UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, DC 20549

FORM 10-K/A

x | Annual report pursuant to section 13 or 15(d) of the Securities Exchange Act of 1934 |

For the fiscal year ended December 31, 2007

or

¨ | Transition report pursuant to section 13 or 15(d) of the Securities Exchange act of 1934 |

For the transition period from to

Commission File No. 0-51669

STERLING MINING COMPANY

Idaho |

| 82-0300575 |

(State or other jurisdiction of incorporation or organization) |

| (IRS Employer Identification No.) |

609 Bank Street, Wallace, ID 83873

(Address of principal executive offices and Zip Code)

(208) 556-0227

(Registrant’s telephone number, including area code)

Securities registered under Section 12(b) of the Act: None

Securities registered under Section 12(g) of the Act: Common Stock, Par Value $0.05

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ¨ No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ¨ No ý

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ý No ¨

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to the this Form 10-K. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a small reporting company.

Large Accelerated Filer ¨ Accelerated Filer ý Non-Accelerated Filer ¨

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ¨ No ý

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $108.3 million.

The number of shares outstanding of the registrant’s class of $0.05 par value common stock as of March 25, 2008 was 38,698,828

DOCUMENTS INCORPORATED BY REFERENCE: None

Explanatory Note - due to a clerical error the Report of Independent Registered Public Accounting Firm on the Consolidated Financial Statement of Sterling Mining Company that was supposed to be presented on page F-2 was mistakenly replaced by the Report of Independent Registered Public Accounting Firm on Internal Control over Financial Reporting. This amendment is filed to present the correct Report on page F-2 of our Consolidated Financial Statements.

TABLE OF CONTENTS

|

|

|

|

|

ITEM NUMBER AND CAPTION |

| Page | ||

|

| |||

1. |

|

| 4 | |

1A. |

|

| 6 | |

1B. |

|

| 11 | |

2. |

|

| 11 | |

3. |

|

| 35 | |

4. |

|

| 35 | |

|

| |||

|

| |||

5. |

|

| 36 | |

6. |

|

| 36 | |

7. |

| Management’s Discussion and Analysis of Financial Condition and Results of Operations |

| 37 |

7A. |

|

| 43 | |

8. |

|

| 43 | |

9. |

| Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

| 43 |

9A. |

|

| 43 | |

9B. |

|

| 47 | |

|

| |||

|

| |||

10. |

|

| 48 | |

11. |

|

| 49 | |

12. |

| Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters |

| 56 |

13. |

|

| 56 | |

14. |

|

| 57 | |

|

| |||

|

| |||

15. |

|

| 58 | |

CAUTIONARY STATEMENT ON FORWARD-LOOKING STATEMENTS

This annual report on Form 10-K may contain certain “forward-looking” statements as such term is defined by the Securities and Exchange Commission in its rules, regulations and releases, which represent the Company’s expectations or beliefs, including but not limited to, statements concerning the Company’s operations, economic performance, financial condition, growth and acquisition strategies, investments, and future operational plans. For this purpose, any statements contained herein that are not statements of historical fact may be deemed to be forward-looking statements. Without limiting the generality of the foregoing, words such as “may,” “will,” “expect,” “believe,” “anticipate,” “intent,” “could,” “estimate,” “might,” “plan,” “predict” or “continue” or the negative or other variations thereof o r comparable terminology are intended to identify forward-looking statements. This information may involve known and unknown risks, uncertainties and other factors which may cause our actual results, performance or achievements to be materially different from the future results, performance or achievements expressed or implied by any forward-looking statements.

This annual report contains forward-looking statements, many assuming that the Company secures adequate financing and is able to continue as a going concern, including statements regarding, among other things, (a) our plans for bringing the Sunshine Mine in Idaho back into silver production, (b) our plans for developing and producing from our properties in Mexico, (c) our plans for exploring out other mineral properties, (d) our growth strategies, (e) anticipated trends in our industry, (f) our future financing plans, (g) our anticipated need for working capital, (h) the impact of environmental laws, (i) the availability of labor and equipment, and (j) title to and rights to exploit our mineral properties. These statements may be found under Item 1. “Business,” “Item 2. Properties” and “Item 7. Management’s Discussion and Analysis of Financial Condition an d Results of Operations,” as well as in this annual report generally. Actual events or results may differ materially from those discussed in forward-looking statements as a result of various factors, including, without limitation, the risks discussed under “Item 1A. Risk Factors” and matters described in this annual report generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this annual report will in fact occur.

Given these risks and uncertainties, readers are cautioned not to place undue reliance on our forward-looking statements.

4

PART I

ITEM 1. | BUSINESS |

General

Sterling Mining Company (“Sterling,” “we,” or the “Company”) is engaged in the business of acquiring, exploring, and developing mineral properties, primarily those containing silver and associated base and precious metals. The Company was incorporated under the laws of the State of Idaho on February 21, 1903.The Company is headquartered at 609 Bank Street, Wallace, ID 83873. The Company’s executive offices are located at 2201 Government Way, Suite E, Coeur d’Alene, Idaho 83814. The Company maintains additional offices in Kellogg, Idaho, and in Zacatecas, Mexico, to support our operations.

The Company was founded in 1903 by John Presley. The Company initially staked the East-West Link claims which are still held by the Company. In the first 30 years, early exploration included the driving of six tunnels onto the property. In 1951, Day Mines and later associated entities leased the key Sterling property for exploration purposes. In 1996, Coeur d’Alene Mines Corporation (through a subsidiary) leased the original Sterling East-West link claims. In 1998, the Company embarked on an expansion program in the Silver Valley to add silver exploration prospects. Beginning with 340 acres of mining claims, this expansion program reached a total of over 23,100 acres under control by ownership, lease or option by 2007.

Sterling is generally not affected by seasonality. The only seasonal affect on the Sunshine Mine could be a delay of supplies in the winter due to extreme snowfall preventing delivery of mine supplies.

Business Plan and Plan of Operations

The Company operates in two geographical locations or segments. The first is the Company’s exploration and development of mineral properties in the Northwestern part of the United States, where the Company’s principal focus is on rehabilitating and bringing back into production the Sunshine Mine in Idaho. The other geographical segment is in Mexico, where the Company has, since 2005, been producing at its Barones facility and exploration on its other prospects and projects in and around the State of Zacatecas, Mexico. Certain financial information pertaining to the Company’s geographical segments for the fiscal years ended December 31, 2007, 2006, and 2005, is presented in Note 11 of the Notes to Consolidated Financial Statements of the Company in this report.

The Company’s corporate business plan is to (i) expand its silver assets and production; (ii) explore and develop the Sunshine Mine with an objective of return to full and sustainable production; (iii) develop and implement a capitalization strategy to increase liquidity for shareholders; and (iv) acquire or develop a pipeline of silver prospects and projects designed to provide leverage to silver and cash flow.

The Company has identified the regional mineral geology of the Pacific Northwest, stretching from the U.S.-Canadian border south through Idaho then turning east into Montana, as a possible area for exploration and the Company has particularly focused on the Coeur d’Alene Mining District in Idaho. Within this district, the Company is seeking, through exploration or acquisition, to build a portfolio of assets ranging from exploration prospects to former producing mines. The Company has chosen silver as the prime metal that it will seek to acquire and develop.

The Company’s primary objective is to return the Sunshine Mine to long-term sustained production; thus the Company has placed a heavy emphasis on a revised business plan, exploration and development, and the addition of an “upper country” exploration strategy, as part of its plan to methodically bring the project forward. In late 2005, and through 2006, the Company’s activity with respect to the Sunshine Mine included finalization of the Phase III Mine Planning Study, surface infrastructure rehabilitation, initiation of underground rehabilitation of infrastructure, and expansion of the surface and underground “upper country” exploration program. The Phase III activities included the following: continued renovation and development of the Sunshine Mine; addition of experienced mining professionals with underground mining experience; assessment of the cost of returning the Mine to full production; review of a con ceptual mine plan by an independent engineering firm; and development of a final mine plan.

