Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration Nos. 333-12965

333-129465-01

333-129465-02

333-129465-03

333-129465-04

333-129465-05

333-129465-06

333-129465-07

333-129465-08

333-129465-09

PROSPECTUS

Exchange Offer for

Floating Rate Senior Notes due 2012

8 1/4% Senior Notes due 2013

8 5/8% Senior Notes due 2015

This is an offer to exchange any Floating Rate Senior Notes due 2012 that you now hold for newly issued Floating Rate Senior Notes due 2012, to exchange any 8 1/4% Senior Notes due 2013 that you now hold for newly issued 8 1/4% Senior Notes due 2013, and to exchange any 8 5/8% Senior Notes due 2015 that you now hold for newly issued 8 5/8% Senior Notes due 2015. This offer will expire at 5:00 p.m. New York City time on March 13, 2006, unless we extend the offer. You must tender your original notes by this deadline in order to receive the new notes. We do not currently intend to extend the expiration date.

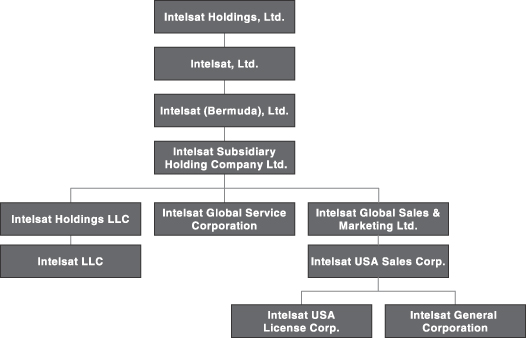

The original notes were issued by Intelsat (Bermuda), Ltd. Since that time, Intelsat (Bermuda), Ltd. transferred substantially all its assets to its wholly-owned subsidiary, Intelsat Subsidiary Holding Company, Ltd., and Intelsat Subsidiary Holding Company, Ltd. at that time assumed substantially all of Intelsat (Bermuda), Ltd.’s obligations, including its obligations in respect of the original notes. Accordingly, Intelsat Subsidiary Holding Company, Ltd. is currently the obligor on the original notes and will be issuing any new notes issued in exchange therefore pursuant to this exchange offer.

The exchange of outstanding original notes for exchange notes in the exchange offer should not constitute a taxable event for U.S. federal income tax purposes. The terms of the exchange notes to be issued in the exchange offer are substantially identical to the original notes, except that the exchange notes will be freely tradeable and will not benefit from the registration and related rights pursuant to which we are conducting this exchange offer. All untendered original notes will continue to be subject to the restrictions on transfer set forth in the original notes and in the applicable indenture.

There is no existing public market for your original notes, and there is currently no public market for the new notes to be issued to you in the exchange offer.

See “Risk Factors” beginning on page 30 for a description of the business and financial risks associated with the new notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is February 10, 2006.

Table of Contents

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with additional or different information. If anyone provides you with different or inconsistent information, you should not rely on it.We are offering to exchange the notes only in jurisdictions where these offers and exchanges are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus.

Consent under the Exchange Control Act 1972 of Bermuda, as amended, and its related regulations has been given by the Bermuda Monetary Authority for the issue and transfer of the new notes between non-residents of Bermuda. Prior to this offering, we intend, if required, to file this prospectus with the Registrar of Companies in Bermuda in accordance with Bermuda law. In granting such consent and in accepting this prospectus for filing, neither the Bermuda Monetary Authority nor the Registrar of Companies in Bermuda accepts any responsibility for our financial soundness or performance or any default of our business, or for the correctness of any of the statements made or opinions expressed in this prospectus or the registration statement of which this prospectus forms a part.

| Page | ||

| 1 | ||

| 27 | ||

| 30 | ||

| 55 | ||

| 57 | ||

| 57 | ||

| 58 | ||

| 59 | ||

Unaudited Pro Forma Condensed Consolidated Financial Information | 62 | |

Management’s Discussion and Analysis of Financial Condition and Results of Operations | 69 | |

| 120 | ||

| 124 | ||

| 158 | ||

| 164 | ||

| 181 | ||

| 186 | ||

| 187 | ||

| 192 | ||

| 266 | ||

| 277 | ||

| 280 | ||

| 281 | ||

| 283 | ||

| 283 | ||

| 283 | ||

| F-1 |

The Floating Rate Senior Notes due 2012 are referred to as the floating rate notes, the 8 1/4% Senior Notes due 2013 are referred to as the 2013 notes and the 8 5/8% Senior Notes due 2015 are referred to as the 2015 notes. The 2013 notes and the 2015 notes are referred to collectively as the fixed rate notes. The floating rate notes and the fixed rate notes are referred to collectively as the notes. Unless we indicate differently, when we use the term “notes,” “new notes,” “floating rate notes,” “2013 notes” or “2015 notes,” we mean the new notes that we will issue to you if you exchange your original notes. However, unless we indicate differently, references to “notes” for periods prior to the exchange of the original notes for new notes means the original notes.

Table of Contents

Intelsat Subsidiary Holding Company, Ltd. will be the obligor under the notes offered hereby. You should read the following summary together with the more detailed information and financial statements and their notes included elsewhere in this prospectus. Investing in the notes involves significant risks, as described in the “Risk Factors” section. Unless otherwise indicated, or the context otherwise requires, financial information identified in this prospectus as pro forma gives effect to the consummation of the Transactions, as defined below in “—The Transactions,” in the manner described under “Unaudited Pro Forma Condensed Consolidated Financial Information.” In this prospectus, unless otherwise indicated or the context otherwise requires, all references to (1) the terms “we,” “us,” and “our” refer to Intelsat, Ltd.’s predecessor, International Telecommunications Satellite Organization, which we refer to as the IGO, with respect to periods prior to July 18, 2001 and otherwise to Intelsat, Ltd. and its currently existing subsidiaries on a consolidated basis, (2) the term “Intelsat Bermuda” refers to Intelsat (Bermuda), Ltd., Intelsat, Ltd.’s direct wholly owned subsidiary, (3) the term “Intelsat Sub Holdco” refers to Intelsat Subsidiary Holding Company, Ltd., Intelsat Bermuda’s wholly owned subsidiary and the obligor of the senior secured credit facilities and the notes offered for exchange hereby, (4) the term “Intelsat Holdings” refers to our parent, Intelsat Holdings, Ltd. (formerly Zeus Holdings Limited) and (5) the term “PanAmSat Acquisition Transactions” means the proposed acquisition of PanAmSat Holding Corporation and the related transactions discussed in this Prospectus Summary. We refer to our purchase of the North American satellites and related customer contracts and other assets from Loral Space & Communications Corporation and certain of its affiliates in March 2004 as the Intelsat Americas Transaction and to the satellites that we acquired as the Intelsat Americas, or IA, satellites. We refer to the satellites that we owned prior to the closing of the Intelsat Americas Transaction as the IS satellites. In this prospectus, unless the context otherwise requires, all references to transponder capacity or demand refer to transponder capacity or demand in the C-band and Ku-band only. Unless otherwise indicated, the description of us and our business does not give effect to, nor reflects the impact of, our proposed acquisition of PanAmSat Holding Corporation, which could close in the second or third quarter of 2006.

Our Company

We are a leading provider of fixed satellite services, with customers that include leading telecommunications companies, multinational corporations, Internet service providers, media broadcasters and government/military organizations. Founded in 1964, we have provided communications capacity for milestone events in the 20th century, including transmitting worldwide the video signals of the first moon walk, providing the “hot line” connecting the White House and the Kremlin and transmitting live television coverage of every Olympics since 1968.

Our goal is to connect people and businesses around the world with reliable, flexible and innovative communications services. We supply voice, data and video connectivity in over 200 countries and territories for over 700 customers, many of which we have had relationships with for over 30 years. We operate in an attractive, well-developed segment of the satellite communications industry that is characterized by steady and predictable contracted revenue streams and strong free cash flows, which represent cash flows from operating activities less capital expenditures. In 2004, the global fixed satellite services, or FSS, sector generated revenue of approximately $7.05 billion, and by that measure we were the second largest operator, according toEuroconsult. We generate revenue primarily from leasing capacity on our satellites, which is generally contracted for periods of up to 15 years. Our backlog, which is our

1

Table of Contents

expected actual future revenue under our customer contracts, was approximately $3.8 billion as of September 30, 2005, 97% of which relates to contracts that are non-cancellable or cancellable only upon payment of substantial termination fees.

