United States Securities and Exchange Commission

100 F Street, N.E.

Washington, D.C. 20549

| Attention: | Tabatha Akins, Staff Accountant |

| Division of Corporate Finance | |

| Telephone Number: (202)551-3658 | |

| Fax Number: (202)772-9217 |

| Re: | Intellect Neurosciences, Inc. |

| Item 4.01 Form 8-K | |

| Filed January 23, 2009 | |

| File No. 333-128226 |

VIA EDGAR AND FACSIMILE

February 4, 2009

Dear Ms. Akins:

On behalf of Intellect Neurosciences, Inc. (the “Company”), we are providing the following responses to the comments set forth in the comment letter dated January 26, 2009 (the “Comment Letter”) from the Staff (the “Staff”) of the Securities and Exchange Commission to Mr. Elliot Maza, President and Chief Financial Officer of the Company.

Item 4.01, Form 8-K filed January 23, 2009,

1. STAFF COMMENT: It appears Eisner LLP disclosed an uncertainty of the Registrant to continue as a going concern in your amended Form 10-KSB filed November 7, 2008. Please revise your disclosure to provide a description of nature of their conclusion. Refer to Item 304(a)(1)(ii) of Regulation S-K.

| COMPANY RESPONSE: | In response to the Staff’s requested revisions as set forth in the Comment Letter, the Company filed an amended report on Form 8-K/A on the date hereof (the “Amended Filing”) to amend its filing on Form 8-K filed January 28, 2009 (the “Original Filing”). A conformed copy of the Amended Filing is being filed herewith. |

Eisner LLP’s (the “Predecessor Auditor”) report contained explanatory language regarding doubt about the ability of the Company to continue as a going concern. The explanatory language was based on information contained in Note 1 to the Financial Statements under subheadings “Operations and Liquidity and Basis of Presentation” on pages F-6 and F-7 of the Company’s Form 10-KSB. This note provided that the Company may be unable to continue as a going concern because of the following: the Company has a negative working capital position, a total capital deficiency, net cash outflows from operating activities, recurring net operating losses, defaults on certain debt obligations and dependence on equity and debt financings to support the Company’s business efforts.

In response to the Staff’s request in Item 1 of the Comment Letter, the Company states that paragraph three of the Amended Filing restates the text of paragraph three of the Original Filing and refers to the explanation above.

2. STAFF COMMENT: Your reference to “During the Period” in the fourth paragraph is too vague; please amend your filing to state, if true, that in connection with the audits of the Company’s financial statements for the fiscal years ended June 30, 2008 and 2007, and in the subsequent interim period through January 19, 2009 (the date of the dismissal of the former accountant, there were no disagreements with Eisner LLP on any matter of accounting principles or practices, financial statement disclosure or auditing scope and procedure which, if not resolved to the satisfaction of the former accountant, would have caused it to make reference to the subject matter of the disagreement in connection with its report. Describe each such disagreement as applicable in accordance with Item 304(a)(1)(iv) of Regulation S-K.

| COMPANY RESPONSE: | In response to the Staff’s request in Item 2 of the Comment Letter, the Company states that paragraph four of the Amended Filing restates the text of paragraph four of the Original Filing while also specifically stating that, in connection with the audits of the Company’s financial statements for the fiscal years ended June 30, 2008 and 2007, and through January 19, 2009 (the date of the dismissal of the Predecessor Auditor), there were no disagreements with the Predecessor Auditor on any matter of accounting principles or practices, financial statement disclosure, or auditing scope and procedure which, if not resolved to satisfaction of the Predecessor Auditor, would have caused it to make reference to the subject matter of the disagreement in connection with the Form 8-K. |

