UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

FOR THE FISCAL YEAR ENDED DECEMBER 31, 2013

Commission No. 333-128166-10

Affinia Group Intermediate Holdings Inc.

(Exact name of registrant as specified in its charter)

Delaware

(State or other jurisdiction of

incorporation or organization)

I.R.S. Employer Identification Number: 34-2022081

1101 Technology Drive

Ann Arbor, MI 48108

(734) 827-5400

Securities registered pursuant to Section 12(b) of the Act: None

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes x No ¨

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ¨ No x

(Note: As a voluntary filer not subject to the filing requirements of Section 13 or 15(d) of the Exchange Act, the registrant has filed all reports required to be filed by Section 13 or 15(d) of the Exchange Act during the preceding 12 months (or for such shorter period that the registrant would have been required to file such reports) as if it were subject to such filing requirements).

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Website, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer. See the definitions of “large accelerated filer”, “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

| | | | | | |

| Large accelerated filer | | ¨ | | Accelerated Filer | | ¨ |

| | | |

| Non-accelerated filer | | x (Do not check if a smaller reporting company) | | Smaller Reporting Company | | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

There were 1,000 shares outstanding of the registrant’s common stock as of March 31, 2014 (all of which are privately owned and not traded on a public market).

TABLE OF CONTENTS

i

ii

Cautionary Note Regarding Forward-Looking Statements

This report includes “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended (the “Securities Act”) and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). These forward-looking statements include statements concerning our plans, objectives, goals, strategies, future events, future revenue or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions, business trends and other information that is not historical information. When used in this report, the words “anticipates,” “believes,” “estimates,” “expects,” “forecasts,” “intends,” “plans,” “projects,” or future or conditional verbs, such as “could” “may,” “should,” or “will,” and variations of such words or similar expressions are intended to identify forward-looking statements. All forward-looking statements, including, without limitation, management’s examination of historical operating trends and data are based upon our current expectations and various assumptions. Our expectations, beliefs and projections are expressed in good faith and we believe there is a reasonable basis for them. However, there is no assurance that these expectations, beliefs and projections will be achieved. With respect to all forward-looking statements, we claim the protection of the safe harbor for forward-looking statements contained in the Private Securities Litigation Reform Act of 1995.

There are a number of risks and uncertainties that could cause our actual results to differ materially from the forward-looking statements contained in this report. Such risks, uncertainties and other important factors include, among others, domestic and global economic conditions and the resulting impact on the availability and cost of credit; financial viability of key customers and key suppliers; our dependence on our largest customers; increased crude oil and gasoline prices and resulting reductions in global demand for the use of automobiles; the shift in demand from premium to economy products; pricing and pressures from imports; increasing costs for manufactured components, raw materials and energy; the expansion of return policies or the extension of payment terms; risks associated with our non-U.S. operations; risks related to our receivables factoring arrangements; product liability and warranty and recall claims brought against us; reduced inventory levels by our distributors resulting from consolidation and increased efficiency; environmental and automotive safety regulations; the availability of raw materials, manufactured components or equipment from our suppliers; challenges to our intellectual property portfolio; our ability to develop improved products; the introduction of improved products and services that extend replacement cycles otherwise reduce demand for our products; our ability to achieve cost savings from our restructuring plans; our ability to successfully effect dispositions of existing lines of business; our ability to successfully combine our operations with any businesses we have acquired or may acquire; risk of impairment charges to our long-lived assets; risk of impairment to intangibles and goodwill; the risk of business disruptions related to a variety of events or conditions including natural and man-made disasters; risks associated with foreign exchange rate fluctuations; risks associated with our expansion into new markets; the impact on our tax rate resulting from the mix of our profits and losses in various jurisdictions; reductions in the value of our deferred tax assets; difficulties in developing, maintaining or upgrading information technology systems; risks associated with doing business in corrupting environments; our ability to effectively transition our corporate office to our Filtration segment headquarters; our ability to complete the sale our Chassis group; and our substantial leverage and limitations on flexibility in operating our business contained in our debt agreements. Additionally, there may be other factors that could cause our actual results to differ materially from the forward-looking statements.

iii

PART I.

The Company

Affinia Group Intermediate Holdings Inc. (“Affinia”) is a leader in the manufacturing and distribution of global filtration products (“Filtration segment”) and replacement products in South America (“Affinia South America segment”). We operate in the Filtration and the Affinia South America operating segments. The Filtration segment, Affinia’s largest, manufactures and distributes filtration products for medium and heavy-duty trucks, construction, agriculture, mining, and forestry vehicles, and light duty, industrial, and marine applications. The Affinia South America segment manufactures and distributes replacement products for on-road and off-road vehicles, principally in Brazil. Based on management’s estimates and certain information from third parties, Management believes that for the year ended 2013, Affinia holds:

| | • | | the #1 market position in North America for aftermarket filtration products |

| | • | | the #2 market position in Brazilian aftermarket parts distribution |

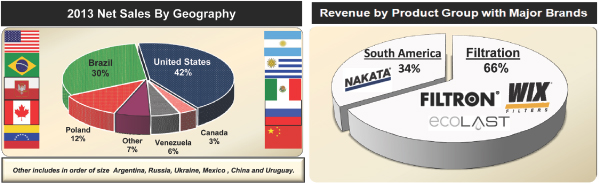

Affinia’s continuing net sales for 2013 were approximately $1.4 billion. The following charts illustrate Affinia’s net sales by geography and segment for continuing operations for the fiscal year ended December 31, 2013.

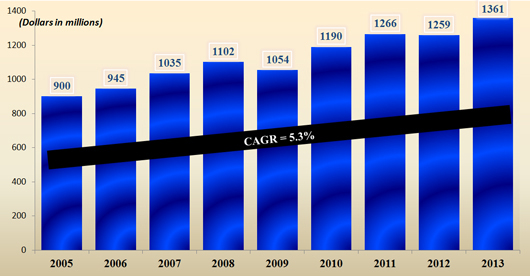

We have successfully entered new markets in Europe and in Central and South America and have grown existing market share in North America, South America and Europe. Additionally, our Affinia South America segment has grown significantly over the past several years. The following chart illustrates the sales growth of Affinia’s continuing operations since our inception.

Contributing to our growth is our long-standing relationship with leading commercial vehicle and automotive parts retailers and wholesale distributors. We have supplied the automotive aftermarket industry for over 70 years and we have supplied our largest customer, NAPA, for over 40 years. We believe that emphasis on our customer service, coupled with the breadth of our product offerings, are key factors in maintaining our leading market positions.

1

Filtration Segment

The Filtration segment is one of the world’s leading designers, manufacturers, marketers, and distributors of a broad range of filtration replacement products . Our filtration business includes manufacturing operations in the U.S., Mexico, Europe, South America and China. It benefits from industry-leading brands, long-standing customer relationships and a global low-cost manufacturing and distribution footprint, along with the all-makes / all-models product line of oil, air, fuel, cabin air, coolant, hydraulic and other filters. For further information about our Filtration segment, refer to “Note 18. Segment Information,” which is included in Item 8. Financial Statements and Supplementary Data.

