Filed by Obsidian Energy Ltd. (Commission File No. 001-32895) Pursuant to Rule 425 under the Securities Act of 1933 Subject Company: Bonterra Energy Corp. Obsidian Energy Corporate Presentation October 2020Filed by Obsidian Energy Ltd. (Commission File No. 001-32895) Pursuant to Rule 425 under the Securities Act of 1933 Subject Company: Bonterra Energy Corp. Obsidian Energy Corporate Presentation October 2020

Important Notice to the Readers This presentation should be read in conjunction with the Company’s unaudited interim consolidated financial statements, Management's Discussion and Analysis ( MD&A ) for the three and six months ended June 30, 2020. All dollar amounts contained in this presentation are expressed in millions of Canadian dollars unless otherwise indicated. Certain financial measures included in this presentation do not have a standardized meaning prescribed by International Financial Reporting Standards (“IFRS”) and therefore are considered non-generally accepted accounting practice (“Non-GAAP ) measures; accordingly, they may not be comparable to similar measures provided by other issuers. This presentation also contains oil and gas disclosures, various industry terms, and forward-looking statements, including various assumptions on which such forward-looking statements are based and related risk factors. Please see the Company's disclosures located in the Appendix & Endnotes at the end of this presentation for further details regarding these matters. All slides in this presentation should be read in conjunction with “Definitions and Industry Terms”, “Non-GAAP Measure Advisory”, “Oil and Gas Information Advisory”, “Reserves Disclosure and Definitions Advisory” and “Forward-Looking Information Advisory”. All locations are considered to be Unbooked locations unless otherwise noted. This presentation does not constitute an offer to buy or sell, or an invitation or a solicitation of an offer to buy or sell, any securities of the Company or Bonterra Energy Corp. (“Bonterra”). The Company’s offer to purchase all of the issued and outstanding common shares of Bonterra for consideration consisting of two common shares of the Company for each Bonterra share (the “Offer”) the offer to purchase and take-over bid circular dated September 21, 2020 and related offer documents (collectively, “Offer Documents”) that were mailed to Bonterra shareholders and have also been filed with the Canadian and United States securities regulators and are available under the Company’s SEDAR profile at www.sedar.com, in the United States on EDGAR at www.sec.gov and on the Company’s website at www.obsidianenergy.com. The Offer is made exclusively by means of, and subject to the terms and conditions set out in, the Offer Documents. While the Offer will be made to all holders of Bonterra shares, the Offer will not be made or directed to, nor will deposits of Bonterra shares be accepted from or on behalf of, holders of Bonterra shares in any jurisdiction in which the making or acceptance of the Offer would not be in compliance with the laws of such jurisdiction. The Offer is open for acceptance until 5:00 p.m. (Mountain Standard Time) on January 4, 2021, unless extended, accelerated or withdrawn. As set out in further detail in the Offer Documents, the Offer is subject to certain conditions, including: that the Bonterra shares validly deposited to the Offer, and not withdrawn, represent at least 66 2/3% of the then outstanding Bonterra shares (on a fully-diluted basis) and certain regulatory and third party approvals (as outlined in the Offer Documents) shall have been obtained, including the Company’s shareholders approving, as required by the rules of the Toronto Stock Exchange, the issuance of the shares to be distributed by the Company in connection with the Offer, and other customary conditions. Subject to applicable law, the Company reserves the right to withdraw, accelerate or extend the Offer and to not take up and pay for any Bonterra shares deposited under the Offer unless each of the conditions of the Offer is satisfied or waived by the Company at or prior to the expiry of the Offer. Bonterra shareholders are strongly encouraged to read the Offer Documents carefully and in their entirety since they contain additional important information regarding the Company and the terms and conditions of the Offer as well as detailed instructions on how Bonterra shareholders can tender their Bonterra shares to the Offer. The offer and sale of shares of the Company pursuant to the Offer is subject to a registration statement (the “Registration Statement”) filed with the United States Securities and Exchange Commission (the “SEC”) under the U.S. Securities Act of 1933, as amended. The Registration Statement includes various documents related to such offer and sale. THE COMPANY URGES INVESTORS AND SHAREHOLDERS OF BONTERRA TO READ THE REGISTRATION STATEMENT AND ANY AND ALL OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH THE SEC IN CONNECTION WITH THE OFFER AND SALE OF OBSIDIAN SHARES AS THOSE DOCUMENTS BECOME AVAILABLE, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION. You will be able to obtain a free copy of such registration statement, as well as other relevant filings regarding the Company or the Offer, at the SEC’s website (www.sec.gov) under the issuer profile for the Company, or on request without charge from the Corporate Secretary of the Company at Suite 200, 207 – 9th Avenue, SW, Calgary, Alberta T2P 1K3. 2Important Notice to the Readers This presentation should be read in conjunction with the Company’s unaudited interim consolidated financial statements, Management's Discussion and Analysis ( MD&A ) for the three and six months ended June 30, 2020. All dollar amounts contained in this presentation are expressed in millions of Canadian dollars unless otherwise indicated. Certain financial measures included in this presentation do not have a standardized meaning prescribed by International Financial Reporting Standards (“IFRS”) and therefore are considered non-generally accepted accounting practice (“Non-GAAP ) measures; accordingly, they may not be comparable to similar measures provided by other issuers. This presentation also contains oil and gas disclosures, various industry terms, and forward-looking statements, including various assumptions on which such forward-looking statements are based and related risk factors. Please see the Company's disclosures located in the Appendix & Endnotes at the end of this presentation for further details regarding these matters. All slides in this presentation should be read in conjunction with “Definitions and Industry Terms”, “Non-GAAP Measure Advisory”, “Oil and Gas Information Advisory”, “Reserves Disclosure and Definitions Advisory” and “Forward-Looking Information Advisory”. All locations are considered to be Unbooked locations unless otherwise noted. This presentation does not constitute an offer to buy or sell, or an invitation or a solicitation of an offer to buy or sell, any securities of the Company or Bonterra Energy Corp. (“Bonterra”). The Company’s offer to purchase all of the issued and outstanding common shares of Bonterra for consideration consisting of two common shares of the Company for each Bonterra share (the “Offer”) the offer to purchase and take-over bid circular dated September 21, 2020 and related offer documents (collectively, “Offer Documents”) that were mailed to Bonterra shareholders and have also been filed with the Canadian and United States securities regulators and are available under the Company’s SEDAR profile at www.sedar.com, in the United States on EDGAR at www.sec.gov and on the Company’s website at www.obsidianenergy.com. The Offer is made exclusively by means of, and subject to the terms and conditions set out in, the Offer Documents. While the Offer will be made to all holders of Bonterra shares, the Offer will not be made or directed to, nor will deposits of Bonterra shares be accepted from or on behalf of, holders of Bonterra shares in any jurisdiction in which the making or acceptance of the Offer would not be in compliance with the laws of such jurisdiction. The Offer is open for acceptance until 5:00 p.m. (Mountain Standard Time) on January 4, 2021, unless extended, accelerated or withdrawn. As set out in further detail in the Offer Documents, the Offer is subject to certain conditions, including: that the Bonterra shares validly deposited to the Offer, and not withdrawn, represent at least 66 2/3% of the then outstanding Bonterra shares (on a fully-diluted basis) and certain regulatory and third party approvals (as outlined in the Offer Documents) shall have been obtained, including the Company’s shareholders approving, as required by the rules of the Toronto Stock Exchange, the issuance of the shares to be distributed by the Company in connection with the Offer, and other customary conditions. Subject to applicable law, the Company reserves the right to withdraw, accelerate or extend the Offer and to not take up and pay for any Bonterra shares deposited under the Offer unless each of the conditions of the Offer is satisfied or waived by the Company at or prior to the expiry of the Offer. Bonterra shareholders are strongly encouraged to read the Offer Documents carefully and in their entirety since they contain additional important information regarding the Company and the terms and conditions of the Offer as well as detailed instructions on how Bonterra shareholders can tender their Bonterra shares to the Offer. The offer and sale of shares of the Company pursuant to the Offer is subject to a registration statement (the “Registration Statement”) filed with the United States Securities and Exchange Commission (the “SEC”) under the U.S. Securities Act of 1933, as amended. The Registration Statement includes various documents related to such offer and sale. THE COMPANY URGES INVESTORS AND SHAREHOLDERS OF BONTERRA TO READ THE REGISTRATION STATEMENT AND ANY AND ALL OTHER RELEVANT DOCUMENTS FILED OR TO BE FILED WITH THE SEC IN CONNECTION WITH THE OFFER AND SALE OF OBSIDIAN SHARES AS THOSE DOCUMENTS BECOME AVAILABLE, AS WELL AS ANY AMENDMENTS OR SUPPLEMENTS TO THOSE DOCUMENTS, BECAUSE THEY CONTAIN OR WILL CONTAIN IMPORTANT INFORMATION. You will be able to obtain a free copy of such registration statement, as well as other relevant filings regarding the Company or the Offer, at the SEC’s website (www.sec.gov) under the issuer profile for the Company, or on request without charge from the Corporate Secretary of the Company at Suite 200, 207 – 9th Avenue, SW, Calgary, Alberta T2P 1K3. 2

