Exhibit 99.1

Exhibit 99.1

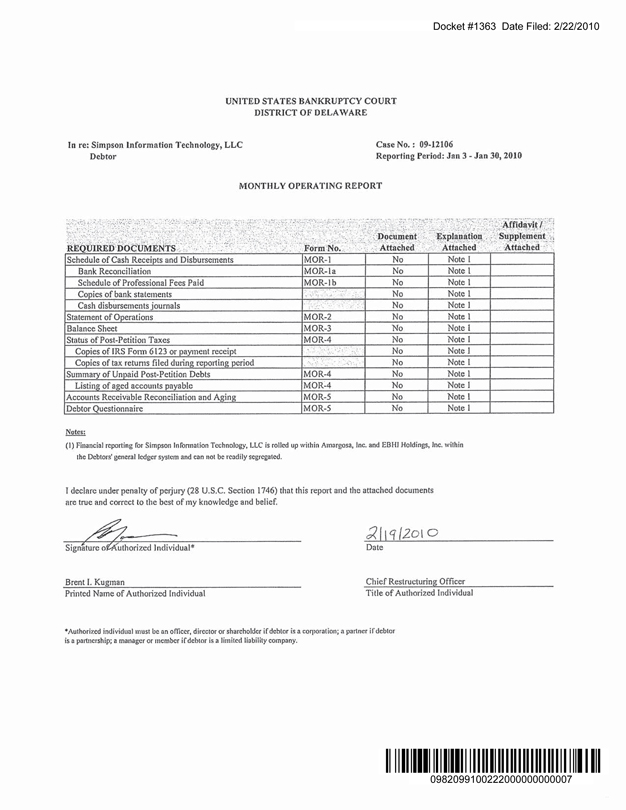

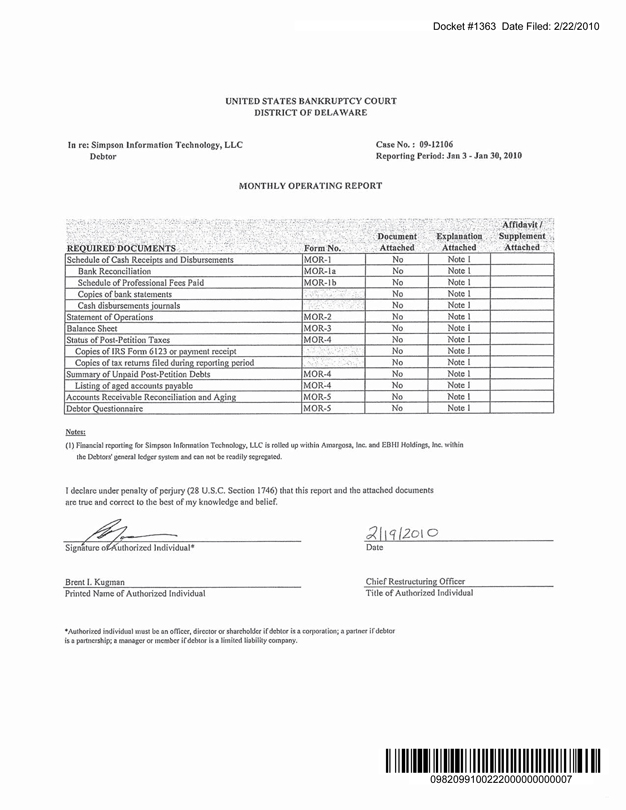

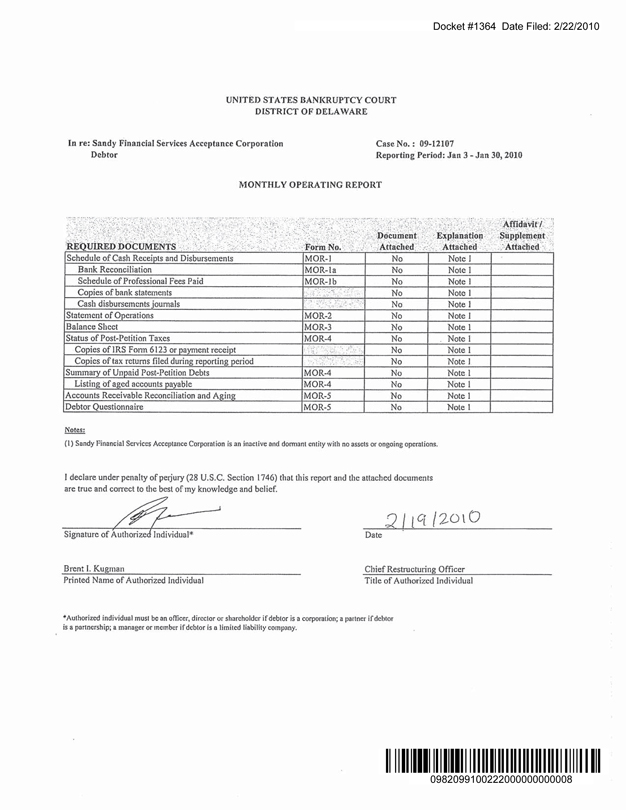

Docket #1357 Date Filed: 2/22/2010

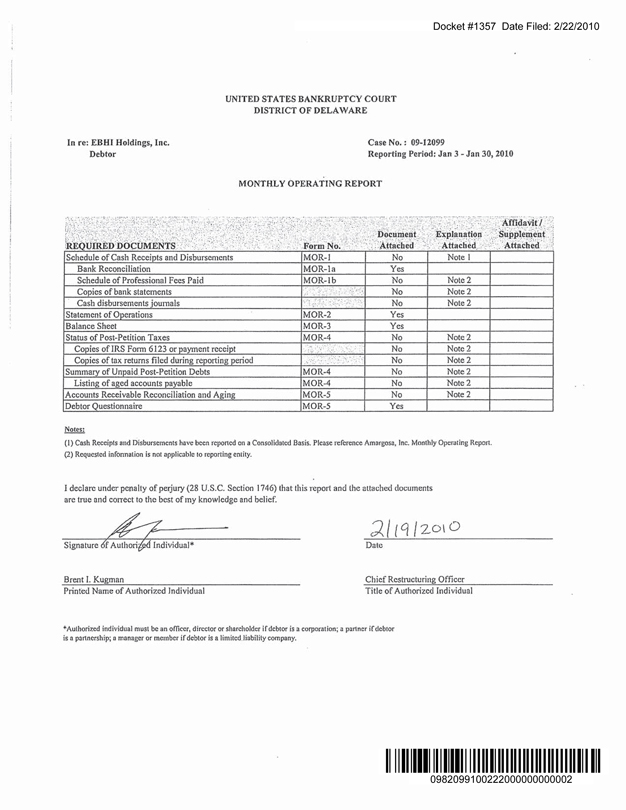

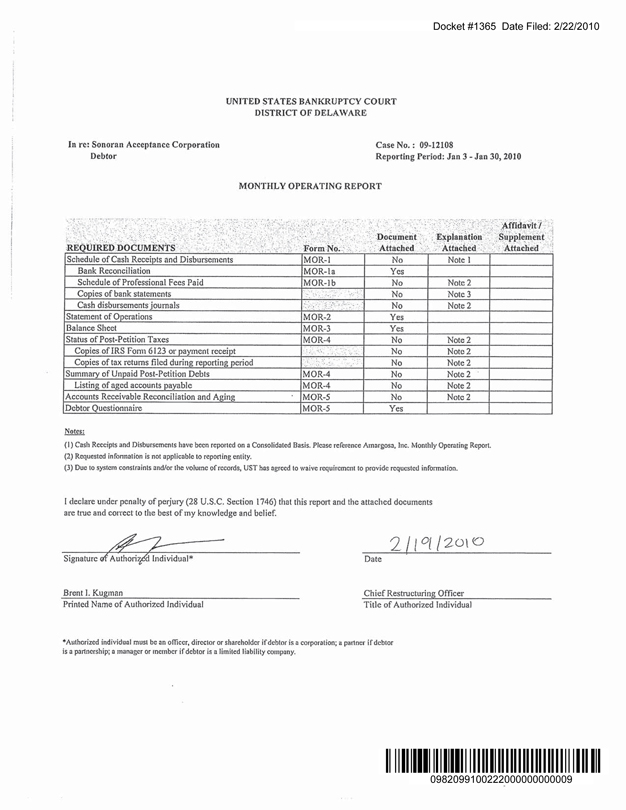

UNITED STATES BANKRUPTCY COURT DISTRICT OF DELAWARE

In re: EBHI Holdings, Inc. Debtor

Case No.: 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Schedule of Cash Receipts and Disbursements

Bank Reconciliation

Schedule of Professional Fees Paid

Copies of bank statements

Cash disbursements journals

Statement of Operations

Balance Sheet

Status of Post-Petition Taxes

Copies of IRS Form 6123 or payment receipt

Copies of tax returns filed during reporting period

Summary of Unpaid Post-Petition Debts

Listing of aged accounts payable

Accounts Receivable Reconciliation and Aging

Debtor Questionnaire

Form No.

MOR-1

MOR-1a

MOR-1b

MOR-2

MOR-3

MOR-4

MOR-4

MOR-4

MOR-5

MOR-5

Document

Attached

No

Yes

No

No

No

Yes

Yes

No

No

No

No

No

No

Yes

Explanation

Attached

Note 1

Note 2

Note 2

Note 2

Note 2

Note 2

Note 2

Note 2

Note 2

Note 2

Affidavit/Supplement Attached

Notes:

(1) Cash Receipts and Disbursements have been responsed on a Consolidated Basis. Please reference Amargosa, Inc. Monthly Operating Report.

(2) Requested information is not applicable to reporting entity.

I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents arc true and correct to the best of my knowledge and belief.

Signature of Authorized Individual*

2/19/2010

Date

Brent I. Kugman

Printed Name of Authorized Individual

Chief Restructuring Officer

Title of Authorized Individual

*Authorized individual must be an officer, director or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company.

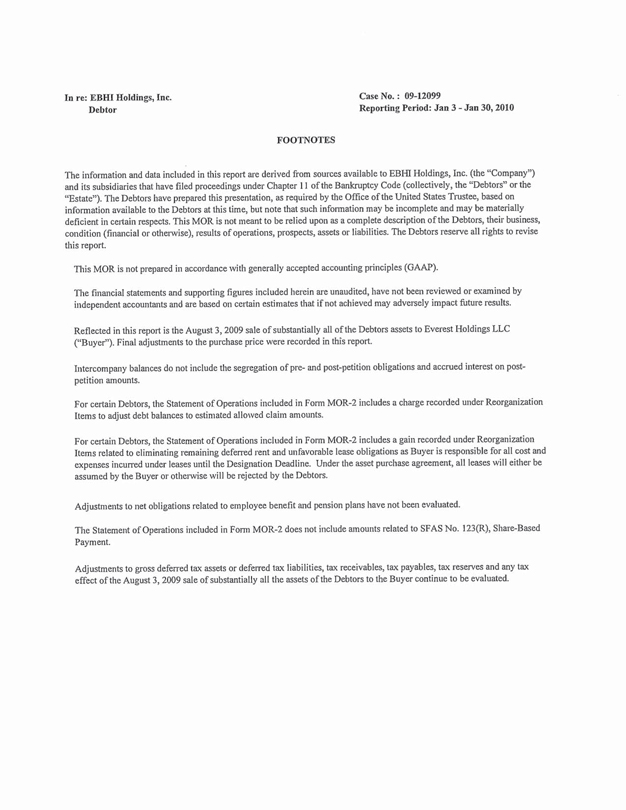

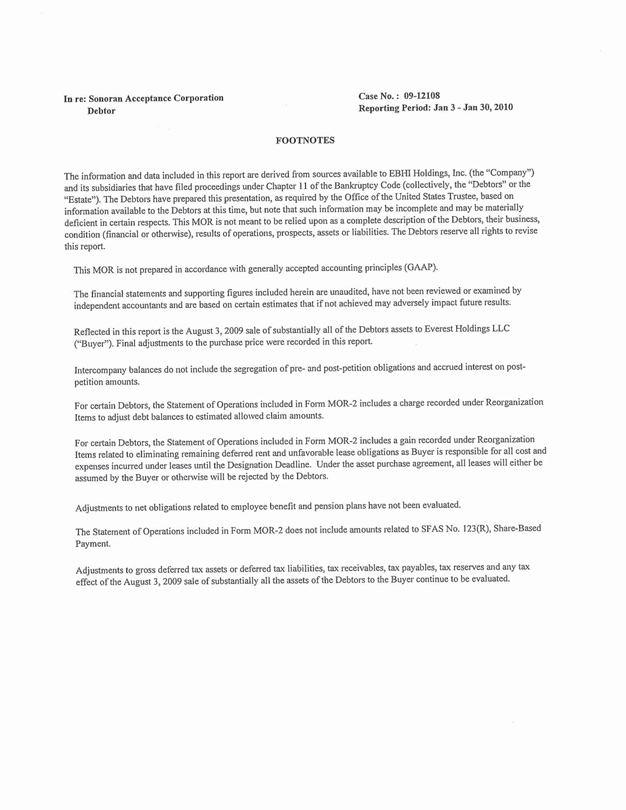

In re: EBHI Holdings, Inc.

Debtor

Case No.: 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter 11 of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post-petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 123(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

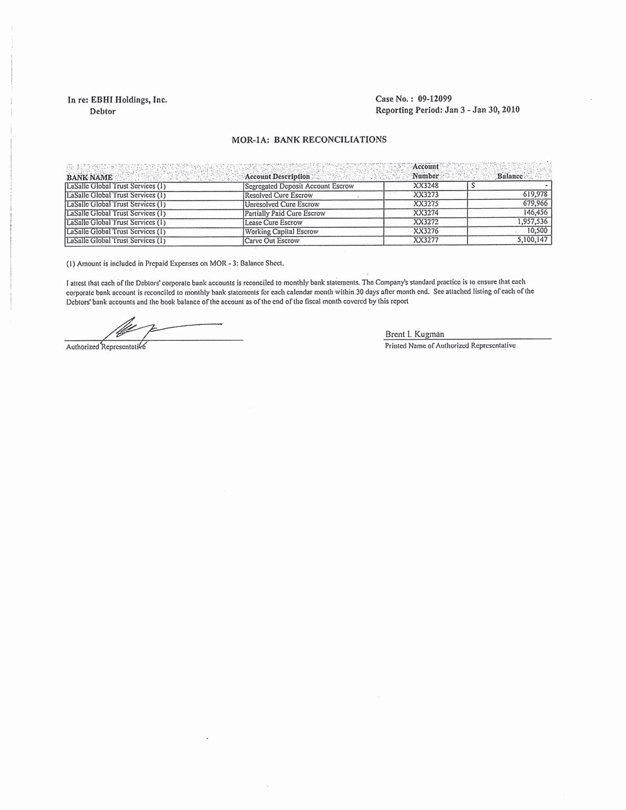

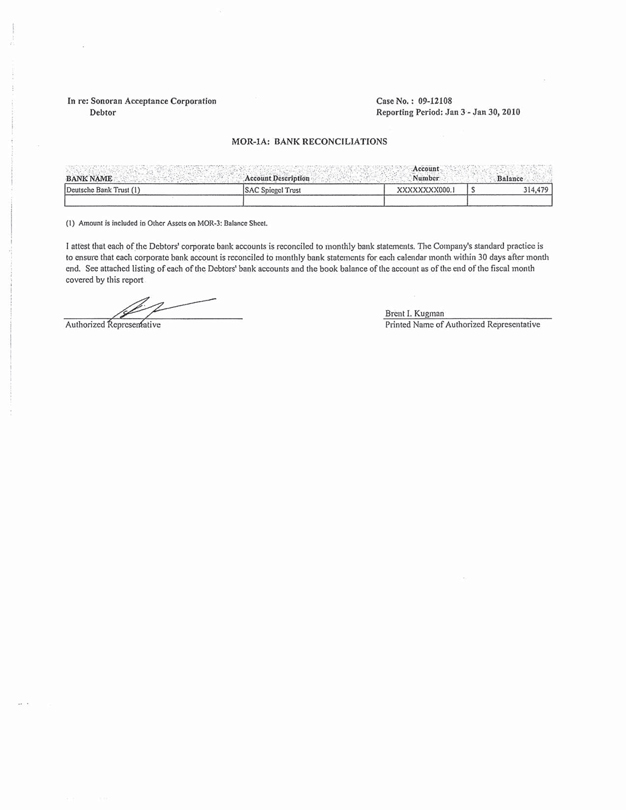

In re: EBHI Holdings, Inc. Debtor

Case No.: 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

MOR-IA: BANK RECONCILIATIONS

BANK NAME

LaSalle Global Trust Services (1)

LaSalle Global Trust Services (1)

LaSalle Global Trust Services (1)

LaSalle Global Trust Services (1)

LaSalle Global Trust Services (1)

LaSalle Global Trust Services (1)

LaSalle Global Trust Services (1)

Account Description

Segregated Deposit Account Escrow

Resolved Cure Escrow

Unresolved Cure Escrow

Partially Paid Cure Escrow

Lease Cure Escrow

Working Capital Escrow

Carve Out Escrow

Account Number

XX3248

XX3273

XX3275

XX3274

XX3272

XX3276

XX3277

Balance

$ -

619,978

679,966

146,456

1,957,536

10,500

5,100,147

(1) Amount is included in Prepaid Expenses on MOP - 3: Balance Sheet.

