Table of Contents

Index to Financial Statements

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

| x | Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the year ended June 30, 2008.

or

| ¨ | Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the transition period from to

Commission File Number 000-51636

TRIPLE CROWN MEDIA, INC.

(Exact name of registrant as specified in its charter)

| Delaware | 20-3012824 | |

(State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) | |

| 725A Old Norcross Rd, Lawrenceville, Georgia | 30045 | |

| (Address of principal executive offices) | (Zip Code) | |

Registrant’s telephone number, including area code (770) 338-7351

Securities registered pursuant to Section 12(b) of the Act:

None

Securities registered pursuant to Section 12(g) of the Act:

Common Stock, $.001 par value.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. ¨ Yes x No

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. ¨ Yes x No

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.x Yes ¨ No

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

| Large accelerated filer ¨ | Accelerated filer ¨ | |

| Non-accelerated filer ¨ | Smaller reporting company x | |

| (Do not check if a smaller reporting company) |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act). ¨ Yes x No

The aggregate market value of the voting and non-voting common equity held by non-affiliates was $26,314,556 based on the price of Triple Crown Media Inc.’s common stock as of December 31, 2007, as reported on the Nasdaq Global Market.

The number of shares outstanding of Triple Crown Media, Inc.’s common stock as of September 29, 2008 was 5,591,626.

DOCUMENTS INCORPORATED BY REFERENCE

Documents | Form 10-K Reference | |

| None | Not Applicable |

Table of Contents

Index to Financial Statements

TRIPLE CROWN MEDIA, INC.

FORM 10-K

For the fiscal year ended June 30, 2008

| Page | ||||

PART I | ||||

Item 1 | 3 | |||

Item 1A | 11 | |||

Item 1B | 17 | |||

Item 2 | 18 | |||

Item 3 | 18 | |||

Item 4 | 18 | |||

PART II | ||||

Item 5 | 19 | |||

Item 6 | 21 | |||

Item 7 | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 23 | ||

Item 7A | 40 | |||

Item 8 | 41 | |||

Item 9 | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 71 | ||

Item 9A | 71 | |||

Item 9B | 72 | |||

PART III | ||||

Item 10 | 73 | |||

Item 11 | 76 | |||

Item 12 | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 93 | ||

Item 13 | Certain Relationships and Related Transactions, and Director Independence | 95 | ||

Item 14 | 95 | |||

PART IV | ||||

Item 15 | 97 | |||

| 100 | ||||

2

Table of Contents

Index to Financial Statements

PART I

| Item 1. | Business |

General

Until December 30, 2005, Triple Crown Media, Inc., or the Company, was comprised of integrated businesses owned and operated by Gray Television, Inc., or Gray, consisting of two reportable segments: Newspaper Publishing and GrayLink Wireless. On December 30, 2005, all shares of the Company’s common stock were distributed to shareholders of Gray and, as a result, the Company became a separate, stand-alone entity, independent of Gray, in a series of transactions referred to as the Spin-off. Immediately following the Spin-off on December 30, 2005, Bull Run Corporation, or Bull Run, was merged into a wholly owned subsidiary of the Company through the issuance of shares of the Company’s common stock in exchange for shares of Bull Run common stock, and the issuance of shares of the Company series A and series B convertible preferred stock for certain shares of Bull Run preferred stock, in a transaction referred to as the Merger. As a result of the Spin-off and the Merger, the Company was comprised of its Newspaper Publishing and GrayLink Wireless segments, plus Bull Run’s Collegiate Marketing segment and Association Management Services segment, both of which were operated by the Company’s wholly owned subsidiary, Host Communications, Inc., or Host. Additional information concerning the Company’s reportable segments is included in Note 15 to the Company’s combined and consolidated financial statements included in this Form 10-K. Hereinafter, all references to Triple Crown Media, Inc., the “Company,” “TCM,” “we,” “us,” or “our” in this Part I of this Form 10-K refer to the combined businesses.

We sold our GrayLink Wireless segment on June 22, 2007. The results of operations for the GrayLink Wireless segment for all periods presented have been reclassified to discontinued operations for financial statement presentation. Additional information regarding the GrayLink Wireless segment and its results of operations are contained elsewhere in this Form 10-K.

We sold our Host Collegiate Marketing segment on November 15, 2007. The results of operations for the Host Collegiate Marketing segment for all periods have been reclassified to discontinued operations for financial statement presentation. Additional information regarding the Host Collegiate Marketing segment and its results of operations are contained elsewhere in this Form 10-K.

We sold our Host Association Management Services segment on November 15, 2007. The results of operations for the Host Association Management Services segment for all periods have been reclassified to discontinued operations for financial statement presentation. Additional information regarding the Host Association Management Services segment and its results of operations are contained elsewhere in this Form 10-K.

Our sole remaining operating segment is comprised of our Newspaper Publishing business. This consists of the ownership and operation of six daily newspapers and one weekly newspaper with a total daily circulation as of June 30, 2008 of approximately 95,200 and a total Sunday circulation as of June 30, 2008 of approximately 131,850. Our newspapers are characterized by their focus on the coverage of local news and local sports. Newspaper Publishing revenue of $46.0 million comprised 100% of our total revenues for the twelve months ended June 30, 2008.

Spin-off and Merger

Immediately prior to the distribution of our common stock in the Spin-off, pursuant to the terms of a separation and distribution agreement between Gray and us, Gray contributed (i) all of the membership interests of Gray Publishing, LLC, which owned and operated the Newspaper Publishing and GrayLink Wireless businesses and (ii) certain other assets to us. In the distribution of our common stock

3

Table of Contents

Index to Financial Statements

pursuant to the Spin-off, each Gray shareholder received (i) one share of our common stock for every 10 shares of Gray common stock that was owned on the date of the Spin-off and (ii) one share of our common stock for every 10 shares of Gray’s Class A common stock that was owned on the date of the Spin-off. On the date of the Spin-off, in partial consideration of the transfer of the membership interests to TCM, we distributed $44.6 million to Gray, including $4.6 million for transaction costs.

Pursuant to the terms of an Agreement and Plan of Merger dated August 2, 2005, by and among us, BR Acquisition Corp. (our wholly owned subsidiary) and Bull Run, Bull Run was merged with and into BR Acquisition Corp. with BR Acquisition Corp. surviving. At the effective time of the Merger: (i) each share of Bull Run common stock was converted into 0.0289 shares of our common stock; (ii) each share of Bull Run Series D preferred stock was converted into one share of our Series A redeemable, convertible preferred stock; (iii) each share of Bull Run Series E preferred stock held by J. Mack Robinson, Gray’s current Chairman and Chief Executive Officer and any transferee of Mr. Robinson was converted into one share of our Series A redeemable, convertible preferred stock; (iv) each share of Bull Run Series E preferred stock held by a Series E preferred shareholder (other than Mr. Robinson and any transferee of Mr. Robinson) was converted into $1,000 in cash; (v) each share of Bull Run Series F preferred stock was converted into 22.56 shares of our common stock; (vi) we paid to each Bull Run Series E preferred shareholder (other than Mr. Robinson and any transferee or affiliate of Mr. Robinson) cash in an amount equal to the accrued and unpaid dividends due to each such shareholder; (vii) all accrued and unpaid dividends (through July 1, 2005) on each outstanding share of Bull Run Series D preferred stock and Bull Run Series E preferred stock held by Mr. Robinson and any transferee or affiliate of Mr. Robinson, was converted into the number of shares of our Series A redeemable, convertible preferred stock determined by dividing the accrued and unpaid dividends due on such shares by $1,000; (viii) all accrued and unpaid dividends (through July 1, 2005) on each outstanding share of Bull Run Series F preferred stock was converted into an aggregate of 12,737 shares of our common stock; and (ix) the cash advances in the aggregate amount of $6.05 million made by Mr. Robinson to Bull Run were converted into 6,050 shares of our Series B redeemable, convertible preferred stock.

