Exhibit 99.2

| First Western Financial, Inc. The First, Western-Based Private Trust Bank First Quarter 2020 Conference Call |

| Safe Harbor 2 This presentation contains “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. These forward-looking statements reflect the current views of First Western Financial, Inc.’s (“First Western”) management with respect to, among other things, future events and First Western’s financial performance. These statements are often, but not always, made through the use of words or phrases such as “may,” “should,” “could,” “predict,” “potential,” “believe,” “will likely result,” “expect,” “continue,” “will,” “anticipate,” “seek,” “estimate,” “intend,” “plan,” “project,” “future” “forecast,” “goal,” “target,” “would” and “outlook,” or the negative variations of those words or other comparable words of a future or forward-looking nature. These forward-looking statements are not historical facts, and are based on current expectations, estimates and projections about First Western’s industry, management’s beliefs and certain assumptions made by management, many of which, by their nature, are inherently uncertain and beyond First Western’s control. Accordingly, First Western cautions you that any such forward-looking statements are not guarantees of future performance and are subject to risks, assumptions and uncertainties that are difficult to predict. Although First Western believes that the expectations reflected in these forward-looking statements are reasonable as of the date made, actual results may prove to be materially different from the results expressed or implied by the forward-looking statements. Those following risks and uncertainties, among others, could cause actual results and future events to differ materially from those set forth or contemplated in the forward-looking statements: the COVID-19 pandemic and related government actions; the risk of geographic concentration in Colorado, Arizona, Wyoming and California; the risk of changes in the economy affecting real estate values and liquidity; the risk in our ability to continue to originate residential real estate loans and sell such loans; risks specific to commercial loans and borrowers; the risk of claims and litigation pertaining to our fiduciary responsibilities; the risk of competition for investment managers and professionals; the risk of fluctuation in the value of our investment securities; the risk of changes in interest rates; and the risk of the adequacy of our allowance for credit losses and the risk in our ability to maintain a strong core deposit base or other low-cost funding sources. Additional information regarding these and other risks and uncertainties to which our business and future financial performance are subject is contained in our Annual Report on Form 10-K filed with the U.S. Securities and Exchange Commission (“SEC”) on March 12, 2020 and other documents we file with the SEC from time to time. All subsequent written and oral forward-looking statements attributable to First Western or persons acting on First Western’s behalf are expressly qualified in their entirety by this paragraph. Forward-looking statements speak only as of the date of this presentation. First Western undertakes no obligation to publicly update or otherwise revise any forward-looking statements, whether as a result of new information, future events or otherwise (except as required by law). Certain of the information contained herein may be derived from information provided by industry sources. The Company believes that such information is accurate and the sources from which it has been obtained are reliable; however, the Company cannot guaranty the accuracy of such information and has not independently verified such information. This presentation contains certain non-GAAP financial measures intended to supplement, not substitute for, comparable GAAP measures. Reconciliations of non-GAAP financial measures to GAAP financial measures are provided at the end of this presentation. Numbers in the presentation may not sum due to rounding. |

| COVID-19 Impact Overview |

| Operational Response 4 .. Business Continuity Plan activated in early February .. Daily meeting of Pandemic Response Team .. All offices open and functioning; client service by appointment only .. 90% of associates working from home routinely, 100% enabled .. All client and support operations fully functional .. Associate support programs Additional PTO and leave options provided for associates with COVID- 19 impact personally or among family members Medical plan changed to cover no cost COVID-19 testing, treatment Behavioral and telemedicine services provided at no cost to associates .. Honoring sponsorship commitments on cancelled non-profit events .. Made COVID-19 targeted donations in support of philanthropic pillars |

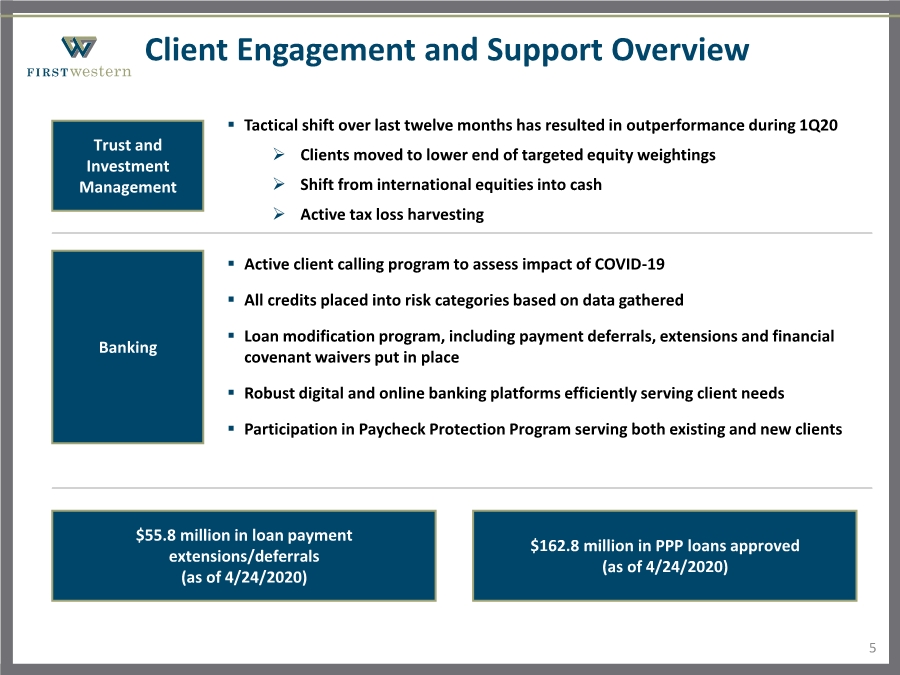

| Client Engagement and Support Overview Trust and Investment Management Banking .. Active client calling program to assess impact of COVID-19 .. All credits placed into risk categories based on data gathered .. Loan modification program, including payment deferrals, extensions and financial covenant waivers put in place .. Robust digital and online banking platforms efficiently serving client needs .. Participation in Paycheck Protection Program serving both existing and new clients $55.8 million in loan payment extensions/deferrals (as of 4/24/2020) 5 .. Tactical shift over last twelve months has resulted in outperformance during 1Q20 Clients moved to lower end of targeted equity weightings Shift from international equities into cash Active tax loss harvesting $162.8 million in PPP loans approved (as of 4/24/2020) |

| Notable Trends and Data Points 6 .. Positive business development trends in January and February Strong loan and deposit growth Steady expansion in net interest margin .. No meaningful change in credit line utilization rate since crisis started .. Loan pipeline slightly down from pre-crisis levels, but still relatively healthy .. Mortgage production remains consistent, largely driven by refinancings .. Mortgage market disruption in March caused unrealized loss in mortgages .. Strong deposit inflow in March from both existing and new clients |

