UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2011

OR

| ¨ | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from to

Commission File No.: 000-51826

MERCER INTERNATIONAL INC.

Exact name of Registrant as specified in its charter

| | |

| Washington | | 47-0956945 |

State or other jurisdiction of incorporation or organization | | IRS Employer Identification No. |

Suite 1120, 700 West Pender Street, Vancouver,

British Columbia, Canada, V6C 1G8

Address of Office

Registrant’s telephone number including area code: (604) 684-1099

Securities registered pursuant to Section 12(b) of the Act:

| | |

Title of each class | | Name of each exchange on which registered |

| Common Stock, par value $1.00 | | NASDAQ Global Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Securities Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of theSecurities Exchange Act of 1934during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No ¨

Indicate by check mark whether registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files). Yes x No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| | | | | | |

| Large accelerated filer | | ¨ | | Accelerated filer | | x |

| | | |

| Non-accelerated filer | | ¨ (Do not check if a smaller reporting company) | | Smaller reporting company | | ¨ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

The aggregate market value of the registrant’s voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2011, the last business day of the registrant’s most recently completed second fiscal quarter, based on the closing price of the voting stock on the NASDAQ Global Market on such date, was approximately $461,949,697.

As of February 17, 2012, the registrant had 55,779,204 shares of common stock, $1.00 par value, outstanding.

DOCUMENTS INCORPORATED BY REFERENCE

Certain information that will be contained in the definitive proxy statement for the Registrant’s annual meeting to be held in 2012 is incorporated by reference into Part III of this Form 10-K.

TABLE OF CONTENTS

2

3

EXCHANGE RATES

Our reporting currency and financial statements included in this report are in Euros, as a significant majority of our business transactions are originally denominated in Euros. We translate non-Euro denominated assets and liabilities at the rate of exchange on the balance sheet date. Revenues and expenses are translated at the average rate of exchange prevailing during the period.

The following table sets out exchange rates, based on the noon buying rates in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York (the “Noon Buying Rate”) for the conversion of Euros and Canadian dollars to U.S. dollars in effect at the end of the following periods, the average exchange rates during these periods (based on daily Noon Buying Rates) and the range of high and low exchange rates for these periods:

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended December 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (€/$) | |

End of period | | | 0.7708 | | | | 0.7536 | | | | 0.6977 | | | | 0.7184 | | | | 0.6848 | |

High for period | | | 0.6723 | | | | 0.6879 | | | | 0.6623 | | | | 0.6246 | | | | 0.6729 | |

Low for period | | | 0.7736 | | | | 0.8362 | | | | 0.7970 | | | | 0.8035 | | | | 0.7750 | |

Average for period | | | 0.7186 | | | | 0.7541 | | | | 0.7176 | | | | 0.6826 | | | | 0.7304 | |

| |

| | | (C$/$) | |

End of period | | | 1.0168 | | | | 1.0009 | | | | 1.0461 | | | | 1.2240 | | | | 0.9881 | |

High for period | | | 0.9448 | | | | 0.9960 | | | | 1.0289 | | | | 0.9717 | | | | 0.9168 | |

Low for period | | | 1.0605 | | | | 1.0776 | | | | 1.2995 | | | | 1.2971 | | | | 1.1852 | |

Average for period | | | 0.9887 | | | | 1.0298 | | | | 1.1412 | | | | 1.0660 | | | | 1.0740 | |

On February 10, 2012, the date of the most recent weekly publication of the Noon Buying Rate before the filing of this annual report on Form 10-K, the Noon Buying Rate for the conversion of Euros and Canadian dollars to U.S. dollars was €0.7583 per U.S. dollar and C$1.0016 per U.S. dollar.

In addition, certain financial information relating to our Celgar mill included in this annual report on Form 10-K is stated in Canadian dollars while we report our financial results in Euros. The following table sets out exchange rates, based on the noon rate provided by the Bank of Canada (the “Daily Noon Rate”), for the conversion of Canadian dollars to Euros in effect at the end of the following periods, the average exchange rates during these periods (based on Daily Noon Rates) and the range of high and low exchange rates for these periods:

| | | | | | | | | | | | | | | | | | | | |

| | | Years Ended December 31, | |

| | | 2011 | | | 2010 | | | 2009 | | | 2008 | | | 2007 | |

| | | (C$/€) | |

End of period | | | 1.3193 | | | | 1.3319 | | | | 1.5000 | | | | 1.7046 | | | | 1.4428 | |

High for period | | | 1.2847 | | | | 1.2478 | | | | 1.4936 | | | | 1.4489 | | | | 1.3448 | |

Low for period | | | 1.4305 | | | | 1.5067 | | | | 1.6920 | | | | 1.7316 | | | | 1.5628 | |

Average for period | | | 1.3761 | | | | 1.3671 | | | | 1.5851 | | | | 1.5603 | | | | 1.4690 | |

On February 20, 2012, the Daily Noon Rate for the conversion of Canadian dollars to Euros was C$1.3148 per Euro.

4

PART I

In this document, please note the following:

| | • | | references to “we”, “our”, “us”, the “Company” or “Mercer” mean Mercer International Inc. and its subsidiaries, unless the context clearly suggests otherwise, and references to “Mercer Inc.” mean Mercer International Inc. excluding its subsidiaries; |

| | • | | references to “ADMTs” mean air-dried metric tonnes; |

| | • | | references to “MW” mean megawatts and “MWh” mean megawatt hours; |

| | • | | information is provided as of December 31, 2011, unless otherwise stated or the context clearly suggests otherwise; |

| | • | | all references to monetary amounts are to “Euros”, the lawful currency adopted by most members of the European Union, unless otherwise stated; and |

| | • | | “€” refers to Euros; “$” refers to U.S. dollars; and “C$” refers to Canadian dollars. |

The Company

General

Mercer Inc. is a Washington corporation and our shares of common stock are quoted and listed for trading on the NASDAQ Global Market (MERC) and the Toronto Stock Exchange (MRI.U).

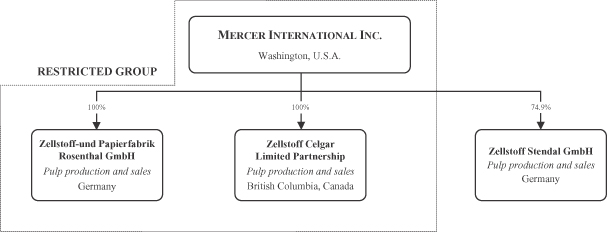

We operate in the pulp business and are the largest publicly traded producer of market northern bleached softwood kraft, or “NBSK”, pulp in the world. We are the sole NBSK producer, and the only significant producer of pulp for resale, known as “market pulp”, in Germany, which is the largest pulp import market in Europe. Our operations are located in Eastern Germany and Western Canada. We currently employ approximately 1,039 people at our German operations, 439 people at our Celgar mill in Western Canada and 17 people at our office in Vancouver, British Columbia, Canada. We operate three NBSK pulp mills with a consolidated annual production capacity of approximately 1.5 million ADMTs:

| | • | | Rosenthal mill. Our wholly-owned subsidiary, Rosenthal, owns and operates a modern, efficient ISO 9001 and 14001 certified NBSK pulp mill that has a current annual pulp production capacity of approximately 345,000 ADMTs. Additionally, the Rosenthal mill is a significant producer of “green” energy and exported 161,286 MWh of electricity in 2011, resulting in approximately €14.9 million in annual revenues. The Rosenthal mill is located near the town of Blankenstein, Germany approximately 300 kilometers south of Berlin. |

| | • | | Celgar mill. Our wholly-owned subsidiary, Celgar, owns and operates the Celgar mill, a modern, efficient ISO 9001 and 14001 certified NBSK pulp mill with an annual pulp production capacity of approximately 520,000 ADMTs. The Celgar mill also produces “green” energy and exported 140,069 MWh of electricity in 2011, resulting in approximately C$14.5 million in annual revenues. The Celgar mill is located near the city of Castlegar, British Columbia, Canada, approximately 600 kilometers east of Vancouver, British Columbia, Canada. |

| | • | | Stendal mill. Our 74.9% owned subsidiary, Stendal, owns and operates a state-of-the-art, single-line, ISO 9001 and 14001 certified NBSK pulp mill that has an annual pulp production capacity of approximately 645,000 ADMTs. The Stendal mill is also a significant producer of “green” energy and exported 350,758 MWh of electricity in 2011, resulting in approximately €32.5 million in annual revenues. The Stendal mill is located near the town of Stendal, Germany, approximately 130 kilometers west of Berlin. |