I attest that each of the Debtors’ corporate bank accounts is reconciled to monthly bank statements. The Company’s standard practice is to ensure that each corporate bank account is reconciled to monthly bank statements for each calendar month within 30 days after month end. See attached listing of each of the Debtors’ bank accounts and the book balance of the account as of the end of the fiscal month covered by this report

Authorized Representative

Brent l. Kugman

Printed Name of Authorized Representative

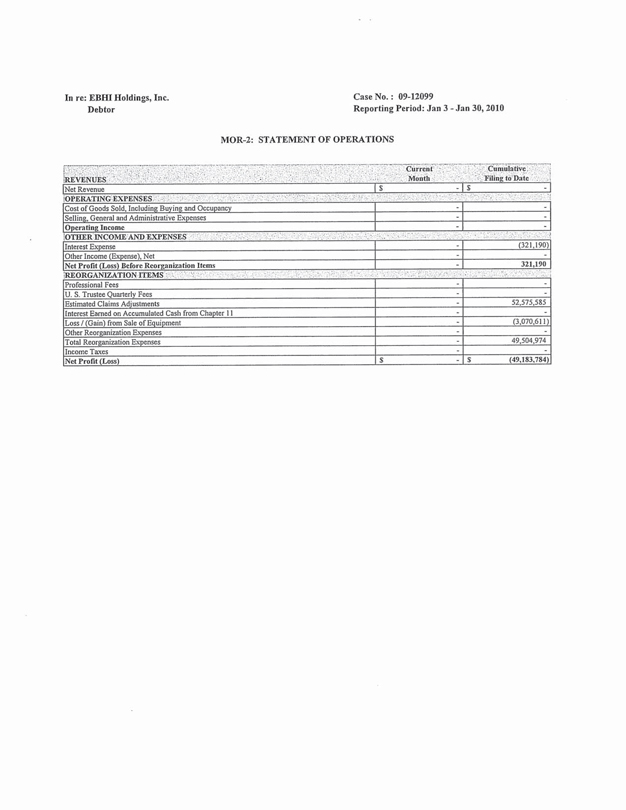

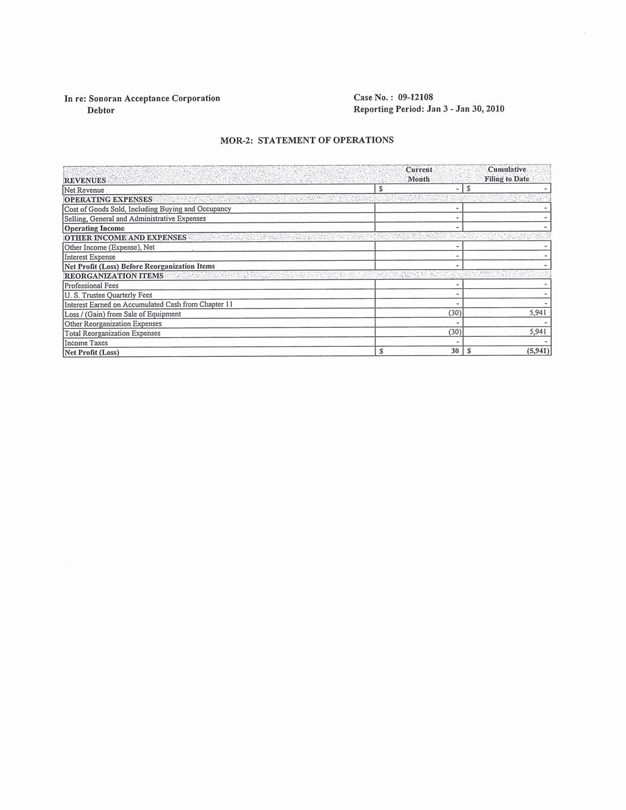

In re: EBHI Holdings, Inc. Debtor

Case No.: 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

REVENUES

Net Revenue

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy

Selling. General and Administrative Expenses

Operating Income

OTHER INCOME AND EXPENSES

Interest Expense

Other Income (Expense), Net

Net Profit (Loss) Before Reorganization Items

REORGANIZATION ITEMS

Professional Fees

U. S. Trustee Quarterly Fees

Estimated Claims Adjustments

Interest Earned on Accumulated Cash from Chapter II

Loss / (Gain) from Sale of Equipment

Other Reorganization Expenses Total Reorganization Expenses

Income Taxes

Net Profit (Loss)

Current Month

$ -

-

-

-

-

-

-

-

-

-

-

-

-

-

-

$ -

Cumulative Filing to Date

$ 1

-

-

-

(321,190)

-

321,190

-

-

52,575,585

-

(3,070,611)

-

49,504,974

-

$(49,I83,784)

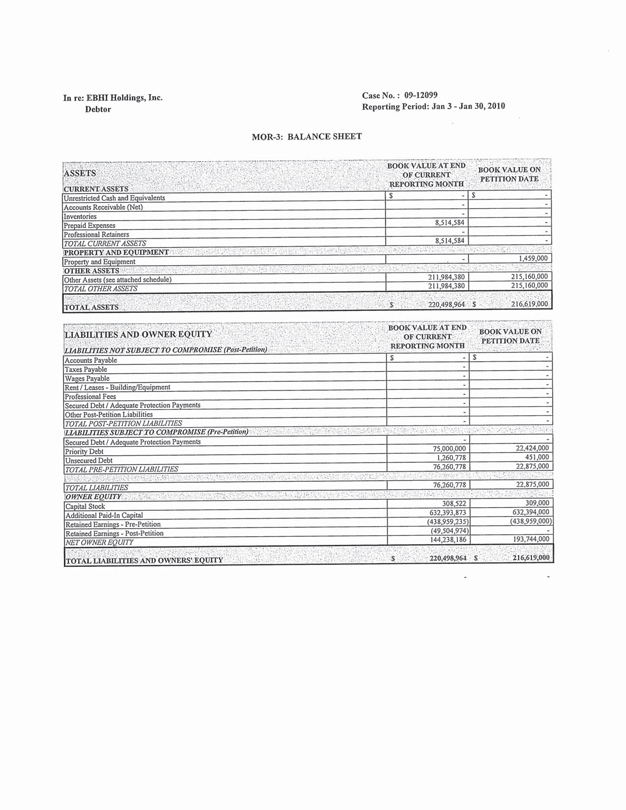

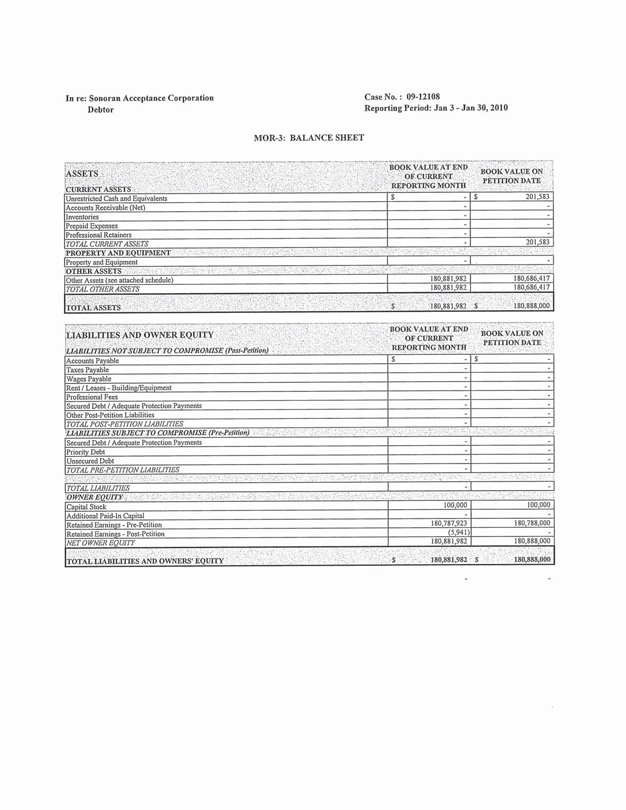

In re: EBHI Holdings, Inc. Debtor

Case No.: 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

MOR-3: BALANCE SHEET

ASSETS

CURRENT ASSETS

Unrestricted Cash and Equivalents

Accounts Receivable (Net)

Inventories

Prepaid Expenses

Professional Retainers

TOTAL CURRENT ASSETS

PROPERTY AND EQUIPMENT

Property and Equipment

OTHER ASSETS

Other Assets (see attached schedule)

TOTAL OTHER ASSETS

TOTAL ASSETS

BOOK VALUE AT END OF CURRENT REPORTING MONTH

$ -

-

-

8,514,584

-

8,514,584

-

211,984,380

211,984.380

$ 220,498,964

BOOK VALUE ON PETITION DATE

$ -

-

-

-

-

-

1,459,000

215,160,000

215,160,000

$ 216,619,000

LIABILITIES AND OWNER EQUITY

LIABILITIES NOT SUBJECT TO COMPROMISE (Post-Petition)

Accounts Payable

Taxes Payable

Wages Payable

Rent / Leases - Building/Equipment

Professional Fees

Secured Debt / Adequate Protection Payments

Other Post-Petition Liabilities

TOTAL POST-PETITION LIABILITIES

LIABILITIES SUBJECT TO COMPROMISE (Pre-Petition)

Secured Debt / Adequate Protection Payments

Priority Debt

Unsecured Debt

TOTAL PRE-PETITION LIABILITIES

TOTAL LIABILITIES

OWNER EQUITY

Capital Stock

Additional Paid-In Capital

Retained Earnings - Pre-Petition

Retained Earnings - Post-Petition

NET OWNER EQUITY

TOTAL LIABILITIES AND OWNERS’ EQUITY

BOOK VALUE AT END OF CURRENT REPORTING MONTH

$ -

-

-

-

-

-

-

-

-

75,000,000

1,260,778

76,260,778

76,260,778

308,522

632,393,873

(438,959,235)

(49,504,974)

144,238,186

$ 220,498,964

BOOK VALUE ON PETITION DATE

$ -

-

-

-

-

-

-

-

22,424,000

451,000

22,875,000

22,875,000

309,000

632,394,000

(438,959,000)

-

193,744,000

$ 216,619,000

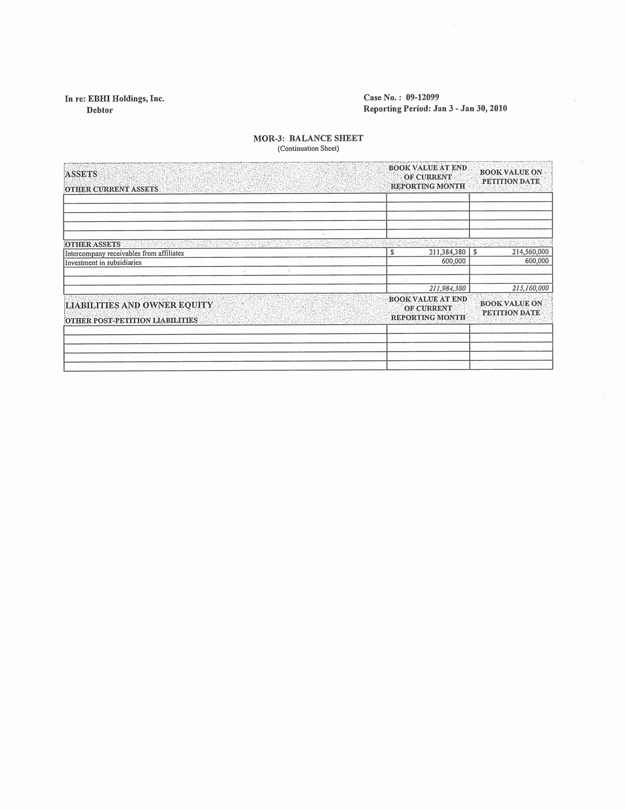

In re: EBHI Holdings, Inc. Debtor

Case No. : 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

MOR-3: BALANCE SHEET

(Continuation Sheet)

ASSETS

OTHER CURRENT ASSETS

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

OTHER ASSETS

Intercompany receivables from affiliates

Investment in subsidiaries

LIABILITIES AND OWNER EQUITY

OTHER POST-PETITION LIABILITIES

$211,384,380

600,000

$214,560,000

600,000

211,984,380

215,160,000

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

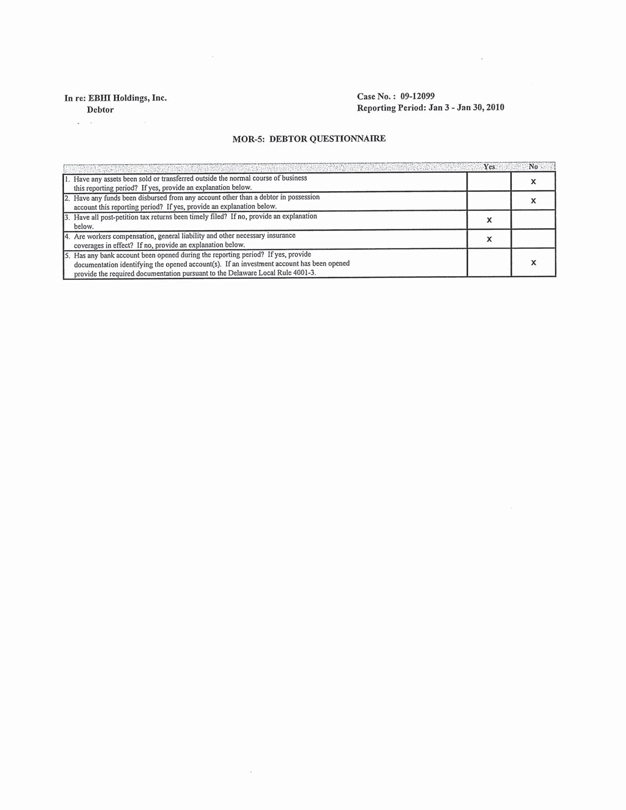

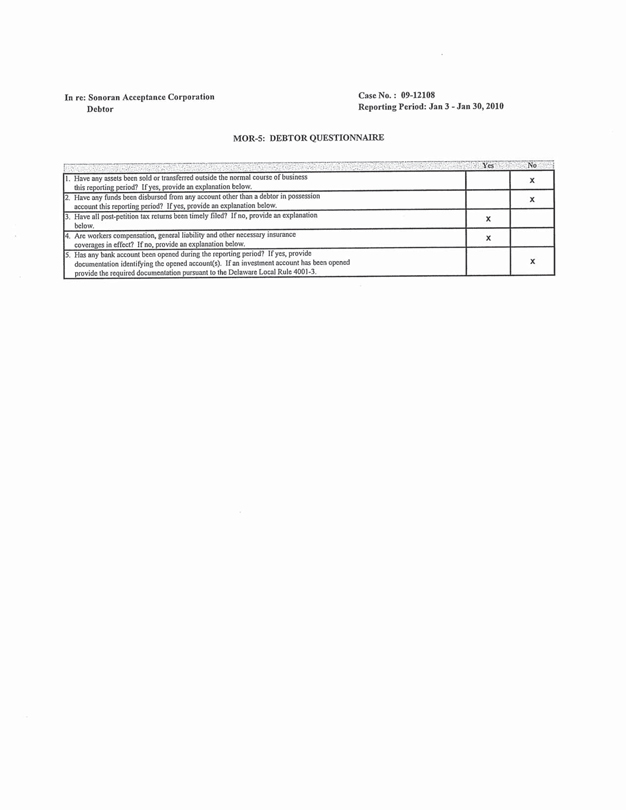

In re: EBHI Holdings, Inc. Debtor

Case No.: 09-12099

Reporting Period: Jan 3 - Jan 30, 2010

MOR-5: DEBTOR QUESTIONNAIRE

1. Have any assets been sold or transferred outside the normal course of business this reporting period? If yes, provide an explanation below.

2. Have any funds been disbursed from any account other than a debtor in possession account this reporting period? If yes, provide an explanation below.

3. Have all post-petition tax returns been timely filed? If no, provide an explanation below.

4. Are workers compensation, general liability and other necessary insurance coverages in effect? If no, provide an explanation below.

5. Has any bank account been opened during the reporting period? If yes, provide documentation identifying the opened account(s). If an investment account has been opened provide the required documentation pursuant to the Delaware Local Rule 4001-3.

x

x

x

x

x

Yes

No

Docket #1358 Date Filed: 2/22/2010

UNITED STATES BANKRUPTCY COURT DISTRICT OF DELAWARE

In re: Amargosa, Inc. Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Schedule of Cash Receipts and Disbursements

Bank Reconciliation

Schedule of Professional Fees Paid

Copies of bank statements

Cash disbursements journals

Statement of Operations

Balance Sheet

Status of Post-Petition Taxes

Copies of IRS Form 6123 or payment receipt

Copies of tax returns filed during reporting period

Summary of Unpaid Post-Petition Debts

Listing of aged accounts payable

Accounts Receivable Reconciliation and Aging

Debtor Questionnaire

Form No.

MOR-l

MOR-1a

MOR-l b

MOR-2

MOR-3

MOR-4

MOR-4

MOR-4

MOR-5

MOR-5

Document Attached

Yes

Yes

No

No

No

Yes

Yes

Yes

No

No

Yes

No

No

Yes

Explanation Attached

Note I

Note 2

Note 2

Note 2

Note 2

Note 2

Note 1

Affidavit/Supplement Attached

MOR-4a & 4b

Notes:

(1) Requested information is not applicable to reporting entity.

(2) Due to system constraints and/or the volume of records, UST has agreed to waive requirement to provide requested information.

I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief:

Signature of Authorized Individual*

2/19/2010

Date

Brent I. Kugman

Printed Name of Authorized Individual

Chief Restructuring Officer

Title of Authorized Individual

*Authorized individual must be an officer, director or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company.

