Table of Contents

As filed with the Securities and Exchange Commission on July 13, 2005

Registration No. 333-124914

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

AMENDMENT NO. 2

TO

FORM S-11

FOR REGISTRATION

Under

THE SECURITIES ACT OF 1933

Belvedere Trust Mortgage Corporation

(Exact Name of Registrant as Specified in Its Governing Instruments)

235 Pine Street, Suite 1800

San Francisco, California 94104

(415) 398-9600

(Address, Including Zip Code, and Telephone Number, including Area Code, of Registrant’s Principal Executive Offices)

Claus H. Lund

Chief Executive Officer

235 Pine Street, Suite 1800

San Francisco, California 94104

(415) 398-9600

(Name, Address, Including Zip Code, and Telephone Number, including Area Code, of Agent for Service)

Copies to:

Mark J. Kelson Armen S. Martin Manatt, Phelps & Phillips, LLP 11355 West Olympic Boulevard Los Angeles, California 90064 (310) 312-4000 | Peter T. Healy C. Brophy Christensen O’Melveny & Myers LLP 275 Battery Street San Francisco, California 94111-3305 (415) 984-8700 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434 of the Securities Act, check the following box. ¨

The registrant hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the Registration Statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities, in any state where the offer or sale is not permitted.

SUBJECT TO COMPLETION, DATED JULY 13, 2005

PROSPECTUS

[LOGO]

Shares

Belvedere Trust Mortgage Corporation

Common Stock

$ per share

We are selling shares of our common stock. We have granted the underwriters an option to purchase up to additional shares of common stock to cover over-allotments.

This is the initial public offering of our common stock. We currently expect the initial public offering price to be between $ and $ per share. Prior to this offering there has been no public market for our common stock. We have applied to have the common stock listed on the New York Stock Exchange under the symbol “BVT.”

We are externally managed and advised by BT Management Company, L.L.C., or BT Management, an affiliate of Anworth Mortgage Asset Corporation (NYSE: ANH), or Anworth. Anworth currently owns all of our stock. After this offering, Anworth will own approximately ___% of our common stock (approximately % if the underwriters exercise their over-allotment option in full). Anworth is not selling any stock in this offering. We are organized and conduct our operations to qualify as a real estate investment trust, or REIT, for federal income tax purposes commencing with the year ending December 31, 2005.

To assist us in qualifying as a REIT, ownership of our common stock by any person is generally limited to 9.8% in value or in number of shares, whichever is more restrictive. In addition, our charter contains various other restrictions on the ownership and transfer of our common stock. For additional information on the ownership and transfer restrictions on our common stock, see “Description of Capital Stock—Restrictions on Ownership and Transfer.”

Investing in our common stock involves risks. See “ Risk Factors” beginning on page 15 for a discussion of these risks, including, among others:

| • | Our use of leverage may increase any losses we incur on our planned investments and may reduce cash available for distribution. |

| • | Our efforts to manage credit risk may not be successful in limiting delinquencies and defaults in underlying loans or losses on our investments. |

| • | Interest rate mismatches between the mortgage-related assets we retain and our borrowings used to fund our purchases of mortgage-related assets might reduce our net income or result in a loss during periods of changing interest rates. |

| • | Our use of short-term debt exposes us to liquidity, market value and securitization execution risks that could result in harm to our operating results. |

| • | The mortgage-related assets and securities we own expose us to concentrated risks and thus are likely to lead to variable returns to us and our stockholders. |

| • | We depend on our manager’s personnel and the loss of any of our manager’s key personnel could severely and detrimentally affect our operations. |

| • | We pay our manager incentive compensation based on our portfolio’s performance and our profit, which may lead our manager to recommend riskier mortgage loan acquisitions in an effort to maximize its incentive compensation. |

| • | If we are disqualified as a REIT, we will be subject to tax as a regular corporation and face substantial tax liability. |

| • | As long as our principal stockholder owns a significant amount of our outstanding capital stock, your voting power may be limited. |

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||||

Public Offering Price | $ | $ | ||||

Underwriting Discount | $ | $ | ||||

Proceeds, before expenses, to us | $ | $ | ||||

The underwriters expect to deliver the shares to purchasers on or about , 2005.

| Citigroup | Flagstone Securities |

, 2005

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any state where the offer is not permitted. You should not assume that the information contained in this prospectus is accurate as of any date other than the date on the front of this prospectus.

| 1 | ||

| 14 | ||

| 15 | ||

| 37 | ||

| 38 | ||

| 38 | ||

| 39 | ||

| 40 | ||

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 41 | |

| 57 | ||

| 70 | ||

| 78 | ||

| 88 | ||

| 91 | ||

| 92 | ||

| 96 | ||

| 98 | ||

| 104 | ||

| 122 | ||

| 124 | ||

| 127 | ||

| 127 | ||

| 127 | ||

| F-1 |

Until , 2005 (25 days after the date of this prospectus), all dealers that buy, sell or trade our common stock, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

i

Table of Contents

This summary highlights information appearing elsewhere in this prospectus. It is not complete and may not contain all of the information that you may want to consider. You should read carefully the more detailed information set forth under “Risk Factors” and the other information included in this prospectus. Except where the context suggests otherwise, the terms “we,” “us” and “our” refer to Belvedere Trust Mortgage Corporation and its subsidiaries; “BT Management” and “our manager” refer to BT Management Company, L.L.C., and “Anworth” refers to Anworth Mortgage Asset Corporation. References in this prospectus to our “management,” “management team,” or “executive officers” refer to the management team of BT Management, except where the context otherwise requires. Unless indicated otherwise, the information included in this prospectus assumes no exercise by the underwriters of their option to purchase up to an additional shares of our common stock to cover over-allotments, if any.

Our Company

Our primary business is acquiring, securitizing and owning residential mortgage loans that we believe will provide attractive risk-adjusted returns. We focus on high credit-quality jumbo adjustable-rate and hybrid first-lien single-family residential mortgage loans. We acquire mortgage loans from various originators and suppliers of mortgage-related assets throughout the United States, including savings and loan associations, banks, and mortgage bankers. We hold these mortgage loans until a sufficient quantity, generally at least $200 million of loans, has been accumulated for securitization into mortgage-backed securities. This holding period may vary, but is typically about two months. We sell a portion of the mortgage-backed securities we generate in securitization transactions to third parties in the secondary market, while retaining certain subordinate and senior securities that we believe will have attractive risk-adjusted returns. To date, we have retained, on average, approximately 19% of the principal balance of the securities issued in our securitizations. While legally in the form of securities, securitized loans appear as assets on our balance sheet and are referred to as residential real estate loans securitized.

We were incorporated in Maryland on October 28, 2003 as a qualified wholly-owned real estate investment trust, or REIT, subsidiary of Anworth Mortgage Asset Corporation, or Anworth, a publicly traded REIT (NYSE: ANH). Anworth is in the business of investing primarily in United States agency and other highly rated single-family adjustable-rate and fixed-rate mortgage-backed securities and, through our company, residential mortgage loans that it acquires in the secondary market and, as of March 31, 2005, managed approximately $7.8 billion in assets. Anworth owns all of our capital stock. After this offering, Anworth will own approximately % of our common stock (approximately % if the underwriters exercise their overallotment option in full). We are externally advised and are managed under a management agreement with BT Management Company, L.L.C., or BT Management, an affiliate controlled by Anworth. Lloyd McAdams and Joe McAdams, who are officers and directors of Anworth, serve on our board of directors and our manager’s board of managers.

