UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F

[X] REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934

OR

[ ] ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended ____________

OR

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from ____________ to ____________

OR

[ ] SHELL COMPANY PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

Date of event requiring this shell company report _____________=

For the transition period from ____________ to ____________

Commission file number N/A

HARD CREEK NICKEL CORPORATION

(Exact name of Registrant as specified in its charter)

Not Applicable

(Translation of Registrant’s name into English)

British Columbia, Canada

(Jurisdiction of incorporation or organization)

1060 – 1090 West Georgia Street Vancouver, British Columbia V6E 3V7 Canada

(Address of principal executive offices)

Copy of communications to:

Bernard Pinsky, Esq.

Clark Wilson LLP

Barristers and Solicitors

Suite 800 – 885 West Georgia Street

Vancouver, British Columbia, Canada V6C 3H1

Telephone: 604-687-5700 Facsimile: 604-687-6314

Securities registered or to be registered pursuant to Section 12(b) of the Act.

| Title of Class | Name of each exchange on which registered |

| Not Applicable | Not Applicable |

2

Securities registered or to be registered pursuant to Section 12(g) of the Act.

Common Shares Without Par Value

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act.

Not Applicable

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common stock as of the close

of the period covered by the annual report.

There were 46,292,676 Common Shares without par value issued and outstanding as at November 16, 2006.

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] YES [X] NO

If this report is an annual or transition report, indicate by check mark if the registrant is not required to file reports

pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. [ ] YES [ ] NO

Note – Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or

15(d) of the Securities Exchange Act of 1934 from their obligations under those Sections.

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or

15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the

registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

[ ] YES [ ] NO

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, or a non-accelerated

filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer [ ] Accelerated filer [ ] Non-accelerated filer [ ]

Indicate by check mark which financial statement item the registrant has elected to follow.

[ ] ITEM 17 [X] ITEM 18

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

[ ] YES [X] NO

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule

12b-2 of the Exchange Act). [ ] YES [ ] NO

TABLE OF CONTENTS

2

FORWARD-LOOKING STATEMENTS

Except for the statements of historical fact contained herein, some information presented in this registration statement constitutes forward-looking statements. When used in this registration statement, the words “estimate”, “project”, “believe”, “anticipate”, “intend”, “expect”, “predict”, “may”, “should”, the negative thereof or other variations thereon or comparable terminology are intended to identify forward-looking statements. Such forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of our company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, changes in project parameters as plans continue to be refined, future prices of nickel, as well as those factors discussed in the section entitled “Risk Factors” on page 8. Although our company has attempted to identify important factors that could cause actual results to differ materially, there may be other factors that cause actual results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, prospective investors should not place undue reliance on forward-looking statements. The forward-looking statements in this registration statement speak only as to the date hereof. Our company does not undertake any obligation to release publicly any revisions to these forward-looking statements to reflect events or circumstances after the date hereof or to reflect the occurrence of unanticipated events.

Although we believe that the expectations reflected in the forward-looking statements are reasonable, we cannot guarantee future results, levels of activity, performance or achievements. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

As used in this prospectus, the terms “we”, “us”, “our” and “Hard Creek” mean Hard Creek Nickel Corporation, unless otherwise indicated.

PART I

FINANCIAL INFORMATION AND ACCOUNTING PRINCIPLES

The financial statements and summaries of financial information contained in this document are reported in Canadian dollars (“$”) unless otherwise stated. A “tonne” is one metric ton or 2204.6 pounds. All such financial statements have been prepared in accordance with United States generally accepted accounting principles.

The financial statements of Hard Creek for the years ended December 31, 2004 and 2003 have been reported on by Dale Matheson Carr-Hilton LaBonte, Chartered Accountants, Suite 1700 – 1140 West Pender Street, Vancouver, British Columbia, V6E 4G1. The financial statements of Hard Creek for the six months ended June 30, 2005 and 2004 have been prepared by management and have neither been reviewed nor audited by Dale Matheson Carr-Hilton LaBonte.

Item 1 Identity of Directors, Senior Management and Advisers

A. Directors and Senior Management

The Directors and the senior management of our company as of November 16, 2006 are as follows:

| Name | Business Address | Function |

Mark Jarvis

| 1060 – 1090 W. Georgia St.

Vancouver, BC V6E 3V7

Canada | As President, Chief Executive Officer and director, Mr. Jarvis is

responsible for the development of our strategic direction and the

management and supervision of our overall business. |

George Sookochoff

| 1305 – 1323 Homer Street

Vancouver, BC V6B 5T1

Canada | As a non-executive director, Mr. Sookochoff is responsible for the

corporate governance of our company.

|

Frank Wright

| 427 Fairway Drive

North Vancouver, BC V7G 1L4

Canada | As a non-executive director, Mr. Wright is responsible for the

corporate governance of our company.

|

2

| Name | Business Address | Function |

Lyle Davis

| 2838 Carnation Street

North Vancouver, BC V7H 1L8

Canada | As a non-executive director, Mr. Davis is responsible for the

corporate governance of our company.

|

Brian Fiddler

| 408 Shiles Street

New Westminster, BC V3L 3K4

Canada | As Controller and Chief Financial Officer, Mr. Fiddler is

responsible for the financial and corporate management and

supervision of the affairs and business of our company. |

Tony Hitchins

| 1060-1090 West Georgia Street

Vancouver, BC V6E 3V7

Canada

| As Chief Operating Officer, Mr. Hitchins is responsible for the

project management, field management and logging core,

supervision of exploration on the Turnagain Nickel Project, hiring

field staff and maintaining claims in good standing. |

Neil Froc

| 42621 Canyon Road

Lindell Beach, BC V2R 5B8

Canada | As Executive Vice President, Mr. Froc is responsible for the

management of engineering and technical studies including

infrastructure and socio-economic project development. |

Leslie Young

| 1060 – 1090 W. Georgia St.

Vancouver, BC V6E 3V7

Canada

| As Corporate Secretary, Ms. Young is responsible for the internal

accounting and record keeping, general administration, and

making all necessary filings and financial reporting for our

company. |

B. Advisers

Our legal advisers are Clark Wilson LLP, Barristers & Solicitors, with a business address at Suite 800, 885 West Georgia Street, Vancouver, British Columbia, Canada V6C 3H1.

C. Auditors

Our auditors are Dale Matheson Carr-Hilton LaBonte, Chartered Accountants, with a business address at Suite 1700 – 1140 West Pender Street, Vancouver, British Columbia, V6E 4G1. Dale Matheson Carr-Hilton LaBonte are members of the Canadian Institute of Chartered Accountants.

Item 2 Offer Statistics and Expected Timetable

Not Applicable.

Item 3 Key Information

A. Selected Financial Data

The following table summarizes selected financial data for our company for the years ended December 31, 2005, 2004, 2003, 2002 and 2001 respectively. The information in the table was extracted from the detailed financial statements and related notes included in this registration statement and should be read in conjunction with such financial statements and with the information appearing under the heading, “Item 5 – Operating and Financial Review and Prospects”.