Corporate Overview Market Summary Ticker Symbol OBE Peace River MM Shares Outstanding 73 2,132 boe/d Q2 2020 Cold flow heavy oil MM Market Capitalization $35 Manage base production MM Net Debt $496 MM Enterprise Value $531 Corporate Summary mmboe Reserves (2P YE 2019) 126 Cardium years RLI (2P YE 2019) 14 22,456 boe/d Q2 2020 Light oil conventional % PDP Decline (YE 2019) 17 development Manufacturing model for MM Tax Pools (YE 2019) $2,547 extensive, repeatable inventory. Leverage shallow decline base Guidance Period H2 2020 boe/d Production 24,000 – 24,500 25,000 – 25,500 MM Capital Expenditures $10 $51 MM Decommissioning $3 $11 Alberta Viking $/boe Operating Costs $12.00 – $12.50 $11.10 – 11.50 880 boe/d Q2 2020 General & Higher GOR oil play $/boe $1.50 – $1.65 $1.50 – 1.60 Administrative Manage base production *Legacy Asset Production of 405 boe/d Q2 2020 3 3 See end notes for additional information Corporate Overview Market Summary Ticker Symbol OBE Peace River MM Shares Outstanding 73 2,132 boe/d Q2 2020 Cold flow heavy oil MM Market Capitalization $35 Manage base production MM Net Debt $496 MM Enterprise Value $531 Corporate Summary mmboe Reserves (2P YE 2019) 126 Cardium years RLI (2P YE 2019) 14 22,456 boe/d Q2 2020 Light oil conventional % PDP Decline (YE 2019) 17 development Manufacturing model for MM Tax Pools (YE 2019) $2,547 extensive, repeatable inventory. Leverage shallow decline base Guidance Period H2 2020 boe/d Production 24,000 – 24,500 25,000 – 25,500 MM Capital Expenditures $10 $51 MM Decommissioning $3 $11 Alberta Viking $/boe Operating Costs $12.00 – $12.50 $11.10 – 11.50 880 boe/d Q2 2020 General & Higher GOR oil play $/boe $1.50 – $1.65 $1.50 – 1.60 Administrative Manage base production *Legacy Asset Production of 405 boe/d Q2 2020 3 3 See end notes for additional information

Short-term Strategic Priorities & H1 2020 Results Short-term Priorities • Pursue successful acquisition of Bonterra to create “The Cardium Champion” • Transformational opportunity for both companies shareholders • Continue operational momentum and cost reduction initiatives to improve the base business • Protect long-term asset value • Substantial future development program optionality exists within Obsidian Energy’s portfolio in both available drilling inventory and product mix (gas/oil) – the asset base allows us significant flexibility to navigate volatility in commodity price environments • Development plans are ready to be executed when the economic environment justifies investment • Expand decommissioning activity utilizing $17 million in grants and $4 million in allocation eligibility within the Alberta Site Rehabilitation Program (ASRP) H1 2020 Results Guidance Results boe/d • Obsidian Energy exceeded all guidance targets in a Production 25,500 – 26,000 26,482 very challenging macro environment Capital MM $43 $41 • Production ahead due to strong Expenditures development program results MM Decommissioning $8 $8 • Capital expenditures lower due to effective execution $/boe Operating Costs $11.50 – 11.90 $10.32 • Operating costs and G&A lower due to cost cutting efforts and proactive decision making General & $/boe $1.65 – 1.85 $1.50 Administrative 4Short-term Strategic Priorities & H1 2020 Results Short-term Priorities • Pursue successful acquisition of Bonterra to create “The Cardium Champion” • Transformational opportunity for both companies shareholders • Continue operational momentum and cost reduction initiatives to improve the base business • Protect long-term asset value • Substantial future development program optionality exists within Obsidian Energy’s portfolio in both available drilling inventory and product mix (gas/oil) – the asset base allows us significant flexibility to navigate volatility in commodity price environments • Development plans are ready to be executed when the economic environment justifies investment • Expand decommissioning activity utilizing $17 million in grants and $4 million in allocation eligibility within the Alberta Site Rehabilitation Program (ASRP) H1 2020 Results Guidance Results boe/d • Obsidian Energy exceeded all guidance targets in a Production 25,500 – 26,000 26,482 very challenging macro environment Capital MM $43 $41 • Production ahead due to strong Expenditures development program results MM Decommissioning $8 $8 • Capital expenditures lower due to effective execution $/boe Operating Costs $11.50 – 11.90 $10.32 • Operating costs and G&A lower due to cost cutting efforts and proactive decision making General & $/boe $1.65 – 1.85 $1.50 Administrative 4

Long-term Strategic Priorities Superior Shareholder Return Generate excess free cash flow while holding Drive per share growth via Create scale and decrease production flat with organic development and cost structure via Cardium growth optionality at debt pay down consolidation strategy increased commodity prices 5Long-term Strategic Priorities Superior Shareholder Return Generate excess free cash flow while holding Drive per share growth via Create scale and decrease production flat with organic development and cost structure via Cardium growth optionality at debt pay down consolidation strategy increased commodity prices 5

Creating The Cardium Champion st On September 21 2020 Obsidian Energy commenced a formal offer to purchase all of the issued and outstanding common shares of Bonterra Energy Corp. • Obsidian Energy has offered 2 Obsidian Energy shares for each Bonterra share Central Pembina • Creates the Cardium Champion with enhanced scale and capital markets relevance • Accretive across all equity metrics resulting in the potential for significant per share value appreciation East to the benefit of both Bonterra and Obsidian Pembina Energy shareholders West Pembina • Up to C$100 million expected in identified financial, operational and other synergies over the first three years resulting in significantly improved free cash flow • The re-introduction of a monthly dividend payment after an appropriate level of debt repayment East • Retain significant upside to higher commodity Crimson prices through continued participation with a 48% pro forma ownership in a stronger combined Crimson Lake company • An outcome far superior to what Bonterra can achieve on a stand-alone basis Obsidian Energy is the #1 Cardium Producer and the Logical Consolidator 6Creating The Cardium Champion st On September 21 2020 Obsidian Energy commenced a formal offer to purchase all of the issued and outstanding common shares of Bonterra Energy Corp. • Obsidian Energy has offered 2 Obsidian Energy shares for each Bonterra share Central Pembina • Creates the Cardium Champion with enhanced scale and capital markets relevance • Accretive across all equity metrics resulting in the potential for significant per share value appreciation East to the benefit of both Bonterra and Obsidian Pembina Energy shareholders West Pembina • Up to C$100 million expected in identified financial, operational and other synergies over the first three years resulting in significantly improved free cash flow • The re-introduction of a monthly dividend payment after an appropriate level of debt repayment East • Retain significant upside to higher commodity Crimson prices through continued participation with a 48% pro forma ownership in a stronger combined Crimson Lake company • An outcome far superior to what Bonterra can achieve on a stand-alone basis Obsidian Energy is the #1 Cardium Producer and the Logical Consolidator 6

