UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM 10-K

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF

THE SECURITIES EXCHANGE ACT OF 1934

Year ended December 31, 2008

8540 Gander Creek Drive

Miamisburg, Ohio 45342

877.855.7243

| | | | | | |

Commission File Number | | Registrant | | IRS Employer Identification Number | | State of Incorporation |

| 001-32956 | | NEWPAGE HOLDING CORPORATION | | 05-0616158 | | Delaware |

| 333-125952 | | NEWPAGE CORPORATION | | 05-0616156 | | Delaware |

Securities Registered Pursuant to Section 12(b) of the Act: None

Securities Registered Pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

| | | | | | |

NewPage Holding Corporation | | Yes | ¨ | | No | x |

NewPage Corporation | | Yes | ¨ | | No | x |

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act.

| | | | | | |

NewPage Holding Corporation | | Yes | ¨ | | No | x |

NewPage Corporation | | Yes | ¨ | | No | x |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

| | | | | | |

NewPage Holding Corporation | | Yes | x | | No | ¨ |

NewPage Corporation | | Yes | x | | No | ¨ |

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K.

|

NewPage Holding Corporation x NewPage Corporation x |

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act:

| | | | |

NewPage Holding Corporation | | Large accelerated filer ¨ | | Accelerated filer ¨ |

| | Non-accelerated filer x | | Smaller reporting company ¨ |

| | | | |

NewPage Corporation | | Large accelerated filer ¨ | | Accelerated filer ¨ |

| | Non-accelerated filer x | | Smaller reporting company ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

| | | | |

NewPage Holding Corporation | | Yes ¨ | | No x |

NewPage Corporation | | Yes ¨ | | No x |

The aggregate market value of NewPage Holding Corporation and NewPage Corporation common stock held by non-affiliates were each $0 as of June 30, 2008.

The number of shares of each Registrant’s Common Stock, par value $0.01 per share, as of February 20, 2009:

| | |

NewPage Holding Corporation | | 10 |

NewPage Corporation | | 100 |

This Form 10-K is a combined annual report being filed separately by two registrants: NewPage Holding Corporation and NewPage Corporation. NewPage Corporation meets the conditions set forth in general instruction I(1)(a) and (b) of Form 10-K and is therefore filing this form with the reduced disclosure format.

DOCUMENTS INCORPORATED BY REFERENCE—None

References to “NewPage Holding” refer to NewPage Holding Corporation, a Delaware corporation; references to “NewPage” refer to NewPage Corporation, a Delaware corporation and a wholly-owned subsidiary of NewPage Holding. As applicable by the context used, references to “we,” “us” and “our” refer to NewPage Holding and its subsidiaries. All assets, liabilities, income, expenses and cash flows presented for all periods represent those of NewPage Holding’s wholly-owned subsidiary, NewPage, except for NewPage Holding’s debt obligation and related financing costs, interest expense, write-off of costs for a withdrawn 2006 initial public offering and income tax effects. Unless otherwise noted, the information provided pertains to both NewPage Holding and NewPage. References to “SENA” are to Stora Enso North America Inc., which we acquired from Stora Enso Oyj (“SEO”) on December 21, 2007 (the “Acquisition”). Following the Acquisition, SENA changed its name to NewPage Consolidated Papers Inc., or NPCP. References to both SENA and NPCP are to the acquired business.

FORWARD-LOOKING STATEMENTS

This annual report contains “forward-looking statements” within the meaning of the Securities Exchange Act of 1934, the Private Securities Litigation Reform Act of 1995 and other related laws. All statements other than statements of historical fact are “forward-looking statements” for purposes of federal and state securities laws. Forward-looking statements may include the words “may,” “plans,” “estimates,” “anticipates,” “believes,” “expects,” “intends” and similar expressions. Although we believe that these forward-looking statements are based on reasonable assumptions, they are subject to numerous factors, risks and uncertainties that could cause actual outcomes and results to be materially different from those projected or assumed in our forward-looking statements. These factors, risks and uncertainties include, among others, the following:

| | • | | our substantial level of indebtedness |

| | • | | changes in the supply of, demand for, or prices of our products |

| | • | | general economic and business conditions in the United States and Canada and elsewhere |

| | • | | the ability of our customers to continue as a going concern, including our ability to collect accounts receivable according to customary business terms |

| | • | | the activities of competitors, including those that may be engaged in unfair trade practices |

| | • | | changes in significant operating expenses, including raw material and energy costs |

| | • | | changes in currency exchange rates |

| | • | | changes in the availability of capital |

| | • | | changes in the regulatory environment, including requirements for enhanced environmental compliance |

| | • | | our ability to realize the anticipated benefits of the acquisition of SENA, including anticipated synergies |

| | • | | the other factors described under “Risk Factors” |

Given these risks and uncertainties, we caution you not to place undue reliance on forward-looking statements. We undertake no obligation to update or revise any forward-looking statements, either to reflect new developments or for any other reason, except as required by law.

1

INDUSTRY DATA

Information in this annual report concerning the paper and forest products industry and our relative position in the industry is based on independent industry analyses, management estimates and competitor announcements.

PART I

General

We believe that we are the largest coated paper manufacturer in North America based on production capacity. Coated paper is used primarily in media and marketing applications, such as corporate annual reports, high-end advertising brochures, direct mail advertising, coated labels, magazines, magazine covers and inserts and catalogs. For the year ended December 31, 2008, we had net sales of $4.4 billion.

We operate 20 paper machines at ten paper mills located in Kentucky, Maine, Maryland, Michigan, Minnesota, Wisconsin and Nova Scotia, Canada. These mills and our distribution centers are strategically located near major print markets, such as New York, Chicago, Minneapolis and Atlanta. As of December 31, 2008, our mills have total annual production capacity of approximately 4.4 million short tons of paper, including approximately 3.2 million short tons of coated paper, approximately 1 million short tons of uncoated paper and approximately 200,000 short tons of specialty paper.

We have long-standing relationships with many leading publishers, commercial printers, retailers and paper merchants. Our key customers include Condé Nast Publications, The McGraw-Hill Companies, Meredith Corporation, News America Group, Pearson Education, Rodale Inc. and Time Inc. in publishing; Quad/Graphics, Quebecor World Inc. and R.R. Donnelley & Sons Company in commercial printing; Sears Holdings Corporation and Williams-Sonoma, Inc. in retailing; and paper merchants Lindenmeyr, a division of Central National-Gottesman Inc., Unisource Worldwide, Inc. and xpedx, a division of International Paper Company. Key customers for specialty paper products include Avery Dennison Corporation and Vacumet Corp.

On December 21, 2007, NewPage acquired all of the issued and outstanding common stock of SENA from SEO. We acquired SENA in order to create a single business platform and to enable us to remain competitive in the marketplace, serve our customers more efficiently and achieve synergies from the Acquisition. The Acquisition more than doubled our production capacity and broadened our product line.

2

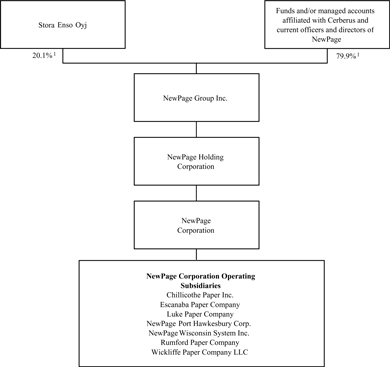

Organization

The following chart shows our organizational structure and ownership as of February 20, 2009. Except as indicated below, each entity in the chart owns 100% of the equity interests of the entity appearing immediately below it.

| (1) | Excludes NewPage Group common stock that may be issued upon exercise of options outstanding or that may be granted under the NewPage Group Equity Incentive Plan. |

3

Industry Overview

The North American paper industry is cyclical and, like other cyclical industries, is largely affected by the interplay of demand and supply. Demand and supply factors affecting our principal paper products, as well as historical price trends, are discussed below.

