QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on October 5, 2005

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Rockwood Specialties Group, Inc.

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) | 2800 (Primary Standard Industrial Classification Code Number) | 52-2277390 (I.R.S. Employer Identification Number) |

100 Overlook Center

Princeton, New Jersey 08540

(609) 514-0300

(Address, Including Zip Code, and Telephone Number,

Including Area Code, of Registrant's Principal Executive Offices)

SEE TABLE OF ADDITIONAL REGISTRANT GUARANTORS

Thomas J. Riordan, Esq.

Senior Vice President, Law & Administration

Rockwood Specialties Group, Inc.

100 Overlook Center

Princeton, New Jersey 08540

(609) 514-0300

(Name, Address, Including Zip Code, and Telephone Number,

Including Area Code, of Agent For Service)

With copies to:

Roxane F. Reardon, Esq.

Simpson Thacher & Bartlett LLP

425 Lexington Avenue

New York, New York 10017

(212) 455-2000

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

| Title of Each Class of Securities to be Registered | Amount to be Registered | Proposed Maximum Offering Price Per Note | Proposed Maximum Aggregate Offering Price(1) | Amount of Registration Fee | ||||

|---|---|---|---|---|---|---|---|---|

| 7.625% Senior Subordinated Notes due 2014 | €375,000,000 | 100% | €375,000,000 | $53,221(2) | ||||

| Guarantees of 7.625% Senior Subordinated Notes due 2014(3) | N/A(4) | (4) | (4) | (4) | ||||

| 7.500% Senior Subordinated Notes due 2014 | $200,000,000 | 100% | $200,000,000 | $23,540 | ||||

| Guarantees of 7.500% Senior Subordinated Notes due 2014(3) | N/A(4) | (4) | (4) | (4) | ||||

- (1)

- Estimated solely for the purpose of calculating the registration fee under Rule 457 of the Securities Act of 1933, as amended (the "Securities Act").

- (2)

- The amount of the registration fee was calculated based on the noon buying rate at September 30, 2005 of $1.2058=EUR 1.00.

- (3)

- See inside facing page for additional registrant guarantors.

- (4)

- Pursuant to Rule 457(n) under the Securities Act, no separate filing fee is required for the guarantees.

The registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANT GUARANTORS

| Exact Name of Registrant as Specified in Its Charter | State or Other Jurisdiction of Incorporation of the Corporation | IRS Employer Identification Number | Address, Including Zip Code and Telephone Number, Including Area Code, of Registrant's Principal Executive Offices | |||

|---|---|---|---|---|---|---|

| Advantis Technologies, Inc. | Delaware | 58-2206931 | 1400 Bluegrass Lakes Parkway Alpharetta, GA, USA 30004 (770) 521-5999 | |||

AlphaGary Corporation | Delaware | 56-1803538 | 170 Pioneer Drive Leominster, MA, USA 01453 (978) 537-8071 | |||

CeramTec North America Innovative Ceramic Engineering Corporation | Delaware | 52-1708698 | One Technology Place Lauren, SC, USA 29360 (864) 682-3215 | |||

Chemetall Chemical Products Inc. | Delaware | 22-3175082 | 50 Valley Road Berkley Heights, NJ, USA 07922 (908) 508-2122 | |||

Chemetall Corporation | Delaware | 22-3140731 | 50 Valley Road Berkley Heights, NJ, USA 07922 (908) 508-2122 | |||

Chemetall Foote Corp. | Delaware | 51-03807781 | 348 Holiday Inn Drive Kings Mountain, NC, USA 28086 (704) 739-2501 | |||

Chemical Specialties, Inc. | North Carolina | 56-0751521 | One Woodlawn Green, Suite 250 200 East Woodlawn Road Charlotte, NC, USA 28217 (704) 522-0825 | |||

Compugraphics U.S.A. Inc. | Delaware | 77-0447768 | 120 C Albright Way Los Gatos, CA USA 95032 (408) 341-1600 | |||

Cyantek Corporation | Delaware | 94-3060725 | 3055 Osgood Court Fremont, CA, USA 94539 (510) 651-3341 | |||

Electrochemicals Inc. | Delaware | 34-1641793 | 5630 Pioneer Creek Drive Maple Plain, MN, USA 55359 (763) 479-2008 | |||

Exsil, Inc. | Delaware | 77-0414711 | 2575 Melville Road Prescott, AZ, USA 86301 (928) 771-8900 | |||

Foote Chile Holding Company | Delaware | 84-1468876 | 348 Holiday Inn Drive Kings Mountain, NC, USA 28086 (704) 739-2501 | |||

Lurex, Inc. | Delaware | 13-5659065 | 7101 Muirkirk Road Beltsville, MD, USA 20705 (301) 210-7800 | |||

Oakite Products, Inc. | Delaware | 13-3218362 | 50 Valley Road Berkley Heights, NJ, USA 07922 (908) 508-2122 | |||

Rockwood America Inc. | Delaware | 52-2071323 | 100 Overlook Center Princeton, NJ, USA 08540 (609) 514-0300 | |||

Rockwood Pigments NA, Inc. | Delaware | 06-0850804 | 7101 Muirkirk Road Beltsville, MD, USA 20705 (301) 210-7800 | |||

Rockwood Specialties Inc. | Delaware | 22-2269008 | 100 Overlook Center Princeton, NJ, USA 08540 (609) 514-0300 | |||

RS Funding Corporation | Delaware | 74-3073388 | 7101 Muirkirk Road Beltsville, MD, USA 20705 (301) 210-7800 | |||

RW Holding Corp. | Delaware | 47-0940470 | 100 Overlook Center Princeton, NJ, USA 08540 (609) 514-0300 | |||

Sachtleben Corporation | Delaware | 13-3798109 | 520 Madison Avenue New York, NY, USA 10028 (212) 715-5828 | |||

Southern Clay Products, Inc. | Texas | 74-4521192 | 5508 Highway 290 West, Suite 206 Austin, TX, USA 78735 (512) 891-9140 | |||

Southern Color N.A., Inc. | Delaware | 36-4521192 | 7 Swisher Drive Cartersville, GA, USA 30120 (770) 386-4766 |

THE INFORMATION IN THIS PROSPECTUS IS NOT COMPLETE AND MAY BE CHANGED. WE MAY NOT SELL THESE SECURITIES UNTIL THE REGISTRATION STATEMENT FILED WITH THE SECURITIES AND EXCHANGE COMMISSION IS EFFECTIVE. THIS PROSPECTUS IS NOT AN OFFER TO SELL THESE SECURITIES AND IT IS NOT SOLICITING AN OFFER TO BUY THESE SECURITIES IN ANY STATE WHERE THE OFFER OR SALE IS NOT PERMITTED.

Subject to completion, dated October 5, 2005

PRELIMINARY PROSPECTUS

OFFER TO EXCHANGE

€375,000,000 principal amount of its 7.625% Senior Subordinated Notes due 2014, which have been registered under the Securities Act of 1933, for any and all of our outstanding 7.625% Senior Subordinated Notes due 2014.

$200,000,000 principal amount of its 7.500% Senior Subordinated Notes due 2014, which have been registered under the Securities Act of 1933, for any and all of our outstanding 7.500% Senior Subordinated Notes due 2014.

The exchange notes will be fully and unconditionally guaranteed on a senior subordinated unsecured basis by certain of our domestic subsidiaries.

We are conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered notes for freely tradeable notes that have been registered under the Securities Act.

The Exchange Offer

- •

- We will exchange all outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are freely tradeable.

- •

- You may withdraw tenders of outstanding notes at any time prior to the expiration date of the exchange offer.

- •

- The exchange offer expires at , New York City time, on , 2005, unless extended. We do not currently intend to extend the expiration date.

- •

- The exchange of outstanding notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes.

- •

- The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes, except that the exchange notes will be freely tradeable.

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act.

Application has been made to the Irish Financial Services Regulatory Authority, as competent authority under Directive 2003/71/EC (the "Prospectus Directive"), for this prospectus to be approved. Application has been made to the Irish Stock Exchange for the Notes issued to be admitted to the Official List and trading on its regulated market.

This prospectus comprises a prospectus for the purposes of Article 5 of the Prospectus Directive and for the purpose of giving information with regard to Rockwood Specialties Group, Inc. and the guarantors named herein.

