Table of Contents

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM6-K

REPORT OF FOREIGN PRIVATE ISSUER

PURSUANT TO RULE13a-16 OR15d-16

UNDER THE SECURITIES EXCHANGE ACT OF 1934

For the month of July 2019

Commission File Number001-33098

Mizuho Financial Group, Inc.

(Translation of registrant’s name into English)

5-5, Otemachi1-chome

Chiyoda-ku, Tokyo100-8176

Japan

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover ofForm 20-F orForm 40-F.Form 20-F ☒ Form 40-F ☐

Indicate by check mark if the registrant is submitting theForm 6-K in paper as permitted byRegulation S-T Rule 101(b)(1): ☐

Indicate by check mark if the registrant is submitting the Form6-K in paper as permitted byRegulation S-T Rule 101(b)(7): ☐

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant toRule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes ☐ No ☒

If “Yes” is marked, indicate below the file number assigned to the registrant in connection with Rule12g3-2(b):82- .

Table of Contents

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, the registrant has duly caused this report to be signed on its behalf by the undersigned, thereunto duly authorized.

| Date: | July 30, 2019 | |

| Mizuho Financial Group, Inc. | ||

| By: | /s/ Makoto Umemiya | |

| Name: | Makoto Umemiya | |

| Title: | Managing Executive Officer / Group CFO | |

Table of Contents

The following is the English translation of excerpt regarding the Basel Pillar 3 disclosures and the relevant information from our Japanese language disclosure material published in July 2019. The Japanese regulatory disclosure requirements are fulfilled with the Basel Pillar 3 disclosures and Japanese GAAP is applied to the relevant financial information. In this report, “we,” “us,” and “our” refer to Mizuho Financial Group, Inc. and, unless the context indicates otherwise, its consolidated subsidiaries. “Mizuho Financial Group” refers to Mizuho Financial Group, Inc.

| 2 | ||||

| 2 | ||||

Status of Mizuho Financial Group’s Consolidated Capital Adequacy | 3 | |||

| 3 | ||||

| 4 | ||||

| 13 | ||||

∎ Linkages between Financial Statements and Regulatory Exposures | 15 | |||

| 18 | ||||

| 37 | ||||

| 45 | ||||

| 52 | ||||

| 55 | ||||

| 55 | ||||

| 56 | ||||

| 57 | ||||

∎ Geographical distribution of credit exposures used in the countercyclical capital buffer | 59 | |||

∎ Indicators for Assessing Global Systemically Important Banks(G-SIBs) | 60 | |||

| 61 | ||||

| 61 | ||||

| 62 | ||||

| 62 | ||||

| 63 | ||||

| 63 | ||||

| 68 | ||||

| 68 | ||||

| 69 | ||||

| 72 | ||||

| 76 | ||||

| 77 | ||||

1

Table of Contents

Under the capital adequacy ratio regulations agreed upon by the Basel Committee on Banking Supervision, banks are required to meet certain minimum capital requirements. We calculate our capital adequacy ratio on a consolidated basis based on “the criteria used by a bank holding company for deciding whether or not the adequacy of equity capital of the bank holding company and its subsidiaries is appropriate in light of the assets owned by the bank holding company and its subsidiaries pursuant to Article52-25 of the Banking Law” (Financial Services Agency, or FSA, Notice No.20 issued in 2006).

We also calculate our leverage ratio on a consolidated basis according to “the criteria for evaluating the soundness of the leverage, prescribed as supplemental requirements of the criteria used by a bank holding company in deciding whether or not the adequacy of equity capital of the bank holding company and its subsidiaries is appropriate in light of the assets owned by the bank holding company and its subsidiaries, pursuant to Article52-25 of the Banking Law” (FSA Notice No.12 issued in 2019.)

Liquidity standards agreed upon by the Basel Committee on Banking Supervision require our liquidity coverage ratio to surpass certain minimum standards. We calculate our consolidated liquidity coverage ratio (the “Consolidated LCR”) in accordance with the regulation “The Evaluation Criterion on the Sound Management of Liquidity Risk Defined, Based on Banking Law Article52-25, as One of Criteria for Bank Holding Companies to Evaluate the Soundness of Their Management and the Ones of Their Subsidiaries and Others, which is also One of Evaluation Criteria on the Soundness of the Banks’ Management”(the FSA Notice No. 62 of 2014 (the “Notice No. 62”)).

KM1: Key Metrics

| (Millions of yen, except percentages) | ||||||||||||||||||||||

| Basel III Template No. | a | b | c | d | e | |||||||||||||||||

| As of March 31, 2019 | As of December 31, 2018 | As of September 30, 2018 | As of June 30, 2018 | As of March 31, 2018 | ||||||||||||||||||

Capital | ||||||||||||||||||||||

| 1 | Common Equity Tier 1 capital | 7,390,058 | 7,326,381 | 7,607,267 | 7,631,486 | 7,437,048 | ||||||||||||||||

| 2 | Tier 1 capital | 9,232,160 | 9,175,195 | 9,434,893 | 9,112,127 | 9,192,244 | ||||||||||||||||

| 3 | Total capital | 10,917,507 | 10,920,208 | 11,214,088 | 10,859,912 | 10,860,440 | ||||||||||||||||

Risk weighted assets | ||||||||||||||||||||||

| 4 | Risk weighted assets | 57,899,567 | 61,655,523 | 60,240,051 | 60,157,998 | 59,528,983 | ||||||||||||||||

Capital ratio | ||||||||||||||||||||||

| 5 | Common Equity Tier 1 capital ratio | 12.76 | % | 11.88 | % | 12.62 | % | 12.68 | % | 12.49 | % | |||||||||||

| 6 | Tier 1 capital ratio | 15.94 | % | 14.88 | % | 15.66 | % | 15.14 | % | 15.44 | % | |||||||||||

| 7 | Total capital ratio | 18.85 | % | 17.71 | % | 18.61 | % | 18.05 | % | 18.24 | % | |||||||||||

Capital buffer | ||||||||||||||||||||||

| 8 | Capital conservation buffer requirement | 2.50 | % | 1.87 | % | 1.87 | % | 1.87 | % | 1.87 | % | |||||||||||

| 9 | Countercyclical buffer requirement | 0.05 | % | 0.03 | % | 0.02 | % | 0.02 | % | 0.01 | % | |||||||||||

| 10 | BankG-SIB/D-SIB additional requirements | 1.00 | % | 0.75 | % | 0.75 | % | 0.75 | % | 0.75 | % | |||||||||||

| 11 | Total of bank CET1 specific buffer requirements | 3.55 | % | 2.65 | % | 2.64 | % | 2.64 | % | 2.63 | % | |||||||||||

| 12 | CET1 available after meeting the bank’s minimum capital requirements | 8.26 | % | 7.38 | % | 8.12 | % | 8.18 | % | 7.99 | % | |||||||||||

Leverage ratio | ||||||||||||||||||||||

| 13 | Total exposures | 208,557,401 | 209,483,123 | 216,920,174 | 217,040,028 | 214,277,824 | ||||||||||||||||

| 14 | Leverage ratio | 4.42 | % | 4.37 | % | 4.34 | % | 4.19 | % | 4.28 | % | |||||||||||

Liquidity coverage ratio (LCR) | ||||||||||||||||||||||

| 15 | Total HQLA allowed to be included in the calculation | 59,797,149 | 59,793,333 | 62,485,008 | 62,777,196 | 60,159,630 | ||||||||||||||||

| 16 | Net cash outflows | 41,447,805 | 41,184,048 | 48,045,874 | 51,729,447 | 50,079,075 | ||||||||||||||||

| 17 | LCR | 144.3 | % | 145.2 | % | 130.1 | % | 121.3 | % | 120.1 | % | |||||||||||

Note:

Base III Template No. from 15 to 17 are quarterly averages.

2

Table of Contents

Status of Mizuho Financial Group’s Consolidated Capital Adequacy

The information disclosed herein is in accordance with “Matters Separately Prescribed by the Commissioner of the Financial Services Agency Regarding Status of the Adequacy of Equity Capital Pursuant to Article19-2, Paragraph 1, Item 5, Subitem (d), etc. of the Ordinance for Enforcement of the Banking Law” (the FSA Notice No. 7 issued in 2014).

(1) Scope of Consolidation for Calculating Consolidated Capital Adequacy Ratio

(A) Difference from the companies included in the scope of consolidation based on consolidation rules for preparation of consolidated financial statements (the “scope of accounting consolidation”)

None as of March 31, 2018 and 2019

(B) Number of consolidated subsidiaries

| As of March 31, 2018 | As of March 31, 2019 | |||||||

Consolidated subsidiaries | 124 | 117 | ||||||

Our major consolidated subsidiaries are Mizuho Bank, Ltd., Mizuho Trust & Banking Co., Ltd. and Mizuho Securities Co., Ltd.