North American coated paper demand is primarily driven by advertising and print media usage. In particular, the demand for certain grades of coated paper is affected by spending on catalog and promotional materials by retailers and spending on magazine advertising, which affects the number of printed pages in magazines. Advertising spending and magazine and catalog circulation tend to rise when GDP in the United States is robust and typically decline in a sluggish economy. During 2008, North American coated paper demand declined significantly compared to 2007, as a result of decreased advertising spending and magazine and catalog circulation resulting from macroeconomic factors. North American customers purchased approximately 12 million short tons of coated paper in 2008 and approximately 13 million short tons of coated paper in 2007.

In North America and the United States, coated paper supply is determined by both local coated paper production and imports from sources outside North America or the United States, principally Europe and Asia. Imports have become a structural part of the North American coated paper marketplace. The volume of coated paper imports from Europe and Asia is a function of worldwide supply and demand for coated paper, the exchange rate of the U.S. dollar relative to other currencies, especially the Euro, market prices in North America and other markets and the cost of ocean-going freight. North American producers, including us, have announced the scheduled shutdown of an aggregate of approximately 2 million short tons of coated paper capacity over the last two years, primarily as a result of higher costs and, more recently, as a result of reduced demand.

Products

Our portfolio of paper products includes coated freesheet, coated groundwood, supercalendered, newsprint and specialty papers. Specialty papers are primarily used in labels and packaging. We offer the broadest coated paper product selection of any North American paper manufacturer. We also sell uncoated paper and market pulp. Our brands are some of the most recognized brands in the industry. Substantially all of our 2008 sales were within North America and approximately 93% were within the United States. Our principal product is coated paper, which represented approximately 81%, 92% and 93% of our net sales for the years ended December 31, 2008, 2007 and 2006.

Coated Paper

We believe that we are the largest coated paper manufacturer in North America based on production capacity. As of December 31, 2008, our mills have total annual production capacity of approximately 3.2 million short tons of coated paper. Coated paper is used primarily in media and marketing applications, including corporate annual reports, high-end advertising brochures, magazines, catalogs and direct mail advertising. Coated paper has a higher level of smoothness than uncoated paper. Increased smoothness is typically achieved by applying a clay-based coating on the surface of the paper and processing that paper under heat and pressure. As a result, coated paper achieves higher reprographic quality and printability.

Coated paper consists of both coated freesheet and coated groundwood, which generally differ in price and quality. The chemically-treated pulp used in freesheet applications produces brighter and smoother paper than the mechanical pulp used in groundwood papers. Coated freesheet papers comprised 56% of the coated paper we produced in 2008. We produce coated freesheet papers in No. 1, No. 2 and No. 3 grades for higher-end uses such as corporate annual reports and high-end advertising, as well as coated one-side paper (C1S), which is used primarily for label and specialty applications.

4

Coated groundwood papers, which represented 44% of the coated paper we produced in 2008, are typically lighter and less expensive than our coated freesheet products. We produce coated groundwood papers in No. 3, No. 4 and No. 5 grades for use in applications requiring lighter paper stock such as magazines, catalogs and inserts.

Each of the paper grades that we manufacture are produced in a variety of weights, sizes and finishes. The coating process changes the gloss, ink absorption qualities, texture and opacity of the paper to meet each customer’s performance requirements. Most of the coated paper that we manufacture is shipped in rolls, with the rest cut into sheets.

Supercalendered Paper

Supercalendered paper is uncoated paper with pigment filler passed through a supercalendering process in which alternating steel and cotton-covered rolls “iron” the paper, giving it a gloss and smoothness similar to coated paper. Our supercalendered paper is primarily used for magazines, catalogs, advertisements, inserts and flyers. We produce supercalendered paper primarily in SC-A and SC-A+ grades.

Newsprint Paper

Newsprint paper is uncoated groundwood paper used primarily for printing daily newspapers and other publications. We are a niche supplier of newsprint paper serving the North American and select international markets in the publishing and printing industry for major end-uses such as inserts/fliers for retail customers.

Specialty Paper

Specialty paper consists of both coated and uncoated paper designed and produced to meet the specific packaging, printing and labeling needs of customers with diverse and specialized paper needs. Specialty papers consist of two primary product lines: technical papers and packaging papers.

Technical papers consist of face papers, thermal transfer, direct thermal base papers and release liners for use in self-adhesive labels. Packaging papers are designed to protect, transport and identify a wide range of products. Flexible packaging papers are often used as part of a multilayer package construction, in combination with film, foil, extruded coatings, board and other materials. For example, flexible packaging papers are used in pouch, lidding, bag, tobacco packaging and spiral can applications.

Other Products

We also produce uncoated paper to enhance our manufacturing efficiency by filling unused capacity, such as when we have excess capacity on a paper machine but not on a coater. Uncoated paper typically is used for business forms and stationery, general printing paper and photocopy paper. We primarily sell uncoated paper to paper merchants, business forms manufacturers and converters.

Manufacturing

We operate 20 paper machines at ten paper mills located in Kentucky, Maine, Maryland, Michigan, Minnesota, Wisconsin and Nova Scotia, Canada. All of these paper mills are at least partially-integrated mills, meaning that they produce paper, pulp and energy. Most of the energy produced at these mills is for internal use. As of December 31, 2008, our mills have total annual production capacity of

5

approximately 4.4 million short tons of paper, including approximately 3.2 million short tons of coated paper, approximately 1 million short tons of uncoated paper and approximately 200,000 short tons of specialty paper. With the exception of our Port Hawkesbury, Nova Scotia, mill, substantially all of our long-lived assets are located within the United States. The following table lists the paper products produced at each of our mills, as well as each mill’s approximate annual paper capacity, as of December 31, 2008:

| | | | |

Mill Location | | Products | | Paper Capacity

(short tons/year) |

Biron, Wisconsin | | Coated paper | | 400,000 |

Duluth, Minnesota | | Supercalendered paper | | 260,000 |

Escanaba, Michigan | | Coated and uncoated paper | | 790,000 |

Luke, Maryland | | Coated and specialty paper | | 530,000 |

Port Hawkesbury, Nova Scotia | | Supercalendered paper and newsprint | | 590,000 |

Rumford, Maine | | Coated and specialty paper | | 570,000 |

Stevens Point, Wisconsin | | Specialty paper | | 170,000 |

Whiting, Wisconsin | | Coated paper | | 260,000 |

Wickliffe, Kentucky | | Coated, specialty and uncoated paper | | 310,000 |

Wisconsin Rapids, Wisconsin | | Coated paper | | 520,000 |

During 2008, we announced restructuring plans which included the shutdown of six of our less efficient, higher cash cost paper machines. We closed the No. 11 paper machine in Rumford, Maine in February 2008, the No. 95 paper machine in Kimberly, Wisconsin in May 2008, the Niagara, Wisconsin paper mill, which included two paper machines, in June 2008 and the Kimberly, Wisconsin mill, which included the two remaining paper machines, in September 2008. We have reallocated production of paper grades across our remaining combined machine base, resulting in the operation of machines in narrower ranges of paper grades around their peak production. In addition, as of December 31, 2008 we ceased substantially all production at our Chillicothe, Ohio converting facility and have transferred production to our remaining two converting facilities in Luke, Maryland and Wisconsin Rapids, Wisconsin. We completed the shutdown of this facility in February 2009. As a result of the restructuring activities undertaken, we have reduced our overall workforce by approximately 8% as of December 31, 2008 as compared to December 31, 2007. For a further discussion of these actions, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview—Anticipated Synergies of the Acquisition and Integration of the Business.”