See "Risk Factors" beginning on page 23 for a discussion of certain risks that you should consider before participating in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.The date of this prospectus is , 2005.

| | Page | |

|---|---|---|

| Prospectus Summary | 1 | |

| Risk Factors | 23 | |

| Forward-Looking Statements | 42 | |

| Use of Proceeds | 43 | |

| Capitalization | 44 | |

| Unaudited Pro Forma Condensed Combined Financial Information | 45 | |

| Selected Financial Data | 51 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 59 | |

| Dynamit Nobel Acquisition | 127 | |

| Business | 130 | |

| Management | 177 | |

| Principal Stockholders | 190 | |

| Related Party Transactions | 193 | |

| Description of Certain Other Indebtedness | 199 | |

| The Exchange Offer | 206 | |

| Description of the Notes | 219 | |

| Book Entry; Delivery and Form | 273 | |

| Certain ERISA Considerations | 279 | |

| Plan of Distribution | 281 | |

| Legal Matters | 282 | |

| Experts | 282 | |

| Listing and General Information | 282 | |

| Summary of Certain Differences Between IAS and IFRS and U.S. GAAP | 285 | |

| Market Share and Industry Data | 292 | |

| Where You Can Find Additional Information | 293 | |

| Index to Combined Financial Statements | F-1 |

This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any notes offered hereby in any jurisdiction where, or to any person to whom, it is unlawful to make such offer or solicitation. The information contained in this prospectus speaks only as of the date of this prospectus unless the information specifically indicates that another date applies. No dealer, salesperson or other person has been authorized to give any information or to make any representations other than those contained in this prospectus in connection with the offers contained herein and, if given or made, such information or representations must not be relied upon as having been authorized by us. Neither the delivery of this prospectus nor any sales made hereunder shall under any circumstances create an implication that there has been no change in our affairs or that of our subsidiaries since the date hereof.

Until the date that is 90 days from the date of this prospectus, all dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers' obligation to deliver a prospectus when acting as underwriters with respect to their unsold allotments or subscriptions.

i

This summary may not contain all of the information that may be important to you. You should read the entire prospectus, including the historical and pro forma financial data and related notes, before making an investment decision. This summary contains forward-looking statements that involve risks and uncertainties. Our actual results may differ significantly from the results discussed in the forward-looking statements as a result of certain factors, including those set forth in "Risk Factors" and "Forward-Looking Statements."

In this prospectus, unless we indicate otherwise or the context otherwise requires, any references to the "Company," "we," "our," and "us" refer to Rockwood Specialties Group, Inc. and its consolidated subsidiaries, and any references to the "issuer" refers to Rockwood Specialties Group, Inc. In addition, when the context so requires, we use the term "Rockwood" to refer to our historical operations prior to the Dynamit Nobel acquisition (described below) and the term "Dynamit Nobel" to refer to the historical operations of the businesses of Dynamit Nobel AG that we acquired from mg technologies ag in July 2004. The historical financial statements and related notes (other than our financial statements as of and for the year ended December 31, 2004 which include the results of operations of the acquired Dynamit Nobel businesses during the five-month period ended December 31, 2004 and the six-month period ended June 30, 2005, respectively) presented in this prospectus are separate financial statements and related notes of Rockwood and Dynamit Nobel.

On November 10, 2004, we completed the private offering of the €375,000,000 7.625% Senior Subordinated Notes due 2014 and the $200,000,000 7.500% Senior Subordinated Notes due 2014, or the outstanding notes. References to the "notes" or the "2014 notes" in this prospectus are references to both the outstanding notes and the exchange notes.

The issuer accepts responsibility for the information contained within this prospectus. To the best knowledge and belief of the issuer (who has taken all reasonable care to ensure that such is the case), such information is in accordance with the facts and does not omit anything likely to affect the import of such information.

We are a leading global developer, manufacturer and marketer of technologically advanced, high value-added specialty chemicals and advanced materials. We believe we have leading market positions in most of our businesses, including lithium compounds, fiber anatase titanium dioxide, color pigments and services, ceramic-on-ceramic components used in hip joint prostheses systems and next generation wood protection products.

We have a number of higher growth businesses such as Advanced Ceramics, Specialty Chemicals and Performance Additives, which are complemented by a diverse portfolio of businesses that historically have generated predictable, stable revenues. Our margins, strong cash flow generation, capital discipline and ongoing productivity improvements provide us with a platform to capitalize on the market growth opportunities.

We operate globally, manufacturing our products in over 100 manufacturing facilities in 25 countries and selling our products and providing our services to more than 60,000 customers, including some of the world's preeminent companies. Our products, consisting primarily of inorganic chemicals and solutions and engineered materials, are often customized to meet the complex needs of our customers and to enhance the value and performance of their end products.

We generally compete in niche markets in a wide range of end-use markets, including construction, life sciences (including pharmaceutical and medical markets), electronics and telecommunications, metal treatment and general industrial and consumer products markets. No single end-use market accounted for more than 19% of our $2,913.0 million 2004 pro forma net sales.

1

Following the acquisition of Dynamit Nobel in July 2004, we operate our business through seven segments:

| Segment | % of 2004 Pro Forma Net Sales | ||

|---|---|---|---|

| Performance Additives | 23 | % | |

| Specialty Compounds | 7 | ||

| Electronics | 6 | ||

| Specialty Chemicals | 26 | ||

| Titanium Dioxide Pigments | 14 | ||

| Advanced Ceramics | 12 | ||

| Groupe Novasep | 12 |

Our Competitive Strengths

Leading market positions. We believe that we hold leading market positions within most of our businesses, including, based on our 2004 pro forma net sales:

| Segment | Products | Market Position | ||||

|---|---|---|---|---|---|---|

| Performance Additives | • | synthetic iron oxide pigments | one of top 3 globally | |||

| • | wood protection products | one of top 3 globally | ||||

| Specialty Chemicals | • | lithium compounds and chemicals | #1 globally | |||

| • | metal surface treatment chemicals and related services | #2 globally | ||||

| Titanium Dioxide Pigments | • | anatase titanium dioxide pigment for the synthetic fiber manufacturing industry | #1 globally | |||

| Advanced Ceramics | • | ceramic-on-ceramic ball head and liner components used in hip joint prostheses systems | #1 globally | |||

| • | ceramics cutting tools | #1 in Europe | ||||

Specialty businesses in niche markets with significant barriers to entry. We believe that nearly all of our businesses operate in niche markets protected by significant barriers to entry. We believe that many of our customers would experience significant disruption and costs if they were to switch to another supplier.

Diverse customer and end-use market base. We operate a diverse portfolio of distinct specialty chemicals and advanced materials businesses that cover a wide variety of industries and geographic areas. Of our 2004 pro forma net sales, 50% were shipments to Europe, 34% to North America and 16% to the rest of the world. No customer accounted for more than 2% of such net sales, and our top ten customers represented only approximately 11% of such net sales.

Limited exposure to raw materials and energy prices. We have a broad raw material base consisting primarily of inorganic (non-petrochemical) materials, most of which are readily available and whose prices follow their own individual supply and demand relationships and have historically shown little correlation to each other. Our exposure to energy prices is limited.

Leading technologies and strong brand names. We believe we are recognized for our use of our technological know-how and expertise to improve, develop and manufacture customized product and process innovations that meet specific customers' performance requirements.

Experienced and proven management team with significant equity interests. Since joining us in 2001, Seifi Ghasemi, our chairman and chief executive officer, and Robert Zatta, our senior vice president

2

and chief financial officer, together with other members of our senior management team, have implemented a series of improvement initiatives designed to increase sales, improve productivity, reduce costs and expand margins. These initiatives have had a positive impact on the cash flow and profitability of Rockwood's historic businesses.

Our Business Strategy

Building on these strengths, we plan to continue our existing strategy to grow revenue and cash flow and increase profitability as follows:

Capitalize on expected market growth opportunities. We expect our businesses to benefit from a number of growth trends, including:

- •

- Advanced Ceramics—a growing trend toward replacing plastics and metals with high-performance ceramics.

- •

- Specialty Chemicals—increased demand for lithium-based batteries for mobile electronic applications.

- •

- Performance Additives—a growing trend toward the use of color in concrete paving stones and other home remodeling.

- •

- Titanium Dioxide Pigments—sales of newly-introduced nano-particle titanium dioxide pigments that are used to provide ultraviolet light protection for plastics and coatings.

Achieve profitable growth through selective acquisitions. We intend to continue to selectively pursue cash flow accretive acquisitions and strategic alliances in order to strengthen and expand our existing business lines and enter into complementary business lines. Although we are not subject to any agreement or binding letter of intent with respect to potential acquisitions, we are engaged in acquisition discussions with other parties.

Apply our proven improvement initiatives to the Dynamit Nobel businesses. We are currently in the process of applying the management initiatives successfully applied to Rockwood's historic businesses to the acquired Dynamit Nobel businesses.

