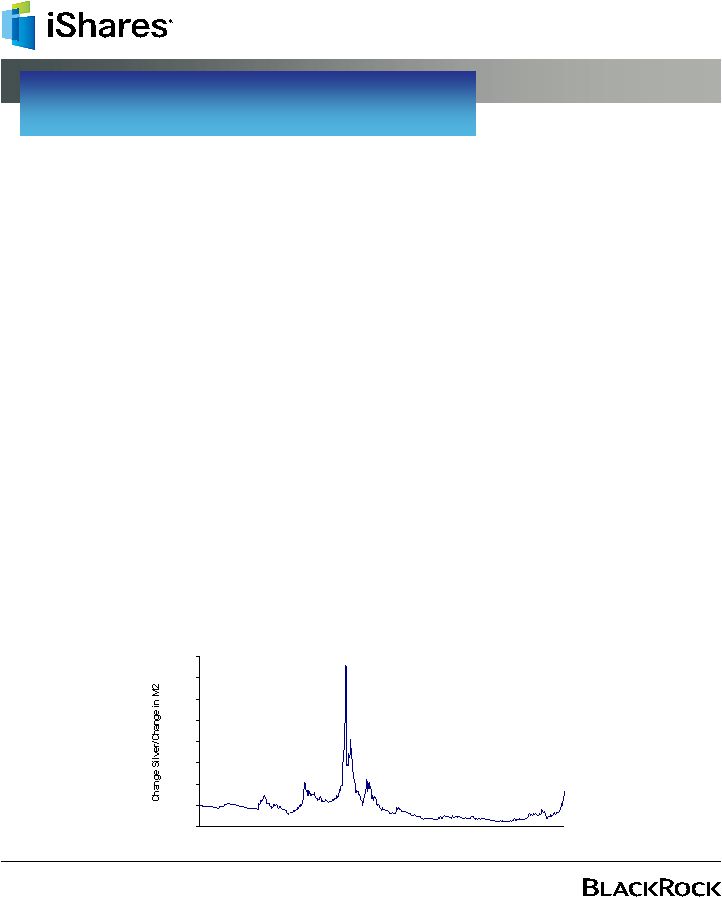

Silver Looking Tarnished? On Thursday, silver climbed above $48/ ounce, the highest level since January of 1980. Silver is now up 42% year-to-date after gaining over 80% in 2010. Since its 2008 lows, silver has gained roughly 400%. Despite a drop in recent days, silver looks very expensive from an historical standpoint. As we started the year recommending silver – a trade we suggested exiting in early March – we thought it would be useful to revisit the outlook. Our view is that given the fact that there does not appear to be any significant changes to the supply/demand balance and that the metal’s valuations look the most extended since the early 1980’s, we’re still very comfortable stepping aside from this trade. One of the reasons we first recommended silver back in December was silver’s economic applications. Roughly half the demand for silver, unlike gold, is tied to industrial uses. As we felt that economic growth would be decent in 2011, but core inflation would remain low, silver appeared to a better trade than gold, which is useful principally as an inflation or dollar hedge. What is interesting is that silver has posted stellar gains despite fairly mediocre growth. In most of the developed world, growth has generally slowed over the past quarter, in part due to rising oil prices. Economic activity cannot come close to explaining the spike in silver. This is particularly true when you consider that other economically sensitive industrial metals are flat to slightly down for the year. Free Writing Prospectus Filed Pursuant to Rule 433 Registration No. 333-170492 May 5, 2011 Investment Strategy Group Update 4 May 2011 If fundamentals are not driving silver, what is? Obviously investors are looking at the metal for more than its practical uses. This opens the question,“is silver in a bubble?” To a large extent, talking about commodity bubbles is a bit meaningless. Unlike stocks, bonds, or real-estate, commodities produce no cash-flow, so there is nothing to compare to price. In effect, commodities are worth whatever someone is willing to pay. That said, by the few objective measures you can use, silver appears very expensive. For example, one useful exercise is to compare the change in the price of a commodity against the change in the supply of money. Over the long-term, changes in price should bear some relationship to the amount of money in the economy, which is, in fact, the case. However, commodity prices can and do diverge from monetary conditions for considerable periods of time. From the mid 1980’s to as recently as late last year, silver prices had appreciated far less than the supply of money would have suggested. That situation has dramatically corrected itself over the past six months. Based on the ratio of the change in silver prices to the change in the money supply, silver has gone from close to ‘fair value’ in January to around 75% over-valued today. While silver reached much more stratospheric heights in the early 1980’s – in January of 1980 it appeared 750% over-valued based on changes in the money supply – the current reading is the most expensive in 30 years. by Russ Koesterich, Managing Director iShares Global Chief Investment Strategist Silver vs. US Money Supply 1959 to Present 0% 100% 200% 300% 400% 500% 600% 700% 800% Feb-59 Feb-65 Feb-71 Feb-77 Feb-83 Feb-89 Feb-95 Feb-01 Feb-07 Source: Bloomberg 4/28/2011 |