Through reallocation of production among our combined mills, we are producing products in closer proximity to our customers to reduce lowering freight costs. In addition, we continue to implement best practices across our combined mill system and focus on increasing our overall profitability, rather than independently at each individual mill.

Since 2000, over $1.4 billion of capital expenditures have been invested in our paper mills currently in operation, to build, maintain and update facilities and equipment, enhance product mix, lower costs and meet environmental requirements. These upgrades also included an upgrade of our papermaking technology to support our high-end coated grade lines.

In addition to the restructuring actions described above, over the last several years, we have significantly reduced our costs by consolidating operations and focusing on operational efficiency. We reduced our salaried headcount by approximately 28% and our hourly headcount by approximately 20% from 2002 to the time of the Acquisition in December 2007. From January 2002 to the time of the Acquisition, we shut down six paper machines, closed one paper mill and reduced maintenance costs by improving our annual maintenance shutdown procedures. From August 2000 to the time of the Acquisition, SENA reduced salaried headcount by approximately 38% and hourly headcount by approximately 40%. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview—Anticipated Synergies of the Acquisition and Integration of the Business.”

6

The first step in the production of paper is to produce pulp from wood. Pulp for groundwood and supercalendered paper is produced using a mechanical or thermo-mechanical process. Pulp for freesheet paper is produced by placing wood chips that are mixed with various chemicals into digester “cooking” vessels. The pulp is then washed and bleached. To turn the pulp into paper, it is processed through a paper machine. Hardwood and softwood pulp is blended based on the desired paper characteristics.

To produce coated paper, uncoated paper is put through a coating process. Our mills have both on-machine coaters, which are integrated with the paper machines, and separate off-machine coaters. On-machine coaters generally are considered to be more efficient, while off-machine coaters generally are considered to have more flexibility. After the coating process is complete, the coated paper is slit and wound into rolls to be sold to customers. We also have converting facilities at which we convert some of these rolls into sheets.

Paper machines are large, complex systems that operate more efficiently when operated continuously. Paper machine production and yield decline when a machine is stopped for any reason. Therefore, we organize our manufacturing processes so that our paper machines and most of our paper coaters run almost continuously throughout the year. Some of our paper machines also offer the flexibility to change the type of paper produced on the machine, which allows easier matching of production schedules and seasonal and geographic demand swings.

Paper production is energy intensive. During 2008, we produced approximately 45% of our energy requirements by means of our mill-generated fuels, which included black liquor, wood waste and bark. The energy we purchased from outside suppliers consisted of a portion of our electricity, natural gas, fuel oil, steam, petroleum coke, tire-derived fuel, wood waste and coal. The majority of our coal needs are purchased under long-term supply contracts, while the other purchased fuels are priced based on current market rates.

Our wholly-owned subsidiary, Consolidated Water Power Company, or CWPCo, provides energy to our mills in central Wisconsin. CWPCo has 33.3 megawatts of generating capacity on 39 generators located in five hydroelectric plants on the Wisconsin River. CWPCo is a regulated public utility and also provides electricity to a small number of other residential, light commercial and light industrial customers.

We also are the general partner and have a 30% investment in Rumford Cogeneration Company L.P., a joint venture created to generate power for us at our Rumford mill and for public sale. We have an option through 2014 to purchase all of our co-investors’ interests in the partnership.

Raw Materials and Suppliers

Pulp and wood fiber are the primary raw materials used in making paper. Pulp is the generic term that describes the cellulose fiber derived from wood. These fibers may be separated by mechanical, thermo-mechanical or chemical processes. The processes we use at our mills to produce pulp for freesheet paper involve removing the glues, which bind the wood fibers, to leave cellulose fibers. We use most of our pulp production internally to reduce the amount of pulp purchased from third parties. We sell our excess hardwood pulp, which we refer to as market pulp, to third parties in the United States and internationally.

The primary sources of wood fiber are timber and its byproducts, such as wood chips. We are a party to various fiber supply agreements to supply our mills with hardwood, softwood, aspen pulpwood and wood chips. These agreements require the counterparty to sell to the mills, and require the mills to purchase, a designated minimum number of tons of pulpwood and wood

7

chips during the specified terms of the arrangement, which have various expiration dates from December 31, 2009 to December 31, 2053. The annual purchase requirement under these agreements is approximately 3 million tons in 2009, approximately 2 million tons per year from 2010 to 2015, approximately 1 million tons per year from 2016 to 2020 and approximately 250,000 tons per year from 2021 to 2026. In 2020, all of the agreements terminate with the exception of the agreement with respect to the Rumford mill, which terminates in 2053. For all of the pulpwood agreements, we may purchase a substantial portion of any additional pulpwood harvested by the counterparty during each year. The prices to be paid under these agreements are determined by formulas based upon market prices in the relevant regions and are subject to periodic adjustments based on procedures stipulated in each agreement. The amount of timber we receive under these agreements has varied, and is expected to continue to vary, according to the price and supply of wood fiber for sale on the open market and the harvest levels the timberland owners deem appropriate in the management of the timberlands.

Our Port Hawkesbury, Nova Scotia mill operates a woodlands unit which manages approximately 1,500,000 acres of land licensed from the Province of Nova Scotia and 59,000 acres of land we own in Nova Scotia. All wood harvested from the licensed lands must be used in our Port Hawkesbury mill unless otherwise agreed to by the Province of Nova Scotia. The license is for a 50 year period, renewable every 10 years, and currently expires in July 2051. The license may be terminated by the Province of Nova Scotia if the Port Hawkesbury mill is not operational for a continuous period of two years.

We seek to fulfill substantially all of our wood needs with timber that is harvested by professional loggers trained in certification programs that are designed to promote sustainable forestry. We do not accept wood from old growth forests, forests of exceptional conservation value or rainforests. We do not accept illegally harvested or stolen wood. We have formally notified our outside wood chip suppliers that we expect their wood supply will be produced by trained loggers in compliance with sustainable forestry principles. Our goal is to ensure that sustainable forestry-trained loggers are used to supply essentially all of the wood to our mills. We oppose and, through our participation in the American Forest and Paper Association, World Resources Institute and other organizations, are working to stop illegal logging in the United States and worldwide.

Chemicals used in the production of paper include latex and starch, which are used to affix coatings to paper; calcium carbonate, which brightens paper; titanium, which makes paper opaque; and other chemicals used to bleach or color paper. We purchase these chemicals from various suppliers and are not dependent on a single supplier for any of these chemicals, although some specialty chemicals are available only from a small number of suppliers.