In re: Amargosa, Inc. Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter 11 of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post-petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 123(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

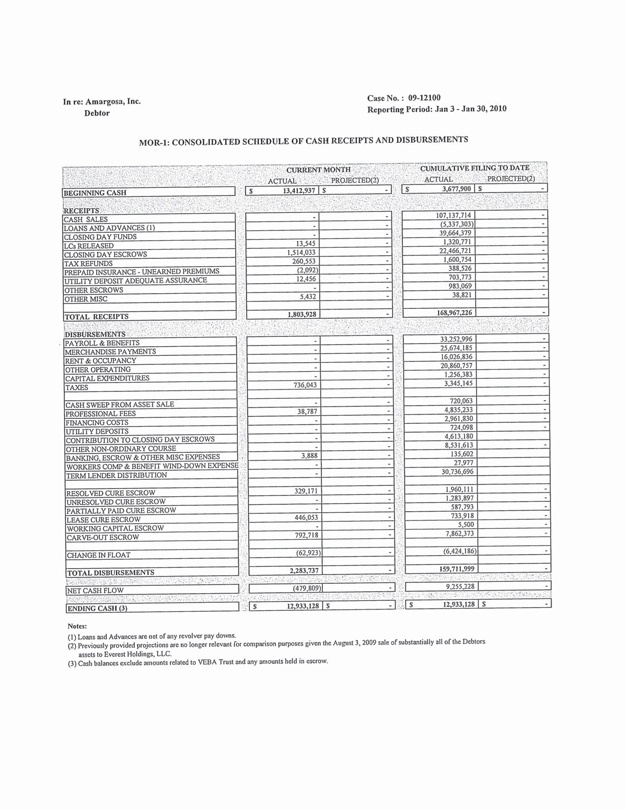

In re: Amargosa, Inc. Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

MOR-1: CONSOLIDATED SCHEDULE OF CASH RECEIPTS AND DISBURSEMENTS

BEGINNING CASH

CASH SALES

LOANS AND ADVANCES (I)

CLOSING DAY FUNDS

LC’s RELEASED

CLOSING DAY ESCROWS

TAX REFUNDS

PREPAID INSURANCE-UNEARNED PREMIUMS

UTILITY DEPOSIT ADEQUATE ASSURANCE

OTHER ESCROWS

OTHER MISC

TOTAL RECEIPTS

DISBURSEMENTS

PAYROLL & BENEFITS

MERCHANDISE PAYMENTS

RENT & OCCUPANCY

OTHER OPERATING

CAPITAL EXPENDITURES

TAXES

CASH SWEEP FROM ASSET SALE

PROFESSIONAL FEES

FINANCING COSTS

UTILITY DEPOSITS

CONTRIBUTION TO CLOSING DAY ESCROWS

OTHER NON-ORDINARY COURSE BANKING, ESCROW & OTHER MISC EXPENSES

WORKERS COMP & BENEFIT WIND-DOWN EXPENSES

TERM LENDER DISTRIBUTION

RESOLVED CURE ESCROW

UNRESOLVED CURE ESCROW

PARTIALLY PAID CURE ESCROW

LEASE CURE ESCROW

WORKING CAPITAL ESCROW

CARVE-OUT ESCROW

CHANGE IN FLOAT

TOTAL DISBURSEMENTS

NET CASH FLOW ENDING CASH (3)

CURRENT MONTH

ACTUAL

PROJECTED(2)

CUMULATIVE FILING TO DATE

ACTUAL

PROJECTED(2)

$ 13.412,937

(479.809)

12,933,128

$13,545

1,514,033

260,553

(2,092)

12,456

5,432

1,803,928

736,043

38,787

3,888

329,171

446,053

792,718

2,283,737

(62,923)

-

-

-

-

-

-

-

-

-

9.255,228

$12,933,128

107,137,714

(5,337,303)

39,664,379

1,320,771

22,466,721

1,600,754

388,526

703,773

983,069

38,821

168,967,226

33.252,996

25,674.185

16.026.836

20,860,757

1,256,383

3,345,145

720,063

4,835,233

2,961,830

724.098

4,613,180

8,531,613

135,602

27,977

30736696

1,960,111

1,283,897

587,793

733,918

5,500

7.862.373

(6,424,186)

159,711,999

Notes:

(I) Loans and Advances are net of any revolver pay downs.

(2) Previously provided projections are no longer relevant for comparison purposes given the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings, LLC.

(3) |

| Cash balances exclude amounts related to VEBA Trust and any amounts held in escrow. |

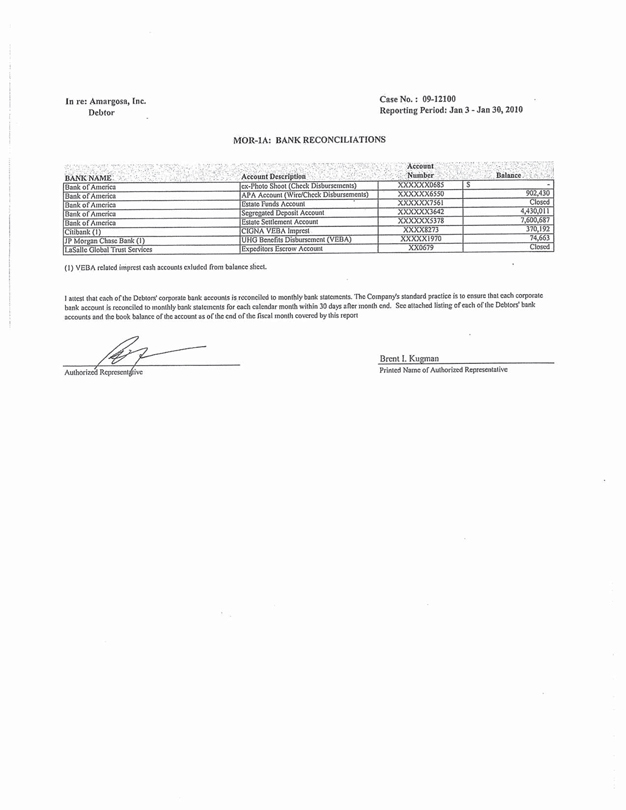

In re: Amargosa, Inc.

Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

MOR-1A: BANK RECONCILIATIONS

BANK NAME

Bank of America

Bank of America

Bank of America

Bank of America

Bank of America

Citibank (I)

JP Morgan Chase Bank (I)

LaSalle Global Trust Services

Account Description

ex-Photo Shoot (Check Disbursements)

APA Account (Wire/Check Disbursements)

Estate Funds Account

Segregated Deposit Account

Estate Settlement Account

CIGNA VEBA Imprest

UHG Benefits Disbursement (VEBA)

Expeditors Escrow Account

Account

Number

XXXXXX0685

XXXXXX6550

XXXXXX7361

XXXXXX3642

XXXXXX5378

XXXX8273

XXXXX1970

XX0679

Balance

$ -

902,430

Closed

4,430,011

7,600,687

370,192

74,663

Closed

(I) VEBA related imprest cash accounts excluded from balance sheet.

I attest that each of the Debtors, corporate bank accounts is reconciled to monthly bank statements. The Company’s standard practice is to ensure that each corporate bank account is reconciled to monthly bank statements for each calendar month within 30 days after month end. See attached listing of each of the Debtors’ bank accounts and the book balance of the account as of the end of the fiscal month covered by this report

Authorized Representative

Brent I. Kugman

Printed Name of Authorized Representative

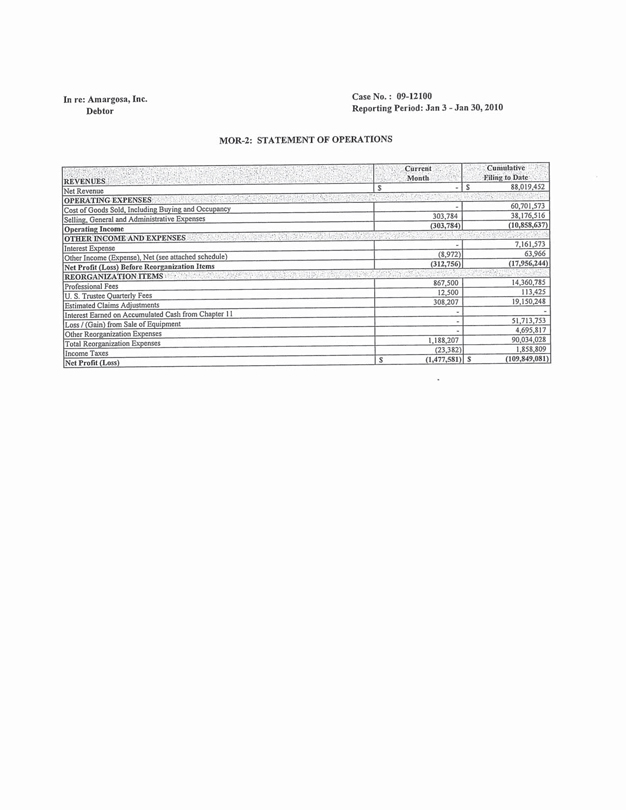

In re: Amargosa, Inc.

Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

REVENUES.

Net Revenue

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy

Selling, General and Administrative Expenses

Operating Income

OTHER INCOME AND EXPENSES

Interest Expense

Other Income (Expense), Net (see attached schedule)

Net Profit (Loss) Before Reorganization Items

REORGANIZATION ITEMS

Professional Fees

U.S. Trustee Quarterly Fees

Estimated Claims Adjustments

Interest Earned on Accumulated Cash from Chapter 11

Loss / (Gain) from Sale of Equipment

Other Reorganization Expenses

Total Reorganization Expenses

Income Taxes

Net Profit (Loss)

Current Month

$ -

303,784

(303,784)

-

(8,972)

(312,756)

867,500

12,500

308,207

-

-

1,188,207

(23,382)

$ (1,477,581)

Cumulative Filing to Date

$ 88,019,452

60,701,573

38,176,516

(10,858,637)

7,161,573

63,966

(17,956,244)

14,360,785

113,425

19,150,248

51,713,753

4,695,817

90,034,028

1,858,809

$ (109,849,081)

In re: Amargosa, Inc.

Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

(Continuation Sheet)

BREAKDOWN OF “OTHER” CATEGORY

Other Income

Equity in (earnings) of foreign joint ventures

Investment income

Bank Fee

Current

Month

$ -

(8,972)

$ (8,972)

Cumulative

Filing to Date

$ 208,264

109

(135,435)

$ 72,938

In re: Amargosa, Inc.

Debtor

Case No. : 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

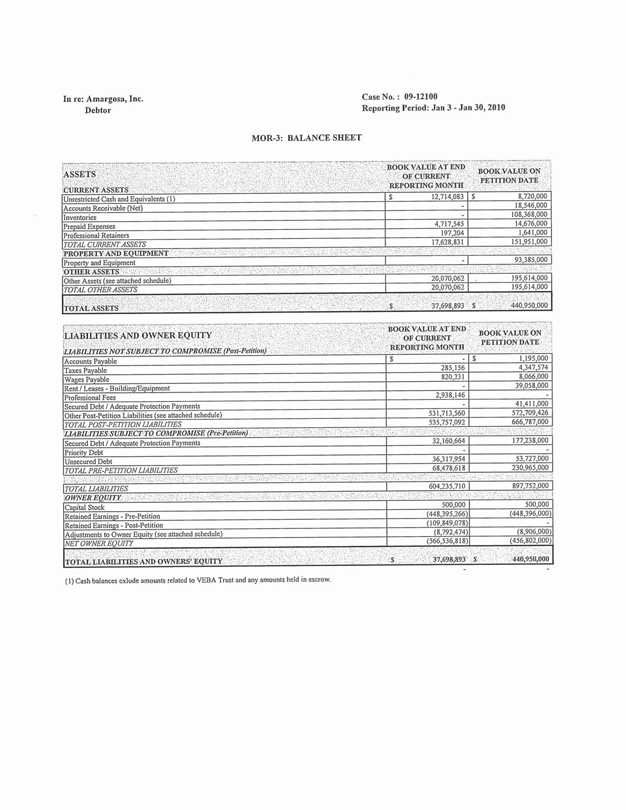

MOR-3: BALANCE SHEET

ASSETS

CURRENT ASSETS

Unrestricted Cash and Equivalents (1)

Accounts Receivable (Net)

Inventories

Prepaid Expenses

Professional Retainers

TOTAL CURRENT ASSETS

PROPERTY AND EQUIPMENT

Property and Equipment

OTHER ASSETS

Other Assets (see attached schedule)

TOTAL OTHER ASSETS

TOTAL ASSETS

BOOK VALUE AT END OF CURRENT

REPORTING MONTH

$ 12,714,083

-

-

4,717,545

197,204

17,628,831

20,070,062

20,070,062

$37,698,893

BOOK VALUE ON

PETITION DATE

$ 8,720,000

18,546,000

108,368,000

14,676,000

1,641,000

151,951,000

93,385,000

195,614,000

195,614,000

$ 440,950,000

LIABILITIES AND OWNER EQUITY

LIABILITIES NOT SUBJECT TO COMPROMISE (Post-Petition)

Accounts Payable

Taxes Payable

Wages Payable

Rent / Leases - Building/Equipment

Professional Fees

Secured Debt / Adequate Protection Payments

Other Post-Petition Liabilities (see attached schedule)

TOTAL POST-PETITION LIABILITIES

LIABILITIES SUBJECT TO COMPROMISE (Pre-Petition)

Secured Debt / Adequate Protection Payments Priority Debt

Unsecured Debt

TOTAL PRE-PETITION LIABILITIES

TOTAL LIABILITIES

OWNER EQUITY

Capital Stock

Retained Earnings - Pre-Petition

Retained Earnings - Post-Petition

Adjustments to Owner Equity (see attached schedule)

NET OWNER EQUITY

TOTAL LIABILITIES AND OWNERS’ EQUITY

BOOK VALUE AT END OF CURRENT

REPORTING MONTH

$ -285,156

820,231

-

2,938,146

531,713,560

535,757,093

32,160,664

-

36,317,954

68,478,618

604,235,710

500,000

(448,395,266)

(109,849,078)

(8,792,474)

(566,536,818)

$ 37,698,893

BOOK VALUE ON

PETITION DATE

$ 1,195,000

4,347,574

8,066,000

39,058,000

-

41,411,000

572,709,426

666,787,000

177,238,000

-

53,727,000

230,965,000

897,752,000

500,000

(448,396,000)

(8,906,000)

(456,803,000

$ 440,950,000

(1) Cash balances exclude amounts related to VEBA Trust and any amounts held in escrow.

In re: Amargosa, Inc.

Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

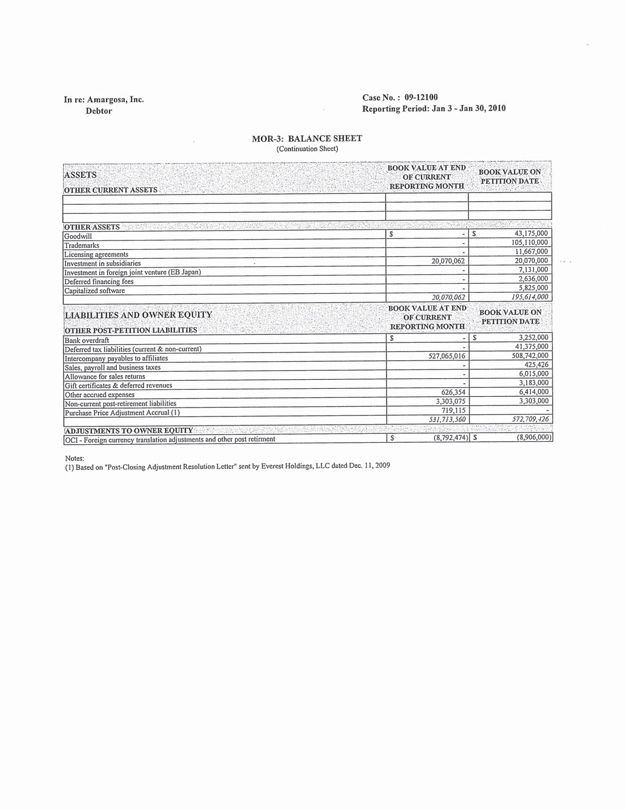

MOR-3: BALANCE SHEET (Continuation Sheet)

ASSETS

OTHER CURRENT ASSETS

OTHER ASSETS

Goodwill Trademarks

Licensing agreements

Investment in subsidiaries

Investment in foreign joint venture (EB Japan)

Deferred financing fees

Capitalized software

LIABILITIES AND OWNER EQUITY

OTHER POST-PETITION LIABILITIES

Bank overdraft

Deferred tax liabilities (current & non-current)

Intercompany payables to affiliates

Sales, payroll and business taxes

Allowance for sales returns

Gift certificates & deferred revenues

Other accrued expenses

Non-current post-retirement liabilities

Purchase Price Adjustment Accrual (1)

ADJUSTMENTS TO OWNER EQUITY

OCI - Foreign currency translation adjustments and other post retirement

BOOK VALUE AT END OF CURRENT

REPORTING MONTH

$-

-

-

20,070,062

-

-

-

20,070,062

BOOK VALUE AT END

-

of current REPORTING MONTH

$ -

-

527,065,016

626,354

3,303,075

719,115

531,713,560

$ (8,792,474)

BOOK VALUE ON PETITION DATE

$ 43,175.000

105,110,000

11,667,000

20,070,000

7,131,000

2,636,000

5,825,000

195,614,000

BOOK VALUE ON

PETITION DATE

$ 3,252,000

41,375,000

508,742,000

425,426

6,015,000

31, 83000

6,414,000

3,303,000

-

572,709,426

$ (8,906,000)

Notes:

(1) Based on “Post-Closing Adjustment Resolution Letter” sent by Everest Holdings, LLC dated Dec. 11, 2009

In re: Amargosa, Inc. Debtor

Case No.: 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

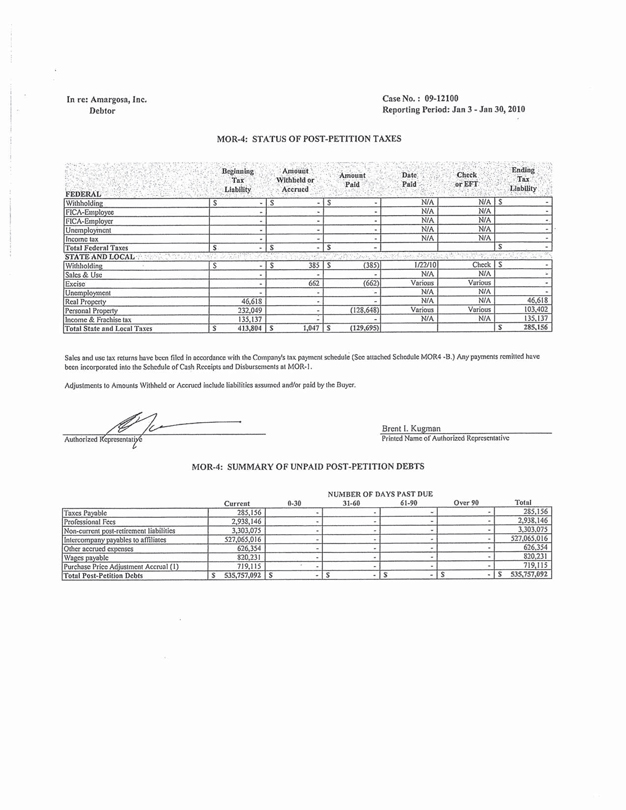

MOR-4: STATUS OF POST-PETITION TAXES

FEDERAL

Withholding

FICA-Employee

FICA-Employer

Unemployment

Income Tax

Total Federal Taxes

STATE AND LOCAL

Withholding

Sales & Use

Excise

Unemployment

Real Property

personal Property

Income & Frachise tax

Total State and Local Taxes

Beginning Tax Liability

$ -

46,618

232,049

135,137

$413,804

Amount Withheld or Accrued

$385-

662-

$1,047

Amount Paid

(385)-

(662)-

(128,648)

$(129,695)

Date Paid N/A

1/22/10 Various

N/A

Check or EFT N/A

Ending Tax Liability

46,618

103,402

135,137

$285,156

Sales and use tax returns have been filed in accordance with the Company’s tax payment schedule (See attached Schedule MOR4-B.) Any payments remitted have been incorporated into the Schedule of Cash Receipts and Disbursements at MOR-l.