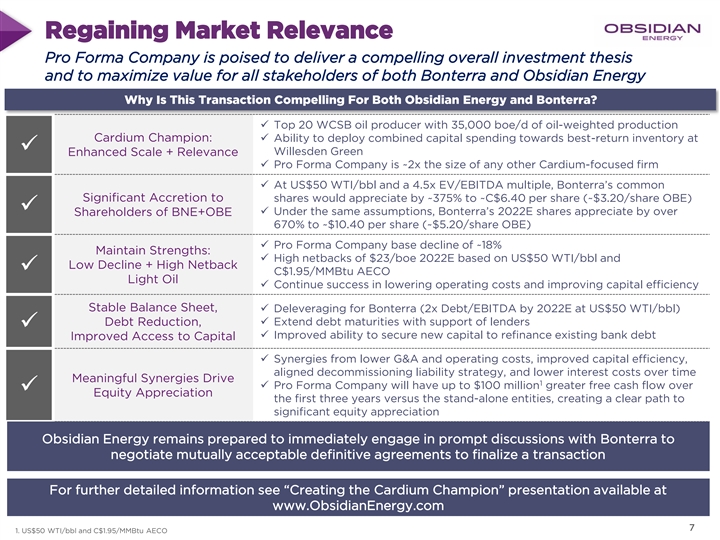

Regaining Market Relevance Pro Forma Company is poised to deliver a compelling overall investment thesis and to maximize value for all stakeholders of both Bonterra and Obsidian Energy Why Is This Transaction Compelling For Both Obsidian Energy and Bonterra? ✓ Top 20 WCSB oil producer with 35,000 boe/d of oil-weighted production Cardium Champion: ✓ Ability to deploy combined capital spending towards best-return inventory at ✓ Willesden Green Enhanced Scale + Relevance ✓ Pro Forma Company is ~2x the size of any other Cardium-focused firm ✓ At US$50 WTI/bbl and a 4.5x EV/EBITDA multiple, Bonterra’s common Significant Accretion to shares would appreciate by ~375% to ~C$6.40 per share (~$3.20/share OBE) ✓ ✓ Under the same assumptions, Bonterra’s 2022E shares appreciate by over Shareholders of BNE+OBE 670% to ~$10.40 per share (~$5.20/share OBE) ✓ Pro Forma Company base decline of ~18% Maintain Strengths: ✓ High netbacks of $23/boe 2022E based on US$50 WTI/bbl and Low Decline + High Netback ✓ C$1.95/MMBtu AECO Light Oil ✓ Continue success in lowering operating costs and improving capital efficiency Stable Balance Sheet, ✓ Deleveraging for Bonterra (2x Debt/EBITDA by 2022E at US$50 WTI/bbl) Debt Reduction,✓ Extend debt maturities with support of lenders ✓ ✓ Improved ability to secure new capital to refinance existing bank debt Improved Access to Capital ✓ Synergies from lower G&A and operating costs, improved capital efficiency, aligned decommissioning liability strategy, and lower interest costs over time Meaningful Synergies Drive 1 ✓ Pro Forma Company will have up to $100 million greater free cash flow over ✓ Equity Appreciation the first three years versus the stand-alone entities, creating a clear path to significant equity appreciation Obsidian Energy remains prepared to immediately engage in prompt discussions with Bonterra to negotiate mutually acceptable definitive agreements to finalize a transaction For further detailed information see “Creating the Cardium Champion” presentation available at www.ObsidianEnergy.com 7 7 1. US$50 WTI/bbl and C$1.95/MMBtu AECORegaining Market Relevance Pro Forma Company is poised to deliver a compelling overall investment thesis and to maximize value for all stakeholders of both Bonterra and Obsidian Energy Why Is This Transaction Compelling For Both Obsidian Energy and Bonterra? ✓ Top 20 WCSB oil producer with 35,000 boe/d of oil-weighted production Cardium Champion: ✓ Ability to deploy combined capital spending towards best-return inventory at ✓ Willesden Green Enhanced Scale + Relevance ✓ Pro Forma Company is ~2x the size of any other Cardium-focused firm ✓ At US$50 WTI/bbl and a 4.5x EV/EBITDA multiple, Bonterra’s common Significant Accretion to shares would appreciate by ~375% to ~C$6.40 per share (~$3.20/share OBE) ✓ ✓ Under the same assumptions, Bonterra’s 2022E shares appreciate by over Shareholders of BNE+OBE 670% to ~$10.40 per share (~$5.20/share OBE) ✓ Pro Forma Company base decline of ~18% Maintain Strengths: ✓ High netbacks of $23/boe 2022E based on US$50 WTI/bbl and Low Decline + High Netback ✓ C$1.95/MMBtu AECO Light Oil ✓ Continue success in lowering operating costs and improving capital efficiency Stable Balance Sheet, ✓ Deleveraging for Bonterra (2x Debt/EBITDA by 2022E at US$50 WTI/bbl) Debt Reduction,✓ Extend debt maturities with support of lenders ✓ ✓ Improved ability to secure new capital to refinance existing bank debt Improved Access to Capital ✓ Synergies from lower G&A and operating costs, improved capital efficiency, aligned decommissioning liability strategy, and lower interest costs over time Meaningful Synergies Drive 1 ✓ Pro Forma Company will have up to $100 million greater free cash flow over ✓ Equity Appreciation the first three years versus the stand-alone entities, creating a clear path to significant equity appreciation Obsidian Energy remains prepared to immediately engage in prompt discussions with Bonterra to negotiate mutually acceptable definitive agreements to finalize a transaction For further detailed information see “Creating the Cardium Champion” presentation available at www.ObsidianEnergy.com 7 7 1. US$50 WTI/bbl and C$1.95/MMBtu AECO

Corporate Cost Improvements Commentary Opex Operating Costs (Opex) • Total reduction in Opex/boe of 26% from 2017 to mid-point of 2020 Guidance ($11.30/boe) • Currently achieving better than 2020 Opex guidance despite lower production volumes • Increase in FY 2020 Opex/boe vs. H1 2020 driven by timing of key activities and return to production of profitable but higher cost of supply assets • Includes temporary field staff salary reductions which began in Q2 Further Opex Improvements G&A • Take advantage of Crimson Lake’s low operating costs with continued development focus • Continue to optimize and drive efficiencies across our entire Cardium footprint G&A • Total reduction in G&A/boe of 42% from 2017 to mid-point of 2020 Guidance • Currently surpassing 2020 G&A guidance despite lower production volumes • Includes temporary office staff salary reductions which began in Q2 8 See end notes for additional information Corporate Cost Improvements Commentary Opex Operating Costs (Opex) • Total reduction in Opex/boe of 26% from 2017 to mid-point of 2020 Guidance ($11.30/boe) • Currently achieving better than 2020 Opex guidance despite lower production volumes • Increase in FY 2020 Opex/boe vs. H1 2020 driven by timing of key activities and return to production of profitable but higher cost of supply assets • Includes temporary field staff salary reductions which began in Q2 Further Opex Improvements G&A • Take advantage of Crimson Lake’s low operating costs with continued development focus • Continue to optimize and drive efficiencies across our entire Cardium footprint G&A • Total reduction in G&A/boe of 42% from 2017 to mid-point of 2020 Guidance • Currently surpassing 2020 G&A guidance despite lower production volumes • Includes temporary office staff salary reductions which began in Q2 8 See end notes for additional information

Obsidian Energy Corporate Breakeven Historical and Projected Obsidian Breakeven WTI Select Intermediate and Junior Peer Breakeven WTI Unhedged Cash Flow (US$/bbl) 2021 Unhedged Cash Flow (US$/bbl) 2020 Breakeven Price ~$US39 WTI including $60 $60 Obsidian Hedge Positions $50 $50 $40 $40 $30 $30 $20 $20 $10 $10 $0 $0 2018 2019 OBE 2020 OBE 2021 Projected Projected Commentary • Our focus on improving the efficiency of the business is yielding material reductions in our WTI break-even assessment • Continued focus on cost optimization throughout the business (G&A/ Opex/ Capex) • Execution of our development and optimization programs yielding top tier results 9 See end notes for additional information Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 Peer 13 Peer 14 Peer 15 Peer 16 Peer 17 Peer 18 Peer 19Obsidian Energy Corporate Breakeven Historical and Projected Obsidian Breakeven WTI Select Intermediate and Junior Peer Breakeven WTI Unhedged Cash Flow (US$/bbl) 2021 Unhedged Cash Flow (US$/bbl) 2020 Breakeven Price ~$US39 WTI including $60 $60 Obsidian Hedge Positions $50 $50 $40 $40 $30 $30 $20 $20 $10 $10 $0 $0 2018 2019 OBE 2020 OBE 2021 Projected Projected Commentary • Our focus on improving the efficiency of the business is yielding material reductions in our WTI break-even assessment • Continued focus on cost optimization throughout the business (G&A/ Opex/ Capex) • Execution of our development and optimization programs yielding top tier results 9 See end notes for additional information Peer 1 Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 10 Peer 11 Peer 12 Peer 13 Peer 14 Peer 15 Peer 16 Peer 17 Peer 18 Peer 19

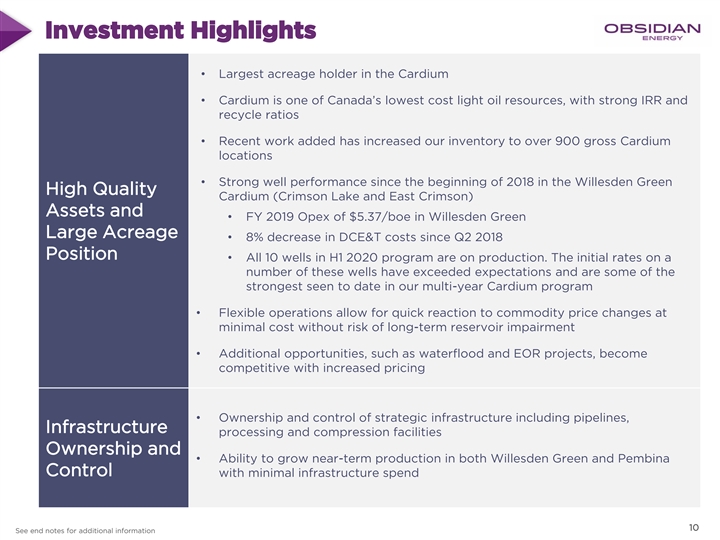

Investment Highlights • Largest acreage holder in the Cardium • Cardium is one of Canada’s lowest cost light oil resources, with strong IRR and recycle ratios • Recent work added has increased our inventory to over 900 gross Cardium locations • Strong well performance since the beginning of 2018 in the Willesden Green High Quality Cardium (Crimson Lake and East Crimson) Assets and • FY 2019 Opex of $5.37/boe in Willesden Green Large Acreage • 8% decrease in DCE&T costs since Q2 2018 Position • All 10 wells in H1 2020 program are on production. The initial rates on a number of these wells have exceeded expectations and are some of the strongest seen to date in our multi-year Cardium program • Flexible operations allow for quick reaction to commodity price changes at minimal cost without risk of long-term reservoir impairment • Additional opportunities, such as waterflood and EOR projects, become competitive with increased pricing • Ownership and control of strategic infrastructure including pipelines, Infrastructure processing and compression facilities Ownership and • Ability to grow near-term production in both Willesden Green and Pembina Control with minimal infrastructure spend 10 See end notes for additional information Investment Highlights • Largest acreage holder in the Cardium • Cardium is one of Canada’s lowest cost light oil resources, with strong IRR and recycle ratios • Recent work added has increased our inventory to over 900 gross Cardium locations • Strong well performance since the beginning of 2018 in the Willesden Green High Quality Cardium (Crimson Lake and East Crimson) Assets and • FY 2019 Opex of $5.37/boe in Willesden Green Large Acreage • 8% decrease in DCE&T costs since Q2 2018 Position • All 10 wells in H1 2020 program are on production. The initial rates on a number of these wells have exceeded expectations and are some of the strongest seen to date in our multi-year Cardium program • Flexible operations allow for quick reaction to commodity price changes at minimal cost without risk of long-term reservoir impairment • Additional opportunities, such as waterflood and EOR projects, become competitive with increased pricing • Ownership and control of strategic infrastructure including pipelines, Infrastructure processing and compression facilities Ownership and • Ability to grow near-term production in both Willesden Green and Pembina Control with minimal infrastructure spend 10 See end notes for additional information