Customers

We have long-standing relationships with many leading publishers, commercial printers, retailers and paper merchants. Our ten largest customers accounted for approximately half of our net sales for 2008. Our key customers include Condé Nast Publications, The McGraw-Hill Companies, Meredith Corporation, News America Group, Pearson Education, Rodale Inc. and Time Inc. in publishing; Quad/Graphics, Quebecor World Inc. and R.R. Donnelley & Sons Company in commercial printing; Sears Holdings Corporation and Williams-Sonoma, Inc. in retailing; and paper merchants Lindenmeyr, a division of Central National-Gottesman Inc., Unisource Worldwide, Inc. and xpedx, a division of International Paper Company. Key customers for specialty paper products include Avery Dennison Corporation and Vacumet Corp.

During 2008, xpedx accounted for 21% of net sales. No other customer accounted for more than 10% of our 2008 net sales.

8

Sales, Marketing and Distribution

We sell our paper products primarily in the United States and Canada, using three sales channels:

| | • | | direct sales, which consist of sales made directly to end-use customers, primarily large companies such as publishers, printers and retailers |

| | • | | merchant sales, which consist of sales made to paper merchants, who in turn sell to end-use customers |

| | • | | specialty sales, which consist of sales made to packaging and label manufacturers |

Across the three channels of our sales network, sales professionals are compensated with a salary and bonus plan based on account profitability and individual assignments. As part of our customer service, we seek to provide value-added services to customers. For example, within the merchant channel, we work closely with customers to meet specifications and to utilize joint marketing efforts when appropriate.

We also emphasize technical support as part of our commitment to customers. We seek to enhance efficiency for customers by enabling them to interact with us online, including through order access, planning, customer data exchange and consumption estimation tools.

The locations of our paper mills and distribution centers also provide certain logistical advantages as a result of their close proximity to several major print markets, including New York, Chicago, Minneapolis and Atlanta, which affords us the ability to more quickly and cost-effectively deliver our products to those markets. We have two major distribution facilities located in Bedford, Pennsylvania and Sauk Village, Illinois. In total, we own two warehouses and lease space in approximately 50 warehouses owned by third parties. Paper merchants also provide warehouse and distribution systems to service the needs of commercial print customers. We use third parties to ship our products by truck and rail. In addition, we utilize integrated tracking systems that track all of our products through the distribution process. Customers can access order tracking information over the internet. Most of our products are delivered directly to printers or converters, regardless of sales channel.

Competition

The North American paper industry is highly competitive. We compete based on a number of factors, including price, product availability, quality, breadth of product offerings, customer service and distribution capabilities. When a coated paper manufacturer announces a price increase, it generally takes effect over time. Whether a price increase is successful depends on supply, demand and other competitive factors in the marketplace.

Our primary competitors for coated paper are AbitibiBowater Inc., Sappi Limited, UPM-Kymmene Corporation and Verso Paper, Inc. Our primary competitors for supercalendered paper are AbitibiBowater Inc., Catalyst Paper Corporation and Irving Paper Ltd. Our primary competitors for newsprint are AbitibiBowater Inc. and Catalyst Paper Corporation.

The competition in the specialty paper category is diverse and highly fragmented, varying by product end use. Our primary competitors for specialty paper products are Appleton Coated LLC, Boise Cascade LLC, Dunn Paper Inc., Fraser Papers Inc., International Paper Company, UPM-Kymmene Corporation and Wausau Paper Corp.

Some of our competitors have greater financial and other resources than we do or may be better positioned than we are to compete for certain opportunities. We also believe that our competitors in China, Indonesia and South Korea have been selling their products in our markets at less than fair value and have been subsidized by their governments.

9

Information Technology Systems

We use integrated information technology systems that help us manage our product pricing, customer order processing, customer billing, raw material purchasing, inventory management, production controls and shipping management, as well as our human resources management and financial management. Our information technology systems utilize principally third-party software. As part of the reorganization plan associated with the Acquisition, we are migrating the acquired mills to our existing ERP system and integrating NPCP’s order management, purchasing, inventory and finance information systems with our existing systems and expect to complete this action during the third quarter of 2009.

Intellectual Property

In general, paper production does not rely on proprietary processes or formulas, except in highly specialized or custom grades. We hold foreign and domestic patents as a result of our research and product development efforts and also have the right to use certain other patents and inventions in connection with our business. We also own registered trademarks for some of our products. Although, in the aggregate, our patents and trademarks are important to our business, financial condition and results of operations, we believe that the loss of any one or any related group of intellectual property rights would not have a material adverse effect on our business, financial condition or results of operations.

Employees

As of December 31, 2008, we had approximately 7,800 employees. Approximately 70% of our employees were represented by labor unions, principally by the United Steelworkers, the International Brotherhood of Electrical Workers, the Communications, Energy and Paperworkers Union of Canada (CEP), the International Association of Machinists and Aerospace Workers and the United Association of Journeymen and Apprentices of the Plumbing and Pipefitting Industry of the United States and Canada.

We have 16 collective bargaining agreements expiring at various times through November 30, 2010. Approximately 925 employees at the Escanaba, Michigan mill are covered under three contracts that expired in June and July of 2008 and are currently under renegotiation. In addition, two contracts covering an aggregate of approximately 750 employees at the Luke, Maryland mill expired December 1, 2008 and January 15, 2009 and are currently under renegotiation. During 2009, one contract for the office workers in central Wisconsin covering approximately 50 employees will expire on April 30, 2009 and three contracts covering an aggregate of approximately 550 employees at our Port Hawkesbury, Nova Scotia, mill will expire on May 31, 2009.

We have not experienced any significant work stoppages or employee-related problems that had a material effect on our operations over the last five years. We consider our employee relations to be good. Our Port Hawkesbury, Nova Scotia, mill was closed from December 2005 until October 2006, before our ownership of the mill, due to a labor dispute.

Environmental and Other Governmental Regulations

Our operations are subject to federal, state, provincial and local environmental laws and regulations in the United States and Canada, such as the Federal Water Pollution Control Act of 1972, the Federal Clean Air Act, the Federal Resource Conservation and Recovery Act, and the Comprehensive Environmental Response, Compensation and Liability Act of 1980, as amended, or CERCLA. Among the activities subject to environmental regulation are the emissions of air pollutants; discharges of wastewater and stormwater;

10

generation, use, storage, treatment and disposal of, or exposure to, materials and waste; remediation of soil, surface water and ground water contamination; and liability for damages to natural resources. In addition, we are required to obtain and maintain environmental permits and approvals in connection with our operations. Many environmental laws and regulations provide for substantial fines or penalties and criminal sanctions for failure to comply with orders and directives requiring that certain measures or actions be taken to address environmental issues.

Certain of these environmental laws, such as CERCLA and analogous state and foreign laws, provide for strict liability, and under certain circumstances joint and several liability, for investigation and remediation of releases of hazardous substances into the environment, including soil and groundwater. These laws may apply to properties presently or formerly owned or operated by or presently or formerly under the charge, management or control of an entity or its predecessors, as well as to conditions at properties at which wastes attributable to an entity or its predecessors were disposed. Under these environmental laws, a current or previous owner or operator of real property or a party formerly or previously in charge, management or control of real property, and parties that generate or transport hazardous substances that are disposed of at real property, may be held liable for the cost to investigate or clean up that real property and for related damages to natural resources.

