UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K

(Mark One)

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2006

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission file number: 000-51406

FEDERAL HOME LOAN BANK OF SEATTLE

(Exact Name of Registrant as Specified in Its Charter)

| | |

| Federally chartered corporation | | 91-0852005 |

| (State or Other Jurisdiction of Incorporation or Organization) | | (I.R.S. Employer Identification No.) |

| |

| 1501 Fourth Avenue, Suite 1800, Seattle, WA | | 98101-1693 |

| (Address of Principal Executive Offices) | | (Zip Code) |

Registrant’s telephone number, including area code: (206) 340-2300

Securities registered pursuant to Section 12(b) of the Act: None

Title of Each Class: None

| | |

Securities registered pursuant to Section 12(g) of the Act: | | Name of Each Exchange on Which Registered: |

Class B Common Stock, $100 par value per share (Title of class) | | N/A |

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large Accelerated Filer ¨ Accelerated Filer ¨ Non-accelerated Filer x

Indicate by Check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act.) Yes ¨ No x

Registrant’s stock is not publicly traded and is only issued to members of the registrant. Such stock is issued and redeemed at par value, $100 per share, subject to certain regulatory and statutory limits. As of June 30, 2006, the aggregate par value of the shares of capital stock of the registrant was $2,210,219,000. As of February 28, 2007, Seattle Bank had outstanding 3,650 shares of its Class A stock and 22,105,793 shares of its Class B stock.

FEDERAL HOME LOAN BANK OF SEATTLE

Form 10-K for the Fiscal Year Ended December 31, 2006

i

Forward-looking Statements

This report contains forward-looking statements that are subject to risk and uncertainty. These statements describe the expectations of the Federal Home Loan Bank of Seattle, or the Seattle Bank, regarding future events and developments, including future operating results, growth in assets, and continued success of our products. These statements include, without limitation, statements as to future expectations, beliefs, plans, strategies, objectives, events, conditions, and financial performance. The words “will,” “believe,” “expect,” “intend,” “may,” “could,” “should,” “anticipate,” and words of similar nature are intended in part to help identify forward-looking statements.

Future results, events, and developments are difficult to predict, and the expectations described in this report, including any forward-looking statements, are subject to risk and uncertainty that may cause actual results to differ materially from those we currently anticipate. Consequently, there is no assurance that the expected events and developments will occur. See “Part I. Item 1A. Risk Factors,” for additional information on risks and uncertainties.

Factors that may cause actual results, events, and developments to differ materially from those discussed in this report include, among others, the following:

| | • | | a significant change in interest rates; |

| | • | | withdrawal of one or more large members or consolidation among our members; |

| | • | | competition from other alternative sources of funding available to our members, including other Federal Home Loan Banks, or FHLBanks; |

| | • | | adverse changes in the market prices of our financial instruments, or our failure to effectively hedge these instruments; |

| | • | | changes in investor demand for consolidated obligations or changes in our ability to participate in the issuance of consolidated obligations; |

| | • | | effects of the recent amendments to our capital plan, as amended, which we refer to as our Capital Plan, including amendments regarding the creation of an excess stock pool and authorization of Class A stock to support new advances; |

| | • | | our members’ willingness to do business with us despite limitations on our payment of dividends and continuing restrictions on repurchases of excess Class B stock; |

| | • | | failure to satisfy hedge accounting criteria under the accounting principles generally accepted in the United States, or U.S. GAAP, in hedging our interest-rate risk; |

| | • | | legislative or regulatory changes or actions initiated by the Federal Housing Finance Board, or the Finance Board, or other body, that could cause us to modify our current structure, policies, or business operations; |

| | • | | changes in accounting rules or in the interpretation of existing accounting rules; |

| | • | | negative changes in our credit agency ratings or ratings applicable to the FHLBanks, the Finance Board, and the Office of Finance, or collectively the FHLBank System; |

| | • | | the need to make principal or interest payments on behalf of another FHLBank as a result of the joint and several liability of all FHLBanks for consolidated obligations; |

| | • | | adverse changes in local and national economic conditions; and |

| | • | | events such as terrorism, natural disasters, or other catastrophic events that could disrupt the financial markets where we obtain funding, our borrowers’ ability to repay advances, or the value of the collateral that we hold. |

1

These cautionary statements apply to all related forward-looking statements, wherever they appear in this report. We do not undertake to update any forward-looking statements that we make in this report or that we may make from time to time.

PART I.

ITEM 1. BUSINESS

Overview

The Seattle Bank, a federally chartered corporation organized in 1964, is a member-owned cooperative. Our mission is to provide liquidity, funding, and services to enhance our members’ success and the availability of affordable homes and economic development in their communities. Our core business is traditional member finance, which includes making advances, providing letters of credit, accepting deposits, and providing securities safekeeping and other services. Historically, we offered products and services through two operating segments, traditional member finance and the Mortgage Purchase Program, or MPP. The MPP segment included mortgage loans held for portfolio as a result of purchases from participating members. During the first quarter of 2005, we decided to exit the MPP.

We conduct most of our business with or through our members, and we do not conduct our business directly with the general public. For the year ended December 31, 2006, we reported net income of $25.8 million, and as of December 31, 2006, we had total assets of $53.5 billion, total deposits of $1.0 billion, and retained earnings of $92.4 million.

We also work with our members and a variety of other entities, including non-profit organizations, to provide affordable housing and community economic development funds through direct subsidy grants and low- or no-interest loans, for individuals and communities in need. We fund these grants and loans through the Affordable Housing Program, or AHP, and a number of other community investment programs.

The Seattle Bank is one of 12 FHLBanks that, along with the Finance Board and the Office of Finance, comprise the FHLBank System. The FHLBank System was created by Congress under the authority of the Federal Home Loan Bank Act of 1932, as amended, or the FHLBank Act, to ensure the availability of housing funds to expand home ownership throughout the nation. The 12 FHLBanks are government-sponsored enterprises, or GSEs, of the United States of America. Each FHLBank is a separate entity with its own board of directors, management, and employees. The 12 FHLBanks are located throughout the United States, with each FHLBank responsible for a particular district. The Seattle Bank is responsible for the Twelfth District, which includes the states of Alaska, Hawaii, Idaho, Montana, Oregon, Utah, Washington, and Wyoming, as well as the U.S. territories of American Samoa, Guam, and the Northern Mariana Islands.

The primary sources of funding for all of the FHLBanks consist of consolidated obligation bonds and discount notes, which are referred to collectively as consolidated obligations. The Office of Finance, a joint office of the FHLBanks created by the Finance Board, acts as an authorized agent of the FHLBanks, facilitating and executing the issuance of consolidated obligations on behalf of the FHLBanks. The U.S. government does not guarantee, directly or indirectly, the consolidated obligations or other obligations of any of the FHLBanks. Consolidated obligations are the joint and several obligations of the 12 FHLBanks. As of December 31, 2006, the aggregate par value of consolidated obligations outstanding for the FHLBank System was $952.0 billion; however, individual banks are primarily liable for an allocated portion of the consolidated obligations in which they participate. As of December 31, 2006, the Seattle Bank was the primary obligor on $49.7 billion par value of consolidated obligations.

In 2006, the Seattle Bank’s annual net income increased to $25.8 million, reversing a trend of declining net income that occurred from 2001 through 2005. Due to actions we initiated at the end of 2004, and which were substantially implemented during 2005 and 2006, we have now refocused our business on providing advances to our members and no longer purchase mortgage loans through the MPP. In changing the direction of our business,

2

we reviewed and improved our operations and reduced our expenses substantially. As a result of these factors, and assuming the interest-rate environment remains substantially unchanged, we anticipate continued improvement in net income. See “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview.”