Reduce financial leverage. We have reduced our financial leverage by using a portion of the net proceeds of our ultimate parent company's initial public offering to repay debt and we intend to continue to reduce our financial leverage by using a significant portion of cash flow from operations after required capital expenditures and payments to service our debt. We believe that our strong cash flow generation will be further strengthened by organic growth opportunities within our existing markets, cost-reduction programs applied to the Dynamit Nobel businesses and improved working capital management.

Risks Relating to Our Business Strategy

We may not be able to continue our product innovation, demand for our products may not develop as expected, and regulation of our raw materials, products and facilities may change in a way that is detrimental to our business. We incurred net losses of $55.2 million, $72.0 million and $148.2 million in 2002, 2003 and 2004, respectively.

In addition, we have a substantial amount of indebtedness. As of June 30, 2005, we had $2,962.3 million of indebtedness outstanding and total stockholders' equity of $785.3 million. This substantial indebtedness may adversely affect our cash flow and our ability to remain in compliance with our debt covenants, make payments on our indebtedness and operate our business. Any of these factors or other factors described in this prospectus under "Risk Factors" may limit our ability to successfully execute our business strategy.

3

On April 19, 2004, we entered into a sale and purchase agreement with mg technologies ag to acquire its wholly-owned specialty chemicals and advanced materials business, Dynamit Nobel. The acquisition was consummated on July 31, 2004. We paid approximately $2,274.0 million (based on the July 31, 2004 exchange rate of €1.00=$1.2040), including assumed debt of $315.1 million and cash acquired of $9.6 million, for the businesses acquired. On July 6, 2005, we paid $16.1 million (based on the July 6, 2005 exchange rate of €1.00=$1.1927) in post-closing adjustments.

In connection with the Dynamit Nobel acquisition, we received a net equity contribution of $404.0 million from affiliates of Kohlberg Kravis Roberts & Co. L.P., or KKR and DLJ Merchant Banking Partners III, L.P. and its affiliated funds, or DLJMB, and we entered into senior secured credit facilities and a senior subordinated loan facility. In addition, an indirect parent exchanged its outstanding dollar-denominated pay-in-kind notes for euro-denominated pay-in-kind notes. The pay-in-kind notes were redeemed in connection with the initial public offering of Rockwood Holdings in August 2005. In this prospectus, we refer to these related financings collectively as the acquisition financings.

In addition, in connection with the Dynamit Nobel acquisition, members of our management and certain other employees made cash equity investments of approximately $7.0 million in Rockwood Holdings, Inc. ("Rockwood Holdings") from September 2004 to December 2004. In this prospectus, we refer to this investment as the 2004 management equity program.

In September 2004, we acquired the pigments and dispersions business of Johnson Matthey Plc. for a purchase price of approximately $47.1 million and in connection with this acquisition borrowed $50.4 million (based on the September 27, 2004 exchange rate of €1.00=$1.2029) under a term loan of the senior secured credit facilities.

In December 2004, in connection with the combination of the three business lines of our Custom Synthesis segment (now known as our Groupe Novasep segment) with Groupe Novasep SAS (or Groupe Novasep), one of our subsidiaries acquired 69.4% of the stock of Groupe Novasep for a total purchase price of approximately $139.7 million, including assumed debt of $48.6 million, cash acquired of $14.6 million and the exchange of the remaining 30.6% of the stock of Groupe Novasep for stock in our acquiring subsidiary. As a result of this transaction, we own approximately 79% of the new Groupe Novasep. We used cash on hand to finance this transaction.

In this prospectus, we refer to the Dynamit Nobel acquisition and related equity and debt financings and Fall 2004 debt refinancings (as defined below), the pigments and dispersions acquisition and related financing and the Groupe Novasep combination collectively as the Transactions.

Recent Developments—Repayment of Debt

On August 22, 2005, Rockwood Holdings, our ultimate parent, completed an initial public offering of 23,469,387 shares of its common stock, which included 3,061,224 shares issued and sold as a result of the underwriters' exercise of the over-allotment option. Net proceeds were $435.7 million. $116.2 million of the net proceeds was used to redeem $101.6 million, or 27%, of the 2011 notes (as defined below) and pay a redemption premium and accrued and unpaid interest. The pro forma as adjusted reduction in cash interest expense as a result of this redemption would be approximately $10.8 million annually. The remaining net proceeds were used to redeem pay-in-kind loans and notes, senior discount notes and redeemable convertible preferred stock, as well as to terminate the management services agreement with affiliates of KKR and DLJMB. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Liquidity."

4

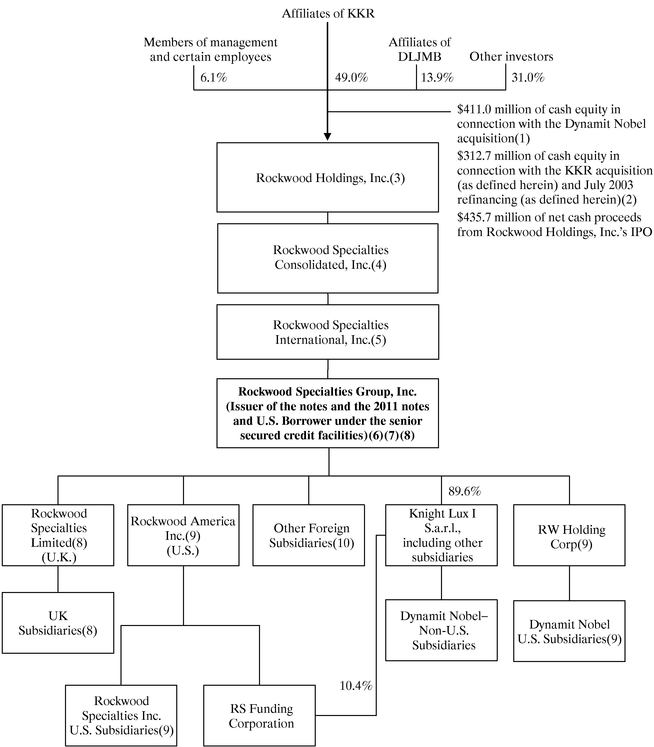

The chart below illustrates our approximate ownership and corporate structure as of August 31, 2005. Ownership of Rockwood Holdings is presented on a fully-diluted basis.

- (1)

- Represents $265.6 million of common equity contributed by affiliates of KKR, $159.4 million of common equity contributed by DLJMB and $7.0 million of common equity contributed by members of our management and certain other employees under the 2004 management equity

5

program, less $20.0 million repayment of a portion of the additional pay-in-kind notes issued in connection with interest payments on the $70.0 million initial aggregate principal amount of pay-in-kind notes and $1.0 million payment of a related fee.

- (2)

- Represents $287.7 million of common equity contributed by affiliates of KKR and our management in connection with the KKR acquisition and $25.0 million of preferred equity contributed by affiliates of KKR in connection with the July 2003 refinancing.

- (3)

- In connection with our July 2003 debt refinancing, Holdings issued 25,000 shares of redeemable convertible preferred stock to an affiliate of KKR, which were redeemed with a portion of the net proceeds of Rockwood Holdings' initial public offering.

- (4)

- In connection with the KKR acquisition, Rockwood Specialties Consolidated, Inc. borrowed $100.0 million under a 15% pay-in-kind unsecured subordinated loan facility, pursuant to which interest was paid by increasing the principal amount outstanding rather than paying cash. $70.0 million of these pay-in-kind loans were exchanged for pay-in-kind notes in February 2001, pursuant to which interest was paid by issuing additional notes rather than paying cash. The pay-in-kind notes (including additional pay-in-kind notes issued in connection with interest payments on these notes) were exchanged for euro-denominated pay-in-kind notes, after the repayment in cash of $20.0 million of such additional pay-in-kind notes, in connection with the Dynamit Nobel acquisition. The pay-in-kind notes were redeemed with a portion of the net proceeds of Rockwood Holdings' initial public offering.

- (5)

- In connection with the July 2003 debt refinancing, Rockwood Specialties International, Inc. issued $70.0 million gross proceeds 12% senior discount notes, which were held by an affiliate of KKR and were redeemed with a portion of the net proceeds of Rockwood Holdings' initial public offering.

- (6)

- We issued the outstanding notes in November 2004.

- (7)

- We issued $375.0 million aggregate principal amount of 105/8% senior subordinated notes due 2011 in connection with the July 2003 debt refinancing, 27% of which were redeemed in connection with our ultimate parent's IPO. In this prospectus, we refer to these notes as the 2011 notes.