The following table sets forth information with respect to our principal consolidated subsidiaries as of March 31, 2019:

Name | Country of organization | Main business | Proportion of ownership interest (%) | Proportion of voting interest (%) | ||||||||

Domestic | ||||||||||||

Mizuho Bank, Ltd. | Japan | Banking | 100.0 | 100.0 | ||||||||

Mizuho Trust & Banking Co., Ltd. | Japan | Trust and banking | 100.0 | 100.0 | ||||||||

Mizuho Securities Co., Ltd. | Japan | Securities | 95.8 | 95.8 | ||||||||

Mizuho Research Institute Ltd. | Japan | Research and consulting | 98.6 | 98.6 | ||||||||

Mizuho Information & Research Institute, Inc. | Japan | Information technology | 91.5 | 91.5 | ||||||||

Asset Management One Co., Ltd. | Japan | Investment management | 70.0 | 51.0 | ||||||||

Mizuho Private Wealth Management Co., Ltd. | Japan | Consulting | 100.0 | 100.0 | ||||||||

Mizuho Credit Guarantee Co., Ltd. | Japan | Credit guarantee | 100.0 | 100.0 | ||||||||

Mizuho Realty Co., Ltd. | Japan | Real estate agency | 100.0 | 100.0 | ||||||||

Mizuho Factors, Limited | Japan | Factoring | 100.0 | 100.0 | ||||||||

Mizuho Realty One Co., Ltd. | Japan | Holding company | 100.0 | 100.0 | ||||||||

Defined Contribution Plan Services Co., Ltd. | Japan | Pension plan-related business | 60.0 | 60.0 | ||||||||

Mizuho-DL Financial Technology Co., Ltd. | Japan | Application and Sophistication of Financial Technology | 60.0 | 60.0 | ||||||||

UC Card Co., Ltd. | Japan | Credit card | 51.0 | 51.0 | ||||||||

J.Score CO., LTD. | Japan | Lending | 50.0 | 50.0 | ||||||||

Mizuho Trust Systems Company, Limited. | Japan | Subcontracted calculation services, software development | 50.0 | 50.0 | ||||||||

Mizuho Capital Co., Ltd. | Japan | Venture capital | 50.0 | 50.0 | ||||||||

Overseas | ||||||||||||

Mizuho Americas LLC | U.S.A. | Holding company | 100.0 | 100.0 | ||||||||

Mizuho Bank (China), Ltd. | China | Banking | 100.0 | 100.0 | ||||||||

Mizuho International plc | U.K. | Securities and banking | 100.0 | 100.0 | ||||||||

Mizuho Securities Asia Limited | China | Securities | 100.0 | 100.0 | ||||||||

Mizuho Securities USA LLC | U.S.A. | Securities | 100.0 | 100.0 | ||||||||

Mizuho Bank Europe N.V. | Netherlands | Banking and securities | 100.0 | 100.0 | ||||||||

Banco Mizuho do Brasil S.A. | Brazil | Banking | 100.0 | 100.0 | ||||||||

Mizuho Trust & Banking (Luxembourg) S.A. | Luxembourg | Trust and banking | 100.0 | 100.0 | ||||||||

Mizuho Bank (USA) | U.S.A. | Banking and trust | 100.0 | 100.0 | ||||||||

Mizuho Securities Europe GmbH | Germany | Securities | 100.0 | 100.0 | ||||||||

Mizuho Capital Markets LLC | U.S.A. | Derivatives | 100.0 | 100.0 | ||||||||

PT. Bank Mizuho Indonesia | Indonesia | Banking | 99.0 | 99.0 | ||||||||

(C) Corporations providing financial services for which Article 9 of the FSA Notice No. 20 is applicable

None as of March 31, 2018 and 2019.

3

Table of Contents

(D) Companies that are in the bank holding company’s corporate group but not included in the scope of accounting consolidation and companies that are not in the bank holding company’s corporate group but included in the scope of accounting consolidation

None as of March 31, 2018 and 2019.

(E) Restrictions on transfer of funds or capital within the bank holding company’s corporate group

None as of March 31, 2018 and 2019.

(F) Names of any other financial institutions, etc., classified as subsidiaries or other members of the bank holding company that are deficient in regulatory capital

None as of March 31, 2018 and 2019.

(1) Summary of Approach to Assessing Capital Adequacy

In order to ensure that risk-based capital is sufficiently maintained in light of the risk held by us, we regularly conduct the following assessment of capital adequacy in addition to adopting a suitable and effective capital adequacy monitoring structure.

Maintaining a sufficient BIS capital ratio

We confirm our maintenance of a high level of financial soundness by conducting regular evaluations to examine whether our risk-based capital is adequate in qualitative as well as quantitative terms, in light of our business plans and strategic targets to match the increase in risk-weighted assets acquired for growth, in addition to maintaining our capital above the minimum requirements of common equity Tier 1 capital ratio, Tier 1 capital ratio, total capital ratio, capital buffer ratio, adequate leverage ratio and TLAC ratio.

Balancing risk and capital

On the basis of the framework for allocating risk capital, after obtaining the clearest possible grasp of the group’s overall risk exposure, we endeavor to control risk so as to keep it within the range of our business capacity by means of allocating capital that corresponds to the amount of risk to the principal banking subsidiaries, etc., within the bounds of our capital, and we conduct regular assessments to ensure that a sufficient level of capital is maintained for our risk profile. When making these assessments, we calculate the potential losses arising from assumed stress events and risk volumes, which we assess whether they balance with the group’s capital. Stress events are based on risk scenarios that are formulated based on the current economic condition and the economic outlook, etc. In addition, we examine whether an appropriate return on risk is maintained in the assessments.

4

Table of Contents

(2) Composition of Capital, etc.

(A) CC1: Composition of Capital Disclosure

| (Millions of yen, except percentage) | ||||||||||||||||||

| a | b | c | ||||||||||||||||

Basel III Template | As of March 31, 2018 | As of March 31, 2019 | Reference to Template CC2 | |||||||||||||||

Common Equity Tier 1 capital: instruments and reserves | (1) | |||||||||||||||||

| 1a+2-1c-26 | Directly issued qualifying common share capital plus related stock surplus and retained earnings | 7,292,638 | 7,207,427 | |||||||||||||||

| 1a | of which: capital and stock surplus | 3,391,471 | 3,395,217 | |||||||||||||||

| 2 | of which: retained earnings | 4,002,350 | 3,915,111 | |||||||||||||||

| 1c | of which: treasury stock (-) | 5,997 | 7,703 | |||||||||||||||

| 26 | of which: national specific regulatory adjustments (earnings to be distributed) (-) | 95,186 | 95,197 | |||||||||||||||

of which: other than above | — | — | ||||||||||||||||

| 1b | Subscription rights to common shares | 1,163 | 707 | |||||||||||||||

| 3 | Accumulated other comprehensive income and other disclosed reserves | 1,677,534 | 1,445,770 | (a | ) | |||||||||||||

| 5 | Common share capital issued by subsidiaries and held by third parties (amount allowed in group CET1) | 14,344 | 6,460 | |||||||||||||||

| 6 | Common Equity Tier 1 capital: instruments and reserves | (A) | 8,985,680 | 8,660,365 | ||||||||||||||

Common Equity Tier 1 capital: regulatory adjustments | (2) | |||||||||||||||||

| 8+9 | Total intangible assets (net of related tax liability, excluding those relating to mortgage servicing rights) | 794,953 | 459,991 | |||||||||||||||

| 8 | of which: goodwill (net of related tax liability, including those equivalent) | 85,103 | 73,003 | |||||||||||||||

| 9 | of which: other intangibles other than goodwill and mortgage servicing rights (net of related tax liability) | 709,850 | 386,987 | |||||||||||||||

| 10 | Deferred tax assets that rely on future profitability excluding those arising from temporary differences (net of related tax liability) | 42,352 | 36,566 | |||||||||||||||

| 11 | Deferred gains or losses on derivatives under hedge accounting | (67,578 | ) | (22,282 | ) | |||||||||||||

| 12 | Shortfall of eligible provisions to expected losses | 61,964 | 96,090 | |||||||||||||||

| 13 | Securitization gain on sale | — | — | |||||||||||||||

| 14 | Gains and losses due to changes in own credit risk on fair valued liabilities | 3,960 | 13,006 | |||||||||||||||

| 15 | Net defined benefit asset | 691,380 | 682,142 | |||||||||||||||

| 16 | Investments in own shares (excluding those reported in the net assets section) | 1,457 | 4,792 | |||||||||||||||

| 17 | Reciprocal cross-holdings in common equity | — | — | |||||||||||||||

| 18 | Investments in the capital of banking, financial and insurance entities that are outside the scope of regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above the 10% threshold) | 20,140 | — | |||||||||||||||

| 19+20+21 | Amount exceeding the 10% threshold on specified items | — | — | |||||||||||||||

| 19 | of which: significant investments in the common stock of financials | — | — | |||||||||||||||

| 20 | of which: mortgage servicing rights | — | — | |||||||||||||||

| 21 | of which: deferred tax assets arising from temporary differences (net of related tax liability) | — | — | |||||||||||||||

| 22 | Amount exceeding the 15% threshold on specified items | — | — | |||||||||||||||

| 23 | of which: significant investments in the common stock of financials | — | — | |||||||||||||||

| 24 | of which: mortgage servicing rights | — | — | |||||||||||||||

| 25 | of which: deferred tax assets arising from temporary differences (net of related tax liability) | — | — | |||||||||||||||

| 27 | Regulatory adjustments applied to Common Equity Tier 1 due to insufficient Additional Tier 1 and Tier 2 to cover deductions | — | — | |||||||||||||||

| 28 | Common Equity Tier 1 capital: regulatory adjustments | (B) | 1,548,631 | 1,270,307 | ||||||||||||||

Common Equity Tier 1 capital (CET1) | ||||||||||||||||||

| 29 | Common Equity Tier 1 capital (CET1) ((A)-(B)) | (C) | 7,437,048 | 7,390,058 | ||||||||||||||

Additional Tier 1 capital: instruments | (3) | |||||||||||||||||

5

Table of Contents

| 30 31a | Directly issued qualifying Additional Tier 1 instruments plus related stock surplus of which: classified as equity under applicable accounting standards and the breakdown | — | — | |||||||||||||||

| 30 31b | Subscription rights to Additional Tier 1 instruments | — | — | |||||||||||||||

| 30 32 | Directly issued qualifying Additional Tier 1 instruments plus related stock surplus of which: classified as liabilities under applicable accounting standards | 1,220,000 | 1,570,000 | |||||||||||||||

| 30 | Qualifying Additional Tier 1 instruments plus related stock surplus issued by special purpose vehicles and other equivalent entities | — | — | |||||||||||||||

| 34-35 | Additional Tier 1 instruments issued by subsidiaries and held by third parties (amount allowed in group AT1) | 31,317 | 28,502 | |||||||||||||||

| 33+35 | Eligible Tier 1 capital instruments subject tophase-out arrangements included in Additional Tier 1 capital: instruments | 577,500 | 303,000 | |||||||||||||||

| 33 | of which: directly issued capital instruments subject to phase out from Additional Tier 1 | 577,500 | 303,000 | |||||||||||||||

| 35 | of which: instruments issued by subsidiaries subject to phase out | — | — | |||||||||||||||

| 36 | Additional Tier 1 capital: instruments | (D) | 1,828,817 | 1,901,502 | ||||||||||||||

