UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number | 811-21820 |

|

Eaton Vance Credit Opportunities Fund |

(Exact name of registrant as specified in charter) |

|

The Eaton Vance Building, 255 State Street, Boston, Massachusetts | | 02109 |

(Address of principal executive offices) | | (Zip code) |

|

Alan R. Dynner |

The Eaton Vance Building, 255 State Street, Boston, Massachusetts 02109 |

(Name and address of agent for service) |

|

Registrant’s telephone number, including area code: | (617) 482-8260 | |

|

Date of fiscal year end: | April 30 | |

|

Date of reporting period: | October 31, 2006 | |

| | | | | | |

Item 1. Reports to Stockholders

Semiannual Report October 31, 2006

EATON VANCE

CREDIT

OPPORTUNITIES

FUND

IMPORTANT NOTICES REGARDING PRIVACY,

DELIVERY OF SHAREHOLDER DOCUMENTS,

PORTFOLIO HOLDINGS AND PROXY VOTING

Privacy. The Eaton Vance organization is committed to ensuring your financial privacy. Each of the financial institutions identified below has in effect the following policy ("Privacy Policy") with respect to nonpublic personal information about its customers:

• Only such information received from you, through application forms or otherwise, and information about your Eaton Vance fund transactions will be collected. This may include information such as name, address, social security number, tax status, account balances and transactions.

• None of such information about you (or former customers) will be disclosed to anyone, except as permitted by law (which includes disclosure to employees necessary to service your account). In the normal course of servicing a customer's account, Eaton Vance may share information with unaffiliated third parties that perform various required services such as transfer agents, custodians and broker/dealers.

• Policies and procedures (including physical, electronic and procedural safeguards) are in place that are designed to protect the confidentiality of such information.

• We reserve the right to change our Privacy Policy at any time upon proper notification to you. Customers may want to review our Policy periodically for changes by accessing the link on our homepage: www.eatonvance.com.

Our pledge of privacy applies to the following entities within the Eaton Vance organization: the Eaton Vance Family of Funds, Eaton Vance Management, Eaton Vance Investment Counsel, Boston Management and Research, and Eaton Vance Distributors, Inc.

In addition, our Privacy Policy only applies to those Eaton Vance customers who are individuals and who have a direct relationship with us. If a customer's account (i.e., fund shares) is held in the name of a third-party financial adviser/broker-dealer, it is likely that only such adviser's privacy policies apply to the customer. This notice supersedes all previously issued privacy disclosures.

For more information about Eaton Vance's Privacy Policy, please call 1-800-262-1122.

Delivery of Shareholder Documents. The Securities and Exchange Commission (the "SEC") permits funds to deliver only one copy of shareholder documents, including prospectuses, proxy statements and shareholder reports, to fund investors with multiple accounts at the same residential or post office box address. This practice is often called "householding" and it helps eliminate duplicate mailings to shareholders.

Eaton Vance, or your financial adviser, may household the mailing of your documents indefinitely unless you instruct Eaton Vance, or your financial adviser, otherwise.

If you would prefer that your Eaton Vance documents not be householded, please contact Eaton Vance at 1-800-262-1122, or contact your financial adviser.

Your instructions that householding not apply to delivery of your Eaton Vance documents will be effective within 30 days of receipt by Eaton Vance or your financial adviser.

Portfolio Holdings. Each Eaton Vance Fund and its underlying Portfolio (if applicable) will file a schedule of its portfolio holdings on Form N-Q with the SEC for the first and third quarters of each fiscal year. The Form N-Q will be available on the Eaton Vance website www.eatonvance.com, by calling Eaton Vance at 1-800-262-1122 or in the EDGAR database on the SEC's website at www.sec.gov. Form N-Q may also be reviewed and copied at the SEC's public reference room in Washington, D.C. (call 1-800-732-0330 for information on the operation of the public reference room).

Proxy Voting. From time to time, funds are required to vote proxies related to the securities held by the funds. The Eaton Vance Funds or their underlying Portfolios (if applicable) vote proxies according to a set of policies and procedures approved by the Funds' and Portfolios' Boards. You may obtain a description of these policies and procedures and information on how the Funds or Portfolios voted proxies relating to portfolio securities during the most recent 12 month period ended June 30, without charge, upon request, by calling 1-800-262-1122. This description is also available on the SEC's website at www.sec.gov.

Eaton Vance Credit Opportunities Fund as of October 31, 2006

I N V E S T M E N T U P D A T E

The Fund

Performance for the Period

· Based on share price, Eaton Vance Credit Opportunities Fund, a closed-end fund traded on the New York Stock Exchange, had a total return of 7.18% for the period from inception on May 31, 2006, through October 31, 2006. That return was the result of an increase in share price to $19.80 on October 31, 2006, from $19.10 (offering price of $20 per share, less all commissions) on May 31, 2006 and the reinvestment of $0.638 in dividends.(1)

· Based on net asset value (NAV), the Fund had a total return of 3.07% for the period from inception on May 31, 2006, through October 31, 2006. That return was the result of a decrease in NAV to $19.04 on October 31, 2006, from $19.10 (offering price of $20 per share, less all commissions) on May 31, 2006, and the reinvestment of all distributions.(1)

· Based on its October 2006 monthly dividend payment of $0.16 and a closing share price of $19.80, the Fund had a market yield of 9.70%.(2)

· For performance comparison, the S&P/LSTA Leveraged Loan Index – an unmanaged index of U.S. dollar-denominated leveraged loans – had a total return of 2.70% for the period from the Fund’s inception on May 31, 2006, through October 31, 2006.(3) The Lipper High Current Yield Funds Classification – the Fund’s peer group – had an average total return of 4.89% for the same period.(3)

The Fund’s Investments

· The Fund’s loan investments included 141 borrowers at October 31, 2006, with no industry constituting more than 8.0% of the Fund’s total investments. Automotive, cable and satellite television, healthcare, leisure goods/activities/movies and business equipment and services were the largest industry weightings.(4)

· The loan market enjoyed relatively stable fundamentals during the period. Technical factors have come more into balance, as record new issuance from strong merger activity has met robust investor demand. As a result, credit spreads have stabilized after a period during which they had narrowed. The Fund also benefited from an increase in the London Inter-Bank Offered Rate (LIBOR) – the benchmark over which loan interest rates are typically set – which rose in response to a rate hike in late June from the Federal Reserve.

· In its initial months of operation, the Fund maintained a somewhat defensive credit posture. Accordingly, the Fund limited its high yield bond exposure in favor of second lien loans – senior floating-rate loans that, in the event of bankruptcy, are paid after first lien lenders but before bondholders and general creditors. Given a slighted inverted yield curve environment, second lien loans offered a yield advantage over high-yield bonds, because LIBOR rates were higher than 10-year Treasury bonds rates, over which most high-yield bonds are quoted.

· The Fund had an 18% exposure to European loans at October 31, 2006. The European loans increased the Fund’s investment universe, presenting further opportunities for diversification. In addition, because European spreads were slightly wider than the U.S.market’s, European exposure provided selected opportunities for yield enhancement. All of the Fund’s foreign loans were either dollar-denominated or hedged to help protect against foreign currency risk.

· At October 31, 2006, the Fund had leverage in the amount of approximately 39.4% of the Fund’s total assets. The Fund employs leverage though the issuance of Auction Preferred Shares (“APS”) and participation in a line of credit.(5) Use of financial leverage creates an opportunity for increased income but, at the same time, creates special risks (including the likelihood of greater volatility of net asset value and market price of common shares). The cost of the Fund’s APS and borrowings rises and falls with changes in short-term interest rates. Such increases/decreases in cost of the Fund’s APS and borrowings may be offset by increased/decreased income from the Fund’s senior loan investments.

The views expressed in this report are those of the portfolio managers and are current only through the end of the period of the report as stated on the cover. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied on as investment advice and, because investment decisions for an Eaton Vance fund are based on many factors, may not be relied on as an indication of trading intent on behalf of any Eaton Vance fund.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or share price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

(1) Performance results reflect the effect of leverage resulting from the Fund’s issuance of Auction Preferred Shares and its participation in a line of credit.

(2) The Fund’s market yield is calculated by dividing the most recent dividend per share by the share price at the end of the period and annualizing the result.

(3) It is not possible to invest directly in an Index or a Lipper Classification. The Index’s total return does not reflect the commissions or expenses that would have been incurred if an investor individually purchased or sold the loans represented in the Index. Unlike the Fund, the Index’s return does not reflect the effect of leverage, such as the issuance of Auction Preferred Shares. The Lipper average is the average total return, at net asset value, of the funds that are in the same Lipper Classification as the Fund. Lipper Classifications may include leveraged and unleveraged funds.

(4) Holdings and industry weightings are subject to change due to active management.

(5) In the event of a rise in long-term interest rates, the value of the Fund’s investment portfolio could decline, which would reduce the asset coverage for its Auction Preferred Shares.

Fund shares are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. Shares are subject to investment risks, including possible loss of principal invested.

1

Eaton Vance Credit Opportunities Fund as of October 31, 2006

P E R F O R M A N C E

Performance(1)

Average Annual Total Return (by share price, NYSE) | | | |

Life of Fund (5/31/06) | | 7.18 | % |

| | | |

Average Annual Total Return (at net asset value) | | | |

Life of Fund (5/31/06) | | 3.07 | % |

(1) Returns are historical and are calculated by determining the percentage change in share price or net asset value with all distributions reinvested. The Fund’s performance at market share price will differ from its results at NAV. Although share price performance generally reflects investment results over time, during shorter periods, returns at share price can also be affected by factors such as changing perceptions about the Fund, market conditions, fluctuations in supply and demand for the Fund’s shares, or changes in Fund distributions. Performance results reflect the effect of leverage resulting from the Fund’s issuance of Auction Preferred Shares and its participation in a line of credit. In the event of a rise in long-term interest rates, the value of the Fund’s investment portfolio could decline, which would reduce the asset coverage for its Auction Preferred Shares.

Past performance is no guarantee of future results. Returns are historical and are calculated by determining the percentage change in net asset value or share price (as applicable) with all distributions reinvested. Investment return and principal value will fluctuate so that shares, when sold, may be worth more or less than their original cost. Performance is for the stated time period only; due to market volatility, the Fund’s current performance may be lower or higher than the quoted return. For performance as of the most recent month end, please refer to www.eatonvance.com.