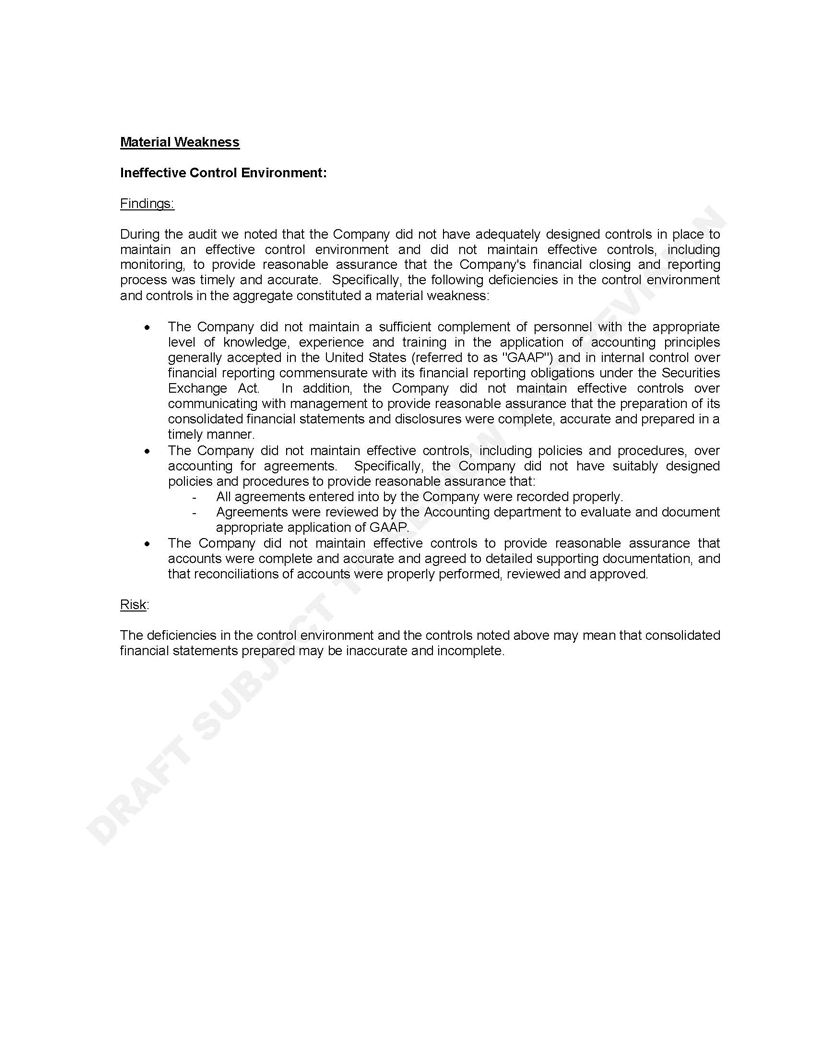

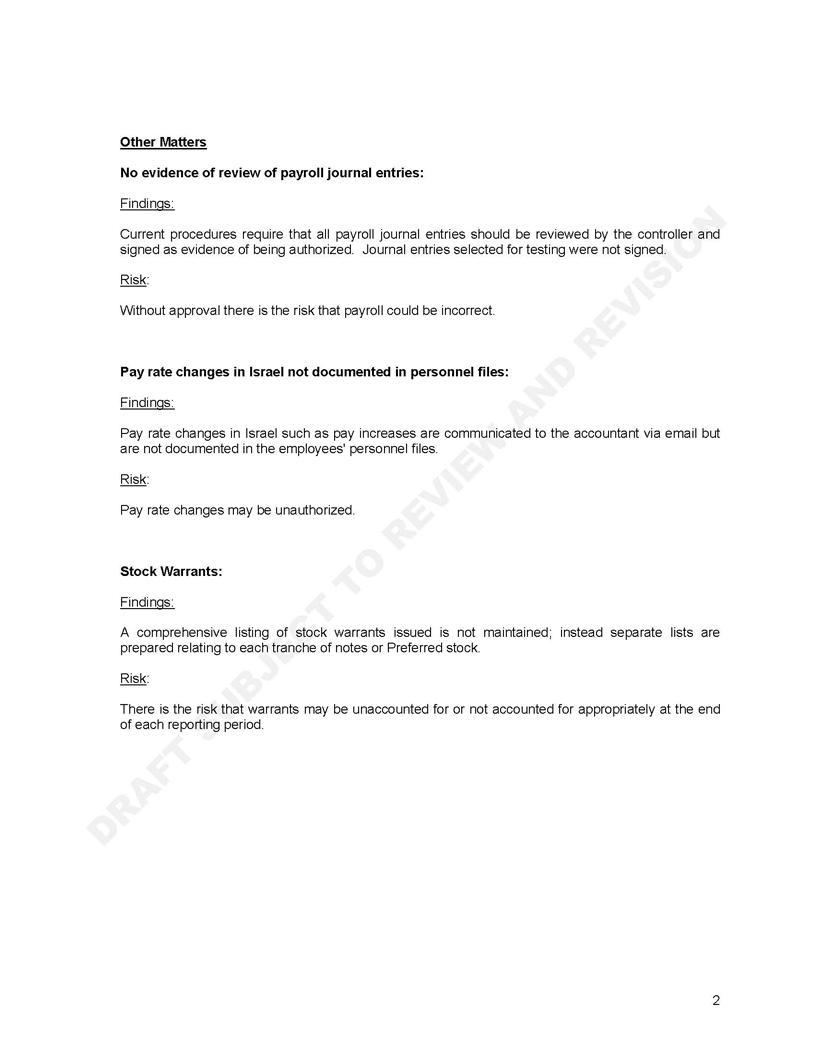

3. STAFF COMMENT: In detail, supplementally describe the nature of each material weakness and the amounts involved, as applicable. Also, tell us:

| a. | in what period each material weakness and accounting error or misapplication of GAAP occurred, |

| b. | the amount of each accounting error and misapplication of GAAP, |

| c. | the reason(s) for each error or misapplication of accounting, and |

| d. | in detail, all the steps you have taken (or plan to take) and procedures you have implemented (or plan to implement) to correct each concern. |

| COMPANY RESPONSE: | In response to the Staff’s request in Item 3 of the Comment Letter, the Company provides the following supplemental information: |

