QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on June 28, 2005

Registration No. 333-125007

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

TO

FORM S-1

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

GOLF GALAXY, INC.

(Exact name of Registrant as specified in its charter)

| Minnesota (State or other jurisdiction of incorporation or organization) | 5940 (Primary Standard Industrial Classification Code Number) | 41-1831724 (I.R.S. Employer Identification No.) | ||

7275 Flying Cloud Drive Eden Prairie, Minnesota 55344 (952) 941-8848 (Address, including zip code, and telephone number, including area code, of Registrant's principal executive offices) | ||||

Randall K. Zanatta President, Chief Executive Officer and Chairman Golf Galaxy, Inc. 7275 Flying Cloud Drive Eden Prairie, Minnesota 55344 (952) 941-8848 (Name, address, including zip code, and telephone number, including area code, of agent for service) | ||||

Copies to: | ||

| John R. Houston, Esq. Robins, Kaplan, Miller & Ciresi L.L.P. 2800 LaSalle Plaza 800 LaSalle Avenue Minneapolis, Minnesota 55402-2015 (612) 349-8500 | David B. Miller, Esq. Michael K. Coddington, Esq. Faegre & Benson LLP 2200 Wells Fargo Center 90 South Seventh Street Minneapolis, Minnesota 55402-3901 (612) 766-7000 | |

Approximate date of commencement of proposed sale to public:

As soon as practicable after this registration statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box: o

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Subject to completion, dated June 28, 2005

The information in this prospectus is not complete and may be changed. We may not sell these securities until the Securities and Exchange Commission declares our registration statement effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Shares

| GOLF GALAXY, INC. |  |

Common Stock

$ per share

- •

- Golf Galaxy, Inc. is offering shares and selling shareholders are offering shares. We will not receive any proceeds from the sale of our shares by the selling shareholders.

- •

- We anticipate that the initial public offering price will be between $ and $ per share.

- •

- This is our initial public offering and no public market currently exists for our shares.

- •

- Reserved trading symbol: Nasdaq National Market—GGXY

This investment involves risk. See "Risk Factors" beginning on page 9.

| | Per Share | Total | ||||

|---|---|---|---|---|---|---|

| Public offering price | $ | $ | ||||

| Underwriting discount | $ | $ | ||||

| Proceeds, before expenses, to Golf Galaxy, Inc. | $ | $ | ||||

| Proceeds, before expenses, to selling shareholders | $ | $ | ||||

The underwriters have a 30-day option to purchase up to additional shares of common stock from selling shareholders to cover over-allotments, if any. We will not receive any of the proceeds from the sale of such shares by the selling shareholders.

Neither the Securities and Exchange Commission nor any state securities commission has approved of anyone's investment in these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Piper Jaffray | William Blair & Company |

| A.G. Edwards | Wedbush Morgan Securities |

The date of this prospectus is , 2005.

| | Page | |

|---|---|---|

| Summary | 1 | |

Risk Factors | 9 | |

A Special Note Regarding Forward Looking Statements | 20 | |

Use of Proceeds | 22 | |

Dividend Policy | 22 | |

Capitalization | 23 | |

Dilution | 26 | |

Selected Financial Information | 28 | |

Management's Discussion and Analysis of Financial Condition and Results of Operations | 32 | |

Business | 52 | |

Management | 71 | |

Certain Relationships and Related Party Transactions | 80 | |

Principal and Selling Shareholders | 82 | |

Description of Capital Stock | 85 | |

Shares Eligible for Future Sale | 88 | |

U.S. Federal Tax Consequences for Non-U.S. Holders | 90 | |

Underwriting | 94 | |

Legal Matters | 97 | |

Experts | 97 | |

Where You Can Find More Information | 97 | |

Index to Financial Statements | F-1 |

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized any other person to provide you with different information. This prospectus is not an offer to sell, nor is it seeking an offer to buy, these securities in any state where the offer or sale is not permitted. The information in this prospectus is complete and accurate as of the date on the front cover, but the information may have changed since that date.

"Golf Galaxy", "Everything for the Game.", "Outward 9", "Rae's Creek" and our other marks mentioned or used in this prospectus are our registered trademarks and service marks. This prospectus also contains trademarks and service marks belonging to other entities.

i

The items in the following summary are described in more detail later in this prospectus. This summary provides an overview of selected information and does not contain all the information you should consider. Therefore, you should also read the more detailed information set out in this prospectus, including the financial statements and the related notes appearing elsewhere in this prospectus.

Golf Galaxy, Inc.

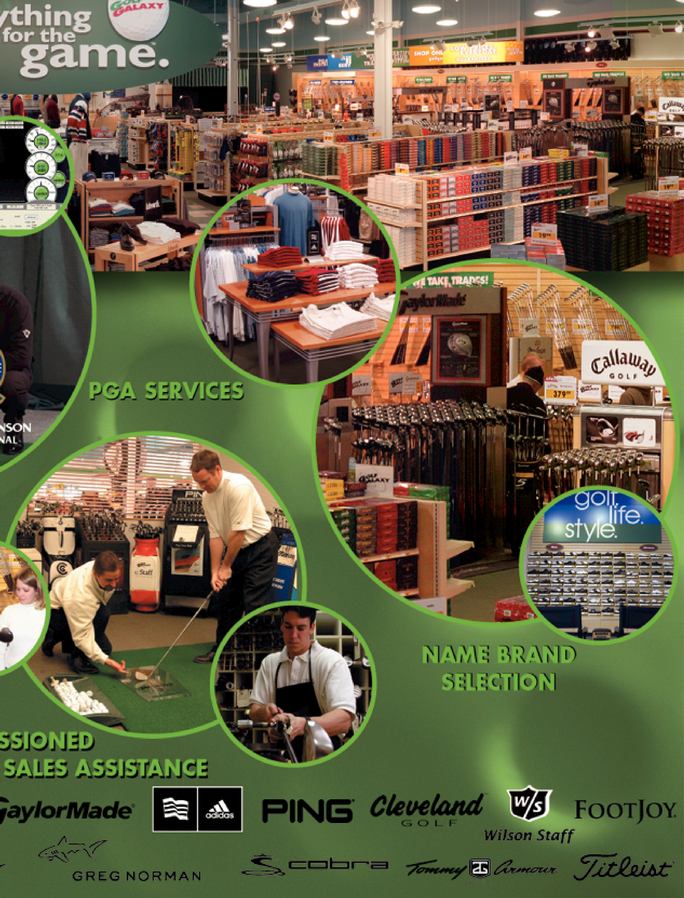

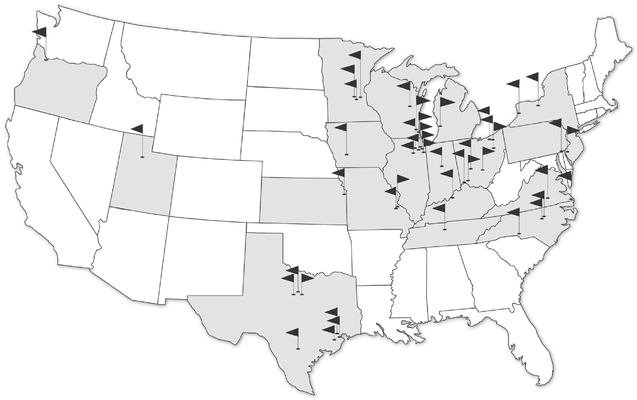

We are a leading golf specialty retailer offering a distinctive combination of competitively priced merchandise from the leading national brands in golf equipment and apparel, together with non-commissioned sales assistance and pro shop services. Our 45 superstores, generally ranging from 13,000 to 18,000 selling square feet, are located in 19 states. Our "Everything for the Game." core strategy is to provide avid and casual golfers, as well as gift purchasers, a category dominant selection of leading national brand products, expert sales assistance and professional services, the combination of which is generally not available elsewhere. We offer our customers an exciting, interactive environment that contrasts sharply with the shopping experience at smaller independent golf stores, on-course pro shops and the golf departments of general sporting goods retailers.

