As filed with the Securities and Exchange Commission on December 14, 2005

Registration No. 333-128554

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 5

TO

FORM S-11

REGISTRATION STATEMENT UNDER THE SECURITIES ACT OF 1933

Republic Property Trust

(Exact Name of Registrant as Specified in Governing Instruments)

1280 Maryland Avenue, S.W., Suite 280

Washington, D.C. 20024

(202) 863-0300

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Mark R. Keller

Chief Executive Officer

Republic Property Trust

1280 Maryland Avenue, S.W., Suite 280

Washington, D.C. 20024

(202) 863-0300

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copies to:

J. Warren Gorrell, Jr., Esq.

Stuart A. Barr, Esq.

Hogan & Hartson L.L.P.

555 Thirteenth Street, N.W.

Washington, D.C. 20004-1109

(202) 637-5600 | Kathleen L. Werner, Esq.

Clifford Chance US LLP

31 West 52nd Street

New York, NY 10019-6131

(212) 878-8000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

The registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Subject to Completion, dated December 14, 2005

The information in this prospectus is not complete and may be changed. These securities may not be sold until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell the securities, nor is it a solicitation of an offer to buy the securities, in any state where an offer or sale of the securities is not permitted.

PROSPECTUS

20,000,000 Shares

Common Shares

This is an initial public offering of common shares of Republic Property Trust. All of the 20,000,000 common shares are being sold by Republic Property Trust. At our request, one of the underwriters has reserved for sale to affiliates of Richard L. Kramer, our Chairman of the Board, an aggregate of $5.0 million of common shares offered by this prospectus at the initial public offering price per share.

Republic Property Trust expects to qualify as a real estate investment trust, or “REIT,” for U.S. federal income tax purposes commencing with its taxable year ending December 31, 2005.

Prior to this offering, there has been no public market for the common shares. It is currently estimated that the initial public offering price per share will be between $14.00 and $16.00. Republic Property Trust’s common shares have been approved for listing on The New York Stock Exchange under the symbol “RPB,” subject to official notice of issuance.

See “Risk Factors” on page 23 of this prospectus to read about factors you should consider before buying our common shares.

| | Per Share | | Total | |

Initial public offering price | | $ | | | $ | | |

Underwriting discount(1) | | $ | | | $ | | |

Proceeds, before expenses, to Republic Property Trust | | $ | | | $ | | |

(1) Excludes a financial advisory fee of % of the public offering price in the aggregate payable to Lehman Brothers and Bear, Stearns & Co. Inc.

We have granted the underwriters a 30-day option to purchase up to an additional 3,000,000 common shares from us on the same terms and conditions as set forth above if the underwriters sell more than 20,000,000 common shares in this offering.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Lehman Brothers, on behalf of the underwriters, expects to deliver the common shares on or about , 2005.

| |

LEHMAN BROTHERS | BEAR, STEARNS & CO. INC. |

WACHOVIA SECURITIES

RAYMOND JAMES

UBS INVESTMENT BANK

KEYBANC CAPITAL MARKETS

, 2005

No dealer, salesperson or other person is authorized to give any information or to represent anything not contained in this prospectus. You must not rely on any unauthorized information or representations. This prospectus is an offer to sell only the shares offered hereby, but only under circumstances and in jurisdictions where it is lawful to do so. The information contained in this prospectus is current only as of its date.

Through and including (the 25th day after the date of this prospectus), all dealers effecting transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to a dealer’s obligation to deliver a prospectus when acting as an underwriter and with respect to an unsold allotment or subscription.

i

PROSPECTUS SUMMARY

You should read the following summary together with the more detailed information regarding our company, including under the caption “Risk Factors,” and the historical and pro forma financial statements, including the related notes, appearing elsewhere in this prospectus. Unless the context otherwise requires or indicates, references in this prospectus to “Republic Property Trust,” “Republic,” “we,” “our company,” “our” and “us” refer to Republic Property Trust, a Maryland real estate investment trust, together with our consolidated subsidiaries, including Republic Property Limited Partnership, a Delaware limited partnership, which we refer to in this prospectus as our “Operating Partnership,” Republic Property TRS, LLC, a Delaware limited liability company, and RKB Washington Property Fund I L.P., and its affiliates, which we refer to in this prospectus as our “predecessor.” In this prospectus we refer to the common shares of beneficial interest of Republic Property Trust as “common shares” or “REIT Shares,” and refer to the limited partnership units of the Operating Partnership as “OP units.” Unless the context otherwise indicates, the information about our company assumes that the formation transactions described in this prospectus have been completed. In addition, the information contained in this prospectus assumes that the underwriters’ option to purchase additional shares is not exercised and the common shares to be sold in this offering are sold at $15.00 per share, which is the mid-point of the price range indicated on the cover page of this prospectus.

Republic Property Trust

Overview

We are a fully integrated, self-administered and self-managed real estate investment trust formed to own, operate, acquire and develop primarily Class A office properties, predominantly in the Washington, D.C. metropolitan, or Greater Washington, D.C., market. We also selectively seek fee-based development opportunities for all real estate classes in various geographic areas inside and outside of Greater Washington, D.C. Headquartered in Washington, D.C., our founders and senior management team have been involved in the acquisition, management and development of more than 5 million square feet of institutional-grade office, office-oriented and mixed-use retail properties in Greater Washington, D.C.

We have substantial expertise in structuring and negotiating public/private partnerships with various governmental entities in Greater Washington, D.C., including local, regional and federal, boards and bodies. In addition, since 2002, our acquisition team has acquired and financed properties located in Greater Washington, D.C. totaling approximately 2 million net rentable square feet.

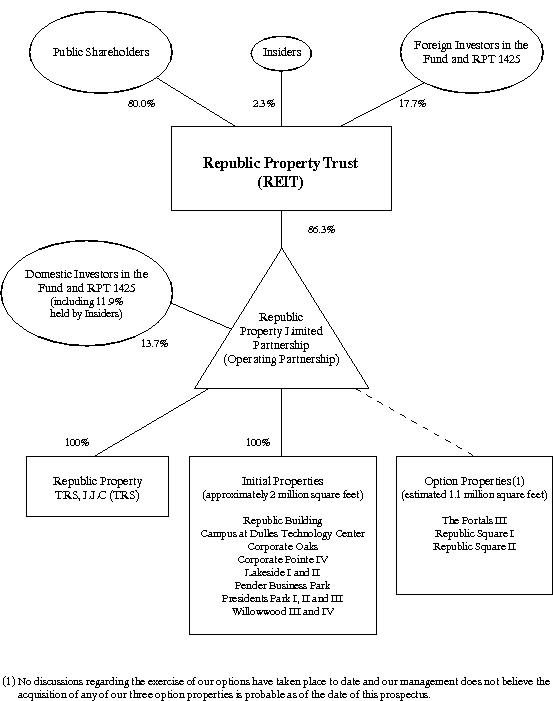

Upon completion of this offering and the formation transactions, we will own 10 commercial properties consisting of 21 institutional-grade office buildings indirectly through our Operating Partnership, in which we will have an approximate 86.3% interest. Our properties are characterized by our tenant base, which includes several U.S. government agencies and Fortune 500 companies, the institutional quality and utility of our office parks and buildings and the substantial amount of space occupied on average by our tenants. As of November 1, 2005, our office properties were approximately 24.3% leased to U.S. government agencies and approximately 55.8% leased to nationally recognized corporate tenants. Our initial portfolio of 10 commercial properties contains an aggregate of approximately 2 million net rentable square feet, with one Class A trophy office property located in the District of Columbia, approximately one half block from the White House, and nine Class A office properties located in Northern Virginia. In addition, we hold an option to acquire three office properties in the District of Columbia, representing an estimated 1.1 million net rentable square feet upon completion. Two of our option properties are currently under development and the remaining property is an undeveloped parcel of land.