5

Organizational Chart

The following chart sets out our directly and indirectly owned principal operating subsidiaries, their jurisdictions of organization and their principal activities:

History and Development of Business

We acquired our initial pulp operations in 1994, with the acquisition of our Rosenthal mill. In late 1999, we completed a major capital project which, among other things, converted it to the production of kraft pulp from sulphite pulp, increased its annual production capacity, reduced costs and improved efficiencies. The aggregate cost of this project was approximately €361.0 million, of which approximately €102.0 million was financed through government grants. Subsequent minor capital investments and efficiency improvements have reduced emissions and energy costs and increased the Rosenthal mill’s annual production capacity to approximately 345,000 ADMTs.

In September 2004, we completed construction of the Stendal mill at an aggregate cost of approximately €1.0 billion. The Stendal mill is one of the largest NBSK pulp mills in Europe. The Stendal mill was financed through a combination of government grants totaling approximately €275.0 million, low-cost, long-term project debt which is largely severally guaranteed by the federal government and a state government in Germany, and equity contributions.

We initially had a 63.6% ownership interest in Stendal and, over time, increased our interest to 74.9%.

We, Stendal and its noncontrolling shareholder are parties to a shareholders’ agreement dated August 26, 2002, as amended, to govern our respective interests in Stendal. The agreement contains terms and conditions customary for these types of agreements, including restrictions on transfers of share capital and shareholder loans other than to affiliates, rights of first refusal on share and shareholder loan transfers, pre-emptive rights and piggyback rights on dispositions of our interest. The shareholders are not obligated to fund any further equity capital contributions to the project. The shareholders’ agreement provides that Stendal’s managing directors are appointed by holders of a simple majority of its share capital. Further, shareholder decisions, other than those mandated by law or for the provision of financial assistance to a shareholder, are determined by a simple majority of Stendal’s share capital.

A significant portion of the capital investments at our German mills, including the construction of the Stendal mill, were financed through government grants. Since 1999, our German mills have benefited from an aggregate €384.9 million in government grants. These grants reduce the cost basis of the assets purchased when the grants are received and are not reported in our income.

6

In February 2005, we acquired the Celgar mill for $210.0 million, of which $170.0 million was paid in cash and $40.0 million was paid in our shares, plus $16.0 million for the defined working capital of the mill. The Celgar mill was completely rebuilt in the early 1990s through a C$850.0 million modernization and expansion project, which transformed it into a modern and competitive producer.

In 2007, we completed a C$28.0 million capital project which improved efficiencies and reliability and, with other measures, increased the Celgar mill’s annual production capacity to 500,000 ADMTs. In September 2010, we completed a capital project, referred to as the “Celgar Energy Project”, to increase the Celgar mill’s production of “green” energy and optimize its power generation capacity, at an aggregate cost of approximately C$64.9 million, of which approximately C$48.0 million was financed by grants from the Canadian federal government. See “—Capital Expenditures”. We have also increased the Celgar mill’s overall annual pulp production capacity to approximately 520,000 ADMTs through increased efficiencies.

Our Competitive Strengths

Our competitive strengths include the following:

| | • | | Modern and Competitive Mills.We operate three large, modern, competitive NBSK pulp mills that produce high quality NBSK pulp, which is a premium grade of kraft pulp. We believe the relative age, production capacity and operating features of our mills provide us with certain manufacturing cost and other advantages over many of our competitors including lower maintenance capital expenditures. |

| | • | | Leading Market Position. Mercer is the largest publicly traded NBSK pulp producer in the world which provides us increased presence and better industry information in the markets in which we operate, and provides for close customer relationships with many large pulp consumers. |

| | • | | Renewable Surplus Energy. Our modern mills generate electricity and steam in their boilers and are generally energy self-sufficient. Such energy is primarily produced from wood residuals which are a renewable carbon neutral source. All of our mills also generate surplus energy which we sell to third parties. Our Rosenthal and Stendal mills benefit from special tariffs under Germany’sRenewable Energy Resources Act, referred to as the “Renewable Energy Act”, which provides for premium pricing and has materially increased their revenues from sales of surplus power. Additionally, our Celgar mill completed the Celgar Energy Project at the end of September 2010 and is party to an electricity purchase agreement, referred to as the “Electricity Purchase Agreement” with the British Columbia Hydro and Power Authority, or “B.C. Hydro”, British Columbia’s primary public utility provider, for the sale of surplus power for ten years. The Celgar Energy Project increased our annual sales of surplus power at our Celgar mill to approximately 140,000 MWh. In total, our mills produced approximately 652,000 MWh of surplus renewable energy in 2011. We believe our generation and sale of surplus renewable “green” energy provides us with a competitive energy advantage over less efficient mills. |

| | • | | Strategic Locations and Customer Service.We are the only significant producer of market pulp in Germany, which is the largest pulp import market in Europe. Due to the proximity of our German mills to most of our European customers, we benefit from lower transportation costs relative to our major competitors. Our Celgar mill, located in Western Canada, is well situated to serve Asian and North American customers. We primarily work directly with customers to capitalize on our geographic diversity, coordinate sales and enhance customer relationships. We believe our ability to deliver high quality pulp on a timely basis and our customer service makes us a preferred supplier for many customers. |

| | • | | Advantageous Capital Investments and Financing.Our German mills are eligible to receive government grants in respect of qualifying capital investments. Over the last twelve years, our German mills have benefited from approximately €384.9 million of such government grants. In addition, in October 2009, our Celgar mill qualified to receive C$57.7 million of credits under the Canadian government’s Pulp and Paper Green Transformation Program, referred to as the “GTP”. These grants |

7

| | reduce the cost basis of the assets purchased when the grants are received and are not reported in our income. Additionally, during the last ten years, capital investments at our German mills have reduced the amount of overall wastewater fees that would otherwise be payable by over €52.8 million. Further, our Stendal mill benefits from German governmental guarantees of its project financing which permitted it to obtain better credit terms and lower interest costs than would otherwise have been available. The project debt of Stendal which matures in 2017, currently bears interest at a substantially fixed rate of 5.28% per annum plus an applicable margin and is non-recourse to our other operations and Mercer Inc. |

| | • | | Proximity of Abundant Fiber Supply.Although fiber is cyclical in both price and supply, there is a significant amount of high-quality fiber within a close radius of each of our mills. This fiber supply, combined with our purchasing power and our current ability to meaningfully switch between whole logs chipped at our mills and sawmill residual chips, enables us to enter into contracts and arrangements which have generally provided us with a competitive fiber supply. |

| | • | | Experienced Management Team.Our directors and senior managers have extensive experience in the pulp and forestry industries. In particular, our Chief Executive Officer has over 17 years’ experience in the pulp industry and has guided the Company’s operations and development over that time. Our Chief Operating Officer and Chief Financial Officer each has over 31 years of industry experience. We also have experienced managers at all of our mills. Our management has a proven track record of implementing new initiatives and programs in order to reduce costs throughout our operations as well as identifying and harnessing new revenue opportunities. |

