UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number: 811-21829

BBH TRUST

On behalf of the following series:

BBH Partner Fund – Small Cap Equity

BBH Select Series – Mid Cap Fund

BBH Partner Fund – International Equity

BBH Limited Duration Fund

BBH Income Fund

BBH Select Series – Large Cap Fund

BBH Intermediate Municipal Bond Fund

BBH U.S. Government Money Market Fund

(Exact name of registrant as specified in charter)

140 Broadway, New York, NY 10005

(Address of principal executive offices) (Zip Code)

Corporation Services Company

251 Little Falls Drive

Wilmington, DE 19808

(Name and address of agent for service)

Registrant’s telephone number, including area code: (800) 575-1265

Date of fiscal year end: October 31

Date of reporting period: October 31, 2022

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders. |

Annual Report

OCTOBER 31, 2022

BBH Partner Fund - Small Cap Equity

BBH PARTNER FUND - SMALL CAP EQUITY

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

October 31, 2022

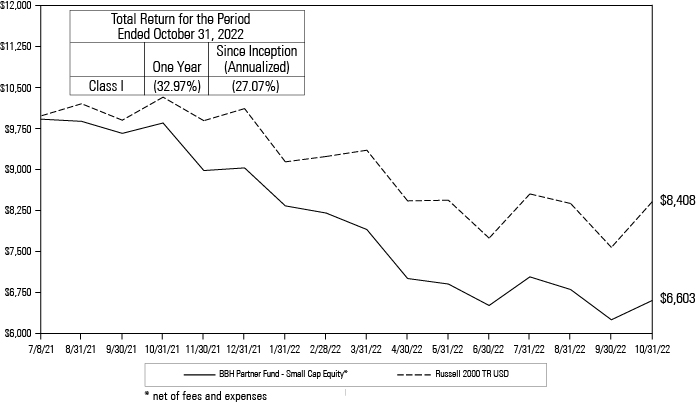

The BBH Partner Fund – Small Cap Equity (“the Fund” or “BBH Small Cap”) returned -32.97%, net of fees, for the fiscal year ended October 31, 2022. During the same twelve-month period, the Fund’s benchmark, the Russell 2000, returned -18.54%. From the inception of the Fund through October 31, 2022, the Fund has generated an annualized return of -27.07%, net of fees, while the Russell 2000 has returned -12.35% per annum.

For fiscal 2022, the Fund underperformed its benchmark, driven by security selection within Health Care, an overweight to Technology and individual security performance from the following holdings: Stitch Fix, Cimpress PLC, Zuora Inc, PagerDuty Inc, and Alarm.com Holdings Inc. The largest positive contributors to performance during the same time period include: Agilysys Inc, Model N Inc, Mimecast Ltd, XPEL Inc, Franklin Covey Co, and an overweight to cash relative to the Russell 2000 Index.

The Fund’s Sub-advisor, Bares Capital Management, LLC (“Bares”), has invested the Fund in a concentrated portfolio of small cap companies that Bares believes can compound intrinsic value at high rates over the long-term. The key criteria that Bares uses to evaluate a company are as follows:

•

Competitive Advantage: to assess a company’s competitive position, the Bares team performs a Porter’s 5 Forces analysis to determine buyer power, supplier power, the threat of substitutes and new entrants, and the competitive rivalry and industry dynamics. They will also analyze the sources of a company’s “moat,” which can be any of the following, including a significant cost advantage, efficient scale, network effects, switching costs, or the possession of intangible assets such as brand power.

•

Management Talent: the Bares team focuses on assessing management’s ability to execute and operate the business, whether they are trustworthy and transparent, and that their incentives are aligned with minority shareholders. Bares must be able to trust that the management team will use capital efficiently to generate the highest returns, which could include reinvesting in the core business, acquiring another company, or repurchasing its own shares in the open market.

•

Growth Potential: the Bares team aims to identify and evaluate companies with underappreciated sources of growth. In addition to determining a reasonable estimate of a business’ total addressable market, the team also qualitatively determines a company’s runway for growth and will selectively reassess the long-term potential if they believe growth can continue at an elevated rate.

Bares believes that the companies with the greatest potential to compound intrinsic value at above-average rates have durable competitive advantages, large growth opportunities, superior returns on equity (achieved without excessive leverage) and that are led by skilled managers who are good stewards of shareholder capital. To find such companies, the Bares team places heavy emphasis on assessing the quality of a business and its management team through extensive, on the ground due diligence and research.

________________

Portfolio holdings are subject to change. |

2

BBH PARTNER FUND - SMALL CAP EQUITY

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (continued)

October 31, 2022

Growth of $10,000 Invested in BBH Partner Fund – Small Cap Equity

The graph below illustrates the hypothetical investment of $10,0001 in the Class I shares of the Fund since inception (July 8, 2021) to October 31, 2022 as compared to the Russell 2000 TR USD.

The annualized gross expense ratio as shown in the March 1, 2022 prospectus for Class I shares was 0.93%.

Performance data quoted represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund performance changes over time and current performance may be lower or higher than what is stated. Fund shares redeemed within 30 days of purchase are subject to a redemption fee of 2.00%. Returns do not reflect the deductions of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. For performance current to the most recent month-end please call 1-800-575-1265.

________________

1 | The Fund’s performance assumes the reinvestment of all dividends and distributions. The Russel 2000 TR USD index has been adjusted to reflect reinvestment of dividends on securities in the index. The Russel 2000 TR USD index is not adjusted to reflect sales charges, expenses or other fees that the Securities and Exchange Commission requires to be reflected in the Fund’s performance. The Russell 2000 TR USD is a stock index that tracks 2,000 publicly traded small-capitalization companies. The index is unmanaged. Investments cannot be made in an index. |

The Fund seeks to generate attractive returns over time but does not attempt to mirror a benchmark or an index. The composition of the Russell 2000 Index is materially different than the Fund’s holdings. |

financial statements october 31, 2022 | 3 |

BBH PARTNER FUND - SMALL CAP EQUITY

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE (continued)

October 31, 2022

Hypothetical performance results are calculated on a total return basis and include all portfolio income, unrealized and realized capital gains, losses and reinvestment of dividends and other earnings. No one shareholder has actually achieved these results and no representation is being made that any actual shareholder achieved, or is likely to achieve, similar results to those shown. Hypothetical performance does not represent actual trading and may not reflect the impact of material economic and market factors. Undue reliance should not be placed on hypothetical performance results in making an investment decision.

4

BBH PARTNER FUND - SMALL CAP EQUITY

REPORT OF INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

To the Trustees of BBH Trust and Shareholders of BBH Partner Fund – Small Cap Equity:

Opinion on the Financial Statements and Financial Highlights

We have audited the accompanying statement of assets and liabilities, including the portfolio of investments, of BBH Partner Fund – Small Cap Equity, one of the funds within BBH Trust (the "Fund"), as of October 31, 2022, the related statement of operations for the year then ended, statements of changes in net assets and financial highlights for the year ended October 31, 2022, and the period from July 8, 2021 (commencement of operations) through October 31, 2021, and the related notes. In our opinion, the financial statements and financial highlights present fairly, in all material respects, the financial position of the Fund as of October 31, 2022, the results of its operations for the year then ended, and the changes in its net assets and the financial highlights for the year ended October 31, 2022, and the period from July 8, 2021 (commencement of operations) through October 31, 2021, in conformity with accounting principles generally accepted in the United States of America.

Basis for Opinion

These financial statements and financial highlights are the responsibility of the Fund's management. Our responsibility is to express an opinion on the Fund's financial statements and financial highlights based on our audits. We are a public accounting firm registered with the Public Company Accounting Oversight Board (United States) (PCAOB) and are required to be independent with respect to the Fund in accordance with the U.S. federal securities laws and the applicable rules and regulations of the Securities and Exchange Commission and the PCAOB.

We conducted our audits in accordance with the standards of the PCAOB. Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement, whether due to error or fraud. The Fund is not required to have, nor were we engaged to perform, an audit of its internal control over financial reporting. As part of our audits we are required to obtain an understanding of internal control over financial reporting but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion.

Our audits included performing procedures to assess the risks of material misstatement of the financial statements and financial highlights, whether due to error or fraud, and performing procedures that respond to those risks. Such procedures included examining, on a test basis, evidence regarding the amounts and disclosures in the financial statements and financial highlights. Our audits also included evaluating the accounting principles used and significant estimates made by management, as well as evaluating the overall presentation of the financial statements and financial highlights. Our procedures included confirmation of securities owned as of October 31, 2022, by correspondence with the custodian and brokers. We believe that our audits provide a reasonable basis for our opinion.

