![]()

| Cu | Au | Ag | U | Mo |

Quaterra Resources Inc.

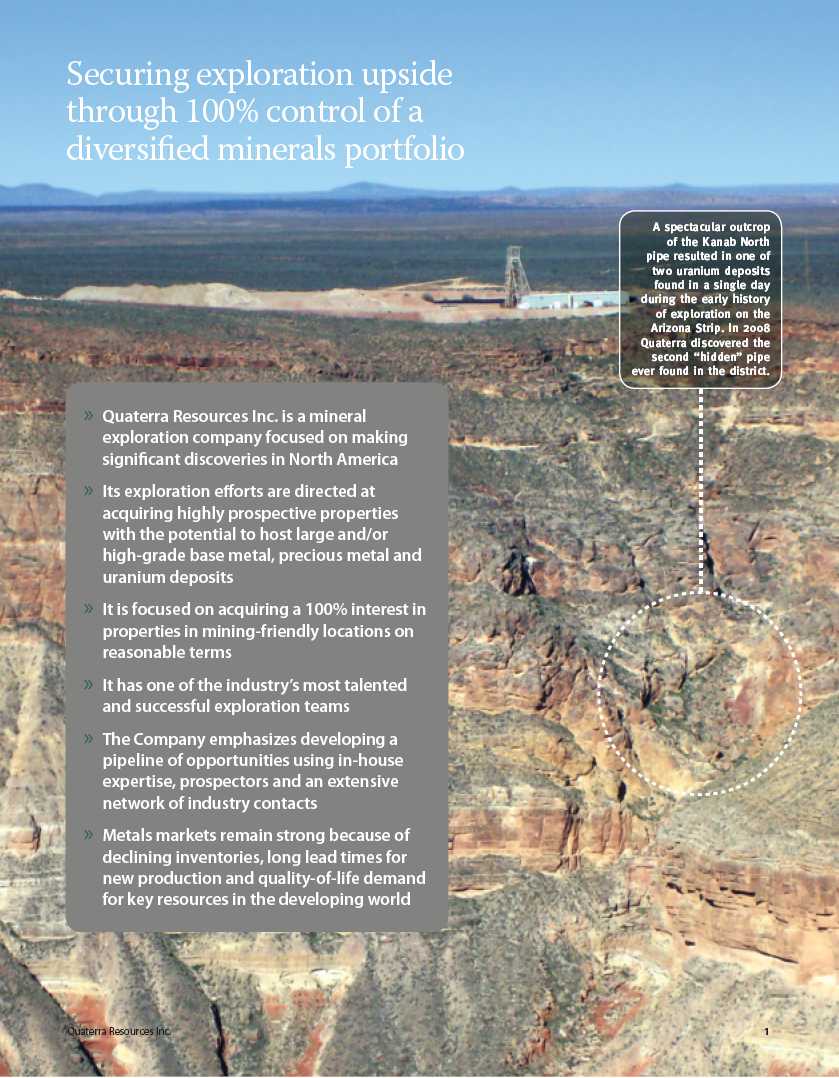

(AMEX: QMM, TSX-V: QTA) is a junior exploration company focused on making significant mineral discoveries in North America. The Company uses in-house expertise and its extensive network of consultants, prospectors and industry contacts to identify, acquire and evaluate prospects in mining-friendly jurisdictions with the potential to host large base metal, precious metal or uranium deposits. The Company’s preference is to acquire a 100% interest in properties on reasonable terms and maintain this interest through initial evaluation.

Forward-looking statements

Statements contained in this annual report that are not historical fact, such as statements regarding the economic prospects of the Company’s projects, the Company’s future plans or future revenues, timing of development or potential expansion or improvements, are forward-looking statements as that term is defined in the Private Securities Litigation Reform Act of 1995. Such forward-looking statements are subject to risks and uncertainties which could cause actual results to differ materially from estimated results. Such risks and uncertainties include, but are not limited to, the Company’s ability to raise sufficient capital to fund development, changes in general economic conditions or financial markets, changes in prices for the Company’s mineral products or increases in input costs, litigation, legislative, environmental and other judicial, regulatory, political and competitive developments in countries where the Company operates, technological and operational difficulties or inability to obtain permits encountered in connection with exploration and development activities, labor relations matters, and changing foreign exchange rates, which are described more fully in the Company’s filings with the Securities and Exchange Commission. The Company does not undertake to update any forward-looking statement that may be made from time to time except in accordance with applicable securities laws.

References may be made in this annual report to historic mineral resource estimates. None of these are NI43-101 compliant and a qualified person has not done sufficient work to classify these historic estimates as a current mineral resource. They should not be relied upon and Quaterra does not treat them as current mineral resources.

Cover photo: Geotech Ltd flies a VTEM survey for Quaterra on the Arizona Strip uranium project.

Contents

Annual General Meeting of Shareholders

The annual general meeting of the shareholders of the Company will take place at 10:00 am on Wednesday, June 18, 2008, in the Company’s offices located at Suite 1100, 1199 West Hastings Street, Vancouver, British Columbia.

| President’s Letter to Shareholders |

| “Propertyand commoditydiversification, and 100%ownership will capture the fullvalue of a majordiscovery.” |

WHEN

PREPAREDNESS

MEETS

OPPORTUNITY

Today’s seemingly incongruous juxtaposition of buoyant commodity prices and a fragile junior resource sector presents opportunities and challenges. Although strong metal prices and a relatively empty development pipeline assure that new discoveries will be major wealth creators, the more selective availability of equity funding for junior companies puts a premium on performance and growth.

In this environment we need to be prepared to work hard to seize opportunity when it presents itself. And with our ongoing strategy of building a portfolio of diversified mineral properties which we control in mining-friendly locations we believe we are ideally positioning ourselves to capture value for our shareholders.

2 Quaterra Resources Inc.

“I’m a great believer in luck, and I find the

harder I work, the more I have of it.”

Thomas Jefferson

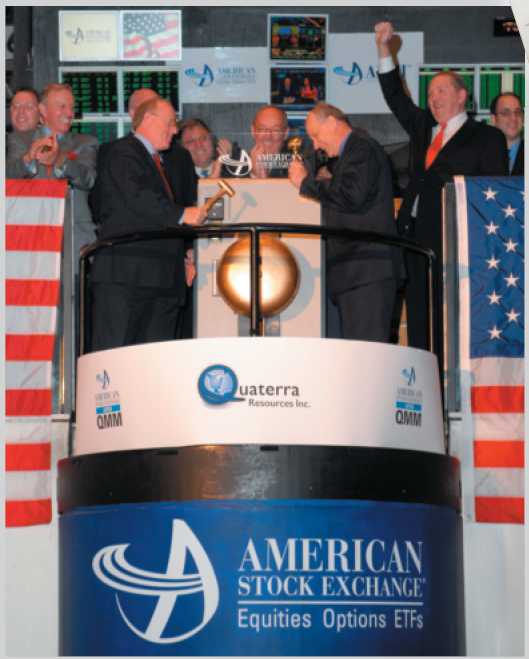

On the corporate side, we achieved a major milestone in the past year with our listing on the American Stock Exchange in March 2008. The AMEX listing will provide a more convenient trading market for U.S. shareholders, facilitate trading liquidity and raise the Company’s profile with U.S.-based institutional investors. Also during the year, Tracy Stevenson was appointed Chairman of the Company’s Board of Directors, adding depth at the executive level. In April 2008, we completed a non-brokered US$11 million financing which will allow us to continue aggressive exploration of our properties, in particular the MacArthur copper and Arizona Strip uranium projects.

On the exploration front, we validated our technical approach at the Arizona Strip with the discovery of a blind uranium pipe; expanded the zone of acid-soluble copper mineralization at MacArthur, Nevada; further delineated both high-grade and potential bulk-mineable silver mineralization at the Nieves property in Zacatecas, Mexico; and acquired the SW Tintic porphyry copper prospect in Utah and the Herbert Glacier gold prospect in Alaska. The due diligence process at Yerington, Nevada has been slow, which we expected, but I remain optimistic that we will achieve a favorable outcome.

Our focus remains squarely on discovering large or high-grade precious metal, base metal and uranium deposits in North America. I want to emphasize that we will continue to evaluate and in some cases acquire new prospects if they meet our geologic, environmental and infrastructure criteria; and if we can obtain a 100% interest on reasonable terms. We will do this not because of dissatisfaction with existing properties, but because the merging of good people with good properties and cutting edge technology gives us the best chance to make discoveries. Our recent exploration success on the Arizona Strip is a good example of this approach.

The successful execution of our strategy provides Quaterra with property and commodity diversifica-tion, and 100% ownership will capture the full value of a major discovery for our company and shareholders. A portfolio of properties at various stages of exploration and development also provides significant option value in the current environment of mergers, spin-offss and corporate acquisitions.

This is a great time to be looking for new mines and I am excited about the year ahead. We will be completing a resource estimate at MacArthur and initiating one at Nieves; aggressively drilling on the Arizona Strip to try to capitalize on our initial success; initiating work at SW Tintic and Herbert Glacier; and expanding our reconnaissance program in central Mexico. And we will continue to evaluate other opportunities, both on the project and corporate level.

The real strength of any company is its people. I would like to thank all the members of the Quaterra team – directors, officers, staffs, consultants and shareholders – for their hard work and loyalty during the past year. Exploration is a difficult and demanding business with frequent highs and lows. The commitment, enthusiasm and competence of our team is always appreciated and never taken for granted.

It is likewise not easy being a shareholder, particularly in today’s volatile environment. Our shareholders are second to none, a fact brought home once again by the large turn-out in October for our MacArthur field trip and in New York on March 28, when our contingent was one of the largest groups ever to attend an AMEX bell ringing ceremony. We appreciate your support of the Company’s activities and will work hard to justify your continued confidence.

As the year unfolds, we have some great opportunities and are well-positioned to capitalize on them. I look forward to sharing results with you as they become available.