Additional Tier 1 capital: regulatory adjustments | ||||||||||||||||||

| 37 | Investments in own Additional Tier 1 instruments | — | 2,900 | |||||||||||||||

| 38 | Reciprocal cross-holdings in Additional Tier 1 instruments | — | — | |||||||||||||||

| 39

| Investments in the capital of banking, financial and insurance entities that are outside the scope of regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above 10% threshold) | 121 | — | |||||||||||||||

| 40 | Significant investments in the capital of banking, financial and insurance entities that are outside the scope of regulatory consolidation (net of eligible short positions) | 73,500 | 56,500 | |||||||||||||||

| 42 | Regulatory adjustments applied to Additional Tier 1 due to insufficient Tier 2 to cover deductions | — | — | |||||||||||||||

| 43 | Additional Tier 1 capital: regulatory adjustments | (E) | 73,621 | 59,400 | ||||||||||||||

Additional Tier 1 capital (AT1) | ||||||||||||||||||

| 44 | Additional Tier 1 capital ((D)-(E)) | (F) | 1,755,195 | 1,842,102 | ||||||||||||||

Tier 1 capital (T1 = CET1 + AT1) | ||||||||||||||||||

| 45 | Tier 1 capital (T1 = CET1 + AT1) ((C) + (F)) | (G) | 9,192,244 | 9,232,160 | ||||||||||||||

Tier 2 capital: instruments and provisions | (4) | |||||||||||||||||

| 46 | Directly issued qualifying Tier 2 instruments plus related stock surplus of which: classified as equity under applicable accounting standards and the breakdown | — | — | |||||||||||||||

| 46 | Subscription rights to Tier 2 instruments | — | — | |||||||||||||||

| 46 | Directly issued qualifying Tier 2 instruments plus related stock surplus of which: classified as liabilities under applicable accounting standards | 828,702 | 1,002,257 | |||||||||||||||

| 46 | Tier 2 instruments plus related stock surplus issued by special purpose vehicles and other equivalent entities | 159,405 | 166,150 | |||||||||||||||

| 48-49 | Tier 2 instruments issued by subsidiaries and held by third parties (amount allowed in group Tier 2) | 10,378 | 7,777 | |||||||||||||||

| 47+49 | Eligible Tier 2 capital instruments subject tophase-out arrangements included in Tier 2:instruments and provisions | 674,824 | 506,118 | |||||||||||||||

| 47 | of which: directly issued capital instruments subject to phase out from Tier 2 | 135,135 | 102,237 | |||||||||||||||

| 49 | of which: instruments issued by subsidiaries subject to phase out | 539,688 | 403,880 | |||||||||||||||

| 50 | Total of general allowance for loan losses and eligible provisions included in Tier 2 | 4,794 | 4,377 | |||||||||||||||

| 50a | of which: general allowance for loan losses | 4,794 | 4,377 | |||||||||||||||

| 50b | of which: eligible provisions | — | — | |||||||||||||||

| 51 | Tier 2 capital: instruments and provisions | (H) | 1,678,105 | 1,686,680 | ||||||||||||||

Tier 2 capital: regulatory adjustments | (5) | |||||||||||||||||

| 52 | Investments in own Tier 2 instruments | 1,892 | 1,333 | |||||||||||||||

| 53 | Reciprocal cross-holdings in Tier 2 instruments and other TLAC liabilities | — | — | |||||||||||||||

| 54 | Investments in the capital and other TLAC liabilities of banking, financial and insurance entities that are outside the scope of regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued common share capital of the entity (amount above the 10% threshold) | 8,016 | — | |||||||||||||||

6

Table of Contents

| 54a | Investments in the other TLAC liabilities of banking, financial and insurance entities that are outside the scope of regulatory consolidation, where the bank does not own more than 10% of the issued common share capital of the entity: amount previously designated for the 5% threshold but that no longer meets the conditions | / | — | |||||||||||||||

| 55 | Significant investments in the capital and other TLAC liabilities of banking, financial and insurance entities that are outside the scope of regulatory consolidation (net of eligible short positions) | — | — | |||||||||||||||

| 57 | Tier 2 capital: regulatory adjustments | (I) | 9,908 | 1,333 | ||||||||||||||

Tier 2 capital (T2) | ||||||||||||||||||

| 58 | Tier 2 capital (T2) ((H)-(I)) | (J) | 1,668,196 | 1,685,347 | ||||||||||||||

Total capital (TC = T1 + T2) | ||||||||||||||||||

| 59 | Total capital (TC = T1 + T2) ((G) + (J)) | (K) | 10,860,440 | 10,917,507 | ||||||||||||||

Risk weighted assets | (6) | |||||||||||||||||

| 60 | Risk weighted assets | (L) | 59,528,983 | 57,899,567 | ||||||||||||||

Capital ratio and buffers (consolidated) | (7) | |||||||||||||||||

| 61 | Common Equity Tier 1 capital ratio (consolidated) ((C)/(L)) | 12.49 | % | 12.76 | % | |||||||||||||

| 62 | Tier 1 capital ratio (consolidated) ((G)/(L)) | 15.44 | % | 15.94 | % | |||||||||||||

| 63 | Total capital ratio (consolidated) ((K)/(L)) | 18.24 | % | 18.85 | % | |||||||||||||

| 64 | Total of bank CET1 specific buffer requirements | 2.63 | % | 3.55 | % | |||||||||||||

| 65 | of which: capital conservation buffer requirement | 1.87 | % | 2.50 | % | |||||||||||||

| 66 | of which: countercyclical buffer requirement | 0.01 | % | 0.05 | % | |||||||||||||

| 67 | of which: bankG-SIB/D-SIB additional requirements | 0.75 | % | 1.00 | % | |||||||||||||

| 68 | CET1 available after meeting the bank’s minimum capital requirements | 7.99 | % | 8.26 | % | |||||||||||||

Regulatory adjustments | (8) | |||||||||||||||||

| 72 | Non-significant investments in the capital and other TLAC liabilities of other financials that are below the thresholds for deduction (before risk weighting) | 745,717 | 540,695 | |||||||||||||||

| 73 | Significant investments in the common stock of financials that are below the thresholds for deduction (before risk weighting) | 142,407 | 250,095 | |||||||||||||||

| 74 | Mortgage servicing rights that are below the thresholds for deduction (before risk weighting) | — | — | |||||||||||||||

| 75 | Deferred tax assets arising from temporary differences that are below the thresholds for deduction (before risk weighting) | 185,172 | 233,628 | |||||||||||||||

Provisions included in Tier 2 capital: instruments and provisions | (9) | |||||||||||||||||

| 76 | Provisions (general allowance for loan losses) | 4,794 | 4,377 | |||||||||||||||

| 77 | Cap on inclusion of provisions (general allowance for loan losses) | 43,678 | 43,521 | |||||||||||||||

| 78 | Provisions eligible for inclusion in Tier 2 in respect of exposures subject to internal ratings-based approach (prior to application of cap) (if the amount is negative, report as “nil”) | — | — | |||||||||||||||

| 79 | Cap for inclusion of provisions in Tier 2 under internal ratings-based approach | 284,521 | 278,991 | |||||||||||||||

Capital instruments subject tophase-out arrangements | (10) | |||||||||||||||||

| 82 | Current cap on AT1 instruments subject tophase-out arrangements | 833,255 | 624,941 | |||||||||||||||

| 83 | Amount excluded from AT1 due to cap (excess over cap after redemptions and maturities) (if the amount is negative, report as “nil”) | — | — | |||||||||||||||

| 84 | Current cap on T2 instruments subject tophase-out arrangements | 674,824 | 506,118 | |||||||||||||||

| 85 | Amount excluded from T2 due to cap (excess over cap after redemptions and maturities) (if the amount is negative, report as “nil”) | 7,304 | 37,812 | |||||||||||||||

Notes: | ||

1. | The above figures are calculated based on the international standard applied on a consolidated basis under the FSA Notice No. 20. | |

2. | As an external audit of calculating the consolidated capital adequacy ratio, we underwent an examination under the procedures agreed with by Ernst & Young ShinNihon LLC, on the basis of “Practical guidance on agreed-upon procedures for the calculation of capital adequacy ratio” (Practical Guideline for specialized fields No. 4465 of the Japanese Institute of Certified Public Accountants). Note that this examination is not a part of the audit performed on our consolidated financial statements or internal controls over financial reporting. Ernst & Young ShinNihon LLC does not give its opinion or conclusion concerning the capital adequacy ratio or our internal control structure regarding the calculation of the capital adequacy ratio. Instead, it performs an examination to the extent both of us agreed to and reports the results to us. | |

7

Table of Contents

(B) CC2:Reconciliation of regulatory capital to consolidated balance sheet

| (Millions of yen) | ||||||||||||||

Items | a | b | c | d | ||||||||||

| Consolidated balance sheet as in published financial statements | Consolidated balance sheet as in published financial statements | Reference to Template CC1 | Cross-reference to Appended template | |||||||||||

| As of March 31, 2018 | As of March 31, 2019 | |||||||||||||

(Assets) | ||||||||||||||

Cash and Due from Banks | 47,725,360 | 45,108,602 | ||||||||||||

Call Loans and Bills Purchased | 715,149 | 648,254 | ||||||||||||

Receivables under Resale Agreements | 8,080,873 | 12,997,628 | ||||||||||||

Guarantee Deposits Paid under Securities Borrowing Transactions | 4,350,527 | 2,578,133 | ||||||||||||

