Use these links to rapidly review the document

TABLE OF CONTENTS

TABLE OF CONTENTS 2

As filed with the Securities and Exchange Commission on November 14, 2013

Registration No. 333-191689

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 3

to

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Xencor, Inc.

(Exact Name of Registrant as Specified in Its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) | 2834 (Primary Standard Industrial Classification Code Number) | 20-1622502 (I.R.S. Employer Identification Number) |

111 West Lemon Avenue

Monrovia, California 91016

(626) 305-5900

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices)

Bassil I. Dahiyat, Ph.D.

President and Chief Executive Officer

Xencor, Inc.

111 West Lemon Avenue

Monrovia, California 91016

(626) 305-5900

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent for Service)

| Copies to: | ||

Thomas A. Coll, Esq. Kenneth J. Rollins, Esq. Cooley LLP 1333 2nd Street, Suite 400 Santa Monica, California 90401 (310) 883-6400 | Bruce K. Dallas, Esq. Davis Polk & Wardwell LLP 1600 El Camino Real Menlo Park, California 94025 (650) 752-2000 | |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, as amended (the "Securities Act"), check the following box. o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of "large accelerated filer," "accelerated filer" and "smaller reporting company" in Rule 12b-2 of the Exchange Act.

| Large accelerated filer o | Accelerated filer o | Non-accelerated filer ý (Do not check if a smaller reporting company) | Smaller reporting company o |

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Amount to be registered(1) | Proposed maximum offering price per share(2) | Proposed maximum aggregate offering price(2) | Amount of registration fee | ||||

|---|---|---|---|---|---|---|---|---|

Common Stock, $0.01 par value per share | 12,305,000 | $7.00 | $86,135,000 | $11,095(3) | ||||

| ||||||||

- (1)

- Includes 1,605,000 shares which the underwriters have the option to purchase from the registrant.

- (2)

- Estimated solely for the purpose of calculating the amount of the registration fee in accordance with Rule 457(a) under the Securities Act. Includes the offering price of shares that the underwriters have the option to purchase to cover over-allotments, if any.

- (3)

- Previously paid.

The Registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

SUBJECT TO COMPLETION DATED NOVEMBER 14, 2013

PRELIMINARY PROSPECTUS

10,700,000 Shares

Common Stock

This is the initial public offering of our common stock. Prior to this offering, there has been no public market for our common stock. The initial public offering price of our common stock is expected to be $7.00 per share.

Our common stock has been approved for listing on the NASDAQ Global Market under the symbol "XNCR."

The underwriters have an option to purchase a maximum of 1,605,000 additional shares of common stock from us.

We are an emerging growth company as that term is used in the Jumpstart Our Business Startups Act of 2012, and, as such, we have elected to comply with certain reduced public company reporting requirements for this prospectus and future filings.

Investing in our common stock involves a high degree of risk. See "Risk Factors" beginning on page 11.

| | Price to Public | Underwriting Discounts and Commissions(1) | Proceeds to Xencor | |||||||

|---|---|---|---|---|---|---|---|---|---|---|

| Per Share | $ | $ | $ | |||||||

| Total | $ | $ | $ | |||||||

- (1)

- See "Underwriting" beginning on page 164 for additional information regarding underwriting compensation.

Delivery of the shares of common stock will be made on or about , 2013.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Credit Suisse | Leerink Swann | |

Wedbush PacGrow Life Sciences | ||

The date of this prospectus is , 2013

| | Page | |||

|---|---|---|---|---|

PROSPECTUS SUMMARY | 1 | |||

RISK FACTORS | 11 | |||

SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS | 40 | |||

USE OF PROCEEDS | 42 | |||

DIVIDEND POLICY | 43 | |||

CAPITALIZATION | 44 | |||

DILUTION | 46 | |||

SELECTED FINANCIAL DATA | 48 | |||

MANAGEMENT'S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 51 | |||

BUSINESS | 78 | |||

MANAGEMENT | 119 | |||

EXECUTIVE AND DIRECTOR COMPENSATION | 128 | |||

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS | 148 | |||

PRINCIPAL STOCKHOLDERS | 151 | |||

DESCRIPTION OF CAPITAL STOCK | 154 | |||

SHARES ELIGIBLE FOR FUTURE SALE | 158 | |||

MATERIAL U.S. FEDERAL INCOME TAX CONSEQUENCES TO NON-U.S. HOLDERS OF OUR COMMON STOCK | 160 | |||

UNDERWRITING | 164 | |||

LEGAL MATTERS | 168 | |||

EXPERTS | 168 | |||

WHERE YOU CAN FIND ADDITIONAL INFORMATION | 168 | |||

INDEX TO THE CONSOLIDATED FINANCIAL STATEMENTS | F-1 | |||

We have not, and the underwriters have not, authorized anyone to provide any information or to make any representations other than those contained in this prospectus or in any free writing prospectuses prepared by or on behalf of us or to which we have referred you. We take no responsibility for, and can provide no assurance as to the reliability of, any other information that others may give you. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus or in any applicable free writing prospectus is current only as of its date, regardless of its time of delivery or any sale of shares of our common stock. Our business, financial condition, results of operations and prospects may have changed since that date.

Until , 2013 (25 days after the commencement of this offering), all dealers that buy, sell or trade shares of our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This delivery requirement is in addition to the obligation of dealers to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

For investors outside the United States: We have not, and the underwriters have not, done anything that would permit this offering or possession or distribution of this prospectus in any jurisdiction where action for that purpose is required, other than in the United States. Persons outside the United States who come into possession of this prospectus must inform themselves about, and observe any restrictions relating to, the offering of the shares of common stock and the distribution of this prospectus outside the United States.

This summary highlights information contained in other parts of this prospectus. Because it is only a summary, it does not contain all of the information that you should consider before investing in shares of our common stock and it is qualified in its entirety by, and should be read in conjunction with, the more detailed information appearing elsewhere in this prospectus. You should read the entire prospectus carefully, especially "Risk Factors" and our financial statements and the related notes, before deciding to buy shares of our common stock.

Unless the context requires otherwise, references in this prospectus to "Xencor," "we," "us" and "our" refer to Xencor, Inc.

Overview

We are a clinical-stage biopharmaceutical company focused on discovering and developing engineered monoclonal antibodies to treat severe and life-threatening diseases with unmet medical needs. We use our proprietary XmAb technology platform to create next-generation antibody product candidates designed to treat autoimmune and allergic diseases, cancer and other conditions. In contrast to conventional approaches to antibody design, which focus on the portion of antibodies that interact with target antigens, we focus on the portion of the antibody that interacts with multiple segments of the immune system. This portion, referred to as the Fc domain, is constant and interchangeable among antibodies. Our engineered Fc domains, the XmAb technology, can be readily substituted for natural Fc domains. We believe our Fc domains enhance antibody performance by, for example, increasing immune inhibitory activity, improving cytotoxicity or extending circulating half-life, while typically maintaining over 99.5% identity in structure and sequence to natural antibodies. By improving over natural antibody function, we believe that our XmAb-engineered antibodies offer innovative approaches to treating disease and potential clinical advantages over other treatments.

Our business strategy is based on the plug-and-play nature of the XmAb technology platform to modify features of natural antibodies and create numerous differentiated antibody product candidates. We have internally generated a pipeline that has allowed us to selectively partner certain development programs while maintaining full ownership of other programs. We also have a number of technology licenses under which we have licensed the XmAb technology platform to pharmaceutical and biotechnology companies for use in a limited number of programs, providing multiple revenue streams that require no further resources from Xencor. There are currently five antibody product candidates in clinical trials that have been engineered with XmAb technology, including four candidates being advanced by licensees and development partners. As of September 30, 2013, our XmAb technology platform is protected by 21 issued U.S. patents and 44 U.S. patent applications, in addition to foreign counterparts.