Key to our strategy is our focus on the leading national brands in golf, rather than promoting private label products or lesser known brands. Our non-commissioned sales associates and PGA professionals offer customers knowledgeable advice and expertise. We believe this selling strategy is distinctive and builds a trust relationship that is critical to creating long-term customer loyalty and encouraging word of mouth referrals. We employ a consultative selling approach that focuses on maximizing each customer relationship for the long-term by delivering the best solution for each golfer. For instance, in the clubs category, we utilize our expertise to custom fit clubs to our customers' needs. We also build customer loyalty through exclusive Advantage Club member in-store events and offers.

Our stores feature full-time Professional Golfers' Association of America (PGA) professionals who offer customers a specialized level of expertise and service. Our value-added pro shop services, directed by our in-store PGA professionals, utilize state-of-the-art technology and facilities. These services, which we refer to as "PGA services", include golf lessons featuring digital video swing analysis, club and ball fittings using high-speed ball launch monitors and full-service club repair and upgrade services. Our professionally designed "superstore" format features a racetrack layout highlighting broad product offerings along with many interactive features, such as an artificial bent grass putting green and golf simulators.

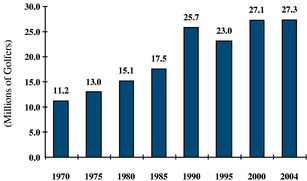

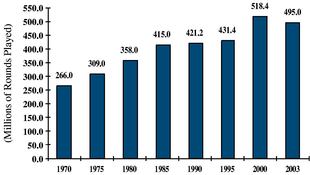

According to the National Golf Foundation (NGF), an independent industry research firm, the aggregate size of the U.S. golf market was estimated at $24.3 billion in 2002, which included spending on greens fees, equipment and accessories, and food and beverages. Golf clubs, balls, bags, gloves and footwear represented $4.7 billion of this total. The golf market, as defined by the NGF, does not include certain products that we sell such as pre-owned clubs, golf and casual apparel, and golf-related gifts, novelties and services. We estimate the total golf market we serve, including these additional products and services, is over $7.5 billion.

We believe our combination of leading national brands, a commitment to superior customer service, and interactive store features, together with our guaranteed low prices, provides a distinctive superstore concept which will enable us to achieve our objective of becoming the nation's leading golf specialty retailer.

1

Competitive Strengths

We believe that a combination of factors creates a distinctive retail concept that distinguishes us from our competitors and is key to our continuing success. These factors include the following:

- •

- our extensive selection of leading national brands in golf equipment, which we believe are preferred by most golfers;

- •

- our extensive assortment and professional merchandising of golf apparel and footwear;

- •

- our commitment to a superior level of customer service, golf expertise and value-added PGA services;

- •

- our full-time, in-store PGA professionals who use our state-of-the-art technology and facilities to provide our customers with specialized PGA services;

- •

- our superstore format that offers a distinctive combination of extensive product assortments and golf-related services in a fun and interactive setting;

- •

- our marketing program that we believe gives us, in most of our markets, the leading share of voice in advertising in the golf category, and which includes our complimentary "Advantage Club" customer loyalty program;

- •

- our "Low Prices. Everyday. Guaranteed." policy that extends 30 days beyond the purchase date to protect our customers in the event they find a lower price;

- •

- our comprehensive competitive shopping program that monitors in-store pricing at our competitors allowing us to proactively adjust our prices to match local competition; and

- •

- our management team with extensive superstore and golf industry experience.

Growth Strategy

Our long-term objectives are to build the Golf Galaxy brand and to become the nation's leading golf specialty retailer. Over the past few years, we have made significant investments in our infrastructure, including information systems and experienced management, to support our growth strategy. To achieve our goal, we plan to expand our store base, including a total of 14 to 16 new stores in the current fiscal year, of which eleven have already been opened, and 14 to 16 new stores in fiscal 2007. We also plan to focus on leveraging our efficient direct-to-store distribution model that eliminates the need to support store growth with costly warehouse facilities, systems and related inventory; pursue a number of initiatives to continue to grow comparable store sales and increase store profitability; and expand our direct sales through both our eCommerce operations and toll-free telephone orders, both of which are supported by our in-house fulfillment and customer contact center.

Risks Affecting Us

Our business is subject to numerous risks as discussed more fully in the section entitled "Risk Factors" immediately following this Summary. In particular, the risks affecting us include the following:

- •

- we depend on the continued popularity of golf and golf-related products, the continued development of new golf-related products, and our ability to purchase and sell such products;

2

- •

- our ability to execute our accelerated growth strategy profitably in new and existing markets;

- •

- the effect of competition in our industry;

- •

- the effects of the economy;

- •

- the effects of weather;

- •

- if our business continues to grow, the continued growth may place strains on our systems and management team; and

- •

- if we are not able to access additional capital, our ability to expand our business may be impaired.

Office Location

Our principal executive offices are located at 7275 Flying Cloud Drive, Eden Prairie, Minnesota 55344 and our telephone number is (952) 941-8848. Our Internet site is located atwww.golfgalaxy.com. The information contained in our Internet site is not a part of this prospectus.

3

The Offering

| | | |||

|---|---|---|---|---|

| Common stock offered: | ||||

| By us | shares | |||

| By selling shareholders | shares | |||

| Total | shares | |||

| Common stock outstanding after the offering | shares | |||

| Offering price | $ per share | |||

| Use of proceeds | We intend to use our net proceeds from this offering, together with cash provided by operations and, if necessary, funds available under our credit facility, to continue to open new retail stores across the country and for general corporate purposes, including potential acquisitions, and we will use approximately $ million of our net proceeds to pay our preferred shareholders all of the accrued and unpaid dividends due upon conversion of their shares of outstanding preferred stock into shares of our common stock. We will not receive any of the proceeds from the sale of common stock offered by the selling shareholders. See "Use of Proceeds." | |||

Reserved Nasdaq National Market symbol | GGXY | |||

The number of shares of common stock outstanding after this offering excludes, as of June 27, 2005:

- •

- 873,125 shares of our common stock issuable upon exercise of currently outstanding options under our 1996 Stock Option and Incentive Plan, as amended (1996 Plan), at a weighted average exercise price of $5.43 per share;

- •

- 30,325 shares of our common stock reserved for future grants under our 1996 Plan;

- •

- 165,900 shares of our common stock issuable upon exercise of currently outstanding options under our 2004 Stock Incentive Plan (2004 Plan), at a weighted average price of $7.69 per share;

- •

- 167,500 shares of our common stock issuable to certain employees upon the exercise of options authorized for issuance under our 2004 Plan effective as of the date of this prospectus, at an exercise price equal to the price per share of our common stock sold in this offering;

- •

- 666,600 shares of our common stock reserved for future grants under our 2004 Plan; and

- •

- 14,921 shares of our common stock issuable upon exercise of an outstanding warrant having an exercise price of $6.30 per share.

Except as otherwise indicated, all information in this prospectus assumes:

- •

- no exercise of the underwriters' over-allotment option;

- •

- all outstanding shares of our preferred stock will convert into shares of common stock upon the closing of this offering; and

- •

- no outstanding options have been exercised since June 27, 2005.

4

You should read the summary financial data presented below in conjunction with the financial statements and the related notes and "Management's Discussion and Analysis of Financial Condition and Results of Operations" included elsewhere in this prospectus. Historical results are not necessarily indicative of the results of operations expected for future periods. Quarterly results are not necessarily indicative of full year results. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Quarterly Results of Operations and Seasonality."