3

Selected Financial Data

(Stated in CAN Dollars)

Fiscal Year Ended December 31

US GAAP | 2005

Audited | 2004

Audited | 2003

Audited | 2002

Unaudited | 2001

Unaudited |

| Net Sales or Operating Revenue | NIL | NIL | NIL | NIL | NIL |

| Net Loss | $3,332,394 | $4,648,724 | $3,215,856 | $676,492 | $368,482 |

| Net Loss from Operations (January 17, 1983 (inception to December 31, 2005) | $19,901,059 | $16,568,665 | $11,919,941 | $8,704,085 | $8,027,593 |

| Depreciation | $6,780 | $6,076 | $2,511 | $808 | NIL |

| General and Administrative Expenses | $890,690 | $1,910,813 | $1,209,312 | $328,370 | $207,315 |

| Mineral Property Exploration Costs | $2,679,212 | $2,987,287 | $2,069,772 | $450,710 | $161,167 |

| Other Income | $237,508 | $249,376 | $63,228 | $102,588 | NIL |

| Basic and Diluted Net Loss per Share | $0.11 | $0.20 | $0.28 | $.08 | $0.07 |

| Assets | $1,697,951 | $1,303,553 | $498,557 | $189,947 | $36,209 |

| Current Assets | $846,465 | $607,583 | $282,752 | $154,905 | $6,209 |

| Capital Stock | $18,632,327 | $15,059,286 | $10,363,422 | $7,200,297 | $6,548,992 |

| Common Stock (adjusted to reflect changes in capital) | 37,675,494

common shares | 28,310,394

common shares | 17,390,189

common shares | 8,103,098

common shares | 5,052,990

common shares |

| Basic and Diluted Net Loss per Common Share | $0.11 | $0.20 | $0.28 | $0.08 | $0.07 |

| Cash Dividends per Common Share | NIL | NIL | NIL | NIL | NIL |

The following table summarizes selected financial data for our company for the six-month interim period ended June 30, 2006 and the six-month interim period ended June 30, 2005, which information is not audited. The information in the table should also be read in conjunction with these financial statements and with the other information appearing under the heading, “Item 5 – Operating and Financial Review and Prospects”.

Selected Financial Data

(Stated in CANADIAN Dollars)

Six-month Interim Period Ended June 30, 2006 (Unaudited)

US GAAP | Six Months ended

June 30, 2006 | Six Months ended

June 30, 2005 |

| Net Sales or Operating Revenue | NIL | NIL |

| Net loss | $2,479,181 | $1,078,835 |

| Net Loss from Operations (January 17, 1983 (inception to June 30, 2006) | $22,380,240 | $21,644,211 |

| Depreciation | $3,164 | $3,152 |

| General and Administrative Expenses | $856,474 | $417,476 |

| Mineral Property Exploration Costs | $1,635,392 | $664,136 |

| Other Income | $15,849 | $5,929 |

| Basic and Diluted Net Loss per Common Share | $0.06 | $0.04 |

4

US GAAP |

At

June 30, 2006 | At

December 31,

2005 |

| Assets | $1,847,332 | $1,697,951 |

| Capital Stock | $1,847,332 | $846,465 |

| Common Stock | $20,360,709 | $18,632,327 |

Common Stock (adjusted to reflect changes in capital)

| 40,884,125

common

shares | 37,675,494

common

share at 12/31 |

| Cash Dividends per Common Share | NIL | NIL |

B. Capitalization and Indebtedness

Our authorized capital consists of an unlimited number of Common Shares without par value and an unlimited number of Class A Preference Shares without par value. As of November 16, 2006, we had 46,292,676 Common Shares and no Class A Preference Shares issued and outstanding.

The table below sets forth our total indebtedness in Canadian dollars and capitalization as of June 30, 2006. You should read this table in conjunction with the audited and unaudited financial statements and accompanying notes, included in this registration statement.

As at June 30, 2006 (unaudited)

| Liabilities | | | |

| Current, unsecured | $ | 715,609 | |

| Long term, unsecured | | | |

| | $ | 715,609 | |

| Shareholders’ Equity | | | |

| Common stock | $ | 20,360,709 | |

| Additional paid-in capital | | 3,342,308 | |

| Deficit | | (22,380,240 | ) |

| | $ | 1,322,777 | |

C. Reasons for the Offer and Use of Proceeds

Not applicable.

D. Risk Factors

This Registration Statement contains forward-looking statements which relate to future events or our future performance, including our future financial performance. In some cases, you can identify forward-looking statements by terminology such as “may”, “should”, “expects”, “plans”, “anticipates”, “believes”, “estimates”, “predicts”, or “potential” or the negative of these terms or other comparable terminology. These statements are only predictions and involve known and unknown risks, uncertainties and other factors, including the risks in enumerated in this section entitled “Risk Factors”, that may cause our company’s or our industry’s actual results, levels of activity, performance or achievements to be materially different from any future results, levels of activity, performance or achievements expressed or implied by these forward-looking statements.

While these forward-looking statements, and any assumptions upon which they are based, are made in good faith and reflect our current judgment regarding the direction of our business, actual results will almost always vary, sometimes materially, from any estimates, predictions, projections, assumptions or other future performance suggested in this Registration Statement. Except as required by applicable law, including the securities laws of the United States, we do not intend to update any of the forward-looking statements to conform these statements to actual results.

5

An investment in our common stock involves a number of very significant risks. You should carefully consider the following risks and uncertainties in addition to other information in this prospectus in evaluating our company and our business before purchasing shares of our company’s common stock. Our business, operating results and financial condition could be seriously harmed due to any of the following risks. The risks described below are not the only ones facing our company. Additional risks not presently known to us may also impair our business operations. You could lose all or part of your investment due to any of these risks.

Risks Associated with Mining

All of our properties are in the exploration stage. There is no assurance that any of our properties contain any mineral resources in commercially exploitable quantities. If we do not discover any mineral resource in a commercially exploitable quantity, our business will fail and investors may lose all of their investment in our company.

Despite exploration work on our mineral properties, we have not established that any of them contain any commercially exploitable mineral reserves, nor can there be any assurance that we will ever find commercially exploitable mineral reserves. The probability of an individual prospect ever having a commercially exploitable mineral reserve is extremely remote; in all probability our mineral resource properties do not contain any reserves and any funds that we spend on exploration will probably be lost. The search for valuable minerals as a business is extremely risky. We can provide investors with no assurance that additional exploration on our properties will establish that commercially exploitable reserves of minerals exist on our mineral properties. Additional potential problems that may prevent us from discovering any reserves of minerals on our property include, but are not limited to, unanticipated problems relating to exploration and additional costs and expenses that may exceed current estimates. Most of these factors are beyond our control, and any of them could increase costs and make extraction of any identified mineral resource unprofitable.

If we are unable to establish the presence of commercially exploitable reserves of minerals on our property, our ability to fund future exploration activities will be impeded, we will not be able to operate profitably and investors may lose all of their investment in our company.

We face intense competition in the mineral exploration and exploitation industry and we compete with our competitors for financing, for new mineral resource properties and for qualified managerial and technical employees.

Our competition there includes large established mining companies with substantial capabilities and with greater financial and technical resources than we have. As a result of this competition, we may have to compete for financing and be unable to acquire financing on terms we consider acceptable. This competition could adversely affect our ability to acquire suitable prospects for exploration in the future. We may also have to compete with the other mining companies in the recruitment and retention of qualified managerial and technical employees. If we are unable to successfully compete for financing or for qualified employees, our exploration programs may be slowed down or suspended. If we are unable to successfully compete for the acquisition of suitable prospects for exploration in the future, there can be no assurance that we will acquire any interest in additional mineral resource properties. The occurrence of any of these things may cause us to cease operations as a company.

Because of the inherent dangers involved in mineral exploration and exploitation, there is a risk that we may incur liability or damages as we conduct our business.

The search for valuable minerals involves numerous hazards. As a result, we may become subject to liability for such hazards, including pollution, cave-ins and other hazards against which we cannot insure or against which we may elect not to insure. At the present time we have no coverage to insure against these hazards. The payment of such liabilities may have a material adverse effect on our financial position.

Our title to our resource properties may be challenged by third parties or the licenses that permit us to explore our properties may expire if we fail to timely renew them and pay the required fees.

We have investigated the status of our title to our mineral resource properties and we are satisfied that the title to these properties is properly registered in the name of our company. but we cannot guarantee that the rights to explore our properties will not be revoked or altered to our detriment. The ownership and validity of mining claims and concessions are often uncertain and may be contested. Should such a challenge to the boundaries or registration of ownership arise, the resolution of disputes or the process of clarifying the accuracy of our mining license registration could take substantial time and money. Further, the preservation of our title to our mineral properties requires that we continue to expend money or work the claims. If we fail to expend the necessary amount of money or if we fail to work our mineral claims, then our title to our mineral properties could expire or be forfeit.

