UNITED STATES SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

| (Mark One) | |

| þ | ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2006 | |

| or | |

| o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the transition period from __________ to __________ | |

Commission file number: 001-32832

Jazz Technologies, Inc.

(Exact name of registrant as specified in its charter)

Delaware | 20-3320580 |

(State of incorporation) | (I.R.S. Employer Identification No.) |

4321 Jamboree Road | |

Newport Beach, California | 92660 |

(Address of principal executive offices) | (Zip code) |

(949) 435-8000

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of Each Class | Name of Each Exchange on Which Registered | |

Common Stock, $0.0001 par value per share | The American Stock Exchange | |

Warrants | The American Stock Exchange | |

Units | The American Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No þ

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Exchange Act. Yes o No þ

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes þ No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of the registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. þ

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o Non-accelerated filer þ

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No þ

The aggregate market value of the common stock held by non-affiliates of the registrant as of June 30, 2006 was approximately $155.3 million. Shares of voting common stock held by directors, executive officers, and by each person who was known to us to beneficially own 10% or more of the outstanding common stock as of such date have been excluded as such persons may be deemed to be affiliates. This determination of affiliate status is not necessarily a conclusive determination for other purposes. The aggregate market value has been computed based on a price of $5.40 per share, which was the closing sale on June 30, 2006 as reported by the American Stock Exchange.

The number of shares outstanding of the registrant’s common stock as of March 13, 2007 was 25,048,924.

JAZZ TECHNOLOGIES, INC.

FORM 10-K

Year Ended December 31, 2006

TABLE OF CONTENTS

Page No. | ||

PART I | ||

| Item 1. | Business | 2 |

| Item 1A. | Risk Factors | 20 |

| Item 1B. | Unresolved Staff Comments | 38 |

| Item 2. | Properties | 38 |

| Item 3. | Legal Proceedings | 38 |

| Item 4. | Submission of Matters to a Vote of Security Holders | 38 |

PART II | ||

| Item 5. | Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities | 39 |

| Item 6. | Selected Financial Data | 41 |

| Item 7. | Management’s Discussion and Analysis of Financial Condition and Results of Operations | 43 |

| Item 7A. | Quantitative and Qualitative Disclosures About Market Risk | 46 |

| Item 8. | Financial Statements and Supplementary Data | 47 |

| Item 9. | Changes in and Disagreements with Accountants on Accounting and Financial Disclosure | 48 |

| Item 9A. | Controls and Procedures | 48 |

| Item 9B. | Other Information | 48 |

PART III | ||

| Item 10. | Directors, Executive Officers and Corporate Governance | 49 |

| Item 11. | Executive Compensation | 53 |

| Item 12. | Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters | 58 |

| Item 13. | Certain Relationships and Related Transactions and Director Independence | 61 |

| Item 14. | Principal Accountant Fees and Services | 63 |

PART IV | ||

| Item 15. | Exhibits and Financial Statement Schedules | 64 |

| SIGNATURES | 68 | |

| EXHIBIT LIST | 69 | |

i

FORWARD-LOOKING INFORMATION

Some of the information contained or incorporated by reference in this annual report constitutes forward-looking statements within the definition of the Private Securities Litigation Reform Act of 1995. You can identify these statements by forward-looking words such as “may,” “expect,” “anticipate,” “contemplate,” “believe,” “estimate,” “intends,” and “continue” or similar words. You should read statements that contain these words carefully because they:

| · | discuss future expectations; |

| · | contain projections of future results of operations or financial condition; or |

| · | state other “forward-looking” information. |

We believe it is important to communicate our expectations to our stockholders. However, there may be events in the future that we are not able to predict accurately or over which we have no control. The risk factors and cautionary language discussed or incorporated by reference in this annual report provide examples of risks, uncertainties and events that may cause actual results to differ materially from the expectations described by us in such forward-looking statements, including among other things:

| · | the amount of cash on hand available to us; |

| · | our business strategy; |

| · | outcomes of government reviews, inquiries, investigations and related litigation; |

| · | continued compliance with government regulations; |

| · | legislation or regulatory environments, requirements or changes adversely affecting the business in which we are engaged; |

| · | fluctuations in customer demand; |

| · | management of rapid growth; and |

| · | general economic conditions. |

You are cautioned not to place undue reliance on these forward-looking statements, which speak only as of the date of this annual report.

All forward-looking statements included or incorporated herein attributable to us or any person acting on our behalf are expressly qualified in their entirety by the cautionary statements contained or referred to in this section. Except to the extent required by applicable laws and regulations, we undertake no obligation to update these forward-looking statements to reflect events or circumstances after the date of this annual report or to reflect the occurrence of unanticipated events.

You should be aware that the occurrence of the events described in the “Risk Factors” portion of this annual report, the documents incorporated herein and our other SEC filings could have a material adverse effect on our business, prospects, financial condition or operating results.

1

PART I

Item 1. Business

Jazz Technologies, Inc. is an independent semiconductor foundry focused on specialty process technologies for the manufacture of analog and mixed-signal semiconductor devices. We believe our specialty process technologies attract customers who seek to produce analog and mixed-signal semiconductor devices that are smaller and more highly integrated, power-efficient, feature-rich and cost-effective than those produced using standard process technologies. Our customers’ analog and mixed-signal semiconductor devices are designed for use in products such as cellular phones, wireless local area networking devices, digital TVs, set-top boxes, gaming devices, switches, routers and broadband modems. Our customers include Skyworks Solutions, Inc., Conexant Systems, Inc., Marvell Technology Group Ltd., RF Micro Devices, Inc., Freescale Semiconductor, Inc., Airoha Technology Corp., Xceive Corporation, RF Magic, Inc. and Mindspeed Technologies, Inc.

We were organized as a Delaware blank check company in August 2005 by Gilbert F. Amelio, Ph. D., Ellen M. Hancock and Steve Wozniak for the purpose of acquiring, through a merger, capital stock exchange, stock purchase, asset acquisition or other similar business combination, one or more domestic and/or foreign operating businesses in the technology, multimedia and networking sectors. On February 16, 2007, we consummated the acquisition of Jazz Semiconductor, Inc., or Jazz Semiconductor, pursuant to an Agreement and Plan of Merger among us, Joy Acquisition Corp., a Delaware corporation and our wholly-owned subsidiary, Jazz Semiconductor and TC Group, L.L.C., as stockholders’ representative, whereby Joy Acquisition Corp. merged with and into Jazz Semiconductor with Jazz Semiconductor becoming our wholly-owned subsidiary.

As used in this annual report, “we,” “us,” “our,” “Jazz,” the “Company” and words of similar import refer to Jazz Technologies, Inc. and, except where the context otherwise requires, our consolidated subsidiary, Jazz Semiconductor, Inc., “Jazz Technologies” refers solely to Jazz Technologies, Inc. and not Jazz Semiconductor, Inc., and “Jazz Semiconductor” refers solely to Jazz Semiconductor, Inc. Jazz Technologies’ historical financial information is presented as of December 31, 2006, the end of its last fiscal year, and Jazz Semiconductor’s historical financial information is presented as of December 29, 2006, the end of its last fiscal year.