Our fiscal year ends on the Saturday closest to the end of February, resulting in fiscal years of 52 or 53 weeks in length. Fiscal 2001, 2002, 2003, 2004 and 2005 represent the periods ended March 3, 2001, March 2, 2002, March 1, 2003, February 28, 2004 and February 26, 2005. Based on this schedule, fiscal 2001 was a 53-week year and all other fiscal years presented were 52-week years.

| | Fiscal Year Ended | Three Months Ended | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | March 3, 2001 | March 2, 2002 | March 1, 2003 | February 28, 2004 | February 26, 2005 | May 29, 2004 | May 28, 2005 | ||||||||||||||||

| | (in thousands, except per share data) | ||||||||||||||||||||||

| Statement of Operations Data | |||||||||||||||||||||||

| Net sales | $ | 77,608 | $ | 88,889 | $ | 85,213 | $ | 99,630 | $ | 133,080 | $ | 38,419 | $ | 58,570 | |||||||||

| Cost of sales | 59,033 | 67,909 | 63,745 | 72,403 | 93,964 | 26,856 | 40,342 | ||||||||||||||||

| Gross profit | 18,575 | 20,980 | 21,468 | 27,227 | 39,116 | 11,563 | 18,228 | ||||||||||||||||

| Operating expenses: | |||||||||||||||||||||||

| Store operating | 15,315 | 16,887 | 15,223 | 16,677 | 24,382 | 6,972 | 10,932 | ||||||||||||||||

| General and administrative | 5,659 | 6,803 | 4,709 | 6,876 | 8,372 | 2,147 | 3,102 | ||||||||||||||||

| Preopening | 1,433 | 260 | 113 | 1,065 | 2,095 | 518 | 1,310 | ||||||||||||||||

| Income (loss) from operations | (3,832 | ) | (2,970 | ) | 1,423 | 2,609 | 4,267 | 1,926 | 2,884 | ||||||||||||||

| Other income | — | — | — | — | 8,410 | (1) | — | — | |||||||||||||||

| Interest (expense) income, net | (441 | ) | (153 | ) | (109 | ) | (177 | ) | (4 | ) | (36 | ) | 15 | ||||||||||

| Income (loss) before income taxes | (4,273 | ) | (3,123 | ) | 1,314 | 2,432 | 12,673 | 1,890 | 2,899 | ||||||||||||||

| Income tax benefit (expense) | — | — | — | 5,145 | (2) | (5,135 | ) | (765 | ) | (1,206 | ) | ||||||||||||

| Net income (loss) | (4,273 | ) | (3,123 | ) | 1,314 | 7,577 | 7,538 | 1,125 | 1,693 | ||||||||||||||

| Less preferred stock dividends | — | (7,546 | ) | (3,169 | ) | (3,430 | ) | (3,696 | ) | (901 | ) | (998 | ) | ||||||||||

| Net (loss) income applicable to common shareholders | $ | (4,273 | ) | $ | (10,669 | ) | $ | (1,855 | ) | $ | 4,147 | $ | 3,842 | $ | 224 | $ | 695 | ||||||

| Net (loss) income per share: | |||||||||||||||||||||||

| Basic | $ | (2.42 | ) | $ | (6.03 | ) | $ | (1.03 | ) | $ | 2.29 | $ | 2.06 | $ | 0.12 | $ | 0.37 | ||||||

| Diluted | $ | (2.42 | ) | $ | (6.03 | ) | $ | (1.03 | ) | $ | 0.99 | $ | 0.98 | $ | 0.11 | $ | 0.21 | ||||||

| Weighted average basic shares outstanding | 1,768 | 1,771 | 1,800 | 1,814 | 1,866 | 1,862 | 1,884 | ||||||||||||||||

| Weighted average diluted shares outstanding | 1,768 | 1,771 | 1,800 | 7,691 | 7,721 | 1,951 | 8,043 | ||||||||||||||||

5

| | Fiscal Year Ended | Three Months Ended | ||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | March 3, 2001 | March 2, 2002 | March 1, 2003 | February 28, 2004 | February 26, 2005 | May 29, 2004 | May 28, 2005 | |||||||||||||||

| | (dollars in thousands) | |||||||||||||||||||||

| Other Financial Data | ||||||||||||||||||||||

| Gross profit as a percentage of sales | 23.9 | % | 23.6 | % | 25.2 | % | 27.3 | % | 29.4 | % | 30.1 | % | 31.1 | % | ||||||||

| Store contribution(3) | $ | 3,260 | $ | 4,093 | $ | 6,245 | $ | 10,550 | $ | 14,734 | $ | 4,591 | $ | 7,296 | ||||||||

| Store contribution margin(4) | 4.2 | % | 4.6 | % | 7.3 | % | 10.6 | % | 11.1 | % | 11.9 | % | 12.5 | % | ||||||||

| Adjusted EBITDA(5) | $ | (1,423 | ) | $ | (334 | ) | $ | 3,821 | $ | 5,010 | $ | 7,496 | $ | 2,633 | $ | 4,026 | ||||||

Store Data | ||||||||||||||||||||||

| Comparable store sales increase (decrease)(6) | 2.4 | % | 0.1 | % | (2.4 | )% | 5.6 | % | 6.7 | % | 7.4 | % | 10.5 | % | ||||||||

| Number of stores at end of period | 19 | 20 | 20 | 24 | 34 | 29 | 45 | |||||||||||||||

| Selling square feet at end of period(7) | 314,861 | 328,257 | 328,257 | 382,169 | 516,551 | 450,370 | 676,380 | |||||||||||||||

| Average inventory per store(8) | $ | 993 | $ | 925 | $ | 870 | $ | 863 | $ | 872 | — | — | ||||||||||

(1)Represents the gain realized on the sale of our equity investment in Golf Town Canada Inc. See "Business—Golf Town Canada."

(2)The income tax benefit in fiscal 2004 is due to the reversal of an income tax valuation allowance against our net deferred tax assets generated in prior fiscal years, partially offset by the fiscal 2004 income tax provision. See "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Notes to Financial Statements" elsewhere in this prospectus for more information.

(3)Store contribution consists of income (loss) from operations, before the effect of general and administrative costs and pre-opening costs. This term, as we define it, may not be comparable to a similarly titled measure used by other companies and is not a measure of performance presented in accordance with GAAP. We use store contribution as a measure of operating performance for our retail operations as a supplement, but not as a substitute for income (loss) from operations or other financial data prepared in accordance with GAAP.

We believe store contribution is useful to an investor evaluating our operating performance because:

- •

- it provides a measure of the incremental contribution of store operations without the impact of general and administrative costs; and

- •

- it helps investors more meaningfully evaluate and compare the results of our operations from period to period by removing the impact of the cost of opening new stores, which varies due to the timing, location, format and number of new store openings.

Our management uses store contribution:

- •

- to assist in evaluating retail operating performance because we believe it provides:

- –

- a measure of the incremental contribution of store operations net of advertising and depreciation without the impact of general and administrative costs; and

- –

- a measure of the results of retail operations excluding the incremental costs related to preparing and opening new stores, which do not directly impact the operating results of existing stores and vary from period to period depending on the timing, location, format and number of new store openings; and

- •

- in presentations to the members of our board of directors to enable our board to have the same consistent measurement basis of operating performance used by management.

