1 SHAREHOLDER UPDATE SPRING 2009 * * * * * * * Exhibit 99.1 |

2 FORWARD LOOKING STATEMENT INFORMATION This presentation may include "forward-looking statements, " which include statements that are based on the Bank’s expectations, estimates, projections and assumptions, including those that relate to the availability and cost of funding, the Bank's liquidity needs and dividends. These statements involve known and unknown risks and uncertainties, many of which may be beyond our control. Actual future results may be materially different from the future results expressed or implied by the forward-looking statements. These forward-looking statements may not be realized due to a variety of factors, including, without limitation: FHLBank Atlanta’s net income results, which drive the determination of dividend payments; legislative and regulatory actions or changes; future economic and market conditions; changes in demand for advances or consolidated obligations of FHLBank Atlanta and/or the FHLBank System; changes in interest rates; political, national and world events; and adverse developments or events affecting or involving other Federal Home Loan Banks or the FHLBank System in general. Additional factors that might cause FHLBank Atlanta’s results to differ from these forward-looking statements are provided in detail in our filings with the Securities and Exchange Commission, which are available at www.sec.gov. |

3 TOPICS • FHLBank Atlanta Financial Review • FHLBank System Issues • Credit and Collateral • Advances |

4 FHLBANK ATLANTA 4 TH QUARTER 2008 • Net Income of $74.6 million • Other-Than-Temporary Impairments (OTTI) charge of $98.7 million • No dividend • Increased Retained Earnings by $74.6 million |

5 FHLBANK ATLANTA FINANCIALS (12/31/2008) • Net Income of $253.8 million • Annual dividend 3.52% – Spread to 3 month LIBOR of 59 bps • Retained Earnings of $434.9 million • Capital/Asset ratio of 4.29% |

6 FACTORS IMPACTING 2008 PERFORMANCE • Lehman Brothers Bankruptcy • Funding • Liquidity • Fair Value Accounting |

7 LEHMAN BROTHERS BANKRUPTCY • One of the Bank’s largest counterparties • Lehman was exposed to Bank • Bank pledged collateral against position • Reserved $170 million |

8 FUNDING • Severe disruption in 3 rd and 4 th quarters • Short-term funding LIBOR minus 50 – 70 bps • Long-term funding LIBOR plus 20 – 50 bps |

9 FAIR VALUE ACCOUNTING • $16 billion in non-agency Mortgage Backed Securities (MBS) • Held to maturity • AAA at purchase • Impacted by illiquidity in market • 3 rd and 4 th quarter charge totaling $186.1 million |

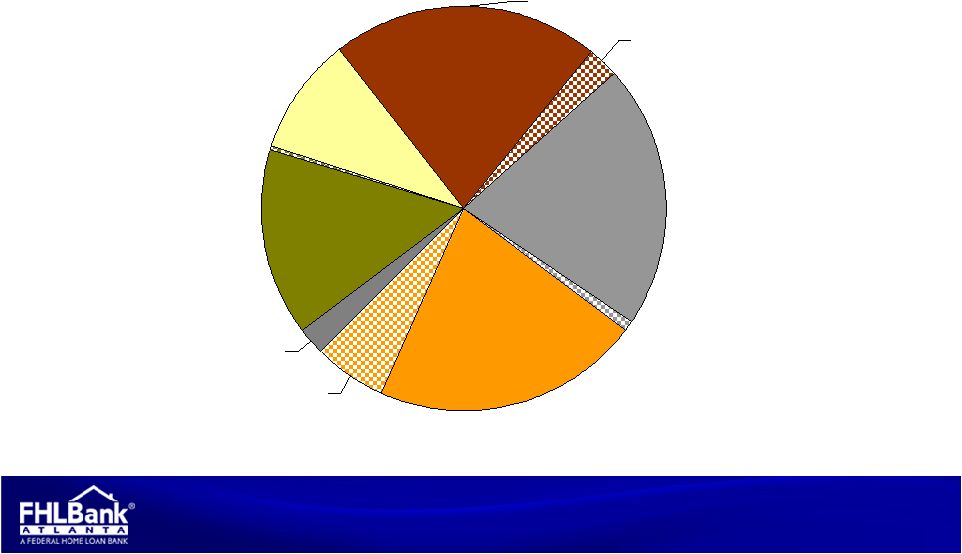

10 MORTGAGE BACKED SECURITIES BREAKDOWN 2008 Prime 2.33% 2007 Prime 14.78% 2007 Alt-A 0.42% 2006 Prime 9.47% 2004 Prime 20.96% 2004 Alt-A 0.97% 2003 & prior Prime 21.17% 2003 & prior Alt-A 5.95% 2005 Alt-A 2.74% 2005 Prime 21.20% Information as of 12/31/08; classifications at issuance |

11 2009 FINANCIALS • Funding • Liquidity • Fair Value Accounting • Advance Levels • Capital – Excess Stock – Dividend |

12 FHLBANK SYSTEM • Federal Housing Finance Agency • Secured lending • Stronger members due to Troubled Asset Relief Program (TARP) and Temporary Liquidity Guarantee Program (TLGP) • Access to Treasury through Credit Facility • FHLBank debt in Federal Reserve buyback program • SEC registrants |

13 FHLBANK SYSTEM • Concerns about exposure to other FHLBanks • FHLBank Atlanta shareholders – FHLBank Atlanta Capital – P&I – Other FHLBank’s Capital • Comparison to Fannie/Freddie |