Adjustments to Amounts Withheld or Accrued include liabilities assumed and/or paid by the Buyer.

Authorized Representative

Brent I. Kugman Printed Name of Authorized Representative

MOR-4: SUMMARY OF UNPAID POST-PETITION DEBTS

NUMBER OF DAYS PAST DUE

Taxes Payable

Professional Fees

Non-current post-retirement liabilities

Intercompany payables to affiliates

Other accured expenses

Wages payable

Purchase Price Adjustment Accrual (1)

Total Post-Petition Debts

Current

285,156

2,938,146

3,303,075

527,065,016

626,354

820,231

719,115

$ 535,757,092

0-30 31-60 61-90 Over 90

Total

285,156

2,938,146

3,303,075

527,065,016

626,354

820,231

719,115

$ 535,757,092

In re: Amargosa, Inc.

Debtor

Case No.: 09-12100

Reporting Period: Jan 3—Jan 30,2010

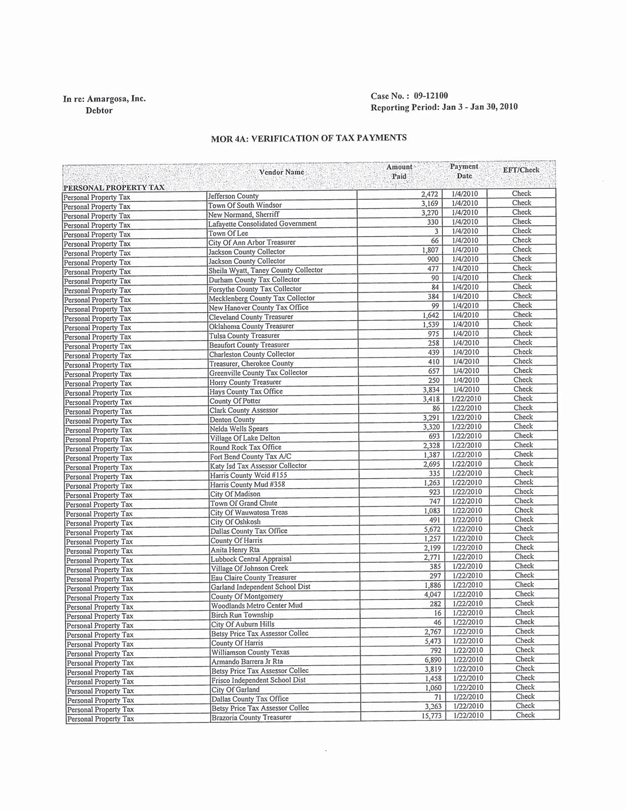

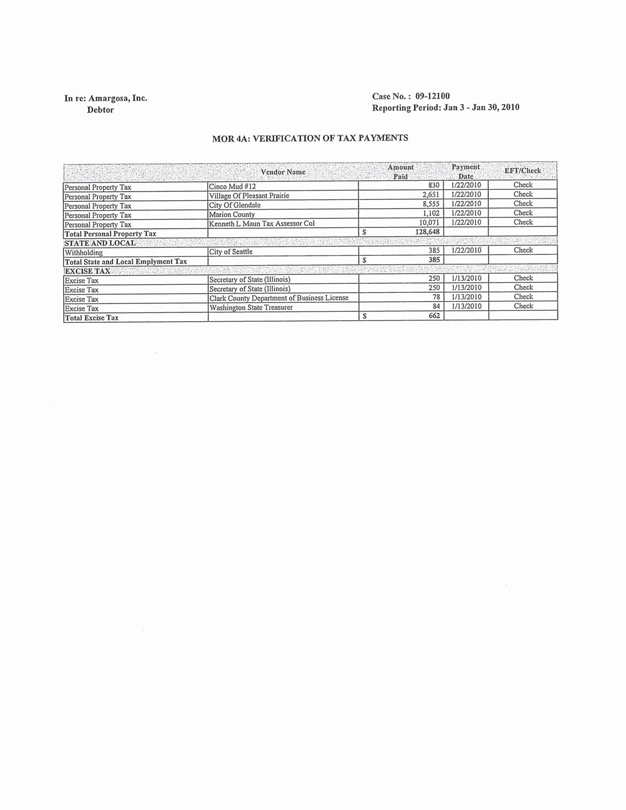

MOR 4A: VERIFICATION OF TAX PAYMENTS

PERSONAL PROPERTY TAX

Personal Property Tax

Vendor Name

Jefferson County

Town Of South Windsor

New Normand, Sherriff

Lafayette Consolidated Government

Town Of Lee

City Of Ann Arbor Treasurer

Jackson County Collector

Jackson County Collector

Sheila Wyatt, Taney County Collector

Durham County Tax Collector

Forsy the County Tax Collector

Mecklenberg County Tax Collector

New Hanover County Tax Office

Cleveland County Treasurer

Oklahoma County Treasurer

Tulsa County Treasurer

Beaufort County Treasurer

Charleston County Collector

Treasurer, Cherokee County

Greenville County Tax Collector

Horry County Treasurer

Hays County Tax Office

County Of Potter

Clark County Assessor

Denton County

Nelda Wells Spears

Village Of Lake Delton

Round Rock Tax Office

Fort Bend County Tax A/C

Katy Isd Tax Assessor Collector

Harris CountyWcid #l55

Harris County Mud #358

City Of Madison

Town Of Grand Chute

City Of Wauwatosa Treas

City Of Oshkosh

Dallas County Tax Office

County Of Harris

Anita Henry Rta

Lubbock Central Appraisal

Village Of Johnson Creek

Eau Claire County Treasurer

Garland Independent School Dist

County Of Montgomery

Woodlands Metro Center Mud

Birch Run Township

City Of Auburn Hills

Betsy Price Tax Assessor Collec

County Of Harris

Williamson County Texas

Amando Barrera Jr Rta

Betsy Price Tax Assessor Collec

Frisco Independent School Dist

City Of Garland

Dallas County Tax Office

Betsy Price Tax Assessor Collec

Brazoria County Treasurer

Amount Paid

2,472 3,169 3,270 330 3 66 1,807 900 477

90 84 384 99 1,642 1,539 975 258 439 410 657 250 3,834 3,418 86 3,291

3,320 693 2,328 1,387 2,695 335 1,263 923 747 1,083 491 5,672 1,257 2,199

2,771 385 297 1,886 4,047 282 16 46 2,767 5,473 792 6,890 3,819 1,458 1,060 71 3,263

15,773 Payment Date 1/4/2010 1/22/2010

EFT/Check

Check

In re: Amargosa, Inc. Debtor

Case No.: 09-12100

Reporting Period: Jan 3—Jan 30, 2010

MOR 4A: VERIFICATION OF TAX PAYMENTS

Personal Property Tax Total Personal Property Tax

STATE AND LOCAL

Withholding

Total State and Local Employment Tax

EXCISE TAX

Excise Tax Total Excise Tax

Vendor Name

Cinco Mud #12

Village Of Pleasant Prairie

City Of Glendale

Marion County

Kenneth L Maun Tax Assessor Col

City of Seattle

Secretary of State (Illinois)

Secretary of State (Illinois)

Clark County Department of Business License

Washington State Treasurer

Amount Paid

830 2,651 8,555 1,102 10,071 $128,648 385 $385 250 250 78 84 $662

Payment Date 1/22/2010 1/13/2010

EFT/Check

Check

In re: Amargosa, Inc. Debtor

Case No. : 09-12100

Reporting Period Jan 3 - Jan 30, 2010

MOR 4B: SUMMARY OF TAX RETURNS FILED DURING REPORTING PERIOD

TAXING AUTHORITY

State

Type of Tax

Due Date

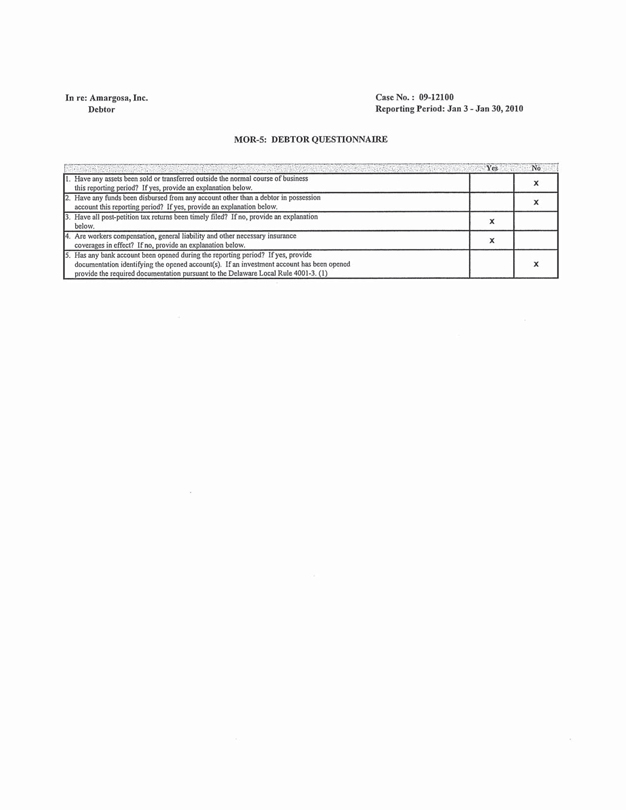

In re: Amargosa, Inc. Debtor

Case No. : 09-12100

Reporting Period: Jan 3 - Jan 30, 2010

MOR-5: DEBTOR QUESTIONNAIRE

1. Have any assets been sold or transferred outside the normal course of business this reporting period? If yes, provide an explanation below.

2. Have any funds been disbursed from any account other than a debtor in possession account this reporting period? If yes, provide an explanation below.

3. Have all post-petition tax returns been timely filed? If no, provide an explanation below.

4. Are workers compensation, general liability and other necessary insurance coverages in effect? If no, provide an explanation below.

5. Has any bank account been opened during the reporting period? If yes, provide documentation identifying the opened account(s). If an investment account has been opened provide the required documentation pursuant to the Delaware Local Rule 4001-3. (1)

Yes X X

No X X X

Docket #1359 Date Filed: 2/22/2010

UNITED STATES BANKRUPTCY COURT DISTRICT OF DELAWARE

In re: Gobi Fulfillment Services, Inc.

Debtor

Case No. : 09-12101

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Schedule of Cash Receipts and Disbursements

Bank Reconciliation

Schedule of Professional Fees Paid

Copies of bank statements

Cash disbursements journals

Statement of Operations

Balance Sheet

Status of Post-Petition Taxes

Copies of IRS Form 6123 or payment receipt

Copies of tax returns filed during reporting period

Summary of Unpaid Post-Petition Debts

Listing of aged accounts payable

Accounts Receivable Reconciliation and Aging

Debtor Questionnaire

Form No.

MOR-1

MOR-1a

MOR-1b

MOR-2

MOR-3

MOR-4

MOR-4

MOR-4

MOR-5

MOR-5

Document

Attached

No

No

No

No

No

Yes

Yes

Yes

No

No

Yes

No

No

Yes

Explanation

Attached

Note 1

Note 2

Note 2

Note 3

Note 3

Note 3

Note 3

Note 3

Note 2

Affidavit /

Supplement

Attached

Notes:

(I) Cash Receipts and Disbursements have been reported on a Consolidated Basis. Please reference Amargosa, Inc. Monthly Operating Report.

(2) |

| Requested information is not applicable to reporting entity. |

(3) Due to system constraints and/or the volume of records, UST has agreed to waive requirement to provide requested information.

I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief.

Signature of Authorized Individual*

Date 2/19/2010

Brent I. Kugman

Printed Name of Authorized Individual

Chief Restructuring Officer Title of Authorized Individual

*Authorized individual must be an officer, director or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company.

In re: Gobi Fulfillment Services, Inc.

Debtor

Case No.: 09-12101

Reporting Period: Jan 3—Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter 11 of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post-petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 123(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

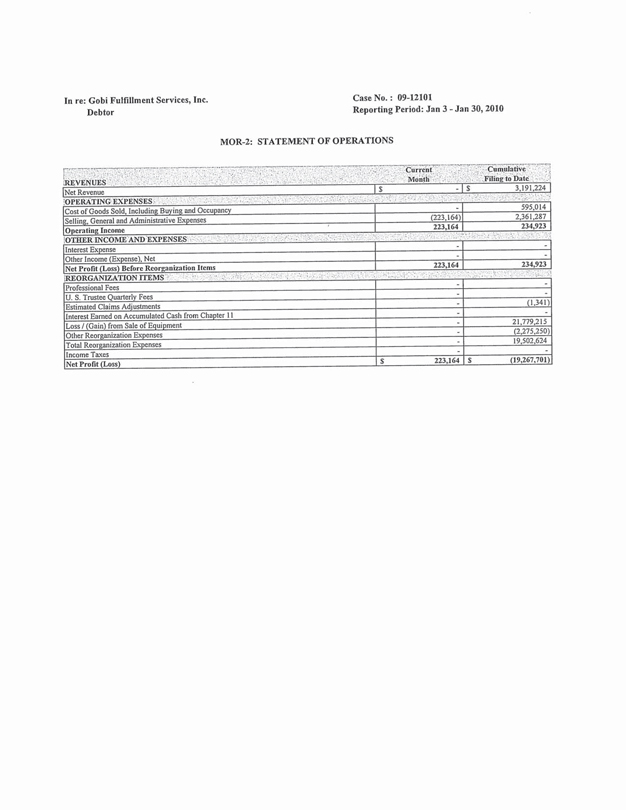

In re: Gobi Fulfillment Services, Inc. Debtor

Case No. : 09-12101

Reporting Period: Jan 3—Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

REVENUES

Net Revenue

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy

Selling, General and Administrative Expenses

Operating Income

OTHER INCOME AND EXPENSES

Interest Expense

Other Income (Expense), Net

Net Profit (Loss) Before Reorganization Items

REORGANIZATION ITEMS

Professional Fees

U. S. Trustee Quarterly Fees

Estimated Claims Adjustments

Interest Earned on Accumulated Cash from Chapter 11

Loss / (Gain) from Sale of Equipment

Other Reorganization Expenses

Total Reorganization Expenses

Income Taxes

Net Profit (Loss)

Current

Month

$—

-

(223.164)

223,164

223,164

-

-

-

-

-

-

-

-

$ 223,164

Cumulative

Filing to Date

$ 3,191,224

595,014

2,361,287

234,923

-

-

234,923

-

(1,341)

-

21,779,215

(2,275,250)

19,502,624

-

$ (19,267,701)

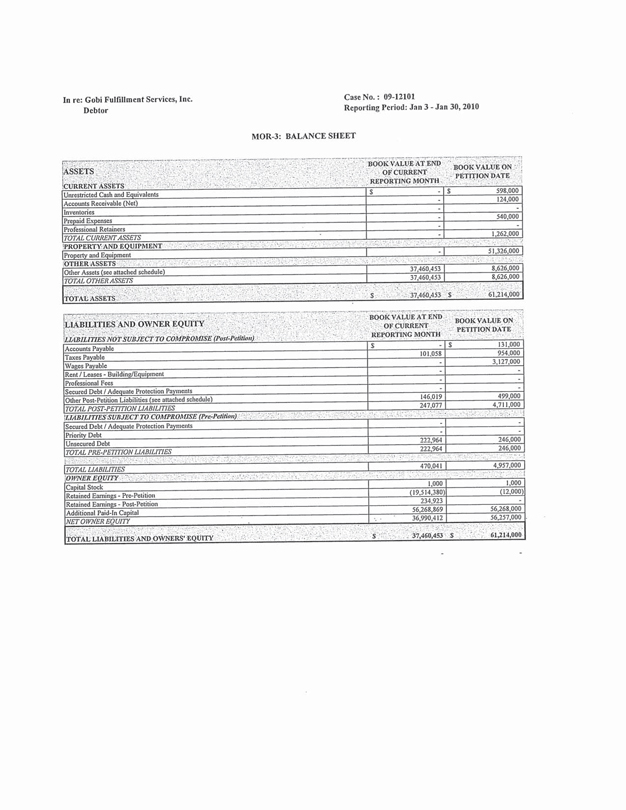

In re: Gobi Fulfillment Services, Inc.

Debtor

Case No.: 09-12101

Reporting Period: Jan 3- Jan 30, 2010

MOR-3: BALANCE SHEET

ASSETS

CURRENT ASSETS

Unrestricted Cash and Equivalents

Accounts Receivable (Net)

Inventories

Prepaid Expenses

Professional Retainers

TOTAL CURRENT ASSETS

PROPERTY AND EQUIPMENT

Property and Equipment

OTHER ASSETS

Other Assets (see attached schedule)

TOTAL OTHER ASSETS

TOTAL ASSETS

BOOK VALUE AT END

OF CURRENT

REPORTING MONTH

$ -

-

-

-

-

-

37,460,453

37,460,453

$ 37,460,453

BOOK VALUE ON PETITION DATE

$ 598,000

124,000

540,000

1,262.000

51,326,000

8,626,000

8,626,000

$ 61,214,000

LIABILITIES AND OWNER EQUITY

LIABILITIES NOT SUBJECT TO COMPROMISE (Post-Petition).

Accounts Payable

Taxes Payable

Wages Payable

Rents / Leases - Building / Equipment

Professional Fees

Secured Debt! Adequate Protection Payments

Other Post-Petition Liabilities (see attached schedule)

TOTAL POST-PETITION LIABILITIES

LIABILITIES SUBJECT TO COMPROMISE (Pre-Petition)

Secured Debt / Adequate Protection Payments

Priority Debt

Unsecured Debt

TOTAL PRE-PETITION LIABILITIES

TOTAL LIABILITIES

OWNER EQUITY

Capital Stock

Retained Earnings - Pre-Petition

Retained Earnings - Post-Petition

Additional Paid-In Capital

NET OWNER EQUITY

TOTAL LIABILITIES AND OWNERS’ EQUITY

BOOK VALUE AT END

OF CURRENT

REPORTING MONTH

$

-

101,058

-

.