As of March 31, 2005, Anworth has provided us with $95.7 million in equity capital. We are conducting this offering to increase our equity capital base and intend to use the net proceeds from this offering primarily to acquire on a leveraged basis mortgage-related assets in accordance with our investment policies. As of the date of this prospectus, we have not identified any specific mortgage-related assets that we intend to acquire with the net proceeds of this offering.

Portfolio and Loan Sourcing Program

Our current portfolio is comprised of high credit-quality jumbo first-lien single-family residential mortgage loans. To a lesser extent, our portfolio also includes high credit-quality mortgage loans with conforming balances less than or equal to $359,650 (the current maximum size to conform to Federal National Mortgage Association,

1

Table of Contents

or Fannie Mae, or Federal Home Loan Mortgage Corporation, or Freddie Mac, mortgage loan requirements) that are generally acquired in larger pools that have also included jumbo mortgage loans. As of March 31, 2005, approximately 70.3% of our portfolio was made up of jumbo loans and 29.7% was made up of conforming loans, as measured by the aggregate outstanding principal balance. Our loan sourcing efforts determine the quality, consistency and volume of loans that we purchase. We have built relationships with and continue to expand upon a network of mortgage loan originators and suppliers of mortgage-related assets. As of March 31, 2005, we have acquired mortgage loans from 14 sellers with whom we have entered into purchase agreements.

As of March 31, 2005, we had a portfolio of mortgage-related assets that totaled $3 billion, which included $2.87 billion in residential mortgage loans securitized, $12 million of loans pending securitization and $59 million of mortgage-backed securities. The underlying assets of our mortgage loan portfolio consisted of 50.7% adjustable-rate mortgage, or ARM loans, 12.6% three-year hybrid mortgage loans, 29.1% five-year hybrid mortgage loans, 6.8% seven-year hybrid mortgage loans, 0.8% 10-year hybrid mortgage loans and included no fixed-rate mortgage loans. As of that date, approximately 70.3% of our mortgage loans by principal amount had initial balances in excess of conforming limits, and 48.3% were purchase loans and 51.7% were refinance loans, each as measured by aggregate outstanding balances. In addition, 53.7% of our loans were “interest-only” loans and the weighted average interest rate of our mortgage loans was 4.68%. At March 31, 2005, our mortgage loans had an average outstanding balance of approximately $377 thousand, a weighted average Fair, Isaac and Company, or FICO, score of 724 and a weighted average loan-to-value of 72.3%.

Financing and Use of Leverage

We rely primarily on securitization transactions to finance our long-term investment in mortgage-related assets. The process of securitization commences when we acquire residential mortgage loans from sellers. We generally seek to build an inventory of these loans that we believe is large enough to support an efficient securitization. We intend to account for our securitizations as financings. We structure securitization transactions primarily through taxable REIT subsidiaries (which generally are subject to full corporate taxation) which in turn establish special purpose entities, or SPEs, that issue securities through real estate mortgage investment conduit, or REMIC, trusts. We sell a portion of the mortgage-backed securities that we generate through securitizations to third parties in the secondary market, while retaining the balance. We also finance our mortgage-related assets using equity capital, unsecured debt, short-term borrowings such as repurchase agreements, whole loan financing facilities, and other collateralized financings that we may establish with approved institutional lenders. We had in place, at March 31, 2005, a variety of short-term borrowing arrangements, including repurchase agreements with four dealers. At March 31, 2005, we also had three whole loan financing facilities with credit limits totaling $950 million.

As of March 31, 2005, our liabilities totaled $2.9 billion, which included $2.3 billion in mortgage-backed securities issued through securitization transactions, $12 million of whole loan financing facilities secured by loans pending securitization and $569 million of repurchase agreements used primarily to finance the securities we have retained, which are included in residential mortgage loans securitized on our balance sheet. From our formation through March 31, 2005, we have securitized approximately $3.3 billion of mortgage loans through seven securitization transactions. Through March 31, 2005, mortgage-backed securities with an initial balance of approximately $2.6 billion had been sold to third parties and we have retained the balance, consisting of approximately $695 million of original principal. As of March 31, 2005, the weighted average interest rate of our liabilities was 3.46%. As of March 31, 2005, we had equity capital, including retained earnings, of approximately $100 million.

Risk Management

We manage credit risk primarily through the selection of high credit-quality mortgage-related assets. When acquiring mortgage loans, we focus on the aspects of a borrower’s profile and the characteristics of a mortgage

2

Table of Contents

loan product that we believe are most important in establishing strong loan performance and reduced credit exposure. We consider loans to be high quality when they are underwritten so that the borrower has adequate income to make the required loan payments, has adequate equity in the underlying property, and is willing and able to repay the mortgage as demonstrated by the borrower’s credit history. We consider a borrower to have adequate income when the borrower’s income is reasonably sufficient to cover the loan payments as well as the borrower’s other debt service obligations. Similarly, we consider loans to possess adequate equity when the unencumbered portion of the value of the property provides an incentive for the borrower to retain possession by keeping the mortgage current. As a result, the loans we acquire generally have an 80% or lower effective loan-to-value ratio based on independently appraised property values, or are seasoned loans with good payment histories. We generally require mortgage insurance on loans with stated loan-to-value ratios in excess of 80%.

We target loans where the borrower’s FICO credit rating score exceeds 660. We will from time to time acquire loans with a FICO lower than 660 when other factors, such as a borrower having high income relative to the borrower’s debt obligations, compensate for the lower credit score. We generally will not acquire loans where the borrower’s FICO score is under 620. As of March 31, 2005, our loans had a weighted average FICO score of 724. We evaluate from time to time the quality of lender underwriting criteria and appraisal standards to determine that the quality of loans, independent of FICO credit scores, meets our requirements. We also consider geographic economic conditions as part of our credit risk analysis. Credit risk mitigation includes monitoring payment performance and initiating corrective action as deemed necessary.

We have implemented a program of quality assurance for the loans we acquire. We generally use third-party firms to re-underwrite loans we acquire and to determine the accuracy of property values as given by originators and sellers. When a trade has been confirmed, we make a selection of loans for quality assurance sampling. The percentage of loans selected may vary from up to 100% for new sellers to 15% or less for sellers with whom we have a well-established track record. We may select different loans for underwriting review and appraisal review. The sample selection is based on the risk characteristics of loans, with those loans having more perceived risks being more likely to be selected for review. While we generally review the seller or originator’s underwriting guidelines, we have not established our own underwriting guidelines. Based on our analytical assessment of credit risk for each type of loan, we establish credit reserves and capital requirements to adjust for the impact of various levels of credit risk.

To the extent consistent with our election to qualify as a REIT, we follow an interest rate risk management program intended to protect our portfolio of mortgage assets and related debt against the effects of major interest rate changes. We primarily use securitization transactions to manage our interest rate risk. We believe securitizations are an attractive source of long-term funding because the terms extend for the life of the securitized mortgage loans and the payments due on the securities generally match the cash-flow from such mortgage loans. Our interest rate management program is formulated with the intent to offset, to some extent, the potential adverse effects resulting from the differences between interest rate adjustment indices and interest rate adjustment periods of our adjustable-rate mortgage-related assets and related borrowings. Prepayment risk is primarily addressed by selecting loans which we believe will exhibit more stable prepayment behaviors, including loans with prepayment penalties.