The Filtration segment products are used in on-road and off-road vehicles, in addition to various industrial, locomotive, and marine applications. The numerous strengths of the Filtration segment have led to a #1 market position in the North America aftermarket and a leading market position in the Eastern Europe aftermarket. The following charts illustrate the historical sales growth, heavy duty and light duty product mix and the sales by geographical location.

Approximately half of the Filtration segment sales are in heavy-duty products. The Filtration segment is among the leading global manufacturers and distributors of aftermarket filters for heavy-duty and off-highway applications, including on-highway trucks, residential and non-residential construction equipment, agricultural, mining, forestry and industrial equipment, severe service vehicles, medium-duty vehicles and marine applications. With over 70 years of experience, Filtration’s heavy-duty filters are designed to withstand harsh elements and provide for optimal filtration and engine protection in less-than-optimal work environments.

Filtration’s full line of heavy-duty products is a key differentiator versus its light duty filtration competitors. In contrast to most light duty competitors, we are able to provide customers with a full suite of filtration options. Customers, particularly distributors, derive value from having a one-stop-shop supplier that is capable of providing products for a diverse range of end markets. Furthermore, heavy-duty filtration products are generally more technologically advanced and are thus typically priced higher than similar light duty products.

The Filtration segment’s automotive and light truck products are at the forefront of filter technology and performance. It’s portfolio of premium line and value line products is designed to exceed performance demands for a variety of applications, including passenger vehicles, sport utility vehicles, motorcycles and ATVs.

We market our Filtration products under a variety of well-known brands, including WIX®, Filtron™ and ecoLAST®. Additionally, we provide private label products to large aftermarket distributors, including NAPA®, CARQUEST® and ACDelco®. We believe that the Filtration segment has achieved its leading market positions due to the quality and reputation of its brands and products among professional installers, who are the primary decision makers for the purchase of the products that we supply to the aftermarket. Our reputation for reliability has helped us penetrate retailers whose customers have become increasingly sophisticated about the quality of the products they install in their vehicles.

2

Filtration Products

Our Filtration segment product lines include oil, air, fuel, hydraulic and other filters for light, medium and heavy duty on and off-highway vehicle, industrial and marine applications. The following chart illustrates the major categories of filter products.

| * | Other consists of cabin air, industrial, hydraulic, coolant, small engine, test kits, gaskets, compressed air and spare products |

The following summarizes a few of our key filter products:

| | |

| |

Oil Filters | | An oil filter traps particles and dirt that might otherwise damage the bearings and rings of a vehicle’s engine. A build-up of particles inside an oil filter can also slow oil flow to the bearings, camshaft and upper valve train components and allow unfiltered oil, possibly containing contaminants, to enter the oil stream and cause accelerated wear on the engine. |

| |

Air Filters | | A vehicle’s air filter traps particles that could otherwise reduce engine performance. A clogged air filter may restrict air flow into the engine, resulting to a shift away from the optimum air to fuel ratio for combustion, and thus reducing gas mileage. |

| |

Fuel Filters | | A vehicle’s fuel filter prevents sediment and rust particles sized three microns or larger from entering and blocking the fuel injector. A clogged fuel filter may restrict fuel flow to the engine, resulting in a loss of fuel pressure and horsepower. |

Filtration Sales Channels and Customers

Our extensive filter product offering fits nearly every car, truck, off-highway and agricultural make and model on the road, allowing us to serve as a full line supplier to our customers for our product categories. These customers primarily comprise large aftermarket distributors and retailers selling to professional technicians or installers. Our customer base also includes original equipment service (“OES”) participants such as ACDelco. Many of our customers are leading aftermarket participants, including NAPA, CARQUEST, Aftermarket Auto Parts Alliance (“the Alliance”), Uni-Select Inc. and O’Reilly Auto Parts. As an active participant in the aftermarket for more than 60 years, we have many long-standing customer relationships.

Approximately 22% and 6% of our 2013 net sales from continuing operations were derived from our two largest customers, NAPA and CARQUEST, respectively. See “Risk Factors—Our business would be materially and adversely affected if we lost any of our larger customers.”

The following table provides a description of the primary sales channels to which we supply our products:

| | | | |

Primary Sales Channels | | Description | | Customers |

| | |

| Traditional | | Warehouses and distribution centers that supply local distribution outlets, which sell to professional installers. | | NAPA, CARQUEST, the Alliance and Uni-Select |

| | |

| Retail | | Retail stores, including national chains that sell replacement parts directly to consumers (the DIY market) and to some professional installers. | | O’Reilly Auto Parts and AutoZone |

| | |

| OES | | Vehicle manufacturers and service departments at vehicle dealerships. | | ACDelco, Robert Bosch, TRW Automotive and Chrysler |

3

The traditional channel is important to us because it is the primary source of products for professional installers. We believe that the quality and reputation of our brands for form, fit, and function promotes significant demand for our products from these installers and throughout the aftermarket supply chain. We have many long-standing relationships with leading distributors in the traditional channel such as NAPA and CARQUEST, for whom we have manufactured products for approximately 40 and 20 years, respectively.

As retailers become increasingly focused on consolidating their supplier base, we believe that our broad product offering, product quality, sales and marketing support and customer service capabilities make us more valuable to these customers.

Affinia South America Segment

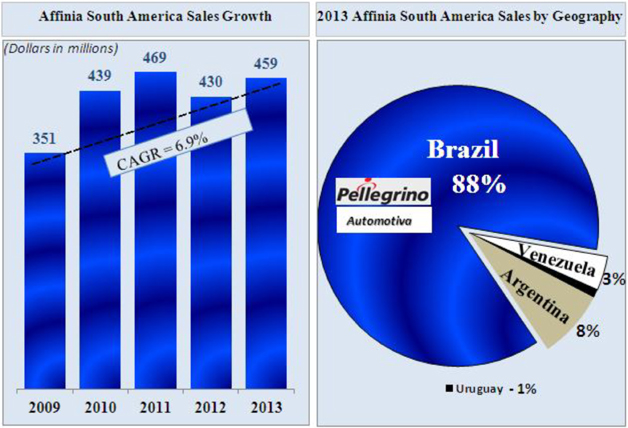

Our Affinia South America segment is a market leader in the distribution and manufacturing of replacement products throughout South America. The segment focuses on distributing and manufacturing products through its operations in Argentina, Brazil, Uruguay and Venezuela. The Affinia South America segment consists of two major operating units: Pellegrino and Automotiva South America (“Automotiva”). The two units are strategically aligned and are operated by the same management team. For further information about our Affinia South America segment, refer to “Note 18. Segment Information,” which is included in Item 8. Financial Statements and Supplementary Data. The following charts show the growth of the Affinia South America segment in U.S. dollars and sales by geography.

Automotiva manufactures shock absorbers in Brazil, brake fluids, antifreeze, and coolants in Argentina, and brake pads and blocks in Uruguay. Automotiva also acts as a master distributor in Brazil, Argentina, and Venezuela. In addition to direct manufacturing, Automotiva is a leader in the supply of chassis components and driveshaft products, assembling, packaging and branding various components from third-party manufacturers. Automotiva’s manufactured and outsourced products are shipped to warehouse distributors both in Brazil and internationally. Pellegrino is Automotiva’s largest customer. In addition, Automotiva exports to Argentina and to 28 other countries around the world. It has a market leading position in a number of products including CV Joints, rear axle sets, chassis parts, universal joint kits, shock absorbers, fuel pumps, and oil pumps. Products are sold under the Nakata®, Spicer® and Power Engine® names.