Cardium Development Program Focused on Delivering Strong Capital Returns Willesden Green • Drilling prioritized to target highest return opportunities Focused • Light oil rich wells ranked by IRR, payout, and recycle ratios Strong Economics • Program is license ready and scalable with an inventory of drill ready Flexible locations to add significant program optionality • Additional capital can be allocated to highly efficient, liquids weighted Optimization optimization projects yielding rapid project returns • Well spacing and frac designed for cost efficiency and Well Design tailored to our target reservoirs • Minimal infrastructure spend required Infrastructure • Drill order optimized to manage infrastructure capacity 11Cardium Development Program Focused on Delivering Strong Capital Returns Willesden Green • Drilling prioritized to target highest return opportunities Focused • Light oil rich wells ranked by IRR, payout, and recycle ratios Strong Economics • Program is license ready and scalable with an inventory of drill ready Flexible locations to add significant program optionality • Additional capital can be allocated to highly efficient, liquids weighted Optimization optimization projects yielding rapid project returns • Well spacing and frac designed for cost efficiency and Well Design tailored to our target reservoirs • Minimal infrastructure spend required Infrastructure • Drill order optimized to manage infrastructure capacity 11

Execute Operationally H1 2020 Development Program Crimson Lake Commentary • Early deliverability results from the first half program to 3 kms INDEX MAP R8W5 date have been above our type curve 2 miles 12-26 Pad: 3 Wells (avg/well) IP10: 1,215 boe/d (82% oil) • Pad 12-26 on-stream delivering IP30: 1075 boe/d (74% oil) IP60: 832 boe/d (66% oil) • IP10: 1,215 boe/d (82% light oil) IP90: 684 boe/d (63% oil) • IP30: 1,075 boe/d (74% light oil) H1 2020 Development • IP60 832 boe/d (66% light oil) Program directly • IP90: 684 boe/d (63% light oil) are our strongest offsetting successful 2018-2019 programs oil-equivalent rates in our primary Cardium program T43 • Five of Obsidian Energy’s ten wells drilled in 2020 were among the top performing wells in the Cardium (June 03-29 Pad: 1 Well (avg/well) 01-27 Pad: 2 Wells (avg/well) IP10: 587 boe/d (95% oil) 2020) IP10:1,222 boe/d (82% oil) IP30: 443 boe/d (93% oil) IP30: 999 boe/d (71% oil) IP60: 397 boe/d (90% oil) IP60: 734 boe/d (66% oil) IP90: 340 boe/d (88% oil) IP90: 619 boe/d (64% oil) June 2020 Top Cardium Wells On Stream Latest Month Volume # of Company Well Name Field Date Oil/C5 bbls Gas mmcf Days Whitecap Rsrcs Inc. WHITECAP HZ WAPITI 15-7- 67- 8 WAPITI 10-Mar-20 15,728 23 30 03-06 Pad: 2 Wells (avg/well) IP10: 493 boe/d (97% oil) Obsidian Enrg Ltd. OBE HZ 102 WILLGR 15-16- 43- 8 WILLESDEN GR 4-Feb-20 14,179 58 29 IP30: 527 boe/d (89% oil) Obsidian Enrg Ltd. OBE HZ 102 WILLGR 5-15- 43- 8 WILLESDEN GR 1-Feb-20 12,809 48 30 IP60: 451 boe/d (84% oil) Orlen Upstream Cda Ltd OUC HZ FERRIER 14-23- 39- 9 FERRIER 4-Mar-20 10,554 63 30 IP90: 399 boe/d (81% oil) NAL Rsrcs Ltd NAL HZ LOCHEND 2-16- 26- 3 LOCHEND 24-Sep-19 7,650 21 30 Ridgeback Rs cs Inc RIDGEBACK ET AL HZ LOCHEND 4-23- LOCHEND 14-Jan-20 7,447 7 30 Orlen Upstream Cda Ltd OUC 102 HZ LOCHEND 1- 11-26- LOCHEND 27-Dec-19 7,442 35 30 14-17 Pad: 2 Wells (avg/well) IP10: 204 boe/d (96% oil) Obsidian Enrg Ltd OBE WILLGR 2- 30- 42-7 WILLESDEN GR 1-Mar-20 7,417 17 30 IP30: 215 boe/d (93% oil) Obsidian Enrg Ltd OBE HZ 102 WILLGR 14-28-43- 8 WILLESDEN GR 1-Feb-20 7,336 35 30 IP60: 219 boe/d (90% oil) Obsidian Enrg Ltd OBE 100 HZ WILLGR 4-30-42-7 WILLESDEN GR 14-Mar-20 7,210 8 30 IP90: 203 boe/d (89% oil) Petrus Rsrcs Corp PETRUS 102 HZ FERRIER 4-16-38-8 FERRIER 12-Mar-20 6,616 25 30 OBE H1 2020 program Whitecap Rsrcs Inc WHITECAP HZ WAPITI 12-30-67-8 WAPITI 11-Mar-20 6,601 4 30 OBE 2018-2019 well NAL Rsrcs Ltd NAL HZ LOCHEND 1-16-26-3 LOCHEND 24-Sep-19 6,530 13 30 Peer well Ridgeback Rsrcs Inc RIDGEBACK HZ 102 BRAZR 15-33-48- PEMBINA 14-Mar-20 6,002 8 29 Unit land OBE Cardium WI land Whitecap Rsrcs Inc WHITECAP 102 HZ WAPITI 13-30-67-8 WAPITI 12-Mar-20 5,980 5 30 Source: GeoLOGIC Systems Ltd., Google, and Raymond James Ltd. 12 See end notes for additional information Execute Operationally H1 2020 Development Program Crimson Lake Commentary • Early deliverability results from the first half program to 3 kms INDEX MAP R8W5 date have been above our type curve 2 miles 12-26 Pad: 3 Wells (avg/well) IP10: 1,215 boe/d (82% oil) • Pad 12-26 on-stream delivering IP30: 1075 boe/d (74% oil) IP60: 832 boe/d (66% oil) • IP10: 1,215 boe/d (82% light oil) IP90: 684 boe/d (63% oil) • IP30: 1,075 boe/d (74% light oil) H1 2020 Development • IP60 832 boe/d (66% light oil) Program directly • IP90: 684 boe/d (63% light oil) are our strongest offsetting successful 2018-2019 programs oil-equivalent rates in our primary Cardium program T43 • Five of Obsidian Energy’s ten wells drilled in 2020 were among the top performing wells in the Cardium (June 03-29 Pad: 1 Well (avg/well) 01-27 Pad: 2 Wells (avg/well) IP10: 587 boe/d (95% oil) 2020) IP10:1,222 boe/d (82% oil) IP30: 443 boe/d (93% oil) IP30: 999 boe/d (71% oil) IP60: 397 boe/d (90% oil) IP60: 734 boe/d (66% oil) IP90: 340 boe/d (88% oil) IP90: 619 boe/d (64% oil) June 2020 Top Cardium Wells On Stream Latest Month Volume # of Company Well Name Field Date Oil/C5 bbls Gas mmcf Days Whitecap Rsrcs Inc. WHITECAP HZ WAPITI 15-7- 67- 8 WAPITI 10-Mar-20 15,728 23 30 03-06 Pad: 2 Wells (avg/well) IP10: 493 boe/d (97% oil) Obsidian Enrg Ltd. OBE HZ 102 WILLGR 15-16- 43- 8 WILLESDEN GR 4-Feb-20 14,179 58 29 IP30: 527 boe/d (89% oil) Obsidian Enrg Ltd. OBE HZ 102 WILLGR 5-15- 43- 8 WILLESDEN GR 1-Feb-20 12,809 48 30 IP60: 451 boe/d (84% oil) Orlen Upstream Cda Ltd OUC HZ FERRIER 14-23- 39- 9 FERRIER 4-Mar-20 10,554 63 30 IP90: 399 boe/d (81% oil) NAL Rsrcs Ltd NAL HZ LOCHEND 2-16- 26- 3 LOCHEND 24-Sep-19 7,650 21 30 Ridgeback Rs cs Inc RIDGEBACK ET AL HZ LOCHEND 4-23- LOCHEND 14-Jan-20 7,447 7 30 Orlen Upstream Cda Ltd OUC 102 HZ LOCHEND 1- 11-26- LOCHEND 27-Dec-19 7,442 35 30 14-17 Pad: 2 Wells (avg/well) IP10: 204 boe/d (96% oil) Obsidian Enrg Ltd OBE WILLGR 2- 30- 42-7 WILLESDEN GR 1-Mar-20 7,417 17 30 IP30: 215 boe/d (93% oil) Obsidian Enrg Ltd OBE HZ 102 WILLGR 14-28-43- 8 WILLESDEN GR 1-Feb-20 7,336 35 30 IP60: 219 boe/d (90% oil) Obsidian Enrg Ltd OBE 100 HZ WILLGR 4-30-42-7 WILLESDEN GR 14-Mar-20 7,210 8 30 IP90: 203 boe/d (89% oil) Petrus Rsrcs Corp PETRUS 102 HZ FERRIER 4-16-38-8 FERRIER 12-Mar-20 6,616 25 30 OBE H1 2020 program Whitecap Rsrcs Inc WHITECAP HZ WAPITI 12-30-67-8 WAPITI 11-Mar-20 6,601 4 30 OBE 2018-2019 well NAL Rsrcs Ltd NAL HZ LOCHEND 1-16-26-3 LOCHEND 24-Sep-19 6,530 13 30 Peer well Ridgeback Rsrcs Inc RIDGEBACK HZ 102 BRAZR 15-33-48- PEMBINA 14-Mar-20 6,002 8 29 Unit land OBE Cardium WI land Whitecap Rsrcs Inc WHITECAP 102 HZ WAPITI 13-30-67-8 WAPITI 12-Mar-20 5,980 5 30 Source: GeoLOGIC Systems Ltd., Google, and Raymond James Ltd. 12 See end notes for additional information