The Company’s business plan for its Mexican properties includes the following: focus on expanding production at its Barones facility; conduct metallurgical tests of exploration properties; drilling and evaluation of these properties in order to develop an exploration program; and seeking joint venture partners.

The Silver Market

Our primary focus is on exploration, development and production of silver. The worldwide demand for silver has exceeded newly-mined production for several years. The difference between demand and supply is primarily being made up by re-melting of bullion and silver coins, and other recycling effects. Much of the future value and/or viability of the Company is dependent on the price of silver, which the Company is unable to control. However, the Company believes, and has established its business strategy

5

accordingly, that if the demand for silver continues to exceed production silver prices will increase further. However, there is no assurance this will occur.

The current principal uses of silver are for industrial uses including electrical and electronic components, batteries, computer chips, electrical contacts, high technology printing, photography, jewelry and silverware. Silver’s strength, malleability, ductility, thermal and electrical conductivity, sensitivity to light and ability to endure extreme changes in temperature combine to make silver a widely used industrial metal. Silver’s anti-bacterial properties also make it usable in medical technology and in water purification.

According to the Silver Institute, an international industry association of miners, refiners, fabricators and silver wholesalers, Global Silver Fabrication, demand for silver was 841 million ounces in 2006. Global Silver Mine production accounts for just over 646 million ounces, resulting in a significant shortfall. Increased demand is not only from the jewelry (25%) and photographic (16%) sectors, traditionally the largest users of silver, but also from growing demand for silver’s industrial (47%) uses in electrical devices and components such as computers and cellular telephones.

A significant portion of all newly mined silver comes as a by-product in the production of other metals such as gold or copper, thus to a certain degree this means that an increase in the price of silver does not automatically bring about an increase in production as it might other commodities. The mining industry is subject to an increasing amount of government regulation and environmental laws over the last 30 years and is highly capital-intensive, thus to put a new mine into production can take two to five years under the best circumstances.

The Price of Silver and Sterling Mining Company

The price of silver can affect the Company in several ways. A low price of silver may permit the Company to acquire silver assets at a lower cost than would otherwise be the case. An increasing price of silver can affect public perception of the value of the Company and its assets, and improve the revenue potential of present and proposed operations. The Company believes a sustained silver price in excess of$6.50 per ounce, depending on the project, is required to permit the possibility of production by the Company.

The following table sets forth the London Metal Exchange’s high and low prices of silver in U.S. dollars per ounce:

|

|

|

|

|

|

|

|

| Silver | ||||

Year |

| High |

| Low | ||

2000 |

| $ | 5.45 |

| $ | 4.57 |

2001 |

|

| 4.82 |

|

| 4.06 |

2002 |

|

| 5.10 |

|

| 4.23 |

2003 |

|

| 5.96 |

|

| 4.37 |

2004 |

|

| 8.29 |

|

| 5.49 |

2005 |

|

| 9.22 |

|

| 6.39 |

2006 |

|

| 14.94 |

|

| 8.83 |

2007 |

|

| 15.82 |

|

| 11.67 |

2008* |

| $ | 20.92 |

| $ | 14.93 |

* | Through March 25, 2008 |

Employees

As of December 31, 2007, the Company had 139 full-time employees in the United States and 45 full-time employees in Mexico. As circumstances require, the Company intends to utilize the service of consultants to provide additional services to the Company.

Competition

There is aggressive competition within the minerals industry to discover and acquire properties considered to have commercial potential. The Company competes for the opportunity to participate in promising exploration projects with other entities, such as Coeur d’Alene Mines Corporation and Hecla Mining Company, Stillwater Mining Company, and Kinross, who have greater resources than the Company. In addition, the Company competes with these entities in efforts to obtain financing to explore and develop mineral properties.

The Company also encounters competition for the hiring of personnel, as the mining industry has a very tight labor situation for experienced mining professionals industry-wide. This competition affects our operations in Idaho, Montana and Mexico. Larger regional companies such as Coeur d’Alene Mines Corporation, Hecla Mining Company, Stillwater Mining Company, and Kinross in the Pacific Northwest can offer better employment terms as compared to smaller companies such as the Company.

6

The Company also competes for mine service companies, in particular drilling companies. Potential suppliers may choose to provide better terms and scheduling to larger companies in the industry.

Regulation

The Company’s activities in the United States are subject to various federal, state, and local laws and regulations governing prospecting, development, production, labor standards, occupational health and mine safety, control of toxic substances and other matters involving environmental protection and taxation. In particular, the Sunshine Mine must follow the rules and regulations of numerous agencies. The Company has hired a full-time Environmental Manager and a part-time Environmental Compliance Manager who was in a similar position at the former Sunshine Mining Company for over 30 years. The Company also has a full-time Safety Officer at the Sunshine Mine.

It is possible that future changes in these laws or regulations could have a significant impact on the Company’s business, causing those activities to be economically reevaluated at that time.

Future Information and Reports

We are required to file with the Securities and Exchange Commission annual reports on Form 10-K, quarterly reports on Form 10-Q, current reports of certain events on Form 8-K, and proxy and information statements disseminated to stockholders in connection with meeting of stockholders and other stockholder actions. Copies of these and any other materials we file with the Commission may be inspected without charge at the public reference facilities maintained by the Commission in Room 1580 – 100 F Street, N.E., Washington, D.C. 20549. Copies of all or any part of our filings may be obtained from the Public Reference Section of the SEC at 100 F Street, N.E., Washington, D.C. 20549, upon payment of the prescribed fees. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The Company’s filings with the Commission are also available through its web site at http://www.sec. gov. We are also required to file annual and quarterly reports with the Toronto Stock Exchange (TSX) which are filed on SEDAR. The Company’s filings with the TSX are available through its web site at http://www.sedar.com.

The Company maintains a website at the following URL:www.sterlingmining.com.

ITEM 1A. | RISK FACTORS |

The following is a discussion of risks we believe to be significant with respect to our business, operations, financial condition and other matters pertaining to an investment in our common stock. It is not possible to anticipate or predict every risk that may, in the future, prove to have a significant affect on the Company. Additional risks, including those that are currently not known to us or that we currently deem immaterial, may also impair our business operations.

Risks Related to our Common Stock

If we complete additional equity financings, our existing shareholders will experience dilution.

Sterling believes its current working capital will be sufficient, based on the current business plan, to complete the development work necessary to reach full production capacity at the Sunshine Mine. We cannot predict, at this time, what level of production may be achieved, how it will impact revenue in 2008, or whether we will achieve positive cash flow from operations. Should unexpected events affect planned production or cash flow from operations not become positive in 2008 for any reason, we may be required to seek additional equity or debt financing. Any additional equity financing that it obtains or the exercise of existing warrants would have the effect of diluting existing shareholders.

There is limited liquidity for our common stock.

Quotations for our common stock are published on the Over the Counter Bulletin Board, and the TSX. The OTC Bulletin Board is an unorganized, inter-dealer, over-the-counter market that provides significantly less liquidity than other markets. Purchasers of our common stock may therefore have difficulty selling their shares should they desire to do so, and the lack of liquidity could adversely affect the market price for our common stock.

Risks Related to our Business

We have a limited recent operating history on which to evaluate our potential for future success. We also have a history of net losses.

