Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

AMENDMENT NO. 1 TO FORM 10

GENERAL FORM FOR REGISTRATION OF SECURITIES

PURSUANT TO SECTION 12(b) OR (g) OF

THE SECURITIES EXCHANGE ACT OF 1934

FEDERAL HOME LOAN BANK OF CHICAGO

(Exact name of registrant as specified in its charter)

Commission File No. 000-51401

| Federally chartered corporation | 36-6001019 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

111 East Wacker Drive Chicago, IL | 60601 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code: (312) 565-5700

Securities to be registered pursuant to Section 12(b) of the Act: None

Securities to be registered pursuant to Section 12(g) of the Act: Capital stock, $100 per share par value

1

Table of Contents

FEDERAL HOME LOAN BANK OF CHICAGO

TABLE OF CONTENTS

Item 1. | Business | 3 | ||

Item 1A. | Risk Factors | 53 | ||

Item 2. | Financial Information | 60 | ||

Item 3. | Properties | 116 | ||

Item 4. | Security Ownership of Certain Beneficial Owners and Management | 117 | ||

Item 5. | Directors and Executive Officers | 119 | ||

Item 6. | Executive Compensation | 123 | ||

Item 7. | Certain Relationships and Related Transactions | 129 | ||

Item 8. | Legal Proceedings | 132 | ||

Item 9. | Market Price of and Dividends on the Registrant’s Common Equity and Related Stockholder Matters | 133 | ||

Item 10. | Recent Sales of Unregistered Securities | 135 | ||

Item 11. | Description of Registrant’s Securities to be Registered | 136 | ||

Item 12. | Indemnification of Directors and Officers | 138 | ||

Item 13. | Financial Statements and Supplementary Data | 139 | ||

Item 14. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 140 | ||

Item 15. | Financial Statements and Exhibits | 141 |

2

Table of Contents

| I tem 1. | Business. |

1.1 | Overview | 4 | ||

1.2 | Business Segments | 7 | ||

1.3 | Funding Services | 40 | ||

1.4 | Use of Interest Rate Derivatives | 44 | ||

1.5 | Regulations | 45 | ||

1.6 | Taxation | 48 | ||

1.7 | REFCORP and AHP Assessments | 49 | ||

1.8 | Competition | 50 | ||

1.9 | Employees | 52 |

3

Table of Contents

Introduction

The Federal Home Loan Bank of Chicago (the “Bank”), a federally chartered corporation and a member–owned cooperative, is one of twelve Federal Home Loan Banks (the “FHLBs”) which, with the Federal Housing Finance Board (the “Finance Board”) and the Office of Finance, comprise the Federal Home Loan Bank System (the “System”). The twelve FHLBs are government-sponsored enterprises (“GSE”) of the United States of America and were organized under the Federal Home Loan Bank Act of 1932, as amended (“FHLB Act”). Each FHLB has members in a specifically defined geographic district. The Bank’s defined geographic membership territory consists of the states of Illinois and Wisconsin.

The mission of the Bank is to promote and support the growth and success of our members’ housing, community investment, and other financing activities by:

| • | Serving as a reliable source of liquidity. |

| • | Providing secured financing and asset liability management capabilities, which create value and are designed to meet our members’ specific needs. |

| • | Contributing direct support to affordable housing and community investment programs delivered through our members. |

The principal sources of credit provided by the Bank are in the form of secured loans, called advances, to members and through the Mortgage Partnership Finance® (MPF®) Program1 under which the Bank, in partnership with its members, provides funding for home mortgage loans. The Bank initiated the MPF Program in 1997. In 2003, the Bank initiated the MPF Shared Funding® program, pursuant to which a member of the Bank forms a trust that issues privately-placed mortgage-backed securities (“MBS”) which are sold to the FHLBs and their members, thereby providing competition in the MBS market.

These programs help the Bank accomplish its mission of supporting housing finance throughout America. All federally-insured depository institutions, insurance companies engaged in residential housing finance, credit unions and community financial institutions (“CFIs”) located in Illinois and Wisconsin are eligible to apply for membership in the Bank. All members are required to purchase capital stock in the Bank as a condition of membership, and all capital stock is owned by the Bank’s members. The capital stock is not publicly-traded.

The Bank combines private capital and public sponsorship to provide its member financial institutions with a reliable flow of credit and other services for housing and community development. The Bank serves the public through member financial institutions by providing members with liquidity and capital markets based financing, thereby enhancing the availability of residential mortgage and community investment credit. The Bank also provides members with funding for home mortgage loans through the MPF Program.

The Bank is supervised and regulated by the Finance Board, which is an independent federal agency in the executive branch of the United States Government. See “Item 1.5—Regulations—Regulatory Oversight.”

A primary source of funds for the Bank is the proceeds from the sale to the public of FHLB debt instruments (“consolidated obligations”) which are, by Finance Board regulation, the joint and several obligations of all the FHLBs. Consolidated obligations are not obligations of the United States Government and the United States Government does not guarantee them. The Office of Finance is a joint office of the FHLBs established by the Finance Board to facilitate issuing and servicing of the consolidated obligations. Additional funds are provided by deposits, other borrowings and the issuance of capital stock. Deposits are received from both member and non-member financial institutions and federal instrumentalities. The Bank also provides members and non-members with correspondent services such as safekeeping, wire transfers, and cash management.

The Bank maintains a web site located at www.fhlbc.com through which it makes available its financial statements and other information regarding the Bank. Following the Bank’s registration under the Securities Exchange Act of 1934, the Bank will be required to file with the Securities and Exchange Commission an annual report on Form 10-K, quarterly reports on Form

| 1 | “Mortgage Partnership Finance,” “MPF,” “ MPF Shared Funding” and “eMPF” are registered trademarks of the Federal Home Loan Bank of Chicago. |

4

Table of Contents

10-Q, and current reports on Form 8-K. The Securities and Exchange Commission maintains a website that contains these reports and other information regarding the Bank’s electronic filings located at www.sec.gov. These reports may also be read and copied at the Securities and Exchange Commission’s Public Reference Room at 100 F Street, NE, Washington, DC 20549. Further information about the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. Information on those websites, or that can be accessed through those websites, does not constitute a part of this registration statement.

Membership Trends

At September 30, 2005, membership in the Bank was 885 members, down eight from December 31, 2004. Although the Bank added 17 new members, 3 members voluntarily withdrew from membership and 22 members were acquired by other institutions (15 within the Bank’s district and 7 outside of the district.) Capital stock decreased $399 million or 9.3% from December 31, 2004 because of voluntary redemptions and members being acquired by out of district financial institutions. On October 18, 2005, the Bank’s Board of Directors discontinued redemptions of voluntary stock for a period of time in order to ensure an adequate capital base for the Bank. Subsequent to the Bank announcing its discontinuation of voluntary capital stock redemptions on October 18, 2005, the Bank received membership withdrawal notices and related redemption requests from five members totaling $235 million through February 6, 2006. These requests were reclassified from equity to a liability upon notice. Redemption is pending the six month notice period and approval from the Finance Board. See “Item 2.2—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Overview—Regulatory Agreement and Related Actions.”

Total membership in the Bank reached an all-time high of 893 members at December 31, 2004, up from 884 at December 31, 2003. Of those members, 79% were commercial banks, 16% thrift institutions, 4% credit unions, and 1% insurance companies. At the end of 2004, 42% of all members had less than $100 million in assets, 53% had assets between $100 million and $1 billion, and 5% had assets in excess of $1 billion.

Credit customers, defined as the number of members which have used advances, the MPF Program or other credit products at any point during the period, were 718 in 2004 compared to 681 during 2003. As a percentage of total membership, credit customer utilization was 80% in 2004 versus 77% in 2003. For the nine months ended September 30, 2005, the number of credit customers was 737, with a credit customer utilization ratio of 83% compared to 705 credit customers with a credit customer utilization ratio of 79% for the nine months ended September 30, 2004.

