UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2007

or

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to .

Commission File No. 001-33050

CBRE REALTY FINANCE, INC.

(Exact name of registrant as specified in its charter)

| | |

| Maryland | | 30-0314655 |

(State or other jurisdiction incorporation or organization) | | (I.R.S. Employer of Identification No.) |

185 Asylum Street, 31st Floor, Hartford, CT 06103

(Address of principal executive offices - zip code)

(860) 275-6200

(Registrant’s telephone number, including area code)

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

| | |

Title of Each Class | | Name of Each Exchange on Which Registered |

| Common Stock, $.01 Par Value | | New York Stock Exchange |

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer or a small reporting company. See the definitions of “large accelerated filer,” “accelerated filer,” “non-accelerated filer,” and “small reporting company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ¨ Accelerated filer x Non-accelerated filer ¨ Small reporting company ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No x

As of March 12, 2008, there were 30,920,225 shares of the Registrant’s common stock outstanding. The aggregate market value of common stock held by non-affiliates of the registrant at June 30, 2007, was $348,688,221. The aggregate market value was calculated by using the price at which our common stock was last sold, which was $11.89 per share on June 29, 2007.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the registrant’s Proxy Statement for the 2008 Annual Stockholders’ Meeting which are expected to be filed within 120 days after the close of the Registrant’s fiscal year are incorporated by reference into Part III of this Annual Report on Form 10-K.

CBRE REALTY FINANCE, INC.

INDEX

PART I

General

CBRE Realty Finance, Inc. was organized in Maryland on May 10, 2005, as a commercial real estate specialty finance company focused on originating and acquiring whole loans, bridge loans, subordinate interests in whole loans, or B Notes, commercial mortgage-backed securities, or CMBS and mezzanine loans, primarily in the United States. As of December 31, 2007, we also own interests in eight joint venture assets, two of which are consolidated in the consolidated financial statements and two direct real estate projects as a result of the foreclosure by us of two mezzanine loans. We commenced operations on June 9, 2005. We are a holding company and conduct our business through wholly-owned or majority-owned subsidiaries.

Unless the context requires otherwise, all references to “we,” “our,” and “us” in this annual report mean CBRE Realty Finance, Inc., a Maryland corporation, our wholly-owned and majority-owned subsidiaries and our ownership in joint venture assets and real estate projects.

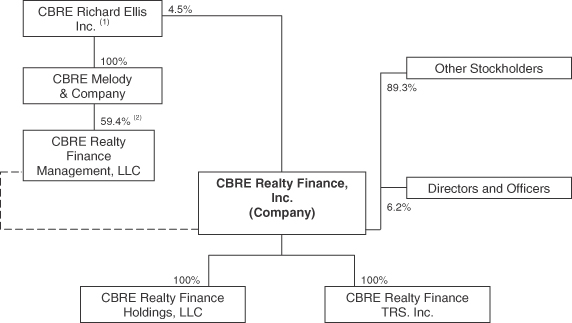

We are externally managed and advised by CBRE Realty Finance Management, LLC, our Manager, an indirect subsidiary of CB Richard Ellis Group, Inc., or CBRE, and a direct subsidiary of CBRE Melody & Company, or CBRE|Melody. As of December 31, 2007, CBRE|Melody also owned an approximately 4.5% interest in the outstanding shares of our common stock. In addition, certain of our executive officers and directors owned an approximately 6.2% interest in the outstanding shares of our common stock.

We have elected to qualify to be taxed as a real estate investment trust, or REIT, for U. S. federal income tax purposes commencing with our taxable year ended December 31, 2005. As a REIT, we generally will not be subject to U. S. federal income tax on that portion of income that is distributed to stockholders if at least 90% of our REIT taxable income is distributed to our stockholders. We conduct our operations so as to not be regulated as an investment company under the Investment Company Act of 1940, as amended, or the 1940 Act. We also conduct business through our wholly-owned taxable REIT subsidiary, or TRS, CBRE Realty Finance TRS, Inc.

Our objective is to grow our portfolio and provide attractive total returns to our investors over time through a combination of dividends and capital appreciation. Our business primarily focuses on originating, acquiring, investing in, financing and managing a diversified portfolio of commercial real estate related loans and securities. Our investment focus is on opportunities in North America.

Historically we have generally matched our assets and liabilities in terms of base interest rates (generally 30-day LIBOR) and expected duration. When markets permit, we generally issue collateralized debt obligations, or CDOs, which enable us to secure term financing and match fund our assets and liabilities to achieve our financing and return objectives.

During 2007, we experienced a number of changes due to company specific and industry wide developments and have taken actions to address such changes, which include: (i) in April 2007, we announced the resignation of our former CEO and President who was replaced in September 2007 by our current CEO and President, Kenneth J. Witkin, (ii) in May 2007, determined to focus on core operations and ceased making equity real estate investments through joint venture arrangements since we did not believe we were receiving appropriate value for such investments in the marketplace combined with the dilutive effect of such investments on our ability to pay dividends, and (iii) in July 2007, when concerns over the sub-prime residential markets began impacting liquidity and valuations in the commercial real estate market, we suspended new investment activity due to the uncertainty about our ability to secure short-term financing under repurchase agreements and long-term financing through the issuance of CDOs. As we await the credit and capital markets to improve and stabilize, our primary focus has been securing our liquidity by paying down outstanding repurchase agreements and managing our existing portfolio of assets to minimize credit risks.

1

The current credit and capital market environment is unstable and we continue to review and analyze the impact on potential avenues of liquidity. We are considering plans to restart our lending program and will resume origination activities when we are comfortable with the expected pricing of, and have reasonable access to, capital both in the debt and equity credit and capital markets that will enable us to achieve our growth objectives. We continue to explore equity and debt capital raising options as well as other strategic alternatives. As a result of the rapidly changing and evolving markets that continue to create challenges in our industry, we may experience: (i) lower loan originations and margins, (ii) reduced access to, and increased cost of, financing and (iii) as our portfolio is reduced by scheduled maturities and prepayments, reduced funds available for distribution as dividends.

As we continue to assess the impact of the credit and capital markets on our long-term business strategy, we have been primarily focused on actively managing our existing investment portfolio. As of December 31, 2007, the net carrying value of our investments was approximately $1.7 billion, including origination costs and fees and net of repayments and sales of partial interests in loans and CMBS, with a weighted average spread to 30-day LIBOR of 317 basis points for our floating rate investments and a weighted average yield of 7.10% for our fixed rate investments. Our portfolio is comprised solely of commercial real estate debt and equity investments with no sub-prime exposure. We have long-term financing in place through our first CDO issuance, which provides approximately $509.0 million of financing with an average cost of 30-day LIBOR plus 50.6 basis points and our second CDO issuance which provides $831.0 million of financing with an average cost of 90-day LIBOR plus 40.6 basis points. Our CDOs contain reinvestment periods of five years during which we can use the proceeds of loan repayments to fund new investments. As of December 31, 2007, we had approximately 3.2 years and 4.2 years remaining in our reinvestment period for our first and second CDO, respectively.