Corporate Strategy

Our corporate strategy is to create shareholder value by focusing on the expansion of our asset and earnings base. Key features of our strategy include:

| | • | | Focus on NBSK Market Pulp.We focus on NBSK pulp because it is a premium grade kraft pulp and generally obtains the highest price relative to other kraft pulps. Although demand is cyclical, between 2000 and 2010, worldwide demand for softwood kraft market pulp grew at an average of approximately 1.6% per annum. We focus on servicing customers that produce high quality printing and writing paper grades and tissue producers. This allows us to benefit from our stable relationships with paper and tissue manufacturers in Europe and Asia as well as participate in strong growth markets such as China where we also have strong customer relationships. |

| | • | | Maximizing Renewable Energy Realizations. We focus on the generation and sales of surplus renewable energy because there are minimal incremental costs associated with our energy production and thus our surplus electricity sales are highly profitable. In 2011, our mills generated a record 652,113 MWh of electricity resulting in revenues of approximately €58.0 million, compared to 520,005 MWh and approximately €44.2 million in revenues in 2010. We are developing other initiatives to increase our overall energy generation and the amount of and price for our surplus power sales. In early 2012, we announced a project, referred to as “Project Blue Mill”, to increase production and efficiency through debottlenecking initiatives and the installation of a 40 MW steam turbine at our Stendal mill. The new turbine is expected to initially produce an additional 109,000 MWh of surplus energy. Based upon the current production levels of our mills, we expect to sell approximately 700,000 MWh of surplus renewable energy in 2012. We expect energy generation and sales to continue to be a key focus for our mills for the foreseeable future. |

| | • | | Enhancing Long-Term Sustainability/Growth. We continually focus on cost reduction and efficiency initiatives while strategically evaluating and pursuing internal, high return capital projects and growth opportunities in order to enhance cash flows and maximize shareholder value. |

8

| | • | | Operating and Maximizing Returns from our Modern, World-Class Mills.In order to keep our operating costs as low as possible, with a goal of generating positive cash flow in all market conditions, we operate large, modern pulp mills. We believe these production facilities provide us with the best platform to be an efficient and competitive producer of high-quality NBSK pulp without the need for significant sustaining capital. Our modern mills are also generally net exporters of renewable energy. We are constantly reviewing opportunities to enhance and maximize the usage of the strengths of our mills, including through increased energy generation, production of premium grades of pulp and other improvements, to capture the highest returns available. |

The Pulp Industry

General

Pulp is used in the production of paper, tissues and paper-related products. Pulp is generally classified according to fiber type, the process used in its production and the degree to which it is bleached. Kraft pulp is produced through a sulphate chemical process in which lignin, the component of wood which binds individual fibers, is dissolved in a chemical reaction. Chemically prepared pulp allows the wood’s fiber to retain its length and flexibility, resulting in stronger paper products. Kraft pulp can be bleached to increase its brightness. Kraft pulp is noted for its strength, brightness and absorption properties and is used to produce a variety of products, including lightweight publication grades of paper, tissues and paper-related products.

NBSK pulp, which is a bleached kraft pulp manufactured using species of northern softwood, is considered a premium grade because of its strength. It generally obtains the highest price relative to other kraft pulps. Southern bleached softwood kraft pulp is kraft pulp manufactured using southern softwood species and does not possess the strength found in NBSK pulp. NBSK pulp is the sole product of our mills.

The selling price of kraft pulp depends in part on the fiber used in the production process. There are two primary species of wood used as fiber: softwood and hardwood. Softwood species generally have long, flexible fibers which add strength to paper while fibers from species of hardwood contain shorter fibers which lend bulk and opacity. Generally, prices for softwood pulp are higher than for hardwood pulp. Most uses of market kraft pulp, including fine printing papers, coated and uncoated magazine papers and various tissue products, utilize a mix of softwood and hardwood grades to optimize production and product qualities. In recent years, production of hardwood pulp, based on fast growing plantation fiber primarily from Asia and South America, has increased much more rapidly than that of softwood grades that have longer growth cycles. As a result of the growth in supply and lower costs, kraft pulp customers have substituted some of the pulp content in their products to hardwood pulp. Counteracting customers’ increased proportionate usage of hardwood pulp has been the requirement for strength characteristics in finished goods. Paper and tissue makers focus on higher machine speeds and lower basis weights for publishing papers which also require the strength characteristics of softwood pulp. We believe that the ability of kraft pulp users to continue to further substitute hardwood for softwood pulp is limited by such requirements.

Kraft pulp can be made in different grades, with varying technical specifications, for different end uses. High-quality kraft pulp is valued for its reinforcing role in mechanical printing papers, while other grades of kraft pulp are used to produce lower priced grades of paper, including tissues and paper-related products.

Markets

We believe that over 125 million ADMTs of kraft pulp are converted annually into printing and writing papers, tissues, carton boards and other white grades of paper and paperboard around the world. We also believe that approximately one third of this pulp is sold on the open market as market pulp, while the remainder is produced for internal purposes by integrated paper and paperboard manufacturers.

9

Demand for kraft pulp is cyclical in nature and is generally related to global and regional levels of economic activity. In 2008, overall global demand for all kraft pulp types, including softwood, was negatively impacted by the weak global economic conditions and global financial and credit turmoil the world began to experience in the second half of that year and which continued into the first half of 2009. Significant producer shutdowns and curtailments, along with strong demand from China, resulted in an improved supply-demand balance and improved prices in the second half of 2009 through 2010. Although global pulp markets continued to strengthen in the first half of 2011, economic uncertainty in Europe and credit tightening in China resulted in a decrease in demand and weaker pulp prices in the fourth quarter of 2011.

Between 2000 and 2010 worldwide demand for softwood market pulp grew at an average rate of approximately 1.6% annually. Demand for softwood market pulp was negatively impacted by weak global economic conditions in 2009. However, the supply/demand balance for softwood market pulp improved in 2010, primarily due to strong demand in China, the residual effects of the Chilean earthquake that affected mills in that region and the net closure of approximately 3.4 million tonnes of production capacity globally since 2006. Since 2007, demand for softwood market pulp has grown in the emerging markets of Asia, Eastern Europe and Latin America. China in particular has experienced substantial growth and its demand for softwood market pulp grew by approximately 15.9% per annum between 2000 and 2010. China now accounts for approximately 20% of global softwood market pulp demand compared to only 5% in 2000. Western Europe currently accounts for approximately 30% of global softwood market pulp demand.

A measure of demand for kraft pulp is the ratio obtained by dividing the worldwide demand of kraft pulp by the worldwide capacity for the production of kraft pulp, or the “demand/capacity ratio”. An increase in this ratio generally occurs when there is an increase in global and regional levels of economic activity. An increase in this ratio generally indicates greater demand as consumption increases, which often results in rising kraft pulp prices, and a reduction of inventories by producers and buyers. As prices continue to rise, producers continue to run at higher operating rates. However, an adverse change in global and regional levels of economic activity generally negatively affects demand for kraft pulp, often leading buyers to reduce their purchases and relying on existing pulp inventories. As a result, producers run at lower operating rates by taking downtime to limit the build-up of their own inventories. The demand/capacity ratio for softwood kraft pulp was approximately 92% in 2011, approximately 93% in 2010 and approximately 91% in 2009.

A significant factor affecting our market is the amount of closures of old, high-cost capacity. In the four-year period from 2006 to 2009, we estimate approximately 5.3 million tonnes of predominantly NBSK capacity was indefinitely closed. Such closures have been partially offset by approximately 1.9 million tonnes restarted in late 2009 and 2010. The net effect of these closures and restarts is an estimated 3.4 million tonnes of capacity removed from the market. We are aware of only one planned NBSK plant expansion worldwide in the next few years. We believe that the absence of other plant expansions is due in part to fiber supply constraints and high capital costs.

Competition

Pulp markets are large and highly competitive. Producers ranging from small independent manufacturers to large integrated companies produce pulp worldwide. Our pulp and customer services compete with similar products manufactured and distributed by others. While many factors influence our competitive position, particularly in weak economic times, a key factor is price. Other factors include service, quality and convenience of location. Some of our competitors are larger than we are in certain markets and have substantially greater financial resources. These resources may afford those competitors more purchasing power, increased financial flexibility, more capital resources for expansion and improvement and enable them to compete more effectively. Our key NBSK pulp competitors are principally located in Northern Europe and Canada.