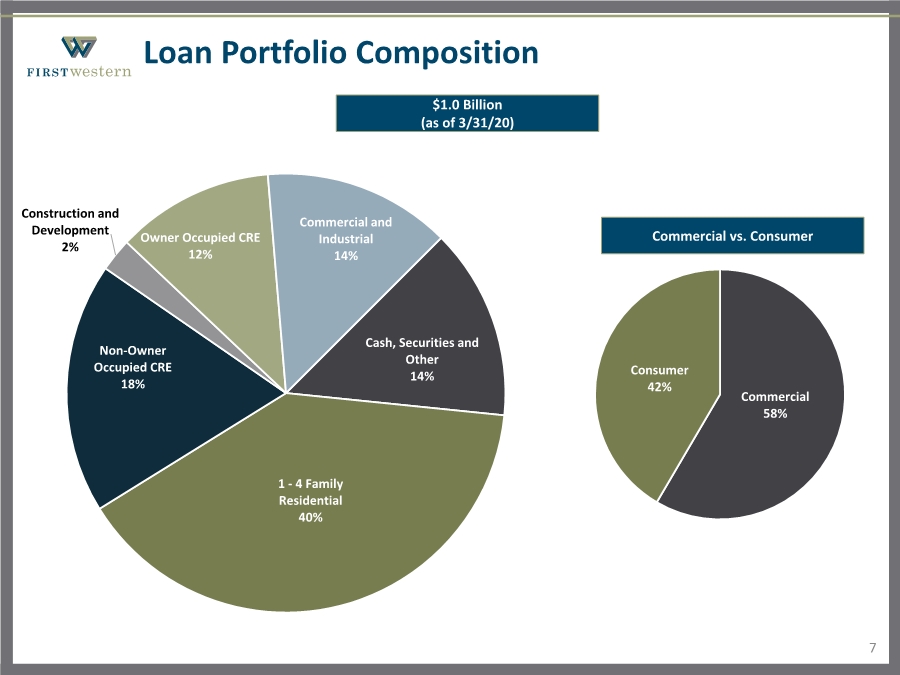

| Loan Portfolio Composition 7 Cash, Securities and Other 14% 1 - 4 Family Residential 40% Non-Owner Occupied CRE 18% Construction and Development 2% Owner Occupied CRE 12% Commercial and Industrial 14% Commercial 58% Consumer 42% $1.0 Billion (as of 3/31/20) Commercial vs. Consumer |

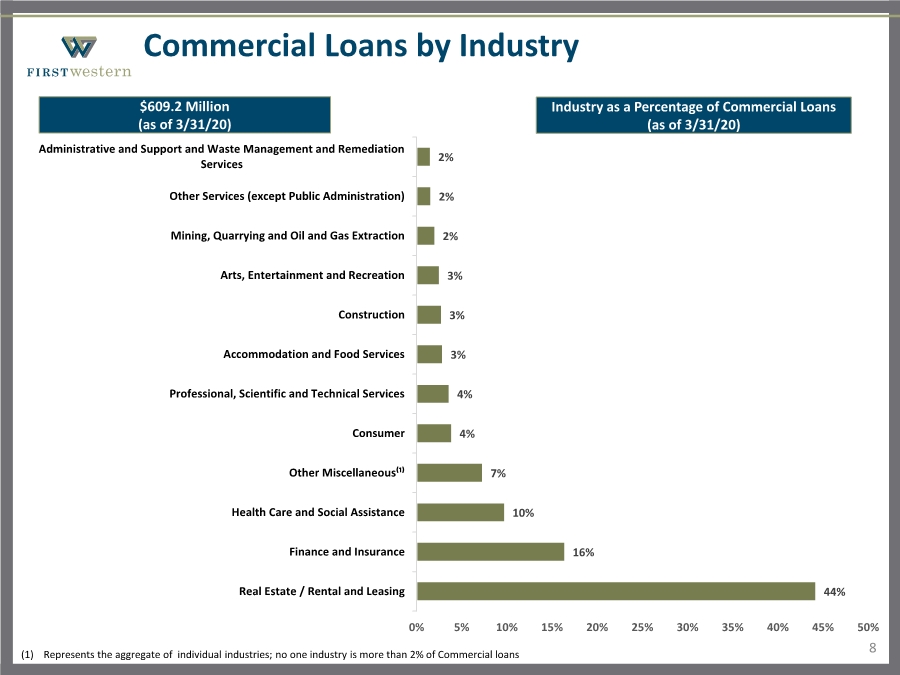

| Commercial Loans by Industry 8 44% 16% 10% 7% 4% 4% 3% 3% 3% 2% 2% 2% Real Estate / Rental and Leasing Finance and Insurance Health Care and Social Assistance Other Miscellaneous⁽¹⁾ Consumer Professional, Scientific and Technical Services Accommodation and Food Services Construction Arts, Entertainment and Recreation Mining, Quarrying and Oil and Gas Extraction Other Services (except Public Administration) Administrative and Support and Waste Management and Remediation Services 0% 5% 10% 15% 20% 25% 30% 35% 40% 45% 50% $609.2 Million (as of 3/31/20) Industry as a Percentage of Commercial Loans (as of 3/31/20) (1) Represents the aggregate of individual industries; no one industry is more than 2% of Commercial loans |

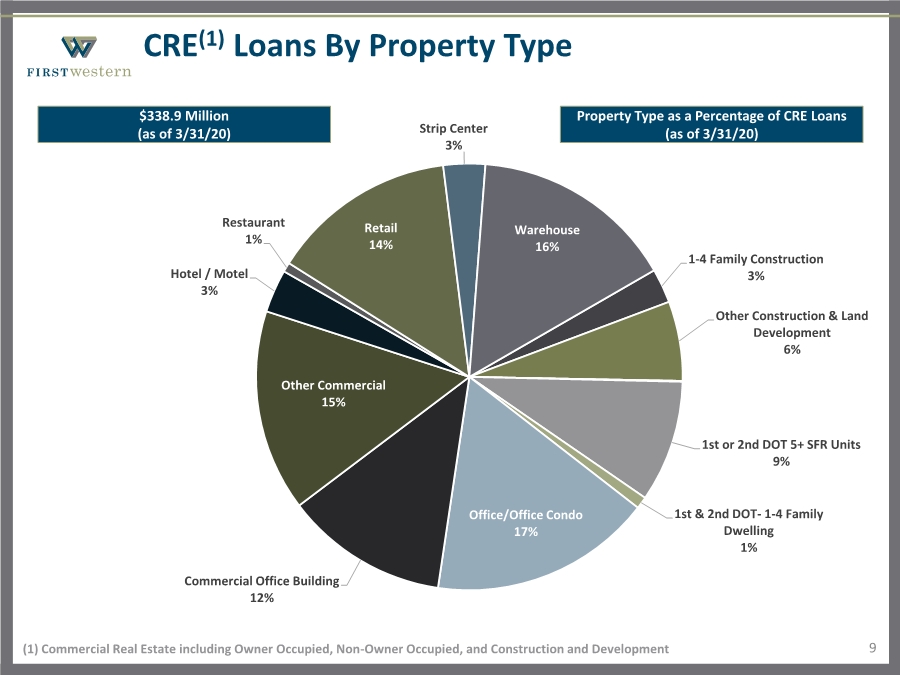

| CRE(1) Loans By Property Type 9 1-4 Family Construction 3% Other Construction & Land Development 6% 1st or 2nd DOT 5+ SFR Units 9% 1st & 2nd DOT- 1-4 Family Dwelling 1% Office/Office Condo 17% Commercial Office Building 12% Other Commercial 15% Hotel / Motel 3% Restaurant 1% Retail 14% Strip Center 3% Warehouse 16% (1) Commercial Real Estate including Owner Occupied, Non-Owner Occupied, and Construction and Development $338.9 Million (as of 3/31/20) Property Type as a Percentage of CRE Loans (as of 3/31/20) |