5

Table of Contents

The table below shows the outstanding advances, capital stock holdings and the geographic locations of the Bank’s members by type:

(Dollars in thousands) | September 30, 2005 | |||||||||||||||||||

Type of Institutions | Advances at Par | Percent of Total | Par Value of Capital Stock Held | Number of Institutions | Percent of Total | |||||||||||||||

| Illinois | Wisconsin | Total | ||||||||||||||||||

Commercial Banks | $ | 14,842,853 | 61.3 | % | $ | 2,300,003 | 474 | 227 | 701 | 79.2 | % | |||||||||

Thrifts | 7,484,295 | 30.9 | % | 996,418 | 100 | 36 | 136 | 15.4 | % | |||||||||||

Credit Unions | 178,685 | 0.7 | % | 294,405 | 16 | 21 | 37 | 4.2 | % | |||||||||||

Insurance Companies | 1,713,000 | 7.1 | % | 313,573 | 9 | 2 | 11 | 1.2 | % | |||||||||||

Total | $ | 24,218,833 | 100.0 | % | $ | 3,904,399 | 599 | 286 | 885 | 100.0 | % | |||||||||

Adjustments | 14,182 | 1 | (13,734 | ) 2 | ||||||||||||||||

Per Financial Statements | $ | 24,233,015 | $ | 3,890,665 | ||||||||||||||||

(Dollars in thousands) | December 31, 2004 | |||||||||||||||||||

Type of Institutions | Advances at Par | Percent of | Par Value of | Number of Institutions | Percent of | |||||||||||||||

| Illinois | Wisconsin | Total | ||||||||||||||||||

Commercial Banks | $ | 14,121,622 | 58.9 | % | $ | 2,312,005 | 478 | 229 | 707 | 79.2 | % | |||||||||

Thrifts | 7,954,899 | 33.2 | % | 1,253,481 | 104 | 37 | 141 | 15.8 | % | |||||||||||

Credit Unions | 174,083 | 0.7 | % | 303,138 | 16 | 19 | 35 | 3.9 | % | |||||||||||

Insurance Companies | 1,718,000 | 7.2 | % | 434,801 | 8 | 2 | 10 | 1.1 | % | |||||||||||

Total | $ | 23,968,604 | 100.0 | % | $ | 4,303,425 | 606 | 287 | 893 | 100.0 | % | |||||||||

Adjustments | 222,954 | 1 | (11,259 | ) 2 | ||||||||||||||||

Per Financial Statements | $ | 24,191,558 | $ | 4,292,166 | ||||||||||||||||

| 1 | Adjustment includes SFAS 133 basis adjustment for advances at par. |

| 2 | Adjustments include SFAS 150 adjustment of mandatorily redeemable capital stock for the par value of capital stock held. |

6

Table of Contents

The Bank manages its operations by grouping its products and services within two operating segments. The measure of profit or loss and total assets for each segment is contained in Note 10—Segment Information to the September 30, 2005 Financial Statements and Notes and in Note 17—Segment Information to the 2004 Annual Financial Statements and Notes. Management’s Discussion and Analysis on the operating results of the segments is contained in “Item 2.2—Management’s Discussion and Analysis of Financial Condition and Results of Operations—Operating Segment Results.” These operating segments are:

| • | Traditional Member Finance: This segment includes traditional funding, liquidity and deposit products consisting of loans to members called advances, standby letters of credit, investments and deposit products; and |

| • | the MPF Program. |

The segments reflect the manner in which financial information is evaluated by management including the chief operating decision makers.

Traditional Member Finance

Advances

The Bank extends advances (fixed or floating rate loans) to its members and eligible housing associates based on the security of mortgages and other collateral that the members and eligible housing associates pledge. Eligible housing associates are non-members that are approved mortgagees under Title II of the National Housing Act for which the Bank is permitted under the FHLB Act to make advances. These eligible housing associates must be chartered under law, be subject to inspection and supervision by some governmental agency, and lend their own funds as their principal activity in the mortgage field. Eligible housing associates are not subject to certain provisions of the FHLB Act that are applicable to members, such as the capital stock purchase requirements, but the same regulatory lending requirements that apply to members apply to them.

Advances generally support residential mortgages held in member portfolios, and may also be used for any valid business purpose in which a member is authorized to invest, including providing funds to any member CFI for secured loans to small businesses, small farms, and small agri-businesses. CFIs are defined as FDIC-insured depository institutions with total average year-end assets at or below a level prescribed by the Finance Board each year for the prior three years. This level was set at $567 million or less as of January 1, 2005 and $548 million or less as of January 1, 2004. Advances can serve as a funding source for a variety of conforming mortgage loans and nonconforming mortgages, including loans that members may be unable or unwilling to sell in the secondary mortgage market. Conforming mortgage loans are mortgage loans which meet Fannie Mae’s or Freddie Mac’s original loan amount limits and underwriting guides. Nonconforming mortgage loans are mortgage loans that do not meet these requirements. Thus, advances support important housing markets, including those focused on low- and moderate-income households. For those members that choose to sell or securitize their mortgages, advances can provide interim funding.

The Bank offers a variety of advances, including the following:

| • | Fixed-Rate Advances. Fixed-rate advances have maturities from two days to ten years. The Bank also offers putable fixed-rate advances in which the Bank has the right to put the advance after a specified lockout period, in whole or in part, at the par value with five business days notice. If the Bank has the right to put the advance, the member must extinguish the advance by using its existing liquidity or by obtaining funds under another advance product offered by the Bank at existing market prices for that member on the date the advance was put back to the member. |

| • | Variable-Rate Advances. Variable-rate advances include advances with maturities from six months to seven years with the interest rates reset periodically at a fixed spread to LIBOR or some other index. Depending upon the variable-rate advance selected, the member can have an interest-rate cap on the advance which limits the amount of interest the member would have to pay, or the member can prepay the advance with or without a prepayment fee. |

7

Table of Contents

| • | Open-Line Advances. Open-line advances are designed to provide flexible funding to meet borrowers’ daily liquidity needs and can be drawn for one day. These advances are automatically payable on demand by the member. Rates are set daily at the end of business. |

| • | Fixed Amortizing Advances. Fixed amortizing advances have maturities that range from one year to 15 years, with the principal repaid over the term of the advances monthly, quarterly or semi-annually. |

| • | Floating to Fixed Convertible Advances. Floating to fixed convertible advances have maturities that range from two years to ten years, with a defined lockout period where the interest rates adjust based on a spread to LIBOR. At the end of the lockout period, these advances convert to fixed-rate advances. The interest rates on the converted advances are set at origination. |

The tables below set forth the outstanding amount of advances by type:

(Dollars in thousands) | September 30, 2005 | |||||||||||||

Advance Type | Carrying Value | Percent of Total | Income for the | Percent of Advance Income | ||||||||||

Fixed-Rate | $ | 19,459,375 | 80.34 | % | $ | 516,191 | 81.53 | % | ||||||

Variable-Rate | 3,627,600 | 14.98 | % | 82,435 | 13.02 | % | ||||||||

Open-Line | 899,803 | 3.72 | % | 25,392 | 4.01 | % | ||||||||

Fixed Amortizing | 177,055 | 0.73 | % | 6,891 | 1.09 | % | ||||||||

Floating to Fixed Convertible | 55,000 | 0.23 | % | 2,219 | 0.35 | % | ||||||||

Total par value of advances | 24,218,833 | 100.00 | % | 633,128 | 100.00 | % | ||||||||

Other | (85 | ) | 561 | |||||||||||

SFAS 133 hedging adjustments | 14,267 | (68,394 | ) | |||||||||||

Total Advances | $ | 24,233,015 | $ | 565,295 | ||||||||||

(Dollars in thousands) | September 30, 2004 | |||||||||||||

Advance Type | Carrying Value | Percent of Total | Income for the | Percent of Advance Income | ||||||||||

Fixed-Rate | $ | 19,995,527 | 80.70 | % | $ | 556,936 | 88.03 | % | ||||||

Variable-Rate | 3,165,200 | 12.78 | % | 52,173 | 8.25 | % | ||||||||

Open-Line | 1,329,381 | 5.37 | % | 11,106 | 1.76 | % | ||||||||

Fixed Amortizing | 230,801 | 0.93 | % | 8,406 | 1.33 | % | ||||||||

Floating to Fixed Convertible | 55,000 | 0.22 | % | 4,004 | 0.63 | % | ||||||||

Total par value of advances | 24,775,909 | 100.00 | % | 632,625 | 100.00 | % | ||||||||

Other | (100 | ) | 3,210 | |||||||||||

SFAS 133 hedging adjustments | 349,091 | (223,884 | ) | |||||||||||

Total Advances | $ | 25,124,900 | $ | 411,951 | ||||||||||

8

Table of Contents

(Dollars in thousands) | December 31, 2004 | |||||||||||||

Advance Type | Carrying Value | Percent of Total | Income for the | Percent of Advance Income | ||||||||||

Fixed-Rate | $ | 19,398,370 | 80.93 | % | $ | 730,263 | 87.83 | % | ||||||

Variable-Rate | 3,207,400 | 13.38 | % | 68,423 | 8.23 | % | ||||||||

Open-Line | 1,085,281 | 4.53 | % | 16,953 | 2.04 | % | ||||||||

Fixed Amortizing | 222,553 | 0.93 | % | 11,049 | 1.33 | % | ||||||||

Floating to Fixed Convertible | 55,000 | 0.23 | % | 4,751 | 0.57 | % | ||||||||

Total par value of advances | 23,968,604 | 100.00 | % | 831,439 | 100.00 | % | ||||||||

Other | (97 | ) | 5,091 | |||||||||||

SFAS 133 hedging adjustments | 223,051 | (282,426 | ) | |||||||||||

Total Advances | $ | 24,191,558 | $ | 554,104 | ||||||||||

(Dollars in thousands) | December 31, 2003 | |||||||||||||

Advance Type | Carrying Value | Percent of Total | Income for the Year Ended | Percent of Advance Income | ||||||||||