Pellegrino is a warehouse distributor that sources products from master distributors and other sources including Automotiva, TRW, Bosch, Philips and Mahle. The product portfolio is composed of leading brands for light and heavy-duty vehicles, motorcycle parts and accessories. Pellegrino sells these products to over 22,000 customers including jobber stores, fleets, and independent repair shops in Brazil. Pellegrino has recently expanded its light duty and heavy-duty product offering to include motorcycle and automotive electronics (e.g. GPS systems, speakers). Pellegrino uses its 20 warehouse locations with over 360,000 square feet of warehouse space to service customers in the northeast, midwest, and southern portions of Brazil. Management believes that Pellegrino’s geographic presence and robust product offering have led it to a #2 market share among warehouse distributors in Brazil.

4

Affinia South America products

We manufacture and/or distribute products in Brazil, Argentina, Uruguay and Venezuela, including fuel and water pumps, universal joint kits, axle sets, shocks, steering, filtration products, CV joints, brake products, suspension parts, motorcycle parts, electronics and other aftermarket products.

Affinia South America Sales Channel and Customers

Automotiva’s products are sold to warehouse distributors, which includes Pellegrino, within Brazil, Argentina, Venezuela and internationally. Pellegrino, a warehouse distributor, sells the majority of its products to retailers and jobber stores, with the balance sold to parties such as auto centers, diesel injection centers, motorcycle retailers, heavy-duty fleets and engine rebuilders. Pellegrino and Automotiva do not distribute to installers or end-consumers.

Discontinued Operations

In addition to our Filtration and Affinia South America segments we have a Chassis group, which manufactures and distributes a broad range of chassis products for the aftermarket. In the fourth quarter of 2013, we made the decision to engage in a plan to sell our Chassis group. An agreement was signed in January 2014 to divest our Chassis operations and the group qualified as discontinued operations (refer to Note 3. Discontinued Operation—Chassis).

History and Ownership

The registrant is a Delaware corporation formed on October 18, 2004 and controlled by affiliates of The Cypress Group L.L.C. (“Cypress”). The registrant’s direct wholly-owned subsidiary Affinia Group Inc., a Delaware corporation formed on June 28, 2004, entered into a stock and asset purchase agreement, as amended (the “Purchase Agreement”), with Dana Corporation (“Dana”) on July 8, 2004. The Purchase Agreement provided for the acquisition by Affinia Group Inc. of substantially all of Dana’s aftermarket business operations (the “Acquisition”). The Acquisition was completed on November 30, 2004.

All references in this report to “Affinia,” “Company,” “we,” “our,” and “us” mean, unless the context indicates otherwise, Affinia Group Intermediate Holdings Inc. and its subsidiaries on a consolidated basis.

As a result of the Acquisition, investment funds controlled by Cypress hold approximately 61% of the common stock of our parent, Affinia Group Holdings Inc. (“Holdings”), which directly owns 100% of our common stock, and therefore Cypress controls us. The other principal investors in Holdings are the following: OMERS Administration Corporation (formerly known as Ontario Municipal Employees Retirement Board), California State Teachers Retirement System, The Northwestern Mutual Life Insurance Company and Stockwell Capital.

On December 15, 2005, Holdings, our parent company, entered into stockholder and other agreements with certain officers, directors and key employees (collectively, the “Executives”) of the Company, pursuant to which those Executives purchased an aggregate of 9,520 shares of Holdings common stock for $100 per Share in cash. Holdings received aggregate proceeds of $952,000 as a result of the offering, which was made pursuant to the Affinia Group Holdings Inc. 2005 Stock Incentive Plan (“2005 Stock Plan”). Since 2005, Holdings has re-purchased some of those shares and has issued additional shares (including pursuant to our deferred compensation program), and a shareholder ceased to be an Executive of the Company, as a result of which there were 14,106 shares of Holdings common stock held by Executives outstanding as of December 31, 2013 (excluding shares that may be issued pursuant to our non-qualified deferred compensation plan).

We have divested three groups since 2010. On February 2, 2010, as part of our strategic plan, we sold our Commercial Distribution Europe business unit. Our Commercial Distribution Europe business unit, also known as Quinton Hazell, was a diverse aftermarket manufacturer and distributor of automotive components throughout Europe. On November 30, 2012, we distributed our Brake North America and Asia group to the shareholders of Holdings, the Company’s parent company and sole stockholder, and it was subsequently sold on March 25, 2013 to a new investor. In December 2013, we made the decision to engage in a plan to sell our Chassis group. An agreement was signed in January 2014 to divest our Chassis operations and the group qualified as discontinued operations (refer to Note 3. Discontinued Operation—Chassis).

Sales by Region

Our broad range of filtration and other products are primarily sold in North America, Europe, South America and Asia. We are also focusing on expanding manufacturing capabilities globally to position us to take advantage of global growth opportunities. For information about our segments and our sales by geographic region, refer to “Note 18. Segment Information,” which is included in Item 8. Financial Statements and Supplementary Data.

5

Our Industry

Statements regarding industry outlook, our expectations regarding the performance of our business and other non-historical statements are forward-looking statements. These forward-looking statements are subject to numerous risks and uncertainties, including, but not limited to, the risks and uncertainties described under “Forward-Looking Statements” and “Risk Factors.” Our actual results may differ materially from those contained in or implied by any forward-looking statements. You should read the following discussion together with “Forward-Looking Statements,” “Item 6. Selected Consolidated and Combined Financial Data” and “Item 8. Financial Statements and Supplementary Data.”

We derived approximately 97% of our 2013 net sales from the on and off-highway replacement products and services industry, which is also referred to as the aftermarket. According to AAIA, there were approximately one billion light, medium and heavy-duty vehicles registered worldwide in 2012. Approximately 254 million, or 25%, of these vehicles were registered in the United States. According to the AAIA, the overall size of the U.S. aftermarket was approximately $307.7 billion in 2012. In addition, according to AAIA, the overall size of the U.S. medium and heavy-duty aftermarket was approximately $76.5 billion in 2012 and is expected to grow by a CAGR of 3.4% from 2012 through 2016. According to the Automotive Aftermarket Industry Association (“AAIA”) 2014 Automotive Aftermarket Factbook, the U.S. motor vehicle aftermarket has increased by 3.5% during 2012. In 2013, the industry was forecasted to increase by 3.4% and to continue in 2014 with 3.3% growth.

We believe that the aftermarket will continue to grow as a result of the increase in the average age of light vehicles and the increase in miles driven. According to AAIA, in 2012 the average light vehicle age in the United States was 11.1 years, compared to an average of 9.6 years in 2002. As the average vehicle age continues to rise, we believe that the use of aftermarket products will generally increase as well. In the United States, the total miles driven rose from 2.29 trillion in 1993 to 2.97 trillion in 2013, an increase of approximately 30%. Since 1980, annual miles driven in the United States have increased every year except for 2008 and 2011, when the combination of a recession and high retail fuel prices curtailed driving habits. We expect miles driven in the United States to return to historic growth rates in the future.