T. C. Patton

May 6, 2008

President and CEO

2007 ANNUAL REPORT 3

| Cu | Au | Ag | U | Mo |

Quaterra commences trading on the AMEX

Quaterraachieved a key milestone when it listed on the American Stock Exchange on March 3, 2008. The Company’s shares trade under the symbol QMM. The listing will raise the Company’s profile in the United States, offer a broader market database to target new investors, better facilitate trading with existing U.S.-based shareholders and assist in increasing institutional investment.

A total of 25 shareholders from across the continent accompanied the Company’s officers, directors and employees at the bell ringing ceremony on the exchange floor in New York on March 28, 2008. President and CEO, Thomas Patton made a short address to the trading floor and then rang the opening bell with Chairman of the Board, Tracy Stevenson. The strong contingent of company attendees set a record for the highest number of guests ever to attend a bell ringing ceremony at the exchange and is a testament to the Company’s loyal shareholder base.

4 Quaterra Resources Inc.Left to right: Robert Wotczak (AMEX), Wayne Booth (shareholder), Tracy Stevenson (Chairman), Gerald Prosalendis (advisor), Larry Page (director), Thomas Patton (CEO & President), Rick Riley (shareholder), Wade Black (joint venture partner) at the bell ringing platform.

| Cu | Au | Ag | U | Mo |

2008 Milestones

2008 Milestones

Quaterra believes that significant goals, or milestones, provide the market with a tool with which to track its progress towards its longer-term objectives. Milestones are formulated to show the progress the Company is making in systematically acquiring and exploring its properties, reducing overall risk and strengthening the Company.

In the next 12 months Quaterra plans to:

Complete a NI43-101 resource estimate at the MacArthur copper project, Nevada

Test the most prospective breccia-pipe targets on the Arizona Strip for uranium

Complete a core drilling program on the Concordia-Arroyo-San Gregorio vein systems and their junctions at Nieves, Mexico

Advance its other central Mexican gold-silver properties and continue aggressive reconnaissance

Complete initial evaluation of the SW Tintic copper project in Utah and the Herbert Glacier gold property in Alaska

Continue to evaluate other high value opportunities

Achievements

In the past 12 months, Quaterra:

Obtained a listing on the American Stock Exchange under the symbol QMM

Discovered the A-1 “blind” breccia pipe on the Arizona Strip uranium property validating the company’s technical approach

Enlarged the zone of acid-soluble copper mineralization at the MacArthur project in Nevada

Delineated both high-grade and potential bulk-mineable silver mineralization at the Nieves property in Zacatecas, Mexico

Completed an environmental assessment at the Yerington project in Nevada as part of due diligence towards acquiring ownership

Acquired the SW Tintic porphyry copper prospect in Utah and the Herbert Glacier gold prospect in Alaska

Drilled two Mexican properties and through reconnaissance staked five additional claim blocks in central Mexico

A portfolio of diversified North American properties

Yerington-MacArthur

Consolidating a copper district

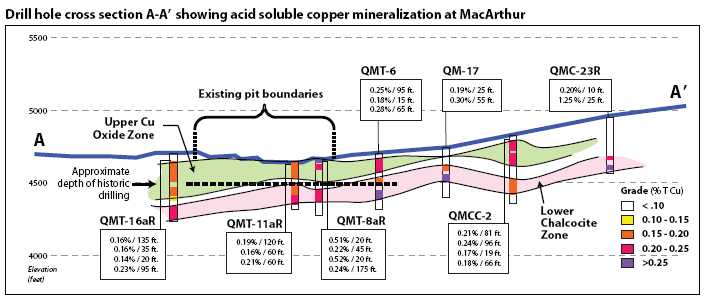

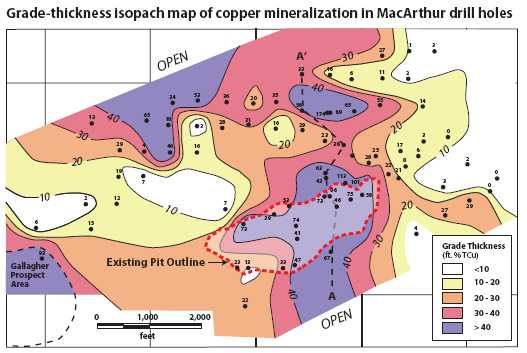

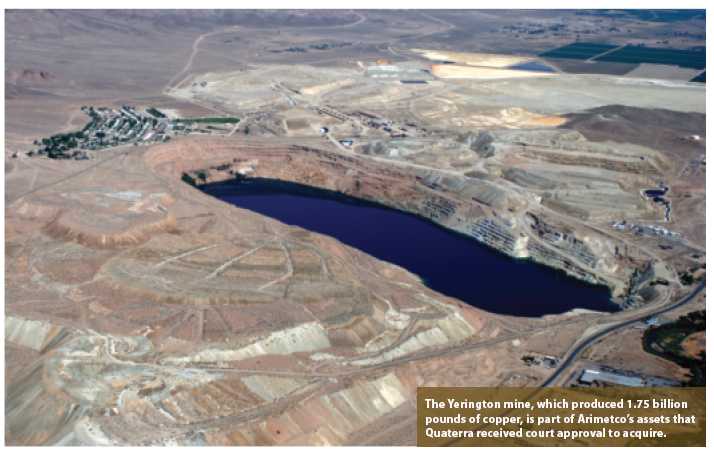

Quaterra’s 2007 drilling program substantially enlarged the acid-soluble copper deposit at MacArthur. And continued exploration may define a resource that is comparable in size and more favorable in economics than many of its neighbors in the Yerington district. Meanwhile, due diligence continues in order to complete the acquisition of the nearby Yerington mine.

Quaterra continues to expand its land position in the Yerington Copper district of northwestern Nevada. With world class potential only 50 miles southeast of Reno, the district has the ideal combination of resources and infrastructure to make Quaterra a major copper producer. The global geologic resources of the Yering-ton district exceed 2.1 billion tons of 0.4% copper and include the MacArthur copper oxide deposit, the Yerington, Ann Mason and Bear-Lagomarsino porphyry copper deposits and the Pumpkin Hollow copper skarn deposit. The resource potential of the district dwarfs past production and presents an attractive target for the Company’s growing land acquisition and copper exploration programs.

The historic MacArthur mine resource of 29 million tons grading 0.28% copper, including 13 million tons of +0.40% copper was substantially enlarged by the Company’s 2007 drilling program.

| Cu | Au | Ag | U | Mo |

Quaterra entered the Yerington district in 2005, with the acquisition of a 100% interest in the MacArthur mine, a fully stripped copper oxide deposit with an historic resource of 29 million tons grading 0.28% copper, including 13 million tons of +0.40% copper (this historic resource estimate, or those that follow, are not NI43-101 compliant and should be read in conjunction with the note on historic resources in the forward-looking statements in the cover of this annual report). The Company subsequently enlarged its land position by staking an area of 9.5 square miles around the existing open pit and initiated a drilling program to expand the deposit. The drilling results began to define a much larger area of copper oxide mineralization in 2006 and provided encouragement to pursue opportunities for further consolidation. In May 2007, Quaterra received approval from the U.S. bankruptcy court to acquire all the assets of Arimetco Inc. in the Yerington mining district, including the historic Yerington open-pit mine and the Bear prospect. The Company is currently conducting due diligence, that if successful, will result in 100% ownership. The momentum of these acquisitions increased the Company’s capacity for growth and motivated the completion of a 2,600 line-mile airborne magnetic survey that resulted in acquisition of the Wassuk copper project in early 2008.

Quaterra’s rapidly growing presence in the Yerington district is giving the Company a strategic position to create value from opportunity. With a drilling program to expand its copper oxide deposit at MacArthur, an option to acquire the Arimetco assets around the Yerington mine and a large land position to explore for new copper porphyry deposits, Quaterra is fast becoming an important player in the revival of a major copper district that has been dormant for almost 30 years.

MacArthur Copper Mine

Quaterra has completed approximately 43,000 feet of drilling in 74 reverse circulation holes and 43 core holes at MacArthur since drilling began in 2006. The program initially targeted the area in and around the pit and an area north of the pit where a

few historic holes intersected chalcocite mineralization. The drilling data defines two mineralized zones with a combined average thickness of over 100 feet that merge and now cover an area of 7,000 feet by 4,000 feet. This zone of secondary, acid-soluble copper mineralization is now approximately five times the size of the original pit area that contains a 29 million ton historic resource and remains open to the north, south and west. Copper mineralization parallels current topography and contains predominately green and black copper oxides grading downward into chalcocite, a secondary copper mineral that is also acid-soluble. Mineralization appears to represent a partially oxidized secondary enrichment blanket.

The most likely source of the secondary copper mineralization, based on results to date, is about 3,000 feet west of the pit in the Gallagher area. The Company’s recently completed drill hole QM-10 targeted this area and discovered new porphyry copper-type mineralization below a large area of iron oxides and phyllic alteration. From 470 to 530 feet, the hole cut 60 feet of 0.73% copper including 15 feet of 2.46% copper. A second mineralized zone at 575 feet assayed 0.40% copper over 50 feet, including 20 feet of 0.79% copper. The mineralization in both intercepts occurs as disseminations and veins of chalcopyrite in quartz mon-zonite. The copper zone includes scattered anomalous gold values up to 370 ppb. The intercepts may represent “fringe” mineralization related to a large porphyry copper system that could be the source of the secondary copper mineralization in the MacArthur pit.

The Company’s 2007 drilling program has substantially enlarged the MacArthur deposit. Continued exploration has the potential to define a resource comparable in size to other deposits in the Yerington district. During 2008, Quaterra will complete detailed geologic mapping and completely define the zone of shallow acid-soluble copper by grid drilling holes on 500 foot centers. The drill data will be used to complete a NI43-101-compliant resource estimate during the second half of 2008. Concurrent with the shallow drilling, deep drill-holes will explore for primary sulfide copper mineralization in the Gallagher area and north of the pit.