/s/ DELOITTE & TOUCHE LLP

Boston, Massachusetts

December 21, 2022

We have served as the auditor of one or more Brown Brothers Harriman investment companies since 1991.

financial statements october 31, 2022 | 5 |

BBH PARTNER FUND - SMALL CAP EQUITY

PORTFOLIO ALLOCATION

October 31, 2022

SECTOR DIVERSIFICATION

U.S. $ Value | Percent of Net Assets | ||||||

Common Stock: | |||||||

Basic Materials | $ | 15,480,000 | 4.5 | % | |||

Communications | 31,565,000 | 9.2 | |||||

Consumer Cyclical | 59,115,000 | 17.2 | |||||

Consumer Non-Cyclical | 82,291,652 | 23.9 | |||||

Financials | 3,732,800 | 1.1 | |||||

Industrials | 13,877,203 | 4.0 | |||||

Technology | 128,515,500 | 37.3 | |||||

Cash and Other Assets in Excess of Liabilities | 9,477,269 | 2.8 | |||||

NET ASSETS | $ | 344,054,424 | 100.0 | % | |||

All data as of October 31, 2022. The Fund's sector diversification is expressed as a percentage of net assets and may vary over time.

The accompanying notes are an integral part of these financial statements.

6

BBH PARTNER FUND - SMALL CAP EQUITY

PORTFOLIO OF INVESTMENTS

October 31, 2022

Shares | Value | ||||||||||

COMMON STOCK (97.2%) | |||||||||||

BASIC MATERIALS (4.5%) | |||||||||||

$ | 900,000 | Element Solutions, Inc. | $ | 15,480,000 | |||||||

Total Basic Materials | 15,480,000 | ||||||||||

| COMMUNICATIONS (9.2%) | ||||||||||

1,750,000 | Despegar.com Corp. (British Virgin Islands)1 | 11,130,000 | |||||||||

500,000 | Upwork, Inc.1 | 6,725,000 | |||||||||

1,000,000 | WideOpenWest, Inc.1 | 13,710,000 | |||||||||

Total Communications | 31,565,000 | ||||||||||

| CONSUMER CYCLICAL (17.2%) | ||||||||||

200,000 | Papa John's International, Inc. | 14,526,000 | |||||||||

2,500,000 | ThredUp, Inc. (Class A)1 | 3,075,000 | |||||||||

600,000 | XPEL, Inc.1 | 41,514,000 | |||||||||

Total Consumer Cyclical | 59,115,000 | ||||||||||

| CONSUMER NON-CYCLICAL (23.9%) | ||||||||||

522,800 | Alarm.com Holdings, Inc.1 | 30,761,552 | |||||||||

400,000 | Cimpress, Plc. (Ireland)1 | 9,312,000 | |||||||||

400,000 | EVERTEC, Inc. (Puerto Rico) | 14,324,000 | |||||||||

150,000 | Franklin Covey Co.1 | 7,590,000 | |||||||||

110,000 | Heska Corp.1 | 7,893,600 | |||||||||

150,000 | Inmode, Ltd. (Israel)1 | 5,148,000 | |||||||||

250,000 | iRadimed Corp. | 7,262,500 | |||||||||

Total Consumer Non-Cyclical | 82,291,652 | ||||||||||

FINANCIALS (1.1%) | |||||||||||

40,000 | StoneX Group, Inc.1 | 3,732,800 | |||||||||

Total Financials | 3,732,800 | ||||||||||

INDUSTRIALS (4.0%) | |||||||||||

1,498,618 | Astronics Corp.1 | 13,877,203 | |||||||||

Total Industrials | 13,877,203 | ||||||||||

TECHNOLOGY (37.3%) | |||||||||||

550,000 | Agilysys, Inc.1 | 35,293,500 | |||||||||

450,000 | Health Catalyst, Inc.1 | 3,969,000 | |||||||||

555,700 | Model N, Inc.1 | 21,116,600 | |||||||||

2,000,000 | Olo, Inc. (Class A)1 | 17,620,000 | |||||||||

225,000 | Onto Innovation, Inc.1 | 15,039,000 | |||||||||

The accompanying notes are an integral part of these financial statements.

financial statements october 31, 2022 | 7 |

BBH PARTNER FUND - SMALL CAP EQUITY

PORTFOLIO OF INVESTMENTS (continued)

October 31, 2022

Shares | Value | ||||||||||

COMMON STOCK (continued) | |||||||||||

TECHNOLOGY (continued) | |||||||||||

960,000 | PagerDuty, Inc.1 | $ | 23,942,400 | ||||||||

1,500,000 | Zuora, Inc. (Class A)1 | 11,535,000 | |||||||||

Total Technology | 128,515,500 | ||||||||||

Total Common Stock | |||||||||||

(Cost $440,916,545) | 334,577,155 | ||||||||||

TOTAL INVESTMENTS (Cost $440,916,545)2 | 97.2 | % | $ | 334,577,155 | ||

CASH AND OTHER ASSETS IN EXCESS OF LIABILITIES | 2.8 | % | 9,477,269 | |||

NET ASSETS | 100.00 | % | $ | 344,054,424 |

____________

1 | Non-income producing security. |

2 | The aggregate cost for federal income tax purposes is $440,916,545, the aggregate gross unrealized appreciation is $18,429,254 and the aggregate gross unrealized depreciation is $124,768,644, resulting in net unrealized depreciation of $106,339,390. |

The accompanying notes are an integral part of these financial statements.

8

BBH PARTNER FUND - SMALL CAP EQUITY

PORTFOLIO OF INVESTMENTS (continued)

October 31, 2022

FAIR VALUE MEASUREMENTS

The Fund is required to disclose information regarding the fair value measurements of the Fund’s assets and liabilities. Fair value is the price that would be received to sell an asset or paid to transfer a liability in an orderly transaction between market participants at the measurement date. The disclosure requirement established a three-tier hierarchy to maximize the use of observable market data and minimize the use of unobservable inputs and to establish classification of fair value measurements for disclosure purposes. Inputs refer broadly to the assumptions that market participants would use in pricing the asset or liability, including for example, the risk inherent in a particular valuation technique used to measure fair value including such a pricing model and/or the risk inherent in the inputs to the valuation technique. Inputs may be observable or unobservable. Observable inputs are inputs that reflect the assumptions market participants would use in pricing the asset or liability developed based on market data obtained from sources independent of the reporting entity. Unobservable inputs are inputs that reflect the Fund’s own considerations about the assumptions market participants would use in pricing the asset or liability developed based on the best information available in the circumstances.

Authoritative guidance establishes three levels of the fair value hierarchy as follows:

— | Level 1 – unadjusted quoted prices in active markets for identical assets and liabilities. |

— | Level 2 – significant other observable inputs (including quoted prices for similar assets and liabilities, interest rates, prepayment speeds, credit risk, etc.). |

— | Level 3 – significant unobservable inputs (including the Fund’s own assumptions in determining the fair value of assets and liabilities). |

Inputs are used in applying the various valuation techniques and broadly refer to the assumptions that market participants use to make valuation decisions, including assumptions about risk. Inputs may include price information, specific and broad credit data, liquidity statistics, and other factors. A financial instrument’s level within the fair value hierarchy is based on the lowest level of any input that is significant to the fair value measurement. However, the determination of what constitutes “observable” requires judgment by the investment adviser. The investment adviser considers observable data to be that market data which is readily available, regularly distributed or updated, reliable and verifiable, not proprietary, and provided by independent sources that are actively involved in the relevant market. The categorization of a financial instrument within the hierarchy is based upon the pricing transparency of the instrument and does not necessarily correspond to the investment adviser’s perceived risk of that instrument.

Financial assets within Level 1 are based on quoted market prices in active markets. The Fund does not adjust the quoted price for these instruments.

The accompanying notes are an integral part of these financial statements.

financial statements october 31, 2022 | 9 |

BBH PARTNER FUND - SMALL CAP EQUITY

PORTFOLIO OF INVESTMENTS (continued)

October 31, 2022

Financial instruments that trade in markets that are not considered to be active but are valued based on quoted market prices, dealer quotations or alternative pricing sources supported by observable inputs are classified within Level 2. These include investment-grade corporate bonds, U.S. Treasury notes and bonds, and certain non-U.S. sovereign obligations, listed equities and over-the-counter derivatives and foreign equity securities whose values could be impacted by events occurring before the Fund’s pricing time, but after the close of the securities’ primary markets and are, therefore, fair valued according to procedures adopted by the Board of Trustees. As Level 2 financial assets include positions that are not traded in active markets and/or are subject to transfer restrictions, valuations may be adjusted to reflect illiquidity and/or non-transferability, which are generally based on available market information.