Cardium Growth & Operational Improvements Commentary Total Cardium Production • Our 2017-2020 drilling programs in Crimson Lake 25,000 have delivered robust production growth with high- Netbacks and low operating costs 20,000 34% • Cardium 35% 37% 15,000 • 25% Liquids Growth since 2017 36% 10% 10% • 22% Total Production growth since 2017 11% 11% 10,000 • Willesden Green 56% 55% • 119% Liquids growth since 2017 5,000 52% 54% • 93% Total Production growth since 2017 0 • 49% Opex/boe improvement since 2017 FY 2017 FY 2018 FY 2019 H1 2020 Oil (bbl/d) NGL (bbl/d) Gas (boe/d) Willesden Green Production Willesden Green Production & Operating Costs 14,000 12,000 38% 10,000 39% 8,000 10% 46% 11% 6,000 45% 13% 4,000 13% 52% 50% 2,000 41% 42% 0 FY 2017 FY 2018 FY 2019 H1 2020 Oil (bbl/d) NGL (bbl/d) Gas (boe/d) 13 See end notes for additional information Average Daily Production (boe/d) Average Daily Production (boe/d)Cardium Growth & Operational Improvements Commentary Total Cardium Production • Our 2017-2020 drilling programs in Crimson Lake 25,000 have delivered robust production growth with high- Netbacks and low operating costs 20,000 34% • Cardium 35% 37% 15,000 • 25% Liquids Growth since 2017 36% 10% 10% • 22% Total Production growth since 2017 11% 11% 10,000 • Willesden Green 56% 55% • 119% Liquids growth since 2017 5,000 52% 54% • 93% Total Production growth since 2017 0 • 49% Opex/boe improvement since 2017 FY 2017 FY 2018 FY 2019 H1 2020 Oil (bbl/d) NGL (bbl/d) Gas (boe/d) Willesden Green Production Willesden Green Production & Operating Costs 14,000 12,000 38% 10,000 39% 8,000 10% 46% 11% 6,000 45% 13% 4,000 13% 52% 50% 2,000 41% 42% 0 FY 2017 FY 2018 FY 2019 H1 2020 Oil (bbl/d) NGL (bbl/d) Gas (boe/d) 13 See end notes for additional information Average Daily Production (boe/d) Average Daily Production (boe/d)

Optimization Finding low cost, high value opportunities in our base Total Optimization Program Production Commentary Optimization at Obsidian 1,800 2019 Annual Average • Multi-year inventory of targeted, low 787 boe/d (71% Oil) 1,600 cost projects to increase base production, improve injection, reduce 1,400 OPEX, maximize reserves recovery 2020 Optimization 1,200 764 boe/d (79% Oil) 1,000 • Maintains very low decline rates and 800 adds to recognized PDP reserves 600 2019 Summary 400 • $8.4MM Capital spend across 200 200 projects - Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec • 12 Month Capital Efficiency 2020 2019 <$8,000/boe with high oil weighting (>70%) Pembina Optimization Program Production 12,000 • PDP additions of 1.1 mmboe 10,000 2020 Summary 8,000 • Q1 spend of $5 MM focused on wellbore stimulations, reactivations, 6,000 and recompletions Shut-in of uneconomic Resumption of 4,000 production and optimization spending deferred maintenance • $3.1 MM planned in H2 2020 2,000 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug 2019 2020 14 boe/d boe/dOptimization Finding low cost, high value opportunities in our base Total Optimization Program Production Commentary Optimization at Obsidian 1,800 2019 Annual Average • Multi-year inventory of targeted, low 787 boe/d (71% Oil) 1,600 cost projects to increase base production, improve injection, reduce 1,400 OPEX, maximize reserves recovery 2020 Optimization 1,200 764 boe/d (79% Oil) 1,000 • Maintains very low decline rates and 800 adds to recognized PDP reserves 600 2019 Summary 400 • $8.4MM Capital spend across 200 200 projects - Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec • 12 Month Capital Efficiency 2020 2019 <$8,000/boe with high oil weighting (>70%) Pembina Optimization Program Production 12,000 • PDP additions of 1.1 mmboe 10,000 2020 Summary 8,000 • Q1 spend of $5 MM focused on wellbore stimulations, reactivations, 6,000 and recompletions Shut-in of uneconomic Resumption of 4,000 production and optimization spending deferred maintenance • $3.1 MM planned in H2 2020 2,000 0 Jan Feb Mar Apr May Jun Jul Aug Sep Oct Nov Dec Jan Feb Mar Apr May Jun Jul Aug 2019 2020 14 boe/d boe/d

Willesden Green Cost Reduction Trajectory Drill, Complete, Equip & Tie-In Costs – (DCET) Commentary Construction Drill cost increase driven by optimization of well design • Utilization and expansion of existing pads leading to increased well lengths $3,700 to reduce construction and infrastructure costs • Construction timing optimization to -$235 -$59 $3,612 reduce weather related impact and $3,600 +$70 equipment mobilization costs Drilling • Monobore where reservoir pressure $3,500 permits • Single bit runs over extended reach HZ wells -$61 • Multi-well pads and geographically $3,400 focused programs mitigate rig move costs • Wells have increased in length by an $3,327 average of 5% to optimize project returns 8% improvement in drilling $3,300 costs since Q2 2018 Completions • Frac optimization and nitrogen reduction • Elimination of c-rings to reduce $3,200 water costs • Utilizing industry proven Coil-Shift Frac technology • Lateral placement targeted to improve $3,100 drilling and completion efficiency Site Facilities • Leverage existing infrastructure and $3,000 inventory H2 2018 Construction Drill Completion Tie-In 2020 H1 • Develop within current infrastructure capacity 15 See end notes for additional information DCET ($M)Willesden Green Cost Reduction Trajectory Drill, Complete, Equip & Tie-In Costs – (DCET) Commentary Construction Drill cost increase driven by optimization of well design • Utilization and expansion of existing pads leading to increased well lengths $3,700 to reduce construction and infrastructure costs • Construction timing optimization to -$235 -$59 $3,612 reduce weather related impact and $3,600 +$70 equipment mobilization costs Drilling • Monobore where reservoir pressure $3,500 permits • Single bit runs over extended reach HZ wells -$61 • Multi-well pads and geographically $3,400 focused programs mitigate rig move costs • Wells have increased in length by an $3,327 average of 5% to optimize project returns 8% improvement in drilling $3,300 costs since Q2 2018 Completions • Frac optimization and nitrogen reduction • Elimination of c-rings to reduce $3,200 water costs • Utilizing industry proven Coil-Shift Frac technology • Lateral placement targeted to improve $3,100 drilling and completion efficiency Site Facilities • Leverage existing infrastructure and $3,000 inventory H2 2018 Construction Drill Completion Tie-In 2020 H1 • Develop within current infrastructure capacity 15 See end notes for additional information DCET ($M)

Cardium Play Fairways A Large High-Graded Inventory West Pembina Central Pembina R10W5 INDEX MAP 132 680 Type Curve Locations Type Curve Locations • Well established • Individual fairways and productive trend unit boundaries in significantly de-risked by historically pressure West major Cardium players supported properties Pembina • Underdeveloped acreage • Ability to waterflood for • Easy access to existing minimal capital through Central OBE facilities and direct existing infrastructure Pembina access to regional • Recent technical work has transportation added ~500 identified inventory locations Crimson Lake East Crimson T45 36 71 Type Curve Locations Type Curve Locations 15 kms 10 miles East • Banked oil from historical • Continued eastward Crimson pressure maintenance extension of Crimson Lake Crimson • Top quality reservoir development program Lake previously • De-risked by new underdeveloped by competitor drilling in OBE Cardium WI land vertical drilling 2018/2019 Peer lands • Recent top quartile results • Existing flexible • Existing flexible infrastructure infrastructure 900+ total identified inventory 135 YE 2019 Net Booked Cardium Locations 16 See end notes for additional information Cardium Play Fairways A Large High-Graded Inventory West Pembina Central Pembina R10W5 INDEX MAP 132 680 Type Curve Locations Type Curve Locations • Well established • Individual fairways and productive trend unit boundaries in significantly de-risked by historically pressure West major Cardium players supported properties Pembina • Underdeveloped acreage • Ability to waterflood for • Easy access to existing minimal capital through Central OBE facilities and direct existing infrastructure Pembina access to regional • Recent technical work has transportation added ~500 identified inventory locations Crimson Lake East Crimson T45 36 71 Type Curve Locations Type Curve Locations 15 kms 10 miles East • Banked oil from historical • Continued eastward Crimson pressure maintenance extension of Crimson Lake Crimson • Top quality reservoir development program Lake previously • De-risked by new underdeveloped by competitor drilling in OBE Cardium WI land vertical drilling 2018/2019 Peer lands • Recent top quartile results • Existing flexible • Existing flexible infrastructure infrastructure 900+ total identified inventory 135 YE 2019 Net Booked Cardium Locations 16 See end notes for additional information