-

-

146,019

247,077

222,964

222,964

470,041

1,000

(19,514,380)

234,923

56,268,869

36,990,412

37,460,453

BOOK VALUE ON PETITION DATE

$ 131,000

954,000

3,127,000

-

-

499,000

4,711,000

246,000

246,000

4.957,000

1,000

(12,000)

-

56,268,000

56,257,000

$ 61,214,000

In re: Gobi Fulfillment Services, Inc. Debtor

Case No.: 09-12101

Reporting Period: Jan 3—Jan 30, 2010

MOR-3: BALANCE SHEET (Continuation Sheet)

ASSETS

OTHER CURRENT ASSETS

BOOK VALUE AT END

OF CURRENT

REPORTING MONTH

BOOK VALUE ON

PETITION DATE

OTHER ASSETS

Intercompany receivables from single affiliates

37,460,453

8,626,000

LIABILITIES AND OWNER EQUITY

OTHER POST PETITION LIABILITIES

Bank overdraft

Accrued expenses

BOOK VALUE AT END

Of CURRENT

REPORTING MONTH

$-

146,019

146,019

BOOK VALUE

PETITION DATE

$ 277,000

222,000

499.000

In re: Gobi Fulfillment Services, Inc. Debtor

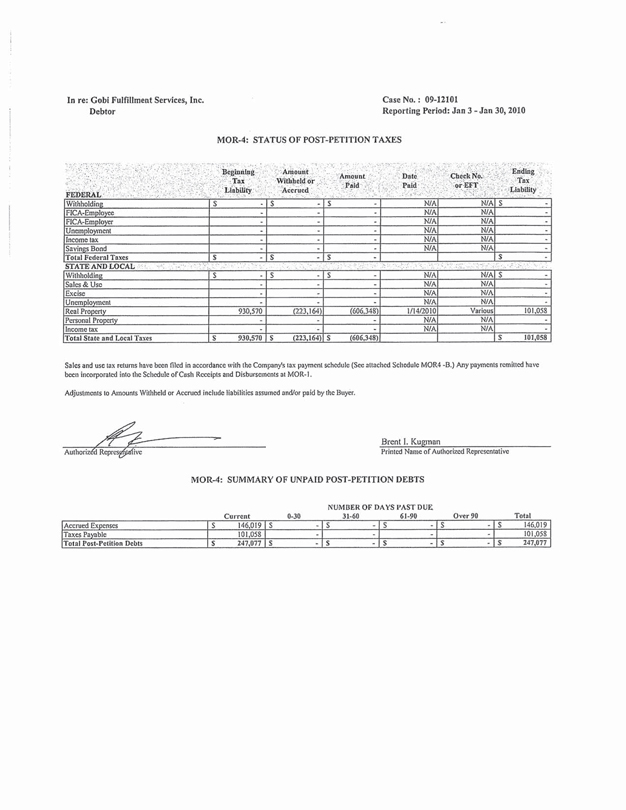

Case No. : 09-12101

Reporting Period: Jan 3—Jan 30, 2010

MOR-4: STATUS OF POST-PETITION TAXES

FEDERAL

Withholding

FICA-Employee

FICA-Employer

Unemployment

Income tax

Savings Bond

Total Federal Taxes

STATE AND LOCAL

Withholding

Sales & Use

Excise

Unemployment

Real Property

Personal Property

Income tax

Total State and Local Taxes

Beginning

Tax

Liability

$ -

-

-

-

-

$ -

$ -

-

-

-

930,570

-

-

$ 930,570

Amount

Withheld or Accrued

$ -

-

-

-

-

-

$

-

$

-

-

-

-

(223,164)

-

-

$

(223,164)

Amount Paid

$ -

-

-

-

-

-

$ -

$ -

-

-

-

(606,348)

-

-

$ (606,348)

Date Paid

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

1/14/2010

N/A

N/A

Check No.

or EFT

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

N/A

Various

N/A

N/A

Ending

Tax

Liability

$ -

-

-

-

-

$-

-

$-

-

-

-

101,058

-

-

$ 101,058

Sales and use tax returns have been filed in accordance with the Company’s tax payment schedule (See attached Schedule MOR4-B.) Any payments remitted have been incorporated into the Schedule of Cash Receipts and Disbursements at MOR-1.

Adjustments to Amounts Withheld or Accrued include liabilities assumed and/or paid by the Buyer.

Authorized Representative

Brent I. Kugman Printed Name of Authorized Representative

MOR-4: SUMMARY OF UNPAID POST-PETITION DEBTS

NUMBER OF

DAYS PAST DUE

Accrued Expenses

Taxes Payable

Total Post-Petition Debts

Current

$

146,019

101,058

$

247,077

0-30

$

-

-

$

-

31-60

$

-

-

$

-

61-90

$

-

-

$

-

Over 90

$

-

-

$

-

Total

146,019

$101,058

$247,077

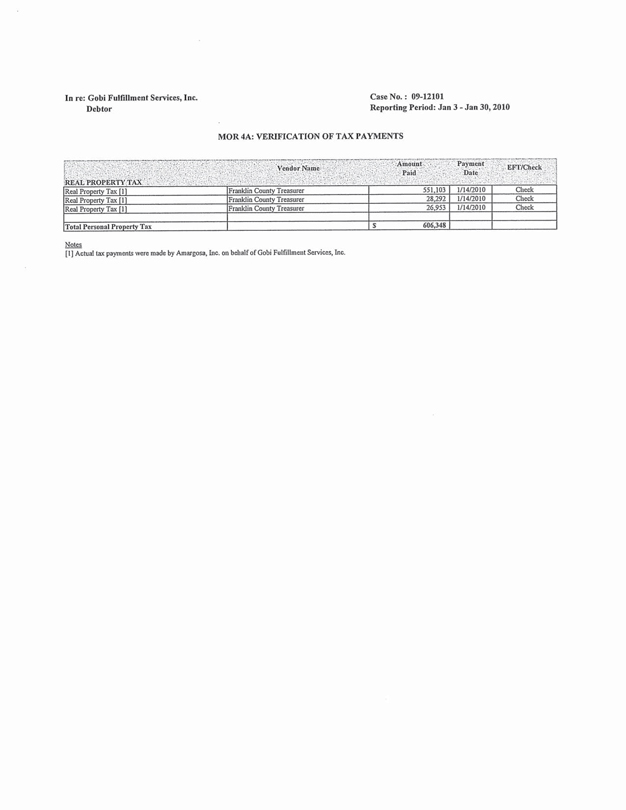

In re: Gobi Fulfillment Services, Inc.

Debtor

Case No.: 09-12101

Reporting Period: Jan 3 - Jan 30, 2010

MOR 4A: VERIFICATION OF TAX PAYMENTS

REAL PROPERTY TAX

Real Property Tax [1]

Total Personal Property Tax

Vendor Name

Franklin County Treasurer

Amount Paid

551,103 28,292 26,953 $ 606,348

Payment Dale 1/14/2010

EFT/Check

Check

Notes

[1] Actual tax payments were made by Amargosa, Inc. on behalf of Gobi Fulfillment Services, Inc.

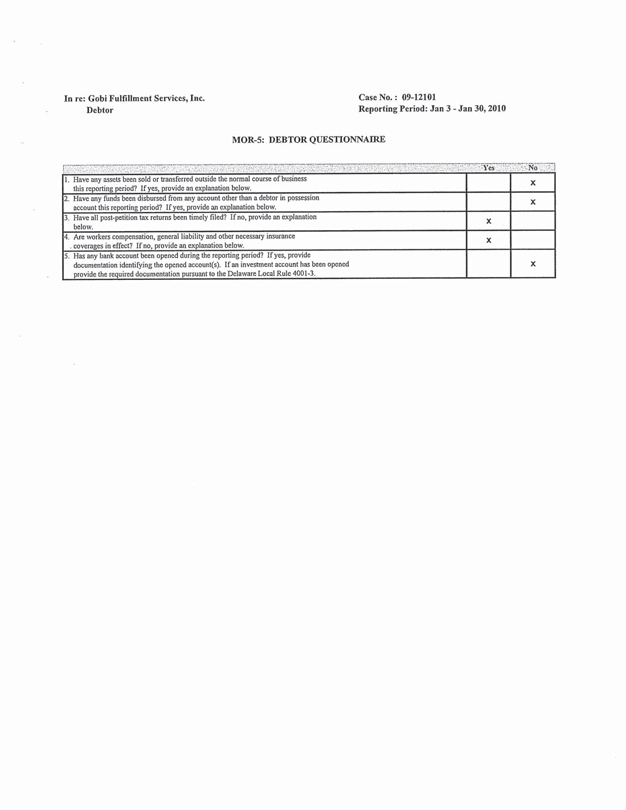

In re: Gobi Fulfillment Services, Inc.

Debtor

Case No.: 09-12101

Reporting Period: Jan 3 - Jan 30, 2010

MOR-5: DEBTOR QUESTIONNAIRE

1. Have any assets been sold or transferred outside the normal course of business this reporting period? If yes, provide an explanation below.

2. Have any funds been disbursed from any account other than a debtor in possession account this reporting period? If yes, provide an explanation below.

3. Have all post-petition tax returns been timely filed? If no, provide an explanation below.

4. Are workers compensation, general liability and other necessary insurance coverages in effect? If no, provide an explanation below.

5. Has any bank account been opened during the reporting period? If yes, provide documentation identifying the opened account(s). If an investment account has been opened provide the required documentation pursuant to the Delaware Local Rule 4001-3.

Yes No x x

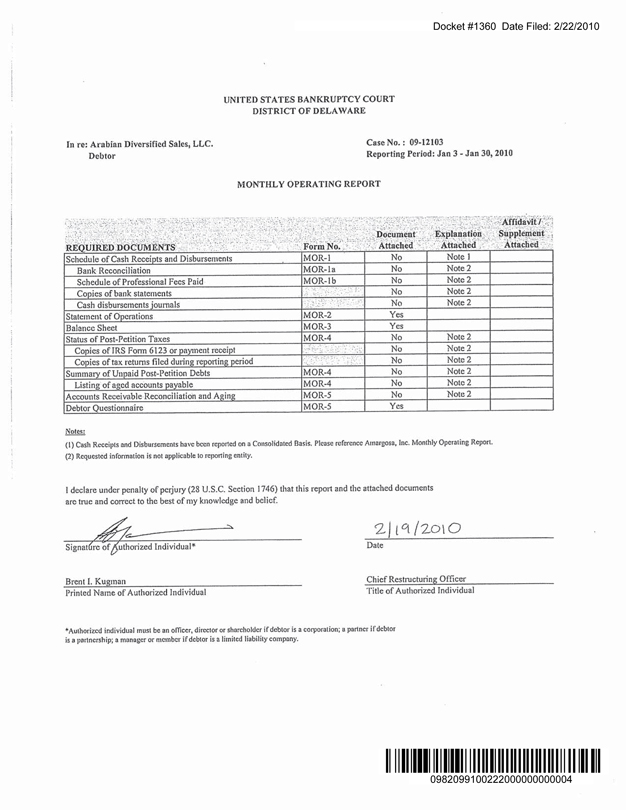

Docket #1360 Date Filed: 2/22/2010

UNITED STATES BANKRUPTCY COURT

DISTRICT OF DELAWARE

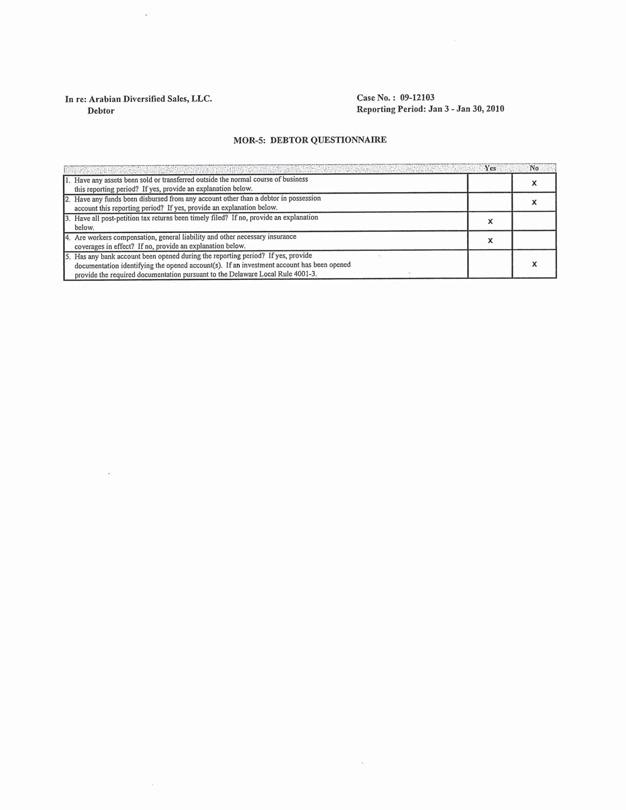

In re: Arabian Diversified Sales, LLC.

Debtor

Case No.: 09-12103

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Schedule of Cash Receipts and Disbursements

Bank Reconciliation

Schedule of Professional Fees Paid

Copies of bank statements

Cash disbursements journals

Statement of Operations

Balance Sheet

Status of Post-Petition Taxes

Copies of IRS Form 6123 or payment receipt

Copies of tax returns filed during reporting period

Summary of Unpaid Post-Petition Debts

Listing of aged accounts payable

Accounts Receivable Reconciliation and Aging

Debtor Questionnaire

Form No. MOR-l MOR-la MOR- lb MOR-2 MOR-3 MOR-4 MOR-5

Document Attached No Yes

Explanation Attached. Note 1 Note 2

Affidavit / I Supplement Attached

Notes:

(1) Cash Receipts and Disbursements have been reported on a Consolidated Basis. Please reference Amargosa, Inc. Monthly Operating Report.

(2) |

| Requested information is not applicable to reporting entity. |

I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief.

Signature of authorized Individual* Date

Brent I. Kugman Printed Name of Authorized Individual

Chief Restructuring Officer Title of Authorized Individual

* Authorized individual must be an officer, director or shareholder if debtor is a corporation; a partner it debtor is a partnership; a manager or member if debtor is a limited liability company.

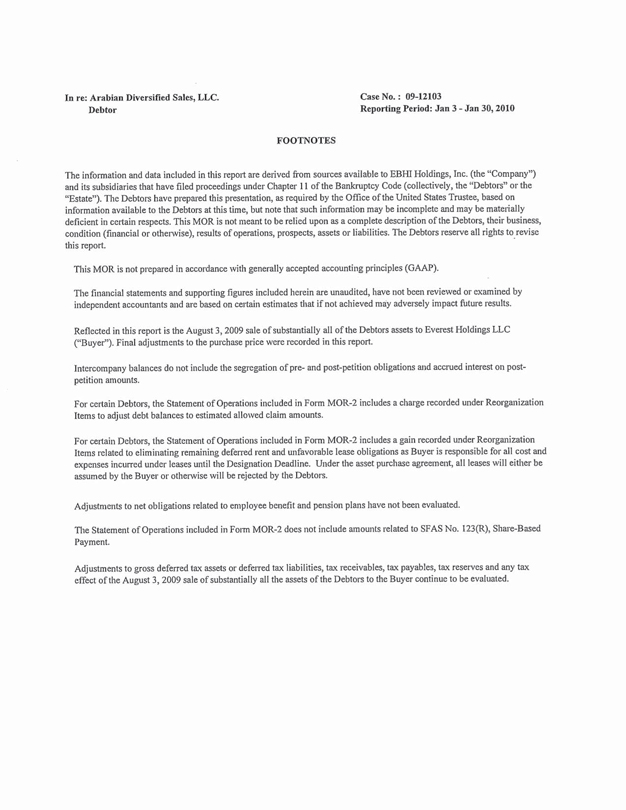

In re: Arabian Diversified Sales, LLC.