Financial assets classified within Level 3 have significant unobservable inputs, as they trade infrequently. Level 3 financial assets include private equity and certain corporate debt securities.

Because of the inherent uncertainties of valuation, the values reflected in the financial statements may materially differ from the value received upon the actual sale of those investments.

The following table summarizes the valuation of the Fund’s investments by the above fair value hierarchy levels as of October 31, 2022.

Investments, at value | Unadjusted Quoted Prices in Active Markets for Identical Investments (Level 1) | Significant Other Observable Inputs (Level 2) | Significant Unobservable Inputs (Level 3) | Balance as of October 31, 2022 | ||||||||||||||||

Common Stock: | ||||||||||||||||||||

Basic Materials | $ | 15,480,000 | $ | – | $ | – | $ | 15,480,000 | ||||||||||||

Communications | 31,565,000 | – | – | 31,565,000 | ||||||||||||||||

Consumer Cyclical | 59,115,000 | – | – | 59,115,000 | ||||||||||||||||

Consumer Non-cyclical | 82,291,652 | – | – | 82,291,652 | ||||||||||||||||

Financials | 3,732,800 | – | – | 3,732,800 | ||||||||||||||||

Industrials | 13,877,203 | – | – | 13,877,203 | ||||||||||||||||

Technology | 128,515,500 | – | – | 128,515,500 | ||||||||||||||||

Total Investments, at value | $ | 334,577,155 | $ | – | $ | – | $ | 334,577,155 | ||||||||||||

The accompanying notes are an integral part of these financial statements.

10

BBH PARTNER FUND - SMALL CAP EQUITY

STATEMENT OF ASSETS AND LIABILITIES

October 31, 2022

ASSETS: | ||||||

Investments in securities, at value (Cost $440,916,545) | $ | 334,577,155 | ||||

Cash | 8,740,399 | |||||

Receivables for: | ||||||

Investments sold | 2,625,084 | |||||

Shares sold | 37,343 | |||||

Interest | 29,529 | |||||

Dividends | 18,000 | |||||

Total Assets | 346,027,510 | |||||

LIABILITIES: | ||||||

Payables for: | ||||||

Investments purchased | 1,339,452 | |||||

Shares redeemed | 333,923 | |||||

Investment advisory and administrative fees | 222,653 | |||||

Professional fees | 51,743 | |||||

Custody and fund accounting fees | 6,802 | |||||

Transfer agent fees | 5,895 | |||||

Board of Trustees' fees | 1,111 | |||||

Accrued expenses and other liabilities | 11,507 | |||||

Total Liabilities | 1,973,086 | |||||

NET ASSETS | $ | 344,054,424 | ||||

Net Assets Consist of: | ||||||

Paid-in capital | $ | 490,835,828 | ||||

Accumulated deficit | (146,781,404 | ) | ||||

Net Assets | $ | 344,054,424 | ||||

NET ASSET VALUE AND OFFERING PRICE PER SHARE | ||||||

($344,054,424 ÷ 52,417,032 shares outstanding) | $ | 6.56 | ||||

The accompanying notes are an integral part of these financial statements.

financial statements october 31, 2022 | 11 |

BBH PARTNER FUND - SMALL CAP EQUITY

STATEMENT OF OPERATIONS

For the year ended October 31, 2022

NET INVESTMENT LOSS: | ||||

Income: | ||||

Dividends (net of foreign withholding taxes of $580) | $ | 540,446 | ||

Interest income from affiliates | 235,002 | |||

Total Income | 775,448 | |||

Expenses: | ||||

Investment advisory and administrative fees | 2,984,455 | |||

Board of Trustees' fees | 59,850 | |||

Professional fees | 53,616 | |||

Transfer agent fees | 35,157 | |||

Custody and fund accounting fees | 25,782 | |||

Miscellaneous expenses | 88,921 | |||

Total Expenses | 3,247,781 | |||

Investment advisory and administrative fee waiver | (2,089 | ) | ||

Net Expenses | 3,245,692 | |||

Net Investment Loss | (2,470,244 | ) | ||

NET REALIZED AND UNREALIZED LOSS: | ||||

Net realized loss on investments in securities | (38,410,400 | ) | ||

Net change in unrealized appreciation/(depreciation) on investments in securities | (101,184,107 | ) | ||

Net Realized and Unrealized Loss | (139,594,507 | ) | ||

Net Decrease in Net Assets Resulting from Operations | $ | (142,064,751 | ) |

The accompanying notes are an integral part of these financial statements.

12

BBH PARTNER FUND - SMALL CAP EQUITY

STATEMENTS OF CHANGES IN NET ASSETS

For the year ended October 31, 2022 | For the period from July 8, 2021 (commencement of operations) to October 31, 2021 | |||||||||

INCREASE IN NET ASSETS FROM: | ||||||||||

Operations: | ||||||||||

Net investment loss | $ | (2,470,244 | ) | $ | (708,006 | ) | ||||

Net realized gain/(loss) on investments in securities | (38,410,400 | ) | 2,758,868 | |||||||

Net change in unrealized appreciation/(depreciation) on investments in securities | (101,184,107 | ) | (5,155,283 | ) | ||||||

Net decrease in net assets resulting from operations | (142,064,751 | ) | (3,104,421 | ) | ||||||

Dividends and distributions declared: | ||||||||||

Class I | (2,050,868 | ) | – | |||||||

Share transactions: | ||||||||||

Proceeds from sales of shares | 214,540,021 | 327,054,355 | ||||||||

Cost of shares redeemed | (48,848,721 | ) | (1,471,191 | ) | ||||||

Net increase in net assets resulting from share transactions | 165,691,300 | 325,583,164 | ||||||||

Total increase in net assets | 21,575,681 | 322,478,743 | ||||||||

NET ASSETS: | ||||||||||

Beginning of year/period | 322,478,743 | – | ||||||||

End of year/period | $ | 344,054,424 | $ | 322,478,743 | ||||||

The accompanying notes are an integral part of these financial statements.

financial statements october 31, 2022 | 13 |

BBH PARTNER FUND - SMALL CAP EQUITY

FINANCIAL HIGHLIGHTS

Selected per share data and ratios for a Class I share outstanding throughout each year/period.

For the year ended October 31, 2022 | For the period from July 8, 2021 (commencement of operations) to October 31, 2021 | ||||||||||

Net asset value, beginning of year/period | $ | 9.85 | $ | 10.00 | |||||||

Income from investment operations: | |||||||||||

Net investment loss1 | (0.05 | ) | (0.03 | ) | |||||||

Net realized and unrealized loss | (3.18 | ) | (0.12 | ) | |||||||

Total loss from investment operations | (3.23 | ) | (0.15 | ) | |||||||

Dividends and distributions to shareholders: | |||||||||||

From net realized gains | (0.06 | ) | — | ||||||||

Total dividends and distributions to shareholders | (0.06 | ) | — | ||||||||

Net asset value, end of year/period | $ | 6.56 | $ | 9.85 | |||||||

Total return2 | (32.97 | )% | (1.50 | )%3 | |||||||

Ratios/Supplemental data: | |||||||||||

Net assets, end of year/period (in millions) | $ | 344 | $ | 322 | |||||||

Ratio of expenses to average net assets before reductions | 0.92 | % | 0.93 | %4 | |||||||

Fee waiver5 | 0.00 | %6 | (0.01 | )%4 | |||||||

Ratio of expenses to average net assets after reductions | 0.92 | % | 0.92 | %4 | |||||||

Ratio of net investment loss to average net assets | (0.70 | )% | (0.83 | )%4 | |||||||

Portfolio turnover rate | 16 | % | 3 | %3 | |||||||

____________

1 | Calculated using average shares outstanding for the year/period. |

2 | Assumes the reinvestment of distributions. |

3 | Not annualized. |

4 | Annualized with the exception of audit fees, legal fees and registration fees. |

5 | The ratio of expenses to average net assets for the year ended October 31, 2022 and the period ended October 31, 2021 reflect fees reduced as result of a voluntary operating expense waiver. For the year ended October 31, 2022 and the period from July 8, 2021 to October 31, 2021 the waived fee were $2,089 and $40,593, respectively. |

6 | Less than 0.01%. |

The accompanying notes are an integral part of these financial statements.