6

The following table provides a reconciliation of income (loss) from operations to store contribution.

| | Fiscal Year Ended | Three Months Ended | |||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | March 3, 2001 | March 2, 2002 | March 1, 2003 | February 28, 2004 | February 26, 2005 | May 29, 2004 | May 28, 2005 | ||||||||||||||

| | (dollars in thousands) | ||||||||||||||||||||

| Income (loss) from operations | $ | (3,832 | ) | $ | (2,970 | ) | $ | 1,423 | $ | 2,609 | $ | 4,267 | $ | 1,926 | $ | 2,884 | |||||

| General and administrative expenses | 5,659 | 6,803 | 4,709 | 6,876 | 8,372 | 2,147 | 3,102 | ||||||||||||||

| Preopening expenses | 1,433 | 260 | 113 | 1,065 | 2,095 | 518 | 1,310 | ||||||||||||||

| Store contribution | $ | 3,260 | $ | 4,093 | $ | 6,245 | $ | 10,550 | $ | 14,734 | $ | 4,591 | $ | 7,296 | |||||||

(4)Calculated as store contribution divided by net sales for the fiscal period. See footnote 3, above, for a discussion of store contribution and a reconciliation of income (loss) from operations to store contribution.

(5)Adjusted EBITDA consists of net income (loss), before the effect of net interest expense, income tax expense or benefit, non-operating income and depreciation and amortization. This term, as we define it, may not be comparable to a similarly titled measure used by other companies and is not a measure of performance presented in accordance with GAAP. We use Adjusted EBITDA as a measure of operating performance, but we do not use it as a measure of liquidity. Adjusted EBITDA should not be used as a measure of liquidity or considered as a substitute for net income (loss), net cash provided by or used in operations, or other financial data prepared in accordance with GAAP.

We believe Adjusted EBITDA is useful to an investor in evaluating our operating performance because:

- •

- it measures our operating performance without regard to items such as depreciation and amortization, which can vary depending upon accounting methods, the book value of assets, and the method by which assets were acquired;

- •

- it helps investors more meaningfully evaluate and compare the results of our operations from period to period by removing the impact of our capital structure, primarily net interest expense from our credit facility, and our non-operating income; and

- •

- it helps investors more meaningfully evaluate and compare the results of our operations from period to period by removing the impact of net income tax expense or benefit, which can vary over time based on changes in management's estimates and assumptions related to current and future operating results, income tax rates and income tax laws.

Our management uses Adjusted EBITDA:

- •

- as a measurement of operating performance because it assists us in comparing our performance on a consistent basis, as it removes from our operating results the impact of:

- –

- our asset base, including the impact of depreciation and amortization of our assets, which can vary depending on the book value and method of acquisition of the assets;

- –

- income tax expense or benefit, which can vary significantly based on management's estimates and assumptions related to current and future operating results, tax rates and regulations;

- –

- our capital structure, including the impact of interest expense from our credit facility and interest income on invested funds; and

- –

- our non-operating income; and

- •

- in presentations to the members of our board of directors to enable our board to have the same consistent measurement basis of operating performance used by management.

7

The following table provides a reconciliation of net income (loss) to Adjusted EBITDA.

| | Fiscal Year Ended | Three Months Ended | |||||||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | March 3, 2001 | March 2, 2002 | March 1, 2003 | February 28, 2004 | February 26, 2005 | May 29, 2004 | May 28, 2005 | ||||||||||||||||

| | (dollars in thousands) | ||||||||||||||||||||||

| Net income (loss) | $ | (4,273 | ) | $ | (3,123 | ) | $ | 1,314 | $ | 7,577 | $ | 7,538 | $ | 1,125 | $ | 1,693 | |||||||

| Adjusted for: | |||||||||||||||||||||||

| Income tax (benefit) expense | — | — | — | (5,145 | ) | 5,135 | 765 | 1,206 | |||||||||||||||

| Interest expense (income), net | 441 | 153 | 109 | 177 | 4 | 36 | (15 | ) | |||||||||||||||

| Other income | — | — | — | — | (8,410 | ) | — | — | |||||||||||||||

| Depreciation and amortization | 2,409 | 2,636 | 2,398 | 2,401 | 3,229 | 707 | 1,142 | ||||||||||||||||

| Adjusted EBITDA | $ | (1,423 | ) | $ | (334 | ) | $ | 3,821 | $ | 5,010 | $ | 7,496 | $ | 2,633 | $ | 4,026 | |||||||

(6)A new or relocated store is included in the comparable store base after it has been in operation for 12 full fiscal months following the month of the store's grand opening weekend. A store that is closed for remodel or repair is excluded from the comparable store sales calculation during the period of closure and the comparable period of the succeeding year. Sales from our eCommerce operations are not included in the comparable store sales calculation. Comparable store results for a 53-week fiscal year are presented on a 52/52 week basis.

(7)We define selling square feet to include all space where we conduct retail activities with our customers, including the PGA services area, hitting nets, golf simulators and check-out areas. Selling square feet excludes our receiving and back room storage areas, management office space, employee breakrooms, restrooms and vacant space.

(8)Average inventory per store represents the 12 fiscal month average inventory for stores open through the full fiscal year excluding our eCommerce operations. Inventory includes inventory at average cost, before adjustments for shrink, obsolescence, capitalized freight and vendor funding.

Recent Developments

For the fiscal month ended July 2, 2005, our net sales were $ , an increase of % over net sales of $ for the comparable period of the prior fiscal year. The increase reflected additional sales from new stores opened in fiscal 2005 and the first quarter of fiscal 2006, and a comparable store sales increase of % for the fiscal month ended July 2, 2005. These results are not necessarily indicative of full quarter or full year results.

8

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below before participating in this offering. If any of the following risks actually occur, our business, financial condition, operating results or cash provided by operations could be materially harmed. As a result, the trading price of our common stock could decline, and you might lose all or part of your investment. When determining whether to buy our common stock, you should also refer to the other information in this prospectus, including our financial statements and the related notes.

Risks Related to Golf Galaxy, Inc.

A decline in the popularity of golf or the market for golf-related products and services could materially adversely affect our sales and profitability.

We generate substantially all of our sales from the sale of golf-related equipment, apparel and services. The demand for our products and services is directly related to the popularity of golf, including the number of golf participants, the number of rounds of golf being played by these participants, and television viewership of and attendance at professional and other golf tournaments and events. According to the NGF, the number of golf rounds played declined slightly from 2001 to 2003 due, we believe, to a number of factors including a decline in the stock market, a weak economy, reduced leisure travel and unfavorable weather. If golf participation or golf rounds played significantly decreases, sales of our products and services could be materially adversely affected. We depend on the exposure of the brands we sell to reinforce the quality of the products we sell. Any significant reduction in television coverage of professional or other golf tournaments and events, or any other significant decreases in either attendance at golf tournaments or viewership of golf tournaments, will reduce the visibility of the brands we sell and could materially adversely affect our sales and profitability.

If our key suppliers limit the amount or variety of products they sell to us or provide us less favorable pricing, allowances or other terms, our sales and profitability could be materially adversely affected.

We rely on a limited number of suppliers of the leading national brands in golf for a majority of our sales. During fiscal 2005, we purchased approximately 60% of our merchandise from our five largest suppliers. Three of our suppliers that provide multiple golf brands, namely Acushnet Company (Titleist,FootJoy andCobra), Callaway Golf Company (Callaway,Odyssey,Top-Flite andBen Hogan) and Taylor Made Golf Company (TaylorMade,adidas andMaxfli), each represented more than 10% of our purchases. Our extensive assortment of leading national brand merchandise is one of our key competitive strengths. Our customers expect to find the leading national brands and the newest products in the market in our stores. We are also subject to risks, such as the unavailability of raw materials, labor disputes, union organizing activity, strikes, inclement weather, natural disasters, war and terrorism, and adverse general economic and political conditions, as well as the high demand for popular products, that might limit our suppliers' ability to provide us with quality merchandise on a timely basis. Due to our extensive purchases of merchandise, we benefit from vendor pricing allowances and marketing support in the ordinary course of business. We have no long-term contractual arrangements providing for continued supply, pricing, allowances or other terms from our key suppliers and our suppliers may discontinue selling to us, or may alter pricing, allowances or other terms at any time. If our suppliers refuse to distribute their products to us, limit the amount or variety of products they distribute to us, or provide us with less favorable pricing, allowances or other terms, our sales and profitability may be materially and adversely affected.