On December 31, 2007, we had approximately $163.0 million of cash and cash equivalents available, of which $26.0 million was unrestricted. We have long-term financing for 86% (95% at March 17, 2008) of our portfolio in place through our existing CDOs and mortgage loans. In order to effectively match-fund our investment portfolio, we have been aggressively reducing amounts outstanding under our repurchase facility with Wachovia Bank, N. A., or Wachovia. Liquidity is a measurement of our ability to meet potential cash requirements, including ongoing commitments to repay borrowings, fund loans and other investments, pay dividends, fund debt service and for other general corporate purposes. Our primary sources of funds for short-term liquidity, including working capital, distributions and additional investments consist of (i) cash flow from operations; (ii) proceeds from our existing CDOs; (iii) proceeds from principal payments on our investments; (iv) proceeds from potential loan and asset sales; and to a lesser extent (v) new financings or additional securitization or CDO offerings and (vi) proceeds from additional common or preferred equity offerings or offerings of trust preferred securities. We believe these sources of funds will be sufficient to meet our liquidity requirements.

Due to recent market turbulence, we do not anticipate having the ability in the near term to access equity capital through the public markets or debt capital through warehouse lines, new CDO issuances, or new trust preferred issuances. However, we continue to explore equity and debt capital raising options as well as other strategic alternatives. However, in the event we are not able to successfully secure financing, we will rely on cash flows from operations, principal payments on our investments, and proceeds from potential joint ventures and asset and loan sales to satisfy these requirements. If we (i) are unable to renew, replace or expand our sources of financing on substantially similar terms, (ii) are unable to execute asset and loan sales on time or to receive anticipated proceeds therefrom, (iii) fully utilize available cash or (iv) are unable to secure a joint venture on favorable terms or at all, it may have an adverse effect on our business, results of operations and our ability to make distributions to our stockholders.

Our current and future borrowings may require us, among other restrictive covenants, to keep uninvested cash on hand, to maintain a certain portion of our assets free from liens and to secure such borrowings with our assets. These conditions could limit our ability to do further borrowings. If we are unable to make required payments under such borrowings, breach any representation or warranty in the loan documents or violate any covenant contained in a loan document, our lenders may accelerate the maturity of our debt or require us to pledge more collateral. If we are unable to pay off our borrowings in such a situation, (i) we may need to

2

prematurely sell the assets securing such debt, (ii) the lenders could accelerate the debt and foreclose on our assets that are pledged as collateral to such lenders, (iii) such lenders could force us into bankruptcy, or (iv) such lenders could force us to take other actions to protect the value of their collateral. Any such event would have a material adverse effect on our liquidity and the price of our common stock.

Our relationship with CBRE provides us with the ability to leverage national and local market expertise and relationships, access to servicing platform, and with underwriting and asset management benefits. Our Manager has significant investment experience and access to a variety of resources, including:

| | • | | a market leading origination platform through CBRE|Melody, the mortgage origination and servicing subsidiary of CBRE and one of the largest real estate intermediaries in the U.S; |

| | • | | access to product and market information resulting from our Manager’s broad relationships with real estate owners and developers, financial institutions and tenants; |

| | • | | market knowledge and insights gained by the scope and expertise of CBRE’s mortgage origination, investment sales, leasing, property management and valuation, industry specialists and research divisions, as well as its mature infrastructure; and |

| | • | | a seasoned management team with significant experience in buying, manufacturing and financing commercial real estate investments, with an average of over 20 years of experience in all aspects of real estate lending, investment, management, finance, underwriting, origination, risk management, capital markets and structured finance. |

Pursuant to the management agreement dated as of June 9, 2005 between us, our Manager, CBRE|Melody and CBRE, the initial term expires on December 31, 2008 and the agreement automatically renews for one year terms subject to our Manager’s right to elect to not renew upon six months notice (June 30, 2008) prior to the expiration of the initial term and each annual renewal period thereafter. See “Management Agreement” section herein for further details. Through the initial term of our management agreement, our Manager and all its 28 employees will be solely dedicated to the operations of our company. Through at least the initial term of our management agreements, we will serve as the exclusive investment vehicle, subject to certain exceptions, sponsored by CBRE that focuses primarily on the acquisition and financing of commercial real estate loans, structured finance debt investments and CMBS.

3

The following chart illustrates the structure and ownership of our company as of December 31, 2007 and the management relationship between our Manager and us.

(1) | Excludes shares of common stock beneficially owned by Mr. Ray Wirta, our chairman of our board of directors, and Mr. Michael Melody, one of our directors |

(2) | The remainder is owned in the aggregate by our executive officers and certain other employees of CBRE|Melody |

Our Business Strategy

The current credit market environment is unstable and we continue to review and analyze the impact on potential avenues of liquidity. We have not entered into a new investment since July 2007. We are considering plans to restart our lending program and will resume origination activities when we are comfortable with the expected pricing of, and have reasonable access to, capital both in the debt and equity markets that will enable us to achieve our growth objectives. We continue to explore equity and debt capital raising options as well as other strategic alternatives.

Our business strategy is to, over time, generate a diversified portfolio of commercial real estate investments and leverage these investments to produce attractive total returns to our stockholders. Historically, we have sourced our investments through two primary channels: the affiliated CBRE system and our internal origination system. In each financing transaction we undertake, we seek to control as much of the capital structure as possible. We generally seek to accomplish this through the direct origination of whole loans and other investments, the ownership of which permits a wide variety of syndication and securitization executions. By providing a single source of financing to a borrower, we streamline the lending process, provide greater certainty to the borrower and retain the portion of the capital structure that will generate the most attractive and appropriate total returns based on our risk assessment of the investment.

The ability to manage our credit and real estate risks is a critical component of our success. We actively manage our portfolio by using our management team’s expertise in understanding the risk characteristics of an investment and, wherever possible, proactively managing the credit risk of investments in our portfolio. We

4

benefit from our access to information resulting from our affiliation with CBRE. We generate income principally from the spread between the yields on our assets and the cost of our borrowing and hedging activities. Future distributions and capital appreciation are not guaranteed, however, and we have only limited operating history and REIT experience upon which you can base an assessment of our ability to achieve our objectives.

Our Financing Strategy

General Policies.Our financing strategy historically focused on the use of match-funded financing structures. This means that we seek to match the maturities and/or repricing schedules of our financial obligations with those of our investments to minimize the risk that we have to refinance our liabilities prior to the maturities of our assets and to reduce the impact of changing interest rates on earnings. As of December 31, 2007, approximately 86% (95% at March 17, 2008) of our portfolio was match-funded. Over the long-term, we intend to finance the acquisition of our investments primarily by borrowing against or leveraging our existing portfolio and using the proceeds to acquire additional investments. We may, if available, from time to time utilize proceeds from equity and/or debt offerings or other forms of debt financing. Our leverage policy permits us to leverage up to 80% of the total value of our assets. Our charter and bylaws do not limit the amount of indebtedness we can incur, and our board of directors has discretion to deviate from or change our indebtedness policy at anytime. As of December 31, 2007, 80.4% of our assets by carrying value were levered. We use leverage for the sole purpose of financing our portfolio and not for the purpose of speculating on changes in interest rates.

Warehouse Facilities. Over the long-term, we intend to use short-term financing, in the form of warehouse facilities. Warehouse lines are typically collateralized loans made to borrowers who invest in securities and loans that in turn pledge the resulting securities and loans to the warehouse lender. As of December 31, 2007, we did not have a facility in place that allowed for additional short-term borrowings.

