October 2006

Business Update

Forward Looking Statements

Under the Private Securities Litigation Reform Act of 1995

This presentation contains forward looking information which is subject to risks and

uncertainties, including, but not limited to, changes in laws and regulations

impacting the gathering and processing industry, the level of creditworthiness of the

Partnership’s counterparties, the Partnership’s ability to access the debt and equity

markets, the Partnership’s use of derivative financial instruments to hedge

commodity and interest rate risks, the amount of collateral required to be posted

from time to time in the Partnership’s transactions, changes in commodity prices,

interest rates, demand for the Partnership’s services, weather and other natural

phenomena, industry changes including the impact of consolidations and changes in

competition, the Partnership’s ability to obtain required approvals for construction or

modernization of the Partnership’s facilities and the timing of production from such

facilities, and the effect of accounting pronouncements issued periodically by

accounting standard setting boards.

Regulation G

This document may include certain non-GAAP financial measures as defined under

SEC Regulation G. In such an event, a reconciliation of those measures to the most

directly comparable GAAP measures is included in this presentation.

2

Agenda

Business Highlights

GSR Acquisition from DEFS

Additional $250 Million Contribution from

DEFS

Base Business Update

3

DCP Midstream Highlights

Successful IPO launched

December 2005

Strong earnings and unit price

performance

Announced agreement with

sponsor to expand gathering and

transportation services in 1Q 2006

Announced NGL pipeline organic

growth project in 1Q 2006

Increased quarterly distribution by

9% in 2Q 2006

Announced GSR contribution from

DEFS in 4Q 2006

Announced DEFS’ intention to

contribute an additional $250

million of assets to DCP (targeted

for 2Q 2007)

___________________________

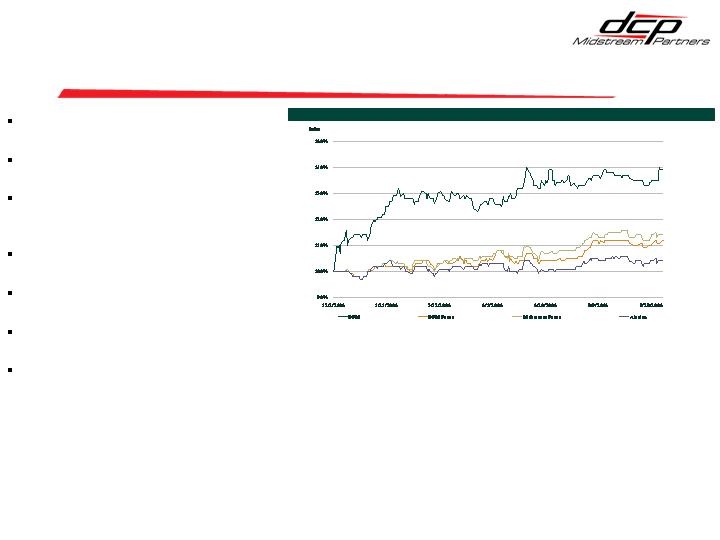

1.

DPM Peer Index includes WPZ, TLP, XTEX, RGNC, HLND, HEP, TCLP, MMLP, MWE and APL.

2.

Midstream Peer Index includes BPL, EEP, EPD, KMP, OKS, PPX, PAA, SXL, TCLP, TPP, VLI, MMP, XTEX, MWE,

MMLP, APL, HEP, HLND, TLP, CPNO, WPZ, RGNC, ETP and BWP.

Total Returns: DPM versus Comparable MLP Indices

Prepared by Lehman Brothers

4

GSR Transaction Overview

DEFS to contribute Gas Supply Resources (GSR)

wholesale propane logistics business to DCP

Transaction valued at approximately $77 million for

base business including new Midland terminal,

subject to standard closing adjustments

DEFS to receive combination of cash and partnership

units

DCP to finance transaction with existing credit facility

GSR 2007 estimated EBITDA: $8.5 million (including

G&A expense)

DEFS to continue to operate post-closing

5

GSR: Key Investment Highlights

Excellent business

Acquisition of a growing franchise, not just assets

Largest propane wholesaler in N.E.