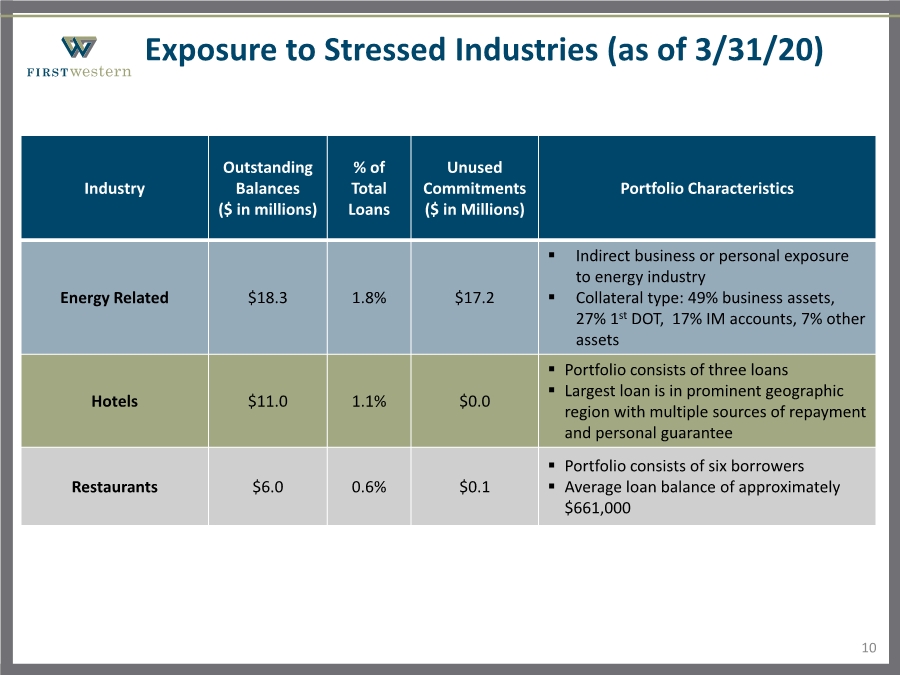

| Exposure to Stressed Industries (as of 3/31/20) 10 Industry Outstanding Balances ($ in millions) % of Total Loans Unused Commitments ($ in Millions) Portfolio Characteristics Energy Related $18.3 1.8% $17.2 .. Indirect business or personal exposure to energy industry .. Collateral type: 49% business assets, 27% 1st DOT, 17% IM accounts, 7% other assets Hotels $11.0 1.1% $0.0 .. Portfolio consists of three loans .. Largest loan is in prominent geographic region with multiple sources of repayment and personal guarantee Restaurants $6.0 0.6% $0.1 .. Portfolio consists of six borrowers .. Average loan balance of approximately $661,000 |

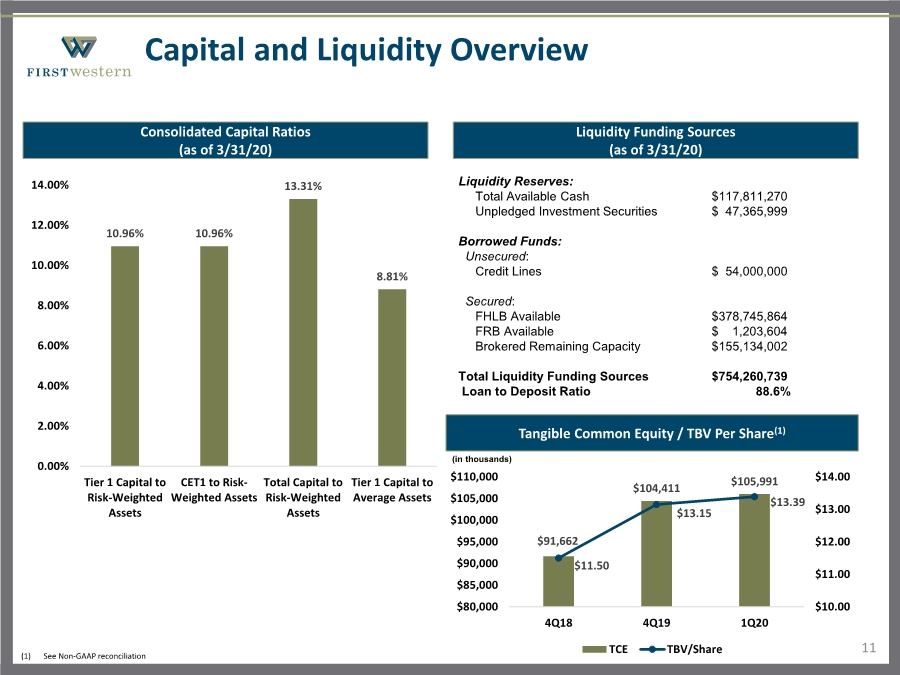

| Capital and Liquidity Overview 11 Liquidity Funding Sources (as of 3/31/20) Liquidity Reserves: Total Available Cash $117,811,270 Unpledged Investment Securities $ 47,365,999 Borrowed Funds: Unsecured: Credit Lines $ 54,000,000 Secured: FHLB Available $378,745,864 FRB Available $ 1,203,604 Brokered Remaining Capacity $155,134,002 Total Liquidity Funding Sources $754,260,739 Loan to Deposit Ratio 88.6% Consolidated Capital Ratios (as of 3/31/20) 10.96% 10.96% 13.31% 8.81% 0.00% 2.00% 4.00% 6.00% 8.00% 10.00% 12.00% 14.00% Tier 1 Capital to Risk-Weighted Assets CET1 to Risk- Weighted Assets Total Capital to Risk-Weighted Assets Tier 1 Capital to Average Assets Tangible Common Equity / TBV Per Share(1) (in thousands) $91,662 $104,411 $105,991 $11.50 $13.15 $13.39 $10.00 $11.00 $12.00 $13.00 $14.00 $80,000 $85,000 $90,000 $95,000 $100,000 $105,000 $110,000 4Q18 4Q19 1Q20 TCE TBV/Share (1) See Non-GAAP reconciliation |

| Near-Term Outlook and Expectations 12 .. Excluding impact of PPP loans, NIM should continue to expand, while fee income should normalize .. Decrease in non-recurring expenses for Q2 - expect core NIE of $14-14.5M .. Share repurchase activity on hold during duration of crisis as capital can be better used supporting clients and communities .. PPP expected to produce fee income from first round of funding of approximately $4.0 million .. Branch purchase and assumption agreement with Simmons Bank on track for planned closing in second quarter, allowing deposit premium price reduction Expands presence in Denver market Adds scale, banking talent and attractive client base |