Collateralized Debt Obligations. We intend to use long-term financing, in the form of securitization structures, particularly CDOs, as well as other match-funded financing structures. We believe CDO financing structures are an appropriate financing vehicle for our targeted real estate asset classes because they will enable us to obtain long-term match-funded cost of funds and minimize the risk that we have to refinance our liabilities prior to the maturities of our investments while giving us the flexibility to manage credit risk and, subject to certain limitations, to take advantage of profit opportunities. As of December 31, 2007, we had issued two CDO transactions totaling approximately $1.3 billion, which provide attractive long-term financing. As noted previously, there has been reduced liquidity in the CDO market and little appetite for new issuances. While we believe the CDO market has solid long-term fundamentals, we are unable to predict when the market will return and to what degree underwriting standards will change.

Term Debt. We intend to explore term financing from bank lenders that is secured by commercial real estate loans, securities or properties. We anticipate using secured leverage to enhance returns on investments. However, there is no assurance that such financing will be available.

Preferred Equity. We may explore financing from preferred equity. We anticipate using any preferred equity proceeds to preserve our liquidity and enhance returns on investments. However, there is no assurance that such financing will be available.

Our Investment Portfolio

Our investments target the following asset classes:

| | • | | Subordinated interests in first mortgage real estate loans, or B Notes; |

5

| | • | | Mezzanine loans related to commercial real estate that is senior to the borrower’s equity position but subordinated to other third-party financing; and |

| | • | | Commercial mortgage-backed securities, or CMBS. |

As of December 31, 2007, our investment portfolio (excluding our two direct real estate assets) of approximately $1.7 billion in assets, including origination costs and fees, and net of repayments and sales of partial interests in loans consisted of the following:

| | | | | | | | | | | | | | | | | | |

Security Description | | Carrying

Value | | | Number of

Investments | | Percent of Total

Investments | | | Weighted Average | |

| | | | | Coupon | | | Yield to

Maturity | | | LTV | |

| | | (In thousands) | | | | | | | | | | | | | | | |

Whole loans(1) | | $ | 881,089 | | | 41 | | 52.3 | % | | 6.78 | % | | 6.58 | % | | 69 | % |

| | | | | | |

B Notes | | | 218,317 | | | 11 | | 13.0 | % | | 7.96 | % | | 8.29 | % | | 67 | % |

| | | | | | |

Mezzanine loans | | | 282,297 | | | 14 | | 16.8 | % | | 9.70 | % | | 9.41 | % | | 73 | % |

| | | | | | |

CMBS | | | 236,134 | | | 67 | | 14.0 | % | | 5.99 | % | | 7.17 | % | | — | |

| | | | | | |

Joint venture investments(2) | | | 66,023 | | | 8 | | 3.9 | % | | — | | | — | | | — | |

| | | | | | | | | | | | | | | | | | |

Total investments | | $ | 1,683,860 | | | 141 | | 100.0 | % | | | | | | | | | |

| | | | | | |

Loan loss reserve | | | (19,650 | ) | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

Total investments, net | | $ | 1,664,210 | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | |

(1) | Includes originated whole loans, acquired whole loans and bridge loans. |

(2) | Includes our equity investment in two limited liability companies which are deemed to be variable interest entities, or VIEs, which we consolidate in our audited financial statements because we are deemed to be the primary beneficiary of these VIEs under Financial Accounting Standards Board Interpretation No. 46R, or FIN 46R. |

Our investment guidelines require us to maintain a geographically diverse portfolio of assets. Our investment focus is on opportunities in North America. Our board of directors may change these guidelines or investment focus at any time without the approval of our stockholders. As of December 31, 2007, our investment portfolio (excluding our two direct real estate assets) consisted of assets primarily located in four regions of the U.S., as defined by the National Council of Real Estate Investment Fiduciaries, or NCREIF, with approximately 30.0% of our investments located in the East, approximately 9.0% in the South, approximately 47.0% in the West and approximately 8.0% in the Midwest. The remaining 6.0% of our investments were located throughout the U.S.

The following is a more detailed description of each of our target asset classes:

Whole Loans. Commercial mortgage loans, or whole loans, are structured to either permit us to retain the entire loan, or to sell or securitize the lower yielding senior portions of the loans and retain the higher yielding subordinate investment or to contribute the entire loan to our CDOs. Typically, borrowers of these loans are institutions and well-capitalized real estate operating companies and investors. These loans are secured by commercial real estate assets in a variety of industries with a variety of characteristics. We expect to originate both fixed and floating rate loans and we expect to hold these investments to maturity. Our primary focus initially is commercial properties in the office, retail, hotel, industrial and apartment sectors.

Historically, we have also acquired seasoned loans in the secondary market secured by single assets and portfolios of performing and sub-performing loans originated by third-party lenders such as banks, life insurance companies and other owners. These loans are secured by commercial properties throughout the U.S.

6

If we anticipate selling the senior portion of our commercial mortgage loans, we will fund the purchase of the loan either through or jointly with our TRS. In instances where we originate or purchase the commercial mortgage loans jointly with our TRS, we will retain the subordinate portion for our own account and our TRS will sell the senior portion. If we purchase the commercial mortgage loans through our TRS, the TRS will sell the subordinate piece of the loan to us at fair market value determined based on arms length dealing, and the TRS will sell the senior piece to third parties. Our TRS will be subject to corporate income tax on any taxable gain recognized by it on the sale of loans to us or to third parties and on its other taxable income. If we anticipate holding a commercial mortgage loan for our own account, we will generally fund the purchase of the loan without funding by our TRS. We and our TRS intend to use warehouse facilities, if available, to provide short-term funding for our third-party loan purchases.

Subject to maintaining our qualification as a REIT, we historically have also offered bridge loans to borrowers who are seeking short-term capital (that is, less than five years) to be used in the acquisition, construction or redevelopment of a property. Typically, the borrower has identified a property in a favorable market that it believes to be poorly managed or undervalued. Bridge financing enables the borrower to secure short-term financing while improving the property and avoid burdening it with restrictive long-term debt. The bridge loans we originate will be predominantly secured by first mortgage liens on the property and we expect to hold these investments to maturity. We believe our bridge loans will lead to additional financing opportunities in the future, as bridge facilities are often a first-step toward permanent financing or a sale.

As of December 31, 2007, we had invested $881.1 million on a carrying value basis, or 52.3% of our total investments in whole loans. None of the whole loans we made investments in were in default at the time of purchase or were in default as of December 31, 2007. However, we may in the future invest in whole loans or seasoned loans that may be in default. As of December 31, 2007, one whole loan investment with a carrying value of $11.9 million was on our watch list and this whole loan went into default in January 2008, which is described further in Item 7 “Management’s Discussion and Analysis of Financial Condition – Risk Management” of this report.