Our Industry

Semiconductors are the building blocks of a broad range of electronic systems such as personal computers, telecommunications equipment, wireless devices, consumer electronics, automotive electronics and industrial electronics. Although global semiconductor sales have experienced significant cyclical variation in annual growth rates, they have increased significantly over the long term. As electronic systems have become more sophisticated and integrated, satisfying the demand for semiconductors used in these systems has required advances in semiconductor design, manufacturing and packaging technologies.

Disaggregation of the Semiconductor Industry and the Success of Foundries

In the past, most semiconductor companies were vertically integrated. They internally designed, fabricated, packaged, tested and marketed their own semiconductors. These vertically integrated semiconductor companies are known as integrated device manufacturers, or IDMs. As the complexity of semiconductor designs has increased, semiconductors have become increasingly challenging to manufacture, requiring both sophisticated manufacturing expertise and significant investment in fabrication facilities, or fabs and the development of leading-edge process technologies.

As the cost and skills required for designing and manufacturing complex semiconductors have increased, the semiconductor industry has become increasingly disaggregated. This disaggregation has fueled the growth of three segments of the semiconductor industry, which together perform the significant functions of an IDM. These are:

| · | fabless semiconductor companies that design and market semiconductors; |

| · | foundries that manufacture semiconductor wafers; and |

2

| · | packaging and test companies that encapsulate and test semiconductors. |

Fabless semiconductor companies are gaining an increasing share of the semiconductor market. According to the Fabless Semiconductor Association, a trade organization, sales of semiconductors by fabless companies as a percentage of worldwide sales more than doubled from approximately 8% in 2000 to approximately 18% in 2005. At the same time, many IDMs have announced that they have reduced their investment in their existing and next-generation manufacturing facilities and process technologies as they seek to increase their flexibility to reallocate their resources and capital expenditures. We believe that IDMs that have adopted this “fab-lite” strategy will continue to outsource an increasing percentage of their manufacturing requirements to foundry service providers. We believe that utilizing foundry service providers allows fabless semiconductor companies and IDMs to reduce their manufacturing costs, more efficiently allocate capital, research and development and management resources, and gain access to manufacturing process technologies and production capacity they do not possess.

Independent foundries have traditionally focused on standard complementary metal oxide semiconductor, or CMOS, processes that are primarily used for digital semiconductor applications. The proliferation of fabless semiconductor companies and the increasing use of outsourcing by many IDMs for a portion of their production have driven the growth of the CMOS foundry industry, including the growth of global Foundry revenues derived from the manufacture of analog and mixed signal semiconductors. We believe that many of these analog and mixed signal semiconductors are manufactured using specialty process technologies. In addition, according to estimates of Semico Research Corporation, a semiconductor marketing and consulting research company, the percentage of total semiconductor device revenues manufactured by third-party foundries has increased from 5.6% in 1995 to 14.1% in 2005, highlighting the increasing role foundries are playing in the semiconductor supply chain.

Proliferation of Analog and Mixed-Signal Semiconductors and the Growing Need for Specialty Process Technologies

The two basic functional technologies for semiconductor products are digital and analog. Digital semiconductors perform arithmetic functions on data represented by a series of ones and zeroes. Digital semiconductors provide critical processing power and have helped enable many of the computing and communication advances of recent years. Analog semiconductors monitor and manipulate real world signals such as sound, light, pressure, motion, temperature, electrical current and radio waves, for use in a wide variety of electronic products such as personal computers, cellular handsets, telecommunications equipment, consumer electronics, automotive electronics and industrial electronics. There is a growing need for analog functionality to enable digital systems to interface with the real world. Analog-digital, or mixed-signal, semiconductors combine analog and digital devices on a single chip to process both analog and digital signals.

Integrating analog and digital components on a single, mixed-signal semiconductor enables smaller and more highly integrated, power-efficient, feature-rich and cost-effective semiconductor devices but presents significant design and manufacturing challenges. For example, combining high-speed digital circuits with sensitive analog circuits on a single, mixed-signal semiconductor can increase electromagnetic interference and power consumption, both of which cause a higher amount of heat to be dissipated and decrease the overall performance of the semiconductor. Challenges associated with the design and manufacture of mixed-signal semiconductors increase as the industry moves toward finer, more advanced process geometries. Standard electronic design automation, or EDA, tools used in the design of digital circuits have limited use in predicting the performance of certain analog and mixed-signal designs. As a result, analog and mixed-signal semiconductors can be complex to manufacture and typically require sophisticated design expertise and strong application specific experience and intellectual property. Analog and mixed-signal semiconductor engineers typically require several years of practical experience and application knowledge to become proficient in the design of complex analog and mixed-signal semiconductors. Manufacturers may also need to make a significant investment in specialty process technologies to manufacture these semiconductors.

Specialty process technologies enable greater analog content and can reduce the die size of an analog or mixed-signal semiconductor, thereby increasing the number of die that can be manufactured on a wafer and reducing final die cost. In addition, specialty process technologies can enable increased performance, superior noise reduction and improved power efficiency of analog and mixed-signal semiconductors compared to traditional standard CMOS processes. These specialty process technologies include advanced analog CMOS, radio frequency CMOS, or RF CMOS, high voltage CMOS, bipolar CMOS, or BiCMOS, silicon germanium BiCMOS, or SiGe BiCMOS, and bipolar CMOS double-diffused metal oxide semiconductor, or BCD.

3

For many applications in the wireless and high-speed wireline communications, consumer electronics, automotive and industrial end markets, the performance characteristics of specialty process technologies can lead customers to select them over digital CMOS process technologies. As semiconductor performance needs continue to increase in these end markets, we believe the demand for specialty process technologies will also increase. For example, Semico Research Corporation estimates that silicon germanium bipolar complementary metal oxide semiconductor usage in wireless, wireline and consumer electronic products will grow at compound annual growth rates of 16%, 12% and 27%, respectively, from 2005 to 2010.

Emerging Trend to Outsource Specialty Process Manufacturing Requirements

We believe that many of the factors and conditions that have driven growth in the outsourcing of manufacturing using standard process technologies will fuel continued growth in the outsourcing of manufacturing using specialty process technologies. There can be no assurance, however, that the factors and conditions that have fueled growth in the outsourcing of manufacturing using standard process technologies will also fuel growth in the outsourcing of manufacturing using specialty process technologies or that any future growth rate in global foundry revenues derived from specialty process technologies will be the same as the growth rate for global foundry revenues derived from standard process technologies. As many IDMs reduce their investment in their existing and next-generation standard CMOS process technologies and manufacturing facilities, it may become less cost-effective for these IDMs to develop, maintain and operate specialty process technology manufacturing lines. We believe these IDMs will increasingly choose to also outsource their specialty process technologies. In addition, we believe that fabless semiconductor companies are increasingly seeking access to specialty process technologies to produce analog and mixed-signal semiconductors.

To date, most independent foundries have focused primarily on standard CMOS processes instead of specialty process technologies. While some IDMs have provided outsourced specialty process technologies, we believe that competing IDMs and fabless design companies may be reluctant to work with and provide confidential information to IDMs that also manufacture products competitive with theirs. Consequently, we believe that there is significant growth potential for independent foundries with a broad platform of specialty process technologies, advanced design and support capabilities and product application expertise that focus primarily on the specialty foundry opportunity.