Our Strategy

We apply an operating discipline with the intent to produce attractive risk-adjusted returns. Our goal is to generate long-term value for stockholders through sustainable earnings, dividend growth and gradual increases to book value. The primary components of our strategy include:

| • | Acquiring Loans. We target acquiring jumbo first-lien single-family residential mortgage loans that are priced attractively relative to the value of mortgage-backed securities that can be issued in a securitization of those loans. We focus on the acquisition of mortgage loans at the high-end of the prime market |

3

Table of Contents

segments to limit our credit risk since we believe that borrowers with better credit histories are less likely to default on their mortgage payments. We also consider geographic diversification to be an important tool in our credit risk analysis. We target adjustable-rate mortgage loans and hybrid adjustable-rate mortgage loans (typically with fixed initial rate periods of 10 years or less). We believe it is less difficult to manage funding and risk exposures in those segments than it is for fixed-rate loans. Prepayment risk is also managed by selecting loans which management believes will exhibit more stable prepayment behaviors, including loans with prepayment penalties. |

| • | Securitizing Acquired Loans. The primary source of long-term funding for our mortgage-related assets is securitization transactions. We believe securitizing the whole loans that we acquire enables us to reduce the interest rate mismatch and prepayment risk inherent in our business. The use of securitizations also allows us to use leverage to seek to enhance spread income, while concurrently seeking to reduce liquidity risks and potentially increasing risk-adjusted returns on capital. |

| • | Owning Mortgage Assets. The primary component of the assets in our portfolio is expected to be residential mortgage loans securitized through our own securitizations. We believe that the ability to select the mortgage loans that constitute collateral for the securitizations promotes a consistent quality profile and provides us with greater certainty regarding expected performance. Based on our expected risk-adjusted returns, we anticipate retaining both senior and subordinate securities from our future securitizations. The securities we retain will be included on our balance sheet as residential mortgage loans securitized and typically will be purchased by one of our qualified REIT subsidiaries in order to maximize tax efficiency and financed with short-term borrowings, such as repurchase agreements. |

| • | Long-Term Growth. We intend to pursue a long-term growth strategy by building the infrastructure necessary to efficiently implement our growth strategy while expanding our capital base to obtain the scaling benefits of managing a large portfolio of assets. We also intend to continue to expand upon our diversified network of mortgage loan originators. In the future, we may acquire other types of mortgage assets, including second-lien mortgage loans, if we believe the risk-adjusted returns are attractive. |

Our Competitive Advantages

We believe our competitive advantages include the following:

| • | Experienced Management Team. Our management has considerable expertise in mortgage finance, asset/liability management and the acquisition and management of mortgage assets, gained from extensive experience at banks, savings and loans and mortgage banking companies. We believe that the experience of our manager’s management team will enable us to better control the acquisition and securitization of mortgage loans, and to effectively manage the credit, interest rate and prepayment risks. |

| • | Limited Fixed Expenses. Our focus is on the acquisition and securitization of whole loans because of our belief that we can utilize mortgage data in concert with our investment tools and disciplines without the corresponding overhead costs and risks associated with originating mortgage loans. We believe that the expense structure, including an expense cap, set forth in the management agreement creates an incentive for BT Management to provide us with cost-efficient services. We do not service mortgage loans ourselves and thereby further limit our fixed expenses. |

| • | Loan Sourcing Program. We have purchase agreements with a number of mortgage originators enabling us to focus on the acquisition of bulk purchases of whole loans rather than mortgage-backed securities. Such agreements and relationships provide us with more stable mortgage loan sourcing while, at the same time, allowing us to maintain more effective quality controls. In addition, due to these relationships, we may be able to negotiate with these originators to provide us with loans which have attractive pricing and features or loans originated to our program and credit guidelines. |

| • | Analytical Approach. We have developed and are using proprietary segmentation, financial and risk management models. These models assist us in acquiring loans that we believe can have more predictable |

4

Table of Contents

behaviors and can better match asset and liability characteristics, thereby increasing our prospects of achieving attractive and more stable investment spreads and returns on our invested capital. |

| • | Securitization. Our wholly-owned subsidiary, BellaVista Funding Corporation, filed a shelf registration and we issue mortgage securities through it. The name recognition of the securities provides us with an efficient way to fund our assets and a competitive advantage relative to most traditional mortgage originators. |

| • | Affiliation with Anworth. We believe a significant competitive advantage that we possess over other financial companies is BT Management’s access to the resources and expertise of Anworth, including with respect to capital markets, finance and management of a public REIT. Anworth has significant and long-standing relationships with financing sources, investment banks and others that have and we believe will continue to benefit us. Certain members of our board of directors are officers and directors of Anworth and officers and managers of BT Management whose experience we will be able to utilize in managing our business. |

Risk Factors

An investment in our common stock involves material risks, including a number of potential conflicts of interests between us, on the one hand, and Anworth, BT Management and their affiliates, on the other hand. Each prospective purchaser of our common stock should consider carefully the matters discussed under “Risk Factors” beginning on page 15 of this prospectus before investing in our common stock. Some of the risks include:

| • | our use of leverage may increase any losses we incur on our planned investments and may reduce cash available for distribution; |

| • | our efforts to manage credit risk may not be successful in limiting delinquencies and defaults in underlying loans or losses on our investments; |

| • | interest rate mismatches between the mortgage-related assets we retain and our borrowings used to fund our purchases of mortgage-related assets might reduce our net income or result in a loss during periods of changing interest rates; |

| • | our use of short-term debt exposes us to liquidity, market value and securitization execution risks that could result in harm to our financial condition; |

| • | we require a significant amount of capital, and if it is not available, our business and financial performance could be significantly harmed; |

| • | increased levels of prepayments of mortgage loans may accelerate our expenses and decrease our net income; |

| • | the mortgage-related assets and securities we own expose us to concentrated risks and thus are likely to lead to variable returns to us and our stockholders; |

| • | as of March 31, 2005, 53.7% of the loans in our portfolio are “interest only” loans, which expose us to increased risk of default; |

| • | we acquire most of our mortgage-related assets from a limited number of originators and if we fail to properly manage those relationships or if these originators experience origination problems, our ability to acquire loans from those originators could be harmed which would negatively affect our operations; |

| • | we depend on our manager’s personnel and the loss of any of our manager’s key personnel could severely and detrimentally affect our operations; |

| • | our business may be significantly harmed by a slowdown in California since as of March 31, 2005, approximately 53% of the residential mortgage loans that we owned were secured by property in California; |

5

Table of Contents

| • | we pay our manager incentive compensation based on our portfolio’s performance and our profit which may lead our manager to recommend riskier mortgage loan acquisitions in an effort to maximize its incentive compensation; |

| • | if we are disqualified as a REIT, we will be subject to tax as a regular corporation and face substantial tax liability; |

| • | a regular trading market for our common stock might not develop, which would harm the liquidity and value of our common stock; and |

| • | as long as our principal stockholder owns a significant amount of our outstanding capital stock, your voting power may be limited. |

Our Manager and Executive Officers

Our day-to-day operations are externally managed and advised by our manager, BT Management, subject to the direction and oversight of our board of directors. BT Management is owned 50% by Anworth and 50% by our executive officers, including 27.5% by Claus Lund, our chief executive officer, 17.5% by Russell Thompson, our chief financial officer, and 5.0% by Lloyd McAdams, our chairman. BT Management was incorporated in October 2003, and all of our officers are employees of BT Management.