Crimson Lake – Near Term Focus Summary Economics • Q2 2020 average production of 10,134 boe/d DCET Capex($MM) $3.2 • Obsidian Energy cornerstone for revitalized primary EUR (Mboe) 229 development on our Cardium acreage Oil IP365 (bbl/d) 157 • Banked oil from historical pressure maintenance in WGCU#9 Total IP365 (boe/d) 235 • Top quality reservoir previously undeveloped due to NPV BTAX 10% ($MM) $2.7 topographic and infrastructure challenges for vertical drilling IRR (%) 118% • Existing flexible infrastructure at the Crimson 13-27 Payout (years) 1.0 facility with optionality to East Crimson Technical F&D ($/boe) $14.00 R7W5 OBE H1 2020 program OBE 2018-2019 well 12 Month Efficiency ($/boed) $13,700 Peer well Inventory Unit land Breakeven (IRR 10%) WTI ($US/bbl) $26.29 OBE Cardium WI land OBE East Crimson land Type Curve – Crimson Lake 500 160 450 T43 140 400 120 350 100 300 250 80 Crimson Lake - Daily Production 200 60 WGCU#9 Crimson Lake - Cumulative Production 5 kms 150 3 miles 40 100 20 50 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 17 See end notes for additional information Average Daily Production (boe/d) Cumulative Production (mboe)Crimson Lake – Near Term Focus Summary Economics • Q2 2020 average production of 10,134 boe/d DCET Capex($MM) $3.2 • Obsidian Energy cornerstone for revitalized primary EUR (Mboe) 229 development on our Cardium acreage Oil IP365 (bbl/d) 157 • Banked oil from historical pressure maintenance in WGCU#9 Total IP365 (boe/d) 235 • Top quality reservoir previously undeveloped due to NPV BTAX 10% ($MM) $2.7 topographic and infrastructure challenges for vertical drilling IRR (%) 118% • Existing flexible infrastructure at the Crimson 13-27 Payout (years) 1.0 facility with optionality to East Crimson Technical F&D ($/boe) $14.00 R7W5 OBE H1 2020 program OBE 2018-2019 well 12 Month Efficiency ($/boed) $13,700 Peer well Inventory Unit land Breakeven (IRR 10%) WTI ($US/bbl) $26.29 OBE Cardium WI land OBE East Crimson land Type Curve – Crimson Lake 500 160 450 T43 140 400 120 350 100 300 250 80 Crimson Lake - Daily Production 200 60 WGCU#9 Crimson Lake - Cumulative Production 5 kms 150 3 miles 40 100 20 50 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 17 See end notes for additional information Average Daily Production (boe/d) Cumulative Production (mboe)

East Crimson – Mid Term Focus Summary Economics • Q2 2020 average production of 3,609 boe/d DCET Capex ($MM) $2.9 • Continued Eastward extension of the successful EUR (Mboe) 203 Crimson Lake development program Oil IP365 (bbl/d) 136 • Area has been de-risked by recent peer drilling results supporting the revitalized development Total IP365 (boe/d) 194 • Shared and scalable infrastructure with the Crimson NPV BTAX 10% ($MM) $2.1 Lake program IRR (%) 90% • Combination of pressure supported edge drilling and underdeveloped unit fairways Payout (years) 1.2 Technical F&D ($/boe) $14.00 R7W5 OBE H1 2020 program 12 Month Efficiency ($/boed) $14,700 OBE 2018-2019 well Peer well Inventory Breakeven (IRR 10%) WTI ($US/bbl) $30.83 Unit land OBE Cardium WI land OBE Crimson land Type Curve – East Crimson 400 140 350 120 T43 300 100 WGCU#1 250 80 WGCU#2 200 East Crimson - Daily Production 60 150 East Crimson - Cumulative Production 5 kms WGCU#6 40 100 3 miles 20 50 WGCU#3 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 18 See end notes for additional information Average Daily Production (boe/d) Cumulative Production (mboe)East Crimson – Mid Term Focus Summary Economics • Q2 2020 average production of 3,609 boe/d DCET Capex ($MM) $2.9 • Continued Eastward extension of the successful EUR (Mboe) 203 Crimson Lake development program Oil IP365 (bbl/d) 136 • Area has been de-risked by recent peer drilling results supporting the revitalized development Total IP365 (boe/d) 194 • Shared and scalable infrastructure with the Crimson NPV BTAX 10% ($MM) $2.1 Lake program IRR (%) 90% • Combination of pressure supported edge drilling and underdeveloped unit fairways Payout (years) 1.2 Technical F&D ($/boe) $14.00 R7W5 OBE H1 2020 program 12 Month Efficiency ($/boed) $14,700 OBE 2018-2019 well Peer well Inventory Breakeven (IRR 10%) WTI ($US/bbl) $30.83 Unit land OBE Cardium WI land OBE Crimson land Type Curve – East Crimson 400 140 350 120 T43 300 100 WGCU#1 250 80 WGCU#2 200 East Crimson - Daily Production 60 150 East Crimson - Cumulative Production 5 kms WGCU#6 40 100 3 miles 20 50 WGCU#3 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 18 See end notes for additional information Average Daily Production (boe/d) Cumulative Production (mboe)

West Pembina – Mid Term Focus Summary Economics • Q2 2020 average production of 4,290 boe/d DCET Capex ($MM) $3.0 • Proven oil rich Cardium trend with undeveloped EUR (Mboe) 196 primary development acreage Oil IP365 (bbl/d) 148 • Significant offsetting production from established Total IP365 (boe/d) 163 Cardium players throughout the West side of Pembina • Underdeveloped core acreage NPV BTAX 10% ($MM) $2.1 • Existing flexible infrastructure with significant available IRR (%) 57% capacity in multiple facilities Payout (years) 1.5 • Additional uncaptured inventory in non-operated lands Technical F&D ($/boe) $15.25 R10W5 Inventory 12 Month Efficiency ($/boed) $18,500 Unit land OBE Cardium WI land OBE Pembina land Breakeven (IRR 10%) WTI ($US/bbl) $28.57 Type Curve – West Pembina 300 120 250 100 T48 200 80 150 60 West Pembina-Daily Production West Pembina Cumulative Production 100 40 50 20 5 kms 0 0 3 miles 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 19 See end notes for additional information Average Daily Production (boe/d) Cumulative Prod (mboe)West Pembina – Mid Term Focus Summary Economics • Q2 2020 average production of 4,290 boe/d DCET Capex ($MM) $3.0 • Proven oil rich Cardium trend with undeveloped EUR (Mboe) 196 primary development acreage Oil IP365 (bbl/d) 148 • Significant offsetting production from established Total IP365 (boe/d) 163 Cardium players throughout the West side of Pembina • Underdeveloped core acreage NPV BTAX 10% ($MM) $2.1 • Existing flexible infrastructure with significant available IRR (%) 57% capacity in multiple facilities Payout (years) 1.5 • Additional uncaptured inventory in non-operated lands Technical F&D ($/boe) $15.25 R10W5 Inventory 12 Month Efficiency ($/boed) $18,500 Unit land OBE Cardium WI land OBE Pembina land Breakeven (IRR 10%) WTI ($US/bbl) $28.57 Type Curve – West Pembina 300 120 250 100 T48 200 80 150 60 West Pembina-Daily Production West Pembina Cumulative Production 100 40 50 20 5 kms 0 0 3 miles 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 19 See end notes for additional information Average Daily Production (boe/d) Cumulative Prod (mboe)