14

BBH PARTNER FUND - SMALL CAP EQUITY

NOTES TO FINANCIAL STATEMENTS

October 31, 2022

1.Organization. The Fund is a separate, non-diversified series of BBH Trust (the “Trust”), which is registered under the Investment Company Act of 1940, as amended (the “1940 Act”), as an open-end management investment company. The Trust was originally organized under the laws of the State of Maryland on July 16, 1990 as BBH Fund, Inc. and re-organized as a Delaware statutory trust on June 12, 2007. The Fund commenced operations on July 8, 2021 and offers one share class, Class I. The investment objective of the Fund is to provide investors with long-term growth of capital. Under normal circumstances, at least 80% of the net assets of the Fund, plus any borrowings for investment purposes, are invested in small cap equity securities publicly traded and issued by domestic issuers directly. As of October 31, 2022, there were eight series of the Trust.

2.Significant Accounting Policies. The Fund’s financial statements are prepared in accordance with Generally Accepted Accounting Principles in the United States of America (“GAAP”). The Fund is an investment company and accordingly follows the investment company accounting and reporting guidance of the Financial Accounting Standards Board (“FASB”) Accounting Standard Codification Topic 946 Financial Services — Investment Companies. The following summarizes significant accounting policies of the Fund:

A.Valuation of Investments. (1) The value of investments listed on a securities exchange is based on the last sale price on that exchange prior to the time when assets are valued, or in the absence of recorded sales, at the average of readily available closing bid and asked prices on such exchange; (2) securities not traded on an exchange are valued at the average of the quoted bid and asked prices in the over-the-counter market; (3) securities or other assets for which market quotations are not readily available are valued at fair value in accordance with procedures established by and under the general supervision and responsibility of the Board of Trustees (the “Board”); (4) short-term investments, which mature in 60 days or less are valued at amortized cost if their original maturity was 60 days or less, or by amortizing their value on the 61st day prior to maturity, if their original maturity when acquired by the Fund was more than 60 days, unless the use of amortized cost is determined not to represent “fair value” by the Board.

B.Accounting for Investments and Income. Investment transactions are accounted for on the trade date. Realized gains and losses on investment transactions are determined based on the identified cost method. Dividend income and other distributions received from portfolio securities are recorded on the ex-dividend date. Non-cash dividends included in dividend income, if any, are recorded at the fair market value of securities received at ex-date. Distributions received on securities that represent a return of capital are recorded as a reduction of cost of investments. Distributions received on securities that represent a capital gain are recorded as a realized gain. Interest income is accrued daily. Investment income is recorded net of any foreign taxes withheld where recovery of such tax is uncertain.

C.Fund Expenses. Most expenses of the Trust can be directly attributed to a specific fund. Expenses which cannot be directly attributed to a fund are generally apportioned among each fund in the Trust

financial statements october 31, 2022 | 15 |

BBH PARTNER FUND - SMALL CAP EQUITY

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2022

on a net assets basis or other suitable method. Expense estimates are accrued in the period to which they relate and adjustments are made when actual amounts are known.

D. Federal Income Taxes. It is the Trust’s policy to comply with the requirements of the Internal Revenue Code (the “Code”) applicable to regulated investment companies and to distribute substantially all of its taxable income to its shareholders. Accordingly, no federal income tax provision is required. The Fund files a tax return annually using tax accounting methods required under provisions of the Code, which may differ from GAAP, which is the basis on which these financial statements are prepared. Accordingly, the amount of net investment income and net realized gain reported in these financial statements may differ from that reported on the Fund’s tax return, due to certain book-to-tax timing differences such as losses deferred due to “wash sale” transactions and utilization of capital loss carryforwards. These differences may result in temporary over-distributions for financial statement purposes and are classified as distributions in excess of accumulated net realized gains or net investment income. These distributions do not constitute a return of capital. Permanent differences are reclassified between paid-in capital and retained earnings/(accumulated deficit) within the Statement of Assets and Liabilities based upon their tax classification. As such, the character of distributions to shareholders reported in the Financial Highlights table may differ from that reported to shareholders on Form 1099-DIV.

The Fund is subject to the provisions of Accounting Standards Codification 740 Income Taxes (“ASC 740”). ASC 740 sets forth a minimum threshold for financial statement recognition of the benefit of a tax position taken or expected to be taken in a tax return. The Fund did not have any unrecognized tax benefits as of October 31, 2022, nor were there any increases or decreases in unrecognized tax benefits for the year then ended. The Fund recognizes interest and penalties, if any, related to unrecognized tax benefits as an income tax expense in the Statement of Operations. During the year ended October 31, 2022, the Fund did not incur any such interest or penalties. The Fund is subject to examination by U.S. federal and state tax authorities for returns filed for open tax period since July 8, 2021 (commencement of operations). The Fund is not aware of any tax positions for which it is reasonably possible that the total amounts of unrecognized tax benefits will significantly change in the next twelve months.

E.Dividends and Distributions to Shareholders. Dividends and distributions from net investment income to shareholders, if any, are paid annually and are recorded on the ex-dividend date. Distributions from net capital gains, if any, are generally declared and paid annually and are recorded on the ex-dividend date. The Fund declared dividends and distributions in the amount of $2,050,868 to Class I shares shareholders, during the year ended October 31, 2022, and did not declare any dividends and distributions to shareholders during the period ended October 31, 2021.

16

BBH PARTNER FUND - SMALL CAP EQUITY

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2022

The tax character of distribution paid during the year ended October 31, 2022 was as follows:

Distribution paid from: | ||||||||||||||||||||

Ordinary income | Net long-term capital gain | Total taxable distributions | Tax return of capital | Total distributions paid | ||||||||||||||||

2022: | $ 2,050,868 | $ — | $ 2,050,868 | $ — | $ 2,050,868 | |||||||||||||||

As of October 31, 2022 and 2021, respectively, the components of retained earnings/(accumulated deficit) were as follows:

Components of retained earnings/(accumulated deficit): | |||||||||||||||||||||||||||||||||||

Undistributed ordinary income | Undistributed long-term capital gain | Accumulated capital and other losses | Other book/tax temporary differences | Late year ordinary loss deferral | Unrealized appreciation/ (depreciation) | Total retained earnings/ (accumulated deficit) | |||||||||||||||||||||||||||||

2022: | $ | — | $ | — | $ | (38,410,400 | ) | $ | — | $ | (2,031,614 | ) | $ | (106,339,390 | ) | $ | (146,781,404 | ) | |||||||||||||||||

2021: | 2,050,862 | — | — | — | — | (5,155,283 | ) | (3,104,421 | ) | ||||||||||||||||||||||||||

The Fund had $38,410,400 of post-December 22, 2010 net capital loss carryforwards as of October 31, 2022, of which $34,332,020 and $4,078,380, is attributable to short-term and long-term capital losses, respectively.

The Fund is permitted to carryforward capital losses for an unlimited period and they will retain their character as either short-term or long-term capital losses rather than being considered all short-term capital losses.

Total distributions paid may differ from amounts reported in the Statements of Changes in Net Assets because, for tax purposes, dividends are recognized when actually paid.

The differences between book-basis and tax-basis unrealized appreciation/(depreciation) would be attributable primarily to the tax deferral of losses on wash sales, if applicable.

To the extent future capital gains are offset by capital loss carryforwards, if any, such gains will not be distributed.

F.Use of Estimates. The preparation of the financial statements in accordance with GAAP requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities in the financial statements, disclosure of contingent assets and liabilities at the date of the

financial statements october 31, 2022 | 17 |

BBH PARTNER FUND - SMALL CAP EQUITY

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2022

financial statements and the reported amounts of increase and decrease in net assets from operations during the reporting period. Actual results could differ from these estimates.

3. Fees and Other Transactions with Affiliates.

A.Investment Advisory and Administrative Fees. Under a combined Investment Advisory and Administrative Services Agreement (“Agreement”) with the Trust, Brown Brothers Harriman & Co. (“BBH”) through a separately identifiable department (“SID” or “Investment Adviser”) provides investment advisory, portfolio management and administrative services to the Fund. BBH employs a “manager-of-managers” investment approach, whereby it allocates the Fund’s assets to the Fund’s sub-adviser, currently Bares Capital Management, Inc. (“Bares Capital Management” or the “Sub-adviser”). The Sub-adviser is responsible for investing the assets of the Fund and the Investment Adviser oversees the Sub-adviser and evaluates its performance results. The Fund pays a combined fee for investment advisory and administrative services calculated daily and paid monthly at an annual rate equivalent to 0.85% per annum on the first $3 billion of the Fund’s average daily net assets and 0.80% per annum on the Fund’s average daily net assets over $3 billion. The Investment Adviser pays its Sub-adviser a percentage from its investment advisory and administrative fees. For the year ended October 31, 2022, the Fund incurred $2,984,455 under the Agreement.