Fixed-Rate | $ | 19,377,117 | 74.91 | % | $ | 800,274 | 89.71 | % | ||||||

Variable-Rate | 5,139,199 | 19.87 | % | 63,846 | 7.16 | % | ||||||||

Open-Line | 997,951 | 3.86 | % | 10,299 | 1.15 | % | ||||||||

Fixed Amortizing | 248,876 | 0.96 | % | 11,959 | 1.34 | % | ||||||||

Floating to Fixed Convertible | 105,000 | 0.40 | % | 5,733 | 0.64 | % | ||||||||

Total par value of advances | 25,868,143 | 100.00 | % | 892,111 | 100.00 | % | ||||||||

Other | (144 | ) | 4,042 | |||||||||||

SFAS 133 hedging adjustments | 575,064 | (340,958 | ) | |||||||||||

Total Advances | $ | 26,443,063 | $ | 555,195 | ||||||||||

(Dollars in thousands) | December 31, 2002 | |||||||||||||

Advance Type | Carrying Value | Percent of Total | Income for the Year Ended | Percent of Advance Income | ||||||||||

Fixed-Rate | $ | 18,805,122 | 78.27 | % | $ | 888,744 | 88.40 | % | ||||||

Variable-Rate | 4,529,598 | 18.85 | % | 88,144 | 8.77 | % | ||||||||

Open-Line | 412,022 | 1.71 | % | 11,087 | 1.10 | % | ||||||||

Fixed Amortizing | 279,130 | 1.16 | % | 11,617 | 1.16 | % | ||||||||

Floating to Fixed Convertible | 1,184 | 0.01 | % | 5,793 | 0.57 | % | ||||||||

Total par value of advances | 24,027,056 | 100.00 | % | 1,005,385 | 100.00 | % | ||||||||

Other | (233 | ) | 748 | |||||||||||

SFAS 133 hedging adjustments | 918,289 | (415,870 | ) | |||||||||||

Total Advances | $ | 24,945,112 | $ | 590,263 | ||||||||||

9

Table of Contents

The Bank’s credit products provide members with asset-liability management capabilities. The Bank offers advances that can be adjusted to help manage the maturity and prepayment characteristics of mortgage loans. These advances can reduce a member’s interest rate risk associated with holding long-term fixed-rate mortgages. Alternatively, members can enter into interest rate derivatives directly with the Bank to reduce their exposure to interest rate risk. In such cases, the Bank acts as an intermediary between the members and other non-member counterparties by entering into offsetting interest rate derivatives. This intermediation allows smaller members indirect access to the derivatives market. The derivatives used in intermediary activities do not qualify for SFAS 133 hedge accounting treatment and are separately recorded at fair value through earnings. At September 30, 2005 and December 31, 2004 and 2003, the Bank had $87.7 million, $127.4 million and $142.6 million in outstanding notional amounts of interest rate exchange agreements, respectively, between the Bank and its members. The fair value of these interest rate derivatives was ($5.0) million, $6.1 million and ($3.6) million at September 30, 2005 and December 31, 2004 and 2003, respectively.

To determine the maximum amount and term of the advances the Bank will lend to a member, the Bank assesses the member’s creditworthiness and financial condition. The Bank also values the collateral pledged to the Bank and conducts periodic collateral reviews to establish the amount it will lend against each collateral type. The Bank requires delivery of all securities collateral and may also require delivery of loan collateral under certain conditions (for example, when a member’s creditworthiness deteriorates).

The Bank is required to obtain and maintain a security interest in eligible collateral at the time it originates or renews an advance. Eligible collateral includes whole first mortgages on improved residential property, or securities representing a whole interest in such mortgages; securities issued, insured, or guaranteed by the U.S. Government or any of its agencies; without limitation mortgage-backed securities issued or guaranteed by the Federal National Mortgage Association (“Fannie Mae”), Federal Home Loan Mortgage Corporation (“Freddie Mac”), or the Government National Mortgage Association (“Ginnie Mae”); FHLB consolidated obligations; cash or deposits in the Bank; and other real estate-related collateral acceptable to the Bank provided that the collateral has a readily ascertainable value and the Bank can perfect a security interest in the related property.

CFIs are subject to expanded statutory collateral provisions which allow them to pledge secured small business, small farm, or small agri-business loans. We refer to this type of collateral as “community financial institution collateral”. As additional security for a member’s indebtedness, the Bank has a statutory lien on a member’s capital stock in the Bank.

The FHLB Act affords any security interest granted to the Bank by any member of the Bank, or any affiliate of any such member, priority over the claims and rights of any party, including any receiver, conservator, trustee, or similar party having rights of a lien creditor. The only two exceptions are claims and rights that would be entitled to priority under otherwise applicable law or are held by actual bona fide purchasers for value or by parties that are secured by actual perfected security interests. The Bank perfects the security interests granted to it by members by taking possession of securities collateral and filing UCC-1 forms on all other collateral.

Collateral arrangements will vary with member credit quality, borrowing capacity, collateral availability, and overall member credit exposure. The Bank manages collateral requirements and increases its monitoring of members when borrowings from all sources exceed 20% of their assets. At September 30, 2005, 14 of the Bank’s members had borrowings from the Bank that exceeded 20% of their assets, totaling $5.4 billion of advances at par value, which represented 22.5% of the Bank’s total advances outstanding at par.

10

Table of Contents

At December 31, 2004, 12 of the Bank’s members had borrowings from the Bank that exceeded 20% of their assets, totaling $2.9 billion of advances at par value, which represented 12% of the Bank’s total advances outstanding at par. At December 31, 2003, the comparable amounts were 11 of the Bank’s members had borrowings from the Bank that exceeded 20% of their assets, totaling $2.6 billion of advances at par, which represented 10% of the Bank’s total advances outstanding at par. In particular, one member accounted for over $2 billion of the outstanding advances at par, which represented 24% of that member’s September 30, 2005 assets and 23% of that member’s 2004 and 2003 assets. The Bank may require the delivery of collateral from any member at any time. The following table illustrates member borrowing capacity based on underlying collateral type:

Types of Collateral | Borrowing Capacity | |

U.S. Treasury and other government agency securities1 | 95 - 97% | |

Non-agency, rated mortgage-backed securities | 85 - 90% | |

Eligible first-lien single or multi-family mortgage loans | 60 - 85% | |

Community financial institution and other eligible collateral | 50% |

| 1 | Includes GSEs such as Fannie Mae, Freddie Mac, and FHLBs, as well as Governmental agencies such as Ginnie Mae, the Farm Services Agency, Small Business Administration, Bureau of Indian Affairs, and the United States Department of Agriculture. |

During the third quarter of 2005, changes were made to the Bank’s Credit Policy. The collateral loan value available to members for 1-4 family first liens pledged under a blanket lien arrangement was increased to 75%, while the collateral loan value available to members for 1-4 family first liens pledged under a comprehensive listing arrangement was increased to 85%.

At September 30, 2005, CFIs had pledged $467.2 million of CFI collateral to the Bank, securing $48.5 million of advances. The CFI collateral amounts pledged in excess of the amounts required to cover existing advances is available (after application of the borrowing capacity percentage) for potential future advances. At December 31, 2004, CFIs had pledged $339.6 million of CFI collateral to the Bank, which secured $52.1 million of advances at December 31, 2004. At December 31, 2003, CFIs had pledged $244 million of CFI collateral to the Bank, securing $45 million of advances at December 31, 2003.

The Bank requires that members annually deliver copies of their audited financial statements or 10-K report filed with the Securities and Exchange Commission. Members that are not otherwise required to produce audited financial statements, are required to submit their year-end call report or thrift report. The Bank also accesses all member quarterly reports filed with their applicable regulators. The Bank regularly reviews this financial information and will make adjustments to a member’s borrowing capacity and collateral requirements as needed.

Members with outstanding advances are required to deliver to the Bank a third party collateral verification report based upon agreed upon procedures attesting to the eligibility and sufficiency of the member’s mortgage collateral. Members are normally required to deliver these reports every two years provided they meet satisfactory credit and collateral conditions. Members that average more than $100 million in outstanding advances each year secured by single family or multiple family mortgage loans are required to deliver a collateral verification report annually. Credit worthy members with average outstanding advances less than $5 million secured by single family or multiple family mortgage loans with an outstanding book value at least 3 times greater than the amount of average outstanding advances are only required to deliver a collateral verification report every three years. Members pledging small business, small farm or small agri-business loans are required to provide the Bank with quarterly collateral listings and the Bank conducts collateral field reviews annually. The Bank conducts field reviews in other circumstances as well in order to determine collateral eligibility and whether any adjustment to a member’s borrowing capacity is necessary.