On December 30, 2005, we executed a new $140 million long-term credit facility that accommodated the payment of the $40 million cash distribution to Gray arising from the Spin-off, the refinancing of all of Bull Run’s long-term debt in connection with the Merger, the payment of the cash portion of the Merger consideration paid to certain Bull Run preferred stockholders and the payment of transaction costs.

Newspaper Publishing

We own and operate six daily newspapers and one weekly newspaper, located in the Southeast with daily circulation ranging from approximately 2,100 to approximately 58,600 and Sunday circulation ranging from approximately 7,800 to approximately 102,600. We believe that our newspapers are an effective medium for advertisers to maximize their reach of the households in the markets served by our newspapers. Our newspapers focus on local content, including coverage of local youth, high school and college sports, as well as local business, politics, entertainment and cultural news. Each of our newspapers is tailored to its market in order to provide local content that radio, television and large metropolitan daily newspapers are unable to provide on a cost-effective basis because of their broader geographic coverage. Our newspapers also differentiate themselves from other forms of media by providing a cost-effective medium for local advertisers to target their customers. We maintain high product quality standards and use extensive process color and compelling graphic design to fully engage existing readers and to attract new readers.

Our Newspaper Publishing revenues for the twelve months ended June 30, 2008 were derived 87% from advertising, 10% from paid circulation and 3% from commercial printing and other revenue.

4

Table of Contents

Index to Financial Statements

Our advertiser base is predominantly local, including the local stores and outlets of major regional and national retailers. Our newspapers seek to produce desirable results for local advertisers by targeting readers based on certain geographic and demographic characteristics. We seek to increase readership, and thereby generate traffic for our advertisers, by focusing on high product quality, compelling and often proprietary local content and creative and interactive promotions. Circulation sales are primarily generated through subscription sales and single copy sales. We promote single copy sales of our newspapers because we believe that such sales tend to generate higher profit margins than subscription sales, as single copy sales generally have higher per unit prices and lower distribution costs. Subscription sales, which provide readers with the convenience of home delivery, are an important component of our circulation base because these readers are very important to advertisers. From time to time, we publish special sections for our newspapers and niche publications. Such special sections and niche publications tend to increase readership within targeted demographic groups and geographic areas and provide opportunities for our newspapers to capture new or additional advertising revenue.

Industrywide, newspaper subscriber circulation levels have been slowly declining. From December 31, 2005 through June 30, 2008, our aggregate daily circulation has declined approximately 11%. We attempt to offset declines in circulation and corresponding circulation revenue with strategies that include readership growth initiatives in Gwinnett and Newton County, Georgia and efforts to increase circulation among cable subscribers in Gwinnett County, Georgia under our unique relationship whereby newspaper subscriptions are sponsored by local cable companies.

Goshen/Jonesboro Swap

On April 7, 2006, we entered into an asset exchange agreement with Community First Holdings, Inc. (CNHI), dated as of April 1, 2006, to exchange The Goshen News for the Jonesboro Group consisting of the Clayton News Daily, Clayton News Weekly, Henry Daily Herald and Jackson Progress-Argus. Subject to the terms and conditions of the agreement, effective as of April 1, 2006, CNHI assumed substantially all of the operating assets and assumed and became liable and otherwise responsible for substantially all of the operating liabilities and obligations of The Goshen News, and we assumed the operating assets and liabilities of the Jonesboro Group. Accordingly, the results of operations for the six months ended June 30, 2006 include only the results of the Jonesboro Group operations for the three months ended June 30, 2006. The results of operations for The Goshen News, for the year ended December 31, 2005 and the six months ended June 30, 2006, have been reclassified to discontinued operations for financial statement presentation. Additional information regarding the Jonesboro Group, its results of operations and its circulation are contained elsewhere in this Form 10-K.

5

Table of Contents

Index to Financial Statements

Operations

We own and operate The Albany Herald, Gwinnett Daily Post, Rockdale Citizen/Newton Citizen and Jonesboro Group. The following sets forth information regarding our newspapers as of June 30, 2008:

Originated | Year Originated | Year Acquired | Principal Location | Daily Circulation (1) | Sunday Circulation (1) | Non-Daily Circulation (2) | ||||||

The Albany | ||||||||||||

Herald | 1891 | 1948 | Albany, GA | 19,300 | 21,400 | 38,500 | ||||||

Rockdale | ||||||||||||

Citizen | 1953 | 1994 | Conyers, GA | 5,000 | 7,800 | |||||||

Newton | ||||||||||||

Citizen | 2004(3) | Covington, GA | 3,900 | n/a | ||||||||

Gwinnett | ||||||||||||

Daily Post | 1970(4) | 1995 | Lawrenceville, GA | 58,600 | 102,600 | |||||||

The Jackson | ||||||||||||

Progress- | 1873 | 2006(5) | Jackson, GA | 3,900 | n/a | |||||||

The Henry | ||||||||||||

Daily Herald | 1867 | 2006(5) | McDonough, GA | 2,400 | n/a | |||||||

The Clayton | ||||||||||||

News Daily | 1964 | 2006(5) | Jonesboro, GA | 2,100 | n/a |

| (1) | Circulation averages are derived from our internal records as of June 30, 2008. These internal records are subject to periodic independent audit by Certified Audit of Circulations, a circulation audit and research organization, but have not been audited as of June 30, 2008. |

| (2) | Non-Daily Distribution includes both paid and free distribution of the Albany Area Advertiser. Non-Daily Distribution reflects the averages according to the most recent internal reports. |

| (3) | In 2004, we began publication of the Newton Citizen. |

| (4) | The Gwinnett Daily Post was originally a weekly newspaper. In 1995, we began publishing the Gwinnett Daily Post on a daily basis. |

| (5) | The Jonesboro Group consists of three newspapers operated as a group sharing the printing facility at the Clayton News Daily. These newspapers were acquired in a swap transaction for The Goshen News as of April 1, 2006. |

The Albany Herald. The Albany Herald newspaper is located in Albany, Georgia and is published seven days a week to serve southwest Georgia. As of June 30, 2008, the Albany Herald has a daily circulation of approximately 19,300 and a Sunday circulation of approximately 21,400. The Albany Herald is the only daily newspaper in Albany, Georgia. The Albany Herald also produces a weekly advertising shopper and other niche publications. The Albany Area Advertiser is a shopper distributed weekly to all households in Dougherty and Lee counties. The Express is an advertising section distributed in selected zip codes, and The Emblem is a newspaper serving Marine Corps Logistics Base—Albany. Albany, situated in the Plantation Trace region, is the primary trade center for southwest Georgia. The city lies at the head of the Flint River, 145 miles south of Atlanta. Although the economy of the Albany region was formerly principally agricultural, it has developed a diversified industrial economy which includes companies such as The Procter & Gamble Company, Miller Brewing and M & M Mars. Albany is approximately 57 square miles and has a population of approximately 96,000.

6

Table of Contents

Index to Financial Statements

Gwinnett Daily Post, Rockdale Citizen and Newton Citizen. The Gwinnett Daily Post, Rockdale Citizen and Newton Citizen are newspapers that serve communities in the metro Atlanta, Georgia area with complete local news, sports and lifestyles coverage together with national stories that directly impact their local communities. The Gwinnett Daily Post, Rockdale Citizen and Newton Citizen are in adjacent metro Atlanta counties and benefit from cross selling advertising to classified and selected display advertisers, utilizing both a combined classified sales staff and major account sales staff located in Gwinnett. Additionally, synergies are derived from a combined production facility and news department copy desk, and centralized business and accounting functions where feasible.