Although the Company was founded in 1903, the Company was dormant for many years and was reactivated in 1998 with substantial activity beginning in 2003. The Company’s business since that time represents a limited operating history upon which shareholders or prospective shareholders can evaluate the Company’s business and prospects. We have a history of net losses. Furthermore, since our reactivation in 1998, we have not generated sufficient revenues to cover our expenses and costs. If we are unsuccessful in generating our business, results of operations and financial condition will be materially and adversely affected.

7

The Company has limited capital and has minimal revenue to date and may thus need to obtain additional capital to continue operations.

Over the five-year period ended December 31, 2007, our cumulative revenues were $3,167,459, and we did not have any significant revenues from operations until 2005. As a mineral exploration company, we will sustain operating expenses without corresponding revenues. This will result in significant net operating losses until the Company can bring a property into production or lease, joint venture or sell the properties. The Company will need to obtain additional financing in the future to fund future exploration and development activities or acquisitions of additional properties or other interests that may be appropriate to enhance the Company’s financial or operating interests. If the Company’s exploration programs successfully locate an economic ore body, additional funds will be required to place it into commercial production. Substantial expenditures would be required to establish ore reserves through drilling, to develop metallurgical processes to extract the metals from the ore and to construct the mining and processing facilities at any site chosen for mining.

If the Company fails to obtain additional financing, it will have to delay or cancel further exploration, and it could lose all of its interest in its properties. The Company has historically raised capital through equity financing and in the future may raise capital through equity or additional debt financing, joint ventures, production sharing arrangements or other means. There can be no assurance that the Company will be able to obtain necessary financing in a timely manner on acceptable terms, if at all. If additional financing is not available, it may have to postpone the development of, or sell, one or more of its property interests.

Our accounting and other estimates may be imprecise.

Preparing financial statements requires management to make estimates and assumptions that affect the reported amounts and related disclosure of assets, liabilities, revenue and expenses at the date of the consolidated financial statements and reporting periods. The more significant areas requiring the use of management assumptions and estimates relate to:

·

Mineral reserves that are the basis for future cash flow estimates and units-of-production depreciation, depletion and amortization calculations;

·

Future metals prices;

·

Environmental, reclamation and closure obligations;

·

Asset impairments, including long-lived assets and investments;

·

Reserves for contingencies and litigation; and

·

Deferred tax asset valuation allowance.

Actual results may differ materially from these estimates using different assumptions or conditions. For additional information, seeCritical Accounting Estimates inMD&A, Note 1 – Significant Accounting Policies of Notes to Consolidated Financial Statements and the risk factors: “Our development of new orebodies and other capital costs may cost more and provide less return than we estimate,” “Our ore reserve estimates may be imprecise” and “Our environmental remediation obligations may exceed the provisions we have made.”

We may lose rights to properties if we fail to meet payment requirements or development or production schedules.

We derive the rights to most of our mineral properties from unpatented mining claims, leaseholds, joint ventures or purchase option agreements, which require the payment of maintenance fees, rents, or purchase price installments, exploration expenditures, or other fees. In 2005, 2006 and 2007, these fees totaled $ 2,794,511, $3,701,487 and $2,644,491 respectively, and, based on properties in which the Company currently has an interest, are expected to total $473,300 for 2008. If we fail to make these payments when they are due, our rights to the various properties may lapse. There can be no assurance that we will always make payments by the requisite payment dates. In addition, some contracts with respect to our mineral properties require development or production schedules. There can be no assurance that we will be able to meet any or all of the development or production schedules. Our ability to purchase, transfer or sell rights to mine ral properties may require government approvals or third party consents, which may not be granted.

The Company’s operations in Mexico are subject to risks associated with the conduct of business in foreign countries.

The Company conducts mining, development or exploration activities in the United States and Mexico. The Company’s foreign mining investments are subject to the risks normally associated with the conduct of business in foreign countries. These risks may include invalidation of governmental permits, uncertain political and economic environments, arbitrary changes in laws or policies and limitations on foreign ownership. The occurrence of one or more of these risks could have a material and adverse effect on our interest and investment in foreign properties, or on the viability of affected foreign operations and our results of operations.

The Company could face environmental liabilities with respect to its Sunshine Mine that could have a significant adverse effect on the Company’s results of operations.

In 1994, Sunshine Mining and Refining Company (former owner of the Sunshine Mine) determined it was a potentially responsible party under the Comprehensive Environmental Response, Compensation and Liability Act of 1980 (“CERCLA”), and entered into a Consent Decree with the Environmental Protection Agency (“EPA”) and the State of Idaho concerning environmental

8

remediation obligations at the Bunker Hill Superfund site, a 21-square mile site located near Kellogg, Idaho. The 1994 Consent Decree (the “1994 Decree”) settled their response-cost responsibility under CERCLA at the Bunker Hill site. In August 2000, Sunshine Mining and Refining Company filed for Chapter 11 bankruptcy and in January 2001, the United States Federal District Court in Idaho approved a new Consent Decree between Sunshine Mining and Refining Company, the U.S. Government and the Coeur d’Alene Indian Tribe, which settled its environmental liabilities in the Coeur d’Alene River Basin and released it from further obligations under the 1994 Decree.

We inherited the Sunshine Mine obligations under the new Consent Decree when we acquired our interest in the property, which means we may be required to pay royalties if the price of silver is at certain levels when we begin recovering silver from the mine. Other properties acquired by Sterling which surround the Sunshine Mine are not subject to the royalty as Sterling is not a party to the Consent Decree. While we do not expect the royalty payments will impact our ability to operate profitably in relation to operation of the mine or our results of operations when production commences, this history highlights the fact that environmental regulation and litigation for past, present, or future mining operations can have significant effects on a mining company and its ability to operate successfully.

Some of the Company’s directors and officers may have conflicts of interest as a result of their involvement with other natural resource companies.

Some of Sterling’s directors and officers are directors or officers of other natural resource or mining-related companies. These associations may give rise to conflicts of interest from time to time. There is no assurance these conflicts will be resolved in favor or to the benefit of Sterling. If a conflict of interest situation arises and it is not resolved appropriately with respect to the interest of Sterling, the result could have an adverse effect on Sterling’s participation in business opportunities, the manner in which the operations of Sterling are managed, or Sterling’s results of operations.

Sterling’s insurance coverage for its mine operations is limited, so the occurrence of a substantial uninsured loss would have significant adverse effect on Sterling’s financial condition and results of operations.

Insurance coverage for Sterling’s mining operations now and in the future is limited by what is affordable to Sterling and by the types and limits of coverage available at rates that are reasonable in relation to the risk. Sterling’s insurance may not provide sufficient insurance coverage for losses related to property, business interruption, or liability. In addition, Sterling does not have coverage for certain environmental losses and other risks; as such coverage cannot be purchased at a commercially reasonable cost. If a substantial uninsured loss or liability should arise, the resulting expense would negatively impact results of operations and paying for the loss or liability would adversely affect the Sterling’s financial condition.

Risks Related to Our Industry

Mineral exploration is by its nature highly speculative and capital intensive.

Most of the Company’s properties are considered mineral exploration properties. Mineral exploration is highly speculative and capital intensive. Most exploration efforts are not successful, in that they do not result in the discovery of mineralization of sufficient quantity or quality to be profitably mined. The operations of the Company are also indirectly subject to all of the hazards and risks normally incident to mineral exploration. These risks include: insufficient ore reserves, fluctuations in production costs that may make mining of reserves uneconomic, significant environmental and other regulatory restrictions, labor disputes, geological problems, failure of pit walls or dams and the risks of injury to persons, property or the environment.

The titles to some of our properties may be uncertain or defective, thus risking our investment in such properties.