2007 ANNUAL REPORT 11

| Cu | Au | Ag | U | Mo |

Yerington Copper Mine, Nevada

The Company’s review of the Arimetco assets in the Yer-ington Mining District has progressed slowly but steadily. The Chambers Group Inc. and Golder Associates Inc. completed a Phase 1 Environmental Site Assessment Report (ESA) in April 2008 as part of the Company’s due diligence.

The purpose of this Phase 1 ESA is to identify conditions indicative of releases or threatened releases of hazardous substances so that the Company may establish liability protection as a bona fide prospective purchaser. This report is essential to obtain requested environmental clearances for past mining-related activities.

The original 180-day review period which began on July 13, 2007, has been extended for an additional 120- day period to May 8, 2008, and may be extended for additional 120-day periods if necessary.

On May 1, 2007, Quaterra received the approval of the appropriate U.S. court for the acquisition by a subsidiary of Quaterra of all Arimetco assets in the Yerington Mining District. Assuming successful completion of due diligence, the Company plans to explore the property as part of its ongoing exploration drilling program at MacArthur.

| Wassuk Project, Nevada |

Quaterra enlarged its stake in the Yerington District in early 2008 following the completion of a 2,600 line-mile airborne magnetic survey conducted by EDCON-PRJ of Tucson, Arizona. Th e geophysical survey covered approximately 140 square miles over most of the historic mines and included detailed surveys of the MacArthur and Bear deposits. The new data was then digitized and merged with older surveys to provide a detailed magnetic map of almost the entire district. |

12 Quaterra Resources Inc.

Other Copper Projects

SW Tintic-Treasure Hill Prospect, Utah

SW Tintic-Treasure Hill Prospect, Utah

In July 2007, Quaterra acquired the Southwest Tintic porphyry copper deposit located in the prolific Tintic mining district in west-central Utah, about 60 miles south of Salt Lake City. The acquisition provides an opportunity to investigate the porphyry copper mineralization in an under-explored area that represents the second most important mining district in Utah.

The project includes approximately five square miles of mineral rights that were acquired by optioning and staking 85 unpatented U.S. lode claims and purchasing 1,511 acres of patented mining claims. The district ranks third in a list of the top ten historic silver producing districts in the U.S. Approximately 285 million ounces of silver, 2.8 million ounces of gold and lesser amounts of base metals were mined from carbonate replacement deposits and mantos hosted by Paleozoic sedimentary rocks. Much of the mineralization may be related to a major porphyry copper system at depth that has not yet been found.

In the early 1970s, Bear Creek Mining Company discovered the deep Southwest Tintic porphyry copper system four miles to the south of the Tintic silver mines. The deposit is hidden 1,100 feet below surface under three square miles of barren quartz-sericite-pyrite alteration. The system was cut by six widely spaced core holes which form the basis for Krahulec and Briggs’ (2006) rough estimate of a global geologic resource – which is not NI43-101 compliant – of more than 400 million tons of 0.33% copper, 0.01% molybdenum and 0.002 oz/ton gold at a 0.3% copper cutoffs. The system could contain several large zones of high grade, structurally controlled copper mineralization that may not have been identified in the earlier drilling.

Wide-spaced drill holes in Diamond Gulch, less than a mile to the north, have shown the presence of a low grade chalcocite blanket presumably derived from enargite-rich veins peripheral to the SW Tintic or another deep porphyry copper center in the Treasure Hill area located two miles farther north. Exxon explored Treasure Hill for high-grade bonanza copper, gold, and silver veins in the early 1980s. The area represents yet another possible porphyry system at depth with three northeast trending zones of copper-gold mineralization in propylitized andesitic volcanics. The primary vein minerals are quartz-alunite, pyrite and enargite with lesser amounts of galena and sphalerite.

The large amount of metal and widespread alteration in the southwest Tintic-Treasure Hill prospect areas are compelling reasons to systematically explore a number of attractive exploration targets. Quaterra is planning an extensive program of mapping, data compilation, geophysics and approximately 5,000 feet of drilling in 2008.

The survey defi ned an interesting magnetic anomaly five miles east of Yerington that became the subject of Quaterra’s newly acquired Wassuk Prospect. Th e property consists of 77 leased claims and 205 newly staked claims over a broad valley covered by alluvium. Along the western margin of the Wassuk anomaly, an outcropping granodiorite with quartz mon- zonite porphyry dikes displays both alteration and copper oxide mineral- ization with a close similarity to the MacArthur deposit. Th e alteration and mineralization is characteristic of what might be expected peripheral to a porphyry system that may lie at depth below the valley to the east. The Wassuk anomaly presents an at- tractive target for copper exploration in 2008. |

| Cu | Au | Ag | U | Mo |

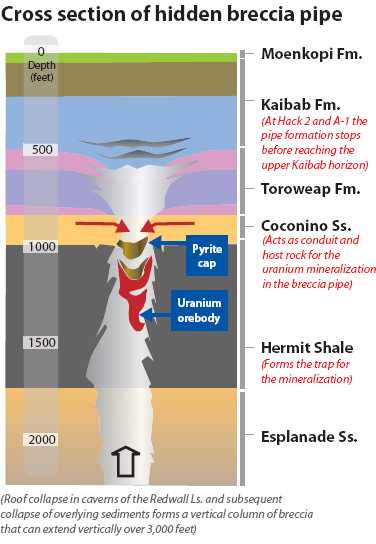

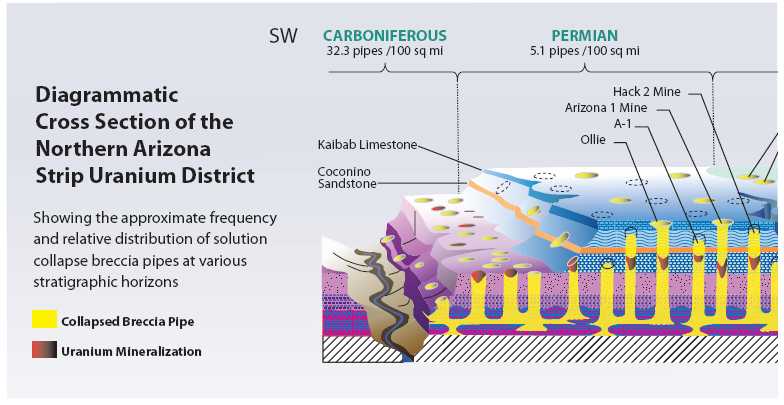

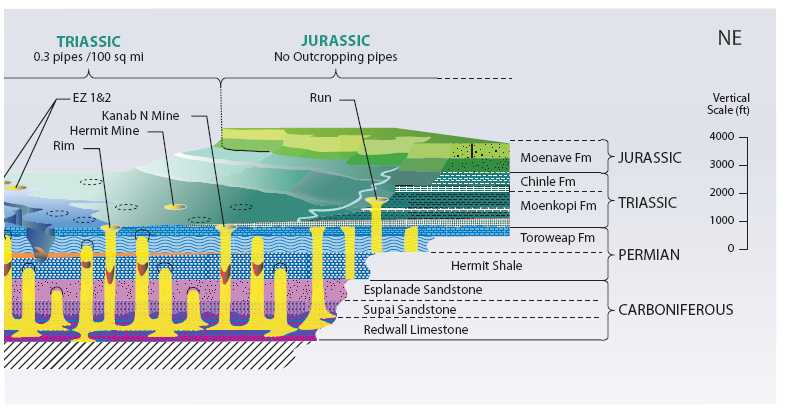

Arizona Strip Uranium District

Proof of principle

Proof of principle

The discovery of a “blind” pipe using a VTEM geophysical system validated Quaterra’s innovative approach to exploring for uranium on the Arizona Strip. And the success of Quaterra’s geophysical approach has opened up new possibilities for discovering a mineable resource.

The Arizona Strip should certainly be at the top of a list of U.S. uranium districts with the greatest possibility of creating signifi-cant wealth through new discoveries. The breccia pipe mines of northwestern Arizona represent some of the highest grade and most profitable per pound uranium production in the country. Prior to the uranium price decline in the late 1980s and early 1990s, they were some of the country’s last hard rock uranium producers. These attributes made the Arizona Strip a prime location for exploration to achieve the Company’s goal to create value through discovery. In Q1 2008, Quaterra made a discovery that could not only make Quaterra the major player in the Arizona Strip, but also redefine the future potential of this prolific district.

From 1980 to 1990, the Arizona Strip produced in excess of 19 million pounds of uranium from seven mines, averaging 0.65% U3O8. The total amount of mineable uranium discovered to date in breccia pipes in northern Arizona is estimated to be in the range of 35 million pounds. One fifth of this total (seven million pounds of U3O8) was mined from a single blind or “hidden” breccia pipe discovered by tracing alteration exposed in Hack Canyon by Western Nuclear in 1979. Until Quaterra’s discovery of the A-1 pipe, Hack 2 represented the only hidden pipe ever found in the district.

14 Quaterra Resources Inc.

| Cu | Au | Ag | U | Mo |

The first VTEM target tested by Quaterra resulted in the discovery

of the first new mineralized breccia pipe found on the Arizona Strip in 18 years

Northern Arizona Strip

Uranium Project

The discovery of new deposits in a mature district requires a determined and innovative approach combined with the latest exploration technology. In early 2007, Quaterra contracted Geotech Ltd. to conduct the fi rst extensive test of an airborne time-domain electromagnetic system on the Arizona Strip. The VTEM system identified most of the known breccia pipes and more than 200 moderate- to high-priority targets with similar geophysical signatures but with little or no outcropping evidence of a collapse feature. The acquisition of the mineral rights to cover the new anomalies increased the Company’s mineral rights to a total area of 85 square miles.