Other Debt Purchased | 2,713,742 | 2,828,959 | ||||||||||||

Trading Assets | 10,507,133 | 12,043,608 | 6-a | |||||||||||

Money Held in Trust | 337,429 | 351,889 | ||||||||||||

Securities | 34,183,033 | 29,774,489 | 2-b,6-b | |||||||||||

Loans and Bills Discounted | 79,421,473 | 78,456,935 | 6-c | |||||||||||

Foreign Exchange Assets | 1,941,677 | 1,993,668 | ||||||||||||

Derivatives other than for Trading Assets | 1,807,999 | 1,328,227 | 6-d | |||||||||||

Other Assets | 4,588,484 | 4,229,589 | 6-e | |||||||||||

Tangible Fixed Assets | 1,111,128 | 1,037,006 | ||||||||||||

Intangible Fixed Assets | 1,092,708 | 620,231 | 2-a | |||||||||||

Net Defined Benefit Asset | 996,173 | 982,804 | 3 | |||||||||||

Deferred Tax Assets | 47,839 | 37,960 | 4-a | |||||||||||

Customers’ Liabilities for Acceptances and Guarantees | 5,723,186 | 6,062,053 | ||||||||||||

Reserves for Possible Losses on Loans | (315,621 | ) | (287,815 | ) | ||||||||||

|

|

|

| |||||||||||

Total Assets | 205,028,300 | 200,792,226 | ||||||||||||

|

|

|

| |||||||||||

(Liabilities) | ||||||||||||||

Deposits | 125,081,233 | 124,311,025 | ||||||||||||

Negotiable Certificates of Deposit | 11,382,590 | 13,338,571 | ||||||||||||

Call Money and Bills Sold | 2,105,293 | 2,841,931 | ||||||||||||

Payables under Repurchase Agreements | 16,656,828 | 14,640,439 | ||||||||||||

Guarantee Deposits Received under Securities Lending Transactions | 1,566,833 | 1,484,584 | ||||||||||||

Commercial Paper | 710,391 | 941,181 | ||||||||||||

Trading Liabilities | 8,121,543 | 8,325,520 | 6-f | |||||||||||

Borrowed Money | 4,896,218 | 3,061,504 | 8-a | |||||||||||

Foreign Exchange Liabilities | 445,804 | 669,578 | ||||||||||||

Short-term Bonds | 362,185 | 355,539 | ||||||||||||

Bonds and Notes | 7,544,256 | 8,351,071 | 8-b | |||||||||||

Due to Trust Accounts | 4,733,131 | 1,102,073 | ||||||||||||

Derivatives other than for Trading Liabilities | 1,514,483 | 1,165,602 | 6-g | |||||||||||

Other Liabilities | 3,685,585 | 4,512,325 | ||||||||||||

Reserve for Bonus Payments | 66,872 | 68,117 | ||||||||||||

Reserve for Variable Compensation | 3,242 | 2,867 | ||||||||||||

Net Defined Benefit Liability | 58,890 | 60,873 | ||||||||||||

Reserve for Director and Corporate Auditor Retirement Benefits | 1,460 | 1,389 | ||||||||||||

Reserve for Possible Losses on Sales of Loans | 1,075 | 630 | ||||||||||||

Reserve for Contingencies | 5,622 | 4,910 | ||||||||||||

Reserve for Reimbursement of Deposits | 20,011 | 19,068 | ||||||||||||

Reserve for Reimbursement of Debentures | 30,760 | 25,566 | ||||||||||||

Reserves under Special Laws | 2,361 | 2,473 | ||||||||||||

Deferred Tax Liabilities | 421,002 | 185,974 | 4-b | |||||||||||

Deferred Tax Liabilities for Revaluation Reserve for Land | 66,186 | 63,315 | 4-c | |||||||||||

Acceptances and Guarantees | 5,723,186 | 6,062,053 | ||||||||||||

|

|

|

| |||||||||||

Total Liabilities | 195,207,054 | 191,598,188 | ||||||||||||

|

|

|

| |||||||||||

8

Table of Contents

(Net Assets) | ||||||||||||||

Common Stock | 2,256,548 | 2,256,767 | 1-a | |||||||||||

Capital Surplus | 1,134,922 | 1,138,449 | 1-b | |||||||||||

Retained Earnings | 4,002,835 | 3,915,521 | 1-c | |||||||||||

Treasury Stock | (5,997 | ) | (7,703 | ) | 1-d | |||||||||

|

|

|

| |||||||||||

Total Shareholders’ Equity | 7,388,309 | 7,303,034 | ||||||||||||

|

|

|

| |||||||||||

Net Unrealized Gains (Losses) on Other Securities | 1,392,392 | 1,186,401 | ||||||||||||

Deferred Gains or Losses on Hedges | (67,578 | ) | (22,282 | ) | 5 | |||||||||

Revaluation Reserve for Land | 144,277 | 137,772 | ||||||||||||

Foreign Currency Translation Adjustments | (85,094 | ) | (111,057 | ) | ||||||||||

Remeasurements of Defined Benefit Plans | 293,536 | 254,936 | ||||||||||||

|

|

|

| |||||||||||

Total Accumulated Other Comprehensive Income | 1,677,534 | 1,445,770 | (a) | |||||||||||

|

|

|

| |||||||||||

Stock Acquisition Rights | 1,163 | 707 | ||||||||||||

Non-Controlling Interests | 754,239 | 444,525 | 7 | |||||||||||

|

|

|

| |||||||||||

Total Net Assets | 9,821,246 | 9,194,038 | ||||||||||||

|

|

|

| |||||||||||

Total Liabilities and Net Assets | 205,028,300 | 200,792,226 | ||||||||||||

|

|

|

| |||||||||||

Note:

The regulatory scope of consolidation is the same as the accounting scope of consolidation.

Appended template

1. Shareholders’ equity

(1) Consolidated balance sheet

(Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

1-a | Common stock | 2,256,548 | 2,256,767 | |||||||||

1-b | Capital surplus | 1,134,922 | 1,138,449 | |||||||||

1-c | Retained earnings | 4,002,835 | 3,915,521 | |||||||||

1-d | Treasury stock | (5,997 | ) | (7,703 | ) | |||||||

| Total shareholders’ equity | 7,388,309 | 7,303,034 | ||||||||||

(2) Composition of capital | ||||||||||||

Basel III | (Millions of yen) | |||||||||||

Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | |||||||||

| Directly issued qualifying common share capital plus related stock surplus and retained earnings | 7,387,824 | 7,302,625 | Shareholders’ equity attributable to common shares (before adjusting national specific regulatory adjustments (earnings to be distributed)) | ||||||||

1a | of which: capital and stock surplus | 3,391,471 | 3,395,217 | |||||||||

2 | of which: retained earnings | 4,002,350 | 3,915,111 | |||||||||

1c | of which: treasury stock (-) | 5,997 | 7,703 | |||||||||

of which: other than above | — | — | ||||||||||

31a | Directly issued qualifying additional Tier 1 instruments plus related stock surplus of which: classified as equity under applicable accounting standards and the breakdown | — | — | |||||||||

2. Intangible fixed assets | ||||||||||||

(1) Consolidated balance sheet | ||||||||||||

| (Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

2-a | Intangible fixed assets | 1,092,708 | 620,231 | |||||||||

2-b | Securities | 34,183,033 | 29,774,489 | |||||||||

of which: share of goodwill of companies accounted for using the equity method | 14,588 | 7,508 | Share of goodwill of companies accounted for using the equity method | |||||||||

| Income taxes related to above | (312,342 | ) | (167,749 | ) | |||||||

9

Table of Contents

(2) Composition of capital | ||||||||||||

| Basel III | (Millions of yen) | |||||||||||

template | Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

| 8 | Goodwill (net of related tax liability, including those equivalent) | 85,103 | 73,003 | |||||||||

| 9 | Other intangibles other than goodwill and mortgage servicing rights (net of related tax liability) | 709,850 | 386,987 | Software and other | ||||||||

Mortgage servicing rights (net of related tax liability) | — | — | ||||||||||

| 20 | Amount exceeding the 10% threshold on specified items | — | — | |||||||||

| 24 | Amount exceeding the 15% threshold on specified items | — | — | |||||||||

| 74 | Mortgage servicing rights that are below the thresholds for deduction (before risk weighting) | — | — | |||||||||

3. Net defined benefit asset | ||||||||||||

(1) Consolidated balance sheet

| ||||||||||||

(Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

3 | Net defined benefit asset | 996,173 | 982,804 | |||||||||

Income taxes related to above | (304,793 | ) | (300,661 | ) | ||||||||

(2) Composition of capital

| ||||||||||||

Basel III | Composition of capital disclosure | (Millions of yen) | ||||||||||

As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||||

| 15 | Net defined benefit asset | 691,380 | 682,142 | |||||||||

4. Deferred tax assets

| ||||||||||||

(1) Consolidated balance sheet

| ||||||||||||

(Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

| 4-a | Deferred tax assets | 47,839 | 37,960 | |||||||||

| 4-b | Deferred tax liabilities | 421,002 | 185,974 | |||||||||

| 4-c | Deferred tax liabilities for revaluation reserve for land | 66,186 | 63,315 | |||||||||

Tax effects on intangible fixed assets | 312,342 | 167,749 | ||||||||||

Tax effects on net defined benefit asset | 304,793 | 300,661 | ||||||||||

(2) Composition of capital

| ||||||||||||

| Basel III | (Millions of yen) | |||||||||||

template | Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

| 10 | Deferred tax assets that rely on future profitability excluding those arising from temporary differences (net of related tax liability) | 42,352 | 36,566 | This item does not agree with the amount reported on the consolidated balance sheet due to offsetting of assets and liabilities. | ||||||||