- (8)

- Our senior secured credit facilities consist of tranche A-1 loans in an aggregate principal amount of €39.1 million (or $47.4 million), tranche A-2 term loans in an aggregate principal amount of €170.4 million (or $206.3 million), tranche C term loans in an aggregate principal amount of €274.8 million (or $332.7 million), tranche D term loans in an aggregate principal amount of $1,145.0 million and a revolving credit facility in an aggregate principal amount of $250.0 million. As of June 30, 2005 and September 30, 2005, we had no amounts outstanding under the revolving credit facility. We had outstanding letters of credit of $21.8 million at September 13, 2005 that reduced our availability under the credit facility. The U.S. dollar equivalents of euro borrowings are based on the exchange rate at June 30, 2005 of €1.00=$1.2106.

- (9)

- All of these entities (other than certain special-purpose entities formed in connection with the previous sale of certain of our accounts receivable) guarantee all amounts outstanding under our senior secured credit facilities on a senior basis and our 2011 notes and 2014 notes on a senior subordinated basis.

- (10)

- Certain of our foreign subsidiaries guarantee amounts borrowed by Rockwood Specialties Limited under our senior secured credit facilities, but do not guarantee the 2011 notes or 2014 notes.

6

| General | In connection with the private offering, we entered into a registration rights agreement with Credit Suisse First Boston (Europe) Limited, Goldman, Sachs & Co., UBS Limited, Credit Suisse First Boston LLC and UBS Securities LLC as the representatives of the several initial purchasers in which we agreed, among other things, to deliver this prospectus to you and to make our best efforts to complete the exchange offer within 300 days after the date of original issuance of the outstanding notes. You are entitled to exchange in the exchange offer your outstanding notes for exchange notes which are identical in all material respects to the outstanding notes except: | |||

• | the exchange notes have been registered under the Securities Act; | |||

• | the exchange notes are not entitled to certain registration rights which are applicable to the outstanding notes under the registration rights agreement; and | |||

• | the additional interest provisions of the registration rights agreement are not applicable. | |||

The Exchange offer | We are offering to exchange: | |||

• | up to €375,000,000 aggregate principal amount of our 7.625% Senior Subordinated Notes due 2014, which have been registered under the Securities Act of 1933, for any and all of our outstanding 7.625% Senior Subordinated Notes due 2014. | |||

• | up to $200,000,000 aggregate principal amount of our 7.500% Senior Subordinated Notes due 2014, which have been registered under the Securities Act of 1933, for any and all of our outstanding 7.500% Senior Subordinated Notes due 2014. | |||

• | You may only exchange outstanding notes in a principal amount of €50,000 or in integral multiples of €1,000 in excess thereof in the case of the outstanding euro notes and in a principal amount of $50,000 or in integral multiples of $1,000 in excess thereof in the case of the outstanding dollar notes. | |||

7

Resale | Based on an interpretation by the staff of the Securities and Exchange Commission, or the SEC, set forth in no-action letters issued to third parties, we believe that the exchange notes to be issued pursuant to the exchange offer in exchange for outstanding notes may be offered for resale, resold and otherwise transferred by you (unless you are our "affiliate" within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that you are acquiring the exchange notes in the ordinary course of your business and that you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. | |||

If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market-making activities or other trading activities, you must acknowledge that you will deliver this prospectus in connection with any resale of the exchange notes. See "Plan of Distribution." | ||||

Any holder of outstanding notes who: | ||||

• | is our affiliate; | |||

• | does not acquire exchange notes in the ordinary course of its business; or | |||

• | tenders its outstanding notes in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of exchange notes | |||

cannot rely on the position of the staff of the SEC enunciated inMorgan Stanley & Co. Incorporated (available June 5, 1991) andExxon Capital Holdings Corporation (available May 13, 1988), as interpreted in the SEC's letter toShearman & Sterling, available July 2, 1993, or similar no-action letters and, in the absence of an exemption therefrom, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. | ||||

Expiration date | The exchange offer will expire at 12:00 a.m. midnight, New York City time, on , 2005, or such date and time to which we extend the exchange offer. | |||

Withdrawal | You may withdraw the tender of your outstanding notes at any time prior to the expiration of the exchange offer. We will return to you any of your outstanding notes that are not accepted for any reason for exchange, without expense to you, promptly after the expiration or termination of the exchange offer. | |||

8

Conditions to the exchange offer | The exchange offer is subject to customary conditions, which we may waive. See "The Exchange Offer—Conditions to the Exchange Offer" for more information regarding conditions to the exchange offer. | |||

Procedures for tendering outstanding notes | If you wish to participate in the exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a facsimile of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must then mail or otherwise deliver the letter of transmittal, or a facsimile of the letter of transmittal, together with the outstanding notes and any other required documents, to the exchange agent at the address set forth on the cover page of the letter of transmittal. If you hold outstanding dollar notes through The Depository Trust Company ("DTC") and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC and if you hold outstanding euro notes through Euroclear Bank S.A./N.V. ("Euroclear") or Clearstream Banking, societe anonyme ("Clearstream, Luxembourg") and wish to participate in the exchange offer, you must comply with the procedures of Euroclear or Clearstream, Luxembourg, as applicable, in each case, by which you will agree to be bound by the letter of transmittal. By signing, or agreeing to be bound by, the letter of transmittal, you will represent to us that, among other things: | |||

• | you are not our "affiliate" within the meaning of Rule 405 under the Securities Act or, if you are our affiliate, that you will comply with any applicable registration and prospectus delivery requirements of the Securities Act; | |||

• | you do not have an arrangement or understanding with any person or entity to participate in the distribution of the exchange notes; | |||

• | you are acquiring the exchange notes in the ordinary course of your business; and | |||

• | if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making activities, that you will deliver a prospectus, as required by law, in connection with any resale of such exchange notes. | |||

9

Special procedures for beneficial owners | If you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender those outstanding notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender those outstanding notes on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed before the expiration date. | |||

Guaranteed delivery procedures | If you wish to tender your outstanding notes and your outstanding notes are not immediately available or you cannot deliver your outstanding notes, the letter of transmittal or any other required documents, or you cannot comply with the applicable procedures under DTC's Automated Tender Offer Program or the procedures of Euroclear or Clearstream, Luxembourg, as applicable, for transfer of book-entry interests, prior to the expiration date, you must tender your outstanding notes according to the guaranteed delivery procedures set forth in this prospectus under "The Exchange Offer—Guaranteed Delivery Procedures." | |||

Effect on holders of outstanding notes | As a result of the making of, and upon acceptance for exchange of all validly tendered outstanding notes pursuant to the terms of the exchange offer, we will have fulfilled a covenant under the registration rights agreement. Accordingly, the increase in the interest rate on the outstanding notes that commenced in May 2005 under the circumstances described in the registration rights agreement will cease upon consummation of the exchange offer. If you do not tender your outstanding notes in the exchange offer, you will continue to be entitled to all the rights and limitations applicable to the outstanding notes as set forth in the indenture, except we will not have any further obligation to you to provide for the exchange and registration of the outstanding notes under the registration rights agreement. To the extent that outstanding notes are tendered and accepted in the exchange offer, the trading market for outstanding notes could be adversely affected. | |||

10

Consequences of failure to exchange | All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with this exchange offer, we do not currently anticipate that we will register the outstanding notes under the Securities Act. | |||

Material U.S. Federal Income Tax Consequences | The exchange of the exchange notes for outstanding notes will not be a taxable event for U.S. federal income tax purposes. See "Material U.S. Federal Income Tax Consequences of the Exchange Offer." | |||

Use of proceeds | We will not receive any cash proceeds from the issuance of exchange notes in the exchange offer. See "Use of Proceeds." | |||

Exchange Agent | The Bank of New York is the exchange agent for the exchange offer. The address and telephone number of the exchange agent are set forth in the section captioned "The Exchange Offer—Exchange Agent" of this prospectus. | |||

11

Issuer | Rockwood Specialties Group, Inc. | |||

Securities offered | €375,000,000 aggregate principal amount of 7.625% Senior Subordinated Notes due 2014. | |||

$200,000,000 aggregate principal amount of 7.500% Senior Subordinated Notes due 2014. | ||||

Maturity date | November 15, 2014. | |||

Interest | 7.625% per year for the euro notes and 7.500% per year for the dollar notes, respectively, in each case, payable semi-annually in arrears on May 15 and November 15, commencing on May 15, 2005. | |||

Subsidiary guarantees | All payments on the notes, including principal, premium, if any, and interest, will be jointly and severally guaranteed on a senior subordinated unsecured basis by certain of our domestic subsidiaries. | |||

Ranking | The notes and the subsidiary guarantees are senior subordinated obligations and will rank: | |||

• | subordinated to all of our and our subsidiary guarantors' existing and future senior indebtedness; | |||

• | structurally subordinated to all of the indebtedness and other liabilities of our non-guarantor subsidiaries (other than indebtedness and other liabilities owed to us); | |||