Market Opportunity

The Greater Washington, D.C. market is the second largest office market in the United States, with approximately 376.7 million square feet of commercial office space in approximately 5,821 individual office properties in the District of Columbia, Northern Virginia and suburban Maryland.

Greater Washington, D.C. is characterized by a predominantly service-based economy and a highly educated workforce that generate significant demand for office space. We believe U.S. government agency spending, along with the industries it supports, provides a unique source of demand for office space in Greater Washington, D.C.

For the period from January 1, 2000 to December 31, 2004, the Greater Washington, D.C. commercial office market exceeded by approximately 97.1% the average cumulative return of its peer markets, which is based on investment income and appreciation, as determined by the National Council of Real Estate Investment Fiduciaries, or NCREIF. During the 20-year period from January 1, 1985 through December 31, 2004, the Greater Washington, D.C. commercial office market exceeded the average cumulative return of its peer markets by approximately 79.9%, as determined by NCREIF. We define our peer markets as the 10 largest office markets in the United States, excluding the District of Columbia.

Our Competitive Strengths

We believe we distinguish ourselves from other owners, operators and developers of office properties in a number of important ways and enjoy significant competitive strengths which include the following:

· Institutional Grade Office Portfolio. Our initial portfolio of 10 properties consists of 21 institutional-grade Class A office buildings with approximately 2 million net rentable square feet. As of November 1, 2005, our initial portfolio had an average age of approximately seven years, a weighted average remaining lease term of approximately four years and a weighted average occupancy rate of approximately 96.2%, excluding our Presidents Park I and II properties. As of November 1, 2005, we had signed leases increasing the amount of space under lease at our Presidents Park I and II properties to approximately 57.9%, an increase of approximately 37.6% from the occupancy rate of 20.3% at the time of acquisition of the properties in December 2004.

· Experienced Senior Management Team. Our senior management team has significant real estate industry experience, including developing the first two phases of The Portals, which comprise two Class A office buildings in the District of Columbia representing approximately 1.1 million net rentable square feet. Our management team also has managed our predecessor, RKB Washington Property Fund I, a commercial real estate investment fund.

· Greater Washington, D.C. Knowledge and Market Presence. Our senior management team has long-standing relationships with institutional investors, fund managers, developers, tenants and local and regional governments. For example, our network of industry contacts has enabled us to acquire all but one of our initial properties in privately negotiated transactions outside a competitive bidding process.

· Development Pipeline of Trophy Office Buildings. We have options to acquire an estimated 1.1 million net rentable square feet of proposed Class A office buildings in the District of Columbia. Our options concern both phases of the Republic Square project and The Portals III, which are located in two prime locations in the Capitol Hill and Southwest submarkets of Washington, D.C. We will also be the developer of these properties pursuant to arrangements we have entered into as part of the formation transactions. No discussions regarding the exercise of our options have taken place to date and our management does not believe the acquisition of any of our three option properties is probable as of the date of this prospectus.

2

· Successful Acquirer of Properties in Greater Washington, D.C. Since 2002, our acquisition team has acquired and financed properties totaling approximately 2 million net rentable square feet.

Our Business and Growth Strategies

Our primary business objectives are to own and operate a balanced portfolio of development, repositioning and stabilized office properties that maximize cash flow available for distribution to our shareholders, and achieve long-term growth in our business in order to maximize shareholder value. Our business and growth strategy consists of the following five elements:

· Maximize Cash Flow at Our Properties. We seek to maximize cash flows for distribution by efficiently managing our operating expenses and retaining and often expanding space occupied by our existing tenants. We intend to manage our portfolio by seeking to lease space in each property over a balanced lease schedule so that the portfolio produces stable rental income.

· Leverage Our Government Leasing Expertise and Relationships with Nationally Recognized Corporate Tenants to Increase the Performance of Our Portfolio. Our substantial in-house government leasing expertise enables us to attract and retain U.S. government agency and nationally recognized corporate tenants. As of November 1, 2005, our tenants on average occupied more than 33,000 net rentable square feet of space at our properties and two of our 10 initial properties, comprising an aggregate of 140,885 net rentable square feet, are fully leased to single tenants.

· Expand our Portfolio by Developing the Three Properties That We Have an Option to Acquire. We intend to develop The Portals III and the Republic Square I and II properties in the District of Columbia, which provide us with an opportunity to acquire an estimated 1.1 million net rentable square feet of office space, of which 890,000 square feet is currently under construction.

· Selectively Pursue Opportunities to Acquire Institutional Quality Office Properties. We generally seek to acquire Greater Washington, D.C. office properties that provide us with the opportunity to increase: (1) cash flow available for distribution, and (2) value through management efficiencies and leasing and marketing efforts. We seek to create stable cash flow and, in some cases, to redevelop and reposition an asset in order to maximize returns and values.

· Target Development Opportunities That We Believe Will Produce Attractive Returns. We believe a significant opportunity exists to maximize returns and achieve portfolio growth through the development and redevelopment of aging or market obsolete Class B and C office assets in Greater Washington, D.C., which is an office market with supply constraints. We also will selectively pursue fee-based development services for all real estate asset classes in order to achieve additional revenue and to secure future investment opportunities.

Our Investment Criteria

We selectively pursue development and redevelopment opportunities in supply constrained markets where we believe our overall development costs are below comparable existing building investment costs. We also pursue acquisition opportunities that will contribute to a balanced portfolio that generates both stable revenue growth and opportunistic returns. In evaluating potential acquisition opportunities, we seek properties that we believe can produce all cash returns in excess of the costs of capital and that meet one or more of the following criteria:

· substantially-leased institutional-grade office properties that require minimal capital improvements and support the tenant’s facility and long-term space requirements;

· properties located in well-established submarkets of Greater Washington, D.C. that possess substantial commercial infrastructure and are accessible to major transportation networks;

3

· stabilized properties in excess of 75,000 net rentable square feet and which have been built or renovated in the past 10 years; and

· properties which we believe can achieve high values and investment growth through the implementation of repositioning strategies and re-leasing and marketing plans.

Summary Risk Factors

You should carefully consider the matters discussed in the section “Risk Factors” prior to deciding whether to invest in our common shares. Some of these risks include:

· Our initial portfolio of properties, together with our three option properties, are all located in Greater Washington, D.C. and any downturn in the area’s economy may negatively affect our operating results;

· The consideration paid by us for the properties and other rights being contributed to us as part of the formation transactions may exceed the fair market value of these assets;

· We depend on a limited number of significant tenants and a payment delinquency, bankruptcy or insolvency of one or more of these tenants could adversely affect the income produced by our properties, which may harm our operating performance;

· We may be unable to renew existing leases or re-let space on terms similar to the existing leases, or at all, as leases expire, or we may expend significant capital in our efforts to re-let space, which may harm our operating performance;

· Our future growth is dependent on our acquisition of the three option properties and our growth may be harmed if our option agreements are terminated upon a change in control of our company or our independent trustees do not approve an acquisition of one or more of the option properties;

· Certain of our trustees and executive officers, and their affiliates, have substantial ownership interests in our three option properties and these interests may conflict with your interests;

· We face competition when pursuing fee-based development opportunities and our inability to capture these opportunities could negatively impact our growth and profitability;

· We may not be successful in identifying and consummating suitable acquisitions of office and office-oriented mixed-use properties meeting our criteria, which may impede our growth and negatively impact the price of our common shares;

· Our operating results will be harmed if we are unable to fully lease-up vacant space at properties such as Presidents Park I and II, which were underperforming at the time we acquired them;

· Required payments of principal and interest on our loan obligations may leave us with insufficient cash to operate our properties or to pay the distributions currently contemplated or necessary to maintain our qualification as a REIT and may expose us to the risk of default under our debt obligations;

· Our ability to pay our estimated initial annual distribution, which represents approximately 148.0% of our estimated cash available for distribution to our common shareholders for the 12 months ending September 30, 2006, depends upon our actual operating results, and we currently expect to borrow funds under our proposed line of credit to pay at least a portion of this distribution, which could slow our growth and depress the price of our common shares;