Subordinate Interests in Whole Loans (B Notes). Historically, we have purchased from third parties and have retained, and in the future may retain, from whole loans we originated and securitized or sold, subordinate interests referred to as B Notes. B Notes are loans secured by a first mortgage and subordinated to a senior interest, referred to as an A Note. The subordination of a B Note is generally evidenced by a co-lender or participation agreement between the holders of the related A Note and the B Note. In some instances, the B Note lender may require a security interest in the stock or partnership interests of the borrower as part of the transaction. B Note lenders have the same obligations, collateral and borrower as the A Note lender, but typically are subordinated in recovery upon a default. B Notes share certain credit characteristics with second mortgages, in that both are subject to the greater credit risk with respect to the underlying mortgage collateral than the corresponding first mortgage or A Note. If we originate first mortgage loans, we may divide them, securitizing or selling the A Note and keeping the B Note for investment. In instances where we divide a first mortgage loan, we will fund the origination of the loan either through or jointly with our TRS. If we originate the first mortgage loan jointly with our TRS, we will retain the B Note for investment and our TRS will sell the A Note. If we originate the first mortgage loans through our TRS, the TRS will sell the B Note to us for investment at fair market value determined based on arms length dealing, and the TRS will sell the A Note to a third party. We may also pay our TRS a fee for the origination services provided by it for the B Notes we acquire for our loan portfolio. Any fee we pay to our TRS for loan origination will be market-based and consistent with fees that would be earned with the origination of mortgage loans on behalf of third parties. Our TRS will be subject to corporate income tax on any taxable gain recognized by it on the sale of B Notes or A Notes to us or to third parties and on its other taxable income.

When we acquire and/or originate B Notes, we may earn income on the investment, in addition to the interest payable on the B Note, in the form of fees charged to the borrower under that note or by receiving principal payments in excess of the discounted price (below par value) we paid to acquire the note. When we originate a B Note out of a whole loan and then sell the A Note through our TRS, we will have to allocate the basis in the whole loan to the two (or more) components to reflect the fair market value of the new instruments.

7

Our TRS may realize a profit on the sale if the allocated value is below the sale price. Our TRS will be subject to corporate income tax on any taxable gain recognized by it on such sales as well as its other taxable income.

Our ownership of a B Note with controlling class rights may, in the event the financing fails to perform according to its terms, cause us to elect to pursue our remedies as owner of the B Note, which may include foreclosure on, or modification of, the note. In some cases the owner of the A Note may be able to foreclose or modify the note against our wishes as holder of the B Note. As a result, our economic and business interests may diverge from the interests of the holders of the A Note. These divergent interests among the holders of each investment may result in conflicts of interest. We expect to hold B Notes to their maturity. We generally structure or acquire B Notes with unilateral foreclosure rights on the underlying mortgage.

As of December 31, 2007, we had invested $218.3 million on a carrying value basis, or 13.0% of our total investments in B Notes. As of December 31, 2007, one B-Note with a carrying value of $42.8 million was in default, which is described further in Item 7 “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Risk Management” of this report.

Mezzanine Financing. Historically, we have invested in mezzanine loans that are senior to the borrower’s common and preferred equity in, and subordinate to a first mortgage loan on, a property. These loans are secured by pledges of ownership interests, in whole or in part, in entities that directly or indirectly own the real property.

Mezzanine loans may have elements of both debt and equity instruments, offering the fixed returns in the form of interest payments and principal payments associated with senior debt, while providing lenders an opportunity to participate in the capital appreciation of a borrower, if any, through an equity interest. Due to their higher risk profile, and often less restrictive covenants, as compared to senior loans, mezzanine loans generally earn a higher return than senior secured loans. Mezzanine loans also may include a “put” feature, which permits the holder to sell its equity interest back to the borrower at a price determined though an agreed upon formula.

We historically have structured our mezzanine loans so that we receive a stated fixed or variable interest rate on the loan. In addition, at times we may also receive a percentage of gross revenues and a percentage of the increase in the fair market value of the property securing the loan, payable upon maturity, refinancing or sale of the property. Our mezzanine loans also generally have prepayment lockouts, penalties, minimum profit hurdles and other mechanisms to protect and enhance returns in the event of premature repayment. Mezzanine loans have maturities that match the maturity of the related mortgage loan but may have shorter or longer terms. We expect to hold these investments to maturity. We expect to hold certain of our mezzanine investments in our TRS.

As of December 31, 2007, we had invested $282.3 million on a carrying value basis, or 16.8% of our total investments in mezzanine financing. As of December 31, 2007, one mezzanine investment with a carrying value of $40.0 million was on our watch list and this mezzanine investment went into default in February 2008, which is described further in Item 7 “Management’s Discussion and Analysis of Financial Condition— Risk Management” of this report.

Commercial Mortgage-Backed Securities. Historically, we have acquired CMBS that are created when commercial loans are pooled and securitized. These securities may or may not be rated investment grade by rating agencies. We may originate CMBS from pools of commercial loans we assemble, in which event we expect to retain the more junior assets. We expect a majority of our CMBS investments to be rated by at least one nationally-recognized rating agency, and to consist of securities that are part of a capital structure or securitization where the rights of such class to receive principal and interest are subordinated to senior classes but senior to the rights of lower rated classes of securities. We intend to invest in CMBS that will yield high current interest income and where we consider the return of principal to be likely.

CMBS are generally pass-through certificates that represent beneficial ownership interests in common law trusts whose assets consist of defined portfolios of one or more commercial mortgage loans. CMBS are secured

8

by or evidenced by ownership interests in a single commercial mortgage loan or a pool of mortgage loans secured by commercial properties. They are typically issued in multiple tranches whereby the more senior classes are entitled to priority distributions from the trust’s income to make specified interest and principal payments on such tranches. Losses and other shortfalls from expected amounts to be received on the mortgage pool are borne by the most subordinate classes, which receive payments only after the more senior classes have received all principal and/or interest to which they are entitled.

The yields on CMBS depend on the timely payment of interest and principal due on the underlying mortgage loans and defaults by the borrowers on such loans may ultimately result in deficiencies and defaults on the CMBS. In the event of a default, the trustee for the benefit of the holders of CMBS has recourse only to the underlying pool of mortgage loans and, if a loan is in default, to the mortgaged property securing such mortgage loan. After the trustee has exercised all of the rights of a lender under a defaulted mortgage loan and the related mortgaged property has been liquidated, no further remedy will be available. However, holders of relatively senior classes of CMBS will be protected to a certain degree by the structural features of the securitization transaction within which such CMBS were issued, such as the subordination of the relatively more junior classes of the CMBS. Historically, we have invested in investment grade and subordinate classes of CMBS, including BBB-rated, BB-rated, B-rated and non-rated classes. We expect to hold CMBS securities to maturity.

As of December 31, 2007, we had invested $236.1 million on a carrying value basis, or 14.0% of our total investments in CMBS. For the year ended December 31, 2007, 1% of our CMBS, based on carrying value, has been downgraded and 6% has been upgraded by nationally recognized statistical rating agencies, such as Standard and Poor’s Rating Service, Fitch Ratings and Moody’s Investors Services, Inc. In the second half of 2007 and beginning of 2008, the CMBS market has experienced significant declines in value and significantly lower trading volumes.

Joint Venture Investments. In 2007, we elected to discontinue seeking new joint venture investments in favor of focusing on our core whole loan, B-notes, Mezzanine and CMBS investments. We continue to actively manage our existing joint venture portfolio.

Certain of our joint venture investment holdings involve the development, redevelopment or re-tenanting of all or a portion of the real estate assets owned by the joint venture. These investments will initially provide a low current dividend or yield, or no current dividend or yield, on our invested equity compared to the dividend or yield that is projected upon stabilization of the underlying real estate assets. Therefore, these assets are likely to have a dilutive effect on our cash flows and results of operations in the short to intermediate term and therefore could affect our ability to make current distributions to our stockholders. If these investments perform according to our expectations, they would be accretive to our cash flow and results of operations once the underlying assets of the joint venture investment are stabilized or are sold or refinanced. However, there can be no assurance as to the successful performance of these joint venture investments.