6

Mineral prices are subject to dramatic and unpredictable fluctuations.

The market price of precious metals and other minerals is volatile and has fluctuated widely, particularly in recent years. The prices of various metals are affected by numerous factors beyond our control, including international economic and political trends, expectations of inflation, currency exchange fluctuations, interest rates and global or regional consumption patterns, speculative activities and increased production due to improved mining and production methods. The supply of and demand for metals are affected by various factors, including political events, economic conditions and production casts in major mineral producing regions. Variations in the market prices of metals may impact on our ability to raise funding to continue exploration of our properties. In addition, any significant fluctuations in metal prices will impact on our decision to accelerate or reduce our exploration activities. If the price of precious metals and other minerals should drop significantly, the cost of mineral extraction may be higher than is economically feasible. The marketability of minerals is also affected by numerous other factors beyond our control, including government regulations relating to royalties, allowable production and importing and exporting of minerals, the effect of which cannot be accurately predicted.

Mineral operations are subject to government regulations which could have the effect of reducing or preventing us from exploiting any possible mineral reserves on our properties.

Exploration activities are subject to national and local laws and regulations governing prospects, taxes, labour standards, occupational health, land use, environmental protection, mine safety and others which may in the future have a substantial adverse impact on our company’s prospects. In order to comply with applicable laws, we may be required to make capital expenditures until a particular problem is remedied. Existing and possible future environmental legislation, regulation and action could cause additional expense, capital expenditure, restriction and delay in the activities of our company, the extent of which cannot be reasonably predicted. If we violate any applicable law or regulation, we could be forced to stop work and we could be fined. If we are forced to suspend our activities or if we are required to pay a large fine for a violation of these applicable laws and regulations, our business could be adversely affected.

Our operations may be subject to environmental regulations which may result in the imposition of fines and penalties.

Our operations may be subject to environmental regulations promulgated by government agencies from time to time. Environmental legislation provides for restrictions and prohibitions on spills, releases or emissions of various substances produced in association with certain mining industry operations, such as seepage from tailings disposal areas, which would result in environmental pollution. A breach of such legislation may result in the imposition of fines and penalties. Environmental legislation is evolving in a manner which means stricter standards, and enforcement; fines and penalties for non-compliance are more stringent. Environmental assessments of proposed projects carry a heightened degree of responsibility for companies and directors, officers and employees. The cost of compliance with changes in governmental regulations has a potential to reduce the profitability of operations.

Risks Related To Our Company

The fact that we have not generated any operating revenues since our incorporation raises substantial doubt about our ability to continue as a going concern.

We have not generated any operating revenues since our incorporation and we will, in all likelihood, continue to incur operating expenses without revenues until our mining properties are fully developed and in commercial production. We had cash in the amount of $1,728,875 as of June 30, 2006. We estimate our average monthly operating expenses to be approximately $60,000 to $70,000 each month. As a result, we need to generate significant revenues from our operations or obtain financing. We cannot assure that we will be able to successfully explore and develop our mining properties or assure that viable reserves exist on the properties for extraction. These circumstances raise substantial doubt about our ability to continue as a going concern as described in an explanatory paragraph to our independent auditors’ report on our financial statements for the year ended December 31, 2005. It is unlikely that we will generate any funds internally until we discover commercially viable quantities of ore. If we are unable to generate revenue from our business during the fiscal year 2006, we may be forced to delay, scale back, or eliminate our exploration activities. If any of these actions were to become necessary, we may not be able to continue to explore our properties or operate our business and if either of those events happen, then there is a substantial risk our business would fail.

We have a limited operating history on which to base an evaluation of our business and prospects.

Although we have been in the business of exploring mineral resource properties since 1983, we have not yet located any mineral reserve. As a result, we have never had any revenues from our operations. In addition, our operating history has been restricted

7

to the acquisition and exploration of our mineral properties and this does not provide a meaningful basis for an evaluation of our prospects if we ever determine that we have a mineral reserve and commence the construction and operation of a mine. We have no way to evaluate the likelihood of whether our mineral properties contain any mineral reserve or, if they do that we will be able to build or operate a mine successfully. We anticipate that we will continue to incur operating costs without realizing any revenues during the period when we are exploring our properties. We expect to continue to incur significant losses into the foreseeable future. We recognize that if we are unable to generate significant revenues from mining operations and any dispositions of our properties, we will not be able to earn profits or continue operations. At this early stage of our operation, we also expect to face the risks, uncertainties, expenses and difficulties frequently encountered by companies at the start up stage of their business development. We cannot be sure that we will be successful in addressing these risks and uncertainties and our failure to do so could have a material adverse effect on our financial condition. There is no history upon which to base any assumption as to the likelihood that we will prove successful and we can provide investors with no assurance that we will generate any operating revenues or ever achieve profitable operations.

We have not generated any revenue from our business and we may need to raise additional funds in the near future. If we are not able to obtain future financing when required, we might be forced to discontinue our business.

Because we have not generated any revenue from our business and we cannot anticipate when we will be able to generate revenue from our business, we will need to raise additional funds for the further exploration and future development of our mining claims and to respond to unanticipated requirements or expenses. We anticipate that we will need to raise $4,000,000 for the 12 month period ending June 30, 2007, and that we will need to raise further capital very soon thereafter in the approximate amount of $5,000,000 to $7,000,000. We do not currently have any arrangements for financing and we can provide no assurance to investors we will be able to find such financing if required. We have no assurance that additional funding will be available to us for further exploration and development of our projects or to fulfil our obligations under any applicable agreements. Although we have been successful in the past in obtaining financing through the sale of equity securities, there can be no assurance that we will be able to obtain adequate financing in the future or that the terms of such financing will be favourable. Failure to obtain such additional financing could result in a delay or indefinite postponement of further exploration and development of our projects with the possible loss of such properties.

Conflicts of interest may arise as a result of our directors and officers being directors and officers of other natural resource companies.

Certain of our directors and officers may continue to be involved in a wide range of business activities through their direct and their indirect participation in corporations, partnerships or joint ventures. Situations may arise in connection with potential acquisitions and investments where the other interests of these directors and officers may conflict with the interests of our company.

Our Articles of Incorporation indemnify our officers and directors against all costs, charges and expenses incurred by them.

Our Articles of Incorporation contain provisions limiting the liability of our officers and directors for their acts, receipts, neglects or defaults and for any other loss, damage or expense incurred by our company which shall happen in the execution of the duties of such officers or directors, unless the officers or directors did not act honestly and in good faith with a view to the best interests of our company. Such limitations on liability may reduce the likelihood of derivative litigation against our officers and directors and may discourage or deter our shareholders from suing our officers and directors based upon breaches of their duties to our company, though such an action, if successful, might otherwise benefit our company and our shareholders.

Risks Relating to our Securities

Trading in our common shares on the TSX Venture Exchange is limited and sporadic, making it difficult for our shareholders to sell their shares or liquidate their investments.

Our common shares are currently listed on the TSX Venture Exchange under the symbol ‘HNC’. The trading price of our common shares has been and may continue to be subject to wide fluctuations. Trading prices of our common shares may fluctuate in response to a number of factors, many of which are beyond our control. In addition, the stock market in general, and the market for base metal exploration companies, including companies exploring for nickel in particular, has experienced extreme price and volume fluctuations that have often been unrelated or disproportionate to the operating performance of such companies. These broad market and industry factors may adversely affect the market price of our shares, regardless of our operating performance. If you invest in our common shares, you could lose some or all of your investment.

8

In the past, following periods of volatility in the market price of a company’s securities, securities class-action litigation has often been instituted. Such litigation, if instituted, could result in substantial costs and a diversion of management’s attention and resources.

Investors’ interests in our company will be diluted and investors may suffer dilution in their net book value per share if we issue additional shares or raise funds through the sale of equity securities.

We are currently without a source of revenue and will most likely be required to issue additional shares to finance our operations and, depending on the outcome of our exploration programs, may issue additional shares to finance additional exploration programs of any or all of our projects or to acquire additional properties. If we are required to issue additional shares to raise financing, your interests in our company will be diluted and you may suffer dilution in your net book value per share depending on the price at which such securities are sold. As at November 16, 2006, there were outstanding an aggregate number of common share purchase warrants and share purchase options as, upon exercise, would result in the issue of an additional 8,606,919 of our common shares which, if exercised, would represent approximately 17% of our issued and outstanding common chares. If all of these share purchase warrants and share purchase options are exercised and these common shares are issued, such issuance also will cause a reduction in the proportionate ownership and voting power of all other shareholders. The dilution may result in a decline in the market price of our common shares.

Investors’ interests in our company will be diluted and investors may suffer dilution in their net book value per share if we issue employee/director/consultant options

We have granted and may in the future continue to grant to some or all of our directors, officers, insiders, and key employees options to purchase our common shares as non-cash incentives to those persons. Such options may be granted at exercise prices equal to market prices, or at such other price as may be permitted under the policies of any stock exchange upon which our securities are traded (currently, our common shares are listed for trading on the TSX Venture Exchange), when the public market is depressed. The issuance of additional shares will cause our existing shareholders to experience dilution of their ownership interests.

We do not expect to declare or pay any dividends.

We have not declared or paid any dividends on our Common Shares since our inception, and we do not anticipate paying any such dividends for the foreseeable future.

U.S. investors may not be able to enforce their civil liabilities against us or our Directors, controlling persons and officers.

It may be difficult to bring and enforce suits against us. We were incorporated under the Company Act (British Columbia) and transitioned under the Business Corporations Act (British Columbia) in June of 2004. All of our directors and officers are residents of countries other than the United States and all of our assets are located outside of the United States. Consequently, it may be difficult for United States investors to effect service of process in the United States upon those directors or officers who are not residents of the United States, or to realize in the United States upon judgments of United States courts predicated upon civil liabilities under the United States Securities Exchange Act of 1934, as amended. There is substantial doubt whether an original action could be brought successfully in Canada against any of such persons or us predicated solely upon such civil liabilities.

Trading of our stock may be restricted by the SEC’s “Penny Stock” regulations which may limit a stockholder’s ability to buy and sell our stock.

The U.S. Securities and Exchange Commission has adopted regulations which generally define “penny stock” to be any equity security that has a market price (as defined) less than $5.00 per share or an exercise price of less than $5.00 per share, subject to certain exceptions. Our securities are covered by the penny stock rules, which impose additional sales practice requirements on broker-dealers who sell to persons other than established customers and “accredited investors.” The term “accredited investor” refers generally to institutions with assets in excess of $5,000,000 or individuals with a net worth in excess of $1,000,000 or annual income exceeding $200,000 or $300,000 jointly with their spouse. The penny stock rules require a broker-dealer, prior to a transaction in a penny stock not otherwise exempt from the rules, to deliver a standardized risk disclosure document in a form prepared by the SEC which provides information about penny stocks and the nature and level of risks in the penny stock market. The broker-dealer also must provide the customer with current bid and offer quotations for the penny stock, the compensation of the broker-dealer and its salesperson in the transaction and monthly account statements showing the market value of each penny stock held in the customer’s account. The bid and offer quotations, and the broker-dealer and salesperson compensation information, must be given to the customer orally or in writing prior to effecting the transaction and must be given to the

9

customer in writing before or with the customer’s confirmation. In addition, the penny stock rules require that prior to a transaction in a penny stock not otherwise exempt from these rules, the broker-dealer must make a special written determination that the penny stock is a suitable investment for the purchaser and receive the purchaser’s written agreement to the transaction. These disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the stock that is subject to these penny stock rules. Consequently, these penny stock rules may affect the ability of broker-dealers to trade our securities. We believe that the penny stock rules discourage investor interest in, and limit the marketability of, our common stock.

U.S. investors could suffer adverse tax consequences if we are characterized as a passive foreign investment company.

We may be treated as a passive foreign investment company, or PFIC, for United States federal income tax purposes during the 2003 tax year or in subsequent years. We may be deemed a PFIC because previous financings combined with proceeds of future financings may produce, or be deemed to be held to produce, passive income. Additionally, U.S. citizens should review the section entitled “Taxation-U.S. Federal Income Taxation - Passive Foreign Investment Companies” contained in this Registration Statement for a more detailed description of the PFIC rules and how those rules may affect their ownership of our capital shares.

If we are or become a PFIC, our U.S. shareholders may be subject to the following adverse tax consequences:

they will be taxed at the highest ordinary income tax rates in effect during their holding period on certain distributions on our capital shares, and gains from the sale or other disposition of our capital shares;

they will be required to pay interest on taxes allocable to prior periods; and

the tax basis of our capital shares will not be increased to fair market value at the date of their date.

Item 4 Information on our Company

A. History and Development of our Company

We were originally incorporated in British Columbia Canada under the Company Act (British Columbia) on January 17, 1983, under the name “Bren-Mar Resources Limited”, with an authorized capital of 50,000,000 Common Shares without par value. On March 15, 2000, we changed our name to “Bren-Mar Minerals Ltd.” and consolidated our then issued and outstanding common shares on the basis of 1 post-consolidation common share for 5 pre-consolidation common shares, and we increased our post-consolidation authorized capital to 50,000,000 common shares. On November 22, 2000, we changed our name to “Canadian Metals Exploration Ltd.”

The Business Corporations Act (British Columbia) came into force on March 29, 2004, repealing the Company Act (British Columbia.) Our company now operates under the Business Corporations Act (British Columbia). On June 25, 2004, we changed our name to “Hard Creek Nickel Corporation”, altered our authorized capital to comprise an unlimited number of common shares and an unlimited number of Class A preferred shares, and adopted our current Articles of Incorporation, which are attached as an exhibit to this form.

We have our head office and principal place of business at Suite 1060 – 1090 West Georgia Street, Vancouver, British Columbia V6E 3V7 Canada (Telephone: 604.681.7896) .

Our common shares are listed on the TSX Venture Exchange under the symbol “HNC”.

Since inception, we have been engaged in natural resource exploration and development primarily in British Columbia and, since 1996, have focused on the Turnagain Property in the Liard Mining Division of northern British Columbia. We first acquired the mineral claims on the Turnagain Property in 1996 under an option agreement with John Schussler and Ernie Hatzl. The original option agreement gave us the right to earn a 100% interest in the mineral claims on the Turnagain Property in exchange for the issuance of 200,000 of our common shares and the expenditure of CAN$1,000,000on exploration of the property within 5 years of acquisition. We have now earned the 100% interest and it is subject to a 4% net smelter royalty on possible future production. We have the right to pay out the net smelter royalty for CAN$1,000,000 for each 1% of the royalty. So, to pay out all 4% of the royalty, we would be required to pay CAN$4,000,000.

On April 25, 2001, we entered into an agreement with Northwest Petroleum Inc. of Bakersfield, California to acquire rights to two separate oil and gas projects located in the state of California, consisting of the Buttonwillow Oil and Gas Leases in Kern

10

County, California and the Moffat Ranch Gas Field in Madera County, California. We subsequently determined in March of 2002 that the Buttonwillow oil and gas leases and the Moffat Ranch Gas Field gas project were not feasible. Accordingly, the agreement with Northwest Petroleum Inc. was terminated on March 21, 2002 and our investment of $143,717 was written off.

On November 28, 2002, we entered into an agreement with John Schussler and Ernie Hatzl to acquire an additional 34 mineral claims, adjacent to the Turnagain Property, Laird Mining Division, British Columbia, in exchange for an aggregate total of 100,000 common shares.

Between November , 2003 and March, 2005 we staked additional claims, enlarging the Turnagain property from 3,700 hectares to approximately 27,500 hectares. In April, 2004, we staked three claim blocks in northern British Columbia. The staked properties vary in size from 1500 to 5500 hectares and total 9000 hectares and are located in northern British Columbia, between 20km west and 100km northwest of the Turnagain property. These three claim blocks are known as the Green, Serp and Cot properties.

In January and February, 2005 we acquired, by staking, four additional claim blocks in central and northern British Columbia for a total area of approximately 27,140 hectares. Some reconnaissance prospecting was completed on the claims with no further work warranted. All of the claims were allowed to lapse and are no longer owned by the company.

In September, 2005 we acquired by staking on-line, one additional claim block of approximately 1,906 hectares located approximately 50km north of the Turnagain property. Some reconnaissance prospecting was completed on the claim with no further work warranted. The claim was allowed to lapse and is no longer owned by the company.

In March, 2006 we acquired by staking on-line, one additional claim block which is known as the Lunar property. It consists of approximately 4,489 hectares and is located approximately 130km southeast of the Turnagain property. Some reconnaissance prospecting was completed in the summer of 2006 with follow up work to be completed in 2007.

In May, 2006 we acquired by staking on-line, two additional claim blocks which are known as the Lime 1 and Lime 2 properties. They consist of approximately 1,133 hectares and are located approximately 15km and 35km west of the Turnagain property. Some reconnaissance prospecting was completed in the summer of 2006 with follow up work to be completed in 2007 or 2008.

In July, 2006 we acquired by staking on-line, one additional claim block which is known as the Conuma property. It consists of approximately 18,050 hectares and is located on the west side of Vancouver Island approximately 130km west of Campbell River, B.C. No work has been completed on the property to date but is scheduled for the summer of 2007.

On October 11, 2006 we acquired by legal action, one additional claim block which is known as the Bobner property. It consists of approximately 150 hectares and is located approximately 8km west of the Turnagain property. No work has been completed on the property to date but is scheduled for the summer of 2007.

Present Operations of Our Company

Turnagain Property Project

Our current mineral exploration activities on the Turnagain Property include core drilling, geological mapping, geochemical surveys, downhole geophysical surveys, baseline environmental and engineering studies, and metallurgical testing. From 2001 to the end of 2005, we had drilled 115 core holes for a total depth of 82,539 feet. Approximate total exploration expenditure during this period was CAN$9,980,000.

B. Business Overview

Nature of Operations and Principal Activities

We are in the mineral resource business. This business generally consists of three stages: exploration, development and production. We are a mineral resource company in the exploration stage because we have not yet found mineral resources in commercially exploitable quantities, and are engaged in exploring land in an effort to discover them. Mineral resource companies that have located a mineral resource in commercially exploitable quantities and are preparing to extract that resource are in the development stage, while those engaged in the extraction of a known mineral resource are in the production stage.

11

Mineral resource exploration can consist of several stages. The earliest stage usually consists of the identification of a potential prospect through either the discovery of a mineralized showing on that property or as the result of a property being in proximity to another property on which exploitable resources have been identified, whether or not they are or have in the past been extracted.

After the identification of a property as a potential prospect, the next stage would usually be the acquisition of a right to explore the area for mineral resources. This can consist of the outright acquisition of the land or the acquisition of specific, but limited, rights to the land (e.g., a license, lease or concession). After acquisition, exploration would probably begin with a surface examination by a prospector or professional geologist with the aim of identifying areas of potential mineralization, followed by detailed geological sampling and mapping of this showing with possible geophysical and geochemical grid surveys to establish whether a known trend of mineralization continues underground, possibly trenching in these covered areas to allow sampling of the underlying rock. Exploration also commonly includes systematic regularly spaced drilling in order to determine the extent and grade of the mineralized system at depth and over a given area, as well as gaining underground access by ramping or shafting in order to obtain bulk samples that would allow one to determine the ability to recover various commodities from the rock. If minerals are found, exploration might culminate in a feasibility study to ascertain if the mining of the minerals would be economic. A feasibility study is a study that reaches a conclusion with respect to the economics of bringing a mineral resource to the production stage.

Our primary natural resource property is the Turnagain Property, located in the Liard Mining Division of northern British Columbia. We also own seven very early stage, mineral properties in central and northern British Columbia. We have not identified the existence of any commercially viable mineral deposits at any of our mineral properties. We intend to conduct prospecting and sampling on several of these properties in 2007.

There is no assurance that a commercially viable mineral deposit exists on any of our properties, and further exploration is required before we can evaluate whether any exist and, if so, whether it would be economically and legally feasible to develop or exploit those resources. Even if we complete our current exploration program and we are successful in identifying a mineral deposit, we would be required to spend substantial funds on further drilling and engineering studies before we could know whether that mineral deposit will constitute a reserve (a reserve is a commercially viable mineral deposit). Please refer to the section entitled “Risk Factors”, beginning on page 8 of this registration statement, for additional information about the risks of mineral exploration.

Revenues

To date we have not generated any revenues from any of our properties.

Principal Market

We do not currently have any market, as we have not yet identified any mineral resource on any of our properties that is of a commercially exploitable quantity. If we succeed in identifying a mineral resource in commercially exploitable quantities, our principal markets should consist of metals refineries and base metal traders and dealers.

Seasonality of our Business

Our mineral exploration activities are subject to seasonal variation due to the winter season in northern British Columbia. Field work is best carried out between mid-May and late-November when day time temperatures average 10 to 15 degrees Celsius. Our other operations, such as metallurgical review and analysis of geochemical survey results, can be carried out all year round.

Sources and Availability of Raw Materials

Other than a paved highway and the small community of Dease Lake, located 70km west of the Turnagain property, there is no infrastructure close to the Turnagain property. A small amount of hydroelectric power is generated near Dease Lake, to supply the town, but there is little excess capacity. The closest suitable source of hydroelectric power for mine development is the transmission line at Meziaden Junction, 300km south along the highway. If a mineral resource is found on our Turnagain property, power generation would be required.

12

Patents and Licenses; Industrial, Commercial and Financial Contracts; and New Manufacturing Processes

In conducting our business operations, we are not dependent on any patented or license processes, technology, industrial, commercial or financial contract or new manufacturing processes.

Competitive Conditions

We compete with other mining companies, some of which have greater financial resources and technical facilities, for the acquisition of mineral interests, as well as for the recruitment and retention of qualified employees. Exploration in British Columbia has experienced a dramatic revival in the past two years and increased activity is forecast for the future. We compete for qualified employees with Vancouver based companies, including Hunter Dickenson Inc., Equity Engineering and Ivanhoe Mines, and international mining companies, including Billiton-BHP, Rio Tinto and Anglo American.

Governmental Regulations

Mining operations are subject to a wide range of government regulations such as restrictions on production, price controls, tax increases, expropriation of property, environmental protection, protection of agricultural territory or changes in conditions under which minerals may be marketed. Mining operations may also be affected by claims of native peoples, any of which could have the effect of reducing or preventing us from exploiting any of our properties.

Mineral claims in British Columbia are of two types. Cell mineral claims are established by electronically selecting the desired land on government claim maps, where the available land is displayed as a grid pattern of open cells, each of approximately 450-500 hectares. Payment of the required recording fees is also conducted electronically. This process for claim staking has been in effect since January, 2005, and is now the only way to stake claims in British Columbia. Prior to January, 2005, legacy claims were staked by walking the perimeter of the desired ground and erecting and marking posts at prescribed intervals. Legacy claims, staked before January, 2005, remain valid and may be converted into cell claims.

Cell mineral claims may be kept in good standing by incurring assessment work or by paying cash-in-lieu of assessment work in the amount of CAN$4.00 per hectare per year during the first 3 years following the location of the mineral claims. This amount is increased to CAN$8.00 per hectare in the fourth and succeeding years.

Legacy mineral claims in British Columbia may be kept in good standing by incurring assessment work or by paying cash-in-lieu of assessment work in the amount of $100 per mineral claim unit per year during the first three years following the location of the mineral claim. This amount increases to $200 per mineral claim unit in the fourth and succeeding years.

We will be required to comply with all regulations, rules and directives of governmental authorities and agencies applicable to the exploration of minerals in the Province of British Columbia and in Canada generally. Under these laws, prior to production, we have the right to explore the property. We are required to file a “Notice of Work and Reclamation” with the British Columbia Ministry of Energy and Mines to conduct exploration works on mineral properties in British Columbia. To obtain a work permit, a company may be required to post a bond. In addition, the production of minerals in the Province of British Columbia requires prior regulatory approval.

Our mineral claims entitle our company to continue exploration activities on our properties, subject to our compliance with various Canadian federal and provincial laws governing land use, the protection of the environment and related matters.

If we locate a commercially viable mineral resource on any of our properties, we would be required to conduct extensive community consultations in northern British Columbia with both Aboriginal and non- Aboriginal groups, environmental surveys both on the property and along transportation corridors. We also would be required to develop a mining plan and a mine closure plan. These surveys and plans would be combined into a comprehensive Environmental Impact Statement and submitted to the British Columbia government for review and approval. Any development or exploitation of such a mineral resource would be subject to Canadian federal and provincial laws governing land use, protection of the environment, occupational health, waste disposal, toxic substances, mine safety and other matters. We had no material costs related to compliance and/or permits in recent years, and anticipate no material costs in the next year.

We will have to sustain the cost of reclamation and environmental mediation for all exploration work undertaken. The amount of these costs is not known at this time as we do not know the extent of the exploration program that will be undertaken beyond completion of the recommended work programs. It is estimated that reclamation of existing exploration drill sites and access roads on the Turnagain property will cost approximately $60,000. Permits and regulations will control all aspects of any production program if the project continues to that stage because of the potential impact on the environment.

13

C. Organizational Structure

We have one wholly owned subsidiary, Canadian Metals Exploration Ltd., incorporated under the Canada Business Corporation Act (Canada) on July 14, 2004. This wholly owned subsidiary is currently inactive.

D. Property, Plant and Equipment

Our executive office is located at 1060 – 1090 West Georgia Street, Vancouver, British Columbia V6E 3V7, Canada. The Company leases the 1,890 sq.ft space for $31,185 per annum and expires on April 30, 2008. This space accommodates all of our executive and administrative offices. We believe that this existing space is adequate for our current needs. Should we require additional space, we believe that such space can be secured on commercially reasonable terms.

We own office equipment with a value of approximately $20,000 and it is located at our Vancouver Office. We lease a photocopier at the rate of $700/three months.

Our company has three significant mineral properties:

| 1. | The Turnagain Property; |

| 2. | Lunar; and, |

| 3. | Serp. |

The Turnagain Property

This section provides a summary of the geology and exploration activities on the Turnagain Property. The technical information regarding the Turnagain Property included in this section is based, in large part, on a Technical Report and Mineral Resource Estimate prepared by Ronald G. Simpson, P.Geo., dated April 13, 2006, and prepared in compliance with the requirements of National Instrument 43-101 and Form 43-101F1 as adopted by the British Columbia Securities Commission. This Technical Report was used as supporting documentation and was filed with the British Columbia Securities Commission and the TSX Venture Exchange. Mr. Ronald G. Simpson is a “qualified person” as the term is defined under National Instrument 43-101.

14

Exploration data collected during the 2004 and 2005 exploration programs, was done under the supervision of Chris Baldys, P. Eng., Neil Froc, P. Eng., and Tony Hitchins, M.Sc.

Location and Accessibility

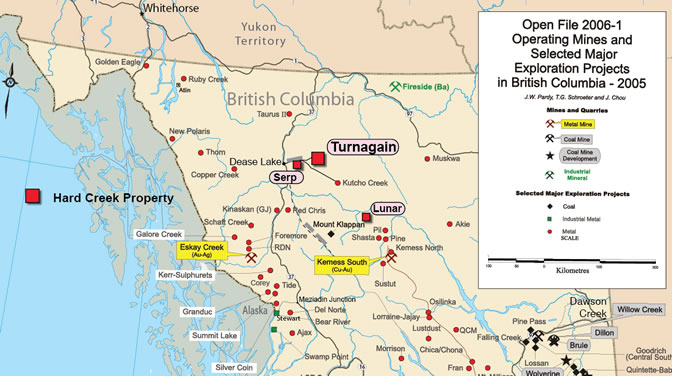

The Turnagain Property consists of 53 contiguous mineral claims situated in the Liard Mining Division of northern British Columbia, 70 kilometres east of Dease Lake and 1350 kilometres north-northwest of Vancouver. Please see the above map to see where the property is located in the province of British Columbia, Canada. The mineral claims collectively cover an area of 29,370 hectares (264 square kilometres.) The Turnagain Property is situated in the Stikine Ranges of the Cassiar Mountains. Elevations range from about 1,000 metres above sea level along the Turnagain River, in the central claim area, to 2,200 metres at an unnamed summit in the north central property area.

The Turnagain Property straddles the Turnagain River near where it joins Hard Creek. The community of Dease Lake, on Highway #37 some 400 kilometres north of the port of Stewart, is 70 kilometres west of the property. Helicopter access from Dease Lake involves a 20 minute flight. A secondary road extending easterly from Dease Lake has been used by large, articulated 4-wheel drive vehicles to convey large jade boulders from the Kutcho Creek area and to supply placer gold operations at Wheaton Creek over the past number of years. A branch of this road network extends into the Turnagain Property with road distance to Dease Lake of about 100 kilometres.

A dirt airstrip, measuring 700 metres, constructed in the 1960s and graded in 2004, is situated within the claims on the northwest side of the Turnagain River and can accommodate small aircraft. This airstrip is immediately adjacent to our current camp facility and core storage. Previous exploration programs have made use of camp facilities at Wheaton Creek (Boulder) which is about 15 kilometres by road west of the Turnagain Property.

Dease Lake has three times a week scheduled airline service and offers some supplies and services. The communities of Terrace and Smithers, both several hundred kilometres south, offer a range of services and supplies which can be trucked to Dease Lake via Highway #37.

The area between Dease Lake and the Turnagain Property features maturely dissected mountains rising to elevations of between 2,000 and 2,425 metres above sea level and separated by wide, drift-filled valleys in which elevations average 1,000 metres. Forest cover, present in valley areas, is replaced by typical alpine flora above 1500 metres. Bedrock is reasonably well exposed in the areas above tree line and along drainages.

Description of Claims

Our Turnagain Property consists of 53 contiguous mineral claims. Hard Creek Nickel Corporation owns a 100% interest in all of these mineral claims subject to a 4% net smelter royalty on possible future production on one mineral claim (Tenure No. 511330 formerly the “Cub” claim). We retain the right to purchase all or part of the net smelter royalty for CAN $1,000,000 per 1%. The following table summarizes the claim name, size, and expiry date for the 53 claims in the Turnagain property as of November 16, 2006

The following table shows details relating to Hard Creek Nickel Corporation’s Turnagain claims and the expiry dates of those claims:

Tenure

Number | Claim Name | Area

(ha) | Record Date | Expiry Date |

| Legacy Mineral Claim | | | |

| 407627 | PUP 4 | 500 | January 1,2004 | January 1,2016 |

| Cell Mineral Claims | | | |

| 501131 | DRIFT 1 | 422 | January 12,2005 | January 12,2008 |

| 501168 | DRIFT 2 | 422 | January 12,2005 | January 12,2008 |

| 501234 | DRIFT 3 | 422 | January 12,2005 | January 12,2008 |

| 501298 | DRIFT 4 | 422 | January 12,2005 | January 12,2008 |

| 508218 | DINAH 1 | 407 | March 3,2005 | March 3,2009 |

| 508219 | DINAH 2 | 407 | March 3,2005 | March 3,2009 |

15

Tenure

Number | Claim Name | Area

(ha) | Record Date | Expiry Date |

| 508221 | DINAH 3 | 407 | March 3,2005 | March 3,2008 |

| 508222 | DINAH 4 | 407 | March 3,2005 | March 3,2009 |

| 508223 | DINAH 5 | 407 | March 3,2005 | March 3,2009 |

| 508225 | DINAH 6 | 407 | March 3,2005 | March 3,2009 |

| 508226 | DINAH 7 | 255 | March 3,2005 | March 3,2009 |

| 508227 | DINAH 8 | 407 | March 3,2005 | March 3,2009 |

| 508228 | DINAH 9 | 136 | March 3,2005 | March 3,2009 |

| 508229 | DINAH 10 | 203 | March 3,2005 | March 3,2009 |

| 528780 | T1 | 67.7 | Feb 23, 2006 | Feb 23, 2007 |

| 528781 | T2 | 203 | Feb 23, 2006 | Feb 23, 2007 |

| 528782 | T3 | 153 | Feb 23, 2006 | Feb 23, 2007 |

| 528784 | T4 | 288 | Feb 23, 2006 | Feb 23, 2007 |

| 528787 | T5 | 170 | Feb 23, 2006 | Feb 23, 2007 |

| 528788 | T6 | 270 | Feb 23, 2006 | Feb 23, 2007 |

| 528789 | T7 | 422 | Feb 23, 2006 | Feb 23, 2007 |

| 528790 | T8 | 254 | Feb 23, 2006 | Feb 23, 2007 |

| Cell Claims Converted from Legacy Claims - April, 2005 | |

| 503365 | HARD 2 | 793 | January 14, 2005 | February 18, 2009 |

| 510889 | FLAT 10,13,15 | 1628 | April 6,7,2004 | April 7,2010 |

| 510892 | FLAT 2,6 | 1219 | April 6,2004 | April 7,2010 |

| 510910 | FLAT 9,12,14 | 1424 | April 18,2004 | April 7,2010 |

| 510911 | FLAT 1,5 | 1067 | April 6,2004 | April 7,2010 |

| 510912 | FLAT 8,11 | 780 | April 5,7,2004 | April 7,2009 |

| 511214 | HARD 4,6 | 980 | February 18,2004 | February 18,2009 |

| 511226 | HILL 1,2 | 1216 | February 18,2004 | February 18,2009 |

| 511227 | HILL 3 | 507 | February 18,2004 | February 17,2009 |

| 511230 | HILL 4,5 | 760 | February 18,2004 | February 17,2009 |

| 511234 | HILL 6 | 186 | February 16,2004 | February 16,2009 |

| 511244 | HARD 5,7 | 490 | February 18,2004 | February 18,2009 |

| 511251 | HARD 8 | 473 | February 17,2004 | February 17,2009 |

| 511257 | HILL 9,10 | 1014 | February 17,2004 | February 17,2009 |

| 511279 | HARD 9,10 | 897 | February 17,2004 | February 17,2009 |

| 511304 | HILL 7,8 | 1150 | February 17,2004 | February 17,2010 |

| 511305 | HOUND 3 | 271 | Sept. 27,2003 | Sept 27,2010 |

| 511306 | TURN 2,FLAT 7 | 881 | February 19,2004 | February 19,2013 |

| 511329 | HOUND 1,2 | 1015 | Sept. 27,2003 | Sept. 27,2010 |

| 511330 | CUB | 593 | May 5,1996 | December 1,2015 |

| 511337 | CUB 10,18,PUP 1 | 1066 | July-Dec.,1996 | December 1,2015 |

| 511340 | CUB 17 | 254 | Sept.17,2002 | December 1,2015 |

16

Tenure

Number | Claim Name | Area

(ha) | Record Date | Expiry Date |

| 511344 | TURN 1 | 271 | 19-Feb-04 | February 19,2013 |

| 511347 | FLAT 3,4 | 474 | April 5,21,2004 | April 7,2013 |

| 511348 | CUB 2 | 389 | June 20,1996 | December 1,2015 |

| 511586 | PUP 2 | 237 | January 1,2004 | January 1,2016 |

| 511593 | PUP 3 | 102 | January 1,2004 | January 1,2016 |

| 511627 | CUB 11 | 592 | July 17,1996 | December 1,2015 |

| 511628 | HARD 1 | 709 | February 18,2004 | February 18,2009 |

| 511629 | HARD 3 | 473 | February 18,2004 | February 18,2009 |

The map below, labelled “Figure 2”, indicates a group of claims held in trust by the Supreme Court of British Columbia. In February 2004, we filed an action in the Supreme Court of British Columbia against Mr. Wolf Wiese, a former consultant to our company. The action sought the transfer to our company of claims neighbouring the Turnagain property, which were staked in the name of Mr. Wiese. We believe that these claims should have been staked in the name of the Company. On July 10, 2006 the Supreme Court of British Columbia ordered that the claims be transferred back to our company. The transfer of ownership has not been completed to date. Mr. Wiese has subsequently filed a Notice of Appeal of the Order.

17

Exploration History

Nickel and copper sulphides were discovered within the current Turnagain property area in a bedrock exposure along Turnagain River in 1956. Mineral claims covering this showing and other occurrences were acquired by Falconbridge Nickel Mines Limited in 1966. Falconbridge Nickel Mines Limited also completed work over the ensuing seven years, including surface and airborne geophysical surveys, geological mapping, geochemical surveys and 2895 metres of conventional and packsack diamond drilling in 40 widely spaced drill holes.

18

Our Turnagain Property represents a unique style of sulphide mineralization associated with a zoned, ultramafic complex. Iron and nickel sulphides of magmatic origin are widespread in dunite and wehrlite near dunite-wehrlite contacts. Exploration on the Turnagain Property between 1967 and 2002 was sporadic and was concentrated in the Horsetrail area or near small exposures of net-textured sulphides. We acquired the property in 1996.

Work Completed by the Registrant

We acquired the Turnagain River property in 1996 and our exploration work that year included 400 line kilometres of airborne magnetic surveys and 795.5 metres of diamond drilling in 5 holes. Additional diamond drilling completed by our company in 1997 and 1998 amounted to 3,123 metres in 14 holes. Related work included 18 line kilometres of surface magnetic surveys covering two areas of the property, bore hole pulse electromagnetic surveys in four of the 1997-1998 drill holes and preliminary metallurgical test work on drill core composites.

In 2002, we performed ground magnetic and Induced Polarization geophysical surveys over part of the claim area and completed 1,687 metres of diamond drilling in 7 holes. Exploratory work in 2003 included geological mapping and prospecting with bedrock, stream sediment and limited soil sampling and 8,669 metres of diamond drilling in 22 holes, including the deepening of one hole started in 2002. Preliminary metallurgical test work was conducted on composite 2002-2003 core samples.

A comprehensive exploration program in 2004 included a helicopter borne magnetic and electromagnetic survey totalling 1,866 line km, 14 km of ground magnetic and electromagnetic surveys, 1:20,000 scale aerial photography of the entire property, collection of more than 3,000 geochemical soil samples, geological mapping, and 7522 metres of diamond drilling in 49 holes. The approximately 4,000 core samples were analysed for 30 elements including nickel, copper, cobalt, sulphur and often platinum and palladium. Extensive metallurgical test work is still in progress on 2003-2004 composite core samples.

Hard Creek Nickel’s 2005 exploratory program consisted of geological mapping, bedrock and soil sampling, and 7,143 metres of diamond drilling in 37 holes. Various mineralogical, environmental baseline, engineering, metallurgical and analytical studies were also undertaken.

Present Condition of the Property

No mining operations have taken place on the property. Diamond drill casings have been left in place and the locations of the bore holes marked with labelled fence posts. There are approximately 32 km of unpaved roads and trails on the property, constructed from the late 1960’s to the present. Reclamation work has been and will be performed on disused roads.

A camp capable of accommodating approximately 30 people has been constructed, consisting of 17 wall tents, 3 trailers and drill core storage facilities. A 700 meter unpaved air strip is adjacent to the camp. Power is provided by an on-site diesel generator

Our properties are without known reserves and our proposed work program is exploratory in nature.

Mineralization

A number of mineral showings, located during early exploration on the Turnagain property consist of net-textured to semi-massive magmatic pyrrhotite (a common iron sulphide mineral) with minor pentlandite (iron and nickel sulphide mineral) in altered ultramafic rocks. Extensive drilling in the Horsetrail Zone on the Turnagain property during the 2002-2005 period outlined broad zones of disseminated to intercumulus (between silicate grains) sulphide mineralization either in dunite or in wehrlite near dunite-wehrlite contacts.

Within the broad zone of disseminated intercumulus mineralization in the Horsetrail area, the sulphide grains range in size from 0.5mm to 5mm with cuspate contacts against oval olivine grains. Pyrrhotite is the most abundant sulphide but usually encloses conspicuous pentlandite grains, especially in the higher grade intervals. Chalcopyrite (copper-iron sulphide), when present, is usually localized along the margins of the pyrrhotite or as minute veinlets extending away from the sulphide grain. Trace to minor quantities of bornite (another copper-iron sulphide), native copper, valleriite, mackinawite, smythite (complex iron-nickel-cobalt-copper sulphide minerals), and several unnamed Ni-Fe-Cu-Co sulphides have been identified in metallurgical concentrates.

The Horsetrail Zone of the Turnagain property comprises several northwest to west-northwest striking zones of more than 0.25% nickel separated by intervals of lower grade nickel sulphide mineralization. Mineralization is interpreted to dip steeply to the north.

19

Platinum and palladium mineralization has been intersected in several drill holes in the D.J. Zone, located on the Turnagain property approximately three kilometres northwest of the Horsetrail Zone. Host for the mineralization is usually magnetite-clinopyroxenite within a dominantly hornblendite lithology. Textural and analytical data suggest a location near the roof of the ultramafic intrusion. Platinum and palladium values in drill holes include 2407 parts per billion (parts per billion) Pt+Pd over 2m in hole 04-59, 1645 parts per billion Pt+Pd over 2.15m in hole 04-44, 1530 parts per billion Pt+Pd over 13m in hole 05-88 and 2320 parts per billion Pt+Pd over 2m in Hole 05-101. Preliminary analysis has identified minor arsenic and antimony in association with platinum and palladium, respectively, but it is not clear whether the mineralization is dominantly magmatic or the result of a post-crystallization hydrothermal (involving water rich fluid) event.

Environmental Surveys

Since the timely collection of long lead-time baseline data on the Turnagain property, such as meteorological, hydrological, water quality, and wildlife, is important to the environmental permitting process, we initiated collection of water quality data and wildlife observations in 2003. The program was expanded in 2004 and 2005 to include hydrological measurements on Hard Creek, ground water quality in the Horsetrail Zone on the Turnagain property, and meteorological data (temperature, precipitation, evaporation, wind speed and direction). A preliminary study to determine the presence and species of fish in the Turnagain River and tributaries of Hard Creek was conducted in 2004.

Although the primary purpose of a geochemical soil survey that we conducted in 2003 was to locate mineralization, it also provided information on background levels of 38 elements in the soil, over the ultramafic complex, prior to any significant future surface disturbance. Our collection of water quality, hydrological, meteorological, and wildlife data on the Turnagain property will continue throughout the next twelve months.

Metallurgical Test Work

Metallurgical test work has been an integral part of the Turnagain property exploration programs; primarily to address the feasibility of producing an acceptable nickel sulphide concentrate from low grade mineralization where much of the nickel was unavailable for economic recovery. Between 1998 and 2005, we have taken approximately 33 drill core composite samples and subjected them to a series of preliminary metallurgical studies to establish the process response of the nickel and cobalt, mineralization. Mineral process testing included conventional froth flotation and some scoping work for gravity and magnetic separation techniques. The metallurgical studies were conducted by recognized, independent testing laboratories, including Lakefield Research, of Lakefield, Ontario; Process Research Associates Ltd., of Vancouver, British Columbia; Billiton Process Research, in South Africa; and Cominco Engineering Services Ltd. (CESL), in Vancouver. All test work by Hard Creek Nickel Corp. and predecessor companies was supervised by consulting metallurgist, Frank Wright, P. Eng.

Evaluation of nickel recovery included 12 tests performed on lower grade composite samples. An additional 13 flotation tests that were performed on composite samples. Eight tests were performed on composite samples. Two locked cycle flotation tests were also performed. Based on the results to date, our company will continue to conduct metallurgical test work.

Recommendations and Cost Estimate

The following exploration program for the Turnagain Property has been recommended to our company by Chris Baldys, P. Eng., Neil Froc, P. Eng., and Tony Hitchins, M.Sc. and is in progress for 2006.

| • | The Horsetrail Zone on the Turnagain property has been the focus of our drilling for the last several years and hosts the resource estimate. Fill-in and step-out drill hole locations are designed to expand the zone of nickel-cobalt mineralization.The 2004 airborne magnetic-electromagnetic survey located a number of significant, untested conductors near the northwestern and southeastern margins of the ultramafic intrusion. We did not test all of the conductors in 2005. Several smaller, isolated conductors, hosted by either ultramafic rocks or the enclosing phyllite are also of interest, especially when enhanced by nickel or coincident Pt-Pd soil anomalies. Additional drilling is recommended to test the geophysical anomalies. Further bedrock sampling in areas of rock exposure, detailed prospecting, mapping, and channel sampling will enable some prioritizing of drill targets and is also recommended. In areas of deeper overburden, drill testing will be the unequivocal test of buried geophysical anomalies. |

| | | |

| • | Further metallurgical testing focusing primarily on grinding, flotation and hydrometallurgical testing is also recommended. |

20

| Diamond Drilling – 21,000 metres @ $102.25/metre plus associated costs | $2,513,850 |

| Road construction, drill pads, etc. | $215,,000 |

| Geophysics Surveying | $59,000 |

| Technical Personnel – Senior Geologists, Junior Geologists , Field assistants | $442,000 |

| Field Labor – Core splitters, road slashing, maintenance, etc. | 276,500 |

| Analytical costs – drill core, bedrock, soil, duplicate & check samples | $415,200 |

| Miscellaneous Field Supplies | $8,000 |

| Camp costs – cooks, room and board, maintenance, etc. | $329,000 |

| Communications – satellite telephone, facsimile, internet | $30,000 |

| Transportation – scheduled airline service | $55,000 |

| - helicopter support | $232,500 |

| - road transport of supplies | $170,000 |

| Data Management | $274,000 |

| Baseline Environmental and Engineering Studies | $149,000 |

| Metallurgical test work and related studies | $620,000 |

| Contingencies @ 10% | $579,000 |

| Total | $6,368,050 |

The Lunar Property

The Lunar property consists of eleven mineral cell claims covering an area of 4489.1 hectares located in central northern British Columbia, within the Stikine Ranges of the Omineca Mountains, approximately 160 km south east of the Turnagain Property. The property covers a large mafic-ultramafic complex.

Access to the claims is by helicopter.

British Columbia Geological Survey geologists reported a rock sample assay of 1017 parts per billion platinum in chromite (reported in the Province of British Columbia Ministry of Energy, Mines and Petroleum Resources Open File 1990-12) on the Lunar property. The presence of sulphide was reported , although apparently not investigated for nickel mineralization. Hard Creek geologists have made an initial property visit and an assessment is pending sample analysis.