• | equally with our existing and future senior subordinated indebtedness, including the 2011 notes; and | |||

• | senior to all of our and our subsidiary guarantors' future expressly subordinated indebtedness. | |||

As of June 30, 2005: | ||||

• | we and our subsidiary guarantors had $2,962.3 million of total indebtedness; | |||

• | we and our subsidiary guarantors had $1,731.4 million of senior indebtedness (we also would have had letters of credit of $18.9 million outstanding); | |||

• | we and our subsidiary guarantors had $1,029.0 million of senior subordinated indebtedness; | |||

• | we and our subsidiary guarantors had no indebtedness expressly subordinated; and | |||

• | our non-guarantor subsidiaries had indebtedness and other liabilities of $1,356.3 million, held approximately 82% of our total assets and during the six months ended June 30, 2005, generated approximately 71% of our net sales. | |||

12

Optional redemption | We may redeem some or all of each series of the notes on or after November 15, 2009 at the redemption prices specified in this prospectus. We may also redeem some or all of each series of the notes at any time prior to November 15, 2009 at a redemption price equal to the make-whole amount set forth in this prospectus. At any time and from time to time on or prior to November 15, 2007, we may redeem up to 40% of the aggregate principal amount of each series of the notes with the net cash proceeds of one or more certain equity offerings. See "Description of the Notes—Optional Redemption." | |||

Change of control | Upon certain change of control events, we will be required to make an offer to repurchase each holder's notes at a repurchase price equal to 101% of their principal amount, plus accrued and unpaid interest, and additional interest if any, to the date of repurchase. See "Description of the Notes—Repurchase at the Option of the Holders—Change of Control." | |||

Certain covenants | The indenture governing the notes contain covenants that, among other things, limit our ability and the ability of our restricted subsidiaries to: | |||

• | incur additional indebtedness; | |||

• | pay dividends or make other distributions or repurchase our capital stock; | |||

• | make investments; | |||

• | create liens; | |||

• | transfer or sell assets; | |||

• | restrict dividends or payments to us; | |||

• | guarantee indebtedness; | |||

• | engage in transactions with affiliates; and | |||

• | merge or consolidate with other companies or sell substantially all of our assets. | |||

These covenants are subject to a number of important exceptions and limitations. See "Description of the Notes." | ||||

No Prior Market | The exchange notes will be freely transferable but will be new securities for which there will not initially be a market. Accordingly, we cannot assure you whether a market for the exchange notes will develop or as to the liquidity of any market. The initial purchasers in the private offering of the outstanding notes have advised us that they currently intend to make a market in the exchange notes. The initial purchasers are not obligated, however, to make a market in the exchange notes, and any such market-making may be discontinued by the initial purchasers in their discretion at any time without notice. | |||

13

Listing | Application has been made to the Irish Financial Services Regulatory Authority, as competent authority under the Prospectus Directive, for this Prospectus to be approved. Application has been made to the Irish Stock Exchange for the notes issued to be admitted to the Official List and trading on its regulated market. | |||

Irish Paying Agent and Listing Agent | AIB/BNY Fund Management and Arthur Cox Listing Services Limited. | |||

Risk Factors | Investment in the exchange notes involves certain risks. You should carefully consider the information in the "Risk Factors" section and all other information included in this prospectus before investing in the exchange notes. | |||

Rockwood Specialties Group, Inc. is a Delaware corporation which was formed on October 19, 2000 in connection with the KKR acquisition. Our principal executive offices are located at 100 Overlook Center, Princeton, New Jersey 08540. Our telephone number is (609) 514-0300. Our website address iswww.rocksp.com. Information contained on our website is not incorporated by reference into this prospectus, and you should not consider information on our website as part of this prospectus.

14

Summary Historical and Pro Forma Financial Data

Set forth below is summary historical financial and summary pro forma financial data of Rockwood, in each case, at the dates and for the periods indicated.

The summary historical financial data presented below for the years ended December 31, 2002 and 2003 and as of and for the year ended December 31, 2004 have been derived from Rockwood's audited consolidated financial statements included elsewhere in this prospectus. The summary financial data presented below for the six-month period ended June 30, 2004 and as of and for the six-month period ended June 30, 2005 have been derived from our unaudited consolidated financial statements included elsewhere in this prospectus. In the opinion of management, the unaudited financial statements for the six months ended June 30, 2004 and 2005, have been prepared on a basis consistent with the audited financial statements and include all adjustments, which are normally recurring adjustments, necessary for a fair presentation of the results of operations for the periods presented. Results of operations for the interim periods are not necessarily indicative of the results that might be expected for any other interim period or for an entire year.

The unaudited pro forma statements of operations data and other pro forma financial data give effect to the Transactions as if they had occurred on January 1, 2004 and is based on the weighted average exchange rate of €1.00 = $1.2669.

As described above, the Transactions include, among other things, the equity and debt financings and Fall 2004 debt refinancings related to the Dynamit Nobel acquisition. Specifically, in connection with the Dynamit Nobel acquisition, we received a net equity contribution of $404.0 million from affiliates of KKR and DLJ Merchant Banking Partners III, L.P. and its affiliated funds, or DLJMB, and we entered into senior secured credit facilities and a senior subordinated loan facility. In addition, an indirect parent company exchanged its outstanding dollar-denominated pay-in-kind notes for euro-denominated pay-in-kind notes. In addition, in connection with the Dynamit Nobel acquisition, members of Rockwood Holding's management and certain other employees made cash equity investments of approximately $7.0 million from September 2004 to December 2004. In this prospectus, we refer to these related financings collectively as the acquisition financings.

In October 2004, we refinanced a portion of our borrowings under the senior subordinated loan facility with additional term loan borrowings under an amendment to the senior secured credit facilities. In November 2004, we refinanced the remaining borrowings under the senior subordinated loan facility with proceeds from the issuance of senior subordinated notes due 2014, which we refer to as the 2014 notes. In December 2004, we refinanced all of our borrowings under one tranche of term loans under our senior secured credit facilities with borrowings under a new tranche of term loans of the same aggregate principal amount bearing a lower interest rate in order to reduce our interest expense. In this prospectus, we refer to these three refinancings collectively as the Fall 2004 debt refinancings.

The summary unaudited pro forma condensed combined financial information is based on the audited and unaudited consolidated financial statements of Rockwood, our audited and unaudited consolidated financial statements and the audited and unaudited combined financial statements of Dynamit Nobel, in each case, included elsewhere in this prospectus, as adjusted to illustrate the estimated pro forma effects of the Transactions.

The summary unaudited pro forma condensed combined financial information is for illustrative purposes only. Such information is not intended to be indicative of the financial condition and the results of operations that would have been achieved had the Transactions for which we are giving pro forma effect actually occurred on the dates referred to above or the financial condition and the results of operations that may be expected in the future. The unaudited pro forma condensed combined financial information has been prepared based upon currently available information and assumptions

15

that we believe are reasonable. Such currently available information and assumptions may prove to be inaccurate over time.

The summary historical and pro forma financial data presented below should be read together with "Selected Financial Data," "Unaudited Pro Forma Condensed Combined Financial Information," "Management's Discussion and Analysis of Financial Condition and Results of Operations," Rockwood's consolidated financial statements and the notes to those statements, our consolidated financial statements and the notes to those statements and Dynamit Nobel's combined financial statements and the notes to those statements, in each case, included elsewhere in this prospectus.

| | | | | | Six Months Ended June 30, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, | Pro Forma Year Ended December 31, 2004 | ||||||||||||||||||

| | 2002 | 2003 | 2004 | 2004 | 2005 | |||||||||||||||

| | ($ in millions) | |||||||||||||||||||

| Statement of operations data: | ||||||||||||||||||||

| Net sales: | ||||||||||||||||||||

| Performance Additives | $ | 443.8 | $ | 477.3 | $ | 630.9 | $ | 674.8 | $ | 312.3 | $ | 349.6 | ||||||||

| Specialty Compounds | 168.8 | 176.4 | 200.4 | 200.4 | 100.4 | 120.2 | ||||||||||||||

| Electronics | 147.3 | 143.6 | 168.1 | 168.1 | 81.6 | 87.7 | ||||||||||||||

| Specialty Chemicals | — | — | 321.1 | 759.6 | — | 439.7 | ||||||||||||||

| Titanium Dioxide Pigments | — | — | 175.7 | 422.0 | — | 213.7 | ||||||||||||||

| Advanced Ceramics | — | — | 146.3 | 349.5 | — | 188.3 | ||||||||||||||

| Groupe Novasep | — | — | 101.0 | 338.6 | — | 187.9 | ||||||||||||||

| Total net sales | 759.9 | 797.3 | 1,743.5 | 2,913.0 | 494.3 | 1,587.1 | ||||||||||||||