Debtor

Case No.: 09-12103

Reporting Period: Jan 3 - Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter 11 of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post-petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 123(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

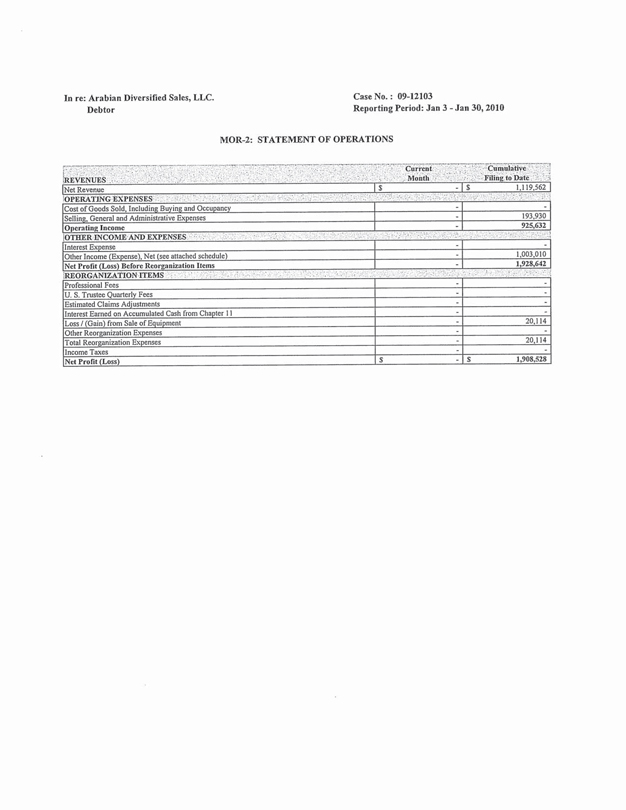

In re: Arabian Diversified Sales, LLC. Debtor

Case No.: 09-12103

Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

REVENUES

Current Month

Cumulative Filing to Date

Net Revenue $ - $ 1,119,562

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy -

Selling, General and Administrative Expenses - 193,930

Operating Income - 925,632

OTHER INCOME AND EXPENSES

Interest Expense -

Other Income (Expense) Net (see attached schedule) - 1,003,010

Net Profit (Loss) Before Reorganization Items - 1,928,642

REORGANIZATION ITEMS

Professional Fees -

U. S. Trustee Quarterly Fees - -

Estimated Claims Adjustments -

Interest Earned on Accumulated Cash from Chapter 11 -

Loss (Gain) from Sale of Equipment - 20,114

Other Reorganization Expenses

Total Reorganization Expenses - 20,114

Income Taxes -

Net Profit (Loss) $ - $ 1,908,528

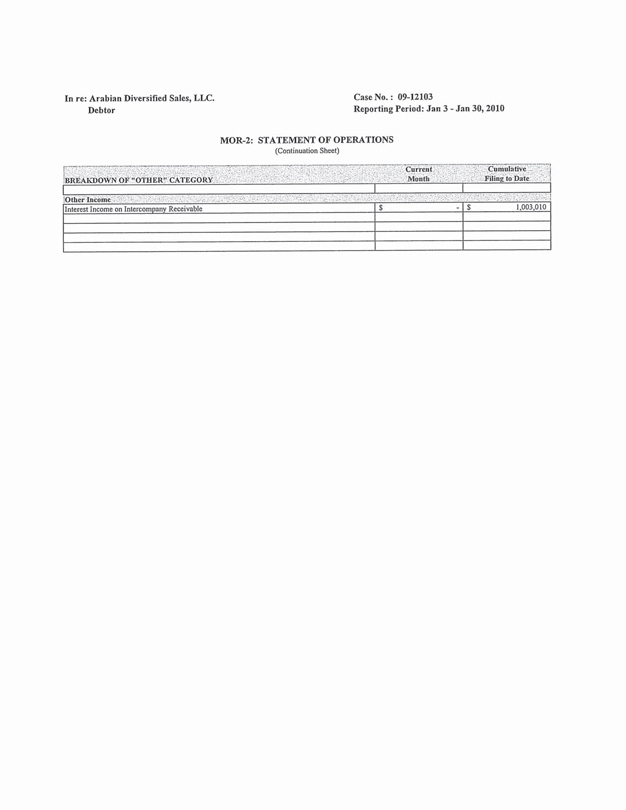

In re: Arabian Diversified Sales, LLC. Debtor

Case No.: 09-12103

Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS (Continuation Sheet)

BREAKDOWN OF “OTHER” CATEGORY

Current Month

Cumulative Filing to Date

Other Income

Interest income on Intercompany Receivable $ - $ 1,003,010

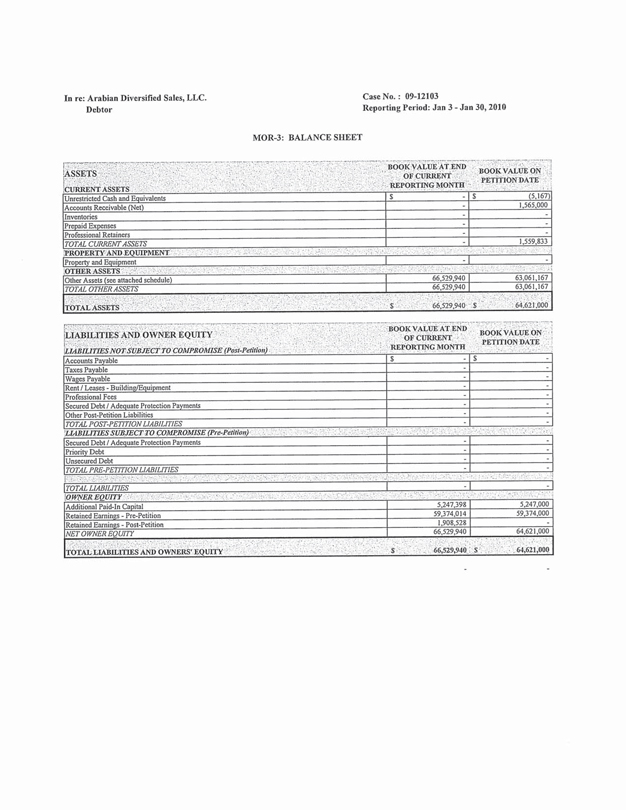

In re: Arabian Diversified Sales, LLC. Debtor

Case No.: 09-12103

Reporting Period: Jan 3 - Jan 30, 2010

MOR-3: BALANCE SHEET

ASSETS

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

CURRENT ASSETS

Unrestricted Cash and Equivalents $ - $ (5.167)

Accounts Receivable (Net) - 1,565.000

Inventories -

Prepaid Expenses -

Professional Retainers -

TOTAL CURRENT ASSETS - 1,559.833

PROPERTY AND EQUIPMENT

Property and Equipment -

OTHER ASSETS

Other Assets (see attached schedule) 66,529,940 63,061,167

TOTAL OTHER ASSETS 66,529,940 63,061,167

TOTAL ASSETS $ 66,529,940 $ 64,621,000

LIABILITIES AND OWNER EQUITY

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

LIABILITIES NOT SUBJECT TO COMPROMISE (Post-Petition)

Accounts Payable $ - $ -

Taxes Payable -

Wages Payable -

Rent / Leases - Building/Equipment -

Professional Fees -

Secured Debt / Adequate Protection Payments -

Other Post-Petition Liabilities -

TOTAL POST-PETITION LIABILITIES -

LIABILITIES SUBJECT TO COMPROMISE (Pre-Petition)

Secured Debt / Adequate Protection Payments -

Priority Debt -

Unsecured Debt -

TOTAL PRE-PETITION LIABILITIES -

TOTAL LIABILITIES

OWNER EQUITY

Additional Paid-in Capital 5,247,398 5,247,000

Retained Earnings - Pre-Petition 59,374,014 59,374,000

Retained Earnings - Post-Petition 1,908,528 -

NET OWNER EQUITY 66,529,940 64,621,000

TOTAL LIABILITIES AND OWNERS’ EQUITY $ 66,529,940 $64,621,000

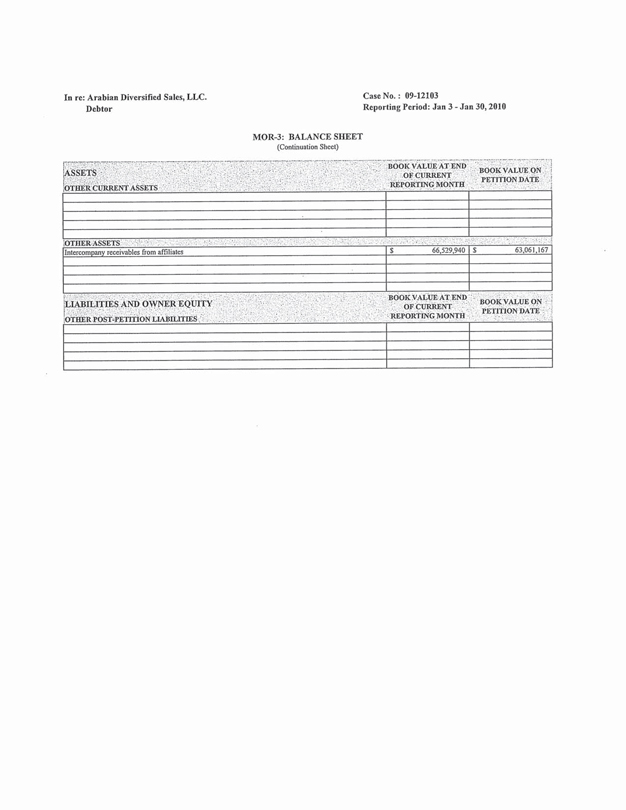

In re: Arabian Diversified Sales, LLC. Debtor

Case No.: 09-12103

Reporting Period: Jan 3 - Jan 30, 2010

MOR-3: BALANCE SHEET

(Continuation Sheet)

ASSETS

OTHER CURRENT ASSETS

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

OTHER ASSETS

Intercompany receivables from affiliates $ 66,529,940 $ 63,061,167

LIABILITIES AND OWNER EQUITY

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

OTHER POST-PETITION LIABILITIES

In re: Arabian Diversified Sales, LLC. Debtor

Case No.: 09-12103 Reporting Period: Jan 3 - Jan 30, 2010

MOR-5: DEBTOR QUESTIONNAIRE

Yes No

1. Have any assets been sold or transferred outside the normal course of business this reporting period? If yes, provide an explanation below.

2. Have any funds been disbursed from any account other than a debtor in possession account this reporting period? If yes, provide an explanation below.

3. Have all post-petition tax returns been timely filed? If no, provide an explanation below.

4. Are workers compensation, general liability and other necessary insurance coverages in effect? If no, provide an explanation below.

5. Has any bank account been opened during the reporting period? If yes, provide documentation identifying the opened account(s). If an investment account has been opened provide the required documentation pursuant to the Delaware Local Rule 4001-3.

X

Docket #1361 Date Filed: 2/22/2010

UNITED STATES BANKRUPTCY COURT

DISTRICT OF DELAWARE

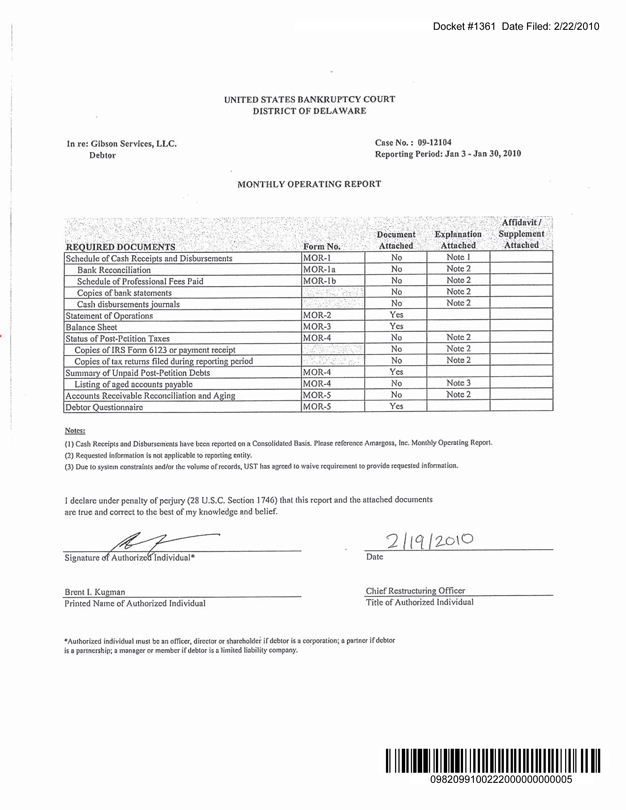

In re: Gibson Services, LLC. Debtor

Case No.: 09-12104

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Form No.

Document Attached

Explanation Attached

Affidavit / Supplement Attached

Schedule of Cash Receipts and Disbursements MOR-1 No Note 1

Bank Reconciliation MOR-la No Note 2

Schedule of Professional Fees Paid MOR-Ib No Note 2

Copies of bank statements No Note 2

Cash disbursements journals No Note 2

Statement of Operations MOR-2 Yes

Balance Sheet MOR-3 Yes

Status of Post-Petition Taxes MOR-4 No Note 2

Copies of IRS Form 6123 or payment receipt No Note 2

Copies of tax returns filed during reporting period No Note 2

Summary of Unpaid Post-Petition Debts MOR-4 Yes

Listing of aged accounts payable MOR-4 No Note 3

Accounts Receivable Reconciliation and Aging MOR-5 No Note 2

Debtor Questionnaire MOR-5 Yes

Notes:

(1) Cash Receipts and Disbursements have been reported on a Consolidated Basis. Please reference Amargosa, Inc. Monthly operating Report.

(2) Requested information is not applicable to reporting entity.

(3) Due to system constraints and/or the volume of records, UST has agreed to waive requirement to provide requested information.

I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief.

Signature of Authorized Individual*

Date Brent I. Kugman

Printed Name of Authorized Individual

Chief Restructuring Officer Title of Authorized Individual

* Authorized individual must be an officer, director or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company.

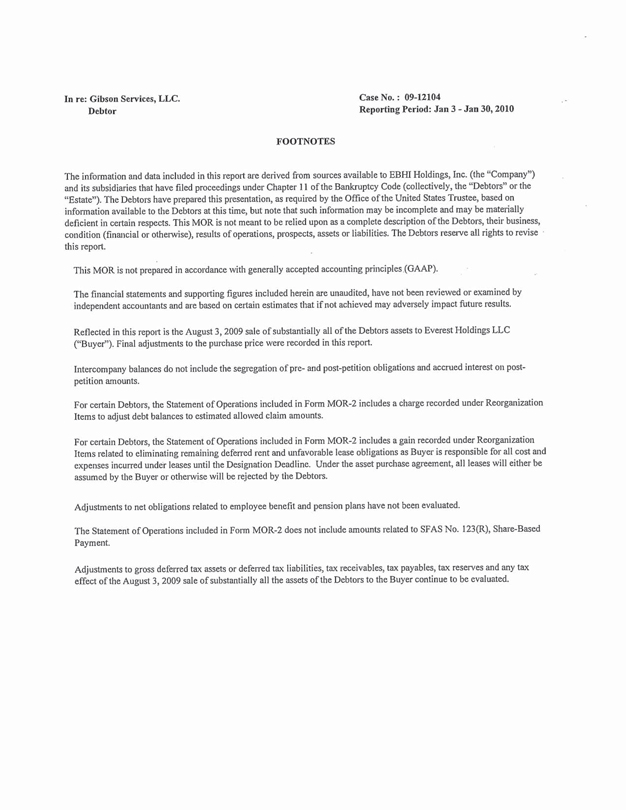

In re: Gibson Services, LLC. Case No.: 09-12104

Debtor Reporting Period: Jan 3 - Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter 11 of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post-petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 123(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

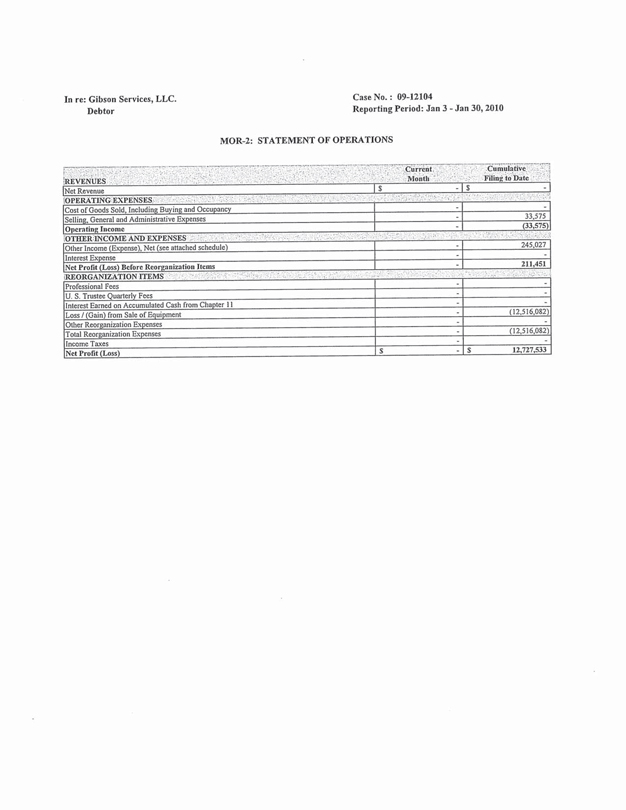

In re: Gibson Services, LLC. Case No.: 09-12104

Debtor Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

Current Month

Cumulative Filing to Date

REVENUES

Net Revenue $ - $ -

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy -

Selling, General and Administrative Expenses - 33,575

Operating Income - (33,575)

OTHER INCOME AND EXPENSES

Other Income (Expense), Net (see attached schedule) - 245,027

Interest Expense -

Net Profit (Loss) Before Reorganization Items - 211,451

REORGANIZATION ITEMS

Professional Fees -

U. S. Trustee Quarterly Fees - -

Interest Earned on Accumulated Cash from Chapter 11 -

Loss \ (Gain) from Sale of Equipment - (12,516,082)

Other Reorganization Expenses -

Total Reorganization Expenses - (12,516,082)

Income Taxes -

Net Profit (Loss) $ - $ 12,727,533

In re: Gibson Services, LLC. Debtor

Case No.: 09-12104

Reporting Period: Jan 3 - Jan 30, 2010

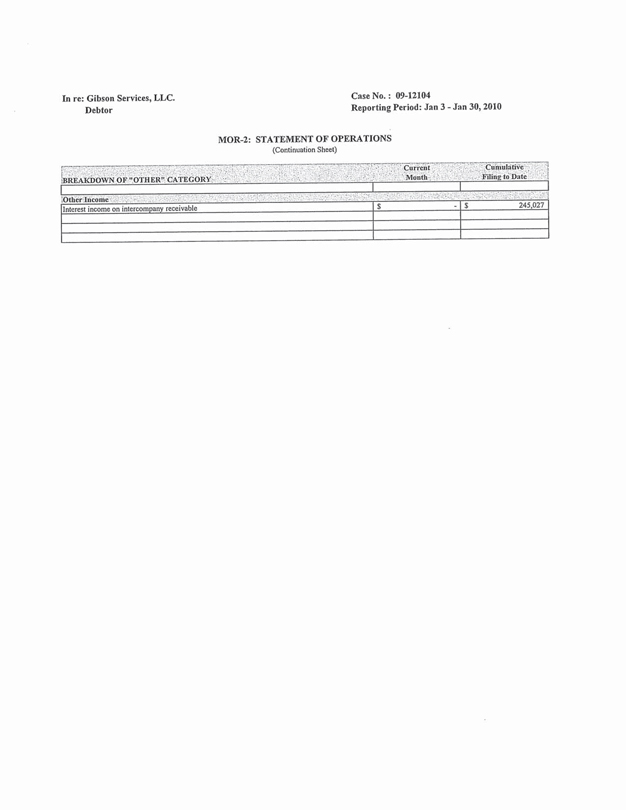

MOR-2: STATEMENT OF OPERATIONS (Continuation Sheet)