Our Solution

We are an independent semiconductor foundry, providing specialty process technologies, design solutions and application knowledge for the manufacture of analog and mixed-signal semiconductors. Key elements of our solution are as follows:

| · | We offer an independent and focused source for the manufacture of semiconductors using specialty process technologies. Most other independent foundries focus on standard process technologies, rather than specialty process technologies. Some IDMs offer specialty process foundry services but also manufacture their own semiconductor products, which may be competitive with the products of their potential customers who seek these services. We combine the benefits of independence with a focus on specialty process technologies. |

| · | We offer a specialized design platform for analog and mixed-signal semiconductors. Our design engineering support team assists our customers with their advanced designs by leveraging our application knowledge and experience to help guide their technology selection and design implementation. Our sophisticated design tools and services are specifically tailored to meet analog and mixed-signal design needs, and include specialized device modeling and characterization features that allow simulation of a variety of real world situations, including different temperatures, power levels and speeds. |

| · | We offer a broad range of specialty process technologies. Our specialty process technology portfolio includes advanced analog CMOS, RF CMOS, high voltage CMOS, BiCMOS and SiGe BiCMOS processes. In addition to these specialty process technologies, we have recently begun to offer BCD processes optimized for analog semiconductors such as power management, high efficiency audio amplification, and optical driver integrated circuits. The breadth of our portfolio allows us to offer our customers a wide range of solutions to address their high-performance, high-density, low-power and low-noise requirements for analog and mixed-signal semiconductors. These semiconductor devices are used in products such as cellular phones, digital TVs, set-top boxes, gaming devices, wireless local area networking devices, digital cameras, switches, routers and broadband modems. We benefit from the development of specialty process technologies by Conexant and its predecessor, Rockwell Semiconductor Systems, over a period of 35 years. |

4

| · | We are a leader in high-performance SiGe process technologies. We offer high performance 150 GHz 0.18 micron SiGe BiCMOS technology, which we believe is one of the most advanced SiGe process technologies in production today. In addition, we recently announced the availability of 200 GHz 0.18 micron SiGe BiCMOS technology. Analog and mixed-signal semiconductors manufactured with SiGe BiCMOS process technologies can be smaller, require less power and provide higher performance than those manufactured with standard CMOS processes. Moreover, SiGe BiCMOS process technologies allow for higher levels of integration of analog and digital functions on the same mixed-signal semiconductor device. |

Our Strategy

Key elements of our strategy are as follows:

| · | Further strengthen our position in specialty process technologies for the manufacture of analog and mixed-signal semiconductors. We are continuing to invest in our portfolio of specialty process technologies to address the key product attributes that make our customers’ products more competitive. |

| · | Target large, growing and diversified end markets. We target end markets characterized by high growth and high performance for which we believe our specialty process technologies have a high value proposition, including the wireless and high-speed wireline communications, consumer electronics, automotive and industrial markets. For example, we believe that our specialty process technologies can provide performance and cost advantages over current CMOS solutions in the integration of power amplifiers with RF transceivers for wireless local area networking applications. |

| · | Continue to diversify our customer base. Since the spin-off of Jazz Semiconductor from Conexant in 2002, Jazz Semiconductor has transitioned its business from a captive manufacturing facility within Conexant to an independent semiconductor foundry with more than 100 post-spin-off customers as of December 29, 2006, the end of Jazz Semiconductor’s latest fiscal year. We intend to continue to grow and diversify Jazz Semiconductor’s business through the acquisition of new customers. For example, under a technology transfer agreement Jazz Semiconductor entered into with Polar Semiconductor, Inc., or PolarFab, PolarFab agreed to help facilitate the transfer to us of certain PolarFab customers that currently use PolarFab’s BCD process technologies. We expect that PolarFab will transfer to us approximately 25 of its customers. Because new customers primarily use our specialty process technologies, we expect that our continued acquisition of new customers will result in a continuing increase in the percentage of our revenues that are derived from specialty process technologies. |

| · | Maintain capital efficiency by leveraging its capacity and manufacturing model. We seek to maximize the utilization of our Newport Beach, California manufacturing facility and leverage our manufacturing suppliers’ facilities in China to meet increased capacity requirements cost-effectively. We can typically increase our specialty process technology capacity and meet our customers’ performance requirements using adapted semiconductor process equipment sets that are typically one or two generations behind leading-edge digital CMOS process equipment. This typically allows us to acquire lower-cost semiconductor process equipment to operate our Newport Beach, California fab. We are also able to access and adapt existing capacity cost-effectively through supply and licensing agreements, such as those with Advanced Semiconductor Manufacturing Corporation, or ASMC, and Shanghai Hua Hong NEC Electronics Co., Ltd., or HHNEC. |

5

Process Technologies

Process technologies are the set of design rules, electrical specifications and process steps that we implement for the manufacture of semiconductors on silicon wafers. In addition to offering standard process technologies, we have a strong heritage of manufacturing analog and mixed-signal semiconductors using specialty process technologies, including advanced analog CMOS, RF CMOS, high voltage CMOS, BiCMOS and SiGe BiCMOS process technologies. These analog and mixed-signal semiconductors are used in products targeting the wireless and high-speed wireline communications, consumer electronics, automotive and industrial end markets. We also now offer BCD process technologies optimized for analog semiconductors such as power management, high-efficiency audio amplification and optical driver integrated circuits.

Our Standard Process Technologies

We refer to our digital CMOS and standard analog CMOS process technologies as standard process technologies. Digital CMOS process technologies are the most widely used process technologies in the semiconductor industry because they require less power than other technologies for digital functions and allow for the dense placement of digital circuits onto a single semiconductor, such as a graphics or baseband processor. We currently have digital CMOS processes in 0.5 micron, 0.35 micron, 0.25 micron and 0.18 micron and have announced the availability of a 0.13 micron process. These digital CMOS process technologies form the baseline for our standard analog CMOS processes.

Standard analog CMOS process technologies have more features than digital CMOS process technologies and are well suited for the design of low-frequency analog and mixed-signal semiconductors. These process technologies generally incorporate basic passive components, such as capacitors and resistors, into a digital CMOS process. We currently have standard analog CMOS processes in 0.5 micron, 0.35 micron, 0.25 micron and 0.18 micron and have announced availability of a 0.13 micron process. These standard analog CMOS process technologies form the baseline for our specialty process technologies.

While other foundries may offer standard analog processes, most do not offer specialty process technologies. Other foundries, however, offer standard analog processes at more advanced geometries than we offer, such as 90 nanometer CMOS process technologies. In certain circumstances, such as when a large amount of digital content is required in a mixed-signal semiconductor and less analog content is required, a customer may choose to design a product in a standard analog CMOS process technology at an advanced geometry, such as 90 nanometer CMOS, instead of choosing a specialty process technology at a larger geometry.

Our Specialty Process Technologies

We refer to our advanced analog CMOS, RF CMOS, high voltage CMOS, BiCMOS, SiGe BiCMOS and BCD process technologies, as specialty process technologies. Most of our specialty process technologies are based on CMOS processes with added features to enable improved size, performance and cost characteristics for analog and mixed-signal semiconductors. Products made with our specialty process technologies are typically more complex to manufacture than products made using standard process technologies employing similar line widths. Generally, customers who use our specialty process technologies cannot easily move designs to another foundry because the analog characteristics of the design are dependent upon its implementation of the applicable process technology. The relatively small engineering community with specialty process know-how has also limited the number of foundries capable of offering specialty process technologies. In addition, the specialty process design infrastructure is complex and includes design kits and device models that are specific to the foundry in which the process is implemented and to the process technology itself.