BT Management manages our day-to-day operations in exchange for an annual base management fee and a quarterly incentive fee. Our management agreement contains an expense structure that we believe provides an incentive for our manager to manage costs carefully and to manage our business in a highly efficient manner. BT Management is responsible for its own expenses in rendering services pursuant to the management agreement, and we do not share in these expenses. The management agreement provides that certain expenses incurred by BT Management on our behalf may be reimburseable by us. The management agreement also contains an expense cap that requires BT Management to pay us for any expense payment reimbursement by it from us for our expenses with respect to any fiscal year to the extent that our operating expenses (as defined in the management agreement) for such fiscal year exceed the greater of 2% of our average historical equity or 25% of our net income for such year. To date, BT Management has not incurred any reimbursable expenses. We believe that this structure has reduced significantly our overhead costs and provided us with an opportunity to provide our stockholders with more attractive returns than would otherwise be the case. BT Management may in the future provide management or other services to other entities but does not currently provide any such services.

From time to time, we will assess whether we should be internally managed. Our assessment will be based on a number of factors deemed relevant by our board of directors, including the cost efficiency of the management agreement versus internal management, our ability to attract and retain full-time employees and the liabilities and expenses related to becoming internally managed.

Our executive officers have extensive experience in the acquisition and securitization of mortgage loans. Claus Lund, our chief executive officer, was executive vice president of mortgage asset management at Bank of America, N.A., where he, at various times, was responsible for pricing, secondary marketing and mortgage capital markets, correspondent lending, mortgage acquisitions, servicing, hedging and acquisitions, and pipeline management. While at Bank of America, Mr. Lund was responsible for management of the bank’s first-lien and second-lien mortgage loan portfolios, which at December 31, 1997, totaled approximately $51.8 billion. Russell Thompson, our chief financial officer, was manager of mortgage capital markets at Bank of America, where he was responsible for the acquisition, sale and securitization of mortgage assets. He also served as a senior vice president at Providian Financial Corporation. Lloyd McAdams, our chairman, has been the chairman and chief executive officer of Anworth since its formation in 1998, and is also chairman of the board, chief investment officer and co-founder of Pacific Income Advisers, Inc., or PIA, an investment advisory firm formed in 1986 that manages more than $4 billion in fixed income assets. He is also the chairman of Syndicated Capital, Inc., a NASD member broker-dealer.

6

Table of Contents

Each of our executive officers are also managers and officers of BT Management, as described in the following table:

Name | Position with BT Management | Position with Us | ||

| Claus H. Lund | President and Manager | Chief Executive Officer and Director | ||

| Russell J. Thompson | Executive Vice President and Treasurer | Chief Financial Officer | ||

| Lloyd McAdams | Chairman of the Board and Chief Executive Officer | Chairman of the Board | ||

The Management Agreement

A management agreement with BT Management governs the relationship between us and BT Management and describes the services to be provided by BT Management and its compensation for those services. Pursuant to the amended and restated management agreement, BT Management, subject to the supervision of our board of directors, implements our strategy, is responsible for our day-to-day operations and performs services and activities relating to our assets and operations in accordance with the terms of the management agreement. BT Management’s services for us can be divided into the following four primary activities:

| • | Asset Management—BT Management advises us with respect to, arranges for and manages the acquisition, financing, servicing, sale and securitization of, our mortgage loans; |

| • | Liability Management—BT Management arranges financing and hedging strategies; |

| • | Capital Management—BT Management coordinates our capital raising activities; and |

| • | Risk Management—BT Management evaluates the credit risk of our mortgage loans considered for acquisition as well as monitors and manages credit, prepayment and interest rate risk in our mortgage portfolio. |

Under the direction and oversight of our board of directors, BT Management advises us on the formulation of, and implements, our operating strategies and policies, arranges for our acquisition of mortgage loans, monitors the performance of our assets, arranges for various types of financing and hedging strategies, arranges for the securitization and/or sale of our mortgage loans and provides administrative and managerial services in connection with our operations.

Pursuant to the management agreement, BT Management may earn or be entitled to receive the following compensation, fees and other benefits:

| • | Base management fee—1.15% per annum of the first $300 million of our average historical equity, plus 0.85% per annum of our average historical equity in excess of $300 million during such fiscal year, calculated on a monthly basis; |

| • | Incentive compensation—for each fiscal quarter, 20% of the amount of our net income, before incentive compensation, for such quarter in excess of the amount that would produce an annualized return on equity equal to the Ten-Year U.S. Treasury Rate for such fiscal quarter plus 1%; and |

| • | Termination fee—payable only upon termination by us without cause or by BT Management upon our change of control. The actual amount of the fee will vary based upon the circumstances and would be effectuated through our purchase of our manager’s assets. |

7

Table of Contents

We believe that the expense structure set forth in the management agreement creates an incentive for BT Management to effectively manage our expenses and to provide us with cost-efficient services. Our operating and other expenses are paid by us and BT Management as follows under the management agreement:

| • | Our expenses. The expenses that we are required to pay include costs incidental to the acquisition, disposition, securitization and financing of mortgage-related assets, the compensation and expenses of operating personnel (currently there are none), marketing expenses, regular legal and auditing fees and expenses, the fees and expenses of our directors, the costs of printing and mailing proxies and reports to stockholders, the fees and expenses of our custodian and agent, if any, and the payment of any obligation of BT Management for any California gross receipts tax liability. |

| • | BT Management expenses. The expenses that BT Management is required to pay include the compensation of personnel who are performing management services for BT Management and the cost of office space, equipment and other overhead-related expenses required in connection with those personnel providing management services for BT Management. |

| • | Expense cap. BT Management is generally required to pay us for any expense payment received by BT Management from us with respect to such fiscal year to the extent that our operating expenses (as defined in the management agreement) for such fiscal year exceed the greater of 2% of our average historical equity or 25% of our net income for such fiscal year. We believe that this obligation provides BT Management with a significant incentive to provide cost-efficient services and to carefully manage our operating expenses. |

For the year ended December 31, 2004, we paid BT Management a base management fee of $624 thousand and incentive compensation of $714 thousand, for total compensation of approximately $1.34 million. Under the management agreement with BT Management the base management fee was calculated as 1.15% of our “average net invested assets,” which equaled $54.3 million for 2004. The incentive fee was calculated for each quarter during 2004 as 20% of the amount of our net income, before incentive compensation, in excess of the amount required to produce an annualized return on equity equal to the Ten-Year U.S. Treasury Rate for such quarter plus 1%, or the Threshold Amount. Our net income prior to incentive compensation for 2004 was $6.76 million and the Threshold Amount was $3.19 million. Consequently, incentive compensation was calculated as 20% of the difference between our net income and the Threshold Amount.

For the three months ended March 31, 2005, we paid BT Management a base management fee of $288 thousand and an incentive fee of $491 thousand, for total compensation of $779 thousand.

For a more detailed discussion of the compensation and other fees payable to BT Management, see “The Manager—The Management Agreement.”