11

Table of Contents

At September 30, 2005 and December 31, 2004 and 2003, the Bank had 611, 586 and 563 advance borrowers, respectively. The table below sets forth the outstanding par amount of advances by the largest advance borrowers:

| Top Ten Largest Advance Borrowers | ||||||||||||||||||

| September 30, 2005 | December 31, 2004 | December 31, 2003 | ||||||||||||||||

(Dollars in thousands) | Advances at Par | % of Total | Advances at Par | % of Total | Advances at Par | % of Total | ||||||||||||

LaSalle Bank, N.A. | $ | 3,151,428 | 13.0 | % | $ | 3,151,471 | 13.2 | % | $ | 3,801,525 | 14.7 | % | ||||||

Mid America Bank, FSB | 2,358,000 | 9.7 | % | 2,188,125 | 9.1 | % | 2,104,375 | 8.1 | % | |||||||||

One Mortgage Partners Corp.1 | 1,615,000 | 6.7 | % | 1,615,000 | 6.7 | % | 4,865,000 | 18.8 | % | |||||||||

M & I Marshall & Ilsley Bank | 1,453,714 | 6.0 | % | 1,654,091 | 6.9 | % | 1,094,114 | 4.2 | % | |||||||||

The Northern Trust Company | 1,270,974 | 5.2 | % | 945,974 | 3.9 | % | 810,974 | 3.1 | % | |||||||||

Associated Bank, N.A. | 1,208,403 | 5.0 | % | 814,040 | 3.4 | % | 754,138 | 2.9 | % | |||||||||

State Farm Bank, FSB | 1,080,000 | 4.5 | % | 1,211,190 | 5.1 | % | 872,791 | 3.4 | % | |||||||||

Bank Mutual | 865,306 | 3.6 | % | 761,525 | 3.2 | % | n/a | n/a | ||||||||||

Anchor Bank, FSB | 710,928 | 2.9 | % | 761,328 | 3.2 | % | 684,618 | 2.6 | % | |||||||||

First Midwest Bank, FSB | 522,900 | 2.2 | % | 512,900 | 2.1 | % | 452,000 | 1.7 | % | |||||||||

Charter One Bank 2 | n/a | n/a | n/a | n/a | 662,154 | 2.6 | % | |||||||||||

All Other Members | 9,982,180 | 41.2 | % | 10,352,960 | 43.2 | % | 9,766,454 | 37.8 | % | |||||||||

Total | $ | 24,218,833 | 100.0 | % | $ | 23,968,604 | 100.0 | % | $ | 25,868,143 | 99.9 | % | ||||||

n/a = Not applicable as advance borrower was not a top 10 largest borrower.

| 1 | Bank One, N.A. was acquired by J.P. Morgan Chase, an out-of-district acquisition. The advance balances of Bank One, N.A. were transferred to its subsidiary, One Mortgage Partners Corp., an in-district member. |

| 2 | Charter One was acquired by an out-of-district institution during 2004, at which time all Charter One’s advances were extinguished. |

Standby Letters of Credit

The Bank also provides members with standby letters of credit to support certain obligations of the members to third parties. Members may use standby letters of credit to facilitate residential housing finance and community lending or for liquidity and asset-liability management purposes. The Bank’s underwriting and collateral requirements for standby letters of credit are the same as the underwriting and collateral requirements for advances. At September 30, 2005 and December 31, 2004 and 2003, the Bank had $554.4 million, $345.7 million and $395.8 million, respectively, in standby letters of credit outstanding.

Other Mission-Related Community Investment Cash Advance Programs

Direct and indirect support for housing and community economic development lending programs are designed to ensure that communities throughout the Bank’s district are safe and desirable places to work and live. Members are assisted in meeting their Community Reinvestment Act responsibilities through a variety of specialized programs. Through the Affordable Housing Program (AHP), Community Investment Program (CIP), and Community Economic Development Advance Program members have access to grants and below-market interest rate advances to help them provide funds for affordable rental housing and home-ownership, small business, and other commercial and economic development opportunities that benefit low- and moderate-income individuals, households, and neighborhoods. In addition, the Bank purchases mortgages that are guaranteed by the U.S. Department of Housing and Urban Development (HUD) under the HUD Section 184 Native American Program. The Bank administers and funds the programs described below:

| • | Affordable Housing Program - AHP subsidies in the form of direct grants and below-market interest rate advances are offered to member financial institutions in partnership with community sponsors to stimulate affordable rental and homeownership opportunities for households with incomes at or below 80% of the area’s median income adjusted for family size. AHP subsidies can be used to fund housing acquisition, rehabilitation, new construction, or to cover down payment and closing costs. This program is funded with approximately 10% of the Bank’s pre-assessment net earnings each year. Since its inception in 1990, the Bank has awarded $203.1 million in AHP subsidies to facilitate the development of projects that provided affordable housing to 49,061 households. |

12

Table of Contents

The Bank awarded AHP competitive subsidies totaling $14.5 million and $16.5 million during the nine months ended September 30, 2005 and 2004, respectively, for projects designed to provide housing to 2,859 and 2,917 households, respectively. The Bank awarded AHP competitive subsidies totaling $32.1 million and $22.2 million for the years ended December 31, 2004 and 2003, respectively, for projects designed to provide housing to 5,680 and 4,469 households, respectively. These subsidies are awarded semi-annually in the second and fourth quarters. Amounts accrued but not awarded are recorded as a liability on the Bank’s Statements of Condition. As a part of its annual affordable housing grant making process, the Bank announced that it anticipates approximately $30 million will be available to members and sponsors during 2006 to support the Bank’s Affordable Housing Program activities.

DownPayment Plus® is a sub-program of the AHP that, in partnership with the Bank’s members, assists primarily first-time home buyers with down payment and closing cost requirements. During the nine months ended September 30, 2005 and 2004, $4.8 million and $7.3 million, respectively, of the AHP was funded through DownPayment Plus® to assist 995 and 1,613 low-and-moderate income homebuyers. During the years ended December 31, 2004 and 2003, $10.4 million and $6.0 million, respectively, of the AHP was allocated to DownPayment Plus® for assistance to 2,278 and 1,648 low- and moderate-income homebuyers.

| • | Community Investment Program/Community Economic Development Advance Program - In addition to the AHP, the Bank offers two programs through which members may apply for advances to support affordable housing development or community economic development lending. These programs provide advance funding that has interest rates below regular advance rates, for terms typically up to 10 years. The Bank’s CIP and Community Economic Development Advance products have been used to finance affordable home ownership housing, multi-family rental projects, new roads and bridges, agriculture and farm activities, public facilities and infrastructure, and small businesses. As of September 30, 2005 and December 31, 2004 and 2003, the Bank had approximately $1.9 billion, $1.5 billion and $1.1 billion, respectively, in advances outstanding under the CIP and Community Economic Development Advance programs. |

| • | Native American Mortgage Purchase Program - Since December 2003, the Bank has purchased mortgages provided by its Wisconsin members on Indian land. These mortgages are fully guaranteed by the U.S. Department of Housing and Urban Development (“HUD”), in the event of default by the homeowner. Since the inception of the program through September 30, 2005, the Bank had purchased 65 mortgages totaling approximately $5.2 million with no default occurrences. |

Investments

The Bank maintains a portfolio of investments for liquidity purposes and to provide additional earnings. To ensure the availability of funds to meet member credit needs, the Bank maintains a portfolio of short-term investments made to highly rated institutions, principally overnight Federal funds. The longer-term investment portfolio includes securities issued by the U.S. Government, U.S. Government agencies, MPF Shared Funding®, and MBS that are issued by government sponsored enterprises or that carry the highest ratings from Moody’s Investors Service (“Moody’s”), Standard and Poor’s Rating Service (“S&P”), or Fitch Ratings, Inc. (“Fitch”). The long-term investment portfolio provides the Bank with higher returns than those available in the short-term money markets. It is not our practice to purchase investment securities issued directly by our members or their affiliates. Investment securities issued by affiliates of our members may be purchased in the secondary market through a third party at arm’s length. See Note 20, “Transactions with Related Parties and Other FHLBs” in the Bank’s 2004 Annual Financial Statements and Notes for further details.