| First Quarter 2020 Financial Review |

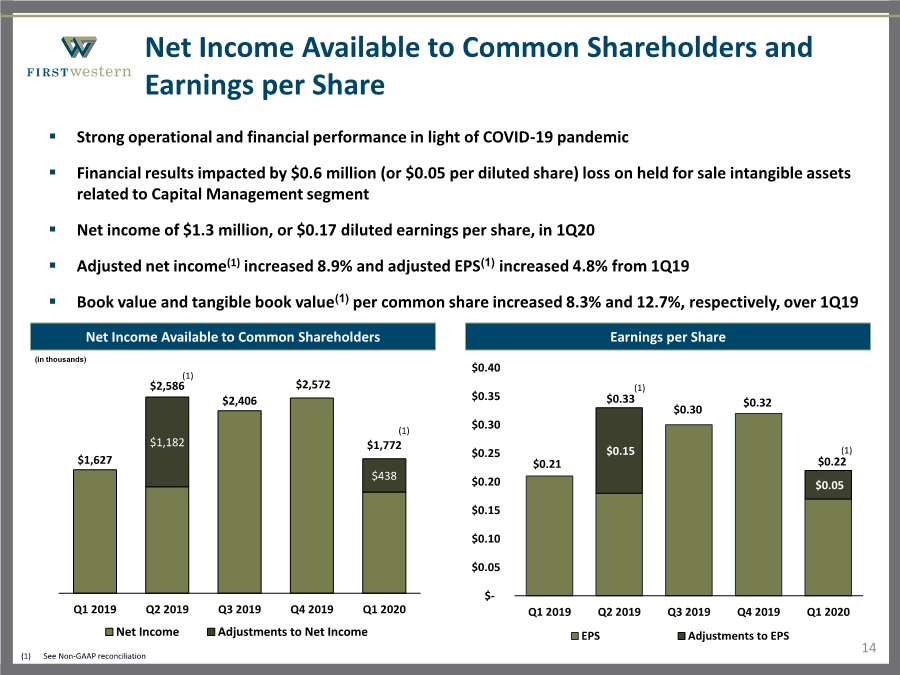

| $0.21 $0.33 $0.30 $0.32 $0.22 $0.15 $0.05 $- $0.05 $0.10 $0.15 $0.20 $0.25 $0.30 $0.35 $0.40 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 EPS Adjustments to EPS (1) (1) Net Income Available to Common Shareholders and Earnings per Share 14 Net Income Available to Common Shareholders .. Strong operational and financial performance in light of COVID-19 pandemic .. Financial results impacted by $0.6 million (or $0.05 per diluted share) loss on held for sale intangible assets related to Capital Management segment .. Net income of $1.3 million, or $0.17 diluted earnings per share, in 1Q20 .. Adjusted net income(1) increased 8.9% and adjusted EPS(1) increased 4.8% from 1Q19 .. Book value and tangible book value(1) per common share increased 8.3% and 12.7%, respectively, over 1Q19 Earnings per Share (in thousands) $1,182 $438 $1,627 $2,586 $2,406 $2,572 $1,772 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Net Income Adjustments to Net Income (1) (1) See Non-GAAP reconciliation (1) |

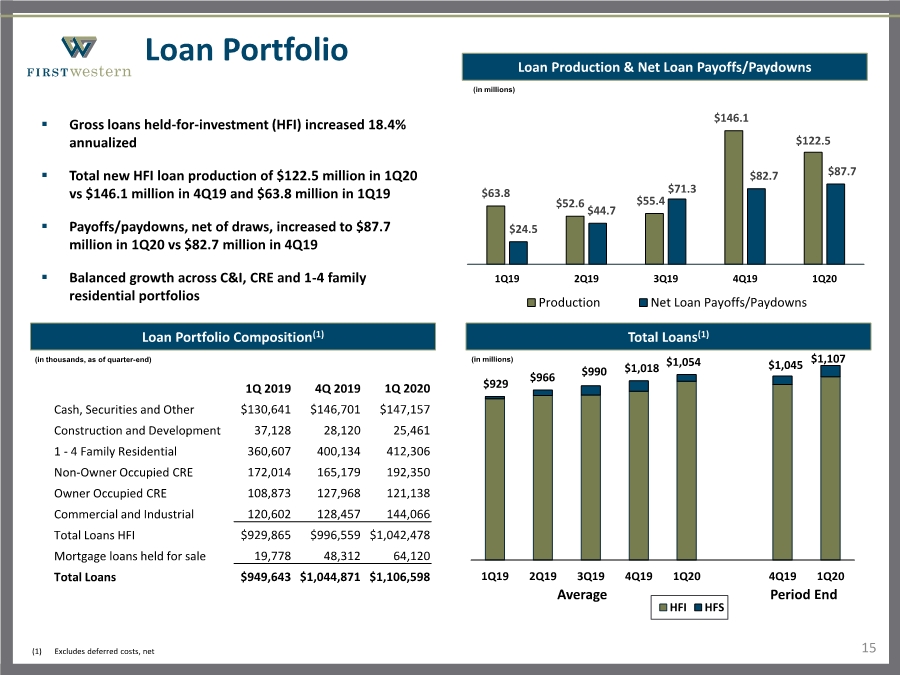

| $929 $966 $990 $1,018 $1,054 $1,045 $1,107 1Q19 2Q19 3Q19 4Q19 1Q20 4Q19 1Q20 HFI HFS Average Period End Loan Portfolio 15 Loan Portfolio Composition(1) .. Gross loans held-for-investment (HFI) increased 18.4% annualized .. Total new HFI loan production of $122.5 million in 1Q20 vs $146.1 million in 4Q19 and $63.8 million in 1Q19 .. Payoffs/paydowns, net of draws, increased to $87.7 million in 1Q20 vs $82.7 million in 4Q19 .. Balanced growth across C&I, CRE and 1-4 family residential portfolios (in thousands, as of quarter-end) Total Loans(1) (in millions) (1) Excludes deferred costs, net 1Q 2019 4Q 2019 1Q 2020 Cash, Securities and Other $130,641 $146,701 $147,157 Construction and Development 37,128 28,120 25,461 1 - 4 Family Residential 360,607 400,134 412,306 Non-Owner Occupied CRE 172,014 165,179 192,350 Owner Occupied CRE 108,873 127,968 121,138 Commercial and Industrial 120,602 128,457 144,066 Total Loans HFI $929,865 $996,559 $1,042,478 Mortgage loans held for sale 19,778 48,312 64,120 Total Loans $949,643 $1,044,871 $1,106,598 Loan Production & Net Loan Payoffs/Paydowns $63.8 $52.6 $55.4 $146.1 $122.5 $24.5 $44.7 $71.3 $82.7 $87.7 1Q19 2Q19 3Q19 4Q19 1Q20 Production Net Loan Payoffs/Paydowns (in millions) |