Deferred tax assets that rely on future profitability arising from temporary differences (net of related tax liability) | 185,172 | 233,628 | This item does not agree with the amount reported on the consolidated balance sheet due to offsetting of assets and liabilities. | |||||||||

| 21 | Amount exceeding the 10% threshold on specified items | — | — | |||||||||

| 25 | Amount exceeding the 15% threshold on specified items | — | — | |||||||||

| 75 | Deferred tax assets arising from temporary differences that are below the thresholds for deduction (before risk weighting) | 185,172 | 233,628 | |||||||||

10

Table of Contents

5. Deferred gains or losses on derivatives under hedge accounting

(1) Consolidated balance sheet |

| (Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

| 5 | Deferred gains or losses on hedges | (67,578 | ) | (22,282 | ) | |||||||

(2) Composition of capital |

| |||||||||||

Basel III template | (Millions of yen) | |||||||||||

Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | |||||||||

11

| Deferred gains or losses on derivatives under hedge accounting | (67,578 | ) | (22,282 | ) | |||||||

6. Items associated with investments in the capital of financial institutions

(1) Consolidated balance sheet |

| (Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

6-a | Trading assets | 10,507,133 | 12,043,608 | Including trading account securities and derivatives for trading assets | ||||||||

6-b | Securities | 34,183,033 | 29,774,489 | |||||||||

6-c | Loans and bills discounted | 79,421,473 | 78,456,935 | Including subordinated loans | ||||||||

6-d | Derivatives other than for trading assets | 1,807,999 | 1,328,227 | |||||||||

6-e | Other assets | 4,588,484 | 4,229,589 | Including money invested | ||||||||

6-f | Trading liabilities | 8,121,543 | 8,325,520 | Including trading account securities sold | ||||||||

6-g | Derivatives other than for trading liabilities | 1,514,483 | 1,165,602 | |||||||||

(2) Composition of capital |

| |||||||||||

Basel III template | (Millions of yen) | |||||||||||

Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | |||||||||

Investments in own capital instruments | 3,349 | 9,026 | ||||||||||

16 | Common equity Tier 1 capital | 1,457 | 4,792 | |||||||||

37 | Additional Tier 1 capital | — | 2,900 | |||||||||

52 | Tier 2 capital | 1,892 | 1,333 | |||||||||

Reciprocal cross-holdings in the capital of banking, financial and insurance entities | — | — | ||||||||||

17 | Common equity Tier 1 capital | — | — | |||||||||

38 | Additional Tier 1 capital | — | — | |||||||||

53 | Tier 2 capital and other TLAC liabilities | — | — | |||||||||

Investments in the capital of banking, financial and insurance entities that are outside the scope of regulatory consolidation, net of eligible short positions, where the bank does not own more than 10% of the issued share capital (amount above 10% threshold) | 773,996 | 540,695 | ||||||||||

18 | Common equity Tier 1 capital | 20,140 | — | |||||||||

39 | Additional Tier 1 capital | 121 | — | |||||||||

54 | Tier 2 capital and other TLAC liabilities | 8,016 | — | |||||||||

72 | Non-significant investments in the capital and other TLAC liabilities of other financials that are below the thresholds for deduction (before risk weighting) | 745,717 | 540,695 | |||||||||

Significant investments in the capital of banking, financial and insurance entities that are outside the scope of regulatory consolidation, net of eligible short positions | 215,907 | 306,595 | ||||||||||

19 | Amount exceeding the 10% threshold on specified items | — | — | |||||||||

23 | Amount exceeding the 15% threshold on specified items | — | — | |||||||||

40 | Additional Tier 1 capital | 73,500 | 56,500 | |||||||||

55 | Tier 2 capital and other TLAC liabilities | — | — | |||||||||

73 | Significant investments in the common stock of financials that are below the thresholds for deduction (before risk weighting) | 142,407 | 250,095 | |||||||||

11

Table of Contents

7.Non-Controlling interests

| ||||||||||||

(1) Consolidated balance sheet

| ||||||||||||

| (Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

7 | Non-Controlling interests | 754,239 | 444,525 | |||||||||

(2) Composition of capital

| ||||||||||||

| Basel III | (Millions of yen) | |||||||||||

template | Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

5 | Common share capital issued by subsidiaries and held by third parties (amount allowed in group CET1) | 14,344 | 6,460 | After reflecting amounts eligible for inclusion(non-controlling interest after adjustments) | ||||||||

30- 31ab-32 | Qualifying additional Tier 1 instruments plus related stock surplus issued by special purpose vehicles and other equivalent entities | — | — | After reflecting amounts eligible for inclusion(non-controlling interest after adjustments) | ||||||||

34-35 | Additional Tier 1 instruments issued by subsidiaries and held by third parties (amount allowed in group AT1) | 31,317 | 28,502 | After reflecting amounts eligible for inclusion(non-controlling interest after adjustments) | ||||||||

46 | Tier 2 instruments plus related stock surplus issued by special purpose vehicles and other equivalent entities | 159,405 | 166,150 | After reflecting amounts eligible for inclusion(non-controlling interest after adjustments) | ||||||||

48-49 | Tier 2 instruments issued by subsidiaries and held by third parties (amount allowed in group Tier 2) | 10,378 | 7,777 | After reflecting amounts eligible for inclusion(non-controlling interest after adjustments) | ||||||||

8. Other capital instruments

| ||||||||||||

(1) Consolidated balance sheet

| ||||||||||||

| (Millions of yen) | ||||||||||||

Ref. | Consolidated balance sheet items | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

8-a | Borrowed money | 4,896,218 | 3,061,504 | |||||||||

8-b | Bonds and notes | 7,544,256 | 8,351,071 | |||||||||

Total | 12,440,475 | 11,412,575 | ||||||||||

(2) Composition of capital

| ||||||||||||

| Basel III | (Millions of yen) | |||||||||||

template | Composition of capital disclosure | As of March 31, 2018 | As of March 31, 2019 | Remarks | ||||||||

32 | Directly issued qualifying additional Tier 1 instruments plus related stock surplus of which: classified as liabilities under applicable accounting standards | 1,220,000 | 1,570,000 | |||||||||

46 | Directly issued qualifying Tier 2 instruments plus related stock surplus of which: classified as liabilities under applicable accounting standards | 828,702 | 1,002,257 | |||||||||

12

Table of Contents

∎ Summary of Risk Management and Risk-weighted Assets (RWA)

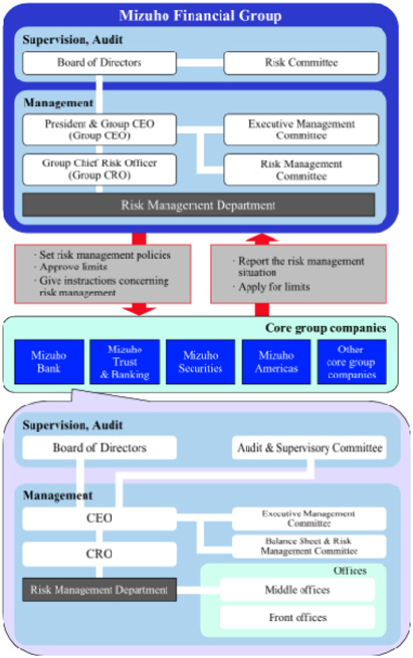

(1) Summary of Our Group’s Risk Profile, Risk Management Policies/ Procedures and Structure

See page 68 for a summary of our group’s risk profile and risk management policies, etc.

(2) Summary of RWA

(A) OV1: Overview of Risk-weighted Assets (RWA)

| (Millions of yen) | ||||||||||||||||||

| a | b | c | d | |||||||||||||||

| RWA | Capital requirements | |||||||||||||||||

| Basel III Template No. | As of March 31, 2019 | As of March 31, 2018 | As of March 31, 2019 | As of March 31, 2018 | ||||||||||||||

| 1 | Credit risk (excluding counterparty credit risk) | 37,656,623 | 38,823,030 | 3,177,419 | 3,275,858 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 2 | of which: standardized approach (SA) | 1,738,523 | 1,820,063 | 139,081 | 145,605 | |||||||||||||

| 3 | of which: internal rating-based (IRB) approach | 34,352,032 | 35,420,038 | 2,913,052 | 3,003,619 | |||||||||||||

of which: significant investments | — | — | — | — | ||||||||||||||

of which: estimated residual value of lease transactions | — | — | — | — | ||||||||||||||

others | 1,566,067 | 1,582,929 | 125,285 | 126,634 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 4 | Counterparty credit risk (CCR) | 4,491,743 | 4,531,171 | 364,208 | 366,994 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 5 | of which:SA-CCR | — | — | — | — | |||||||||||||

of which: current exposure method | 139,720 | 216,424 | 11,518 | 17,723 | ||||||||||||||

| 6 | of which: expected positive exposure (EPE) method | 878,845 | 887,843 | 73,961 | 74,632 | |||||||||||||

of which: credit valuation adjustment (CVA) risk | 2,457,535 | 2,539,780 | 196,602 | 203,182 | ||||||||||||||

of which: central counterparty-related | 190,997 | 193,088 | 15,279 | 15,447 | ||||||||||||||

Others | 824,644 | 694,035 | 66,846 | 56,009 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 7 | Equity positions in banking book under market-based approach | 2,492,949 | 2,972,073 | 211,402 | 252,031 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 8 | Equity investments in funds–Look-through approach | 2,620,615 | / | 220,993 | / | |||||||||||||

| 9 | Equity investments in funds–Mandate-based approach | — | / | — | / | |||||||||||||

Equity investments in funds–Simple approach (subject to 250% RW) | — | / | — | / | ||||||||||||||