The fi rst VTEM target tested by Quaterra resulted in the discovery of the fi rst new mineralized breccia pipe found on the Arizona Strip in 18 years. Discovery Hole A-01-31 intercepted a thickness of 57 feet averaging 0.33% U3O8 at a depth of 1,034 feet. The intercept includes a higher grade interval of 28 feet averaging 0.58% U3O8. The drill-hole data indicate that the A-1 structure is a hidden breccia pipe. Upward collapse of the A-1 pipe stopped more than 400 feet below the surface. The A-1 discovery proved the concept of airborne geophysical detection of hidden pipes and gives Quaterra a unique advantage in the search for uranium deposits in the district.

The A-1 discovery represents the only hidden pipe discovered in 28 years. Most of the breccia pipes with structures visible at the surface have been found by past exploration. Many of the future discoveries in the district will probably be hidden breccia pipes and they could also be some of the most important. Hack 2, the largest and one of the highest grade uranium deposits ever discovered on the Arizona Strip, may have this status precisely because it is a hidden pipe. When

internal collapse causing the upward growth of breccia pipes continues after ore deposition, the uranium deposit can be destroyed as mineralization is displaced and disseminated downward through the structure.

Hidden pipes may also be the most numerous type of mineralized structure in the district. The U.S. Geological Survey Open File Report (OFR-89-550) shows the mapped locations of 1,296 pipes in northwestern Arizona. The number of outcropping pipes decreases dramatically below the cover of successive layers of younger sediments until fewer than two pipes are evident over a surface area of 500 square miles in the younger rocks. Clearly the upper level of stoping by collapse varies and many pipes may occur at depth and lie hidden with no surface evidence of a pipe throat. If these structures penetrate the Coconino Sandstone in a favorable area of the district, an orebody can exist at depth with no pipe structure at the surface. The number of pipes identifi ed to date could represent only a small fraction of the number of mineralized hidden pipes that lie waiting to be discovered at depth.

Quaterra is planning an active program of exploration drilling in 2008 to investigate the Company’s many high-priority VTEM targets. The program anticipates approximately 50,000 feet of drilling to test at least 12 new targets with both shallow and deep holes. The program is planned to follow-up with the defi nition of high-grade mineralization in the A-1 pipe and includes ground geophysical surveys to more precisely define drill targets within the airborne anomalies. With continued exploration, the Arizona Strip may soon become one of the more significant producing uranium districts in the United States.

Other uranium projects

Quaterra’s early entry into uranium exploration in the western U.S. allowed the acquisition of several key land positions over and immediately adjacent to the formerly producing Snow, Probe, and Sinbad uranium mines in southern Utah and the Shirley Basin mine in central Wyoming. Most of the properties were acquired from North Exploration, which staked claims simply on the basis of high drill-hole densities in close proximity to old mines. Some of the properties represent the drilled out and defined “reserves” for uranium operations that were shut down in the 1980s due to low prices. Although nearly all of the Company’s mineral rights are now surrounded by claims of competing companies, the Wyoming and Utah assets present a portfolio of opportunities that will continue to be evaluated.

Alaska exploration

Duke Island Cu-Ni-PGE Project

Quaterra’s 100%-owned Duke Island Cu-Ni-PGE prospect is located in southeast Alaska about 30 miles south of Ketchikan. The project consists of 129 unpatented Federal lode mining claims and 11 state of Alaska mining claims that cover an area of six square miles of multiple-use lands open to mineral development within the Tongass National Forest.

The Duke Island complex appears to have all the principal ingredients necessary to host a large Cu-Ni-PGE deposit. Consisting of two separate areas of well-exposed zoned ultramafics, the complex shows compositional layering due to changes in magma chemistry and subsequent fractionation and precipitation of mineral crystals settling through the lighter melt. Flow textures, graded bedding and dislodged xenolith fragments observable in outcrop and drill core indicate the presence of sill-like intrusions that form magma conduits for large volumes of mafic magmas. Net textured sulfides visible in the rock are thought to have accumulated by gravity separation from the ultramafi c magma. A detailed review of the Duke Island data in 2007 suggested that sulfide mineralization may be related to an elongate sill complex, not a typical Ural Alaska ultramafic intrusive. Similar layered intrusive complexes host some of the world’s largest copper-nickel systems.

Nine occurrences of Cu-Ni-PGE sulfide mineralization have been identified in outcrops within an area of four square miles at Duke Island. Drilling has encountered large zones of sulfide mineralization including up to 387 feet of 0.2% copper, but with low nickel tenors. Grab rock samples returned values of up to 1.95% copper, 0.25% nickel and 1 g/t combined platinum and palladium. The rock outcrops and subcrops characteristically occur in low boggy areas with heavy red-brown clay suggestive of acid weathering of sulfi des.

In early 2008, Quaterra contracted Fugro Airborne Surveys Inc. to fl y a deep-looking airborne time domain EM survey (TDEM) to identify new drilling targets within these areas and at depth below previously investigated targets. The geophysical survey covered 20 square miles with 240 miles of flight lines. A review of the TDEM data is currently in progress to determine if any of the identified anomalies have potential for massive copper-nickel mineralization.

Quaterra has discovered a dynamic ultramafi c intrusive complex at Duke Island. Extensive areas of outcropping sulfide mineralization have been identified and sampled. Shallow diamond drilling has intersected thick zones of low-grade copper mineralization. If the geophysical data suggest that higher sulfide concentrations may exist below the depth of previous exploration, the Company is planning a 10,000-foot drilling program during the summer field season of 2008.

18 Quaterra Resources Inc.

Herbert Glacier Gold Project

In October 2007, Quaterra acquired the Herbert Glacier gold property in the historic Juneau Gold Belt of southeast Alaska. Located 20 miles north of Juneau, the prospect presents an attractive opportunity for the discovery of a high-grade gold deposit in a district that has produced nearly seven million ounces of gold since discovery in 1880.

![]() The Herbert Glacier property consists of 91 unpatented Federal lode mining claims that host four main composite vein-fault structures with ribbon structure quartz-sulfide veins. Although the southernmost of the four vein systems was known in the early days of the Juneau district, the receding Herbert Glacier exposed a succession of parallel gold mineralized structures that strike east-west and dip steeply to the north. One of the four known vein systems was drilled in 1986 and 1988 by Tenneco Minerals and its successor Echo Bay Mining Co. The Main Herbert structure was explored on 200 foot intervals along a 2,000 foot strike length with 5,272 feet of drilling in 19 core holes. Shallow angle holes established continuity of gold mineralization in the vein system and over a distance of 1,500 feet found intercepts of up to 14 feet averaging 0.98 oz/ton gold. Sampling in 2007 shows that all four structures locally have high-grade gold-quartz mineralization and should be drill tested.

The Herbert Glacier property consists of 91 unpatented Federal lode mining claims that host four main composite vein-fault structures with ribbon structure quartz-sulfide veins. Although the southernmost of the four vein systems was known in the early days of the Juneau district, the receding Herbert Glacier exposed a succession of parallel gold mineralized structures that strike east-west and dip steeply to the north. One of the four known vein systems was drilled in 1986 and 1988 by Tenneco Minerals and its successor Echo Bay Mining Co. The Main Herbert structure was explored on 200 foot intervals along a 2,000 foot strike length with 5,272 feet of drilling in 19 core holes. Shallow angle holes established continuity of gold mineralization in the vein system and over a distance of 1,500 feet found intercepts of up to 14 feet averaging 0.98 oz/ton gold. Sampling in 2007 shows that all four structures locally have high-grade gold-quartz mineralization and should be drill tested.

The Herbert Glacier vein systems are strongly enriched in gold. Of 199 rock chip samples collected during a reconnaissance mapping and sampling program in the summer of 2007, almost half (94 samples) contained more than one g/t gold; 33 samples contained more than 10 g/t; and 12 contained more than one ounce of gold per ton. One 1.5 ft (about 46 cm) banded quartz vein with visible gold assayed 81.9 g/t (about 2.39 oz/ton) gold. Veins typically pinch and swell, but individual veins are as much as 14 feet thick and composite veins are up to more than 20 feet across. The veins are competent, but occur within halos of altered quartz diorite, and are generally marked on surface by deep trenches eroded from the incompetent altered host rocks. Gold is accompanied, in approximate decreasing order by arse-nopyrite, pyrite and galena with lesser amounts of scheelite, chalcopyrite and sphalerite. Trace elements are typical of the Juneau Gold Belt and the mesothermal aspect of the ribboned quartz veins suggest that the mineralized structures of the Herbert Glacier property could be persistent in strike and depth over a range of thousands of feet. A metallurgical study on a 240 pound composite sample by the U.S. Bureau of Mines indicated that 88% of the gold was free milling and could be recovered by gravity methods (Herbert Glacier – No. JU097, ARDF fi le, Juneau Quadrangle, U.S. Geological Survey).

Quaterra is planning a 4,500 foot core drilling program to explore the Herbert Glacier project in the late summer field season of 2008. The helicopter-assisted program is designed to test the Main Herbert and Deep Trench veins over a vertical extent of 300 to 400 feet. Past drilling and sampling programs have demonstrated a system of high-grade gold mineralization with near surface continuity in one structure on the property. If this year’s program can define similar grades and tonnages at depth and in the other parallel veins, the Her-bert Glacier project could become an important gold discovery for the Company.

Mexico

Staking rush

Quaterra stepped up the pace of exploration in Mexico this past year. Seven geologists are now working in the country under the supervision of Tom Turner, Quaterra’s Manager of Mexican Exploration.

Quaterra drilled a total of 16,602 meters on three projects in Mexico in 2007. A 16-hole core drilling program at Nieves brought new life into the project. While drilling at Crestones and Mirasol did not intersect signifi cant mineralization, it did provide valuable geologic information that will be useful in identifying new targets that the Company still considers prospective.