We handle and dispose of wastes arising from our mill operations, including by the operation of a number of landfills. We may be subject to liability, including liability for investigation and cleanup costs, if contamination is discovered at one of these mills, landfills, or at another location where we have disposed of, or arranged for the disposal of, waste. While we believe, based upon current information, that we are in substantial compliance with applicable environmental laws and regulations, we could be subject to potentially significant fines or penalties for failing to comply with environmental laws and regulations. MeadWestvaco and SEO have separately agreed to indemnify us for certain environmental liabilities related to the properties acquired from them, subject to certain limitations. We agreed to indemnify the purchaser of our carbonless paper business for certain environmental liabilities, subject to certain limitations.

Compliance with environmental laws and regulations is a significant factor in our business. We incurred capital expenditures of $1 million in 2008 in order to maintain compliance with applicable environmental laws and regulations and to meet new regulatory requirements. We do not expect to incur any environmental capital expenditures in 2009. Environmental compliance may require significant capital or operating expenditures over time as environmental laws or regulations, or interpretation thereof, change or the nature of our operations require us to make significant additional expenditures.

Our operations also are subject to a variety of worker safety laws in the United States and Canada. The Occupational Safety and Health Act, U.S. Department of Labor Occupational Safety and Health Administration regulations and analogous state and provincial laws and regulations mandate general requirements for safe workplaces for all employees. We believe that we are operating in material compliance with applicable employee health and safety laws.

Available Information

Our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to those reports are available without charge on our website, www.newpagecorp.com, as soon as is reasonably practicable after they are filed electronically with the SEC. We will also provide a free copy of any of our filed documents upon written request to: General Counsel, NewPage Corporation, 8540 Gander Creek Drive, Miamisburg, Ohio 45342.

11

The public may read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street NE, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC (http://www.sec.gov).

The risks discussed below, any of which could materially affect our business, financial condition or results of operations, are not the only risks facing us. Additional risks and uncertainties not currently known to us or that we currently deem to be immaterial may also materially and adversely affect our business, financial condition or results of operations.

Our substantial level of indebtedness could adversely affect our business, financial condition or results of operations.

We have substantial indebtedness. As of December 31, 2008, we had $3,152 million of total indebtedness (excluding $87 million in outstanding letters of credit). Total indebtedness for NewPage was $2,962 million at December 31, 2008. As of December 31, 2008, our revolving senior secured credit facility also permitted additional borrowings of up to a maximum of $500 million. In addition, subject to restrictions in our debt instruments, we may incur additional indebtedness. If new debt is added to our and our subsidiaries’ current debt levels, the related risks that we now face could intensify.

Our substantial indebtedness could have important consequences, including the following:

| | • | | it may be difficult for us to satisfy our obligations with respect to our outstanding indebtedness |

| | • | | our ability to obtain additional financing for working capital, debt service requirements, general corporate or other purposes may be impaired |

| | • | | we must use a substantial portion of our cash flow to pay interest and principal on our indebtedness, which reduces the funds available to us for other purposes |

| | • | | we are more vulnerable to economic downturns and adverse industry conditions |

| | • | | our ability to capitalize on business opportunities and to react to competitive pressures and changes in our industry as compared to our competitors may be compromised due to our high level of indebtedness |

| | • | | our ability to refinance our indebtedness may be limited |

In addition, we cannot assure you that we will be able to refinance any of our debt or that we will be able to refinance on commercially reasonable terms. If we were unable to make payments or refinance our debt or obtain new financing under these circumstances, we would have to consider other options, such as:

| | • | | negotiations with our lenders to restructure the applicable debt |

| | • | | cash equity contributions from our controlling equity owner or others |

Our debt instruments may restrict, or market or business conditions may limit, our ability to use some of our options.

12

A substantial portion of our debt bears interest at variable rates. If market interest rates increase, it could materially increase our cash interest payments.

As of December 31, 2008, $1,999 million of our debt consisted of borrowings that bear interest at variable rates, representing 63% of our total indebtedness. Variable-rate indebtedness at NewPage was $1,809 million at December 31, 2008, representing 61% of its total indebtedness. If market interest rates increase, variable-rate debt will create higher debt service requirements, which could adversely affect our cash flow and compliance with our debt covenants. As of December 31, 2008, weighted average interest rates were 5.3% on borrowings under the NewPage senior secured term loan due 2014, 9.4% on the NewPage floating rate senior secured notes due 2012 and 10.3% on the NewPage Holding floating rate senior unsecured PIK Notes due 2013 (the “NewPage Holding PIK Notes”). Each one-eighth percentage-point change in LIBOR would result in a $2.0 million change in annual interest expense on the NewPage senior secured term loan, a $0.3 million change in annual interest expense on the NewPage floating rate notes, a $0.2 million change in annual interest expense on the NewPage Holding PIK Notes, and, assuming the entire revolving credit facility were drawn, a $0.6 million change in interest expense on the revolving credit facility, in each case, without taking into account any interest rate derivative agreements. While we may enter into agreements limiting our exposure to higher market interest rates, these agreements may not offer complete protection from this risk.

Servicing our indebtedness will require a significant amount of cash. Our ability to generate sufficient cash depends on numerous factors beyond our control, and we may be unable to generate sufficient cash flow to service our debt obligations.

Our ability to make payments on and to refinance our indebtedness will depend on our ability to generate cash in the future. This, to a certain extent, is subject to general economic, political, financial, competitive, legislative, regulatory and other factors that are beyond our control.

During 2008, we expended approximately $267 million to service our indebtedness as compared to approximately $202 million during 2007 (without giving effect to the repayment of $450 million under our pre-Acquisition credit facility at the closing of the Acquisition). We cannot assure you that our business will generate sufficient cash flow from operations, or that future borrowings will be available to us under our senior secured credit facilities, in an amount sufficient to enable us to pay our indebtedness or to fund our other liquidity needs. If our cash flows and capital resources are insufficient to allow us to make scheduled payments on our indebtedness, we may need to reduce or delay capital expenditures, sell assets, seek additional capital or restructure or refinance all or a portion of our indebtedness on or before maturity. We cannot assure you that we will be able to refinance any of our indebtedness, or that we will be able to refinance on commercially reasonable terms. If we are unable to generate sufficient cash flow or refinance our debt on favorable terms it could have a material adverse effect on our financial condition, the value of the outstanding debt and our ability to make any required cash payments under our indebtedness.

Our senior secured credit facilities are secured by substantially all of our assets and our notes rank junior in right of payment to indebtedness under our senior secured credit facilities to the extent of the collateral securing the senior secured credit facilities.

NewPage Holding and most of the subsidiaries of NewPage are guarantors of NewPage’s senior secured credit facilities. The guarantees are secured by collateral comprising substantially all of our assets. Holders of secured debt have claims that are prior to those of other debt holders up to the value of the assets. On December 31, 2008, there was $1,584 million of senior secured indebtedness outstanding under the senior secured credit facilities (excluding $87 million in outstanding letters of credit). The senior secured credit facilities permit additional borrowings of up to a maximum of $500 million under the revolving portion of the facility. If our secured creditors, including lenders under our senior secured credit facilities, exercise their rights with respect to their collateral, the secured creditors would be entitled to be repaid in full from the proceeds of those assets before those proceeds would

13

be available for distribution to other creditors. If our assets are distributed or paid in a foreclosure, dissolution, winding-up, liquidation, reorganization or other bankruptcy proceeding, holders of secured debt will have prior claim to our assets that constitute their collateral. If any of the foregoing events occur, we cannot assure you that there will be sufficient assets to pay amounts due on more junior borrowings.