Certain of our United States mineral rights consist of “patented” and “unpatented” mining claims created and maintained in accordance with the U.S. General Mining Law of 1872. Unpatented mining claims are unique U.S. property interests, and are generally considered to be subject to greater title risk than other real property interests because the validity of unpatented mining claims is often uncertain. This uncertainty arises, in part, out of the complex federal and state laws and regulations that supplement the General Mining Law. Also, patented and unpatented mining claims and related rights, including rights to use the surface, are subject to possible challenges by third parties or contests by the federal government. The validity of an unpatented mining claim, in terms of both its location and its maintenance, is dependent on strict compliance with a complex body of federal and state statutory and decisional law. In addition, there are few pu blic records that definitively control the issues of validity and ownership of unpatented mining claims. While we have no reason to believe that the existence and extent of any of our properties are in doubt, title to mining properties are subject to potential claims by third parties claiming an interest in them.

Our development of new orebodies and other capital costs may cost more and provide less return than we estimated.

Capitalized development projects may cost more and provide less return than we estimate. If we are unable to realize a return on these investments, we may incur a related asset write-down that could adversely affect our financial results or condition.

9

Our ability to sustain or increase our current level of production of metals partly depends on our ability to develop new orebodies and/or expand existing mining operations. Before we can begin a development project, we must first determine whether it is economically feasible to do so. This determination is based on estimates of several factors, including:

·

Ore reserves;

·

Expected recovery rates of metals from the ore’

·

Future metals prices;

·

Facility and equipment costs;

·

Availability of affordable sources of power and adequacy of water supply;

·

Exploration and drilling success;

·

Capital and operating costs of a development project;

·

Environmental considerations and permitting;

·

Adequate access to the site, including competing land uses (such as agriculture and illegal mining);

·

Currency exchange and repatriation risks;

·

Applicable tax rates;

·

Foreign currency fluctuation and inflation rates;

·

Political risks and regulatory climate in the foreign countries in which we operate; and

·

Availability of financing.

These estimates are based on geological and other interpretive data, which may be imprecise. As a result, actual cash operating costs and returns from a development project may differ substantially from our estimates as a result of which it may not be economically feasible to continue with a development project.

Our ore reserve estimates may be imprecise.

Our ore reserve figures and costs are primarily estimates and are not guarantees that we will recover the indicated quantities of these metals. You are strongly cautioned not to place undue reliance on estimates of reserves. Reserves are estimates made by our professional technical personnel, and no assurance can be given that the estimated amount of metal or the indicated level of recovery of these metals will be realized. Reserve estimation is an interpretive process based upon available data and various assumptions. Our reserve estimates, particularly those for properties that have not yet started producing, may change based on actual production experience. Further, reserves are valued based on estimates of costs and metals prices, which may not be consistent among our operating and nonoperating properties. The economic value of ore reserves may be adversely affected by:

·

Declines in the market price of the various metals we mine;

·

Increased production or capital costs;

·

Reduction in the grade or tonnage of the deposit;

·

Increase in the dilution of the ore; and

·

Reduced recovery rates.

Short-term operating factors relating to our ore reserves, such as the need to sequentially develop orebodies and the processing of new or different ore grades, may adversely affect our ash flow. We may use forward sales contracts and other hedging techniques to partially offset the effects of a drop in the market prices of the metals we mine. However, if the prices of metals that we produce decline substantially below the levels used to calculate reserves for an extended period, we could experience:

·

Delays in new project development;

·

Net losses;

·

Reduced cash flow;

·

Reductions in reserves; and

·

Write-down of asset values.

Reserve estimation is a major risk inherent in mining. Our reserve estimates, which drive our mining investment plans and many of our costs, may change based on economic factors and actual production experience.

Exploration programs may not result in a commercial mining operation, resulting in expensing our investment.

Mineral exploration involves significant risk because few explored properties contain bodies of ore that would be commercially economic to develop into producing mines. The determination of whether the extraction and production of mineral deposits are economic is affected by numerous factors beyond our control. These factors include market price fluctuations for precious metals, the proximity and capacity of natural resource markets, processing equipment and government regulations. If exploration programs do not result in the discovery of commercial ore, our investments in the properties will be expensed.

We may be subject to risks and expenditures that may be financially burdensome in connection with the safety and regulation of operations at the Sunshine Mine.

10

Our U.S. mining operations are subject to inspection and regulation by the Mine Safety and Health Administration of the United States Department of Labor (“MSHA”) under the provisions of the Mine Safety and Health Act of 1977. The Occupational Safety and Health Administration (“OSHA”) also has jurisdiction over safety and health standards not covered by MSHA. Our policy is to comply with applicable directives and regulations of MSHA and OSHA. We have made, and expect to make in the future, significant expenditures to comply with these laws and regulations. Changes to the current laws and regulations governing the operations and activities of mining companies, including changes to the U.S. General Mining Law of 1872, and permitting, environmental, title, health and safety, labor and tax laws, are actively considered from time to time. We cannot predict which changes may be considered or adopted and changes in these laws and regulations could have a material adverse impact on our business. Expenses associated with the compliance with new laws or regulations could be material. Further, increased expenses could prevent or delay exploration or mine development projects and could therefore affect future levels of mineral production.

The Company may be significantly affected by fluctuations in the price of silver.

The business and financial performance of the Company will be significantly affected by fluctuations in the price of silver. The price of silver is volatile, can fluctuate substantially and is affected by numerous factors that are beyond the control of Sterling, including industrial and jewelry demand around the world, the strength of U.S. dollars and of other currencies, inflation and regional and global politics. If silver prices should decline significantly and remain at low market levels for a sustained period, the Company would be adversely affected and it may be unable to operate at a profit.

A substantial or extended decline in metals prices would have a material adverse effect on us.

The majority of our revenue is derived from the sale of silver and, as a result, our earnings are directly related to the prices of these metals. Silver prices fluctuate widely and are affected by numerous factors, including:

·

Speculative activities;

·

Relative exchange rates of the U.S. dollar;

·

Global and regional demand and production; and

·

Political and economic conditions.

These factors are largely beyond our control and are difficult to predict. If the market prices for these metals fall below our production or development costs for a sustained period of time, we will experience losses and may have to discontinue exploration, development or operations, or incur asset write-downs at one or more of our properties.

The following table sets forth the average daily closing prices of silver for 2001 through 2007.

| 2007 | 2006 | 2005 | 2004 | 2003 | 2002 | 2001 |

Silver(1) (per oz.) | $11.55 | $11.57 | $7.31 | $6.66 | $4.88 | $4.60 | $4.37 |

(1)London Fix

On December 31, 2007, the closing price for silver was $16.74 per ounce.

We may be subject to environment risks and land reclamation requirements for mineral properties that may be financially burdensome.

We are subject to potential risks and liabilities associated with environmental compliance and the disposal of waste rock and materials that could occur as a result of our mineral exploration and production. To the extent that we are subject to environmental liabilities, the payment of such liabilities or the costs that we may incur to remedy any non-compliance with environmental laws would reduce funds otherwise available to us and could have a material adverse effect on our financial condition or results of operations. If we are unable to fully remedy an environmental problem, we might be required to suspend operations or enter into interim compliance measures pending completion of the required remedy. The potential exposure may be significant and could have a material adverse effect on our operations and financial condition. We have not purchased insurance for environmental risks (including potential liability for pollution or other ha zards as a result of the disposal of waste products occurring from exploration and production) because it is not generally available at a reasonable price or at all.

Although variable depending on location and the governing authority, land reclamation requirements are generally imposed on mineral exploration companies in order to minimize long term effects of land disturbance. Reclamation may include requirements to control dispersion of potentially deleterious effluents and to reasonably re-establish pre-disturbance land forms and vegetation. In order to carry out reclamation obligations imposed on the Company in connection with its mineral exploration, the Company must allocate financial resources that might otherwise be spent on further exploration programs.