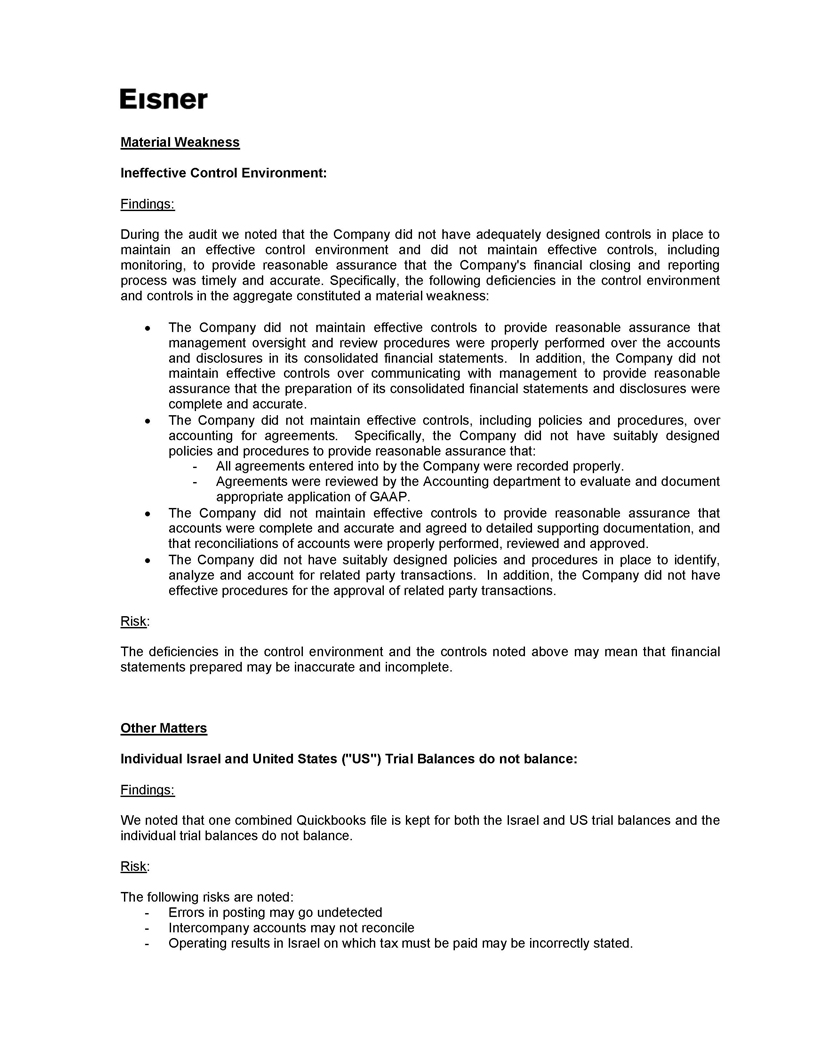

| The Company disclosed in its Form 10-KSB filed November 7, 2008 that it identified a material weakness in internal control over financial reporting. The material weakness in internal control is a qualitative issue that the Company believes does not lend itself to direct quantitative identification. However, the Company recorded certain audit adjustments (see response to Staff Comment 4). |

| The material weakness resulted from the Company’s lack of adequate personnel to separately review the books and records and individual accounting entries as contemplated by prevailing standards for internal controls over financial reporting. Upon identification of the material weakness, the Audit Committee of the Company’s Board of Directors consulted with Company management regarding the material weakness identified above and related remediation efforts. The Company intends to engage sufficient part time external personnel to assist in the preparation and review of the financial statements at each financial reporting cycle to compensate for the lack of adequate full time personnel in the Company’s accounting function. |

4. STAFF COMMENT: Please provide us with a schedule of your fiscal year end fourth quarter adjustments to close the books, or adjustments recorded in connection with or as a result of the audit. Clearly explain the reason for each adjustment. For each adjustment, show us the impact on pre-tax net loss. Quantify the net effect of all adjustments on pre-tax net income (loss). Provide us with the same information for any quarterly review adjustments. Also, tell us why none of the adjustments relate to prior period. Explain in detail why you believe the timing of each adjustment is appropriate.

| COMPANY RESPONSE: | In response to the Staff’s request in Item 4 of the Comment Letter, the Company states that the Company recorded certain fourth quarter adjustments for the fiscal year end relating to its closure of its research laboratory in Israel and certain audit adjustments. The adjustments are attached hereto as Exhibit A and hereby submitted to the Staff as supplemental materials. Also, the Company recorded certain adjustments at the close of each quarter during the fiscal year ended June 30, 2008, which are listed on Exhibit B attached hereto and hereby submitted to the Staff as supplemental materials. |

5. STAFF COMMENT: Provide us with any letter or written communication to and from the Former Auditors regarding any disagreements or reportable events to management or the Audit Committee.