To facilitate efficient inventory management and timely vehicle owner customer service, many of our customers and professional installers rely on larger suppliers like us to have full line product offerings, consistent value-added services and timely delivery. There are important advantages to having meaningful size and scale in the aftermarket, including the ability to support significant distribution operations, offer sophisticated supply chain management capabilities and provide a broad line of quality products.

In general, aftermarket industry participants can be categorized into three major groups: (1) manufacturers of parts, (2) distributors of replacement parts (without manufacturing capabilities) and (3) installers, both professional and do-it-yourself (“DIY”) customers. Distributors purchase products from manufacturers and sell them to wholesale or retail operations, which in turn sell them to installers.

6

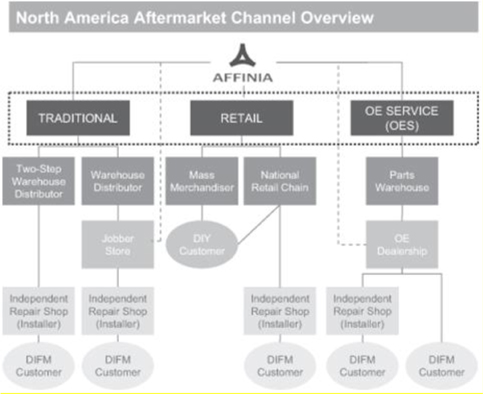

The distribution business is comprised of the (1) traditional, (2) retail and (3) OES channels as illustrated by the chart below.

Typically, professional installers purchase their products through the traditional channel, and DIY customers purchase products through the retail channel. The traditional channel includes such well-known distributors as NAPA, CARQUEST, the Alliance and Uni-Select. Through a network of distribution centers, these distributors sell primarily to owned or affiliated stores, which in turn supply professional installers. The retail channel includes merchants such as AutoZone, O’Reilly Auto Parts and Canadian Tire. The OES channel consists primarily of vehicle manufacturers’ service departments at new vehicle dealerships. Our Affinia South America segment mainly serves the traditional and retail channels.

Customer Support

We believe that our emphasis on customer support has been a key factor in maintaining our leading market positions. We continuously seek to improve service, order turnaround time, product coverage and order accuracy. In order to maintain the competitiveness of our existing customers and maximize new sales opportunities, we have extensive product coverage. In turn, this has allowed our customers to develop a reputation for carrying the parts their customers need, especially for newer vehicles for which warranties may not have expired and aftermarket parts are not generally available.

In addition, as the aftermarket becomes more electronically integrated, customers often prefer to receive their application information electronically as well as in print form. We provide both printed and electronic catalog media. We also provide products which are problem solvers for professional installers, such as alignment products that allow installers to properly align a vehicle, even though the vehicle was not equipped with adjustment features. We provide many other support features, such as technical support hot lines and training and electronic systems which interface with customers and conform to aftermarket industry standards.

Intellectual Property

We strategically manage our portfolio of patents, trade secrets, copyrights, trademarks and other intellectual property.

As of December 31, 2013, we maintain and have pending approximately 250 patents and patent applications on a worldwide basis of which 64 relate to the Chassis group. These patents expire over various periods up to the year 2033. We do not materially rely on any single patent or group of patents. In addition, we believe that the expiration of any single patent or group of patents will not materially affect our business. We have proprietary trade secrets, technology, know-how, processes and other intellectual property rights that are not registered.

7

Trademarks are important to our business activities. We have a robust worldwide program of trademark registration and enforcement to maintain and strengthen the value of the trademarks and prevent the unauthorized use of our trademarks. The WIX trade name is highly recognizable to the public and is a valuable asset. Additionally, we use numerous other trademarks which are registered worldwide or for which we claim common law rights. As of December 31, 2013, we had approximately 800 active trademark registrations and applications worldwide of which 32 related to the Chassis group.

Raw Materials and Manufactured Components

We use a broad range of manufactured components and raw materials in our products, including steel, steel-related components, filtration media, aluminum, brass, iron, rubber, resins, plastics, paper and packaging materials. We purchase raw materials from a wide variety of domestic and international suppliers, and we have not, in recent years, experienced any significant shortages of these items and normally do not carry inventories of these items in excess of those reasonably required to meet our production and shipping schedule. Raw materials comprise the largest component of our manufactured goods cost structure. Commodity prices were generally flat during 2013 in comparison to 2012. We also purchase finished goods from a wide variety of sources for both of our segments. Our costs of purchased filters decreased slightly in 2013 in comparison to 2012.

With our commitment to globalization, we are subject to increases in freight costs due to increased oil prices. We try to recover or offset material cost increases through price increases to our customers and through initiatives to reduce costs, including material substitution, process improvement and product redesigns. The Company experienced no significant supply problems in the purchase of its major raw materials.

Seasonality

In a typical year, we build inventory during the first and second quarters to accommodate our peak sales during the second and third quarters. Our working capital requirements therefore tend to be highest from March through August. In periods of weak sales, inventory can increase beyond typical levels, as our product delivery lead times are less than two days while certain components we purchase from overseas require lead times of approximately 90 days.

Backlog

Substantially all of the orders on hand at December 31, 2013 are expected to be filled during 2014. We do not view our backlog as being insufficient, excessive or problematic, or a significant indication of 2014 sales.

Research and Development Activities

We provide information regarding our research and development activities in “Note 2. Summary of Significant Accounting Policies” to our consolidated financial statements, which is included in “Item 8. Financial Statements and Supplementary Data.”

Competition

The light duty filter aftermarket is comprised of several large U.S. manufacturers that compete with us, including United Components, Inc. under the brand name Champ, FRAM Group, LLC under the brand name FRAM and Purolator Filters NA LLC under the brand name Purolator, along with several international light duty filter suppliers. The heavy-duty filter aftermarket is comprised of several manufacturers that compete with us, including Cummins, Inc. under the brand name Fleetguard, CLARCOR Inc. under the brand name Baldwin and Donaldson Company Inc. under the brand name Donaldson. The Affinia South America segment competitors include Dpk Distribuidora de Pecas, Ltda, Pacaembu Autopeças, Polipeças Comercial e Importadora Ltda and Comdip Comercial Distribuidora de Peças Ltda. We compete on, among other things, quality, price, service, brand reputation, delivery, technology and product offerings.

Employees

As of December 31, 2013, we had 6,266 employees, of whom 2,813 were employed in North America, 1,768 were employed in South America, 1,510 were employed in Europe and 175 were employed in Asia. Approximately 31% of our employees are salaried and the remaining approximately 69% of our employees are hourly. We consider our relations with our employees to be good. Included in our headcount are 354 Chassis group employees in North America.

Environmental Matters

We are subject to a variety of federal, state, local and foreign environmental laws and regulations, including those governing the discharge of pollutants into the air or water, the emission of noise and odors, the management and disposal of hazardous substances or wastes, the clean-up of contaminated sites and human health and safety. Some of our operations require environmental permits and controls to prevent or reduce air and water pollution, and these permits are subject to modification, renewal and revocation by issuing authorities. Contamination has been discovered at certain of our owned properties, which is currently being monitored and/or remediated. We are not aware of any contaminated sites which we believe will result in material liabilities; however, the discovery of additional remedial obligations at these or other sites could result in significant liabilities.ASC Topic 410, “Asset Retirement and Environmental Obligations,” requires that a liability for the fair value of an Asset Retirement Obligation (“ARO”) be recognized in the period in which it is incurred if it can be reasonably estimated, with the offsetting associated asset retirement costs capitalized as part of the carrying amount of the long-lived asset.