14 CREDIT AND COLLATERAL • State of the business • Changes in 2009 • Focus on collateral |

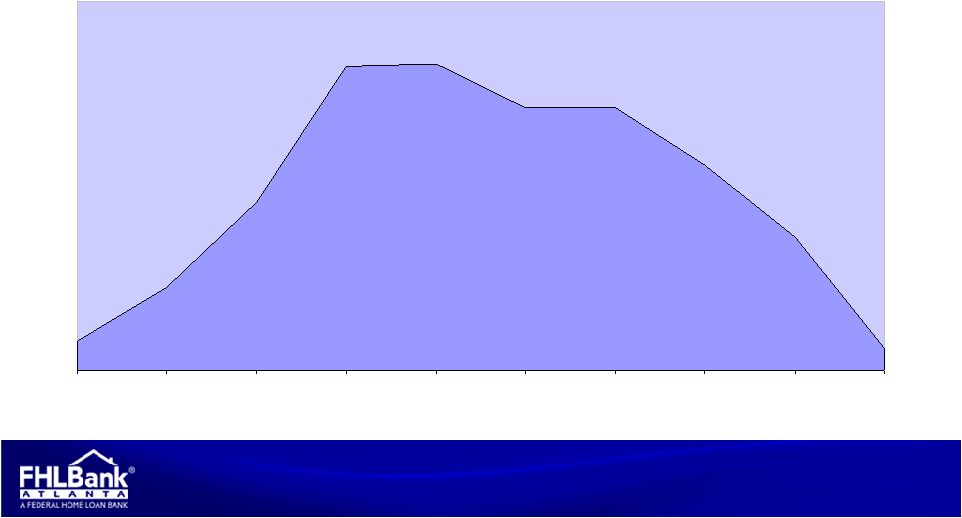

15 12/31/07 CREDIT SCORE DISTRIBUTIONS 1 2 3 4 5 6 7 8 9 10 Pro forma calculation |

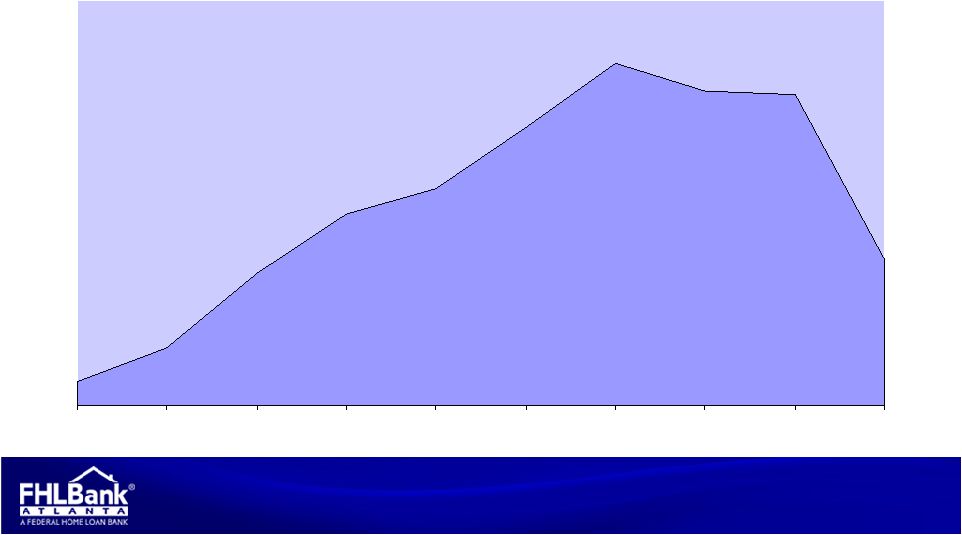

16 12/31/08 CREDIT SCORE DISTRIBUTIONS 1 2 3 4 5 6 7 8 9 10 |

17 AVERAGE RATIOS BY CREDIT SCORE 8.96 9.81 -5.12 6.11 10 10.59 5.93 -1.43 9.41 9 10.75 3.84 -0.21 10.97 8 12.04 1.78 -1.06 16.41 7 13.85 1.67 -0.04 13.12 6 13.29 1.38 0.68 10.07 5 13.94 1.11 0.85 10.74 4 16.66 1.06 2.24 12.08 3 30.61 1.02 1.19 12.36 2 51.20 0.71 1.48 15.18 1 Liquidity % Slow Loans % ROA % Core Capital % Credit Score |

18 IMPACT OF CREDIT SCORE 9 • Required to maintain 110% collateral maintenance level • May be required to deliver loan collateral • Advance terms may be restricted to less than 12 months • May be required to collateralize prepayment fees • Monthly Qualifying Collateral Reports (and loan status updates) may be required |

19 IMPACT OF CREDIT SCORE 10 • Required to maintain 125% collateral maintenance level • Credit Availability may be rescinded • May be required to deliver loan collateral • Advance terms may be restricted to less than 12 months • May be required to collateralize prepayment fees • Monthly Qualifying Collateral Reports (and loan status updates) may be required |

20 CHANGES IN 2009 • Collateral – Now accept medical related office properties – Collateral verification reviews have additional elements – Loans Held for Sale program has been expanded • Upcoming changes to prepay fees • Continue to monitor collateral discounts |

21 ADVANCES • Availability – Short – Long • Structured products – Variable maturity – Fixed maturity • Letter of Credit – Webinar scheduled for April 14, 2009 |

22 SUMMARY • Solid performance in a difficult year • Maintained funding to customers • Challenges ahead – Markets – Credit and collateral – Consolidation |

23 QUESTIONS? * * * * * * * |