Opportunity to extend into upper Midwest & other areas

Well suited for MLP ownership

Fee-like earnings, qualifying income (but seasonal variability)

Base load sales to market

Organic and acquisition growth opportunities

Minimal maintenance capital

Supports DCP Midstream objectives

Increase cash distributions

Acquire business with growth opportunities

Benefit from strong sponsorship

Diversify asset/earnings portfolio

6

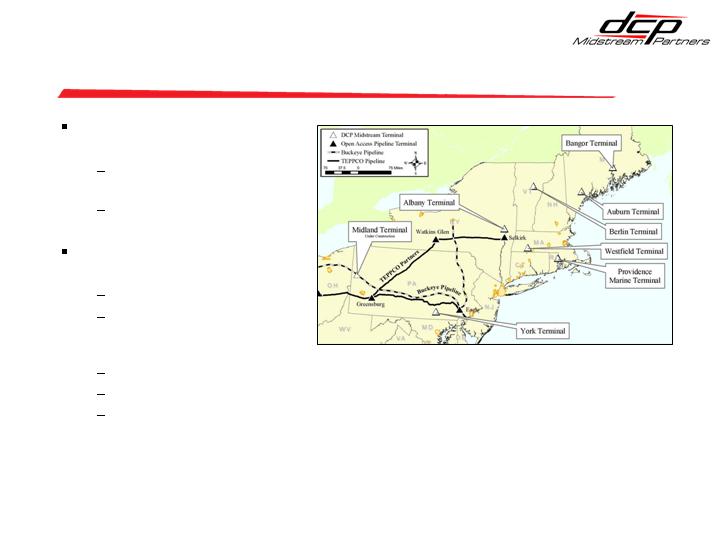

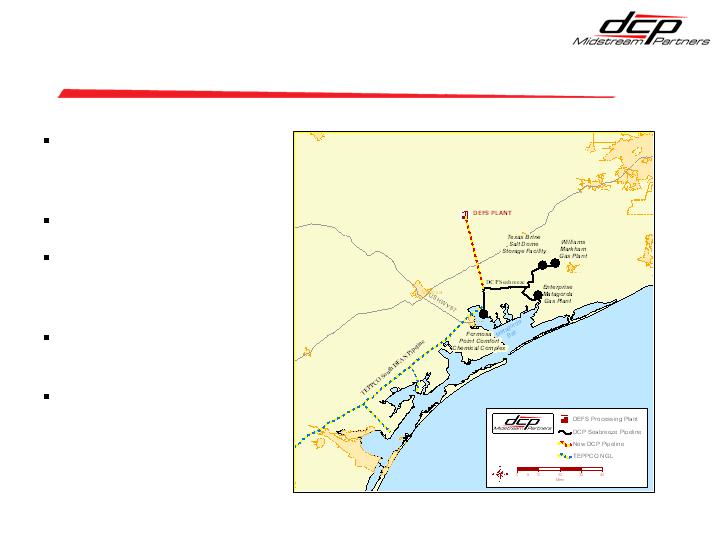

GSR Wholesale Propane Logistics

Largest wholesale propane

supplier in the Northeast

Purchases propane and

sells to retail distributors

Annually Markets

25+ MBbl/d

Integrated and strategically

located business

Six owned rail terminals

New Midland, PA pipeline

terminal: Projected 4Q

2006 start-up

Leased marine terminal

475,000 barrels storage

Marketing at several open

access pipeline terminals

7

GSR Growth Opportunities

Midland, PA pipeline terminal under construction

Market reception has exceeded expectations

Projected 4Q 2006 startup

Receives propane off Buckeye pipeline

Terminals have excess capacity and expansion

potential, providing opportunities to increase volumes

at minimal cost

Actively seeking new rail terminals through

acquisition and/or construction

8

Supply Diversity = Competitive Advantage

Sources:

Pipelines (10%)

TEPPCO

Buckeye

Rail (70%)

Canada (various)

Midwest

Waterbourne (20%)

Shell

Other international LPG

Greater seasonal volume flexibility allows GSR to

become retail customers’ preferred provider

(1)

(1) Propane suppliers typically require customers to draw some fraction of their winter requirements during

the summer months. Due to GSR’s flexibility of supply sources in the winter, the winter deliverability is

higher than the competition.