As of June 30, 2008, the Gwinnett Daily Post is published Tuesday through Sunday and has a daily circulation of approximately 58,600 and a Sunday circulation of approximately 102,300. Since 1995, the frequency of publication has increased from three to six days per week and the circulation has grown from approximately 13,000 (daily) to its present levels. Gwinnett County is located 30 miles northeast of Atlanta, Georgia. The county is approximately 437 square miles in size and has a population of approximately 776,000. The offices of the Gwinnett Daily Post are located in Lawrenceville, Georgia, which is the county seat of Gwinnett County.

The Rockdale Citizen. The Rockdale Citizen was established in 1953 and is published seven days a week with weekday circulation of approximately 5,000 and Saturday and Sunday circulation of approximately 7,800 as of June 30, 2008. In 1999, the Rockdale Citizen began a zoned version of the newspaper in neighboring Newton County. As this product developed it was spun off as a separate publication in April 2004, known as the Newton Citizen, and it is published weekdays with circulation of approximately 3,900. Advertising is sold into the weekday products of both Citizens on a combined basis reaching approximately 8,900 households. The Rockdale Citizen maintains offices located in Conyers, the county seat of Rockdale County, and the Newton Citizen maintains offices located in Covington, the county seat of Newton County. Rockdale County is located 20 miles east of downtown Atlanta on Interstate 20, is approximately 130 square miles in size and has a population of approximately 82,000. Newton County is located 35 miles east of Atlanta on Interstate 20, is approximately 276 square miles in size and has a population of approximately 96,000.

Jonesboro Group.The Jonesboro Group consists of three newspapers in adjacent counties in the suburban Atlanta, Georgia area. The Clayton News Daily has been serving Clayton County since 1964 with a daily circulation as of June 30, 2008 of approximately 2,100 published Monday through Saturday. The Clayton County area has an estimated population of approximately 272,200. The Henry Daily Herald has been serving Henry County since 1867 with a daily circulation as of June 30, 2008 of approximately 2,400 published Monday through Saturday. The Henry County area has an estimated population of 186,000 and is expected to grow by 6% through 2009. The Jackson Progress-Argus has been serving Butts County since 1873, published every Wednesday with a circulation of approximately 3,900 as of June 30, 2008. Butts County has an estimated population of 23,700.

Advertising

Advertising revenue is the largest component of the total revenue from Newspaper Publishing, accounting for approximately 87%, 88%, 87% and 87% of the total revenue from Newspaper Publishing for the year ended December 31, 2005, the six months ended June 30, 2006 and the twelve months ended June 30, 2007 and 2008, respectively. We derive our advertising revenue from retail (local department stores, local accounts at national department stores, specialty shops and other retailers), national (national advertising accounts), classified (employment, automotive, real estate and personals) and other advertising. Our advertising rate structures vary among our publications and are a function of various factors, including advertising effectiveness, local market conditions, competition, circulation, readership, demographics and type of advertising (whether display or classified).

7

Table of Contents

Index to Financial Statements

The majority of Newspaper Publishing advertising revenue is derived from a diverse group of local retailers and classified advertisers. We believe, based upon our operating experience that our advertising revenue tends to be more stable than the advertising revenue of large metropolitan daily newspapers because our publications rely primarily on local advertising. Local advertising has historically been more stable than national advertising because local businesses generally have fewer effective advertising channels through which to reach their customers. Moreover, we are less reliant than large metropolitan daily newspapers upon classified advertising, which is generally more sensitive to economic conditions.

We do not rely upon any one company or industry for our advertising revenue, but rather are supported by a variety of companies and industries, including financial institutions, realtors, automobile dealerships, grocery stores, universities, hospitals and many other local businesses. No single advertiser represented more than 2% of the total revenue for the twelve months ended June 30, 2008 from Newspaper Publishing.

Our corporate management works with our local newspaper management to approve advertising rates and to establish goals for each year during a detailed annual budget process. We share advertising concepts among our publications, enabling our advertising managers and publishers to leverage advertising products and sales strategies that have already been successful in other markets that we serve.

Circulation

Circulation revenue accounted for approximately 12%, 10%, 10% and 10% of the total revenue from Newspaper Publishing for the year ended December 31, 2005, the six months ended June 30, 2006 and the twelve months ended June 30, 2007 and 2008, respectively. While our circulation revenue is not as significant as our advertising revenue, circulation trends impact the decisions of advertisers and advertising rates. Substantially all of our circulation revenue is derived from home delivery sales of publications to subscribers and single copy sales made through retailers and vending racks. Our corporate management works with our local newspaper management to establish subscription and single copy rates. In addition, we track rates of newspaper returns and customer service calls in an effort to optimize the number of newspapers available for sale and to improve delivery and customer service.

Our six paid daily and one paid weekly publications range in circulation from approximately 2,100 to approximately 58,600 (daily) and from approximately 7,800 to approximately 102,600 (Sunday). Set forth below is the percent change in our daily circulation from December 31, 2005 to June 30, 2008:

Percent Change in Daily Circulation

| December 31, 2005 | June 30, 2008 | Decrease | |||||

Daily circulation: | |||||||

Gwinnett Daily Post | 60,700 | 58,600 | -3.5 | % | |||

The Albany Herald | 26,100 | 19,300 | -26.1 | % | |||

Jonesboro Group (1) | 10,000 | 8,400 | -16.0 | % | |||

Rockdale Citizen/Newton Citizen | 10,700 | 8,900 | -16.8 | % | |||

Total | 107,500 | 95,200 | -11.4 | % | |||

| 1. | The Jonesboro Group consists of the Jackson Progress-Argus, Henry Daily Herald and Clayton News Daily. |

8

Table of Contents

Index to Financial Statements

Job Printing

We operate three printing facilities. To the extent we have excess press capacity at these facilities, we have from time to time provided commercial printing services to third parties, primarily for commercial materials, including other newsprint publications, to produce incremental revenue from existing equipment and personnel. Job printing and other revenue accounted for only approximately 1%, 2%,3%, and 3% of the total revenue from Newspaper Publishing for the year ended December 31, 2005, the six months ended June 30, 2006 and the twelve months ended June 30, 2007 and 2008, respectively.

Online Operations

All of our daily newspapers have their own free-access websites. Our objective is to have our websites complement our print newspapers by providing certain content from our newspapers, as well as unique content and interactive features. Our websites also provide an online marketplace for our advertisers.

The following is a list of our websites:

Newspaper | Website | |||

The Albany Herald | www.albanyherald.com | |||

Gwinnett Daily Post | www.gwinnettdailypost.com | |||

Rockdale Citizen | www.rockdalecitizen.com | |||

Newton Citizen | www.newtoncitizen.com | |||

Clayton News Daily | www.new-daily.com | |||

Henry Daily Herald | www.henryherald.com | |||

Jackson Progress-Argus | www.jacksonprogress-argus.com | |||

Online revenue is currently a mix of retail advertising, sold as a single product comprised of both printed and online advertising with proceeds allocated between the two, and classified advertising. For the twelve months ended June 30, 2008, our websites generated approximately $0.5 million of revenue. This revenue was insignificant in prior years.

Editorial

Our newspapers generally contain 16 to 100 pages with editorial content that emphasizes local news and topics of interest to the communities that they serve, such as local business, politics, entertainment and culture, as well as local youth, high school, college and professional sports. National and world news stories are sourced from the Associated Press. The editorial staff at each of our newspapers typically consists of a managing editor and several assistant editors and field reporters, who identify and report the local news in their communities. As of June 30, 2008, we employed 76 full-time and 2 part-time editorial personnel that we believe provide the most comprehensive local news coverage in the communities we serve. Approximately 58% of our total pages for the twelve months ended June 30, 2008 were devoted to news content.