We face competition in the acquisition of mining properties and the recruitment and retention of qualified personnel.

The Company competes with other mineral exploration and mining companies, many of which have greater financial resources than us, for the acquisition of mineral claims, leases and other mineral interests as well as for the recruitment and retention of qualified

11

employees and other personnel. If the Company requires and is unsuccessful in acquiring additional mineral properties or personnel, it will not be able to grow at the rate it desires or at all.

ITEM 1B. | UNRESOLVED STAFF COMMENTS |

We have no unresolved staff comments with the Securities and Exchange Commission.

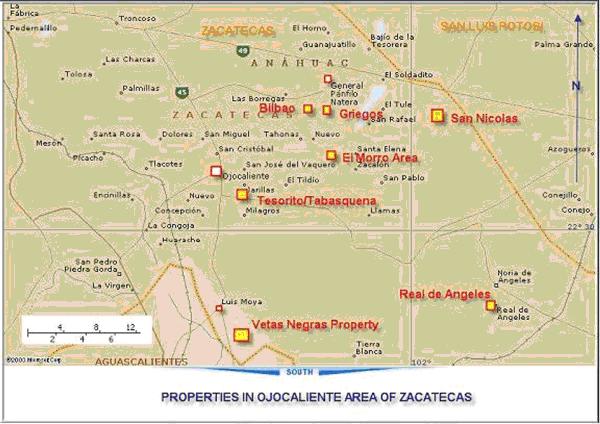

ITEM 2. | PROPERTIES |

COEUR D’ALENE MINING DISTRICT

Overview

The Silver Valley of Idaho, a region noted for its historical silver production, is located in a heavily mineralized zone in northern Idaho. In the Silver Belt of the region, mineralization is found primarily in the Revett and St. Regis Formations.

The Company is primarily focused on locating, purchasing or leasing mining claims in key positions throughout the Silver Valley. Through December 31, 2007, the Company controlled through ownership or lease over 23,100 acres.

The Sunshine Mine property is the flagship of Sterling-controlled landholdings from which to develop other properties and landholdings within the Coeur d’Alene Mining District.

The following map shows the locations of our various properties in the Coeur D’Alene Mining District near Kellogg, Idaho.

The table below summarizes the Company’s Coeur d’Alene Mining District land holdings by property and their corresponding acreage:

|

|

|

|

|

|

|

|

| ||||||

Property |

| No. |

| Approximate |

| Lease Term |

| Nature of | ||||||

Coeur d’Alene Mining District Total Sterling Holdings |

| 1,163 |

| 23,171 |

|

|

|

| ||||||

Sunshine Group* |

| 361 |

| 6,147 |

|

|

|

| ||||||

|

|

|

|

|

|

|

|

| ||||||

East Silver Valley Group: |

|

|

|

|

|

|

|

| ||||||

Banner Idaho |

| 5 |

| 74 |

| — |

| Own | ||||||

Beacon light |

| 11 |

| 220 |

| — |

| Own | ||||||

Boulder Creek |

| 4 |

| 80 |

| Until 2023 |

| Lease | ||||||

Bullion Creek |

| 2 |

| 40 |

| Until 2023 |

| Lease | ||||||

Conjecture Silver |

| 19 |

| 200 |

| — |

| Own | ||||||

Military Gulch |

| 2 |

| 40 |

| — |

| Own | ||||||

Rock Creek—Idaho |

| 26 |

| 520 |

| Until 2031 |

| Lease | ||||||

East Silver Belt |

| 243 |

| 4,860 |

| — |

| Own | ||||||

Silver Mountain Lead 1 |

| N/A |

| 268 |

| — |

| Own | ||||||

Silver Mountain Lead 2 |

| 24 |

| 424 |

| — |

| Own | ||||||

12

Snowstorm |

| 25 |

| 500 |

| — |

| Own | ||||||

|

|

|

|

|

|

|

|

| ||||||

East Silver Valley Group Total |

| 361 |

| 7,226 |

|

|

|

| ||||||

|

|

|

|

| ||||||||||

Central Silver Valley Group: |

|

|

|

|

|

|

|

| ||||||

East-West |

| 17 |

| 340 |

| — |

| Own | ||||||

Noble Group |

| 32 |

| 640 |

| — |

| Own | ||||||

Idaho-Leadville |

| 67 |

| 1,340 |

| — |

| Own | ||||||

Royal Apex |

| 4 |

| 80 |

| — |

| Own | ||||||

|

|

|

|

|

|

|

|

| ||||||

Central Silver Valley Group Total |

| 120 |

| 2,400 |

| Until 2018 |

| Lease | ||||||

West Silver Valley Group |

| 8 |

| 160 |

| — |

| Own | ||||||

Alhambra |

| 32 |

| 640 |

| — |

| Own | ||||||

Big Iron |

| 17 |

| 340 |

| — |

| Own | ||||||

Highland Surprise |

| 5 |

| 79 |

| Until 2018 |

| Lease | ||||||

Liberal King |

| 136 |

| 2720 |

| Until 2018 |

| Lease | ||||||

Pine Creek |

| 8 |

| 160 |

| — |

| Own | ||||||

Silver Bowl |

| 11 |

| 106 |

| Until 2018 |

| Lease | ||||||

New Era |

| 5 |

| 82 |

| Until 2018 |

| Lease | ||||||

State Lease Tracts |

| N/A |

| 1,110 |

| Annual |

| Lease | ||||||

|

|

|

|

|

|

|

|

| ||||||

West Silver Valley Group Total |

| 321 |

| 7,398 |

|

|

|

| ||||||

* | Sunshine group includes the leased Chester, Mineral Mountain, Merger, Metropolitan, Bismark and United Mines properties. See “Sunshine Property” table for detail on the Sunshine Group properties. |

Geology of the District

The district is hosted by the rocks of the Pre-Cambrian Belt super group. These sedimentary rocks were deposited approximately 1.6 billion years ago. At various times these rocks were faulted, leached, altered and re-mineralized. The Belt super group has been divided into the Prichard group, Ravalli group, Middle Carbonate group, and Missoula group. Within the Coeur d’Alene Mining District, rocks of the Prichard, Ravalli, and Middle Carbonate groups can be found. The formations comprising the Ravalli group are the preferred host rocks for silver mineralization in the district. These formations are from older to younger Burke, Revett, and Saint Regis.

The District has a history of intense faulting and folding of these rock formations. Two major east-west fault zones, the Osburn and Placer Creek faults, cut through the District and, although mineralization does not necessarily occur along these fault zones, the district ore bodies are intimately associated with this and other faulting.

The combination of faults, fractures, folds and favorable host rocks found in the District has created suitable conditions for lead-zinc-silver mineralization. The geology of the District may display little or no indication of mineralization on the surface, and many of the successful silver mines in the District did not realize their full potential and best grade of ore until after a depth of at least 1,700 feet was reached in the development and exploration. Examples include the Galena, Sunshine and Lucky Friday Mines, thus mining claims in the District often require deep drilling from the surface or underground drilling to determine whether commercial grade ore bodies are present. Exploration of land near major mines is often easier to target for exploration and development from existing shafts. In other silver producing areas, a deposit may bottom out at a few thousand feet below surface. However, in the Coeur d’Alene Mining Distri ct, this is not necessarily the case, as deep extensions of primarily silver mineralization are faulted and folded, which may have moved the favorable host rocks deeper.

Sunshine Property

Background

The Sunshine Mine was a significant primary silver mine from 1884 to 2001. The mine facility includes extensive underground workings including shafts, levels, raises and ramp systems extending to depths of 6,000 feet below ground and a broad database reflecting over 100 years of exploration, development and production.