As of December 31, 2006, 2005, and 2004, we had net unrealized market value losses of $245.0 million, $363.1 million, and $257.3 million, which are not reflected in our December 31, 2006, 2005, or 2004 Statements of Condition and which are likely to depress our net income over future periods. Because of these net unrealized market value losses, the ratio of the market value of our equity to the book value of our equity was 89.0%, 83.5%, and 87.8% as of December 31, 2006, 2005, and 2004. We measure the market value of our equity as the present value of the expected net cash flows from all our existing assets, liabilities, and commitments. The amount of our net unrealized market value losses involves estimates of the market values of our assets, liabilities, and commitments, which we discuss in greater depth in Note 17 in “Part II. Item 8. Financial Statements and Supplementary Data—Audited Financial Statements—Notes to Financial Statements.”

As a result of our 2004 Finance Board examination, we entered into an agreement with the Finance Board in December 2004, which we refer to as the Written Agreement. The Written Agreement required us to develop a three-year business and capital management plan and submit it to the Finance Board’s Office of Supervision, and imposed certain other requirements and limitations. In May 2005, the Finance Board accepted our three-year business and capital management plan, subject to our adoption of certain dividend and stock repurchase restrictions. On January 11, 2007, due to, among other things, our successful progress on the implementation of our business plan, the Finance Board terminated the Written Agreement. We refer to the three-year business and capital management plan, as updated from time to time, as the business plan.

To implement the business plan, we undertook significant changes to our business, operations, and capital policies, including refocusing our strategic direction and marketing efforts on advances, beginning our exit from the MPP, and substantially reducing our operating expenses, primarily through reductions in staff and facilities costs. To lead the Seattle Bank in refocusing our business, our Board of Directors, or Board, appointed James E. Gilleran as our president and chief executive officer effective June 2005, appointed Richard M. Riccobono as our executive vice president, chief operating officer effective August 2005, and appointed Mark R. Szczepaniak as our chief financial officer effective July 2005. In February 2007, Mr. Gilleran announced his resignation effective April 30, 2007, and the Board appointed Mr. Riccobono as our president and chief executive officer effective May 1, 2007. For more information regarding these matters, see “—Regulation—Written Agreement and Business Plan,” and “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview—Historical Operations,” and “Part III. Item 10. Directors, Executive Officers and Corporate Governance.”

Membership and Market

The Seattle Bank is a cooperative that is owned by member financial institutions located within our district. All federally insured depository institutions and insurance companies engaged in residential housing finance and community financial institutions located in the Seattle Bank’s district are eligible to apply for membership. Eligible institutions must purchase capital stock in the Seattle Bank as a condition of membership. Members generally are assigned a credit line at the time they join, based on our evaluation of their financial condition, and are eligible to receive dividends, when and if payable, on their capital stock investment. Members are subject to activity-based capital stock requirements, which may require them to purchase additional stock if the amount of business they do with us increases. All of our outstanding capital stock is owned by our members, except in limited circumstances, for example, for a period after a member is acquired by a nonmember.

As of December 31, 2006, the Seattle Bank had 379 members, which represented approximately 38% of the financial institutions in our district eligible for membership. We also had six stockholders that were nonmembers

3

holding capital stock as a result of acquisitions that are awaiting redemption of their stock by us. Additionally, we had six approved housing associates that were not required to purchase our stock to use our services within the parameters of our regulations and policies. As of December 31, 2006, 10 of our members had requested withdrawal from membership. On March 27, 2007, one member rescinded its withdrawal request.

Since 1999, membership has grown from 336, although our membership growth has slowed in recent years. The composition of our membership has remained essentially the same during that time, with commercial banks and thrifts comprising between 77% and 86% and credit unions between 14% and 22% of our membership. The following tables show the capital stock holdings and the geographic locations of our stockholders, by type, as of December 31, 2006.

| | | | | |

Type of Institution | | Number of

Institutions | | Total Value

of Capital

Stock Held* |

| (dollars in thousands) | | | | |

Commercial banks | | 253 | | $ | 1,042,050 |

Thrifts | | 37 | | | 1,016,881 |

Credit unions | | 84 | | | 141,679 |

Insurance companies | | 5 | | | 9,609 |

| | | | | |

Total | | 379 | | $ | 2,210,219 |

| | | | | |

| * | Includes $69.2 million in mandatorily redeemable Class B stock. See “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Capital Resources and Liquidity–Capital Resources–Seattle Bank Stock.” |

| | | | | | | | | | |

State or Territory | | Commercial

Banks | | Thrifts | | Credit

Unions | | Insurance

Companies | | Total |

Alaska | | 6 | | 1 | | 5 | | | | 12 |

American Samoa | | 1 | | | | | | | | 1 |

Guam | | 2 | | 1 | | 1 | | | | 4 |

Hawaii | | 5 | | 2 | | 5 | | | | 12 |

Idaho | | 12 | | 3 | | 2 | | 1 | | 18 |

Montana | | 61 | | 2 | | 7 | | | | 70 |

Ohio* | | 1 | | | | | | | | 1 |

Oregon | | 30 | | 2 | | 18 | | 1 | | 51 |

Utah | | 35 | | 3 | | 12 | | 1 | | 51 |

Washington | | 66 | | 20 | | 30 | | 2 | | 118 |

Wyoming | | 34 | | 3 | | 4 | | | | 41 |

| | | | | | | | | | |

Total | | 253 | | 37 | | 84 | | 5 | | 379 |

| | | | | | | | | | |

| * | Out-of-district nonmember stockholder holding capital stock as a result of an acquisition, pending redemption. |

The Seattle Bank’s market area is the same as its membership district. Institutions that are members of the Seattle Bank must have their principal places of business within this market area but may also operate elsewhere. The value of membership in the Seattle Bank has historically been derived primarily from the following aspects of our business:

| | • | | the relatively low rates at which members can borrow from us, which stems from our ability to raise funds in the financial markets at favorable interest rates through consolidated obligations, due primarily to the FHLBank System’s “AAA” credit rating; |

| | • | | the access we provide to readily available funding for liquidity purposes; |

| | • | | the access we provide to grants and below-market-rate loans for affordable housing and economic development; |

4

| | • | | the access we historically provided as a competitively priced secondary mortgage market alternative; and |

| | • | | the dividends that we have paid to members until recently, which historically have represented a significant portion of our earnings. |

To provide value to our members, we leverage our capital stock through the issuance of FHLBank System debt in the form of consolidated obligations. We have used a majority of the proceeds from the sale of consolidated obligations on which we are the primary obligor to provide advances to member and approved nonmember borrowers and historically to purchase mortgage loans under the MPP. We have also used the proceeds from consolidated obligations on which we are the primary obligor to purchase investments in high-quality financial instruments, including consolidated obligations on which other FHLBanks are the primary obligors, with the goal of achieving market-rate returns on our investments. Interest income from our credit products, mortgage loans, and investments is used to pay our interest expenses, operating expenses, other costs, and dividends to our members.

Our Business

We manage and report our operations as a single business segment, traditional member finance, which includes making advances, providing letters of credit, accepting deposits, and providing securities safekeeping and other services. Historically, we offered products and services through two operating segments, traditional member finance and the MPP. The MPP segment consisted of mortgage loans held for portfolio as a result of purchases from participating members. During the first quarter of 2005, we decided to exit the MPP. As a result of this decision, Seattle Bank management no longer manages the business using separate operating segments and the operating results of the former MPP segment are aggregated with the traditional member finance segment for decision-making purposes. See “Segment Disclosure” in Note 1 in “Part II. Item 8. Financial Statements and Supplementary Data—Audited Financial Statements—Notes to Financial Statements.”

Products and Services

Advances

We make advances to our member and approved nonmember borrowers at competitive rates, with maturities ranging from overnight to 30 years. Advances can be customized to meet a borrower’s special funding needs, using a variety of interest-rate indices, maturities, amortization schedules, and embedded options such as call or put options. Borrowers pledge mortgage loans and other eligible collateral, such as U.S. Treasury or agency securities, to secure these advances. With the exception of overnight and other very short-term advances, we generally do not make advances of less than $100,000.