Our advanced analog CMOS process technologies have more features than standard analog CMOS process technologies and are well suited for higher performance or more highly integrated analog and mixed-signal semiconductors, such as high-speed analog-to-digital or digital-to-analog converters and mixed-signal semiconductors with integrated data converters. These process technologies generally incorporate higher density passive components, such as capacitors and resistors, as well as improved active components, such as native or low voltage devices, and improved isolation techniques, into standard analog CMOS process technologies. We currently have advanced analog CMOS process technologies in 0.5 micron, 0.35 micron, 0.25 micron and 0.18 micron and have announced the availability of a 0.13 micron process. These advanced analog CMOS processes form the baseline for our other specialty process technologies.

6

Our RF CMOS process technologies have more features than advanced analog CMOS process technologies and are well suited for wireless semiconductors, such as highly integrated wireless transceivers, power amplifiers, and television tuners. These process technologies generally incorporate integrated inductors, high performance variable capacitors, or varactors, and RF laterally diffused metal oxide semiconductors into an advanced analog CMOS process technology. In addition to the process features, our RF offering includes design kits with RF models, device simulation and physical layouts tailored specifically for RF performance. We currently have RF CMOS process technologies in 0.25 micron and 0.18 micron and have announced availability of a 0.13 micron process. These RF CMOS process technologies form the baseline for some of our other specialty process technologies.

Our high voltage CMOS and BCD process technologies have more features than advanced analog CMOS processes and are well suited for power and driver semiconductors such as voltage regulators, battery chargers, power management products and audio amplifiers. These process technologies generally incorporate higher voltage CMOS devices such as 5V, 8V, 12V and 40V devices, and, in the case of BCD, bipolar devices, into an advanced analog CMOS process. We currently have high voltage CMOS offerings in 0.5 micron, 0.35 micron, 0.25 micron and 0.18 micron, and BCD offerings in 0.5 micron. We are working on extending the high voltage options to include a 0.35 micron BCD process technology and 60V and 120V capabilities in the future to enable higher levels of analog integration at voltage ranges that are suitable for automotive electronics and line power conditioning for consumer devices.

Our BiCMOS process technologies have more features than RF CMOS process technologies and are well suited for RF semiconductors such as wireless transceivers and television tuners. These process technologies generally incorporate high-speed bipolar transistors into an RF CMOS process. The equipment requirements for BiCMOS manufacturing are specialized and require enhanced tool capabilities to achieve high yield manufacturing. We currently have BiCMOS process technologies in 0.35 micron.

Our SiGe BiCMOS process technologies have more features than BiCMOS processes and are well suited for more advanced RF semiconductors such as high-speed, low noise, highly integrated multi-band wireless transceivers, television tuners and power amplifiers. These process technologies generally incorporate a silicon germanium bipolar transistor, which is formed by the deposition of a thin layer of silicon germanium within a bipolar transistor, to achieve higher speed, lower noise, and more efficient power performance than a BiCMOS process technology. It is also possible to achieve speeds using SiGe BiCMOS process technologies equivalent to those demonstrated in standard CMOS processes that are two process generations smaller in line-width. For example, a 0.18 micron SiGe BiCMOS process is able to achieve speeds comparable to a 90 nanometer RF CMOS process. As a result, SiGe BiCMOS makes it possible to create analog products using a larger geometry process technology at a lower cost while achieving similar or superior performance to that achieved using a smaller geometry standard CMOS process technology. The equipment requirements for SiGe BiCMOS manufacturing are similar to the specialized equipment requirements for BiCMOS. We have developed enhanced tool capabilities in conjunction with large semiconductor tool suppliers to achieve high yield SiGe manufacturing. We believe this equipment and related process expertise makes us one of the few silicon manufacturers with demonstrated ability to deliver SiGe BiCMOS products. We currently have SiGe BiCMOS process technologies at 0.35 micron and 0.18 micron and are developing a 0.13 micron SiGe BiCMOS process.

We continue to invest in technology that helps improve the performance, integration level and cost of analog and mixed-signal products. This includes improving the density of passive elements such as capacitors and inductors, improving the analog performance and voltage handling capability of active devices, and integrating advanced features in our specialty CMOS processes that are currently not readily available. Examples of such features currently under development include technologies aimed at integrating micro-electro-mechanical devices with CMOS for higher quality passive elements, manufacturing tools that can increase the density of our capacitors with improved dielectric films, and scaling the features we offer today to the 0.13 micron process technology.

7

Manufacturing

We have placed significant emphasis on achieving and maintaining a high standard of manufacturing quality. We seek to enhance our production capacity for our high-demand specialty process technologies and to design and implement manufacturing processes that produce consistently high manufacturing yields. Our production capacity in each of our specialty process technologies enables us to provide our customers with volume production, flexibility and quick-to-market manufacturing services. All of our process research and development is performed in our manufacturing facility in Newport Beach, California.

Capacity

We currently have the capacity to commence the fabrication process for approximately 17,000 eight-inch wafers per month, depending on process technology mix, in our Newport Beach, California fab. Our fab generally operates 24 hours per day, seven days per week. We provide a variety of services in Newport Beach, California from full scale production to small engineering qualification lot runs to probe services. We have the ability to rapidly change the mix of production processes in use in order to respond to changing customer needs and maximize utilization of the fab. We have made, and are continuing to make, capital investments in our Newport Beach, California fab to shift capacity from standard CMOS process technologies to specialty process technologies and to expand overall capacity.

We also plan to seek opportunities to add manufacturing capacity outside of this facility as needed by expanding our existing manufacturing supply relationships, entering into new relationships with other manufacturers or acquiring existing manufacturing facilities. Consistent with this strategy, we have entered into supply agreements with each of ASMC and HHNEC, two of China’s leading silicon semiconductor foundries. These agreements are designed to provide us with low-cost, scalable production capacity and multiple location sourcing for our customers. To date, we have not utilized significant capacity from our manufacturing suppliers. While these suppliers have substantially met our requests for wafers to date, if we had a sudden significant increase in demand for their services, it is unlikely that they would be able to satisfy our increased demand in the short term.

Equipment

Our policy is to qualify the vendors from which we purchase equipment to assure process consistency, expedite installation and production release, reduce consumable inventories, combine equipment support resources and maximize supplier leverage. The principal equipment we use to manufacture semiconductor wafers are scanners, steppers, track equipment, etchers, furnaces, automated wet stations, implanters and metal sputtering, chemical vapor deposition and chemical mechanical planarization equipment. We can expand our specialty process manufacturing capacity by purchasing lower-cost equipment because we are able to meet our customers’ performance requirements using adapted digital CMOS equipment sets that are typically one or two generations behind leading-edge digital CMOS process equipment.

Our Newport Beach, California fab is organized into bays based on function with manufacturing operations performed in clean rooms in order to maintain the quality and integrity of wafers that it produces. Clean rooms have historically been rated on the number of 0.5 micron particles allowable within a cubic foot of air and we generally refer to them as class-1, 10, 100, 1,000, 10,000, or 100,000 on that basis. A significant majority of our current clean rooms operate at a class-10 level.