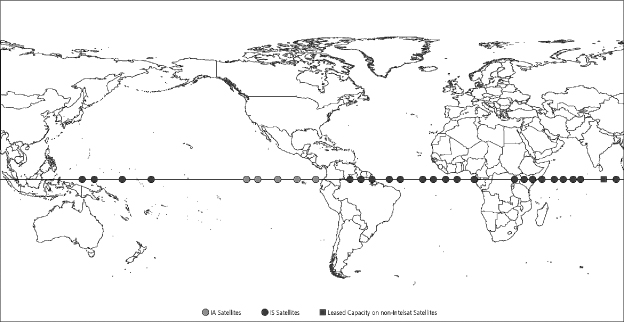

We believe that we have one of the largest, most flexible and reliable satellite fleets. Our in-orbit satellite fleet, which covers 99% of the world’s population, includes 28 satellites and leased capacity on one additional satellite, excluding our ownership interest in the Marisat-F2 satellite, which we acquired as part of the COMSAT General Transaction. Many of our satellites have steerable beams that can be reconfigured to provide different areas of coverage, and many of our satellites can be relocated to other orbital locations. The flexibility of our fleet allows us to respond quickly to changes in market conditions and customer demand. During the past 30 years, excluding the IS-804 satellite, each of the station-kept satellites we launched or acquired in the Intelsat Americas Transaction has exceeded, or is expected to exceed, its design life. Our satellite fleet is operated via ground facilities used to monitor and control our satellites and is complemented by a terrestrial network of teleports, points of presence and leased fiber links for the provision of our managed solutions.

We have invested heavily in our communications network over the past several years. Consequently, in the near term, we expect our level of capital expenditures to be significantly lower than that of recent years. We have spent approximately $2.5 billion on nine satellite launches since June 2001 in connection with our most recent satellite fleet renewal and deployment cycle, which was completed with the launch of our IA-8 satellite on June 23, 2005. The IA-9 is currently our only satellite under construction, and we do not plan to launch this satellite until 2007. The average remaining orbital maneuver life of our satellites was approximately twelve years as of September 30, 2005, weighted on the basis of available capacity for the 23 station-kept satellites of the 28 satellites we own. Assuming we complete our proposed acquisition of PanAmSat Holding Corporation, our capital expenditures are expected to increase as PanAmSat Corporation is planning to launch a number of satellites over the next few years. See “The PanAmSat Acquisition Transactions.”

In 2004, we completed two transactions in growing segments of the FSS sector. In March 2004, we completed the Intelsat Americas Transaction. The satellites and related assets acquired in the Intelsat Americas Transaction have further strengthened our leading position in the FSS sector by enhancing our capabilities for video, corporate network and government/military applications. We also purchased the business of COMSAT General Corporation and certain of its affiliates in October 2004. This transaction, which we refer to as the COMSAT General Transaction, has further strengthened our leading position in providing services for government and other military service applications.

On January 28, 2005, Intelsat Holdings acquired Intelsat, Ltd. for total cash consideration of approximately $3 billion. See “The Transactions—The Acquisition Transactions” for a description of the transaction agreement with Intelsat Holdings.

On August 28, 2005, Intelsat Bermuda entered into a Merger Agreement with PanAmSat Holding Corporation and Proton Acquisition Corporation, a wholly owned subsidiary of Intelsat Bermuda, pursuant to which Intelsat Bermuda agreed to acquire PanAmSat Holding Corporation for total cash consideration of approximately $3.2 billion. As part of this transaction, approximately $3.2 billion in debt of PanAmSat Holding Corporation and its subsidiaries will either be refinanced or remain outstanding. See “—The Transactions—The PanAmSat Acquisition Transactions” and “The PanAmSat Acquisition Transactions” for more information concerning this pending transaction.

2

Table of Contents

Our Service Sectors

We provide satellite capacity and related communications services for the transmission of voice, data and video connectivity. Our customer contracts offer different service commitment types, which fall primarily into four categories: (1) leases, (2) channel, which is primarily for voice services, (3) managed solutions and (4) mobile satellite services. Our leases and channel service commitments provide wholesale satellite capacity to our customers. Our managed solutions, which have grown rapidly since being introduced in 2001, combine satellite capacity, teleports, satellite communications hardware, fiber optic cable and other ground facilities to provide broadband, video and private network services to our customers. Our services are used to serve three sectors: (1) network services and telecom, (2) media and (3) government (for which we began tracking and reporting on January 1, 2003), each of which is described below.

Network Services and Telecom

The network services and telecom sector represented 61.6% of our revenue for the nine months ended September 30, 2005 and 67.4% of our revenue for the year ended December 31, 2004. We provide satellite capacity and managed solutions to telecommunications carriers, Internet service providers, or ISPs, and multinational corporations to support voice and data applications, including point-to-point and point-to-multipoint connections between telecommunication hubs. Highlights include the following:

| • | We were the leading provider of satellite capacity for voice and data applications in 2004, derived from data presented byEuroconsult. |

| • | We believe that the demand for satellite capacity for certain niche voice and data applications will grow. For example, the proliferation of wireless services worldwide has created demand to use satellite services for backhaul and network extensions in developing regions, due to unreliable or non-existent terrestrial infrastructure. |

| • | Our revenue from voice and data applications is highly predictable and benefits from primarily non-cancelable contracts. Based on our backlog at December 31, 2004, we expected to recognize $517.3 million in voice and data applications revenue for the nine months ended September 30, 2005, and we ultimately recognized $540.3 million in actual revenue for that period from these applications. |

| • | We provide point-to-multipoint connections for corporate network applications, including very small aperture terminals, or VSATs. |

Media

The media sector represented 17.0% of our revenue for the nine months ended September 30, 2005 and 18.7% of our revenue for the year ended December 31, 2004. Video applications currently use more FSS capacity than any other application, representing about 61% of total global FSS transponder demand in 2004, with North America being the largest user of satellite capacity for video applications, according toNorthern Sky Research. We currently offer three types of services to our media customers:

| • | video distribution services, which include the transmission of television programming for broadcasters, cable networks and other redistribution systems; |

| • | video contribution services, which include the transmission of news, sports and other video programming from various locations to a central video production studio; and |

3

Table of Contents

| • | direct-to-home, or DTH, services, which include the transmission of television channels for household reception. |

Highlights include the following:

| • | In North America, we believe that we are a leading provider of FSS capacity for the distribution of broadcast video. We also believe that we are one of the leading providers of FSS capacity for ethnic programming distribution in North America, with over 150 channels broadcast. |

| • | We are a leading provider of FSS capacity for DTH services, delivering programming to millions of viewers and supporting 11 DTH platforms around the world. |

| • | Global transponder demand for FSS video applications is forecasted to grow overall at a compound annual growth rate, or CAGR, of approximately 4.1% from 2005 to 2010, according toNorthern Sky Research. |

Government

The government sector represented 21.0% of our revenue for the nine months ended September 30, 2005 and 13.6% of our revenue for the year ended December 31, 2004. We provide satellite capacity and managed solutions for a number of applications to various government and military entities, including the U.S. government and its defense and civilian agencies, as well as NATO members. Highlights include the following:

| • | We were the largest FSS provider of government satellite services in 2004, according toEuroconsult. |

| • | The reliability of, and the ability to reconfigure, our fleet allow us to address changing demand for satellite coverage and provide mission-critical communications capability. |

| • | The U.S. government and military is the largest end user of commercial FSS satellites for government/military applications on a global basis. We currently serve more than 60 U.S. government and military users and NATO entities, either directly or as a sub-contractor. |

| • | Demand for transponder capacity on commercial FSS satellites to support U.S. government and military applications is expected to grow at a CAGR of approximately 8.4% between 2005 and 2010, according toNorthern Sky Research. |

Our Strengths

Our business is characterized by the following key strengths:

Strong Free Cash Flow and Near-Term Revenue Visibility

We believe that our increasing revenues, combined with our modest capital expenditures profile, low tax obligations and limited working capital requirements, will result in the generation of significant free cash flow. The FSS sector requires sizable up-front investment to develop and launch satellites. However, once satellites are operational, the costs of sales and operations do not vary significantly as usage of our system increases and are, with sufficient scale, low relative to the revenue that may be generated, typically resulting in high margins and

4

Table of Contents

strong free cash flow. We have spent approximately $2.5 billion on nine satellites launched since June 2001 in connection with our most recent satellite fleet renewal and deployment cycle, which was completed with the launch of our IA-8 satellite on June 23, 2005, and approximately $967.1 million to acquire four operational satellites and other assets in the Intelsat Americas Transaction. The IA-9 is currently our only satellite under construction, and we do not plan to launch this satellite until 2007. As a result, in the near term, we expect our level of capital expenditures to be significantly lower than that of recent years. Due to available capacity in our fleet, we have the potential to add customers and increase revenue without near term satellite investment or a significant increase in our costs of operations, which should increase cash flow. Assuming we complete our proposed acquisition of PanAmSat Holding Corporation, our capital expenditures are expected to increase as PanAmSat Corporation is planning to launch a number of satellites over the next few years.