8

In addition, many of our current and former facilities are located on properties with long histories of industrial or commercial operations. Because some environmental laws can impose liability for the entire cost of clean-up upon any of the current or former owners or operators, regardless of fault, we could become liable for investigating or remediating contamination at these properties if contamination requiring such activities is discovered in the future. We have incurred environmental remediation costs associated with the comprehensive restructuring and the acquisition restructuring.

We are also subject to the U.S. Occupational Safety and Health Act and similar state and foreign laws regarding worker safety. We believe that we are in substantial compliance with all applicable environmental, health and safety laws and regulations. Historically, our costs of achieving and maintaining compliance with environmental and health and safety requirements have not been material to our operations.

Internet Availability

Available free of charge through our internet website,www.affiniagroup.com, under the investor relations tab are our recent filings of forms 10-K, 10-Q, 8-K and amendments to those reports filed with the Securities and Exchange Commission. These reports can be found on our internet website as soon as reasonably practicable after they are electronically filed with, or furnished to, the Securities and Exchange Commission (“SEC”). The information contained on or connected to our website is not incorporated by reference into this Annual Report on Form 10-K and should not be considered part of this or any other report filed with the SEC.

9

If any of the following events discussed in the following risks were to occur, our results of operations, financial conditions, or cash flows could be materially affected. Additional risks and uncertainties not presently known by us may also constrain our business operations.

Risks Relating to Our Industry and Our Business

Domestic and global economic conditions, including conditions in the global capital and credit markets, have affected and may continue to materially and adversely affect our business, financial condition and results of operations, as well as our ability to access credit and have affected and may continue to materially and adversely affect the financial soundness of our customers and suppliers.

Our business and operating results have been, and will continue to be, affected by domestic and global economic conditions, including conditions in the global capital and credit markets. Domestic and global economies had until recently experienced a period of significant uncertainty, characterized by very weak or negative economic growth, high unemployment, reduced spending by consumers and businesses, bankruptcy, collapse or sale of various financial institutions and a considerable level of intervention from the United States federal government and various foreign governments. Downgrades of long-term sovereign debt issued by the United States and various European countries by Standard & Poor’s, Moody’s and other rating agencies could also affect global and domestic financial markets and economic conditions. Recessionary conditions have materially and adversely affected the demand for our products and services and, therefore, reduced purchases by our customers, which has negatively affected our revenue growth and caused a decrease in our profitability.

Although many vehicle maintenance and repair expenses are non-discretionary, difficult economic conditions may reduce miles driven and thereby increase periods between maintenance and repairs. In addition, interest rate fluctuations, financial market volatility or credit market disruptions may limit our access to capital, and may also negatively affect our customers’ and our suppliers’ ability to obtain credit to finance their businesses on acceptable terms. As a result, our customers’ need for and ability to purchase our products or services may decrease, and our suppliers may increase their prices, reduce their output or change their terms of sale. If our customers’ or suppliers’ operating and financial performance deteriorates, or if they are unable to make scheduled payments or obtain credit, our customers may not be able to pay, or may delay payment of, accounts receivable owed to us, and our suppliers may restrict credit or impose different payment terms. Any inability of customers to pay us for our products and services, or any demands by suppliers for different payment terms, may materially and adversely affect our earnings and cash flow.

If these economic conditions do not improve or continue to deteriorate, our results of operations or financial condition could limit our ability to take actions pursuant to certain covenants in our debt agreements that are tied to ratios based on our financial performance. Such covenants include our ability to incur additional indebtedness, make investments or pay dividends.

Our business would be materially and adversely affected if we lost any of our larger customers.

For the year ended December 31, 2013, approximately 22% and 6% of our net sales from continuing operations were to NAPA and CARQUEST, respectively. To compete effectively, we must continue to satisfy these and other customers’ pricing, service, technology and increasingly stringent quality and reliability requirements. Additionally, our revenues may be affected by decreases in NAPA’s or CARQUEST’s business or market share. Consolidation among our customers may also negatively impact our business. We cannot provide any assurance as to the amount of future business with these or any other customers. While we intend to continue to focus on retaining and winning these and other customers’ business, we may not succeed in doing so. Although business with any given customer is typically split among numerous contracts, the loss of, or significant reduction in purchases by, one of those major customers could materially and adversely affect our business, financial condition and results of operations.

CARQUEST represented our second largest customer for the year ended December 31, 2013. On January 2, 2014, General Parts International, Inc., which owned and operated stores under the CARQUEST brand and also provided services to independently owned stores that operated under the CARQUEST brand, was acquired by Advance Auto Parts, Inc. This merger could materially and adversely affect our business, financial condition and results of operations.

Increased crude oil and gasoline prices could reduce global demand for and use of automobiles and increase our costs, which could have a material and adverse effect on our business, financial condition and results of operations.

Material increases in the price of crude oil have historically been a contributing factor to the periodic reduction in the global demand for and use of automobiles. An increase in the price of crude oil could reduce global demand for and use of automobiles and continue to shift customer demand away from larger cars and light trucks (including sport utility vehicles (“SUVs”), which we believe have more frequent replacement intervals for our products, which could have a material and adverse effect on our business, financial condition and results of operations. Demand for traditional SUVs and vans have declined in the past due, in part, to higher gasoline prices. If this trend were to continue, or if total miles driven were to decrease for a number of years, it could have a material and adverse effect on our business, financial condition and results of operations. Further, as higher gasoline prices result in a reduction in discretionary spending for auto repair by the end users of our products, our results of operations have been, and could continue to be, impacted. Additionally, higher gasoline prices have a material and adverse impact on our freight expenses.

10

The shift in demand from premium to economy brands may require us to produce value products at the expense of premium products, resulting in lower prices, thereby reducing our margins and decreasing our net sales.

We estimate that a majority of our net sales are currently derived from products we consider to be premium products. There has been, and may continue to be, a shift in demand from premium products, on which we can generally command premium pricing and generate enhanced margins, to value products. If such a trend continues, we may be forced to expand our production and/or purchases of value products at competitive prices. In addition, we could be forced to further reduce our prices to remain competitive, in which case our margins will decrease unless we make corresponding reductions in our cost structure.

We are subject to increasing pricing pressure from imports, particularly from lower labor cost countries.

Price competition from other aftermarket manufacturers particularly those based in lower labor cost countries, such as China, have historically played a role and may play an increasing role in the aftermarket sectors in which we compete. While aftermarket manufacturers in these locations have historically competed primarily in markets for less technologically advanced products and manufactured a limited number of products, many are expanding their manufacturing capabilities to produce a broad range of lower labor cost, higher quality products and provide an expanded product offering. In the future, competitors in Asia or other lower labor cost sources may be able to effectively compete in our premium markets and produce a wider range of products which may force us to move additional manufacturing capacity offshore and/or lower our prices, reducing our margins and/or decreasing our net sales.