Raw Materials

Our manufacturing processes use highly specialized materials, including semiconductor wafers, chemicals, gases and photomasks. These raw materials are generally available from several suppliers. However, we often select one vendor to provide us with a particular type of material in order to obtain preferred pricing. In those cases, we generally also seek to identify, and in some cases qualify, alternative sources of supply.

We generally maintain sufficient stock of principal raw material for two-weeks’ production based on historical usage at our Newport Beach, California fab. Our vendors also generally keep four to six weeks of pre-approved material at their local warehouse in order to support changes that may occur in our requirements and to respond to quality issues. Although some of our blanket purchase order contracts contain price and capacity commitments, these commitments tend to be short term in nature. However, we have agreements with several key material suppliers under which they hold similar levels of inventory at our warehouse and fab for our use. We are not under any obligation under these agreements to purchase raw material inventory that is held by our vendors at our site until we actually use it, unless we hold the inventory beyond specified time limits.

8

Some of our material providers are our sole source for those materials. The most important raw material used in our production processes is silicon wafers, which is the basic raw material from which integrated circuits are made. The sole supplier of our wafers is Wacker Siltronic Corporation. Siltronic supplies our wafer requirements from three separate facilities, providing redundancy in the event a facility’s operations are interrupted. In addition, Siltronic maintains an approximately six week supply of inventory at our fab. Through Conexant and its predecessor, Rockwell, we have had a long-term supply relationship with Siltronic. We believe that qualification of a second wafer supplier could take from six months to one year.

Photronics, Inc. is the sole-source supplier of photomasks for use in our Newport Beach, California fab. We have entered into a supply agreement with Photronics that provides us with guaranteed pricing for photomasks through 2008, but allows us to negotiate with Photronics annually to obtain reductions in the base price of the masks. Photronics maintains manufacturing facilities in the United States, Singapore and Taiwan. We believe it would take between ten and 12 months to qualify a new supplier if Photronics was unable or unwilling to continue as a supplier.

We receive one of our liquid chemicals, EKC 652, which is used in the etch process, from E.I. du Pont de Nemours and Company. DuPont is the sole source supplier of this chemical and its chemistry is unique. We believe that it would take between four and six months to replace this chemical in the event DuPont were unable or unwilling to continue as a supplier.

We use a large amount of water in our manufacturing process. We obtain water supplies from the local municipality. We also use substantial amounts of electricity supplied by Southern California Edison in the manufacturing process. We maintain back-up generators that are capable of providing adequate amounts of electricity to maintain vital life safety systems, such as toxic gas monitors, fire systems, exhaust systems and emergency lighting in case of power interruptions, which we have experienced from time to time.

Quality Control

We seek to attract and retain leading international and domestic semiconductor companies as customers by establishing and maintaining a reputation for high quality and reliable services and products. Our Newport Beach, California fab has achieved ISO9001:2000 certification and has also been certified as meeting the standards of ISO 14001 and ISO/IEC 27001:2005. ISO9001:2000 sets the criteria for developing a fundamental quality management system. This system focuses on continuous improvement, defect prevention and the reduction of variation and waste. ISO 14001 consists of a set of standards that provide guidance to the management of organizations to achieve an effective environmental management system. ISO/IEC 27001:2005 replaces the previous BS7799 standard, and is the new global certification that focuses on security information management activities associated with the reduction of security breaches.

Our policy is to implement quality control measures that are designed to ensure high yields at our facilities. We test and monitor raw materials and production at various stages in the manufacturing process before shipment to customers. Quality assurance also includes on-going production reliability audits and failure tracking for early identification of production problems.

We also conduct routine quality audits of ASMC and HHNEC with respect to the manufacture of semiconductors for us. These quality audits involve our engineers and management meeting with representatives of ASMC and HHNEC, reviewing and assessing their quality controls and procedures and implementing changes and enhancements designed to ensure that each entity has adopted quality control standards similar to ours.

9

Our Services

We primarily manufacture semiconductor wafers for our customers. We focus on providing a high level of customer service in order to attract customers, secure production from them and maintain their continued loyalty. We emphasize responsiveness to customer needs, flexibility, on-time delivery, speed to market and accuracy. Our customer-oriented approach is evident in two prime functional areas of customer interaction: customer design development and manufacturing services. Throughout the customer engagement process, we offer services designed to provide our customers with a streamlined, well-supported, easy to monitor product flow. We believe that this process enables our customers to get their products to market quickly and efficiently.

Wafer manufacturing requires many distinct and intricate steps, each of which must be completed accurately in order for finished semiconductor devices to work as intended. After a design moves into volume production, we continue to provide ongoing customer support through all phases of the manufacturing process.

The processes required to take raw wafers and turn them into finished semiconductor devices are generally accomplished through five steps: circuit design, mask making, wafer fabrication, probe, and assembly and test. The services we offer to our customers in each of the five steps are described below.

Circuit Design

We interact closely with customers throughout the design development and prototyping process to assist them in the development of high performance and low power consumption semiconductor designs and to lower their final die, or individual semiconductor, costs through die size reductions and integration. We provide engineering support and services as well as manufacturing support in an effort to accelerate our customers’ design and qualification process so that they can achieve faster time to market. We have entered into alliances with Cadence Design Systems, Inc., Synopsys, Inc. and Mentor Graphics Corp., leading suppliers of electronic design automation tools, and also licensed technology from ARM Holdings plc and Synopsys, Inc., leading providers of physical intellectual property components for the design and manufacture of semiconductors. Through these relationships, we provide our customers with the ability to simulate the behavior of our processes in standard electronic design automation, or EDA, tools. To provide additional functionality in the design phase, we offer our customers standard and proprietary models within design kits that we have developed. These design kits, which collectively comprise our design library, or design platform, allow our customers quickly to simulate the performance of a semiconductor design in our processes, enabling them to refine their product design before actually manufacturing the semiconductor.

The applications for which our specialty process technologies are targeted present challenges that require an in-depth set of simulation models. We provide these models as an integral part of our design platform. At the initial design stage, our customers’ internal design teams use our proprietary design kits to design semiconductors that can be successfully and cost-effectively manufactured using our specialty process technologies. Our engineers, who typically have significant experience with analog and mixed-signal semiconductor design and production, work closely with our customers’ design teams to provide design advice and help them optimize their designs for our processes and their performance requirements. After the initial design phase, we provide our customers with a multi-project wafer service to facilitate the early and rapid use of our specialty process technologies, which allows them to gain early access to actual samples of their designs. Under this multi-project wafer service, we schedule a bimonthly multi-project wafer run in which we manufactures several customers’ designs in a single mask set, providing our customers with an opportunity to reduce the cost and time required to test their designs. We believe our circuit design expertise and our ability to accelerate our customers’ design cycle while reducing their design costs represents one of our competitive strengths.

Photomask Making

Our engineers generally assist our customers to design photomasks that are optimized for our specialty process technologies and equipment. Actual photomask production occurs at independent third parties that specialize in photomask making.

10

Wafer Fabrication

We provide wafer fabrication services to our customers using specialty process technologies, including advanced analog CMOS, RF CMOS, high voltage CMOS, BiCMOS, SiGe BiCMOS and BCD processes, as well as using standard CMOS process technologies. During the wafer fabrication process, we perform procedures in which a photosensitive material is deposited on the wafer and exposed to light through a mask to form transistors and other circuit elements comprising a semiconductor. The unwanted material is then etched away, leaving only the desired circuit pattern on the wafer. By using our ebizz web site, customers are able to access their lot status and work-in-process information via the Internet.