Our backlog was approximately $3.8 billion as of September 30, 2005. We currently expect to deliver services associated with $896 million, or 24%, of our September 30, 2005 backlog over the twelve months ending September 30, 2006. Our backlog provides significant near-term revenue visibility, particularly since 97% of our total backlog as of September 30, 2005 relates to contracts that either are non-cancelable or have substantial termination fees. In each of the last three years, the revenue that we expected to generate from our backlog at the beginning of the year represented in excess of 80% of that year’s actual revenue.

Fleet of Reliable, Flexible, Healthy Satellites

We believe that we have one of the most technologically advanced and largest fleets of satellites in the FSS sector. Other than the IS-804 satellite which recently experienced an anomaly resulting in a total loss, the average remaining orbital maneuver life of our satellites was approximately twelve years as of September 30, 2005, weighted on the basis of available capacity for the 23 station-kept satellites of the 28 satellites we own. Our state-of-the-art engineering standards, with built-in redundancies on all of our satellites, provide for a reliable, flexible, healthy fleet. For the 365-day period ended September 30, 2005, the transponder availability rate for satellites owned and operated by us, as of that date, was 99.9919%. During the past 30 years, other than the IS-804 satellite, each of our station-kept satellites has exceeded, or is expected to exceed, its design life.

Our satellites cover 99% of the world’s population, and we provide satellite capacity in the C- and Ku-bands in over 200 countries and territories. With the launch of our IA-8 satellite, we are also able to provide satellite capacity in the Ka-band. Our fleet includes satellites in prime orbital locations with coverage of key regions such as North America and the Middle East. We also have terrestrial assets consisting of teleports, points of presence and leased fiber connectivity that complement our satellite network and enable us to provide customized managed services.

We believe that the flexibility of our satellite fleet provides us with an advantage relative to other satellite providers. Many of our satellites are equipped with steerable beams that can be moved to cover areas with higher demand. In addition, many of our satellites can be relocated to different orbital locations. The design flexibility of our satellites enables us to respond rapidly to changing market conditions and to changes in demand for satellite capacity. As an example, in 2004, the consolidation of our fleet in the Pacific Ocean Region and deployment of the 10-02 satellite to 359°E resulted in the release of two Intelsat satellites that were redeployed to address the increased demand for satellite capacity in the Africa and Middle East regions.

5

Table of Contents

Diversified Revenue and Backlog

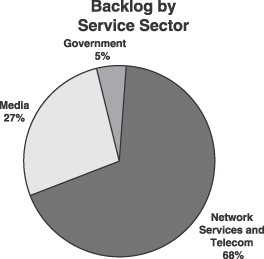

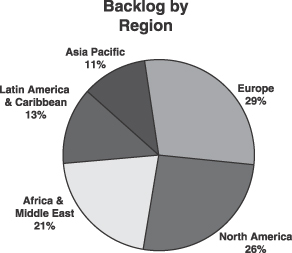

Our revenue and backlog are diversified among service sectors, geographic regions, satellites and customers. None of our satellites generated more than 10% of our revenue for the nine-month period ended September 30, 2005, and no single customer accounted for more than approximately 5% of our revenue during this period. The diversity of our revenue allows us to benefit from changing market conditions and minimizes our risk from fluctuations in any one of these categories and from difficulties that any one customer may experience. By service sector and region, our backlog as of September 30, 2005 was as follows:

|  | |

| Note: | Backlog data is calculated based on our backlog as of September 30, 2005. Regional designation for backlog is based on customer billing addresses. |

Established Relationships with Premier Customers

We provide satellite services to over 700 customers, including many of the world’s leading telecommunications companies, multinational corporations, ISPs, media broadcasters and government/military organizations. We have served many of our largest customers, including the majority of our top ten customers and their predecessors, for over 30 years. The following table includes examples of our customers for each service sector:

| Service Sector Category | Customers | |

| Network Services and Telecom | Central Bank of the Russian Federation, Equant, Hughes Network Services, Schlumberger, United Nations, World Bank | |

| AT&T, British Telecommunications, China Telecom, Global Crossing, Vodacom | ||

| Cable and Wireless, Link Africa, Sprint | ||

| Media | BBC World, Canal Digital, CBS, CNN International, MTV3, Playboy Entertainment | |

| Government | U.S. Department of Defense’s Armed Forces Radio & Television Service, Artel, National Oceanic and Atmospheric Administration, U.S. Department of State, U.S. Navy | |

6

Table of Contents

Strong Position in Growing Customer Sectors

We have strong positions in areas of the FSS sector that are experiencing growth, such as data applications, primarily for corporate and broadband data, government/military applications and video.

We were the leading provider of capacity for satellite voice and data services worldwide in 2004, derived from data presented byEuroconsult. Global transponder demand for all voice and data services is forecasted to grow at a CAGR of approximately 1.9% from 2005 to 2010, according toNorthern Sky Research. Of this growth, the majority is expected to come from enterprise and small and medium enterprise, or SME, broadband Internet protocol-based, or IP, VSAT services, which is forecasted to grow at a CAGR of approximately 12.4% from 2004 to 2009, according toNorthern Sky Research. We expect growth in the use of VSATs to continue as businesses further globalize and realize the benefits of communicating via a comprehensive satellite-based network. We also believe growth in this business will be facilitated by the continued growth of virtual private networks, referred to as VPNs, and emerging applications such as voice over Internet protocol and video over Internet protocol. Satellites are inherently well suited to deliver multiregional Internet protocol-based, or IP, networks due to their multicasting capabilities and large geographic footprints.

We were the largest FSS provider of government satellite services in 2004, according toEuroconsult. U.S. government and military demand for capacity on commercial FSS satellites is expected to grow at a CAGR of approximately 8.4% between 2005 and 2010, according toNorthern Sky Research. As a result of the current geopolitical environment and the increasing homeland security requirements of the U.S. government, government/military customers are expected to require greater commercial communications capacity for mission-critical defense and civilian applications. We attribute our strength in this area to the flexibility of our satellite fleet and the reliability of our satellites in transmitting mission-critical communications.

We are a leading provider of FSS capacity for broadcast video distribution in North America and for video contribution and DTH services around the world. Global transponder demand for FSS video applications is forecasted to grow overall at a CAGR of approximately 4.1% from 2005 to 2010, according toNorthern Sky Research. High definition television, or HDTV, programming, which requires significantly more satellite capacity to transmit a given amount of content than digital programming requires, is expected to grow rapidly in the near to mid term, especially in North America. As one of the leaders in serving North American broadcast networks, we are using our position to enable early high-definition adopters, such as CBS Sports, to move high-definition content from the creation source to their studios via our satellite network and terrestrial networks. We believe that our Intelsat Americas satellites are well positioned to serve both the cable and broadcast communities. In addition, ethnic programming in the United States has increased dramatically in the last few years to over 300 channels. Our IA-5 satellite carries over 150 channels offering such programming, including many that are brought to the United States on our system, and we believe that IA-5 carries more non-English and non-Spanish language programming than any other satellite in North America. We believe that we are well positioned in another growing video application, the distribution of DTH programming around the world. Currently, our network supports 11 DTH platforms, providing content to millions of households. We will continue our focus on developing our DTH platform business in higher-growth regions including Eastern Europe, Africa and parts of Asia, where we believe that we are well positioned.