| Cost of products sold | 542.5 | 581.4 | 1,267.6 | 2,008.9 | 353.3 | 1,098.5 | ||||||||||||||

| Gross profit | 217.4 | 215.9 | 475.9 | 904.1 | 141.0 | 488.6 | ||||||||||||||

| Selling, general and administrative expenses | 112.9 | 118.0 | 327.7 | 617.1 | 71.1 | 307.7 | ||||||||||||||

| Impairment charges(1) | 50.0 | 35.0 | 11.0 | 11.0 | — | — | ||||||||||||||

| Restructuring charges | 1.2 | 1.8 | 1.1 | 1.1 | — | 5.8 | ||||||||||||||

| Operating income | 53.3 | 61.1 | 136.1 | 274.9 | 69.9 | 175.1 | ||||||||||||||

| Other income (expenses): | ||||||||||||||||||||

| Interest expense, net(2) | (88.2 | ) | (85.8 | ) | (127.7 | ) | (211.4 | ) | (29.1 | ) | (103.9 | ) | ||||||||

| Foreign exchange loss (gain)(3) | (24.6 | ) | (18.5 | ) | (113.2 | ) | (113.2 | ) | 8.6 | 100.5 | ||||||||||

| Refinancing expenses(4) | — | (38.3 | ) | (26.1 | ) | (26.1 | ) | — | — | |||||||||||

| Loss on receivables sold | (1.2 | ) | — | — | — | — | ||||||||||||||

| Stamp duty tax and other(5) | — | — | (4.3 | ) | (0.2 | ) | (4.0 | ) | — | |||||||||||

| (Loss) income before taxes and other adjustments | (60.7 | ) | (81.5 | ) | (135.2 | ) | (76.0 | ) | 45.4 | 171.7 | ||||||||||

| Income tax (benefit) provision | (5.5 | ) | (9.5 | ) | 13.0 | 46.7 | 19.6 | 41.7 | ||||||||||||

| Minority interest | — | — | — | — | — | 1.7 | ||||||||||||||

| Net (loss) income | $ | (55.2 | ) | $ | (72.0 | ) | $ | (148.2 | ) | $ | (122.7 | ) | $ | 25.8 | $ | 131.7 | ||||

| Cash flow data: | ||||||||||||||||||||

| Net cash (used in) provided by operating activities | $ | (3.4 | ) | $ | 45.7 | $ | 179.6 | $ | 44.7 | $ | 63.1 | |||||||||

| Net cash used in investing activities | (30.4 | ) | (48.5 | ) | (2,249.9 | ) | (13.3 | ) | (76.6 | ) | ||||||||||

| Net cash (used in) provided by financing activities | (19.1 | ) | (1.2 | ) | 2,133.4 | (4.5 | ) | (15.6 | ) | |||||||||||

| Effect of exchange rate changes on cash | 2.6 | 3.8 | 5.6 | (1.3 | ) | (0.3 | ) | |||||||||||||

| Net (decrease) increase in cash and cash equivalents | $ | (50.3 | ) | $ | (0.2 | ) | $ | 68.7 | $ | 25.6 | $ | (29.4 | ) | |||||||

| Other financial data: | ||||||||||||||||||||

| Depreciation and amortization | $ | 46.3 | $ | 52.4 | $ | 115.2 | $ | 179.8 | $ | 28.2 | $ | 105.2 | ||||||||

| Capital expenditures | 36.0 | 34.3 | 112.8 | 211.5 | 13.3 | 76.8 | ||||||||||||||

| Ratio of earnings to fixed charges(6) | — | — | — | — | 2.4 | x | 2.6 | x | ||||||||||||

| EBITDA(7) | 73.8 | 56.7 | 107.7 | 315.2 | 102.7 | 380.8 | ||||||||||||||

| Non-cash charges and gains included in EBITDA(8) | 74.6 | 90.4 | 138.4 | 138.4 | (8.6 | ) | (100.5 | ) | ||||||||||||

| Other special charges and gains included in EBITDA(9) | 2.0 | 2.4 | 86.3 | 86.3 | 5.1 | 13.4 | ||||||||||||||

16

| | As of December 31, 2004 | As of June 30, 2005 | ||||

|---|---|---|---|---|---|---|

| | (as restated) | | ||||

| Balance sheet data (in millions): | ||||||

| Cash and cash equivalents | $ | 111.4 | $ | 82.0 | ||

| Working capital(10) | 495.2 | 464.6 | ||||

| Property, plant and equipment, net | 1,566.8 | 1,440.6 | ||||

| Total assets | 5,386.6 | 4,920.2 | ||||

| Long-term debt(11) | 3,124.1 | 2,962.3 | ||||

| Stockholders' equity | 904.0 | 785.3 | ||||

- (1)

- As part of our impairment testing in late 2002, 2003 and 2004, we determined that there were goodwill impairments of $50.0 million, $19.3 million and $4.0 million, respectively, in our Electronics segment. We also determined that there was a property, plant and equipment impairment of $15.7 million and $7.0 million in 2003 and 2004, respectively, in our Electronics segment.

- (2)

- For the years ended December 31, 2002, 2003 and 2004 and the six months ended June 30, 2004 and 2005, interest expense, net included (losses) gains of $(11.6) million, $(16.5) million, $6.8 million, $8.6 million and $6.2 million, respectively, representing the movement in the mark-to-market valuation of our interest rate and cross-currency hedging instruments for the periods as well as $6.2 million, $4.3 million, $5.6 million, $0.9 million and $4.7 million, respectively, of amortization expense related to deferred financing costs.

- (3)

- Represents the non-cash translation impact on our euro-denominated debt resulting from the strengthening (weakening) of the euro against the U.S. dollar during the applicable periods. In the year ended December 31, 2004, this amount also included a $10.9 million mark-to-market realized loss on foreign currency derivative agreements that we entered into in connection with the Dynamit Nobel acquisition.

- (4)

- In July 2003, we wrote off $36.9 million of deferred debt issuance costs relating to our previous long-term debt that was repaid as part of the July 2003 debt refinancing. In December 2003, we expensed $1.4 million of investment banking and professional fees in connection with the December 2003 refinancing of borrowings under the then new senior secured credit facilities. In July 2004, we wrote off $1.8 million of deferred debt issuance costs relating to our previous long-term debt that was repaid as part of the acquisition financings. We wrote off $6.1 million of deferred financing costs in connection with the October 8, 2004 amendment of the secured credit facilities. In November 2004, we wrote off $17.2 million of deferred financing costs incurred in connection with the bridge loan repayments in connection with the issuance of the notes. In December 2004, we expensed $1.0 million in connection with the second amendment.

- (5)

- Represents the tax on certain assets transferred in the United Kingdom in connection with the KKR acquisition of $4.0 million plus $0.3 million related to disposal of property, plant and equipment.

- (6)

- For the purposes of computing the ratio of earnings to fixed charges, earnings represent net income before taxes and fixed charges. Fixed charges consist of interest expense, net and one-third of rental expense. Earnings were insufficient to cover fixed charges by $60.7 million, $81.5 million and $135.2 million for years ended December 31, 2002, 2003 and 2004, respectively.

- (7)

- EBITDA is defined as net income plus interest expense, net, income tax provision (benefit) and depreciation and amortization. EBITDA is not a recognized term under U.S. GAAP and is not intended to be an alternative to net (loss) income as an indicator of operating performance or to cash flows from operating activities as a measure of liquidity. Additionally, EBITDA is not

17

intended to be a measure of free cash flow for management's discretionary use, as it does not consider certain cash requirements such as interest payments, tax payments and debt service requirements.

The amounts shown for EBITDA in this prospectus differ from the amounts calculated under the definition of EBITDA used in our debt agreements. The definition of EBITDA used in our debt agreements permits further adjustments for certain cash and non-cash charges and gains; the indentures governing the notes and the 2011 notes exclude certain adjustments permitted under the senior secured credit agreement (in particular, certain non-recurring charges and business interruption costs and insurance recovery). EBITDA as adjusted is used in our debt agreements to determine compliance with financial covenants and our ability to engage in certain activities, such as incurring additional debt and making certain payments. In addition to covenant compliance, our management also uses EBITDA as adjusted, calculated using the same definition as used in our senior secured credit agreement, to assess our operating performance, and to calculate performance-based cash bonuses and determine whether certain performance-based stock options vest, as both such bonuses and options are tied to EBITDA as adjusted targets. For a discussion of the adjustments, uses and the limitations on the use of EBITDA as adjusted, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Special Note Regarding Non-GAAP Financial Measures."