Printing and Distribution

We operate three newspaper production and distribution facilities. The production facility for The Albany Herald is located in Albany, Georgia. The production facility in Jonesboro, Georgia is shared by the Jackson Progress-Argus, Henry Daily Herald and Clayton News Daily. The production facility located in Lawrenceville, Georgia is shared by the Gwinnett Daily Post and the Rockdale Citizen/Newton Citizen. By using this production facility for three daily newspapers, we are able to reduce the operating costs of our newspapers while increasing the quality of our newspapers. Our newspapers are generally fully paginated utilizing image-setter technology, which allows for design flexibility and high-quality reproduction of color graphics. Our newspapers are printed on efficient, high-speed web offset presses. The distribution of our daily newspapers is outsourced to independent, third-party distributors.

9

Table of Contents

Index to Financial Statements

Newsprint

The basic raw material of newspapers is newsprint. Newsprint represents one of our largest costs of producing our publications. In the twelve months ended June 30, 2008, we consumed approximately 8,500 metric tons of newsprint. We are currently operating under a contract with Abitibi Consolidated to purchase newsprint at prices that we believe are competitive for similar volume purchasers. Our current contract with Abitibi expires in 2012. We incurred newsprint expense related to our publications of approximately $4.8 million for the twelve months ended June 30, 2008.

Historically, the price of newsprint has been cyclical and volatile. The industry average price of newsprint for the twelve months ended June 30, 2008 was approximately $610 per metric ton. Prices fluctuate based upon factors that include both foreign and domestic production capacity and consumption. Price fluctuations can have a significant effect on our results of operations. We seek to manage the effects of increases in prices of newsprint through a combination of technology improvements, page width and page count reductions, inventory management and advertising and circulation price increases.

Competition

Our newspaper in Albany, Georgia is the dominant print editorial and advertising voice for the communities it serves. In Albany, The Herald is the only daily newspaper serving the primary market area with the exception of very limited circulation efforts by statewide and national newspapers, The Atlanta Journal-Constitution and USA Today. Our six Atlanta suburban newspapers enjoy a circulation advantage over The Atlanta Journal-Constitution in each paper’s designated market area, Gwinnett, Rockdale, Newton, Jackson (Butts County), Henry and Clayton, but The Atlanta Journal-Constitution has greater overall circulation in the Atlanta metro area.

Each of our newspapers competes for advertising and circulation revenue with local, regional and national newspapers, shoppers, magazines, radio, broadcast and cable television, direct mail, the Internet and other media sources. Competition for newspaper advertising revenue is based largely on advertising results, advertising rates, readership demographics and circulation levels. Competition for circulation revenue is generally based on the content of the newspaper, its price and editorial quality.

We differentiate our publications from other newspapers and media by focusing on local news and local sports coverage. We clearly identify the markets we wish to target and seek to become the primary source for local news and advertising information within those markets. We believe that our newspapers co-exist well with our larger competitors through our targeted distribution strategies that are designed to maximize unduplicated reach for advertisers and avoid head-to-head competition. We provide our readers with community-specific content, which is generally not available on a consistent basis from our larger competitors. Local advertisers, especially businesses located within a small community, typically target advertising towards customers living or working within their own communities. We believe that each of our newspapers generally capture the largest share of local advertising as a result of our direct and focused coverage of the market and our cost-effective advertising rates relative to the more broadly circulated newspapers of our larger competitors.

Although alternative media may be available, we believe that local advertisers generally regard newspapers as the most cost-effective method of advertising time-sensitive promotions and price-specific advertisements, as compared with broadcast and cable television, which are generally used to advertise image, or radio, which is usually used to recall images or brands in the minds of listeners. We have, however, over the past several years faced increased competition for classified advertising from online advertising.

10

Table of Contents

Index to Financial Statements

Environmental Matters

We are subject to a wide range of federal, state and local environmental laws and regulations pertaining to air and water quality, storage tanks and the management and disposal of waste at our facilities. To the best of our knowledge, our operations are in material compliance with applicable environmental laws and regulations as currently interpreted. We believe that continued compliance with these laws and regulations will not have a material adverse effect on our financial condition or results of operations.

Employees

At June 30, 2008, we employed approximately 340 persons, of which approximately 300 were full-time and 44 were part-time employees of the Newspaper Publishing business. None of our employees are covered by collective bargaining agreements. We consider our relationship with our employees to be satisfactory.

Available Information

Our Internet address iswww.triplecrownmedia.com, where we make available, free of charge, our Annual Reports on Form 10-K, Quarterly Reports on Form 10-Q, Current Reports on Form 8-K and any amendments to those reports, as soon as practicable after such reports are electronically filed with, or furnished to, the SEC. The SEC reports can be accessed through the “SEC Reports” link in the index on our website. Other information found on our website is not part of this or any other report we file with, or furnish to, the Securities and Exchange Commission, or the SEC.

Code of Ethics

We have adopted a Code of Ethics that applies to all of our directors, officers and employees. The Code is available on our website. If any waivers of the Code are granted, the waivers will be disclosed in an SEC filing on Form 8-K. Our website also includes the Charters of the Audit Committee and the Nominating, Corporate Governance, Compensation and Stock Option Committee. Stockholders may request free copies of these documents by writing to Mark G. Meikle, 725 Old Norcross Road, Lawrenceville, GA, 30045, by calling 770-338-7351 or sending an email request to mark.meikle@triplecrownmedia.com.

The public may also read and copy any materials we file with the SEC at the SEC’s Public Reference Room at 100 F Street, N.E., Washington, D.C. 20549. Information on the operation of the Public Reference Room may be obtained by calling 1-800-SEC-0330. The SEC maintains an Internet site that contains reports, proxy and information statements, and other information regarding issuers that file electronically with the SEC, atwww.sec.gov.

| Item 1A. | Risk Factors |

Going Concern

We do not anticipate meeting future debt compliance covenants in the fiscal year ending June 30 2009. Without waiver of these violations, which could occur at any time between now and June 30, 2009, and/or restructuring of our debt, our bank could accelerate our payment provisions. Further, the sale of Host and Pinnacle resulted in $2.6 million of tax liabilities to various taxing authorities which began to come due on September 15, 2008. Assuming no acceleration of payments, material portions of our debt facilities become due in December 2009, June 2010 and December 2010. In order to meet these obligations, we will be required to restructure our current credit facilities, refinance with another lender or, in the case of our income tax obligations successfully negotiate with the taxing authorities to

11

Table of Contents

Index to Financial Statements

arrange a payment plan which will allow us to spread our payments over an extended period of time. Should we be unsuccessful in these restructuring efforts, we will attempt to derive capital from alternate sources which may include any of the following; public equity offering, private placement, the issuance of additional shares of preferred stock or other means not yet identified. In the event that we are not able to arrange a payment plan for our tax obligations, or refinance our debt obligations, we may not have sufficient liquidity to operate.

These factors raise substantial doubt as to our ability to continue as a going concern. The accompanying financial statements have been prepared as on a going concern basis which assumes continuity of operations and realization of assets and liabilities in the ordinary course of business. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Our flexibility is limited by the terms of our senior secured credit facility.

Our senior secured credit facility prevents us from taking certain actions and requires us to meet certain tests. These limitations and tests include, without limitation, the following:

| • | limitations on liens; |

| • | limitations on incurrence of debt; |

| • | limitations on making dividends and distributions; |

| • | provisions for mandatory prepayments; |

| • | limitations on transactions with affiliates; |

| • | limitations on guarantees; |

| • | limitations on asset sales; |

| • | limitations on sale-leaseback transactions; |

| • | limitations on acquisitions; |

| • | limitations on changes in our business; |

| • | limitations on mergers and other corporate reorganizations; |

| • | limitations on loans, investments and advances, including investments in joint ventures and foreign subsidiaries; |

| • | financial ratio and condition tests; and |

| • | increases in our cost of borrowings or inability or unavailability of additional debt or equity capital. |

These restrictions and tests may prevent us from taking action that could increase the value of our securities, or may require actions that decrease the value of our securities. In addition, we may fail to meet the tests and thereby default under our senior secured credit facility. If we default on our obligations, our lenders could require immediate payment of the obligations or foreclose on collateral. If this happened, we could be forced to sell assets or take other action that would reduce the value of our securities.