Probe

After a visual inspection, individual die on a wafer are tested, or “probed,” electrically to identify die that fail to meet required standards. Die that fail this test are marked to be discarded. We generally offer wafer probe services at the customer’s request and conduct those services internally in order to more quickly obtain accurate data on manufacturing yield rates. At times when wafers are ordered in excess of our probe capacity in our Newport Beach, California fab, we may offer to coordinate shipping of completed wafers to third-party vendors for probe services.

Assembly and Test

Following wafer probe, wafers go through the assembly and test process to form finished semiconductor products. We typically refer our customers to third-party providers of assembly and test services.

Sales and Marketing

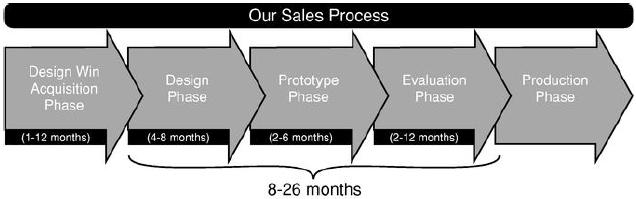

We seek to establish and maintain relationships with our customers by providing a differentiated process technology portfolio, effective technical services and support and flexible manufacturing. Our sales process is a highly technical and lengthy process. The entire cycle from design win to volume production typically takes between eight and 26 months. During this cycle, our customers typically dedicate anywhere from three to 12 engineers to support the design, prototype and evaluation phases of their products.

Our Sales Process

The following chart portrays our sales process.

Design Win Acquisition Phase. Our sales personnel work closely with current and potential customers to identify opportunities for them to pursue product designs using our process technologies. The customer’s decision to design a semiconductor product using one of our process technologies is based upon several technical and economic factors, including choosing the optimal process technology to achieve a cost-effective solution for their semiconductor device.

11

The decision to use a specialty process technology also generally requires the customer to select our specialty process foundry. Customers do not typically move a given design between foundries until the next generation of that design is evaluated because of the highly sensitive and variable nature of specialty process production. The same semiconductor design produced at different specialty process foundries, or even at different times in the same foundry, may have materially different performance characteristics. As a result, customers place significant value upon a given foundry’s ability to produce devices that consistently meet specifications, and may be reluctant to shift to another foundry once the process has been stabilized. Given the high switching costs associated with specialty process devices, the design decision process represents a significant commitment by the customer, consuming between one and 12 months and often involving the customer’s product architects, design engineers, purchasing personnel and executive management. Our customers will often install our proprietary design platform, which runs on industry standard EDA tools. The customer will often design a test circuit for our process in order to evaluate how the circuit performs in an actual silicon implementation. We refer to a potential customer’s decision to design a specific semiconductor using one of our processes as a design win. As of any particular date, we define a customer as any party from whom we have recognized revenues in the prior twelve months. As of December 29, 2006, Jazz Semiconductor had more than 300 design wins from over 100 customers. A design win commences the design phase.

Design Phase. The design phase typically involves from three to 12 of our customer’s design engineers and one of our technical support engineers. This phase generally takes from four to 12 months, after which time the customer provides a circuit data file for which we purchase mask reticles for the manufacture of the semiconductor and commence manufacturing of the customer’s design, which is considered a “tape-in,” at which point the prototype phase commences.

Prototype Phase. During the prototype phase, we manufacture the customer’s prototype semiconductor and ship the silicon wafers to the customer for functional testing and verification. The customer may test the devices at the wafer or die level, or may package and test the prototype semiconductor devices. Once the customer tests its product design in an actual silicon implementation, the customer may need to make modifications to its design in order to increase performance, add features or correct a design error. The prototype phase typically requires two to 12 months, depending on the number of design modifications required. Once the customer determines that the semiconductors they have developed are ready to ship to its end-customers for evaluation, the evaluation phase commences.

Evaluation Phase. After the customer receives functioning semiconductors, it typically provides them to its own end-customers for evaluation. These semiconductors are generally application specific devices targeted for products such as cellular phones, digital TVs, set-top boxes, gaming devices, wireless local area networking devices, digital cameras, switches, routers and broadband modems. If our customer successfully wins a sub-system or system level design with its customers, which typically takes from two months to 12 months, it in turn places orders with us to satisfy its customer’s requirements, and production manufacturing commences. Once 100 wafers incorporating a particular design have been ordered, the evaluation phase is complete, the design is classified as being in volume production and it is removed from the design win total. If at any time during the process our customer determines to abandon its design effort, we consider the design a “lost design win” and no longer count it towards our total number of design wins. Once the design cycle is complete and the customer has ordered 100 wafers based on the design, the design is reclassified as a design in volume production, and is no longer considered a design win.

Sales Contracts

Our major customers purchase services and products from us on a contract basis. Most other customers purchase from us using purchase orders. We price our products for these customers on a per wafer or per die basis, taking into account the complexity of the technology, the prevailing market conditions, volume forecasts, the strength and history of our relationship with the customer and our current capacity utilization.

12

Most of our customers usually place their orders only two to four months before shipment; however our major customers are obligated to provide us with longer forecasts of their wafer needs.

Marketing

We advertise in trade journals, organize technology seminars, publish press releases, opinion editorials and whitepapers, perform presentations and speeches at industry conferences, participate in panel sessions, hold a variety of regional and international technology conferences, and attend and exhibit at a number of industry trade fairs to promote our products and services. We discuss advances in our process technology portfolio and progress on specific relevant programs with our prospective and major customers as well as industry analysts and research analysts on a regular basis.

Customers, Markets and Applications

Our customers use our processes to design and market a broad range of digital, analog and mixed-signal semiconductors for diverse end markets including wireless and high-speed wireline communications, consumer electronics, automotive and industrial. We manufacture products that are used for high-performance applications such as transceivers and power management for cellular phones; transceivers and power amplifiers for wireless local area networking products; power management, audio amplifiers and driver integrated circuits for consumer electronics; tuners for digital televisions and set-top boxes; modem chipsets for broadband access devices and gaming devices; serializer/deserializers, or SerDes, for fiber optic transceivers; focal plan arrays for imaging applications; and wireline interfaces for switches and routers.

Conexant and Skyworks were Jazz Semiconductor’s largest customers during 2005 and 2006, together accounting for approximately 60.5% and 38.9% of its revenues, respectively (which includes the effect of a charge against revenue from Conexant of $17.5 million during the second quarter of 2006 associated with the termination of the Conexant wafer supply agreement). Conexant and Jazz Semiconductor entered into a wafer supply agreement as part of the spin-off of Jazz Semiconductor. The wafer supply agreement contained, among other terms and conditions, minimum purchase requirements and provided Conexant with wafer credits applicable to discount the price of future wafers orders. Conexant’s minimum purchase requirements under this agreement terminated in March 2005. Jazz Semiconductor and Conexant agreed to terminate Conexant’s wafer supply agreement as of June 26, 2006 because the agreement, which was entered into at the time of Jazz Semiconductor’s spin-off, no longer reflected the terms and conditions on which the parties wished to conduct business. In connection with the termination of the Conexant wafer supply agreement, as consideration for wafer credits that had not be used by Conexant under this agreement at the time of its termination, Jazz Semiconductor agreed to issue 7,583,501 shares of its common stock to Conexant and to forgive $1.2 million owed to Jazz Semiconductor by Conexant for reimbursement of property taxes previously paid by Jazz Semiconductor. In addition, Jazz Semiconductor agreed, under certain circumstances to issue additional shares of its common stock so that the aggregate value of the common stock received by Conexant equaled $16.3 million. This wafer supply termination agreement was subsequently amended in connection with the execution of the merger agreement relating to the acquisition of Jazz Semiconductor to provide for the repurchase of such shares immediately prior to the completion of the merger and the termination of the obligation to issue additional shares for an aggregate consideration of $16.3 million in cash. Because Conexant did not have any minimum purchase obligations under the wafer supply agreement at the time it was terminated, there was no change in Conexant’s obligation to place orders with Jazz Semiconductor. Jazz Semiconductor also entered into a wafer supply agreement Skyworks. The initial term of the Skyworks wafer supply agreement expires in March 2007; however, the minimum purchase requirements under this agreement also terminated in March 2005. We are currently focused on developing and broadening our relationships with our other post-spin-off customers.