Under Finance Board regulations, the Bank is prohibited from trading securities for speculative purposes or market-making activities. Additionally, the Bank is prohibited from investing in certain types of securities or loans, including:

| • | Instruments, such as common stock, that represent an ownership in an entity, other than common stock in small business investment companies, or certain investments targeted to low-income persons or communities; |

13

Table of Contents

| • | Instruments issued by non-U.S. entities, other than those issued by U.S. branches and agency offices of foreign commercial banks; |

| • | Non-investment grade debt instruments, other than certain investments targeted to low-income persons or communities, or instruments that were downgraded after purchase by the Bank; |

| • | Whole mortgages or other whole loans, other than, (1) those acquired under the Bank’s MPF Program, (2) certain investments targeted to low-income persons or communities, (3) certain marketable direct obligations of State, local, or tribal government units or agencies, having at least the second highest credit rating from a Nationally-Recognized Statistical Rating Organization (“NRSRO”), (4) MBS or asset-backed securities backed by manufactured housing loans or home equity loans; and, (5) certain foreign housing loans authorized under section 12(b) of the FHLB Act; and |

| • | Non-U.S. dollar denominated securities. |

The Finance Board regulations further limit the Bank’s investment in MBS and asset-backed securities. This regulation requires that the total carrying value of MBS owned by the Bank not exceed 300% of the Bank’s previous month-end capital on the day it purchases the securities. At September 30, 2005 and December 31, 2004 and 2003, the Bank’s MBS securities to total capital ratio was 105%, 119% and 87%, respectively. In addition, the Bank is prohibited from purchasing:

| • | Interest-only or principal-only stripped MBS; |

| • | Residual-interest or interest-accrual classes of collateralized mortgage obligations (“CMO”) and Real Estate Mortgage Investment Conduit (“REMIC”); and |

| • | Fixed rate MBS or floating rate MBS that on the trade date are at rates equal to their contractual cap and that have average lives that vary by more than 6 years under an assumed instantaneous interest rate change of 300 basis points. |

At September 30, 2005, the Bank held $34.1 million of consolidated obligations at fair market value ($33.0 million at par value) of other FHLBs that were purchased from 1995 to 1997. Of these consolidated obligations, $8.2 million (at par value) are scheduled to mature in the fourth quarter of 2005 with the remaining $24.8 million (at par value) scheduled to mature in 2008. These investments are classified as Trading on the statements of condition. The Bank was authorized to purchase these consolidated obligations in the secondary markets after their initial offering period because they qualified as authorized investments under the Finance Board’s Financial Management Policy. The Bank is the secondary obligor for consolidated obligations that it acquires and holds for investment purposes. Acquiring consolidated obligations of other FHLBs is not part of the Bank’s existing investment strategy. As a result, the Bank does not intend to purchase any additional consolidated obligations of other FHLBs.

14

Table of Contents

The Bank’s investment portfolio at fair value by type of investment and credit rating is shown in the following tables:

Investment Securities

September 30, 2005

(Dollars in thousands) | Long Term Rating | Short Term Rating | |||||||||||||

Total Portfolio | U.S. Government Agency and Government Sponsored Enterprises | AAA | AA | A-1 or Higher | Total | ||||||||||

Commercial paper | $ | — | $ | — | $ | — | $ | 449,405 | $ | 449,405 | |||||

Government-sponsored enterprises1 | 2,311,629 | — | — | — | 2,311,629 | ||||||||||

Other FHLB1 | 34,090 | — | — | — | 34,090 | ||||||||||

State or local housing agency obligations | — | 21,445 | 60,872 | — | 82,317 | ||||||||||

SBA/SBIC | 319,665 | — | — | — | 319,665 | ||||||||||

Mortgage-backed securities (MBS) | 2,864,961 | 1,589,132 | 11,530 | — | 4,465,623 | ||||||||||

Total investment securities | $ | 5,530,345 | $ | 1,610,577 | $ | 72,402 | $ | 449,405 | $ | 7,662,729 | |||||

Further Detail of MBS issued, Guaranteed or Fully insured By: | |||||||||||||||

Pools of Mortgages | |||||||||||||||

Government-sponsored enterprises1 | $ | 1,577,165 | $ | — | $ | — | $ | — | $ | 1,577,165 | |||||

Government-guaranteed | 57,002 | — | — | — | 57,002 | ||||||||||

CMOs/REMICS | |||||||||||||||

Government-sponsored enterprises1 | 1,216,626 | — | — | — | 1,216,626 | ||||||||||

Government-guaranteed | 14,168 | — | — | — | 14,168 | ||||||||||

MPF Shared Funding | — | 425,454 | 11,146 | — | 436,600 | ||||||||||

Privately issued MBS | |||||||||||||||

Non-conforming MBS | — | 62,567 | — | — | 62,567 | ||||||||||

CMOs/REMICS | — | 40,486 | 384 | — | 40,870 | ||||||||||

Asset Backed Securities | — | 312,725 | — | — | 312,725 | ||||||||||

Home Equity Loans | — | 747,900 | — | — | 747,900 | ||||||||||

Total Mortgage Backed Securities | $ | 2,864,961 | $ | 1,589,132 | $ | 11,530 | $ | — | $ | 4,465,623 | |||||

| 1 | Securities issued by government sponsored enterprises are not guaranteed by the U.S. federal government. |

15

Table of Contents

Investment Securities

December 31, 2004

(Dollars in thousands) | Long Term Rating | Short Term Rating | |||||||||||||

Total Portfolio | U.S. Government Agency and Government Sponsored Enterprises | AAA | AA | A-1 or Higher | Total | ||||||||||

Commercial paper | $ | — | $ | — | $ | — | $ | 699,722 | $ | 699,722 | |||||

Government-sponsored enterprises1 | 1,731,387 | — | — | — | 1,731,387 | ||||||||||

Other FHLB1 | 71,731 | — | — | — | 71,731 | ||||||||||

State or local housing agency obligations | — | 32,080 | 68,610 | — | 100,690 | ||||||||||

SBA/SBIC | 743,193 | — | — | — | 743,193 | ||||||||||

Mortgage-backed securities (MBS) | 3,198,200 | 2,294,138 | 11,845 | — | 5,504,183 | ||||||||||

Total investment securities | $ | 5,744,511 | $ | 2,326,218 | $ | 80,455 | $ | 699,722 | $ | 8,850,906 | |||||

Further Detail of MBS issued, Guaranteed or Fully insured By: | |||||||||||||||

Pools of Mortgages | |||||||||||||||

Government-sponsored enterprises1 | $ | 1,786,593 | $ | — | $ | — | $ | — | $ | 1,786,593 | |||||

Government-guaranteed | 74,984 | — | — | — | 74,984 | ||||||||||

CMOs/REMICS | |||||||||||||||

Government-sponsored enterprises1 | 1,316,163 | — | — | — | 1,316,163 | ||||||||||

Government-guaranteed | 20,460 | — | — | — | 20,460 | ||||||||||

MPF Shared Funding | — | 501,697 | 11,285 | — | 512,982 | ||||||||||

Non-Federal Agency MBS | |||||||||||||||

Non-conforming MBS | — | 85,177 | — | — | 85,177 | ||||||||||

CMOs/REMICS | — | 50,741 | 560 | — | 51,301 | ||||||||||

Asset Backed Securities | — | 366,797 | — | — | 366,797 | ||||||||||

Home Equity Loans | — | 1,289,726 | — | — | 1,289,726 | ||||||||||

Total Mortgage Backed Securities | $ | 3,198,200 | $ | 2,294,138 | $ | 11,845 | $ | — | $ | 5,504,183 | |||||

| 1 | Securities issued by government sponsored enterprises are not guaranteed by the U.S. federal government. |

16

Table of Contents

Investment Securities

December 31, 2003

(Dollars in thousands) | Long Term Rating | Short Term Rating | |||||||||||||

Total Portfolio | U.S. Government Agency and Government Sponsored Enterprises | AAA | AA | A-1 or Higher | Total | ||||||||||

U.S. Treasury obligations | $ | 50,246 | $ | — | $ | — | $ | — | $ | 50,246 | |||||

Commercial paper | — | — | — | 99,991 | 99,991 | ||||||||||

Government-sponsored enterprises1 | 1,608,285 | — | — | — | 1,608,285 | ||||||||||

Other FHLB1 | 75,700 | — | — | — | 75,700 | ||||||||||

State or local housing agency obligations | — | 43,795 | 88,593 | — | 132,388 | ||||||||||

SBA/SBIC | 598,981 | — | — | — | 598,981 | ||||||||||

Mortgage-backed securities (MBS) | 1,321,842 | 2,638,647 | 12,648 | — | 3,973,137 | ||||||||||

Total investment securities | $ | 3,655,054 | $ | 2,682,442 | $ | 101,241 | $ | 99,991 | $ | 6,538,728 | |||||

Further Detail of MBS issued, Guaranteed or Fully insured By: | |||||||||||||||

Pools of Mortgages | |||||||||||||||

Government-sponsored enterprises1 | $ | 1,001,887 | $ | — | $ | — | $ | — | $ | 1,001,887 | |||||

Government-guaranteed | 112,775 | — | — | — | 112,775 | ||||||||||

CMOs/REMICS | |||||||||||||||

Government-sponsored enterprises1 | 183,947 | — | — | — | 183,947 | ||||||||||

Government-guaranteed | 23,233 | — | — | — | 23,233 | ||||||||||

MPF Shared Funding | — | 610,004 | 11,455 | — | 621,459 | ||||||||||

Non-Federal Agency MBS | |||||||||||||||

Non-conforming MBS | — | 165,941 | — | — | 165,941 | ||||||||||

CMOs/REMICS | — | 134,252 | 1,193 | — | 135,445 | ||||||||||

Asset Backed Securities | — | 397,514 | — | — | 397,514 | ||||||||||

Home Equity Loans | — | 1,330,936 | — | — | 1,330,936 | ||||||||||

Total Mortgage Backed Securities | $ | 1,321,842 | $ | 2,638,647 | $ | 12,648 | $ | — | $ | 3,973,137 | |||||

| 1 | Securities issued by government sponsored enterprises are not guaranteed by the U.S. federal government. |

Deposits

Deposit programs provide a portion of the Banks’ funding resources. The Bank accepts deposits from its members, institutions eligible to become members, any institution for which it is providing correspondent services, other FHLBs, or other government instrumentalities. The Bank offers several types of deposit programs to its deposit customers including demand, overnight, and term deposits.