All operations are conducted through NewPage and its subsidiaries, none of which have guaranteed the NewPage Holding PIK Notes.

All of our operations are conducted through NewPage and its subsidiaries. The NewPage Holding PIK Notes are not guaranteed by NewPage or any of its subsidiaries, and are effectively subordinated to all of our subsidiaries’ current and future indebtedness, including our borrowings under NewPage’s senior secured credit facilities and its other indebtedness. As a result, in the event of the bankruptcy, liquidation or dissolution of NewPage or any subsidiary, the assets of the applicable subsidiary would be available to pay obligations under the NewPage Holding PIK Notes only after all payments had been made on the indebtedness of the applicable subsidiary. Sufficient assets may not remain after all of these payments have been made to make any payments on the NewPage Holding PIK Notes and our other obligations. On December 31, 2008, the $190 million of NewPage Holding PIK Notes were effectively subordinated to $2,962 million of indebtedness of NewPage and its subsidiaries (excluding $87 million in outstanding letters of credit), and up to a maximum of $500 million of additional availability under NewPage’s revolving senior secured credit facility. NewPage and its subsidiaries are permitted to incur substantial additional indebtedness in the future under the terms of the indentures governing our existing indebtedness.

Our debt instruments impose significant operating and financial restrictions on us.

The indentures and other agreements governing our notes and our debt instruments impose significant operating and financial restrictions on us. These restrictions limit our ability to, among other things:

| | • | | incur additional indebtedness or guarantee obligations |

| | • | | repay indebtedness prior to stated maturities |

| | • | | pay dividends or make certain other restricted payments |

| | • | | make investments or acquisitions |

| | • | | create liens or other encumbrances |

| | • | | transfer or sell certain assets or merge or consolidate with another entity |

| | • | | engage in transactions with affiliates |

| | • | | engage in certain business activities |

In addition to the covenants listed above, our senior secured credit facilities require us to meet specified financial ratios and tests and restrict our ability to make capital expenditures. The required financial covenant levels become more restrictive over the term of the senior secured credit facilities. By December 31, 2009, the leverage ratio declines to 5.00 with further decreases over the following three years to 3.75, the senior leverage ratio declines to 2.50 with further decreases over the following three years to 1.25, the interest coverage ratio increases to 2.00 with a further increase to 2.50 the following year and the fixed charge coverage ratio increases to 1.10. Certain items included in results of operations are excluded under the definition of “consolidated adjusted EBITDA” used to calculate compliance with the financial covenants in our senior secured credit facilities. These include items such as equity award expense, the effect of LIFO inventory accounting, non-cash pension expense, cost of restructuring activities and costs related to the integration of the two businesses, among other items. Any of these restrictions could limit our ability to plan for or react to market conditions or meet extraordinary capital needs and could otherwise restrict corporate activities.

Our ability to comply with these covenants may be affected by events beyond our control, and an adverse development affecting our business could require us to seek waivers or amendments of covenants, alternative or additional sources of financing or reductions in expenditures. We cannot assure you that these waivers, amendments or alternative or additional financings could be obtained, or if obtained, would be on terms acceptable to us.

14

A breach of any of the covenants or restrictions contained in any of our existing or future financing agreements, including our inability to comply with the required financial covenants in our senior secured credit facilities, could result in an event of default under those agreements. Our default could allow the lenders under our financing agreements, if the agreements so provide, to discontinue lending, to accelerate the related debt as well as any other debt to which a cross acceleration or cross default provision applies, and to declare all borrowings outstanding under our financing arrangements to be due and payable. In addition, the lenders could terminate any commitments they had made to supply us with further funds. If the lenders require immediate repayments, we will not be able to repay them, or the other holders of our debt, in full.

We may not have the ability to raise the funds necessary to finance the change of control offers required by the indentures governing our indebtedness.

Upon the occurrence of a change of control, we must offer to buy back certain indebtedness at a price greater than par, together with any accrued and unpaid interest to the date of the repurchase. Our failure to purchase, or give notice of purchase of, this indebtedness would be a default under the indentures governing the applicable indebtedness, which would also be a default under our senior secured credit facilities.

If a change of control occurs, it is possible that we may not have sufficient assets at the time of the change of control to make the required repurchase of indebtedness or to satisfy all obligations under our senior secured credit facilities and the indentures governing our indebtedness. In order to satisfy our obligations, we could seek to refinance the indebtedness under our senior secured credit facilities and the indentures governing the indebtedness or obtain a waiver from the lenders or holders of the indebtedness. We cannot assure you that we would be able to obtain a waiver or refinance our indebtedness on terms acceptable to us, if at all.

Our controlling equity holder may take actions that conflict with interests of the debtholders.

A substantial portion of the voting power of our equity is held indirectly by affiliates of Cerberus. Accordingly, Cerberus indirectly controls the power to elect our directors and officers, to appoint new management and to approve all actions requiring the approval of the holders of our equity (subject to certain specified consent rights of SEO under the security holders agreement between NewPage Group and SEO), including adopting amendments to our constituent documents and approving mergers, acquisitions or sales of all or substantially all of our assets. The directors have the authority, subject to the terms of our debt, to issue additional indebtedness or equity, implement equity repurchase programs, declare dividends and make other such decisions about our equity.

In addition, the interests of our controlling equity holder could conflict with those of our debtholders if, for example, we encounter financial difficulties or are unable to pay our debts as they mature. Our controlling equity holder also may have an interest in pursuing acquisitions, divestitures, financings or other transactions that, in its judgment, could enhance its equity investment, even though these transactions might involve risks to our debtholders.

Demand for coated paper has declined due to recent macroeconomic events. Further declines in demand could have a material adverse effect on our business, financial condition and results of operations.

Deteriorating general economic conditions have had an adverse effect on the demand for our products since the second half of 2008. North American coated paper demand is primarily driven by advertising and print media usage. In particular, the demand for certain grades of coated paper is affected by spending on catalog and promotional materials by retailers and spending on magazine advertising, which affects the number of printed pages in magazines. Since the second half of 2008, advertising and print media usage has declined. Coated paper prices increased during the first three quarters of 2008. However, sales prices began to decline during the fourth quarter of 2008 as a result of lower demand in the current economic environment. Given the slowdown in the global economic outlook and the decline in demand for coated paper exceeding the decline in supply, we expect this trend could continue through 2009. Further declines in the general economic environment could have a material adverse effect on our business, financial condition and results of operations.

We have limited ability to pass through increases in our costs. Increases in our costs or decreases in our paper prices could adversely affect our business, financial condition and results of operations.

Our earnings are sensitive to changes in the prices of our paper products. Fluctuations in paper prices, and coated paper prices in particular, historically have had a direct effect on our net income (loss) and EBITDA for several reasons:

| | • | | Market prices for paper products are a function of supply and demand, factors over which we have limited influence. We therefore have limited ability to control the pricing of our products. Market prices of grade No. 3 coated paper, 60 lb. weight, which is an industry benchmark for coated freesheet paper pricing, have fluctuated since 2000 from a high of $1,100 per ton to a low of $705 per ton. Market prices of grade No. 4 coated paper, 50 lb. weight, which is an industry benchmark for coated groundwood paper pricing, and grade SC-A, 35 lb. weight, which is an industry benchmark for supercalendered paper pricing, have generally followed similar trends. Because market conditions determine the price for our paper products, the price for our products could fall below our production costs. |

15

| | • | | Market prices for paper products typically are not directly affected by raw material costs or other costs of sales, and consequently we have limited ability to pass through increases in our costs to our customers absent increases in the market price. Thus, even though our costs may increase, our customers may not accept price increases for our products, or the prices for our products may decline. |

| | • | | Paper manufacturing is highly capital-intensive and a large portion of our and our competitors’ operating costs are fixed. Additionally, paper machines are large, complex systems that operate more efficiently when operated continuously. Consequently, both we and our competitors typically continue to run our machines whenever marginal sales exceed the marginal costs. |

Our ability to achieve acceptable margins is, therefore, principally dependent on managing our cost structure and managing changes in raw materials prices, which represent a large component of our operating costs and fluctuate based upon factors beyond our control. If the prices of our products decline, or if our raw material costs increase, or both, it could have a material adverse effect on our business, financial condition and results of operations. For a further discussion of the variability of our paper prices and our costs and expenses, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Selected Factors That Affect Our Operating Results.”