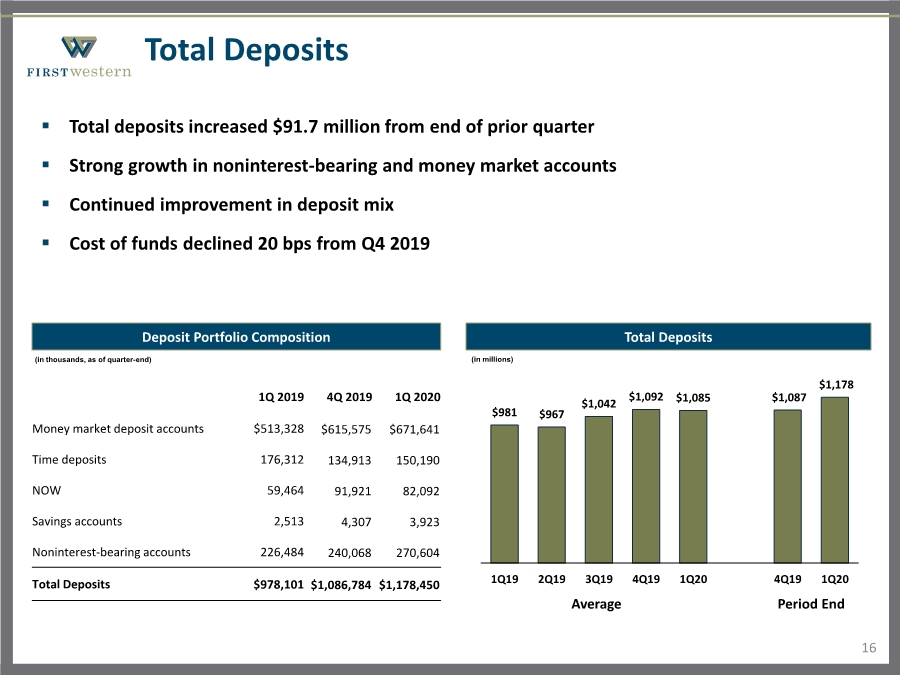

| $981 $967 $1,042 $1,092 $1,085 $1,087 $1,178 1Q19 2Q19 3Q19 4Q19 1Q20 4Q19 1Q20 Average Period End Total Deposits 16 Deposit Portfolio Composition .. Total deposits increased $91.7 million from end of prior quarter .. Strong growth in noninterest-bearing and money market accounts .. Continued improvement in deposit mix .. Cost of funds declined 20 bps from Q4 2019 1Q 2019 4Q 2019 1Q 2020 Money market deposit accounts $513,328 $615,575 $671,641 Time deposits 176,312 134,913 150,190 NOW 59,464 91,921 82,092 Savings accounts 2,513 4,307 3,923 Noninterest-bearing accounts 226,484 240,068 270,604 Total Deposits $978,101 $1,086,784 $1,178,450 (in thousands, as of quarter-end) Total Deposits (in millions) |

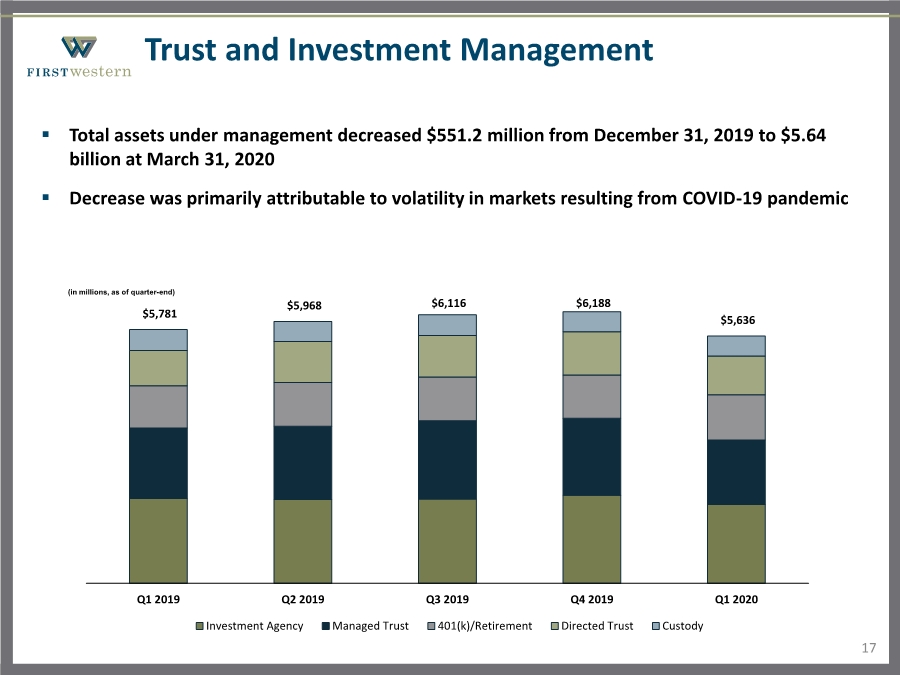

| Trust and Investment Management .. Total assets under management decreased $551.2 million from December 31, 2019 to $5.64 billion at March 31, 2020 .. Decrease was primarily attributable to volatility in markets resulting from COVID-19 pandemic $5,781 $5,968 $6,116 $6,188 $5,636 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Investment Agency Managed Trust 401(k)/Retirement Directed Trust Custody (in millions, as of quarter-end) 17 |

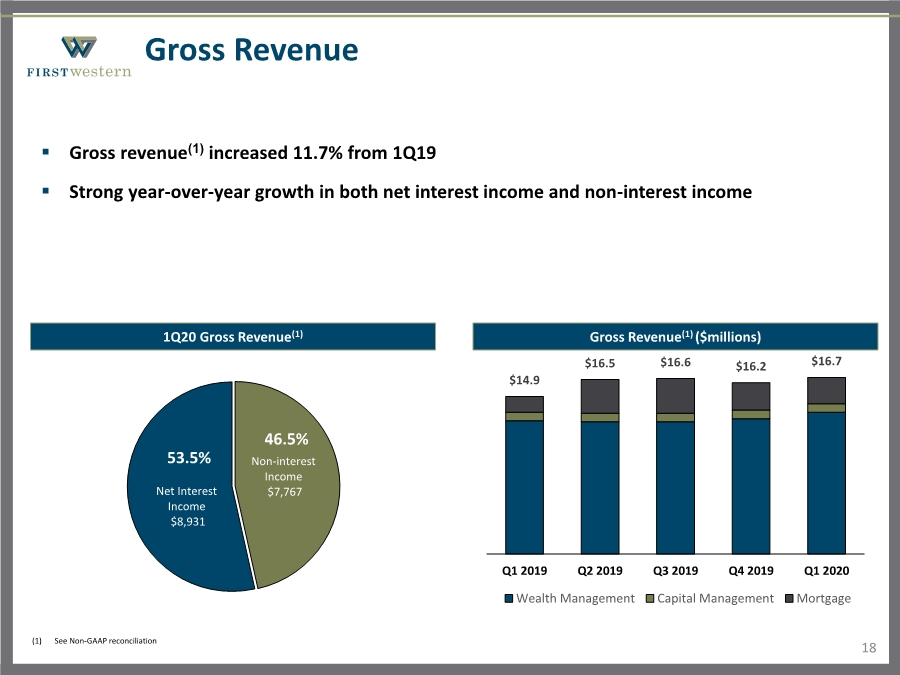

| Non-interest Income $7,767 Net Interest Income $8,931 53.5% 46.5% Gross Revenue 18 (1) See Non-GAAP reconciliation 1Q20 Gross Revenue(1) .. Gross revenue(1) increased 11.7% from 1Q19 .. Strong year-over-year growth in both net interest income and non-interest income Gross Revenue(1) ($millions) $14.9 $16.5 $16.6 $16.2 $16.7 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Wealth Management Capital Management Mortgage |