As of December 31, 2006, we had 222 member borrowers with outstanding advances totaling $28.0 billion, and two approved nonmember borrower with outstanding advances totaling $7.9 million.

Advances to Members. Advances generally support our members’ mortgage lending activities. In addition, advances made to member community financial institutions may be used for the purpose of providing loans to small businesses, small farms, and small agribusinesses. Community financial institutions are financial institutions that, in 2006, had average assets over the last three years of no more than $587.0 million.

Advances help our members manage their assets and liabilities and serve as a funding source for a variety of member uses, including mortgage loans that members may be unable or unwilling to sell in the secondary mortgage market. Advances matched to the maturity and prepayment characteristics of mortgage loans can reduce a member’s interest-rate risk associated with holding mortgage loans. Accordingly, advances support important housing markets, including those focused on low- and moderate-income households. In addition, advances provide members with a low-cost source of liquidity, reducing their need to hold low-yielding liquid assets financed with longer-term, more expensive debt, and provide long-term financing to support our members’ balance sheet management strategies. For example, for members that choose to sell their mortgage loans in the

5

secondary mortgage markets, advances can provide funding for temporary liquidity needs. Advances also provide competitively priced wholesale funding to smaller community lenders that typically do not have access to many of the funding alternatives available to larger financial organizations, such as repurchase agreements, commercial paper, and brokered deposits.

Advances to Nonmembers. Under the FHLBank Act, we are permitted to make advances to nonmembers that are approved under Title II of the National Housing Act, which we also refer to as approved nonmember borrowers. These approved nonmember borrowers are not subject to all of the provisions of the FHLBank Act that apply to our members. For example, they have no capital stock purchase requirements, although the same regulatory lending requirements generally apply to them as apply to members. An approved nonmember borrower must be a government agency or be chartered under federal or state law with rights and powers similar to those of a corporation, and it must lend its own funds as its principal activity in the mortgage lending field. The financial condition of an approved nonmember borrower must be such that, in our sole opinion, we can safely make advances to the approved nonmember borrower.

Types of Advances. The Seattle Bank offers a variety of advances, including variable interest-rate, fixed interest-rate, and structured advances. Structured advances are either fixed interest-rate or variable interest-rate advances that include certain options that are affected by interest rates or that alter the cash flows.

Variable Interest-Rate Advances

Cash Management Advances. Cash management advances are short-term, variable interest-rate advances designed to provide immediate and flexible funding to meet borrowers’ daily liquidity needs. A cash management advance is an open-note program, similar to a revolving line of credit or a federal funds line. Outstanding cash management advance balances are automatically renewed unless paid off by the borrower. Borrowers can increase or decrease cash management advance balances daily. Cash management advance rates are based on overnight federal funds rates and are reset daily. There are no minimum dollar amounts for cash management advances.

Adjustable Advances. Adjustable advances are variable interest-rate, fixed-term advances with interest rates based on a spread to a specified market interest-rate index, such as the London Interbank Offered Rate, known as LIBOR, or prime. Maturities range from one to five years. Adjustable advances are subject to prepayment fees. The prepayment fee requirement is intended to make us economically indifferent to a borrower’s decision to prepay an advance. However, because interest rates on adjustable advances track interest rates in the financial markets, prepayment fees are generally minimal.

Fixed Interest-Rate Advances

Fixed Interest-Rate Advances. Fixed interest-rate advances include short-term advances with maturities from seven days to one year and long-term, fixed interest-rate advances with maturities from one year to 30 years. In both cases, principal is due at maturity. Principal may be prepaid prior to maturity, subject to a prepayment fee. We determine the amount of fees charged for prepayments using the interest rate, the amount, the remaining time to maturity of the prepaid advance, and our cost of funds at the time the advance is prepaid. The prepayment fee requirement is intended to make us economically indifferent to a borrower’s decision to prepay an advance.

Amortizing Advances. Amortizing advances are fixed interest-rate, fixed-term advances, where the principal is repaid over the term of the advance, generally on a straight-line basis. Maturities range from two to 30 years. Amortizing advances allow borrowers to reduce the principal level of their advances in tandem with their funded assets, such as mortgage loans.

Structured Advances

Putable Advances. Putable advances have a fixed interest rate and include an option for us to terminate the advance on specific dates throughout the term of the advance following a specified period of time, which we

6

refer to as a lock-out period. In exchange for our option, the borrower pays a lower interest rate on the advance. Maturities range from one to 10 years, with lock-out periods from three months to five years or longer. At the end of the lock-out period, and on a periodic basis thereafter, we may terminate the advance at our discretion. If we elect to terminate the advance, the member may apply for a new advance at the then-current advance rates, subject to all applicable credit requirements.

Knockout Advances. Knockout advances are a type of putable advance that is automatically canceled by the Seattle Bank in the event LIBOR exceeds a pre-determined interest rate on set future dates. If the advance is canceled, the member may apply for a new advance at the then-current advance rates, subject to all applicable credit requirements.

Capped Floater Advances. A capped floater advance is an adjustable interest-rate advance that is capped at a pre-determined interest rate. The funding structure allows the borrower to benefit from lower borrowing costs should interest rates decline, while offering protection against a significant increase in interest rates.

Floored Advances. A floored advance is an adjustable interest-rate advance that contains a long position in an interest- rate floor that is based on a benchmark index rate such as LIBOR. If interest rates decline below a pre-determined interest rate, the borrower’s rate will be reduced to an interest rate that reflects the lower index rate less the difference between the pre-determined interest rate and the index rate. This advance offers the borrower protection from exposure to falling interest rates.

Floating-to-Fixed Convertible Advances. A blend of an adjustable interest-rate advance and a putable advance, the floating-to-fixed convertible, or FFC, advance initially has a floating or variable interest rate, which “flips” to a fixed rate of interest on a pre-determined date if we do not exercise our option to cancel the advance on that date. In addition, the FFC advance has an option for us to cancel the advance on specific dates throughout the term of the advance, including the “flip” date, following the lock-out period. The FFC advance offers sub-LIBOR, variable interest-rate funding in exchange for selling the Seattle Bank the right to cancel the advance on pre-determined dates.

Returnable Advances. This fixed interest-rate advance gives the borrower the right to prepay the advance to the Seattle Bank on pre-determined dates without a prepayment penalty. The cost of purchasing the option is reflected in an interest rate that is higher than that of a standard fixed-rate advance.

The types of advances outstanding as of December 31, 2006 and the amount of income generated by each advance type for the year ended December 31, 2006 are described in the table below.

| | | | | | | | | | | | |

| | | As of December 31, 2006 | | | For the Year Ended

December 31, 2006 | |

Advance Type | | Advances

Outstanding | | Percent of Total

Advances

Outstanding | | | Advances

Income* | | Percent of Total

Advances

Income | |

| (dollars in thousands) | | | |

Variable interest-rate advances | | | | | | | | | | | | |

Cash management advances | | $ | 1,151,020 | | 4.11 | % | | $ | 76,007 | | 6.06 | % |

Adjustable advances | | | 10,891,978 | | 38.93 | | | | 322,713 | | 25.72 | |

Fixed interest-rate advances | | | | | | | | | | | | |

Fixed interest-rate advances | | | 11,792,206 | | 42.13 | | | | 658,751 | | 52.51 | |