Our internally-generated pipeline includes the following three lead XmAb-engineered antibodies that are currently in development:

- •

- XmAb5871 is being developed for the treatment of autoimmune diseases, including rheumatoid arthritis and lupus. It uses our Immune Inhibitor Fc Domain and targets B cells, an important component of the immune system. We believe XmAb5871 has the potential to address a key unmet need in autoimmune therapies due to its combination of potent B-cell inhibition without B-cell depletion. We are currently conducting a Phase 1b/2a clinical trial for XmAb5871 in rheumatoid arthritis patients with active disease on stable non-biologic disease modifying anti-rheumatic drug (DMARD) therapy. We expect to report preliminary data from this trial in the second half of 2014. Our partner, Amgen Inc. (Amgen), has an option to acquire an exclusive worldwide license for XmAb5871, exercisable at any time before completion of a data review period following our planned subsequent Phase 2b proof-of-concept clinical trial. Until the option exercise, we lead research, development and manufacturing activities for XmAb5871 with collaborative input and development support from Amgen. According to the American College

1

- •

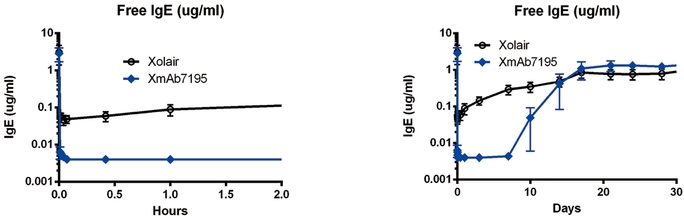

- XmAb7195 is being developed for the treatment of severe asthma and allergic diseases. It uses our Immune Inhibitor Fc Domain and is designed to reduce blood plasma levels of IgE, which mediates allergic responses and allergic disease. Its three specific mechanisms of action give it potential advantages over current therapies: (i) increased IgE binding, (ii) inhibition of IgE production and (iii) rapid clearance of IgE from circulation. We anticipate filing an investigational new drug application (IND) with the United States Food and Drug Administration (FDA) and initiating a Phase 1a clinical trial in the first half of 2014. We plan to report preliminary data from this trial at the end of 2014. According to the U.S. Centers for Disease Control and Prevention (CDC), one in 12 Americans has asthma, and there were 1.8 million emergency room visits caused by asthma in 2010. Xolair, the leading antibody therapy for the treatment of severe refractory asthma, generated approximately $1.3 billion in worldwide sales in 2012.

- •

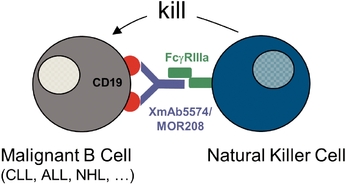

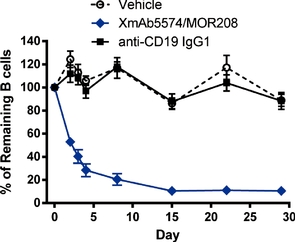

- XmAb5574/MOR208 is being developed for the treatment of blood-based cancers and uses our Cytotoxic Fc Domain. Our partner, MorphoSys AG (MorphoSys), is currently conducting two Phase 2 clinical trials of XmAb5574/MOR208 in patients with B-cell acute lymphoblastic leukemia (B-ALL) and non-Hodgkin lymphomas (NHL). According to the Leukemia and Lymphoma Society, over 60,000 Americans are diagnosed with these cancers each year. Rituxan, the leading antibody therapy for NHL, generated approximately $6.1 billion in worldwide oncology sales in 2012.

of Rheumatology, rheumatoid arthritis and lupus affect approximately 1.3 million and 160,000 adults in the United States, respectively. Humira, the leading antibody therapy for autoimmune diseases, generated sales of approximately $9.3 billion worldwide in 2012.

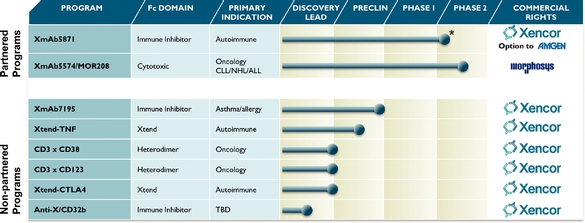

Product Pipeline and Platform

A summary of the partnered and non-partnered product development programs that we have generated internally is shown below.

- *

- Currently enrolling Phase 2a portion of Phase 1b/2a clinical trial.

In addition, we have licensed our XmAb technology to pharmaceutical and biotechnology companies for use in a limited number of their programs. These licensees include Boehringer Ingelheim, CSL, Janssen, Merck and Alexion, and collectively these licensees have three Phase 1 clinical development-stage programs and four pre-clinical development-stage programs.

2

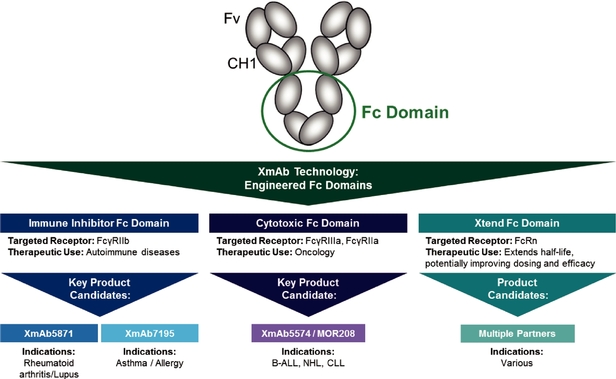

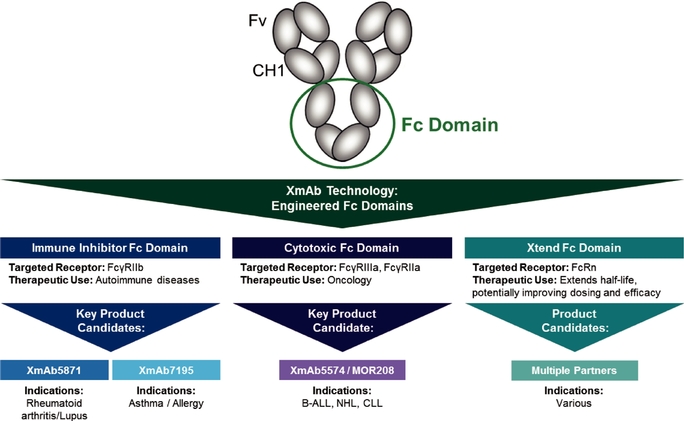

Antibody Structure and Fc Domain Function

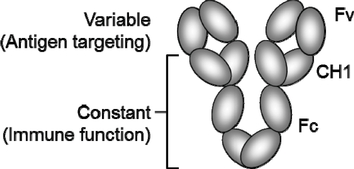

Antibodies are Y-shaped proteins that are produced by B cells and used by the immune system to target and neutralize foreign objects known as antigens. These objects may include tumor cells, bacteria and viruses. Antibodies are composed of two structurally independent parts, the variable domain (the Fv domain) and the constant domain (the Fc domain and the CH1 domain). The Fv domain is responsible for targeting a specific antibody to a specific antigen, and is different for every type of antibody. The Fc domain interacts with various receptors on immune cells and other cells and, rather than binding antibodies to target antigens, it endows antibodies with properties beyond simple binding, such as immune response regulation and cytotoxicity. Importantly, Fc domains are the same and interchangeable from antibody to antibody.