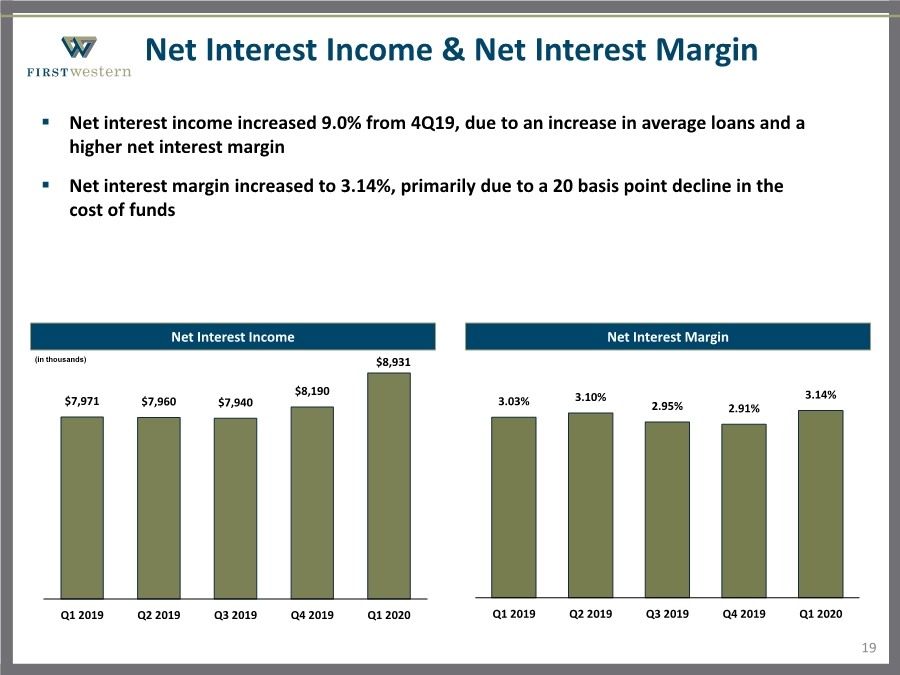

| Net Interest Income & Net Interest Margin 19 Net Interest Income .. Net interest income increased 9.0% from 4Q19, due to an increase in average loans and a higher net interest margin .. Net interest margin increased to 3.14%, primarily due to a 20 basis point decline in the cost of funds Net Interest Margin 3.03% 3.10% 2.95% 2.91% 3.14% Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 $7,971 $7,960 $7,940 $8,190 $8,931 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 (in thousands) |

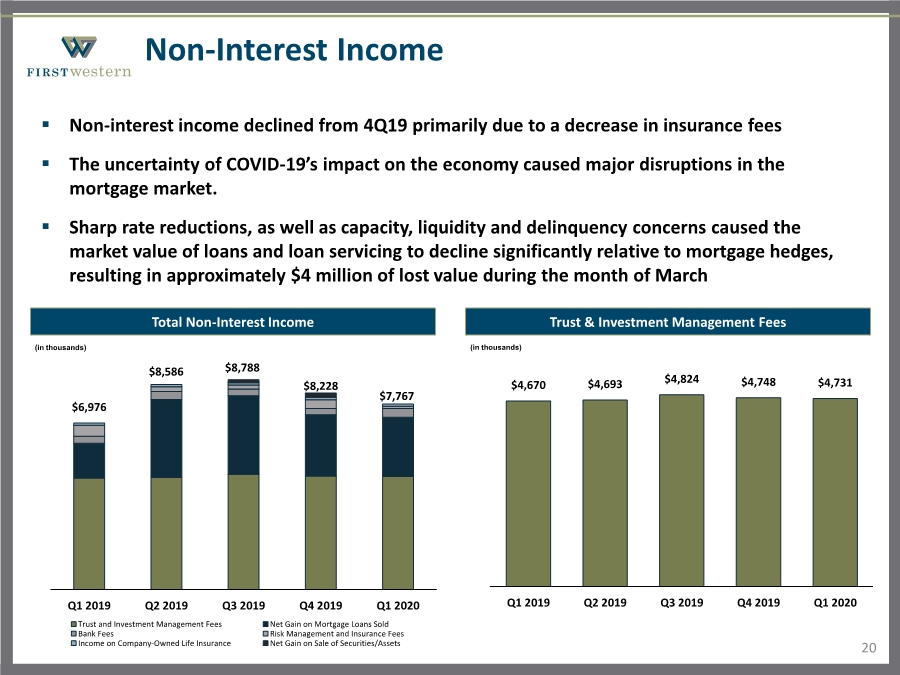

| $4,670 $4,693 $4,824 $4,748 $4,731 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Non-Interest Income 20 Total Non-Interest Income .. Non-interest income declined from 4Q19 primarily due to a decrease in insurance fees .. The uncertainty of COVID-19’s impact on the economy caused major disruptions in the mortgage market. .. Sharp rate reductions, as well as capacity, liquidity and delinquency concerns caused the market value of loans and loan servicing to decline significantly relative to mortgage hedges, resulting in approximately $4 million of lost value during the month of March Trust & Investment Management Fees $6,976 $8,586 $8,788 $8,228 $7,767 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Trust and Investment Management Fees Net Gain on Mortgage Loans Sold Bank Fees Risk Management and Insurance Fees Income on Company-Owned Life Insurance Net Gain on Sale of Securities/Assets (in thousands) (in thousands) |