Diversification by Industries(2)

By total investments

Automotive | | 7.1 | % |

Cable & Satellite Television | | 7.0 | |

Health Care | | 6.4 | |

Leisure Goods/Activities/Movies | | 6.4 | |

Business Equip. & Services | | 6.1 | |

Electronics/Electrical | | 5.3 | |

Oil & Gas | | 5.2 | |

Telecommunications | | 5.2 | |

Lodging & Casinos | | 4.2 | |

Radio & Television | | 4.0 | |

Chemicals & Plastics | | 3.9 | |

Food Products | | 3.6 | |

Building & Development | | 3.5 | |

Retailers (Except Food & Drug) | | 3.2 | |

Industrial Equipment | | 2.9 | |

Financial Intermediaries | | 2.5 | |

Containers & Glass Products | | 2.5 | |

Air Transport | | 2.3 | |

Conglomerates | | 2.2 | |

Publishing | | 2.2 | |

Utilities | | 2.0 | |

Clothing/Textiles | | 1.5 | |

Food Service | | 1.5 | |

Forest Products | | 1.5 | |

Food/Drug Retailers | | 1.0 | |

Nonferrous Metals/Minerals | | 1.0 | |

Aerospace & Defense | | 0.9 | |

Ecological Services & Equip. | | 0.9 | |

Surface Transport | | 0.8 | |

Beverage & Tobacco | | 0.8 | |

Home Furnishings | | 0.7 | |

Cosmetics/Toiletries | | 0.7 | |

Insurance | | 0.5 | |

Equipment Leasing | | 0.4 | |

Drugs | | 0.3 | |

(2) Reflects the Fund’s investments as of October 31, 2006. Industries are shown as a percentage of the Fund’s total loan and corporate bond and note investments. Portfolio information may not be representative of current or future investments and may change due to active management.

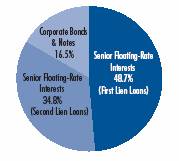

Diversification by Sectors(3)

By total investments

(3) Diversification by Sectors reflects the Fund’s investments as of October 31, 2006. Sectors are shown as a pecentage of the Fund’s total investments. Fund statistics may not be representative of the Fund’s current or future investments and may change due to active management.

2

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited)

| Senior, Floating Rate Interests — 136.2%(1) | | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Aerospace and Defense — 1.5% | | | |

| Forgins International Holdings | | | |

| $ | 951,950 | | | Term Loan, 9.71%, Maturing February 11, 2015 | | $ | 960,677 | | |

| Wesco Aircraft Hardware Corp. | | | |

| | 1,000,000 | | | Term Loan, 11.13%, Maturing September 29, 2014 | | | 1,015,000 | | |

| | | | | | | $ | 1,975,677 | | |

| Air Transport — 3.7% | | | |

| Airport Development and Investment | | | |

| GBP | 1,000,000 | | | Term Loan, 9.12%, Maturing April 7, 2011 | | $ | 1,911,833 | | |

| Delta Air Lines, Inc. | | | |

| | 1,000,000 | | | Term Loan, 10.02%, Maturing March 16, 2008 | | | 1,021,019 | | |

| Northwest Airlines, Inc. | | | |

| | 1,000,000 | | | DIP Loan, 7.90%, Maturing August 21, 2008 | | | 1,004,375 | | |

| United Airlines, Inc. | | | |

| | 124,375 | | | Term Loan, 9.13%, Maturing February 1, 2012 | | | 126,552 | | |

| | 870,625 | | | Term Loan, 9.25%, Maturing February 1, 2012 | | | 885,861 | | |

| | | | | | | $ | 4,949,640 | | |

| Automotive — 8.0% | | | |

| Axletech International Holding, Inc. | | | |

| $ | 909,091 | | | Term Loan, 11.87%, Maturing April 21, 2013 | | $ | 917,425 | | |

| Collins & Aikman Products Co. | | | |

| | 1,903,861 | | | Term Loan, 11.75%, Maturing August 31, 2009(5) | | | 692,529 | | |

| | 593,278 | | | Revolving Loan, 11.75%, Maturing August 31, 2009(5) | | | 217,288 | | |

| Dana Corp. | | | |

| | 1,000,000 | | | DIP Loan, 7.65%, Maturing April 13, 2008 | | | 1,001,500 | | |

| Dayco Products, LLC | | | |

| | 2,000,000 | | | Term Loan, 11.28%, Maturing December 31, 2011 | | | 2,046,666 | | |

| Goodyear Tire & Rubber Co. | | | |

| | 2,000,000 | | | Term Loan, 8.89%, Maturing March 1, 2011 | | | 2,029,166 | | |

| Insurance Auto Auctions, Inc. | | | |

| | 445,652 | | | Term Loan, 7.54%, Maturing May 19, 2012(2) | | | 448,437 | | |

| R.J. Tower Corp. | | | |

| | 1,000,000 | | | DIP Revolving Loan, 8.94%, Maturing February 2, 2007 | | | 970,625 | | |

| Trimas Corp. | | | |

| | 281,250 | | | Term Loan, 8.13%, Maturing August 2, 2011 | | | 283,359 | | |

| | 1,218,750 | | | Term Loan, 8.25%, Maturing August 2, 2013 | | | 1,227,891 | | |

| Vanguard Car Rental USA | | | |

| | 935,000 | | | Term Loan, 8.35%, Maturing June 14, 2013 | | | 942,947 | | |

| | | | | | | $ | 10,777,833 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Beverage and Tobacco — 1.3% | | | |

| Le-Nature's, Inc. | | | |

| $ | 1,000,000 | | | Term Loan, 9.39%, Maturing March 1, 2011(3) | | $ | 850,000 | | |

| Sunny Delight Beverages Co. | | | |

| | 957,447 | | | Term Loan, 11.39%, Maturing August 20, 2010 | | | 946,975 | | |

| | | | | | | $ | 1,796,975 | | |

| Building and Development — 5.4% | | | |

| LNR Property Corp. | | | |

| $ | 1,000,000 | | | Term Loan, 8.22%, Maturing July 3, 2011 | | $ | 1,004,896 | | |

| Panolam Industries Holdings, Inc. | | | |

| | 1,544,130 | | | Term Loan, 8.12%, Maturing September 30, 2012 | | | 1,551,851 | | |

| Rubicon GSA II, LLC | | | |

| | 1,000,000 | | | Term Loan, 8.07%, Maturing July 31, 2008 | | | 1,000,000 | | |

| TE / Tousa Senior, LLC | | | |

| | 1,000,000 | | | Term Loan, 8.25%, Maturing August 1, 2008 | | | 769,500 | | |

| TRU 2005 RE Holding Co. | | | |

| | 2,000,000 | | | Term Loan, 8.32%, Maturing December 9, 2008 | | | 2,006,250 | | |

| United Subcontractors, Inc. | | | |

| | 1,000,000 | | | Term Loan, 12.86%, Maturing June 27, 2013 | | | 970,000 | | |

| | | | | | | $ | 7,302,497 | | |

| Business Equipment and Services — 8.6% | | | |

| Affinion Group, Inc. | | | |

| $ | 1,950,000 | | | Term Loan, 8.17%, Maturing October 17, 2012 | | $ | 1,963,102 | | |

| Allied Security Holdings, LLC | | | |

| | 995,455 | | | Term Loan, 8.37%, Maturing June 30, 2010 | | | 1,004,165 | | |

| Audatex North America, Inc. | | | |

| EUR | 1,000,000 | | | Term Loan, 9.13%, Maturing January 13, 2013 | | | 1,307,063 | | |

| Language Line, Inc. | | | |

| | 555,079 | | | Term Loan, 9.63%, Maturing June 11, 2011 | | | 559,156 | | |

| N.E.W. Holdings I, LLC | | | |

| | 200,000 | | | Term Loan, 12.35%, Maturing February 8, 2014 | | | 204,000 | | |

| Nielsen Finance, LLC | | | |

| | 1,000,000 | | | Term Loan, 8.19%, Maturing August 9, 2013 | | | 1,004,766 | | |

| Quantum Corp. | | | |

| | 500,000 | | | Term Loan, 12.94%, Maturing August 22, 2013 | | | 498,125 | | |

| Quintiles Transnational Corp. | | | |

| | 2,000,000 | | | Term Loan, 9.37%, Maturing March 31, 2014 | | | 2,036,562 | | |

| Sungard Data Systems, Inc. | | | |

| | 989,924 | | | Term Loan, 8.00%, Maturing February 11, 2013 | | | 1,000,401 | | |

| TDS Investor Corp. | | | |

| | 910,778 | | | Term Loan, 8.37%, Maturing August 23, 2013 | | | 914,682 | | |

| | 89,222 | | | Term Loan, 8.37%, Maturing August 23, 2013 | | | 89,604 | | |

See notes to financial statements

3

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Business Equipment and Services (continued) | | | |

| Western Inventory Services | | | |

| $ | 975,016 | | | Term Loan, 7.82%, Maturing March 31, 2011 | | $ | 979,891 | | |

| | | | | | | $ | 11,561,517 | | |

| Cable and Satellite Television — 9.7% | | | |

| Atlantic Broadband Finance, LLC | | | |

| $ | 750,000 | | | Term Loan, 0.00%, Maturing February 10, 2011(2) | | $ | 760,312 | | |

| Cequel Communications, LLC | | | |

| | 2,010,089 | | | Term Loan, 11.49%, Maturing May 5, 2014 | | | 1,997,944 | | |

| Charter Communications Operating, LLC | | | |

| | 1,006,209 | | | Term Loan, 8.01%, Maturing April 28, 2013 | | | 1,016,019 | | |

| Insight Midwest Holdings, LLC | | | |

| | 312,500 | | | Term Loan, 0.00%, Maturing April 6, 2014(2) | | | 314,966 | | |

| | 937,500 | | | Term Loan, 7.57%, Maturing April 6, 2014 | | | 944,897 | | |

| NTL Investment Holdings, Ltd. | | | |

| GBP | 1,000,000 | | | Term Loan, 7.64%, Maturing March 30, 2013 | | | 1,933,475 | | |