Increasing costs for manufactured components, raw materials and energy prices may materially and adversely affect our business, financial condition and results of operations.

We use a broad range of manufactured components and raw materials in our products, including raw steel, steel-related components, filtration media, aluminum, brass, iron, rubber, resins, plastics, paper and packaging materials. Materials comprise the largest component of our manufactured goods cost structure. Increases in the price of these items could materially increase our operating costs and materially and adversely affect our profit margins. In addition, in connection with passing through steel and other raw material price increases to our customers, there has typically been a delay of up to several months in our ability to increase prices, which has temporarily impacted profitability. In the future, it may be difficult to pass further price increases on to our customers, especially if we experience additional cost increases soon after implementing price increases. In addition, we have experienced longer than typical lead times in sourcing some of our steel-related components and certain finished products, which has caused us to buy from non-preferred vendors at higher costs.

If our customers seek more expansive return policies or practices, such as extended payment terms, our cash flows and results of operations could be materially and adversely affected.

We are subject to product returns from customers, some of which manage their excess inventory by returning product to us. Our contracts with our customers typically include provisions that permit our customers to return specified levels of their purchases. Returns on a continuing operations basis have historically represented less than 1% of our sales. If returns from our customers significantly increase, our business, financial condition and results of operations may be materially and adversely affected. In addition, some customers in the aftermarket are pursuing ways to shift their costs of working capital, including extending payment terms. To the extent customers extend payment terms, our cash flows and results of operations may be materially and adversely affected.

We are subject to other risks associated with our non-U.S. operations.

We have significant manufacturing operations outside the United States. In 2013, approximately 58% of our net sales from continuing operations originated outside the United States. Risks inherent in international operations include:

| | • | | multiple regulatory requirements that are subject to change and that could restrict our ability to manufacture, market or sell our products; |

| | • | | inflation, recession, fluctuations in foreign currency exchange and interest rates and discriminatory fiscal policies; |

| | • | | trade protection measures; including increased duties and taxes, and import or export licensing requirements; |

| | • | | exposure to possible expropriation or other government actions; |

| | • | | differing local product preferences and product requirements; |

| | • | | difficulty in establishing, staffing and managing operations; |

11

| | • | | differing labor regulations; |

| | • | | potentially negative consequences from changes in or interpretations of tax laws; |

| | • | | political and economic instability and possible terrorist attacks against American interests; |

| | • | | enforcement of remedies in various jurisdictions; and |

| | • | | diminished protection of intellectual property in some countries. |

These and other factors may have a material and adverse effect on our international operations or on our business, financial condition and results of operations. In addition, we may experience net foreign exchange losses due to currency fluctuations.

We are exposed to risks related to our receivables factoring arrangements.

We have entered into agreements with third-party financial institutions to factor on a non-recourse basis certain receivables. The terms of the factoring arrangements provide for the factoring of certain U.S. Dollar-denominated or Canadian Dollar-denominated receivables, which are purchased at the face amount of the receivable discounted at the annual rate of LIBOR plus a bank-determined spread on the purchase date. The amount factored is not contractually defined by the factoring arrangements and our use will vary each month based on the amount of underlying receivables and our cash flow needs. We began factoring certain of our receivables during 2010. For the years ended December 31, 2012 and 2013, we factored $668 million and $541 million of receivables, respectively, and incurred costs on factoring of $5 million and $4 million, respectively, which included our Chassis group and our Brake North America and Asia group. Accounts receivable factored by us are accounted for as a sale and removed from the balance sheet at the time of factoring and the cost of the factoring is accounted for in either other income or discontinued operations if it relates to our Chassis group and our Brake North America and Asia group. If any of the financial institutions we have factoring arrangements with experience financial difficulties or are otherwise unable or unwilling to honor the terms of, or otherwise terminate, our factoring arrangements, we may experience material and adverse economic losses due to the impact of such failure on our liquidity, which could have a material and adverse effect upon our financial condition, results of operations and cash flows.

We may incur material losses and costs as a result of product liability and warranty and recall claims that may be brought against us.

We may be exposed to product liability and warranty claims in the event that our products actually or allegedly fail to perform as expected or the use of our products results, or is alleged to result, in bodily injury and/or property damage. Accordingly, we could experience material warranty or product liability losses in the future and incur significant costs to defend these claims.

In addition, if any of our products are, or are alleged to be, defective, we may be required to participate in a recall of that product if the defect or the alleged defect relates to vehicle safety. Our costs associated with providing product warranties could be material. Product liability, warranty and recall costs may have a material and adverse effect on our business, financial condition and results of operations. Our insurance may not be sufficient to cover such costs.

As a result of the consolidation driven by improved logistics and data management, distributors have reduced their inventory levels, which have reduced and could continue to reduce our sales.

Warehouse distributors have consolidated through acquisition and rationalized inventories, while streamlining their distribution systems through more timely deliveries and better data management. The corresponding reduction in purchases by distributors has negatively impacted our sales. Further consolidation or improvements in distribution systems could have a similar material and adverse impact on our sales.

We are subject to costly regulation, particularly in relation to environmental, health and safety matters, which could materially and adversely affect our business, financial condition and results of operations.

We are subject to a substantial number of costly regulations. In particular, we are required to comply with frequently changing and increasingly stringent requirements of federal, state and local environmental and occupational safety and health laws and regulations in the United States and other countries, including those governing emissions to air, discharges to air and water, and the creation and emission of noise and odor; the generation, handling, storage, transportation, treatment and disposal of waste materials; and the cleanup of contaminated properties and occupational health and safety. We could incur substantial costs, including cleanup costs, fines and civil or criminal sanctions, third-party property damage or personal injury claims, or costs to upgrade or replace existing equipment, as a result of violations of or liabilities under environmental, health and safety laws or non-compliance with environmental permits required at our facilities. In addition, many of our current and former facilities are located on properties with long histories of industrial or commercial operations. Because some environmental laws can impose joint and several liability for the entire cost of cleanup upon any of the current or former owners or operators, regardless of fault, we could become liable for investigating and/or remediating contamination at these properties if contamination requiring such activities is discovered in the future. We cannot assure that we have been, or will at all times be, in complete compliance with all environmental requirements, or

12

that we will not incur material costs or liabilities in connection with these requirements in excess of amounts we have reserved. In addition, environmental requirements are complex, change frequently and have tended to become more stringent over time. These requirements may change in the future in a manner that could have a material and adverse effect on our business, financial condition and results of operations. We have made and will continue to make expenditures to comply with environmental requirements. These requirements, responsibilities and associated expenses and expenditures, if they continue to increase, could have a material and adverse effect on our business and results of operations. While our costs to defend and settle claims arising under environmental laws in the past have not been material, we cannot assure you that this will remain the case in the future. For more information about our environmental compliance and potential environmental liabilities, see “Item 1. Business—Environmental Matters” and “Item 3. Legal Proceedings.”

Our operations would be materially and adversely affected if we are unable to purchase raw materials, manufactured components or equipment from our suppliers.