Competition for land in central Mexico has intensified as a result of major new discoveries at Peñasquito, La Pitarilla and Camino Rojo. Quaterra has staked five new prospects in San Luis Potosi covering 69,034 hectares (266.54 square miles) and has added claims at Mirasol and Las Americas in Durango. Reconnaissance work continues. Quaterra now has a 100% interest in claims covering 631.03 square miles in Durango and San Luis Potosi and a 50% interest in an additional 23.36 square miles at Nieves in Zacatecas. Details of these programs are discussed below.

| Cu | Au | Ag | U | Mo |

Nieves

Nieves

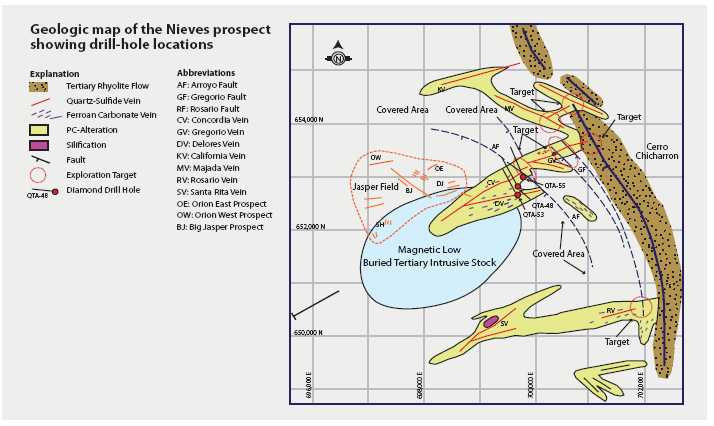

The Company owns a 50% interest in the Nieves silver property located in northern Zacatecas State, Mexico, about 90 kilometers north of Penoles’ world-class Fresnillo silver mine. The project occurs within a northwest trending mineral belt known as the Faja de Plata, which hosts many of the world’s premier silver deposits including San Martin, Fresnillo, Za-catecas and Real de Angeles. The land block consists of 16 mineral concessions covering an area of approximately 60 square kilometers (23.3 square miles). Mineralization is related to a low temperature silver-gold-lead-zinc epither-mal vein system similar to the world-class Fresnillo and Zacatecas Districts in central Zacatecas.

A 16-hole, 5,388.8 -meter drilling program, consisting primarily of infill holes on the Concordia vein, was completed between September and December 2007. The program was successful in extending the Concordia high-grade silver vein mineralization and intersected significant new mineralization in the adjacent Arroyo fault, which may be a new mineralized structure or host the faulted extension of the Concordia vein. Highlights are as follows, with key holes referenced on the geologic map:

Concordia vein:Twelve holes tested the Concordia vein system, one of three east-west striking veins systems on the Nieves property. The best mineralized interval is in hole QTA-48 with 47.48 meters averaging 142 g/t silver, 0.13 g/t gold, 0.37% lead and 0.37% zinc, including

22 Quaterra Resources Inc.

Mirasol-Americas

a 4.67 meter interval with 777 g/t silver (22.7 oz/ton), 0.53 g/t gold, 2.45% lead and 2.20% zinc. Hole QTA-53 cut the highest grade intercept with a 1.22 meter interval averaging 1.8 kg/t silver (52.6 oz/ton), 0.32 g/t gold, 2.06% lead and 0.69% zinc.

a 4.67 meter interval with 777 g/t silver (22.7 oz/ton), 0.53 g/t gold, 2.45% lead and 2.20% zinc. Hole QTA-53 cut the highest grade intercept with a 1.22 meter interval averaging 1.8 kg/t silver (52.6 oz/ton), 0.32 g/t gold, 2.06% lead and 0.69% zinc.

The Concordia vein hosts moderate- to high-grade silver-gold-lead-zinc mineralization at shallow depth proximal to its intercept with the Arroyo fault. The best mineralized segment of the vein currently extends for at least 400 meters along strike and over a vertical distance of 300 meters. It has a gentle rake to the southwest where it remains open.

Arroyo fault:Hole QTA-55 was collared 120 meters northeast of hole QTA-48 and tested the junction of the Concordia vein with the Arroyo fault. The mineralized intercept starts at 62 meters and includes 37.6 meters of 108 g/t silver, 0.15 g/t gold, 0.10% lead and 0.14% zinc. Within this zone is a 3.3 meter interval that averages 331 g/t silver (9.6 oz/ton), 0.29 g/t gold, 0.17% lead and 0.28% zinc. Mineralization consists of sheeted veinlets, and because of its shallow depth and relatively uniform grade has open pit potential. The Arroyo vein-fault system appears to strike northwest with a moderate southwest dip. Additional drilling will be necessary to determine the extent and significance of this mineralization.

2008 exploration plans:Additional core drilling will start during the second quarter of 2008, concentrating on the Concordia-Arroyo-San Gregorio vein systems and their junctions. Any new prospects identifi ed by mapping will also be tested. All work plans are made in consultation with the U.S.-based Blackberry Ventures 1, LLC, investment partnership, which will continue to contribute its share of ongoing exploration costs.

The Mirasol and Americas projects are located in the Municipality of Simon Bolivar, Durango, Mexico, about midway between the cities of Durango and Torreon in the central part of the Mexico Silver Belt or Faja de Plata. The property is adjacent to the east boundary of Hecla Mining’s San Sebastián Project. The project initially consisted of two separate land blocks until mapping suggested that the open area between Americas and Mirasol was also prospective. The intervening area was staked to form one large land block consisting of 13 concessions totaling 82,926 hectares (320.18 square miles), which are 100%-owned by Quaterra through its Mexico subsidiary Agua Tierra SA de CV.

Both Mirasol and Americas were past producers of mercury and antimony during the 1940s and 1950s as evidenced by hundreds of small mines and prospects spread across the property.

Most of the operators were small miners who hand sorted the ores and sold them to concentrate buyers in Monter-rey, Mexico. Most mining was terminated by the early 1970s. More recently, Hecla produced gold and silver from its adjacent San Sebastián property. The Francine and Don Sergio veins produced 11.2 million ounces of silver and 155,937 ounces of gold from 2001 to 2005. Hecla continues to actively explore its property and maintains a working mill at Valardeña, Durango.

A 1:5,000-scale geologic map of the original Mirasol and Cerro Concessions completed in 2007 identified a seven by five kilometer area of si-licified and brecciated limestone with quartz-calcite veinlets and accessory fluorite-alunite-stibnite-cinnabar. A 5,050-meter, 38-hole RC “scout” drill program was completed late in 2007 to test the large alteration area at depth and probe for potential feeder zones.

| Cu | Au | Ag | U | Mo |

24 Quaterra Resources Inc.

Americas appears to be the top of an epithermal system with a possible

gold-silver zone interpreted to be closest to surface below the north stockwork veining.

Holes drilled to an average depth of 150 meters demonstrated that the silicified and brecciated limestone is restricted to a 20 to 40 meter thick horizontal band that formed along the unconformable contact between the limestone and the overlying conglomerate. The conglomerate has since been largely eroded away, exposing the silicified limestone.

Drilling shows that in some areas the silicified limestone is cut by a complex series of faults, altered quartz porphyry dikes and silicified breccia dikes that served as hydrothermal feeders for the alteration system. These feeders are strongly anomalous in indicator elements arsenic, antimony and mercury but do not contain detectable amounts of gold or silver. Mirasol appears to be the top of an epithermal hydrothermal system. The gold-silver mineral zone, if present, could be up to 300 meters below the present erosion surface.

The Americas prospect is in the far west portion of the Mirasol concessions and is part of Hecla’s San Sebastian hydrothermal system. It is underlain by Cretaceous limestone and flysch unconformably overlain by Tertiary rhyododacite tuffs and post-mineral Late-Tertiary basalt flows.

The property encompasses an elongate, northeasterly-trending zone of hydrothermally altered rhyodacite and several large white silica “crestones” or veins that are up to 30 meters in width and outcrop up to a kilometer along strike.

There are numerous old mercury mines with ruins, dumps and open pits up to 40 meters wide, 75 meters long and 25 to 35 meters deep. The mercury occurs in both the oxidized altered rhyolite as native mercury and in the white silica as finely disseminated cinnabar.

An 800-meter diameter rhyodacite breccia that appears to be an eruptive vent outcrops in the center of the property. Hydrothermal breccia dikes are common peripheral to the large breccia. Mapping and sampling has identified a two by six kilometer area of stockwork veining along the north margin of the hydrothermal alteration shell that is open to the northeast. Grab samples of the vein material are anomalous in gold and silver, with values ranging from 0.025 to 0.91 g/t gold and 1.4 to 86 g/t silver.

Large parts of the Americas project are covered by alluvium and thin, post-mineral basalt flows. The size of the Ameri-cas hydrothermal system is presently not defined, but may be as large as 15 by four kilometers. As with Mirasol, Americas appears to be the top of an epithermal system with a possible gold-silver zone interpreted to be closest to surface below the north stockwork veining.

The work plan for Americas is to extend the geologic mapping survey east towards Mirasol and cover the identifi ed targets with a grid IP-magnetic geophysical survey. With positive results, the best targets will be tested with a core drill program.

2007 ANNUAL REPORT 25

| Cu | Au | Ag | U | Mo |

Crestones-Inde

Crestones-Inde

Crestones is composed of three concessions totaling 5,485.63 hectares (21.2 square miles) that abut the Inde concessions at their west end. Title is still pending on two Inde concessions that total 3,151.37 hectares (12.2 square miles).

Geologic mapping at a 1:5,000 scale identi-fied a large hydrothermal system consisting of an eight square kilometer area of silicified limestone cut by three elongate siliceous hydrothermal silica breccia bodies. Rock samples from the siliceous hydrothermal breccia contain elevated antimony-arsenic-mercury values and anomalous gold-silver values with occasional spikes up to ore grade. The presence of hot spring bedded siliceous sinter indicates that the outcropping alteration-mineralization is high level and formed close to surface.