Amortizing advances | | | 675,669 | | 2.41 | | | | 36,090 | | 2.88 | |

Structured advances | | | | | | | | | | | | |

Putable advances | | | 3,195,946 | | 11.42 | | | | 153,772 | | 12.25 | |

Capped floater advances | | | 140,000 | | 0.50 | | | | 5,381 | | 0.43 | |

Floating-to-fixed convertible advances | | | 140,000 | | 0.50 | | | | 1,912 | | 0.15 | |

| | | | | | | | | | | | |

Total par value of advances | | $ | 27,986,819 | | 100.00 | % | | $ | 1,254,626 | | 100.00 | % |

| | | | | | | | | | | | |

| * | Advances income excludes hedging adjustments, amortization of discounts on AHP advances, commitment fees, and amortization of prepayment fees. |

7

Security Interests.We are required under the FHLBank Act to obtain and maintain a security interest in eligible collateral at the time we originate or renew an advance. Eligible collateral for member borrowers includes:

| | • | | whole first mortgage loans on improved residential property or securities representing a whole interest in the mortgage loans; |

| | • | | securities issued, insured, or guaranteed by the U.S. government or any of its agencies, such as mortgage-backed securities issued or guaranteed by the Government National Mortgage Association, or Ginnie Mae; |

| | • | | mortgage-backed securities issued or guaranteed by Federal National Mortgage Association, or Fannie Mae, or Federal Home Loan Mortgage Corporation, or Freddie Mac, neither of which are guaranteed, directly or indirectly, by the U.S. government; |

| | • | | cash or other deposits in the Seattle Bank; and |

| | • | | other acceptable real estate-related collateral that has a readily ascertainable value, can be liquidated in due course, and in which we can perfect a security interest. |

As additional security for a member borrower’s indebtedness, we have a statutory lien on our member borrowers’ capital stock in the Seattle Bank. Community financial institutions have the benefit of expanded statutory collateral provisions dealing with small business, small farm, or small agribusiness loans.

Nonmember borrowers are subject to more stringent collateral requirements than are member borrowers. For example, collateral generally is limited to whole first mortgage loans on improved residential real estate that are insured by the Federal Housing Administration, or FHA, of the U.S. Department of Housing and Urban Development under Title II of the National Housing Act. Securities that represent a whole interest in the principal and interest payments due on a pool of FHA mortgage loans also are eligible. Collateral for nonmember borrowers is maintained in the physical possession of the Seattle Bank.

We use three basic categories of collateral control arrangements to secure our interests: blanket pledge, segregation/listing, and physical possession.

| | | | |

Control Category | | Physical Delivery

(Yes / No) | | Summary Description |

Blanket Pledge | | Loans: No Securities: Yes | | Members are not required to physically deliver loan documents to us. Instead, we monitor estimated collateral levels from regulatory financial reports filed quarterly with the member’s regulator or, for types of collateral not readily ascertainable from the regulatory financial reports, from specific member-prepared schedules provided to us on a periodic basis. All securities collateral must be specifically pledged and delivered to a controlled account at either the Seattle Bank or a third-party custodian approved by us. |

| | |

Segregation/Listing | | Loans: No Securities: Yes | | Members are required to periodically submit a listing of their pledged loan collateral and must be prepared to deliver the collateral to us if requested to do so. All securities collateral must be specifically pledged and delivered to a controlled account at either the Seattle Bank or a third-party custodian approved by us. |

| | |

Physical Possession | | Loans: Yes Securities: Yes | | All collateral used in determining borrowing capacity is delivered to us. Securities pledged are delivered to a controlled account at either the Seattle Bank or a third-party custodian approved by us. |

We determine the appropriate collateral control category based on a risk analysis of the member borrower, using regulatory financial reports and other information. In general, collateral needed to meet minimum

8

requirements must be owned by the member borrower, or in certain cases, a member’s affiliate approved by us, and must be identified on the member’s or affiliate’s books and records as being pledged to us. Member borrowers must comply with collateral requirements before we fund an advance. Member borrowers are required to maintain eligible collateral, free and clear of pledges, liens, or other encumbrances of third parties, in an amount that covers outstanding indebtedness due to us. Member borrowers must maintain appropriate tracking controls and reports to ensure compliance with this requirement.

The Competitive Equality Banking Act of 1987 affords priority to any security interest granted to us by any of our member borrowers over the claims and rights of any party, including any receiver, conservator, trustee, or similar party having rights as a lien creditor. The only two exceptions to this priority are claims and rights that would be entitled to priority under otherwise applicable law or that are held by actual bona fide purchasers for value or by parties that have actual perfected security interests in the collateral. In addition, our claims are given certain preferences pursuant to the receivership provisions in the Federal Deposit Insurance Act. Most member borrowers grant us a blanket lien covering substantially all of the member borrower’s assets and consent to our filing a financing statement evidencing the blanket lien, which we do as a standard practice.

Based on the security provided by the blanket lien, the financing statement, and the statutory preferences, we do not take control of the collateral, other than securities collateral, pledged by member borrowers under the blanket pledge or segregation/listing categories. We generally will further secure our security interests by taking physical possession (or control) of the supporting collateral if we determine the financial or other condition of a particular member borrower so warrants. In addition, we generally take physical possession of collateral pledged by non-depository institutions (e.g., insurance companies and approved nonmember borrowers) to ensure that an advance is as secure as the security interest in collateral pledged by depository institutions.

Typically, we charge collateral management and safekeeping fees on collateral delivered to the Seattle Bank or its custodians.

Borrowing Capacity.Borrowing capacity depends on the type of collateral provided by a borrower, whether a member or a nonmember. The following table shows, for each type of collateral, the borrowing capacity as a percentage of the collateral’s value. To determine the value against which we apply these specified discounts, we generally use discounted cash flows for mortgage loans and a third-party pricing source for securities for which there is an established market.

| | |

Type of Collateral | | Borrowing Capacity |

U.S. Treasury and other government agency* securities | | 95 – 97% |

| |

U.S. Treasury and other government agency* debentures and non-agency-rated mortgage-backed securities | | 80 – 87% |

| |

Eligible first-lien single or multi-family mortgage loans | | 80 – 83% |

| |

Other eligible collateral and community financial institution collateral | | 50 – 75% |

| * | Includes GSEs such as Fannie Mae, Freddie Mac, and other FHLBanks, as well as other U.S. agencies such as Ginnie Mae, the Farm Services Agency, Small Business Administration, Bureau of Indian Affairs, and the United States Department of Agriculture. |

On a case-by-case basis, we accept certain categories of first-lien single-family subprime mortgage loans as collateral under our subprime collateral program. Prior to being approved for this program, members must complete a separate application process which includes a thorough assessment of their credit and collateral administration policies and procedures for subprime lending. Also, our credit department staff reviews individual subprime loans for compliance with the policies and also tests for loans with predatory characteristics and compliance with our responsible lending policy. Borrowing capacity rates for approved subprime loans vary from 50% to 75%, according to loan characteristics. The policy adopted by our Board to govern the subprime collateral program prohibits as eligible collateral: loans delinquent more than sixty days, second liens, loans

9

with a debt-to-income ratio in excess of 49%, and non-owner occupied properties. In addition, certain state concentration limits were established. The market value of the subprime loans is determined regularly by a third-party expert in mortgage valuation, contracted by the Seattle Bank.

Management of Credit Risk. In order to manage the credit risk of our advances, we monitor our member borrowers’ financial condition using quarterly reports submitted by our members to their regulators. We perform quarterly analyses and reviews of member borrowers whose financial performance does not fall within the key performance parameters defined in our credit monitoring system. For example, member borrowers falling within the following performance categories will be analyzed and reviewed:

| | • | | member borrowers that report a net operating loss for the quarter; |

| | • | | member borrowers that report a ratio of nonperforming assets to equity and loss reserves in excess of 20%; |

| | • | | member borrowers with a composite CAMELS score of 3 or worse; or |

| | • | | member borrowers with: (1) a quarterly Portfolio Analysis and Monitoring System, or PAMS, score of 15 or less on a scale of 50 points, (2) a quarterly PAMS score decline of 10 points or more during the most recent quarter, or (3) a 10-point drop in weighted-average PAMS score over two quarters. |

The CAMELS rating system generates a regulatory rating of a financial institution’s overall condition, based on on-site examinations of six factors: capital adequacy, asset quality, management quality, earnings, liquidity, and sensitivity to market risk. Each financial institution’s regulator assigns the institution a score on a scale of 1 (best) to 5 (worst) for each of the six factors, along with a composite or overall rating for a financial institution that is based on a combination of the factors’ scores and an overall evaluation. Financial institutions with a composite rating of 1 or 2 are considered to be high-quality institutions that present few, if any, supervisory concerns. PAMS is an internal scoring system we use to evaluate and classify various credit risks associated with members. We use a number of credit quality ratios, such as non-performing loans to total loans, as well as profitability, capital, and liquidity ratios to determine a member borrower’s score.