9

Favorable Contracts

Propane purchase and sale

index-based prices are

generally matched, allowing

DCP to lock in margins and

create fee-like earnings

Diverse customer base

Supplier agreements allow

DCP to minimize working

capital needs

Long term contracts

Propane supply with Aux

Sable (2008 and 2016) and

Shell (2008)

Term rail agreements

Top 3 customers (~30%)

Suburban Propane

Amerigas Partners

Valley National Gas

Top 3 suppliers (~70%)

Aux Sable

Shell

Provident Energy

10

GSR Financial Overview

11

$8.5

EBITDA

1.2

Depreciation and Amortization

4.3

Interest Expense

Add:

$3.0

Net Income

(1)

(2)

(1)

Note 2007 economics assume capital spending of $2.3 million to relocate the York terminal

to access a different railroad line. These expenditures result in future operating cost

savings.

(2)

DCP and DEFS negotiated a $2 million increase to the Omnibus Agreement to cover G&A.

Public company costs and insurance are estimated at an additional $0.3 million.

(3)

Reconciliation of Non-GAAP Measure ($ in millions):

(3)

2007 Estimate

($ in millions)

O&M and G&A Expenses

14.0

$

EBITDA

8.5

$

$250 Million DEFS Contribution

DEFS committed to contribute an additional $250

million of assets

Timing: Targeted for 2Q 2007

Specific assets not yet identified

Transaction subject to approval by board of directors

for both DEFS and DCP as well as DCP conflicts

committee

12

Base Business Update (YTD 2Q 2006)

Solid operating performance results in 9% distribution

increase for 2Q 2006

Net income at 6/30/06 = $14.2 million

Strong commodity prices drive increased processing

margins and marketing opportunities

Drilling activity remains strong

Increased volumes create expansion opportunities

Wilbreeze NGL pipeline on track for 4Q 2006 start-up

13

Key Investment Highlights

Ability to capitalize on strong sponsorship

Assets with strong market positions

Stable cash flows from fee and

substantially hedged commodity

positions

Experienced management team with a

demonstrated track record of growing

midstream and MLP businesses

Low cost of capital to facilitate growth

Identified organic growth

Well Positioned to Execute Growth Strategies

14

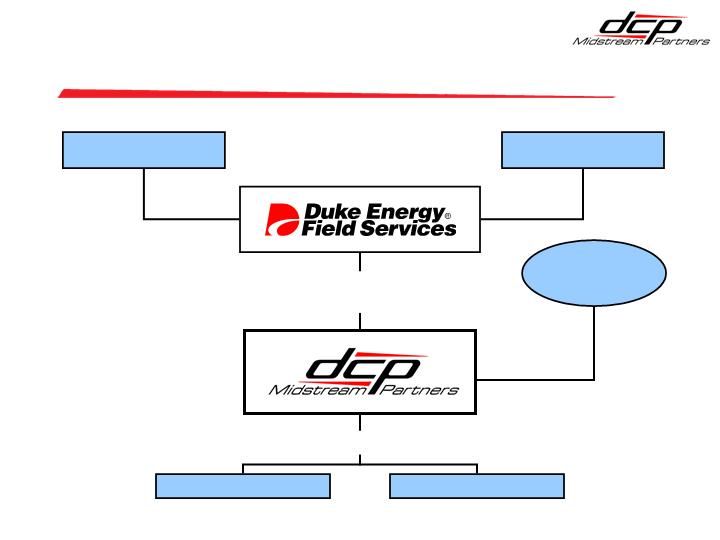

Appendix

58% Common

LP Interest

(10.4MM units)

40.0% Subordinated LP Interest

(7.1MM units)

2.0% GP Interest

NYSE: DPM

50%

50%

Duke Energy

ConocoPhillips

Public

Unitholders

Natural Gas Services

Strong Sponsorship

NGL Logistics

(1)

(1) Pre-GSR acquisition structure

16

DEFS Highlights

One of the nation’s largest natural gas

gatherers

Largest NGL producer in U.S.

Major wholesale propane supplier to northeast

U.S.