B.Investment Advisory and Administrative Fee Waivers. The Investment Adviser voluntarily agreed to limit the annual fund operating expenses (excluding interest, taxes, brokerage commissions, other expenditures that are capitalized in accordance with GAAP and other extraordinary expenses not incurred in the ordinary course of the Fund’s business) of Class I. This is a voluntary waiver that can be changed at any time at the sole discretion of the Investment Adviser. For the year ended October 31, 2022, the Investment Adviser waived fees in the amount of $2,089 for Class I.

C.Custody and Fund Accounting Fees. BBH acts as a custodian and fund accountant and receives custody and fund accounting fees from the Fund calculated daily and incurred monthly. BBH holds all of the Fund’s cash and investments and calculates the Fund’s daily net asset value. The custody fee is an asset and transaction-based fee. The fund accounting fee is an asset-based fee calculated at 0.004% per annum of the Fund’s net asset value. For the year ended October 31, 2022, the Fund incurred $25,782 in custody and fund accounting fees. As per agreement with the Fund’s custodian, the Fund receives interest income on cash balances held by the custodian at the BBH Base Rate. The BBH Base Rate is defined as BBH’s effective trading rate in local money markets on each day. The total interest earned by the Fund for the year ended October 31, 2022 was $235,002. This amount is included in "Interest income from affiliates" in the Statement of Operations. In the event that the Fund is overdrawn, under the custody agreement with BBH, BBH will make overnight loans to the Fund to cover overdrafts. Pursuant to their agreement, the Fund will pay the BBH Overdraft Base Rate plus 2% on the day of the overdraft. The total interest incurred by the Fund for the year ended October 31, 2022, was $1,860. This amount is included under line item “Custody and fund accounting fees” in the Statement of Operations.

18

BBH PARTNER FUND - SMALL CAP EQUITY

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2022

D.Board of Trustees’ Fees. Each Trustee who is not an “interested person” as defined under the 1940 Act receives an annual fee as well as reimbursement for reasonable out-of-pocket expenses from the Fund. For the year ended October 31, 2022, the Fund incurred $59,850 in independent Trustee compensation and expense reimbursements.

E.Officers of the Trust. Officers of the Trust are also employees of BBH. Officers are paid no fees by the Trust for their services to the Trust.

4.Investment Transactions. For the year ended October 31, 2022, the cost of purchases and the proceeds of sales of investment securities, other than short-term investments, were $240,668,466 and $50,141,985, respectively.

5.Shares of Beneficial Interest. The Trust is permitted to issue an unlimited number of Class I shares of beneficial interest at no par value. Transactions in Class I shares were as follows:

For the year ended October 31, 2022 | For the period ended October 31, 2021* | |||||||||||||||

Shares | Dollars | Shares | Dollars | |||||||||||||

Class I | ||||||||||||||||

Shares sold | 26,759,570 | $ | 214,540,021 | 32,889,385 | $ | 327,054,355 | ||||||||||

Shares redeemed | (7,079,879 | ) | (48,848,721 | ) | (152,044 | ) | (1,471,191 | ) | ||||||||

Net increase | 19,679,691 | $ | 165,691,300 | 32,737,341 | $ | 325,583,164 | ||||||||||

* The period represented is from July 8, 2021 (commencement of operations) to October 31, 2021.

6. Principal Risk Factors and Indemnifications.

A.Principal Risk Factors. Investing in the Fund may involve certain risks, as discussed in the Fund’s prospectus, including but not limited to, those described below:

A shareholder may lose money by investing in the Fund (investment risk). The Fund is actively managed and the decisions by the Investment Adviser may cause the Fund to incur losses or miss profit opportunities (management risk). Price movements may occur due to factors affecting individual companies, such as the issuance of an unfavorable earnings report, or other events affecting particular industries or the equity market as a whole (equity securities risk). Small cap companies, when compared to larger companies, may experience lower trading volume and could be subject to greater and less predictable price changes (small cap company risk). The fund will invest 25% or more of its net assets in the Software & Services Industry Group. When a fund focuses its investments in a particular industry, group of industries, or sector, financial, economic business and other developments affecting issuers in those industries or groups of industries will have a greater effect on the fund than if the fund did not focus on an industry or group of industries (Software & Service

financial statements october 31, 2022 | 19 |

BBH PARTNER FUND - SMALL CAP EQUITY

NOTES TO FINANCIAL STATEMENTS (continued)

October 31, 2022

Industry Group Concentration risk). The value of securities held by the Fund may fall due to changing economic, political, regulatory or market conditions, or due to a company’s or issuer’s individual situation. Natural disasters, the spread of infectious illness and other public health emergencies, recession, terrorism and other unforeseeable events may lead to increased market volatility and may have adverse effects on world economies and markets generally (market risk). In the normal course of business, the Fund invests in securities and enters into transactions where risks exist due to assumption of large positions in securities of a small number of issuers (non-diversification risk). The Fund’s shareholders may be adversely impacted by asset allocation decisions made by an investment adviser whose discretionary clients make up a large percentage of the Fund’s shareholders (large shareholder risk). The extent of the Fund’s exposure to these risks in respect to these financial assets is included in their value as recorded in the Fund’s Statement of Assets and Liabilities.

Please refer to the Fund’s prospectus for a complete description of the principal risks of investing in the Fund.

B.Indemnifications. Under the Trust’s organizational documents, its officers and Trustees may be indemnified against certain liabilities and expenses arising out of the performance of their duties to the Fund, and shareholders are indemnified against personal liability for the obligations of the Trust. Additionally, in the normal course of business, the Fund enters into agreements with service providers that may contain indemnification clauses. The Fund’s maximum exposure under these arrangements is unknown as this would involve future claims that may be made against the Fund that have not yet occurred. The risk of material loss from such claims is considered remote.

7.Subsequent Events. On November 30, 2022, BBH and State Street Corporation (“State Street”) decided to terminate the agreement under which State Street would have acquired BBH’s Investor Services business.

Management has evaluated events and transactions that have occurred since October 31, 2022 through the date the financial statements were issued and determined that there were no other subsequent events that would require recognition or additional disclosure in the financial statements.

20

BBH PARTNER FUND - SMALL CAP EQUITY

DISCLOSURE OF FUND EXPENSES

October 31, 2022 (unaudited)

EXAMPLE

As a shareholder of the Fund, you may incur two types of costs: (1) transaction costs, including sales charges (loads) on purchase payments, reinvested distributions, or other distributions; redemption fees; and exchange fees; and (2) ongoing costs, including management fees; distribution 12b-1 fees; and other Fund expenses. This Example is intended to help you understand your ongoing costs (in dollars) of investing in the Fund and to compare these costs with the ongoing costs of investing in other mutual funds.

The Example is based on an investment of $1,000 invested at the beginning of the period and held for the entire period (May 1, 2022 to October 31, 2022).

ACTUAL EXPENSES

The first line of the table below provides information about actual account values and actual expenses. You may use information in this line, together with the amount you invested, to estimate the expenses that you paid over the period. Simply divide your account value by $1,000 (for example, an $8,600 account value divided by $1,000 = 8.6), then multiply the result by the number in the first line under the heading entitled “Expenses Paid During the Period” to estimate the expenses you paid on your account during the period.

HYPOTHETICAL EXAMPLE FOR COMPARISON PURPOSES

The second line of the table below provides information about hypothetical account values and hypothetical expenses based on the Fund’s actual expense ratio and an assumed rate of return of 5% per year before expenses, which is not the Fund’s actual return. The hypothetical account values and expenses may not be used to estimate the actual ending account balance or expenses you paid during the period. You may use this information to compare the ongoing costs of investing in the Fund and other funds. To do so, compare this 5% Hypothetical Example with the 5% hypothetical examples that appear in the shareholder reports of other funds.

financial statements october 31, 2022 | 21 |

BBH PARTNER FUND - SMALL CAP EQUITY

DISCLOSURE OF FUND EXPENSES (continued)

October 31, 2022 (unaudited)

Please note that the expenses shown in the table are meant to highlight your ongoing costs only and do not reflect any transactional costs, such as redemption fees or exchange fees. Therefore, the second line of the table is useful in comparing ongoing costs only, and will not help you determine the relative total costs of owning different funds. In addition, if these transactional costs were included, your costs would have been higher.