Jazz Semiconductor’s backlog, which represents the aggregate purchase price of orders received from customers, but not yet recognized as revenues, was approximately $41.1 million, $63.6 million and $56.0 million at December 31, 2004, December 30, 2005 and December 29, 2006, respectively. We expect to fill a significant majority of orders in backlog at December 29, 2006 within the current fiscal year. All of our orders, however, are subject to possible rescheduling by its customers. Rescheduling may relate to quantities or delivery dates, but sometimes relates to the specifications of the products it is shipping. Our supply contracts with our largest customers provide for penalties if firm orders are cancelled. Other customers do business with us on a purchase order basis, and some of these orders may be cancelled by the customer without penalty. We also may elect to permit cancellation of orders without penalty where management believes it is in our best interests to do so. Consequently, we cannot be certain that orders on backlog will be shipped when expected or at all. For these reasons, as well as the cyclical nature of our industry, we believe that our backlog at any given date is not a meaningful indicator of our future revenues.

13

Our Major Customers

Skyworks Solutions, Inc. is an industry leader in radio solutions and precision analog semiconductors servicing a diversified set of mobile communications customers. Skyworks was formed upon the spin-off of Conexant’s wireless communications division and subsequent merger with Alpha Industries, Inc. We work closely with Skyworks to define the process technologies it requires to design certain of its next-generation products for its target markets. The products that we manufacture for Skyworks include semiconductors used in RF transceivers and power control devices for cellular phone applications. We have also entered into a wafer supply agreement with Skyworks.

Conexant Systems, Inc. is a leading semiconductor supplier providing system solutions that enable digital information and entertainment networks. Conexant’s product portfolio includes the building blocks required for bridging cable, satellite, and terrestrial data, digital video networks and wireless local area networks. We continue to produce a significant percentage of Conexant’s wafer requirements. Conexant remains a large and important customer for us and we continue to work closely with Conexant to capture its new design opportunities. The products that we manufacture for Conexant include semiconductors used in analog, DSL and cable modems, personal computers, set-top boxes and gaming devices.

Marvell Technology Group Ltd. specializes in the design of high performance, mixed-signal and digital semiconductors aimed at the high-speed computer, storage, communications and multimedia markets. Marvell has designed semiconductors utilizing our SiGe BiCMOS process technology for use in its wireless local area networking products for the portable and fixed gaming console markets, as well as the cellular handset market.

RF Micro Devices, Inc. designs, develops, manufactures and markets proprietary radio frequency integrated circuits, or RFICs, primarily for wireless communications products and applications such as cellular phones and base stations, wireless local area networking devices and cable modems. RF Micro Devices offers a broad array of products, including amplifiers, mixers, modulators/demodulators, and single-chip receivers, transmitters and transceivers that represent a substantial majority of the RFICs required in wireless handsets. RF Micro Devices formed a strategic relationship with Jazz Semiconductor in October 2002 that included a wafer supply agreement, a master development agreement and an equity investment in Jazz Semiconductor, which was sold to us in connection with our acquisition of Jazz Semiconductor.

Freescale Semiconductor, Inc. designs and manufactures embedded semiconductors for the automotive, consumer, industrial, network and wireless markets. In June 2005, we entered into a wafer supply and foundry agreement with Freescale. The products that we manufacture for Freescale under this agreement include RF transceivers for cellular products and ultra wideband transceivers.

Airoha Technology Corp. is a leading wireless communication integrated circuit design company in Taiwan, which produces highly integrated RF mixed-signal integrated circuits for wireless communication applications. Airoha has designed semiconductors using our SiGe BiCMOS process technology for use in its wireless LAN and personal handy phone system products.

Xceive Corporation is a fabless semiconductor company that produces RF-to-baseband transceiver integrated circuits for TVs and set-top boxes. Xceive has designed semiconductors using our 0.18 micron SiGe BiCMOS process technology for use in its personal computer and mobile television tuner products.

RF Magic, Inc. is a fabless semiconductor company that provides a diversified portfolio of RF Systems on a Chip ICs for consumer electronic applications. RF Magic has designed semiconductors using our 0.35 micron BiCMOS and 0.35 micron SiGe BiCMOS process technology for use in its wireless transceivers and silicon television tuner products.

14

Mindspeed Technologies, Inc. designs, develops and sells semiconductor solutions for communications applications in enterprise, access, metropolitan and wide area networks. Mindspeed has designed semiconductors using our analog CMOS, advanced analog CMOS, BiCMOS and SiGe BiCMOS process technologies for use in its high-speed networking integrated circuits and video products.

New Customer Development

Through Jazz Semiconductor’s focus on developing new customer relationships, at December 29, 2006, Jazz Semiconductor had secured over 300 design wins with over 100 post-spin-off customers across a broad range of end markets. We believe our continuous focus on achieving design wins as well as on ramping up production volumes of our current design wins will allow us to continue to diversify and grow our revenue base. The following table provides a summary of end-user applications as well as representative products addressed by its design wins and designs in volume production:

Wireless Communications | Consumer Electronics | Wireline Communications | Other Markets | |||||

| Representative end market products | · Cellular phones · Wireless networking systems | · Digital TVs · DVD players · Cordless phones · Gaming devices · Set-top boxes | · Switches · Optical transceivers · Broadband modems · Analog modems | · Imaging products · Military products · Automotive radar · Sensors | ||||

| Representative semiconductors | · GSM/GPRS/ EDGE transceivers · Power amplifiers · WCDMA transceivers · Ultra wideband transceivers | · DSL and cable modem chipsets · Digital and mobile TV tuners · DVD laser drivers · Power management | · SerDes for transceiver modules · Analog to digital converters | · Image sensors · Focal plane arrays | ||||

| Representative publicly-announced customers | · Airoha · Freescale · Marvell Technology · RF Micro Devices · Skyworks | · Conexant · Xceive · Micro Linear · RF Magic | · Conexant · Mindspeed · Texas Instruments | · DRS Systems · Rockwell Scientific |

Jazz Semiconductor recently entered into a technology license agreement and a technology transfer agreement with PolarFab pursuant to which we acquired, directly and by license, certain process technologies that we intend to incorporate into our BCD process technologies. PolarFab is obligated to cooperate with us to transfer at least 50% of its foundry services, including its third-party customers utilizing the acquired technologies, to us by June 2007, and 95% of these foundry services to us by February 2008. We are required to make payments to Polar Fab based on milestones associated with the qualification of the acquired process technology and royalty payments based on a percentage of revenue from sales of devices using the acquired technology. The technology license agreement restricts us from manufacturing more than 250 wafers per quarter for certain current customers of PolarFab until May 2007. This restriction does not apply to the manufacture and sale of analog devices to current customers of either PolarFab or us if such devices are of a type that have not been previously manufactured by PolarFab for the respective customer.