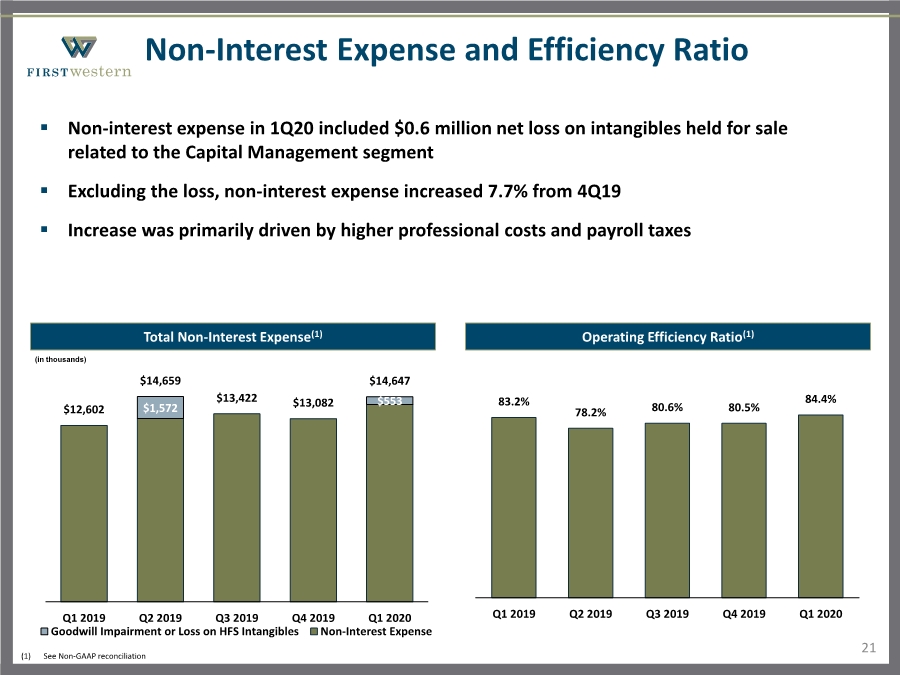

| Non-Interest Expense and Efficiency Ratio 21 Total Non-Interest Expense(1) .. Non-interest expense in 1Q20 included $0.6 million net loss on intangibles held for sale related to the Capital Management segment .. Excluding the loss, non-interest expense increased 7.7% from 4Q19 .. Increase was primarily driven by higher professional costs and payroll taxes Operating Efficiency Ratio(1) 83.2% 78.2% 80.6% 80.5% 84.4% Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 $1,572 $553 $12,602 $14,659 $13,422 $13,082 $14,647 Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 Goodwill Impairment or Loss on HFS Intangibles Non-Interest Expense (in thousands) (1) See Non-GAAP reconciliation |

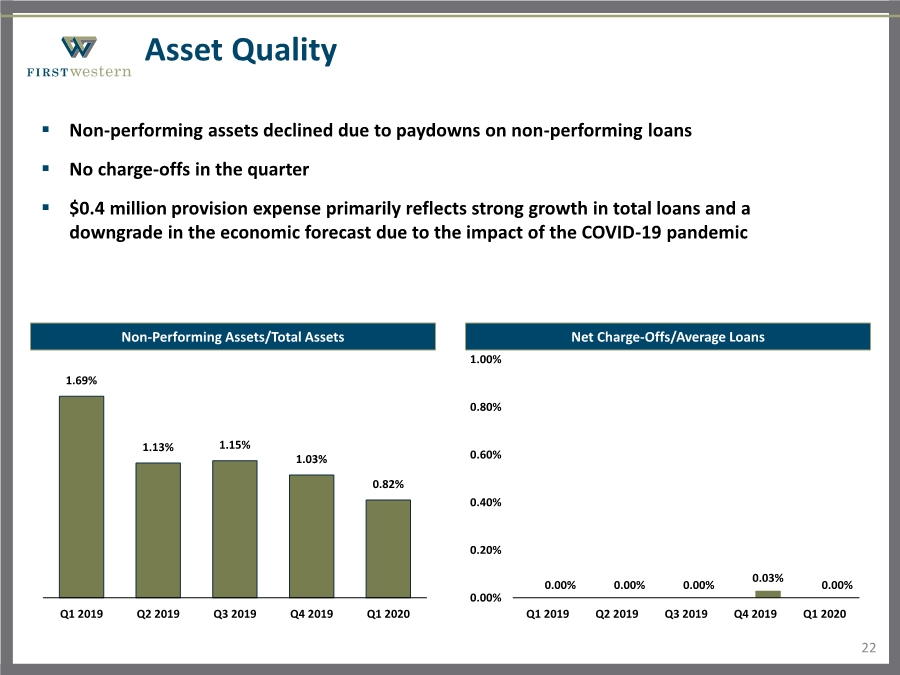

| Asset Quality 22 Non-Performing Assets/Total Assets .. Non-performing assets declined due to paydowns on non-performing loans .. No charge-offs in the quarter .. $0.4 million provision expense primarily reflects strong growth in total loans and a downgrade in the economic forecast due to the impact of the COVID-19 pandemic Net Charge-Offs/Average Loans 0.00% 0.00% 0.00% 0.03% 0.00% 0.00% 0.20% 0.40% 0.60% 0.80% 1.00% Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 1.69% 1.13% 1.15% 1.03% 0.82% Q1 2019 Q2 2019 Q3 2019 Q4 2019 Q1 2020 |

| Appendix |

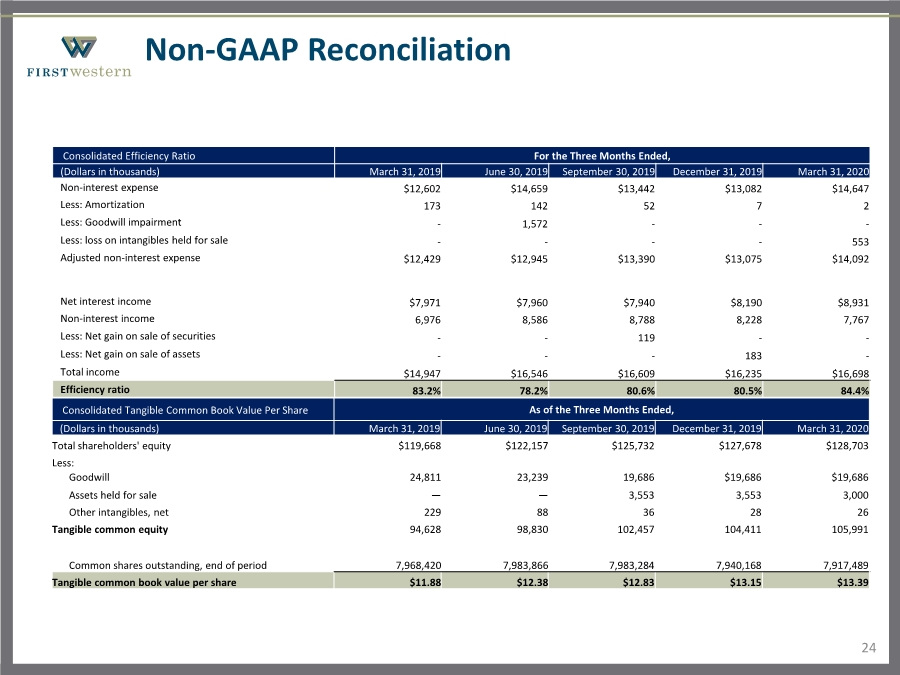

| 24 Non-GAAP Reconciliation Consolidated Efficiency Ratio For the Three Months Ended, (Dollars in thousands) March 31, 2019 June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Non-interest expense $12,602 $14,659 $13,442 $13,082 $14,647 Less: Amortization 173 142 52 7 2 Less: Goodwill impairment - 1,572 --- Less: loss on intangibles held for sale ---- 553 Adjusted non-interest expense $12,429 $12,945 $13,390 $13,075 $14,092 Net interest income $7,971 $7,960 $7,940 $8,190 $8,931 Non-interest income 6,976 8,586 8,788 8,228 7,767 Less: Net gain on sale of securities -- 119 -- Less: Net gain on sale of assets --- 183 - Total income $14,947 $16,546 $16,609 $16,235 $16,698 Efficiency ratio 83.2% 78.2% 80.6% 80.5% 84.4% Consolidated Tangible Common Book Value Per Share As of the Three Months Ended, (Dollars in thousands) March 31, 2019 June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Total shareholders' equity $119,668 $122,157 $125,732 $127,678 $128,703 Less: Goodwill 24,811 23,239 19,686 $19,686 $19,686 Assets held for sale —— 3,553 3,553 3,000 Other intangibles, net 229 88 36 28 26 Tangible common equity 94,628 98,830 102,457 104,411 105,991 Common shares outstanding, end of period 7,968,420 7,983,866 7,983,284 7,940,168 7,917,489 Tangible common book value per share $11.88 $12.38 $12.83 $13.15 $13.39 |