Conflicts of Interest

We are subject to potential conflicts of interest involving us, Anworth and BT Management, of which Anworth owns a controlling interest. Potential conflicts of interest are as follows:

BT Management

| • | BT Management is permitted to advise accounts of other clients, and certain investment opportunities appropriate for us also will be appropriate for these accounts; |

| • | three of our directors are managers and officers of BT Management, two of whom are also owners of BT Management; |

| • | two of our executive officers are managers, officers and owners of BT Management; and |

8

Table of Contents

| • | the incentive compensation, which is based on our net income, may create an incentive for BT Management, its officers and managers, including certain of our executive officers and directors, to recommend investments with greater income potential, which may be relatively more risky than would be the case if BT Management’s compensation from us did not include an incentive-based component. |

Anworth

| • | upon completion of this offering, Anworth will own approximately % of our outstanding capital stock (approximately % of our common stock if the underwriters exercise their overallotment option in full), providing it with influence or control over matters subject to our stockholders’ approval; |

| • | Anworth owns 50% of BT Management, which is our manager; our chairman, is also chairman and chief executive officer of Anworth and owns 5% of BT Management; |

| • | two of our directors, Lloyd McAdams and Joe McAdams, are officers and directors of Anworth; |

| • | as long as Anworth controls us through the ownership of our stock, it can determine the members of our board of directors and can amend our charter and bylaws; |

| • | Anworth and its affiliates are not limited or restricted from engaging in any business or rendering services to any other person, including, without limitation, the purchase of, or rendering advice to others purchasing, mortgage-related assets including mortgage-backed securities that meet our investment guidelines; |

| • | Anworth and BT Management will enter into a services agreement upon completion of this offering under which Anworth will provide administrative services to BT Management for an agreed upon fee; and |

| • | if Anworth owns more than 50% of our common stock, it is required to consolidate us in its financial statements and could require us to take actions that may not be beneficial to our stockholders but that are beneficial to Anworth’s interests. |

For a more detailed discussion of potential conflicts of interests between us, on the one hand, and Anworth, BT Management and their affiliates, on the other hand, see “Conflicts of Interests; Certain Relationships and Related Transactions.”

Benefits to Anworth

Anworth will receive benefits in connection with and immediately following this offering. These benefits include an accretive increase in the value of our common stock held by it based on an assumed initial public offering price of $ , which is the midpoint of the range listed on the cover page of this prospectus. See “Dilution.” Further, immediately following this offering, Anworth will receive a grant of shares of restricted common stock. These restricted shares will vest equally on the first, second and third anniversaries of the date of the grant. In addition, Anworth, through its 50% ownership of BT Management, will indirectly benefit to the extent BT Management earns greater base management fees under the management agreement as a result of increased assets under management following the investment of the proceeds of this offering.

9

Table of Contents

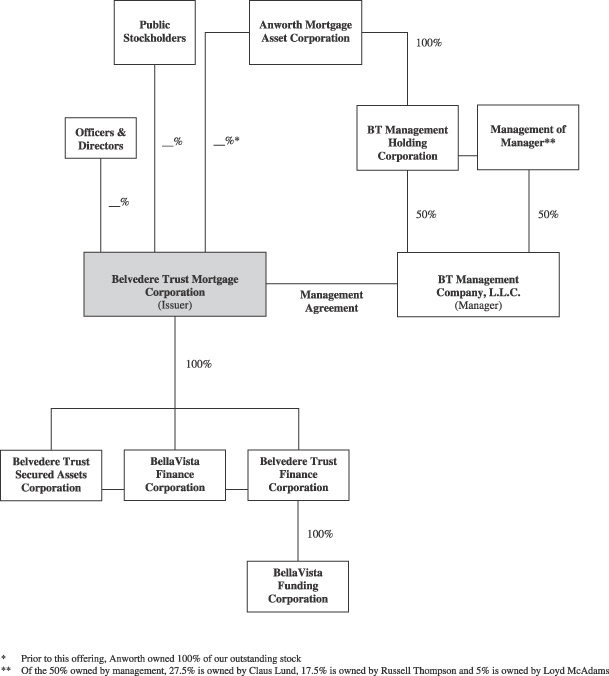

Our Structure

The chart below depicts our ownership and corporate structure immediately following this offering, and the ownership and structure of BT Management.

10

Table of Contents

The Offering

Common stock offered by us(1) | shares |

Common stock to be outstanding after this offering(2) | shares |

Use of proceeds | We estimate that the net proceeds from this offering will be approximately $ after deducting the underwriting discount and estimated offering expenses payable by us. If the underwriters exercise in full their option to purchase up to an additional shares of our common stock to cover over-allotments, our net proceeds will be approximately $ million. |

We intend to use the net proceeds of this offering to acquire on a leveraged basis mortgage-related assets in accordance with our investment policies. We will also use the net proceeds of this offering for general corporate uses. Pending these uses, we intend to invest the net proceeds of this offering in interest-bearing, short-term, marketable investment grade securities or money market accounts that are consistent with our intention to qualify as a REIT. |

Proposed NYSE symbol | “BVT” |

| (1) | Excludes up to shares of common stock that may be issued by us upon any exercise of the underwriters’ over-allotment option. |

| (2) | Includes 7,500,000 shares of our common stock outstanding prior to the offering, 2,500,000 shares of our common stock into which our outstanding preferred stock will convert upon the completion of this offering, shares of restricted common stock to be granted to our non-executive directors and employees of our manager pursuant to our 2005 Equity Incentive Plan, or the Incentive Plan, and shares of restricted common stock to be granted to our principal stockholder that will be granted separately from the Incentive Plan, concurrently with the completion of this offering. |

Unless otherwise indicated, the information in this prospectus reflects the conversion of all outstanding preferred stock into common stock upon the completion of this offering.

11

Table of Contents

Stock Ownership Limit

Subject to certain exceptions specified in our charter, no person may own, or be deemed to own by virtue of various attribution and constructive ownership provisions of the Internal Revenue Code of 1986, as amended, or the Code, more than 9.8% in value or number of shares, whichever is more restrictive, of the outstanding shares of our common stock or more than 9.8% in value of the outstanding shares of our capital stock. Our amended and restated charter will contain an exemption for Anworth from the 9.8% ownership limitation.

Our Tax Status

We intend to qualify and will elect to be taxed as a REIT under the Code commencing with our taxable year ending December 31, 2005. Provided we qualify as a REIT, we generally will not be subject to U.S. federal corporate income tax on taxable income that we distribute to our stockholders. Certain of our direct and indirect subsidiaries, however, are taxable REIT subsidiaries and, as such, are liable for corporate income tax expenses.

REITs are subject to a number of organizational and operational requirements, including a requirement that they currently distribute at least 90% of their annual REIT taxable income excluding net capital gain and the dividends paid deduction. We face the risk that we might not be able to comply with all of the REIT requirements in the future. Failure to qualify as a REIT would render us subject to U.S. federal income tax (including any applicable alternative minimum tax) on our taxable income at regular tax rates.

Investment Company Act Exemption

We intend to operate our business so as to be exempt from registration under the Investment Company Act of 1940, as amended. We will monitor our portfolio periodically and prior to each investment to confirm that we continue to qualify for the exemption. To qualify for the exemption, we intend to make investments so that at least 55% of the assets we own consist of qualifying mortgages and other liens on and interests in real estate (collectively, “qualifying real estate assets”) and so that at least another 25% of the assets we own consist of real estate-related assets (or additional qualifying real estate assets).

We generally expect that our investments in mortgage loans, mortgage-backed securities and commercial real estate debt will be considered either qualifying real estate assets or real estate-related assets under Section 3(c)(5)(C) of the Investment Company Act. To determine whether the mortgage-backed securities and commercial real estate debt constitute qualifying real estate assets or real estate-related assets we will consider the characteristics of the underlying collateral and our rights with respect to that collateral, including whether we have foreclosure rights with respect to the underlying real estate collateral.

Qualification for this exemption limits our ability to make certain investments.