For a description of the Bank’s liquidity requirements with respect to deposits see “Item 2.2—Management’s Discussion and Analysis of Financial Conditions and Results of Operations—Liquidity and Capital Resources—Liquidity.”

17

Table of Contents

The tables below present the maturities for term deposits in denominations of $100 thousand or more:

(Dollars in thousands) | |||||||||

By remaining maturity | September 30, 2005 | December 31, 2004 | December 31, 2003 | ||||||

3 months or less | $ | 39,000 | $ | 28,000 | $ | 472,250 | |||

Over 3 months but within 6 months | 1,000 | 59,000 | 51,000 | ||||||

Over 6 months but within 12 months | 1,000 | 2,000 | 15,150 | ||||||

Total | $ | 41,000 | $ | 89,000 | $ | 538,400 | |||

Mortgage Partnership Finance® Program

Introduction

The MPF® Program is a unique secondary mortgage market structure under which participating FHLBs (“MPF Banks”) serve as a source of liquidity to their participating financial institution members (“PFIs”) who originate mortgage loans. The MPF Banks do this by either purchasing mortgage loans after they have been originated by the PFIs or, alternatively, by funding the mortgage loans themselves. In this regard, the mortgage loans purchased or funded are held on the MPF Bank’s balance sheet.

Under the MPF 100 product, the MPF Bank table funds MPF Loans, which means that the MPF Bank provides the funds, through the PFI as its agent, to make the MPF Loan to the borrower. The PFI performs all the traditional retail loan origination functions under this and all MPF products. The MPF Bank is considered the originator of the MPF Loan for accounting purposes since the PFI is acting as its agent when originating the MPF Loan. This differs from other MPF products in which the MPF Bank purchases loans that have already been closed by the PFI with its own funds. See “– MPF Products” for a description of products offered under the MPF Program.

The current MPF Banks are the Federal Home Loan Banks of: Atlanta, Boston, Chicago, Dallas, Des Moines, New York, Pittsburgh, San Francisco and Topeka. The Federal Home Loan Bank of Chicago acts as “MPF Provider” and provides programmatic and operational support to the MPF Banks and their PFIs.

MPF Program assets are qualifying conventional conforming and Government (i.e., FHA insured and VA guaranteed) fixed-rate mortgage loans and participations in pools of such mortgage loans, secured by one-to-four family residential properties, with maturities ranging from 5 to 30 years (“MPF Loans”). The Finance Board’s Acquired Member Asset regulation (12 C.F.R. § 955) (“AMA Regulation”) requires MPF Loans to be funded or purchased by the MPF Banks through or from PFIs and to be credit enhanced in part by the PFIs. MPF Banks generally acquire whole loans from their respective PFIs but may also acquire them from a member of another MPF Bank with permission of the PFI’s respective MPF Bank or may acquire participations from another MPF Bank. The AMA Regulation authorizes MPF Banks to fund loans, which the Bank does through funding arrangements with PFIs. The acquisition of eligible Bank funded loans and closed loans is consistent with and authorized as a core mission activity under the Finance Board regulations.

The Bank, in its role as MPF Provider, establishes the eligibility standards under which an MPF Bank member may become a PFI, establishes the structure of MPF products and the eligibility rules for MPF Loans, manages the pricing and delivery mechanism for MPF Loans, and manages the back-office processing of MPF Loans in its role as master servicer. The Bank publishes and maintains the MPF Origination Guide and MPF Servicing Guide (together “MPF Guides”), which detail the rules PFIs must follow in originating or selling and servicing MPF Loans. When a PFI fails to comply with the requirements of the PFI Agreement, MPF Guides, applicable law or terms of mortgage documents, the PFI may be required to repurchase the MPF Loans which are impacted by such failure. Reasons for which a PFI could be required to repurchase an MPF Loan may include but are not limited to MPF Loan ineligibility, failure to perfect collateral with an approved custodian, a servicing breach, fraud, or other misrepresentation.

For the nine months ended September 30, 2005 and 2004, respectively, the Bank’s PFIs were required to repurchase 0.03% and 0.02% of the average daily balance of conventional outstanding MPF Loans, respectively, for a total of $11.5 million

18

Table of Contents

and $9.4 million, respectively. Annually, in each of the three years ended December 31, 2004, 2003 and 2002, the Banks’ PFIs were required to repurchase less than 0.03% of the average daily balance of conventional MPF Loans outstanding for a total of $13.1 million, $9.8 million and $2.0 million, respectively. The Bank has not experienced any losses related to these conventional MPF Loan repurchases.

Without limiting or waiving the PFIs obligation as servicer to advance principal and interest under the scheduled/scheduled servicing option, the PFI may, under the terms of the MPF Servicing Guide, elect to repurchase any Government MPF Loan for an amount equal to 100 percent of the Government MPF Loan’s then current scheduled principal balance and accrued interest thereon provided there has been no payment made by the borrower for three consecutive months. This policy allows PFIs to comply with loss mitigation requirements of FHA, VA and HUD in order to preserve the insurance or guaranty coverage. In addition, just as for conventional MPF Loans, if a PFI fails to comply with the requirements of the PFI Agreement, MPF Guides, applicable law or terms of mortgage documents, the PFI may be required to repurchase the Government MPF Loans which are impacted by such failure. In the nine months ended September 30, 2005 and 2004, the Bank’s PFIs repurchased Government MPF Loans totaling $74.7 million and $8.7 million, respectively, which represents 1.13% and 0.13% of the average daily balance of Government MPF Loans outstanding during these respective periods. For the years ended December 31, 2004, 2003 and 2002, the Bank’s PFIs repurchased Government MPF Loans totaling $14.8 million, $75.8 million and $131.5 million, respectively, which represents 0.23%, 0.94% and 1.93% of the average daily balance of Government MPF Loans outstanding during these respective periods. The increase in Government MPF Loan repurchases during the nine months ended September 30, 2005 was the result of a change in repurchase policy by one of the Bank’s PFIs. In April 2005, one of the Bank’s PFIs changed its repurchase policy to seek approval to repurchase its Government MPF Loans immediately upon their becoming greater than ninety days past due, which is permitted within the Bank’s MPF Servicing Guide. Prior to the PFI’s internal change in policy, a majority of its repurchases occurred over a greater period of time after the MPF Loans became ninety days past due. The Bank has not experienced any losses related to the repurchase of Government MPF Loans.

PFIs are paid a credit enhancement fee as an incentive to minimize credit losses and share in the risk of loss on MPF Loans and to pay for Supplemental Mortgage Insurance (“SMI”), rather than paying a guaranty fee to other secondary market purchasers. These fees are paid monthly and are determined based on the remaining unpaid principal balance of the MPF Loans. The required credit enhancement obligation amount may vary depending on the MPF product alternatives selected. Credit enhancement fees, payable to a member as compensation for assuming credit risk, are recorded as an offset to mortgage loan interest income when paid by the Bank. The Bank also pays performance credit enhancement fees which are based on actual performance of the mortgage loans. In general, performance based fees are net of cumulative unrecovered losses paid by the Bank. To the extent that losses in the current month exceed performance credit enhancement fees accrued, the remaining losses are recovered from future performance credit enhancement fees payable to the member. The Bank recorded total credit enhancement fees of $35.4 million and $38.4 million for the nine months ended September 30, 2005 and 2004, respectively. The Bank recorded total credit enhancement fees of $51.0 million, $39.4 million and $18.1 million for the years ended December 31, 2004, 2003 and 2002, respectively.

The MPF Program has grown to $82.0 billion (at par) in outstanding assets for all MPF Banks at September 30, 2005, of which $43.4 billion (par value) were owned or participated in by the Bank and the remaining $38.6 billion (par value) were owned or participated in by the other MPF Banks. More than 930 commercial banks, thrifts, credit unions and insurance companies are approved PFIs that deliver MPF Loans into the MPF Program secured by homes in all 50 states, the District of Columbia and Puerto Rico.

At September 30, 2005 and December 31, 2004 and 2003, the Bank had $43.2 billion, $46.9 billion and $47.6 billion of MPF Loans outstanding, respectively. As of September 30, 2005, the Bank had 304 members that were approved as PFIs; 230 of those PFIs actively participated in the MPF Program during the nine months ended September 30, 2005. The Bank acquired $1.5 billion and $3.5 billion in MPF Loans from or through the Bank’s PFIs in the nine months ended September 30, 2005 and 2004, respectively; and acquired $4.1 billion, $15.9 billion and $5.8 billion in the three years ended December 31, 2004, 2003 and 2002, respectively, from or through the Bank’s PFIs. Of these purchases, the Bank participated out $878.9 million in participation interests to the FHLB of Topeka during the year ended December 31, 2004 under the MPF Program. The Bank did not transfer any participation interests to other FHLBs in the nine months ended September 30, 2005 and during the years ended December 31, 2003 and 2002. The Bank purchased participation interests from other FHLBs totaling $1.6 billion and $4.5 billion in the nine months ended September 30, 2005 and 2004, respectively. The Bank purchased participation interests from other FHLBs totaling $4.9 billion, $20.9 billion and $10.7 billion in the years ended December 31, 2004, 2003 and 2002, respectively.