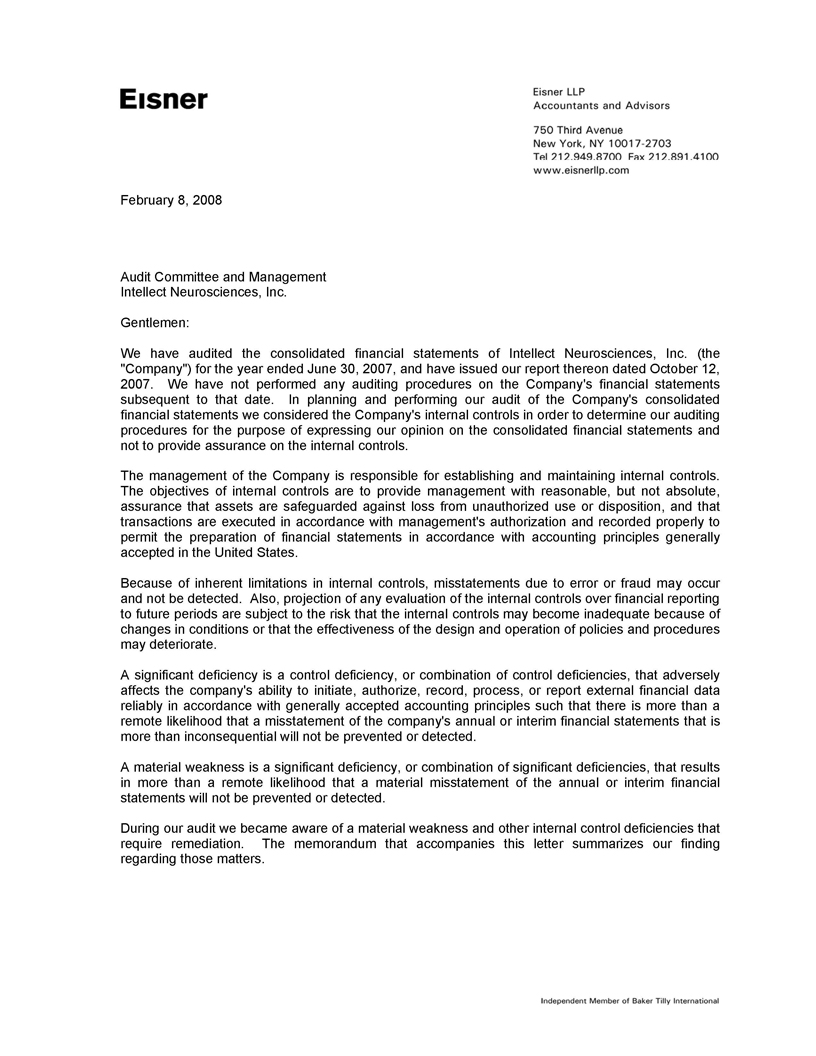

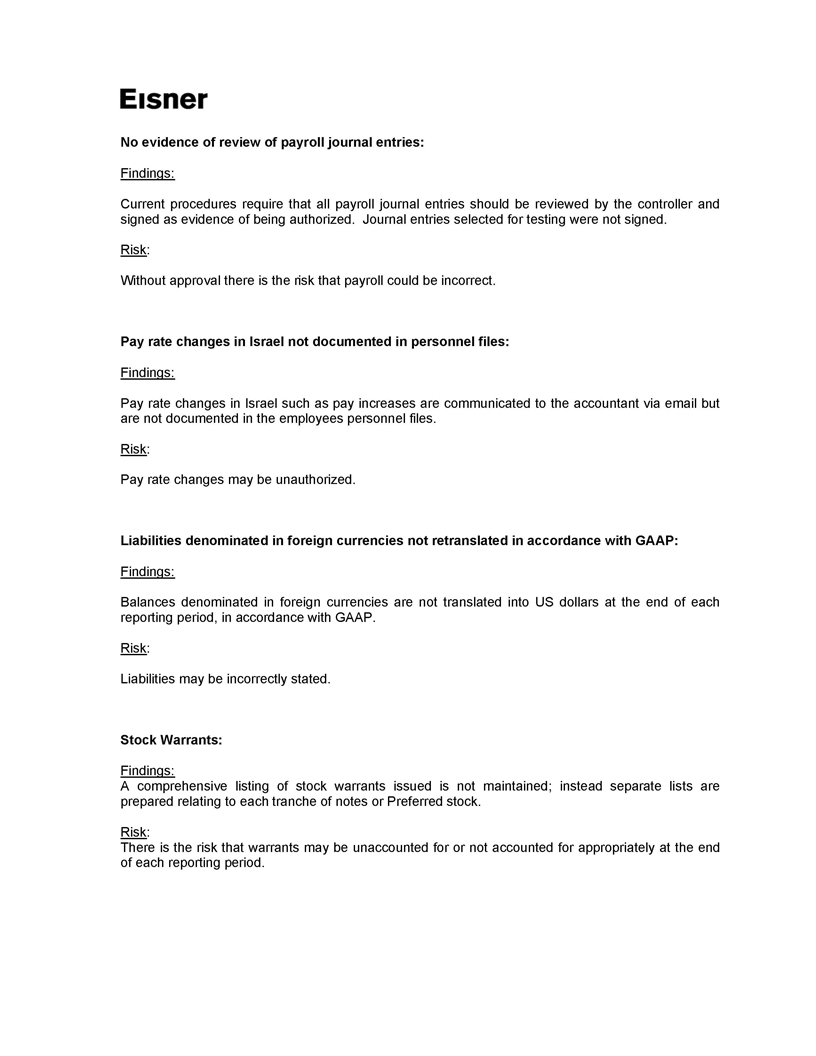

| COMPANY RESPONSE: | In response to the Staff’s request in Item 5 of the Comment Letter, the Company states that for the fiscal years ended June 30, 2008 and 2007, and through January 19, 2009, there were no reportable events communicated by the Predecessor Auditor either to the Company’s management or to the Audit Committee of the Company except as described in the attached Letters from the Predecessor Auditor to the Audit Committee and Management of Intellect Neurosciences, Inc. attached hereto as Exhibit C and Exhibit D and hereby submitted to the Staff as supplemental material. Further, the Company states that for the fiscal years ended June 30, 2008 and 2007, and through January 19, 2009, there were no disagreements between the Predecesor Auditor and the Company or its management during these periods. |

6. STAFF COMMENT: Your reference to “During the period” in the ninth paragraph is too vague. Please amend your filing to specifically state whether, during your past two fiscal years ended June 30, 2008 and 2008, through the date of engagement (January 19, 2009), you consulted Eisner, LLP regarding any of the matters outlined in Item 304(a)(2) of Regulation S-K.