Servicing our debt will require a significant amount of cash, and our ability to generate sufficient cash depends on many factors, some of which are beyond our control.

Our total debt as of June 30, 2008 was $70.8 million and as of the date of this filing we do not anticipate meeting our bank covenants in fiscal year 2009. Without waivers of these expected violations and restructuring of our debt, our bank could accelerate our payment provisions. Assuming

12

Table of Contents

Index to Financial Statements

no acceleration of payments, material portions of our debt facilities become due in December 2009, June 2010, and December 2010. Further, the sale of Host and Pinnacle Sports Production LLC, or Pinnacle, resulted in a $2.6 million tax liability which became due in September 2008 for which we are currently negotiating a payment plan with the taxing autorities. In order to meet these obligations, we will be required to restructure our current credit facilities, refinance with another lender or, in the case of our income tax obligations, attempt to arrange a payment plan which will allow us to spread our payments over an extended period of time. Should we be unsuccessful in these restructuring efforts, we will attempt to derive capital from alternate sources which may include any of the following; public equity offering, private placement, the issuance of additional shares of preferred stock or other means not yet identified. In the event that we are not able to arrange a payment plan for our tax obligations, or refinance our debt obligations, we may not have sufficient liquidity to operate.

We depend on the economies and the demographics of the local communities that our newspaper publications serve and we are also susceptible to general economic downturns, which could adversely affect our advertising and circulation revenue and our profitability.

Our advertising revenue and, to a lesser extent, circulation revenue depend upon a variety of factors specific to the communities that our publications serve. These factors include, among others:

| • | local economic conditions in general; |

| • | the economic condition of the retail segments of the communities that our publications serve; |

| • | the popularity of our publications; |

| • | the size and demographic characteristics of the local population; |

| • | pricing fluctuations in local and national advertising; |

| • | the activities of our competitors, including increased competition from other forms of advertising-based mediums; and |

| • | changing consumer lifestyles. |

Our newspapers operate in six suburban Atlanta counties—Gwinnett, Rockdale, Newton, Butts, Henry and Clayton counties, and Dougherty County in southwest Georgia. If the local economy, population or prevailing retail environment of a community served by our publications experiences a downturn, our publications, revenue and profitability in that market would be adversely affected. Our advertising and circulation revenue are also susceptible to negative trends in the general economy that affect consumer spending. The advertisers in our newspapers and related publications are primarily retail businesses, which can be significantly affected by regional or national economic downturns and other developments.

In the newspaper industry, we rely on advertising and paid circulation revenue, for which we face competition from other newspapers, some significantly larger than us, as well as other communications, media and web-based sources.

Our newspapers and other publications are located primarily in small metropolitan and suburban areas in the United States. Our newspapers operate in six suburban Atlanta counties—Gwinnett, Rockdale, Newton, Butts (Jackson Progress-Argus), Henry and Clayton counties, and Dougherty County in southwest Georgia. Revenue from Newspaper Publishing primarily consists of advertising and paid circulation. Competition for advertising expenditures and paid circulation comes from local, regional and national newspapers, shoppers, television, radio, direct mail, Internet and other forms of communication and advertising media. Competition for newspaper advertising expenditures is based largely upon advertiser results, readership, advertising rates, demographics and circulation levels,

13

Table of Contents

Index to Financial Statements

while competition for circulation and readership is based largely upon the content of the newspaper, its price and the effectiveness of its distribution. In recent years, web sites dedicated to recruitment, real estate and automotive sales have become significant competitors of our newspapers for classified advertising. Our six Atlanta suburban newspapers face competition from the larger metropolitan newspaper, The Atlanta Journal-Constitution, which serves the entire Atlanta metropolitan area and much of the state of Georgia. The Atlanta Journal-Constitution is significantly larger than our newspapers. Both advertising and circulation revenues are being affected by consumer trends, including declining newspaper buying by young people and the migration to other available forms of media for news.

Any significant increases in newsprint costs could have a material adverse effect on our operating results.

The basic raw material for newspapers is newsprint. Historically, the industry price of newsprint has been cyclical and volatile. The average price of newsprint was $610 and $643 per metric ton during the twelve months ended June 30, 2008 and June 30, 2007, respectively. During the twelve months ended June 30, 2008, we consumed approximately 8,500 metric tons of newsprint, the cost of which represented approximately 10.5% of the total revenue from Newspaper Publishing during such period. We have a contract with Abitibi Consolidated to purchase newsprint at prices pegged to industry averages and we expect price increases in fiscal 2009 up to $100 per metric ton. Our contract with Abitibi expires on December 31, 2012. Significant increases in newsprint costs could have a material adverse effect on our operating results.

We may be unable to identify or integrate acquisitions of daily and non-daily newspapers and similar publications successfully or on commercially acceptable terms and such failure could adversely affect our business, financial condition and results of operations.

We have made several acquisitions and in the future may make additional acquisitions of daily and non-daily newspapers and similar publications. We cannot assure you that we will be able to identify suitable acquisition candidates in the future. Even if we do identify suitable candidates, we cannot assure you that we will be able to make acquisitions on commercially acceptable terms. In making acquisitions, we compete for acquisition targets with other companies, many of which are larger and have greater financial resources than us. Our failure to acquire suitable candidates, or the consummation of a future acquisition at a price or on other terms that prove to be unfavorable, could adversely affect our business, financial condition and results of operations. In addition, acquisitions may expose us to particular business and financial risks that include:

| • | diverting management’s attention; |

| • | incurring significant additional liabilities, capital expenditures, transaction and operating expenses and non-recurring acquisition-related charges; |

| • | experiencing an adverse impact on our earnings from the amortization or impairment of acquired goodwill and other intangible assets; |

| • | failing to integrate the operations, facilities and personnel of the acquired newspapers and publications; |

| • | entering new markets with which we are not familiar; and |

| • | failing to retain key personnel of the acquired newspapers and publications. |

We may not be able to manage acquired newspapers and publications successfully. If we are unable successfully to implement our acquisition strategy or address the risks associated with acquisitions, or if we encounter unforeseen expenses, difficulties, complications or delays frequently encountered in connection with the integration of acquired entities and the expansion of operations, our

14

Table of Contents

Index to Financial Statements

growth and ability to compete may be impaired. We may fail to achieve acquisition synergies and we may be required to focus resources on the integration of operations rather than more profitable areas.

We will need to incur debt or issue equity securities to pay for any future acquisitions and to pay for increased capital expenditures following any acquisitions. However, debt or equity financing may not be available in sufficient amounts or on terms acceptable to us, or at all, and equity financing could be dilutive to our stockholders.

Changes in the regulations that govern our business might increase competition or make it more difficult or costly to operate our business or comply with such changes.

The FCC has broad authority to promulgate and enforce regulations that could adversely affect us. The FCC’s rules prohibit or place limitations on common ownership, including common officers or directors, of companies publishing newspapers or operating television stations in the same market. Because of ongoing administrative and judicial proceedings, these rules will remain in effect for the foreseeable future. As a result, our ability to acquire newspapers in areas served by Gray’s television stations could be foreclosed or limited to the term remaining on the television station’s license, a period not to exceed eight years. In certain instances, the ownership rules could result in our being required to divest our ownership interest in a newspaper whose city of publication is encompassed by the Grade A service contour of a station owned or acquired by Gray.

We may be required to take additional impairment charges on our goodwill, which may have a material effect on the value of our total assets.