| Persona Communications Corp. | | | |

| | 1,000,000 | | | Term Loan, 11.37%, Maturing April 12, 2014 | | | 1,006,250 | | |

| PKS Media (Netherlands) B.V. | | | |

| EUR | 1,000,000 | | | Term Loan, 5.74%, Maturing October 5, 2013 | | | 1,294,570 | | |

| EUR | 1,000,000 | | | Term Loan, 6.24%, Maturing October 5, 2014 | | | 1,300,654 | | |

| UPC Broadband Holding B.V. | | | |

| EUR | 441,667 | | | Term Loan, 5.51%, Maturing March 31, 2013 | | | 564,337 | | |

| EUR | 500,000 | | | Term Loan, 5.51%, Maturing December 31, 2013 | | | 638,968 | | |

| Ypso Holding S.A. | | | |

| EUR | 320,000 | | | Term Loan, 8.09%, Maturing July 28, 2014 | | | 400,373 | | |

| EUR | 680,000 | | | Term Loan, 8.09%, Maturing July 28, 2015 | | | 850,792 | | |

| | | | | | | $ | 13,023,557 | | |

| Chemicals and Plastics — 5.9% | | | |

| Brenntag Holding GmbH and Co. KG | | | |

| $ | 2,000,000 | | | Term Loan, 12.08%, Maturing December 23, 2015 | | $ | 2,049,062 | | |

| Cognis Deutschland Eins GmbH | | | |

| | 500,000 | | | Term Loan, 10.03%, Maturing November 11, 2009 | | | 512,500 | | |

| Ineos Group | | | |

| EUR | 2,000,000 | | | Term Loan, 7.28%, Maturing December 14, 2012 | | | 2,598,490 | | |

| Lucite International Group Holdings | | | |

| | 259,542 | | | Term Loan, 0.00%, Maturing July 7, 2013(2) | | | 261,735 | | |

| | 738,607 | | | Term Loan, 8.07%, Maturing July 7, 2013 | | | 744,848 | | |

| Solo Cup Co. | | | |

| | 750,000 | | | Term Loan, 11.37%, Maturing March 31, 2012 | | | 769,687 | | |

| Solutia, Inc. | | | |

| | 1,000,000 | | | DIP Loan, 8.96%, Maturing March 31, 2007 | | | 1,003,750 | | |

| | | | | | | $ | 7,940,072 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Clothing / Textiles — 1.5% | | | |

| Hanesbrands, Inc. | | | |

| $ | 2,000,000 | | | Term Loan, 9.19%, Maturing March 5, 2014 | | $ | 2,052,858 | | |

| | | | | | | $ | 2,052,858 | | |

| Conglomerates — 3.5% | | | |

| Euramax International, Inc. | | | |

| $ | 1,000,000 | | | Term Loan, 12.37%, Maturing June 28, 2013 | | $ | 1,007,500 | | |

| Johnson Diversey, Inc. | | | |

| | 455,341 | | | Term Loan, 7.97%, Maturing December 16, 2011 | | | 459,539 | | |

| Polymer Group, Inc. | | | |

| | 994,987 | | | Term Loan, 7.61%, Maturing November 22, 2012 | | | 997,060 | | |

| PP Acquisition Corp. | | | |

| EUR | 1,000,000 | | | Term Loan, 6.37%, Maturing November 12, 2011 | | | 1,281,136 | | |

| RGIS Holdings, LLC | | | |

| | 995,065 | | | Term Loan, 7.87%, Maturing February 15, 2013 | | | 994,755 | | |

| | | | | | | $ | 4,739,990 | | |

| Containers and Glass Products — 3.0% | | | |

| Bluegrass Container Co. | | | |

| $ | 484,848 | | | Term Loan, 10.32%, Maturing December 30, 2013 | | $ | 491,440 | | |

| | 1,515,152 | | | Term Loan, 10.32%, Maturing December 30, 2013 | | | 1,535,748 | | |

| JSG Acquisitions | | | |

| EUR | 500,000 | | | Term Loan, 5.96%, Maturing December 31, 2014 | | | 642,658 | | |

| EUR | 500,000 | | | Term Loan, 6.46%, Maturing December 31, 2014 | | | 645,514 | | |

| Kranson Industries, Inc. | | | |

| | 700,000 | | | Term Loan, 8.17%, Maturing July 31, 2013 | | | 703,937 | | |

| | | | | | | $ | 4,019,297 | | |

| Cosmetics / Toiletries — 1.0% | | | |

| American Safety Razor Co. | | | |

| $ | 1,000,000 | | | Term Loan, 11.72%, Maturing July 31, 2014 | | $ | 1,020,000 | | |

| Revlon Consumer Products Corp. | | | |

| | 334,867 | | | Term Loan, 11.44%, Maturing July 9, 2010 | | | 343,796 | | |

| | | | | | | $ | 1,363,796 | | |

| Drugs — 0.6% | | | |

| Warner Chilcott Corp. | | | |

| $ | 128,049 | | | Term Loan, 7.87%, Maturing January 18, 2012 | | $ | 128,872 | | |

| | 121,324 | | | Term Loan, 7.87%, Maturing January 18, 2012 | | | 121,840 | | |

| | 24,265 | | | Term Loan, 7.87%, Maturing January 18, 2012 | | | 24,368 | | |

| | 466,396 | | | Term Loan, 7.93%, Maturing January 18, 2012 | | | 469,394 | | |

| | | | | | | $ | 744,474 | | |

See notes to financial statements

4

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Ecological Services and Equipment — 1.4% | | | |

| PHS Group PIC | | | |

| GBP | 500,000 | | | Term Loan, 7.69%, Maturing July 5, 2010 | | $ | 958,393 | | |

| GBP | 500,000 | | | Term Loan, 8.19%, Maturing July 5, 2011 | | | 963,876 | | |

| | | | | | | $ | 1,922,269 | | |

| Electronics / Electrical — 8.4% | | | |

| Advanced Micro Devices, Inc. | | | |

| $ | 625,000 | | | Term Loan, 7.57%, Maturing December 31, 2013 | | $ | 625,000 | | |

| Aspect Software, Inc. | | | |

| | 2,000,000 | | | Term Loan, 12.38%, Maturing July 11, 2013 | | | 2,008,334 | | |

| Infor Enterprise Solutions Holdings | | | |

| | 1,314,286 | | | Term Loan, 9.12%, Maturing July 28, 2012 | | | 1,326,059 | | |

| | 685,714 | | | Term Loan, 9.12%, Maturing July 28, 2012 | | | 691,857 | | |

| Network Solutions, LLC | | | |

| | 1,989,975 | | | Term Loan, 10.37%, Maturing January 9, 2012 | | | 2,014,850 | | |

| Open Solutions, Inc. | | | |

| | 900,000 | | | Term Loan, 11.90%, Maturing March 3, 2012 | | | 922,500 | | |

| Rayovac Corp. | | | |

| | 1,828,974 | | | Term Loan, 8.39%, Maturing February 7, 2012 | | | 1,836,486 | | |

| Telcordia Technologies, Inc. | | | |

| | 1,989,899 | | | Term Loan, 8.15%, Maturing September 15, 2012 | | | 1,919,009 | | |

| | | | | | | $ | 11,344,095 | | |

| Equipment Leasing — 0.7% | | | |

| Awas Capital, Inc. | | | |

| $ | 974,235 | | | Term Loan, 11.44%, Maturing March 22, 2013 | | $ | 983,978 | | |

| | | | | | | $ | 983,978 | | |

| Financial Intermediaries — 2.6% | | | |

| Citgo III, Ltd. | | | |

| $ | 500,000 | | | Term Loan, 8.14%, Maturing August 3, 2013 | | $ | 503,906 | | |

| | 500,000 | | | Term Loan, 8.64%, Maturing August 3, 2014 | | | 505,781 | | |

| E.A. Viner International Co. | | | |

| | 1,496,250 | | | Term Loan, 8.12%, Maturing July 31, 2013 | | | 1,511,212 | | |

| LPL Holdings, Inc. | | | |

| | 1,000,000 | | | Term Loan, 8.30%, Maturing June 30, 2013 | | | 1,012,656 | | |

| | | | | | | $ | 3,533,555 | | |

| Food Products — 5.2% | | | |

| Acosta, Inc. | | | |

| $ | 997,500 | | | Term Loan, 8.08%, Maturing July 28, 2013 | | $ | 1,007,682 | | |

| Black Lion Beverages III B.V. | | | |

| EUR | 2,000,000 | | | Term Loan, 8.31%, Maturing January 24, 2016 | | | 2,606,679 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Food Products (continued) | | | |

| Picard Surgeles S.A. | | | |

| EUR | 500,000 | | | Term Loan, 5.44%, Maturing June 4, 2014 | | $ | 643,440 | | |

| QCE Finance, LLC | | | |

| | 2,000,000 | | | Term Loan, 11.12%, Maturing November 5, 2013 | | $ | 2,033,000 | | |

| Ruby Acquisitions Ltd. | | | |

| EUR | 500,000 | | | Term Loan, 8.82%, Maturing July 5, 2015 | | | 650,938 | | |

| | | | | | | $ | 6,941,739 | | |

| Food Service — 1.6% | | | |

| SSP Financing, Ltd. | | | |

| EUR | 660,290 | | | Term Loan, 5.93%, Maturing June 15, 2014 | | | 849,784 | | |

| EUR | 145,182 | | | Term Loan, 5.93%, Maturing June 15, 2014 | | | 186,693 | | |

| EUR | 660,290 | | | Term Loan, 6.43%, Maturing June 15, 2015 | | | 853,647 | | |

| EUR | 145,182 | | | Term Loan, 6.43%, Maturing June 15, 2015 | | | 187,388 | | |

| | | | | | | $ | 2,077,512 | | |

| Food / Drug Retailers — 1.5% | | | |

| Roundy's Supermarkets, Inc. | | | |

| $ | 994,987 | | | Term Loan, 8.42%, Maturing November 3, 2011 | | $ | 1,004,067 | | |

| The Jean Coutu Group (PJC), Inc. | | | |

| | 994,472 | | | Term Loan, 7.94%, Maturing July 30, 2011 | | | 998,967 | | |

| | | | | | | $ | 2,003,034 | | |

| Forest Products — 2.2% | | | |

| Georgia-Pacific Corp. | | | |

| $ | 2,000,000 | | | Term Loan, 8.39%, Maturing December 23, 2013 | | $ | 2,028,046 | | |

| NewPage Corp. | | | |

| | 901,983 | | | Term Loan, 8.36%, Maturing May 2, 2011 | | | 913,258 | | |

| | | | | | | $ | 2,941,304 | | |

| Healthcare — 8.4% | | | |

| FHC Health Systems, Inc. | | | |

| $ | 2,000,000 | | | Term Loan, 11.40%, Maturing June 27, 2008 | | $ | 2,075,000 | | |

| HealthSouth Corp. | | | |

| | 1,995,000 | | | Term Loan, 8.62%, Maturing March 10, 2013 | | | 2,005,530 | | |

| Matria Healthcare, Inc. | | | |

| | 2,000,000 | | | Term Loan, 12.15%, Maturing January 19, 2007 | | | 2,040,000 | | |

| Medassets Inc. | | | |

| | 500,000 | | | Term Loan, 7.82%, Maturing October 23, 2013 | | | 500,000 | | |

| Moon Acquisition Co. AB | | | |

| EUR | 500,000 | | | Term Loan, 5.88%, Maturing November 4, 2013 | | | 647,023 | | |

| EUR | 1,000,000 | | | Term Loan, 5.88%, Maturing November 4, 2013 | | | 1,292,304 | | |

| EUR | 500,000 | | | Term Loan, 6.38%, Maturing November 4, 2014 | | | 649,755 | | |