Distribution Policy

To maintain our qualification as a REIT, we intend to make quarterly distributions to our stockholders that will result in annual distributions of at least 90% of our REIT taxable income, determined without regard to the deduction for dividends paid and by excluding any net capital gains. REIT taxable income is calculated pursuant to standards in the Code and will not necessarily be the same as our net income as calculated in accordance with generally accepted accounting principles in the United States of America, or GAAP. Our board of directors may, in its discretion, cause us to make additional distributions of cash legally available for that purpose. Our distributions from quarter to quarter will depend on our taxable earnings, financial condition and such other factors as our board of directors deems relevant. In the future, our board of directors may elect to adopt a dividend reinvestment plan.

12

Table of Contents

Lock-Up Arrangements

We, our directors, officers and principal stockholder will enter into lock-up agreements with the underwriters prior to the commencement of this offering pursuant to which each of these persons, with limited exceptions, for a period of 180 days for us, our directors and officers and 360 days for our principal stockholder, after the date of this prospectus, may not, without the prior written consent of Citigroup, dispose of or hedge any shares of our common stock or any securities convertible into or exchangeable for our common stock, subject to the possible extension of such restrictions under specific circumstances.

Company Information

We were incorporated in the State of Maryland in October 2003. Our headquarters are located at 235 Pine Street, Suite 1800, San Francisco, California 94104. Our phone number at that address is (415) 398-9600. Our Internet address will be www.belvederetrust.com. The information on our website or on any website referring to us is not part of this prospectus.

13

Table of Contents

The summary information presented below at or for each of the periods presented is derived from our consolidated financial statements. You should read the following selected financial data in conjunction with our consolidated financial statements and the related notes thereto, as well as with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” which are included elsewhere in this prospectus. Our past performance may not be indicative of our future results.

Quarter ended March 31, | Year ended December 31, 2004 | November 3, 2003 (inception) through December 31, 2003 | ||||||||||||||

| 2005 | 2004 | |||||||||||||||

| (in thousands, except per share data) | ||||||||||||||||

| (unaudited) | ||||||||||||||||

Consolidated Statement of Income Data: | ||||||||||||||||

Interest income | $ | 27,643 | $ | 676 | $ | 35,783 | $ | — | ||||||||

Interest expense | (23,070 | ) | (306 | ) | (27,766 | ) | — | |||||||||

Net interest income | 4,573 | 370 | 8,017 | — | ||||||||||||

Allowance for loan losses | (297 | ) | — | (591 | ) | — | ||||||||||

Other income: | ||||||||||||||||

Interest income on note receivable from stockholder | — | 349 | 330 | 416 | ||||||||||||

Gain on sale of securities | — | 157 | 158 | — | ||||||||||||

Net gain on derivative instruments | — | (203 | ) | 340 | — | |||||||||||

Total other income | — | 303 | 828 | 416 | ||||||||||||

Other expenses: | ||||||||||||||||

Incentive compensation to related party | (491 | ) | — | (714 | ) | — | ||||||||||

Management fees to related party | (288 | ) | (74 | ) | (624 | ) | (48 | ) | ||||||||

Professional services | (97 | ) | (63 | ) | (309 | ) | — | |||||||||

Set-up costs | — | — | — | (102 | ) | |||||||||||

Other expenses | (251 | ) | (155 | ) | (564 | ) | — | |||||||||

Total other expenses | (1,127 | ) | (292 | ) | (2,211 | ) | (150 | ) | ||||||||

Net income | 3,149 | 381 | 6,043 | 266 | ||||||||||||

Preferred dividend | 625 | 625 | 2,500 | 416 | ||||||||||||

Net income available to common stockholders | $ | 2,524 | $ | (244 | ) | $ | 3,543 | $ | (150 | ) | ||||||

Weighted average common shares outstanding, basic | 7,074 | 56 | 2,793 | 2 | ||||||||||||

Earnings per share, basic | $ | 0.36 | $ | (4.39 | ) | $ | 1.27 | $ | (75 | ) | ||||||

Weighted average common shares outstanding, diluted | 9,574 | 56 | 5,293 | 2 | ||||||||||||

Earnings per share, diluted | $ | 0.33 | $ | (4.39 | ) | $ | 1.14 | $ | (75 | ) | ||||||

| March 31, 2005 | December 31, 2004 | December 31, 2003 | ||||||||||||||

| (unaudited) | ||||||||||||||||

Balance Sheet Data: | ||||||||||||||||

Residential real estate loans | $ | 2,879,583 | $ | 2,628,334 | $ | — | ||||||||||

Total assets | 2,975,205 | 2,702,814 | 24,918 | |||||||||||||

Repurchase agreements | 568,888 | 544,506 | — | |||||||||||||

Whole loan financing facilities | 11,683 | 556,233 | — | |||||||||||||

Mortgage-backed securities issued | 2,259,808 | 1,494,851 | — | |||||||||||||

Total liabilities | 2,874,863 | 2,604,909 | 48 | |||||||||||||

Total stockholder’s equity | 100,342 | 97,905 | 24,870 | |||||||||||||

14

Table of Contents

An investment in our common stock involves risks. You should carefully consider the following risk factors which we believe are all of the significant risks related to this initial public offering, in addition to other information contained in this prospectus before purchasing the common stock we are offering. If any of the risks discussed in this prospectus actually occur, our business, financial condition, liquidity and results of operations could be materially harmed. If this were to occur, the price of our common stock could decline significantly. You may lose all or part of your investment. Some statements in this prospectus, including statements in the following risk factors, constitute forward looking statements. Please refer to the section entitled “Statements Regarding Forward-Looking Information.”

Risks Related to Our Business

A prolonged economic downturn or recession would harm our financial results.

The United States economy has undergone in the past and may, in the future, undergo a period of economic slowdown. An economic downturn or a recession may have a significant adverse impact on our operations and our financial condition because it could negatively affect the value of properties underlying our mortgage loans at a time when defaults on our mortgage loans are more likely. As of March 31, 2005, 4.2% of our loans had loan-to-value ratios in excess of 80% as measured by outstanding balances. Increases in unemployment rates and decreases in personal income may make it more difficult for borrowers to make payments on their loans, increasing the incidence of default. In the event of a default on any loans that we hold, we would bear the loss between the realized value of the mortgaged property and the principal amount of the loan, as well as foreclosure costs and the loss of interest. Costs of foreclosure, including costs to maintain the property and selling costs, would reduce the proceeds available to us upon default and increase our losses. As a result, if the rate of default increases, we will incur more loan losses. If property values decline, the size of losses will also increase as the value of the property securing a loan may decrease below the balance of the loan. Accordingly, we could experience larger than anticipated losses on our residential mortgage loans due to a higher loss rates on our residential mortgage loans.

Our use of short-term debt exposes us to liquidity, market value and securitization execution risks that could result in harm to our financial condition.

In order to continue our securitization operations, we require access to short-term debt. Short-term debt allows us to finance loan accumulation prior to securitization. In times of market dislocation, this type of short-term debt might become unavailable from time to time. During such periods we must reduce the volume of our loan accumulation and the number of securitizations that we undertake. We use the loans that we accumulate to collateralize the debt. The debt is recourse to us, and if the market value of the collateral declines we may need to increase the amount of collateral pledged to secure the debt or to reduce the debt amount.

Our payment of commitment fees and other expenses to obtain and maintain short-term debt may not protect us from liquidity issues or losses. Variations in lenders’ ability to access funds, lender confidence in us, lender collateral requirements, available borrowing rates, the acceptability and market values of our collateral, and other factors could force us to utilize our liquidity reserves or to sell assets and, thus, could harm our operating results, liquidity, financial condition, and earnings.

We intend to leverage our equity which may increase any losses we incur on our planned investments and may reduce cash available for distribution to you.