7

Table of Contents

Our Business Strategy

Our goal is to sustain our leadership position in the FSS sector and enhance our free cash flow by pursuing the following key business strategies:

Grow Our Business in the Network Services and Telecom, Media and Government Sectors

We believe that the network services and telecom, media, and government sectors represent opportunities for revenue growth over the long term for operators in FSS services. We intend to focus our resources on penetrating these sectors further in order to increase our revenue and cash flow and to continue to diversify our customer base.

Network Services and Telecom

We believe the primary growth area for voice and data customers will be our managed solutions business. Customers are increasingly looking for more integrated services to meet their communications needs. We intend to use our leadership in providing voice and data services, as well as our flexible and reliable network, technical expertise and well-established customer relationships, to offer new services, such as our managed solutions, to existing customers and to broaden the types of customers we serve.

We are also focusing on providing capacity for niche voice and data applications, such as connectivity services for wireless operators in newly deregulated regions. We believe new carrier companies and providers of competitive services, such as wireless communications and Internet services, in these regions are seeking to introduce their services quickly and independently of the established local carriers. There are still many regions of the world that lack direct access to cable interconnects or whose internal infrastructure either does not exist or is unreliable. We intend to increase our focus on customers requiring satellite capacity for reliable connections between low-traffic communications hubs in smaller cities and from cable interconnects and communications hubs to telecommunications central offices in remote and underserved areas where we can provide a critical portion of the telecommunications infrastructure.

Media

We believe that we are well positioned to grow both the distribution and contribution portions of our video business, including capturing growth from the expected increase in demand from HDTV programming. We also intend to continue to expand our ability to offer high-definition programmers an end-to-end service, using our terrestrial network with points of presence at sports stadiums and top media centers to capture content in high definition, or HD, at the creation source and to transport it through our satellite network and terrestrial networks. This strategy has proven particularly successful in supporting HD coverage of major professional sports such as baseball and basketball. In the nine months ended September 30, 2005, we supported more than 100 transmissions in HD on our North America video fiber network.

We believe that the acquisition of the Intelsat Americas fleet has strengthened our position in the North America media sector, particularly in the areas of broadcast contribution and distribution, as well as the distribution of niche and ethnic programming. We also believe we have the ability to further strengthen our position in the distribution of ethnic programming. Our IA-5 satellite carries over 150 such channels, including many that are brought to the United

8

Table of Contents

States on our system, and we believe that IA-5 carries more non-English and non-Spanish language programming than any other satellite in North America. We intend to expand the ethnic programming neighborhood on our IA-5 satellite to accommodate demand. In addition, many U.S. cable operators are increasingly faced with the need to offer ethnic programming to compete effectively with providers of direct broadcast satellite services in the United States. We believe we can offer cable operators a rebroadcast package of international channels that is attractive from the standpoint of both cost and technical efficiency.

Additionally, we will continue to develop our DTH platform business, targeting Eastern Europe, Africa and regions within Asia where we can use our available capacity and the flexibility of our satellite fleet to capture opportunities.

Government

We were the largest provider of wholesale commercial satellite capacity to the U.S. government and military in 2004, according toEuroconsult. We believe that the defense and civilian agencies of various governments are experiencing an increased need for commercial satellite communications services, due in part to anti-terrorism efforts, conflicts in the Middle East and increased worldwide military activity. We believe we are well positioned to increase our leading position in the growing area of commercial satellite-based government/military service applications as we continue to capitalize on our strong government relationships, serving more than 60 U.S. government and NATO users, and our flexible and reliable network.

We believe that our acquisition of the Intelsat Americas fleet has strengthened our position in this sector by providing us with greater coverage of North America, which allows us to offer additional satellite capacity and services to various defense and civilian agencies of the U.S. government. The COMSAT General Transaction further strengthened our leading position serving this sector with the addition of certain managed solutions capabilities and high-level personnel who have security clearances and long-standing government customer relationships.

Capitalize on Opportunities in the Next Phase of our Transition from an IGO

We are the successor to the IGO, which was created in 1964. In July 2001, the IGO privatized by transferring substantially all of its assets and liabilities to Intelsat, Ltd. and its subsidiaries. Prior to the privatization, as the IGO, we were restricted in terms of both the services we could offer and the pricing for our services. Since privatization, we have sought to expand our service offerings, improve our sales and marketing organization and diversify our revenue through targeted acquisitions in growth areas. We believe actions in the last 24 months, many of which have only recently begun to translate into financial results, have positioned us to improve our commercial operations. We believe there are significant opportunities yet to be achieved as we enter the next phase of our transition from an IGO under private equity ownership.

Our sales and marketing team was strengthened through increased technical skills and substantially reorganized in April 2003 to better focus on capturing a larger amount of the demand in growing customer applications, where we are well positioned with the necessary capacity, and on growing our managed solutions business, which we were previously restricted in offering. The continuing decline in our channel business over the last twelve months has been largely offset in terms of backlog, which we attribute primarily to the improved performance of our sales and marketing team, expanded market opportunities as a result of the Intelsat Americas Transaction and the success of our managed solutions business, which has grown rapidly since its introduction in 2001.

9

Table of Contents

We intend to manage our operating expenses to optimize margins and free cash flow. During the last few years, we had higher staffing levels than we believe are required today to efficiently run our business. At June 1, 2004, we had 981 full-time regular employees. By the end of September 2005, we had 787 full-time regular employees, or 20% fewer employees than we had at June 1, 2004.

Build on Proven Track Record to Pursue a Disciplined Acquisition Strategy

Over the past several years, the FSS sector has been, and continues to be, reshaped as a result of consolidation, deregulation, privatization and, more recently, the increase in private equity ownership of satellite operators. Post-privatization, we have sought to strengthen our business through targeted acquisitions, and we have a successful track record of executing strategic transactions. For example, the Intelsat Americas Transaction provided us with comprehensive coverage of North America, which has significantly enhanced our video business, and the COMSAT General Transaction is strengthening our ability to provide services to government and other customers. In connection with our acquisition of the Intelsat Americas assets, we have integrated the acquired customers and assumed full control and operation of the acquired satellites with minimal increases in operational and sales staff and ahead of schedule. We have also pursued the strategic acquisition of rights to operate at certain new orbital locations, and have recently entered into a merger agreement with PanAmSat Holding Corporation. See “—The Transactions —The PanAmSat Acquisition Transactions” and “The PanAmSat Acquisition Transactions.” We believe that our two companies are complementary in customer, geographic and product focus, and that the acquisition will enable us to offer our customers expanded coverage with additional back-up satellites. We also intend to continue to evaluate and pursue strategic transactions that can broaden our customer base, provide enhanced geographic presence, provide complementary technical and commercial capabilities, further utilize our infrastructure and create operational efficiencies.

The Transactions

The Acquisition Transactions

On January 28, 2005, Intelsat, Ltd. was acquired by Intelsat Holdings for total cash consideration of approximately $3 billion with pre-acquisition debt of approximately $1.9 billion remaining outstanding. Intelsat Holdings is a Bermuda company which was formed at the direction of funds advised by or associated with Apax Partners Worldwide LLP and Apax Partners, Inc., referred to jointly as Apax Partners, Apollo Management V, L.P., referred to as Apollo, MDP Global Investors Limited, referred to as MDP Global, and Permira Advisers LLC, referred to as Permira. Each of Apax Partners, Apollo, MDP Global and Permira is referred to as a Sponsor and the funds advised by or associated with each Sponsor are referred to as an Investor group. The Investor groups collectively are referred to as the Investors. As part of the Acquisition Transactions, the Investors and certain members of management purchased preferred and ordinary shares of Intelsat Holdings, referred to as the equity contributions. Prior to the Acquisition Transactions, funds advised by or associated with MDP Global transferred less than 0.1% of their interest in Intelsat Holdings to an unaffiliated investment partnership. References to the Investors include this partnership. In connection with this acquisition transaction, the following transactions, referred to as the Amalgamation Transactions, occurred:

| • | Zeus Merger One Limited, referred to as Zeus Merger 1, a wholly owned direct subsidiary of Intelsat Holdings, amalgamated with Intelsat, Ltd., with the resulting |

10

Table of Contents

company being a direct wholly owned subsidiary of Intelsat Holdings and being named Intelsat, Ltd.; upon this amalgamation, Intelsat, Ltd.’s equity holders immediately prior to the amalgamation ceased to hold shares or other equity interests in Intelsat, Ltd.; and |

| • | Zeus Merger Two Limited, referred to as Zeus Merger 2, a wholly owned direct subsidiary of Zeus Merger 1, amalgamated with Intelsat Bermuda, which is the direct or indirect parent of all of our operating subsidiaries, with the resulting company being a direct wholly owned subsidiary of resulting Intelsat, Ltd. and being named Intelsat (Bermuda), Ltd. |

Intelsat Holdings, Zeus Merger 1 and Zeus Merger 2 were Bermuda companies that were newly formed for the purpose of consummating the Acquisition Transactions.