9

Our sales and profitability could be materially adversely affected if our suppliers fail to develop and introduce new products or if the introduction of new products results in excessive close-outs of existing inventories.

Our future success will depend, in part, upon our suppliers' continued ability to develop and introduce innovative products in the golf equipment market that appeal to our customers. The success of new products depends in part upon the various subjective preferences of golfers, including a golf club's "look and feel," and the level of acceptance that the golf product has among professional and recreational golfers. The subjective preferences of purchasers of golf products are difficult to predict and may be subject to rapid and unanticipated changes. If our suppliers fail to successfully develop and introduce innovative and popular products on a timely basis, then our sales and profits may suffer materially. If our suppliers introduce new products too rapidly, however, it could result in close-outs of existing inventories. Close-outs can result in reduced margins on the sale of older products, as well as reduced sales of new products given the availability of older products at lower prices. These reduced margins and sales may materially adversely affect our results of operations.

Our operating results are subject to seasonal fluctuations which could cause the market price of our common stock to decline.

Our business is highly seasonal. Our sales during our first two fiscal quarters of each year, which include Father's Day, and our sales during the year-end holiday selling season, have historically contributed and are expected to continue to contribute a disproportionate percentage of our sales. Our occupancy costs, which are included in cost of sales, and a significant portion of our store operating expenses and general and administrative expenses, do not vary proportionately with fluctuations in sales. As a result, all our income from operations has been generated during the first two fiscal quarters of the year, and we expect this seasonality to continue. In addition, we expect quarterly fluctuations in our operating results to continue as a result of seasonal demand in our markets. Such patterns may change, however, as a result of entering new markets. We also make decisions regarding merchandise well in advance of the season in which it will be sold, particularly for Father's Day and the year-end holiday selling season. We incur significant additional expenses in our first two fiscal quarters and the December holiday season in anticipation of higher sales in those periods, including acquiring additional inventory, preparing and mailing our direct mail pieces, advertising, creating in-store promotions and hiring additional employees. This seasonality may result in volatility or have an adverse effect on the market price for our common stock.

Our profitability may be materially adversely affected due to weather conditions in our markets.

The golf season and the number of rounds played in the markets in which our stores are located fluctuate based on, among other things, the weather. In the event of unseasonable weather in our markets, our sales may be lower. In addition, if our sales during our peak seasons are lower than we expect for any reason as a result of weather or otherwise, we may not be able to adjust our expenses and inventory in a timely fashion. As a result, our profitability may be materially adversely affected.

Our current concentration of stores in northern and midwestern states makes us highly susceptible to adverse conditions in these regions, including unseasonable weather, which could materially adversely affect our sales and profitability.

Most of our stores are located in northern and midwestern states. As a result, our operations could be more susceptible to regional factors than the operations of more geographically diversified competitors. These factors include regional economic and weather conditions, natural disasters, and demographic and population changes in the states in which we operate. If these regions were to suffer an economic downturn, unseasonable weather or other adverse event, our operating results could suffer.

10

If we cannot successfully implement our growth strategy, the profitability of our company as a whole could be materially adversely affected.

Our growth strategy will require the deployment of a significant amount of capital and may not be profitable. We opened no new stores in fiscal 2003. During fiscal 2004, we opened four new stores. During fiscal 2005, we opened ten new stores and prepared to open eleven new stores in the first quarter of fiscal 2006, all of which were opened.

We currently plan to spend approximately $1.1 million per store to open a total of 14 to 16 new stores in fiscal 2006, of which eleven have already been opened. In addition, we plan to open 14 to 16 new stores in fiscal 2007. These amounts are estimates and actual store opening costs may vary.

The ability to open new stores, the related opening costs and the profitability of our new stores are subject to various contingencies, some of which are beyond our control. These contingencies include our ability to:

- •

- locate suitable store sites;

- •

- negotiate acceptable lease terms;

- •

- build out or refurbish sites on a timely and cost-effective basis;

- •

- hire, train and retain skilled managers and PGA professionals;

- •

- hire sales associates;

- •

- obtain adequate capital resources; and

- •

- integrate new stores into existing operations successfully.

We intend to open additional stores in some of our existing markets. Because our stores typically draw customers from their local areas, a new store may draw customers away from nearby existing stores and may cause sales performance and customer counts at those existing stores to decline, which may materially adversely affect our overall operating results.

We also intend to open stores in new markets. The risks associated with entering a new market include difficulties in attracting customers due to a reduced level of customer familiarity with our brand, our lack of familiarity with local customer preferences, seasonal differences in the market, and difficulties in hiring a sufficient number of qualified store associates. In addition, entry into new markets may bring us into competition with new, unfamiliar competitors or with existing competitors with a large, established market presence. We cannot assure you that we will be successful in operating our stores in new markets on a profitable basis. If we are not, then the profitability of our company as a whole may be materially adversely affected.

In addition to these risks and uncertainties, our new stores may add strain on our management information systems and may divert our management's attention from existing operations. We cannot assure you that our new stores will be a profitable deployment of our capital resources. If any of our new stores are not profitable, then the profitability of our company as a whole may be materially adversely affected.

11

Competition in the golf and sporting goods retail industry and from prospective competitors could materially adversely affect our sales and profitability.

The retail market for golf-related products and services is highly fragmented and competitive. Our current and prospective competitors include companies that have substantially greater market presence, name recognition, and financial, marketing and other resources than we do and may be able to devote greater resources to sourcing, promoting and selling their products. We compete with the following categories of companies: other golf specialty retailers, on-course pro shops, catalog and Internet retailers, franchise and independent golf retailers, general sporting goods retailers and mass merchants. Traditional and golf specialty retailers are expanding more aggressively in marketing leading national brand golf equipment, thereby competing directly with us for products, customers and locations. In addition, some of our key suppliers have begun to operate retail stores or Internet sites that sell directly to consumers and may compete with us and reduce our sales. Pressure from our competitors could require us to reduce our prices or increase our spending for advertising and promotion which would erode our margins. As a result of this competition, we may experience lower sales or greater operating costs, such as marketing costs, which would have a material adverse effect on our profitability.

A decline in discretionary consumer spending could harm our operating results.

Our products are recreational in nature and, therefore, are discretionary purchases for consumers. Consumers are generally more willing to make discretionary purchases of golf-related products and services during favorable economic conditions. Discretionary spending is affected by many factors, including, among others, general business conditions, interest rates, inflation, consumer debt levels, the availability of consumer credit, taxation, stock market performance, unemployment trends, terrorist attacks and acts of war and other matters that influence consumer confidence and spending.

Our customers' purchases of discretionary items, including our products and services, could decline during periods when disposable income is lower or periods of actual or perceived unfavorable economic conditions. If this occurs, our operating results could suffer materially.

The growth of our business will be dependent upon the availability of adequate capital.

The growth of our business will depend on the availability of adequate capital, which in turn will depend in large part on cash flow generated by our business and the availability of equity and debt financing. We cannot assure you that our operations will generate positive cash flow or that we will be able to obtain equity or debt financing on acceptable terms or at all. Our credit facility contains provisions that restrict our ability to incur additional indebtedness or make substantial asset sales that might otherwise be used to finance our expansion. The security interests in our inventory and financial assets that secure our obligations under the credit facility may further limit our access to certain capital markets or lending sources. The actual availability of funds under our credit facility is limited to specified percentages of our eligible inventory. Accordingly, opportunities for increasing our cash on hand through sales of inventory would be partially offset by reduced availability under our credit facility. As a result, we cannot assure you that we will be able to finance our current expansion plans.