10

NBSK Pulp Pricing

Pulp prices are highly cyclical. Global economic conditions, changes in production capacity, inventory levels, and currency exchange rates are the primary factors affecting NBSK pulp list prices. The average annual European list prices for NBSK pulp since 2000 have ranged from a low of approximately $447 per ADMT to a high of $1,030 per ADMT.

Starting in 2006, pulp prices increased steadily from approximately $600 per ADMT in Europe to $870 per ADMT at the end of 2007. These price increases resulted from the closure of several pulp mills, particularly in North America, which reduced NBSK capacity by approximately 1.3 million ADMTs and better demand.

In the second half of 2008, list prices for NBSK pulp decreased markedly due to weak global economic conditions. As a result, list prices for NBSK pulp in Europe decreased from $900 per ADMT in mid-2008 to $635 per ADMT at the end of the year. Such price weakness continued into early 2009 as list prices in Europe fell to approximately $575 per ADMT. Commencing in mid-2009, pulp markets began to strengthen which led to improved prices. Strong demand from China, capacity closures and historically low global inventories for bleached softwood kraft pulp helped support upward price momentum. During the second half of 2009, several price increases raised European list prices by a total of $170 per ADMT to $800 per ADMT by year end. Such price increases were partially offset by the continued weakening of the U.S. dollar versus the Euro and Canadian dollar during the period. In December 2009, list prices for pulp were approximately $800 per ADMT in Europe, $830 per ADMT in North America and $700 per ADMT in China. In 2010, several increases lifted prices to record levels in the middle of the year and at the end of 2010 list prices were near historic highs of $950, $960 and $840 per ADMT in Europe, North America and China, respectively. Although pulp prices remained strong in 2011, reaching record levels of $1,030 per ADMT in Europe and $1,035 and $920 per ADMT in North America and China, respectively, uncertainty concerning the economic situation in Europe, along with credit tightening in China, caused pulp prices to drop to $825 per ADMT in Europe and $890 and $670 per ADMT in North America and China, respectively, by the end of the year. As pulp prices are highly cyclical, there can be no assurance that prices will not decline in the future.

A producer’s net sales realizations are list prices, net of customer discounts, commissions and other selling concessions. While there are differences between NBSK list prices in Europe, North America and Asia, European prices are generally regarded as the global benchmark and pricing in other regions tends to follow European trends. The nature of the pricing structure in Asia is different in that, while quoted list prices tend to be lower than Europe, customer discounts and commissions tend to be lower resulting in net sales realizations that are generally similar to other markets.

The majority of market NBSK pulp is produced and sold by Canadian and Scandinavian producers, while the price of NBSK pulp is generally quoted in U.S. dollars. As a result, NBSK pricing is affected by fluctuations in the currency exchange rates for the U.S. dollar versus the Canadian dollar, the Euro and local currencies. NBSK pulp price increases during 2006, 2007 and the first half of 2008 were in large part offset by the weakening of the U.S. dollar. Similarly, the strengthening of the U.S. dollar against the Canadian dollar and the Euro towards the end of 2008 helped partially offset pulp price decreases caused by the deterioration in global economic conditions. The overall strengthening of the U.S. dollar against the Euro in 2010, and in particular in the first half of 2010, improved the operating margins of our German mills. Although the U.S. dollar weakened against the Euro for most of 2011, it began to strengthen again at the end of the year.

11

The following chart sets out the changes in list prices for NBSK pulp in Europe, as stated in U.S. dollars, Canadian dollars and Euros for the periods indicated.

Source: Pulp & Paper Week and Bloomberg

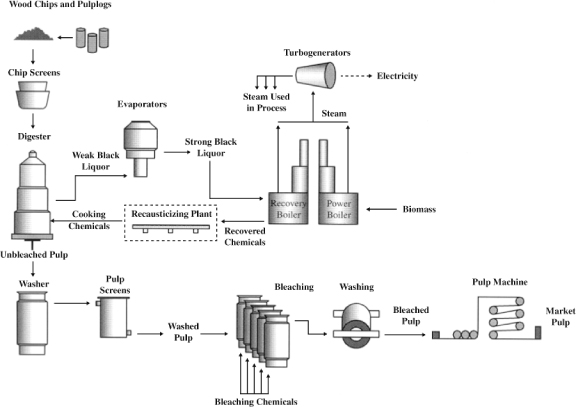

The Manufacturing Process

The following diagram provides a simplified description of the kraft pulp manufacturing process at our pulp mills:

12

In order to transform wood chips into kraft pulp, wood chips undergo a multi-step process involving the following principal stages: chip screening, digesting, pulp washing, screening, bleaching and drying.

In the initial processing stage, wood chips are screened to remove oversized chips and sawdust and are conveyed to a pressurized digester where they are heated and cooked with chemicals. This occurs in a continuous process at the Celgar and Rosenthal mills and in a batch process at the Stendal mill. This process softens and eventually dissolves the phenolic material called lignin that binds the fibers to each other in the wood.

Cooked pulp flows out of the digester and is washed and screened to remove most of the residual spent chemicals and partially cooked wood chips. The pulp then undergoes a series of bleaching stages where the brightness of the pulp is gradually increased. Finally, the bleached pulp is sent to the pulp machine where it is dried to achieve a dryness level of more than 90%. The pulp is then ready to be baled for shipment to customers.

A significant feature of kraft pulping technology is the recovery system, whereby chemicals used in the cooking process are captured and extracted for re-use, which reduces chemical costs and improves environmental performance. During the cooking stage, dissolved organic wood materials and used chemicals, collectively known as black liquor, are extracted from the digester. After undergoing an evaporation process, black liquor is burned in a recovery boiler. The chemical compounds of the black liquor are collected from the recovery boiler and are reconstituted into cooking chemicals used in the digesting stage through additional processing in the recausticizing plant.

The heat produced by the recovery boiler is used to generate high-pressure steam. Additional steam is generated by a power boiler through the combustion of biomass consisting of bark and other wood residuals from sawmills and our woodrooms and residue generated by the effluent treatment system. Additionally, during times of upset, we may use natural gas to generate steam. The steam produced by the recovery and power boilers is used to power a turbine generator to generate electricity, as well as to provide heat for the digesting and pulp drying processes.

Our Product

We manufacture and sell NBSK pulp produced from wood chips and pulp logs.

The kraft pulp produced at the Rosenthal mill is a long-fibered softwood pulp produced by a sulphate cooking process and manufactured primarily from wood chips and pulp logs. A number of factors beyond economic supply and demand have an impact on the market for chemical pulp, including requirements for pulp bleached without any chlorine compounds or without the use of chlorine gas. The Rosenthal mill has the capability of producing both “totally chlorine free” and “elemental chlorine free” pulp. Totally chlorine free pulp is bleached to a high brightness using oxygen, ozone and hydrogen peroxide as bleaching agents, whereas elemental chlorine free pulp is produced by substituting chlorine dioxide for chlorine gas in the bleaching process. This substitution virtually eliminates complex chloro-organic compounds from mill effluent.

Kraft pulp is valued for its reinforcing role in mechanical printing papers and is sought after by producers of paper for the publishing industry, primarily for magazines and advertising materials. Kraft pulp is also an important ingredient for tissue manufacturing, and tissue demand tends to increase with living standards in developing countries. Kraft pulp produced for reinforcement fibers is considered the highest grade of kraft pulp and generally obtains the highest price. The Rosenthal mill produces pulp for reinforcement fibers to the specifications of certain of our customers. We believe that a number of our customers consider us their supplier of choice.

The kraft pulp produced at the Stendal mill is of a slightly different grade than the pulp produced at the Rosenthal mill as the mix of softwood fiber used is slightly different. This results in a complementary product more suitable for different end uses. The Stendal mill is capable of producing both totally chlorine free and elemental chlorine free pulp.

13

The Celgar mill produces high-quality kraft pulp that is made from a unique blend of slow growing/long-fiber Western Canadian tree species. It is used in the manufacture of high-quality paper and tissue products. We believe the Celgar mill’s pulp is known for its excellent product characteristics, including tensile strength, wet strength and brightness. The Celgar mill is a long-established supplier to paper producers in Asia.