Most of the raw material, labor and other cost of sales at our Port Hawkesbury, Nova Scotia, mill are denominated in Canadian dollars. North American sales prices for the products produced at Port Hawkesbury are determined primarily by the U.S. dollar price per ton charged by U.S. producers. In 2008, a stronger U.S. dollar helped profitability at our Port Hawkesbury mill compared to 2007. If the U.S. dollar were to weaken significantly against the Canadian dollar, it would impair the ability of the Port Hawkesbury mill to profitably compete.

The markets in which we operate are highly competitive and imports could materially adversely affect our business, financial condition and results of operations.

Our business is highly competitive. Competition is based largely on price. We compete with numerous North American paper manufacturers. We also face competition from foreign producers, some of which we believe are lower cost producers than we are. Foreign overcapacity could result in an increase in the supply of paper products available in the North American market. Asian producers, in particular, have significantly increased imports to the U.S. in recent years, and we believe that producers in China, Indonesia and South Korea have been selling in our markets at less than fair value and have been subsidized by their governments.

Our non-U.S. competitors may develop a competitive advantage over us and other U.S. producers if the U.S. dollar strengthens in comparison to the home currency of those competitors, if the home currency of those competitors (particularly in China) is maintained by their governments at a low value compared to the U.S. dollar, if those competitors receive governmental subsidies or incentives or if ocean shipping rates decrease. If the U.S. dollar strengthens, if foreign currencies are maintained at low values, if

16

shipping rates decrease, if foreign producers receive governmental subsidies or incentives or if overseas supply exceeds demand, imports may increase, which, in turn, would cause the supply of paper products available in the North American market to increase. An increased supply of paper could cause us to lower our prices or lose sales to competitors, either of which could have a material adverse effect on our business, financial condition and results of operations.

In addition, the following factors will affect our ability to compete:

| | • | | the quality of our products |

| | • | | our breadth of product offerings |

| | • | | our ability to maintain plant efficiencies and high operating rates and thus lower our average manufacturing costs per ton |

| | • | | our ability to provide customer service that meets customer requirements and our ability to distribute our products on time |

| | • | | costs to comply with environmental laws and regulations |

| | • | | our ability to produce products that meet customer requirements for the use of sustainable forestry principles, recycled content and environmentally friendly energy sources |

| | • | | the availability or cost of chemicals, wood, energy and other raw materials and labor |

Furthermore, some of our competitors have greater financial and other resources than we do or may be better positioned than we are to compete for certain opportunities.

If we are unable to obtain raw materials, including petroleum-based chemicals, at favorable prices, or at all, it could adversely affect our business, financial condition and results of operations.

We have no significant timber holdings and purchase wood, chemicals and other raw materials from third parties. We may experience shortages of raw materials or be forced to seek alternative sources of supply. If we are forced to seek alternative sources of supply, we may not be able to do so on terms as favorable as our current terms or at all. The prices for many chemicals, especially petroleum-based chemicals, have increased over the last few years, including substantial increases during 2008. Chemical prices have historically been and are expected to continue to be volatile. In addition, chemical suppliers that use petroleum-based products in the manufacture of their chemicals may, due to a supply shortage, ration the amount of chemicals available to us or we may not be able to obtain the chemicals we need at favorable prices, if at all. Chemical suppliers also may be adversely affected by, among other things, hurricanes and other natural disasters. Certain specialty chemicals that we purchase are available only from a small number of suppliers. We may experience additional cost pressures if merger and acquisition activity occurs among our major chemical suppliers. If any of our major chemical suppliers were to cease operations or cease doing business with us, we may be unable to obtain these chemicals at favorable prices, if at all.

In addition, wood prices are dictated largely by demand. The primary source for wood fiber is timber. Environmental litigation and regulatory developments have caused, and may cause in the future, significant reductions in the amount of timber available for commercial harvest in Canada and the United States. In addition, future domestic or foreign legislation, litigation advanced by aboriginal groups, litigation concerning the use of timberlands, the protection of threatened or endangered species, the promotion of forest biodiversity and the response to and prevention of catastrophic wildfires and campaigns or other measures by environmental activists could also affect timber supplies. Availability of harvested timber may further be limited by factors such as fire and fire

17

prevention, insect infestation, disease, ice and wind storms, drought, floods and other natural and man-made causes, thereby reducing supply and increasing prices. We buy wood chips from lumber producers as a by product of their lumber production. Declines in their business conditions could affect the availability and price of wood chips.

Any disruption in the supply of chemicals, wood or other inputs could affect our ability to meet customer demand in a timely manner and could harm our reputation. As we have limited ability to pass through increases in our costs to our customers absent increases in market prices for our products, material increases in the cost of our raw materials could have a material adverse effect on our business, financial condition and results of operations.

We are involved in continuous manufacturing processes with a high degree of fixed costs. Any interruption in the operations of our manufacturing facilities may affect our operating performance.

We seek to run our paper machines and pulp mills on a nearly continuous basis for maximum efficiency. Any unplanned plant downtime at any of our paper mills results in unabsorbed fixed costs that negatively affect our results of operations. Due to the extreme operating conditions inherent in some of our manufacturing processes, we may incur unplanned business interruptions from time to time and, as a result, we may not generate sufficient cash flow to satisfy our operational needs. In addition, many of the geographic areas where our production is located and where we conduct our business may be affected by natural disasters, including snow storms, tornadoes, forest fires and flooding. These natural disasters could disrupt the operation of our mills, which could have a material adverse effect on our business, financial condition and results of operations. Furthermore, during periods of weak demand for paper products or periods of rising costs, we may need to schedule market-related downtime, which could have a material adverse effect on our financial condition and results of operations. We took 91,000 tons of market-related downtime of coated paper during 2008 and have announced that we intend to take an additional 150,000 tons of market-related downtime of coated paper in the first quarter of 2009.

Our operations require substantial ongoing capital expenditures, and we may not have adequate capital resources to fund all of our required capital expenditures.

Our business is capital intensive, and we incur capital expenditures on an ongoing basis to maintain our equipment and comply with environmental laws and regulations, as well as to enhance the efficiency of our operations. We expect to spend approximately $75 million in 2009 on capital expenditures, including approximately $13 million for maintenance capital expenditures, approximately $55 million for improvements in machinery and equipment efficiency or cost-effectiveness and approximately $7 million primarily for costs of integrating the two businesses, including investments in information systems. We anticipate that cash generated from operations will be sufficient to fund our operating needs and capital expenditures for the foreseeable future. However, if we require additional funds to fund our capital expenditures, we may not be able to obtain them on favorable terms, or at all. If we cannot maintain or upgrade our facilities and equipment as we require or to ensure environmental compliance, it could have a material adverse effect on our business, financial condition and results of operations.