13

The mine ceased production in the first quarter of 2001 as a result of several factors, including the low price of silver and the lack of regular and consistent exploration and development activities. The Company acquired control of the Sunshine Mine in June 2003 through a lease with option to purchase agreement. Beginning in August 2003, and followed by the initial drilling in the fall of 2004, the Company is continuing and expanding an exploration program. The process of rehabilitation of the underground areas of the mine began in 2004. The Company commenced initial production in December 2007 and is methodically working towards returning the Sunshine Mine to long-term sustained production.

Land Position and Ownership

The Sunshine property comprises 5,930 patented and unpatented acres including substantial infrastructure and equipment. Mine workings and surface facilities include: the Jewell surface shaft, two surface access levels, six internal shafts, 17 major underground levels, numerous raises, boreholes, sublevels and inclined haul roads, the Polaris concentrating mill, machines shops, warehouses and offices. The Sunshine property also includes the Chester, Mineral Mountain, Merger, Metropolitan, Bismark and United Mines properties that are leased by the Company. These properties are described in more detail below.

The following table sets out the various properties that comprise the Sunshine property:

|

|

|

|

|

|

|

|

|

|

|

Property |

| Owner |

| Term ofLease |

| PatentedClaims |

| UnpatentedClaims |

| Acreage |

Sunshine |

| SPMI |

| Until 2018 |

| 144 |

| 47 |

| 2940 |

Sunshine |

| Sterling |

| N/A |

| 6 |

| 68 |

| 1051 |

Metropolitan |

| Metropolitan |

| Until Cancelled |

| 2 |

| 67 |

| 1020 |

Chester |

| Chester |

| Until 2029 |

| 6 |

|

|

| 106 |

Bismark |

| Western Continental |

| Until 2029 |

| 3 |

|

|

| 62 |

Mineral Mountain |

| Mineral Mountain |

| Until 2029 |

| 4 |

|

|

| 46 |

Merger |

| Merger Mines |

| Until 2029 |

| 14 |

|

|

| 356 |

Merger CAMP |

| Sterling below -900 el |

| Until 2029 |

| 21 |

|

|

| 313 |

United Mines |

| United Mines |

| Until 2012 |

|

|

| 2 |

| 36 |

Total |

|

|

|

|

| 202 |

| 184 |

| 5930 |

On June 6, 2003, the Company leased the Sunshine Mine and infrastructure, including historical records, from Sunshine Precious Metals, Inc. (“SPMI”) for a term of 15 years. Annual lease payments are $120,000 per year, payable in monthly increments. The Company also agreed to assume approximately $840,000 in outstanding county property tax liabilities and, in a separate transaction, purchased various items of equipment in exchange for $396,000, payable in six monthly installments. The Company has the option to purchase the property at a price ranging from $3.0 to $5.0 million, depending on the spot price of silver as of the date of exercise.

In late 1998, SPMI implemented a Consent Agreement which settled various issues with the EPA, State and Coeur d’Alene Tribe as SPMI’s settlement of a federal natural resource damage suit involving active mining companies in the Coeur d’Alene Mining District. In addition to conveying surface ownership of some patented mining claims, portions of the property may be subject to certain royalties to government and tribal entities as part of a settlement action. Specifically, the Company may be required to pay a royalty indexed to the average silver price. The quarterly NSR royalty payment ranges from zero percent (0%) at silver prices less than $6.00 to a maximum of seven percent (7%) at silver prices $10.00 and over. The Company cannot predict or control the future price of silver and therefore cannot predict the royalties or if they will be material.

Access

The Jewell Shaft side or west side of the Sunshine Mine is approximately three miles south from Interstate 90 at Exit 54 via Big Creek Road. Big Creek Road is a two-lane, paved road to the mine site and is suitable for all transportation needs of the mine.

The Silver Summit side, or east side, of the mine is approximately 1,000 feet south on Johnson Street from its intersection with Yellowstone Avenue in the city of Osburn, Idaho, via paved and maintained gravel roads suitable for routine mining and exploration activities at this mine entrance.

The Chester, Mineral Mountain, Merger and United Mines lease groups that are part of the Sunshine mining block are accessible via National Forest Service road NF-330 from Big Creek Road approximately 200 feet south of Interstate 90 Exit 54. This is an unimproved dirt road suitable for exploration access and activities.

The Metropolitan mining lease group that is part of the Sunshine mining block is accessible via Big Creek Road approximately one mile south of the Sunshine Mine. This is an improved Shoshone County maintained dirt road suitable for exploration access and activities.

14

The Bismark mining lease group that is part of the Sunshine mining block is accessible via West Fork Big Creek Road from its junction with Big Creek Road approximately three-quarters of a mile south of the Sunshine Mine. This is an unimproved to primitive dirt road suitable for exploration access and activities.

Power and Water

Electrical power to the Sunshine Mine is provided by Avista Utilities, Inc. (formerly Washington Water Power) at 13,200 volts from two separate primary feeds. The first is adjacent to Big Creek Road to the mine site where it supplies power to two on-site substation metering points, the north and the south. Both on-site substations reduce the feed voltage to either 2,300 or 480 volts depending on motor requirements. The south substation metering point feeds 13,200 volts down the Jewell Shaft to underground substations for transformation to lower voltages.

The second primary feed is brought to the Silver Summit mine site (east side of the mine) adjacent to Johnson Street in the City of Osburn, Idaho. A small transformer is located at the mine site to provide 480 volt power to surface facilities. The primary feed is taken underground at 13,200 volts via the Silver Summit Tunnel to the Silver Summit hoist room, where it is transformed to 2,400 or 480 volts depending on motor requirements.

Water for mine and processing operational requirements, including fire protection, is supplied via Big Creek, a tributary to the South Fork of the Coeur d’Alene River, upon which sufficient water rights are controlled to provide water for any foreseeable needs. Water conservation is practiced in both mine and processing operations.

Infrastructure

Surface mine plant facilities at the Sunshine Mine include the Jewell Shaft hoisting machinery, compressor plant and distribution system, 13,200 volt electrical substations, complete concentrating mill, repair shops, electrical shop, warehouse, water distribution system, independent fire protection system, heating plant, change rooms, office buildings and the Big Creek tailings impoundment.

The Sunshine Mine is serviced by the Jewell Shaft, Sterling Tunnel and Silver Summit Tunnel and Shaft. The Sterling Tunnel accesses the “upper country” of the mine and connects to the Silver summit Tunnel. The Jewell Shaft is the primary entry and the primary escapeway to and from lower levels while the Silver Summit is used as a secondary access and is the required secondary escapeway from lower levels of the Sunshine Mine. Both shafts are an integral part of the mine ventilation system. Five additional shafts on deeper levels are used for various purposes, including ventilation and water management. The Jewell Shaft, which extends vertically down to the 4,000 foot level is serviced by a Nordberg 700 horsepower double drum hoist for ore, waste and large equipment movement and a separate Nordberg “chippy” (single drum) hoist is used to distribute personnel, small equipment and supplies. The Silver Summit Shaft is servic ed by a completely renovated 600 horsepower Coeur d’Alene double drum hoist.

Since 2003, the Company has been actively renovating and maintaining the mine facilities and equipment. Completion of the lower mine’s secondary escapeway was achieved in December 2007 and will allow production to resume from lower levels. Mine activities continue to be guided by a plan developed to rehabilitate the infrastructure and mine plant in order to sustain and increase production that commenced in December 2007.

Mineralogy

Typically the Sunshine ore consists principally of tetrahedrite, the high silver-containing copper antimony sulfide. This silver bearing tetrahedrite is properly called freibergite. Freibergite contains three to thirty percent silver substituting for the copper in the crystal structure. Galena is present in the West Chance Vein.