The following table sets forth a reconciliation of net loss to EBITDA for the periods indicated.

| | | | | | Six Months Ended June 30, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, | Pro Forma Year Ended December 31, 2004 | |||||||||||||||||

| | 2002 | 2003 | 2004 | 2004 | 2005 | ||||||||||||||

| | ($ in millions) | ||||||||||||||||||

| Net (loss) income | $ | (55.2 | ) | $ | (72.0 | ) | $ | (148.2 | ) | $ | (122.7 | ) | $ | 25.8 | $ | 131.7 | |||

| Interest expense, net | 88.2 | 85.8 | 127.7 | 211.4 | 29.1 | 103.9 | |||||||||||||

| Income tax (benefit) provision | (5.5 | ) | (9.5 | ) | 13.0 | 46.7 | 19.6 | 41.7 | |||||||||||

| Depreciation and amortization | 46.3 | 52.4 | 115.2 | 179.8 | 28.2 | 105.2 | |||||||||||||

| EBITDA (before minority interest) | 73.8 | 56.7 | 107.7 | 315.2 | 102.7 | 382.5 | |||||||||||||

| Minority interest | — | — | — | — | — | (1.7 | ) | ||||||||||||

| EBITDA | $ | 73.8 | $ | 56.7 | $ | 107.7 | $ | 315.2 | $ | 102.7 | $ | 380.8 | |||||||

- (8)

- EBITDA, as defined above, contains the following non-cash charges and gains for which we believe adjustment is permitted under our senior secured credit agreement, each of which is described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Factors Which Affect Our Results of Operations—Special Charges":

| | | | | | Six Months Ended June 30, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, | Pro Forma Year Ended December 31, 2004 | |||||||||||||||||

| | 2002 | 2003 | 2004 | 2004 | 2005 | ||||||||||||||

| | ($ in millions) | ||||||||||||||||||

| Impairment charges | $ | 50.0 | $ | 35.0 | $ | 11.0 | $ | 11.0 | $ | — | $ | — | |||||||

| Write-off of deferred debt issuance costs | — | 36.9 | 25.1 | 25.1 | — | — | |||||||||||||

| Foreign exchange loss (gain) | 24.6 | 18.5 | 102.3 | 102.3 | (8.6 | ) | (100.5 | ) | |||||||||||

| $ | 74.6 | $ | 90.4 | $ | 138.4 | $ | 138.4 | $ | (8.6 | ) | $ | (100.5 | ) | ||||||

- (9)

- In addition to non-cash charges and gains, EBITDA contains the following other special charges and gains for which we believe adjustment is permitted under our senior secured credit agreement,

18

each of which is described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Factors Which Affect Our Results of Operations—Special Charges":

| | | | | | Six Months Ended June 30, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, | Pro Forma Year Ended December 31, 2004 | |||||||||||||||||

| | 2002 | 2003 | 2004 | 2004 | 2005 | ||||||||||||||

| | ($ in millions) | ||||||||||||||||||

| Systems/organization establishment expenses | $ | 1.6 | $ | 1.6 | $ | 4.8 | $ | 4.8 | $ | 1.0 | $ | 1.9 | |||||||

| Inventory write-up reversal | — | 0.2 | 61.1 | 61.1 | — | 3.1 | |||||||||||||

| Stamp duty tax | — | — | 4.0 | 4.0 | 4.0 | — | |||||||||||||

| Business interruption costs and insurance recovery(a) | (2.2 | ) | (4.5 | ) | — | — | — | — | |||||||||||

| Cancelled acquisition and disposal costs | 0.2 | 1.9 | 0.5 | 0.5 | 0.1 | 0.6 | |||||||||||||

| Loss on receivables sold | 1.2 | — | — | — | — | — | |||||||||||||

| Loss on disposed businesses | — | — | 0.8 | 0.8 | — | — | |||||||||||||

| Restructuring and related charges | 1.2 | 1.8 | 1.1 | 1.1 | — | 6.3 | (b) | ||||||||||||

| Costs incurred related to debt modifications | — | 1.4 | 1.0 | 1.0 | — | — | |||||||||||||

| Foreign exchange loss on foreign currency derivatives | — | — | 10.9 | 10.9 | — | — | |||||||||||||

| CCA litigation defense costs | — | — | — | — | — | 1.5 | |||||||||||||

| Other | — | — | 2.1 | 2.1 | — | — | |||||||||||||

| $ | 2.0 | $ | 2.4 | $ | 86.3 | $ | 86.3 | $ | 5.1 | $ | 13.4 | ||||||||

- (a)

- Business interruption costs and insurance recovery is not included as an adjustment under the indentures governing the notes and the 2001 notes. See "Description of the Notes—Certain Definitions—EBITDA."

- (b)

- Includes inventory writedowns of $0.5 million recorded in cost of products sold.

- (10)

- Working capital is defined as current assets less current liabilities.

- (11)

- Includes the current portion of long-term debt of $47.2 million and $65.1 million as of December 31, 2004 and June 30, 2005, respectively, on an actual basis.

19

Dynamit Nobel Summary Financial Data

The summary financial data of Dynamit Nobel presented below as of and for the years ended September 30, 2001 and 2002, and the three months ended December 31, 2002 and the year ended December 31, 2003 have been derived from its audited combined financial statements included elsewhere in this prospectus. The summary financial data of Dynamit Nobel presented below for the six months ended June 30, 2003 and as of and for the six months ended June 30, 2004 have been derived from its unaudited condensed combined financial statements, included elsewhere in this prospectus. In the opinion of our management, the unaudited financial statements have been prepared on a basis consistent with the audited financial statements and include all adjustments, which are normally recurring adjustments, necessary for a fair presentation of the results of operations for the periods presented. Results of operations for the interim periods are not necessarily indicative of the results that might be expected for any other interim period or for an entire year.

In September 2002, Dynamit Nobel changed its fiscal year end from September 30 to December 31, which resulted in a short financial year from October 1, 2002 to December 31, 2002.

The summary financial data presented below should be read together with Dynamit Nobel's combined financial statements and the notes to those statements and "Management's Discussion and Analysis of Financial Condition and Results of Operations" included elsewhere in this prospectus.

| | Year Ended September 30, | | | Six Months Ended June 30, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Three Months Ended December 31, 2002 | Year Ended December 31, 2003 | |||||||||||||||||

| | 2001 | 2002 | 2003 | 2004 | |||||||||||||||

| | ($ in millions) | ||||||||||||||||||

| Statement of operations data: | |||||||||||||||||||

| Net sales | $ | 1,446.5 | $ | 1,421.9 | $ | 336.9 | $ | 1,595.9 | $ | 800.0 | $ | 885.5 | |||||||

| Cost of sales | (949.5 | ) | (914.7 | ) | (219.3 | ) | (1,060.0 | ) | (524.9 | ) | (587.0 | ) | |||||||

| Gross profit | 497.0 | 507.2 | 117.6 | 535.9 | 275.1 | 298.5 | |||||||||||||

| Operating expenses(a) | (286.4 | ) | (300.9 | ) | (84.6 | ) | (353.2 | ) | (171.3 | ) | (194.3 | ) | |||||||

| Operating income | 210.6 | 206.3 | 33.0 | 182.7 | 103.8 | 104.2 | |||||||||||||

| Other income, net(a) | 4.9 | 3.8 | 2.2 | 5.8 | 0.8 | 0.5 | |||||||||||||

| Interest expense, net | (24.2 | ) | (22.8 | ) | (6.9 | ) | (25.2 | ) | (13.6 | ) | (14.4 | ) | |||||||

| Income before taxes and other adjustments | 191.3 | 187.3 | 28.3 | 163.3 | 91.0 | 90.3 | |||||||||||||

| Income tax provision | 94.1 | 80.4 | 11.8 | 61.7 | 34.2 | 32.1 | |||||||||||||

| Other adjustments(1) | 1.3 | 3.4 | 0.3 | (0.7 | ) | 1.1 | — | ||||||||||||

| Net income | $ | 98.5 | $ | 110.3 | $ | 16.8 | $ | 100.9 | $ | 57.9 | $ | 58.2 | |||||||

| Cash flow data: | |||||||||||||||||||

| Net cash provided by (used in) operating activities | $ | 128.0 | $ | 142.1 | $ | 42.1 | $ | 267.0 | $ | 57.6 | $ | (18.2 | ) | ||||||

| Net cash used in investing activities(2) | (60.3 | ) | (62.5 | ) | (23.8 | ) | (102.7 | ) | (9.0 | ) | (45.0 | ) | |||||||

| Net cash (used in) provided by financing activities(3) | (82.3 | ) | (95.9 | ) | (30.9 | ) | (196.8 | ) | (56.6 | ) | 71.7 | ||||||||

| Exchange-rate-related change in cash and cash equivalents | 8.3 | 15.1 | 10.2 | 33.3 | 6.1 | (6.9 | ) | ||||||||||||

| Net (decrease) increase in cash and cash equivalents | $ | (6.3 | ) | $ | (1.2 | ) | $ | (2.4 | ) | $ | 0.8 | $ | (1.9 | ) | $ | 1.6 | |||

