenses) and other rights that by their express terms prohibit the assignment thereof or the grant of a security interest therein. Some of these may be material to us and such exclusion could have a material adverse effect on the value of the collateral.

Value of Collateral Securing the Notes—The fair market value of the collateral securing the Notes may not be sufficient to pay the amounts owed under the Notes.

The proceeds of any sale of collateral following an event of default with respect to the Notes may not be sufficient to satisfy, and may be substantially less than, amounts due on the Notes. No appraisal has been made of the collateral. The total value of the collateral is likely less than the amount due on the Notes.

The value of the collateral in the event of liquidation will depend upon market and economic conditions, the availability of buyers and similar factors. By its nature, some or all of the collateral may not have a readily ascertainable market value or may not be saleable or, if saleable, there may be substantial delays in its liquidation. To the extent that liens, security interests and other rights granted to other parties (including the lenders under our Credit Facility) encumber assets owned by us, those parties have or may exercise rights and remedies with respect to the property subject to their liens that could adversely affect the value of that collateral and the ability of the trustee under the indenture governing the Notes or the holders of the Notes to realize or foreclose on that collateral. Consequently, we cannot give assurance that liquidating the collateral securing the Notes would produce proceeds in an amount sufficient to pay any amounts due under the Notes after also satisfying the obligations to pay any creditors with prior claims on the collateral.

In addition, under the intercreditor agreement between the trustees under the indenture governing the Notes and the lenders under our Credit Facility, the right of the lenders to exercise remedies with respect to the collateral could delay liquidation of the collateral. The gaming licensing process, along with bankruptcy laws and other laws relating to foreclosure and sale, as discussed below, also could substantially delay or prevent the ability of the trustee or any holder of the Notes to obtain the benefit of

21

Table of Contents

any collateral securing the Notes. Such delays could have a material adverse effect on the value of the collateral.

The indenture governing the Notes also permits us to designate one or more of our restricted subsidiaries as an unrestricted subsidiary. If we designate a restricted subsidiary as an unrestricted subsidiary, all of the liens on any collateral owned by the unrestricted subsidiary or any of its subsidiaries and any guarantees of the Notes by the unrestricted subsidiary or any of its subsidiaries will be released under the indenture but not necessarily under our Credit Facility. Designation of an unrestricted subsidiary will reduce the aggregate value of the collateral securing the Notes to the extent that liens on the assets of the unrestricted subsidiary and its subsidiaries are released. In addition, the creditors of the unrestricted subsidiary and its subsidiaries will have a prior claim (ahead of the Notes) on the assets of such unrestricted subsidiary and its subsidiaries.

If the proceeds of any sale of collateral are not sufficient to repay all amounts due on the Notes, the holders of the Notes (to the extent not repaid from the proceeds of the sale of the collateral), would have only an unsecured claim against our remaining assets.