Our Fc Domain Focused Approach

The global market for antibody therapeutics was estimated to be approximately $45.0 billion in 2011, of which the U.S. market was estimated to be $20.0 billion. Intense competition drives companies to develop differentiated antibody drugs, often because of the common pursuit of the same antigen Fv targets across the industry. Industry efforts have focused on engineering Fv domains since the mid-1980s to enhance performance. More recently, many efforts at differentiation have attempted to improve upon antibody performance by drastically changing the antibody structure or substituting new molecules altogether, for example, new antibody-like scaffolds, bi-specific antibodies and antibody-drug conjugates. A challenge to these efforts has been making these new drug molecules replicate the beneficial features of natural antibodies, including ease of production, safety, efficacy and simplicity. These efforts, however, have largely ignored the Fc domain.

In contrast, in the last decade Xencor has focused on Fc engineering. Fc engineering involves additional complexities, particularly consideration of simultaneous interactions with multiple Fc receptors and immune cell types and requires significant expertise in structural biology and immunology. Our XmAb Fc domain technology is a platform of patented antibody components that enable the creation of therapeutic antibody candidates that have novel interactions with the human immune and antibody regulation systems. Each XmAb Fc domain consists of a naturally occurring Fc domain with a small number of amino acid changes found to be critical for modulating interactions with the desired Fc receptors. We have identified a set of Fc domains, each of which is engineered with particular amino acid changes to augment a specific naturally-occurring antibody function based on its Fc receptor binding profile, including:

- •

- Immune Inhibitor Fc Domain—selective immune inhibition and rapid target clearance, targeting the receptor FcgRIIb;

- •

- Cytotoxic Fc Domain—increased cytotoxicity, targeting the receptors FcgRIIIa on natural killer (NK) cells and FcgRIIa on other immune system cells; and

- •

- Xtend Fc Domain—extended antibody half-life, targeting the receptor FcRn on endothelial cells.

With such limited modifications of the natural Fc domain, XmAb-engineered antibodies are typically over 99.5% identical in structure and sequence to natural antibodies, simplifying product

3

development yet enhancing function. A summary of the Fc domain properties improved by our XmAb technology and the associated product candidates and targeted indications are summarized below:

Our Strategy

Our goal is to become a leading biopharmaceutical company focused on developing and commercializing engineered monoclonal antibodies to treat severe and life-threatening diseases with unmet medical needs. Key elements of our strategy are to:

- •

- Advance the clinical development of our lead Immune Inhibitor Fc Domain product candidates. We are developing XmAb5871, in partnership with Amgen, for the treatment of autoimmune diseases and are developing XmAb7195 independently for the treatment of asthma and allergic diseases.

- •

- Continue to monetize and expand the use of our XmAb technology platform. We are seeking additional licensing and partnering opportunities, similar to our partnerships with Amgen and with MorphoSys for XmAb5574/MOR208, with leading pharmaceutical and biotechnology companies.

- •

- Build a large and diversified portfolio of product candidates. We aim to create new XmAb-engineered antibody product candidates that exploit the novel properties of our XmAb technology platform.

- •

- Broaden the functionality of our XmAb technology platform. We are conducting further research into the function and application of antibody Fc domains in order to expand the scope of our XmAb technology platform.

- •

- Continue to expand our patent portfolio protecting our XmAb technology platform. We seek to expand and protect our development programs and product candidates by filing and prosecuting patent applications in the United States and other countries.

4

Risks Associated with Our Business

Our business is subject to numerous risks and uncertainties, including those highlighted in the section entitled "Risk Factors" immediately following this prospectus summary. These risks include, but are not limited to, the following:

- •

- We have incurred significant losses since our inception and anticipate that we will continue to incur significant losses for the foreseeable future. Our accumulated deficit was $223.9 million as of September 30, 2013, representing our cumulative losses since our inception in 1997.

- •

- Biopharmaceutical product development is a highly speculative undertaking and involves a substantial degree of uncertainty. We have never generated any revenue from product sales and may never be profitable.

- •

- We will require additional financing and may be unable to raise sufficient capital, which could lead us to delay, reduce or abandon research and development programs or commercialization.

- •

- If we are unable to obtain, maintain and enforce intellectual property protection covering our products, others may be able to make, use or sell products substantially the same as ours, which could adversely affect our ability to compete in the market.

- •

- The development and commercialization of biologic products is subject to extensive regulation, and we may not obtain regulatory approvals for any of our product candidates.

- •

- Even if we receive regulatory approval for any of our product candidates, we will be subject to ongoing regulatory obligations and continued regulatory review, which may result in significant additional expense. Additionally, our product candidates, if approved, could be subject to labeling and other restrictions and market withdrawal and we may be subject to penalties if we fail to comply with regulatory requirements or experience unanticipated problems with our products.

- •

- We may not be successful in our efforts to use and expand our XmAb technology platform to build a pipeline of product candidates and develop marketable products.

- •

- Our existing partnerships are important to our business, and future partnerships may also be important to us. If we are unable to maintain any of these partnerships, or if these partnerships are not successful, our business could be adversely affected.

- •

- We face significant competition from other biotechnology and pharmaceutical companies and our operating results will suffer if we fail to compete effectively.

Corporate and Other Information

We were incorporated in California in August 1997 under the name Xencor, Inc. In September 2004, we reincorporated in the state of Delaware under the name Xencor, Inc. Our principal executive offices are located at 111 West Lemon Avenue, Monrovia, California, 91016, and our telephone number is (626) 305-5900. Our corporate website address is www.xencor.com. Information contained on or accessible through our website is not a part of this prospectus, and the inclusion of our website address in this prospectus is an inactive textual reference only.

This prospectus contains references to our trademarks and to trademarks belonging to other entities. Solely for convenience, trademarks and trade names referred to in this prospectus, including logos, artwork and other visual displays, may appear without the ® orTM symbols, but such references are not intended to indicate, in any way, that their respective owners will not assert, to the fullest extent under applicable law, their rights thereto. We do not intend our use or display of other companies' trade names or trademarks to imply a relationship with, or endorsement or sponsorship of us by, any other companies.

5

Implications of Being an Emerging Growth Company

As a company with less than $1.0 billion in revenue during our last fiscal year, we qualify as an "emerging growth company" as defined in the Jumpstart Our Business Startups Act (JOBS Act) enacted in April 2012. An "emerging growth company" may take advantage of reduced reporting requirements that are otherwise applicable to public companies. These provisions include, but are not limited to:

- •

- being permitted to present only two years of audited financial statements and only two years of related Management's Discussion and Analysis of Financial Condition and Results of Operations in this prospectus;

- •

- not being required to comply with the auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002, as amended;

- •

- reduced disclosure obligations regarding executive compensation in our periodic reports, proxy statements and registration statements; and

- •

- exemptions from the requirements of holding a nonbinding advisory vote on executive compensation and stockholder approval of any golden parachute payments not previously approved.

We may use these provisions until the last day of our fiscal year following the fifth anniversary of the completion of this offering. However, if certain events occur prior to the end of such five-year period, including if we become a "large accelerated filer," our annual gross revenues exceed $1.0 billion or we issue more than $1.0 billion of non-convertible debt in any three-year period, we will cease to be an emerging growth company prior to the end of such five-year period.

We have elected to take advantage of certain of the reduced disclosure obligations in the registration statement of which this prospectus is a part and may elect to take advantage of other reduced reporting requirements in future filings. As a result, the information that we provide to our stockholders may be different than you might receive from other public reporting companies in which you hold equity interests.

The JOBS Act provides that an emerging growth company can take advantage of an extended transition period for complying with new or revised accounting standards. We have irrevocably elected not to avail ourselves of this exemption and, therefore, we will be subject to the same new or revised accounting standards as other public companies that are not emerging growth companies.