19

Table of Contents

The Bank has been acquiring fewer participation interests in the MPF Loans of other MPF Banks. Instead the Bank has been charging a fee for acting as MPF Provider. In December 2003, the Bank began purchasing MPF Loans directly from PFIs of the FHLB of Dallas. The FHLB of Dallas acts as marketing agent for the Bank and receives a fee for its services rather than purchasing MPF Loans from its PFIs. Direct acquisitions from another FHLB’s members are permitted under the AMA Regulation with the consent of that FHLB. The Bank elected to purchase whole MPF Loans instead of participations in this instance because whole loans are more liquid assets than participation interests. The Bank purchased MPF Loans from the FHLB of Dallas’ PFIs totaling $162.9 million and $336.0 million during the nine months ending September 30, 2005 and 2004, respectively. The Bank purchased MPF Loans from the FHLB of Dallas’ PFIs totaling $568.9 million and $1.2 billion for the periods ending December 31, 2004 and 2003, respectively.

The MPF Program is designed to allocate the risks of MPF Loans among the MPF Banks and PFIs and to take advantage of their respective strengths. PFIs have direct knowledge of their mortgage markets and have developed expertise in underwriting and servicing residential mortgage loans. By allowing PFIs to originate MPF Loans, whether through retail or wholesale operations, and to retain or acquire servicing of MPF Loans, the MPF Program gives control of those functions that most impact credit quality to PFIs. The credit enhancement structure motivates PFIs to minimize MPF Loan losses. The MPF Banks are responsible for managing the interest rate risk, prepayment risk and liquidity risk associated with owning MPF Loans.

The MPF Program was established to help fulfill the FHLBs’ housing finance mission. The Finance Board’s regulations define the acquisition of AMA or “acquired member assets” as a core mission activity of the FHLBs. The MPF Program offers a structure in which the risk of loss associated with MPF Loans is shared with the PFIs while allowing the Bank to diversify its assets beyond its Traditional Member Finance.

Mortgage Standards

The MPF Guides set forth the eligibility standards for MPF Loans. PFIs are free to use an approved automated underwriting system or to underwrite MPF Loans manually when originating or acquiring loans though the loans must meet MPF Program underwriting and eligibility guidelines outlined in the MPF Origination Guide. In some circumstances, a PFI may be granted a waiver exempting it from complying with specified provisions of the MPF Guides.

The current underwriting and eligibility guidelines with respect to MPF Loans are broadly summarized as follows:

| • | Conforming loan size, which is established annually as required by the AMA Regulation and may not exceed the loan limits permitted to be set by the Office of Federal Housing Enterprise Oversight (“OFHEO”) each year; |

| • | Fixed-rate, fully-amortizing loans with terms from 5 to 30 years; |

| • | Secured by first liens on residential owner occupied primary residences and second homes; primary residences may be up to four units; |

| • | Condominium, planned unit development and manufactured homes are acceptable property types as are mortgages on leasehold estates (though manufactured homes must be on land owned in fee simple by the borrower); |

| • | 95% maximum loan-to-value ratio (“LTV”); except for FHLB AHP mortgage loans which may have LTVs up to 100% (but may not exceed 105% total LTV, which compares the property value to the total amount of all mortgages outstanding against a property) and Government MPF Loans which may not exceed the LTV limits set by FHA and VA; |

| • | MPF Loans with LTVs greater than 80% require certain amounts of mortgage guaranty insurance (“MI”), called primary MI, from an MI company rated at least “AA” or “Aa” and acceptable to S&P; |

| • | Unseasoned or current production with up to five payments made by the borrowers; |

| • | Credit reports and credit scores for each borrower; for borrowers with no credit score, alternative verification of credit is permitted; |

| • | Analysis of debt ratios; |

| • | Verification of income and sources of funds, if applicable; |

| • | Property appraisal; |

| • | Customary property or hazard insurance, and flood insurance, if applicable, from insurers acceptably rated as detailed in the MPF Guides; |

| • | Title insurance or, in those areas where title insurance is not customary, an attorney’s opinion of title; |

| • | The mortgage documents, mortgage transaction and mortgaged property must comply with all applicable laws and loans must be documented using standard Fannie Mae/Freddie Mac Uniform Instruments; |

20

Table of Contents

| • | Loans that are not ratable by a rating agency are not eligible for delivery under the MPF Program; and |

| • | Loans that are classified as high cost, high rate, high risk, Home Ownership and Equity Protection Act (HOEPA) loans or loans in similar categories defined under predatory lending or abusive lending laws are not eligible for delivery under the MPF Program. |

In addition to the underwriting guidelines, the MPF Guides contain MPF Program policies which include anti-predatory lending policies, eligibility requirements for PFIs such as insurance requirements and annual certification requirements, loan documentation and custodian requirements, as well as detailing the PFI’s servicing duties and responsibilities for reporting, remittances, default management and disposition of properties acquired by foreclosure or deed in lieu of foreclosure.

Upon any MPF Loan becoming 90 days or more delinquent, the master servicer monitors and reviews the PFI’s default management activities for that MPF Loan, including timeliness of notices to the mortgagor, forbearance proposals, property protection activities, and foreclosure referrals, all in accordance with the MPF Guides. Upon liquidation of any MPF Loan and submission of each realized loss calculation from the PFI, the master servicer reviews the realized loss calculation for conformity with the primary mortgage insurance requirements, if applicable, and conformity to the cost and timeliness standards of the MPF Guides, and disallows the reimbursement to the PFI of any servicing advances related to the PFI’s failure to perform in accordance with the MPF Guides standards.

During the third quarter of 2005, the Bank announced a special disaster relief initiative to lessen the hardship for victims of Hurricane Katrina. See “Item 1.2 – Business Segments – Mortgage Partnership Finance® – MPF® Servicing” for additional information.

Services Agreement

MPF Loans are delivered to each MPF Bank through the infrastructure maintained by the Bank, which includes both a telephonic delivery system and a web based delivery system accessed through the eMPF® website. The Bank has entered into an agreement (“Services Agreement”) with each of the other MPF Banks to make the MPF Program available to their respective PFIs. The Services Agreement sets forth the terms and conditions of the MPF Bank’s participation in the MPF Program. The Services Agreement outlines the Bank’s agreement to provide transaction processing services to the MPF Banks, including acting as master servicer and master custodian for the MPF Banks with respect to the MPF Loans. The Bank has engaged Wells Fargo Bank N.A. as its vendor for master servicing and as the primary custodian for the MPF Program, and has also contracted with other custodians meeting MPF Program eligibility standards at the request of certain PFIs. Such other custodians are typically affiliates of PFIs and in some cases a PFI acts as self-custodian.

Historically, in order to compensate the Bank, as MPF Provider, for its transaction processing services, the Bank has required that each of the MPF Banks sell to it not less than a twenty-five percent (25%) participation interest in MPF Loans acquired by that MPF Bank. Currently, all but one of the MPF Banks compensate the MPF Provider for its transaction processing services by paying a transactions services fee instead of granting the MPF Provider the right to purchase a participation interest with respect to MPF Loans acquired after 2003. One MPF Bank continues to compensate the MPF Provider for its transaction processing services by selling to the Bank not less than twenty-five percent (25%) participation interests in its MPF Loans. The Bank recorded $2.2 million and $812.1 thousand as transaction services fees in the nine months ended September 30, 2005 and 2004, respectively. The Bank recorded $1.2 million in transaction service fees for the year ended December 31, 2004, which was the first year in which the Bank recorded such fees.

In addition to buying participation interests as compensation for providing transaction processing services, the Bank may purchase participation interests in MPF Loans through an agreement with the relevant MPF Bank, and may also sell participation interests to other MPF Banks at the time MPF Loans are acquired, although it is the Bank’s intent to hold all MPF Loans for investment. As such, the participation percentages in MPF Loans may vary by each pool of MPF Loans funded or purchased by the MPF Bank (“Master Commitment”), by agreement of the MPF Bank selling the participation interests (the “Owner Bank”), and the MPF Provider and other MPF Banks purchasing a participation interest. In order to detail the responsibilities and obligations for all participation interests sold by an Owner Bank to the MPF Provider or to other participating MPF Banks, each Owner Bank has entered into a participation agreement with the MPF Provider and, as applicable, any other participant MPF Banks. For an explanation of participation arrangements, see “Item 1.2—Business Segments—Mortgage Partnership Finance Program—MPF Bank Participations.”