Rising energy or chemical prices or supply shortages could adversely affect our business, financial condition and results of operations.

Although a significant portion of our energy requirements is satisfied by steam produced as a byproduct of our manufacturing process, we purchase natural gas, coal and electricity to run our mills. Energy costs continued to increase during much of 2008 and are expected to remain volatile for the foreseeable future. In addition, energy suppliers and chemical suppliers that use petroleum-based products in the manufacture of their chemicals may, due to supply shortages, ration the amount of energy or chemicals

18

available to us and we may not be able to obtain the energy or chemicals we need to operate our business at acceptable prices or at all. Any significant energy or chemical shortage or significant increase in our energy or chemical costs in circumstances where we cannot raise the price of our products due to market conditions could have a material adverse effect on our business, financial condition and results of operations. We estimate that for each $1 increase in the cost of a barrel of crude oil, our direct energy costs, other than electricity, and indirect costs, such as costs for transportation and petroleum-derived chemicals, increase approximately $6 million annually. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Selected Factors That Affect Our Operating Results—Cost of Sales.” Furthermore, we are required to post letters of credit or other financial assurance obligations with certain of our energy and other suppliers, which could limit our financial flexibility. Additionally, we have experienced some fuel surcharges (primarily diesel fuel) by suppliers, distributors and freight carriers. If fuel surcharges increase significantly, and we are not able to pass these costs through to our customers, they could have a material adverse effect on our business, financial condition and results of operations.

In addition, an outbreak or escalation of hostilities between the United States and any foreign power and, in particular, events in the Middle East, or weather events such as hurricanes, could result in a real or perceived shortage of oil or natural gas, which could result in an increase in energy or chemical prices.

We depend on a small number of customers for a significant portion of our business.

Our largest customer, xpedx, a division of International Paper Company, accounted for 21% of 2008 net sales. Our ten largest customers (including xpedx) accounted for approximately 50% of 2008 net sales. The loss of, or significant reduction in orders from, any of these customers or other customers could have a material adverse effect on our business, financial condition and results of operations, as could significant customer disputes regarding shipments, price, quality or other matters.

Furthermore, we extend trade credit to certain of our customers to facilitate the purchase of our products and rely on their creditworthiness and ability to obtain credit from lenders. Accordingly, a bankruptcy or a significant deterioration in the financial condition of any of our significant customers could have a material adverse effect on our business, financial condition and results of operations, due to a reduction in purchases, a longer collection cycle or an inability to collect accounts receivable.

19

We may not realize the anticipated benefits of the Acquisition.

We completed the Acquisition on December 21, 2007. Although we expect to realize strategic, operational and financial benefits as a result of the Acquisition, we cannot predict whether and to what extent these benefits will be achieved. Successful integration of NewPage and NPCP will depend on management’s ability to manage the combined operations effectively and to benefit from cost savings and operating efficiencies. There are significant challenges to integrating the NPCP operations into our business, including:

| | • | | potential disruptions of our business caused by the integration activities |

| | • | | the diversion of management’s and other’s attention |

| | • | | maintaining effective internal control procedures for the combined company |

| | • | | integrating management information, inventory, accounting and sales systems of NewPage and NPCP |

| | • | | sufficient customer demand necessary to support volume levels needed to achieve anticipated economies of scale |

In addition, the Acquisition created a significantly larger combined company, which may increase the challenge of integrating the NPCP operations into our business.

We expect to generate annualized synergies as a result of the Acquisition of approximately $265 million. As of December 31, 2008, we remain on track to meet our long-term target in annualized synergies from the Acquisition. However, full realization of the synergies from anticipated economies of scale may be delayed somewhat by the slowdown in demand and volume. We cannot assure you that these synergies will be achieved on the timetable contemplated and in the amounts expected, or at all. Achieving the expected synergies, as well as the costs of achieving them, is subject to a number of uncertainties, including customer demand necessary to support volume levels needed to achieve anticipated economies of scale and our ability to make necessary investments in information systems in a timely and cost efficient manner. If we encounter difficulties in achieving the expected synergies, incur significantly greater costs related to these synergies than we anticipate or activities related to these synergies have unintended consequences, our business, financial condition and results of operations could be adversely affected.

Litigation could be costly and harmful to our business.

We are involved in various claims and lawsuits from time to time. For example, in 1998 and 1999, the Environmental Protection Agency, or EPA, issued Notices of Violation, or NOV, to eight paper industry facilities, including our Luke, Maryland mill, alleging violation of certain Prevention of Significant Deterioration, or PSD, regulations under the Clean Air Act. In 2000, an enforcement action was brought in Federal District Court in Maryland against the predecessor of MeadWestvaco, asserting that the predecessor did not obtain PSD permits or install required pollution controls in connection with capital projects carried out in the 1980s at the Luke mill. The complaint sought penalties of $27,500 per day for each claimed violation together with the installation of additional air pollution control equipment. MeadWestvaco has agreed to indemnify us for certain liability under these claims to the extent reserves were not previously established or the liability exceeds amounts budgeted by MeadWestvaco in connection with these matters. However, if we incur liability for this lawsuit and we are unable to obtain indemnification from MeadWestvaco, we may incur substantial costs, which may include costs in connection with the penalties and the installation of additional pollution control equipment.

In March 2000, the EPA issued a NOV and a Finding of Violation, or FOV, to our Wisconsin Rapids pulp mill alleging violation of the PSD regulations and the New Source Performance Standard, or NSPS, requirements under the Clean Air Act arising from projects implemented at the mill between 1983 and 1991. The EPA is seeking the installation of additional air pollution control

20

equipment and an $8 million penalty. The matter has been referred to the Department of Justice. In July 2002, the EPA issued a NOV and a FOV to our Niagara mill alleging PSD and NSPS violations relating to projects implemented at the mill from 1995 to 1997. SEO has agreed to indemnify us for 75% of certain expenses relating to these matters, including losses arising from the design and installation of air pollution control equipment and for 75% of air compliance penalties, provided the expenses and penalties are incurred within a five-year period following closing of the Acquisition and that SEO’s obligations with respect to the boiler Maximum Achievable Control Technology rule is limited to 50% of the initial $35 million of certain compliance costs. If we incur liability for these actions and we are unable to obtain indemnification from SEO, we may incur substantial costs in connection with penalties and the installation of additional pollution control equipment.

In April 2008, NewPage Wisconsin System Inc. (formerly Stora Enso North America Corp. and the successor by merger to Consolidated Papers, Inc.), along with several other defendants, was served with a summons and complaint seeking to allocate among the defendants the cleanup costs and natural resource damages associated with the remediation of PCB contamination in the Lower Fox River and to require the defendants and the other responsible parties to pay for the upcoming remedial work and natural resource damages. The complaint does not specify our alleged allocable share of these costs and damages. We do not believe that we are responsible for any PCB contamination in the Lower Fox River. We have submitted the claim to SEO, which is required to defend and indemnify us for 75% of any environmental liability associated with the Lower Fox River, provided the liabilities are incurred within the five-year period following closing of the Acquisition. We cannot assure you that we will not be held responsible for PCB contamination in the Lower Fox River or that SEO will satisfy any indemnification obligation to us.