Equity investments in funds–Simple approach (subject to 400% RW) | 598,267 | / | 50,733 | / | ||||||||||||||

| 10 | Equity investments in funds–Fall-back approach | 19,489 | / | 1,563 | / | |||||||||||||

Fund exposures–standardized approach | / | — | / | — | ||||||||||||||

Fund exposures–regarded method | / | 3,515,582 | / | 297,289 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 11 | Settlement risk | 2,705 | 4,574 | 229 | 386 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 12 | Securitization exposures in banking book | 1,050,204 | 379,016 | 84,016 | 32,003 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 13 | of which: Securitisation IRB approach(SEC-IRBA) or internal assessment approach(IAA) | 735,081 | / | 58,806 | / | |||||||||||||

| 14 | of which: Securitisation external ratings-based approach(SEC-ERBA) | 304,189 | / | 24,335 | / | |||||||||||||

| 15 | of which: Securitisation standardised approach(SEC-SA) | — | / | — | / | |||||||||||||

of which: IRB ratings-based approach (RBA) or IRB internal assessment approach (IAA) | / | 110,551 | / | 9,374 | ||||||||||||||

of which: IRB supervisory formula approach (SFA) | / | 231,492 | / | 19,630 | ||||||||||||||

of which: SA/simplified supervisory formula approach (SSFA) | / | 25,711 | / | 2,056 | ||||||||||||||

of which: 1250% risk weight is applied | 10,933 | 11,261 | 874 | 941 | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 16 | Market risk | 2,034,213 | 2,470,321 | 162,737 | 197,625 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 17 | of which: standardized approach (SA) | 1,172,343 | 1,406,398 | 93,787 | 112,511 | |||||||||||||

| 18 | of which: internal model approaches (IMA) | 861,870 | 1,063,922 | 68,949 | 85,113 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 19 | Operational risk | 3,236,495 | 3,411,289 | 258,919 | 272,903 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 20 | of which: basic indicator approach | 628,110 | 591,083 | 50,248 | 47,286 | |||||||||||||

| 21 | of which: standardized approach | — | — | — | — | |||||||||||||

| 22 | of which: advanced measurement approach | 2,608,385 | 2,820,206 | 208,670 | 225,616 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 23 | Exposures of specified items not subject to regulatory adjustments | 1,209,277 | 818,950 | 99,743 | 67,224 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

Amounts included in RWA subject tophase-out arrangements | — | — | — | — | ||||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 24 | Floor adjustment | — | — | — | — | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 25 | Total (after applying the scaling factor) | 57,899,567 | 59,528,983 | 4,631,965 | 4,762,318 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

13

Table of Contents

(B) Credit Risk-weighted Assets by Asset Class and Ratings Segment

| (Billions of yen) | ||||||||||||||||||||||||

| As of March 31, 2018 | As of March 31, 2019 | |||||||||||||||||||||||

| EAD | RWA | Risk Weight (%) | EAD | RWA | Risk Weight (%) | |||||||||||||||||||

Internal ratings-based approach | 188,162.7 | 47,619.7 | 25.30 | 188,866.1 | 42,309.2 | 22.40 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Corporate, etc. | 162,853.7 | 29,536.1 | 18.13 | 171,471.5 | 29,822.5 | 17.39 | ||||||||||||||||||

Corporate (except specialized lending) | 79,917.9 | 27,232.1 | 34.07 | 87,608.9 | 27,339.1 | 31.20 | ||||||||||||||||||

RatingsA1-B2 | 58,776.0 | 13,840.5 | 23.54 | 65,892.5 | 13,942.5 | 21.15 | ||||||||||||||||||

RatingsC1-D3 | 19,376.2 | 11,569.6 | 59.71 | 20,261.6 | 12,045.7 | 59.45 | ||||||||||||||||||

RatingsE1-E2 | 1,182.2 | 1,625.0 | 137.45 | 867.6 | 1,105.3 | 127.39 | ||||||||||||||||||

RatingsE2R-H1 | 583.3 | 196.7 | 33.73 | 587.1 | 245.4 | 41.81 | ||||||||||||||||||

Sovereign | 76,803.1 | 833.9 | 1.08 | 77,227.7 | 963.2 | 1.24 | ||||||||||||||||||

RatingsA1-B2 | 76,674.5 | 758.3 | 0.98 | 77,117.9 | 886.3 | 1.14 | ||||||||||||||||||

RatingsC1-D3 | 128.2 | 75.2 | 58.70 | 108.0 | 73.8 | 68.33 | ||||||||||||||||||

RatingsE1-E2 | 0.3 | 0.2 | 82.31 | 1.8 | 3.0 | 169.08 | ||||||||||||||||||

RatingsE2R-H1 | 0.0 | 0.0 | 39.56 | 0.0 | 0.0 | 40.96 | ||||||||||||||||||

Bank | 5,986.3 | 1,313.1 | 21.93 | 6,461.1 | 1,338.4 | 20.71 | ||||||||||||||||||

RatingsA1-B2 | 5,447.4 | 1,002.1 | 18.39 | 5,951.3 | 1,027.1 | 17.25 | ||||||||||||||||||

RatingsC1-D3 | 537.5 | 310.5 | 57.77 | 508.5 | 310.7 | 61.10 | ||||||||||||||||||

RatingsE1-E2 | 0.0 | 0.0 | 129.81 | 0.0 | 0.0 | 153.40 | ||||||||||||||||||

RatingsE2R-H1 | 1.2 | 0.3 | 29.94 | 1.2 | 0.3 | 32.33 | ||||||||||||||||||

Specialized lending | 146.3 | 156.9 | 107.22 | 173.5 | 181.6 | 104.67 | ||||||||||||||||||

Retail | 11,629.8 | 3,818.0 | 32.83 | 11,046.3 | 3,526.3 | 31.92 | ||||||||||||||||||

Residential mortgage | 9,046.0 | 2,508.1 | 27.72 | 8,716.2 | 2,338.3 | 26.82 | ||||||||||||||||||

Qualifying revolving loan | 673.7 | 513.0 | 76.14 | 642.9 | 504.2 | 78.42 | ||||||||||||||||||

Other retail | 1,910.0 | 796.8 | 41.72 | 1,687.1 | 683.7 | 40.52 | ||||||||||||||||||

Equities | 5,136.2 | 8,436.2 | 164.25 | 4,407.4 | 7,183.3 | 162.98 | ||||||||||||||||||

PD/LGD approach | 4,162.6 | 5,279.2 | 126.82 | 3,559.8 | 4,445.9 | 124.89 | ||||||||||||||||||

Market-based approach | 973.5 | 3,157.0 | 324.26 | 847.6 | 2,737.4 | 322.95 | ||||||||||||||||||

Regarded-method exposure | 2,102.9 | 3,716.1 | 176.70 | / | / | / | ||||||||||||||||||

Securitizations | 4,169.4 | 371.5 | 8.91 | / | / | / | ||||||||||||||||||

Others | 2,270.5 | 1,741.5 | 76.70 | 1,940.7 | 1,776.9 | 91.56 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Standardized approach | 18,603.6 | 3,294.7 | 17.71 | 4,620.6 | 3,282.2 | 71.03 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Equity investments in funds | / | / | / | 2,262.8 | 3,416.1 | 150.96 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Securitization exposures | / | / | / | 4,185.2 | 972.7 | 23.24 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

CVA risk | / | 2,539.7 | / | / | 2,457.5 | / | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Central counterparty-related | / | 193.0 | / | / | 190.9 | / | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

Total | 206,766.4 | 53,647.3 | 25.94 | 199,934.8 | 52,628.8 | 24.99 | ||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||

| Note 1: | “Specialized lending” is specialized lending exposure under supervisory slotting criteria. | |

| Note 2: | “Equity investments in funds” is total of look-though approach, mandate-based approach, simple approach and fall-back approach. | |

| Note 3: | “Equity investments in funds” and “Securitization exposures” as of March 31, 2019 are disclosed out of Internal ratings-based approach due to revision of FSA Notice No.20. |

14

Table of Contents

∎ Linkages between Financial Statements and Regulatory Exposures

(A) LI1: Differences between Accounting and Regulatory Scopes of Consolidation and Mapping of Financial Statement Categories with Regulatory Risk Categories

| (Millions of yen) | ||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||

| As of March 31, 2018 | ||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||

| a | b | c | d | e | f | g | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

| Carrying values of items: | ||||||||||||||||||||||||||||

| Carrying values as reported in published financial statements/ | Carrying values under scope of regulatory consolidation | Subject to credit risk framework | Subject to counterparty credit risk framework | Subject to the securitization framework | Subject to the market risk framework | Not subject to capital requirements or subject to deduction from capital | ||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||

Cash and Due from Banks | 47,725,360 | 47,725,360 | — | — | — | — | ||||||||||||||||||||||

Call Loans and Bills Purchased | 715,149 | 715,149 | — | — | — | — | ||||||||||||||||||||||

Receivables under Resale Agreements | 8,080,873 | — | 8,080,873 | — | — | — | ||||||||||||||||||||||

Guarantee Deposits Paid under Securities Borrowing Transactions | 4,350,527 | — | 4,350,527 | — | — | — | ||||||||||||||||||||||

Other Debt Purchased | 2,713,742 | 2,127,247 | — | 551,092 | — | 35,402 | ||||||||||||||||||||||

Trading Assets | 10,507,133 | — | 5,318,732 | — | 10,507,133 | 2,249 | ||||||||||||||||||||||

Money Held in Trust | 337,429 | 337,429 | — | — | — | — | ||||||||||||||||||||||

Securities | 34,183,033 | 32,788,339 | — | 1,287,391 | — | 107,303 | ||||||||||||||||||||||

Loans and Bills Discounted | 79,421,473 | 77,937,924 | 1,305 | 1,475,430 | — | 6,812 | ||||||||||||||||||||||