We review and validate collateral pledged by member borrowers on a risk-based schedule, according to the member’s financial condition, collateral quality, or other credit considerations. Member borrowers who fully collateralize their indebtedness with marketable securities in a pledged account under the control of the Seattle Bank are generally not subject to collateral verifications.

Financial information on nonmember borrowers is generally limited to annual reports, which include fiscal year-end financial data. Nonmember borrowers that request recurring borrowing facilities are reviewed periodically. Certifications relating to their status as an eligible nonmember borrower, use of proceeds, and eligibility of collateral are required with each advance. Nonmember borrowers must provide current financial statements and meet all eligibility tests prior to consideration of borrowing requests.

Concentration and Pricing of Advances.Our advance balances are concentrated with commercial banks and thrift institutions. As of December 31, 2006, five members held 69.5% of the par value of our outstanding advances, with two of these members holding 56.8% of the par value of our outstanding advances. No borrower other than Bank of America Oregon, N.A. and Washington Mutual Bank, F.S.B., held more than 10% of the par value of our total advances outstanding as of December 31, 2006.

10

The following table identifies our top five borrowers’ advance balances and their percentage of our total par value of advances, as well as the income and percentage of our total advance income from these advances for the year ended December 31, 2006.

| | | | | | | | | | | | |

| | | As of December 31, 2006 | | | For the Year Ended

December 31, 2006 | |

Name | | Advances at

Par Value | | Percent

of Total

Advances | | | Advances

Income | | Percent

of Total

Advances

Income | |

| (dollars in thousands) | | | | | | | | | | |

Bank of America Oregon, N.A. | | $ | 10,060,394 | | 36.0 | % | | $ | 400,472 | | 31.1 | % |

Portland, OR | | | | | | | | | | | | |

| | | | |

Washington Mutual Bank, F.S.B. | | | 5,821,822 | | 20.8 | | | | 216,143 | | 16.8 | |

Seattle, WA | | | | | | | | | | | | |

| | | | |

Washington Federal Savings Bank | | | 1,500,000 | | 5.4 | | | | 69,654 | | 5.4 | |

Seattle, WA | | | | | | | | | | | | |

| | | | |

Sterling Savings Bank | | | 1,306,008 | | 4.7 | | | | 59,896 | | 4.6 | |

Spokane, WA | | | | | | | | | | | | |

| | | | |

American Savings Bank, F.S.B. | | | 730,000 | | 2.6 | | | | 39,980 | | 3.1 | |

Honolulu, HI | | | | | | | | | | | | |

We are not subject to any regulatory or other restrictions on concentrations of advances with particular categories of institutions or with individual borrowers. Nevertheless, we monitor our advance activity and provide a variety of information to our Board regarding advance balances and activity trends by type of advance, customer, and other relevant measures. Because a large concentration of our advances is held by only a few members, changes in their borrowing decisions can significantly affect the amount of our advances outstanding. We expect that the concentration of advances with our largest borrowers will remain significant for at least 2007 and several years thereafter.

There are three primary means of pricing advances:

| | • | | Advance window. All borrowers receive the same pricing, which is posted on our website. |

| | • | | Auction funding. Through this alternative, borrowers can generally save five or more basis points on advance rates. Auction funding is available two times per week when the Seattle Bank participates in consolidated obligation discount note issuances from the Office of Finance. Borrowers do not know the interest rate of the advance until the auction is complete. |

| | • | | Differential pricing. Borrowers can request a lower advance rate and, subject to specific criteria and delegated authority, certain staff members may adjust the pricing levels. |

We significantly increased our use of differential pricing in 2006 and 2005 as we refocused our business on advances. The differential pricing option is administered by specified employees within parameters established by our asset and liability management committee (consisting of Seattle Bank employees) under authority delegated by our president and chief executive officer and overseen by the Board. For the year ended December 31, 2006, the amount of differentially priced advances accounted for 79.5% of new advances, compared to 46.0% for the year ended December 31, 2005. The amount of window advances and auction-priced advances accounted for 10.0% and 10.5% of new advances made for the year ended December 31, 2006, compared to 45.5% and 8.5% of advances made for the year ended December 31, 2005.

We believe that the use of differential pricing gives us greater flexibility to compete with regard to rates for more advance business. This means that rates on advances may be lower for some members than for others in order to be competitive with lower rates available to those members that have alternative funding sources. In

11

general, our larger members have more alternative funding sources and are able to access funding at lower rates than our smaller members. We believe that the use of differential pricing has increased our advance balance and will continue to do so in the future, and that the increased volume compensates us for any reduction in overall yield due to differential pricing. For additional discussion on advances, see “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Financial Condition—Advances—Member Demand for Advances.”

The weighted-average interest rates of advances are highly dependent upon origination date and time to maturity. The federal funds rate increased by 100 basis points during 2006, 200 basis points during 2005, and 125 basis points during 2004, from historically low levels in 2003 and 2002. As a result, shorter-term, fixed interest-rate advances have higher weighted-average interest rates than those with longer terms. The table below provides information on the type, weighted-average interest rates, and terms of advances held by our five largest borrowers and all other borrowers as of December 31, 2006.

| | | | | | | | | | | | | | | | | | | | |

| | | Top Five Borrowers | | All Other Borrowers |

Advance Type | | Advances

Outstanding | | Weighted-

Average

Percent

Interest

Rate | | | Weighted-

Average

Term

(months) | | Weighted-

Average

Remaining

Term

(months) | | Advances

Outstanding | | Weighted-

Average

Percent

Interest

Rate | | | Weighted-

Average

Term

(months) | | Weighted-

Average

Remaining

Terms

(months) |

| (dollars in thousands) | | | | | | | | | | | | | | | | | | |

Variable interest-rate advances | | | | | | | | | | | | | | | | | | | | |

Cash management advances | | $ | 17,256 | | 5.63 | % | | 11.97 | | 3.39 | | $ | 1,133,764 | | 5.63 | % | | 11.98 | | 5.96 |

Adjustable advances | | | 9,883,000 | | 5.32 | | | 20.81 | | 12.72 | | | 1,008,978 | | 5.53 | | | 24.53 | | 16.48 |

Fixed interest-rate advances | | | | | | | | | | | | | | | | | | | | |

Fixed interest-rate advances | | | 7,379,752 | | 5.24 | | | 9.56 | | 3.28 | | | 4,412,454 | | 4.71 | | | 36.38 | | 18.72 |

Amortizing advances | | | 322,466 | | 5.45 | | | 178.86 | | 119.97 | | | 353,203 | | 4.79 | | | 128.40 | | 82.55 |

Structured advances | | | | | | | | | | | | | | | | | | | | |

Putable advances | | | 1,815,750 | | 4.71 | | | 116.42 | | 72.72 | | | 1,380,196 | | 4.62 | | | 106.98 | | 70.51 |

Capped floater advances | | | | | | | | | | | | | 140,000 | | 5.63 | | | 44.60 | | 32.15 |

Floating-to-fixed convertible advances | | | | | | | | | | | | | 140,000 | | 4.22 | | | 114.25 | | 110.47 |

| | | | | | | | | | | | | | | | | | | | |

Total par value of advances | | $ | 19,418,224 | | 5.24 | | | 28.09 | | 16.51 | | $ | 8,568,595 | | 4.93 | | | 48.16 | | 29.34 |

| | | | | | | | | | | | | | | | | | | | |

Other Mission-Related Community Investment Programs.We provide direct and indirect support for programs designed to make communities better places to work and live. We assist members in meeting their Community Reinvestment Act responsibilities through a variety of specialized funding programs. Through our AHP and our other community investment programs, members have access to grants and subsidized and other low-cost funding to help them provide affordable rental and home ownership opportunities and take part in commercial and economic development activities that benefit low- and moderate-income neighborhoods. We also provide subsidy grants and loans to members for community and economic development. We administer and fund the programs described below.