6

Common stock offered by us | 10,700,000 shares | |

Common stock to be outstanding after this offering | 27,392,576 shares | |

Option to purchase additional shares | The underwriters have a 30-day option to purchase a maximum of 1,605,000 additional shares of common stock from us. | |

Use of proceeds | We intend to use the net proceeds from this offering to fund the clinical development of XmAb5871 and XmAb7195, product candidate discovery, technology development, patent prosecution activities, working capital and other general corporate purposes, including the costs associated with being a public company. See "Use of Proceeds." | |

Risk factors | See "Risk Factors" beginning on page 11 and the other information included in this prospectus for a discussion of factors to consider carefully before deciding to purchase any shares of our common stock. | |

NASDAQ Global Market symbol | "XNCR" |

The number of shares of our common stock to be outstanding after this offering is based on 16,692,576 shares of common stock outstanding as of September 30, 2013, after giving effect to the conversion of our outstanding convertible preferred stock into 16,620,274 shares of common stock and excludes:

- •

- 1,803,685 shares of common stock issuable upon the exercise of outstanding stock options as of September 30, 2013, at a weighted-average exercise price of $1.61 per share;

- •

- 2,390,448 shares of common stock reserved for future issuance under our 2013 equity incentive plan (the 2013 plan), which will become effective as of the date of the effectiveness of the registration statement of which this prospectus forms a part (including 880,771 shares of common stock reserved for issuance under our 2010 equity incentive plan (the 2010 pre-IPO plan), which shares will be added to the shares reserved under the 2013 plan upon its effectiveness); and

- •

- 267,741 shares of common stock reserved for future issuance under our 2013 employee stock purchase plan (the 2013 purchase plan), which will become effective as of the date of the effectiveness of the registration statement of which this prospectus forms a part.

Unless otherwise indicated, all information contained in this prospectus and the number of shares of common stock outstanding as of September 30, 2013 assumes:

- •

- the conversion of all our outstanding convertible preferred stock outstanding as of September 30, 2013 into an aggregate of 16,620,274 shares of common stock upon the effectiveness of the registration statement of which this prospectus is a part;

- •

- no exercise by the underwriters of their over-allotment option to purchase up to an additional 1,605,000 shares of our common stock;

- •

- the filing of our amended and restated certificate of incorporation and the adoption of our amended and restated bylaws immediately prior to the closing of this offering; and

- •

- a 3.1-for-one reverse stock split of our common stock effected on November 1, 2013.

7

The following table summarizes certain of our financial data. We derived the summary statement of operations data for the years ended December 31, 2012 and 2011 from our audited financial statements and related notes appearing elsewhere in this prospectus. The summary statement of operations data for the nine months ended September 30, 2013 and 2012 and the summary balance sheet data as of September 30, 2013 were derived from our unaudited financial statements appearing elsewhere in this prospectus. The unaudited financial data, in management's opinion, have been prepared on the same basis as the audited financial statements and related notes included elsewhere in this prospectus, and include all adjustments, consisting only of normal recurring adjustments, that management considers necessary for a fair presentation of the information for the periods presented. Our historical results are not necessarily indicative of the results that may be expected in the future and results of interim periods are not necessarily indicative of the results for the entire year. The summary financial data should be read together with our financial statements and related notes, "Selected Financial Data" and "Management's Discussion and Analysis of Financial Condition and Results of Operations" appearing elsewhere in this prospectus.

| | Year Ended December 31, | Nine Months Ended September 30, | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | 2011 | 2012 | 2012 | 2013 | |||||||||

| | (in thousands, except share and per share data) | ||||||||||||

| | (Restated) | | (unaudited) | ||||||||||

Statement of Operations Data: | |||||||||||||

Revenues | $ | 6,849 | $ | 9,524 | $ | 7,099 | $ | 8,428 | |||||

Operating expenses: | |||||||||||||

Research and development | 12,663 | 12,668 | 8,725 | 12,857 | |||||||||

General and administrative | 3,638 | 3,086 | 2,081 | 2,381 | |||||||||

Total operating expenses | 16,301 | 15,754 | 10,806 | 15,238 | |||||||||

Loss from operations | (9,452 | ) | (6,230 | ) | (3,707 | ) | (6,810 | ) | |||||

Other income (expenses) | |||||||||||||

Interest income | 34 | 11 | 11 | 7 | |||||||||

Interest expense | (1,850 | ) | (2,461 | ) | (1,811 | ) | (1,212 | ) | |||||

Other income (expense) | 65 | 86 | 24 | 15 | |||||||||

Loss on settlement of notes(1) | — | — | — | (48,556 | ) | ||||||||

Total other income (expenses), net | (1,751 | ) | (2,364 | ) | (1,776 | ) | (49,746 | ) | |||||

Net loss | (11,203 | ) | (8,594 | ) | (5,483 | ) | (56,556 | ) | |||||

Net deemed contribution on exchange and sale of preferred stock(2) | — | — | — | 144,765 | |||||||||

Net income (loss) attributable to common stockholders | $ | (11,203 | ) | $ | (8,594 | ) | $ | (5,483 | ) | $ | 88,209 | ||

Net income (loss) per share attributable to common stockholders(3): | |||||||||||||

Basic | $ | (154.95 | ) | $ | (118.86 | ) | $ | (75.83 | ) | $ | 1,220.01 | ||

Diluted | $ | (154.95 | ) | $ | (118.86 | ) | $ | (75.83 | ) | $ | (4.10 | ) | |

Weighted average shares of common stock used in computing net income (loss) per share attributable to common stockholders: | |||||||||||||

Basic | 72,302 | 72,302 | 72,302 | 72,302 | |||||||||

Diluted | 72,302 | 72,302 | 72,302 | 13,794,138 | |||||||||

Pro forma net loss per share of common stock, basic and diluted (unaudited)(4) | $ | (0.51 | ) | $ | (0.48 | ) | |||||||

Weighted average shares used in computing pro forma net loss per share of common stock, basic and diluted (unaudited)(4) | 16,692,576 | 16,692,576 | |||||||||||

- (1)

- See note 3 to our interim financial statements appearing elsewhere in this prospectus for a description of the adjustment to net loss resulting from exchange of convertible notes for preferred stock.

- (2)

- See notes 8 and 3 to our annual and interim financial statements, respectively, appearing elsewhere in this prospectus for a description of the deemed contribution on exchange and sale of preferred stock.

- (3)

- See notes 1 and 5 to our annual and interim financial statements, respectively, appearing elsewhere in this prospectus for a description of the method used to calculate basic and diluted loss per common.

8

- (4)

- Pro forma net loss per share attributable to common stockholders excludes the impact of non-recurring items recognized in income attributable to common stockholders for the periods presented. We calculated pro forma weighted average shares outstanding for the nine months ended September 30, 2013 to give effect to the automatic conversion into shares of common stock, on a 3.1:1 basis, of all shares of convertible preferred stock outstanding at September 30, 2013. We calculated pro forma weighted average shares outstanding for the year ended December 31, 2012 to give effect to the automatic conversion into shares of common stock, on a 3.1:1 basis, of all shares of convertible preferred stock outstanding at September 30, 2013, which includes 13,666,071 shares of common stock issuable upon conversion of the shares of preferred stock received in connection with the exchange of our outstanding promissory notes on June 13, 2013. We believe the calculation of pro forma shares described above is the most meaningful to investors, as such calculation represents the actual number of shares of common stock our notes became convertible into, and prior to the exchange of our convertible notes in June 2013, such notes were not convertible at the option of the holders, and the number of shares of common stock such notes were automatically convertible into upon an initial public offering was contingent on the public offering price, which was not known at the time of the conversion of the notes or applicable to the actual number of shares of common stock issued upon conversion of the notes.