As of June 30, 2008, the book value of our goodwill was $12.6 million in comparison to total assets of approximately $40.6 million. Not less than annually, we are required to evaluate our goodwill to determine if the estimated fair value of goodwill is less than its book value. If the estimated fair value of goodwill is less than book value, we will be required to record a non-cash expense to write down the book value of the goodwill to the estimated fair value. We cannot make any assurances that any required impairment charges will not have a material effect on our total assets.

We may incur significant capital and operating expenditures to achieve and maintain compliance with applicable environmental laws and regulations, or associated with environmental liabilities, and if such expenses significantly exceed our expectations, our operating income may be adversely affected.

Our business is subject to a wide range of federal, state and local environmental laws and regulations. We may incur significant capital and operating expenditures to achieve and maintain compliance with applicable environmental laws and regulations. Our failure to comply with applicable environmental laws and regulations or permit requirements could result in substantial civil or criminal fines or penalties or enforcement actions. As an owner and operator of real estate, we may be responsible under environmental laws and regulations for the investigation, remediation and monitoring, as well as associated costs, expenses and third-party damages, including tort liability relating to past or present releases of hazardous substances on or from our properties. Liability under these laws may be imposed without regard to whether we knew of, or were responsible for, the presence of those substances on our property and may not be limited to the value of the property. We also may be responsible under environmental laws and regulations for the investigation, remediation and monitoring, as well as associated costs, expenses and third-party damages, including tort liability, related to facilities or sites to which we have sent hazardous waste materials. In addition, situations may give rise to material environmental liabilities that have not yet been discovered. New environmental laws (or regulations or changes in existing laws) may be enacted that require significant expenditures by us. If the resulting expenses significantly exceed our expectations, our operating income may be adversely affected.

15

Table of Contents

Index to Financial Statements

Our success depends on our senior management.

Our success depends to a significant extent on the efforts of our senior management. As a result, if any of these individuals were to leave, we could face substantial difficulty in hiring and retaining qualified successors and could experience a loss in productivity while any successors gain the necessary experience.

Our historical financial information may not be representative of our results, as our Newspaper Publishing business previously operated as a subsidiary or division of Gray.

Our historical financial information for the year ended December 31, 2005, included in this Form 10-K may not be representative of our results of operations, financial position and cash flows had our Newspaper Publishing business operated as an independent company rather than as a subsidiary or division of Gray during the periods presented or of our results of operations, financial position and cash flows in the future. This results from the following:

| • | in preparing this historical financial information, adjustments and allocations were made because Gray did not account for this business as, and this business never operated as, a stand-alone business for any periods presented until the Spin-off on December 30, 2005; and |

| • | the information does not reflect many changes that have occurred in our funding and operations as a result of the Spin-off and the Merger. |

The agreements governing our relationship with Gray following the Spin-off were negotiated while we were a subsidiary of Gray and, as a result, we cannot assure you that the agreements are on terms favorable to us.

The agreements governing our relationship with Gray following the Spin-off were negotiated in a parent-subsidiary context and were negotiated in the overall context of our separation from Gray. At the time of these negotiations, our officers were employees of Gray, and each of the members of our board of directors was also a member of Gray’s board of directors. Accordingly, we cannot assure you that the terms of these agreements were the same as the terms that would have resulted from arm’s-length negotiations between third parties. These agreements include a separation and distribution agreement, as amended, a tax sharing agreement and a lease agreement.

After the separation, certain members of management and directors of Gray and TCM, who are also shareholders of both companies, may face issues with respect to their relationships with Gray and TCM when the interests of Gray and TCM are not aligned or with respect to the allocation of their time between Gray and TCM.

The management and directors of Gray and TCM own our common stock and both Gray Class A common stock and Gray common stock. For instance, J. Mack Robinson is the Chairman and Chief Executive Officer of Gray and the beneficial owner of approximately 9% of the outstanding shares of our common stock and all of the outstanding shares of our preferred stock. Robert S. Prather, Jr. is the President, Chief Operating Officer and a director of Gray and the Chief Executive Officer and a director of TCM. Hilton H. Howell, Jr. is the Vice Chairman and a director of Gray and the Chairman of the Board of TCM. This ownership overlap and these common directors could create, or appear to create, potential issues when Gray’s and TCM’s management and directors face decisions where our interests and Gray’s interests are not aligned. For example, potential issues could arise in connection with the resolution of any dispute between Gray and us regarding the terms of the agreements governing the separation and the relationship between Gray and us. These agreements include a separation and distribution agreement, as amended, a tax sharing agreement and a lease agreement. Each of Mr. Prather and Mr. Howell may also face issues with regard to the allocation of his time between Gray and us.

16

Table of Contents

Index to Financial Statements

The market price for our common stock may be volatile and stockholders may not be able to sell our common stock at a favorable price or at all.

Many factors could cause the market price of our common stock to rise and fall, including:

| • | variations in our quarterly results; |

| • | announcements of technological innovations by us or by our competitors; |

| • | introductions of new products or new pricing policies by us or by our competitors; |

| • | acquisitions or strategic alliances by us or by our competitors; |

| • | recruitment or departure of key personnel; |

| • | the gain or loss of significant customers; |

| • | changes in the estimates of our operating performance or changes in recommendations by any securities analysts that elect to follow our common stock; and |

| • | market conditions in our industry, the industries of our customers, and the economy as a whole. |

On April 15, 2007 we received an initial notification from The Nasdaq Stock Market that we had not maintained a minimum market value of its shares of common stock in accordance with Marketplace Rule 4450(e)(1) and would be required to regain compliance by July 14, 2008. On July 16, 2008 we received a follow-up notification from The Nasdaq Stock Market that we had not regained compliance in accordance with Marketplace Rule 4450(e)(1). Accordingly, our securities were delisted from The Nasdaq Global Market. Trading of our common stock was suspended at the opening of business on July 25, 2008, and a Form 25-NSE was filed with the SEC, which removed our securities from listing and registration on The Nasdaq Stock Market. Our securities will continue to be quoted in the pink sheets under the symbol TCMI.

Change in control provisions could make it more difficult for a third party to acquire us and discourage a takeover, even when such attempts may be in the best interests of our stockholders or on terms where our stockholders may be able to receive a premium for their shares over then current market prices.

Our amended and restated certificate of incorporation and the Delaware General Corporation Law, or the DGCL, contain provisions that may have the effect of making more difficult or delaying attempts by others to obtain control of us, even when these attempts may be in the best interests of stockholders. These include provisions authorizing our board of directors, without stockholder approval, to issue one or more series of preferred stock, which could have voting and conversion rights that adversely affect or dilute the voting power of the holders of our common stock. The DGCL also imposes conditions on certain business combination transactions with “interested stockholders.” These provisions and others that could be adopted in the future could deter unsolicited takeovers or delay or prevent changes in our control or management, including transactions in which stockholders might otherwise receive a premium for their shares over then current market prices. These provisions may limit the ability of stockholders to approve transactions that they may deem to be in their best interests.

We may be unable to restructure our senior secured facility.

Recent news accounts report that Wachovia Corporation, the administrative agent within the Company’s lending group, is to be acquired in a transaction structured with the assistance of federal regulators. Wachovia’s situation could further complicate our debt restructuring progress.

| Item 1B. | Unresolved Staff Comments |

None.

17

Table of Contents

Index to Financial Statements

| Item 2. | Properties |

Our executive offices are located in Lawrenceville, Georgia in office space leased under an agreement that expires October 2013.