| COMPANY RESPONSE: | The Company assumes that the Staff’s inquiry as to the Company’s consultations with “Eisner, LLP” was instead to identify the Company’s consultations with the Company’s new independent registered accounting firm, Paritz & Company, P.A. (“Paritz”). |

| Accordingly, in response to the Staff’s request in Item 6 of the Comment Letter, paragraph nine of the Amended Filing restates the text of paragraph nine of the Original Filing while also specifically stating that for the fiscal years ended June 30, 2008 and 2007, through the date of engagement (January 19, 2009), neither the Company nor anyone acting on its behalf consulted with Paritz regarding either (i) the application of accounting principles to a specified transaction, either completed or proposed, or the type of audit opinion that might be rendered on the Company’s consolidated financial statements, and neither a written report nor oral advice was provided to the Company that Paritz concluded was an important factor considered by the Company in reaching a decision as to an accounting, auditing or financial reporting issue; or (ii) any matter that was either the subject of a disagreement (as defined in paragraph (a)(1)(iv) of Item 304 of Regulation S-K and the related instructions thereto) or reportable event (as described in paragraph (a)(1)(v) of Item 304 of Regulation S-K). |

7. STAFF COMMENT: Upon amending your filing, please include, as Exhibit 16, an updated letter from your former accountants, Eisner, LLP, as required by Item 304(a)(3) of Regulation S-K. Please ensure that your former accountants date their letter.

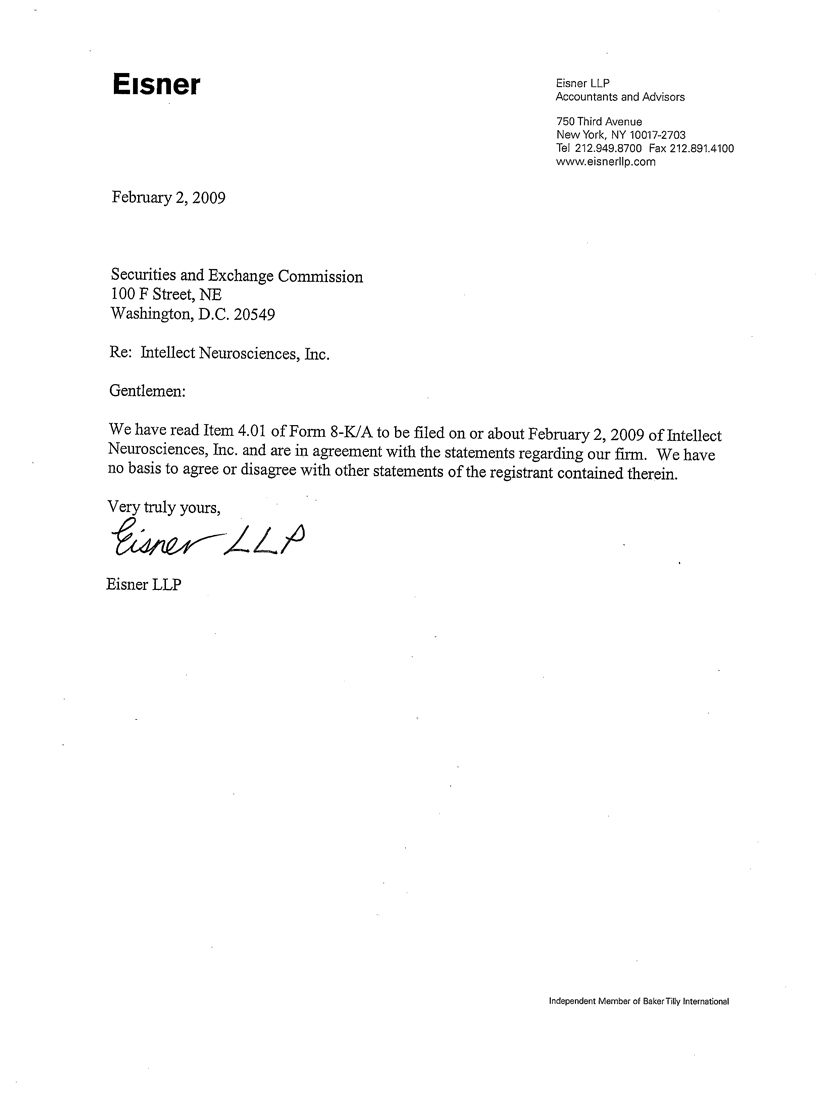

| COMPANY RESPONSE: | We have included an updated letter from our Predecessor Auditor, attached hereto as Exhibit D. A copy of such letter, dated February 2, 2009, has been filed with the Amended Filing as Exhibit 16.1. |

8. The Company acknowledges that the Company is responsible for the adequacy and accuracy of the disclosure in the filing, that Staff comments or changes to disclosure in response to Staff comments do not foreclose the Commission from taking any action with respect to the filing, and that the Company may not assert Staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States.

Please do not hesitate to call Elliot Maza at 212-448-9300 with any questions or further comments you may have regarding this filing or if you wish to discuss the responses above.

| Sincerely, |

| INTELLECT NEUROSCIENCES, INC. |

| /s/ Elliot Maza |

| Elliot Maza |

| President and Chief Financial Officer |

Attachment A

Conformed copy of the Company’s amended report on Form 8-K/A filed on the date hereof to amend its filing on Form 8-K filed January 28, 2009

[See attached.]