In connection with the completion of the Amalgamation Transactions, Zeus Merger 2, which later amalgamated with Intelsat Bermuda, established a new $300 million revolving credit facility and borrowed approximately $150 million under a new $350 million term loan facility, referred to together as the senior secured credit facilities, and issued the original notes. The proceeds from the equity contributions, borrowings under the senior secured credit facilities and the issuance of the original notes offered, together with cash on hand, were used to consummate the transactions described above and to pay related fees and expenses.

The Amalgamation Transactions occurred concurrently with the establishment of the senior secured credit facilities and the issuance of the original notes. Following the consummation of the Amalgamation Transactions, Intelsat Bermuda became the borrower under the senior secured credit facilities and the obligor under the original notes. Following the consummation of the Amalgamation Transactions, the original notes and the senior secured credit facilities were guaranteed by Intelsat, Ltd. and certain subsidiaries of Intelsat Bermuda.

The acquisition transactions and related financings described above are referred to collectively in this prospectus as the Acquisition Transactions.

On February 28, 2005, Intelsat Bermuda, drew $200 million under the $350 million term loan facility to fund the payment of Intelsat, Ltd.’s then existing $200 million of Eurobond 8 1/8% notes due 2005, referred to herein as the 2005 Eurobond Notes, at maturity in February 2005.

Approximately $1.7 billion of Intelsat, Ltd.’s existing debt remained outstanding following the Acquisition Transactions and repayment at maturity of the 2005 Eurobond Notes. This existing debt of Intelsat, Ltd. is not, and is not expected to be, guaranteed by Intelsat Bermuda or any of its subsidiaries and does not include Intelsat, Ltd.’s obligations as a co-obligor on the discount notes issued on February 11, 2005, as described below under “—The Transfer Transactions”. Approximately $57 million of Intelsat Bermuda’s and its subsidiaries’ existing debt, including capital lease obligations, remained outstanding following the Acquisition Transactions.

The Transfer Transactions

Following the Acquisition Transactions, Intelsat, Ltd. formed a new wholly owned subsidiary, Zeus Special Subsidiary Limited (which we refer to as Finance Co.), and Intelsat Bermuda formed a new wholly owned subsidiary, Intelsat Sub Holdco. On February 11, 2005, Finance Co. issued $478.7 million aggregate principal amount at maturity of 9 1/4% Senior Discount Notes due 2015, referred to as the discount notes, which yielded approximately $305 million of net proceeds at issuance.

11

Table of Contents

Following the issuance of the discount notes and the deposit of the gross proceeds by Finance Co. in a special account established by Finance Co., the following transactions took place:

| • | we filed applications with the U.S. Federal Communications Commission, referred to as the FCC, for approval of the pro forma indirect transfer of control of, and the change in indirect foreign ownership of, the five subsidiaries of our company holding FCC authorizations; |

| • | on March 3, 2005, Intelsat Bermuda transferred substantially all of its assets to Intelsat Sub Holdco and Intelsat Sub Holdco assumed substantially all of the then-existing liabilities of Intelsat Bermuda, including the original notes; and Intelsat Bermuda also became a guarantor of the senior secured credit facilities and the original notes upon the consummation of the Transfer Transactions; and |

| • | Finance Co. amalgamated with Intelsat Bermuda, with the resulting company being named Intelsat (Bermuda), Ltd. and Intelsat Bermuda becoming an obligor on the discount notes. |

Following consummation of these transactions, the proceeds of the offering of the discount notes, together with cash on hand, were used to pay a dividend from Intelsat Bermuda to its parent, Intelsat, Ltd., which Intelsat, Ltd. used to make a return of capital distribution equal to the amount of the dividend to its parent, Intelsat Holdings, which in turn used those funds to repurchase a portion of the outstanding preferred shares of Intelsat Holdings. The repurchased preferred shares were held by the Investors and certain members of our management. We refer to all of these transactions collectively as the Transfer Transactions.

12

Table of Contents

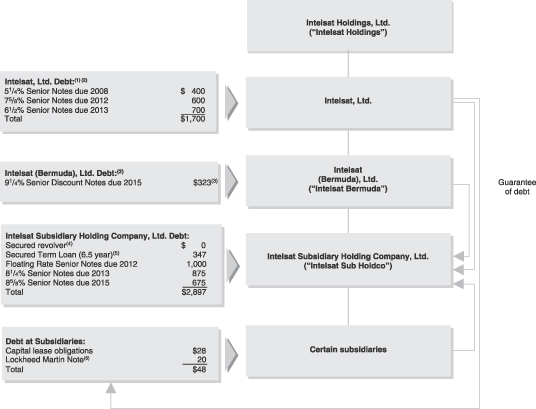

Ownership and Corporate Structure

The following chart summarizes our ownership, corporate structure and principal amount of indebtedness outstanding as of September 30, 2005.

(dollars in millions)

| (1) | Intelsat, Ltd.’s senior notes were issued at discounts. The amounts shown here do not reflect the issuance discounts. The amounts shown here do not reflect Intelsat, Ltd.’s obligations as co-obligor on the discount notes. |

| (2) | Intelsat, Ltd. is co-obligor on the discount notes. |

| (3) | This amount will accrete to approximately $478.7 million aggregate principal amount at February 1, 2010. |

| (4) | Total facility size of $300 million. |

| (5) | The term loan is a $350 million facility. |

| (6) | This note is guaranteed by Intelsat, Ltd. |

13

Table of Contents

The PanAmSat Acquisition Transactions

On August 28, 2005, Intelsat Bermuda entered into a Merger Agreement, referred to as the Merger Agreement, with PanAmSat Holding Corporation, referred to as PanAmSat, and Proton Acquisition Corporation, a wholly owned subsidiary of Intelsat Bermuda and referred to as Merger Sub. Pursuant to the Merger Agreement, Intelsat Bermuda agreed to acquire PanAmSat for total cash consideration of approximately $3.2 billion, with the shareholders of PanAmSat generally being entitled to receive $25.00 per common share (plus a pro rata share of undeclared regular quarterly dividends, if any, for the quarter in which the acquisition is consummated). Merger Sub was newly formed for the purpose of consummating the PanAmSat Acquisition Transactions (as defined below) and currently has no independent operations or assets. As part of this transaction, approximately $3.2 billion in debt of PanAmSat and its subsidiaries will either be refinanced or remain outstanding.

In connection with, and in order to effect, the transactions contemplated by the Merger Agreement and the related financing, the following transactions have occurred or are expected to occur:

| • | Intelsat Bermuda has created a new direct wholly owned subsidiary, Intelsat Intermediate Holding Company, Ltd., referred to as Intermediate Holdco; |

| • | Intelsat Bermuda will transfer substantially all its assets (other than the capital stock of Merger Sub) and liabilities (including the discount notes) to Intermediate Holdco, but will remain a guarantor of the notes and the senior secured credit facilities and will become a guarantor of the discount notes; and |

| • | Merger Sub will merge with PanAmSat, with PanAmSat continuing as the surviving corporation and being a direct wholly owned subsidiary of Intelsat Bermuda. Upon completion of this merger, referred to as the Merger Transaction, PanAmSat’s equity holders immediately prior to the merger will cease to hold shares or other equity interests in PanAmSat. |

Consummation of the Merger Transaction is subject to various closing conditions, including but not limited to the satisfaction or waiver of conditions regarding the receipt of requisite regulatory approvals, the receipt of financing by Intelsat Bermuda and the adoption of the Merger Agreement by a majority of PanAmSat’s stockholders. Under the terms of the Merger Agreement, if the agreement is terminated under specified circumstances relating to our inability to obtain financing or requisite regulatory approvals, we may be required to pay PanAmSat a termination fee of $250 million. Investment vehicles affiliated with Kohlberg Kravis Roberts & Co., the Carlyle Group and Providence Equity Partners together own approximately 58% of PanAmSat’s common stock and agreed to vote in favor of the adoption of the Merger Agreement. On October 26, 2005, PanAmSat informed us that a majority of its stockholders approved and adopted the Merger Agreement. We believe that the Merger Transaction could close in the second or third quarter of 2006.