· Our management has limited experience operating as a REIT or a public company, and we cannot assure you that our limited experience will not harm our business and operating results;

4

· Our organizational documents contain provisions which may discourage a takeover of us and depress our common share price;

· Upon completion of this offering and the formation transactions, our Chairman of the Board, our President and Chief Development Officer, our Chief Executive Officer and our Chief Operating Officer and General Counsel, and their affiliates, will own approximately 7.6%, 1.6%, 1.5% and 2.8%, respectively, of our outstanding common shares and partnership units of our Operating Partnership on a fully-diluted basis and will have the ability to exercise significant control over our operations and any matter presented to our shareholders;

· Our Chairman of the Board and our President and Chief Development Officer have substantial outside business interests, including interests in Portals Development Associates Limited Partnership and Republic Properties Corporation, rights to continued management and development fee income in connection with The Portals Properties and ownership interests in the lessor of some of our office space, which give rise to various conflicts of interest with us and could harm our business;

· Our business and growth strategies could be harmed if key personnel with well-established ties to the Greater Washington, D.C. real estate market terminate their employment with us; and

· Failure to qualify as a REIT would subject us to U.S. federal income tax and would subject us and our shareholders to other adverse consequences.

5

Our Initial Properties

Upon completion of this offering and the formation transactions, we will own 10 Class A office properties (comprising 21 buildings), one of which is located in the District of Columbia and nine of which are located in Northern Virginia. The following table provides summary information regarding our initial properties as of November 1, 2005:

Office Properties(1) | | | | Location | | Number of

Buildings at

Property | | Year Built

(Renovated) | | Net Rentable

Square Feet(2) | | Percent

Leased(3) | | Annualized

Rent(4) | | Annualized

Rent Per

Leased

Square Foot(5) | |

Campus at Dulles Technology Center | |

Herndon,

Virginia

| | | 7 | | | 1998, 1999 | | | 349,839 | | | | 96.1 | % | | $ | 7,963,231 | | | $ | 23.69 | | |

Corporate Oaks | | Herndon,

Virginia | | | 1 | | | 1986 (1999) | | | 60,767 | | | | 100.0 | % | | $ | 1,243,175 | | | $ | 20.46 | | |

Corporate Pointe IV | | Chantilly,

Virginia | | | 1 | | | 1998 | | | 80,118 | | | | 100.0 | % | | $ | 1,399,466 | | | $ | 17.47 | | |

Lakeside I and II | | Chantilly,

Virginia | | | 2 | | | 1989, 1999 | | | 173,218 | | | | 85.7 | % | | $ | 3,048,268 | | | $20.54 | | |

Pender Business Park | | Fairfax,

Virginia | | | 4 | | | 2000 | | | 170,940 | | | | 100.0 | % | | $ | 4,183,718 | | | $ | 24.47 | | |

Presidents Park I | | Herndon,

Virginia | | | 1 | | | 1999 | | | 200,531 | | | | 83.4 | % | | $ | 1,440,978 | (6) | | $ | 23.11 | (6) | |

Presidents Park II | | Herndon,

Virginia | | | 1 | | | 2000 | | | 200,511 | | | | 32.5 | % | | $ | 1,293,372 | (7) | | $28.15 | (7) | |

Presidents Park III | | Herndon,

Virginia | | | 1 | | | 2001 | | | 200,135 | | | | 92.7 | % | | $ | 4,034,137 | | | $ | 21.74 | | |

The Republic Building | | Washington,

D.C. | | | 1 | | | 1992 | | | 276,018 | | | | 100.0 | % | | $ | 11,439,546 | | | $ | 41.44 | | |

Willowwood III and IV | | Fairfax,

Virginia | | | 2 | | | 1998 | | | 279,175 | | | | 97.3 | % | | $ | 7,114,341 | | | $26.20 | | |

Portfolio Total/ Weighted Average: | | | | | 21 | | | 1998 | | | 1,991,252 | | | | 88.5 | % | | $ | 43,160,232 | | | $ | 26.35 | | |

(1) Upon completion of this offering and the formation transactions, each property will be 100% indirectly owned in fee by our Operating Partnership.

(2) Net rentable square feet includes retail and storage space, but excludes on-site parking and rooftop leases.

(3) Includes leases or lease amendments that have been executed, regardless of whether or not occupancy has commenced.

(4) Annualized rent represents base rent, as determined from the date of the most recent amendment to a lease agreement, or from the original date of an agreement if not amended, for all leases in place in which tenants are in occupancy at November 1, 2005 as follows: total base rent to be received during the entire term of each lease (assuming no exercise of early termination options), divided by the total number of months in the term for such leases, multiplied by 12. Base rent includes historical contractual increases and excludes percentage rents, additional rent payable by tenants (such as common area maintenance and real estate taxes), contingent rent escalations and parking rents.

(5) Annualized rent per leased square foot represents annualized rent as computed above, divided by occupied net rentable square feet as of the same date.

(6) Excludes any annualized rent associated with a lease and an amendment to Network Solutions, LLC for 104,860 net rentable square feet because the rent commencement date under this lease is December 2005.

(7) Excludes any annualized rent associated with an amendment to our lease with iDirect, Inc. for an additional 19,215 net rentable square feet because the rent commencement date for this additional space is February 2006.

6

Option Properties

Simultaneously with the completion of this offering and the formation transactions, our Operating Partnership will enter into option agreements with entities controlled by some of our executive officers and trustees that grant us the right to acquire three office properties, two of which are under development and one of which is an undeveloped parcel of land. Each of these executive officers and trustees will benefit from any decision by us to exercise our options. See “Certain Relationships and Related Transactions—Formation Transactions—Option Properties.” We are not responsible for any of the costs associated with the development of, and do not currently own any interests in, these properties.

As described under the heading “Business and Properties—Terms of Option,” we have options to acquire the three properties described in the table below:

We have exclusive options to acquire each of the above three option properties during the period beginning after a property receives a certificate of occupancy. If we acquire an option property after it is 85% leased, then, subject to the approval of the majority of our independent trustees, the initial purchase price will equal, at our election, either: (1) the annualized net operating income divided by the then prevailing market capitalization rate for the option property as determined by an independent, third-party appraisal process completed immediately prior to our exercise of the option or (2) the annualized net operating income divided by 6.5%. In addition to the initial purchase price described above, an additional purchase price will be paid on an “earn-out” basis with respect to any initially unleased space that is leased during the period beginning after our purchase and ending on the earlier to occur of (1) the date the property first becomes 95% leased or (2) the second anniversary of the date of purchase of such property. We also may elect to acquire a property prior to it becoming 85% leased, but then the purchase price will be on terms and conditions to be determined by the seller and us (in each of our sole discretion); however, such an election by us must be unanimously approved by all of the independent members of our Board of Trustees. No discussions regarding the exercise of our options have taken place to date and our management does not believe the acquisition of any of our three option properties is probable as of the date of this prospectus.

For more information regarding the terms of our options, see “Business and Properties—Terms of Option.’’

Formation Transactions

Consideration for Assets Contributed

Prior to or concurrently with the completion of this offering, we will engage in a series of transactions, which we refer to in this prospectus as the formation transactions, that are intended to reorganize our company and facilitate this offering. In connection with these transactions, we have determined that:

· Fund Properties. 11,090,411 common shares of beneficial interest of us (with an aggregate value of approximately $166.4 million, based upon the mid-point of the price range indicated on the cover page of this prospectus), will be allocable to investors in RKB Washington Property Fund I L.P., or the Fund, prior to taking into account the individual elections of non-U.S. investors to receive REIT shares or cash, as consideration for the contribution of a 100% interest in the Fund properties;

7

· The Republic Building. $18.0 million will be allocable to investors of RPT 1425 Investors L.P., or RPT 1425, prior to taking into account the individual elections of non-U.S. investors to receive REIT shares or cash, in exchange for their contribution of a 100% interest in RPT 1425 (which indirectly holds a 100% interest in the Republic Building); and

· Management and Development Rights. Messrs. Kramer, Grigg and Keller and Republic Properties Corporation, a private real estate development, redevelopment and management company founded by Messrs. Kramer and Grigg, in exchange for their contribution of certain management and development rights, will receive an aggregate of 482,192 OP units (with an aggregate value of approximately $7.2 million, based upon the mid-point of the price range indicated on the cover page of this prospectus).