Acquired and managed general partner of

TEPPCO (March 2000 – February 2005)

2005 EBITDA of $1.5 billion, excluding

TEPPCO gain on sale

DEFS’ Industry-Leading Midstream Business

DCP Midstream

56,000 miles of pipelines

52 plants; 11 fractionators

8 propane terminals

4 offices

(1)

(1) Pre-GSR acquisition by DCP Midstream

17

Pursue strategic and accretive acquisitions

Consolidate with and expand existing infrastructure

Pursue new lines of business and geographic areas

Potential to acquire assets from Sponsors

Acquire:

Capitalize on organic expansion opportunities

Expand existing infrastructure

Develop projects in new areas

Build:

Maximize profitability of existing assets

Increase capacity utilization

Expand market access

Enhance operating efficiencies

Leverage ability to provide integrated services

Optimize:

Our Primary Business Objective: Increase our Cash Distribution per Unit

Business Strategies

18

Enhanced growth

opportunities

Infrastructure to

support business

objectives

Operational

Commercial

Technical

Risk Management

Administrative

Talent / Infrastructure

Industry

relationships and

reputation

Access to deal flow

Potential to acquire

assets directly from

Sponsors

Joint-transaction

opportunities

Relationships

DCP Midstream Growth

+

=

DCP Midstream Benefits from its Sponsors

DEFS / Duke Energy / ConocoPhillips

19

Platform of Integrated Businesses

Natural Gas Services

Minden and Ada natural gas

gathering and processing

systems

PELICO pipeline system

NGL Logistics

Seabreeze NGL pipeline

Black Lake NGL pipeline

DCP Midstream Operates in Two Business Segments

Natural Gas Services Segment

NGL Logistics Segment

(1)

(1) Pre-GSR acquisition structure

20

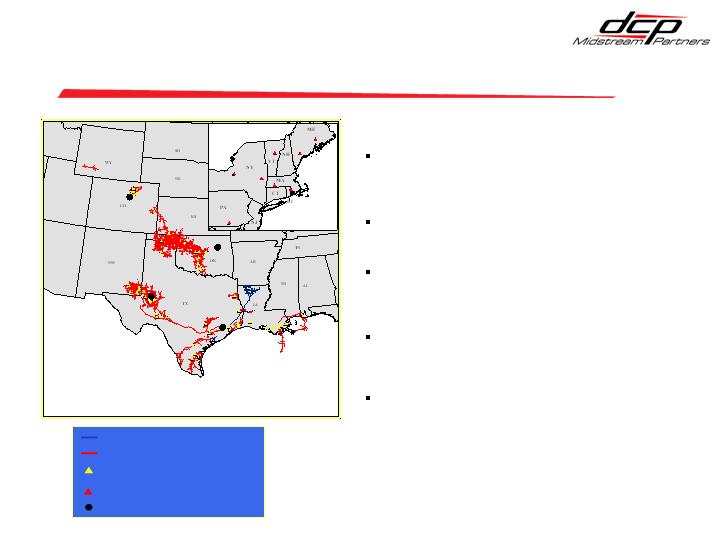

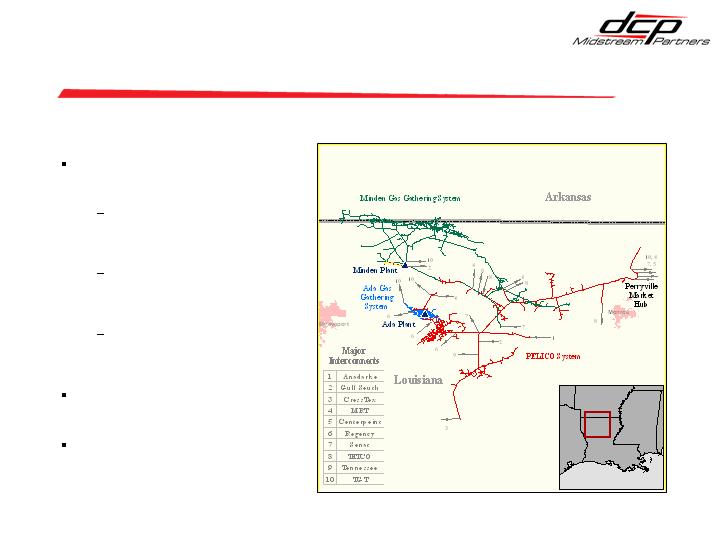

Overview of Natural Gas Services Segment

Minden, Ada and PELICO

systems

One of North Louisiana’s

largest gathering and

processing systems

Interconnects with 7 inter- and

2 intrastate pipelines / critical

west-to-east conduit

160 MMcf/d of processing

capacity and 1,430 miles of

pipeline

Bundled “wellhead-to-market”