If we lose the services of key members of our management team, we may not be able to manage our operations and implement our growth strategy effectively.

Our future success depends, in large part, on the efforts and abilities of our senior management, including our Chief Executive Officer and co-founder, Randall K. Zanatta; our Chief Operating Officer and co-founder, Gregory B. Maanum; our Chief Financial Officer, Richard C. Nordvold; our Chief Marketing Officer, Michael W. McCormick; and our Senior Vice President—Sales and Operations, Ronald G. Hornbaker. Our senior management team may terminate their employment with us and are

12

precluded from competing with us for only six months after such termination. We do not maintain key person insurance on any employees except for Messrs. Zanatta and Maanum. If we lose the services of one or more of our key executives, we may not be able to manage our business successfully or achieve our growth objectives. As our business grows, we will need to attract and retain additional qualified management personnel in a timely manner.

We rely heavily on our management information and other systems for inventory management, distribution and other functions. If our systems fail to perform these functions adequately or if we experience an interruption in their operation or security, our business and results of operations could be materially adversely affected.

The efficient operation of our business is dependent on our management information systems. We rely heavily on our management information systems to manage order entry, order fulfillment, point-of-sale and inventory replenishment processes. The failure of our management information systems to perform as we anticipate could disrupt our business and could result in decreased sales, increased overhead costs, excess inventory and product shortages, causing our business and results of operations to suffer materially.

In addition, our management information systems are vulnerable to damage or interruption from:

- •

- earthquake, fire, flood and other natural disasters; and

- •

- power loss, computer systems failure, Internet and telecommunications or data network failure.

Any such interruption could have a material adverse effect on our business.

If we are unable to protect the confidential information provided by our eCommerce customers, our sales and profitability may be materially adversely affected.

The success of our eCommerce operations depends on the secure transmission of confidential information over public networks. There can be no assurance that advances in computer capabilities, new discoveries in the field of cryptography, or other events or developments will not result in a compromise or breach of the algorithms we use to protect customer transactions and personal data contained in our customer database. If any such compromise of our security were to occur, it could have a material adverse effect on our reputation, business, operating results and financial condition and may cost us additional expense to protect against such security breaches.

A disruption in or failure to expand our systems supporting our eCommerce operations, particularly as our eCommerce sales grow, may materially adversely affect our results of operations.

Our eCommerce sales will depend on the number of visitors who shop on our Internet site and the volume of orders we can fill on a timely basis. We rely on several third party providers to host our Internet site and support our electronic data interchange, or EDI, system. Technical problems either we or our third party service providers experience with our Internet site or order fulfillment systems could materially reduce the volume of goods sold and the attractiveness of purchasing our merchandise through our Internet site. Also, we or our third party service providers may be required to further expand and upgrade our technology, transaction processing systems and network infrastructure if there is a substantial increase in the volume of traffic on our Internet site or the number of orders placed by our customers. We cannot assure you that we will be able to project accurately the rate or timing of increases, if any, or be able to negotiate with our third party providers, to expand and upgrade our systems and infrastructure to accommodate such increases on a timely basis.

13

A change in U.S. GAAP accounting standards for employee stock options will have a significant adverse effect on the reporting of our results of operations.

In December 2004, the Financial Accounting Standards Board (FASB) issued a revision to Statement of Financial Accounting Standards (SFAS) No. 123,Accounting for Stock-Based Compensation, which requires the calculation of the fair value of stock-based compensation, estimation of future forfeitures and income taxes, and recognition of the fair value as a non-cash expense over the vesting period of the underlying instruments. SFAS No. 123(R),Share-Based Payment, eliminates the ability to account for stock-based compensation transactions using the footnote disclosure-only provisions of Accounting Principles Board (APB) Opinion No. 25,Accounting for Stock Issued to Employees, and instead requires that such transactions be recognized and reflected in financial statements using a fair-value-based method. Based on current guidance, we will be required to implement the provisions of SFAS No. 123(R) beginning in fiscal 2007. We are currently evaluating option valuation methodologies and assumptions. We expect that we will record substantial non-cash compensation expenses as a result of the adoption of SFAS No. 123(R), which will have a significant adverse impact on our results of operations.

If we do not anticipate and respond to the changing preferences of our customers, we could be required to take significant markdowns in inventory and our sales could materially decline.

Our success depends, in large part, on our ability to identify and anticipate the changing preferences of our customers and stock our stores with a wide selection of quality merchandise that appeals to their preferences. Our customers' preferences for merchandise and particular brands vary from location to location, and may vary significantly over time. We cannot guarantee that we will accurately identify or anticipate the changing preferences of our customers or stock our stores with merchandise that appeals to them. If we do not accurately identify and anticipate our customers' preferences, we may lose sales, which may in turn cause us to lose volume purchasing allowances from vendors, or we may overstock merchandise, which may require us to take significant markdowns on our inventory. In either case, our sales could significantly decline and our business and financial results may suffer materially.

A disruption in the services of our primary common carriers may decrease our profitability.

We do not maintain a central distribution facility. Instead, one of our key strategies is that our manufacturers distribute their products directly to our retail stores, enabling us to more effectively control the level and mix of inventory at our stores. We use United Parcel Service of America, Inc. (UPS) and Roadway Express, Inc. (Roadway) for substantially all of our ground shipments of products sold in our stores. Any significant interruption in UPS or Roadway services or in common carrier services generally due to strikes, terrorism, inclement weather or otherwise, would impede our ability to receive merchandise on a timely basis and maintain appropriate inventory levels and product mixes in our stores. This impediment could cause us to lose sales and customers. In the event of such an interruption, we may not be able to engage appropriate alternatives to distribute our products in a timely manner on equally favorable terms. If we incur higher shipping costs, we may be unable to pass these costs on to our customers, which could materially decrease our profitability.

If we are unable to enforce our intellectual property rights, or if we are accused of infringing on a third party's intellectual property rights, our sales and profitability may be materially adversely affected.

We currently own two registered trademarks and three registered service marks in the U.S. The exclusive right to use these trademarks and service marks has helped establish our market share. The loss or reduction of any of our significant proprietary rights could hurt our ability to distinguish our stores from our competitors' stores, causing us to lose significant market share. If we lose market share, our sales and profitability may be materially adversely affected.

14

Additionally, third parties may assert claims against us alleging infringement, misappropriation or other violations of patent, trademark or other proprietary rights, whether or not such claims have merit. Such claims can be time consuming and expensive to defend and could require us to cease using and selling the allegedly infringing products, which may have a significant impact on our sales and cause us to incur significant litigation costs and expenses.

We may pursue strategic acquisitions, which could have a material adverse impact on our business.

While we are not currently considering any acquisitions, we have considered acquisitions in the past and we may from time to time acquire complementary businesses, products or technologies. Acquisitions may result in difficulties in assimilating acquired companies, and may result in the diversion of our capital and our management's attention from other business issues and opportunities. We may not be able to successfully integrate companies that we acquire, including their personnel, financial systems, distribution, operations and general store operating procedures. If we fail to successfully integrate acquired companies, our business could suffer. In addition, the integration of any acquired company, and its financial results, into ours may materially adversely affect our operating results.

Our net income in fiscal 2004 and fiscal 2005 was positively impacted by non-recurring items which might cause investors to overestimate our future net income.