BREAKDOWN OF “OTHER” CATEGORY

Current Month

Cumulative Filing to Date

Other Income

Interest income on Intercompany receivable $ - $ 245,027

In re: Gibson Services, LLC. Debtor

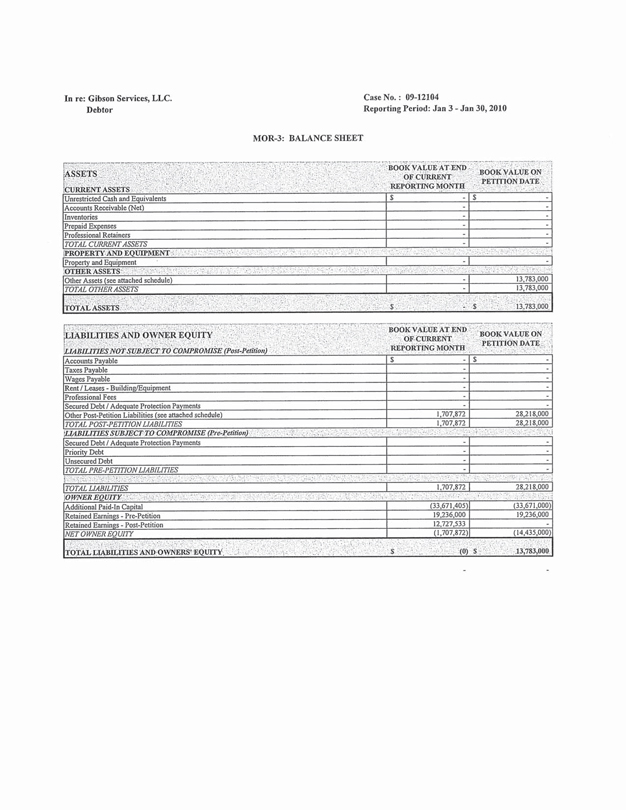

MOR-3: BALANCE SHEET

Case No. : 09-12104

Reporting Period: Jan 3 - Jan 30, 2010

ASSETS

CURRENT ASSETS

BOOK VALUE ON OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

Unrestricted Cash and Equivalents $ - $ -

Accounts Receivable (Net) -

Inventories -

Prepaid Expenses -

Professional Retainers -

TOTAL CURRENT ASSETS -

PROPERTY AND EQUIPMENT

Property and Equipment -

OTHER ASSETS

Other Assets (see attached schedule) - - 13,783,000

TOTAL OTHER ASSETS - 13,783,000

TOTAL ASSETS $- $ 13,783,000

LIABILITIES AND OWNER EQUITY

BOOK VALUE ON OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

LIABILITIES NOT SUBJECT TO COMPROMISE (Post-Petition)

Accounts Payable $ - $ -

Taxes Payable -

Wages Payable -

Rent / Leases - Building/Equipment -

Professional Fees -

Secured Debt / Adequate Protection Payments -

Other Post-Petition Liabilities (see attached schedule) 1,707,872 28,218,000

TOTAL POST-PETITION LIABILITIES 1,707,872 28,218,000

LIABILITIES SUBJECT TO COMPROMISE (Pre-Petition)

Secured Debt / Adequate Protection Payments -

Priority Debt -

Unsecured Debt

TOTAL PRE-PETITION LIABILITIES

TOTAL LIABILITIES 1,707,872 28,218,000

OWNER EQUITY

Additional Paid-In Capital (33,671,405) (33,671,000)

Retained Earnings - Pre-Petition 19,236,000 19,236,000

Retained Earnings - Post-Petition 12,727,533

NET OWNER EQUITY (1,707,872) (14,435,000)

TOTAL LIABILITIES AND OWNERS’ EQUITY $ (0) $ 13,783,000

In re: Gibson Services, LLC. Debtor

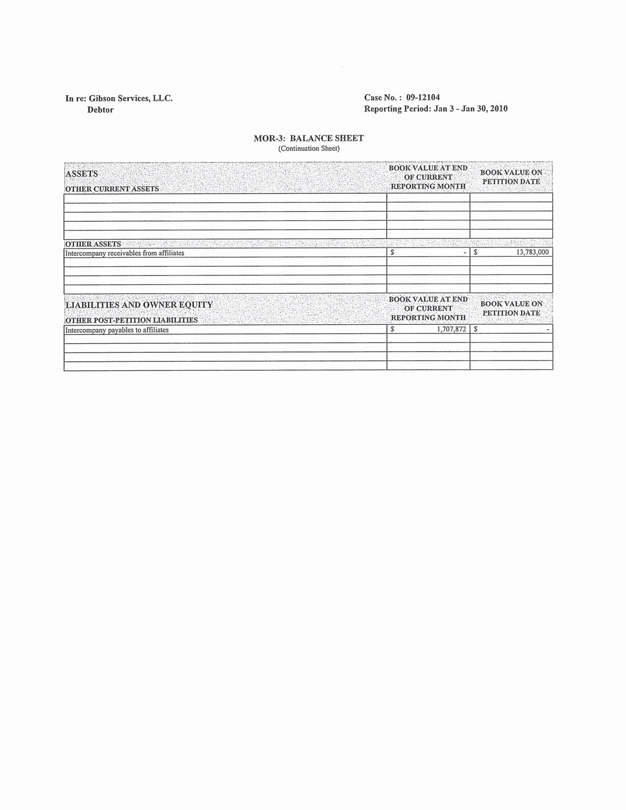

MOR-3: BALANCE SHEET (Continuation Sheet)

Case No.: 09-12104 Reporting Period: Jan 3 - Jan 30, 2010

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

ASSETS

OTHER CURRENT ASSETS

OTHER ASSETS

Intercompany receivables from affiliates $ 13,783,000

LIABILITIES AND OWNER EQUITY

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

OTHER POST-PETITION LIABILITIES

Intercompany payables to affiliates $1,707,872 $ -

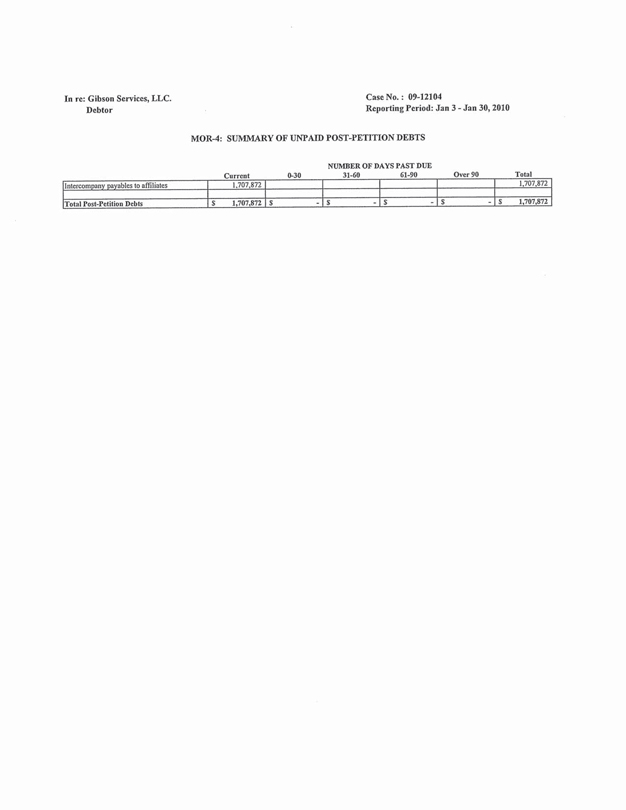

Case No.: 09-12104 Reporting Period: Jan 3 - Jan 30, 2010

MOR-4: SUMMARY OF UNPAID POST-PETITION DEBTS

NUMBER OF DAYS PAST DUE

0-30 31-60 61-90 Over 90

In re: Gibson Services, LLC. Debtor

Current

Total

Intercompany payables to affiliates 1,707,872 1,707,872

Total Post-Petition Debts $1,707,872 $—$—$—$ 1,707,872

In re: Gibson Services, LLC.

Debtor

MOR-5: DEBTOR QUESTIONNAIRE

Case No.: 09-12104

Reporting Period: Jan 3 - Jan 30, 2010

1. Have any assets been sold or transferred outside the normal course of business this reporting period? If yes, provide an explanation below.

2. Have any funds been disbursed from any account other than a debtor in possession account this reporting period? If yes, provide an explanation below.

3. Have all post-petition tax returns been timely filed? If no, provide an explanation below.

4. Are workers compensation, general liability and other necessary insurance coverages in effect? If no, provide an explanation below.

5. Has any bank account been opened during the reporting period? If yes, provide documentation identifying the opened account(s). If an investment account has been opened provide the required documentation pursuant to the Delaware Local Rule 4001-3.

X X X X X

Yes No

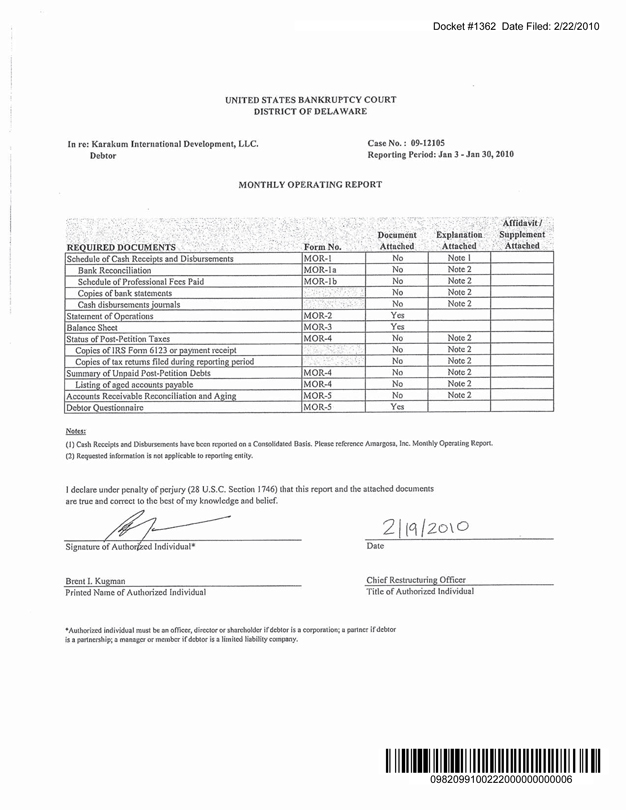

Docket #1362 Date Filed: 2/22/2010

UNITED STATES BANKRUPTCY COURT

DISTRICT OF DELAWARE

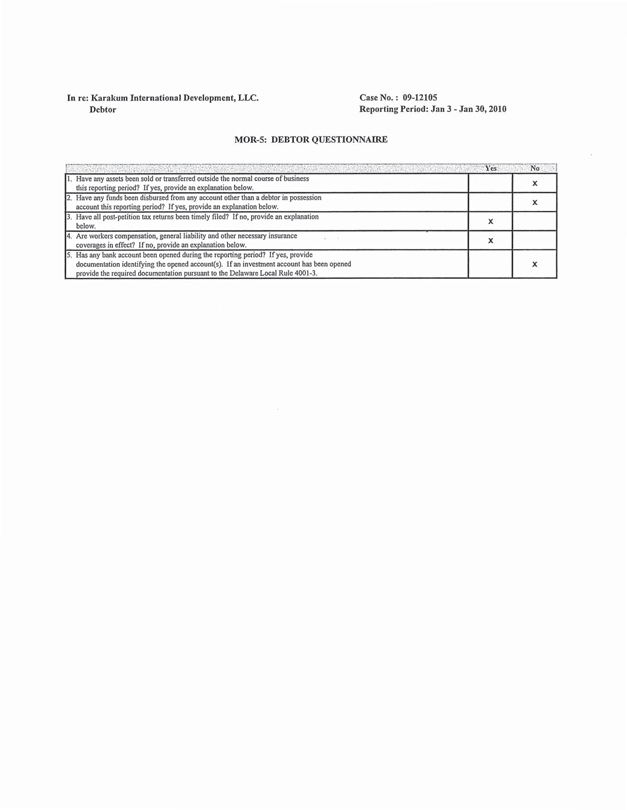

In re: Karakum International Development, LLC. Debtor

Case No.: 09-12105

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Form No.

Document Attached

Explanation Attached

Affidavit / Supplement Attached

Schedule of Cash Receipts and Disbursements

MOR-l

No Note 1 Bank Reconciliation MOR-la No Note 2 Schedule of Professional Fees Paid MOR-1b No Note 2 Copies of bank statements Cash disbursements journals Statement of Operations

MOR-2 Yes Balance Sheet MOR-3 Status of Post-Petition Taxes

MOR-4 Copies of IRS Form 6123 or payment receipt Copies of tax returns filed during reporting period

Summary of Unpaid Post-Petition Debts

MOR-4 Listing of aged accounts payable MOR-4 Accounts Receivable Reconciliation and Aging MOR-5 Debtor Questionnaire MOR-5 Yes Notes: (1) Cash Receipts and Disbursements have been reported on a Consolidated Basis. Please reference, Inc. Monthly Operating Report. (2) Requested information is not applicable to reporting entity. I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief.

Brent I. Kugman

Printed Name of Authorized Individual

Chief Restructuring Officer Title of Authorized Individual

Authorized individual must be on officer, director or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company.

0982099100222000000000006

Signature of Authorized Individual*

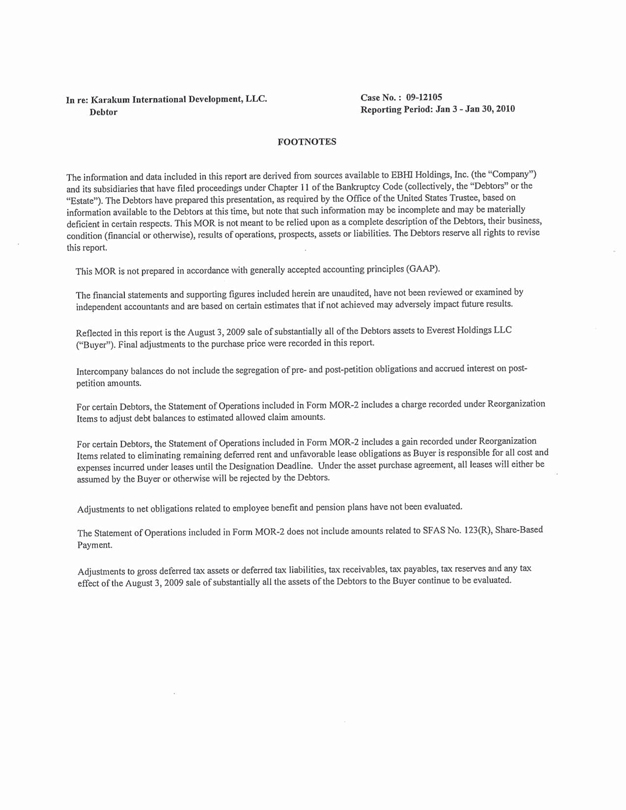

In re: Karakum International Development, LLC. Case No.: 09-12105

Debtor Reporting Period: Jan 3 - Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter 11 of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post-petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 1 23(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

In re: Karakum International Development, LLC. Case No. : 09-12105

Debtor Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

REVENUES

Current Month

Cumulative Filing to Date

Net Revenue $- $ 919,101

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy

Selling, General and Administrative Expenses - 47,599

Operating Income - 871,501

OTHER INCOME AND EXPENSES

Other Income (Expense) Net (see attached schedule) - 710,688

Interest Expense

Net Profit (Loss) Before Reorganization Items - 1,582,190

REORGANIZATION ITEMS

Professional Fees - -

U.S. Trustee Quarterly Fees - - -

Interest Earned on Accumulated Cash from Chapter 11

Loss / (Gain) from Sale of Equipment - -

Other Reorganization Expenses - -

Total Reorganization Expenses - -

Income Taxes -

Net Profit (Loss) $- $ 1,582,190

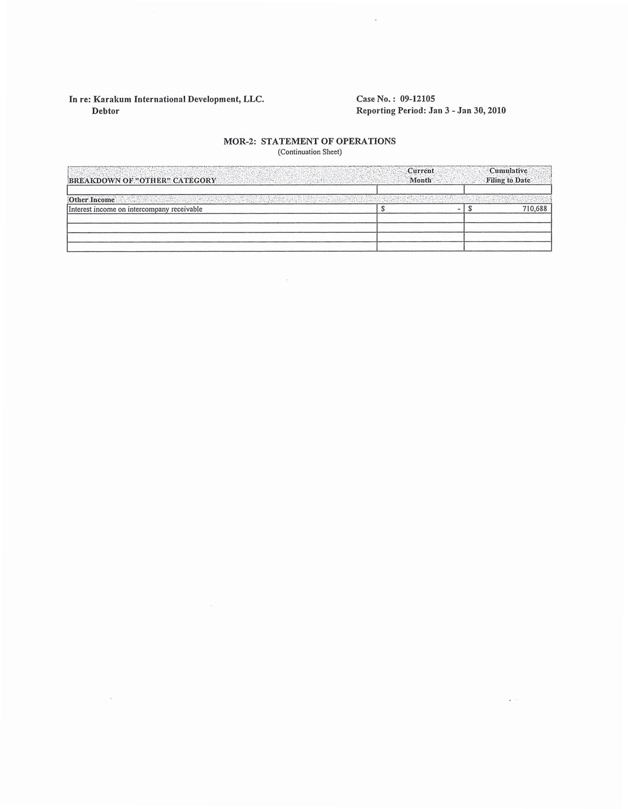

In re: Karakum International Development, LLC. Debtor

Case No. : 09-12105

Reporting Period: Jan 3 - Jan 30, 2010

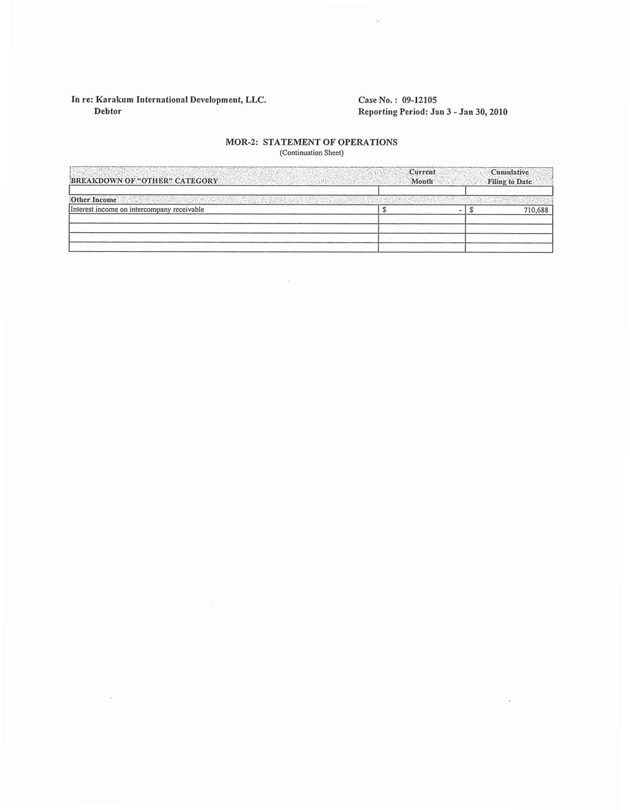

MOR-2: STATEMENT OF OPERATIONS

(Continuation Sheet)

BREAKDOWN OF “OTHER” CATEGORY

Current Month

Cumulative Filing to Date

Other Income

Interest income on Intercompany receivable $- $ 710,688

In re: Karakum International Development, LLC.