Upon completion of the PanAmSat Acquisition Transactions, PanAmSat and Intelsat Sub Holdco will be direct or indirect wholly owned subsidiaries of Intelsat Bermuda, and PanAmSat and its subsidiaries will continue as separate corporate entities.

David McGlade is expected to continue to serve as Chief Executive Officer, or CEO, and a Director of Intelsat, Ltd. following the consummation of the Merger Transaction. Joseph Wright,

14

Table of Contents

the current Chief Executive Officer and a Director of PanAmSat, is expected to become our Chairman upon completion of the Merger Transaction, pending successful negotiation of the terms and conditions of his employment.

Intelsat Bermuda has received financing commitments for the full amount of the purchase price from a group of financial institutions. The funding of the commitments is subject to certain conditions, including satisfaction of the conditions to the Merger Transaction. A substantial portion of the financing for the PanAmSat Acquisition Transactions is expected to be raised by Intelsat Bermuda, with additional financing expected to be raised by PanAmSat, PanAmSat Corporation (a direct subsidiary of PanAmSat) and Intelsat Sub Holdco. A portion of the financing raised by Intelsat Bermuda may be guaranteed by Intelsat Sub Holdco and certain of its subsidiaries. The net proceeds from these funding transactions, together with cash on hand, will be used to consummate the PanAmSat Acquisition Transactions and to pay related fees and expenses.

Consummation of the Merger Transaction is expected to result in a change of control under the indentures governing certain outstanding notes of PanAmSat and its subsidiary, PanAmSat Corporation, giving the holders of these notes the right to require the issuers thereof to repurchase these notes at the prices stated in these indentures. We believe, based on current trading levels of these notes, that the holders of these notes are not likely to exercise these rights, although there is no assurance that this will be the case. In addition, consummation of the Merger Transaction will require us to seek consents and obtain certain amendments under our existing senior secured credit facilities and the secured credit facilities of PanAmSat Corporation. We believe we will be able to obtain these consents and amendments, although there is no assurance that this will be the case. The financing commitments referred to above include a commitment from the financial institutions party thereto to provide us with funding to cover these repurchase obligations in the event the holders of these notes exercise these repurchase rights and to provide us and PanAmSat Corporation with replacement credit facilities in the event the required consents and amendments under existing credit facilities are not obtained.

The transactions described above, including the Merger Transaction, the funding transactions and the use of cash on hand, are referred to collectively in this prospectus as the PanAmSat Acquisition Transactions. For more information regarding the PanAmSat Acquisition Transactions, see “The PanAmSat Acquisition Transactions.”

The Acquisition Transactions, the Transfer Transactions and the PanAmSat Acquisition Transactions are referred to collectively in this prospectus as the Transactions.

15

Table of Contents

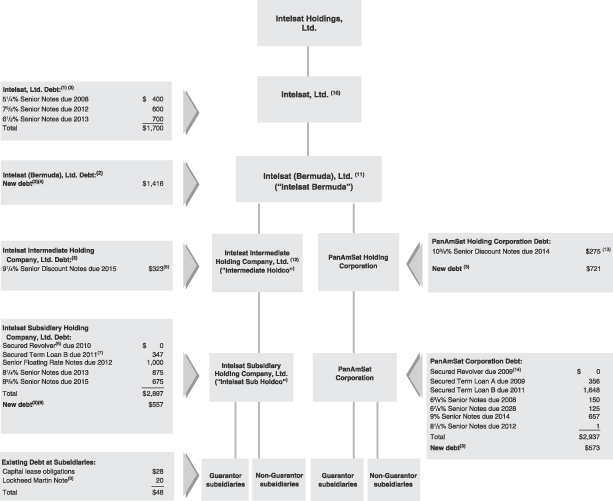

The following chart summarizes our expected ownership, corporate structure and principal amount of indebtedness outstanding upon completion of the PanAmSat Acquisition Transactions. The amount of existing indebtedness shown below for each of Intelsat, Ltd. and its subsidiaries and PanAmSat and its subsidiaries is as of September 30, 2005.

(dollars in millions)

| (1) | Intelsat, Ltd.’s senior notes were issued at discounts. The amounts shown here do not reflect the issuance discounts. The amounts shown here do not reflect Intelsat, Ltd.’s obligations as co-obligor on the discount notes. |

| (2) | Intelsat, Ltd. is co-obligor on the discount notes. |

| (3) | The amount of new debt is based on current expectations and is subject to change. The actual amount and type of debt to be incurred by each of Intelsat Bermuda, Intelsat Sub Holdco, PanAmSat Holding Corporation and PanAmSat Corporation will be determined based on market conditions, as well as on cash flows on the closing date of the PanAmSat Acquisition Transactions, and will be issued in a manner consistent with applicable requirements of covenants in indentures and credit facilities. The aggregate amount of new debt to be incurred by these entities in connection with the PanAmSat Acquisition Transactions is not expected to exceed $3.267 billion in aggregate principal amount. This chart also assumes no exercise of the rights of holders of PanAmSat Holding Corporation’s and PanAmSat Corporation’s outstanding notes to require the issuers thereof to repurchase these notes upon a change ofcontrol. |

(footnotes continued on next page)

16

Table of Contents

| (4) | This amount of new debt does not include an additional $357 million of debt that may be issued by Intelsat Bermuda, which debt is expected to be guaranteed by Intelsat Sub Holdco and its subsidiariesthat guarantee Intelsat Sub Holdco’s notes. |

| (5) | This amount will accrete to approximately $478.7 million aggregate principal amount at February 1, 2010. |

| (6) | Total facility size of $300 million. |

| (7) | The term loan is a $350 million facility. |

| (8) | This note is guaranteed by Intelsat, Ltd. |

| (9) | The amount of new debt to be issued by Intelsat Sub Holdco includes $357 million of debt that may be issued by Intelsat Bermuda and is expected to be guaranteed by Intelsat Sub Holdco and its subsidiariesthat guarantee Intelsat Sub Holdco’s notes. |

| (10) | Intelsat, Ltd. guarantees the debt of Intelsat Sub Holdco. |

| (11) | Intelsat Bermuda is expected to guarantee the debt of Intermediate Holdco and Intelsat Sub Holdco. |

| (12) | Intermediate Holdco is expected to guarantee the debt of Intelsat Sub Holdco. |

| (13) | This amount will accrete to approximately $416 million aggregate principal amount at November 1, 2014. |

| (14) | Total facility size of $250 million. |

Recent Development

On November 4, 2005, Intelsat Sub Holdco paid a dividend of approximately $198.8 million to its parent Intelsat Bermuda, which in turn paid a dividend of that same amount to its parent Intelsat, Ltd., which in turn paid a dividend of that same amount to its parent Intelsat Holdings. On November 4, 2005, Intelsat Holdings used these funds to repurchase all of the outstanding preferred shares of Intelsat Holdings, which were held by the Investors and certain members of our management. The dividend paid by Intelsat Sub Holdco was funded with cash generated from the operating activities of its subsidiaries.

17

Table of Contents

The Sponsors

Apax Partners

Apax Partners, which includes Apax Partners Worldwide LLP, Apax Partners, L.P. and their affiliates, is a leading global private equity firm, with offices in London, Madrid, Menlo Park, Milan, Munich, New York, Paris, Stockholm and Tel Aviv. With over 30 years of experience, Apax Partners focuses on the following industry sectors: information technology, telecommunications, healthcare, media, financial services and retail/consumer. Funds advised by Apax Partners invest in companies at different stages of development from late venture through to buy-out. Apax Partners has funds under advice or management totaling approximately $20 billion globally.

Apollo Management, L.P.

Apollo Management, L.P. was founded in 1990 and is among the most active and successful private investment firms in the United States in terms of both the number of investment transactions completed and aggregate dollars invested. Since its inception, Apollo and its affiliated investment entities have invested in excess of $13 billion in corporate transactions, in a wide variety of industries, both domestically and internationally. Apollo has significant expertise in the satellite sector through investments in Sirius Satellite Radio Inc. and SkyTerra Communications, Inc.