services

Multiple market outlets provide

premium netback economics,

market optionality and liquidity

Integrated Business with Strong Market Position

21

Seabreeze is a 68-mile

intrastate pipeline system

located in Southeast TX

Sole NGL outlet for 2 large

third party gas plants and sole

market outlet for South DEAN

Pipeline

Black Lake (45% non-operating

interest) is a 317-mile interstate

pipeline system located in LA

and TX

Sole NGL pipeline serving 5

gas plants in LA and TX

Overview of NGL Logistics Segment

3rd Party Gas Plant

DEFS Gas Plant

DCP Midstream Minden Gas Plant

Access to Key Markets / Fee-Based Cash Flows

22

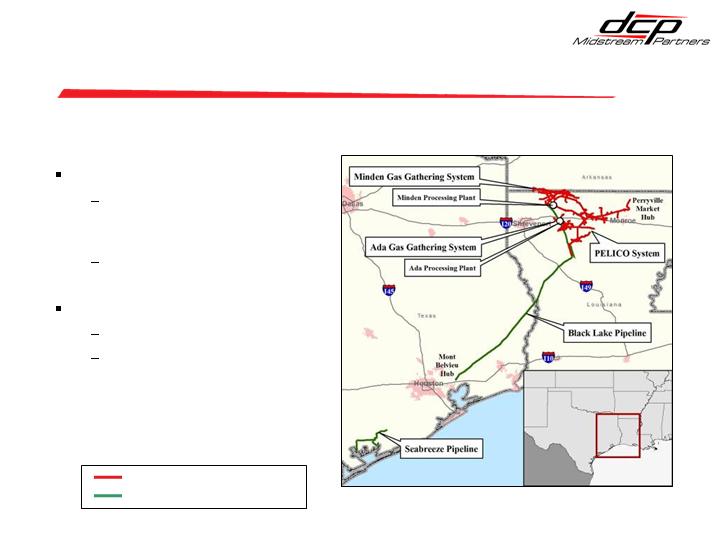

New Wilbreeze Pipeline

37-mile pipeline to

connect to DEFS’

plant

$12 million capital

10-year product

dedication from

DEFS

DEFS’ avg. volume of

5,300 bpd

Est. completion date:

4Q 2006

23

DCP Midstream Board of Directors

Former group VP, gathering & processing of DEFS, former director of TEPPCO’s GP

Michael J. Bradley, President

and CEO

Former Group VP and chief development officer of Duke Energy, former CEO of DEFS,

former chairman and director of TEPPCO’s GP

Jim W. Mogg, Chairman

Former president and CEO of GPM Gas Corporation

Michael J. Panatier

Former senior VP and CFO of Phillips Petroleum Company

Thomas C. Morris

Former chairman and CEO of Kerr McGee, former director of ConocoPhillips

Frank A. McPherson

Executive VP of planning, strategy and corporate affairs for ConocoPhillips, director of DEFS

John E. Lowe

Former senior VP and treasurer of Duke Energy, former senior VP and CFO of PanEnergy,

former director and chair of audit committee of TEPPCO’s GP

Paul Ferguson, Jr.

Chairman, president and CEO of DEFS

William H. Easter III

Director at CenterPoint Energy, Inc., former director of TEPPCO’s GP, former EVP of Texas

Eastern Corp., former chairman and CEO of Texas Eastern Gas Pipeline Company

Derrill Cody

Chairman of CenterPoint Energy, Inc., founder and chairman of Instrument Products, Inc.,

chairman of Healthcare Service Corporation, director of Eagle Global Logistics, Inc., former

director of PanEnergy and TEPPCO’s GP

Milton Carroll

24