Debtor

Case No.: 09-12105

Reporting Period: Jan 3 - Jan 30, 2010

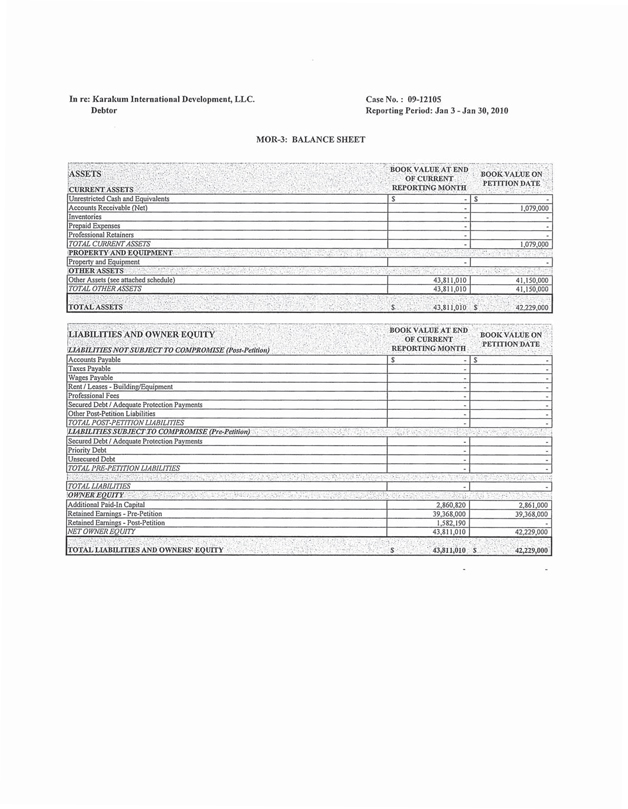

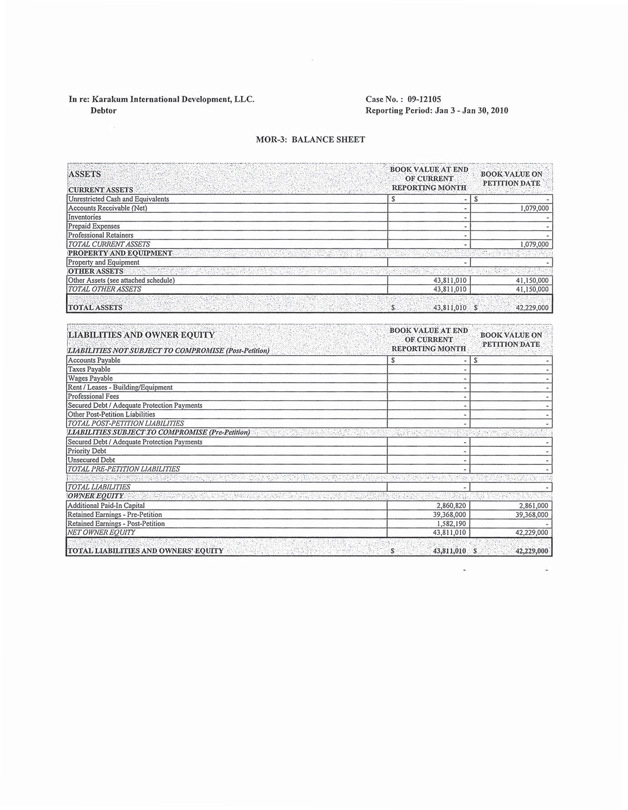

MOR-3: BALANCE SHEET

ASSETS

CURRENT ASSETS

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

Unrestricted Cash and Equivalents $ - $ -

Accounts Receivable (Net) - 1,079,000

Inventories

Prepaid Expenses

Professional Retainers

TOTAL CURRENT ASSETS - 1,079,000

PROPERTY AND EQUIPMENT

Property and Equipment -

OTHER ASSETS

Other Assets (see attached schedule) 43,811,010 41,150,000

TOTAL OTHER ASSETS $ 43,811,010 $ 41,150,000

LIABILITIES AND OWNER EQUITY

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

LIABILITIES NOT SUBJECT TO COMPROMISE (Post -Petition)

Accounts Payable $ - $ -

Taxes Payable -

Wages Payable -

Rent / Leases – Building/Equipment -

Professional Fee -

Secured Debt / Adequate Protection Payments

Other Post-Petition Liabilities

TOTAL POST-PETITION LIABILITIES

LIABILITIES SUBJECT TO COMPROMISE (Pre-Petition)

Secured Debt / Adequate Protection Payments

Priority Debt

Unsecured Debt

TOTAL PRE-PETITION LIABILITIES

TOTAL LIABILITIES - -

OWNER EQUITY

Additional Paid-In Capital 2,860,820 2,861,000

Retained Earnings - Pre-Petition 39,368,000 39,368,000

Retained Earnings - Post-Petition 1,582,190 -

NET OWNER EQUITY 43,811,010 42,229,000

TOTAL LIABILITIES AND OWNERS’ EQUITY $ 43,811,010 $ 42,229,000

In re: Karakum International Development, LLC. Debtor

Case No.: 09-12105

Reporting Period: Jan 3-Jan 30, 2010

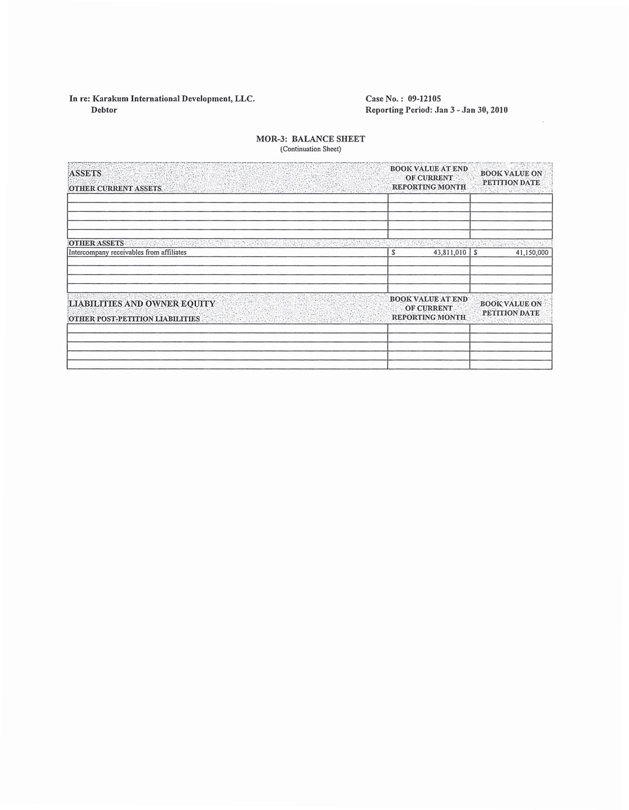

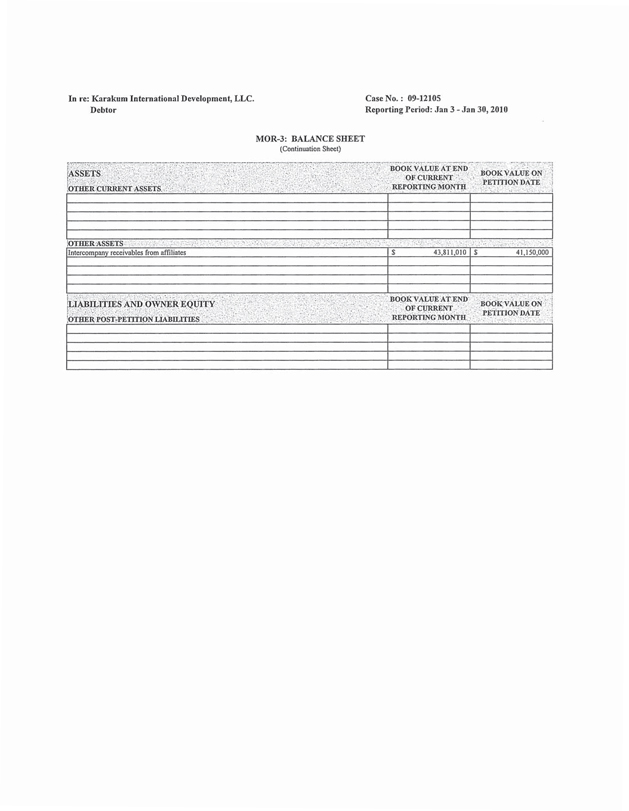

MOR-3: BALANCE SHEET

(Continuation Sheet)

ASSETS

OTHER CURRENT ASSETS

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

OTHER ASSETS $43,811,010 $41,150,000

(INTER COMPANY RECEIVED))

LIABILITIES AND OWNER EQUITY

BOOK VALUE AT END OF CURRENT REPORTING MONTH

BOOK VALUE ON PETITION DATE

OTHER POST-PETITION LIABILITIES

In re: Karakum International Development, LLC. Debtor

Case No.: 09-12105

Reporting Period: Jan 3 - Jan 30, 2010

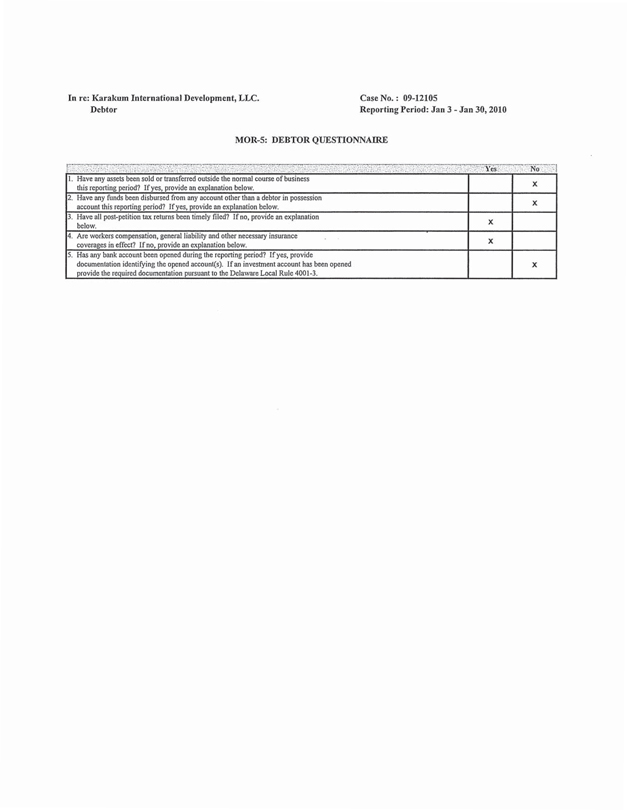

MOR-5: DEBTOR QUESTIONNAIRE

Yes No

1. Have any assets been sold or transferred outside the normal course of business this reporting period? If yes, provide an explanation below.

2. Have any funds been disbursed from any account other than a debtor in possession account this reporting period? If yes, provide an explanation below.

3, Have all post-petition tax returns been timely filed? If no, provide an explanation below.

4. Are workers compensation, general liability and other necessary insurance coverages in effect? If no, provide an explanation below.

5. Has any bank account been opened during the reporting period? If yes, provide documentation identifying the opened account(s). If an investment account has been opened provide the required documentation pursuant to the Delaware Local Rule 4001-3.

X X X X X

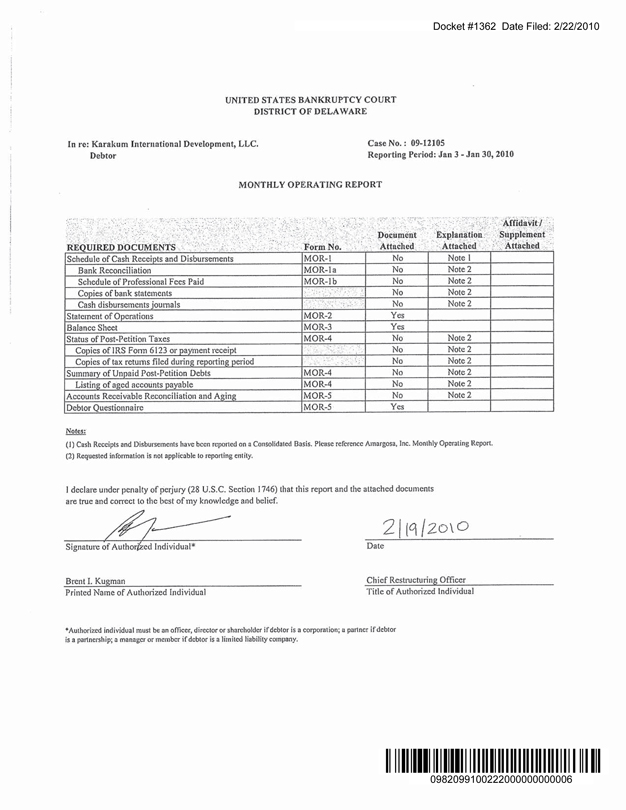

Docket #1362 Date Filed: 2/22/2010

UNITED STATES BANKRUPTCY COURT

DISTRICT OF DELAWARE

In re: Karakum International Development, LLC. Debtor

Case No. : 09-12105

Reporting Period: Jan 3 - Jan 30, 2010

MONTHLY OPERATING REPORT

REQUIRED DOCUMENTS

Form No.

Document Attached

Explanation Attached

Affidavit / Supplement Attached

Schedule of Cash Receipts and Disbursements

MOR-l No Note 1 Bank Reconciliation MOR-la No

Note 2 Schedule of Professional Fees Paid MOR-1b No

Note 2 Copies of bank statements No

Note 2 Cash disbursements journals No

Note 2 Statement of Operations MOR-2 Yes

Balance Sheet MOR-3 Yes

Status of Post-Petition Taxes MOR-4 No Note 2 Copies of IRS Form 6123 or payment receipt No Note 2 Copies of tax returns filed during reporting period No

Note 2 Summary of Unpaid Post-Petition Debts MOR-4 No Note 2 Listing of aged accounts payable MOR-4 No

Note 2 Accounts Receivable Reconciliation and Aging MOR-5 No

Note 2 Debtor Questionnaire MOR-5 Yes

Notes:

(1) Cash Receipts and Disbursements have been reported on a Consolidated Basis. Please reference Amargosa, Inc. Monthly Operating Report.

(2) |

| Requested information is not applicable to reporting entity. |

I declare under penalty of perjury (28 U.S.C. Section 1746) that this report and the attached documents are true and correct to the best of my knowledge and belief.

2/19/2010

Brent I. Kugman Printed Name of Authorized Individual Signature of Authorized Individual* Chief Restructuring Officer Title of Authorized Individual

*Authorized individual must be an officer, director or shareholder if debtor is a corporation; a partner if debtor is a partnership; a manager or member if debtor is a limited liability company.

0982099100222000000000006

In re: Karakum International Development, LLC. Case No.: 09-12105

Debtor Reporting Period: Jan 3 - Jan 30, 2010

FOOTNOTES

The information and data included in this report are derived from sources available to EBHI Holdings, Inc. (the “Company”) and its subsidiaries that have filed proceedings under Chapter II of the Bankruptcy Code (collectively, the “Debtors” or the “Estate”). The Debtors have prepared this presentation, as required by the Office of the United States Trustee, based on information available to the Debtors at this time, but note that such information may be incomplete and may be materially deficient in certain respects. This MOR is not meant to be relied upon as a complete description of the Debtors, their business, condition (financial or otherwise), results of operations, prospects, assets or liabilities. The Debtors reserve all rights to revise this report.

This MOR is not prepared in accordance with generally accepted accounting principles (GAAP).

The financial statements and supporting figures included herein are unaudited, have not been reviewed or examined by independent accountants and are based on certain estimates that if not achieved may adversely impact future results.

Reflected in this report is the August 3, 2009 sale of substantially all of the Debtors assets to Everest Holdings LLC (“Buyer”). Final adjustments to the purchase price were recorded in this report.

Intercompany balances do not include the segregation of pre- and post-petition obligations and accrued interest on post- petition amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a charge recorded under Reorganization Items to adjust debt balances to estimated allowed claim amounts.

For certain Debtors, the Statement of Operations included in Form MOR-2 includes a gain recorded under Reorganization Items related to eliminating remaining deferred rent and unfavorable lease obligations as Buyer is responsible for all cost and expenses incurred under leases until the Designation Deadline. Under the asset purchase agreement, all leases will either be assumed by the Buyer or otherwise will be rejected by the Debtors.

Adjustments to net obligations related to employee benefit and pension plans have not been evaluated.

The Statement of Operations included in Form MOR-2 does not include amounts related to SFAS No. 123(R), Share-Based Payment.

Adjustments to gross deferred tax assets or deferred tax liabilities, tax receivables, tax payables, tax reserves and any tax effect of the August 3, 2009 sale of substantially all the assets of the Debtors to the Buyer continue to be evaluated.

In re: Karakum International Development, LLC. Case No. : 09-12105

Debtor Reporting Period: Jan 3 - Jan 30, 2010

MOR-2: STATEMENT OF OPERATIONS

REVENUES

Current Month

Cumulative Filing to Date

Net Revenue $ - $ 919,101

OPERATING EXPENSES

Cost of Goods Sold, Including Buying and Occupancy - -

Selling, General and Administrative Expenses - 47,599

Operating Income - 871,501

OTHER INCOME AND EXPENSES

Other Income (Expense), Net (see attached schedule) - 710,688

Interest Expense - -

Net Profit (Loss) Before Reorganization Items - 1,582,190

REORGANIZATION ITEMS

Professional Fees -

U. S. Trustee Quarterly Fees - -

Interest Earned on Accumulated Cash from Chapter II

Loss / (Gain) from Sale of Equipment -

Other Reorganization Expenses -