As of December 31, 2007, we had invested approximately $77.2 million in joint venture investments which, after recognition of depreciation and operating losses, have a carrying value of $66.0 million, or 3.9% of our total investments. Included in this total is our equity investment in two limited liability companies that are deemed to be VIEs that we consolidate in our audited financial statements because we are deemed to be the primary beneficiary of these VIEs under FIN 46R.

Other Real Estate-Related Investments. We also may make investments in other types of commercial real estate assets. These may include acquisitions of real property, net leased property, distressed and stressed debt securities, RMBS, CDOs and equity and debt issued by REITs or other real estate companies. We have authority to issue our common stock or other equity or debt securities in exchange for property. Subject to gross income and asset tests necessary for REIT qualification, we may also invest in securities of other REITs, or other entities engaged in real estate activities or securities of other issuers, including for the purpose of exercising control over such entities.

9

Some of these investments may be equity interests in properties with no stated maturity or redemption date, or long-term leasehold interests with expiration dates as long as 40 years beyond the date of our investment. We expect that we would hold these investments for between several months and up to ten years, depending upon the risk profile of the investment and our investment rationale. The timing of our sale of these investments, or of their repayment, is frequently tied to certain events involving the underlying property, such as new tenants or superior financing.

As of December 31, 2007, we had one investment in other real estate-related investments. The investment was in a CDO bond with a carrying value of $3.3 million, which we included in our CMBS carrying amount of $236.1 million. As of December 31, 2007, we had direct real estate ownership interests in our Rodgers Forge and Monterey properties.

Sourcing Potential Investment Opportunities

We recognize that investing in our targeted asset classes is highly competitive, and that we compete with many mortgage REITs, other specialty finance companies, private equity and other discretionary funds and other lenders for profitable investment opportunities. Given this competitive environment, it is important for us to have access to the broadest supply of new investment and finance opportunities, which we refer to as our gross origination flow, so that we can be highly selective in those opportunities that we decide to pursue. Historically, we have sourced our investment opportunities through two primary channels: the affiliated CBRE system and our internal origination system. As we continue to monitor the credit and capital markets and look for opportunities to start making new investments, we will continue to leverage these channels where possible and seek additional sourcing opportunities.

Affiliated CBRE System. We believe that CBRE|Melody has one of the strongest and most active origination systems in the U.S. We believe our affiliation with CBRE and CBRE|Melody is an advantage for us in sourcing, analyzing and managing investments across all of our product types. All of our Manager’s investment professionals have direct and substantial interaction with sales, leasing and financing brokers within CBRE and CBRE|Melody. As a result, we are introduced to numerous investment opportunities.

Our Internal Origination System. Our management team’s deep experience in all aspects of real estate lending, investment, capital markets and management also provides us with a valuable origination system. Over the years, our management team has developed extensive relationships with borrowers, sellers of whole loans, various financial institutions and other financial intermediaries throughout the U.S. These relationships provide us with a broad range of investment and finance opportunities, including seasoned loans, purchased securities and private equity. The depth and diversity of these relationships will provide us with investment and finance opportunities across all major product types and markets.

Our Investment Process

In evaluating potential investments, our Manager employs an active five-step investment process consisting of:

Information Research. Our Manager continuously monitors the property, credit and capital markets to adjust its investment strategy seeking to optimize the performance of our portfolio. We believe we have strong research capabilities due to the resources and activities of CBRE. We have access to all property market and economic data research produced by CBRE and provided to its clients. In addition, we have direct access to CBRE’s leasing, sales, property management, appraisal and industry specialists, which provides us with additional market and property specific information. We have developed a proprietary database to capture this information and provide our management team with a very effective tool for refining our investment strategies and goals. We utilize the information provided by CBRE and its affiliates as well as a variety of independent sources to refine our strategy. Some of the key elements we generally focus on are:

| | • | | fundamental supply and demand characteristics of markets; |

10

| | • | | performance characteristics of all property types; |

| | • | | macro-economic trends and local market; |

| | • | | quotes on various structures and products; |

| | • | | market makers and leaders; |

Once we identify our target markets and borrowers/partners in those markets, we conduct a second level of research including: detailed information on the borrower/partner, leasing and sales comparables by product type in each market, recent financing quotes and market specific capital flows. This approach allows us to focus on investment opportunities that are best for us and fall within our investment guidelines. To limit due diligence costs, all potential investments that fall within our investment guidelines are reviewed by our investment committee, prior to the decision to pursue such an investment, for overall compatibility with our investment portfolio.

Screening and Pursuit of Potential Transactions. When we have identified a potential transaction, we analyze it to determine if the particular investment meets our stated objectives. We review the potential investment to determine its risk/return profile and how it would fit within our overall portfolio. Our goal is to quickly determine if we should pursue a potential investment. To make the determination at this stage requires a comprehensive review of the materials provided by the borrower concerning itself and its assets, quick analysis of the market in which the investment is located and our own modeling of the property’s projected financial performance.

When we identify an investment opportunity that warrants continued review and resources, the investment is placed on our “Pipeline Report.” Once placed on the report, we will prepare a written summary of the transaction for the investment committee. The purpose of the brief is to introduce the opportunity to the investment committee and seek its initial guidance. The brief will include review of the following elements:

| | • | | the borrower’s reputation, credit and payment performance; |

| | • | | an initial review of the asset, including market analysis, property valuation, risk assessment and physical examination; |

| | • | | consideration of environmental, structural and zoning factors; |

| | • | | the proposed transaction structure; |

| | • | | initial financial modeling; and |

| | • | | initial REIT and 1940 Act compliance. |

We believe that this approach allows us to be responsive to prospective borrowers, clients and partners while enabling us to stay focused on which potential investments will best help us accomplish our goals. Once the investment committee agrees to place the prospective investment on its “Pipeline Report,” we will then begin a more detailed and thorough underwriting and due diligence.

Thorough Underwriting and Due Diligence. Following the decision to pursue an investment, each potential transaction, whether a single asset or a portfolio of assets, is subject to a review of the underlying real estate

11

collateral, the borrower and the associated debt/equity structure. Our Manager has developed a rigorous and disciplined review approach that allows us to determine whether a prospective investment can achieve our targeted returns. From a real estate perspective, the due diligence includes, but is not limited to:

| | • | | conducting a thorough analysis, regardless of the recourse nature of a loan, of the borrower’s investment history, reputation, credit history, investment focus and expertise; |

| | • | | making site visits to assess the economic viability of the collateral including tenant and overall property viability; |

| | • | | reviewing submarket supply and demand and existing and planned competitive properties; |

| | • | | reviewing local submarket rental and sales comparables; |

| | • | | reviewing issuer and third party valuations and appraisals of the property, if applicable, and the LTV ratio with respect to the collateral; |

| | • | | performing in-depth legal, accounting, environmental, zoning, structural analyses of the property and borrower; |

| | • | | reviewing the level and stability of cash flow from the underlying collateral to service the mortgage debt; |

| | • | | analyzing the availability of capital for refinancing by the borrower if the loan does not fully amortize; |

| | • | | reviewing loan documents to determine the lender’s rights, including personal guarantees, additional collateral, default covenants and other remedies as well as the lender’s rights under any intercreditor agreements; and |

| | • | | making appropriate modifications to reflect the underlying collateral and borrower credit risk, including requiring letters of credit or other liquid instruments to ensure timely payments and loan to value ratios appropriate for the yield. |

Additionally, all investments are considered in the context of their risk and yield profile, reviewing such factors as match-funding and hedging efficiency and overall concentration considerations, such as investment size, product type, tenants, borrower, sector, floating vs. fixed rates and maturity. Our focus is on risk management and understanding the impact of any investment on our investment portfolio prior to closing.