20

| Other financial data: | |||||||||||||||||||

| Depreciation and amortization | $ | 103.3 | $ | 83.1 | $ | 21.1 | $ | 94.6 | $ | 45.7 | $ | 52.0 | |||||||

| Capital expenditures | 125.1 | 112.0 | 26.3 | 122.0 | 39.4 | 58.2 | |||||||||||||

| EBITDA(4) | 320.1 | 295.8 | 56.6 | 282.7 | 151.7 | 156.7 | |||||||||||||

| Non-cash charges and gains included in EBITDA(5) | (2.7 | ) | (3.4 | ) | (1.6 | ) | (2.4 | ) | (6.0 | ) | (1.1 | ) | |||||||

| Other special charges and gains included in EBITDA(6) | (58.2 | ) | (20.4 | ) | 2.6 | 31.8 | 8.3 | 2.7 |

| | As of September 30, | As of December 31, | | |||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | As of June 30, 2004 | |||||||||||||||

| | 2001 | 2002 | 2002 | 2003 | ||||||||||||

| | ($ in millions) | |||||||||||||||

| Balance sheet data: | ||||||||||||||||

| Cash and cash equivalents | $ | 10.7 | $ | 9.5 | $ | 7.0 | $ | 7.8 | $ | 9.5 | ||||||

| Working capital deficiency(7) | (67.9 | ) | (139.6 | ) | (56.2 | ) | (103.6 | ) | (153.2 | ) | ||||||

| Property, plant and equipment | 663.3 | 723.9 | 766.2 | 918.2 | 886.2 | |||||||||||

| Total assets | 1,596.7 | 1,732.5 | 2,144.7 | 2,431.6 | 2,430.7 | |||||||||||

| Long-term debt(8) | 137.9 | 94.1 | 201.6 | 231.6 | 203.3 | |||||||||||

| Investment by mg technologies ag | 599.8 | 602.6 | 966.3 | 1,036.7 | 1,037.8 | |||||||||||

- (a)

- Certain amounts have been reclassified to conform to Rockwood's historical presentation.

- (1)

- Other adjustments include earnings (loss) from discontinued operations, cumulative effects from changes in accounting principles and minority interest.

- (2)

- Net cash used in investing activities primarily represents capital expenditures, net of proceeds from dispositions of businesses and fixed assets.

- (3)

- Net cash (used in) provided by financing activities primarily represents net changes in external debt and the net change in intercompany balances with Dynamit Nobel's parent, mg technologies ag.

- (4)

- EBITDA is defined as net income plus interest expense, net, income tax provision (benefit) and depreciation and amortization. EBITDA is not a recognized term under U.S. GAAP and is not intended to be an alternative to net (loss) income as an indicator of operating performance or to cash flows from operating activities as a measure of liquidity. Additionally, EBITDA is not intended to be a measure of free cash flow for management's discretionary use, as it does not consider certain cash requirements such as interest payments, tax payments and debt service requirements.

The amounts shown for EBITDA in this prospectus differ from the amounts calculated under the definition of EBITDA used in our debt agreements. The definition of EBITDA used in our debt agreements permits further adjustments for certain cash and non-cash charges and gains; the indentures governing the 2011 notes and 2014 notes exclude certain adjustments permitted under the senior secured credit agreement. EBITDA as adjusted is used in our debt agreements to determine compliance with financial covenants and our ability to engage in certain activities, such as incurring additional debt and making certain payments. In addition to covenant compliance, our management also uses EBITDA as adjusted, calculated using the same definition as used in our senior secured credit agreement, to assess our operating performance, and to calculate performance-based cash bonuses and determine whether certain performance-based stock options vest, as both such bonuses and options are tied to EBITDA as adjusted targets. For a discussion of the adjustments, uses and the limitations on the use of EBITDA as adjusted, see "Management's

21

Discussion and Analysis of Financial Condition and Results of Operations—Special Note Regarding Non-GAAP Financial Measures."

The following is a reconciliation of Dynamit Nobel's net income to EBITDA:

| | Year Ended September 30, | | | Six Months Ended June 30, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Three Months Ended December 31, 2002 | | ||||||||||||||||

| | Year Ended December 31, 2003 | |||||||||||||||||

| | 2001 | 2002 | 2003 | 2004 | ||||||||||||||

| | ($ in millions) | |||||||||||||||||

| Net income | $ | 98.5 | $ | 110.3 | $ | 16.8 | $ | 100.9 | $ | 57.9 | $ | 58.2 | ||||||

| Interest expense, net | 24.2 | 22.8 | 6.9 | 25.2 | 13.6 | 14.4 | ||||||||||||

| Income tax provision | 94.1 | 80.4 | 11.9 | 61.7 | 34.2 | 32.1 | ||||||||||||

| Depreciation and amortization | 103.3 | 83.1 | 21.1 | 94.6 | 45.7 | 52.0 | ||||||||||||

| EBITDA | 320.1 | 296.6 | 56.7 | 282.4 | 151.4 | 156.7 | ||||||||||||

| Minority interest | — | (0.8 | ) | (0.1 | ) | 0.3 | 0.3 | — | ||||||||||

| EBITDA (before minority interest) | $ | 320.1 | $ | 295.8 | $ | 56.6 | $ | 282.7 | $ | 151.7 | $ | 156.7 | ||||||

- (5)

- EBITDA, as defined above, contains the following non-cash charges and gains for which we believe adjustment is permitted under our senior secured credit agreement, which are described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Factors Which Affect Our Results of Operations—Special Charges":

| | Year Ended September 30, | | | Six Months Ended June 30, | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Three Months Ended December 31, 2002 | | |||||||||||||||||

| | Year Ended December 31, 2003 | ||||||||||||||||||

| | 2001 | 2002 | 2003 | 2004 | |||||||||||||||

| | ($ in millions) | ||||||||||||||||||

| Earnings from discontinued operations | $ | (1.3 | ) | $ | (2.6 | ) | $ | (0.2 | ) | $ | (1.4 | ) | $ | (1.4 | ) | $ | — | ||

| Cumulative effect of change in accounting principle | — | — | — | 1.8 | — | — | |||||||||||||

| Foreign exchange loss (gain) | (1.4 | ) | (0.8 | ) | (1.4 | ) | (2.8 | ) | (4.6 | ) | (1.1 | ) | |||||||

| $ | (2.7 | ) | $ | (3.4 | ) | $ | (1.6 | ) | $ | (2.4 | ) | $ | (6.0 | ) | $ | (1.1 | ) | ||

- (6)

- In addition to non-cash charges and gains for which we believe adjustment is permitted under our senior secured credit agreement, our EBITDA contains the following other special charges and gains, which are described under "Management's Discussion and Analysis of Financial Condition and Results of Operations—Factors Which Affect Our Results of Operations—Special Charges":

| | Year Ended September 30, | | | Six Months Ended June 30, | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Three Months Ended December 31, 2002 | Year Ended December 31, 2003 | ||||||||||||||||

| | 2001 | 2002 | 2003 | 2004 | ||||||||||||||

| | ($ in millions) | |||||||||||||||||

| Non-recurring charges(a) | $ | (0.3 | ) | $ | (1.9 | ) | $ | — | $ | 12.6 | $ | 5.6 | $ | 2.3 | ||||

| Restructuring and closure charges | 2.4 | 3.3 | 2.6 | 14.6 | 2.2 | 0.4 | ||||||||||||

| Adjustment related to divested businesses | (60.3 | ) | (21.8 | ) | — | 4.6 | 0.5 | — | ||||||||||

| $ | (58.2 | ) | $ | (20.4 | ) | $ | 2.6 | $ | 31.8 | $ | 8.3 | $ | 2.7 | |||||

- (a)

- These non-recurring charges are not included as an adjustment under the indentures governing the notes and the 2011 notes. See "Description of the Notes—Certain Definitions—EBITDA."

- (7)

- Working capital is defined as current assets less current liabilities.

- (8)

- Excludes the current portion of long-term debt.

22

You should carefully consider these risk factors in evaluating our business. In addition to the following risks, there may also be risks that we do not yet know of or that we currently think are immaterial that may also affect our business. If any of the following risks occur, our business, results of operation or financial condition could be adversely affected.

Risk Factors Related to the Exchange Offer and the Exchange Notes