Central Pembina – Long Term Focus Summary Economics • Q2 2020 average production of 4,679 boe/d DCET Capex ($MM) $2.3 • The epicenter of low decline and pressure maintained EUR (Mboe) 184 development Oil IP365 (bbl/d) 101 • Recent technical work led to over 500 additional identified locations in Central Pembina, using Total IP365 (boe/d) 120 techniques consistent with peer modeling NPV BTAX 10% ($MM) $1.7 • Ability to de-risk through geological and reservoir IRR (%) 59% modelling • Proven and booked waterflood response as the Payout (years) 1.6 foundation for growth – Strong F&D Technical F&D ($/boe) $12.25 • Ability to grow waterflood scale through existing wells and infrastructure for minimal capital cost allows for 12 Month Efficiency ($/boed) $18,900 corporate decline maintenance Inventory Breakeven (IRR 10%) WTI ($US/bbl) $27.69 Unit land OBE Cardium WI land OBE Pembina land Type Curve – Central Pembina 200 100 180 90 160 80 140 70 10 kms 120 60 5 miles Pembina-Daily Production 100 50 80 Pembina Cumulative Production 40 60 30 40 20 20 10 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 20 See end notes for additional information Average Daily Production (boe/d) Cumulative Prod (mboe)Central Pembina – Long Term Focus Summary Economics • Q2 2020 average production of 4,679 boe/d DCET Capex ($MM) $2.3 • The epicenter of low decline and pressure maintained EUR (Mboe) 184 development Oil IP365 (bbl/d) 101 • Recent technical work led to over 500 additional identified locations in Central Pembina, using Total IP365 (boe/d) 120 techniques consistent with peer modeling NPV BTAX 10% ($MM) $1.7 • Ability to de-risk through geological and reservoir IRR (%) 59% modelling • Proven and booked waterflood response as the Payout (years) 1.6 foundation for growth – Strong F&D Technical F&D ($/boe) $12.25 • Ability to grow waterflood scale through existing wells and infrastructure for minimal capital cost allows for 12 Month Efficiency ($/boed) $18,900 corporate decline maintenance Inventory Breakeven (IRR 10%) WTI ($US/bbl) $27.69 Unit land OBE Cardium WI land OBE Pembina land Type Curve – Central Pembina 200 100 180 90 160 80 140 70 10 kms 120 60 5 miles Pembina-Daily Production 100 50 80 Pembina Cumulative Production 40 60 30 40 20 20 10 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 20 See end notes for additional information Average Daily Production (boe/d) Cumulative Prod (mboe)

AB Viking – Mid Term Focus Summary Economics • Q2 2020 average production of 880 boe/d DCET Capex($MM) $1.2 • Sweet, light oil development play with significant EUR (Mboe) 74 drilling inventory, including both low risk infill and step- out development Oil IP365 (bbl/d) 57 • Low DCET well costs, combined with owned and Total IP365 (boe/d) 96 controlled infrastructure and direct market access yields superior netbacks NPV BTAX 10% ($MM) $0.6 • Shallow, low geological risk resource play IRR (%) 47% • Asset is proximal to multiple, successful offset Payout (years) 1.7 producers Technical F&D ($/boe) $16.25 OBE Inventory 12 Month Efficiency ($/boed) $12,600 Viking Producer OBE Viking WI Land Industry Land Breakeven (IRR 10%) WTI ($US/bbl) $29.04 Type Curve – AB Viking 200 60 180 50 160 140 40 120 AB Viking-Daily Production 100 30 80 AB Viking-Cumulative Production 20 60 5 kms 40 10 20 3 miles 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 21 See end notes for additional information Average Daily Production (boe/d) Cumulative Prod (mboe)AB Viking – Mid Term Focus Summary Economics • Q2 2020 average production of 880 boe/d DCET Capex($MM) $1.2 • Sweet, light oil development play with significant EUR (Mboe) 74 drilling inventory, including both low risk infill and step- out development Oil IP365 (bbl/d) 57 • Low DCET well costs, combined with owned and Total IP365 (boe/d) 96 controlled infrastructure and direct market access yields superior netbacks NPV BTAX 10% ($MM) $0.6 • Shallow, low geological risk resource play IRR (%) 47% • Asset is proximal to multiple, successful offset Payout (years) 1.7 producers Technical F&D ($/boe) $16.25 OBE Inventory 12 Month Efficiency ($/boed) $12,600 Viking Producer OBE Viking WI Land Industry Land Breakeven (IRR 10%) WTI ($US/bbl) $29.04 Type Curve – AB Viking 200 60 180 50 160 140 40 120 AB Viking-Daily Production 100 30 80 AB Viking-Cumulative Production 20 60 5 kms 40 10 20 3 miles 0 0 0 12 24 36 Months *Economics Flat Pricing Assumptions: WTI USD$50.00, Ed Par Diff USD$6.00, AECO CAD$2.25, FX CAD/USD $1.36 21 See end notes for additional information Average Daily Production (boe/d) Cumulative Prod (mboe)

Peace River Oil Partnership (PROP) Summary PROP • Q2 2020 average production of 2,132 boe/d, with an R25 R20 R15W5 average of 1,701 boe/d shut-in during quarter in T90 response to low commodity prices • 85% of previously shut-in production has been returned to production as of July 1, 2020 • Large contiguous heavy oil resource developed with cold-flow, multi-leg horizontal wells • Reliable and steady base production with Nampa multiple sales points to allow for pricing optimization T85 • Emerging Clearwater formation oil play and Cadotte EOR potential provides additional upside Historical Production (boe/d) 6,000 Seal Harmon Valley Shut-in of temporarily South uneconomic production – 85% of shut-in volumes returned to production July 1 T80 4,000 2,000 T75 OBE land 0 22 See end notes for additional information Average Daily Production (boe/d) Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20Peace River Oil Partnership (PROP) Summary PROP • Q2 2020 average production of 2,132 boe/d, with an R25 R20 R15W5 average of 1,701 boe/d shut-in during quarter in T90 response to low commodity prices • 85% of previously shut-in production has been returned to production as of July 1, 2020 • Large contiguous heavy oil resource developed with cold-flow, multi-leg horizontal wells • Reliable and steady base production with Nampa multiple sales points to allow for pricing optimization T85 • Emerging Clearwater formation oil play and Cadotte EOR potential provides additional upside Historical Production (boe/d) 6,000 Seal Harmon Valley Shut-in of temporarily South uneconomic production – 85% of shut-in volumes returned to production July 1 T80 4,000 2,000 T75 OBE land 0 22 See end notes for additional information Average Daily Production (boe/d) Jan-18 Feb-18 Mar-18 Apr-18 May-18 Jun-18 Jul-18 Aug-18 Sep-18 Oct-18 Nov-18 Dec-18 Jan-19 Feb-19 Mar-19 Apr-19 May-19 Jun-19 Jul-19 Aug-19 Sep-19 Oct-19 Nov-19 Dec-19 Jan-20 Feb-20 Mar-20 Apr-20 May-20 Jun-20

Reducing Decommissioning Liability Commentary Demonstrated Reduction in Well Abandonment Costs Compelling Decommissioning Liability reductions Wainwright 2019 Cardium 2019 12 Wells 115 Wells • Multi-year trend of decommissioning liability reduction 50% Decrease in $5.0 $0.8 Q2 2020: $604MM undiscounted 35% Per-Well Decrease Abandonment • Active participant in AER’s Area-Base Closure (ABC) Costs Below D11 $4.0 $0.6 Near-term spending minimized $3.0 • 2020 ABC spend requirements suspended; YTD 2020 spend fully creditable to 2021 requirements $0.4 $2.0 Government support & engagement $0.2 • Obsidian sites awarded $17MM million in grants and $1.0 additional $4MM allocation eligibility to date on our 3,492 applications within the ASRP $0.0 $0.0 D11 XI Actuals D11 XI Actuals • Actively engaged with EPAC and the AER to improve closure programs and regulations Historical Reductions in Abandonment Costs – Obsidian Energy Undiscounted & Uninflated Targeted, Efficient spending Decommissioning Liability • Focus on inactive Legacy assets to eliminate fixed OPEX from non-productive assets at costs well below D11 estimates • Shallow decline, long life, high netback, oil-weighted Pembina assets extend ARO requirements 76% decrease in Obsidian Energy ARO liability since 2015 over a long time period, stretching well into the future • Many wells in the Cardium can be reactivated, recompleted, or repurposed for use in reservoir monitoring See end notes for additional information 23 Well Abaondonment Costs ($MM) Well Abandonment Costs ($MM)Reducing Decommissioning Liability Commentary Demonstrated Reduction in Well Abandonment Costs Compelling Decommissioning Liability reductions Wainwright 2019 Cardium 2019 12 Wells 115 Wells • Multi-year trend of decommissioning liability reduction 50% Decrease in $5.0 $0.8 Q2 2020: $604MM undiscounted 35% Per-Well Decrease Abandonment • Active participant in AER’s Area-Base Closure (ABC) Costs Below D11 $4.0 $0.6 Near-term spending minimized $3.0 • 2020 ABC spend requirements suspended; YTD 2020 spend fully creditable to 2021 requirements $0.4 $2.0 Government support & engagement $0.2 • Obsidian sites awarded $17MM million in grants and $1.0 additional $4MM allocation eligibility to date on our 3,492 applications within the ASRP $0.0 $0.0 D11 XI Actuals D11 XI Actuals • Actively engaged with EPAC and the AER to improve closure programs and regulations Historical Reductions in Abandonment Costs – Obsidian Energy Undiscounted & Uninflated Targeted, Efficient spending Decommissioning Liability • Focus on inactive Legacy assets to eliminate fixed OPEX from non-productive assets at costs well below D11 estimates • Shallow decline, long life, high netback, oil-weighted Pembina assets extend ARO requirements 76% decrease in Obsidian Energy ARO liability since 2015 over a long time period, stretching well into the future • Many wells in the Cardium can be reactivated, recompleted, or repurposed for use in reservoir monitoring See end notes for additional information 23 Well Abaondonment Costs ($MM) Well Abandonment Costs ($MM)