The Company completed a 13-hole, 6,163.4 -meter core drilling program during 2007. Six holes totalling 3,043.4 meters were completed during the second quarter. An additional seven holes totalling 3,120 meters were completed during the third quarter. The first six drill-holes of the program did not intersect the targeted breccia feeder vents; the second phase of the program produced similar results with a few narrow low-grade intercepts of silver-gold-lead-zinc mineralization within the hydrothermal breccia.

Numerous drill holes passed through the silicified limestone and siliceous breccias and bottomed in fresh limestone providing evidence that the outcropping alteration, brecciation and porphyry stocks are displaced by a series of listric faults that have offsset the entire hydrothermal system to the northeast for an undetermined distance. The faults outcrop on the west side of the Crestones alteration system, strike northwest, and have a moderate to flat northeast dip with normal offsset. This fault system greatly complicates further exploration at Crestones as the presumed source area to the southwest is covered by post-mineral volcanics and alluvium.

With encouraging results, an IP survey may be carried out in the

alluvium-filled valley between Crestones and Inde to look for the downward

continuation of the Crestones mineral system.

26 Quaterra Resources Inc.

Possible additional exploration at Crestones will be dependent on results at Inde. As soon as title is received, the concessions will be mapped. With encouraging results, an IP survey may be carried out in the alluvium-filled valley between Crestones and Inde to look for the downward continuation of the Crestones mineral system.

Jaboncillo

Jaboncillo consists of a single 1,689 hectare (6.5 square miles) concession located on the north edge of a series of concessions controlled by Excellon Minerals about 12 kilometers north-northwest of its Platosa Mine at the northern terminus of the Sierra Bermajillo.

Geologic mapping at a scale of 1:5,000 was completed in the first quarter of 2008. The prospect is centered on an eruptive quartz porphyry that intrudes limestone. Two types of rhyolite have been identifi ed: an older quartz-eye rhyolite porphyry with up to 20% one to three millimeter clear partially terminated quartz-eyes; and a very fi ne-grained rhyolite which is locally flow banded. The quartz-eye rhyolite appears to be the initial explosive eruptive and the fine-grained rhyolite is the younger rhyolite that intrudes as dikes and flow-domes along the vent rim.

The Jaboncillo prospect has two exploration targets. The fi rst is a Peñasquito type gold-silver-lead-zinc sulfide deposit at depth in the eruptive breccia. The second target is an oxide gold deposit hosted in the silicified and brecciated late rhyolite dikes and small fl ow domes. Grab samples show localized anomalous arsenic and mercury. The geologic report with map and sections is not yet finalized.

An IP survey is planned later in the year to define possible drill targets.

| Reconnaissance Program |

Five 100%-owned new concessions – the Carolina, Caro- lina 2, Los Azafranes, Tian and Lupita – covering a total of 69,034 hectares (266.54 square miles) have been staked in San Luis Potosi. Th ese are all early-stage precious metal prospects that Quaterra hopes to advance through geologic mapping and sampling followed by geophysics if warranted. |

| Cu | Au | Ag | U | Mo |

Biographies

| BOARD OF DIRECTORS |

| Tracy Stevenson,B.S. Accountingmagna cum laude Chairman of the Board |

Mr. Stevenson is a senior mining industry executive with international experience in finance, mergers and acquisitions, strategic planning, corporate governance, auditing, administration and information systems and technology. He worked for Rio Tinto plc, the world’s second largest mining company, and related companies for 26 years. He held a number of senior leadership positions and was involved with many major exploration, development and financing projects. During the past five years, Mr. Stevenson was the global head of information systems and shared services for Rio Tinto. He previously served for four years as Executive Vice President, CFO and a director of Comalco Ltd., an Australia-based international aluminum company partially owned by Rio Tinto, and a further four years as CFO and a director of Kennecott Corporation, a $3.5 billion diversified North American mining company owned by Rio Tinto. He also has “Big 5” public accounting experience with Coopers & Lybrand (now PriceWaterhouseCoopers). Mr. Stevenson was appointed to the Quaterra Board of Directors by shareholder vote in July 2007. He is also a director of Vista Gold Company (VGZ; TSX, AMEX). He has a B.S. Accounting Magna Cum Laude from the University of Utah and is a member of the Advisory Board of the University of Utah David Eccles School Of Business.

Mr. Stevenson is a senior mining industry executive with international experience in finance, mergers and acquisitions, strategic planning, corporate governance, auditing, administration and information systems and technology. He worked for Rio Tinto plc, the world’s second largest mining company, and related companies for 26 years. He held a number of senior leadership positions and was involved with many major exploration, development and financing projects. During the past five years, Mr. Stevenson was the global head of information systems and shared services for Rio Tinto. He previously served for four years as Executive Vice President, CFO and a director of Comalco Ltd., an Australia-based international aluminum company partially owned by Rio Tinto, and a further four years as CFO and a director of Kennecott Corporation, a $3.5 billion diversified North American mining company owned by Rio Tinto. He also has “Big 5” public accounting experience with Coopers & Lybrand (now PriceWaterhouseCoopers). Mr. Stevenson was appointed to the Quaterra Board of Directors by shareholder vote in July 2007. He is also a director of Vista Gold Company (VGZ; TSX, AMEX). He has a B.S. Accounting Magna Cum Laude from the University of Utah and is a member of the Advisory Board of the University of Utah David Eccles School Of Business.

Thomas C. Patton, B.Sc., M.Sc., Ph.D.

President & CEO, Director

Dr. Patton graduated from the University of Washington in 1971 (Ph.D.) and has worked in the exploration industry for thirty-five years as a fi eld geologist, consultant and executive officer of both junior and senior mining companies. His work has been primarily in North America, where he and his teams have played major roles in several significant discoveries and reserve expansions of existing operations. Before joining Quaterra on a full-time basis, Tom was President and COO of Western Silver Corporation from 1998 to May 2006. The highlights of this period were the discovery and delineation of the world-class Peñasquito silver-gold-lead-zinc deposit in Zacatecas, Mexico, and the subsequent sale of the company to Glamis Gold Ltd.

Eugene Spiering,B.Sc.

VP Exploration, Director

Mr. Spiering has over 30 years of experience in the mining and exploration industries. He most recently held the position of Vice President, Exploration at Rio Narcea Mines Ltd., where he managed a team that discovered two gold deposits and completed the final definition of one nickel deposit in Spain. Prior to his tenure at Rio Narcea, Mr. Spiering held the position of senior geologist with Energy Fuels Nuclear, Inc. where his responsibilities included drilling supervision, geologic mapping, and ore reserve calculations related to uranium exploration in northern Arizona and gold exploration in the western U.S. and Venezuela. He received his Bachelor of Science-Geology degree from the University of Utah.

Robert J. Gayton, Ph.D., FCA

Director

Robert J. Gayton graduated from the University of British Columbia in 1962 with a Bachelor of Commerce and in 1964 earned the chartered accountant (CA) designation while at Peat Marwick Mitchell. Mr. Gayton joined the Faculty of Business Administration at the University of British Columbia in 1965, beginning 10 years in the academic world, including time at the University of California, Berkeley, earning a Ph.D. in Business. Mr. Gayton rejoined Peat Marwick Mitchell in 1974 and became a partner in 1976 where he provided audit and consulting services to private and public company clients for 11 years. Mr. Gayton has directed the accounting and financial matters of public companies in the resource and non-resource fi elds since 1987. He currently serves as a director for five public companies.

John R. Kerr,B.Sc.

Director

Mr. Kerr holds bachelor degrees in applied science and geological engineering from the University of British Columbia. Over the course of a career of more than 30 years he has been continuously engaged in mineral exploration and has extensive fi eld experience throughout North America. Mr. Kerr has been a geological consulting engineer since 1970 and has held senior positions with a number of public companies, both as an officer and director. He has been involved with the discovery of a number of significant mineral deposits, including two producing mines and two additional projects currently awaiting production decisions.

28 Quaterra Resources Inc.

Lawrence Page,QC

Director

Lawrence Page obtained his law degree from the University of Brit-ish Columbia in 1964 and was called to the Bar of British Columbia in 1965. Thereafter he studied labor law and industrial relations in Sydney, Australia, as a Commonwealth Scholar, returning to active practice in Vancouver in 1967. In 1970, he was a founding partner of Worrall and Page where he practiced until 1995. He currently practices on his own in Vancouver. Mr. Page’s preferred areas of practice are commercial litigation, native law, natural resource law and securities law. He has been admitted to the Bar of Ontario for the purpose of acting as counsel in specifi ed litigation. Mr. Page was awarded the distinction of Queen’s Counsel in 1988. Through his experience with natural resource companies and, in particular, precious metals development, Mr. Page has established a unique relationship with fi nanciers, geologists and consultants and has been counsel for and a director of Corona Corporation (now Homestake) and Prime Resources Corporation which have brought into production and operate Canadian gold mines He currently serves as a director for nine public companies.

Roy Wilkes,P.Eng

Director

Mr. Wilkes recently retired as president of Washington Group International’s Mining Business Unit. As leader of this group he participated in many developing mining projects throughout the world, including Latin America, Canada, Europe and the United States. Mr. Wilkes was also the Chief Operating Officer of Santa Fe Pacific Gold Corporation during the expansion of its Nevada operations. He was also involved in the development of such projects as Greens Creek, Alaska; Stillwater, Montana; and Las Pelameres in Chile, while serving as Senior Vice President of Business Development for Anaconda Minerals. Mr. Wil-kes is a graduate mining engineer from the Montana School of Mines.

| MANAGEMENT & CONSULTANTS |

Thomas C. Patton,B.Sc., M.Sc., Ph.D.

President & CEO, Director

Eugene Spiering,B.Sc.