MDP Global Investors Limited

MDP Global Investors Limited is affiliated with Madison Dearborn Partners, LLC, a private equity firm, based in Chicago, referred to as Madison Dearborn Partners. Madison Dearborn Partners is one of the largest and most experienced private equity firms in the United States. Madison Dearborn Partners has $8 billion of equity capital under management and makes new investments through its most recent fund, Madison Dearborn Capital Partners IV, L.P., a $4 billion fund raised in 2001. Madison Dearborn Partners focuses on management buyout and other private equity investments across a broad spectrum of industries, including basic industries, communications, consumer, financial services and healthcare. Over the last decade, Madison Dearborn Partners has been an active investor in the communications sector, with investments in such companies as Clearnet Communications, Nextel Partners, Omnipoint Corporation, Telemundo Communications Group and XM Satellite Radio.

Permira

Permira, which includes Permira Advisers LLC and various other entities which act as advisers and consultants to the Permira funds, is a leading global private equity firm, advising funds of $13 billion. Permira is an independent business with offices in New York, Frankfurt, London, Madrid, Milan, Paris, Stockholm and Tokyo, focusing on buyout transactions across a number of sectors, including technology and telecommunications, consumer, business services, chemicals, industrial products and services, and healthcare. Since 1985, funds advised by Permira have invested in more than 260 transactions and have an investor base comprising principally public and corporate pension funds and other institutions.

18

Table of Contents

The Exchange Offer

Notes Offered for Exchange | We are offering up to: |

| • | $1,000,000,000 in aggregate principal amount of our new Floating Rate Senior Notes due 2012 in exchange for an equal aggregate principal amount of our original Floating Rate Senior Notes due 2012 on a one-for-one basis; |

| • | $875,000,000 in aggregate principal amount of our new 8 1/4% Senior Notes due 2013 in exchange for an equal aggregate principal amount of our original 8 1/4% Senior Notes due 2013 on a one-for-one basis; and |

| • | $675,000,000 in aggregate principal amount of our new 8 5/8% Senior Notes due 2015 in exchange for an equal aggregate principal amount of our original 8 5/8% Senior Notes due 2015 on a one-for-one basis. |

The new notes have substantially the same terms as the original notes you hold, except that the new notes have been registered under the Securities Act of 1933, as amended, referred to as the Securities Act of 1933, and therefore will be freely tradable and will not contain the provisions for an increase in the interest rate related to defaults in our agreement to carry out this exchange offer. |

The Exchange Offer | We are offering to exchange $1,000 principal amount of new notes for each $1,000 principal amount of your original notes. In order to be exchanged, your original notes must be properly tendered and accepted. All original notes that are validly tendered and not withdrawn will be exchanged. |

Ability to Resell Notes | We believe that the new notes issued in the exchange offer may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act of 1933 if: |

| • | the notes issued in the exchange offer are being acquired in the ordinary course of your business; |

| • | you are not participating, do not intend to participate and have no arrangement with any person to participate in the distribution of notes issued to you in the exchange offer; |

| • | you are not an affiliate of ours; and |

| • | you are not a broker-dealer tendering original notes acquired directly from us for your own account. |

19

Table of Contents

By tendering your original notes as described below, you will be making representations to this effect. See “The Exchange Offer—Representations We Need From You Before You May Participate in the Exchange Offer.” |

Those Excluded from the Exchange Offer | You may not participate in the exchange offer if you are: |

| • | a holder of original notes in any jurisdiction in which the exchange offer is not, or your acceptance will not be, legal under the applicable securities or blue sky laws of that jurisdiction; or |

| • | a holder of original notes who is an affiliate of ours. |

Consequences of Failure to Exchange Your Original Notes | After the exchange offer is complete, you will no longer be entitled to exchange your original notes for registered notes. If you do not exchange your original notes for new notes in the exchange offer, your original notes will continue to have the restrictions on transfer contained in the original notes and in the indenture governing the original notes. In general, your original notes may not be offered or sold unless registered under the Securities Act of 1933, unless there is an exemption from, or unless in a transaction not governed by, the Securities Act of 1933 and applicable state securities laws. We have no current plans to register your original notes under the Securities Act of 1933. |

Expiration Date | The exchange offer expires at 5:00 p.m., New York City time, on March 13, 2006, the expiration date, unless we extend the offer. We do not currently intend to extend the expiration date. |

Conditions to the Exchange Offer | The exchange offer has customary conditions that may be waived by us. There is no minimum amount of original notes that must be tendered to complete the exchange offer. |

Procedures for Tendering Your Original Notes | If you wish to tender your original notes for exchange in the exchange offer, you or the custodial entity through which you hold your notes must send to Wells Fargo Bank, National Association, the exchange agent, on or before the expiration date of the exchange offer: |

| • | a properly completed and executed letter of transmittal, which has been provided to you with this prospectus, together with your original notes and any other documentation requested by the letter of transmittal; and |

20

Table of Contents

| • | for holders who hold their positions through The Depository Trust Company, referred to as DTC: |

| – | an agent’s message from DTC stating that the tendering participant agrees to be bound by the letter of transmittal and the terms of the exchange offer; |

| – | your original notes by timely confirmation of book-entry transfer through DTC; and |

| – | all other documents required by the letter of transmittal. |

Holders who hold their positions through Euroclear and Clearstream, Luxembourg must adhere to the procedures described in “The Exchange Offer—Procedures for Tendering Your Original Notes.” |

Special Procedures for Beneficial Owners | If you beneficially own original notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and you wish to tender your original notes in the exchange offer, you should contact the registered holder promptly and instruct it to tender on your behalf. |

Guaranteed Delivery Procedures for Tendering Original Notes | If you wish to tender your original notes and the original notes are not immediately available, or time will not permit your original notes or other required documents to reach Wells Fargo Bank, National Association before the expiration date, or the procedure for book-entry transfer cannot be completed on a timely basis, you may tender your original notes according to the guaranteed delivery procedures set forth under “The Exchange Offer—Guaranteed Delivery Procedures.” |

Withdrawal Rights | You may withdraw the tender of your original notes at any time prior to 5:00 p.m., New York City time, on the expiration date. |

U.S. Tax Considerations | The exchange of original notes for new notes should not constitute a taxable event for U.S. federal income tax purposes. Rather, the notes you receive in the exchange offer will be treated as a continuation of your investment in the original notes. For additional information regarding U.S. federal income tax considerations, you should read the discussion under “Taxation—United States.” |

Use of Proceeds | We will not receive any proceeds from the issuance of the notes in the exchange offer. We will pay all expenses incidental to the exchange offer. |

21

Table of Contents

Exchange Agent | Wells Fargo Bank, National Association is serving as the exchange agent. Its address, telephone number and facsimile number are: |

Wells Fargo Bank, N.A.

Corporate Trust Services

608 2nd Avenue South

Northstar East Building—12th Floor

Minneapolis, MN 55402

Telephone: (800) 334-5128

Fax: (612) 667-6282

Please review the information under the heading “The Exchange Offer” for more detailed information concerning the exchange offer.

22

Table of Contents

The Notes

The summary below describes the principal terms of the notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The “Description of the Notes” section of this prospectus contains a more detailed description of the terms and conditions of the notes.