Generation and Sales of “Green” Energy at our Mills

Climate change concerns have caused a proliferation of renewable or “green” energy legislation, incentives and commercialization in both Europe and, increasingly, in North America. This has generated an increase in demand and legislated requirements for “carbon neutral” sources of energy supply. Our pulp mills are large scale bio-refineries that produce both pulp and surplus “carbon neutral” or “green” energy. As part of the pulp production process our mills generate “green” energy using carbon-neutral biofuels such as black liquor and wood waste. Through the incineration of biofuels in the recovery and power boilers, our mills produce sufficient steam to cover all of our steam requirements and allows us to produce surplus energy which we sell to third party utilities.

Our surplus energy sales provide our mills with a new stable revenue source unrelated to pulp prices. We believe that this revenue source from power sales gives our mills a competitive advantage over other older mills which do not have the equipment or capacity to produce and/or sell surplus power in a meaningful amount.

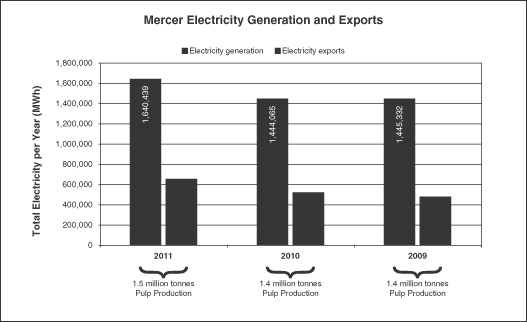

In 2011 and 2010, we sold 652,113 MWh and 520,005 MWh of surplus energy, respectively, and recorded revenues of €58.0 million and €44.2 million, respectively, from such energy sales. Since our energy production is a by-product of our pulp production process, there are minimal incremental costs and our surplus energy sales are highly profitable. The following table sets out our electricity generation and surplus energy sales for the last three years:

14

German Mills

Since January 2009, our Rosenthal and Stendal mills have participated in a program established pursuant to the Renewable Energy Act. The Renewable Energy Act, in existence since 2000, requires that public electric utilities give priority to electricity produced from renewable energy resources by independent power producers and pay a fixed tariff for a period of 20 years. Previously, this legislation was only applicable to installations with a capacity of 20MW or less, effectively excluding our Rosenthal and Stendal mills. Subsequent amendments to the Renewable Energy Act have removed this restriction. Under the program, our German mills now sell their surplus energy to the local electricity grid at the rates stipulated by the Renewable Energy Act for biomass energy.

Since 2005, our German mills have also benefited from the sale of emission allowances under the European Union Carbon Emissions Trading Scheme, referred to as “EU ETS”. However, our eligibility for special tariffs under the Renewable Energy Act has reduced the amount of emissions allowances granted to our German mills under the EU ETS.

In January 2012, we announced Project Blue Mill which is designed to increase the Stendal mill’s annual pulp production by 30,000 ADMTs and initially produce an additional 109,000 MW of surplus renewable energy. Project Blue Mill is eligible for €12.0 million of non-refundable government grants and the Stendal mill has secured a new €17.0 million five-year amortizing secured term debt facility, of which 80% will be government guaranteed. The balance of Project Blue Mill will be funded through operating cash flow of the Stendal mill and up to an aggregate of €6.5 million in pro rata shareholder loans from Mercer Inc. and its noncontrolling shareholder.

Celgar Mill

In September 2010, we completed the Celgar Energy Project at the Celgar mill, to increase the mill’s production of “green” energy and optimize its power generation capacity. The project included the installation of a 48 MW condensing turbine, which brought the mill’s installed generating capacity up to 100 MW, and upgrades to the mill’s bark boiler and steam consuming facilities. The Celgar mill has an Electricity Purchase Agreement with B.C. Hydro for the sale of power generated from such project. Under the Electricity Purchase Agreement, the Celgar mill agreed to supply a minimum of approximately 238,000 MWh of surplus electrical energy annually to the utility over a ten-year term.

We financed the Celgar Energy Project largely with funding from the GTP. In early October 2009, we received notification from Natural Resources Canada, or “NRCan”, of the Celgar mill’s original allocation of approximately C$57.7 million in credits under the GTP. In November 2009, we entered into a non-repayable contribution agreement, referred to as the “Contribution Agreement”, with NRCan whereby NRCan provided us with approximately C$40.0 million in grants (of our allocated C$57.7 million) towards certain costs associated with the Celgar Energy Project. Subsequently, NRCan provided an additional C$8.0 million pursuant to the terms of the Contribution Agreement. In 2011, NRCan agreed to allocate approximately C$1.6 million under its Transformative Technologies Program and we entered into additional contribution agreements bringing the total received from NRCan to C$56.1 million.

In 2011, we produced and sold roughly 140,069 MWh of surplus renewable electricity at our Celgar mill which generated approximately C$14.5 million in annual revenues.

Operating Costs

Our major costs of production are labor, fiber, energy and chemicals. Fiber comprised of wood chips and pulp logs is our most significant operating expense. Given the significance of fiber to our total operating expenses and our limited ability to control its costs, compared with our other operating costs, volatility in fiber costs can materially affect our margins and results of operations.

15

Labor

Our labor costs tend to be generally steady, with small overall increases due to inflation in wages and health care costs. Over the last three years, we have been able to generally offset such increases by increasing our efficiencies and production and streamlining operations.

Fiber

Our mills are situated in regions which generally provide a relatively stable supply of fiber. The fiber consumed by our mills consists of wood chips produced by sawmills as a by-product of the sawmilling process and pulp logs. Wood chips are small pieces of wood used to make pulp and are either wood residuals from the sawmilling process or logs or pulp logs chipped especially for this purpose. Pulp logs consist of lower quality logs not used in the production of lumber. Wood chips and pulp logs are cyclical in both price and supply.

Generally, the cost of wood chips and pulp logs are primarily affected by the supply and demand for lumber. Additionally, regional factors such as harvesting levels and weather conditions can also have a material effect on the supply, demand and price for fiber.

In Germany, since 2006, the price and supply of wood chips has been affected by increasing demand from alternative or renewable energy producers and government initiatives for carbon neutral energy. Declining energy prices and weakening economies in the first half of 2009 tempered the increased demand for wood chips that resulted from initiatives by European governments to promote the use of wood as a carbon neutral energy. Over the long-term, we expect this non-traditional demand for fiber to continue to increase.

In April 2008, the Russian government raised tariffs on the export of sawmill and pulp wood to 25% from the 20%. A further increase to 80% was initially scheduled for January 1, 2009 but was officially deferred twice and Russia’s export tariff remained unchanged at 25% in 2011. In early 2012, Russia agreed to enter the World Trade Organization, or “WTO”. It is currently expected that Russia will formally enter the WTO in June 2012 and will lower its export tariffs to between 13% and 15% which we believe will have a positive impact on the European fiber supply.

Offsetting some of the increases in demand for wood fiber have been initiatives in which we and other producers are participating to increase harvest levels in Germany, particularly from small private forest owners. We believe that Germany has the highest availability of softwood forests in Europe suitable for harvesting and manufacturing. We believe private ownership of such forests is approximately 50%. Many of these forest ownership stakes are very small and have been harvested at rates much lower than their rate of growth. In early 2009, in response to slowing economies and weaker demand for pulp logs, forest owners reduced their harvesting rates slightly. While prices for pulp logs in Germany remained relatively low in the first half of 2009, further reductions in harvesting rates led to an undersupply which resulted in increased fiber prices later that year. Fiber prices continued to increase through most of 2010 and 2011, driven by lower levels of harvesting in central Germany, combined with increased demand for wood from the energy sector for heating and other bio-energy purposes.