As a result of this extensive real estate review, a cash flow forecast for each collateral property is prepared, and a valuation is assigned. The performance of the respective investment is then forecasted to derive the projected return. Sensitivity analyses are performed in consideration of differing levels of the property’s cash flow, loan losses, variances in the timing of loan payoffs or prepayments, loan extension scenarios and changing interest rates. In all cases, we consider the potential impact on the risk profile of our investment portfolio and the impact on cash flow after we implement financing at the company level, whether in the form of a CDO or some other debt instrument.

Upon completion of due diligence, we consider the impact of any material findings on the transaction’s risk profile. Once final due diligence is substantially complete, the investment professionals prepare and submit a final investment committee brief to the investment committee, which consists of Messrs. Ray Wirta, our chairman, Michael Melody, a director, David Marks, a director, Kenneth J. Witkin, our chief executive officer, president and a director, and four other representatives of our Manager.

Investment Committee Approval. The investment committee will review the final investment committee brief prepared by our Manager and decide to approve or decline the investment. Should the investment be approved, we will move to close the investment or financing with the assistance of legal, accounting, tax and other specialists appropriate for that particular investment.

All transactions are reported to our board of directors. Our investment committee consults regularly with our board of directors, the executive committee of our board of directors, and various CBRE and CBRE|Melody

12

professionals to understand and take advantage of the latest available market information and trends. The majority vote (which must include the affirmative vote of our chief executive officer) of all members of our investment committee is required to approve all investments and dispositions, including investments and dispositions of up to $25 million (except for (i) investments and dispositions having credit ratings of “A” or better by a major rating agency, such threshold will be up to $50 million and (ii) with respect to aggregate CMBS investments of up to $15 million having credit ratings of “B” or better and consistent with our operating guidelines, only two members of the investment committee must approve the investment; however, the majority vote of all members of our investment committee will be required to approve aggregate CMBS investments over $15 million). Separate approvals by our executive committee and our board of directors are not required under the following circumstances. Our executive committee, which consists of Messrs. Ray Wirta, our chairman, Michael Melody, a director, David Marks, a director, and Kenneth J. Witkin, our chief executive officer, president and a director, has the authority delegated by our board of directors to authorize transactions consistent with our investment guidelines and must approve, by a majority vote (which must include the affirmative vote of the independent director), investments and dispositions aggregating greater than $25 million and up to $50 million (except for investments and dispositions having credit ratings of “A” or better by a major rating agency, such threshold will be greater than $50 million and up to $75 million). A majority of the members of our board of directors must approve all investments and dispositions greater than such amounts identified above.

Closing. The closing process is extensive due to the documentation associated with all of our investment products. Non-CMBS closings are completed, to the extent possible, on our own standard documentation. Those documents are negotiated by our Manager with the support of one of our executive vice presidents and outside counsel.

Asset Management and Servicing

With respect to managing the investments made by us, our Manager (with the assistance of GEMSA Loan Services, L.P., or GEMSA, a joint venture between CBRE|Melody and GE Capital Real Estate) or a third party (as servicer where appropriate) seeks to address the following issues:

| | • | | Investment Monitoring. Our Manager actively monitors and manages our investments. Our Manager’s asset managers have been trained to identify asset level risks early and to take measures to mitigate those concerns. Our management team reviews our portfolio quarterly on a formal basis and more frequently, on an informal basis, to consider any “early watch list,” “watch list,” or “non-performing” assets and determine any appropriate actions and reserve strategies. Assets are managed aggressively through maturity. |

| | • | | Cash Collections. When we originate a new loan, we evaluate whether it is appropriate to require a lock box agreement (or cash management account), based on certain criteria, such as the debt service coverage ratio, LTV ratio and quality of sponsorship. As determined appropriate, we will require the borrower to establish a cash management account at a commercial bank acceptable to us. Tenants will be required to deposit all rents, revenues and receipts with respect to the property into the cash management account. Generally, the debt service, loan escrows and reserves are paid from this account, and any balance remaining is remitted to the borrower. |

| | • | | Collateral Valuation. Our Manager is responsible for determining the value of the collateral property, including an analysis of the condition of the property, existing tenant base, current information and comparable market rents, occupancy and sales. When appropriate, our Manager also conducts an investigation of the borrower to identify other potential sources of recovery, including other non-real estate collateral and guarantees. Our Manager is also responsible for reviewing the collateral operating statements on an ongoing basis and within the market in order to accurately track asset value and its cash flow performance. |

| | • | | Recovery Strategies. To the extent a default is realized with respect to an investment, our Manager is responsible for recommending and implementing the appropriate recovery strategy in order to produce |

13

| | the highest present value recovery. Our management team’s real estate operating and distressed debt workout management experience put us in a strong position to manage problems that may arise. We may also utilize a special servicer, which in some instances, where appropriate, may be an affiliate of us, CBRE or CBRE|Melody (including GEMSA), to manage, modify and resolve loans and other investments that fail to perform under the terms of the loan agreement, note, indenture, or other governing documents. Special servicers are most frequently employed in connection with whole loans, B Notes and first-loss classes of CMBS. For the years ended December 31, 2007 and 2006, we paid or had payable an aggregate of approximately $251,000 and $82,000, respectively, in fees to GEMSA in its capacity as a special servicer to our company. |

Our Operating Policies

Our Investment and Borrowing Guidelines. We have adopted general guidelines for our investments and borrowings to the effect that:

| | • | | no investment will be made that would cause us to fail to qualify as a REIT for U.S. federal income tax purposes; |

| | • | | no investment will be made that would cause us to be regulated as an investment company under the 1940 Act; |

| | • | | no more than 25% of our equity, determined as of the date of such investment, will be invested in any single asset; |

| | • | | no more than 25% of our equity, determined as of the date of such investment, will be invested in any single borrower; |

| | • | | our leverage will generally not exceed 80% of the value of our assets, in the aggregate; |

| | • | | the majority vote (which must include the affirmative vote of our chief executive officer) of all members of our investment committee will be required to approve all investments and dispositions, including investments and dispositions of up to $25 million (except for (i) investments and dispositions having credit ratings of “A” or better by a major rating agency, such threshold will be up to $50 million and (ii) with respect to aggregate CMBS investments of up to $15 million having credit ratings of “B” or better and consistent with our operating guidelines, only two members of the investment committee must approve the investment; however, the majority vote of all members of our investment committee will be required to approve aggregate CMBS investments over $15 million); the majority vote (which must include the affirmative vote of the independent director) of our executive committee will be required to approve investments and dispositions aggregating greater than $25 million and up to $50 million (except for investments and dispositions having credit ratings of “A” or better by a major rating agency, such threshold will be greater than $50 million and up to $75 million); and a majority of our board of directors must approve all investments and dispositions greater than such amounts identified above; and |

| | • | | we will maintain a portfolio of geographically diverse assets. |

Our Manager is required to seek the approval of a majority of the independent members of our board of directors before we engage in a material transaction with our Manager or any of its affiliates. These investment guidelines may be changed by our board of directors without the approval of our stockholders.