Structure

We summarize below the structure of our formation transactions undertaken in connection with this offering:

Contribution of Interests in the Nine Fund Properties

Nine of the 10 properties in which we will own 100% interests upon completion of this offering are currently held indirectly by the Fund. The Fund will, pursuant to contribution and related agreements, contribute all of its assets and liabilities, as well as direct and indirect interests in the nine properties, to our Operating Partnership in exchange for the consideration described above. As part of this consideration, the Fund will receive and then distribute OP units to its partners, some of which are entities owned or controlled by members of our Board of Trustees and members of our senior management team.

Contribution of Interests in the Republic Building

The investors in RPT 1425, which indirectly holds a 100% interest in the Republic Building, will, pursuant to contribution and related agreements, contribute all of their interests in RPT 1425 to our Operating Partnership. In exchange for the contribution of these interests to our Operating Partnership, the foreign partners of RPT 1425 will receive, based on a previous election made by each such partner, either (1) a specified number of REIT shares, or (2) a specified combination of REIT shares and cash. Domestic partners of RPT 1425 will receive a specified number of OP units.

Merger of RKB Holding L.P. into Our Operating Partnership

RKB Holding L.P., a Delaware limited partnership with no independent operations other than its role as a limited partner of the Fund, will merge with and into our Operating Partnership, and the partners of RKB Holding L.P. will receive, based on a previous election made by each such partner, either (1) a specified number of REIT shares, (2) a specified amount of cash, or (3) a specified combination of REIT shares and cash. In connection with the merger, our Operating Partnership will assume all of the obligations of RKB Holding L.P., including a loan made by RKB Finance L.P., a company affiliated with RKB Holding L.P. formed to facilitate the investment by certain non-U.S. investors in the Fund, in the amount of approximately $44.5 million and a tax liability estimated to be approximately $22.0 million. The consideration paid by the Operating Partnership in the merger will be reduced by the amount of this loan and tax liability. Following the merger, our Operating Partnership will repay this loan in part with proceeds from this offering and in part with REIT shares. See “Use of Proceeds.”

Management and Development Services

Contribution of Management and Development Services by Republic Properties Corporation—We have entered into agreements with Republic Properties Corporation pursuant to which Republic Properties Corporation will directly or indirectly contribute certain management, leasing and real estate development operations to our Operating Partnership. The assets contributed include agreements to provide management services for the 10 properties that will be included in our initial portfolio, agreements to provide fee-based development and management services with respect to Republic Square I and II, an agreement to provide fee-based development services to the City of West Palm Beach in connection with

8

the City Center project and other assets that will be used by the Operating Partnership in connection with the performance of these services.

Republic Properties Corporation will receive an aggregate of 415,210 OP units for the contribution of the assets described above, with the exception of the agreement to provide development and management services with respect to Republic Square II. Republic Properties Corporation will not receive any consideration for its contribution of the rights related to Republic Square II. Republic Properties Corporation is a District of Columbia corporation 85% owned by Mr. Kramer and 15% owned by Mr. Grigg.

The development fee payable to us with respect to Republic Square I will be based on the remaining development fees scheduled to be paid pursuant to the development agreement that will be assigned to us upon completion of this offering and the formation transactions. The development agreement provides for the payment of a total development fee of $3.5 million, approximately $1.7 million of which had been paid to Republic Properties Corporation for development services provided through October 31, 2005. Upon completion of this offering and the formation transactions, we will have a right to receive the remaining portion of the development fee in exchange for providing development services to the project. The development fee payable to us with respect to Republic Square II will equal 3% of the development costs, which are calculated net of land acquisition, interest and loan expenses, and cash concessions to tenants. The management fee payable to us with respect to Republic Square I and II, when completed and in advance of our option to acquire these properties, will equal 1% of the gross revenues of each property and a payment to cover the cost of corporate and property labor and overhead for providing these services.

The agreements providing for management and development services to Republic Square I and II and the City Center project in the City of West Palm Beach and certain other assets associated with management and development activities will be contributed by the Operating Partnership to Republic Property TRS, LLC, a taxable REIT subsidiary of ours.

Outsourcing of Management and Development Services for The Portals Properties—Messrs. Kramer and Grigg and Republic Properties Corporation, each general partners of Portals Development Associates Limited Partnership, or PDA, have certain rights to provide management and development services and currently receive fees from PDA in connection with providing management and development services to a group of properties and parcels of land in the District of Columbia known as The Portals, which consists of two completed office buildings, The Portals I and II, and three development properties, The Portals III, IV and V (“The Portals Properties”). Currently, The Portals III is under construction and The Portals IV and V are undeveloped parcels of land. The terms of the PDA partnership agreement provide that any fee amounts earned but unpaid are accumulated as internal preferences with respect to future partnership distributions. We have entered into agreements with Messrs. Kramer and Grigg and Republic Properties Corporation, which we will transfer following the closing to Republic Property TRS, LLC, a taxable REIT subsidiary of ours, to provide:

· management services to The Portals I and II, in exchange for a fee equal to 1% of the gross revenues of each property and a payment to cover the cost of the corporate and property labor and overhead for providing those services;

· development services to The Portals III, in exchange for a fee equal to 3% of the remaining development costs, which are defined as net of land acquisition, interest and loan expenses, and cash concessions to tenants;

· development services to The Portals IV and V, in exchange for a fee equal to 3% of the development costs, which are defined as net of land acquisition, interest and loan expenses, and cash concessions to tenants; and

· management services to The Portals III, IV and V, when completed, and in the case of The Portals III in advance of any exercise by us of our option to acquire The Portals III, in exchange for a fee equal to 1% of the gross revenues of each property and a payment to cover the cost of the corporate and property labor and overhead for providing those services.

9

Republic Properties Corporation and Messrs. Kramer and Grigg, the general partners of PDA, will receive an aggregate of 66,982 OP units in consideration of the contribution of their right to provide development and management services to The Portals III. Of these 66,982 OP units, Republic Properties Corporation and Messrs. Kramer and Grigg will receive 22,327, 37,957 and 6,698 OP units, respectively. Republic Properties Corporation and Messrs. Kramer and Grigg will not receive any consideration for the contribution of the rights to provide development and management services to The Portals I, II, IV and V, or the engagement of the Operating Partnership to provide corporate and administrative services to PDA.

We believe the fees described above are at competitive market rates for management and development services in the office sector generally. These fees will be payable to us on a monthly basis. These fees represent only a portion of (and will be payable out of) the management and development fees that will continue to be payable to Messrs. Kramer and Grigg and Republic Properties Corporation through PDA, which include, among other items:

· a development fee equal to 5% of all development costs;

· a construction management fee equal to 5% of all direct costs of construction (of which 1/8th is payable to East Coast Development Corporation, the unaffiliated general partner);

· a management fee equal to 5% of gross rental receipts; and

· a leasing fee equal to 3% of the gross rental receipts, which may be reduced by up to 2% to the extent unaffiliated brokers or leasing agents are engaged to perform leasing services.

The fees described above, which are payable to Messrs. Kramer and Grigg and Republic Properties Corporation (out of which a portion will be payable to us) are payable only out of net cash flow and net refinancing and sale proceeds realized by PDA that are available for distribution. The portion of the fees payable to us will be paid on a priority basis prior to payment of the remaining balance of such fees to Messrs. Kramer and Grigg and Republic Properties Corporation.