We incur leverage by borrowing against a substantial portion of the market value of our mortgage-related assets. Leverage increases risks, including a decline in the market value of our mortgage-related assets or a

15

Table of Contents

default of a mortgage loan. In the following ways, the use of leverage increases our risk of loss and may reduce our net income:

| • | The use of leverage increases our risk of loss resulting from various factors including rising interest rates, prepayment rates, increased interest rate volatility, downturns in the economy and reductions in the availability of financing or deterioration in the conditions of any of our mortgage-related assets. |

| • | A majority of our borrowings, including repurchase agreements, are secured by our mortgage-related assets. A decline in the market value of the mortgage-related assets used to secure these debt obligations could limit our ability to borrow or result in lenders requiring us to pledge additional collateral to secure our borrowings. In such event, we could be required to sell mortgage-related assets under adverse market conditions in order to repay our borrowings. If these sales are made at prices lower than the carrying value of the mortgage-related assets, we would experience losses. |

| • | A default of a mortgage loan that constitutes collateral for a whole loan financing could also result in an involuntary liquidation of the mortgage loan. This would result in a loss to us of the difference between the carrying value of the mortgage loan upon liquidation and the amount borrowed against the mortgage loan. |

| • | Our debt service payments will reduce the net income available for distributions to you. We may not be able to meet our debt service obligations and, to the extent that we cannot, we risk the loss of some or all of our assets to sale or foreclosure to satisfy our debt obligations. |

| • | We intend to use leverage through repurchase agreements. A decrease in the value of the assets may lead to margin calls which we will have to satisfy. We may not have the funds available to satisfy any such margin calls. There is no limitation on our leverage ratio or on the aggregate amount of our borrowings. |

| • | To the extent we are compelled to liquidate qualified REIT assets to repay debts, our compliance with the REIT requirements regarding our assets and our sources of income could be affected, which could jeopardize our status as a REIT. Losing our REIT status would cause us to lose tax advantages applicable to REITs and may decrease our overall profitability and distributions to our stockholders. |

If we are unable to complete securitizations or if we experience delayed mortgage loan sales or securitization closings, we could face a liquidity shortage which would harm our operating results.

We rely significantly upon securitizations to generate cash proceeds to repay borrowings and replenish our borrowing capacity. If there is a delay in a securitization closing or any reduction in our ability to complete securitizations, we may be required to utilize other sources of financing, which, if available at all, may not be on similar terms. In addition, delays in completing securitizations will expose us to credit and interest rate risks for this extended period of time. Several factors could affect our ability to complete securitizations of our mortgages, including, among others, the following:

| • | conditions in the securities and secondary markets; |

| • | credit quality of the mortgage loans acquired; |

| • | volume of our mortgage loan acquisitions; |

| • | our ability to obtain credit enhancements; |

| • | downgrades by rating agencies of our previous securitizations; and |

| • | lack of investor demand for purchasing components of the securities. |

Possible market developments could cause our lenders to require us to pledge additional assets as collateral. If our assets are insufficient to meet the collateral requirements, then we may be compelled to liquidate particular assets at an inopportune time.

Possible market developments, including a sharp rise in interest rates, a change in prepayment rates or increasing market concern about the value or liquidity of one or more types of mortgage-related assets in which

16

Table of Contents

our portfolio is concentrated, may reduce the market value of our portfolio, which may cause our lenders to require additional collateral. Our borrowings under repurchase agreements and whole loan financing facilities may require additional collateral if the lender determines that the collateral securing the debt is insufficient. As of March 31, 2005, we had borrowed $569 million under repurchase agreements and $12 million under whole loan financing facilities. This requirement for additional collateral may compel us to liquidate our assets at a disadvantageous time, thus harming our operating results, liquidity, financial condition, and earnings.

Interest rate mismatches between the mortgage-related assets we retain and our borrowings used to fund our purchases of the mortgage-related assets might reduce our net income or result in a loss during periods of changing interest rates.

As of March 31, 2005, all of our residential mortgage loans were subject to adjustable interest rates, including 50.7% traditional ARMs and 49.3% hybrid mortgage loans. This means that the interest rates of these assets may vary over time based on changes in a short-term interest rate index, of which there are many. We finance our acquisitions of mortgage-related assets in part with borrowings that have interest rates based on indices and repricing terms similar to, but perhaps with shorter maturities than, the interest rate indices and repricing terms of the assets. During periods of changing interest rates, this interest rate mismatch between our assets and liabilities could reduce or eliminate our net income and dividend yield and could cause us to suffer a loss. In particular, the interest rates on hybrid mortgage loans are fixed for an initial period (usually three to 10 years) during which time the assets may be funded with liabilities which have substantially shorter maturities. Some of our mortgage loans have interest rates which are based on lagging indices. The interest rates on these mortgage loans may increase slowly, even during a period of rapidly rising interest rates. In a period of rising interest rates, we could experience a decrease in, or elimination of, net income or a net loss because the interest rates on our borrowings adjust faster than the interest rates on our mortgage-related assets.

Interest rate fluctuations will also cause variances in the yield curve, which may reduce our net income. The relationship between short-term and longer-term interest rates is often referred to as the “yield curve.” If short-term interest rates rise disproportionately relative to longer-term interest rates (a flattening of the yield curve), our borrowing costs may increase more rapidly than the interest income earned on our assets. Because our assets may bear interest based on longer-term rates than our borrowings, a flattening of the yield curve would tend to decrease our net income and the market value of our mortgage-related assets. Additionally, to the extent cash flows from investments that return scheduled and unscheduled principal are reinvested in mortgage loans, the spread between the yields on the new investments and available borrowing rates may decline, which would likely decrease our net income. It is also possible that short-term interest rates may exceed longer-term interest rates (a yield curve inversion), in which event our borrowing costs may exceed our interest income and we could incur operating losses.

We may choose not to hedge, and may not be able to hedge, the risks of the interest rate mismatches.

Our business may be significantly harmed by a slowdown in the economy of California resulting in potentially higher delinquencies and increased loan losses.

At March 31, 2005, approximately 53% of the residential mortgage loans that we own are secured by property in California. An overall decline in the economy or the residential real estate market, or the occurrence of a natural disaster that is not covered by standard homeowners’ insurance policies, such as an earthquake, could decrease the value of mortgaged properties in California. This, in turn, would increase the risk of delinquency, default or foreclosure on mortgage loans held by us or underlying our mortgage-backed securities. This could cause us to experience credit losses and may harm other aspects of our business, including our ability to securitize mortgage loans.

17

Table of Contents

We have only limited experience in the business of acquiring and securitizing whole mortgage loans and we may not be successful.

We began operations in November 2003 as a subsidiary of Anworth to engage in the business of acquiring and securitizing mortgage loans. Accordingly, we have a limited operating history and no experience operating as a REIT. The acquisition of whole loans and the securitization process are inherently complex and involve risks related to the types of mortgage loans we seek to acquire, interest rate changes, funding sources, delinquency rates, prepayment rates, borrower bankruptcies and other factors that we may not be able to manage. Incorrect management of these risks may take years to become apparent. If we fail to manage these and other risks, this could harm our business and our operating results, liquidity, financial condition, and earnings. There can be no assurance that we will be able to generate sufficient revenue from operations to pay our operating expenses and make or sustain distributions to stockholders.

Our investment strategy of acquiring, accumulating and securitizing loans involves credit risk that could result in loan losses and could harm our operating results.