In addition:

| | • | | we will monitor all multiple asset types, sector markets, and tranches to identify attractive total return investments; |

| | • | | our asset allocation will be determined by market conditions and driven by exploitable market inefficiencies on either the asset or structuring side or both; and |

14

| | • | | we will emphasize the following investment themes: |

| | • | | high quality investments carefully screened and selected from our origination channels; |

| | • | | disciplined asset selection and bottom-up underwriting; |

| | • | | use of asset and liability structuring to lock-in attractive total returns and to minimize risk; and |

| | • | | hands on asset management and exit strategy/realization monitoring. |

Credit Risk Management. We are exposed to various levels of credit and special hazard risk depending on the nature of our underlying assets and the nature and level of credit enhancements supporting our assets. Historically, we have originated or purchased mortgage loans that meet minimum debt service coverage standards established by us. Our Manager reviews and monitors credit risk and other risks of loss associated with each investment. In addition, our Manager seeks to diversify our portfolio of assets to avoid undue geographic, issuer, industry and certain other types of concentrations. Our board of directors monitors the overall portfolio risk and reviews levels of provision for loss.

Interest Rate Risk Management. To the extent consistent with maintaining our qualification as a REIT, we follow an interest rate risk management policy intended to mitigate the negative effects of major interest rate changes. We minimize our interest rate risk from borrowings by attempting, if possible, to structure the key terms of our borrowings to generally correspond to the interest rate term of our assets.

Hedging Activities. We engage in hedging transactions to protect our investment portfolio from interest rate fluctuations and other changes in market conditions. These transactions may include interest rate swaps, the purchase or sale of interest rate collars, caps or floors, options, mortgage derivatives and other hedging instruments. These instruments may be used to hedge as much of the interest rate risk as our Manager determines is in the best interest of our stockholders, given the cost of such hedges and the need to maintain our qualification as a REIT. We may from time to time enter into interest rate swap agreements to offset the potential adverse effects of rising interest rates under certain short-term repurchase agreements. Our Manager may elect to have us bear a level of interest rate risk that could otherwise be hedged when it believes, based on all relevant facts, that bearing such risk is advisable.

Disposition Policies. Our Manager evaluates our asset portfolio on a regular basis to determine if it continues to satisfy our investment criteria. Subject to certain restrictions applicable to REITs, our Manager may cause us to sell our investments opportunistically and use the proceeds of any such sale for debt reduction, additional acquisitions or working capital purposes.

Equity Capital Policies. Subject to applicable law, our board of directors has the authority, without further stockholder approval, to issue additional authorized common stock and preferred stock or otherwise raise capital, including through the issuance of trust preferred securities or senior securities, in any manner and on the terms and for the consideration it deems appropriate, including in exchange for property. We may also raise funds through the retention of cash flow (subject to provisions in the Internal Revenue Code concerning distribution requirements and the taxability of undistributed REIT taxable income). In the event that our board of directors determines to raise additional equity capital, it has the authority, without stockholder approval (unless required under rules of the New York Stock Exchange, or the NYSE), to issue additional common stock, preferred stock, trust preferred securities or other senior securities in any manner and on such terms and for such consideration as it deems appropriate, at any time. Our existing stockholders and potential investors will have no preemptive right to additional shares issued in any offering, and any offering might cause a dilution of investment. We may in the future issue common stock in connection with acquisitions.

We may, under certain circumstances, repurchase our common stock in the open market or through private transactions with our stockholders, if those purchases are approved by our board of directors. Our board of directors has no present intention of causing us to repurchase any shares, and any action would only be taken in

15

conformity with applicable federal and state laws and the applicable requirements for qualifying as a REIT, for so long as the board of directors concludes that we should remain a REIT. We also have the authority to offer equity or debt securities in exchange for property.

Other Policies. We intend to operate in a manner that will not subject us to regulation under the 1940 Act. Subject to gross income and asset tests necessary for REIT qualification, we may invest in securities of other REITs, other entities engaged in real estate activities or securities of other issuers, including for the purpose of exercising control over such entities. We may engage in the purchase and sale of investments. We also may make loans to third parties. We will not underwrite the securities of other issuers.

Future Revisions in Policies and Strategies. Our board of directors has approved the investment policies, the operating policies and other strategies set forth in this prospectus. Our board of directors has the power to modify or waive these policies and strategies, or amend the management agreement with our Manager, without the consent of our stockholders to the extent that the board of directors (including a majority of our independent directors) determines that such modification or waiver is in our best interest and the best interest of our stockholders. Among other factors, developments in the market that either affect the policies and strategies mentioned herein or which change our assessment of the market may cause our board of directors to revise its policies and strategies. However, if such modification or waiver involves the relationship of, or any transaction between, us and our Manager or any affiliate of our Manager, the approval of a majority of our independent directors is also required.

Competition

Over the long-term, growth in our net income depends, in large part, on our Manager’s ability to originate and acquire structured investments with spreads over our borrowing costs. In originating and acquiring these investments, our Manager competes with other commercial mortgage REITs, specialty finance companies, savings and loan associations, banks, mortgage brokers, insurance companies, mutual funds, institutional investors, private investment funds, investment banking firms, other lenders, governmental bodies and other entities. In addition, there are numerous commercial REITs with asset acquisition objectives similar to ours, and others may be organized in the future. The effect of the existence of additional REITs may be to increase competition for the available supply of commercial real estate finance products suitable for purchase by us. Some of our anticipated competitors are significantly larger than us, have access to greater capital and other resources and may have other advantages over us.

Conflicts of Interests

We are entirely dependent upon our Manager for our day-to-day management and do not have any employees or independent officers. Ray Wirta, our chairman, is the vice chairman of CBRE and Michael Melody, one of our directors, is the vice chairman of CBRE|Melody. Our chairman, chief executive officer, chief financial officer and executive vice presidents also serve as officers of our Manager. As a result, we, our Manager, our executive officers and directors and CBRE may face conflicts of interests because of our relationships with each other. These conflicts include the following:

| | • | | The management agreement between us and our Manager was negotiated between related parties, and the terms, including fees payable, may not be as favorable to us as if it had been negotiated with an unaffiliated third party. The interests of these officers and directors in the affairs of CBRE and CBRE|Melody, respectively, may conflict from time to time with our interests. |

| | • | | CBRE or its affiliates provide various services to our company, including but not limited to, the provision of certain research, appraisal and servicing activities for which CBRE and its affiliates are provided market rate fees. Although such arrangements are approved by a majority of our independent directors, they are negotiated among related parties. |