MPF Loans are funded through or purchased directly from PFIs by MPF Banks through the transactional services provided by the Bank. Under the Services Agreement between the MPF Bank and the Bank, the Bank provides the necessary systems for PFIs to deliver MPF Loans to the MPF Bank, establishes daily pricing for MPF Loans, prepares reports for both the PFI and the MPF Bank, and provides quality control services on purchased MPF Loans.

21

Table of Contents

The Bank calculates and publishes on its eMPF website pricing grids with the prices expiring at midnight the following day. The prices, rates and fees associated with the various MPF products are set by the Bank, in its role of MPF Provider, using observable third party pricing sources as inputs to its proprietary pricing model. If market prices move beyond preset ranges, the Bank will reset all or some of the prices at any time during a given business day. In limited circumstances, an MPF Bank may elect to apply alternative pricing to a specific pool of MPF Loans delivered by one of its PFIs.

Participating Financial Institution Agreement

A member (or eligible housing associate) of an MPF Bank must specifically apply to become a PFI. The MPF Bank reviews the general eligibility of the member while the Bank, as MPF Provider, reviews the member’s servicing qualifications and ability to supply documents, data and reports required to be delivered by PFIs under the MPF Program. The member and its MPF Bank sign an MPF Program Participating Financial Institution Agreement (“PFI Agreement”) that creates a relationship framework for the PFI to do business with its MPF Bank. The PFI Agreement provides the terms and conditions for the origination of the MPF Loans to be funded or purchased by the MPF Bank and establishes the terms and conditions for servicing MPF Loans for the MPF Bank. If a member is an affiliate of a holding company which has another affiliate that is an active PFI, the member is only eligible to become a PFI if it is a member of the same MPF Bank as the existing PFI. The eligibility requirements for holding company affiliates do not apply to the Mortgage Purchase Program but pertain solely to participation in the MPF Program. The Bank does not participate in the Mortgage Purchase Program, a competing program offered by other FHLBs, which may include member participants that are affiliates of PFIs participating in the MPF Program.

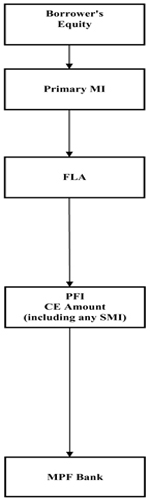

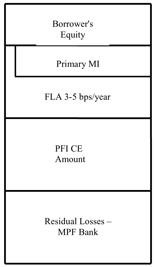

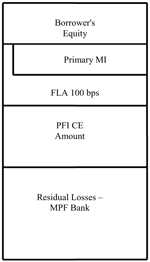

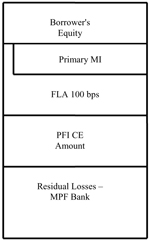

The PFI’s credit enhancement obligation (“CE Amount”) arises under its PFI Agreement while the amount and nature of the obligation are determined with respect to each Master Commitment. Under the AMA Regulation the PFI must “bear the economic consequences” of certain losses with respect to a Master Commitment based upon the MPF product and other criteria.

The PFI’s CE Amount for a Master Commitment covers the loan losses for that Master Commitment in excess of the first loss account (“FLA”), if any, up to an agreed upon amount. The final CE Amount is determined once the Master Commitment is closed (i.e., when the maximum amount of MPF Loans are delivered or the expiration date has occurred).

The table below summarizes the average CE Amount as a percentage of MPF Program Master Commitments participated in or held by the Bank:

MPF Program PFI CE Amount as % of

Master Commitments Participated in or Held by the Bank

| As of September 30, | As of December 31, | |||||||||||

| 2005 | 2004 | 2003 | 2002 | |||||||||

Original MPF | 1.73 | % | 1.64 | % | 1.53 | % | 1.97 | % | ||||

MPF 100 | 0.49 | % | 0.44 | % | 0.39 | % | 0.46 | % | ||||

MPF 125 | 0.82 | % | 0.71 | % | 0.59 | % | 0.76 | % | ||||

MPF Plus * | 1.34 | % | 1.35 | % | 1.37 | % | 1.77 | % | ||||

Original MPF for FHA/VA | N/A | N/A | N/A | N/A | ||||||||

| * | CE Amount includes SMI policy coverage |

The risk characteristics of each MPF Loan (as provided by the PFI) are analyzed by the MPF Provider using S&P’s LEVELS® model in order to determine the required CE Amount for a loan or group of loans to be funded or acquired by an MPF Bank (“MPF Program Methodology”) but which leaves the decision whether or not to deliver the loan or group of loans into the MPF Program with the PFI.

22

Table of Contents

The AMA Regulation provides the authority for the Bank’s investment in residential mortgage loans. As required by the AMA Regulation, the MPF Program credit enhancement methodology has been confirmed by S&P, a NRSRO, as providing an analysis of each Master Commitment that is “comparable to a methodology that the NRSRO would use in determining credit enhancement levels when conducting a rating review of the asset or pool of assets in a securitization transaction.” The AMA Regulation requires that MPF Loans be credit enhanced sufficient so that the risk of loss is limited to the losses of an investor in an “AA” rated mortgage backed security, unless additional retained earnings plus a general allowance for losses are maintained. The Bank is required to recalculate the estimated credit rating of a Master Commitment if there is evidence of a decline in credit quality of the related MPF Loans. The required amount of additional retained earnings is an amount equal to the outstanding balance of the MPF Loans under the related Master Commitment multiplied by the applicable factor listed below that is associated with the putative credit rating of the Master Commitment.

Putative rating of single-family mortgage assets | Percentage applicable to on-balance sheet equivalent value of AMA | ||

Third highest investment grade | 0.90 | % | |

Fourth highest investment grade | 1.50 | % | |

If downgraded to below investment grade after acquisition by Bank: | |||

Highest below investment grade | 2.25 | % | |

Second highest below investment grade | 2.60 | % | |

All other below investment grade | 100.00 | % |

For purposes of determining the appropriate amount of additional retained earnings as described in the preceding paragraph, the Bank must determine the estimated rating of the pool of MPF Loans for each Master Commitment. This determination is made based upon the MPF Program Methodology under S&P’s LEVELS program and the product type of the related MPF Loans. For a description of the different MPF product types and the calculation of the PFI’s CE Amount by product type see “Item 1.2—Business Segments—Mortgage Partnership Finance Program—MPF Products.”

The estimated rating for each Master Commitment is based upon the size of the PFI’s CE Amount and the Bank’s effective FLA exposure (after consideration of the Bank’s ability to reduce a PFI’s performance based credit enhancement fees) so that the Bank is in a position equivalent to that of an investor in a “AA” mortgage backed security. However, in June of 2002, the Bank agreed with the Finance Board that in determining the estimated rating for Master Commitments with an FLA equal to 100 basis points (all MPF 100, MPF 125 and some MPF Plus Master Commitments), the Bank will only partially rely on its ability to reduce performance based credit enhancement fees when measuring the Bank’s effective FLA exposure. As a result, the Bank either holds additional retained earnings against the related Master Commitments in accordance with the AMA regulations or purchases SMI to upgrade the estimated rating of the Master Commitment to the equivalent of a “AA” rated mortgage backed security. As of September 30, 2005, the outstanding balance of MPF Loans for which the Bank has purchased SMI in order to increase the estimated credit rating of a Master Commitment is $4.1 billion.

Under the MPF Program, the PFI’s credit enhancement may take the form of a direct liability to pay losses incurred with respect to that Master Commitment, or may require the PFI to obtain and pay for an SMI policy insuring the MPF Bank for a portion of the losses arising from the Master Commitment, or the PFI may contract for a contingent performance based credit enhancement fee whereby such fees are reduced by losses up to a certain amount arising under the Master Commitment. Under the AMA Regulation, any portion of the CE Amount that is a PFI’s direct liability must be collateralized by the PFI in the same way that advances from the MPF Bank are collateralized. The PFI Agreement provides that the PFI’s obligations under the PFI Agreement are secured along with other obligations of the PFI under its regular advances agreement with the MPF Bank and further, that the MPF Bank may request additional collateral to secure the PFI’s obligations.

Typically, a PFI will sign one Master Commitment to cover all the conventional MPF Loans it intends to deliver to the MPF Bank in a year. However, a PFI may also sign a Master Commitment for Government MPF Loans, it may choose to deliver MPF Loans under more than one conventional product, or it may choose to use different servicing remittance options and thus have several Master Commitments opened at any one time. Master Commitments may be for shorter periods than one year and may be extended or increased by agreement of the MPF Bank and the PFI. The Master Commitment defines the pool of MPF Loans for which the CE Amount is set so that the risk associated with investing in such pool of MPF Loans is equivalent to investing in a “AA” rated asset without giving effect to the MPF Bank’s obligation to incur losses up to the amount of the initial FLA.

23

Table of Contents

PFIs request funding or purchase commitments (“Delivery Commitments”) from their respective MPF Bank based on the Bank’s published daily pricing schedules. The PFI enters into a Delivery Commitment, which is a mandatory commitment of the PFI to sell or originate eligible mortgage loans.