We believe we are the largest consumer of wood chips and pulp logs in Germany and often provide the best, long-term economic outlet for the sale of wood chips in Eastern Germany. We coordinate the wood procurement activities for our German mills to reduce overall personnel and administrative costs, provide greater purchasing power and coordinate buying and trading activities. This coordination and integration of fiber flows also allows us to optimize transportation costs, and the species and fiber mix for both mills.

In 2011, the Rosenthal mill consumed approximately 1.8 million cubic meters of fiber. Approximately 70% of such consumption was in the form of sawmill wood chips and approximately 30% was in the form of pulp logs. The wood chips for the Rosenthal mill are sourced from approximately 31 sawmills located primarily in the states of Bavaria, Baden-Württemberg and Thüringia and are within a 300 kilometer radius of the Rosenthal mill.

16

Within this radius, the Rosenthal mill is the largest consumer of wood chips. Given its location and size, the Rosenthal mill is often the best economic outlet for the sale of wood chips in the area. Approximately 73% of the fiber consumed by the Rosenthal mill is spruce and the remainder is pine. While fiber costs and supply are subject to cyclical changes largely in the sawmill industry, we expect that we will be able to continue to obtain an adequate supply of fiber on reasonably satisfactory terms for the Rosenthal mill due to its location and our long-term relationships with suppliers. We have not historically experienced any significant fiber supply interruptions at the Rosenthal mill.

Wood chips for the Rosenthal mill are normally sourced from sawmills under one year or quarterly supply contracts with fixed volumes, which provide for price adjustments. Substantially all of our chip supply is sourced from suppliers with which we have a long-standing relationship. We generally enter into annual contracts with such suppliers. Pulp logs are sourced from the state forest agencies in Thüringia, Saxony and Bavaria on a contract basis and partly from private holders on the same basis as wood chips. Like the wood chip supply arrangements, these contracts tend to be of less than one-year terms with quarterly adjustments for market pricing. We organize the harvesting of pulp logs sourced from the state agencies in Thüringia, Saxony and Bavaria after discussions with the agencies regarding the quantities of pulp logs that we require.

In 2011, the Stendal mill consumed approximately 3.2 million cubic meters of fiber. Approximately 25% of such fiber was in the form of sawmill wood chips and approximately 75% in the form of pulp logs. The core wood supply region for the Stendal mill includes most of the Northern part of Germany within an approximate 300 kilometer radius of the mill. We also purchase wood chips from Southwestern and Southern Germany. The fiber base in the wood supply area for the Stendal mill consisted of approximately 68% pine and 32% spruce and other species in 2011. The Stendal mill has sufficient chipping capacity to fully operate solely using pulp logs, if required. We source pulp logs partly from private forest holders and partly from state forest agencies in Thüringia, Saxony-Anhalt, Mecklenburg-Western Pomerania, Saxony, Lower Saxony, North Rhine-Westphalia, Hesse and Brandenburg.

In 2011, the Celgar mill consumed approximately 2.6 million cubic meters of fiber. Approximately 61% of such fiber was in the form of sawmill wood chips and the remaining 39% came from pulp logs processed through its woodroom or chipped by a third party. The source of fiber at the mill is characterized by a mixture of species (whitewoods and cedar) and the mill sources fiber from a number of Canadian and U.S. suppliers.

As a result of the cyclical decline in sawmill chip availability resulting from lower lumber production in British Columbia, the Celgar mill has increased its U.S. purchases of fiber, diversified its suppliers and, where possible, increased chip production through third party field chipping contracts and existing sawmill suppliers. Additionally, in the early part of 2009, the Celgar mill completed a project to upgrade its woodroom which, along with subsequent improvements during the year, increased its capacity to be able to process up to 50% of the mill’s fiber needs compared to only approximately 10% previously. The woodroom upgrades also increased the mill’s ability to process small diameter logs and facilitate an efficient flow of fiber. This has increased the overall volume of fiber being processed and helped mitigate increases in the price of fiber.

The Celgar mill has access to over 35 different suppliers from Canada and the U.S., representing approximately 75% of its total annual fiber requirements. The Celgar mill’s woodroom supplied the remaining 25% of the mill’s fiber requirements in 2011. Chips are purchased in Canada and the U.S. in accordance with chip purchase agreements. Generally, pricing is reviewed and adjusted periodically to reflect market prices. Several of the longer-term contracts are so-called “evergreen” agreements, where the contract remains in effect until one of the parties elects to terminate. Termination requires a minimum of two, and in some cases, five years’ written notice. Certain non-evergreen long-term agreements provide for renewal negotiations prior to expiry.

17

To secure the volume of pulp logs required by its woodroom, the Celgar mill has entered into annual pulp log supply agreements with a number of different suppliers, many of whom are also contract chip suppliers to the mill. All of the pulp log agreements can be terminated by either party for any reason, upon seven days’ written notice.

On the fiber demand side, increased competition for fiber from the growing renewable or “green” energy sector in British Columbia in the second half of 2011 led to moderately higher fiber costs. Although not nearly as advanced as Europe, British Columbia’s growing green energy sector is expected to continue to create additional competition for fiber over time.

Energy

Our energy is primarily generated from renewable carbon neutral sources, such as black liquor and wood waste. Our mills produce all of our steam requirements and generally generate excess energy which we sell to third party utilities. In 2011, we generated 1,640,439 MWh and we sold 652,113 MWh of surplus energy. See also “—Generation and Sales of ‘Green’ Energy at our Mills”. We utilize fossil fuels, such as natural gas, in limited circumstances primarily in our lime kilns and we use a limited amount for start-up and shutdown operations. Additionally, from time to time, mill process disruptions occur and we consume small quantities of purchased electricity and fossil fuels to maintain operations. As a result, all of our mills are subject to fluctuations in the prices for fossil fuels.

Chemicals

Our mills use certain chemicals which are generally available from several suppliers and sourcing is primarily based upon pricing and location. Although chemical prices have risen slightly over the last three years, we have been able to reduce our costs through improved efficiencies and capital expenditures.

Cash Production Costs

Consolidated cash production costs per ADMT for our pulp mills are set out in the following table for the periods indicated:

| | | | | | | | | | | | |

| | | Years Ended December 31, | |

| | | 2011 | | | 2010 | | | 2009 | |

| | | (per ADMT) | |

Cash Production Costs | | | | |

Fiber | | € | 275 | | | € | 256 | | | € | 207 | |

Labor | | | 43 | | | | 42 | | | | 37 | |

Chemicals | | | 46 | | | | 41 | | | | 43 | |

Energy | | | 13 | | | | 17 | | | | 13 | |

Other | | | 56 | | | | 54 | | | | 42 | |

| | | | | | | | | | | | |

Total cash production costs(1) | | € | 433 | | | € | 410 | | | € | 342 | |

| | | | | | | | | | | | |

| (1) | Cost of production per ADMT produced excluding depreciation. |

18

Sales, Marketing and Distribution

The distribution of our pulp sales revenues by geographic area are set out in the following table for the periods indicated:

| | | | | | | | | | | | |

| | | Years Ended December 31, | |

| | | 2011 | | | 2010 | | | 2009 | |

| | | (in thousands) | |

Revenues by Geographic Area | | | | |

Germany | | € | 256,563 | | | € | 278,348 | | | € | 154,323 | |

China | | | 234,654 | | | | 196,022 | | | | 146,613 | |

Italy | | | 51,509 | | | | 56,301 | | | | 44,616 | |

Other European Union countries(1) | | | 175,937 | | | | 182,246 | | | | 107,276 | |

Other Asia | | | 30,872 | | | | 37,561 | | | | 38,946 | |

North America | | | 69,345 | | | | 92,628 | | | | 68,213 | |

Other countries | | | 823 | | | | 1,503 | | | | 8,312 | |

| | | | | | | | | | | | |

Total(2) | | € | 819,703 | | | € | 844,609 | | | € | 568,299 | |

| | | | | | | | | | | | |

| (1) | Not including Germany or Italy; includes new entrant countries to the European Union from their time of admission. |

| (2) | Excluding intercompany sales and third party transportation revenues. |

The following charts illustrate the geographic distribution of our pulp revenues for the periods indicated:

| | | | |

Year Ended December 31, 2011 | | Year Ended December 31, 2010 | | Year Ended December 31, 2009 |

| |  | |  |

| (1) | Includes new entrant countries to the European Union from their time of admission. |

Our global sales and marketing group is responsible for conducting all sales and marketing of the pulp produced at our mills and currently has approximately 19 employees engaged full time in such activities. The global sales and marketing group handles sales to over 180 customers. We coordinate and integrate the sales and marketing activities of our German mills to realize on a number of synergies between them. These include reduced overall administrative and personnel costs and coordinated selling, marketing and transportation activities. We also coordinate sales from the Celgar mill with our German mills on a global basis, thereby providing our larger customers with seamless service across all major geographies. In marketing our pulp, we seek to establish long-term relationships by providing a competitively priced, high-quality, consistent product and excellent service. In accordance with customary practice, we maintain long-standing relationships with our customers pursuant to which we periodically reach agreements on specific volumes and prices.