Messrs. Kramer and Grigg and Republic Properties Corporation, collectively, earned approximately $3.3 million and $4.0 million in aggregate fees from PDA for management and development services provided to The Portals I, II and III during the year ended December 31, 2004 and the ten-month period ended October 31, 2005, respectively. If we had performed these services during the same periods pursuant to the terms of our agreements with Messrs. Kramer and Grigg and Republic Properties Corporation, we would have received approximately $2.2 million and $2.4 million in aggregate fees.

Our Operating Partnership

Following completion of this offering and the formation transactions, substantially all of our assets will be held by, and our operations conducted by, our Operating Partnership. We will contribute the proceeds of this offering to our Operating Partnership in exchange for a number of OP units equal to the number of common shares issued in this offering. Certain other entities and individuals, including Messrs. Kramer, Grigg, Keller and other members of our senior management, will own the remaining units and be limited partners of our Operating Partnership. Our primary asset will be our general and limited partner interests in our Operating Partnership. This structure is commonly referred to as an umbrella partnership REIT, or UPREIT, structure.

Restrictions on Transfer

Under our partnership agreement, OP unitholders do not have redemption or exchange rights and may not otherwise transfer their units, except under certain limited circumstances, for a period of 12 months from the completion of this offering. In addition, our trustees, trustee nominees and executive officers, including Messrs. Kramer, Grigg and Keller, have agreed not to sell or otherwise transfer or encumber any of our common shares or securities convertible or exchangeable into our common shares (including OP units) owned by them at the completion of this offering or thereafter acquired by them prior to July 1, 2007, other than permitted transfers, without the consent of Lehman Brothers Inc. and Bear, Stearns & Co. Inc., on behalf of the underwriters.

10

Our Structure

The following chart reflects our organizational structure upon completion of this offering and the formation transactions:

11

Benefits to Related Parties

Upon completion of this offering and the formation transactions, our senior management and members of our Board of Trustees will receive material financial and other benefits, as shown below. For a more detailed discussion of these benefits, see “Certain Relationships and Related Transactions.”

Formation Transactions

Messrs. Kramer, Grigg, Keller and certain other members of our senior management will contribute interests in certain assets, including interests in the Fund properties, the Republic Building and project-related management and development rights, as summarized below:

· the contribution by the Fund of interests in entities holding nine properties to our Operating Partnership;

· the contribution by the investors in RPT 1425 of their interests in RPT 1425 (which indirectly holds a 100% interest in the Republic Building) to our Operating Partnership;

· the contribution by Republic Properties Corporation of management and development services for our 10 portfolio properties, Republic Square I and II and the City Center project in the City of West Palm Beach, Florida; and

· the outsourcing by Messrs. Kramer and Grigg and Republic Properties Corporation of management and development services for The Portals Properties.

In connection with the above transactions, Messrs. Kramer, Grigg, Keller and Siegel, and/or their affiliates, will receive OP units in the following amounts:

| | | | OP Units | |

Name (1) | | | | Contribution Transactions | | Number | | Value(2) | |

Richard L. Kramer | | Property: | | | | | |

| | RKB Fund | | 1,274,811 | | $ | 19,122,165 | |

| | Republic Building | | 160,733 | | 2,410,995 | |

| | Management and/or Development Rights: | | | | | |

| | Initial Properties | | 207,391 | | 3,110,865 | |

| | The Portals III | | 56,935 | | 854,025 | |

| | Republic Square I | | 41,095 | | 616,425 | |

| | City Center | | 85,199 | | 1,277,985 | |

| | Total: | | 1,826,164 | | $ | 27,392,460 | |

Steven A. Grigg | | Property: | | | | | |

| | RKB Fund | | 371,102 | | $ | 5,566,530 | |

| | Republic Building | | 1,428 | | 21,420 | |

| | Management and/or Development Rights: | | | | | |

| | Initial Properties | | 36,599 | | 548,985 | |

| | The Portals III | | 10,047 | | 150,705 | |

| | Republic Square I | | 7,252 | | 108,780 | |

| | City Center | | 15,035 | | 225,525 | |

| | Total: | | 441,463 | | $ | 6,621,945 | |

Mark R. Keller | | Property: | | | | | |

| | RKB Fund | | 313,592 | | $ | 4,703,880 | |

| | Republic Building | | 4,500 | | 67,500 | |

| | Management and/or Development Rights: | | | | | |

| | Initial Properties | | 22,639 | | 339,585 | |

| | Total: | | 340,731 | | $ | 5,110,965 | |

Gary R. Siegel(3) | | Property: | | | | | |

| | RKB Fund | | 762,571 | | $ | 11,438,565 | |

| | Republic Building | | 17,539 | | 263,085 | |

| | Total: | | 780,110 | | $ | 11,701,650 | |

| | | | | | | | | | |

(1) Includes affiliates of named person, including Republic Properties Corporation, a District of Columbia corporation owned by Messrs. Kramer and Grigg.

(2) Based upon an assumed initial public offering price of $15.00 per share, which is the mid-point of the price range indicated on the cover page of this prospectus.

(3) Includes an aggregate of 718,656 OP units with a value of $10,779,840 owned by certain trusts for the benefit of Mr. Kramer’s affiliates for which Mr. Siegel acts as trustee and over which Mr. Siegel disclaims any beneficial ownership.

12

Option Properties

Our Operating Partnership has entered into agreements with entities in which Messrs. Kramer, Grigg and Keller have ownership interests that, upon completion of this offering and the formation transactions, grant us options to acquire The Portals III and Republic Square I and II. The Portals III and Republic Square I are each currently under development while Republic Square II is an undeveloped parcel of land. The purchase price for these properties, if we exercise an option, is payable in OP units or cash and the assumption (or discharge if such assumption is not permitted by the lender) of any indebtedness or other obligations. However, Messrs. Kramer, Grigg and Keller will only receive OP units in connection with the acquisition of an option property. Each of Messrs. Kramer, Grigg and Keller will benefit from any decision by us to exercise our options. The terms of the option agreements are described under the heading “Business and Properties—Option Properties.”

Employment and Noncompetition Agreements

Upon completion of this offering, we will enter into an employment agreement with Mr. Keller providing for his employment through December 2009, with automatic one-year renewals and providing for salary, bonus and other benefits, including severance upon a change in control or termination of employment under certain circumstances. In addition, Mr. Keller’s employment agreement will contain certain covenants not to compete with us, and such covenants will be effective during the term of his employment plus a period of 18 months after Mr. Keller’s termination of employment. We also have entered into an employment agreement with Michael J. Green pursuant to which he will serve as an Executive Vice President and our Chief Financial Officer, and we will enter into employment agreements with Steven A. Grigg pursuant to which Mr. Grigg will serve as our President, Chief Development Officer and Vice Chairman of the Board, and with Gary R. Siegel pursuant to which Mr. Siegel will serve as our Chief Operating Officer and General Counsel. Mr. Green’s employment agreement, as amended, became effective on October 31, 2005. Messrs. Grigg’s and Siegel’s employment agreements will become effective upon the closing of this offering. Messrs. Grigg’s, Siegel’s and Green’s employment agreements provide for their employment through December 2009, with automatic one-year renewals, and provide for salary, bonus and other benefits, including severance upon termination of employment under certain circumstances. Additionally, Messrs. Grigg, Siegel and Green will each enter into a noncompetition agreement pursuant to which they will agree not to compete with us for a period that is the longer of three years or the period of their employment plus an additional 18-month period. We also will enter into noncompetition agreements with Mr. Kramer, our Chairman of the Board, and Republic Properties Corporation. In the case of the noncompetition agreements with Mr. Kramer and Republic Properties Corporation, the covenants not to compete will be effective for the longer of three years or Mr. Kramer’s tenure on our Board plus, unless Mr. Kramer is removed from our Board without cause, 18 months thereafter. The noncompetition agreements with Mr. Kramer and Republic Properties Corporation will terminate upon a change in control of us. In addition, Mr. Kramer and Republic Properties Corporation have agreed to refer without consideration to us any investment and fee-based development opportunities for commercial office properties in Greater Washington, D.C. which are presented to them for at least three years following this offering. See “Management—Employment and Noncompetition Agreements.”