Because we purchase from suppliers various types of raw materials, finished goods, equipment and component parts, we may be materially and adversely affected by the failure of those suppliers to perform as expected. This non-performance may consist of delivery delays or failures caused by production issues or delivery of non-conforming products. The risk of non-performance may also result from the insolvency or bankruptcy of one or more of our suppliers. Our suppliers’ ability to supply products to us is also subject to a number of risks, including availability of raw materials, such as steel, destruction of their facilities or work stoppages. In addition, our failure to promptly pay, or order sufficient quantities of inventory from, our suppliers may increase the cost of products we purchase or may lead to suppliers refusing to sell products to us at all. Our efforts to protect against and to minimize these risks may not always be effective.

Our intellectual property portfolio could be subject to legal challenges and we may be subject to certain intellectual property claims.

We have developed and actively pursue developing a considerable amount of proprietary technology in the replacement products industry and rely on intellectual property laws of the United States and other countries to protect such technology. In doing so, we incur ongoing costs to enforce and defend our intellectual property. We have from time to time been involved in litigation regarding patents and other intellectual property. We may be subject to material intellectual property claims in the future or we may incur significant costs or losses related to such claims, including payments for licenses that may not be available on reasonable terms, if at all. Our proprietary rights may be challenged, invalidated or circumvented. Moreover, third parties may independently develop technology or other intellectual property that is comparable with or similar to our own, and we may not be able to prevent the use of it.

Our success depends in part on our development of improved products, and our efforts may fail to meet the needs of customers on a timely or cost-effective basis.

Our continued success depends on our ability to maintain advanced technological capabilities, machinery and knowledge necessary to adapt to changing market demands as well as to develop and commercialize innovative products. We cannot assure you that we will be able to develop new products as successfully as in the past or that we will be able to keep pace with technological developments by our competitors and the industry generally. In addition, we may develop specific technologies and capabilities in anticipation of customers’ demands for new innovations and technologies. If such demand does not materialize, we may be unable to recover the costs incurred in such programs. If we are unable to recover these costs or if any such programs do not progress as expected, our business, financial condition or results of operations could be materially and adversely affected.

The introduction of new and improved products and services may reduce our future sales.

Improvements in technology and product quality may extend the longevity of vehicle component parts and delay aftermarket sales. In particular, in our oil filter business the introduction of oil change indicators and the use of synthetic motor oils may further extend oil filter replacement cycles. The introduction of electric, fuel cell and hybrid automobiles may pose a long-term risk to our business because these vehicles may alter demand for our primary product lines. In addition, the introduction by OEMs of increased warranty and maintenance service initiatives, which are gaining popularity, have the potential to decrease the demand for our products in the traditional and retail sales channels.

We may not realize the cost savings that we expect from the restructuring of our operations.

At the end of 2005 we announced the comprehensive restructuring through which we sought to lower costs and improve profitability by rationalizing manufacturing operations and to focus on low-cost sourcing opportunities. We have completed the comprehensive restructuring plan and have realized approximately $100 million in cost savings as a result of the comprehensive restructuring to date. We recently announced the consolidation of our corporate office into our Filtration headquarters in 2014. We may not be able to achieve the level of benefits that we expected to realize or we may not be able to realize these benefits within the timeframes we currently expect. Our expectations regarding cost savings are also predicated upon maintaining our sales levels. Furthermore, the majority of our comprehensive restructuring related to our Brake North America and Asia group, which was distributed from the Company on November 30, 2012, and the related cost savings will no longer benefit us.

13

The consolidation of our corporate office into our Filtration headquarters could adversely affect our business in the current year.

During 2014, we will begin the process of transitioning our corporate office to our Filtration headquarters. This will involve hiring new employees and consolidating certain functions. This may occupy the attention and focus of management, primarily during the first half of 2014, as the transition occurs. The transition involves numerous risks due to significant turnover and the potential diversion of management’s attention from other business concerns.

Any dispositions we make could disrupt our business and materially and adversely affect our business, financial condition and results of operations.

We may, from time to time, consider dispositions of existing lines of business. For example, we distributed our Brake North America and Asia group to the shareholders of Holdings in 2012, and we entered into a purchase agreement to sell our Chassis group in January 2014. Dispositions involve numerous risks, including the diversion of our management’s attention from other business concerns and potential adverse effects on existing business relationships with current customers and suppliers. Additionally, there are risks associated with our chassis products group successfully segregating from the Brake North America and Asia group. Any of these factors could materially and adversely affect our business, financial condition and results of operations.

Any acquisitions we make could disrupt our business and materially and adversely affect our business, financial condition and results of operations.

We may, from time to time, consider acquisitions of complementary companies, products or technologies. Acquisitions involve numerous risks, including the diversion of our management’s attention from other business concerns and potential adverse effects on existing business relationships with current customers and suppliers. Any acquisitions could present difficulties in the assimilation of the acquired business and involve the incurrence of substantial additional indebtedness. We cannot assure that we will be able to successfully integrate any acquisitions that we pursue or that such acquisitions will perform as planned or prove to be beneficial to our operations and cash flow. Any of these factors could materially and adversely affect our business, financial condition and results of operations.

Cypress controls us and may have conflicts of interest with us or the holders of our notes in the future.

Cypress beneficially owns 61% of the outstanding shares of our common stock. As a result, Cypress has control over our decisions to enter into any corporate transaction and has the ability to prevent any transaction that requires the approval of stockholders regardless of whether or not other stockholders or note holders believe that any such transactions are in their own best interests. Additionally, Cypress is in the business of making investments in companies and may from time to time acquire and hold interests in businesses that compete directly or indirectly with us. Cypress may also pursue, for its own account, acquisition opportunities that may be complementary to our business, and, as a result those acquisition opportunities may not be available to us. So long as Cypress continues to own a significant amount of the outstanding shares of our common stock, even if such amount is less than 50%, it will continue to be able to strongly influence or effectively control our decisions including director and officer appointments, potential mergers and acquisitions, asset sales and other significant corporate transactions.

Our ability to maintain our ongoing operations could be impaired.

To be successful and achieve our objectives under our strategic plan, we must retain qualified personnel. The sale of our Chassis group could create uncertainty for our employees and this uncertainty may adversely affect our ability to retain key employees, including our senior management, and to hire new talent necessary to maintain our ongoing operations which could have a material adverse effect on our business. Accordingly, we may fail to maintain our ongoing operations, or execute our strategic plan if we are unable to manage such changes effectively.

We may be required to recognize impairment charges for our long-lived assets, which include fixed assets, intangible assets, and goodwill.

At December 31, 2013, the net carrying value of long-lived assets (property, plant and equipment) totaled $123 million. In accordance with GAAP, long-lived assets shall be tested for recoverability whenever events or changes in circumstances, such as, significant negative industry or economic trends, disruptions to our business, unexpected significant changes or planned changes in use of the assets, divestitures and market capitalization declines indicate that its carrying amount may not be recoverable and may result in charges to long-lived asset impairments. Future impairment charges could significantly affect our results of operations in the periods recognized. Impairment charges would also reduce our consolidated net worth and increase our debt to total capitalization ratio, which could negatively impact our access to the public debt and equity markets.