Our net income in fiscal 2005 included a one-time gain on the sale of our Golf Town Canada Inc. stock which increased net income by $5.0 million, after taxes, and our net income for fiscal 2004 included a non-cash income tax benefit totaling $6.2 million resulting from the reversal of a previously established income tax valuation allowance. These non-recurring items might cause investors to overestimate net income results in future years if the non-recurring items are not fully considered.

Risks Related to this Offering

We may issue shares of preferred stock without shareholder approval, which could materially adversely affect the rights of holders of our common stock.

Our articles of incorporation permit us to establish the rights, privileges, preferences and restrictions, including voting rights, of future series of our preferred stock and to issue such stock without approval from our shareholders. The rights of holders of our common stock may suffer materially as a result of the rights granted to holders of preferred stock that may be issued in the future. In addition, we could issue preferred stock to prevent a change in control of our company, depriving holders of our common stock of an opportunity to sell their stock at a price in excess of the prevailing market price.

Certain provisions of Minnesota law and our articles of incorporation and bylaws may make a takeover of our company more difficult, depriving shareholders of opportunities to sell shares at above-market prices.

Certain provisions of Minnesota law and our bylaws may have the effect of discouraging attempts to acquire us without the approval of our board of directors. Section 302A.671 of the Minnesota Statutes, with certain exceptions, requires approval of any acquisition of the beneficial ownership of 20% or more of our voting stock then outstanding by a majority vote of our shareholders prior to its consummation. In general, shares acquired in the absence of such approval are denied voting rights and are redeemable by us at their then fair market value within 30 days after the acquiring person failed to give a timely information statement to us or the date our shareholders voted not to grant voting rights to the acquiring person's shares. Section 302A.673 of the Minnesota Statutes generally prohibits any business combination by us, with an interested shareholder, which includes any shareholder that purchases 10% or more of our voting shares within four years following such

15

interested shareholder's share acquisition date, unless the business combination is approved by a committee of one or more disinterested members of our board of directors before the interested shareholder's share acquisition date. In addition, our bylaws, effective upon the closing of this offering, provide for an advance notice procedure for nomination of candidates to our board of directors that could have the effect of delaying, deterring or preventing a change in control. Consequently, our holders of our common stock may lose opportunities to sell their stock for a price in excess of the prevailing market price due to these statutory protective measures.

In addition, our board of directors has amended our articles of incorporation and bylaws, effective upon the closing of this offering, to classify our board of directors so that only one-third of our directors are elected each year. Our shareholders approved the amendments to our articles of incorporation at a meeting held on June 15, 2005. A classified board will have the effect of discouraging, delaying or preventing a change in control or an unsolicited proposal that a shareholder might consider favorable, including a proposal that might result in the payment of a premium over the market price for the shares held by shareholders.

See "Description of Capital Stock—Potential Anti-Takeover Effects of Certain Provisions of Minnesota State Law and Our Articles of Incorporation and Bylaws—Articles of Incorporation and Bylaws" for more information regarding these provisions of Minnesota law.

Our management will have broad discretion regarding the use of proceeds from this offering and we may use our proceeds from this offering in ways with which you may disagree.

We estimate that we will receive net proceeds from this offering of approximately $ million. We intend to use the net proceeds from our sale of shares in this offering to continue to open new retail stores across the country and for general corporate purposes, and we will use approximately $ million of our net proceeds to pay our preferred shareholders all of the accrued and unpaid dividends due upon conversion of their shares of preferred stock into shares of our common stock. Our management will have broad discretion, however, regarding how we use our proceeds from this offering and the occurrence of unforeseen events or changes in business conditions could result in the application of our net proceeds from this offering in a manner other than described in this prospectus and you may disagree with the way our management allocates these funds.

We will face new challenges and increased costs as a public company.

As a public company with a listed equity security, we will need to comply with new laws, regulations and requirements, certain provisions of the Sarbanes-Oxley Act of 2002, related Securities and Exchange Commission (SEC) regulations and requirements of the Nasdaq National Market with which we are not required to comply as a private company. Complying with these statutes, regulations and requirements will occupy a significant amount of the time of our board of directors and management and will increase our costs and expenses. We will need to:

- •

- create or expand the roles and duties of our board of directors, our board committees and management;

- •

- establish an internal audit function;

- •

- institute a more comprehensive compliance function;

- •

- design, establish, evaluate and maintain a system of internal control over financial reporting in compliance with the requirements of Section 404 of the Sarbanes-Oxley Act

16

- •

- prepare and distribute periodic public reports in compliance with our obligations under the federal securities laws;

- •

- establish new internal policies, such as those relating to disclosure controls and procedures and insider trading;

- •

- Involve and retain to a greater degree outside counsel and accountants in the above activities; and

- •

- enhance our investor relations function.

of 2002 and the related rules and regulations of the SEC and the Public Company Accounting Oversight Board (PCAOB);

In addition, we expect that being a public company subject to these rules and regulations will make it more expensive for us to obtain director and officer liability insurance, and we may be required to accept reduced coverage or incur substantially higher costs to obtain coverage. These factors could also make it more difficult for us to attract and retain qualified members of our board of directors, particularly to serve on our audit and compensation committees, and qualified executive officers.

We will be exposed to risks relating to evaluations of controls required by Section 404 of the Sarbanes-Oxley Act of 2002.

Following this offering, we will begin evaluating our internal controls systems to allow management to report on, and our independent auditors to attest to, our internal control over financial reporting. We will be performing the system and process evaluation and testing (and any necessary remediation) required to comply with the management certification and auditor attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002. We are required to comply with Section 404 by no later than March 3, 2007. However, we cannot be certain as to the timing of completion of our evaluation, testing and remediation actions or the impact of the same on our operations. Furthermore, upon completion of this process, we may identify control deficiencies of varying degrees of severity under applicable SEC and PCAOB rules and regulations that remain unremediated. As a public company, we will be required to report, among other things, control deficiencies that constitute a "material weakness" or changes in internal controls that, or are reasonably likely to, materially affect our internal control over financial reporting. A "material weakness" is a significant deficiency, or combination of significant deficiencies, that results in more than a remote likelihood that a material misstatement of the annual or interim financial statements will not be prevented or detected. If we fail to implement the requirements of Section 404 in a timely manner, we might be subject to sanctions or investigation by regulatory authorities such as the SEC or the Nasdaq National Market, and if we fail to remedy any material weakness, our financial statements may be inaccurate, we may face restricted access to the capital markets and our stock price may be adversely affected.

We cannot assure you that a market will develop for our common stock or, if a market develops, what the market price of our common stock will be.

The initial public offering price for our common stock will be determined through our negotiations with the underwriters and may not bear any relationship to the market price at which it will trade after this offering. Before this offering, there was no public trading market for our common stock and we cannot assure you that one will develop or be sustained after this offering. If a market does not develop or is not sustained, it may be difficult for you to sell your shares of common stock at an attractive price or at all. We cannot predict the prices at which our common stock will trade.

17

The price of our common stock may be volatile.

The trading price of our common stock following this offering may fluctuate substantially. The price of our common stock after this offering may be higher or lower than the price you pay, depending on many factors, some of which are beyond our control and may not be related to our operating performance. These fluctuations could cause you to lose part or all of your investment in shares of our common stock. The factors that could cause fluctuations include, but are not limited to, the following:

- •

- price and volume fluctuations in the overall stock market from time to time;

- •

- significant volatility in the market price and trading volume of the stock of golf specialty, sporting goods and other retail companies;

- •

- actual or anticipated changes in our net income, fluctuations in our operating results or the failure to meet the expectations of financial market analysts and investors;

- •

- investor perceptions of the golf and sporting goods industry and retail industries in general and our company in particular;

- •

- the operating and stock performance of comparable companies and our competitors;

- •

- the opening of new stores and the closing of existing stores;

- •

- general economic conditions and trends;

- •

- major catastrophic events;

- •

- changes in accounting standards, policies, guidance, interpretation or principles;

- •

- unseasonable weather conditions in our markets;

- •

- loss of external funding sources;

- •

- adverse events affecting our key suppliers;

- •

- sales of large blocks of our stock or sales by insiders; or

- •

- departures of key personnel.