16

| | • | | We have not adopted a policy that expressly prohibits our directors, officers, security holders or affiliates from having a direct or indirect pecuniary interest in any investment to be acquired or disposed of by us or any of our subsidiaries or in any transaction to which we or any of our subsidiaries is a party or has an interest. Nor do we have a policy that expressly prohibits any such persons from engaging for their own account in business activities of the types conducted by us. However, our code of business conduct and ethics contain a conflict of interest policy that prohibits our directors, officers and employees from engaging in any transaction that involves an actual or apparent conflict of interest with us. |

| | • | | The compensation we pay to our Manager consists of both a base management fee that is not tied to our performance and an incentive management fee that is based entirely on our performance. The risk of the base management fee component is that it may not provide sufficient incentive to our Manager to seek to achieve attractive returns to us. The risk of incentive management fee component is that it may cause our Manager to place undue emphasis on the maximization of short-term net income at the expense of other criteria, such as preservation of capital, in order to achieve a higher incentive fee. Investments with higher yield potential are generally riskier or more speculative. This could result in increased risk to the value of our investment portfolio. |

| | • | | Our Manager does not assume any responsibility beyond the duties specified in the management agreement and will not be responsible for any action of our board of directors in following or declining to follow its advice or recommendations. Our Manager and its officers, managers, employees and affiliates will not be liable to us, our directors or our stockholders for, and we have agreed to indemnify them for all claims and damages arising from, acts or omissions performed in good faith in accordance with and pursuant to the management agreement, except by reason of acts constituting bad faith, willful misconduct, gross negligence, or reckless disregard of their duties under the management agreement. As a result, we could experience poor performance or losses for which our Manager would not be liable. |

Conflicts of Interests Resolution Policies

We have implemented several policies, through board action and through the terms of our constituent documents and of our agreements with CBRE, to help address potential conflicts of interest:

| | • | | Our board of directors has adopted a policy that a majority of our board of directors will be independent directors, and that a majority of our independent directors must make any determinations on our behalf with respect to the relationships or transactions that present a conflict of interest for our directors or officers; |

| | • | | Our board of directors has adopted a policy that decisions concerning our management agreement with our Manager, including termination, renewal and enforcement thereof, or concerning any acquisition of assets from CBRE or its affiliates or other participation in any transactions with CBRE or its affiliates outside of the management agreement must be reviewed and approved by a majority of our independent directors; |

| | • | | Our management agreement provides that our determinations to terminate the management agreement for cause or because the management fees are unfair to us or because of a change in control of our Manager will be made by a majority vote of our independent directors. |

| | • | | Our independent directors will periodically review the general investment standards established for our Manager under the management agreement; and |

| | • | | Our management agreement with our Manager provides that our Manager may not assign certain duties under the management agreement, except to certain of its affiliates, without the approval of a majority of our independent directors. |

17

Management Agreement

We have entered into a management agreement with our Manager that provides for the day-to-day management of our operations. The management agreement requires our Manager to manage our business affairs in conformity with the policies and the investment guidelines that are approved and monitored by our board of directors. Our Manager’s role as manager is under the supervision and direction of our board of directors.

The initial term of the management agreement expires on December 31, 2008 and will be automatically renewed for a one-year term each anniversary date thereafter, subject to certain termination provisions. After the initial term, our independent directors will review our Manager’s performance annually and our management agreement may be terminated annually based upon (i) unsatisfactory performance that is materially detrimental to us (as determined by (1) affirmative vote of at least two-thirds of our independent directors, or (2) a vote of the holders of at least a majority of the outstanding shares of our common stock), or (ii) a determination by our independent directors that the compensation payable to our Manager is not fair, subject to our Manager’s right to prevent such a compensation termination by accepting a mutually acceptable adjustment of management fees. A termination fee will be paid to our Manager upon such termination. We may also terminate our management agreement with 60 days’ prior written notice from our board of directors, without payment of a termination fee, for cause, as defined in our management agreement.

The management agreement can also be terminated by our Manager who may elect to no longer act in that capacity. Our Manager must provide 180 days notice upon making such a decision. No termination fee is payable in such circumstance.

Pursuant to the management agreement, our Manager is entitled to receive a base management fee, incentive compensation and, in certain circumstances, a termination fee and reimbursement of certain expenses as described in the management agreement. The following table summarizes the fees and expenses payable to our Manager pursuant to the management agreement.

18

| | |

Fee | | Summary Description |

| Base Management Fee | | Payable monthly in arrears in an amount equal to 1/12th of the sum of (i) 2.0% of the first $400 million of our gross stockholders’ equity (as defined in the management agreement), or equity, (ii) 1.75% of our equity in an amount in excess of $400 million and up to $800 million and (iii) 1.50% of our equity in excess of $800 million. Our Manager uses the proceeds from its management fee in part to pay compensation to its officers and employees who, notwithstanding that certain of them also are our officers, receive no cash compensation directly from us. |

| |

| Incentive Fee | | Payable quarterly in an amount equal to the product of: • 25% of the dollar amount by which • our Funds From Operations (as defined in the management agreement) (after the base management fee and before incentive compensation) per share of our common stock for such quarter (based on the weighted average number of shares outstanding for such quarter) • exceeds an amount equal to • the weighted average of the price per share of our common stock in our June 2005 private offering, our October 2006 initial public offering, or IPO, and the prices per share of our common stock in any subsequent offering by us, in each case at the time of issuance thereof, multiplied by the greater of • 2.25% or • 0.75% plus one-fourth of the Ten Year Treasury Rate (as defined in the management agreement) for such quarter; |

| |

| | • multiplied by the weighted average number of shares of our common stock outstanding during such quarter. |

| |

| Termination Fee | | Payable upon termination without cause or non-renewal of the management agreement by us in an amount equal to three times the sum of the annual base management fee and the annual incentive compensation earned by our Manager during the previous 12-month period immediately preceding the date of termination, calculated as of the end of the most recently completed fiscal quarter prior to the date of termination. |

| |

| Expenses | | Payable monthly in arrears to our Manager for all documented expenses incurred by our Manager on our behalf. The expenses include all operating and administrative expenses incurred by the employees of our Manager. |

For the twelve months ended December 31, 2007 and the 2006, our Manager had earned base management fees of approximately $7.7 million and $6.5 million, respectively. We did not accrue or pay any incentive fees through December 31, 2007.

Our Distribution Policy

U.S. federal income tax law requires that a REIT distribute annually at least 90% of its net taxable income, determined without regard to the deduction for dividends paid and excluding net capital gain.

In order to maintain our REIT qualification and to generally not be subject to U.S. federal income and excise tax, we intend to make regular quarterly distributions of all or substantially all of our net taxable income to holders of our common stock. Any future distributions we make will be at the discretion of our board of directors

19

and will depend upon, among other things, our actual results of operations. These results and our ability to pay distributions will be affected by various factors, including the net interest and other income from our portfolio, our operating expenses and any other expenditure.

To the extent that our cash available for distribution is less than 90% of our net taxable income, we may consider various funding sources to cover any such shortfall, including borrowing under our warehouse facilities, selling certain of our assets or using a portion of the net proceeds we receive in this offering or future offerings. Our distribution policy enables us to review the alternative funding sources available to us from time to time.

Exclusion From Regulation Under the 1940 Act

We conduct our operations so that we are not required to register as an investment company. Under Section 3(a)(1) of the 1940 Act, a company is not deemed to be an “investment company” if:

| | • | | it neither is, nor holds itself out as being, engaged primarily, nor proposes to engage primarily, in the business of investing, reinvesting or trading in securities; or |