Issuer | Intelsat Sub Holdco |

The Notes | The terms of the new notes will be identical in all material respect to the terms of the original notes, except that the new notes have been registered and therefore will not contain transfer restrictions and will not contain the provisions for an increase in the interest rate related to defaults in the agreement to carry out this exchange offer. |

Maturity | The Floating Rate Notes will mature on January 15, 2012; |

The 2013 Notes will mature on January 15, 2013; and |

The 2015 Notes will mature on January 15, 2015. |

Interest Rate | The Floating Rate Notes will bear interest at a rate per annum equal to LIBOR plus 4 7/8%, with interest on the Floating Rate Notes resetting semi-annually; |

The 2013 Notes will bear interest at a rate of 8 1/4% per annum; and |

The 2015 Notes will bear interest at a rate of 8 5/8% per annum. |

Interest Payment Dates | Interest will be paid on the Floating Rate Notes and the Fixed Rate Notes on each January 15 and July 15, beginning on July 15, 2006, including accrued interest from the most recent date on which interest was paid on the original notes. |

Guarantees | Intelsat, Ltd., Intelsat Bermuda, Intermediate Holdco (expected upon consummation of the PanAmSat Acquisition Transactions) and certain of the direct and indirect subsidiaries of Intelsat Sub Holdco that guarantee Intelsat Sub Holdco’s obligations under the senior secured credit facilities will unconditionally guarantee the notes. |

The subsidiaries of Intelsat Sub Holdco that will not guarantee the notes represented approximately 21% of Intelsat Sub Holdco’s consolidated total revenue and approximately 8% of operating income for the period February 1, 2005 to September 30, 2005 and approximately 4% of its consolidated total assets as of September 30, 2005. |

23

Table of Contents

In the future, certain other of our subsidiaries may guarantee the notes. |

Ranking | The notes will rank equally in right of payment with all of Intelsat Sub Holdco’s existing and future senior unsecured debt. The notes will be effectively subordinated to Intelsat Sub Holdco’s existing and future secured debt to the extent of the assets securing that indebtedness and structurally subordinated to all obligations of each of our existing and future subsidiaries that are not guarantors. |

The guarantees of the notes will be the guarantors’ senior unsecured obligations, ranking equally in right of payment with all of each guarantor’s existing and future senior unsecured debt. The guarantees will be effectively subordinated to each guarantor’s existing and future secured debt to the extent of the assets securing that indebtedness and structurally subordinated to all obligations of any subsidiary of a guarantor if that subsidiary is not a guarantor. |

As of September 30, 2005, Intelsat Sub Holdco and its subsidiaries had approximately $2.94 billion principal amount of total debt, $347.4 million of which was secured debt, and $211.1 million of availability under our revolving credit facility. As of September 30, 2005, Intelsat, Ltd. had approximately $1.7 billion principal amount of indebtedness outstanding, excluding its guarantees of the senior secured credit facilities, the original notes, a note payable to Lockheed Martin Corporation and its obligations as co-obligor on the discount notes. As of September 30, 2005, Intelsat Bermuda had approximately $323 million principal amount of indebtedness outstanding, excluding its guarantees of the senior secured credit facilities and the original notes. |

As of September 30, 2005, pro forma for the PanAmSat Acquisition Transactions (assuming the transactions and the related financings close on the terms and in the amounts described herein), (w) Intelsat Sub Holdco and its subsidiaries would have had approximately $3.50 billion principal amount of total debt (including the guarantee by Intelsat Sub Holdco and certain of its subsidiaries of debt issued by Intelsat Bermuda), (x) Intermediate Holdco (which, following consummation of the PanAmSat Acquisition Transactions, is expected to be an obligor of the discount notes) would have had approximately $323 million principal amount of total debt (excluding guarantees of subsidiary debt), (y) Intelsat Bermuda would have had approximately $1.4 billion principal amount of total debt (excluding guarantees of subsidiary debt and debt issued by Intelsat Bermuda that is guaranteed by |

24

Table of Contents

Intelsat Sub Holdco and certain of its subsidiaries) and (z) Intelsat, Ltd. would have had approximately $11.4 billion principal amount of total indebtedness on a consolidated basis, $2.7 billion of which would have been secured debt. The amounts of indebtedness described in the previous sentence are estimates only and may change based on market conditions, available cash flows of the issuers and the actual types and amounts of debt outstanding and issued on the closing date. See “—The Transactions — The PanAmSat Acquisition Transactions” and “The PanAmSat Acquisition Transactions.” |

Optional Redemption | Intelsat Sub Holdco may redeem all or a portion of the 2013 Notes at any time prior to January 15, 2009 and the 2015 Notes at any time prior to January 15, 2010, in each case at a price equal to 100% of the principal amount thereof plus the make-whole premium described in the “Description of the Notes” section under the heading “Optional Redemption.” |

Thereafter, in each of the aforementioned cases, and after July 15, 2005 in the case of the Floating Rate Notes, Intelsat Sub Holdco may redeem all or a portion of the new notes at the redemption prices listed in the “Description of the Notes” section under the heading “Optional Redemption,” plus accrued and unpaid interest. |

Optional Redemption After Equity Offerings | At any time, which may be more than once, before January 15, 2008, Intelsat Sub Holdco can choose to redeem up to 35% of the applicable outstanding Fixed Rate Notes with the proceeds of certain equity offerings and capital contributions, as long as: |

| • | Intelsat Sub Holdco pays a redemption price equal to: 108.25% of the principal amount thereof in the case of the 2013 Notes and 108.625% of the principal amount thereof in the case of the 2015 Notes, in each case, plus accrued and unpaid interest to the date of redemption; |

| • | the applicable notes are redeemed within 90 days of completing such equity offering or of such capital contribution; and |

| • | at least 65% of the aggregate principal amount of the applicable series of notes remains outstanding afterwards. |

Change of Control Offer | If a change of control of Intelsat Sub Holdco occurs (other than the Acquisition Transactions and any related change in the composition of our Board of Directors), Intelsat |

25

Table of Contents

Sub Holdco must give holders of the notes the opportunity to sell Intelsat Sub Holdco their notes at 101% of their face amount, plus accrued interest. |

Intelsat Sub Holdco might not be able to pay you the required price for notes you present to us at the time of a change of control, because: |

| • | Intelsat Sub Holdco might not have enough funds at that time; or |

| • | the terms of Intelsat Sub Holdco’s other debt may prevent us from paying. |

Asset Sale Proceeds | If Intelsat Sub Holdco or its subsidiaries engage in asset sales or receive certain proceeds from certain events of loss, Intelsat Sub Holdco generally must either invest the net cash proceeds from such sales or events of loss in our business within a specified period of time, prepay senior debt or make an offer to purchase a principal amount of the notes equal to the excess net cash proceeds. The purchase price of the notes will be 100% of their principal amount, plus accrued interest. |

Certain Indenture Provisions | The indenture governing each series of the notes will contain covenants that, among other things, limit Intelsat Sub Holdco’s and certain of its subsidiaries’ ability to: |

| • | incur additional debt; |

| • | pay dividends or distributions on Intelsat Sub Holdco’s ordinary shares or repurchase Intelsat Sub Holdco’s ordinary shares; |

| • | make certain investments; |

| • | create liens on their assets to secure debt; |

| • | enter into transactions with affiliates; |

| • | merge, consolidate or amalgamate with another company; and |

| • | transfer and sell assets. |

These covenants are subject to a number of important limitations and exceptions. |

Risk Factors | Investing in the notes involves substantial risks. See “Risk Factors” for a description of certain of the risks you should consider before investing in the notes. |

26

Table of Contents

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL DATA

The following information is only a summary and should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” “Unaudited Pro Forma Condensed Consolidated Financial Information” and our consolidated audited and unaudited financial statements and their notes included elsewhere in this prospectus, as well as the other financial information included in this prospectus. Because of our disposal of our investment in Galaxy Satellite TV Holdings Limited, referred to as Galaxy, in December 2004, our historical financial information for the years ended December 31, 2003 and 2004 and the nine months ended September 30, 2004 has been adjusted to present Galaxy’s activities as discontinued operations.

The summary historical consolidated financial data for Intelsat, Ltd. as of and for the years ended December 31, 2002, 2003 and 2004 has been derived from our audited financial statements for these years, which have been prepared in accordance with U.S. GAAP. The consolidated statement of operations data for each of the years in the three-year period ended December 31, 2004 and the consolidated balance sheet data as of December 31, 2003 and 2004 have been derived from Intelsat, Ltd.’s consolidated financial statements included elsewhere in this prospectus. The consolidated balance sheet data as of December 31, 2002 has been derived from consolidated financial statements that are not included in this prospectus. The consolidated statement of operations data for the nine months ended September 30, 2004, for the periods January 1 to January 31, 2005 (predecessor entity) and February 1 to September 30, 2005 (successor entity) and the consolidated balance sheet data as of September 30, 2005 are derived from unaudited financial statements included elsewhere in this prospectus. The unaudited financial statements have been prepared on the same basis as the audited financial statements and, in the opinion of our management, include all adjustments, consisting only of normal recurring adjustments, necessary for a fair presentation of the information set forth herein. Interim financial results are not necessarily indicative of results that may be expected for the full year or any future reporting period.