See notes to financial statements

5

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Healthcare (continued) | | | |

| National Mentor Holdings, Inc. | | | |

| $ | 56,000 | | | Term Loan, 5.32%, Maturing June 29, 2013 | | $ | 56,280 | | |

| | 941,640 | | | Term Loan, 7.87%, Maturing June 29, 2013 | | | 946,348 | | |

| Sheridan Healthcare, Inc. | | | |

| | 1,000,000 | | | Term Loan, 12.37%, Maturing November 9, 2012 | | | 1,008,750 | | |

| | | | | | | $ | 11,220,990 | | |

| Home Furnishings — 1.1% | | | |

| National Bedding Co., LLC | | | |

| $ | 1,500,000 | | | Term Loan, 10.37%, Maturing August 31, 2012 | | $ | 1,514,063 | | |

| | | | | | | $ | 1,514,063 | | |

| Industrial Equipment — 4.7% | | | |

| Aearo Technologies, Inc. | | | |

| $ | 2,000,000 | | | Term Loan, 11.87%, Maturing September 24, 2013 | | $ | 2,030,000 | | |

| Gleason Corp. | | | |

| | 2,000,000 | | | Term Loan, 10.94%, Maturing December 31, 2013 | | | 2,025,000 | | |

| Prysmian S.R.L | | | |

| EUR | 500,000 | | | Term Loan, 7.88%, Maturing August 22, 2014 | | | 641,188 | | |

| EUR | 500,000 | | | Term Loan, 6.29%, Maturing August 22, 2015 | | | 644,025 | | |

| TFS Acquisition Corp. | | | |

| | 1,000,000 | | | Term Loan, 8.92%, Maturing August 11, 2013 | | | 1,007,500 | | |

| | | | | | | $ | 6,347,713 | | |

| Insurance — 0.8% | | | |

| CCC Information Services Group | | | |

| $ | 1,000,000 | | | Term Loan, 7.87%, Maturing February 10, 2013 | | $ | 1,005,625 | | |

| | | | | | | $ | 1,005,625 | | |

| Leisure Goods / Activities / Movies — 8.5% | | | |

| Bombardier Recreational Product | | | |

| $ | 2,000,000 | | | Term Loan, 8.13%, Maturing June 28, 2013 | | $ | 2,000,000 | | |

| Butterfly Wendel US, Inc. | | | |

| | 250,000 | | | Term Loan, 8.15%, Maturing June 22, 2013 | | | 253,477 | | |

| | 250,000 | | | Term Loan, 7.90%, Maturing June 22, 2014 | | | 252,227 | | |

| Carmike Cinemas, Inc. | | | |

| | 1,989,925 | | | Term Loan, 8.65%, Maturing May 19, 2012 | | | 2,011,482 | | |

| Cedar Fair, L.P. | | | |

| | 1,000,000 | | | Term Loan, 7.87%, Maturing August 30, 2012 | | | 1,012,109 | | |

| Fender Musical Instruments Co. | | | |

| | 2,000,000 | | | Term Loan, 11.38%, Maturing October 1, 2012 | | | 2,020,000 | | |

| Red Football Ltd. | | | |

| GBP | 1,500,000 | | | Term Loan, 10.08%, Maturing August 16, 2016 | | | 2,923,457 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Leisure Goods / Activities / Movies (continued) | | | |

| Six Flags Theme Parks, Inc. | | | |

| $ | 994,911 | | | Term Loan, 8.66%, Maturing June 30, 2009 | | $ | 1,007,115 | | |

| | | | | | | $ | 11,479,867 | | |

| Lodging and Casinos — 4.5% | | | |

| Bally Technologies, Inc. | | | |

| $ | 1,988,791 | | | Term Loan, 9.33%, Maturing September 5, 2009 | | $ | 1,995,836 | | |

| Fairmont Hotels and Resorts, Inc. | | | |

| | 1,153,464 | | | Term Loan, 8.57%, Maturing May 12, 2011 | | | 1,163,557 | | |

| Gala Electric Casinos, Ltd. | | | |

| GBP | 1,000,000 | | | Term Loan, 8.05%, Maturing December 12, 2014 | | | 1,933,755 | | |

| VML US Finance, LLC | | | |

| | 1,000,000 | | | Term Loan, 8.12%, Maturing May 25, 2013 | | | 1,007,734 | | |

| | | | | | | $ | 6,100,882 | | |

| Nonferrous Metals / Minerals — 1.5% | | | |

| Magnum Coal Co. | | | |

| $ | 90,909 | | | Term Loan, 8.57%, Maturing March 15, 2013 | | $ | 91,250 | | |

| | 904,545 | | | Term Loan, 8.62%, Maturing March 15, 2013 | | | 907,937 | | |

| Murray Energy Corp. | | | |

| | 1,000,000 | | | Term Loan, 13.90%, Maturing August 9, 2011 | | | 1,025,000 | | |

| | | | | | | $ | 2,024,187 | | |

| Oil and Gas — 5.5% | | | |

| Coffeyville Resources, LLC | | | |

| $ | 2,000,000 | | | Term Loan, 12.13%, Maturing June 24, 2013 | | $ | 2,063,750 | | |

| Concho Resources, Inc. | | | |

| | 1,995,000 | | | Term Loan, 9.37%, Maturing July 6, 2011(3) | | | 1,988,816 | | |

| El Paso Corp. | | | |

| | 325,000 | | | Term Loan, 5.33%, Maturing July 31, 2011(4) | | | 327,582 | | |

| Primary Natural Resources, Inc. | | | |

| | 1,990,000 | | | Term Loan, 9.35%, Maturing July 28, 2010(3) | | | 1,983,831 | | |

| Targa Resources, Inc. | | | |

| | 194,332 | | | Term Loan, 7.62%, Maturing October 31, 2012 | | | 195,547 | | |

| | 801,619 | | | Term Loan, 7.63%, Maturing October 31, 2012 | | | 806,630 | | |

| | | | | | | $ | 7,366,156 | | |

| Publishing — 3.4% | | | |

| Gatehouse Media Operating, Inc. | | | |

| $ | 391,579 | | | Term Loan, 7.57%, Maturing June 6, 2013 | | $ | 392,558 | | |

| Philadelphia Newspapers, LLC | | | |

| | 997,500 | | | Term Loan, 8.12%, Maturing June 29, 2013 | | | 993,759 | | |

See notes to financial statements

6

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Publishing (continued) | | | |

| Springer Science+Business Media | | | |

| EUR | 536,240 | | | Term Loan, 5.63%, Maturing May 5, 2011 | | | 691,369 | | |

| EUR | 231,880 | | | Term Loan, 6.00%, Maturing May 5, 2012 | | | 300,338 | | |

| EUR | 231,880 | | | Term Loan, 6.00%, Maturing May 5, 2012 | | | 300,347 | | |

| Xsys, Inc. | | | |

| EUR | 1,500,000 | | | Term Loan, 9.31%, Maturing September 27, 2015 | | | 1,949,825 | | |

| | | | | | | $ | 4,628,196 | | |

| Radio and Television — 4.9% | | | |

| CMP Susquehanna Corp. | | | |

| $ | 1,000,000 | | | Term Loan, 0.00%, Maturing May 5, 2011(2) | | $ | 950,000 | | |

| HEI Acquisition, LLC | | | |

| | 1,000,000 | | | Term Loan, 8.38%, Maturing December 31, 2011 | | | 1,000,000 | | |

| P7S1 Holding II S.A.R.L. | | | |

| EUR | 2,000,000 | | | Term Loan, 7.26%, Maturing July 18, 2011 | | | 2,563,868 | | |

| PanAmSat Corp. | | | |

| | 1,000,000 | | | Term Loan, 7.87%, Maturing January 3, 2014 | | | 1,009,514 | | |

| Patriot Media and Communications CNJ, LLC | | | |

| | 1,000,000 | | | Term Loan, 10.50%, Maturing October 6, 2013 | | | 1,017,188 | | |

| | | | | | | $ | 6,540,570 | | |

| Retailers (Except Food and Drug) — 3.9% | | | |

| La Petite Academy, Inc. | | | |

| $ | 1,000,000 | | | Term Loan, 12.61%, Maturing February 21, 2013 | | $ | 1,012,500 | | |

| Neiman Marcus Group, Inc. | | | |

| | 500,000 | | | Term Loan, 7.64%, Maturing April 5, 2013 | | | 504,532 | | |

| Oriental Trading Co., Inc. | | | |

| | 750,000 | | | Term Loan, 11.47%, Maturing January 31, 2013 | | | 753,125 | | |

| Pep Boys - Manny, Moe, & Jack, (The) | | | |

| | 1,990,000 | | | Term Loan, 8.07%, Maturing January 27, 2011 | | | 2,014,875 | | |