While we securitize the loans in order to improve our access to financing, we bear the risk of loss on any loans that we acquire and which we subsequently securitize. Accordingly, we have risk of loss for all loans we have on our balance sheet. We acquire loans that are typically not credit enhanced and that do not have the backing of Fannie Mae or Freddie Mac. Accordingly, we are subject to risks of borrower default, bankruptcy and special hazard losses (such as those occurring from earthquakes) with respect to those loans to the extent that there is any deficiency between the value of the mortgage collateral and insurance and the principal amount of the loan and any premium paid for the loan. In the event of a default on any such loans that we hold, we would bear the loss of principal between the realized value of the mortgaged property and the principal amount of the loan, as well as foreclosure costs and the loss of interest. We have not established any limits upon the geographic concentration or the credit quality of suppliers of the mortgage loans that we acquire.

Our efforts to manage credit risk may not be successful in limiting delinquencies and defaults in underlying loans or losses on our investments.

As of March 31, 2005, approximately 1.28% of the loans in our portfolio were 30 days or more delinquent by outstanding principal balance. We have incurred no losses to date, but anticipate that we will incur losses in the future. Based on our current analysis, we project loan losses to approximate 0.19% of the loan balances. This analysis is based on factors related to borrower credit, such as FICO score, as well as the value of the underlying properties relative to the loan balances.

Loan losses may be greater than we anticipated. Despite our efforts to manage credit risk, there are many aspects of credit that we cannot control, and there can be no assurance that our quality control and loss mitigation operations will be successful in limiting future delinquencies, defaults and losses. Our underwriting reviews or third-party reviews may not be effective. The securitizations in which we invest may not receive funds that we believe are due from mortgage insurance companies. Loan servicing companies may not cooperate with our loss mitigation efforts, or such efforts may otherwise be ineffective. Various service providers to securitizations, such as trustees, bond insurance providers, and custodians, may not perform in a manner that promotes our interests. The value of the homes collateralizing residential loans may decline. We acquire loans that allow for negative amortization; if the borrowers make payments that are less than the amount required to pay the interest due on these loans, the principal balance of the loans will increase. If loans become “real estate owned,” servicing companies will have to manage these properties and may not be able to sell them. Changes in consumer behavior, bankruptcy laws, and other laws may increase loan losses. In most cases, the value of the underlying property will be the sole source of funds for any recoveries. Additional loss mitigation efforts in the event that defaults increase could increase our operating costs.

An increase in interest rates might harm our book value which could harm the value of our stock.

Increases in the general level of interest rates can cause the fair market value of our assets to decline. Our hybrid adjustable-rate mortgage-related assets (during the fixed-rate component of the mortgages underlying

18

Table of Contents

such securities) and our fixed-rate mortgage-related assets, if any, will generally be more negatively affected by such increases than our adjustable-rate mortgage-related assets. In accordance with GAAP, we will be required to reduce the carrying value of any mortgage-backed securities which are held for sale by the amount of any decrease in the fair value of our mortgage-backed securities compared to their respective amortized costs. If unrealized losses in fair value occur, we will have to either reduce current earnings or reduce stockholders’ equity without immediately affecting current earnings, depending on how we classify such mortgage-backed securities under GAAP. In either case, our net book value will decrease to the extent of any realized or unrealized losses in fair value.

We require a significant amount of capital, and if it is not available, our business and financial performance could be significantly harmed.

We require substantial capital to fund our loan acquisitions, to pay our loan acquisition expenses and to hold our loans prior to securitization. Pending sale or securitization of a pool of mortgage loans, we acquire mortgage-related assets that we expect to finance through borrowings from whole loans financing facilities and repurchase facilities. It is possible that our lenders could experience changes in their ability to advance funds to us, independent of our performance or the performance of our loans. We anticipate that our repurchase facilities will be dependent on the ability of counterparties to re-sell our obligations to third parties. If there is a disruption of the repurchase market generally, or if one of our counterparties is itself unable to access the repurchase market, our access to this source of liquidity could be adversely affected. Working capital could also be required to meet margin calls under the terms of our borrowings in the event that there is a decline in the market value of the loans that collateralize our debt, the terms of short-term debt become less attractive, or for other reasons. Any of these events would harm our operating results, liquidity, financial condition, and earnings.

To date, we have been funded by our principal stockholder, Anworth Mortgage Asset Corporation, or Anworth, which had invested approximately $95.7 million in our company as of March 31, 2005 to capitalize our mortgage operations. If we fully invest all of the net proceeds of this offering and are unable to access additional external sources of capital, then we will need to either restructure the securities supporting our portfolio or, if we are unable to sell additional securities on reasonable terms or at all, we will need to either reduce our acquisition business or sell a higher portion of our loans. In the event that our liquidity needs exceed our access to liquidity, we may need to sell assets at an inopportune time, thus reducing our earnings. Adverse cash flow could threaten our ability to maintain our solvency or to satisfy the income and asset requirements necessary to elect and maintain REIT status.

We depend on borrowings to purchase mortgage-related assets and attain our desired amount of leverage. If we fail to obtain or renew sufficient funding on favorable terms, we will be limited in our ability to acquire loans and our earnings and profitability would decline.

We depend on short-term borrowings to fund acquisitions of mortgage-related assets and attain our desired amount of leverage. Accordingly, our ability to achieve our investment and leverage objectives depends to a great degree on our ability to borrow money in sufficient amounts and on favorable terms. In addition, we must be able to renew or replace our maturing short-term borrowings on a continuous basis. Moreover, we depend on a limited number of lenders to provide the primary credit facilities for our purchases of mortgage-related assets.

If we cannot renew or replace maturing borrowings, we may have to sell some of our mortgage-related assets under adverse market conditions and may incur permanent capital losses as a result. Any number of these factors in combination may cause difficulties for us, including a possible liquidation of a major portion of our portfolio at disadvantageous prices with consequent losses, which may render us insolvent.

Increased levels of prepayments of mortgage loans may accelerate our expenses and decrease our net income.

Prepayments on our mortgage-related assets generally increase when interest rates decrease,. If we acquire mortgages at a premium and they are subsequently repaid before their final maturity, we must accelerate the

19

Table of Contents

recognition of the expense for the unamortized premium at the time of the prepayment. Also, if prepayments on mortgages increase when interest rates are declining, our net interest income may decrease if we cannot reinvest the prepaid principal in mortgage-related assets bearing comparable rates or higher rates. Accordingly, prepayments could harm our operating results, liquidity, financial condition, and earnings.

Representations and warranties made by us in loan sales and securitizations may subject us to liability that could result in loan losses and could harm our operating results.

In connection with securitizations, we make representations and warranties regarding the mortgage-related assets transferred into securitization trusts. The trustee in the securitizations has recourse to us with respect to the breach of the standard representations and warranties regarding the loans made at the time such mortgage-related assets are transferred. While we generally have recourse to our loan originators for any such breaches, there can be no assurance of the originators’ abilities to honor their respective obligations. We attempt to generally limit the potential remedies of the trustee to the potential remedies we receive from the originators from whom we acquired the mortgage loans. However, in some cases, the remedies available to the trustee may be broader than those available to us against the originators of the mortgage-related assets and should the trustee enforce its remedies against us, we may not always be able to enforce whatever remedies we have against our originators. Furthermore, if we discover, prior to the securitization of a loan, that there is any fraud or misrepresentation with respect to the mortgage and the originator fails to repurchase the mortgage, then we may not be able to sell the mortgage or may have to sell the mortgage at a discount.

Any hedging strategies we utilize may not be successful in mitigating our risks associated with interest rates and could result in loan losses.