Exhibit A

Fiscal Year End Fourth Quarter Adjustments

Adjustments related to closure of Israeli research laboratory

1. We disclosed in Note 1, Nature of Operations and Basis of Presentation and Note 14. Commitments and Other Matters, and in the accompanying Management’s Discussion and Analysis of Financial Condition and Results of Operations (“MD&A”) to our financial statements for the fiscal year ended June 30, 2008, that during the fourth quarter of fiscal 2008, Intellect effectively closed its Israeli laboratory and terminated all but three of the remaining employees due to a lack of funds. In accordance with SFAS No. 146, “Accounting for Costs Associated with Exit or Disposal Activities”, we have included $62,167 of rent expense for our Israeli laboratory for the year ended June 30, 2008, representing the present value of the excess of our rental commitment in Israel through October 2011 over the estimated future sublease income from the laboratory during that period. The total amount of rent expense for our Israeli laboratory for the year ended June 30, 2008 is approximately $230,994. Total rent expense amounted to $373,624 and $258,736 for the years ended June 30, 2008 and June 30, 2007, respectively.

| Debit: R&D (Israel rent) | $ | 62,167 | |||

| Credit: Cash | $ | 62,167 |

To record R&D expense from Israel laboratory rent, including giving effect to the shut down of the laboratory. Pre-tax net loss is increased by the full amount of the incremental rent recognition ($62,167).

2. As a result of closing the Israel laboratory, we have reflected our remaining laboratory equipment on our balance sheet as being held for sale at an amount equal to the estimated fair value of such equipment and have taken a corresponding charge for the write-down.

| Debit: Israel accumulated depreciation | $ | 148,735 | |||

| Credit: Israel fixed assets | $ | 148,735 |

To record write down of remaining laboratory equipment to fair market value. Pre-tax net loss is increased by the full amount of the incremental rent recognition ($148,735).

Fiscal Year End Audit Adjustments

Audit adjustment related to revenue recognition

We disclosed in Note 1, Nature of Operations and Basis of Presentation and Note 6. Research and License Agreements, and in the accompanying MD&A to our financial statements for the fiscal year ended June 30, 2008, In May, 2008, that Intellect entered into a License Agreement (the “Agreement”) by and among Intellect and AHP MANUFACTURING BV, acting through its Wyeth Medica Ireland Branch, (“Wyeth”) and ELAN PHARMA INTERNATIONAL LIMITED (“Elan”) to provide Wyeth and Elan (collectively, the “Licensees”) with certain license rights under certain of our patents and patent applications (the “Licensed Patents”) relating to certain antibodies that may serve as potential therapeutic products for the treatment for Alzheimer’s Disease (the “Licensed Products”) and for the research, development, manufacture and commercialization of Licensed Products.

As a result of a continuing obligation to incur patent or program research related expenses or additional licensing, Management recorded an adjustment to record the up-front payment of $1 million received from the Licensees as a deferred credit on our consolidated balance sheet, rather than as revenue from the License arrangement. The deferred credit represents our obligation to fund future patent or program research related expenses if no additional license agreements are executed. We will amortize the deferred credit over the remaining life of the License, which approximates the remaining life of the underlying patents.

| Debit: License Revenue | $ | 1,000,000 | |||

| Credit: Deferred Credit | $ | 1,000,000 |

To reduce revenue by the full amount of the License payment and reclassify the payment as a Deferred Credit. Pre-tax net loss is increased by the full amount of the payment ($1,000,000).

Other audit adjustments at fiscal year end

| Debit: R&D Expense | $ | 179,072 | |||

| Credit: Accrued expenses | $ | 179,072 |

To record additional accruals at 6/30/08

| Debit: Interest expense | $ | 22,341 | |||

| Credit: Accrued interest payable | $ | 22,341 |

To adjust interest accrual at 6/30/08

| Debit: Prepaid expense | $ | 12,050 | |||

| Credit: G&A expense | $ | 12,050 |

To adjust for overstatement of rent expense for period ended 6/30/08

Exhibit B

Interim Review Adjustments

Adjustments for Quarter Ended September 30, 2007

| Debit: Note payable | $ | 59,508 | |||

| Credit: Interest expense | $ | 59,508 |

To correct the value of warrants issued on 7/21/07 for extension of notes to 10/31/07

| Debit: Interest expense | $ | 320,176 | |||

| Credit: APIC | $ | 320,176 |

To correct the value of common stock issued on 7/12/07 for extension of notes to 9/21/07

Adjustments for Quarter Ended December 31, 2007

| Debit: Common stock | $ | 50 | |||

| Debit: APIC | $ | 119,950 | |||

| Credit: Investor relations expense | $ | 120,000 |

To reverse expense recorded in Q2 that should have been recorded in Q1for contract that was executed on 7/15/07 (restate Q1 quarterly report on Form 10QSB)

Adjustments for Quarter Ended March 31, 2008

| Debit: Note payable | $ | 75,000 | |||

| Credit: Interest expense | $ | 75,000 | |||

| Debit: Interest expense | $ | 11,100 | |||

| Credit: APIC | $ | 11,100 | |||

| Debit: APIC | $ | 23,400 | |||

| Credit: Note payable | $ | 23,400 |

All of the above to correctly reflect the rescission of shares previously issued to note holder for extension of note in exchange for a new (additional) note with a face amount of $75,000. Rescission transaction was entered into on 2/15/08.