| Savers, Inc. | | | |

| | 456,853 | | | Term Loan, 8.16%, Maturing August 11, 2012 | | | 459,994 | | |

| | 543,147 | | | Term Loan, 8.16%, Maturing August 11, 2012 | | | 546,881 | | |

| | | | | | | $ | 5,291,907 | | |

| Surface Transport — 1.4% | | | |

| Ozburn-Hessey Holding Co., LLC | | | |

| $ | 997,052 | | | Term Loan, 8.78%, Maturing August 9, 2012 | | $ | 998,299 | | |

| Sirva Worldwide, Inc. | | | |

| | 908,863 | | | Term Loan, 11.61%, Maturing December 1, 2010 | | | 840,415 | | |

| | | | | | | $ | 1,838,714 | | |

Principal

Amount | |

Borrower/Tranche Description | |

Value | |

| Telecommunications — 7.2% | | | |

| American Cellular Corp. | | | |

| $ | 500,000 | | | Term Loan, 7.63%, Maturing August 7, 2013 | | $ | 503,125 | | |

| | 500,000 | | | Term Loan, 7.63%, Maturing August 7, 2013(2) | | | 501,875 | | |

| Asurion Corp. | | | |

| | 2,000,000 | | | Term Loan, 11.58%, Maturing January 13, 2013 | | | 2,026,250 | | |

| BCM Luxembourg Ltd. | | | |

| EUR | 1,000,000 | | | Term Loan, 7.81%, Maturing March 31, 2016 | | | 1,313,159 | | |

| IPC Acquisition Corp. | | | |

| | 1,000,000 | | | Term Loan, 11.87%, Maturing September 29, 2014 | | | 1,007,500 | | |

| NTelos, Inc. | | | |

| | 994,960 | | | Term Loan, 7.57%, Maturing August 24, 2011 | | | 999,438 | | |

| TDC AS (Nordic Telephone Company) | | | |

| EUR | 500,000 | | | Term Loan, 5.54%, Maturing April 10, 2014 | | | 644,424 | | |

| EUR | 500,000 | | | Term Loan, 6.04%, Maturing April 10, 2015 | | | 647,136 | | |

| Triton PCS, Inc. | | | |

| | 994,937 | | | Term Loan, 8.57%, Maturing November 18, 2009 | | | 1,004,471 | | |

| Westcom Corp. | | | |

| | 1,000,000 | | | Term Loan, 12.54%, Maturing May 17, 2011 | | | 1,006,875 | | |

| | | | | | | $ | 9,654,253 | | |

| Utilities — 3.1% | | | |

| Astoria Generating Co. | | | |

| $ | 2,000,000 | | | Term Loan, 9.14%, Maturing August 23, 2013 | | $ | 2,032,916 | | |

| BRSP, LLC | | | |

| | 1,000,000 | | | Term Loan, 8.58%, Maturing July 13, 2009 | | | 1,005,000 | | |

| Calpine Corp. | | | |

| | 1,095,745 | | | DIP Loan, 9.37%, Maturing February 27, 2008 | | | 1,117,203 | | |