Foreign Exchange Assets | 1,941,677 | 1,941,677 | — | — | — | — | ||||||||||||||||||||||

Derivatives Other than for Trading Assets | 1,807,999 | — | 1,807,999 | — | — | — | ||||||||||||||||||||||

Other Assets | 4,588,484 | 1,549,959 | 1,936,112 | 4,161 | — | 1,098,251 | ||||||||||||||||||||||

Tangible Fixed Assets | 1,111,128 | 1,111,128 | — | — | — | — | ||||||||||||||||||||||

Intangible Fixed Assets | 1,092,708 | 312,342 | — | — | — | 780,365 | ||||||||||||||||||||||

Net Defined Benefit Asset | 996,173 | 304,793 | — | — | — | 691,380 | ||||||||||||||||||||||

Deferred Tax Assets | 47,839 | 5,487 | — | — | — | 42,352 | ||||||||||||||||||||||

Customers’ Liabilities for Acceptances and Guarantees | 5,723,186 | 5,722,952 | 234 | — | — | — | ||||||||||||||||||||||

Reserves for Possible Losses on Loans | (315,621) | (314,330 | ) | — | — | — | (1,291 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Total assets | 205,028,300 | 172,265,461 | 21,495,785 | 3,318,075 | 10,507,133 | 2,762,827 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Liabilities | ||||||||||||||||||||||||||||

Deposits | 125,081,233 | — | — | — | — | 125,081,233 | ||||||||||||||||||||||

Negotiable Certificates of Deposit | 11,382,590 | — | — | — | — | 11,382,590 | ||||||||||||||||||||||

Call Money and Bills Sold | 2,105,293 | — | — | — | — | 2,105,293 | ||||||||||||||||||||||

Payables under Repurchase Agreements | 16,656,828 | — | 16,656,828 | — | — | — | ||||||||||||||||||||||

Guarantee Deposits Received under Securities Lending Transactions | 1,566,833 | — | 1,566,833 | — | — | — | ||||||||||||||||||||||

Commercial Paper | 710,391 | — | — | — | — | 710,391 | ||||||||||||||||||||||

Trading Liabilities | 8,121,543 | — | 4,936,441 | — | 8,121,543 | — | ||||||||||||||||||||||

Borrowed Money | 4,896,218 | — | — | — | — | 4,896,218 | ||||||||||||||||||||||

Foreign Exchange Liabilities | 445,804 | — | — | — | — | 445,804 | ||||||||||||||||||||||

Short-term Bonds | 362,185 | — | — | — | — | 362,185 | ||||||||||||||||||||||

Bonds and Notes | 7,544,256 | — | — | — | — | 7,544,256 | ||||||||||||||||||||||

Due to Trust Accounts | 4,733,131 | — | — | — | — | 4,733,131 | ||||||||||||||||||||||

Derivatives other than for trading liabilities | 1,514,483 | — | 1,514,483 | — | — | — | ||||||||||||||||||||||

Other Liabilities | 3,685,585 | — | 76,599 | — | — | 3,608,986 | ||||||||||||||||||||||

Reserve for Bonus Payments | 66,872 | — | — | — | — | 66,872 | ||||||||||||||||||||||

Reserve for variable compensation | 3,242 | — | — | — | — | 3,242 | ||||||||||||||||||||||

Net Defined Benefit Liability | 58,890 | — | — | — | — | 58,890 | ||||||||||||||||||||||

Reserve for Director and Corporate Auditor Retirement Benefits | 1,460 | — | — | — | — | 1,460 | ||||||||||||||||||||||

Reserve for possible losses on sales of loans | 1,075 | — | — | — | — | 1,075 | ||||||||||||||||||||||

Reserve for contingencies | 5,622 | 56 | — | — | — | 5,566 | ||||||||||||||||||||||

Reserve for reimbursement of deposits | 20,011 | — | — | — | — | 20,011 | ||||||||||||||||||||||

Reserve for reimbursement of debentures | 30,760 | — | — | — | — | 30,760 | ||||||||||||||||||||||

Reserves under Special Laws | 2,361 | — | — | — | — | 2,361 | ||||||||||||||||||||||

Deferred Tax Liabilities | 421,002 | — | — | — | — | 421,002 | ||||||||||||||||||||||

Deferred Tax Liabilities for Revaluation Reserve for Land | 66,186 | — | — | — | — | 66,186 | ||||||||||||||||||||||

Acceptances and Guarantees | 5,723,186 | — | — | — | — | 5,723,186 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Total liabilities | 195,207,054 | 56 | 24,751,187 | — | 8,121,543 | 167,270,708 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

| Notes: | ||

| 1. | Since the scope of accounting consolidation and that of regulatory consolidation are the same, the column (a) and (b) have been combined. | |

| 2. | Market risk includes foreign exchange risk and commodities risk in the banking book, but only those items in the trading book are recorded. | |

15

Table of Contents

| (Millions of yen) | ||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||

| As of March 31, 2019 | ||||||||||||||||||||||||||||

| ||||||||||||||||||||||||||||

| a | b | c | d | e | f | g | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

|

| |||||||||||||||||

| Carrying values of items: | ||||||||||||||||||||||||||||

| Carrying values as reported in published financial statements/ | Carrying values under scope of regulatory consolidation | Subject to credit risk framework | Subject to counterparty credit risk framework | Subject to the securitization framework | Subject to the market risk framework | Not subject to capital requirements or subject to deduction from capital | ||||||||||||||||||||||

Assets | ||||||||||||||||||||||||||||

Cash and Due from Banks | 45,108,602 | 45,108,602 | — | — | — | — | ||||||||||||||||||||||

Call Loans and Bills Purchased | 648,254 | 648,254 | — | — | — | — | ||||||||||||||||||||||

Receivables under Resale Agreements | 12,997,628 | — | 12,997,628 | — | — | — | ||||||||||||||||||||||

Guarantee Deposits Paid under Securities Borrowing Transactions | 2,578,133 | — | 2,578,133 | — | — | — | ||||||||||||||||||||||

Other Debt Purchased | 2,828,959 | 2,205,129 | — | 589,211 | — | 34,619 | ||||||||||||||||||||||

Trading Assets | 12,043,608 | — | 6,074,759 | — | 12,043,608 | — | ||||||||||||||||||||||

Money Held in Trust | 351,889 | 351,889 | — | — | — | — | ||||||||||||||||||||||

Securities | 29,774,489 | 28,542,167 | — | 1,168,312 | — | 64,008 | ||||||||||||||||||||||

Loans and Bills Discounted | 78,456,935 | 77,017,297 | 456 | 1,439,181 | — | — | ||||||||||||||||||||||

Foreign Exchange Assets | 1,993,668 | 1,993,668 | — | — | — | — | ||||||||||||||||||||||

Derivatives Other than for Trading Assets | 1,328,227 | — | 1,328,227 | — | — | — | ||||||||||||||||||||||

Other Assets | 4,229,589 | 1,465,349 | 1,557,007 | 6,724 | — | 1,200,507 | ||||||||||||||||||||||

Tangible Fixed Assets | 1,037,006 | 1,037,006 | — | — | — | — | ||||||||||||||||||||||

Intangible Fixed Assets | 620,231 | 167,749 | — | — | — | 452,482 | ||||||||||||||||||||||

Net Defined Benefit Asset | 982,804 | 300,661 | — | — | — | 682,142 | ||||||||||||||||||||||

Deferred Tax Assets | 37,960 | 1,393 | — | — | — | 36,566 | ||||||||||||||||||||||

Customers’ Liabilities for Acceptances and Guarantees | 6,062,053 | 6,060,193 | 7 | 1,852 | — | — | ||||||||||||||||||||||

Reserves for Possible Losses on Loans | (287,815) | (287,794 | ) | — | — | — | (20 | ) | ||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Total assets | 200,792,226 | 164,611,568 | 24,536,221 | 3,205,281 | 12,043,608 | 2,470,306 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Liabilities | ||||||||||||||||||||||||||||

Deposits | 124,311,025 | — | — | — | — | 124,311,025 | ||||||||||||||||||||||

Negotiable Certificates of Deposit | 13,338,571 | — | — | — | — | 13,338,571 | ||||||||||||||||||||||

Call Money and Bills Sold | 2,841,931 | — | — | — | — | 2,841,931 | ||||||||||||||||||||||

Payables under Repurchase Agreements | 14,640,439 | — | 14,640,439 | — | — | — | ||||||||||||||||||||||

Guarantee Deposits Received under Securities Lending Transactions | 1,484,584 | — | 1,484,584 | — | — | — | ||||||||||||||||||||||

Commercial Paper | 941,181 | — | — | — | — | 941,181 | ||||||||||||||||||||||

Trading Liabilities | 8,325,520 | — | 5,745,580 | — | 8,325,520 | — | ||||||||||||||||||||||

Borrowed Money | 3,061,504 | — | — | — | — | 3,061,504 | ||||||||||||||||||||||

Foreign Exchange Liabilities | 669,578 | — | — | — | — | 669,578 | ||||||||||||||||||||||

Short-term Bonds | 355,539 | — | — | — | — | 355,539 | ||||||||||||||||||||||

Bonds and Notes | 8,351,071 | — | — | — | — | 8,351,071 | ||||||||||||||||||||||

Due to Trust Accounts | 1,102,073 | — | — | — | — | 1,102,073 | ||||||||||||||||||||||

Derivatives other than for trading liabilities | 1,165,602 | — | 1,165,602 | — | — | — | ||||||||||||||||||||||

Other Liabilities | 4,512,325 | — | 55,033 | — | — | 4,457,291 | ||||||||||||||||||||||

Reserve for Bonus Payments | 68,117 | — | — | — | — | 68,117 | ||||||||||||||||||||||