Exhibit C

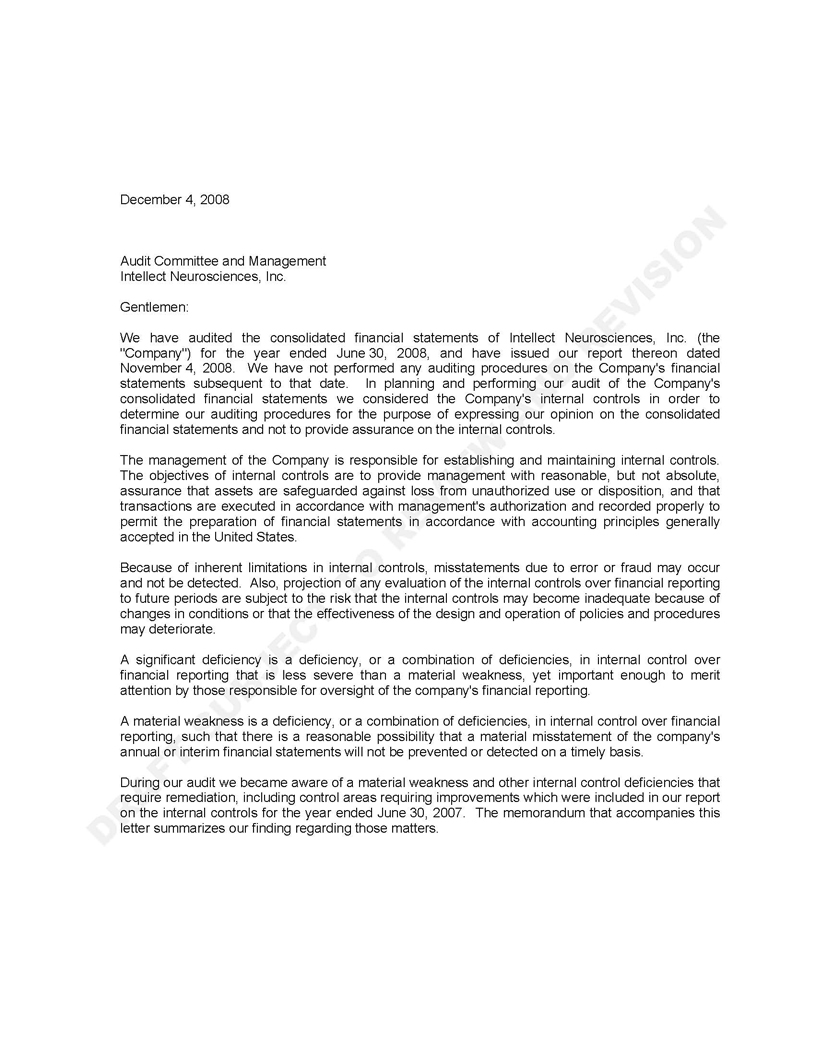

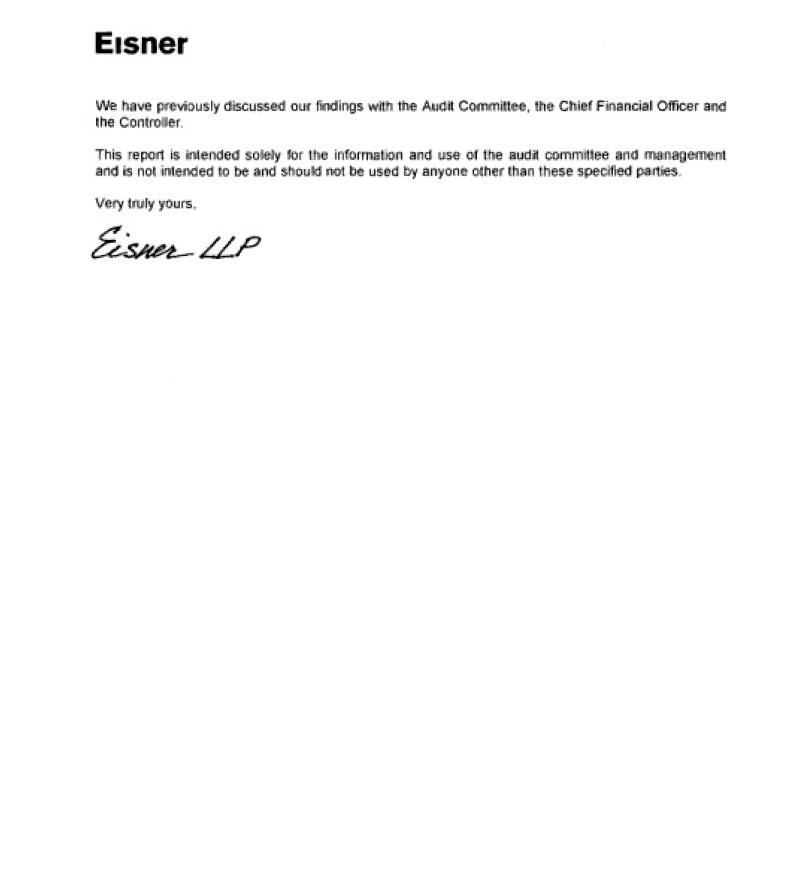

Letter from Eisner, LLP to the Audit Committee and Management of Intellect Neurosciences, Inc. dated December 4, 2008

[See attached.]

Exhibit D

Letter from Eisner, LLP to the Audit Committee and Management of Intellect Neurosciences, Inc. dated February 8, 2008

[See attached.]

Attachment A

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 8-K/A

CURRENT REPORT

Pursuant to Section 13 or 15(d)

of the Securities Exchange Act of 1934

Date of Report (Date of earliest event reported): January 19, 2009

Intellect Neurosciences, Inc.