| | | | | | | $ | 4,155,119 | | |

| | | Total Senior, Floating Rate Interests

(identified cost $182,956,706) | | $ | 183,163,911 | | |

| Corporate Bonds & Notes — 26.9% | | | |

Principal Amount

(000's omitted) | | Security | | Value | |

| Aerospace and Defense — 0.0% | | | |

| Argo Tech Corp., Sr. Notes | | | |

| $ | 20 | | | 9.25%, 6/1/11 | | $ | 20,850 | | |

| | | | | | | $ | 20,850 | | |

See notes to financial statements

7

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | | Security | | Value | |

| Automotive — 3.5% | | | |

| Altra Industrial Motion, Inc. | | | |

| $ | 1,000 | | | 9.00%, 12/1/11 | | $ | 1,025,000 | | |

| Ford Motor Credit Co. | | | |

| | 2,000 | | | 6.625%, 6/16/08 | | | 1,962,980 | | |

| Ford Motor Credit Co., Sr. Notes | | | |

| | 375 | | | 9.875%, 8/10/11 | | | 387,859 | | |

| General Motors Acceptance Corp. | | | |

| | 255 | | | 8.00%, 11/1/31 | | | 273,990 | | |

| Tenneco Automotive, Inc., Series B | | | |

| | 1,000 | | | 10.25%, 7/15/13 | | | 1,100,000 | | |

| | | | | | | $ | 4,749,829 | | |

| Building and Development — 0.3% | | | |

| Goodman Global Holdings, Inc., Sr. Notes, Variable Rate | | | |

| $ | 155 | | | 8.329%, 6/15/12 | | $ | 157,712 | | |

| Interline Brands, Inc., Sr. Sub. Notes | | | |

| | 50 | | | 8.125%, 6/15/14 | | | 51,375 | | |

| Nortek, Inc., Sr. Sub. Notes | | | |

| | 150 | | | 8.50%, 9/1/14 | | | 144,000 | | |

| Panolam Industries International, Sr. Sub. Notes | | | |

| | 10 | | | 10.75%, 10/1/13(4) | | | 10,250 | | |

| | | | | | | $ | 363,337 | | |

| Business Equipment and Services — 1.3% | | | |

| Education Management, LLC, Sr. Sub. Notes | | | |

| $ | 1,045 | | | 10.25%, 6/1/16(4) | | $ | 1,089,412 | | |

| Hertz Corp., Sr. Sub. Notes | | | |

| | 595 | | | 8.875%, 1/1/14(4) | | | 624,750 | | |

| Lamar Media Corp., Sr. Sub. Notes | | | |

| | 70 | | | 6.625%, 8/15/15(4) | | | 67,725 | | |

| Sungard Data Systems, Inc. | | | |

| | 6 | | | 10.25%, 8/15/15 | | | 6,315 | | |

| | | | | | | $ | 1,788,202 | | |

| Cable and Satellite Television — 1.7% | | | |

| Cablevision Systems Corp., Sr. Notes, Series B, Variable Rate | | | |

| $ | 180 | | | 9.87%, 4/1/09 | | $ | 189,450 | | |

| CCH I, LLC/CCH I Capital Co. | | | |

| | 50 | | | 11.00%, 10/1/15 | | | 48,437 | | |

| CCO Holdings, LLC / CCO Capital Corp., Sr. Notes | | | |

| | 700 | | | 8.75%, 11/15/13 | | | 715,750 | | |

| CSC Holdings, Inc., Series B | | | |

| | 70 | | | 8.125%, 8/15/09 | | | 72,537 | | |

Principal Amount

(000's omitted) | | Security | | Value | |

| Cable and Satellite Television (continued) | | | |

| CSC Holdings, Inc., Sr. Notes, Seriers B | | | |

| $ | 10 | | | 8.125%, 7/15/09 | | $ | 10,362 | | |

| Mediacom Broadband Corp., LLC, Sr. Notes | | | |

| | 125 | | | 8.50%, 10/15/15(4) | | | 125,469 | | |

| National Cable, PLC | | | |

| | 1,070 | | | 8.75%, 4/15/14 | | | 1,130,187 | | |

| | | | | | | $ | 2,292,192 | | |

| Chemicals and Plastics — 0.4% | | | |

| Equistar Chemical, Sr. Notes | | | |

| $ | 40 | | | 10.625%, 5/1/11 | | $ | 43,000 | | |

| Hexion U.S. Finance/Nova Scotia Finance | | | |

| | 25 | | | 9.00%, 7/15/14 | | | 28,250 | | |

| Ineos Group Holdings PLC | | | |

| | 440 | | | 8.50%, 2/15/16(4) | | | 425,700 | | |

| Reichhold Industries, Inc., Sr. Notes | | | |

| | 70 | | | 9.00%, 8/15/14(4) | | | 70,000 | | |

| | | | | | | $ | 566,950 | | |

| Clothing / Textiles — 1.0% | | | |

| Levi Strauss & Co., Sr. Notes | | | |

| $ | 50 | | | 9.75%, 1/15/15 | | $ | 53,250 | | |

| | 200 | | | 8.875%, 4/1/16 | | | 206,500 | | |

| Oxford Industries, Inc., Sr. Notes | | | |

| | 1,000 | | | 8.875%, 6/1/11 | | | 1,031,250 | | |

| Perry Ellis International, Inc., Sr. Sub. Notes | | | |

| | 15 | | | 8.875%, 9/15/13 | | | 15,112 | | |

| | | | | | | $ | 1,306,112 | | |

| Conglomerates — 0.0% | | | |

| Mueller Holdings, Inc., (0.00%) until 4/15/09) | | | |

| $ | 5 | | | 14.75%, 4/15/14 | | $ | 4,425 | | |

| | | | | | | $ | 4,425 | | |

| Containers and Glass Products — 1.0% | | | |

| Berry Plastics Holding Corp. | | | |

| $ | 80 | | | 8.875%, 9/15/14(4) | | $ | 81,200 | | |

| Berry Plastics Holding Corp., Variable Rate | | | |

| | 60 | | | 9.265%, 9/15/14(4) | | | 60,975 | | |

| Intertape Polymer US, Inc., Sr. Sub. Notes | | | |

| | 20 | | | 8.50%, 8/1/14 | | | 18,100 | | |

| Pliant Corp. (PIK) | | | |

| | 1,100 | | | 11.85%, 6/15/09 | | | 1,200,265 | | |

| | | | | | | $ | 1,360,540 | | |

See notes to financial statements

8

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | | Security | | Value | |

| Cosmetics / Toiletries — 0.1% | | | |

| Amscan Holdings, Inc., Sr. Sub. Notes | | | |

| $ | 85 | | | 8.75%, 5/1/14 | | $ | 80,750 | | |

| | | | | | | $ | 80,750 | | |

| Ecological Services and Equipment — 0.0% | | | |

| Waste Services, Inc., Sr. Sub. Notes | | | |

| $ | 25 | | | 9.50%, 4/15/14 | | $ | 25,750 | | |

| | | | | | | $ | 25,750 | | |

| Electronics / Electrical — 0.2% | | | |

| Avago Technologies Finance PTE, Sr. Notes | | | |

| $ | 50 | | | 10.125%, 12/1/13(4) | | $ | 53,250 | | |

| NXP BV/NXP Funding, LLC, Sr. Notes | | | |

| | 240 | | | 9.50%, 10/15/15(4) | | | 243,300 | | |

| | | | | | | $ | 296,550 | | |

| Financial Intermediaries — 1.5% | | | |

| Gmac LLC | | | |

| $ | 1,000 | | | 6.125%, 1/22/08 | | $ | 995,381 | | |

| Sonata Securities S.A., Series 2006-5 | | | |

| | 500 | | | 8.999%, 6/27/07 | | | 503,550 | | |

| Sonata Securities S.A., Series 2006-6 | | | |

| | 500 | | | 8.999%, 6/27/07 | | | 503,455 | | |

| | | | | | | $ | 2,002,386 | | |

| Food Products — 0.8% | | | |

| Nutro Products, Inc., Sr. Notes, Variable Rate | | | |

| $ | 1,000 | | | 9.40%, 10/15/13(4) | | $ | 1,032,500 | | |

| | | | | | | $ | 1,032,500 | | |

| Food Service — 0.9% | | | |

| Buffets, Inc. | | | |

| $ | 115 | | | 12.50%, 11/1/14(4) | | $ | 116,150 | | |

| NPC International, Inc., Sr. Sub. Notes | | | |

| | 1,070 | | | 9.50%, 5/1/14(4) | | | 1,088,725 | | |

| | | | | | | $ | 1,204,875 | | |

| Food / Drug Retailers — 0.1% | | | |

| Rite Aid Corp. | | | |

| $ | 145 | | | 6.125%, 12/15/08(4) | | $ | 142,100 | | |

| | 50 | | | 8.125%, 5/1/10 | | | 50,750 | | |

| | | | | | | $ | 192,850 | | |

Principal Amount

(000's omitted) | | Security | | Value | |

| Forest Products — 0.2% | | | |

| Domtar, Inc. | | | |

| $ | 175 | | | 7.125%, 8/1/15 | | $ | 168,000 | | |

| NewPage Corp. | | | |

| | 35 | | | 10.00%, 5/1/12 | | | 36,837 | | |

| Stone Container Corp. | | | |

| | 100 | | | 7.375%, 7/15/14 | | | 92,375 | | |

| | | | | | | $ | 297,212 | | |

| Healthcare — 2.2% | | | |

| AMR HoldCo, Inc./EmCare HoldCo, Inc., Sr. Sub. Notes | | | |

| $ | 15 | | | 10.00%, 2/15/15 | | $ | 16,162 | | |

| HCA, Inc. | | | |

| | 20 | | | 8.75%, 9/1/10 | | | 20,250 | | |

| Multiplan, Inc., Sr. Sub. Notes | | | |

| | 1,020 | | | 10.375%, 4/15/16(4) | | | 1,025,100 | | |

| National Mentor Holdings, Inc., Sr. Sub. Notes | | | |

| | 70 | | | 11.25%, 7/1/14(4) | | | 73,850 | | |

| Service Corp. International, Sr. Notes | | | |

| | 195 | | | 7.625%, 10/1/18(4) | | | 201,337 | | |

| Triad Hospitals, Inc., Sr. Notes | | | |

| | 70 | | | 7.00%, 5/15/12 | | | 69,825 | | |

| Triad Hospitals, Inc., Sr. Sub. Notes | | | |

| | 85 | | | 7.00%, 11/15/13 | | | 83,087 | | |

| US Oncology, Inc. | | | |

| | 335 | | | 10.75%, 8/15/14 | | | 370,175 | | |

| VWR International, Inc., Sr. Sub. Notes | | | |

| | 1,000 | | | 8.00%, 4/15/14 | | | 1,032,500 | | |

| | | | | | | $ | 2,892,286 | | |

| Leisure Goods / Activities / Movies — 1.9% | | | |

| Marquee Holdings, Inc., Sr. Disc. Notes, (0.00% until 2009) | | | |

| $ | 2,000 | | | 12.00%, 8/15/14 | | $ | 1,575,000 | | |

| Six Flags Theme Parks, Inc., Sr. Notes | | | |

| | 1,020 | | | 9.625%, 6/1/14 | | | 938,400 | | |

| Universal City Florida Holdings, Sr. Notes, Variable Rate | | | |

| | 70 | | | 10.12%, 5/1/10 | | | 72,362 | | |

| | | | | | | $ | 2,585,762 | | |

| Lodging and Casinos — 2.3% | | | |

| CCM Merger, Inc. | | | |

| $ | 45 | | | 8.00%, 8/1/13(4) | | $ | 43,594 | | |

| Host Hotels & Resorts L.P., Sr. Notes | | | |

| | 95 | | | 6.875%, 11/1/14(4) | | | 95,712 | | |

See notes to financial statements

9

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | | Security | | Value | |

| Lodging and Casinos (continued) | | | |

| Inn of the Mountain Gods, Sr. Notes | | | |

| $ | 10 | | | 12.00%, 11/15/10 | | $ | 10,750 | | |

| Las Vegas Sands Corp. | | | |

| | 150 | | | 6.375%, 2/15/15 | | | 141,750 | | |

| Station Casinos, Inc. | | | |

| | 30 | | | 7.75%, 8/15/16 | | | 30,975 | | |

| Station Casinos, Inc., Sr. Notes | | | |

| | 50 | | | 6.00%, 4/1/12 | | | 47,937 | | |

| Trump Entertainment Resorts, Inc. | | | |

| | 2,190 | | | 8.50%, 6/1/15 | | | 2,154,413 | | |

| Tunica-Biloxi Gaming Authority, Sr. Notes | | | |

| | 160 | | | 9.00%, 11/15/15 | | | 166,000 | | |

| Turning Stone Resort Casinos, Sr. Notes | | | |

| | 40 | | | 9.125%, 9/15/14(4) | | | 40,900 | | |

| Waterford Gaming, LLC, Sr. Notes | | | |

| | 318 | | | 8.625%, 9/15/12(4) | | | 338,670 | | |

| | | | | | | $ | 3,070,701 | | |

| Metals and Mining — 0.1% | | | |

| AK Steel Corp. | | | |

| $ | 120 | | | 7.875%, 2/15/09 | | $ | 121,050 | | |

| | | | | | | $ | 121,050 | | |

| Nonferrous Metals / Minerals — 0.1% | | | |

| FMG Finance PTY, Ltd. | | | |

| $ | 100 | | | 10.625%, 9/1/16(4) | | $ | 99,000 | | |

| | | | | | | $ | 99,000 | | |

| Oil and Gas — 3.0% | | | |

| Allis-Chalmers Energy, Inc., Sr. Notes | | | |

| $ | 1,090 | | | 9.00%, 1/15/14(4) | | $ | 1,092,725 | | |

| Kinder Morgan Finance Co. | | | |

| | 145 | | | 5.35%, 1/5/11 | | | 141,746 | | |

| Ocean Rig Norway AS, Sr. Notes | | | |

| | 50 | | | 8.375%, 7/1/13(4) | | | 52,938 | | |

| Petrohawk Energy Corp., Sr. Notes | | | |

| | 1,320 | | | 9.125%, 7/15/13(4) | | | 1,353,000 | | |

| Quicksilver Resources, Inc. | | | |

| | 115 | | | 7.125%, 4/1/16 | | | 109,250 | | |

| Semgroup L.P., Sr. Notes | | | |

| | 145 | | | 8.75%, 11/15/15(4) | | | 146,813 | | |

| SESI, LLC, Sr. Notes | | | |

| | 30 | | | 6.875%, 6/1/14(4) | | | 29,925 | | |

Principal Amount

(000's omitted) | | Security | | Value | |

| Oil and Gas (continued) | | | |

| Stewart & Stevenson, LLC, Sr. Notes | | | |

| $ | 95 | | | 10.00%, 7/15/14(4) | | $ | 96,663 | | |

| United Refining Co., Sr. Notes | | | |

| | 1,000 | | | 10.50%, 8/15/12 | | | 1,045,000 | | |

| | | | | | | $ | 4,068,060 | | |