VP Exploration, Director

Scott B. Hean,B.A., MBA, ICD.D

CFO

Mr. Hean has held senior management and executive positions with J.P. Morgan of New York, primarily financing junior oil and gas companies and Bank of Montreal as Senior Vice President and Managing Director responsible for fi nancing in the natural resources sectors in North America. Currently he serves as a director of Great Quest Metals Inc., and is past Chair of the Audit Committee, Sabina Silver Corporation, both publicly-traded companies on the Toronto Venture Exchange. He is Chair of the Bill Reid Trust and has served on numerous not-for-profit Boards, including Outward Bound and B.C. Children’s Hospital. He graduated from Simon Fraser University, Brit-ish Columbia, in 1973 and from the Ivey School of Business, London, Ontario, in 1975 with an MBA. Mr. Hean graduated in 2006 from the Institute of Corporate Directors, Directors Education Program.

Thomas R. Turner,B.Sc., M.Sc.

Manager of Mexican Exploration

Mr. Turner graduated from Michigan Technological University and has worked as an exploration geologist in various technical and managerial capacities for 34 years. His work experience extends from Alaska to Ecuador and includes management of exploration projects for numerous types of precious and base metal mineral systems, both for major mining companies and junior exploration companies. For the last eleven years, he has worked exclusively in Mexico and Central America. He was a consultant to Western Silver Corporation from 1998 to 2006 and managed its Mexican exploration programs including its Peñasquito project, which culminated in the discovery of two world-class gold-silver-lead-zinc deposits and the discovery of economic gold-silver mineralization at the nearby Noche Buena project, and the Company’s sale to Glamis Gold Ltd. in May, 2006. Prior to joining Western Silver, Mr. Turner managed Mar-West Resources Ltd.’s exploration projects in Guatemala which resulted in the discovery of the Cerro Blanco hot spring gold deposit. Cerro Blanco is currently the subject of a feasibility study by Glamis Gold Ltd., which acquired Mar-West in 1998.

Hector J. Fernández,G. B.Sc.

Consulting geologist

Mr. Fernández graduated from the University of San Luis Potosi, Mexico, in 1973 and has worked in exploration for 32 years as a field geologist, consultant and exploration manager for senior mining companies. Before joining Quaterra in 2003, he worked for Minera Cuicuilco (Cyprus) from 1974 to 1986, and was directly responsible for the Cieneguita (Chihuahua, Mexico) gold-silver mine discovery that was sold to Glamis Gold Ltd. From 1990 to 1996, he worked as Mexico’s Exploration Manager for Minera San Bernardo (ASARCO). From 1999 to 2002, he worked for Quebec Iron and Titanium (RTZ) in its Pluma Hidalgo (Oaxaca, Mexico) project. Mr. Fernández has been responsible for Quaterra’s Nieves silver project in Zacatecas, Mexico, since the last quarter of 2003, and he is currently preparing to begin drilling the Company’s Crestones project in Durango, Mexico.

Curtis J. Freeman,B.A., M.A.

President of Avalon Development Corporation, a consulting mineral exploration fi rm, Fairbanks, Alaska

Curt earned his Bachelor’s degree in Geology in 1978 from the College of Wooster, Ohio, and his Master’s Degrees in Economic Geology in 1980 from the University of Alaska. Curt has been employed in the minerals industry in Alaska, the Yukon, the western United States, Central America, South America, New Zealand and Africa for the past 25 years. Curt is a U.S. Certified Professional Geologist (CPG #6901) and is a licensed geologist in the State of Alaska (Lic. # AA 159). He is a member and past director of the Alaska Miners Association, Society of Economic Geologists, Geological Society of Nevada, British Columbia and Yukon Chamber of Mines and Prospectors and Developers Association of Canada. Curt also serves on the University of Alaska Department of Geology Advisory Board and the State Division of Geological and Geophysical Survey Geologic Mapping Board. Curt has worked for and consulted for numerous major and junior mining companies in addition to consulting for individuals. Curt and his team of professionals have been involved in a number of gold, silver, platinum group and base metal discoveries in Alaska and other parts of the world.

2007 ANNUAL REPORT 29

| Cu | Au | Ag | U | Mo |

Biographies

Roman Friedrich III

Financial advisor

Mr. Friedrich has been an investment banker to the mining and metals industries for over twenty years. Immediately prior to establishing Roman Friedrich & Company, he was the Managing Director at TD Securities responsible for its global mining M&A business. Early in his career he spent ten years at the Chase Manhattan Bank where among other positions he was Vice President for Latin America, President of Chase Manhattan Canada Limited, and Managing Director responsible for North American investment banking. From 1979 to April 1991 he was a partner at Burns Fry, a Managing Director at First Chicago and a partner at Wood Gundy. In 1991 he was a founding partner of the New York office of Lancaster Financial Corporation (a fi rm specializing in mergers and acquisitions). TD Securities, a subsidiary of Toronto Dominion Bank, acquired Lancaster in 1994. Leaving TD in April 1997, he started Roman Friedrich & Company in July the same year. Over his career, he has provided numerous companies with advice on acquisitions, mergers and divestitures, as well as providing valuations and fairness opinions to companies in the mining, metals and other industries. His investment banking activities have included the raising of equity and debt capital to the arranging of project finance. He holds a B.A. from Rutgers University and attended business school at New York University. Mr. Friedrich is on the Board of Directors of StrataGold Corporation, Gateway Gold Corp., GFM Resources Ltd., and is Chairman of Dreman Claymore Dividend and Income Fund. Mr. Friedrich is also President of GFM Resources Ltd. Mr. Friedrich is an independent director of a family of closed end mutual funds and ETFs managed by Claymore Investments Inc.

Charles C. Hawley,B.A., Ph.D.

VP Exploration, Alaska

A director and Chairman of Piper Capital, Inc., Dr. Hawley graduated from Hanover College, Indiana, with a B.A. in geology in 1951 and joined the U.S. Geological Survey in 1952 after graduate studies at the University of Wisconsin. He earned a Ph.D. in geology from the University of Colorado in 1963. Dr. Hawley worked for the Geological Survey until 1968. During his Survey years he specialized in uranium, precious metals, and beryllium primarily in the Rocky Mountain states. Since 1969, he has worked in the exploration industry as a field geologist, consultant and executive officer of junior mining companies, mainly in Alaska. Dr. Hawley has been instrumental in developing coal resources in the Wishbone, Beluga, and Nenana fields and precious metals and copper in the Alaska Range, Seward Peninsula and Brooks Range. In addition to his field studies, he served as Executive Director of the Alaska Miners Association from 1976 to 1979 and on the National Advisory Committee to the U.S. Bureau of Land Management from 1989 to 1992 where he chaired the Mining Law Task Force. He is a member of SME and Fellow of the Society of Economic Geologists. He is registered as a geologist in the State of Oregon and is a Certifi ed Professional Geologist in the AIPG.

Nicole Rizgalla,B.A.

Corporate Communications Manager

Ms. Rizgalla is communications specialist with over 12 years of global experience working in corporate communications, investor relations, public relations and marketing communications. She held corporate communications roles with Western Copper Corp. and Western Silver Corp.; was the media advisor to the Minister for Sustainability and Environment in Victoria, Australia; was marketing communications manager for London Remade within the Mayor of London’s office (UK); and public relations manager for The Body Shop’s Australasian headquarters. She has also consulted for leading communications firms including James Hoggan & Associates in Vancouver, Hill and Knowlton in London, UK and Porter Novelli in Sydney and Melbourne. She holds a Bachelor of Arts in Management Communication.

Abelardo Garza Hernández,B.Sc.

Consulting geologist, registered surveyor, landman and environmental consultant, México

Mr. Garza graduated from the University of Texas at Austin in 1975, and has worked in the mining and exploration industry for the last 30 years as a fi eld and mine geologist, consultant, landman, legal representive and administrator of Mexican subsidiaries of both junior and senior mining companies. His work has been in North America, where he has played major support roles in several suc-cesful exploration projects, including the world-class Peñasquito silver-gold-lead-zinc deposit in Zacatecas, Mexico, and the subsequent sale of the company to Glamis Gold Ltd. Prior to becoming a consultant, he worked for Exxon, Industrial Minera México, Grupo Frisco up until 1984, and since then he has been an independent consultant, having provided services to many diffserent companies such as Quaterra and Southern Silver, among others. Mr. Garza is a member of the Asociación de Ingenieros de Minas, Metalurgistas y Geólogos de México and the Society for Mining, Metallurgical and Exploration Inc. (SME), and a registered surveyor in México.

Patrick Hillard,B.Sc., M.Sc.

Consulting exploration geologist

Mr. Hillard graduated from the New Mexico School of Mines in 1969, and has worked in mining exploration for 37 years, with a significant portion of this time in supervisory positions. His work has been in North America, South America, Papua New Guinea and Spain. He has participated in the discovery of several uranium orebodies, and was in charge of exploration teams which discovered several breccia pipe orebodies which became profitable mines. He was Vice-President of Exploration for Arequipa Resources and played a signifi cant role in the discovery of the Pierina gold ore-body in Peru, after which Arequipa was bought out by Barrick Gold Corporation. Mr. Hillard was Chief Geologist for Western Nuclear, a Phelps-Dodge subsidiary, and Manager of Exploration for Energy Fuels. He is a member of the American Institute of Mining and Metallurgical Engineers.

30 Quaterra Resources Inc.

Joseph R. Inman, B.Sc., M.Sc.