13

Restricted Shares

In connection with this offering, we will grant an aggregate of 260,384 restricted REIT shares to certain of our trustees, trustee nominees, executive officers and certain other employees of our company. The restricted shares are immediately vested but may not be directly or indirectly offered, pledged, sold, transferred, other than permitted transfers, or otherwise disposed of prior to July 1, 2007. We will also grant to these individuals a cash award in the aggregate amount of $2.6 million.

The following individuals will receive the number of restricted REIT shares and cash as set forth below:

Name | | Title | | Number of Shares | | Cash Award($) | |

Executive Officers | | | | | | | | | | | |

Mark R. Keller | | Chief Executive Officer | | | 86,795 | | | | $ | 867,946 | | |

Michael J. Green | | Chief Financial Officer | | | 28,932 | | | | 289,315 | | |

Gary R. Siegel | | Chief Operating Officer/General Counsel | | | 28,932 | | | | 289,315 | | |

Thomas G. Archer, Jr. | | Senior Vice President | | | 12,151 | | | | 121,512 | | |

Peter J. Cole | | Senior Vice President | | | 12,151 | | | | 121,512 | | |

Frank M. Pieruccini | | Senior Vice President | | | 12,151 | | | | 121,512 | | |

Geoffrey N. Azaroff | | Senior Vice President | | | 8,679 | | | | 86,795 | | |

Michael C. Jones | | Vice President | | | 12,151 | | | | 121,512 | | |

Andrew G. Pulliam | | Vice President | | | 12,151 | | | | 121,512 | | |

Other Employees | | | | | 26,038 | | | | 260,384 | | |

Board of Trustees | | | | | | | | | | | |

Richard L. Kramer | | Chairman of the Board of Trustees | | | 2,893 | | | | 28,932 | | |

John S. Chalsty | | Trustee Nominee | | | 4,340 | | | | 43,397 | | |

Gregory H. Leisch | | Trustee Nominee | | | 4,340 | | | | 43,397 | | |

Ronald D. Paul | | Trustee Nominee | | | 4,340 | | | | 43,397 | | |

| | Trustee Nominee(1) | | | 4,340 | | | | 43,397 | | |

Total: | | | 260,384 | | | | $ | 2,603,835 | | |

(1) The Board of Trustees intends to appoint an additional independent trustee after completion of this offering and expects to issue additional restricted shares and cash to such person as indicated above.

Conflicts of Interest

Following completion of this offering and the formation transactions, conflicts of interest will exist between our trustees and executive officers and our company, as detailed below:

· Messrs. Kramer, Grigg and Keller and their affiliates have substantial ownership interests in our three option properties and while any decisions regarding whether or not to purchase these properties in the future will be made by a vote of our independent trustees, we cannot assure you that we will not be adversely affected by conflicts arising from Messrs. Kramer, Grigg and Keller’s existing and ongoing economic interest in these properties, including the possible diversion of these individuals’ time and attention away from focusing on our business in an effort to enhance the value of the option properties for which they will receive significant compensation upon exercise of our option. See “Risk Factors—Risks related to our business and properties.”

· Upon completion of this offering and the formation transactions, Messrs. Kramer, Grigg, Keller and Siegel and their affiliates will own approximately 7.6%, 1.6%, 1.5% and 2.8%, respectively, of our outstanding common shares and partnership units of our Operating Partnership on a fully-

14

diluted basis and will have the ability to exercise significant control over our operations and any matter presented to our shareholders. See “Risk Factors—Risks related to our organization and structure.”

· Messrs. Kramer and Grigg have substantial outside business interests, including interests in PDA and Republic Properties Corporation and rights to continued management and development fee income in connection with The Portals Properties and ownership interests in the lessor of our office space, which give rise to various conflicts of interest with us and could harm our business. See “Risk Factors—Risks related to our organization and structure’’ and “Certain Relationships and Related Transactions—Excluded Assets.”

· Although we will enter into employment agreements with Messrs. Keller and Grigg and noncompetition agreements with Messrs. Kramer, Keller and Grigg, each of them will be permitted to pursue specified business interests that may divert some of their time and attention from our business, as long as such interests do not materially and adversely interfere with their duties for us, in the case of Messrs. Keller and Grigg, and do not violate their noncompetition agreements. While we currently believe that Mr. Keller will devote substantially all of his time to our operations and Mr. Grigg will spend less than 10% of his time managing his outside business interests, these amounts could vary at any time or from time to time based on the particular needs of those outside business interests.

· We may pursue less vigorous enforcement of the terms of our agreements with members of our senior management, including Messrs. Kramer, Grigg and Keller, and their affiliated entities because of our dependence on them as well as conflicts of interest that exist. See “Risk Factors—Risks related to our organization and structure.”

· Gregory H. Leisch, who has agreed to become one of our independent trustees upon completion of this offering, is Chief Executive of Delta Associates, a Washington, D.C.-based real estate consulting firm. We have relied in the past, and expect that we will in the future rely, upon market research prepared by Delta Associates.

· An affiliate of Lehman Brothers Inc., one of the managing underwriters of this offering, has (1) agreed to provide to us up to $50 million to refinance the existing mortgage loans secured by the Presidents Park I, II and III properties if this offering is not consummated prior to the January 2006 maturity date of the existing mortgage indebtedness on those properties, and (2) has entered into a commitment letter to provide us with a $150 million senior secured revolving credit facility following completion of this offering. The Lehman Brothers Inc. affiliate has received a commitment fee for agreeing to provide the Presidents Park financing and affiliates of Lehman Brothers Inc. will receive future fees under the credit facility, including a facility underwriting fee and an annual administrative agency fee. The lenders under the credit facility will also be paid commitment fees based on their respective commitment levels. Lehman Brothers Inc. will act as sole advisor, lead arranger and bookrunner for the credit facility. We also expect that affiliates of Bear, Stearns & Co. Inc., Wachovia Capital Markets, LLC, Raymond James & Associates, Inc., UBS Securities LLC and KeyBanc Capital Markets may be lenders under the credit facility. These financing transactions create potential conflicts of interest for the underwriters participating in them because such underwriters and their affiliates have additional interests in the successful completion of this offering beyond the underwriting discounts and commissions and financial advisory fees they will receive. Additional potential conflicts of interest may arise in determining the size or price of the offering because the closing of the credit facility is contingent upon, among other things, this offering closing with minimum gross proceeds of $225 million.

In addition, conflicts of interest could arise in the future as a result of the relationships between us and our affiliates, on the one hand, and our Operating Partnership or any partner thereof, on the other.

15

Our trustees and officers have duties to our company and our shareholders under applicable Maryland law in connection with their management of our company. At the same time, we have fiduciary duties, as a general partner, to our Operating Partnership and to the limited partners under Delaware law in connection with the management of our Operating Partnership. Our duties as a general partner to our Operating Partnership and its partners may come into conflict with the duties of our trustees and officers to our company and our shareholders. The partnership agreement of our Operating Partnership provides that, in the event of a conflict of interest between our shareholders and the limited partners of our Operating Partnership, we will endeavor in good faith to resolve the conflict in a manner not adverse to either our shareholders or the limited partners or our Operating Partnership, and, if we, in our sole discretion as general partner of the Operating Partnership, determine that a conflict cannot be resolved in a manner not adverse to either our shareholders or the limited partners of our Operating Partnership, the conflict will be resolved in favor of our shareholders.

Our Tax Status

We intend to elect and qualify to be taxed as a REIT under the Internal Revenue Code of 1986, as amended, or the Internal Revenue Code, commencing with our taxable year ending December 31, 2005. Our qualification as a REIT depends upon our ability to meet on a continuing basis, through actual annual and quarterly operating results, various complex requirements under the Internal Revenue Code relating to, among other things, the nature and sources of our gross income, the composition and values of our assets, our distribution levels and the diversity of ownership of our shares. We believe that we will be organized in conformity with the requirements for qualification and taxation as a REIT under the Internal Revenue Code, and that our intended manner of operation will enable our company to meet the requirements for qualification and taxation as a REIT for U.S. federal income tax purposes.