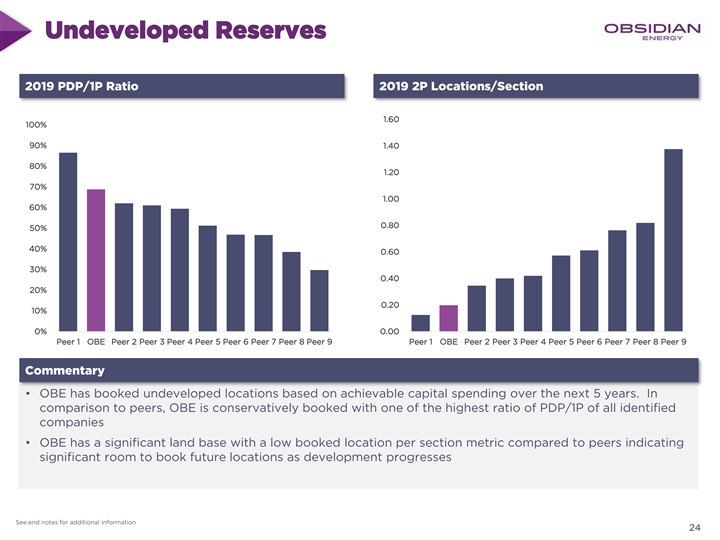

Undeveloped Reserves 2019 PDP/1P Ratio 2019 2P Locations/Section 1.60 100% 90% 1.40 80% 1.20 70% 1.00 60% 0.80 50% 40% 0.60 30% 0.40 20% 0.20 10% 0% 0.00 Peer 1 OBE Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 1 OBE Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Commentary • OBE has booked undeveloped locations based on achievable capital spending over the next 5 years. In comparison to peers, OBE is conservatively booked with one of the highest ratio of PDP/1P of all identified companies • OBE has a significant land base with a low booked location per section metric compared to peers indicating significant room to book future locations as development progresses See end notes for additional information 24Undeveloped Reserves 2019 PDP/1P Ratio 2019 2P Locations/Section 1.60 100% 90% 1.40 80% 1.20 70% 1.00 60% 0.80 50% 40% 0.60 30% 0.40 20% 0.20 10% 0% 0.00 Peer 1 OBE Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Peer 1 OBE Peer 2 Peer 3 Peer 4 Peer 5 Peer 6 Peer 7 Peer 8 Peer 9 Commentary • OBE has booked undeveloped locations based on achievable capital spending over the next 5 years. In comparison to peers, OBE is conservatively booked with one of the highest ratio of PDP/1P of all identified companies • OBE has a significant land base with a low booked location per section metric compared to peers indicating significant room to book future locations as development progresses See end notes for additional information 24

Current Hedge Strategy and Position Hedging Strategy • Hedge up to 50% of production volumes after royalty • Hedge at price levels to: • Protect FFO • Support economic capital program • Potential debt repayment • Hedges are done on a $CAD basis to avoid FX management Hedged Oil Position & Exercise Price (CAD$/bbl) Hedged AECO Gas Position & Exercise Price (CAD$/GJ) Volumes hedged physically to ensure positive NOI on specific heavy oil assets *Hedged Positions are current as of Sept. 30, 2020 25 See end notes for additional information Current Hedge Strategy and Position Hedging Strategy • Hedge up to 50% of production volumes after royalty • Hedge at price levels to: • Protect FFO • Support economic capital program • Potential debt repayment • Hedges are done on a $CAD basis to avoid FX management Hedged Oil Position & Exercise Price (CAD$/bbl) Hedged AECO Gas Position & Exercise Price (CAD$/GJ) Volumes hedged physically to ensure positive NOI on specific heavy oil assets *Hedged Positions are current as of Sept. 30, 2020 25 See end notes for additional information

Environmental, Social & Governance Environmental Governance Social Obsidian Energy is committed to Obsidian Energy is committed to Obsidian Energy makes it a minimizing the impact of our making a positive impact in the priority to ensure all operations on the environment. communities in which we stakeholders have a clear operate and live. understanding of our approach The ABC program allows for to business operations and our significant progress on Obsidian Energy supported and expectations for regulatory abandonment and reclamation donated to children’s compliance. of areas as a whole while development organizations, the increasing efficiencies and Prostate Cancer Center, and The Board is comprised of 88% decreasing costs of managing mental health organizations in independents, with an average our ARO profile. 2019. tenure for Board members of 3 years. Our environmental programs Obsidian Energy is a member of aim to meet or exceed all Explorers and Producers Our governance policies include environmental regulation, Association of Canada (EPAC), written documents such as a encompass stakeholder supporting Canada’s Diversity Policy, Business communication, resource conventional energy producers Conduct, Ethics Code of conservation, and proper site and its employees across Conduct and Whistleblower abandonment and reclamation western Canada. Policy. practices. 26Environmental, Social & Governance Environmental Governance Social Obsidian Energy is committed to Obsidian Energy is committed to Obsidian Energy makes it a minimizing the impact of our making a positive impact in the priority to ensure all operations on the environment. communities in which we stakeholders have a clear operate and live. understanding of our approach The ABC program allows for to business operations and our significant progress on Obsidian Energy supported and expectations for regulatory abandonment and reclamation donated to children’s compliance. of areas as a whole while development organizations, the increasing efficiencies and Prostate Cancer Center, and The Board is comprised of 88% decreasing costs of managing mental health organizations in independents, with an average our ARO profile. 2019. tenure for Board members of 3 years. Our environmental programs Obsidian Energy is a member of aim to meet or exceed all Explorers and Producers Our governance policies include environmental regulation, Association of Canada (EPAC), written documents such as a encompass stakeholder supporting Canada’s Diversity Policy, Business communication, resource conventional energy producers Conduct, Ethics Code of conservation, and proper site and its employees across Conduct and Whistleblower abandonment and reclamation western Canada. Policy. practices. 26

Experienced management and strong technical team Stephen E. Loukas, Interim President and Chief Executive Officer Financial and commercial • Vast experience in corporate transactions, capital markets, corporate finance Strong financial, and leadership commercial and capital $ • Mr. Loukas is a partner, managing member, and portfolio manager at $ markets experience FrontFour Capital Group LLC, one of the Company’s top shareholders, and leading the Company has been a member of the Board of Directors since 2018 Peter D. Scott, Senior Vice President, Chief Financial Officer Drilling, completions and Subsurface technical • 30 years of extensive financial experience, 20 years in CFO roles primarily in Canadian Oil and Gas companies Strong understanding of • Previously, Senior Vice President and Chief Financial Officer at Ridgeback geological subsurface, Resources Inc., previously Lightstream Resources Ltd. reservoir modelling, advanced design, construction and Aaron Smith, Senior Vice President, Development & Operations production of multi-stage • 20 years of engineering expertise across a broad range of technical and fractured horizonal wells leadership roles • Prior to Obsidian, VP-level leadership roles at Sinopec Canada and early career experience in Corporate Planning, Completions, and Reservoir Engineering Encana Corp. Operations Well-established routines Gary Sykes, Vice President, Commercial with methodical planning ▪ Over 25 years of experience in a variety of technical, operational and and preparations, which managerial positions in domestic and international oil and gas, primarily with has resulted in exemplary ConocoPhillips safety performance • Extensive Board experience, including the Qatargas 3 joint venture, The Mackenzie Valley Pipeline Board and Calgary Zoo Employees Mark Hawkins, Vice President, Legal, General Counsel and Deeply experienced with Corporate Secretary long track-record, • Served as the corporate secretary at Obsidian Energy since 2015 and was formerly the General Counsel and Corporate Secretary representing the top tier • 15 years of legal experience of Cardium expertise 27Experienced management and strong technical team Stephen E. Loukas, Interim President and Chief Executive Officer Financial and commercial • Vast experience in corporate transactions, capital markets, corporate finance Strong financial, and leadership commercial and capital $ • Mr. Loukas is a partner, managing member, and portfolio manager at $ markets experience FrontFour Capital Group LLC, one of the Company’s top shareholders, and leading the Company has been a member of the Board of Directors since 2018 Peter D. Scott, Senior Vice President, Chief Financial Officer Drilling, completions and Subsurface technical • 30 years of extensive financial experience, 20 years in CFO roles primarily in Canadian Oil and Gas companies Strong understanding of • Previously, Senior Vice President and Chief Financial Officer at Ridgeback geological subsurface, Resources Inc., previously Lightstream Resources Ltd. reservoir modelling, advanced design, construction and Aaron Smith, Senior Vice President, Development & Operations production of multi-stage • 20 years of engineering expertise across a broad range of technical and fractured horizonal wells leadership roles • Prior to Obsidian, VP-level leadership roles at Sinopec Canada and early career experience in Corporate Planning, Completions, and Reservoir Engineering Encana Corp. Operations Well-established routines Gary Sykes, Vice President, Commercial with methodical planning ▪ Over 25 years of experience in a variety of technical, operational and and preparations, which managerial positions in domestic and international oil and gas, primarily with has resulted in exemplary ConocoPhillips safety performance • Extensive Board experience, including the Qatargas 3 joint venture, The Mackenzie Valley Pipeline Board and Calgary Zoo Employees Mark Hawkins, Vice President, Legal, General Counsel and Deeply experienced with Corporate Secretary long track-record, • Served as the corporate secretary at Obsidian Energy since 2015 and was formerly the General Counsel and Corporate Secretary representing the top tier • 15 years of legal experience of Cardium expertise 27

Appendix & Endnotes 28Appendix & Endnotes 28