Pro forma net loss attributable to common stockholders (in thousands):

| | Year Ended December 31, 2012 | Nine Months Ended September 30, 2013 | |||||

|---|---|---|---|---|---|---|---|

Net income (loss) attributable to common stockholders | $ | (8,594 | ) | $ | 88,209 | ||

Loss on settlement of notes | — | 48,556 | |||||

Net deemed contribution on exchange and sale of preferred stock | — | (144,765 | ) | ||||

Pro forma net loss attributable to common stockholders | $ | (8,594 | ) | $ | (8,000 | ) | |

Pro forma weighted average shares outstanding, basic and diluted:

| | Year Ended December 31, 2012 | Nine Months Ended September 30, 2013 | |||||

|---|---|---|---|---|---|---|---|

Common stock | 72,302 | 72,302 | |||||

Preferred Stock | 16,620,274 | 16,620,274 | |||||

Pro forma weighted average shares outstanding, basic and diluted | 16,692,576 | 16,692,576 | |||||

Pro forma net loss per share of common stock, basic and diluted (unaudited) | $ | (0.51 | ) | $ | (0.48 | ) | |

9

| | As of September 30, 2013 | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|

| | Actual | Pro Forma(1) | Pro Forma as Adjusted(2)(3) | |||||||

| | (in thousands) | |||||||||

| | (unaudited) | |||||||||

Balance Sheet Data: | ||||||||||

Cash and cash equivalents | $ | 9,621 | $ | 9,621 | $ | 76,778 | ||||

Working capital | 2,127 | 2,127 | 69,284 | |||||||

Patents, licenses, and other intangible assets, net | 9,013 | 9,013 | 9,013 | |||||||

Total assets | 20,206 | 20,206 | 87,363 | |||||||

Deferred revenue, less current portion | 7,000 | 7,000 | 7,000 | |||||||

Convertible preferred stock | 79,601 | — | — | |||||||

Total stockholders' equity (deficit) | (75,029 | ) | 4,572 | 71,729 | ||||||

- (1)

- Pro forma amounts reflect the conversion of all our outstanding shares of convertible preferred stock outstanding as of September 30, 2013 into an aggregate of 16,620,274 shares of our common stock.

- (2)

- Pro forma as adjusted amounts reflect the pro forma conversion adjustments described in footnote (1) above, as well as the sale of 10,700,000 shares of our common stock in this offering at an assumed initial public offering price of $7.00 per share, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

- (3)

- A $1.00 increase (decrease) in the assumed initial public offering price would increase (decrease) each of cash, cash equivalents, working capital, total assets and total stockholders' equity by approximately $10.0 million, assuming the number of shares offered by us as stated on the cover page of this prospectus remains unchanged and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us. Similarly, a one million share increase (decrease) in the number of shares offered by us, as set forth on the cover page of this prospectus, would increase (decrease) each of cash and cash equivalents, working capital, total assets and total stockholders' equity by approximately $6.5 million, assuming the assumed initial public offering price of $7.00 per share remains the same, and after deducting the estimated underwriting discounts and commissions and estimated offering expenses payable by us.

10

An investment in shares of our common stock involves a high degree of risk. You should carefully consider the following information about these risks, together with the other information appearing elsewhere in this prospectus, before deciding to invest in our common stock. The occurrence of any of the following risks could have a material adverse effect on our business, financial condition, results of operations and future growth prospects. In these circumstances, the market price of our common stock could decline, and you may lose all or part of your investment.

Risks Relating to Our Business and to the Discovery, Development and Regulatory Approval of Our Product Candidates

We have incurred significant losses since our inception and anticipate that we will continue to incur significant losses for the foreseeable future.

We are a clinical-stage biopharmaceutical company. To date, we have financed our operations primarily through private placements of convertible debt and preferred stock and our research and licensing agreements and have incurred significant operating losses since our inception in 1997. Our net loss for the nine months ended September 30, 2013 was $56.6 million (including a $48.6 million loss on settlement of convertible notes) and for the years ended December 31, 2011 and 2012 it was $11.2 million and $8.6 million, respectively. As of September 30, 2013, we had an accumulated deficit of $223.9 million. Such losses are expected to increase in the future as we execute our plan to continue our discovery, research and development activities, including the ongoing and planned clinical development of our antibody product candidates, and incur the additional costs of operating as a public company. We are unable to predict the extent of any future losses or when we will become profitable, if ever. Even if we do achieve profitability, we may not be able to sustain or increase profitability on an ongoing basis which would adversely affect our business, prospects, financial condition and results of operations.

For the reasons cited above, without giving effect to the proceeds of this offering, the report of our independent registered public accountant on our financial statements as of and for the year ended December 31, 2012 includes explanatory language describing the existence of substantial doubt about our ability to continue as a going concern. There have been no adjustments in the accompanying financial statements to reflect this uncertainty.

Biopharmaceutical product development is a highly speculative undertaking and involves a substantial degree of uncertainty. We have never generated any revenue from product sales and may never be profitable.

We have devoted substantially all of our financial resources and efforts to developing our proprietary XmAb technology platform, identifying potential product candidates and conducting preclinical studies and clinical trials. We and our partners are still in the early stages of developing our product candidates, and we have not completed development of any products. Our revenue to date has been primarily revenue from the license of our proprietary XmAb technology platform for the development of product candidates by others or revenue from our partners. Our ability to generate revenue and achieve profitability depends in large part on our ability, alone or with partners, to achieve milestones and to successfully complete the development of, obtain the necessary regulatory approvals for, and commercialize, product candidates. We do not anticipate generating revenues from sales of products for the foreseeable future. Our ability to generate future revenues from product sales depends heavily on our and our partners' success in:

- •

- completing clinical trials through all phases of clinical development of our current product candidates, XmAb5871 and XmAb7195, as well as the product candidates that are being developed by our partners and licensees;

11

- •

- seeking and obtaining marketing approvals for product candidates that successfully complete clinical trials;

- •

- launching and commercializing product candidates for which we obtain marketing approval, with a partner or, if launched independently, successfully establishing a sales force, marketing and distribution infrastructure;

- •

- identifying and developing new XmAb-engineered therapeutic antibody candidates;

- •

- establishing and maintaining supply and manufacturing relationships with third parties;

- •

- obtaining additional licensing and partnering opportunities, similar to our partnership with MorphoSys for XmAb5574/MOR208, with leading pharmaceutical and biotechnology companies;

- •

- achieving the milestones set forth in our agreements with our partners;

- •

- conducting further research into the function and application of antibody Fc domains in order to expand the scope of our proprietary XmAb technology platform;

- •

- maintaining, protecting, expanding and enforcing our intellectual property; and

- •

- attracting, hiring and retaining qualified personnel.

Because of the numerous risks and uncertainties associated with biologic product development, we are unable to predict the timing or amount of increased expenses and when we will be able to achieve or maintain profitability, if ever. In addition, our expenses could increase beyond expectations if we are required by the U.S. Food and Drug Administration (FDA), or foreign regulatory agencies, to perform studies and trials in addition to those that we currently anticipate, or if there are any delays in our or our partners completing clinical trials or the development of any of our product candidates. If one or more of the product candidates that we independently develop is approved for commercial sale, we anticipate incurring significant costs associated with commercializing such product candidates. Even if we or our partners are able to generate revenues from the sale of any approved products, we may not become profitable and may need to obtain additional funding to continue operations, which may not be available to us on favorable terms, if at all. Even if we do achieve profitability, we may not be able to sustain or increase profitability on a quarterly or annual basis. Our failure to become and remain profitable would depress the value of our company and could impair our ability to raise capital, expand our business, maintain our research and development efforts, diversify our product offerings or even continue our operations. A decline in the value of our company could also cause you to lose all or part of your investment.

We will require additional financing and may be unable to raise sufficient capital, which could lead us to delay, reduce or abandon research and development programs or commercialization.