Our pulp sales are on customary industry terms. At December 31, 2011, we had no material payment delinquencies. In 2011, no single customer accounted for more than 10% of our pulp sales. In 2010, one customer which purchased for several of its mills accounted for 11% of pulp sales and, in 2009, no single customer accounted for more than 10% of our pulp sales. We don’t believe our pulp sales are dependent upon the activities of any single customer.

19

Our German mills are currently the only market kraft pulp producers in Germany, which is the largest import market for kraft pulp in Europe. We therefore have a competitive transportation cost advantage compared to Canadian and Scandinavian pulp producers when shipping to customers in Europe. Due to the location of our German mills, we are able to deliver pulp to many of our customers primarily by truck. Most trucks that deliver goods into Eastern Germany generally do not have significant backhaul opportunities as the region is primarily an importer of goods. We are therefore frequently able to obtain relatively low backhaul freight rates for the delivery of our products to many of our customers. Since many of our customers are located within a 500 kilometer radius of our German mills, we can generally supply pulp to customers of these mills faster than our competitors because of the short distances between the mills and our customers.

The Celgar mill’s pulp is transported to customers by rail, truck and ocean carrier using third party warehouses to ensure timely delivery. The majority of Celgar’s pulp for overseas markets is initially delivered primarily by rail to the Port of Vancouver for shipment overseas by ocean carrier. Based in Western Canada, the Celgar mill is well positioned to service Asian customers. The majority of the Celgar mill’s pulp for domestic markets is shipped by rail to third party warehouses in the U.S. or directly to the customer.

Approximately 58%, 55% and 51% of our sales were to tissue and specialty paper product manufacturers for the years ended December 31, 2011, 2010 and 2009, respectively. The balance of our sales for such periods was to other paper product manufacturers. Sales to tissue and specialty paper product manufacturers are a key focus for us, as they generally are not as sensitive to cyclical declines in demand caused by downturns in economic activity.

Capital Expenditures

In 2011, we continued with our capital investment programs designed to increase pulp and green energy production capacity and improve efficiency and environmental performance at our mills. The improvements made at our mills over the past eight years have reduced operating costs and increased the competitive position of our facilities.

Total capital expenditures at the Rosenthal mill in 2011, 2010 and 2009 were €13.7 million, €4.0 million and €9.1 million, respectively. Capital investments at the Rosenthal mill in 2011, primarily related to the installation of a new chipper and upgrades to the recovery process, while in 2010 and 2009 capital expenditures related mainly to the upgrade of a bleaching line and a washer project, which helped offset three years of wastewater fees that would otherwise be payable.

Our Stendal mill’s total capital expenditures in 2011, 2010 and 2009 were €8.3 million, €3.6 million and €2.0 million, respectively. Capital investments at the Stendal mill in 2011 and 2010 related mainly to relatively small projects designed to improve safety and environmental performance as well as improve the overall efficiency of the mill.

In January 2012, Mercer announced Project Blue Mill which is intended to increase production and efficiency at the Stendal mill through debottlenecking initiatives including the installation of an additional 40 MW steam turbine. Project Blue Mill is estimated to require approximately €40.0 million in capital expenditures over about 21 months, which will be primarily funded through €12.0 million of non-refundable German government grants and a new €17.0 million five-year amortizing secured term facility, of which 80% will be government guaranteed. The balance of Project Blue Mill will be funded through operating cash flow of the Stendal mill and up to an aggregate of €6.5 million in pro rata shareholder loans from Mercer Inc. and Stendal’s noncontrolling shareholder. Project Blue Mill is currently designed to be completed and start to generate power resources in or about September 2013.

Certain of our capital investment programs in Germany were partially financed through government grants made available by German federal and state governments. Under legislation adopted by the federal and certain

20

state governments of Germany, government grants are provided to qualifying businesses operating in Eastern Germany to finance capital investments. The grants are made to encourage investment and job creation. Currently, grants are available for up to 15% of the cost of qualified investments. Previously, government grants were available for up to 35% of the cost of qualified investments, such as for the construction of our Stendal mill. These grants at the 35% of cost level required that at least one permanent job be created for each €0.5 million of capital investment eligible for such grants and that such jobs be maintained for a period of five years from the completion of the capital investment project. Generally, government grants are not repayable by a recipient unless it fails to complete the proposed capital investment or, if applicable, fails to create or maintain the requisite amount of jobs. In the case of such failure, the government is entitled to revoke the grants and seek repayment unless such failure resulted from material unforeseen market developments beyond the control of the recipient, wherein the government may refrain from reclaiming previous grants. Pursuant to such legislation in effect at the time, the Stendal mill received approximately €278.0 million of government grants. We believe that we are in compliance in all material respects with all of the terms and conditions governing the government grants we have received in Germany.

The following table sets out for the periods indicated the effect of these government grants on the recorded value of such assets in our consolidated balance sheets:

| | | | | | | | | | | | |

| | | As at December 31, | |

| | | 2011 | | | 2010 | | | 2009 | |

| | | (in thousands) | |

Property, plant and equipment, gross amount less amortization | | € | 1,112,639 | | | € | 1,144,759 | | | € | 1,152,288 | |

Less: government grants less amortization | | | 291,665 | | | | 297,992 | | | | 283,730 | |

| | | | | | | | | | | | |

Property, plant and equipment, net (as shown on the Consolidated Balance Sheets) | | € | 820,974 | | | € | 846,767 | | | € | 868,558 | |

| | | | | | | | | | | | |

Qualifying capital investments at industrial facilities in Germany that reduce effluent discharges offset wastewater fees that would otherwise be required to be paid. For more information about our environmental capital expenditures, see “—Environmental”.

Total capital expenditures at the Celgar mill in 2011, 2010 and 2009 were €15.7 million, €30.6 million and €17.8 million, respectively. In 2011, capital expenditures related primarily to a project to improve the Celgar mill’s fiber line and oxygen delignification process, referred to as the “Oxygen Delignification Project”, and a project to recover/recycle chemicals from the mill’s effluent, referred to as the “GAP Project”.

We completed the Celgar Energy Project in 2010 as part of our continued focus on energy production and sales and to increase the mill’s production of “green” energy and optimize its power generation capacity. The project was designed as a high return capital project at a cost of approximately C$64.7 million (€49.0 million). It included the installation of a second turbine generator with a design capacity of 48 MW.

In October 2009, as part of the GTP, the Canadian government through NRCan agreed to provide approximately C$57.7 million in credits towards the capital costs associated with the Celgar mill, including the Celgar Energy Project. Such credits reduced the cost basis of the assets purchased and were not recorded in our income. The majority of the remaining credits not used for the Celgar Energy Project are available for use by the Celgar mill on other qualifying projects until March 31, 2012. To be eligible for GTP credits, projects must meet certain energy efficiency or environmental improvement requirements. Specifically, we applied to NRCan to utilize approximately C$10.9 million of our allocated GTP funding towards the Oxygen Delignification Project and several small projects at our Celgar mill. As at December 31, 2011, we had spent approximately C$8.6 million to complete the Oxygen Delignification Project. In 2011, as part of the NRCan Transformative Technologies Program, we received C$1.6 million from NRCan which was utilized towards the GAP Project. As at December 31, 2011, we had spent approximately C$2.7 million on the GAP Project and expect to spend approximately C$0.7 million in 2012.