As a REIT, we generally will not be subject to U.S. federal income tax on our taxable income that we distribute currently to our shareholders. If we fail to qualify as a REIT in any taxable year, we will be subject to U.S. federal income tax at regular corporate rates even if we distribute our income. Even if we satisfy the requirements for taxation as a REIT, we may be subject to some federal, state and local taxes on our income and property, and certain of our subsidiaries that will be “taxable REIT subsidiaries” will be subject to federal, state and local income taxes.

We expect to conduct some of our operations through taxable REIT subsidiaries. Our taxable REIT subsidiaries will be subject to U.S. federal income tax as corporations on their taxable income. The income earned by our taxable REIT subsidiaries, after payment of applicable corporate income taxes, may be retained by the taxable REIT subsidiaries and, unless distributed to the REIT, will not affect the amount that the REIT is required to distribute to its shareholders in order to satisfy the 90% distribution requirement and avoid a corporate tax liability. The value of securities we hold in our taxable REIT subsidiaries cannot exceed 20% of the total value of our assets. We expect that, as of the close of the first quarter after the close of this offering and the formation transactions, the aggregate value of the securities of our taxable REIT subsidiaries which we hold will represent less than 5.0% of the value of our total assets. The treatment of our taxable REIT subsidiaries is discussed in greater detail below under the section entitled “Material United States Federal Income Tax Considerations—Taxation of the Company as a REIT—Taxable REIT Subsidiaries’’ and “Material United States Federal Income Tax Considerations—Tax Aspects of Our Investments in Taxable REIT Subsidiaries.”

16

Restrictions on Ownership of our Common Shares

In order to qualify as a REIT under the Internal Revenue Code, we must satisfy certain ownership diversification requirements and related party tenant rules. Because our Board of Trustees believes that it is essential for us to qualify as a REIT, our Declaration of Trust will contain restrictions on the number of our shares of beneficial interest, including our common shares, that a person may own in order to assist us in maintaining our REIT qualification. Generally, our Declaration of Trust will provide that:

· no person may own directly, or be deemed to own by virtue of the attribution provisions of the Internal Revenue Code, more than 9.8%, in value or number of shares, whichever is more restrictive, of the issued and outstanding shares of any class or series of our shares of beneficial interest;

· no person may beneficially or constructively own our shares of beneficial interest that would result us in being “closely held” under Section 856(h) of the Internal Revenue Code or otherwise cause us to fail to qualify as a REIT;

· no person may transfer our shares of beneficial interest if such transfer would result in our shares of beneficial interest being owned by fewer than 100 persons; and

· any purported transfer of our shares of beneficial interest or any other event that would otherwise result in any person violating any one or more of the limits on the ownership and transferability of our shares of beneficial interest will be void and of no force or effect with respect to the prohibited transferee with respect to that number of shares that exceeds the ownership limit and the prohibited transferee would not acquire any right or interest in the shares, or the shares will be transferred to a trust for the benefit of a charitable beneficiary.

In addition, in order to assist us with the enforcement of the restrictions on the ownership of our shares of beneficial interest, our Declaration of Trust requires a holder of our shares of beneficial interest to comply with various notice and information provision requirements with respect to its ownership of our shares. See “Description of Shares—Restrictions on Ownership and Transfer.”

Our Distribution Policy

To satisfy the requirements to qualify as a REIT, and to avoid paying tax on our income, we intend to make regular quarterly distributions of all, or substantially all, of our taxable income (including net capital gains) to holders of our common shares and OP units. We intend to pay a pro rata initial distribution with respect to the period commencing on the completion of this offering and ending December 31, 2005, based on a distribution of $0.206 per share for a full quarter. On an annualized basis, this would be $0.825 per share, or an annual distribution rate of approximately 5.5% based on an initial public offering price of $15.00 per share, which is the mid-point of the range indicated on the cover page of this prospectus.

We estimate that this initial annual rate of distribution will represent approximately 148.0% of our estimated cash available for distribution to our common shareholders and OP unitholders for the 12 months ending September 30, 2006. This estimate is based upon our pro forma operating results and does not take into account our growth initiatives, which we believe will increase our cash available for distribution, nor does it take into account any unanticipated expenditures we may have to make or any debt we may have to incur. If sufficient cash is not generated from operations to pay our estimated initial annual distribution or to satisfy the requirement that we distribute at least 90% of our taxable income (excluding net capital gains) to avoid paying tax on our REIT taxable income, we expect to borrow to fund the shortfall. To the extent that we make distributions in excess of our earnings and profits, as computed for federal income tax purposes, these distributions will represent a return of capital, rather than a dividend, for federal income tax purposes.

17

Any future distributions we make will be at the discretion of our Board of Trustees and will depend upon, among other things, our actual results of operations. See “Distribution Policy.” Our actual results of operations and our ability to pay distributions will be affected by a number of factors, including the rental revenue from our properties, management and development fees, our operating expenses, interest expense, recurring capital expenditures and unanticipated expenditures. For more information regarding risk factors that could materially adversely affect our actual results of operations, please see “Risk Factors.”

About Our Company

Our principal executive office is located at 1280 Maryland Avenue, S.W., Washington, D.C. 20024. Our telephone number is (202) 863-0300. We maintain a website at www.republicpropertytrust.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider information contained on our website to be part of this prospectus.

About This Prospectus

Throughout this prospectus, we use market data which we have obtained from publicly available market research and industry publications. These sources generally state that the information they provide has been obtained from sources believed to be reliable, but that the accuracy and completeness of the information are not guaranteed. Similarly, we believe that the market research others have performed is reliable, but we have not independently verified this information. In addition, we have utilized data derived from publicly available market research compiled by Delta Associates. Gregory H. Leisch, Delta Associates’ Chief Executive, has agreed to become a member of our Board of Trustees upon completion of this offering. None of the market research provided to us by Delta Associates for use in this prospectus was prepared specifically for us.

18

The Offering

Issuer | | Republic Property Trust |

Common shares offered by us | | 20,000,000 shares |

Underwriters’ option to purchase additional shares from Republic Property Trust | | 3,000,000 shares |

Common shares to be outstanding after this offering(1) | | 24,605,332 shares |

Common shares and OP units to be outstanding after this offering(1)(2) | | 28,500,481 shares and units |

Use of proceeds | | We estimate that our net proceeds of this offering will be approximately $272.5 million (approximately $314.4 million if the underwriters exercise their option to purchase additional shares in full), after taking into account estimated underwriting discounts, commissions and offering expenses. We intend to use our net proceeds of this offering to repay existing indebtedness, to satisfy certain tax and other liabilities assumed by our Operating Partnership in connection with its merger with RKB Holding L.P., to redeem the interests of some of the partners in the Fund as part of the formation transactions, to pay certain assumption fees in connection with our outstanding indebtedness and for general corporate and working capital purposes, including acquisitions of office properties. An affiliate of Lehman Brothers Inc. has agreed to provide to us up to $50 million to refinance the existing mortgage loans secured by the Presidents Park I, II and III properties to the extent that we do not repay in full the outstanding balances under these loans with proceeds from this offering. See “Risk Factors—Risks related to this offering—The refinancing of certain indebtedness and our revolving credit facility may create a potential conflict of interest for certain of our underwriters’’ and “Underwriting.’’ |

New York Stock Exchange symbol | | RPB |

Risk Factors | | For a discussion of certain risks relating to our business and an investment in our common shares, see “Risk Factors” beginning on page 23 of this prospectus. |

(1) The number of common shares to be outstanding after this offering gives effect to (a) the sale of 20,000,000 common shares in this offering, (b) the issuance of 4,344,848 common shares in the formation transactions, (c) the grant of 260,384 restricted common shares to certain of our trustees, trustee nominees, executive officers and certain other employees immediately prior to the completion of this offering, and excludes shares reserved under our 2005 Omnibus Long-Term Incentive Plan, and (d) 100 common shares representing our initial capitalization.