Beginning Account Value May 1, 2022 | Ending Account Value October 31, 2022 | Expenses Paid During Period May 1, 2022 to October 31, 20221 | |||||||||||||

Class I | |||||||||||||||

Actual | $ | 1,000 | $ | 943 | $ | 4.49 | |||||||||

Hypothetical2 | $ | 1,000 | $ | 1,021 | $ | 4.67 | |||||||||

____________

1 | Expenses are equal to the Fund’s annualized expense ratio of 0.92% for Class I, multiplied by the average account value over the period, multiplied by 184/365. |

2 | Assumes a return of 5% before expenses. For the purposes of the calculation, the applicable annualized expense ratio for each class of shares is subtracted from the assumed return before expenses. |

22

BBH PARTNER FUND - SMALL CAP EQUITY

CONFLICTS OF INTEREST

October 31, 2022 (unaudited)

Description of Potential Material Conflicts of Interest - Investment Adviser and Sub-Adviser

BBH, including the Investment Adviser, and the Sub-Adviser provide discretionary and non-discretionary investment management services and products to corporations, institutions and individual investors throughout the world. As a result, in the ordinary course of its businesses, BBH, including the Investment Adviser, and the Sub-Adviser may engage in activities in which its interests or the interests of its clients may conflict with or be adverse to the interests of the Fund. In addition, certain of such clients (including the Fund) utilize the services of BBH for which they will pay to BBH customary fees and expenses that will not be shared with the Fund.

The Investment Adviser and the Sub-Adviser have adopted and implemented policies and procedures that seek to manage conflicts of interest. Pursuant to such policies and procedures, the Investment Adviser and the Sub-Adviser monitor a variety of areas, including compliance with fund investment guidelines and compliance with their respective Codes of Ethics.

The Trust also manages these conflicts of interest. For example, the Trust has designated a Chief Compliance Officer (“CCO”) and has adopted and implemented policies and procedures designed to manage the conflicts identified below and other conflicts that may arise in the course of the Fund’s operations in such a way as to safeguard the Fund from being negatively affected as a result of any such potential conflicts. From time to time, the Trustees receive reports from the Investment Adviser, the Sub-Adviser and the Trust’s CCO on areas of potential conflict.

Investors should carefully review the following, which describes potential and actual conflicts of interest that BBH, the Investment Adviser and Sub-Adviser can face in the operation of their respective investment management services. This section is not, and is not intended to be, a complete enumeration or explanation of all of the potential conflicts of interest that may arise. The Investment Adviser, the Sub-Adviser and the Fund have adopted policies and procedures reasonably designed to appropriately prevent, limit or mitigate the conflicts of interest described below. Additional information about potential conflicts of interest regarding the Investment Adviser is set forth in the Investment Adviser’s Form ADV. A copy of Part 1 and Part 2A of the Investment Adviser’s Form ADV is available on the SEC’s website (www.adviserinfo.sec.gov). In addition, many of the activities that create these conflicts of interest are limited and/or prohibited by law, unless an exception is available.

Other Clients and Allocation of Investment Opportunities. BBH, the Investment Adviser, and the Sub-Adviser manage funds and accounts of clients other than the Fund (“Other Clients”). In general, BBH, the Investment Adviser, and the Sub-Adviser face conflicts of interest when they render investment advisory services to different clients and, from time to time, provide dissimilar investment advice to different clients. Investment decisions will not necessarily be made in parallel among the Fund and Other Clients. Investments made by the Fund do not, and are not intended to, replicate the investments, or the investment methods and strategies, of Other Clients. Accordingly, such Other Clients may produce results that are materially different from those experienced by the Fund. Certain other conflicts of interest may arise in connection with a portfolio manager’s management of the Fund’s investments, on the one hand, and the investments of other funds or accounts for which the portfolio manager is responsible, on the other. For example, it is possible that the various funds or accounts managed by the Investment Adviser or Sub-Adviser could have different

financial statements october 31, 2022 | 23 |

BBH PARTNER FUND - SMALL CAP EQUITY

CONFLICTS OF INTEREST

October 31, 2022 (unaudited)

investment strategies that, at times, might conflict with one another to the possible detriment of the Fund. From time to time, the Investment Adviser and Sub-Adviser sponsor funds and other investment pools and accounts which engage in the same or similar businesses as the Fund using the same or similar investment strategies. To the extent that the same investment opportunities might be desirable for more than one account or fund, possible conflicts could arise in determining how to allocate them because the Investment Adviser or Sub-Adviser may have an incentive to allocate investment opportunities to certain accounts or funds. However, BBH, the Investment Adviser and Sub-Adviser have implemented policies and procedures designed to ensure that information relevant to investment decisions is disseminated promptly within its portfolio management teams and investment opportunities are allocated equitably among different clients. The policies and procedures require, among other things, objective allocation for limited investment opportunities, and documentation and review of justifications for any decisions to make investments only for select accounts or in a manner disproportionate to the size of the account. Nevertheless, access to investment opportunities may be allocated differently among accounts due to the particular characteristics of an account, such as size of the account, cash position, tax status, risk tolerance and investment restrictions or for other reasons.

Actual or potential conflicts of interest may also arise when a portfolio manager has management responsibilities to multiple accounts or funds, resulting in unequal commitment of time and attention to the portfolio management of the funds or accounts.

Affiliated Service Providers. Other potential conflicts might include conflicts between the Fund and its affiliated and unaffiliated service providers (e.g., conflicting duties of loyalty). In addition to providing investment management and administrative services through the SID, BBH provides custody, shareholder servicing and fund accounting services to the Fund. BBH may have conflicting duties of loyalty while servicing the Fund and/or opportunities to further its own interest to the detriment of the Fund. For example, in negotiating fee arrangements with affiliated service providers, BBH may have an incentive to agree to higher fees than it would in the case of unaffiliated providers. BBH acting in its capacity as the Fund’s administrator is the primary valuation agent of the Fund. BBH values securities and assets in the Fund according to the Fund’s valuation policies. Because the Investment Adviser’s advisory and administrative fees are calculated by reference to a Fund’s net assets, BBH and its affiliates may have an incentive to seek to overvalue certain assets.

Aggregation. Potential conflicts of interest also arise with the aggregation of trade orders. Purchases and sales of securities for the Fund may be aggregated with orders for other client accounts managed by the Sub-Adviser. The Sub-Adviser, however, is not required to aggregate orders if portfolio management decisions for different accounts are made separately, or if it is determined that aggregating is not practicable, or in cases involving client direction. Prevailing trading activity frequently may make impossible the receipt of the same price or execution on the entire volume of securities purchased or sold. When this occurs, the various prices may be averaged, and the Fund will be charged or credited with the average price. Thus, the effect of the aggregation may operate on some occasions to the disadvantage of the Fund. In addition, under certain circumstances, the Fund will not be charged the same commission or commission equivalent rates in connection with an aggregated order.

24

BBH PARTNER FUND - SMALL CAP EQUITY

CONFLICTS OF INTEREST (continued)

October 31, 2022 (unaudited)

Cross Trades. Under certain circumstances, the Sub-Adviser, on behalf of the Fund, may seek to buy from or sell securities to another fund or account advised by the Sub-Adviser. Subject to applicable law and regulation, the Sub-Adviser may (but is not required to) effect purchases and sales between client accounts that it manages (“cross trades”), including the Fund, if the Sub-Adviser believes such transactions are appropriate based on each party’s investment objectives and guidelines. There may be potential conflicts of interest or regulatory issues relating to these transactions which could limit the Sub-Adviser’s decision to engage in these transactions for the Fund. The Sub-Adviser may have a potentially conflicting division of loyalties and responsibilities to the parties in such transactions.

Soft Dollars. The Sub-Adviser may direct brokerage transactions and/or payment of a portion of client commissions (“soft dollars”) to specific brokers or dealers or other providers to pay for research or other appropriate services which provide, in the Sub-Adviser’s view, appropriate assistance in the investment decision-making process (including with respect to futures, fixed price offerings and over-the-counter transactions). The use of a broker that provides research and securities transaction services may result in a higher commission than that offered by a broker who does not provide such services. The Sub-Adviser will determine in good faith whether the amount of commission is reasonable in relation to the value of research and services provided and whether the services provide lawful and appropriate assistance in its investment decision-making responsibilities.