14

We have $63 million of recorded intangible assets and goodwill on our consolidated balance sheet as of December 31, 2013. These assets may become impaired with the loss of significant customers or a decline of profitability. In assessing the recoverability of goodwill, projections regarding estimated future cash flows and other factors are made to determine the fair value of the respective reporting unit. If these estimates or related projections change in the future, we may be required to record impairment charges for goodwill at that time. If our trade names carrying values exceed fair value we will be required to record an impairment charge.

While our intangibles with definite lives may not be impaired, the useful lives are subject to continual assessment, taking into account historical and expected losses of relationships that were in the base at time of acquisition. This assessment may result in a reduction of the remaining useful life of these assets, resulting in potentially significant increases to non-cash amortization expense that is charged to our consolidated statement of operations. An intangible asset or goodwill impairment charge, or a reduction of amortization lives, could have a material and adverse effect on our results of operations.

Business disruptions could materially and adversely affect our future sales and financial condition or increase our costs and expenses.

Our business may be disrupted by a variety of events or conditions, including, but not limited to, threats to physical security, acts of terrorism, labor stoppages or disruptions, raw material shortages, natural and man-made disasters, information technology failures and public health crises. Any of these disruptions could affect our internal operations or services provided to customers, and could impact our sales, increase our expenses or materially and adversely affect our reputation.

Foreign exchange rate fluctuations could cause a decline in our financial condition, results of operations and cash flows.

As a result of our international operations, we are subject to risk because we generate a significant portion of our revenues and incur a significant portion of our expenses in currencies other than the U.S. Dollar. Our international presence is most significant in Brazil, Canada, China, Mexico and Poland. To the extent that we have significantly more costs than revenues generated in a foreign currency, we are subject to risk if the foreign currency appreciates because the appreciation effectively increases our cost in that country to a greater extent than our revenues. To the extent that we are unable to match revenues received in foreign currencies with costs paid in the same currency, foreign exchange rate fluctuations in that currency could have a material and adverse effect on our financial condition, results of operations and cash flows. In addition, the financial condition, results of operations and cash flows of some of our operating entities are reported in foreign currencies and then translated into U.S. Dollars at the applicable foreign exchange rate for inclusion in our consolidated financial statements. As a result, appreciation of the U.S. Dollar against these foreign currencies generally will have a negative impact on our reported sales and profits.

For example, the Venezuelan government devalued the country’s currency, Bolivar Fuerte (“VEF”), in 2010 and 2013. The 2010 devaluation had a $2 million negative impact on our pre-tax net income in 2010. The 2013 devaluation had a $3 million negative impact on our pre-tax net income in 2013. Further depreciation of the VEF, or depreciation of the currencies of other countries in which we do business, could materially and adversely affect our business, financial condition, results of operations and cash flows. See “Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Business Environment.”

We use a combination of natural hedging techniques and financial derivatives to protect against certain foreign currency exchange rate risks. Such hedging activities may be ineffective or may not offset more than a portion of the adverse financial impact resulting from foreign currency variations. Gains or losses associated with hedging activities also may negatively impact operating results.

Entering new markets poses new competitive threats and commercial risks.

In recent years we have sought to expand our manufacturing and sales into new markets. Expanding into new markets requires investments and resources that may not be available as needed. We cannot guarantee that we will be successful in leveraging our capabilities to compete favorably in new markets or that we will be able to recoup our significant investments in expansion projects. If our customers in new markets experience reduced demand for their products or financial difficulties, our future prospects will be negatively affected as well.

The mix of profits and losses in various jurisdictions may have an impact on our overall tax rate, which in turn, may materially and adversely affect our profitability.

Tax expenses and benefits are determined separately for each of our taxpaying entities or groups of entities that is consolidated for tax purposes in each jurisdiction. Losses in such jurisdictions may provide no current financial statement tax benefit. As a result, changes in the mix of projected profits and losses between jurisdictions, among other factors, could have a significant impact on our overall effective tax rate.

15

The value of our deferred tax assets could become impaired, which could materially and adversely affect our operating results.

As of December 31, 2013, we had $117 million in net deferred tax assets. These deferred tax assets include net operating loss carryforwards that can be used to offset taxable income in future periods and reduce income taxes payable in those future periods. We periodically determine the probability of the realization of deferred tax assets, using significant judgments and estimates with respect to, among other things, historical operating results, expectations of future earnings and tax planning strategies. If we determine in the future that there is not sufficient positive evidence to support the valuation of these assets, due to the factors described above or other factors, we may be required to further adjust the valuation allowance to reduce our deferred tax assets. Such a reduction could result in material non-cash expenses in the period in which the valuation allowance is adjusted and could have a material and adverse effect on our results of operations.

Our ability to utilize our net operating loss carryforwards may be limited and delayed. As of December 31, 2013, we had U.S. net operating loss carryforwards of $301 million. Certain provisions of the Internal Revenue Code of 1986, as amended (the “Code”) could limit our annual utilization of the net operating loss carryforwards. There can be no assurance that we will be able to utilize all of our net operating loss carryforwards and any subsequent net operating loss carryforwards in the future.

We must successfully maintain and/or upgrade our information technology systems.

We rely on various information technology systems to manage our operations. We are currently implementing modifications and upgrades to our systems, including making changes to legacy systems, replacing legacy systems with successor systems with new functionality and acquiring new systems with new functionality. These types of activities subject us to inherent costs and risks associated with replacing and changing these systems, including impairment of our ability to fulfill customer orders, potential disruption of our internal control structure, substantial capital expenditures, additional administration and operating expenses, retention of sufficiently skilled personnel to implement and operate the new systems, demands on management time, and other risks and costs of delays or difficulties in transitioning to new systems or of integrating new systems into our current systems. Our system implementations may not result in productivity improvements at a level that outweighs the costs of implementation, or at all. In addition, the implementation of new technology systems may cause disruptions in our business operations and have an adverse effect on our business and operations, if not anticipated and appropriately mitigated.

Our international operations are subject to political and economic risks of developing countries and special risks associated with doing business in corrupting environments.

We design, manufacture, distribute and market a broad range of aftermarket products in various regions, some of which are less developed, have less stability in legal systems and financial markets and are generally recognized as potentially more corrupt business environments than the United States, and therefore present greater political, economic and operational risks. We have in place certain policies, procedures and certain ongoing training of employees with regard to business ethics and many key legal requirements, such as applicable anti-corruption laws, including the U.S. Foreign Corrupt Practices Act (the “FCPA”), which make it illegal for us to give anything of value to foreign officials in order to obtain or retain any business or other advantages; however, there can be no assurance that our employees will adhere to our code of business conduct and ethics or any other of our policies, applicable anti-corruption laws, including the FCPA, or other legal requirements. If we fail to enforce our policies and procedures properly or fail to maintain adequate record-keeping and internal accounting practices to accurately record our transactions, we may be subject to regulatory sanctions. In the event that we believe or have reason to believe that our employees have or may have violated applicable anti-corruption laws, including the FCPA, or other laws or regulations, we are required to investigate or have outside counsel investigate the relevant facts and circumstances, and if violations are found or suspected we could face civil and criminal penalties, and significant costs for investigations, litigation, fees, settlements and judgments, which in turn could have a material and adverse effect on our business.

Risks Relating to Our Indebtedness

Our substantial leverage could harm our business by limiting our available cash and our access to additional capital and, to the extent of our variable rate indebtedness, exposing us to interest rate risk.