(Exact Name Of Registrant As Specified In Its Charter)

Delaware

(State or Other Jurisdiction of Incorporation)

| 333-128226 | 20-2777006 |

| (Commission File Number) | (I.R.S. Employer Identification No.) |

| 7 West 18th Street, New York, NY | 10011 |

| (Address of Principal Executive Offices) | (Zip Code) |

(212) 448-9300

(Registrant’s Telephone Number, Including Area Code)

(Former Name or Former Address, if Changed Since Last Report)

Check the appropriate box below if the Form 8-K filing is intended to simultaneously satisfy the filing obligation of the registrant under any of the following provisions (see General Instruction A.2. below):

o Written communications pursuant to Rule 425 under the Securities Act (17 CFR 230.425) |

o Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 CFR 240.14a-12) |

o Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act (17 CFR 240.14d-2(b)) |

o Pre-commencement communications pursuant to Rule 13e-4(c) under the Exchange Act (17 CFR 240.13e-4(c)) |

Item 4.01. Changes in and Disagreements With Accountants on Accounting and Financial Disclosure.

Dismissal of previous independent registered public accounting firm

This Amendment amends the Current Report on Form 8-K filed on January 23, 2009 (the “Original 8-K”) by Intellect Neurosciences, Inc. (the “Company”) relating to changes in the Company’s independent registered public accounting firm. As disclosed in the Original 8-K, effective January 19, 2009, the Company dismissed Eisner LLP (“Eisner”), which served as the Company’s independent auditor for the period from May 10, 2007 to January 19, 2009 (the “Period”). The Board of Directors of the Company approved the dismissal of Eisner.

Except as noted in the following paragraph, Eisner’s reports during the Period did not contain an adverse opinion or disclaimer of opinion, nor were they qualified or modified as to uncertainty, audit scope or accounting principles.

The audit report prepared by Eisner relating to the Company’s consolidated financial statements for the period ended June 30, 2008 and disclosed in the Company’s Form 10-KSB filed November 7, 2008 includes an explanatory paragraph expressing the substantial doubt about the Company’s ability to continue as a going concern. The conclusion of Eisner that the Company may be unable to continue as a going concern was based on the following: the Company has a negative working capital position, a total capital deficiency, net cash outflows from operating activities, recurring net operating losses, defaults on certain debt obligations and dependence on equity and debt financings to support the Company’s business efforts.

In connection with the audits of the Company’s financial statements for the fiscal years ended June 30, 2008 and 2007, and in the subsequent interim period through January 19, 2009 (the date of the dismissal of Eisner), there were no disagreements with Eisner on any matter of accounting principles or practices, financial statement disclosure, or auditing scope and procedure which, if not resolved to the satisfaction of Eisner, would have caused it to make reference to the subject matter of the disagreement in connection with its report.

Except as noted in the following paragraph, during the Period, there were no reportable events as defined in Item 304(a)(1)(v) of Regulation S-K.

As disclosed in the Company’s Annual Report on Form 10-KSB/A for the fiscal year ended June 30, 2008, the Company identified a material weakness in internal control over financial reporting arising from failure to maintain a sufficient complement of personnel with the appropriate level of knowledge, experience and training in the application of accounting principles generally accepted in the United States and in internal control over financial reporting commensurate with the Company’s financial reporting obligations under the Securities Exchange Act of 1934, as amended and the Company’s resultant non-compliance with Section 404 of the Sarbanes-Oxley Act and current SEC regulations which require the Company to furnish a report of management regarding the Company’s internal control over financial reporting. Upon identification of the material weakness, the Audit Committee of the Board of Directors consulted with Company management regarding the material weakness identified above and related remediation efforts. There was no disagreement with Eisner concerning management’s disclosure of this material weakness in internal control over financial reporting by the Company.

The Company made the contents of the Original 8-K filing and this current report on Form 8-K/A available to Eisner and requested it to furnish a letter to the Company addressed to the Securities and Exchange Commission as to whether or not Eisner agrees or disagrees with, or wishes to clarify the Company’s expression of its views. A copy of such letter, dated February 2, 2009, is filed as Exhibit 16.1 to this Current Report on Form 8-KA.

New independent registered public accounting firm

As was also reported in the Original 8-K, effective January 19, 2009, the Company engaged Paritz & Company, P.A. (“Paritz”) as its independent registered accounting firm for the fiscal year ending June 30, 2009. The Board of Directors of the Company approved the appointment of Paritz.

For the fiscal years ended June 30, 2008 and 2007, through the date of engagement (January 19, 2009), neither the Company nor anyone acting on its behalf consulted with Paritz regarding either (i) the application of accounting principles to a specified transaction, either completed or proposed, or the type of audit opinion that might be rendered on the Company’s consolidated financial statements, and neither a written report nor oral advice was provided to the Company that Paritz concluded was an important factor considered by the Company in reaching a decision as to an accounting, auditing or financial reporting issue; or (ii) any matter that was either the subject of a disagreement (as defined in paragraph (a)(1)(iv) of Item 304 of Regulation S-K and the related instructions thereto) or reportable event (as described in paragraph (a)(1)(v) of Item 304 of Regulation S-K).

Item 9.01 Financial Statements and Exhibits

(d) Exhibits

| Exhibit No. | Description of Exhibit | |

| 16.1 | Letter from Eisner LLP to Securities and Exchange Commission dated February 2, 2009. |

SIGNATURES

Pursuant to the requirements of the Securities Exchange Act of 1934, this report has been signed below by the following persons on behalf of the registrant and in the capacities and on the dates indicated.

| INTELLECT NEUROSCIENCES, INC. | ||

| Date: February 4, 2009 | By: | /s/ Elliot Maza |

| Name: Elliot Maza | ||

Title: President and CFO | ||

Exhibit 16-1 to Form 8-K/A

Exhibit C

Exhibit D