Property Location | Use | Owned or Leased | Approximate Size (Sq. Ft.) | Lease Expiration Date | ||||

Albany, GA | Offices and production facility for The Albany Herald | Owned | 83,000 | n/a | ||||

Conyers, GA | Offices forRockdale Citizen | Owned | 20,000 | n/a | ||||

Conyers, GA | Warehouse | Leased | 9,600 | 3/08 | ||||

Covington, GA | Offices forNewton Citizen | Leased | 3,750 | 4/10 | ||||

Duluth, GA | Circulation distribution center | Leased | 7,866 | 8/08 | ||||

Lawrenceville, GA | Offices and production facility forGwinnett Daily Postand Rockdale Citizen/Newton Citizen | Leased | 72,000 | 10/13 | ||||

Bethlehem, GA | Circulation distribution center | Leased | 5,600 | 6/09 | ||||

Jonesboro, GA | Offices and production facility forClayton News Daily, Henry Daily Herald and Jackson Progress-Argus | Owned | 19,275 | n/a | ||||

Jackson, GA | Offices forJackson Progress-Argus | Owned | 3,096 | n/a | ||||

McDonough, GA | Offices forHenry Daily Herald | Leased | 2,400 | 12/08 | ||||

In addition, we have approximately 4,300 square feet of office space under lease in New York City through August 2010, all of which has been subleased, and also have small regional and local field offices primarily located close to the universities and conferences that we used to do business with when we owned Host.

We believe our facilities are adequate for the continuing operations of our existing businesses. Our Credit Facilities, as described in Note 8 to the financial statements are secured by all property that we own.

| Item 3. | Legal Proceedings |

We are subject to various legal proceedings in the ordinary course of business, none of which is required to be disclosed under this item 3.

| Item 4. | Submission of Matters to a Vote of Security Holders |

No matters were submitted to a vote of security holders during the fourth quarter of the fiscal year ended June 30, 2008.

18

Table of Contents

Index to Financial Statements

PART II

| Item 5. | Market for the Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities |

Market Information

Our common stock, par value $.001 per share, has been listed and traded on the Nasdaq Global Market (“NASDAQ”) since December 20, 2005 under the symbol “TCMI.”

On April 15, 2008, we received an initial notification from The Nasdaq Stock Market that we had not maintained a minimum market value of our shares of common stock in accordance with Marketplace Rule 4450(e)(1) and would be required to regain compliance by July 14, 2008. On July 16, 2008, we received a follow-up notification from The Nasdaq Stock Market that we had not regained compliance in accordance with Marketplace Rule 4450(e)(1). Accordingly, our securities were delisted from The Nasdaq Global Market. Trading of our common stock was suspended at the opening of business on July 25, 2008, and a Form 25-NSE was filed with the SEC, which removed our securities from listing and registration on The Nasdaq Stock Market. Our securities will continue to be quoted in the pink sheets under the symbol TCMI.

The following table sets forth the high and low sale prices of our common stock for the periods indicated. The high and low sales prices are as reported by the NASDAQ.

Quarter Ended | High | Low | ||||

Fiscal 2008 | ||||||

September 30, 2007 | $ | 10.44 | $ | 5.72 | ||

December 31, 2007 | $ | 6.50 | $ | 4.40 | ||

March 31, 2008 | $ | 5.55 | $ | 2.71 | ||

June 30, 2008 | $ | 2.80 | $ | 0.47 | ||

Fiscal 2007 | ||||||

September 30, 2006 | $ | 8.66 | $ | 7.15 | ||

December 31, 2006 | $ | 7.98 | $ | 6.80 | ||

March 31, 2007 | $ | 11.31 | $ | 7.88 | ||

June 30, 2007 | $ | 10.49 | $ | 8.30 | ||

Fiscal 2006 | ||||||

March 31, 2006 | $ | 12.00 | $ | 5.66 | ||

June 30, 2006 | $ | 8.67 | $ | 5.00 | ||

Fiscal 2005 | ||||||

December 31, 2005 | $ | 15.50 | $ | 11.01 | ||

As of September 15, 2008, we had approximately 380 stockholders of record.

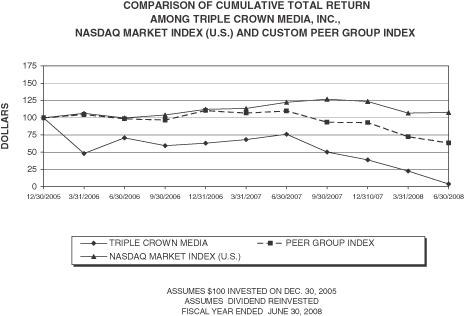

The following graphs compare the cumulative total return of our common stock from December 30, 2005 to June 30, 2008 as compared to the stock market total return indexes for (1) the NASDAQ Market Index and (2) a Custom Peer Group Index based upon the Hemscott Marketing Services Industry Group Index (50.7%) and Hemscott Publishing—Newspaper Industry Group Index (49.3%). These percentages are based on relative revenue and profitability of each of our primary business segments.

19

Table of Contents

Index to Financial Statements

The graphs assume the investment of $100 in the common stock, the NASDAQ Market Index and the Custom Peer Group Index on December 30, 2005. Dividends are assumed to have been reinvested as paid.

Dividends

We have not declared or paid a cash dividend on our common stock. It is the present policy of our Board of Directors to retain all earnings to finance the development and growth of our business. Our future dividend policy will depend upon our earnings, capital requirements, financial condition and other relevant circumstances existing at that time. Our bank credit agreements also contain restrictions on our ability to declare and pay dividends on our common stock.

Equity Compensation Plan Information

See “Item 12—Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters—Equity Compensation Plan Information” for disclosure regarding our equity compensation plans.

20

Table of Contents

Index to Financial Statements

| Item 6. | Selected Financial Data |

The following table sets forth our summary historical financial information after giving effect to the Spin-off and Merger. The summary selected historical statement of operations data for the years ended December 31, 2003 and 2004 and the summary selected balance sheet data as of December 31, 2003 and 2004 was derived from our audited financial statements as of and for the years then ended. The summary selected historical statement of operations data for the year ended December 31, 2005 was derived from our audited financial statements for the year then ended, and includes the combined operating results for 364 days as part of Gray through the date of the Spin-off and the consolidated operating results for the one day after the Spin-off (which are included in discontinued operations). The summary selected statement of operations data for the six months ended June 30, 2006 and the twelve months ended June 30, 2007 and 2008 was derived from our audited financial statements. The summary selected balance sheet data as of December 31, 2005 and June 30, 2006, 2007 and 2008 was derived from our audited financial statements. The audited financial statements include all adjustments, consisting of normal recurring items, which we consider necessary for a fair statement of our financial position and results of operations for those periods. For the periods and dates prior to the Spin-off, the financial statements were derived from the financial statements and accounting records of Gray using the historical results of operations and historical basis of the assets and liabilities of the Newspaper Publishing segment and the GrayLink Wireless segment and include those assets, liabilities, revenues, and expenses directly attributable to the operations of the Newspaper Publishing and the GrayLink Wireless segments and allocations of certain Gray corporate expenses to the Newspaper Publishing and the GrayLink Wireless segments. These amounts were allocated to us on the basis that was considered by us and Gray to reflect most fairly or reasonably the utilization of the services provided, or the benefit received by, us. All significant intercompany amounts and transactions were eliminated. The GrayLink Wireless segment is included in discontinued operations as further discussed in footnote 10 to the consolidated financial statements. The summary historical financial information presented for periods prior to the Spin-off is not necessarily indicative of our past or future performance as an independent company. The summary historical financial information as of December 31, 2005 include the effect of the Merger, including the operating results of the Collegiate Marketing and Association Management Services segments for the one day subsequent to the Merger (which is accounted for in discontinued operations as further discussed in footnote 10 to the consolidated financial statements). This information should be read in conjunction with our combined financial statements and notes thereto and the discussion under “Management’s Discussion and Analysis of Financial Condition and Results of Operations” contained elsewhere in this Form 10-K.