Reserve for variable compensation | 2,867 | — | — | — | — | 2,867 | ||||||||||||||||||||||

Net Defined Benefit Liability | 60,873 | — | — | — | — | 60,873 | ||||||||||||||||||||||

Reserve for Director and Corporate Auditor Retirement Benefits | 1,389 | — | — | — | — | 1,389 | ||||||||||||||||||||||

Reserve for possible losses on sales of loans | 630 | — | — | — | — | 630 | ||||||||||||||||||||||

Reserve for contingencies | 4,910 | 100 | — | — | — | 4,809 | ||||||||||||||||||||||

Reserve for reimbursement of deposits | 19,068 | — | — | — | — | 19,068 | ||||||||||||||||||||||

Reserve for reimbursement of debentures | 25,566 | — | — | — | — | 25,566 | ||||||||||||||||||||||

Reserves under Special Laws | 2,473 | — | — | — | — | 2,473 | ||||||||||||||||||||||

Deferred Tax Liabilities | 185,974 | — | — | — | — | 185,974 | ||||||||||||||||||||||

Deferred Tax Liabilities for Revaluation Reserve for Land | 63,315 | — | — | — | — | 63,315 | ||||||||||||||||||||||

Acceptances and Guarantees | 6,062,053 | — | — | — | — | 6,062,053 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

Total liabilities | 191,598,188 | 100 | 23,091,239 | — | 8,325,520 | 165,926,908 | ||||||||||||||||||||||

|

|

|

|

|

|

|

|

|

|

| ||||||||||||||||||

| Notes: | ||

| 1. | Since the scope of accounting consolidation and that of regulatory consolidation are the same, the column (a) and (b) have been combined. | |

| 2. | Market risk includes foreign exchange risk and commodities risk in the banking book, but only those items in the trading book are recorded. | |

16

Table of Contents

(B) LI2: Main Sources of Differences between Regulatory Exposure Amounts and Carrying Values in Financial Statements

| (Millions of yen) | ||||||||||||||||||||||||||

| As of March 31, 2018 | ||||||||||||||||||||||||||

| a | b | c | d | e | ||||||||||||||||||||||

| Total | Items subject to: | |||||||||||||||||||||||||

| Credit risk framework | Counterparty credit risk framework | Securitization framework | Market risk framework | |||||||||||||||||||||||

| 1 | Asset carrying value amount under scope of regulatory consolidation (as per template LI1) | 202,265,473 | 172,265,461 | 21,495,785 | 3,318,075 | 10,507,133 | ||||||||||||||||||||

| 2 | Liabilities carrying value amount under regulatory scope of consolidation (as per template LI1) | 27,936,345 | 56 | 24,751,187 | — | 8,121,543 | ||||||||||||||||||||

| 3 | Total net amount under regulatory scope of consolidation | 174,329,127 | 172,265,405 | (3,255,401 | ) | 3,318,075 | 2,385,589 | |||||||||||||||||||

| 4 | Off-balance sheet amounts | 17,311,153 | 16,446,822 | — | 864,331 | — | ||||||||||||||||||||

| 5 | Differences due to consideration of provision for loan losses and write-offs | 401,252 | 401,252 | — | — | — | ||||||||||||||||||||

| 6 | Differences due to derivative transactions, etc. | 1,887,980 | — | 1,887,980 | — | — | ||||||||||||||||||||

| 7 | Differences due to repurchase transactions | 17,310,011 | — | 17,310,011 | — | — | ||||||||||||||||||||

| 8 | Other differences | (523,103 | ) | (907,644 | ) | — | — | — | ||||||||||||||||||

| 9 | Exposure amounts considered for regulatory purposes | 210,716,420 | 188,205,836 | 15,942,589 | 4,182,406 | 2,385,589 | ||||||||||||||||||||

| Notes: | ||

| 1. | Column (a) is not necessarily equal to the sum of columns (b) to (e) due to assets being riskweighted more than once. | |

| 2. | Differences between regulatory exposure amounts and carrying values in consolidated financial statements and the main sources of the differences are as follows. | |

• Off-balance sheet amounts correspond to the differences produced mainly by adding exposures to undrawn commitments and by multiplying customer liabilities for acceptances and guarantees by the credit conversion factor (CCF) assigned tooff-balance sheet items under the regulatory capital requirements.

• Differences due to consideration of provision for loan losses, and write-offs are produced mainly by adding general provisions for loan losses, specific provisions for loan losses and partial direct bad debt write-offs to those assets subject to the advanced internal ratings-based approach.

• Differences due to derivative transactions, etc. are produced mainly by incorporating future market value fluctuations and the effect of netting into regulatory exposure amounts. Derivative transactions, etc. include long-settlement transactions.

• Differences due to repurchase transactions are mainly produced by adding the exposure amounts related to assets pledged as collateral and considering the effect of netting and collateral.

• Other differences are produced mainly by considering the offsetting of deferred tax assets against deferred tax liabilities and the regulatory recognized effectiveness of hedging and making regulatory prudential adjustments. | ||

| (Millions of yen) | ||||||||||||||||||||||||||

| As of March 31, 2019 | ||||||||||||||||||||||||||

| a | b | c | d | e | ||||||||||||||||||||||

| Total | Items subject to: | |||||||||||||||||||||||||

| Credit risk framework | Counterparty credit risk framework | Securitization framework | Market risk framework | |||||||||||||||||||||||

| 1 | Asset carrying value amount under scope of regulatory consolidation (as per template LI1) | 198,321,920 | 164,611,568 | 24,536,221 | 3,205,281 | 12,043,608 | ||||||||||||||||||||

| 2 | Liabilities carrying value amount under regulatory scope of consolidation (as per template LI1) | 25,671,280 | 100 | 23,091,239 | — | 8,325,520 | ||||||||||||||||||||

| 3 | Total net amount under regulatory scope of consolidation | 172,650,640 | 164,611,467 | 1,444,982 | 3,205,281 | 3,718,088 | ||||||||||||||||||||

| 4 | Off-balance sheet amounts | 18,704,303 | 17,707,842 | — | 996,461 | — | ||||||||||||||||||||

| 5 | Differences due to consideration of provision for loan losses and write-offs | 372,837 | 372,837 | — | — | — | ||||||||||||||||||||

| 6 | Differences due to derivative transactions, etc. | 1,818,614 | — | 1,818,614 | — | — | ||||||||||||||||||||

| 7 | Differences due to repurchase transactions | 11,473,212 | — | 11,473,212 | — | — | ||||||||||||||||||||

| 8 | Other differences | (21,575 | ) | (350,755 | ) | — | — | — | ||||||||||||||||||

| 9 | Exposure amounts considered for regulatory purposes | 204,998,031 | 182,341,391 | 14,736,809 | 4,201,743 | 3,718,088 | ||||||||||||||||||||

| Notes: | ||

| 1. | Column (a) is not necessarily equal to the sum of columns (b) to (e) due to assets being riskweighted more than once. | |

| 2. | Differences between regulatory exposure amounts and carrying values in consolidated financial statements and the main sources of the differences are as follows. | |

• Off-balance sheet amounts correspond to the differences produced mainly by adding exposures to undrawn commitments and by multiplying customer liabilities for acceptances and guarantees by the credit conversion factor (CCF) assigned tooff-balance sheet items under the regulatory capital requirements.

• Differences due to consideration of provision for loan losses, and write-offs are produced mainly by adding general provisions for loan losses, specific provisions for loan losses and partial direct bad debt write-offs to those assets subject to the advanced internal ratings-based approach.

• Differences due to derivative transactions, etc. are produced mainly by incorporating future market value fluctuations and the effect of netting into regulatory exposure amounts. Derivative transactions, etc. include long-settlement transactions.

• Differences due to repurchase transactions are mainly produced by adding the exposure amounts related to assets pledged as collateral and considering the effect of netting and collateral.

• Other differences are produced mainly by considering the offsetting of deferred tax assets against deferred tax liabilities and the regulatory recognized effectiveness of hedging and making regulatory prudential adjustments. | ||

17

Table of Contents

(1) Summary of Risk Profile, Risk Management Policies/ Procedures and Structure

See pages 69 to 71 for a summary of our credit risk profile and credit risk management policies, etc.

(2) Summary of Provision for Loan Losses and Charge-offs

See page 70 for a summary of provision for loan losses and charge-offs.

(3) Quantitative Disclosure on Credit Risk

Counterparty credit risk exposures, securitization exposures, and regarded-method exposures are excluded from the amount of credit risk exposures below.

(A) CR1: Credit Quality of Assets

| (Millions of yen) | ||||||||||||||||||

| As of March 31, 2018 | ||||||||||||||||||

| a | b | c | d | |||||||||||||||

| Gross carrying values of | ||||||||||||||||||

| Defaulted exposures | Non-defaulted exposures | Reserve | Net values (a+b-c) | |||||||||||||||

| On-balance sheet exposures | ||||||||||||||||||

| 1 | Loans | 645,060 | 77,305,616 | 271,369 | 77,679,307 | |||||||||||||

| 2 | Debt securities | 5,946 | 26,116,905 | — | 26,122,851 | |||||||||||||

| 3 | Otheron-balance sheet debt exposures | 2,652 | 51,697,897 | 2,526 | 51,698,023 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 4 | Totalon-balance sheet exposures (1+2+3) | 653,659 | 155,120,419 | 273,896 | 155,500,182 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| Off-balance sheet exposures | ||||||||||||||||||

| 5 | Guarantees | 13,776 | 5,709,421 | 30,819 | 5,692,378 | |||||||||||||

| 6 | Commitments | 15,249 | 25,189,759 | — | 25,205,009 | |||||||||||||

|

|

|

|

|

|

|

| |||||||||||

| 7 | Totaloff-balance sheet exposures (5+6) | 29,026 | 30,899,180 | 30,819 | 30,897,388 | |||||||||||||

|