(2) The number of common shares and OP units to be outstanding after this offering gives effect to the issuance of 3,895,149 OP units in the formation transactions.

19

Summary Consolidated Financial Data

The following table sets forth certain financial data on a pro forma basis and on a historical consolidated basis for our predecessor. Our predecessor will contribute nine of our initial 10 properties to us as part of the formation transactions. The historical operating results of our predecessor include management expenses, as our predecessor was not self-managed. Following completion of the offering, we will be a self-managed real estate investment trust. In addition, the historical and pro forma operating results of our predecessor do not include any management or development fee revenue that we expect to receive from contracts to be contributed to us in connection with the formation transactions. See “Formation Transactions—Management and Development Services.” For information regarding the historical operating results of the 1425 New York Avenue property, the 10th property to be contributed to us as part of the formation transactions, please see the financial statements beginning on page F-57 of this prospectus.

The unaudited pro forma operating data presented below for the nine months ended September 30, 2005 and for the year ended December 31, 2004 give effect to this offering and the formation transactions as if each had occurred on January 1, 2004. Pro forma balance sheet data are presented as if the offering and formation transactions had occurred on September 30, 2005. For more information regarding the formation transactions, please see “Formation Transactions.” The pro forma data below do not include adjustments for income and costs associated with our third-party fee-based development and management arrangements for future services. The pro forma data do not purport to represent what our actual financial position or results of operations would have been as of or for the periods indicated, nor do they purport to represent any future financial position or results of operation for any future periods.

Per share data are reflected only for the pro forma information. Per share data are not relevant for the historical consolidated financial statements of our predecessor since such financial statements are a consolidated presentation of the predecessor, a partnership and its wholly owned single-purpose entities organized as limited liability companies. Historical operating results, including net income, may not be comparable to future operating results because of the historically greater leverage of our predecessor.

The following summary historical financial information as of September 30, 2005 and for the nine months ended September 30, 2005 and 2004 has been derived from our unaudited, interim financial statements and includes all adjustments, consisting only of normal, recurring accruals, which management considers necessary for a fair presentation of the historical financial statements for such periods.

The following summary historical financial information as of December 31, 2004 and 2003 and for each of the years then ended and for the period from August 21, 2002 (inception) through December 31, 2002 was derived from our audited financial statements included elsewhere in this prospectus.

20

You should read the information below together with all of the financial statements and related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” included elsewhere in this prospectus.

Statement of Operations Data:

| | Nine Months Ended

September 30,

(unaudited) | | Year Ended December 31, | | Period from

August 21,

2002

(inception)

through

December 31, | |

($ in thousands, except per share data) | | 2005 | | 2005 | | 2004 | | 2004 | | 2004 | | 2003 | | 2002 | |

| | (pro forma) | | | | | | (pro forma) | | | | | | | |

| | | | | | | | (unaudited) | | | | | | | |

Revenues: | | | | | | | | | | | | | | | | | | | | | |

Rental income | | | $ | 36,341 | | | $ | 26,410 | | $ | 19,539 | | | $ | 47,560 | | | $ | 26,512 | | $ | 13,219 | | | $ | 1,863 | | |

| | | 36,341 | | | 26,410 | | 19,539 | | | 47,560 | | | 26,512 | | 13,219 | | | 1,863 | | |

Expenses: | | | | | | | | | | | | | | | | | | | | | |

Real estate taxes | | | 3,292 | | | 2,299 | | 1,285 | | | 4,195 | | | 1,752 | | 810 | | | 121 | | |

Insurance | | | 267 | | | 194 | | 129 | | | 526 | | | 168 | | 70 | | | 15 | | |

Property operating costs | | | 6,529 | | | 4,640 | | 3,006 | | | 8,763 | | | 4,391 | | 1,774 | | | 166 | | |

Management fees | | | — | | | 2,318 | | 1,502 | | | — | | | 2,030 | | 953 | | | 130 | | |

Depreciation and amortization | | | 12,244 | | | 8,188 | | 5,600 | | | 16,646 | | | 7,512 | | 3,355 | | | 384 | | |

General and administrative | | | 3,307 | | | 467 | | 716 | | | 4,409 | | | 914 | | 701 | | | 555 | | |

| | | 25,639 | | | 18,106 | | 12,238 | | | 34,539 | | | 16,767 | | 7,663 | | | 1,371 | | |

Operating income | | | 10,702 | | | 8,304 | | 7,301 | | | 13,021 | | | 9,745 | | 5,556 | | | 492 | | |

Other income and expense: | | | | | | | | | | | | | | | | | | | | | |

Interest income | | | 120 | | | 120 | | 34 | | | 50 | | | 50 | | 15 | | | 4 | | |

Interest expense | | | (8,347 | ) | | (13,871 | ) | (5,246 | ) | | (11,184 | ) | | (7,286 | ) | (3,707 | ) | | (611 | ) | |

Net income (loss) before minority interest | | | 2,475 | | | (5,447 | ) | 2,089 | | | 1,887 | | | 2,509 | | 1,864 | | | (115 | ) | |

Minority interest | | | (338 | ) | | — | | — | | | (258 | ) | | — | | — | | | — | | |

Net income (loss) | | | $ | 2,137 | | | $ | (5,447 | ) | $ | 2,089 | | | $ | 1,629 | | | $ | 2,509 | | $ | 1,864 | | | $ | (115 | ) | |

Pro forma earnings (loss) per share—basic and diluted | | | $ | 0.09 | | | — | | — | | | $ | 0.07 | | | — | | — | | | — | | |

Pro forma weighted average common shares outstanding—basic and diluted | | | 24,605,332 | | | — | | — | | | 24,605,332 | | | — | | — | | | — | | |

Funds From Operations Data: (1)

| | Nine Months Ended

September 30,

(unaudited) | | Year Ended December 31, | | Period from

August 21,

2002

(inception)

through

December 31, | |

($ in thousands) | | 2005 | | 2005 | | 2004 | | 2004 | | 2004 | | 2003 | | 2002 | |

| | (pro forma) | | | | | | (pro forma) | | | | | | | |

| | | | | | | | (unaudited) | | | | | | | |

Net income (loss) | | | $ | 2,137 | | | $ | (5,447 | ) | $ | 2,089 | | | $ | 1,629 | | | $ | 2,509 | | $ | 1,864 | | | $ | (115 | ) | | |

Plus: | | | | | | | | | | | | | | | | | | | | | | |

Real estate depreciation and amortization | | | 12,244 | | | 8,188 | | 5,600 | | | 16,646 | | | 7,512 | | 3,355 | | | 384 | | | |

Minority interest in operating partnership | | | 338 | | | — | | — | | | 258 | | | — | | — | | | — | | | |

Funds from operations | | | $ | 14,719 | | | $ | 2,741 | | $ | 7,689 | | | $ | 18,533 | | | $ | 10,021 | | $ | 5,219 | | | $ | 269 | | | |

(Footnote follows on next page)

21

Balance Sheet Data:

| | September 30, | | | | | | | |

| | (unaudited) | | December 31, | |

($ in thousands) | | 2005 | | 2005 | | 2004 | | 2003 | | 2002 | |

| | (pro forma) | | | | | | | | | |

Investments in real estate, net | | | $ | 444,332 | | | $ | 283,006 | | $ | 289,836 | | $ | 115,660 | | $ | 40,070 | |

Total assets | | | 492,331 | | | 312,564 | | 314,094 | | 125,260 | | 42,974 | |

Mortgage notes payable | | | 199,017 | | | 251,155 | | 256,250 | | 90,383 | | 31,218 | |

Minority interest(2) | | | 37,316 | | | — | | — | | — | | — | |