Affordable Housing Program. Through the AHP, we offer grants and discounted advances to member financial institutions that partner with community sponsors to stimulate affordable rental and home ownership opportunities for low- or moderate-income households, which are defined as households with income below 80% of the area’s median income adjusted for family size. AHP grants can be used to fund the acquisition, rehabilitation, or construction of housing, to reduce principal or interest rates on loans, or to assist in covering down payments or closing costs. We fund this program with approximately 10% of our net income each year. Over the last 16 years, the AHP has provided significant resources to members for housing development across the Seattle Bank’s district to assist in the purchase, construction, and rehabilitation of housing for low- and moderate-income households. We awarded AHP grants of $4.2 million, net of withdrawals, in 2006, funding over 1,006 housing units in 13 states or territories. From the inception of the program in 1990 through the end of 2006, we awarded $167.6 million in AHP grants to facilitate development of projects to create more than 33,450 housing units.

The Home$tart Program. The Home$tart Program is a subprogram of the AHP that, through our members, provides first-time home buyers with down payment and closing cost assistance by matching financial contributions made by the home buyers. We match $3 for every $1 put up by the home buyer, up to $5,000.

12

| | For home buyers already receiving public housing assistance, we match $2 for every $1 put up by the home buyer, up to $10,000. In 2006, $2.0 million was distributed as part of the Home$tart program. |

Community Investment Program/Economic Development Fund. In addition to the AHP, we offer two programs, the Community Investment Program and the Economic Development Fund, through which our members can apply for advances to support affordable housing initiatives or fund economic development. These programs provide advance funding with interest rates 10 to 25 basis points below our regular advance rates, for terms of five to 30 years. Rate locks are also available for periods of up to 24 months. These advances are especially effective when they support housing and commercial development in distressed or rural areas where financial resources are scarce. Our Community Investment Program/Economic Development Fund advances have been used to build affordable homes, fund multi-family rental projects, construct new roads and bridges, create sewage treatment plants, and finance new small businesses. As of December 31, 2006, we had $671.0 million in advances outstanding under these programs.

ACCESS Fund. Between 2000 and 2004, we set aside up to $200,000 per year to fund ACCESS, a recoverable loan fund that covers predevelopment costs associated with community-based economic development projects and loan loss reserves of community-based financial intermediaries. ACCESS granted $1.1 million in support of 24 projects between 2000 and 2005. In 2005, we suspended making contributions to this program. Our Board may consider reinstituting this or a similar program once we have established a trend of consistent profitability.

Challenge Fund. The Challenge Fund is a revolving fund that provides grants of up to $20,000 to subsidize predevelopment expenses associated with affordable housing projects. When a project moves forward, the grant is repaid. If a project does not move forward, the grant may be forgiven. In 2005, we suspended this program. Our Board may consider reinstituting this or a similar program once we have established a trend of consistent profitability.

Letters of Credit

The Seattle Bank issues letters of credit that provide members an efficient and low-cost vehicle to secure contractual agreements, enhance credit profiles, improve asset and liability management, and collateralize public deposits. Terms are individually structured to meet member needs. As of December 31, 2006, our outstanding letters of credit totaled approximately $135.6 million.

Mortgage Loans Held for Portfolio

Many of our members originate mortgage loans. However, for a variety of reasons, including liquidity, mortgage servicing, and risk management purposes, our members often sell their mortgage loans into the secondary mortgage market rather than holding them in their portfolios. We designed the MPP in collaboration with certain other FHLBanks to provide participating members with: (i) an alternative to the sale of whole mortgage loans into the traditional secondary mortgage market, and (ii) an enhanced ability to provide attractive financing to home buyers in their communities. Under the MPP, we purchased loans directly from our members, without the use of any intermediary, such as an intervening trust. The MPP was designed as a risk-sharing arrangement under which we would manage the liquidity, interest rate, and prepayment risk of purchased mortgage loans, while members would retain the primary credit risk. Since the inception of the MPP in 2001, we generally operated our MPP independently without participation from other FHLBanks, except for certain coordination and limited cost-sharing arrangements relating to software enhancements and upgrades and, when beneficial to the FHLBanks that offer an MPP, joint negotiation with common vendors, such as master servicing providers and supplemental mortgage insurance companies.

In March 2005, we announced that we were refocusing our business on advances, and in our business plan, we outlined a strategy to exit the MPP. We ceased entering into new master commitment contracts in 2005 and have terminated all open contracts. In August 2005, we sold $1.4 billion of government-insured mortgage loans

13

to Bank of America, N.A., an affiliate of one of our members, Bank of America Oregon, N.A. In September 2005, we reclassified the remaining government-insured mortgages as held for portfolio. We expect that the balance of our mortgage loans held for portfolio will continue to decrease as those loans are paid off.

Our MPP business was concentrated among a small number of participating members as the following table shows, and we were not subject to any regulatory or other restrictions on concentrations of MPP business with particular categories of institutions or with individual customers. The following table presents our historical purchases from our three largest MPP participating members through December 31, 2006.

| | | | | | |

| | | Through December 31, 2006 | |

Name | | Par Value of

Purchases | | Percent of Total

Par Value of

MPP Purchases | |

| (dollars in thousands) | | | | | |

Washington Mutual Bank, F.S.B. Seattle, WA | | $ | 15,200,050 | | 83.5 | % |

| | |

Wells Fargo Bank Northwest, N.A Salt Lake City, UT | | | 1,491,887 | | 8.2 | |

| | |

Bank of America Oregon, N.A. Portland, OR | | | 923,209 | | 5.1 | |

Eligible Loans. Through the MPP, we purchased directly from participating members fixed interest-rate, fully amortizing, government-insured mortgage loans and conventional, one- to four-family residential mortgage loans with principal balances that would have made them eligible for purchase by Fannie Mae and Freddie Mac. The government-insured mortgage loans we purchased are insured by the FHA. As of December 31, 2006, our mortgage loan portfolio was composed of government-insured mortgage loans with a par value totaling $292.1 million and conventional mortgage loans with a par value totaling $6.0 billion. As of December 31, 2006, the MPP portfolio consisted of 38,711 mortgage loans, which were originated throughout the United States. For additional information regarding mortgage loan holdings by state and geographic concentration, see “Part II. Item 8. Financial Statements and Supplementary Data—Unaudited Supplementary Data—Geographic Concentration of Mortgage Loans.”

We do not service the mortgage loans we purchased from our participating members. Under the MPP, participating members that sold mortgage loans to us could either continue to service the mortgage loans or independently sell the servicing rights to a service provider acceptable to us. If the participating member released its servicing rights to another service provider on our pre-approved list, the member typically received a servicing released premium for selling the servicing under the servicing released option.