Reserve Statement

Sterling commissioned Behre Dolbear & Company (USA), Inc. (Behre Dolbear), an independent consulting firm, to provide a feasibility analysis of the re-start of operations at Sterling’s Sunshine Mine in the Coeur d’Alene Mining District at Big Creek near Kellogg, Idaho, and based on the feasibility analysis, determine the Proven and Probable Reserves present at the property. Behre Dolbear produced a report titled “Sterling Mining Company, Sunshine Mine, Phase 2, Development of Mineable Reserves and Re-start of Sunshine Mine Operations.”

The report on the analysis reads in part “Behre Dolbear has verified that the plans for future operations have been based on adequate data formulated in accordance with sound mining and engineering practice, to assure that the mine can achieve its intended capacity within the capital and cost budget estimates.” The report adds “This Phase 2 feasibility study indicates that 23,486,698 ounces of silver, currently [sic] classified as Mineralized Material has been brought into the classification of Proven and/or Probable Reserves.” It was noted in the report that “Behre Dolbear has not included unidentified mineralization in the mining reserve and has restricted the economic analysis to Proven and Probable ore reserves.

15

Sterling did not mine any of the proven and probable reserves during the fiscal year ended December 31, 2007, but has begun mining these reserves in 2008. A 15% mine recovery loss was deducted to arrive at Behre Dolbear’s estimate of Mineable Proven Reserves presented herein. The proven and probable reserves at Sterling’s Sunshine Mine at December 31, 2007 are shown in the table below as developed in the Behre Dolbear report.

Sunshine Mine Reserves | |||

Reserve Category | Short Tons | Grade oz/t (1) (2) | Ag Ounces |

Proven | 1,049,396 | 22.1 | 23,237,689 |

Probable | 11,577 | 21.5 | 249,009 |

Total | 1,060,973 | 22.1 | 23,486,698 |

(1) Silver grades are rounded numbers

(2) The above reserves were calculated using operating costs of $6.92 per Ag oz., and a silver price of $10.00.

Metallurgy and Milling

The current metallurgical facilities include a 1,000-ton per day flotation mill with a projected silver recovery rate of 96 to 97 percent. Both silver and lead concentrates were formerly produced and shipped to the former ASARCO East Helena Smelter which is now closed. Future production could most likely need to be shipped to an offshore smelter. Sunshine silver concentrate typically exceeds 1,000 ounces per ton silver.

In 2006, Sterling purchased a tailings pond, critical to the disposal of tailings after ore processing, and related water discharges.

In September 2007, the Number 3 ball mill was returned to operation allowing processing of upper country vein material that culminated in shipping the mine’s first concentrates to a smelter in December 2007. The Company is currently studying terms and options for a longer term smelter contract.

Environmental

The Sunshine Mine, which Sterling acquired in 2003, operated near continuously from 1884 to 2001, with various changes in production levels and extraction, beneficiation and processing method since that time. As such, many process emissions, discharges and waste management activities may be grandfathered under the state and federal regulatory framework. Further, the land position involves mostly patented claims; therefore surface and underground operations have required less regulatory burden that would have been the case if incurred on unpatented mining claims. In addition, in late 1998, Sunshine Precious Metals, Inc. implemented a Consent Agreement which settled various issues with the EPA, State and Coeur d’Alene Tribe. The Company has a full-time Environmental Manager, an Environmental Specialist, and a part-time Environmental Compliance Manager, who continually review environmental matters and requirements for future plans.

To the best of the Company’s knowledge, all required permits are in place, or under extension where applicable, to operate the Sunshine facility. A preliminary environmental assessment was completed and supports the past understanding of permits and environmental conditions at the project. Further environmental assessments will be ongoing to better understand current conditions and operations permit conditions.

The Company operates in an environmentally sensitive area and nearby is a “Superfund” designated site. It is to be expected, notwithstanding the consent decree signed in 2001 by the former operator, that ongoing environmental issues will require our attention.

Prior to closure, the Sunshine Mining Company settled a natural resources damage suit with the federal government that gave surface rights to many patented claims to the Environmental Protection Agency (EPA) and the Coeur d’Alene Tribe. The settlement included a royalty payable to the Coeur d’Alene Tribe that is indexed to the price of silver for production from those claims owned by Sunshine at the time of the suit. This action limits future disturbance on the surface covered by those claims and may result in the need for negotiations for any future surface access. However, it is important to note that all access by way of underground workings for either exploration or production was retained by the mine.

After closure of the mine, Sunshine Mining Company sold the Big Creek tailings impoundment, the antimony plant and silver refinery to Essential Metals Company, but retained rights to use the impoundment. This right to use the tailings impoundment was covered in the Company’s lease agreement. In 2006, the Company purchased the tailings impoundment from Essential Metals Company.

A water treatment facility is being installed to treat mine waters from dewatering activities. The Company will continue to review water treatment technology for potential improvements to the system being installed.

16

One other significant environmental issue is site remediation and reclamation following ultimate closure. The Company has purchased a Certificate of Deposit, required by the state to address the issue of future mine remediation and reclamation costs.

Business Plan

The Company established a goal of returning the Sunshine Mine to long-term, sustainable production. To this end, the Company has developed a three-phase plan to accomplish this goal.

The Sunshine Mine or the associated properties had been in continuous operation for 100 years, and the extensive quantity of geologic, mine, and operational data provide a unique opportunity to assess the property and develop costs associated with resuming production. Previously, Sunshine Precious Metals, Inc. developed a ten-year plan that was peer reviewed by outside experts in 1999. The Company plans to use this data, projected costs and other pertinent information to support its project review. The mine has been idle for several years; hence there will be additional startup costs beyond those identified in the original plan developed several years ago. The Company has been working to update the plan with current economic information and assess the rehabilitation required.

In April 2007, the Sterling Tunnel Project was completed with the underground mining contractor advancing the project 2,519 feet during the year, including 164 feet of tracked drift to connect with the Silver Summit – Polaris Tunnel. The contractor continued with secondary excavation work totaling 880 feet to access portions of the Sunshine vein structure west of Polaris workings and 167 feet of track drift to start a diamond drill access east of Polaris workings.

The Company’s underground diesel equipment began arriving on site in July and Sterling mining crews began limited mining activities in August. In addition to starting a second crosscut to the Sunshine vein, crews began drifting on mineralization in an unmined portion of the Sunshine vein west of the historic Polaris mine area. By year end crews had completed 876 feet of vein drifting on the initial (I-drift) cut and a second cut that yielded approximately 5,630 tons of mill feed containing an estimated 32,408 ounces of silver based on daily vein sampling.

To the east, crews resumed Polaris track drift development advancing 142 feet to complete a drill station currently in use to explore lower elevations of the Sunshine-Polaris veins and the Yankee Girl vein 1,200 feet to the south. In addition to “upper country” mining, Sterling crews excavated 110 feet of track drift adjacent to the Jewell Shaft for a primary 13,200 to 2,400 volt substation to feed 2700 and 3100 levels.

During 2007, the Company completed underground diamond drilling from locations in the Sterling Tunnel and the connecting Silver Summit drift. Diamond drilling for the year totaled 18,355 feet of which 7,493 feet was in-house and 10,862 feet contracted. Drill results continue to guide additional drilling and exploration activities in the “upper country” of the mine. Diamond drilling to guide stope development below 2700 level in the West Chance commenced in February 2008.

After 18 months of rehabilitation, re-engineering and repair, the Silver Summit hoist became operational on August 10, 2007, and was certified to carry personnel to begin shaft repair in September. Shaft repair crews working on a double shift basis reached 3000 level on December 20, 2007, thus completing the lower mine’s secondary escapeway system. In-depth rehabilitation work on 3000 is currently in progress; however, the secondary escapeway was inspected and approved for use in January and February, 2008.