| Publishing — 0.1% | | | |

| Houghton Mifflin Co., Sr. Sub. Notes | | | |

| $ | 85 | | | 9.875%, 2/1/13 | | $ | 91,481 | | |

| | | | | | | $ | 91,481 | | |

| Radio and Television — 1.6% | | | |

| Advanstar Communications, Inc. | | | |

| $ | 2,010 | | | 10.75%, 8/15/10 | | $ | 2,173,313 | | |

| XM Satellite Radio, Inc. | | | |

| | 20 | | | 9.75%, 5/1/14 | | | 19,100 | | |

| | | | | | | $ | 2,192,413 | | |

| Rail Industries — 0.0% | | | |

| Kansas City Southern Railway Co. | | | |

| $ | 35 | | | 9.50%, 10/1/08 | | $ | 36,969 | | |

| | | | | | | $ | 36,969 | | |

| Retailers (Except Food and Drug) — 1.2% | | | |

| Bon-Ton Department Stores, Inc. | | | |

| $ | 170 | | | 10.25%, 3/15/14 | | $ | 173,188 | | |

| GameStop Corp. | | | |

| | 105 | | | 8.00%, 10/1/12 | | | 109,463 | | |

| Michaels Stores, Inc., Sr. Notes | | | |

| | 115 | | | 10.00%, 11/1/14(4) | | | 115,863 | | |

| Michaels Stores, Inc., Sr. Sub. Notes | | | |

| | 95 | | | 11.375%, 11/1/16 | | | 95,831 | | |

| Neiman Marcus Group, Inc. | | | |

| | 1,000 | | | 9.00%, 10/15/15 | | | 1,077,500 | | |

| | 20 | | | 10.375%, 10/15/15 | | | 21,975 | | |

| Toys "R" Us | | | |

| | 50 | | | 7.375%, 10/15/18 | | | 37,625 | | |

| | | | | | | $ | 1,631,445 | | |

| Telecommunications — 1.3% | | | |

| Digicel Ltd., Sr. Notes | | | |

| $ | 40 | | | 9.25%, 9/1/12(4) | | $ | 41,700 | | |

| Intelsat Bermuda Ltd. | | | |

| | 120 | | | 9.25%, 6/15/16(4) | | | 128,700 | | |

See notes to financial statements

10

Eaton Vance Credit Opportunities Fund as of October 31, 2006

PORTFOLIO OF INVESTMENTS (Unaudited) CONT'D

Principal Amount

(000's omitted) | | Security | | Value | |

| Telecommunications (continued) | | | |

| Intelsat Ltd., Sr. Notes | | | |

| $ | 1,050 | | | 5.25%, 11/1/08 | | $ | 1,021,125 | | |

| Qwest Capital Funding, Inc. | | | |

| | 40 | | | 7.00%, 8/3/09 | | | 40,650 | | |

| Qwest Communications International, Inc., Sr. Notes | | | |

| | 25 | | | 7.50%, 11/1/08 | | | 25,500 | | |

| West Corp., Sr. Notes | | | |

| | 235 | | | 9.50%, 10/15/14(4) | | | 235,588 | | |

| West Corp., Sr. Sub. Notes | | | |

| | 25 | | | 11.00%, 10/15/16(4) | | | 25,188 | | |

| Windstream Corp., Sr. Notes | | | |

| | 145 | | | 8.125%, 8/1/13(4) | | | 155,513 | | |

| | 30 | | | 8.625%, 8/1/16(4) | | | 32,513 | | |

| | | | | | | $ | 1,706,477 | | |

| Utilities — 0.1% | | | |

| NRG Energy, Inc. | | | |

| $ | 50 | | | 7.25%, 2/1/14 | | $ | 50,688 | | |

| NRG Energy, Inc., Sr. Notes | | | |

| | 25 | | | 7.375%, 2/1/16 | | | 25,344 | | |

| Reliant Energy, Inc. | | | |

| | 85 | | | 9.25%, 7/15/10 | | | 88,400 | | |

| | | | | | | $ | 164,432 | | |

| | | Total Corporate Bonds & Notes

(identified cost $35,711,166) | | $ | 36,245,386 | | |

| | | Gross Investments — 163.1%

(identified cost $218,667,872) | | $ | 219,409,297 | | |

| | Less Unfunded Loan

Commitments — (2.0)% | | | | | $ | (2,718,781 | ) | |

| | | Net Investments — 161.1%

(identified cost $215,949,091) | | $ | 216,690,516 | | |

| | Other Assets, Less Liabilities — (0.7)% | | | | | $ | (875,880 | ) | |

| | Auction Preferred Shares Plus

Cumulative Unpaid

Dividends — (60.4)% | | | | | $ | (81,308,686 | ) | |

| | | Net Assets Applicable to Common

Shares — 100.0% | | $ | 134,505,950 | | |

EUR - Euro

GBP - British Pound

PIK - Payment In Kind.

(1) Senior floating-rate interests often require prepayments from excess cash flows or permit the borrower to repay at its election. The degree to which borrowers repay, whether as a contractual requirement or at their election, cannot be predicted with accuracy. As a result, the actual remaining maturity may be substantially less than the stated maturities shown. However, it is anticipated that the senior floating-rate interests will have an expected average life of approximately two to three years. The stated interest rate represents the weighted average interest rate of all contracts within the senior loan facility. Senior Loans typically have rates of interest which are redetermined either daily, monthly, quarterly or semi-annually by reference to a base lending rate, plus a premium. These base lending rates are primarily the London - -Interbank Offered Rate ("LIBOR"), and secondarily the prime rate offered by one or more major United States banks (the "Prime Rate") and the certificate of deposit ("CD") rate or other base lending rates used by commercial lenders.

(2) Unfunded loan commitments. See Note 1G for description.

(3) Security valued at fair value using methods determined in good faith by or at the direction of the Trustees.

(4) Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities may be sold in transactions exempt from registration, normally to qualified institutional buyers. At October 31, 2006, the aggregate value of the securities is $10,984,380 or 8.2% of the net assets.

(5) Defaulted Security. Currently the issuer is in default with respect to interest payments.

See notes to financial statements

11

Eaton Vance Credit Opportunities Fund as of October 31, 2006

FINANCIAL STATEMENTS (Unaudited)

Statement of Assets and Liabilities

As of October 31, 2006

| Assets | |

| Investments, at value (identified cost, $215,949,091) | | $ | 216,690,516 | | |

| Cash | | | 1,311,197 | | |

| Foreign currency, at value (identified cost, $38,870) | | | 41,184 | | |

| Receivable for investments sold | | | 1,909,746 | | |

| Receivable from the Investment Adviser | | | 15,500 | | |

| Interest receivable | | | 2,803,871 | | |

| Prepaid expenses | | | 6,606 | | |

| Total assets | | $ | 222,778,620 | | |

| Liabilities | |

| Demand note payable | | $ | 5,900,000 | | |

| Payable for investments purchased | | | 487,440 | | |

| Payable to affiliate for investment advisory fees | | | 102,825 | | |

| Payable for open forward foreign currency contracts | | | 230,736 | | |

| Accrued expenses | | | 242,983 | | |

| Total liabilities | | $ | 6,963,984 | | |

Auction preferred shares (3,250 shares outstanding) at

liquidation value plus cumulative unpaid dividends | | $ | 81,308,686 | | |

| Net assets applicable to common shares | | $ | 134,505,950 | | |

| Sources of Net Assets | |

Common Shares, $0.01 par value, unlimited number of shares

authorized, 7,062,982 shares issued and outstanding | | $ | 70,630 | | |

| Additional paid-in capital | | | 133,467,309 | | |

Accumulated undistributed net realized gain (computed on the basis

of identified cost) | | | 76,374 | | |

| Accumulated undistributed net investment income | | | 378,432 | | |

| Net unrealized appreciation (computed on the basis of identified cost) | | | 513,205 | | |

| Net assets applicable to common shares | | $ | 134,505,950 | | |

| Net Asset Value Per Common Share | |

| ($134,505,950 ÷ 7,062,982 shares of beneficial interest outstanding) | | $ | 19.04 | | |

Statement of Operations

For the Period Ended

October 31, 2006(1)

| Investment Income | |

| Interest | | $ | 6,510,216 | | |

| Dividends | | | 52,190 | | |

| Total investment income | | $ | 6,562,406 | | |

| Expenses | |

| Investment adviser fee | | $ | 574,978 | | |

| Legal and accounting services | | | 53,202 | | |

| Preferred shares remarketing agent fee | | | 45,634 | | |

| Custodian fee | | | 35,473 | | |

| Transfer and dividend disbursing agent fees | | | 25,012 | | |

| Organization expenses | | | 15,500 | | |

| Printing and postage | | | 7,896 | | |

| Interest expense | | | 114,707 | | |

| Miscellaneous | | | 27,969 | | |

| Total expenses | | $ | 900,371 | | |

Deduct —

Reduction of Investment Adviser fee | | $ | 153,334 | | |

| Expense reimbursement | | | 15,500 | | |

| Total expense reductions | | $ | 168,834 | | |

| Net expenses | | $ | 731,537 | | |

| Net investment income | | $ | 5,830,869 | | |

| Realized and Unrealized Gain (Loss) | |

Net realized gain (loss) —

Investment transactions (identified cost basis) | | $ | 8,050 | | |

| Foreign currency and forward foreign currency exchange contract transactions | | | 68,324 | | |

| Net realized gain | | $ | 76,374 | | |

Change in unrealized appreciation (depreciation) —

Investments (identified cost basis) | | $ | 741,425 | | |

| Foreign currency and forward foreign currency exchange contracts | | | (228,220 | ) | |

| Net change in unrealized appreciation (depreciation) | | $ | 513,205 | | |

| Net realized and unrealized gain | | $ | 589,579 | | |

| Distributions to preferred shareholders from net investment income | | $ | (962,576 | ) | |

| Net increase in net assets from operations | | $ | 5,457,872 | | |

(1) For the period from the start of business, May 31, 2006, to October 31, 2006.

See notes to financial statements

12

Eaton Vance Credit Opportunities Fund as of October 31, 2006

FINANCIAL STATEMENTS (Unaudited) CONT'D

Statements of Changes in Net Assets

Increase (Decrease)

in Net Assets | | Period Ended

October 31, 2006(1) | |

| From operations — | |

| Net investment income | | $ | 5,830,869 | | |

Net realized gain from investment transactions, foreign currency

and forward foreign currency exchange contract transactions | | | 76,374 | | |

Net change in unrealized appreciation (depreciation) from investments,

foreign currency and forward foreign currency exchange contracts | | | 513,205 | | |

Distributions to preferred shareholders —

From net investment income | | | (962,576 | ) | |

| Net increase in net assets from operations | | $ | 5,457,872 | | |

Distributions to common shareholders —

From net investment income | | $ | (4,489,861 | ) | |

| Total distributions to common shareholders | | $ | (4,489,861 | ) | |

Capital share transactions —

Proceeds from sale of common shares (2) | | $ | 133,700,000 | | |

| Reinvestment of distributions to common shareholders | | | 1,104,633 | | |

| Offering costs and preferred shares underwriting discounts | | | (1,366,694 | ) | |

| Total increase in net assets from capital share transactions | | $ | 133,437,939 | | |

| Net increase in net assets | | $ | 134,405,950 | | |

| Net Assets Applicable to Common Shares | |

| At beginning of period | | $ | 100,000 | | |

| At end of period | | $ | 134,505,950 | | |

Accumulated undistributed net

investment income included in

net assets applicable to common shares | |

| At end of period | | $ | 378,432 | | |

(1) For the period from the start of business, May 31, 2006, to October 31, 2006.

(2) Proceeds from sales of shares net of sales load paid of $6,300,000.