Our operations have used substantial amounts of cash since inception. Our research and development expenses were $12.9 million for the nine months ended September 30, 2013, and $12.7 million for each of the years ended December 31, 2011 and 2012, respectively. We expect our expenses to increase in connection with our ongoing development activities, including the continuation of our ongoing Phase 1b/2a clinical trial of XmAb5871 in patients with rheumatoid arthritis, the initiation of additional clinical trials of XmAb5871 and the submission of an investigational new drug application (IND) to the FDA for XmAb7195 to be followed by our first clinical trial of XmAb7195. Identifying potential product candidates and conducting preclinical testing and clinical trials are time-consuming, expensive and uncertain processes that takes years to complete, and we or our partners may never generate the necessary data or results required to obtain regulatory approval and achieve product sales. In addition, our product candidates, if approved, may not achieve commercial success.

12

Our commercial revenues, if any, will be derived from sales of products that we do not expect to be commercially available for many years, if at all. If we obtain regulatory approval for any of our product candidates, we expect to incur significant commercialization expenses related to product manufacturing, marketing, sales and distribution. Furthermore, after the closing of this offering, we expect to incur additional costs associated with operating as a public company. Accordingly, we will need to obtain substantial additional funding in connection with our continuing operations. If we are unable to raise capital when needed or on attractive terms, we could be forced to delay, reduce or eliminate our research and development programs or any future commercialization efforts.

We believe that the net proceeds from this offering and our existing cash, together with interest thereon, will be sufficient to fund our operations through 2016. However, changing circumstances or inaccurate estimates by us may cause us to use capital significantly faster than we currently anticipate, and we may need to spend more money than currently expected because of circumstances beyond our control. For example, our planned clinical trials for XmAb5871 may encounter technical, enrollment or other issues that could cause our development costs to increase more than we expect. Even with the expected net proceeds from this offering, we do not have sufficient cash to complete the clinical development of any of our product candidates and will require additional funding in order to complete the development activities required for regulatory approval of either XmAb5871 or XmAb7195 or any future product candidates that we develop independently. Because successful development of our product candidates is uncertain, we are unable to estimate the actual funds we will require to complete research and development and commercialize our product candidates. Adequate additional financing may not be available to us on acceptable terms, or at all. In addition, we may seek additional capital due to favorable market conditions or strategic considerations; even if we believe we have sufficient funds for our current or future operating plans. If we are unable to raise capital when needed or on attractive terms, we could be forced to delay, reduce or eliminate our research and development programs or any future commercialization efforts.

The development and commercialization of biologic products is subject to extensive regulation, and we may not obtain regulatory approvals for any of our product candidates.

The clinical development, manufacturing, labeling, packaging, storage, recordkeeping, advertising, promotion, export, import, marketing and distribution and other possible activities relating to XmAb5871, XmAb7195 and XmAb5574/MOR208, our current lead antibody product candidates, as well as any other antibody product candidate that we may develop in the future, are subject to extensive regulation in the United States as biologics. Biologics require the submission of a Biologics License Application (BLA) to the FDA and we are not permitted to market any product candidate in the United States until we obtain approval from the FDA of a BLA for that product. A BLA must be supported by extensive clinical and preclinical data, as well as extensive information regarding chemistry, manufacturing and controls (CMC) sufficient to demonstrate the safety, purity, potency and effectiveness of the applicable product candidate to the satisfaction of the FDA.

Regulatory approval of a BLA is not guaranteed, and the approval process is an expensive and uncertain process that may take several years. The FDA and foreign regulatory entities also have substantial discretion in the approval process. The number and types of preclinical studies and clinical trials that will be required for BLA approval varies depending on the product candidate, the disease or the condition that the product candidate is designed to target and the regulations applicable to any particular product candidate. Despite the time and expense associated with preclinical studies and clinical trials, failure can occur at any stage, and we could encounter problems that require us to repeat or perform additional preclinical studies or clinical trials or generate additional CMC data. The FDA and similar foreign authorities could delay, limit or deny approval of a product candidate for many reasons, including because they:

- •

- may not deem our product candidate to be adequately safe and effective;

13

- •

- may not find the data from our preclinical studies and clinical trials or CMC data to be sufficient to support a claim of safety and efficacy;

- •

- may not approve the manufacturing processes or facilities associated with our product candidate;

- •

- may conclude that we have not sufficiently demonstrated long-term stability of the formulation of the drug product for which we are seeking marketing approval;

- •

- may change approval policies or adopt new regulations; or

- •

- may not accept a submission due to, among other reasons, the content or formatting of the submission.

Generally, public concern regarding the safety of drug and biologic products could delay or limit our ability to obtain regulatory approval, result in the inclusion of unfavorable information in our labeling, or require us to undertake other activities that may entail additional costs.

We have not submitted an application for approval or obtained FDA approval for any product. This lack of experience may impede our ability to obtain FDA approval in a timely manner, if at all, for our product candidates.

To market any biologics outside of the United States, we and current or future collaborators must comply with numerous and varying regulatory and compliance related requirements of other countries. Approval procedures vary among countries and can involve additional product testing and additional administrative review periods, including obtaining reimbursement and pricing approval in select markets. The time required to obtain approval in other countries might differ from that required to obtain FDA approval. The regulatory approval process in other countries may include all of the risks associated with FDA approval as well as additional, presently unanticipated, risks. Regulatory approval in one country does not ensure regulatory approval in another, but a failure or delay in obtaining regulatory approval in one country may negatively impact the regulatory process in others, including the risk that our product candidates may not be approved for all indications requested and that such approval may be subject to limitations on the indicated uses for which the drug may be marketed. Certain countries have a very difficult reimbursement environment and we may not obtain reimbursement or pricing approval, if required, in all countries where we expect to market a product, or we may obtain reimbursement approval at a level that would make marketing a product in certain countries not viable.

If we experience delays in obtaining approval or if we fail to obtain approval of our product candidates, the commercial prospects for our product candidates may be harmed and our ability to generate revenues will be materially impaired which would adversely affect our business, prospects, financial condition and results of operations.

Even if we receive regulatory approval for any of our product candidates, we will be subject to ongoing regulatory obligations and continued regulatory review, which may result in significant additional expense. Additionally, our product candidates, if approved, could be subject to labeling and other restrictions and market withdrawal and we may be subject to penalties if we fail to comply with regulatory requirements or experience unanticipated problems with our products.

Any regulatory approvals that we or our partners receive for our product candidates may also be subject to limitations on the approved indicated uses for which the product may be marketed or to the conditions of approval, or contain requirements for potentially costly post-marketing testing, including Phase 4 clinical trials, and surveillance to monitor the safety and efficacy of the product candidate. In addition, if the FDA or a comparable foreign regulatory authority approves any of our product candidates, the manufacturing processes, labeling, packaging, distribution, adverse event reporting, storage, advertising, promotion, import, export and recordkeeping for the product will be subject to

14

extensive and ongoing regulatory requirements. These requirements include submissions of safety and other post-marketing information and reports, registration, as well as continued compliance with current good manufacturing practices (cGMPs), and current good clinical practices (cGCPs), for any clinical trials that we conduct post-approval. Later discovery of previously unknown problems with a product, including adverse events of unanticipated severity or frequency, undesirable side effects caused by the product, problems encountered by our third-party manufacturers or manufacturing processes, or failure to comply with regulatory requirements, either before or after product approval, may result in, among other things:

- •

- restrictions on the marketing or manufacturing of the product;

- •

- requirements to include additional warnings on the label;

- •

- requirements to create a medication guide outlining the risks to patients;

- •

- withdrawal of the product from the market;

- •

- voluntary or mandatory product recalls;

- •

- requirements to change the way the product is administered or for us to conduct additional clinical trials;

- •

- fines, warning letters or holds on clinical trials;

- •

- refusal by the FDA to approve pending applications or supplements to approved applications filed by us or our strategic partners, or suspension or revocation of product license approvals;

- •

- product seizure or detention, or refusal to permit the import or export of products;

- •

- injunctions or the imposition of civil or criminal penalties; and

- •

- harm to our reputation.