21

Table of Contents

Index to Financial Statements

Statement of Operations Data: (Dollars in thousands, except per share data) | ||||||||||||||||||||||

| Year Ended December 31, (1) | Six Months Ended June 30, 2006 | Twelve Months Ended June 30, 2007 | Twelve Months Ended June 30, 2008 (2) | |||||||||||||||||||

| 2003 | 2004 | 2005 | ||||||||||||||||||||

Operating revenues | $ | 36,670 | $ | 38,790 | $ | 40,237 | $ | 22,047 | $ | 48,464 | $ | 46,021 | ||||||||||

Operating income | 8,927 | 9,002 | 7,782 | 2,893 | 6,894 | 1,444 | ||||||||||||||||

Earnings (loss) from continuing operations | 5,238 | 5,681 | 4,679 | (2,276 | ) | (5,062 | ) | (17,994 | ) | |||||||||||||

Income (loss) from discontinued operations, net of tax | 1,691 | 1,574 | (262 | ) | 987 | 1,967 | (37,189 | ) | ||||||||||||||

Gain (loss) on disposal of discontinued operations, net of tax | — | — | — | 5,685 | (381 | ) | (3,767 | ) | ||||||||||||||

Net income | 6,929 | 7,255 | 4,417 | 4,396 | (3,476 | ) | (58,950 | ) | ||||||||||||||

Net income available to common stockholders | 6,929 | 7,255 | 4,414 | 3,854 | (4,562 | ) | (60,040 | ) | ||||||||||||||

Basic and diluted net income (loss) per common share (3) | ||||||||||||||||||||||

Earnings (loss) from continuing operations | $ | 1.08 | $ | 1.17 | $ | 0.96 | $ | (0.44 | ) | $ | (0.96 | ) | $ | (3.24 | ) | |||||||

Income (loss) from discontinued operations | $ | 0.35 | $ | 0.32 | $ | (0.05 | ) | $ | 0.19 | $ | 0.37 | $ | (6.70 | ) | ||||||||

Gain (loss) on disposal of discontinued operations, net of tax | $ | — | $ | — | $ | — | $ | 1.11 | $ | (0.07 | ) | $ | (0.68 | ) | ||||||||

Net income (loss) | $ | 1.42 | $ | 1.49 | $ | 0.91 | $ | 0.86 | $ | (0.66 | ) | $ | (10.62 | ) | ||||||||

Net income (loss) available to common stockholders | $ | 1.42 | $ | 1.49 | $ | 0.91 | $ | 0.75 | $ | (0.87 | ) | $ | (10.81 | ) | ||||||||

Weighted average shares outstanding | 4,870 | 4,870 | 4,871 | 5,139 | 5,246 | 5,553 | ||||||||||||||||

| (1) | Operating revenues and income have been adjusted for discontinued operations of The Goshen News and GrayLink, LLC, or Graylink, discussed elsewhere in this Form 10-K. See footnote 11 to the consolidated financial statements contained elsewhere in this Form 10-K for further information. |

| (2) | Income (loss) from discontinued operations, net of tax, includes a $27.3 million goodwill impairment charge. |

| (3) | For the years ended December 31, 2003, 2004 and 2005, the (basic and diluted) income from continuing operations per share gives effect to the issuance of 4,870,000 shares of our common stock in the Spin-off as if it had occurred at the beginning of the periods presented. For the day of December 31, 2005, 5,128,000 shares of our common stock were assumed to be outstanding, including 258,000 shares to be issued in exchange for shares of Bull Run common stock. Average shares outstanding for the six months ended June 30, 2006 and the twelve months ended June 30, 2007 were 5,138,775 and 5,246,249, respectively. |

We did not pay or declare any cash dividends during the periods presented.

| (Dollars in thousands) | As of December 31, | As of June 30, | ||||||||||||||||||||

| 2003 | 2004 | 2005 | 2006 | 2007 | 2008 | |||||||||||||||||

Total assets | $ | 37,818 | $ | 39,240 | $ | 171,029 | $ | 163,575 | $ | 174,462 | $ | 40,625 | ||||||||||

Long-term debt (including current portion) | 56 | — | 121,939 | 119,276 | 124,770 | 70,802 | ||||||||||||||||

Owner’s net investment / Stockholder’s equity (deficit) | 29,254 | 29,800 | (7,210 | ) | (2,714 | ) | (5,872 | ) | (64,962 | ) | ||||||||||||

22

Table of Contents

Index to Financial Statements

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations |

Executive Overview

Introduction

The following analysis of our financial condition and results of operations should be read in conjunction with our audited combined financial statements and notes thereto included elsewhere in this Form 10-K. All references to Triple Crown Media, Inc., “TCM”, “we,” “us,” or “our” in this discussion refer to the consolidated Newspaper Publishing business. The Newspaper Publishing business has historically operated as a wholly-owned subsidiary or division of Gray and since June 30, 2005, has operated as Gray Publishing LLC, a wholly-owned limited liability company and subsidiary of Gray prior to the Spin-off and of TCM, subsequent to the Spin-off.

We do not anticipate meeting certain future debt compliance covenants (First Lien leverage and total leverage ratio) in the fiscal year ending June 30 2009. Without waiver of these violations, which could occur at any time between now and June 30, 2009, and/or restructuring of our debt, our bank could accelerate our payment provisions. Further, the sale of Host and Pinnacle resulted in $2.6 million of tax liabilities which began to come due on September 15, 2008. Assuming no acceleration of payments, material portions of our debt facilities become due in December 2009, June 2010 and December 2010. In order to meet these obligations, we will be required to restructure our current credit facilities and refinance with another lender. In the case of our income tax obligations, we are negotiating with the taxing authorities to arrange a payment plan which will allow us to spread our payments over an extended period of time. Should we be unsuccessful in these restructuring efforts, we will attempt to derive capital from alternate sources which may include any of the following; private placement, the issuance of additional shares of preferred stock or other means not yet identified. In the event that we are not able to arrange a payment plan for our tax obligations, or refinance our debt obligations, we may not have sufficient liquidity to operate.

These factors raise substantial doubt as to our ability to continue as a going concern. The accompanying financial statements have been prepared on a going concern basis which assumes continuity of operations and realization of assets and liabilities in the ordinary course of business. The financial statements do not include any adjustments that might result from the outcome of this uncertainty.

Change in Year End

In April 2006, we elected to change our fiscal year end from December 31 to a new fiscal year end of June 30. In view of this change, this Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” (“MD&A”) compares the consolidated financial statements as of and for the twelve months ended June 30, 2008 with the combined financial statements as of and for the twelve months ended June 30, 2007. Note that although the combined financial statements are not presented as of and for the twelve months ended June 30, 2006, we have included summary information in the MD&A for this period for comparability purposes.

Throughout the MD&A, data for all periods, except as of and for the twelve months ended June 30, 2006, are derived from our audited combined and consolidated financial statements, which appear in this report. All data as of and for the twelve months ended June 30, 2006, are derived from our unaudited combined financial statements, which are not presented herein. Summary financial information for this period can be found in Note 16 to the consolidated financial statements contained elsewhere in this Form 10-K.

23

Table of Contents

Index to Financial Statements

Overview

We derive revenue from our Newspaper Publishing operations. Our Newspaper Publishing operations derive revenue primarily from three sources: retail advertising, circulation and classified advertising

Our Newspaper Publishing operations’ advertising contracts are generally entered into annually and provide for a commitment as to the volume of advertising to be purchased by an advertiser during the year. Our Newspaper Publishing operations’ advertising revenues are primarily generated from local advertising and are generally highest in the second and fourth quarters of each calendar year.

Industrywide, newspaper subscriber circulation levels have been slowly declining. From December 31, 2005 through June 30, 2008, our aggregate daily circulation has declined approximately 11%. We attempt to offset declines in circulation and corresponding circulation revenue with strategies that include readership growth in Gwinnett and Newton County, Georgia and efforts to increase circulation among cable subscribers in Gwinnett County, Georgia under our unique relationship whereby newspaper subscriptions are sponsored by local cable companies.