Competition

We compete internationally and domestically with dedicated foundry service providers such as Taiwan Semiconductor Manufacturing Company, United Microelectronics Corporation, Semiconductor Manufacturing International Corporation and Chartered Semiconductor Manufacturing Ltd., which, in addition to providing leading edge complementary metal oxide semiconductor process technologies, also have capacity for some specialty process technologies. We also compete with integrated device manufacturers that have internal semiconductor manufacturing capacity or foundry operations, such as IBM. In addition, several new dedicated foundries have commenced operations and may compete directly with us. Many of our competitors have higher capacity, longer operating history, longer or more established relationships with their customers, superior research and development capability and greater financial and marketing resources than us. As a result, these companies may be able to compete more aggressively over a longer period of time than us.

15

IBM competes in both the standard CMOS segment and in specialty process technologies. In addition, there are a number of smaller participants in the specialty process arena. We believe that most of the large dedicated foundry service providers compete primarily in the standard CMOS segment, but they also have capacity for specialty process technologies. Prior to Jazz Semiconductor’s separation from Conexant, Conexant entered into a long-term licensing agreement with Taiwan Semiconductor Manufacturing Company under which Taiwan Semiconductor Manufacturing Company licensed from Conexant the right to manufacture semiconductors using Conexant’s then existing 0.18 micron or greater SiGe BiCMOS process technologies. We do not believe that Taiwan Semiconductor Manufacturing Company has focused its business on the SiGe BiCMOS market to date. However, Taiwan Semiconductor Manufacturing Company publicly announced in 2001 that it planned to use the licensed technology to accelerate its own foundry processes for the networking and wireless communications markets. Since the spin-off of Jazz Semiconductor from Conexant, Jazz Semiconductor has continued to make improvements in its SiGe BiCMOS process technology. We have not licensed any of these improvements to Taiwan Semiconductor Manufacturing Company. We do not believe that the license of SiGe BiCMOS process technology by Taiwan Semiconductor Manufacturing Company has had any significant effect on our business or competitive position. In the event Taiwan Semiconductor Manufacturing Company determines to focus its business on the SiGe BiCMOS market, it may use and develop the technology licensed to it in 2001 to compete directly with us in the specialty market, and such competition may harm our business.

As our competitors continue to increase their manufacturing capacity, there could be an increase in specialty semiconductor capacity during the next several years. As specialty capacity increases there may be more competition and pricing pressure on our services, which may result in underutilization of our capacity. Any significant increase in competition or pricing pressure may erode our profit margins, weaken our earnings or increase our losses.

Additionally, some semiconductor companies have advanced their complementary metal oxide semiconductor designs to 90 nanometer or smaller geometries. These smaller geometries may provide the customer with performance and integration features that may be comparable to, or exceed, features offered by our specialty process technologies, and may be more cost-effective at higher production volumes for certain applications, such as when a large amount of digital content is required in a mixed-signal semiconductor and less analog content is required. Our specialty process technologies will therefore compete with these advanced CMOS processes for customers and some of our potential and existing customers could elect to design these advanced CMOS processes into their next generation products. We are not currently capable, and do not currently plan to become capable, of providing CMOS processes at these smaller geometries. If our existing customers or new customers choose to design their products using these CMOS processes our business may suffer.

The principal elements of competition in the semiconductor foundry industry include:

· technical competence;

· production speed and cycle time;

· time-to-market;

· research and development quality;

16

· available capacity;

· fab and manufacturing yields;

· customer service;

· price;

· management expertise; and

· strategic relationships.

There can be no assurance that we will be able to compete effectively on the basis of all or any of these elements. Our ability to compete successfully may depend to some extent on factors outside of our control, including industry and general economic trends, import and export controls, exchange controls, exchange rate fluctuations, interest rate fluctuations and political developments. If we cannot compete successfully in our industry, our business and results of operations will be harmed.

Research and Development

The semiconductor industry is characterized by rapid changes in technology. As a result, effective research and development is essential to our success. Jazz Semiconductor invested approximately $22.8 million in 2003, $18.7 million in 2004, $19.7 million in 2005 and $20.1 million in 2006 in research and development, which represented 12.3%, 8.5%, 9.9% and 9.5% of its revenues in each period, respectively. We plan to continue to invest significantly in research and development activities to develop advanced process technologies for new applications. As of March 1, 2007, we employed 80 professionals in our research and development department, approximately 24 of whom hold Ph.D. degrees.

Our research and development activities seek to upgrade and integrate manufacturing technologies and processes. Although we emphasize firm-wide participation in the research and development process, we maintain a central research and development team primarily responsible for developing cost-effective technologies that can serve the manufacturing needs of our customers. A substantial portion of our research and development activities are undertaken in cooperation with our customers and equipment vendors.

Intellectual Property

Our success depends in part on our ability to obtain patents, licenses and other intellectual property rights covering and relating to wafer manufacturing and production processes, semiconductor structures and other structures fabricated on wafers. To that end, we have acquired certain patents and patent licenses and intend to continue to seek patents covering and relating to wafer manufacturing and production processes, semiconductor structures and other structures fabricated on wafers. As of March 1, 2007, we had 140 patents in force in the United States and 13 patents in force in foreign countries. We also had 24 pending patent applications in the United States, 31 pending patent applications in foreign countries and one pending patent application under the Patent Cooperation Treaty.

The Patent Cooperation Treaty permits us to simultaneously seek protection for an invention in over one hundred member countries. Under this treaty, our application is first subjected to a search for published documents that could affect the patentability of the invention. After the search, we may request a preliminary examination on patentability, or submit an application in elected countries. We may also request a preliminary examination that will result in a Patent Cooperation Treaty written opinion on patentability before we submits an application in elected countries. Upon submitting an application in elected countries, the search result or the written opinion on patentability will be used by each country to determine patentability of the invention. The Patent Cooperation Treaty process is an optional formal and preliminary process to reduce costs by centralizing the search and preliminary examination that each country would otherwise have to perform. Furthermore, the Patent Cooperation Treaty process permits us to avoid translation costs and patent office costs associated with filing an application in a member country before making a preliminary examination of whether the patent application is likely to be accepted.

17

Our issued patents have expiration dates ranging from 2007 to 2024. We consider our patent portfolio to be important to our business, but do not view any single patent as material in relation to our overall revenues. We believe that our SiGe and BiCMOS portfolios are material to our business. Patents within our SiGe portfolio expire at various times from 2020 to 2024. Patents within our RF CMOS portfolio expire at various times from 2018 to 2024. Patents within our BiCMOS portfolio expire at various times from 2008 to 2024.

Our expired patents generally related to legacy technologies that were developed by our predecessors, namely Rockwell. Due to the rapid pace of technological changes and advancement in the field of semiconductor fabrication and processing, we do not believe that the expiration of these patents materially affected our competitive position.