If you purchase shares of common stock sold in this offering, you will experience immediate dilution.

If you purchase shares of our common stock in this offering, you will experience significant immediate dilution, which would have been $ per share as of based on an assumed initial public offering price of $ per share, because the price that you pay will be substantially greater than the net book value per share of the shares you acquire. You will experience additional dilution upon the exercise of options and the warrant to purchase our common stock, including those options currently outstanding and those granted in the future, and any issuance of restricted stock or other equity awards under our stock incentive plans.

18

We do not anticipate paying cash dividends on shares of our common stock in the foreseeable future.

We have never declared or paid any cash dividends on shares of our common stock. We intend to retain any future earnings to fund the operation and expansion of our business and, therefore, we do not anticipate paying cash dividends on shares of our common stock in the foreseeable future. In addition, our credit facility restricts, among other things, our ability to pay cash dividends or other non-stock distributions on any shares of our common stock.

Our principal shareholders, directors and executive officers may exercise significant control over our company.

Our principal shareholders, directors and executive officers, and entities affiliated with them, will own approximately % of the outstanding shares of our common stock after this offering. As a result, these shareholders, if acting together, will be able to influence or control matters requiring approval by our shareholders, including the election of directors and the approval of mergers or other extraordinary transactions. They may also have interests that differ from yours and may vote in a way with which you disagree and which may be adverse to your interests. The concentration of ownership may have the effect of delaying, preventing or deterring a change of control of our company, could deprive our shareholders of an opportunity to receive a premium for their common stock as part of a sale of our company and might ultimately affect the market price of our common stock.

Common stock available for future sale by our shareholders may materially adversely affect our stock price.

We may sell additional shares of common stock in subsequent public offerings. We may also issue additional shares of common stock to finance future acquisitions. After the completion of this offering, we will have outstanding shares of common stock. This number includes shares that we are selling in this offering, which may be resold immediately in the public market. shares of our common stock, or % of our total outstanding shares, are restricted from immediate resale under the federal securities laws and the lock-up agreements between certain of our current shareholders and the underwriters described in the section entitled "Underwriting," but may be sold into the market in the near future. These shares will become available for sale at various times following the expiration of the lock-up agreements which, without the prior consent of Piper Jaffray, is 180 days (subject to an extension of no more than 34 days as a result of an earnings release by us) after the date of this prospectus, subject to volume limitations and manner-of-sale requirements under Rule 144 of the Securities Act of 1933, as amended (Securities Act). However, Piper Jaffray may release all or a portion of these shares subject to lock-up agreements at any time without notice. The period immediately following expiration of the lock-up agreements may experience relatively higher levels of selling activity.

After this offering, several of our existing shareholders owning shares of our common stock, are expected to be parties to a registration rights agreement with us. Under that agreement, these shareholders will have the right, after the expiration of the lock-up period, to require us to effect the registration of their shares. In addition, if we propose to register, or are required to register following the exercise of a "demand" registration right as described in the previous sentence, any of our shares of common stock under the Securities Act, all the shareholders who are parties to the registration rights agreement will be entitled to include their shares of common stock in that registration. We cannot predict the size of future issuances of our common stock or the effect, if any, that future issuances and sales of shares of our common stock will have on the market price of our common stock. Sales of substantial amounts of our common stock (including shares issued in connection with an acquisition), or the perception that such sales could occur, may materially adversely affect prevailing market prices for our common stock. These sales could also make it more difficult for us to issue and sell shares of our common stock or other equity securities in the future.

19

A SPECIAL NOTE REGARDING FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements that are based on our beliefs, assumptions and expectations of future events taking into account the information currently available to us. All statements other than statements of historical fact contained in this prospectus are forward-looking statements. Many of the forward-looking statements are contained in the sections entitled "Summary," "Risk Factors," "Use of Proceeds," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business." These statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performances, financial condition or achievements to differ materially from the expected future results, performances, financial condition or achievements as expressed or implied in any forward-looking statements. Factors that could contribute to these differences include but are not limited to:

- •

- the continued popularity of golf and golf-related products;

- •

- the continued development of new golf-related products and our ability to purchase and sell such products;

- •

- our dependence on key suppliers;

- •

- our ability to execute our growth strategy profitably in new and existing markets;

- •

- the effect of competition in our industry;

- •

- the regional concentration of our stores and the seasonal fluctuations in our business;

- •

- the effects of weather in our markets;

- •

- the effects of the economy;

- •

- our ability to access adequate capital;

- •

- our ability to attract and retain management talent;

- •

- our ability to develop and maintain our management information and other systems;

- •

- our ability to anticipate and respond to the changing preferences of our customers;

- •

- the uninterrupted service of the common carriers we use;

- •

- our ability to enforce our intellectual property rights and avoid claims of infringement of a third party's intellectual property rights; and

- •

- other factors discussed under the headings "Risk Factors," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business."

In some cases, you can identify forward-looking statements by terms such as "anticipates," "believes," "estimates," "expects," "intends," "plans," "seeks," "predicts," "projects," "strives," "potential," "objective," "may," "could," "should," "would," "will" and similar expressions intended to identify forward-looking statements. Forward-looking statements reflect our current views with respect to future events, are based on our assumptions and are subject to risks and uncertainties. Given these

20

uncertainties, you should not place undue reliance on these forward-looking statements. You should read this prospectus and the documents that we reference in this prospectus and have filed as exhibits to the registration statement completely and with the understanding that our actual future results may be materially different from what we expect them to be.

Our forward-looking statements speak only as of the date of this prospectus. We assume no obligation to update or revise any forward-looking statements publicly, or to update the reasons actual results could differ materially from those anticipated in any forward-looking statements, even if new information becomes available in the future.

21

The net proceeds from our sale of shares of our common stock are estimated to be approximately $ million, based on an estimated offering price of $ per share, after deducting underwriting discounts and commissions and estimated offering expenses payable by us.

We intend to use the net proceeds from our sale of shares in this offering, together with cash provided by operations and, if necessary, funds available under our credit facility, to continue to open new retail stores across the country and for general corporate purposes, and we will use approximately $ million of our net proceeds to pay our preferred shareholders all of the accrued and unpaid dividends due upon conversion of their shares of preferred stock into shares of our common stock. During fiscal 2005, we opened ten new stores and we expect to open a total of 28 to 32 stores in fiscal 2006 and fiscal 2007, of which eleven have already been opened. In fiscal 2006, we expect our capital expenditures to be approximately $14.0 million, substantially all of which will relate to planned store openings in fiscal 2006 and the first quarter of fiscal 2007. Our preferred shareholders have agreed to convert their shares of our preferred stock into shares of our common stock simultaneously with the closing of this offering. See "Certain Relationships and Related Party Transactions." All accrued and unpaid dividends on our preferred stock will be paid in connection with this offering.

The foregoing represents our current intentions based upon our current plans and business condition. Management will have broad discretion in the application of our net proceeds from this offering, and the occurrence of unforeseen events or changes in business conditions could result in the application of our net proceeds from this offering in a manner other than as described in this prospectus. From time to time, we evaluate potential acquisitions of complementary businesses, products and technologies. Should we determine to employ cash resources for acquisitions, the amounts available for the purposes described above may be significantly reduced. At this time, we have no specific agreements, understandings, commitments or arrangements with respect to any acquisition. Pending application of our net proceeds, we intend to invest the net proceeds in short-term, interest-bearing, investment-grade securities.