Additionally if any of our product candidates receives marketing approval, the FDA could require us to adopt a Risk Evaluation and Mitigation Strategy (REMS) to ensure that the benefits of the therapy outweigh its risks, which may include, among other things, a medication guide outlining the risks for distribution to patients and a communication plan to health care practitioners.

Any of these events could prevent us from achieving or maintaining market acceptance of the product or the particular product candidate at issue and could significantly harm our business, prospects, financial condition and results of operations.

The FDA's policies may change and additional government regulations may be enacted that could prevent, limit or delay regulatory approval of our product candidates. We cannot predict the likelihood, nature or extent of government regulation that may arise from future legislation or administrative action, either in the United States or abroad. If we are slow or unable to adapt to changes in existing requirements or the adoption of new requirements or policies, or if we are not able to maintain regulatory compliance, we may lose any marketing approval that we may have obtained and we may not achieve or sustain profitability, which would adversely affect our business, prospects, financial condition and results of operations.

If we experience delays or difficulties in the enrollment of patients in clinical trials, our receipt of necessary regulatory approvals could be delayed or prevented.

We may not be able to initiate or continue clinical trials for our product candidates if we are unable to locate and enroll a sufficient number of eligible patients to participate in these trials as required by the FDA or similar regulatory authorities outside the United States. In addition, some of our competitors have ongoing clinical trials for product candidates that treat the same indications as

15

our product candidates, and patients who would otherwise be eligible for our clinical trials may instead enroll in clinical trials of our competitors' product candidates.

Patient enrollment is affected by other factors including:

- •

- the severity of the disease under investigation;

- •

- the patient eligibility criteria for the study in question;

- •

- the perceived risks and benefits of the product candidate under study;

- •

- our payments for conducting clinical trials;

- •

- the patient referral practices of physicians;

- •

- the ability to monitor patients adequately during and after treatment; and

- •

- the proximity and availability of clinical trial sites for prospective patients.

For example, in our Phase 1a clinical trial of XmAb5871, which we completed in December 2012, delays in patient enrollment that were outside our control caused several weeks of delay that we did not predict at the outset of that clinical trial. Our inability to enroll a sufficient number of patients for any of our clinical trials could result in significant delays and could require us to abandon one or more clinical trials altogether. Enrollment delays in our clinical trials may result in increased development costs for our product candidates and in delays to commercially launching our product candidates, if approved, which would cause the value of our company to decline and limit our ability to obtain additional financing.

The manufacture of biopharmaceutical products, including XmAb-engineered antibodies, is complex and manufacturers often encounter difficulties in production. If we or any of our third-party manufacturers encounter any loss of our master cell banks or if any of our third-party manufacturers encounter other difficulties, or otherwise fail to comply with their contractual obligations, our ability to provide product candidates for clinical trials or our products to patients, once approved, the development or commercialization of our product candidates could be delayed or stopped.

The manufacture of biopharmaceutical products is complex and requires significant expertise and capital investment, including the development of advanced manufacturing techniques and process controls. We and our contract manufacturers must comply with cGMP regulations and guidelines. Manufacturers of biopharmaceutical products often encounter difficulties in production, particularly in scaling up and validating initial production and contamination. These problems include difficulties with production costs and yields, quality control, including stability of the product, quality assurance testing, operator error, shortages of qualified personnel, as well as compliance with strictly enforced federal, state and foreign regulations. Furthermore, if microbial, viral or other contaminations are discovered in our products or in the manufacturing facilities in which our products are made, such manufacturing facilities may need to be closed for an extended period of time to investigate and remedy the contamination.

All of our XmAb engineered antibodies are manufactured by starting with cells which are stored in a cell bank. We have one master cell bank for each antibody manufactured in accordance with cGMP and multiple working cell banks and believe we would have adequate backup should any cell bank be lost in a catastrophic event. However, it is possible that we could lose multiple cell banks and have our manufacturing severely impacted by the need to replace the cell banks.

We cannot assure you that any stability or other issues relating to the manufacture of any of our product candidates or products will not occur in the future. Additionally, our manufacturer may experience manufacturing difficulties due to resource constraints or as a result of labor disputes or unstable political environments. If our manufacturers were to encounter any of these difficulties, or

16

otherwise fail to comply with their contractual obligations, our ability to provide any product candidates to patients in clinical trials and products to patients, once approved, would be jeopardized. Any delay or interruption in the supply of clinical trial supplies could delay the completion of clinical trials, increase the costs associated with maintaining clinical trial programs and, depending upon the period of delay, require us to commence new clinical trials at additional expense or terminate clinical trials completely. Any adverse developments affecting clinical or commercial manufacturing of our product candidates or products may result in shipment delays, inventory shortages, lot failures, product withdrawals or recalls, or other interruptions in the supply of our product candidates or products. We may also have to take inventory write-offs and incur other charges and expenses for product candidates or products that fail to meet specifications, undertake costly remediation efforts or seek more costly manufacturing alternatives. Accordingly, failures or difficulties faced at any level of our supply chain could materially adversely affect our business and delay or impede the development and commercialization of any of our product candidates or products and could have a material adverse effect on our business, prospects, financial condition and results of operations.

Adverse side effects or other safety risks associated with our product candidates could delay or preclude approval, cause us to suspend or discontinue clinical trials, abandon product candidates, limit the commercial profile of an approved label, or result in significant negative consequences following marketing approval, if any.

Undesirable side effects caused by our product candidates could result in the delay, suspension or termination of clinical trials by us, our collaborators, the FDA or other regulatory authorities for a number of reasons. If we elect or are required to delay, suspend or terminate any clinical trial of any product candidates that we develop, the commercial prospects of such product candidates will be harmed and our ability to generate product revenues from any of these product candidates will be delayed or eliminated. Serious adverse events observed in clinical trials could hinder or prevent market acceptance of the product candidate at issue. Any of these occurrences may harm our business, prospects, financial condition and results of operations significantly.

In our Phase 1a clinical trial of XmAb5871, for example, some subjects reported mild to severe gastrointestinal symptoms including nausea, vomiting, abdominal pain, abdominal discomfort, epigastric discomfort (upper stomach pain) and diarrhea. As of September 30, 2013, one patient in our on-going Phase 1b clinical trial of XmAb5871 experienced an infusion related reaction with hypotension and other adverse events that have been reported by investigators include nausea, vomiting, fever-increased temperature, headache and bronchitis. If these or other side effects cause excessive discomfort, safety risks or reduction in acceptable dosage, then the development and commercialization of XmAb5871 could suffer significant negative consequences. We cannot predict if additional types of adverse events or more serious adverse events will be observed in future clinical trials of XmAb5871, XmAb7195 or any future product candidate.

In addition, we observed detectable levels of immunogenicity, or the creation by the immune system of anti-XmAb5871 antibodies, in 44% of subjects receiving XmAb5871 in the Phase 1a clinical trial. While a common occurrence for antibody therapies, immunogenicity to XmAb5871 or any of our other product candidates could neutralize the therapeutic effects of XmAb5871 or such other candidates and/or alter their pharmacokinetics, which could have a material adverse effect on the effectiveness of our product candidates and on our ability to commercialize them.

We may not be successful in our efforts to use and expand our XmAb technology platform to build a pipeline of product candidates and develop marketable products.