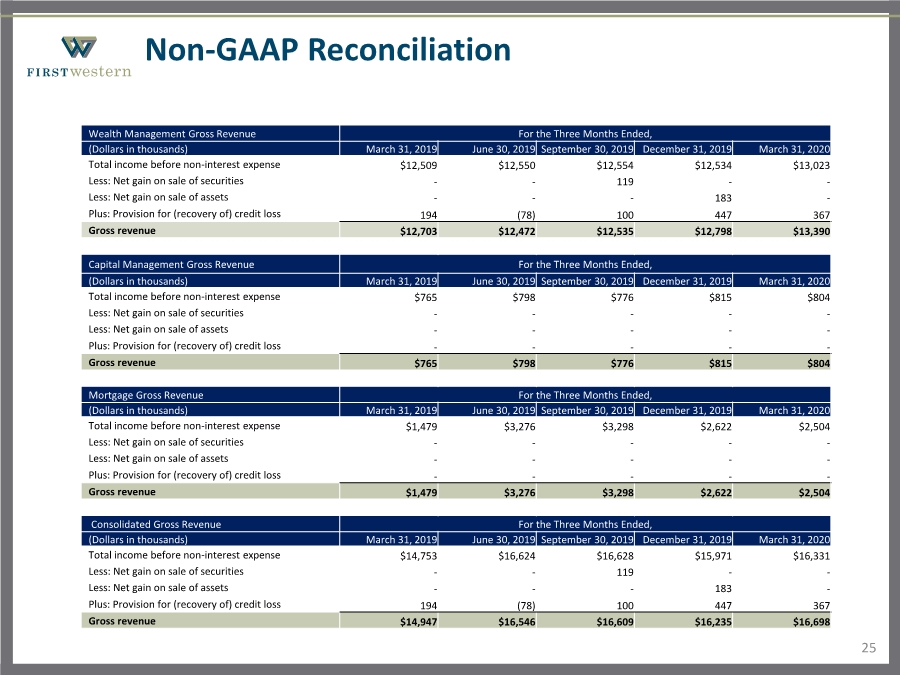

| 25 Non-GAAP Reconciliation Wealth Management Gross Revenue For the Three Months Ended, (Dollars in thousands) March 31, 2019 June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Total income before non-interest expense $12,509 $12,550 $12,554 $12,534 $13,023 Less: Net gain on sale of securities -- 119 -- Less: Net gain on sale of assets --- 183 - Plus: Provision for (recovery of) credit loss 194 (78) 100 447 367 Gross revenue $12,703 $12,472 $12,535 $12,798 $13,390 Capital Management Gross Revenue For the Three Months Ended, (Dollars in thousands) March 31, 2019 June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Total income before non-interest expense $765 $798 $776 $815 $804 Less: Net gain on sale of securities ----- Less: Net gain on sale of assets ----- Plus: Provision for (recovery of) credit loss ----- Gross revenue $765 $798 $776 $815 $804 Mortgage Gross Revenue For the Three Months Ended, (Dollars in thousands) March 31, 2019 June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Total income before non-interest expense $1,479 $3,276 $3,298 $2,622 $2,504 Less: Net gain on sale of securities ----- Less: Net gain on sale of assets ----- Plus: Provision for (recovery of) credit loss ----- Gross revenue $1,479 $3,276 $3,298 $2,622 $2,504 Consolidated Gross Revenue For the Three Months Ended, (Dollars in thousands) March 31, 2019 June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Total income before non-interest expense $14,753 $16,624 $16,628 $15,971 $16,331 Less: Net gain on sale of securities -- 119 -- Less: Net gain on sale of assets --- 183 - Plus: Provision for (recovery of) credit loss 194 (78) 100 447 367 Gross revenue $14,947 $16,546 $16,609 $16,235 $16,698 |

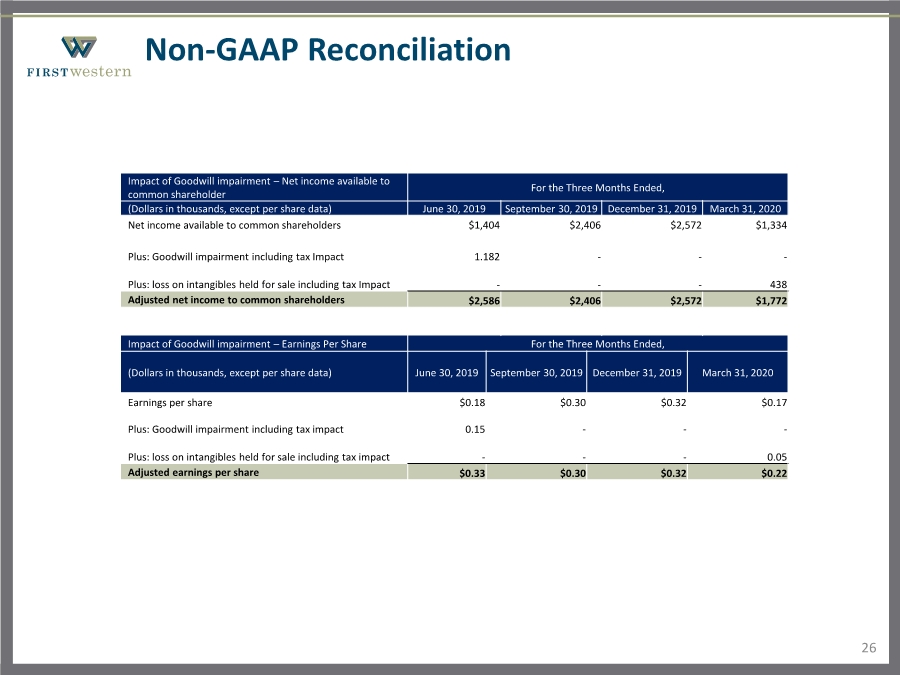

| 26 Non-GAAP Reconciliation Impact of Goodwill impairment – Net income available to common shareholder For the Three Months Ended, (Dollars in thousands, except per share data) June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Net income available to common shareholders $1,404 $2,406 $2,572 $1,334 Plus: Goodwill impairment including tax Impact 1.182 --- Plus: loss on intangibles held for sale including tax Impact --- 438 Adjusted net income to common shareholders $2,586 $2,406 $2,572 $1,772 Impact of Goodwill impairment – Earnings Per Share For the Three Months Ended, (Dollars in thousands, except per share data) June 30, 2019 September 30, 2019 December 31, 2019 March 31, 2020 Earnings per share $0.18 $0.30 $0.32 $0.17 Plus: Goodwill impairment including tax impact 0.15 --- Plus: loss on intangibles held for sale including tax impact --- 0.05 Adjusted earnings per share $0.33 $0.30 $0.32 $0.22 |