See notes to financial statements

13

Eaton Vance Credit Opportunities Fund as of October 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

Selected data for a common share outstanding during the periods stated

| | | Period Ended

October 31, 2006

(Unaudited)(1)(2) | |

| Net asset value — Beginning of period | | $ | 19.100 | (3) | |

| Income (loss) from operations | |

| Net investment income | | $ | 0.830 | | |

| Net realized and unrealized gain | | | 0.080 | | |

| Distributions to preferred shareholders from net investment income | | | (0.137 | ) | |

| Total income from operations | | $ | 0.773 | | |

| Less distributions to common shareholders | |

| From net investment income | | $ | (0.638 | ) | |

| Total distributions to common shareholders | | $ | (0.638 | ) | |

| Preferred and Common shares offering costs charged to paid-in capital | | $ | (0.079 | ) | |

| Preferred Shares underwriting discounts | | $ | (0.116 | ) | |

| Net asset value — End of period (Common shares) | | $ | 19.040 | | |

| Market value — End of period (Common shares) | | $ | 19.800 | | |

| Total Investment Return on Net Asset Value(4) | | | 3.07 | % | |

| Total Investment Return on Market Value(4) | | | 7.18 | % | |

See notes to financial statements

14

Eaton Vance Credit Opportunities Fund as of October 31, 2006

FINANCIAL STATEMENTS CONT'D

Financial Highlights

Selected data for a common share outstanding during the periods stated

| | | Period Ended

October 31, 2006

(Unaudited)(1)(2) | |

| Ratios/Supplemental Data† | |

| Net assets applicable to common shares, end of period (000's omitted) | | $ | 134,506 | | |

| Ratios (As a percentage of average net assets appicable to common shares): | |

| Net expenses(6) | | | 1.30 | %(5) | |

| Net investment income(6) | | | 10.33 | %(5) | |

| Portfolio Turnover | | | 22 | % | |

† The ratios reported are based on net assets applicable solely to common shares. The ratios based on net assets, including amounts related to preferred shares,

are as follows:

| Ratios (As a percentage of average total net assets applicable to common and preferred shares): | |

| Net expenses(6) | | | 0.81 | % | |

| Net investment income(6) | | | 6.43 | % | |

| Senior Securities: | |

| Total preferred shares outstanding | | | 81,250 | | |

| Asset coverage per preferred share(7) | | $ | 66,405 | | |

| Involuntary liquidation preference per preferred share(8) | | $ | 25,000 | | |

| Approximate market value per preferred share(8) | | $ | 25,000 | | |

(1) For the period from the start of business May 31, 2006, to October 31, 2006.

(2) Net investment income per share was computed using average common shares outstanding.

(3) Net asset value at beginning of period reflects the deduction of the sales load of $0.900 per share paid by the shareholder from the $20.000 offering price.

(4) Total investment return on net asset value is calculated assuming a purchase at the offering price of $20.00 less the sales load of $0.90 per share paid by the shareholder on the first day and a sale at the net asset value on the last day of the period reported. Total investment return on market value is calculated assuming a purchase at the offering price of $20.00 less the sales load of $0.90 per share by the shareholder on the first day and a sale at the current market price on the last day of the period reported. Total investment return on net asset value and total investment return on market value are not computed on an annualized basis.

(5) Annualized.

(6) Ratios do not reflect the effect of dividend payments to preferred shareholders.

(7) Calculated by subtracting the Fund's total liabilities (not including the preferred shares) from the Fund's total assets, and dividing this by the number of preferred shares outstanding.

(8) Plus accumulated and unpaid dividends.

See notes to financial statements

15

Eaton Vance Credit Opportunities Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS (Unaudited)

1 Significant Accounting Policies

Eaton Vance Credit Opportunities Fund (the "Fund") is registered under the Investment Company Act of 1940 (the 1940 Act), as amended, as a diversified, closed-end management investment company. The Fund was organized as a Massachusetts business trust on October 5, 2005. The Fund's primary investment objective is to provide a high level of current income. The Fund will, as a secondary objective, also seek capital appreciation. The Fund pursues its objectives primarily by investing opportunistically in various credit-related investments. The following is a summary of significant accounting policies of the Fund. The policies are in conformity with accounting principles generally accepted in the United States of America.

A Investment Valuation — The Fund's investments include interests in senior floating rate loans (Senior Loans). Certain Senior Loans are deemed to be liquid because reliable market quotations are readily available for them. Liquid Senior Loans are valued on the basis of prices furnished by a pricing service. Other Senior Loans are valued at fair value by the Fund's investment adviser, Eaton Vance Management (EVM), under procedures approved by the Trustees. In connection with determining the fair value of a Senior Loan, the investment adviser makes an assessment of the likelihood that the borrower will make a full repayment of the Senior Loan. The primary factors considered by the investment adviser when making this assessment are (i) the creditworthiness of the borrower, (ii) the value of the collateral backing the Senior Loan, and (iii) the priority of the Senior Loan versus other creditors of the borrower. If, based on its assessment, the investment adviser believes there is a reasonable likelihood that the borrower will make a full repayment of the Senior Loan, the investment adviser will determine the fair value of the Senior Loan using a matrix pricing approach that considers the yield on the Senior Loan relative to yields on other loan interests issued by companies of comparable credit quality. If, based on its assessment, the investment adviser believes there is not a reasonable likelihood that the borrower will make a full repayment of the Senior Loan, the investment adviser will determine the fair value of the Senior Loan using analyses that include, but are not limited to (i) a comparison of the value of the borrower's outstanding equity and debt to that of comparable public companies; (ii) a discounted cash flow analysis; or (iii) when the investment adviser belie ves it is likely that a borrower will be liquidated or sold, an analysis of the terms of such liquidation or sale. In certain cases, the investment adviser will use a combination of analytical methods to determine fair value, such as when only a portion of a borrower's assets are likely to be sold. In conducting its assessment and analyses for purposes of determining fair value of a Senior Loan, the investment adviser will use its discretion and judgment in considering and appraising such factors, data and information and the relative weight to be given thereto as it deems relevant, including without limitation, some or all of the following: (i) the fundamental characteristics of and fundamental analytical data relating to the Senior Loan, including the cost, size, current interest rate, maturity and base lending rate of the Senior Loan, the terms and conditions of the Senior Loan and any related agreements, and the position of the Senio r Loan in the borrower's debt structure; (ii) the nature, adequacy and value of the collateral securing the Senior Loan, including the Fund's rights, remedies and interests with respect to the collateral; (iii) the creditworthiness of the borrower, based on an evaluation of, among other things, its financial condition, financial statements and information about the borrower's business, cash flows, capital structure and future prospects; (iv) information relating to the market for the Senior Loan, including price quotations for and trading in the Senior Loan and interests in similar Senior Loans and the market environment and investor attitudes towards the Senior Loan and interests in similar Senior Loans; (v) the experience, reputation, stability and financial condition of the agent and any intermediate participants in the Senior Loan; and (vi) general economic and market conditions affecting the fair value of the Senior Loan. Fair value determinations are made by the portfolio managers of a Fund based on in formation available to such managers. The portfolio managers of other funds managed by Eaton Vance that invest in Senior Loans may not possess the same information about a Senior Loan borrower as the portfolio managers of Credit Opportunities Fund. At times, the fair value of a Senior Loan determined by the portfolio managers of other funds managed by Eaton Vance that invest in Senior Loans may vary from the fair value of the same Senior Loan determined by the portfolio managers of Credit Opportunities Fund. The fair value of each Senior Loan is periodically reviewed and approved by the investment adviser's Valuation Committee and by the Trustees based upon procedures approved by the Trustees. Junior Loans are valued in the same manner as Senior Loans.

Non-loan porfolio holdings (other than short-term obligations maturing in sixty days or less), including

16

Eaton Vance Credit Opportunities Fund as of October 31, 2006

NOTES TO FINANCIAL STATEMENTS (Unaudited) CONT'D

listed securities and securities for which price quotations are available and forward contracts, will normally be valued on the basis of market valuations furnished by dealers or pricing services. Financial futures contracts listed on commodity exchanges and exchange-traded options are valued at closing settlement prices. Over-the-counter options are valued at the mean between the bid and asked prices provided by dealers. Marketable securities listed on the NASDAQ National Market System are valued at the NASDAQ official closing price. The value of interest rate swaps will be based upon a dealer quotation. Short-term obligations and money market securities maturing in sixty days or less are valued at amortized cost which approximates value. Investments for which reliable market quotations are unavailable and investments for which the price of the security is not believed to represent its fair market value, are valued at fair valu e using methods determined in good faith by or at the direction of the Trustees of the Fund.

Occasionally, events affecting the value of foreign securities may occur between the time trading is completed abroad and the close of the Exchange which will not be reflected in the computation of the Trust's net asset value (unless the Trust deems that such event would materially affect its net asset value in which case an adjustment would be made and reflected in such computation). The Trust may rely on an independent fair valuation service in making any such adjustment.

B Income — Interest income is recorded on the basis of interest accrued, adjusted for amortization of premium or accretion of discount. Fees associated with loan amendments are recognized immediately. Dividend income is recorded on the ex-dividend date for dividends received in cash and/or securities.

C Federal Taxes — The Fund's policy is to comply with the provisions of the Internal Revenue Code applicable to regulated investment companies and to distribute to shareholders each year all of its taxable income, including any net realized gain on investments. Accordingly, no provision for federal income or excise tax is necessary.

D Foreign Currency Translation — Investment valuations, other assets, and liabilities initially expressed in foreign currencies are converted each business day into U.S. dollars based upon current exchange rates. Purchases and sales of foreign investment securities and income and expenses are converted into U.S. dollars based upon currency exchange rates prevailing on the respective dates of such transactions. Recognized gains or losses on investment transactions attributable to changes in foreign currency exchange rates are recorded for financial statement purposes as net realized gains and losses on investments. That portion of unrealized gains and losses on investments that results from fluctuation s in foreign currency exchange rates is not separately disclosed.

E Forward Foreign Currency Exchange Contracts — The Fund may enter into forward foreign currency exchange contracts for the purchase or sale of a specific foreign currency at a fixed price on a future date. Risks may arise upon entering these contracts from the potential inability of counterparties to meet the terms of their contracts and from movements in the value of a foreign currency relative to the U.S. dollar. The Fund will enter into forward contracts for hedging purposes as well as non-hedging purposes. The forward foreign currency exchange contracts are adjusted by the daily exchange rate of the underlying currency and any gains or losses are recorded for financial statement purposes as unrealized until such time as the contracts have been closed.

F When Issued and Delayed Delivery Transactions — The Fund may engage in when-issued and delayed delivery transactions. The Fund records when-issued securities on trade date and maintain security positions such that sufficient liquid assets will be available to make payments for the securities purchased. Securities purchased on a when-issued or delayed delivery basis are marked-to-market daily and begin earning interest on settlement date.

G Unfunded Loan Commitments — The Fund may enter into certain credit agreements all or a portion of which may be unfunded. The Fund is obligated to fund these commitments at the borrower's discretion. These commitments are disclosed in the accompanying Portfolio of Investments.