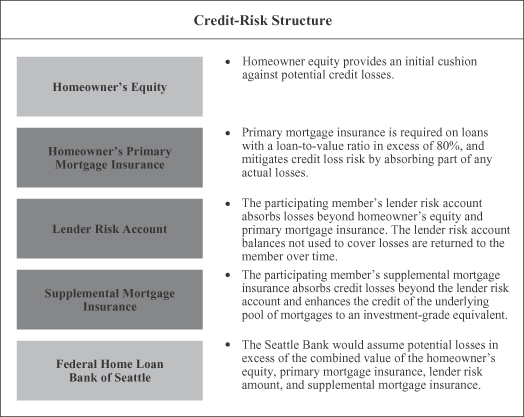

Management of Credit Risk. To ensure member retention of most of the credit risk and to cover, at a minimum, the expected losses on the conventional mortgage loans originated or acquired by a member and purchased under the MPP, we require the member to fund a lender risk account. The lender risk account is funded in one of two ways: (i) historically, by an up-front reduction to the proceeds paid to the member for its mortgage loans; or (ii) by an additional modification to the yield on the mortgage loans purchased such that a portion of the amount paid by the member each month is designated for the lender risk account. The lender risk account is used to cover potential mortgage loan losses in excess of the homeowner’s equity in the underlying collateral and any private mortgage insurance for the mortgage loan. This account is established to conform to federal regulation covering acquired member asset programs. These regulations stipulate that a member is responsible for all expected losses on the mortgage loans it sells to an FHLBank. The participating member’s master commitment contract relating to the MPP specifies the funding level required for the member’s lender risk account. In accordance with the applicable contract, either the purchase price for the mortgage loans purchased under a member’s master commitment contract was discounted or the amount paid monthly by the member is increased to fund the lender risk account. If the member’s lender risk account is funded through monthly

14

payments, the member remains obligated under the master commitment contract to pay the monthly amounts that fund the lender risk account whether or not any of the purchased mortgage loans are in default.

We require each member that sold conventional mortgage loans to us to provide additional credit enhancements that, combined with the lender risk account, effectively make the purchased mortgage loan portfolio equivalent to an investment that has been highly rated by Moody’s Investor’s Service, or Moody’s, or Fitch Investor’s Service, or Fitch. This was accomplished, in part, through the participating member’s purchase of supplemental mortgage insurance. We evaluated the proposed conventional mortgage loans to be purchased (either the specific portfolio or a representative sample) to determine the amount of expected losses from the mortgage loans. The amount funded into the lender risk account by the member was the greater of these expected losses or the minimum required by the supplemental mortgage insurance provider in order to provide supplemental mortgage insurance. As with some of the funding of the lender risk account, a portion of the monthly interest was set aside to fund the supplemental mortgage premium. If the lender risk account and the standard supplemental mortgage insurance policy did not combine to provide sufficient loss protection to support the equivalent of an investment-grade rating, the member was required to purchase additional supplemental mortgage insurance coverage called SMI Plus. This policy provides additional credit enhancement coverage to achieve an equivalent of an investment-grade rating.

The lender risk account funds and any payments made under supplemental mortgage insurance may be used to offset any losses that may occur over the life of the mortgage loans. To the extent that amounts deposited in the lender risk account exceed losses on the purchased mortgage loans, we return the remaining lender risk account funds to the participating member in accordance with the release schedule in the participating member’s master commitment contract. No lender risk account or other enhanced credit feature is required on U.S. government-insured mortgage loans that we purchased from our participating members.

15

As a result of the credit enhancements described above, we and our participating members share the credit risk of the mortgage loans sold to us under the MPP. The participating member assumes a first-loss obligation in the event of a mortgage borrower default equivalent to a minimum of the expected losses through its lender risk account after the exhaustion of the borrower’s equity and any primary mortgage insurance coverage, if required. If the participating member’s lender risk account is insufficient to cover any losses, then the supplemental mortgage insurance coverage is used. Only after exhausting the supplemental mortgage insurance coverage will the Seattle Bank absorb any potential losses. Under this credit enhancement structure, the value of a foreclosed property must fall below 50% of the outstanding mortgage loan balance to result in a loss to us. The following table sets out the credit-risk structure described above.

To date, all supplemental mortgage insurance has been underwritten by one mortgage insurance company. This company has the following claims-paying ability ratings: Standard & Poor’s, “AA,” Moodys, “Aa2,” Fitch, “AA+.” We monitor the claims-paying ability ratings of this insurance company as part of our overall credit rating monitoring processes. We have approved other mortgage insurance companies to supply supplemental mortgage insurance, but do not expect to utilize those companies because of our exit from the MPP.

Management of Interest-Rate and Prepayment Risk. The market value of the fixed interest-rate mortgage loans that we purchased changes as interest rates change. Typically, when interest rates rise, the market value of a fixed interest-rate mortgage loan depreciates, and as interest rates fall, the value of a fixed interest-rate mortgage loan appreciates. However, because borrowers can prepay the loans with no penalty, mortgage loans have inherent prepayment risk. Borrowers may prepay their mortgage loans for a variety of reasons, including refinancing their mortgage loans at a lower rate or sale of their homes. As a result of a borrower’s option to repay a mortgage loan at any time, the term of our investment in a mortgage loan is less predictable. We estimate the propensity of borrowers to prepay their mortgage loans using a third-party vendor prepayment model. The model

16

estimates, using a variety of market variables, the expected cash flows of the mortgage loans under various interest-rate environments.

Our primary method of managing interest-rate risk for our MPP portfolio is to finance the mortgage loans with fixed interest-rate consolidated obligation debt of varying terms and maturities to simulate the expected cash flows of the underlying mortgage loans. The market value of the fixed interest-rate debt typically appreciates when rates rise, moving in the opposite direction of the mortgage loans, which generally depreciate under a rising interest-rate environment. Likewise, the fixed interest-rate debt typically depreciates when rates fall, whereas the mortgage loans may appreciate in such an environment.

We manage prepayment risk by financing the mortgage loans with callable debt where we have the option to call or repay the debt prior to the stated maturity date with no penalty. We generally repay or refinance the callable debt when interest rates fall, mirroring the prepayment option held by the borrower. Likewise, the callable debt may be extended to its maturity date when interest rates rise.

We also enter into interest-rate exchange agreements, such as interest-rate caps, floors, and options to purchase interest-rate exchange agreements, or swaptions, to further limit the interest-rate and prepayment risk inherent in mortgage loans. When interest rates are volatile, the prepayment option in a mortgage loan is less predictable and therefore the value of a mortgage loan depreciates. We offset this volatility risk by issuing callable debt and purchasing swaptions or interest-rate caps or floors. Interest-rate caps and payer swaptions appreciate in value as interest rates rise and as interest-rate volatility increases, offsetting the decrease in market value of the mortgage loans. Interest-rate floors and receiver swaptions appreciate in value as interest rates fall and as interest-rate volatility increases, offsetting the prepayment risk of the mortgage loans, which increases when rates fall.

We manage and measure the interest-rate and prepayment risk exposures of the mortgage loans and the associated debt and other financial obligations on an overall basis with all other assets, liabilities, and other financial obligations. We use a variety of risk measurement methods and techniques, including duration of equity, key-rate duration-of-equity mismatch, convexity of equity, and market value of equity sensitivity. Each of these methods provides different analytical information that we use to manage our interest-rate risks. We take rebalancing actions based on a number of factors that include these measurement methods. For further discussion, see “Part II. Item 7A. Quantitative and Qualitative Disclosures About Market Risk.”

Although we utilized a variety of measures, including some of those described above, to manage both the interest-rate risk and the prepayment risk on the mortgage loans we purchased under the MPP, we were only partially successful in managing these risks. As we describe in more detail under “Part II. Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview—Historical Operations,” we did not successfully anticipate either the interest-rate volatility or the rapid rate of prepayments that we experienced in 2004 and 2003. The fact that the MPP exposed us to these risks accounted in part for the decline in our earnings in 2005 and 2004 and contributed to our decision to exit the MPP. The sale of $1.4 billion of government-insured mortgage loans in August 2005 reduced both our interest-rate risk and our prepayment risk on our mortgage loans held for portfolio.