Consulting geophysicist, explorer

Mr. Inman graduated from the University of Utah in 1973 (M.Sc.) and has more than 30 years experience in mineral exploration and environmental studies. He has extensive experience and expertise in nearly all geophysical methods including magnetics, gravity, induced polarization/resistivity (IPR), electromagnetics including both time-domain EM and frequency-domain EM (CSAMT, MaxMin), and radiometrics all in airborne, ground and downhole configurations. Recent experience and areas of interest include the application of seismic methods to mineral exploration as well as data inversion techniques of all geophysical data sets, including integrated earth modeling. Mr. Inman has been involved in all aspects of applying geophysics to exploration including survey design (technical speci-fications), data acquisition, contractor evaluation and selection, data processing and interpretation. He was a key member of the exploration teams that discovered the Crandon, Wisconsin, VMS deposit; and the A154 and Tli Kwi Cho kimberlite deposits, NWT, Canada. Most recently he provided and managed geophysics programs for the Western Silver team that explored and expanded the Peñasquito, Mexico, discovery into a world-class silver-gold-lead-zinc deposit. Prior to becoming a consulting geophysicist, he was Director of Technical Support and Services at Kennecott Exploration, responsible for ensuring Kennecott’s geologists, geophysicists and data managers had knowledge of, access to and made best use of state-of-the-art exploration methods including geophysics, geochemistry, remote sensing and data/information management technologies. Mr. Inman is a member of the Society of Exploration Geophysicists and a registered professional geophysicist in the state of California.

Gerald Prosalendis

Corporate advisor

Mr. Prosalendis is a corporate advisor who specializes in markets, corporate development, shareholder relations and the media. He was Vice President Corporate Development of Western Silver Corporation and was involved in the successful sale of the company in 2006 to Glamis Gold Ltd. for $1.6 billion. He was Vice President Corporate Development of Dia Met Minerals Ltd. and was a member of the team that developed the Ekati Diamond Mine. He was involved in initiating the marketing campaign for Ekati diamonds and the sale of Dia Met to BHP Billiton for $687 million in 2001. Mr. Prosalendis has been a consultant to Anderson & Schwab Inc., a mineral and business firm based in New York, a Senior Counselor for James Hoggan & Associates of Vancouver, an advisor to public and private companies and Business Editor of The Vancouver Sun. He also worked as a financial services analyst for a brokerage firm.

2007 ANNUAL REPORT 31

Corporate Directory

Board of Directors

| Shareholder Information | |||

| Listing:TSX-V: QTA, AMEX: QMM (listed as of Mar. 3, 2008) | |||

| Shares outstanding | 83,167,005 | ||

| Options outstanding | 5,559,500 | ||

| Warrants outstanding | 0 | ||

| Fully diluted | 88,726,505 | ||

| (As at Dec. 31, 2007) | |||

| Share trading information(fiscal 2007) | |||

| High | Low | ||

| Q1 | $2.75 close Mar. 31/07 | $2.96 | $2.29 |

| Q2 | $3.77 close June 30/07 | $4.18 | $2.60 |

| Q3 | $2.76 close Sept. 30/07 | $3.84 | $2.21 |

| Q4 | $3.15 close Dec. 31/07 | $3.99 | $2.66 |

Tracy Stevenson (Chairman)

Thomas C. Patton

Eugene Spiering

Robert J. Gayton

John R. Kerr

Lawrence Page, QC

Roy Wilkes

Officers

Thomas C. Patton

President and CEO

Eugene Spiering

VP Exploration

Scott B. Hean

CFO

Transfer Agent and Registrar

CIBC Mellon

Suite 1600, 1066 West Hastings Street

Vancouver, B.C., V6C 3X1

Canada

Auditors

Smythe Ratcliffe

7th Floor, Marine Building

355 Burrard Street

Vancouver, B.C., V6C 2G8

Canada

Corporate Office

Suite 1100, 1199 West Hastings Street

Vancouver, B.C., V6E 3T5

Canada

Tel: 604-681-9059

Fax: 604-688-4670

Toll Free: 1-888-456-1112

Website: www.quaterra.com

Cusip No.

747952 109

Quaterra Resources Inc.

1100 – 1199 West Hastings Street,

Vancouver, BC, V6E 3T5

Tel: 604-681-9059 Fax: 604-688-4670

www.quaterraresources.com

Management’s Discussion & Analysis

In respect to the Year ended December 31, 2007

Dated: March 26, 2008

| Quaterra Resources Inc. | 1 |

MANAGEMENT’S DISCUSSION & ANALYSIS

| A. | Introduction |

The following Management Discussion and Analysis (“MD&A”) of the operating results and financial condition of Quaterra Resources Inc. (the “Company”) compares results for the year ended December 31, 2007 (“2007”) to the year ended December 31, 2006 (“2006”). This MD&A should be read in conjunction with the audited financial statements for the years ended December 31, 2007, December 31, 2006 and Decem-ber 31, 2005. All notes referenced herein may be found in the consolidated financial statements dated December 31, 2007.

The financial statements were prepared in accordance with Canadian generally accepted accounting principles. This MD&A, dated as of March 26, 2008, was prepared to conform to National Instrument 51-102 F1 and was approved by the Board of Directors prior to release.

The Company is a reporting issuer in British Columbia and Alberta and its shares trade on the Tier 2 Board of the TSX Venture Exchange (“TSX.V”) under the symbol QTA and on American Stock Exchange (“AMEX”) under the symbol QMM.

The Company’s reporting currency is the Canadian dollar and all dollar amounts are in Canadian dollars, unless otherwise indicated.

Certain forward-looking statements are discussed in the MD&A with respect to the Company’s activities and future financial results. These are subject to significant risks and uncertainties that may cause projected results or events to differ materially from actual results or events.

Additional information relating to the Company, including detailed drill results previously disclosed in news releases, is available on SEDAR at www.sedar.com. Terms of property option agreements are described more fully in the notes to the consolidated financial statements.

| B. | Qualified Person |

Dr. Thomas C. Patton, P. Geo., the President and Chief Executive Officer of the Company, is the qualifi ed person responsible for the preparation of the technical information included in this MD&A. Dr. Patton graduated from the University of Washington in 1971 (Ph.D.) and has worked with both junior and senior mining companies. His exploration efforts have concentrated on North America and have resulted in several significant discoveries and led to the expansion of mineral reserves at existing operations. He served as the President and Chief Operating Officer for Western Silver Corporation from January 1998 to May, 2006. Previously, Dr. Patton held senior positions with Rio Tinto PLC and Kennecott Corporation. Dr. Patton is a member of the Society of Economic Geologists and the American Institute of Mining & Metallurgical Engineers.

Eugene Spiering joined the company on January 10, 2006 as Vice President of Exploration. Mr. Spiering has over 28 years of experience in the mining exploration industry. He most recently held the position of Vice President, Exploration at Rio Narcea Mines Ltd., where he managed a team that discovered two gold deposits and completed the final definition of one nickel deposit in Spain. All three of these deposits are currently in production. Prior to his tenure at Rio Narcea, Mr. Spiering held the position of senior geologist with Energy Fuels Nuclear, Inc. where his responsibilities included uranium exploration in northern Arizona and gold exploration in western US and Venezuela. He received his Bachelor of Science-Geology degree from the University of Utah. Mr. Spiering is a member of the Society of Economic Geologists, the Australasian Institute of Mining and Metallurgy and the American Association of Petroleum Geologists.

| C. Exchange information and conversion tables. |

For ease of reference, the following information is provided:

| U.S. Dollars to Canadian Dollars | ||

| December 31, | ||

| 2007 | 2006 | |

| Rate at end of period | 0.98200 | 1.16640 |

| Average rate for period | 1.07440 | 1.13461 |

| High for period | 1.18730 | 1.17960 |

| Low for period | 0.90570 | 1.09260 |

www.oanda.com

| Conversion Table | ||||

| Imperial | Metric | |||

| 1 Acre | = | 0.404686 | Hectares | |

| 1 Foot | = | 0.304800 | Metres | |

| 1 Mile | = | 1.609344 | Kilometres | |

| 1 Ton | = | 0.907185 | Tonnes | |

| 1 Ounce (troy)/ton | = | 34.285700 | Grams/Tonne |

Information from www.onlineconversion.com

| 2 | 2007 Annual Report |

MANAGEMENT’S DISCUSSION & ANALYSIS

| Precious metal units and conversion factors | ||||||||||

| ppb | - Part per billion | 1 | ppb | = | 0.0010 | ppm | = | 0.000030 | oz/t | |

| ppm | - Part per million | 100 | ppb | = | 0.1000 | ppm | = | 0.002920 | oz/t | |

| oz | - Ounce (troy) | 10,000 | ppb | = | 10.0000 | ppm | = | 0.291670 | oz/t | |

| oz/t | - Ounce per ton (avdp.) | 1 | ppm | = | 1.0000 | ug/g | = | 1.000000 | g/tonne | |

| g | - Gram | |||||||||

| g/tonne | - gram per metric ton | 1 | oz/t | = | 34.2857 | ppm | ||||

| mg | - milligram | 1 | Carat | = | 41.6660 | mg/g | ||||

| kg | - kilogram | 1 | ton (avdp.) | = | 907.1848 | kg | ||||

| ug | - microgram | 1 | oz (troy) | = | 31.1035 | g | ||||

Information from www.onlineconversion.com

| D. | Description of Business |

The Company acquires and explores mineral properties in the Americas. It is currently exploring for base and precious metals in Mexico and Alaska, uranium in Arizona, and copper in Nevada.

| E. | Description of Mineral Properties |

i) Nieves Property – Mexico

Quaterra’s 50% owned Nieves silver property is located about 90 kilometers north of Penoles’ world-class Fresnillo silver mine in Zacatecas, Mexico. The project occurs within a northwest trending mineral belt known as the Faja de Plata or Silver Belt, which hosts many of the world’s premier silver deposits. Quaterra’s land block consists of 15 concessions covering an area of more than 18 square miles and has good road access and excellent regional and local infrastructure.

The Nieves property hosts at least three steep-dipping vein systems that cross the property in an east-west direction. Both the Concordia-Delores-San Gregorio and the Santa Rita vein systems have excellent potential for both narrow zones of +500 g/t silver and a surrounding envelope of stockwork mineralization with +50 g/t silver that may represent a bulk tonnage target.