Research or other services obtained in this manner may be used in servicing any or all of the Fund and other accounts managed by the Sub-Adviser, including in connection with accounts that do not pay commissions to the broker related to the research or other service arrangements. Such products and services may disproportionately benefit other client accounts relative to the Fund based on the amount of brokerage commissions paid by the Fund and such other accounts. To the extent that the Sub-Adviser uses soft dollars, it will not have to pay for those products and services itself.

The Sub-Adviser may receive research that is bundled with the trade execution, clearing, and/or settlement services provided by a particular broker-dealer. To the extent that the Sub-Adviser receives research on this basis, many of the same conflicts related to traditional soft dollars may exist. For example, the research effectively will be paid by client commissions that also will be used to pay for the execution, clearing, and settlement services provided by the broker-dealer and will not be paid by the Sub-Adviser.

Arrangements regarding compensation and delegation of responsibility may create conflicts relating to selection of brokers or dealers to execute Fund portfolio trades and/or specific uses of commissions from Fund portfolio trades, administration of investment advice and valuation of securities.

Investments in BBH Funds. From time to time, BBH will invest a portion of the assets of its discretionary investment advisory clients in the Fund. That investment by BBH on behalf of its discretionary investment advisory clients in the Fund may be significant at times.

Increasing the Fund’s assets may enhance investment flexibility and diversification and may contribute to economies of scale that tend to reduce the Fund’s expense ratio. In selecting the Fund for its discretionary investment advisory clients, BBH may limit its selection to funds managed by BBH or the Investment Adviser.

financial statements october 31, 2022 | 25 |

BBH PARTNER FUND - SMALL CAP EQUITY

CONFLICTS OF INTEREST (continued)

October 31, 2022 (unaudited)

BBH may not consider or canvass the universe of unaffiliated investment companies available, even though there may be unaffiliated investment companies that may be more appropriate or that have superior performance. BBH, the Investment Adviser and their affiliates providing services to the Fund benefit from additional fees when the Fund is included as an investment for a discretionary investment advisory client.

BBH reserves the right to redeem at any time some or all of the shares of the Fund acquired for its discretionary investment advisory clients’ accounts. A large redemption of shares of the Fund by BBH on behalf of its discretionary investment advisory clients could significantly reduce the asset size of the Fund, which might have an adverse effect on the Fund’s investment flexibility, portfolio diversification and expense ratio.

Valuation. When market quotations are not readily available or are believed by BBH to be unreliable, the Fund’s investments will be valued at fair value by BBH pursuant to procedures adopted by the Fund’s Board of Trustees in accordance with Rule 2a-5 under the 1940 Act. When determining an asset’s “fair value,” BBH seeks to determine the price that a Fund might reasonably expect to receive from the current sale of that asset in an arm’s-length transaction. The price generally may not be determined based on what the Fund might reasonably expect to receive for selling an asset at a later time or if it holds the asset to maturity. While fair value determinations will be based upon all available factors that BBH deems relevant at the time of the determination and may be based on analytical values determined by BBH using proprietary or third-party valuation models, fair value represents only a good faith approximation of the value of a security. The fair value of one or more securities may not, in retrospect, be the price at which those assets could have been sold during the period in which the particular fair values were used in determining the Fund’s net asset value. As a result, the Fund’s sale or redemption of its shares at net asset value, at a time when a holding or holdings are valued by BBH (pursuant to Board-adopted procedures) at fair value, may have the effect of diluting or increasing the economic interest of existing shareholders.

Referral Arrangements. BBH may enter into advisory and/or referral arrangements with third parties. Such arrangements may include compensation paid by BBH to the third party. BBH may pay a solicitation fee for referrals and/or advisory or incentive fees. BBH may benefit from increased amounts of assets under management.

Personal Trading. BBH, including the Investment Adviser, and any of their respective partners, principals, directors, officers, employees, affiliates or agents, face conflicts of interest when transacting in securities for their own accounts because they could benefit by trading in the same securities as the Fund, which could have an adverse effect on the Fund. However, BBH, including the Investment Adviser, has implemented policies and procedures concerning personal trading by BBH Partners and employees. The policies and procedures are intended to prevent BBH Partners and employees with access to Fund material non-public information from trading in the same securities as the Fund.

Gifts and Entertainment. From time to time, employees of BBH, including the Investment Adviser, and any of their respective partners, principals, directors, officers, employees, affiliates or agents, may receive gifts and/or entertainment from clients, intermediaries, or service providers to the Fund or BBH, including the Investment Adviser, which could have the appearance of affecting or may potentially affect the judgment of the employees, or the manner in which they conduct business. The Investment Adviser has implemented policies and procedures concerning gifts and entertainment to mitigate any impact on the judgment of BBH Partners and employees.

26

BBH PARTNER FUND - SMALL CAP EQUITY

ADDITIONAL FEDERAL TAX INFORMATION

October 31, 2022 (unaudited)

In January 2023, shareholders will receive Form 1099-DIV, which will include their share of qualified dividends distributed during the calendar year 2022. Shareholders are advised to check with their tax advisers for information on the treatment of these amounts on their individual income tax returns.

financial statements october 31, 2022 | 27 |

TRUSTEES AND OFFICERS OF BBH PARTNER FUND - SMALL CAP EQUITY

(unaudited)

Information pertaining to the Trustees and executive officers of the Trust as of October 31, 2022 is set forth below. The mailing address for each Trustee is c/o BBH Trust, 140 Broadway, New York, NY 10005.

Name and Birth Year | Position(s) Held with the Trust | Term of Office and Length of Time Served# | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Trustee^ | Other Public Company or Investment Company Directorships held by Trustee During Past 5 Years | |||||

Independent Trustees | ||||||||||

H. Whitney Wagner Birth Year: 1956 | Chairman of the Board and Trustee | Chairman Since 2014; Trustee Since 2007 and 2006-2007 with the Predecessor Trust | President, Clear Brook Advisors, a registered investment adviser. | 8 | None. | |||||

Andrew S. Frazier Birth Year: 1948 | Trustee | Since 2010 | Retired. | 8 | None. | |||||

Mark M. Collins Birth Year: 1956 | Trustee | Since 2011 | Partner of Brown Investment Advisory Incorporated, a registered investment adviser. | 8 | Chairman of Dillon Trust Company. | |||||

John M. Tesoro Birth Year: 1952 | Trustee | Since 2014 | Retired. | 8 | Independent Trustee, Bridge Builder Trust (11 funds) and Edward Jones Money Market Fund; Director, Teton Advisers, Inc. (a registered investment adviser) (2014 – 2021). | |||||

28

TRUSTEES AND OFFICERS OF BBH PARTNER FUND - SMALL CAP EQUITY

(unaudited)

Name and Birth Year | Position(s) Held with the Trust | Term of Office and Length of Time Served# | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Trustee^ | Other Public Company or Investment Company Directorships held by Trustee During Past 5 Years | |||||

Joan A. Binstock Birth Year: 1954 | Trustee | Since 2019 | Partner, Chief Financial and Operations Officer, Lord Abbett & Co. LLC (1999-2018); Lovell Minnick Partners, Advisors Counsel (2018- Present). | 8 | Independent Director, Morgan Stanley Direct Lending Fund; KKR Real Estate Interval Fund. |

financial statements october 31, 2022 | 29 |

TRUSTEES AND OFFICERS OF BBH PARTNER FUND - SMALL CAP EQUITY

(unaudited)

Name, Address and Birth Year | Position(s) Held with the Trust | Term of Office and Length of Time Served# | Principal Occupation(s) During Past 5 Years | Number of Portfolios in Fund Complex Overseen by Trustee^ | Other Public Company or Investment Company Directorships held by Trustee During Past 5 Years | |||||

Interested Trustees | ||||||||||

Susan C. Livingston+ 50 Post Office Square Boston, MA 02110 Birth Year: 1957 | Trustee | Since 2011 | Partner (since 1998) and Senior Client Advocate (since 2010) for BBH&Co. | 8 | None. | |||||

John A. Gehret+ 140 Broadway New York, NY 10005 Birth Year: 1959 | Trustee | Since 2011 | Limited Partner of BBH&Co. (2012-present). | 8 | None. | |||||

30

TRUSTEES AND OFFICERS OF BBH PARTNER FUND - SMALL CAP EQUITY

(unaudited)

Name, Address and Birth Year | Position(s) Held with the Trust | Term of Office and Length of Time Served# | Principal Occupation(s) During Past 5 Years | |||