Investment Strategy Group Update To say that silver has momentum would obviously be a gross understatement. With the metal catching everyone’s attention, it is of little use forecasting a top. The fact that silver appears expensive provides no hard ceiling to how high the price can go. Over-the-counter stocks were clearly expensive in the summer of 1999, but that did not stop them from doubling over the next 6 months. What we can say is that there are no obvious fundamental catalysts to justify the recent spike and the metal appears very expensive based on several metrics. Given this dynamic, we’re still comfortable with our decision to step aside. For investors looking for precious metal exposure, we would prefer gold. ___________________________________________________ Russ Koesterich, CFA, is the iShares Global Chief Investment Strategist as well as the Global Head of Investment Strategy for BlackRock Scientific Active Equities. Russ initially joined the firm (originally Barclays Global Investors) in 2005 as a Senior Portfolio Manager in the US Market Neutral Group. Prior to joining BGI, Russ managed several research groups focused on quantitative and top down strategy. Another way to look at the relative value of silver is to compare it to something else, gold being a logical choice. Over the past forty years, silver has averaged roughly 1/55th the price of gold. While there have been significant variations – it has traded as high as 1/15th the price of gold and as low as 1/90th – the ratio has been relatively stable over the past thirty years. Today, silver trades at approximately 1/30th the price of gold, the most expensive relative to the yellow metal since 1980. Source: Bloomberg, 3/31/11 Ratio of Spot Gold to Silver 1971 to Present 0 20 40 60 80 100 120 Jan-71 Jan-76 Jan-81 Jan-86 Jan-91 Jan-96 Jan-01 Jan-06 Jan-11 |

iShares Silver Trust (the “Silver Trust”) has filed a registration statement (including a prospectus) with the SEC for the offering to which this communication relates. Before you invest, you should read the prospectus and other documents the Silver Trust has filed with the SEC for more complete information about the issuer and this offering. You may get these documents for free by visiting www.iShares.com or EDGAR on the SEC website at www.sec.gov. Alternatively, the Silver Trust will arrange to send you the prospectus if you request it by calling toll-free 1-800-474-2737. Investing involves risk, including possible loss of principal. The iShares Silver Trust is not an investment company registered under the Investment Company Act of 1940 or a commodity pool for purposes of the Commodity Exchange Act. Shares of the Silver Trust are not subject to the same regulatory requirements as mutual funds. Because shares of the iShares Silver Trust are expected to reflect the price of the silver held by the Silver Trust, the market price of the shares will be as unpredictable as the price of silver has historically been. Additionally, shares of the Silver Trust are bought and sold at market price (not NAV). Brokerage commissions will reduce returns. Shares of the Silver Trust are created to reflect, at any given time, the market price of silver owned by the trust at that time less the trust’s expenses and liabilities. The price received upon the sale of shares of the Silver Trust, which trade at market price, may be more or less than the value of the silver represented by them. If an investor sells the shares at a time when no active market for them exists, such lack of an active market will most likely adversely affect the price received for the shares. For a more complete discussion of risk factors relative to the Silver Trust, carefully read the prospectus. Following an investment in the iShares Silver Trust, several factors may have the effect of causing a decline in the prices of silver and a corresponding decline in the price of the shares. Among them: (i) A change in economic conditions, such as a recession, can adversely affect the price of silver. Silver is used in a wide range of industrial applications, and an economic downturn could have a negative impact on its demand and, consequently, its price and the price of the shares. (ii) A significant change in the attitude of speculators and investors towards silver. Should the speculative community take a negative view towards silver, a decline in world silver prices could occur, negatively impacting the price of the shares. (iii) A significant increase in silver price hedging activity by silver producers. Traditionally, silver producers have not hedged to the same extent as other producers of precious metals (gold, for example) do. Should there be an increase in the level of hedge activity of silver producing companies, it could cause a decline in world silver prices, adversely affecting the price of the shares. Shares of the iShares Silver Trust are not deposits or other obligations of or guaranteed by BlackRock, Inc., and its affiliates, and are not insured by the Federal Deposit Insurance Corporation or any other governmental agency. BlackRock Asset Management International Inc. (“BAMII”) is the sponsor of the Silver Trust. BlackRock Fund Distribution Company (“BFDC”), a subsidiary of BAMII, assists in the promotion of the Silver Trust. BAMII is an affiliate of BlackRock, Inc. When comparing commodities and the iShares Silver Trust, it should be remembered that the sponsor’s fee associated with the Trust is not borne by investors in individual commodities. Buying and selling shares of the iShares Silver Trust will result in brokerage commissions. Because the expenses involved in an investment in physical silver will be dispersed among all holders of shares of the Silver Trust, an investment in the Silver Trust may represent a cost-efficient alternative to investments in silver for investors not otherwise able to participate directly in the market for physical silver. Certain sectors and markets perform exceptionally well based on current market conditions. Achieving such exceptional returns involves the risk of volatility and investors should not expect that such results will be repeated. This material represents an assessment of the market environment at a specific time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any security in particular. ©2011 BlackRock Institutional Trust Company, N.A. All rights reserved. iShares is a registered trademark of BlackRock Institutional Trust Company, N.A. All other trademarks, servicemarks or registered trademarks are the property of their respective owners. iS-4678- 0511 |