Re-establishment of the escapeway system allows mining activities to proceed on the 2700 and 3100 levels of the mine where production was suspended by former operators in February, 2001. Following re-establishment of communications and compressed air, work was accelerated to re-establish electrical services across 3100 in order to supply power for fans, pumps, drill jumbo and shop facilities that service the Sunshine ramp production and development area. Similar work is underway on 2700 level in the West Chance ore zone to restart production from that area.

Sterling mill and maintenance crews returned the concentrating facility to operational status using the Number 3 ball mill in late September. The regrind mill and Number 2 ball mill became operational in January and February 2008. Installation of a conveyor feed system to allow upper country ore to be introduced into the coarse ore bin was completed. Vein material from exploration drifting on the Sterling Tunnel level currently provides mill feed that will be augmented by 2700 and 3100 level production in early 2008. Resulting concentrates are stockpiled until an appropriate amount is available for shipment to a smelter. Concentrate load-out facilities were renovated during the year including a new heated, environmentally engineered truck loading pad. The first shipment of concentrates to a smelter was made on December 20, 2007 thereby marking the Sunshine Mine’s return to production.

Jewell shaft dewatering began in April 2007, since then water in the shaft has been lowered 95 feet and is currently 220 feet below the 3100 level. Progress was slowed late in the year by receiving additional quantities of water from 3000 level in advance of Silver Summit shaft repair. Water treatment equipment located adjacent to the tailings pond was installed and made operational during the year. Start-up tailings will report to the tailings pond and sand storage tanks until renovation of the underground sandfill distribution system is complete in early 2008. Until the system is operational, waste rock from mine development will be used to fill stopes in order to maintain ore production. During the year the 14-inch tailings distribution line around the pond was renovated and an 8-inch water line from the mine was completed to enhance mine dewatering.

17

The Company hired 88 full time employees at the Sunshine Mine during 2007. The total mine workforce at year end was 118 employees. The mine continues to hire as operations expand.

Five-1.25 cubic yard and four-2.5 cubic yard underground diesel loaders for development and production, three single-boom hydraulic drill machines for development and one seven-ton haul truck were received during 2007. The Company continued to order and receive equipment and supplies and re-stock the mine warehouse to meet the development plan and production goals.

Other Sunshine Group Properties

The Chester, Bismark, Merger, Mineral Mountain, Metropolitan and United Mines properties are included in the Sunshine Property group. For the most part, these properties were originally leased by SPMI prior to its bankruptcy in 2001.

Chester and Bismark Group

In 2004, the Company leased the Chester and Bismark claim groups pursuant to a 25-year lease, renewable for an additional 25 years. The lease, which expires in 2029, requires the annual payment of 50,000 shares of the Company’s common stock, a $7,200 annual advance royalty payable in monthly installments, and a 4% Net Smelter Return (“NSR”). The Company has no work obligations under the lease. Specifically, with respect to Chester Mining Company we lease six patented mining claims covering 106 acres, which are part of the Sunshine Mine property. In October 2006, we entered into an agreement with Chester Mining Company under which we sold 50% of our interest in the Tabasquena Mine in Mexico for 600,000 restricted common shares of Chester Mining Company. Under a separate agreement, we issued 400,000 restricted shares of our common stock to Chester Mining Company in exchange for 675,000 outstanding common shares of Chester Mining Company. As a result of these transactions we now hold approximately 47% of the issued and outstanding common shares of Chester Mining, which management believes to be to the advantage of the Company because of its leasehold interest in Chester Mining Company’s patented mining claims described above.

Mineral Mountain Group

In 2004, the Company leased the Mineral Mountain claim groups pursuant to a 25-year lease, renewable for an additional 25 years. The lease, which expires in 2029, required the issuance to the lessor of 30,000 shares of the Company’s common stock, and provides for an annual advance royalty payment of $3,600, and a 3% NSR. The Company has no work obligations under the lease. As part of the lease, the Company received an option to buy up to 1,000,000 shares of the lessor.

Metropolitan Group

In 2004, the Company entered into an agreement pertaining to the Metropolitan claim groups, which expire when cancelled. The agreement provided for the issuance to the Company of 200,000 shares of the stock in the owner of the Metropolitan claim groups and an annual advance royalty payment by the Company to the lessor of $12,000.

The Metropolitan Mining Company property consists of 2 patented and 40 unpatented mineral lode claims. These claims lay immediately to the south of the primary workings of the Sunshine Mine and immediately to the west of the ConSil Mine. The workings of the Metropolitan Mine are inaccessible. At depth the claims intersect several veins mined from the Sunshine Mine.

The Metropolitan Mine is located on the south limb of the Big Creek Anticline, in the south dipping rocks of the lower Wallace Formation. There are two veins in the Metropolitan Mine. The north and south veins. The north vein is characterized by a very narrow quartz band, accompanied by a two foot zone of intensely sheared rock with loose, muddy gouge on either wall. The quartz carries pyrite, minor siderite and occasional tetrahedrite and chalcopyrite. The vein strikes east-west and dips at approximately 45 to 60 degrees. The south vein is composed of a zone a few inches to three feet in width, made up of stringers of quartz carrying siderite and pyrite. Some tetrahedrite is found in the included country rock and in the adjacent hanging wall. The property also covers the Big Creek Fault Zone that separated the rocks of the Wallace and St. Regis Formations on the footwall from rocks of the Revett Formation on the hanging wal l. It is likely that the north and south veins have never been explored in the more favorable quartzite units. It has been postulated that the north vein should intersect the quartzites of the Revett Formation around 2,700 feet. The south vein is projected to intersect with the Big Creek Fault at the 1,900 foot level and may host potential ore zones in the Revett Formation.

Sunshine Mining Company explored the Metropolitan property from the 3,100 foot level with the development of the Metropolitan cross-cut. A number of narrow quartz-siderite zones were encountered, but no commercial ore-shoots were intersected.

The Yankee Girl Vein on Sunshine claims lies immediately to the north of the Metropolitan property, and dips onto Metropolitan claims. Issues regarding ownership of the Yankee Girl Vein have prevented exploration of this structure in the past. The Yankee Girl Vein is believed to host mineralization along 10,000 feet of strike length.

18

The Company proposes to extend the area of existing surface exploration on the Sunshine property onto Metropolitan land holdings. The program consists of both induced polarization and resistivity geophysics. Drilling is best deferred until drill stations can be accessed underground from the Sunshine workings. Drilling will test for the down-dip projection of the Yankee Girl Vein as well as the Metropolitan North and South Veins.

Merger Group

In 2004, the Company leased the Merger claim groups pursuant to a 25-year lease, renewable for an additional 25 years. The lease, which expires in 2029, required the issuance by the Company to the lessor of 20,000 shares of the Company’s common stock and the payment by the Company of annual advance royalty payments as follows: $2,500 for each of the first five years of the lease; $5,000 for each of the second five years of the lease; $7,500 for each of the next ten years of the lease; and $10,000 for each of the next five years of the lease. In addition, the Company has agreed to pay a 5% NSR. The lease is subject to minimum work obligations of approximately $25,000 annually throughout the term of the lease.

The Merger claim groups consist of 35 patented lode claims. The northerly section of the property (21 patented claims) is part of the CAMP project between Coeur d’Alene Mines Corporation, Plainview, and Merger, leased to Silver Valley Resources, Inc. (Coeur d’Alene Mines Corporation), and the southerly section (14 patented claims) is located between Sterling’s Sunshine and Link property. Production from the CAMP ground above a minus 900 feet sea level elevation is for the benefit of the CAMP interests, while production from below this elevation (approximately 3,600 foot level Sunshine) is part of the Sunshine Mine and would benefit Sterling.