21

The Celgar Energy Project increased the mill’s installed generating capacity to 100 MW, and upgraded the mill’s bark boiler and steam facilities. In January 2009, the Celgar mill finalized the Electricity Purchase Agreement under which it will sell electrical energy generated by the Celgar Energy Project to B.C. Hydro.

Excluding costs for projects financed through government grants, capital expenditures for all of our mills in 2012 are expected to be approximately €40.8 million, comprised of Project Blue Mill at our Stendal mill and an array of small projects at our other mills.

Environmental

Our operations are subject to a wide range of environmental laws and regulations, dealing primarily with water, air and land pollution control. We devote significant management and financial resources to comply with all applicable environmental laws and regulations. Our total capital expenditures on environmental projects at our mills were approximately €7.1 million in 2011 (€2.5 million in 2010). The Oxygen Delignification Project is intended to generate environmental improvements by reducing the organic and chemical loading on the effluent treatment system at our Celgar mill.

We believe we have obtained all required environmental permits, authorizations and approvals for our operations. We believe our operations are currently in substantial compliance with the requirements of all applicable environmental laws and regulations and our respective operating permits.

Under German state environmental rules relating to effluent discharges, industrial users are required to pay wastewater fees based upon the amount of their effluent discharge. These rules also provide that an industrial user which undertakes environmental capital expenditures and lowers certain effluent discharges to prescribed levels may offset the amount of these expenditures against the wastewater fees that they would otherwise be required to pay. We estimate that the aggregate wastewater fees we saved in 2011 as a result of environmental capital expenditures and initiatives to reduce allowable emissions and discharges at our Stendal mill was approximately €4.2 million. The estimated amount of accrued wastewater fees we expect to recover at our Rosenthal mill is approximately €2.2 million. We expect that capital investment programs and other environmental initiatives at our German mills will mostly offset the wastewater fees that may be payable for 2012 and we believe they will ensure that our operations continue in substantial compliance with prescribed standards.

Environmental compliance is a priority for our operations. To ensure compliance with environmental laws and regulations, we regularly monitor emissions at our mills and periodically perform environmental audits of operational sites and procedures both with our internal personnel and outside consultants. These audits identify opportunities for improvement and allow us to take proactive measures at the mills as considered appropriate.

The Rosenthal mill has a relatively modern biological wastewater treatment and oxygen bleaching facility. We have significantly reduced our levels of absorbable organic halogen discharge at the Rosenthal mill and we believe the Rosenthal mill’s absorbable organic halogen and chemical oxygen demand discharges are in compliance with the standards currently mandated by the German government.

The Stendal mill, which commenced operations in September 2004, has been in substantial compliance with applicable environmental laws, regulations and permits. Management believes that, as the Stendal mill is a state-of-the-art facility, it will be able to continue to operate in compliance with the applicable environmental requirements.

The Celgar mill has been in substantial compliance with applicable environmental laws, regulations and permits.

22

In November 2008, the Celgar mill suffered a spill of diluted weak black liquor into the nearby Columbia River. The spill was promptly reported by the mill to authorities and remediated. An environmental impact report prepared by independent consultants engaged by the mill concluded that the environmental impact of the spill was minimal. The spill was also investigated by federal and provincial environmental authorities and, in January 2009, the Celgar mill received a government directive requiring it to take a number of measures relating to the retention capacity of spill ponds. These measures were completed to the satisfaction of the overseeing environmental authorities. However, in September 2009, the Celgar mill received a summons in connection with this spill for charges under the CanadianFisheries Act and the British ColumbiaEnvironmental Management Act, primarily relating to alleged effluent exceedances under the Celgar mill’s discharge permit. See “Legal Proceedings”.

The Celgar mill operates two landfills, a newly commissioned site and an older site. The mill intends to decommission the older landfill and is developing a closure plan and reviewing such plan with the British Columbia Ministry of Environment, or “MOE”. Since a portion of the older landfill continues to be active, the mill has not been able to move forward with the closure. We expect to receive provincial regulatory approval for our closure plan for our older landfill in 2012 and intend to commence closure activities based on a timetable agreed to by both Celgar and the MOE. The cost of closing the landfill is expected to be approximately €2.1 million.

Future regulations or permits may place lower limits on allowable types of emissions, including air, water, waste and hazardous materials, and may increase the financial consequences of maintaining compliance with environmental laws and regulations or conducting remediation. Our ongoing monitoring and policies have enabled us to develop and implement effective measures to maintain emissions in substantial compliance with environmental laws and regulations to date in a cost-effective manner. However, there can be no assurances that this will be the case in the future.

Climate Change

There are numerous differing scientific studies and opinions relating to the severity, extent and speed at which climate change is or may be occurring. As a result, we are currently unable to identify and predict all of the specific consequences of climate change on our business and operations.

To date, the potential and/or perceived effects of climate change and social and governmental responses to it have created both business opportunities and the potential for negative consequences for our business.

The focus on climate change has generated a substantial increase in demand and in legislative requirements for “carbon neutral” or “green” energy in both Europe and, increasingly, in North America. Pulp mills consume wood residue, being wood chips and pulp logs, as the base raw material for their production process. Wood chips are residue left over from lumber production and pulp logs are generally lower quality logs left over from logging that are unsuitable for the production of lumber.

As part of their production process, our mills take wood residue and process it through a digester where cellulose is separated from the wood to be used in pulp production and the remaining residue, called “black liquor”, is used for green energy production. As a result of their use of wood residue and because our mills generate combined heat and power, they are efficient producers of energy. This energy is carbon neutral and produced from a renewable source. Our relatively modern mills generate a substantial amount of energy that is surplus to their requirements.

These factors, along with governmental initiatives in respect of renewable or green energy legislation, have provided business opportunities for us to enhance our generation and sales of green energy and to participate in the sale of emission allowances under the EU ETS. In January 2012, we announced a project at our Stendal mill to install a new 40 MW steam turbine which we expect will initially produce an additional 109,000 MWh of surplus renewable energy at the mill.

23

Currently, we are exploring other initiatives to enhance our generation and sales of surplus green energy. Other potential opportunities that may result from climate change include:

| | • | | the expansion of softwood forests and increased growth rates for such forests; |

| | • | | more intensive forestry practices and timber salvaging versus harvesting standing timber; |

| | • | | greater demand for sustainable energy and cellulosic biomass fuels; and |

| | • | | additional governmental incentives and/or legislative requirements to enhance biomass energy production. |

At this time, we cannot predict which, if any, of these potential opportunities will be available to or realized by us or their economic effect on our business.

While all of the specific consequences to our business from climate change are not yet predictable, the most visible negative consequence is that the focus on renewable energy will continue to create greater demand for the wood residuals or fiber that is consumed by our mills as part of their production process.

In Germany since 2006, the price and supply of wood residuals have been affected by an increasing demand from alternative or renewable energy producers and governmental initiatives for carbon neutral energy. Over the long term, this non-traditional demand for fiber is expected to increase in Europe. Additionally, the growing interest and focus in British Columbia for renewable green energy is also expected to create additional competition for such fiber in that region over time. Such additional demand for wood residuals may increase the competition and prices for wood residuals over time. See “—Operating Costs—Fiber”.

Governmental action or legislation may also have an important effect on the demand and prices for wood residuals. As governments pursue green energy initiatives, they risk creating incentives and demand for wood residuals from renewable energy producers that “cannibalizes” or adversely affects existing traditional users, such as lumber and pulp and paper producers. We are continually engaged in dialogue with government to educate and try to ensure potential initiatives recognize the traditional and continuing role of our mills in the overall usage of forestry resources and the economies of local communities.

Other potential negative consequences from climate change over time that may affect our business include: