Table of Contents

As filed with the Securities and Exchange Commission on January 31, 2006

Registration No. 333-129361

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 5

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

AMERICAN TELECOM SERVICES, INC.

(Exact Name of Registrant as Specified in its Charter)

| Delaware | 5065 | 77-0602480 | ||

| (State of Incorporation) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

2466 Peck Road

City of Industry, California 90601

(562) 908-1287

(Address and Telephone Number of Registrant’s Principal Executive Offices)

Bruce Hahn

Chief Executive Officer

American Telecom Services, Inc.

2466 Peck Road

City of Industry, California 90601

(562) 908-1287

(Name, Address and Telephone Number of Agent for Service)

Copies to:

Ira I. Roxland, Esq. Sonnenschein Nath & Rosenthal LLP 1221 Avenue of the Americas New York, New York 10020 (212) 768-6700 Fax: (212) 768-6800 | David Alan Miller, Esq. Graubard Miller The Chrysler Building 405 Lexington Avenue New York, New York 10174-1901 (212) 818-8800 Fax: (212) 818-8881 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. x

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, check the following box. ¨

Table of Contents

CALCULATION OF REGISTRATION FEE

Title of Each Class of Securities to be Registered(1) | Amount to be Registered | Proposed Maximum Aggregate Price Per Security(2) | Proposed Maximum Aggregate Offering Price | Amount of Registration Fee | |||||||||||

Common stock, par value $0.001 per share, to be sold by issuer in the offering(3) | 3,220,000 | $ | 5.05 | $ | 16,261,000.00 | $ | 1,913.92 | ||||||||

Warrants to be sold by issuer in the offering(4) | 3,220,000 | $ | 0.05 | $ | 161,000.00 | $ | 18.95 | ||||||||

Representative’s purchase option | 1 | — | $ | 100.00 | (5 | ) | |||||||||

Common stock issuable upon exercise of the representative’s purchase option | 280,000 | $ | 6.3125 | $ | 1,767,500.00 | $ | 208.03 | ||||||||

Warrants issuable upon exercise of the representative’s purchase option | 280,000 | $ | 0.625 | $ | 17,500.00 | $ | 2.06 | ||||||||

Common stock issuable upon exercise of the warrants sold by issuer in the offering (including the warrants underlying the representative’s purchase option) | 3,500,000 | $ | 5.05 | $ | 17,675,000.00 | $ | 2,080.35 | ||||||||

Common stock to be sold by selling securityholders(6) | 750,240 | $ | 5.05 | $ | 3,788,712.00 | $ | 445.93 | ||||||||

Warrants to be sold by selling securityholders(6) | 1,475,667 | $ | 0.05 | $ | 73,783.30 | $ | 8.68 | ||||||||

Common stock to be sold by selling securityholders upon their exercise of warrants(6) | 1,475,667 | $ | 5.05 | $ | 7,452,118.35 | $ | 877.11 | ||||||||

Common stock to be issued upon exercise of warrants after sale thereof in open market transactions(6) | 1,475,667 | $ | 5.05 | $ | 7,452,118.35 | $ | 877.11 | ||||||||

Total | $ | 54,648,832.00 | $ | 6,432.14 | (7) | ||||||||||

| (1) | Pursuant to Rule 416 under the Securities Act of 1933, this registration statement also covers any additional securities that may be offered or issued in connection with any stock split, stock dividend or similar transaction. |

| (2) | Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(c). |

| (3) | Includes 420,000 shares of common stock issuable upon exercise of the underwriters’ over-allotment option. |

| (4) | Includes 420,000 warrants issuable upon exercise of the underwriters’ over-allotment option. |

| (5) | No fee pursuant to Rule 457(g). |

| (6) | Securities being sold by the selling securityholders identified in this registration statement. |

| (7) | $6,431.96 of registration fee previously paid. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

EXPLANATORY NOTE

This registration statement contains two forms of prospectus: (a) one to be used in connection with an offering by the registrant of 2,800,000 shares of common stock and 2,800,000 redeemable warrants (the “Registrant’s Prospectus”) and (b) one to be used in connection with (i) the resale of up to 750,240 shares of common stock and 1,475,667 redeemable warrants (and the 1,475,667 shares of common stock underlying such warrants) by the holders named therein and (ii) the issuance by the registrant of up to 1,475,667 shares of common stock upon the exercise of redeemable warrants purchased by others in the open market from such selling securityholders (the “Selling Securityholders’ Prospectus”).

The complete Registrant’s Prospectus follows immediately. Following the Registrant’s Prospectus are certain pages of the Selling Securityholders’ Prospectus, which include: (i) an alternate front cover page, (ii) an alternate section entitled “Prospectus Summary — The Offering,” (iii) an alternate section entitled “Use of Proceeds,” (iv) an alternate section entitled “Selling Securityholders” and (v) an alternate section entitled “Plan of Distribution.”

All other pages of the Registrant’s Prospectus and the Selling Securityholders’ Prospectus are the same, except that the Selling Securityholders’ Prospectus will not have a section entitled “Underwriting.”

Table of Contents

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated January 31, 2006

PROSPECTUS

2,800,000 shares of common stock

2,800,000 redeemable common stock purchase warrants

American Telecom Services, Inc.

This is an initial public offering of our securities. We are offering 2,800,000 shares of our common stock and 2,800,000 redeemable common stock purchase warrants. Each redeemable warrant entitles the holder to purchase one share of our common stock at a price of $5.05 and will expire on February 1, 2011, or earlier upon redemption. The redeemable warrants are redeemable at our option, with the consent of HCFP/Brenner Securities LLC, the representative of the underwriters, as set forth in this prospectus.

We have agreed to sell to the representative, for $100, an option to purchase up to 280,000 shares of our common stock at $6.3125 per share and/or up to 280,000 of our redeemable warrants, identical to those offered by this prospectus, at $0.0625 per warrant. The purchase option and its underlying securities have been registered under the registration statement of which this prospectus forms a part.

There is presently no public market for our securities. We anticipate that our common stock and redeemable warrants will be approved for listing on the American Stock Exchange under the symbols “TES” and “TES.WS,” respectively.

An aggregate of 2,225,907 shares of common stock and 1,475,667 warrants are being registered for resale under the registration statement of which this prospectus forms a part. Except for 79,926 shares and 58,333 redeemable warrants that are subject to a lock-up agreement, such shares and warrants will be immediately saleable into the market following the completion of this offering.

Investing in our securities involves a high degree of risk. See “Risk Factors” beginning on page 7 of this prospectus for a discussion of information that should be considered in connection with an investment in our company.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Per Warrant | Total | |||||||

Public offering prices | $ | 5.05 | $ | 0.05 | $ | 14,280,000 | |||

Underwriting discount and the representative’s 2% nonaccountable expense allowance | $ | 0.505 | $ | 0.005 | $ | 1,428,000 | |||

Proceeds to us (before expenses) | $ | 4.545 | $ | 0.045 | $ | 12,852,000 | |||

We have granted to the underwriters a 45-day option to purchase up to an additional 420,000 shares of our common stock and/or an additional 420,000 redeemable warrants from us at the public offering prices, less the underwriting discount, solely to cover over-allotments.

HCFP/Brenner Securities LLC, acting as representative of the underwriters, expects to deliver the shares of our common stock and the redeemable warrants to investors in this offering on or about , 2006.

HCFP/Brenner Securities LLC | Brean Murray, Carret & Co., LLC |

, 2006

Table of Contents

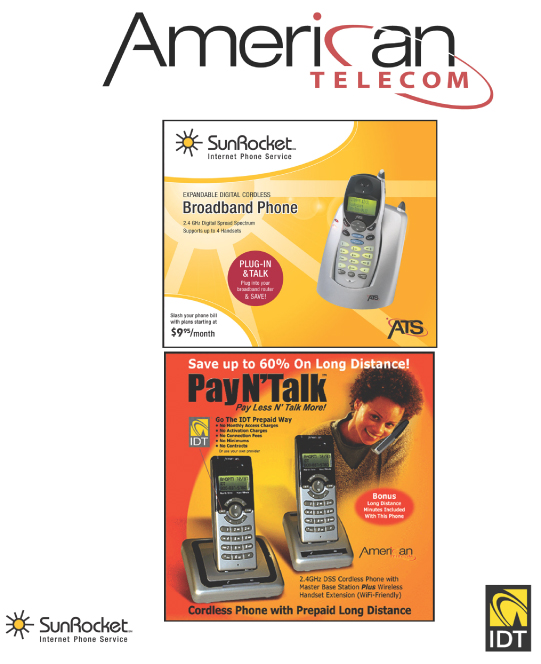

We currently offer broadband phone (Voice-over-Internet-Protocol

or “VolP”) and prepaid long distance communications services that are bundled

with our digital, cordless multi-handset phones. Our strategic

partners include SunRocket, Inc. and IDT Corporation.

Table of Contents

Our company

We currently offer broadband phone (Voice-over-Internet-Protocol or “VoIP”) and prepaid long distance communications services that are bundled with our digital, cordless multi-handset phones. We sell our phone/service bundles through major retailers under our “American Telecom”, “ATS” or “Pay N’ Talk” brand names. Our digital spread spectrum (“DSS”) telecom platform is designed to enable seamless access to the communications services provided by our strategic partners. Our strategic partners include SunRocket, Inc., a growing provider of VoIP services, for our VoIP service offering, and IDT Corporation, an established communications carrier, for our prepaid long distance service offering. Under the agreements with each of these service providers, we will receive a percentage of the monthly service revenues generated by users of our service offerings, in addition to the revenues we generate through the sale of our phone hardware. We are a development stage company that has only recently begun to generate operating revenues. We are initially targeting the U.S. residential and small office/home office (“SOHO”) markets.

Since our formation, we have devoted our resources to creating our initial phone/service bundles and establishing contractual relationships with our strategic communications services and manufacturing partners. Recently, we commenced our initial marketing efforts, focusing on securing approved vendor status with numerous national and regional retail channels. A vendor must obtain approved status before retailers will purchase from such vendor. We have obtained approved vendor status from retailers such as Staples, Best Buy, Fry’s, Brooks/Eckerd, Home Depot, Wal-Mart, K-Mart, JCPenney, Amazon.com, Target.com, Costco.com, Sears, JCPenney.com, Staples.com, CVS, QVC and Tiger Direct, of whom Staples, Brooks/Eckerd, Sears, CVS, QVC and Tiger Direct are current customers. The achieving of approved vendor status does not create an obligation on the part of the retailer to purchase our phone/service bundles or open their distribution channels to us.

We received our initial purchase orders in September 2005 and shipments of our phones began arriving in retail stores in October 2005. Subsequent to September 2005, we have received additional purchase orders and began fulfilling these orders in October 2005. We expect to recognize net revenues of approximately $290,000 and incur cost of revenues of approximately $218,000 during our fiscal quarter ended December 31, 2005, substantially all of which was attributable to the sale of our prepaid long distance phone/service bundles. We expect our selling, general and administrative expenses and other expenses during our fiscal quarter ended December 31, 2005 to be approximately $1,050,000 in the aggregate, inclusive of approximately $170,000 of expenses related to interest, amortization of debt discounts and amortization of debt issuance costs associated with our convertible notes. As of the date of this prospectus, both our prepaid long distance and VoIP phone/service bundles are available through our retail customers. We seek to expand our retail channels to include the following categories:

| • | Office superstores; |

| • | Electronics stores; |

| • | Drugstore chains; |

| • | Do-it-yourself retailers; |

| • | Mass retailers and department stores; |

| • | Internet-based retail distribution outlets; |

| • | Live shopping networks; and |

| • | Direct marketers. |

Our VoIP offering

Our VoIP offering provides customers with a DSS multi-handset, plug-and-play, broadband phone, a phone number and VoIP-based communications services, including inbound and outbound local calling service, long

1

Table of Contents

distance service, enhanced 911 emergency calling (which routes calls directly to emergency operators along with caller address information and automatic phone number identification) and other standard and competitive services.

The VoIP services accessible through our broadband phones are provided in the United States by SunRocket. SunRocket is a VoIP communications service provider founded by former executives of MCI, Inc. Under the terms of our agreement with SunRocket, purchasers of our broadband phones are offered an exclusive low-cost rate plan in addition to all other plans marketed by SunRocket to its customers. We receive an agreed-upon percentage of SunRocket’s monthly service revenues generated by users of our broadband phones.

Most currently available VoIP services require some combination of an adaptor, modem and/or router and often require cable companies or other service providers to engage in varying degrees of rewiring in the customer location to establish VoIP service. Our cordless broadband phone, however, is plugged directly into a customer’s Internet router or modem, without use of an adaptor or additional hardware, and does not require any complex rewiring. Our VoIP phone/service bundle can easily be installed by customers and requires no installation appointments with the cable company or other service provider. Our broadband phone may be used in rooms other than those with an Internet connection by carrying the wireless handset from room to room in the same manner as traditional cordless phones. Our multi-handset design allows customers to add additional handsets to their system and place extensions in other rooms without any rewiring. SunRocket provides VoIP services at what we believe are among the lowest rates currently available. Accordingly, we believe our VoIP phone/service bundle represents one of the easiest and most cost-efficient means for customers to acquire VoIP service.

Our prepaid long distance offering

Our phones that are bundled with prepaid long distance services are branded as “Pay N’ Talk” and marketed in the United States. Prepaid long distance service on each of these phones is accessible, on demand, with the press of the LDS (Long Distance Service) auto-key on the handset dial pad. This process provides the user with an immediate and seamless connection to prepaid long distance services provided by IDT. As a promotion, we are providing a specified number of initial minutes of long distance service at no additional charge to purchasers of these phone/service bundles. According to a 2005 report on prepaid markets by Atlantic-ACM, a telecommunications industry research firm, prepaid long distance service is an $11.8 billion global market that has experienced steady growth over the last ten years.

Under our agreement with IDT, prepaid long distance service is offered to our customers at a current rate of 3.9 cents per minute for domestic calls, inclusive of all fees and taxes. International calling is available at low, competitive per-minute rates under a rate plan that IDT created for our customers. Through IDT, our customers are able to purchase a specified number of minutes or create an automatic recharge account by which additional minutes are added whenever their account balance falls below pre-set limits. We believe that the prepaid long distance rates available to users of our phones will be among the lowest available for such service. We will receive an agreed-upon percentage of IDT’s monthly service revenues generated by users of our phones.

Our strategy

We believe that currently there are a limited number of providers of bundled communications phone/service offerings. Our objective is to expand and become a leader in the market for bundled communications phone/service offerings by combining our phones with attractively priced service offerings, thereby creating a compelling proposition for value purchasers. Key elements of our strategy include:

| • | developing high-quality end user communications hardware that enhances the accessibility and utility of the communications services with which our hardware is bundled; |

| • | expanding our existing relationships with SunRocket and IDT by expanding the communications services that are bundled with our hardware, expanding our joint marketing initiatives and increasing the retail distribution channels which we provide; |

2

Table of Contents

| • | establishing relationships with other providers of communications services inside and outside of the United States; |

| • | obtaining retail shelf space and Internet presence for our bundled communications phone/service offerings by utilizing our management’s broad retail experience and providing retailers the opportunity to share in our service revenues; and |

| • | utilizing our management’s extensive manufacturing and sourcing experience (particularly in China) to expand and diversify our supplier base for phone hardware, services and technology in order to maximize cost efficiency and support the diversification of our bundled communications phone/service offerings. |

Since we are an early stage company seeking to introduce new phone/service bundled offerings into a rapidly evolving communications market, we may not be successful in implementing some or all of the elements of our strategy. Our ability to implement our strategy will be subject to numerous risks, including those discussed in this prospectus under “Risk Factors.”

Private Placements

In June 2005, we issued and sold an aggregate of $50,000 principal amount of our 6% senior secured promissory notes, or “6% notes,” and common stock purchase warrants, or “private warrants,” to purchase 66,666 shares of our common stock. The aggregate purchase price of the 6% notes and private warrants was $50,000. During the period from July 2005 through September 2005, we issued and sold an aggregate of $2,113,500 in principal amount of our 8% senior secured promissory notes, or “8% notes,” and private warrants to purchase 1,409,001 shares of our common stock. The aggregate purchase price of the 8% notes and private warrants was $2,113,500. The terms of these securities are described in this prospectus under “Description of Securities.” All of these securities were sold to accredited investors under an exemption from the registration requirements (Section 4(2)) of the Securities Act of 1933. Upon consummation of this offering, all of the principal of and accrued interest on the 6% notes and 8% notes will convert into 750,240 shares of our common stock at a conversion price of $3.00 per share and all of the private warrants will be automatically converted into a like number of warrants of the same class as the redeemable warrants being sold in this offering. Such common stock and warrants, as well as the common stock issuable upon exercise of such warrants, have been registered for resale under the registration statement of which this prospectus forms a part.

Additional information

We were incorporated under the laws of the State of Delaware on June 16, 2003. Our principal offices are located at 2466 Peck Road, City of Industry, California, 90601 and our telephone number is (562) 908-1287.

3

Table of Contents

THE OFFERING

Securities offered | 2,800,000 shares of our common stock and 2,800,000 redeemable warrants. |

Common stock:

Number of shares outstanding before this offering | 2,750,240 shares, assuming, and giving effect to, the conversion of $2,163,500 principal amount of our outstanding notes (and all accrued and unpaid interest thereon, estimated at approximately $87,000) into 750,240 shares of our common stock upon the consummation of this offering. |

Number of shares to be outstanding after this offering | 5,550,240 shares. |

Redeemable warrants:

Number of redeemable warrants outstanding before this offering | 1,475,667 redeemable warrants, after giving effect to the issuance of such redeemable warrants in exchange for 1,475,667 of our outstanding private warrants. |

Number of redeemable warrants to be outstanding after this offering | 4,275,667 redeemable warrants. |

Exercisability | Each redeemable warrant is exercisable for the purchase of one share of our common stock. |

Exercise price | $5.05, subject to adjustment in the event of a stock dividend or split, reorganization, recapitalization or similar event. |

Exercise period | The redeemable warrants are exercisable immediately and will expire on February 1, 2011, or earlier upon redemption. |

Redemption | Subject to the prior consent of HCFP/Brenner Securities, we may redeem the outstanding redeemable warrants: |

| • | in whole and not in part; |

| • | at a price of $.05 per warrant; |

| • | upon a minimum of 30 days’ advance written notice of redemption; |

| • | if, and only if, the last sales price per share of our common stock equals or exceeds 190% (currently $9.60) during the first three months after the consummation of this offering, or 150% (currently $7.58) thereafter, of the then effective exercise price of the redeemable warrants for all 15 of the trading days ending within three business days before we send the notice of redemption; and |

| • | if, and only if, we then have an effective registration statement covering the shares issuable upon exercise of the redeemable warrants. |

4

Table of Contents

Use of proceeds | We intend to use the net proceeds from the sale of our securities in this offering for contract manufacturing and shipping and warehousing of inventory; for sales and marketing activities, including salaries and fees of sales and marketing personnel and consultants; for product enhancement and new product development; for the purchase and/or lease of tooling equipment; for the purchase and/or lease of office equipment; and for working capital and general corporate purposes. See “Use of Proceeds.” |

Proposed American Stock Exchange symbols for our:

Common stock | “TES” |

Warrants | “TES.WS” |

Unless otherwise indicated, information contained in this prospectus regarding the number of shares of our common stock that will be outstanding after this offering includes the 750,240 shares of common stock issuable upon conversion of the outstanding principal of our notes and all accrued interest thereon concurrently with the consummation of this offering, but does not include up to an aggregate of 6,275,667 shares comprised of:

| • | 2,800,000 shares reserved for issuance upon exercise of the redeemable warrants to be sold in this offering; |

| • | 1,475,667 shares reserved for issuance upon exercise of the redeemable warrants issued in exchange for the private warrants; |

| • | 420,000 shares reserved for issuance upon exercise of the underwriters’ over-allotment option and 420,000 shares reserved for issuance upon exercise of the redeemable warrants issuable upon exercise of the underwriters’ over-allotment option; |

| • | 280,000 shares reserved for issuance upon exercise of the representative’s purchase option and 280,000 shares reserved for issuance upon exercise of the redeemable warrants issuable upon exercise of the representative’s purchase option; and |

| • | 600,000 shares reserved for the grant of restricted stock and issuance upon exercise of options that will or may be granted under our 2005 stock option plan, including (i) options exercisable for an aggregate of 195,000 shares that will be granted upon consummation of this offering, comprised of options exercisable for an aggregate of 150,000 shares that will be granted to our officers, employee-directors and certain affiliates and 45,000 of which will be granted to our non-employee directors, each with an exercise price of $5.05 per share and (ii) an aggregate of 325,000 shares of performance accelerated restricted stock to be granted to our executive officers, our Chairman and one consultant upon consummation of this offering. In addition, after consummation of this offering, each of our non-employee directors will receive options to purchase 5,000 shares per quarter at an exercise price per share equal to not less than the fair market value per share of our common stock at the time of grant. |

In addition, unless otherwise indicated, information contained in this prospectus regarding the number of redeemable warrants that will be outstanding after this offering includes 1,475,667 redeemable warrants issuable in exchange for the private warrants, but does not include:

| • | the 420,000 redeemable warrants issuable upon exercise of the underwriters’ over-allotment option; or |

| • | the 280,000 redeemable warrants issuable upon exercise of the representative’s purchase option. |

5

Table of Contents

The table below provides summary financial information as of the date indicated. You should read this information with our financial statements and the related notes and the section entitled “Plan of Operations,” all of which are included in this prospectus.

| For the fiscal year ended June 30, | For the three months ended September 30, | For the period from June 16, 2003 (inception) to September 30, 2005 | ||||||||||||||||||

| Statement of Operations: | 2005 | 2004 | 2005 | 2004 | ||||||||||||||||

Revenues | $ | — | $ | — | $ | — | $ | — | $ | — | ||||||||||

Expenses: | ||||||||||||||||||||

Marketing and development | 84,813 | 22,058 | 116,703 | 3,233 | 223,574 | |||||||||||||||

General and administrative | 84,435 | 3,000 | 188,563 | 6,027 | 275,998 | |||||||||||||||

Total expenses | 169,248 | 25,058 | 305,266 | 9,260 | 499,572 | |||||||||||||||

Other expenses: | ||||||||||||||||||||

Interest and bank charges | 75 | — | 35,721 | — | 35,796 | |||||||||||||||

Amortization of debt discounts and debt issuance costs | 925 | — | 77,709 | — | 78,634 | |||||||||||||||

Net loss | $ | (170,248 | ) | $ | (25,058 | ) | $ | (418,696 | ) | $ | (9,260 | ) | $ | (614,002 | ) | |||||

Net loss per common share: | ||||||||||||||||||||

Basic and diluted | $ | (0.09 | ) | $ | (0.01 | ) | $ | (0.21 | ) | $ | — | |||||||||

Weighted average shares outstanding: | ||||||||||||||||||||

Basic and diluted | 1,996,261 | 1,740,490 | 2,000,000 | 1,984,833 | ||||||||||||||||

| As of September 30, 2005 | ||||||

| Balance Sheet Data: | Actual | As adjusted | ||||

Working capital | $ | 1,176,572 | $ | 13,261,954 | ||

Cash and cash equivalents | $ | 1,334,018 | $ | 13,419,400 | ||

Total assets | $ | 2,259,851 | $ | 13,777,645 | ||

Total liabilities | $ | 883,098 | $ | 515,691 | ||

Shareholders’ equity | $ | 1,376,753 | $ | 13,261,954 | ||

The “as adjusted” information as of September 30, 2005 gives effect at that date to the following events:

| • | the automatic conversion upon the consummation of this offering of all $2,163,500 principal amount of our outstanding notes and all accrued and unpaid interest thereon (approximately $87,000); and |

| • | our receipt of the estimated net proceeds (i.e., gross proceeds less the underwriting discount and the estimated offering expenses payable by us from the offering proceeds) from the sale of 2,800,000 shares of our common stock and 2,800,000 warrants in this offering and our anticipated application of those proceeds. See “Use of Proceeds.” |

6

Table of Contents

An investment in our securities involves a high degree of risk. You should consider carefully all of the material risks described below, together with the other information contained in this prospectus before making a decision to invest in our securities.

Risks related to our business

We only recently commenced our commercial operations, have a very limited operating history and our independent registered public accountants have issued an explanatory paragraph in their opinion in connection with our financial statements that expresses substantial doubt about our ability to continue as a going concern unless we obtain the financing sought in this offering.

We were incorporated in June 2003 and only recently completed the development of our first phones and secured our initial strategic relationships with communications service and manufacturing service providers. We have only recently received our first purchase orders and made initial shipments of our phones in September 2005. We generated no revenues during the fiscal year ended June 30, 2005 and the three months ended September 30, 2005. We expect to recognize net revenues of approximately $290,000 and incur cost of revenues of approximately $218,000 during our fiscal quarter ended December 31, 2005. We expect our selling, general and administrative expenses and other expenses during our fiscal quarter ended December 31, 2005 to be approximately $1,050,000 in the aggregate, inclusive of approximately $170,000 of expenses related to interest, amortization of debt discounts and amortization of debt issuance costs associated with our convertible notes. Revenue from the sales of our phones is recognized when title and risk of loss transfer to our retail customers in accordance with the terms of an agreement, assuming all other revenue recognition criteria are met based on our revenue policy. We have no real operating history upon which you can evaluate our business strategy or future prospects, and have negative working capital. As a result, our independent registered public accounting firm has issued an explanatory paragraph in their opinion in connection with our financial statements included herein that expresses substantial doubt about our ability to continue as a going concern unless we obtain the financing sought in this offering. While this offering addresses such concern, our ability to generate revenues going forward that are capable of supporting our operations without other financing sources will depend on whether we can successfully commercialize our phones and make the transition from a development stage company to an operating company. We may not achieve and/or sustain profitability. In making your evaluation of our prospects, you should consider that we are an early-stage business engaged principally in the development and marketing of bundled communications phone/service offerings that have minimal, if any, proven market acceptance. We operate in a rapidly evolving industry. As a result, we may encounter many expenses, delays, problems and difficulties that we have not anticipated and for which we have not planned.

The agreements with the strategic partners that provide the communications services accessible through our phones require us to meet certain minimum requirements, which, if not met, could lead to our loss of certain material rights.

Under our agreements with SunRocket and IDT, users of our phones must activate certain minimum numbers of accounts with these providers within certain time periods. Under our agreement with IDT, users of our phones must activate at least 150,000 accounts by December 31, 2006. If we do not meet this requirement, IDT, in its discretion, may terminate our agreement or renegotiate its terms. Under our agreement with SunRocket, we were required to activate at least 10,000 accounts by December 31, 2005 in order to retain exclusivity as to a particular sub-$10 pricing plan. Since we only recently commenced operations, we did not meet this requirement, thereby affording SunRocket the right, but not the obligation, to treat our exclusive pricing plan as nonexclusive. We have had no indication to date that SunRocket will terminate our exclusivity as to that particular rate plan. Although arrangements similar to those we currently have with our strategic partners may be readily available from other communications providers, we cannot assure you that we would be able to secure such alternate arrangements on a timely basis or at all or efficiently configure our phones to work seamlessly with such services. Our failure to maintain our agreements with our current strategic partners or to secure alternate arrangements with other communications service providers if needed on substantially similar terms could materially adversely affect our ability to favorably price our offerings to customers and could harm our operating margins and financial results.

7

Table of Contents

If we are unable to effectively manage the transition from development stage to commercial operations, our financial results will be negatively affected.

For the period from our inception in June 2003 through September 2005, we have incurred aggregate net losses in our development stage of $614,002 and had an accumulated deficit of $614,002 as of September 30, 2005. Upon consummation of our initial public offering, such losses would increase by a non-cash interest charge of approximately $2.3 million resulting from the amortization of the carrying value of the original issue discount due to the immediate conversion of the notes issued in our private placement into shares of common stock and the amortization of the carrying value of debt issuance costs. Our losses are expected to increase in the short term as we commence full scale manufacturing, marketing and deployment of our phone/service bundles and transition from a development stage company to an operating company. As we make such transition, we expect our business to grow significantly in size and complexity. This growth is expected to place significant additional demands on our management, systems, internal controls and financial and physical resources. As a result, we will need to expend additional funds to secure necessary assets and hire additional qualified personnel for our marketing activities, for the development of appropriate control systems and for the expansion of our information technology and operating infrastructures. Our inability to secure additional resources and personnel, as and when needed, or manage our growth effectively, if and when it occurs, would significantly hinder our transition to an operating company, as well as diminish our prospects of generating revenues and, ultimately, achieving profitability.

Our failure to quickly and positively distinguish our phone/service bundles from other available communications solutions could limit the adoption curve associated with their market acceptance and negatively affect our operations.

We may be slow to achieve, or may never achieve, market acceptance for our phone/service bundles. Failure to distinguish our phones and services from competing communications solutions would hinder market acceptance of our phone/service bundles. Meaningful numbers of customers may not be willing to adopt our phones and services until they have been proven, both initially and over time, to be viable communications solutions. There is also no way to determine the adoption curve that will be associated with our phone/service bundles. Non-acceptance or delayed acceptance of our phones and/or services could force reductions in contemplated sales prices of our phones, reduce our overall sales and gross margins and negatively affect our operations and prospects.

We may not be able to meet our future capital requirements solely through revenues generated from our operations, and the cost of additional equity or debt capital could be prohibitive or result in dilution to existing securityholders.

Our business model is capital intensive, requiring significant expenditures ahead of projected revenues. Based on our current operating plan, we anticipate that the net proceeds of our previous 2005 financings and this offering, together with anticipated revenues from operations and accounts receivable financing that we believe will be available to us, will allow us to meet our cash requirements for approximately 12 months following the date of this prospectus. If revenues from operations are not sufficient to meet all of our capital needs after such time, or we do not obtain accounts receivable financing, we will need to obtain additional sources of capital. Further, if the assumptions currently underlying our business plan prove incorrect, we may need to seek additional financing prior to that time. In addition, if and when we achieve initial market acceptance for our initial phone/service bundles, we may desire to accelerate our growth to take advantage of increasing demand. Accordingly, we may wish to raise additional capital to offset increased capital expenditures and costs associated with accelerated growth. Any source of additional capital could be in the form of public or private equity or debt financing. Such financing may not be available to us on commercially reasonable terms, or at all. If additional capital is needed and is either unavailable or cost prohibitive, we may need to change our business strategy or reduce or curtail our operations. In addition, if we raise additional funds by issuing equity securities, our securityholders will experience dilution.

8

Table of Contents

Our business may be materially and adversely affected by our high level of debt.

In order to finance the potential growth of our business, we may incur debt, including loans or convertible debt financing, in the future. A high level of debt, arduous or restrictive terms and conditions related to accessing certain sources of funding, poor business performance or lower than expected cash inflows could materially and adversely affect our ability to fund the operation of our business. Other effects of a high level of debt include the following:

| • | we may have difficulty borrowing money in the future or accessing other sources of funding; |

| • | we may need to use a large portion of our cash flow from operations to pay principal and interest on our indebtedness, which would reduce the amount of cash available to finance our operations and other business activities; |

| • | a high debt level, arduous or restrictive terms and conditions, or lower than expected cash flows would make us more vulnerable to economic downturns and adverse developments in our business; and |

| • | if operating cash flows are not sufficient to meet our operating expenses, capital expenditures and debt service requirements as they become due, we may be required, in order to meet our debt service obligations, to delay or reduce capital expenditures or the introduction of new phones, sell assets and/or forego business opportunities. |

Our inability to establish cost-effective sales channels would negatively affect our revenue potential.

While we have secured approved vendor status with numerous national and regional retailers, there is no obligation for these retailers to purchase our phone/service bundles or open their distribution channels to us. We currently have only limited internal sales, marketing and distribution capabilities. In order to commercialize our phones and services, we will have to develop a sales and marketing infrastructure and/or rely on third parties to perform these functions. To market directly, we will have to develop a marketing and sales force with technical expertise, which would require the dedication of significant capital, management resources and time. We could also be required to expend significant capital and other resources in developing third-party distribution channels. Further, any agreement to sell our phones and services through a third party could hamper our ability to sell our phones and services to that third party’s competitors. Due to our limited financial resources, we may not be able to establish an appropriate sales force or make adequate third-party distribution arrangements. Our failure to do so would limit our ability to expand sales and would negatively affect our operations, financial results and long-term growth.

Failure to obtain satisfactory performance from our strategic and contract manufacturing partners and other third party vendors on whom we will be dependent for our phones and services could cause us to lose sales, incur additional costs and lose credibility in the market place.

We will rely on third-party sources to manufacture our phones and will rely on third-party communications service providers to provide users of our phones with communications services. The failure of any of these third party providers to perform satisfactorily or the loss of any of them could cause us to fail to meet customer expectations, lose sales and expose us to product and service quality issues. In turn, this could damage our relationships with customers and harm our reputation, business, financial condition and results of operations. If our third-party providers increase their prices and we do not have access to alternative providers, we could be required to raise the price of our phone/service bundles to customers to cover all or part of the increased costs. Our inability to obtain phones and services at the prices we desire could hurt our sales and lower our margins. Generally, we will not own or control the vast majority of the equipment, tools and molds used in the manufacturing process. As a result, difficulties encountered by our third-party manufacturers that result in product defects, production delays, cost overruns or the inability to fulfill orders on a timely basis could harm our operations. Our operations would be adversely affected if we were to lose our relationships with our primary suppliers, if our suppliers’ operations were interrupted or terminated, or if overseas or air transportation services were disrupted, even for a relatively short period of time. We do not expect to maintain a product inventory that is sufficient to provide protection for any significant period against an interruption of the supply of our hardware.

9

Table of Contents

We currently rely on a limited number of manufacturers for the production of our phone hardware and a limited number of service providers for the provision of the communications services accessible through our phones and the loss of any of their services could be disruptive to our operations.

We currently rely substantially on one outside manufacturer to produce our phone hardware and on SunRocket and IDT for the provision of the communications services accessible through our phones. The loss of service of any of our suppliers would require us to find alternative suppliers. While we believe such alternative suppliers are readily available, securing relationships with alternative suppliers and integrating them into our business process would take time and could require us to make significant expenditures.

Since our hardware will be sourced from parties outside of the United States, we will face certain risks inherent in conducting business in foreign countries.

We will produce our phones under manufacturing arrangements with third-party manufacturers, including those located in China. Our reliance on our third-party manufacturers to provide personnel and facilities in their country of operations and the potential imposition of quota limitations on imported goods from certain Asian countries expose us to certain economic and political risks, including transportation delays and interruptions, political instability, the business and financial condition of our third party manufacturer, the possibility of expropriation, supply disruption, currency controls, and currency exchange fluctuations, changes in tax laws, tariffs, and freight rates, as well as strikes, work slow downs, or lockouts at ports where our phones arrive in the United States. Protectionist trade legislation in either the United States or foreign countries, such as a change in the current tariff structures, export compliance laws, or other trade policies, could adversely affect our ability to purchase our phones from foreign suppliers at a price that will enable us to sell those phones profitably.

We may not be successful if the Internet is not adopted by a significant number of users as a means of communications.

If the market for IP-based communications and the related services that we will make available does not grow at the rate we anticipate or at all, we will not be able to realize our anticipated revenues with respect to our broadband phones. To be successful, IP-based communications require validation as an effective means of communication and as a viable alternative to traditional phone service. Demand and market acceptance for newly introduced services are subject to a high level of uncertainty. The Internet may not prove to be a viable alternative to traditional phone service for reasons including:

| • | inconsistent quality or speed of service; |

| • | traffic congestion on the Internet; |

| • | potentially inadequate development of the necessary infrastructure; |

| • | lack of acceptable security technologies; |

| • | lack of timely development and commercialization of performance improvements; and |

| • | unavailability of cost-effective, high-speed access to the Internet. |

A significant number of the companies with which we will compete have substantially greater resources and longer operating histories than we do, and we may not be able to compete with them effectively, even if our phones and services are technically superior.

We engage in an intensely competitive business that has been characterized by price erosion, rapid technological change and foreign competition. We will compete with major domestic and international companies. Many of our competitors have greater market recognition and substantially greater financial, technical, marketing, distribution, and other resources than we possess. Emerging companies also may increase their participation in the phone hardware or communications service markets. Our ability to compete successfully depends on a number of factors both within and outside our control, including:

| • | the quality, performance, reliability, features, ease of use, pricing, and diversity of our phones and the communications services accessed through them; |

| • | our ability to address the evolving demands of our customers; |

10

Table of Contents

| • | our success in designing and manufacturing new phones, including those implementing new technologies and services; |

| • | the availability of adequate sources of raw materials, finished components, and other supplies at acceptable prices; |

| • | our suppliers’ efficiency of production; |

| • | new product introductions by our competitors; |

| • | the number, nature, and success of our competitors in a given market; and |

| • | general market and economic conditions. |

Decreasing telecommunications rates may diminish or eliminate any competitive pricing advantage we may have previously established.

International and domestic telecommunications rates have decreased significantly over the last few years in most of the markets in which we expect to operate, and we anticipate that rates will continue to be reduced in all of the markets in which we expect to do business. Decreasing telecommunications rates may diminish or eliminate any competitive pricing advantage we may have previously been able to establish for the communications services available to our hardware users. Purchasers who select our services to take advantage of the current pricing differential between our rates and rates otherwise available to them for the same service may not purchase our phones if such pricing differentials diminish or disappear. In addition, rate decreases would reduce our gross profit margin from the services we make available to purchasers of our phones and services.

Government regulation and legal uncertainties relating to VoIP telephony could harm our business.

Historically, voice communications services have been provided by regulated telecommunications common carriers. For some of our phones, we will offer voice communications to the public for international and domestic calls using VoIP telephony. Based on specific regulatory classifications and recent regulatory decisions, we believe such services qualify for certain exemptions from telecommunications common carrier regulation in many of our markets. However, the growth of VoIP telephony has led to close examination of its regulatory treatment in many jurisdictions, making the legal status of such services uncertain and subject to change as a result of future regulatory action, judicial decisions or legislation in the jurisdictions in which we expect to operate. Established regulated telecommunications carriers have sought and may continue to seek regulatory actions to restrict the ability of companies such as our communications service providers to provide services or to increase the cost of providing such services. In addition, such services may be subject to regulation if regulators distinguish between phone-to-phone telephony service using VoIP and other technologies over privately-managed networks, such as our services, and integrated PC-to-PC and PC-originated voice services over the Internet. Some regulators may decide to treat the former as regulated common carrier services and the latter as unregulated enhanced or information services. Application of new regulatory restrictions or requirements to our service providers could increase our cost of doing business or otherwise prevent or restrict us from delivering our services through our current arrangements. Such regulations could limit our service phone/service bundles, raise our costs and restrict our pricing flexibility, and potentially limit our ability to compete effectively.

If we don’t enhance our phone/service bundles and develop new phones and services to keep pace with rapid technological and consumer demand changes in the communications industry, we may lose any market share we were previously able to establish.

Our industry is subject to rapid changes in technology and consumer demand. We cannot predict the effect of technological changes or the changes of consumer demand on our business. In addition, widely accepted standards have not yet developed for the technologies we use, such as VoIP. We expect that new services and technologies will emerge over time in the markets in which we compete. These new services and technologies may be superior to the services and technologies that we make available, or these new services may render the

11

Table of Contents

services and technologies that we make available obsolete or less attractive to consumers. To be successful, we must adapt to our rapidly changing market by continually improving and expanding the scope of services we make available and by developing new services and technologies to meet consumer needs.

The loss of any of the members of our management or certain other key personnel could harm our business.

Our development and operations to date have been, and our proposed operations will be, substantially dependent upon the efforts and abilities of our senior management and technical personnel. Although, prior to the consummation of this offering, we will acquire $3,000,000 of key-person life insurance on the life of Bruce Hahn, our Chief Executive Officer, the loss of his services or the services of other existing key personnel or the failure to recruit and retain necessary additional personnel would adversely affect our business prospects. We cannot provide assurance that we will be able to retain our current personnel or that we will be able to attract and retain necessary additional personnel. Our internal growth and the expansion of our product lines will require additional expertise in such areas as product design, operational management, and sales and marketing. Such growth and expansion activities will increase further the demand on our resources and require the addition of new personnel and the development of additional expertise by existing personnel. Our failure to attract and retain personnel possessing the requisite expertise or to develop such expertise internally could adversely affect the prospects for our success.

Our business may suffer if it is alleged or found that our phones infringe the intellectual property rights of others.

Although we attempt to avoid infringing known proprietary rights of third parties in our product development efforts, from time to time we may receive notice that a third party believes that our phones may be infringing certain trademarks, patents or other intellectual property rights of that third party. We may also be contractually obligated to indemnify our customers or other third parties associated with our phones in the event they are alleged to infringe a third party’s intellectual property rights in connection with our phones. Responding to those claims, regardless of their merit, can be time consuming, result in costly litigation, divert management’s attention and resources and cause us to incur significant expenses. Thus, even if our phones do not infringe, we may elect to take a license or settle to avoid incurring such costs. In the event our phones are infringing upon the intellectual property rights of others, we may elect or be required to redesign our phones so that they do not incorporate any intellectual property to which the third party has or claims rights. As a result, some of our phone/service bundles could be delayed, or we could be required to cease distributing some of our phones. Alternatively, we could seek a license for the third party’s intellectual property, but it is possible that we would not be able to obtain such a license on reasonable terms, or at all. Any delays that we might then suffer or additional expenses that we might then incur could adversely affect our revenues, operating results and financial condition.

Risks related to this offering

The American Stock Exchange may delist our securities from quotation on its exchange which could limit investors’ ability to make transactions in our securities and subject us to additional trading restrictions.

We expect our securities will be approved for initial listing on the American Stock Exchange. We cannot assure you that our securities will continue to be listed on the American Stock Exchange in the future. If the American Stock Exchange delists our securities from trading on its exchange, we could face significant material adverse consequences including:

| • | a limited availability of market quotations for our securities; |

| • | a determination that our common stock is a “penny stock” which will require brokers trading in our common stock to adhere to more stringent rules and possibly resulting in a reduced level of trading activity in the secondary trading market for our common stock; |

| • | a limited amount of analyst coverage for our company, and |

| • | a decreased ability to issue additional securities or obtain additional financing in the future. |

12

Table of Contents

If our common stock becomes subject to the SEC’s penny stock rules, broker-dealers may experience difficulty in completing customer transactions and trading activity in our securities may be severely limited.

If at any time we have net tangible assets of $5,000,000 or less and our common stock has a market price per share of less than $5.00, transactions in our common stock may be subject to the “penny stock” rules promulgated under the Securities Exchange Act of 1934. Under these rules, broker-dealers who recommend such securities to persons other than institutional investors:

| • | must make a special written suitability determination for the purchaser; |

| • | receive the purchaser’s written agreement to a transaction prior to sale; |

| • | provide the purchaser with risk disclosure documents which identify risks associated with investing in “penny stocks” and which describe the market for these “penny stocks” as well as a purchaser’s legal remedies; and |

| • | obtain a signed and dated acknowledgment from the purchaser demonstrating that the purchaser has actually received the required risk disclosure document before a transaction in a “penny stock” can be completed. |

As a result of these requirements, broker-dealers may find it difficult to effectuate customer transactions and trading activity in our stock will be significantly limited. Accordingly, the market price of our stock may be depressed, and you may find it more difficult to sell your shares.

Future sales of our common stock may cause the prevailing market price to decrease and impair our capital raising abilities.

Immediately following this offering, we will have options and warrants outstanding that are exercisable for the purchase of an aggregate of 4,835,667 shares of our common stock, comprised of the 2,800,000 redeemable warrants issued in this offering, the 1,475,667 redeemable warrants that will be issued in exchange for our outstanding private warrants, the option to purchase 280,000 shares (and the 280,000 warrants purchasable under such option, which are exercisable for the purchase of an additional 280,000 shares) issued to the representative. Following this offering, we also will have granted or may grant options and other stock-based awards for up to an aggregate of 600,000 shares of our common stock under our 2005 stock option plan. If, and to the extent, outstanding options and warrants are exercised, you will experience dilution to your holdings. An aggregate of 2,225,907 shares of common stock and 1,475,667 warrants are being registered for resale under the registration statement of which this prospectus forms a part. Except for 79,926 shares and 58,333 redeemable warrants beneficially owned by Lawrence Burstein, our Chairman, which shares and warrants are subject to the lock-up agreement described in the following sentence, such shares and warrants will be immediately saleable into the market following the completion of this offering. Our officers, directors and principal securityholders and certain of their family members have entered into lock-up agreements with the representative by which they have agreed not to sell or otherwise dispose of any shares of our common stock (other than an aggregate of 200,000 shares as a group) for a period of 12 months after the later of the date of this prospectus and the date any state or regulatory agency imposed lockups placed upon them have expired. After this lock-up period, however, these securityholders may sell their shares. We cannot predict whether following this offering substantial amounts of our common stock and/or warrants will be sold in the open market in anticipation of, or following, any future divestiture of our shares by these or other of our officers, directors or principal securityholders. In addition, after this offering, we will have more than 28.8 million shares of our common stock authorized and not yet issued or reserved against. In general, we may issue all of these shares, as well as 5,000 shares of preferred stock which may have rights and preferences superior to that of our common stock, without any action or approval by our securityholders. If a large number of shares of our common stock are sold in the open market after this offering, or if the market perceives that such sales will occur as a result of any of the foregoing, the trading price of our common stock could decrease. In addition, the sale of these shares could impair our ability to raise capital through the sale of additional common stock.

13

Table of Contents

Failure to maintain a current prospectus relating to the common stock underlying the redeemable warrants may deprive the redeemable warrants of any value and the market for the redeemable warrants may be limited.

No redeemable warrants will be exercisable unless at the time of exercise a prospectus relating to common stock issuable upon exercise of the redeemable warrants is current and the common stock has been registered or qualified or deemed to be exempt under the securities laws of the state of residence of the holder of the redeemable warrants. Under the terms of the warrant agreement, we have agreed to meet these conditions and to maintain a current prospectus relating to common stock issuable upon exercise of the redeemable warrants until the expiration of the redeemable warrants. However, we cannot assure you that we will be able to do so. The redeemable warrants may be deprived of any value and the market for the redeemable warrants may be limited if the prospectus relating to the common stock issuable upon the exercise of the redeemable warrants is not current or if the common stock is not qualified or exempt from qualification in the jurisdictions in which the holders of the redeemable warrants reside.

As we do not anticipate paying cash dividends, you should not expect any return on your investment except through appreciation, if any, in the value of our common stock.

You should not rely on an investment in our common stock to provide dividend income, as we have not paid any cash dividends on our common stock and do not plan to pay dividends on our common stock in the foreseeable future. Thus, if you are to receive any return on your investment in our common stock it will likely have to come from the appreciation, if any, in the value of our common stock. The payment of future cash dividends, if any, will be reviewed periodically by the board of directors and will depend upon, among other things, our financial condition, funds from operations, the level of our capital and development expenditures, any restrictions imposed by present or future debt instruments and changes in federal tax policies, if any.

Our officers, directors and affiliated entities own a large percentage of our company, and they could make business decisions with which you disagree that will affect the value of your investment.

We anticipate that our executive officers, directors and other 5% or greater securityholders will, in total, beneficially own approximately 28.4% of our outstanding common stock after this offering. These securityholders will be able to influence significantly all matters requiring approval by our securityholders, including the election of directors. Thus, actions might be taken even if other securityholders, including those who purchase shares in this offering, oppose them. This concentration of ownership might also have the effect of delaying or preventing a change of control of our company, which could cause our stock price to decline.

Our management will have substantial discretion over the use of proceeds of this offering and may not apply them effectively.

Our management will have significant flexibility in applying the net proceeds of this offering and may apply the proceeds in ways with which you do not approve. Although the proposed allocation of the net proceeds of this offering represents our management’s best estimate of the expected utilization of funds to finance our activities in accordance with our management’s current objectives and market conditions, the failure of our management to apply these funds effectively could materially harm our business.

Our founders and other existing securityholders effectively paid or will have paid prices for their shares of common stock that are substantially lower than the price being paid by investors in this offering and, accordingly, you will experience immediate and substantial dilution from the purchase price of our common stock.

The difference between the public offering price per share of our common stock and the pro forma net tangible book value per share of our common stock after this offering constitutes the dilution to you and the other investors in this offering. The fact that our founders acquired their shares of common stock at par value ($.001 per share) and holders of our notes will effectively acquire their shares of common stock upon conversion of their

14

Table of Contents

notes at a price of $3.00 per share will significantly contribute to this dilution. New investors will incur an immediate and substantial dilution of approximately 53% or $2.66 per share (the difference between the as adjusted net tangible book value per share of $2.39 and the initial offering price of $5.05 per share).

Provisions in our corporate documents and our certificate of incorporation and bylaws, as well as Delaware General Corporation Law, may hinder a change of control.

Provisions of our certificate of incorporation and bylaws, as well as provisions of the Delaware General Corporation Law, could discourage unsolicited proposals to acquire us, even though such proposals may be beneficial to you. These provisions include:

| • | a classified board of directors that cannot be replaced without cause by a majority vote of our securityholders; |

| • | our board of director’s authorization to issue shares of preferred stock, on terms as the board of directors may determine, including terms superior to those provided by our common stock, without securityholder approval; and |

| • | provisions of Delaware General Corporation Law that restrict many business combinations. |

We are also subject to the provisions of Section 203 of the Delaware General Corporation Law, which could prevent us from engaging in a business combination with a 15% or greater securityholder for a period of three years from the date it acquired that status unless appropriate board or securityholder approvals are obtained.

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes “forward-looking statements” based on our current expectations, assumptions, estimates and projections about our business and our industry. They include statements relating to, among other things:

| • | future revenues, expenses and loss or profitability; |

| • | the completion and commercialization of one or more of our phones; |

| • | projected capital expenditures; |

| • | competition; |

| • | the effectiveness, quality and cost of our intended phones and services; |

| • | anticipated trends in the telecommunications industry; and |

| • | the marketability of our bundled communications solutions as a cost effective, easily deployable and comparable or higher quality alternative to existing solutions. |

You can identify forward-looking statements by the use of words such as “may,” “should,” “will,” “could,” “estimates,” “predicts,” “potential,” “continue,” “anticipates,” “believes,” “plans,” “expects,” “future” and “intends” and similar expressions which are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements. In evaluating these forward-looking statements, you should carefully consider the risks and uncertainties described in “risk factors” and elsewhere in this prospectus. These forward-looking statements reflect our view only as of the date of this prospectus. All forward-looking statements attributable to us or persons acting on our behalf are expressly qualified in their entirety by the cautionary statements and risk factors contained throughout this prospectus.

15

Table of Contents

We estimate that the aggregate net proceeds to us from the sale of the 2,800,000 shares of our common stock and 2,800,000 redeemable warrants in this offering will be approximately $12,032,000, after deducting the underwriting discount and expenses and approximately $820,000 of estimated offering expenses that will be payable by us from the proceeds of this offering.

We expect to use these net proceeds for the following purposes:

| Dollar Amount | Percent | |||||

Contract manufacturing of phones and related components | $ | 9,250,000 | 77.0 | % | ||

Sales and marketing, including salaries of personnel | 800,000 | 6.6 | ||||

Product enhancement and new product development | 350,000 | 2.9 | ||||

Tooling | 150,000 | 1.2 | ||||

Purchase and/or lease of office equipment | 150,000 | 1.2 | ||||

Working capital and general corporate purposes | 1,332,000 | 11.1 | ||||

TOTAL | $ | 12,032,000 | 100.0 | % | ||

We expect that the net proceeds from this offering will enable us to:

| • | expand manufacturing and commercial distribution of our multi-handset, cordless phones bundled with Pay N’ Talk prepaid long distance provided by IDT and our digital, multi-handset broadband phones bundled with VoIP services provided by SunRocket; |

| • | develop enhanced product features and additional service features and design and develop new phone/service bundles; and |

| • | expand our sales and marketing capabilities. |

We intend to use approximately $9,250,000 of the net proceeds of this offering for the contract manufacturing of our multi-handset cordless phones for bundling with Pay N’ Talk prepaid long distance services, and our digital, multi-handset broadband phones for bundling with VoIP services, as well as for the purchase of related components and the shipping and warehousing of completed inventory. Manufacturing of our phones and components will be done to our specifications based upon our designs and will be provided on a contract basis by overseas providers. Although we intend to carry inventory, the actual amount of proceeds expended on our design, engineering and manufacturing efforts and the allocation of such proceeds between our phone/service bundles will depend on actual demand for our phones.

We intend to use approximately $800,000 of the net proceeds of this offering to support and expand our sales and marketing infrastructure and activities. These expenses shall include (i) the payment of fees to Future Marketing, LLC (a multi-person marketing and sales company under common ownership with The Future, LLC, one of our founding shareholders) that, among other things, assists in the development and execution of our marketing plans, manages our accounts, assists in our product development and handles our back-office customer functions, (ii) the payment of salaries and benefits for existing and newly hired marketing, sales and project management personnel, including certain salaries accrued since July 1, 2005, (iii) costs associated with the development of packaging, advertising, retail displays and collateral marketing materials and (iv) costs related to the establishment of sales channels into targeted retail outlets.

We intend to use approximately $350,000 of the net proceeds of this offering for product enhancement and development and related activities. This amount includes approximately $275,000 for sourcing and internal design of product improvements and new phones, as well as for external engineering and product development conducted in China through companies we presently utilize for manufacturing services, and approximately $75,000 for technology and support services in the United States to coordinate our overseas development efforts.

We intend to use approximately $150,000 of the net proceeds of the offering for the design and development of tools (molds) in cooperation with our third-party contract manufacturers of our next generation of multi-handset Pay N’ Talk phones and multi-handset broadband phones.

16

Table of Contents

We intend to use approximately $150,000 of the net proceeds of this offering for the purchase and/or lease of computers and other equipment and for the installation of computer systems and office equipment at our offices in Atlanta, Georgia, City of Industry, California and our overseas office in Shanghai, China.

The remaining net proceeds of this offering will be allocated to working capital and general corporate purposes, including payments to our service providers, office space lease payments, directors and officers insurance premiums, salaries and benefits for executive and administrative personnel, including travel and associated expenses, and other general and administrative costs.

The above represents our best estimate of the allocation of net proceeds of this offering. We may, as our development and marketing efforts progress, find it necessary to reallocate a portion of the proceeds within the above-described categories or use portions of the proceeds for other purposes, including for acquisitions of complementary businesses, phones or technologies; however, we have no current agreements or commitments to make any potential acquisition. In addition, our estimates may prove to be inaccurate, new phones or product changes may be undertaken which may require us to modify manufacturing requirements and/or product delivery schedules, or which may require additional expenditures and/or unforeseen expenses may occur.

Based on current assumptions relating to our business plan, we anticipate that the net proceeds of this offering, together with certain baseline levels of anticipated revenues and accounts receivable financing, will satisfy our capital requirements for approximately 12 months following the consummation of this offering. These assumptions include the following:

| • | our initial phones are produced, shipped and delivered on schedule; |

| • | expected customer purchase commitments for phones are received; |

| • | end users who purchase our bundled services remain active users of such services at anticipated rates; |

| • | we are able to secure necessary accounts receivable financing; and |

| • | customers pay for our phones in a timely manner. |

If we determine to accelerate our business plan or if our plans otherwise change or our assumptions prove inaccurate, we may need to seek financing sooner than currently anticipated, incur additional financing or reduce or curtail our operations. We cannot assure you that financing will become available as and when needed. We have broad discretion over the ultimate specific allocation of the proceeds of this offering.

If the underwriters exercise their over-allotment option in full, we will realize additional net proceeds of approximately $1,970,640, which will be added to our working capital. All or a portion of these over-allotment proceeds may be used to acquire complementary businesses or technologies or otherwise obtain the right to use complementary technologies that could broaden or enhance our phones. However, we have no current agreements or commitments to make any potential acquisition. In addition, if the 2,800,000 redeemable warrants offered pursuant to this prospectus and the 1,475,667 redeemable warrants issued in exchange for our private warrants are exercised, we will realize proceeds related to their exercise of approximately $21,592,118 before payment of any solicitation fees that may be due. If and when we receive these additional proceeds, they are also expected to be allocated to our working capital.

We will invest proceeds not immediately required for the purposes described above principally in United States government securities, short-term certificates of deposit, money market funds or other short-term interest-bearing investments.

We have never paid any cash dividends and intend, for the foreseeable future, to retain any future earnings for the development of our business. Our future dividend policy will be determined by the board of directors on the basis of various factors, including our results of operations, financial condition, capital requirements and investment opportunities.

17

Table of Contents

The difference between the public offering price per share of our common stock and the as adjusted net tangible book value per share of our common stock after this offering constitutes the dilution to investors in this offering. Net tangible book value per share is determined by dividing our net tangible book value, which is our total tangible assets less total liabilities, by the number of outstanding shares of our common stock.