Officers | ||||||

Jean-Pierre Paquin 140 Broadway New York, NY 10005 Birth Year: 1973 | President and Principal Executive Officer | Since 2016 | Partner of BBH&Co. since 2015; joined BBH&Co. in 1996. | |||

Daniel Greifenkamp 140 Broadway New York, NY 10005 Birth Year: 1969 | Vice President | Since 2016 | Managing Director of BBH&Co. since 2014; joined BBH&Co. in 2011. | |||

Charles H. Schreiber 140 Broadway New York, NY 10005 Birth Year: 1957 | Treasurer and Principal Financial Officer | Since 2007 2006-2007 with the Predecessor Trust | Senior Vice President of BBH&Co. since 2001; joined BBH&Co. in 1999. | |||

Paul F. Gallagher 140 Broadway New York, NY 10005 Birth Year: 1959 | Chief Compliance Officer (“CCO”) | Since 2015 | Senior Vice President of BBH&Co. since 2015. | |||

Nicole English 140 Broadway New York, NY 10005 Birth Year: 1981 | Anti-Money Laundering Officer (“AMLO”) | Since 2022 | Vice President of BBH&Co. since 2019; joined BBH&Co. in 2016. |

financial statements october 31, 2022 | 31 |

TRUSTEES AND OFFICERS OF BBH PARTNER FUND - SMALL CAP EQUITY

(unaudited)

Name, Address and Birth Year | Position(s) Held with the Trust | Term of Office and Length of Time Served# | Principal Occupation(s) During Past 5 Years | |||

Brian J. Carroll 50 Post Office Square Boston, MA 02110 Birth Year: 1985 | Secretary | Since 2021 | Assistant Vice President of BBH&Co. since 2022; joined BBH&Co. in 2014. | |||

Crystal Cheung 140 Broadway New York, NY 10005 Birth Year: 1974 | Assistant Treasurer | Since 2018 | Assistant Vice President of BBH&Co. since 2016; joined BBH&Co. 2014. |

________________

# | All officers of the Trust hold office for one year and until their respective successors are chosen and qualified (subject to the ability of the Trustees to remove any officer in accordance with the Trust’s By-laws). Mr. Wagner previously served on the Board of Trustees of the Predecessor Trust. |

+ | Ms. Livingston and Mr. Gehret are “interested persons” of the Trust as defined in the 1940 Act because of their positions as Partner and Limited Partner of BBH&Co., respectively. |

^ | The Fund Complex consists of the Trust, which has eight series, and each is counted as one “Portfolio” for purposes of this table. |

32

BBH PARTNER FUND - SMALL CAP EQUITY

OPERATION AND EFFECTIVNESS OF THE FUND’S LIQUIDITY RISK MANAGEMENT PROGRAM

October 31, 2022 (unaudited)

The Securities and Exchange Commission adopted Rule 22e-4 under the Investment Company Act of 1940, as amended (the “Liquidity Rule”) to promote effective liquidity risk management throughout the open-end investment company industry in order to reduce the risk that funds will be unable to meet their redemption obligations and mitigate dilution of the interests of fund shareholders.

The Board of Trustees (the “Board”) of BBH Trust met on March 8, 2022 to review the liquidity risk management program (the “Program”) for the funds of BBH Trust (the “Funds”) pursuant to the Liquidity Rule. The Board has appointed three members of the Brown Brothers Harriman & Co. Mutual Fund Advisory Department, the Investment Adviser to the Funds, as the Program Administrator for each Fund’s Program. The Program Administrator provided the Board with a report (the “Report”) that addressed the operations of the Program and assessed its adequacy and effectiveness of the Program. The Report covered the period from February 1, 2021 through January 31, 2022 (the “Reporting Period”).

The Report noted that the Program complied with the key factors for consideration under the Liquidity Rule for assessing, managing and periodically reviewing a Fund’s liquidity risk, including the following points.

Liquidity classification. The Report described the Program’s liquidity classification methodology for categorizing the Funds’ investments into one of four liquidity buckets.

Highly Liquid Investment Minimum. The Report noted that one aspect of the Liquidity Rule is a requirement that funds that are expected to have less than 50% of assets classified as other than “highly liquid” should establish a minimum percentage of highly liquid assets that the fund is expected to hold on an on-going basis. The Program Administrator monitors the percentages of assets in each category on an ongoing basis and, given that no Fund has approached the 50% threshold, has made the determination that it is not necessary to assign a Highly Liquid Investment Minimum as provided for in the Liquidity Rule to any of the Funds.

The Fund’s investment strategy and liquidity of portfolio investments during normal and reasonably foreseeable stressed market conditions. During the Reporting Period, the Program Administrator reviewed whether each Fund’s investment strategy is appropriate for an open-end fund structure with a focus on Funds with more significant and consistent holdings of less liquid and illiquid assets and factored a Fund’s concentration in an issuer into the liquidity classification methodology by taking issuer position sizes into account.

Short-term and long-term cash flow projections during normal and reasonably foreseeable stressed market conditions. During the Reporting Period, the Program Administrator reviewed historical redemption activity and used this information as a component to establish each Fund’s reasonably anticipated trading size. The Program Administrator also took into consideration other factors such as shareholder ownership concentration, applicable distribution channels and the degree of certainty associated with a Fund’s short-term and long-term cash flow projections.

Holdings of cash and cash equivalents. The Program Administrator considered the degree to which each Fund held cash and cash equivalents as a component of each Fund’s ability to meet redemption requests.

financial statements october 31, 2022 | 33 |

BBH PARTNER FUND - SMALL CAP EQUITY

OPERATION AND EFFECTIVENESS OF THE FUND’S LIQUIDITY RISK MANAGEMENT PROGRAM (continued)

October 31, 2022 (unaudited)

There were no material changes to the Program during the Reporting Period. The Program Administrator has informed the Board that it believes that the Fund’s Program is adequately designed, has been implemented as intended, and has operated effectively since its implementation. No material exceptions have been noted since the implementation of the Program, and there were no liquidity events that impacted the Fund or its ability to meet redemption requests on a timely basis during the Reporting Period.

34

Administrator Brown Brothers Harriman & Co. 140 Broadway New York, NY 10005

Distributor ALPS Distributors, Inc. 1290 Broadway, Suite 1000 Denver, CO 80203

Shareholder Servicing Agent Brown Brothers Harriman & Co. 140 Broadway New York, NY 10005 1-800-575-1265 | Investment Adviser Brown Brothers Harriman Mutual Fund Advisory Department 140 Broadway New York, NY 10005 |

To obtain information or make shareholder inquiries:

By telephone: | Call 1-800-575-1265 |

By E-mail send your request to: | bbhfunds@bbh.com |

On the internet: | www.bbhfunds.com |

This report is submitted for the general information of shareholders and is not authorized for distribution to prospective investors unless preceded or accompanied by an effective prospectus. Nothing herein contained is to be considered an offer of sale or a solicitation of an offer to buy shares of the Fund.

For more complete information, visit www.bbhfunds.com for a prospectus. You should consider the Fund’s investment objectives, risks, charges and expenses carefully before you invest. Information about these and other important subjects is in the Fund’s prospectus, which you should read carefully before investing.

Holdings and allocations are subject to change. Fund holdings should not be relied on in making investment decisions and should not be construed as research or investment advice regarding particular securities. Current and future holdings are subject to risk.

The Fund files a complete schedule of portfolio holdings with the Securities and Exchange Commission (SEC) for the first and third quarters of each fiscal year as an exhibit to its reports on Form N-PORT. The Fund’s Forms N-PORT are available electronically on the SEC’s website (sec.gov). For a complete list of a fund’s portfolio holdings, view the most recent holdings listing, semi-annual report, or annual report on the Fund’s web site at http://www.bbhfunds.com.

A summary of the Fund’s Proxy Voting Policy that the Fund uses to determine how to vote proxies, if any, relating to securities held in the Fund’s portfolio, as well as a record of how the Fund voted any such proxies during the most recent 12-month period ended June 30, is available, without charge, upon request by calling the toll-free number listed above. This information is also available on the SEC’s website at www.sec.gov.

NOT FDIC INSURED NO BANK GUARANTEE MAY LOSE VALUE

Annual Report

OCTOBER 31, 2022

BBH Select Series - Mid Cap Fund

BBH SELECT SERIES - MID CAP FUND

MANAGEMENT’S DISCUSSION OF FUND PERFORMANCE

October 31, 2022