Investments

We maintain a portfolio of short- and long-term-to-maturity investments for liquidity purposes and to generate income on member capital. Our liquidity portfolio consists of short-term investments issued by highly rated institutions. Our short-term investments generally include overnight and term federal funds, repurchase agreements, interest-bearing certificates of deposit, and commercial paper. We also maintain a longer-term investment portfolio, which includes consolidated obligations of other FHLBanks, securities issued by U.S. government agencies, and debentures and mortgage-backed securities that are issued by other GSEs or that carry the highest credit ratings from Moody’s or Standard & Poor’s. The U.S. government does not guarantee,

17

directly or indirectly, the consolidated obligations or other obligations of any of the FHLBanks, or the securities or debt obligations of other GSEs such as Fannie Mae and Freddie Mac.

The Seattle Bank does not have any specific policy covering the level of investments it may make in its members or their affiliates compared to nonmembers. In general, the Seattle Bank makes investment decisions as to securities of members and their affiliates in accordance with its policies applicable to all investments, which reflect the regulatory restrictions and the credit-risk management policies described below. For short-term investments only, our credit-risk management policies permit the Seattle Bank to require a higher standard of credit quality for nonmembers and affiliates of members than for members. For example, for short-term investments in nonmembers or affiliates of members we may require higher minimum long-term credit ratings than for counterparties that are members, and require nonmembers or affiliates of members to hold higher amounts of tier-one capital (or equivalent capital measurement) than counterparties that are members. The Seattle Bank believes that the difference in these criteria for short-term investments in members is justified by the fact that the Seattle Bank has a blanket security interest in certain assets of its members.

When we refer to mortgage-backed securities in this report, we mean both collateralized mortgage obligations and mortgage-backed pass-through securities. Mortgage-backed pass-through securities are securities issued by Fannie Mae, Freddie Mac, or Ginnie Mae. Collateralized mortgage obligations are mortgage-backed securities where the underlying pools of mortgage loans have been separated into different maturity classes. Collateralized mortgage obligations may be issued by the above GSEs, Ginnie Mae, or private issuers. When we refer to mortgage-based assets, we mean mortgage-backed securities as defined above, plus mortgage loans purchased through the MPP.

As of December 31, 2006, our long-term investment portfolio totaled $13.7 billion. The table below provides our investments by type and credit rating as of December 31, 2006.

| | | | | | | | | | | | |

| | | Long-Term Rating | | Total |

As of December 31, 2006 | | AAA or

Government

Agency | | AA | | Unrated | |

| (dollars in thousands) | | | | | | | | |

Consolidated obligation bonds of other FHLBanks | | $ | 4,224,959 | | $ | | | $ | | | $ | 4,224,959 |

Other U.S. agency obligations | | | 146,298 | | | | | | | | | 146,298 |

Government-sponsored enterprise obligations (excluding consolidated obligations of other FHLBanks and mortgage-backed securities)* | | | 2,661,622 | | | | | | 29,616 | | | 2,691,238 |

State or local housing investments | | | 4,987 | | | 7,080 | | | | | | 12,067 |

Mortgage-backed securities | | | 6,613,347 | | | | | | | | | 6,613,347 |

| | | | | | | | | | | | |

Total long-term investment securities | | $ | 13,651,213 | | $ | 7,080 | | $ | 29,616 | | $ | 13,687,909 |

| | | | | | | | | | | | |

Further detail of mortgage-backed securities | | | | | | | | | | | | |

Collateralized mortgage obligations: | | | | | | | | | | | | |

Fannie Mae | | | 666,378 | | | | | | | | | 666,378 |

Freddie Mac | | | 1,004,330 | | | | | | | | | 1,004,330 |

Private issuer | | | 4,826,508 | | | | | | | | | 4,826,508 |

| | | | | | | | | | | | |

Subtotal | | $ | 6,497,216 | | | | | | | | $ | 6,497,216 |

| | | | | | | | | | | | |

Mortgage-backed pass-through securities | | | | | | | | | | | | |

Fannie Mae | | | 91,761 | | | | | | | | | 91,761 |

Freddie Mac | | | 17,407 | | | | | | | | | 17,407 |

Ginnie Mae | | | 6,963 | | | | | | | | | 6,963 |

| | | | | | | | | | | | |

Subtotal | | | 116,131 | | | | | | | | | 116,131 |

| | | | | | | | | | | | |

Total mortgage-backed securities | | $ | 6,613,347 | | | | | | | | $ | 6,613,347 |

| | | | | | | | | | | | |

| * | These primarily include Fannie Mae and Freddie Mac debentures. |

18

Prohibited Investments. Under federal regulation, we are prohibited from investing in certain types of securities, including:

| | • | | instruments, such as common stock, that represent an ownership in an entity, other than stock in small business investment companies or certain investments targeted to low-income persons or communities; |

| | • | | instruments issued by non-U.S. entities, other than those issued by U.S. branches and agency offices of foreign commercial banks; |

| | • | | non-investment-grade debt instruments, other than certain investments targeted to low-income persons or communities and instruments that were downgraded after purchase by the Seattle Bank; |

| | • | | whole mortgages or other whole loans, other than: |

| | o | those acquired under the MPP, |

| | o | certain investments targeted to low-income persons or communities, |

| | o | certain marketable direct obligations of state, local, or tribal government units or agencies, having at least the second-highest credit rating from a nationally recognized statistical rating organization, or NRSRO, such as Moody’s or Standard & Poor’s, at the time of purchase, |

| | o | mortgage-based securities or asset-backed securities backed by manufactured housing loans or home equity loans, and |

| | o | certain foreign housing loans authorized under section 12(b) of the FHLBank Act; and |

| | • | | non-U.S. dollar denominated securities. |

Finance Board regulations further limit our investment in mortgage-backed securities and mortgage-related asset-backed securities (such as those backed by home equity loans or Small Business Administration loans) by requiring that the total book value of such securities owned by us not exceed 300% of our previous month-end capital on the day we purchase the securities. In addition, we are prohibited from purchasing:

| | • | | interest-only or principal-only mortgage-backed securities; |

| | • | | residual-interest or interest-accrual classes of collateralized mortgage obligations and real estate mortgage investment companies; and |

| | • | | fixed interest-rate or variable interest-rate mortgage-backed securities at interest rates equal to their contractual cap that, on the trade date, have average lives that vary by more than six years under an assumed instantaneous interest-rate change of 300 basis points. |

Additional Restrictions. Money market issuers and obligors must have long-term ratings of at least “A3” by Moody’s or “A-” by Standard & Poor’s and maintain certain capital measurements. Member bank counterparties must have a minimum long-term credit rating of “Baa” by Moody’s or “BBB-” by Standard & Poor’s and meet other capital measurements.

Our investments in direct obligations of U.S. government-sponsored agencies or instrumentalities other than the other FHLBanks are limited to the lower of 100% of our total capital or the issuer’s total capital.

Pursuant to a regulatory interpretation issued by the Finance Board in March 2005, the Finance Board clarified that it generally prohibits a FHLBank from purchasing any FHLBank consolidated obligation as part of the consolidated obligation’s initial issuance, either directly from the Office of Finance or indirectly through an underwriter. In 2004 and 2003, we purchased consolidated obligations of other FHLBanks with funds received primarily from the issuance of consolidated obligations on which we are the primary obligor and from accumulated cash from the maturity and nonrenewal of advances and the prepayment of mortgage-backed assets. By issuing debt with differing maturities and payment terms from the investments we were contemporaneously purchasing, we attempted to earn a favorable spread over our cost of funding on these investments. Nearly 90% of the aggregate amount of the consolidated obligations of other FHLBanks that we purchased was callable, but the debt issued contemporaneously was largely noncallable.

19