We are using our proprietary XmAb technology platform to develop engineered antibodies, with an initial focus on three properties: immune inhibition, cytotoxicity and extended half-life. This platform has led to our three lead product candidates, XmAb5871, XmAb7195 and

17

XmAb5574/MOR208 as well as the other programs that utilize our technology and that are being developed by our partners and licensees. While we believe our preclinical and clinical data to date, together with our established partnerships, has validated our platform to a degree, we are at a very early stage of development and our platform has not yet, and may never lead to, approved or marketable therapeutic antibody products. Even if we are successful in continuing to build our pipeline, the potential product candidates that we identify may not be suitable for clinical development, including as a result of their harmful side effects, limited efficacy or other characteristics that indicate that they are unlikely to be products that will receive marketing approval and achieve market acceptance. If we do not successfully develop and commercialize product candidates based upon our technological approach, we may not be able to obtain product or partnership revenues in future periods, which would adversely affect our business, prospects, financial condition and results of operations.

We face significant competition from other biotechnology and pharmaceutical companies and our operating results will suffer if we fail to compete effectively.

The biotechnology and pharmaceutical industries are intensely competitive. We have competitors both in the United States and internationally, including major multinational pharmaceutical companies, biotechnology companies, universities and other research institutions. Many of our competitors have substantially greater financial, technical and other resources, such as larger research and development staff and experienced marketing and manufacturing organizations and well-established sales forces. Competition may increase further as a result of advances in the commercial applicability of technologies and greater availability of capital for investment in these industries. Our competitors may succeed in developing, acquiring or licensing on an exclusive basis drug products that are more effective or less costly than any product candidate that we are currently developing or that we may develop.

We face intense competition in autoimmune disease drug development from multiple monoclonal antibodies, other biologics and small molecules approved for the treatment of rheumatoid arthritis and autoimmune diseases many of which are being developed or marketed by large multinational pharmaceutical companies such as GlaxoSmithKline plc, AbbVie Inc., Janssen Pharmaceuticals, Inc., Roche/Genentech Inc. and Amgen Inc. GlaxoSmithKline's Benlysta (belimumab) is currently the only monoclonal antibody that we are aware of that is approved for the treatment of lupus although we believe that Biogen Idec/Genentech's Rituxan (rituximab) is prescribed, off label, for this indication. Pfizer's Xeljanz (tofacitinib), AbbVie's Humira (adalimumab), Amgen's Enbrel (etanercept), Janssen Pharmaceuticals, Inc.'s Remicade (infliximab) and Simponi (golimumab), Bristol-Myers Squibb's Orencia (abatacept) and Rituxan, among others, are approved for the treatment of rheumatoid arthritis. In addition, these and other pharmaceutical companies have monoclonal antibodies or other biologics in clinical development for the treatment of autoimmune diseases.

Many companies have approved therapies or are developing drugs for the treatment of asthma including multinational pharmaceutical companies such as GlaxoSmithKline, Roche/Genentech, Novartis AG and AstraZeneca plc. Monoclonal antibody drug development has primarily focused on allergic asthma. Xolair is currently the only monoclonal antibody that we are aware of that is approved for the treatment of severe asthma. In addition, Novartis, AstraZeneca/MedImmune and Genentech each have an antibody targeting IgE in Phase 1 or 2 clinical development for asthma.

Competition in blood cancer drug development is intense, with more than 250 compounds in clinical trials by large multinational pharmaceutical companies and Rituxan is just one of many monoclonal antibodies approved for the treatment of non-Hodgkin lymphomas or other blood cancers.

Our ability to compete successfully will depend largely on our ability to leverage our experience in drug discovery and development to:

- •

- discover and develop products that are superior to other products in the market;

18

- •

- attract qualified scientific, product development and commercial personnel;

- •

- obtain and maintain patent and/or other proprietary protection for our products and technologies;

- •

- obtain required regulatory approvals; and

- •

- successfully collaborate with pharmaceutical companies in the discovery, development and commercialization of new products.

The availability and price of our competitors' products could limit the demand, and the price we are able to charge, for any of our product candidates, if approved. We will not achieve our business plan if acceptance is inhibited by price competition or the reluctance of physicians to switch from existing drug products to our products, or if physicians switch to other new drug products or choose to reserve our products for use in limited circumstances.

Established biopharmaceutical companies may invest heavily to accelerate discovery and development of products that could make our product candidates less competitive. In addition, any new product that competes with an approved product must demonstrate compelling advantages in efficacy, convenience, tolerability and safety in order to overcome price competition and to be commercially successful. Accordingly, our competitors may succeed in obtaining patent protection, receiving FDA approval or discovering, developing and commercializing medicines before we do, which would have a material adverse impact on our business. We will not be able to successfully commercialize our product candidates without establishing sales and marketing capabilities internally or through collaborators.

Risks Relating to Our Dependence on Third Parties

Our existing partnerships are important to our business, and future partnerships may also be important to us. If we are unable to maintain any of these partnerships, or if these partnerships are not successful, our business could be adversely affected.

Because developing biologics products, conducting clinical trials, obtaining regulatory approval, establishing manufacturing capabilities and marketing approved products are expensive, we have entered into partnerships, and may seek to enter into additional partnerships, with companies that have more resources and experience than us, and we may become dependent upon the establishment and successful implementation of partnership agreements.

Our partnership and license agreements include those we have announced with Amgen, MorphoSys, Boehringer Ingelheim and others. These partnerships and license agreements also have provided us with important funding for our development programs, and we expect to receive additional funding under these partnerships in the future. Our existing partnerships, and any future partnerships we enter into, may pose a number of risks, including the following:

- •

- collaborators have significant discretion in determining the efforts and resources that they will apply to these partnerships;

- •

- collaborators may not perform their obligations as expected;

- •

- collaborators may not pursue development and commercialization of any product candidates that achieve regulatory approval or may elect not to continue or renew development or commercialization programs based on clinical trial results, changes in the collaborators' strategic focus or available funding, or external factors, such as an acquisition, that divert resources or create competing priorities;

- •

- collaborators may delay clinical trials, provide insufficient funding for a clinical trial program, stop a clinical trial or abandon a product candidate, repeat or conduct new clinical trials or require a new formulation of a product candidate for clinical testing;

19

- •

- collaborators could independently develop, or develop with third parties, products that compete directly or indirectly with our products or product candidates if the collaborators believe that competitive products are more likely to be successfully developed or can be commercialized under terms that are more economically attractive than ours, which may cause collaborators to cease to devote resources to the commercialization of our product candidates;

- •

- a collaborator with marketing and distribution rights to one or more of our product candidates that achieve regulatory approval may not commit sufficient resources to the marketing and distribution of such product or products;

- •

- disagreements with collaborators, including disagreements over proprietary rights, contract interpretation or the preferred course of development, might cause delays or termination of the research, development or commercialization of product candidates, might lead to additional responsibilities for us with respect to product candidates, or might result in litigation or arbitration, any of which would be time-consuming and expensive;

- •

- while we have generally retained the right to maintain and defend our intellectual property under our agreements with collaborators, certain collaborators may not properly maintain or defend certain of our intellectual property rights or may use our proprietary information in such a way as to invite litigation that could jeopardize or invalidate our intellectual property or proprietary information;

- •

- collaborators may infringe the intellectual property rights of third parties, which may expose us to litigation and potential liability;

- •

- collaborators may learn about our technology and use this knowledge to compete with us in the future;

- •

- results of collaborators' preclinical or clinical studies could produce results that harm or impair other products using our XmAb technology platform;

- •

- there may be conflicts between different collaborators that could negatively affect those partnerships and potentially others; and

- •

- the number and type of our partnerships could adversely affect our attractiveness to future collaborators or acquirers.